OPPORTUNITIES FOR DISTRIBUTED GENERATION IN CANADA

56

OPPORTUNITIES FOR DISTRIBUTED GENERATION IN CANADA Ganesh Doluweera, Director of Research Webinar April 21, 2020 www.ceri.ca Choose one of the following for audio: • Mic & Speakers to use VoIP • Telephone and dial: • CANADA: 1-647-497-9385 • US: 1-213-929-4231 • ACCESS CODE: 246-506-339 Flagship Sponsor

Transcript of OPPORTUNITIES FOR DISTRIBUTED GENERATION IN CANADA

OPPORTUNITIES FOR DISTRIBUTED GENERATION IN CANADA

Ganesh Doluweera, Director of ResearchWebinarApril 21, 2020

www.ceri.ca

Choose one of the following for audio:• Mic & Speakers to use VoIP• Telephone and dial:

• CANADA: 1-647-497-9385• US: 1-213-929-4231• ACCESS CODE: 246-506-339

Flagship Sponsor

2

WEBINAR PARTICIPATION

2

AudioYour microphone has been muted for the duration of this presentation. To hear webinar audio: Choose Mic & Speakers to use VoIP Choose Telephone and dial using the

information provided: CANADA: 1-647-497-9385 US: 1-213-929-4231 ACCESS CODE: 246-506-339

Questions Please submit your text questions and

comments using the Questions panel. Questions will be answered during the Q&A

period following the presentation.

Note: A copy of this presentation can be downloaded by selecting the document in the Handouts panel.

Allan Fogwill

CANADIAN ENERGY RESEARCH INSTITUTE

OverviewFounded in 1975, the Canadian Energy Research Institute (CERI) is an independent, registered charitable organization specializing in the analysis of energy economics and related environmental policy issues in the energy production, transportation, and consumption sectors.

Our mission is to provide relevant, independent, and objective economic research of energy and environmental issues to benefit business, government, academia and the public.

CERI publications include:

• Market specific studies

• Geopolitical analyses

• Quarterly commodity reports (crude oil, electricity and natural gas)

In addition, CERI hosts a series of study overview events and an annual Petrochemicals Conference.

3

CORE FUNDERS

FUNDING SUPPORT

IVEY FOUNDATION

IN-KIND SUPPORTAlberta Energy Regulator | Bow Valley College | CEPA Foundation

JWN Energy | Northern Alberta Institute of Technology Petroleum Services Association of Canada

S.M. BLAIR FAMILY FOUNDATION

AGENDA

• Introduction

• Study Scope & Objectives

• Data and Methods

• Results (Preliminary)

• Observation

5

Introduction

• Rapid growth in the integration of distributed energy resources (DER) is one of themost significant and important trends in the electricity industry around the world

• DER encompasses electricity generation systems, storage systems, andcontrollable loads that are connected to the distribution system at or closer to finalconsumers of electricity

• Distributed generation (DG) is a major and one of the well understood DER

• Interest on DG is not new – has been there (at least) for the past few decades

• In Canada, DG technologies are being promoted as a complementary policy tool toachieve energy and environmental goals

• However, higher integration of decentralized generation systems will bringchallenges

• The trade-offs of DG need to be assessed and quantified.

6

Distributed Generation - Definition

1) Electricity generation at distribution system levels • Smaller nameplate capacity (between 1kW and 15MW ) • Backup generator for an airport is about 4MW and 5MW

2) The generating system is located near or at the point of consumption

3) The output (electricity generation) is used to meet all or at least a fraction of the electricity needs of a house or small business

4) Makes use of technologies that rely on locally extracted primary energy resources (wind, solar, hydro, biomass, or geothermal)

7

Perceived Benefits of DG

8

Study Scope and Objectives

9

Our study has three main objectives:

The study is currently in progress and this webinar will review some of the results

Review of DG Policies and Programs

10

Provincial DG Programs

• A common drivers:• Climate policies• Promotion of renewable energy• Supporting local economies • Enhanced electricity access

• Differs by:• Technology choice• Formal procurement programs (or lack thereof) • Compensation mechanism (e.g., Fixed feed in tariff, net energy

metering, net billing)

11

British Columbia

DG Policies

• Net Metering Program (2004)• Initial limit of 50kW – increased to 100kW in 2008

