Rethinking health innovation from the South - Some south driven initiatives

Open Services Innovation: Rethinking Your Business to

C t d G i N ECompete and Grow in a New Era

K t P t ti t VIA L d F XIIKeynote Presentation to VIA Leaders Forum XII

Henry ChesbroughHaas School of Business, UC Berkeley

Esade Business SchoolOpen Services Innovation Presentation by Professor Henry Chesbrough is licensed under a Creative Commons Attribution 3 0 Unported License

© 2011 Henry Chesbrough 1

Open Services Innovation Presentation by Professor Henry Chesbrough is licensed under a Creative Commons Attribution 3.0 Unported License.Permissions beyond the scope of this license may be available at www.openinnovation.net.

2003

2006

© 2010 Henry Chesbrough 22011

The Current Paradigm: The Current Paradigm: ggA Closed Innovation SystemA Closed Innovation System

ScienceThe

Market

Science&

Technology MarketTechnologyBase

ResearchInvestigations

Development New Products /Services

3R D

Open Innovationp

O

Other firm´s market

Our new market

I t l

License, spin out, divest

Internal technology base

Our currentI t l/ t l Our current market

External technology

Internal/external venture handling

External technology insourcing

External technology base

Stolen with pride from Prof Henry Chesbrough UC Berkeley, Open Innovation: Renewing Growth from Industrial R&D, 10th Annual Innovation Convergence, Minneapolis Sept 27, 2004

Open Innovation:Then and Now

Then

• In April of 2003, the term “open innovation”In April of 2003, the term open innovation yielded ~200 Google pages, before I published the bookthe book

Now

• In April of 2010, a search on the same term yielded 21 9 million pages!yielded 21.9 million pages!– 5 orders of magnitude in 7 years

2003: We broke up the fortress 2003: We broke up the fortress …

Philips Research,Ronald Wolf, 10/08

Bringing in the right partners – Open innovationBringing in the right partners Open innovation

> 75 companies and > 75 companies and > 7000 people at High Tech Campus Eindhoven

Research institutes

Corporate innovators

Economic development companies

Consultancy & services

Philips Research,Ronald Wolf, 10/08 7

The expansion of the corporate funnelp p

InsourcedIdeas /Technology ODM

OEM

Spin inStart upsIP insourcing AcquisitionsOEMIP insourcing Acquisitions

Front – end Development Commercializa

Incubators Spin outIP LicensingAlliances

Philips Research,Ronald Wolf, 10/08

Philips’ Open Innovation Tools, MethodsOI Power Questions Patent Scans

Literature Scans

Co-creation platforms

Landscape Expert

Internet searchesLandscape Expert

Networks

SMIS MarketSMIS Market Scans

ConnectUs

Website portal

9

DIY NDATechnology CarrouselSupplier

Roadshow

Procter & Gamble

• P&G used to be a VERY closed organization– “We invented Not Invented Here” – J. Weedman

• P&G financial crisis in 2000• P&G financial crisis, in 2000– Missed a series of quarterly financial estimates– Stock market lost confidence in the company– Stock price fell by more than half in 4 months!– CEO (Jagr) was fired

© 2008 Henry Chesbrough 10

P&G’s Stock Price: 8/1998-3/2000P&G s Stock Price: 8/1998-3/2000P&G Stock Price

120

130

100

110

80

90

Pric

e pe

r sha

re

60

70

P

40

50

98 98 98 98 98 98 98 98 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 00 00 00 00 00 00 00

© 2008 Henry Chesbrough 11

9/17/199810/1/199810/15 /199810/29 /199811/12 /199811/26 /199812/10 /199812/24 /1998

1/7/1 9991/21/1999

2/4/1 9992/18/1999

3/4/1 9993/18/1999

4/1/1 9994/15/19994/29/19995/13/19995/27/19996/10/19996/24/1999

7/8/1 9997/22/1999

8/5/1 9998/19/1999

9/2/1 9999/16/19999/30/199910/14 /199910/28 /199911/11 /199911/25 /1999

12/9/199912/23 /1999

1/6/2 0001/20/2000

2/3/2 0002/17/2000

3/2/2 0003/16/20003/30/2000

Searching for the Root Cause

• “We fundamentally had a growth problem. Our current brands were performing well. But we weren’t developing many new p g ybrands.” – C. Wynett

• To get new brands P&G needed to open up• To get new brands, P&G needed to open up.• Connect and Develop

– SpinBrush, Swiffer, Regenerist

© 2008 Henry Chesbrough 12

Example: Proctor & Gamble

A.G. LafleyPresident and CEOP&GP&G

“We will acquire 50% of our innovations from outside P&G”

Jeff Weedman 28 External Business Development managers

VP, External Business Development

Nabil Y. SakkadSVP, R&D, Global Fabric & Home Care

“There’s 1 5 Million people in the world who“We don’t care where good ideas come from.”

There s 1.5 Million people in the world who know about my business. I want them on my

team”

Larry Huston (just retired)120 Technology Entrepreneurs

VP, Knowledge & Innovation, Corporate R&D

P&G Share Price Restored!

The New P&G

• Many processes to enable open innovation– Technology scouts– Legal templates for IP, partneringLegal templates for IP, partnering– Investments in Innovation Intermediaries

Th G l N B h• The Goal Now: Become the open innovation partner of choice

© 2008 Henry Chesbrough 15

Motorola’s Razr

© 2010 Henry Chesbrough 16

Initial Success

• More than 50 million units sold• Motorola became world #1 handset

manufacturermanufacturer

• Then….

© 2010 Henry Chesbrough 17

… The Trap Closes

• Motorola Krazr not a hit• Nokia phones overtake Motorola

Becomes the new #1– Becomes the new #1– Plus new entrants from Asia:

S• Samsung• HTC

• Motorola falls to #7 handset manufacturer todayy

© 2010 Henry Chesbrough 18

Nokia’s Own Trap

• Nokia becomes world leader in handsets• Global distribution, cost leader• Strong position in emerging economies• Strong position in emerging economies• But…

© 2010 Henry Chesbrough 19

The Trap Closes…. The Trap Closes

Ph b l i l di• Phones become gateway to multiple media and uses– Users personalize phones with apps

A l RIM d G l b ildi i ifi t• Apple, RIM and Google building significant platforms for third parties to build upon– Microsoft also trying to get back in

• Nokia remains #1 in units but not in profit• Nokia remains #1 in units, but not in profit

© 2010 Henry Chesbrough 20

Paul Horn’s ProblemPaul Horn s Problem

• More than half of IBM’s revenue is coming from its Global Services business

• Circa 2004, few if any IBM Research Staff were working on services innovation opportunitiesworking on services innovation opportunities

• How to sustain Industrial Research, if that research is not relevant to more than half ofresearch is not relevant to more than half of the company’s business?

21© 2010 Henry Chesbrough

Innovation in Products and Technologies

=

Innovation in Services

22© 2010 Henry Chesbrough

Porter’s Value ChainPorter s Value Chain

Source: Michael Porter, Competitive Advantage, 198523© 2010 Henry Chesbrough

A Services Value WebA Services Value Web

BoundaryCo‐

creationCustomer

Engagement

Boundaryof the Firm

Customer

Elicit TacitService

Customer Experience Surrounding

EnvironmentKnowledgeOffering ‐ Partners

‐ Complementors‐ Investors

Design Experience Points

Investors‐ Third Parties

24© 2010 Henry Chesbrough

This is Not New ThinkingThis is Not New Thinking• “What the customer buys and considers value is never aWhat the customer buys and considers value is never a

product. It is always utility – that is, what a product does for him.”

– Peter Drucker, Management: Tasks, Responsibilities, Practices

• “People don't want to buy a quarter‐inch drill. They want a quarter‐inch hole!”

– Ted Levitt, Marketing Myopia

• “… it is the customer who drives the business, and customers are not differentiating between personalized, customized, or standardized offerings; they just want to get what they want.”

F k Pill 2007– Frank Piller, 200725© 2010 Henry Chesbrough

The Utilization DifferentialThe Utilization Differential

• Assume your car is driven 12,000 miles/year

• Assume your average speed is 30 mph

• You are driving the vehicle for roughly 400 hours– There are 8,760 hours in a yearThere are 8,760 hours in a year

– Therefore, your utilization is about 4.6%

• If your transportation were a service that untapped• If your transportation were a service, that untapped 95.4% becomes a source of value

Share vehicle acquisition operation maintenance costs– Share vehicle acquisition, operation, maintenance costs

– A potential Economy of Scale

26© 2010 Henry Chesbrough

Diamler’s Car2Go ServiceDiamler s Car2Go Service

• Carsharing program: www.car2go.comL h d i Ul G i• Launched in Ulm, Germany in

2008; Austin, TX in 2010• Ultra‐convenient: no fixed station to pick up or drop off; no required return time• No upfront commitment: no psecurity deposit, monthly fee, reservation cost

© 2010 Henry Chesbrough 27

UPS – Open Services Changes p gCustomers’ Processes

Customer CustomerCustomerOperations

CustomerShipping

CustomerOperationsOperations

UPS takes over customers’

© 2010 Henry Chesbrough 28

UPS takes over customers shipping dept!