• Standing Offer Program – SOP (2008)• Systems with nameplate capacity between 100kW and 15MW• Participants are compensated through Electricity Purchase

Agreements

• Micro-SOP (2014)• Targeting First Nation’s communities (between 100kW and 1MW)• The First Nation community needs to keep at least 50% ownership• Compensated through Electricity Purchase Agreements

12

British Columbia

Results• As of 2019, more than 1800 customers in the Net Metering

Program• Installed capacity of about 13MW• 98% are using PV systems

• As of 2018, there were about 170MW contracted under the SOP and Micro-SOP programs

• The initial target for the SOP program was 100MW

• SOP and Micro-SOP have now been cancelled over concerns on the impacts on electricity rates

• BC Hydro applied to the BCUC to amend the Net Metering Program to limit the max capacity of DG

13

Alberta

DG Policies

• Microgeneration Regulation (2008)• Initially a max capacity of 1MW, increased in to 5MW in 2016• Compensation through net billing mechanism

• Renewable Electricity Act (2016)• Set a target of 30% of electricity to come from renewable sources by

2030

14

Alberta

Results

• As of Feb 2020, there were more than 5000 sites registered under the Micro-generation Regulation

• Total installed capacity of 68MW from micro-generators• About 94.5% using PV systems

• Renewable Electricity Act and the Micro-Generation Regulation remained unchanged

15

Ontario

DG Policies

• Renewable Energy Standard Offer Program - RESOP (2006)• Systems between 1kW and 10MW• Exclusive for systems connecting to the distribution system• Subject to 20 year contracts

• Feed-in Tariff (FIT) program (2009)• Large-FIT: Systems greater than 500kW (connected to Tx or Dx)• Small-FIT: Systems between 10kW and 500kW (Dx)• Micro-FIT: Systems less than 10kW (Dx)• Subject to long-term fixed-price contracts with IESO (20 years on

average)

16

Ontario

Results

• RESOP• 825MW of contracted capacity

• Large-FIT program cancelled in 2016• Currently has 896MW of contracted capacity (Dx)

• Small-FIT program cancelled in 2016• Currently has 573MW of contracted capacity

• Micro-FIT program cancelled in 2017• Currently has 261MW of contracted capacity

• 62% are solar PV system, 17% wind, 8% hydro, 4.5% CHP

17

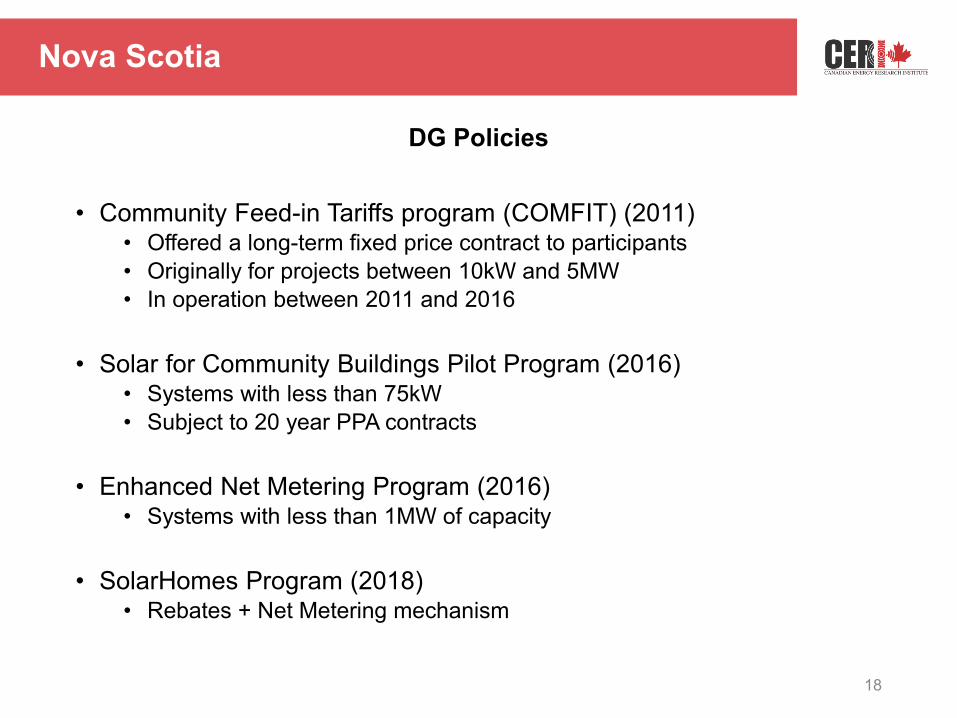

Nova Scotia

DG Policies

• Community Feed-in Tariffs program (COMFIT) (2011)• Offered a long-term fixed price contract to participants• Originally for projects between 10kW and 5MW• In operation between 2011 and 2016