Amazon – Open Services Creates Economies of Scope

• Amazon allows third party merchants to use its own tools tomerchants to use its own tools to create Amazon web pages• Creates consistent shopping experience for users • Increases “share of wallet” for AAmazon• Makes Amazon.com a more attractive Internet destination forattractive Internet destination for merchants

© 2010 Henry Chesbrough 29

Amazon Web Services – Open Services Creates Economies of Scale

• Amazon hosts other companies’ web sitescompanies web sites

• Converts fixed server farms to variable costs for customerscustomers• Increases Amazon’s utilization of its servers• Lowers Amazon’s own costs as a result

• Rapidly growing and profitable business forprofitable business for Amazon

© 2010 Henry Chesbrough 30

Asian PaintsAsian Paints

• Paint is a true commodity

• Fragmented distributionFragmented distribution– Distributors, jobbers, retailers, applicators

N i ibili f d f A i P i– No visibility of end customer for Asian Paints

– Little “do it yourself” interest by customers

• Brand Repositioning failed

• How to sustain differentiation?• How to sustain differentiation?

© 2010 Henry Chesbrough 31

Asian Paint’s PlatformAsian Paint s Platform• Provide the “back end” function for its distribution partners– Each applicator job had its own record– Save them time, money, and more information – Now Asian Paints can see through to the end customer for the first time!customer for the first time!

• Tremendous savings in supplying paints, fewer out‐of‐stock situationsout‐of‐stock situations

• Differentiation vs. competition, without relying on pricerelying on price

© 2010 Henry Chesbrough32

Evolution of d d lSemiconductor Business Models

System System System System

dTSMC IP

Foundry

Foundry

Open InnovationPl f

CaptiveMemory

IDMMemory Chip

DesignChipDesign

Platform External IP

Design Design

Integrated IDM FablessF d

TSMCOpen InnovationSystem Model Foundry

ModelOpen Innovation

Platform 33

© 2010 Henry Chesbrough

Implications for LeadershipImplications for Leadership …

El t th i t l d i i• Elevate the importance placed on services in your organization.

• Identify the utility of your offering to your• Identify the utility of your offering to your customers. How can you enhance it?

• Search for underutilized assets in your• Search for underutilized assets in your organization, and ways to unlock their value

• Create a platform that intertwines your product• Create a platform that intertwines your product and your service. Invite others to participate, both customers and third parties.p– Look for platforms you can join, to expand your business

© 2010 Henry Chesbrough 34

35© 2010 Henry Chesbrough

BackupBackup

© 2010 Henry Chesbrough 36

Concept Map – Open Services Innovation

Thi k f

Service Value Chain UtilizationProduct Platforms

Service Platforms

Changing the Offer

Think of Your

Business as a ServiceNew Revenue Models

Open Open

a Service

Transformed Tacit Knowledge

Knowledge AdvantageNew Revenue Models

Inertia

Services InnovationServices

InnovationCo‐CreationBusiness

Models

Experience PointsCoherence

Open I i

Customers Innovate TooFront End/Back End Platforms, part II

InnovationIntegration of InternalAnd External Knowledge

Increased Participation Ecosystems

Economies of Scale

Economies of Scope

Increased Participation Ecosystems

37© 2010 Henry Chesbrough

Top Ten Nations in 2003 by Labor Force SizeA = Agriculture, G = Goods, S = Services

Nation % WWLabor

% A

%G

%S

25 yr %delta S

China 21.0 50 15 35 191

India 17 0 60 17 23 28India 17.0 60 17 23 28

U.S. 4.8 3 27 70 21

Indonesia 3 9 45 16 39 35Indonesia 3.9 45 16 39 35

Brazil 3.0 23 24 53 20

Russia 2 5 12 23 65 38Russia 2.5 12 23 65 38

Japan 2.4 5 25 70 40

Nigeria 2 2 70 10 20 30Nigeria 2.2 70 10 20 30

Banglad. 2.2 63 11 26 30

Germany 1.4 3 33 64 44

38

Germany 1.4 3 33 64 44

>50% (S) services, >33% (S) services Source: http://www.nationmaster.comOECD reports; IBM Corporation© 2010 Henry Chesbrough

Business Model Maturity StagesBusiness Model Maturity Stagesy gy g6. Platform business

model

6 Stages: 5. Integrated business d l

modelope

4. Externally aware business model

model

en

3. Segmented business model

y

2.Differentiated business model

3. Segmented business model

clos

1 Undifferentiated business model

2.Differentiated business model ed

39

1. Undifferentiated business model

© 2010 Henry Chesbrough

Selection of Vehicle

Delivery of Vehicle

Maintenance of Vehicle

Information & Training

Payment/ Financing

Protection/ Insurance

Car Purchase or Lease

Customer chooses

Customer picks from dealer stock

Customer does this

Customer does this

Customer, dealer or third party

Customer provides

Lease (Product focused

h)

dealer stock third party

approach)

Taxi Supplier chooses

Customer is picked up

Supplier does this

Supplier does this

By the ride, based on

Supplier provideschooses picked up does this does this based on

time and distance

provides

Enterprise Car Rental

Customer chooses from local

Customer picks up, or is picked up

Supplier does this

Supplier does this

By the day Customer is responsible

stock

Zip Car Customer chooses

From ZipCar locations

Supplier does this

Supplier does this

By the hour Customer purchaseschooses

from local stock

locations does this does this purchases from supplier40© 2010 Henry Chesbrough

Services PlatformsServices Platforms

• How can you sustain differentiation in services?– Little or no IP

Observable experiences– Observable experiences

– Therefore, easy to copy (?)

© 2010 Henry Chesbrough 41

Services PlatformsServices Platforms

H i diff i i i i ?• How can you sustain differentiation in services?– Little or no IPOb bl i– Observable experiences

– Therefore, easy to copy (?)

• Service Platforms can sustain differentiation• Service Platforms can sustain differentiation– Platform: a multi‐sided market The company’s technologies become the basis for others’– The company s technologies become the basis for others technologies and innovations

– The company is able to shape the direction of evolutionp y p– Others invest their money, making your service more valuable (value multiplier): iFund

© 2010 Henry Chesbrough 42

By understanding and accelerating work evolution, Service Science will impact productivity of human-tool systems

ToolSystem

HumanSystem

Collaborate(incentives)

Augment(tool)

Help meby doing some ( ) ( )

of it for me(custom) 21 Z

Automate(self-service)

Delegate(outsource)

Help meby doing allof it for meof it for me

(standard)Organize People

(Socio-economic models with intentional agents)Harness Nature(Techno-scientific models with stochastic parts)

43

Example: Call Centers

Collaborate(1970)

Augment(1980)

Delegate(2000)

Automate(2010)

M k t L t h (I di ) T h l V i t

Example: Call Centers

43

Experts: High skill people on phones Tools: Less skill with FAQ tools Market: Lower cost geography (India) Technology: Voice response system