• Solar for Community Buildings Pilot Program (2016)• Systems with less than 75kW• Subject to 20 year PPA contracts

• Enhanced Net Metering Program (2016)• Systems with less than 1MW of capacity

• SolarHomes Program (2018)• Rebates + Net Metering mechanism

18

Nova Scotia

Results

• Community Feed-in Tariffs program (COMFIT)• Created 150MW of renewable capacity• Mostly small wind projects

• Solar for Community Buildings Pilot Program• Brought 1.5MW of solar capacity• Program is now closed

• Enhanced Net Metering Program• Uptake was relatively limited at the beginning (130 systems)

• SolarHomes + Net Metering Program (after 2018)• If all projects are completed, the small solar generation capacity

could reach up to 12.2MW

19

DG Technology Assessment

By Population Centers(Census of Population – 2016)

20

Solar PV Assessment – BC and Alberta

21

Most population centers

British Columbia: 90Alberta: 108

Why Solar PV?

Solar PV Assessment – Ontario & Nova Scotia

22

Most population centers

Ontario: 255Nova Scotia: 31

Electricity Production – Capacity Factor

23

Levelized cost of Electricity – Residential Solar PV

24

Capital cost = $2.5/WDC

13-16 cents/kWh 10-12 cents/kWh 16-17 cents/kWh 11-16 cents/kWh Retail electricity prices (Major cities)

Up to 10kW

If 50% of the detached houses in 108 population centers in Alberta installed solar PV (8kW/system), the annual energy production will be 4000 GWh/year (5% of provincial electricity demand)

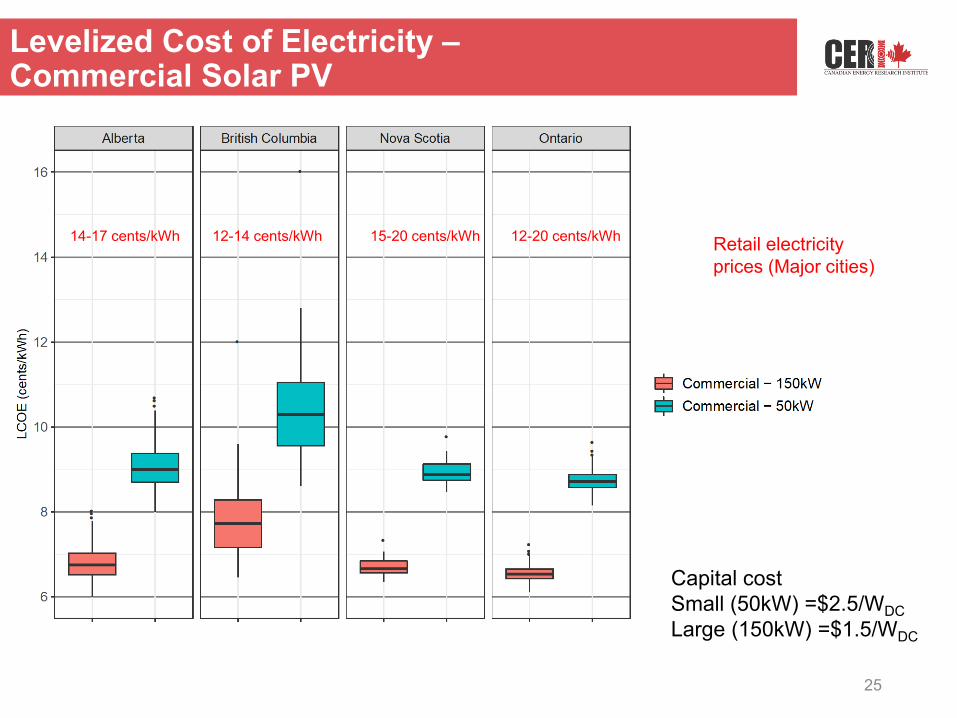

Levelized Cost of Electricity –Commercial Solar PV

25

Capital costSmall (50kW) =$2.5/WDCLarge (150kW) =$1.5/WDC

14-17 cents/kWh 12-14 cents/kWh 15-20 cents/kWh 12-20 cents/kWh Retail electricity prices (Major cities)

Biomass and MSW Assessment

• Assessed the potential and economics of DG with biomass and municipal solid waste (MSW) by population center

• Data availability is sparse and somewhat unreliable• Existing resources are matched with conversion technologies• Solid biomass

• Incineration with steam turbines (ST)• Gasification with internal combustion engines (ICE)

• MSW• Incineration with steam turbines (ST)• Anaerobic digestion with internal combustion engines (ICE)

• Resource availability varies significantly • Biomass/MSW based DG can provide on demand power

26

Biomass and MSW Assessment

27

Lethbridge (AB) Penticton (BC) London (ON)

Biomass

Supply (kt/year) 772 7 2683

Electricity potential (GWh/year) 800-1000 7-12 3000-4000

MSW

Supply (kt/year) 42 16 182

Electricity potential (GWh/year) 4-25 2-9 20-90

DG with Biomass

28

DG with MSW

29

Natural Gas CHP Assessment (Micro CHP)

30Sources: Renewableenergyhub, 2020, CIEEDAC (2016), Electropaedia (2018), Tan, K. (2018)

Type of Micro CHP systemsOverall

Efficiency(%)

ElectricalEnergy

Efficiency(%)

Heat to PowerRatio

ThermalEnergy

Qualities

Gas Turbines 70 – 85% 24 – 42% 1.3 – 2.0 HighReciprocating Engine 75 – 85% 33 – 53% 0.5 – 2.5 LowMicro Turbines 60 – 75% 15 – 33% 1.3 – 2.0 Medium to LowFuel Cells (PEMFC) 75 – 85% 25 – 60% 0.33 – 2.0 LowFuel Cells (SOFC) 75 – 85% 35 – 43% 1 – 2.5 High

CHP = Combined heat and power

Micro CHP: Electricity capacity of few kW

• Eligibility for NG CHP for DG programs varies by province• Alberta NG CHP is eligible• In Ontario, NG CHP is not eligible for DG programs

• ATCO has two units in service on dairy farms in Taber, Alberta, which have produced close to a 90% utilization of the m-CHP

• In 2017, Enbridge teamed up with ATCO for a residential-energy-emissions pilot project called the Alberta Hybrid House Project. the two companies retrofitted seven employee-owned homes in Calgary and Edmonton with micro-generation technologies—solar panels and a natural-gas-fired, micro-combined heat and power (m-CHP) unit

• Alberta government partnered with Alberta Milk and provided a one-time grant for ATCO Ltd. to install 24 Aisin 1.5 kW m-CHP units in dairy farms across the province that began in fall 2019

31

Natural Gas CHP Assessment (Micro CHP)

Micro CHP ( Apartment Building)

32

Micro CHP technology 100 kW Packaged ICEAnnual Operating Savings Compared to No CHP $79 kPayback (year) 10NPV $45 kIRR 8%

Facility Description Apartment High riseFacility size (sq. m) 13,824Floors 18Number of units /Occupancy 142Monthly Electricity consumption 150,320 Monthly Fuel consumption_MMBtu 1,301

electricity price 2019 ($/kWh) $0.1NG price 2019 ($/MMBtu) $6.0the efficiency of thermal equipment 80%the CHP equipment service life (Years) 20Incentives NoDiscount Rate 7%

Micro CHP (Hospital)

33

Micro CHP technlogy 550 kW Packaged ICEAnnual Operating Savings Compared to No CHP $181 kPayback (year) 9.5NPV $185 kIRR 9%

Facility Description Hospital/InpatientFacility size (sq. m) 18,725Floors 5Monthly Electrcity consumption (kWh) 384,936 Monthly Fuel consumption_MMBtu 2,616

electricity price 2019 ($/kWh) $0.1NG price 2019 ($/MMBtu) $2.6the efficiency of thermal equipment 80%the CHP equipment service life (Years) 20Incentives NoDiscount Rate 7%