Source: IBM Research

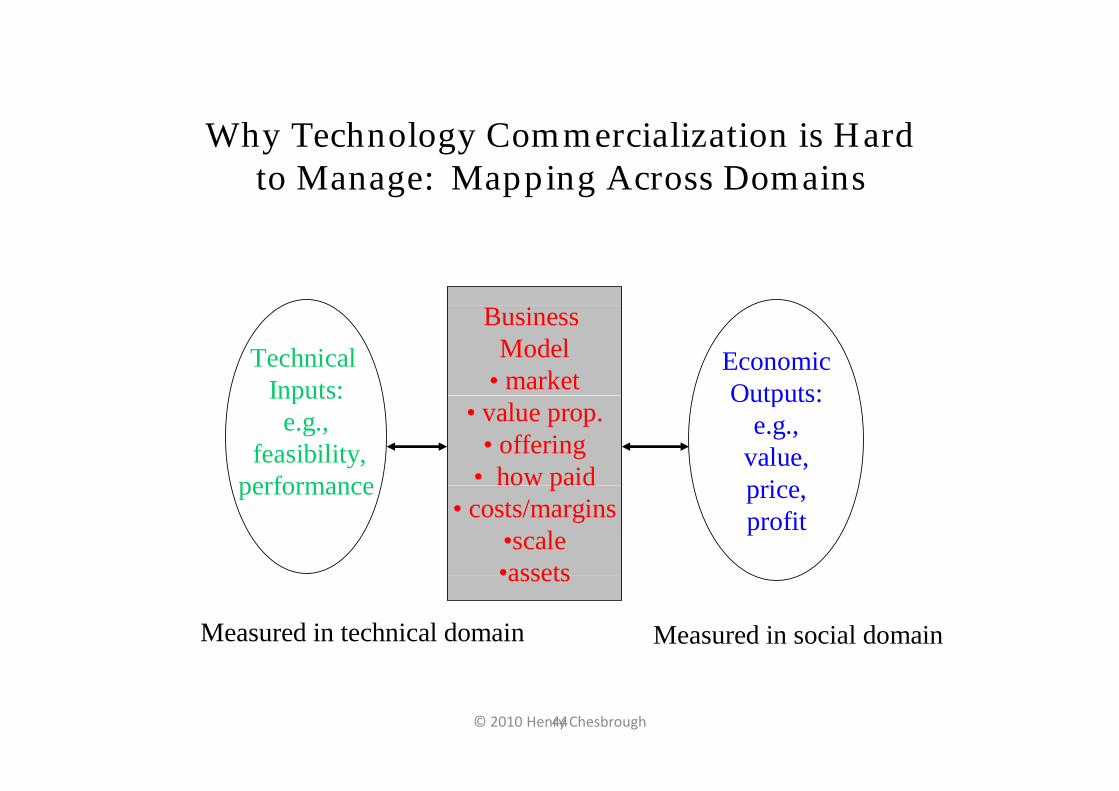

Wh T h l C i li ti i H d Why Technology Commercialization is Hard to Manage: Mapping Across Domains

Technical Inputs:

EconomicOutputs:

Business Model

• marketInputs:e.g.,

feasibility,performance

Outputs:e.g.,

value,i

• value prop.• offering

• how paidperformance price,profit

ow pa d• costs/margins

•scale•assets•assets

Measured in technical domain Measured in social domain

44© 2010 Henry Chesbrough

Engineering Business ModelsEngineering Business Models

• Given path‐dependent effects and cognitive limits on search….

• Can organizations develop processes to construct refine and pro actively changeconstruct, refine, and pro‐actively change their business models?

45© 2010 Henry Chesbrough

Other Companies StudiedOther Companies Studied

• IBM• IBM• Xerox• GE Aircraft Engines• Johnson & Johnson• Music industry• KLM Airlines (Holland)• KLM Airlines (Holland)• Ericsson (Sweden)• TSMC (Taiwan)• London Tube/Alstom (UK)• Asian Paints (India)• ShaanGu (China)ShaanGu (China)• SSIPEX (China)• El Bulli (Spain)

© 2010 Henry Chesbrough 46

Blueprint for Overnight Hotel Stay Service Common Restaurant, Mikko Järvilehto – Innovation in Services and Business Models Course

Physical Evidence Menu

ElevatorsHallways

Cart for bagsEmployee

Delivery trayFood

BillLobbyRoom

AmenitiesFood

Desk PaperworkHotel exterior Cart for bags

EmployeeAd/WebsiteRestaurant exterior

Employees desk and

Interior, Table and

Drink /Food

Employees Supply of f d& RestroomBill

Restaurant exteriorPay

C t

Evidence MenuHallwaysRoom

Employee dress

Food appearance Hotel exterior

Parking

AmenitiesBathroom

FoodLobbyKey

Parking Employee dress

Ad/Website exteriorParking

desk anddress

Table andtableware

/Food menu

memo food&drinks

RestroomBill exteriorParking

Pay options

O t

Customer Actions Give bags to

bellperson Arrive at hotel Check in Go to room Receive bags Call room service

Receive food Sign/tip Eat Sleep/shower Check out

and leaveMake

reservation

Line of Interaction

Arrive at restaurant

Ask for table

Go to table

Receive menu

Order drinks and food

Eat OrderBill

Pay Visit Toilet

Leave

Onstage Contact

Employee Actions

Greet and take bags

Process registration Deliver bags Deliver food Process

checkout

Line of Visibility

Greet &Check re‐servations

EscortUse payment system

Delivermenu

Write order

DeliverFood

DeliverBill

Backstage Contact

Employee Actions

Make reservation for guest

Take bags to room

Take food order

Li f I t l I t ti

Take food Order

Support Processes

Prepare food Registration system

Registration system

Reservation system

Line of Internal Interaction

Payment system

PrepareFood

TableChart

47© 2010 Henry Chesbrough

48© 2010 Henry Chesbrough