Determining the Value of DG

34

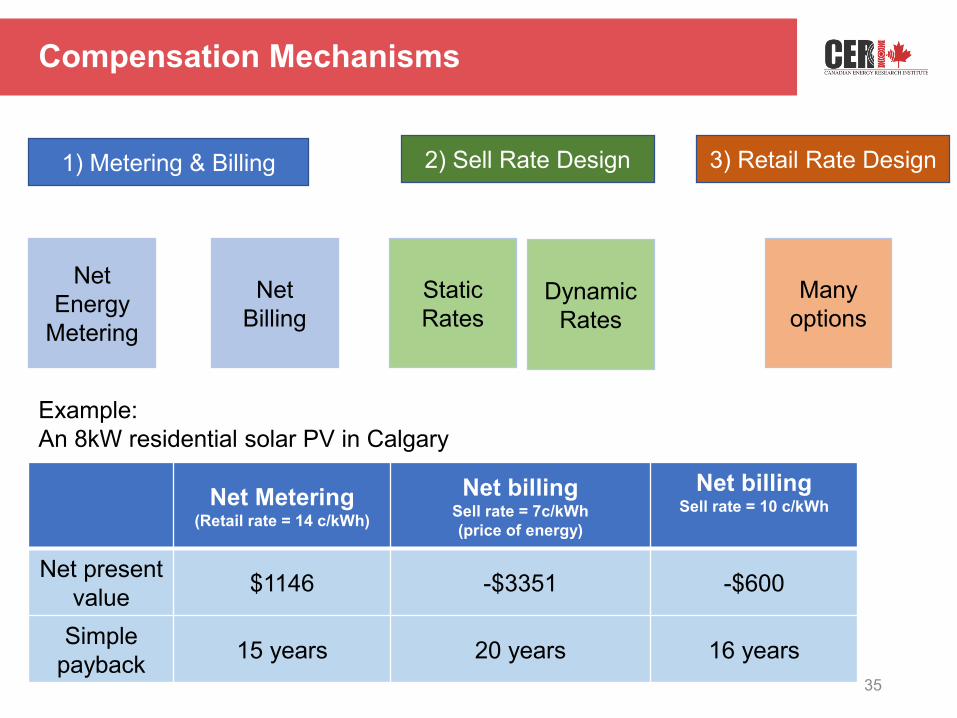

Compensation Mechanisms

35

1) Metering & Billing 2) Sell Rate Design

Net Energy

Metering

Net Billing

Static Rates

Dynamic Rates

Example:An 8kW residential solar PV in Calgary

Net Metering(Retail rate = 14 c/kWh)

Net billingSell rate = 7c/kWh(price of energy)

Net billingSell rate = 10 c/kWh

Net present value $1146 -$3351 -$600

Simple payback 15 years 20 years 16 years

3) Retail Rate Design

Many options

Observations & Unanswered Questions

• DG is being promoted in most of Canada• Going forward, Solar PV is likely one of the most widespread DG

technologies • Compensation mechanisms must be designed by balancing the

private and public costs and benefits of DG• Public benefits and costs of DG (e.g., savings due to differed

assets, demand reduction) are difficult to quantify • CERI study will quantify some of the public benefits and costs• Higher quality data is available for some DG resource

assessments• More work is needed with technologies such as biomass, MSW,

and systems level cost benefit analysis

36

37

Opportunities for Distributed Generation In Canada

• Final report• A comprehensive data portalExpected to be published by the end of May, 2020

QUESTIONS?

38

Please submit your text questions and comments using the Questions panel.

A recording of the presentation will be sent to you following the event.

UPCOMING EVENTS

39Register at www.ceri.ca/events

40

THANK YOUCanadian Energy Research Instituteceri_canada

Visit www.ceri.ca for the latest research

Appendix – Compensation Mechanisms

41

Net Energy Metering

42Figure Source: Zinaman, Owen, et al. "Grid-connected distributed generation: compensation mechanism basics." National Renewable Energy Laboratory: Golden, CO, USA (2017).

Net Billing

43Figure Source: Zinaman, Owen, et al. "Grid-connected distributed generation: compensation mechanism basics." National Renewable Energy Laboratory: Golden, CO, USA (2017).

Buy All, Sell All

44Figure Source: Zinaman, Owen, et al. "Grid-connected distributed generation: compensation mechanism basics." National Renewable Energy Laboratory: Golden, CO, USA (2017).

Appendix – DG policies & programs

45

Saskatchewan

DG Policies

• Small Power Producer Program (2007)• Limit of 100kW systems

• Power Generation Partner Program (2018)• Limit of 1MW for renewable technologies• Limit of 5MW for flair gas and waste heat generation

• Net-Metering Program (2018)• Replaces the Small Power Producer Program (capacity limit of

100kW)

46

Saskatchewan

Results

• Net-Metering program reached its 16MW cap two years in advance

• The second round is offering a less generous rate structure to subscribers

• Power Generation Partner Program has resulted in 20MW of capacity from waste heat generation

• A cap of 10MW per year of installed capacity for renewable sources• A cap of 25MW per year of installed capacity for flare gas and waste

heat recovery

• SaskPower is prepared to add between 70 and 105 MW of new installed capacity within the next 3 years

47

Manitoba

DG Policies

• In 2003, Manitoba Hydro published the Technical Requirements for Connecting Distributed Resources to the Distribution System

• Less than 200kW systems under net-billing mechanism• Greater than 200kW systems under PPA contracts with Manitoba

Hydro

• Solar Energy Pilot Program (2016)• Subject to net-billing mechanism• Only for PV systems• Generating limit size of 200kW

48

Manitoba

Results

• No data available for the Technical Requirements for Connecting Distributed Resources to the Distribution System

• Solar Energy Pilot Program resulted in 2.6MW of installed capacity

• Program was cancelled in May, 2018• The subsidies included in the program were deemed too costly (i.e.,

risk of rate increases)

• New government agency (Efficiency Manitoba) to take over some energy related initiatives

• No clear direction in terms of DG

49

Quebec

DG Policies

• Net-Metering Program (2016)• Less than 50kW systems

Results• No reports available• Quebec generates about one third of total Canadian generation• Well connected in every direction – net exporter of electricity• They have the lowest electricity bills for consumers in the country• The government is not keen about promoting DG

50

New Brunswick

DG Policies

• Locally Owned Renewable Energy Projects that are Small in Scale ~ LORESS (2015)

• NB Power directed to contract 80MW of renewable energy

• Net-Metering Program • Systems less than 100kW

• Embedded Generation Program • Systems between 100kW and 3MW• Cap of 20MW• Subject to FIT compensation (long-term fixed price)

• Community Energy Program• Targeting First Nations communities • Cap of 40MW

51

New Brunswick

Results

• Net Metering program is ongoing• No official reports on total installed capacity

• Embedded Generation Program – fully subscribed• 20MW of capacity

• No information available regarding the progress of the Community Energy Program

52

Prince Edward Island

DG Policies

• Renewable Energy Act (2005)• Mandated utilities to source at least 15% of electricity from

renewables

• Net-Metering Program (2005)• Official regulatory framework to promote DG• Systems with generating capacity less than 100kW

• Amendments to the Renewable Energy Act (2015)• Cancelled the mandate to source 15% of electricity from renewables

53

Prince Edward Island

Results

• No official results on the Net-Metering program

• The province is officially pursuing other policies to address the high costs of electricity

• Energy efficiency and conservation• Demand management• Promote utility-scale solar generation project

54

Newfoundland and Labrador

DG Policies

• Provincial Energy Plan: Focusing our Energy (2007)• Commitment to develop a regulatory framework to promote DG

• Net-Metering Policy Framework (2015)• Systems with generating capacity less than 100kW• Provincial cap of 5MW

• Biogas Electricity Generation Pilot Program (2015)• Systems with less than 2MW of capacity• Participants get compensated a variable rate (90% of the avoided

system marginal cost) • Provincial cap of 5MW

55

Newfoundland and Labrador

Results

• Net-Metering Policy Framework• As of 2019, there were 419.5kW of installed capacity • Newfoundland and Labrador Hydro has one customer under this rate

structure (18kW)

• Biogas Electricity Generation Pilot Program• No official reports

56