OMAR WAQQAS 760314-T131 WASEEM BAHADUR 870202-T216418118/FULLTEXT01.pdf · OMAR WAQQAS 760314-T131...

87

OMAR WAQQAS 760314-T131 WASEEM BAHADUR 870202-T216 Corporate Social Responsibility and Corporate Governance for Sustainable Service Business A Case Study of Zong (China Mobile Pakistan) and Telenor in Pakistan Business Administration Master‟s Thesis 30 ECTS Term: HT 2010 Supervisors: Samuel Petros Sebhatu Bo Enquist

Transcript of OMAR WAQQAS 760314-T131 WASEEM BAHADUR 870202-T216418118/FULLTEXT01.pdf · OMAR WAQQAS 760314-T131...

OMAR WAQQAS 760314-T131

WASEEM BAHADUR 870202-T216

Corporate Social Responsibility and Corporate Governance for Sustainable

Service Business

A Case Study of Zong (China Mobile Pakistan) and Telenor in Pakistan

Business Administration

Master‟s Thesis

30 ECTS

Term: HT 2010

Supervisors: Samuel Petros Sebhatu

Bo Enquist

1

ABSTRACT

In the last decade or so the climate of doing business changed dramatically, coming up with

many new dimensions of the business. A few of them are service dominant logic, corporate

social responsibility and corporate governance. The notion of a „business case‟ for corporate

sustainability has increasingly been used by the corporate sector, environmental

organizations, consultancies and by many others to seek justification for sustainability

strategies within organizations.

These concepts if not complete but must have major impact on all business decisions now a

days. No business can survive longer by disintegrating itself from these practices. So it has

become the need of the hour to understand these terms and incorporate them in business

social culture, to be part of responsible corporate citizenship in today‟s business world.

Moreover, the paper will try to study the level of CSR activities according to CSR pyramid in

terms of economical, legal, social and philanthropic aspects and these will be analyzed with

gathered data about companies under review. The research work undertaken will focus on

CSR and CG practices prevailing in telecom sector of Pakistan especially taking Zong as our

case study basis and Telenor for its comparison. The research will see the internal service

dimensions and will analyze if the business is based on five principles of value based service

business. The paper is qualitative in its nature, relying on the data obtained through

interviews regarding the companies under discussion.

2

ACKNOWLEDGEMENTS

We would like to take this opportunity to first of all thank Almighty Allah who has given us

the courage to do this thesis. Then our families back home who were very supportive and

encouraging in every up and down times during the tenure of this thesis so that to take up and

complete this thesis in time.

We would like to express our gratitude to our supervisors Bo Enquist and especially Samuel

Petros who guided us all the way and made it possible to successfully complete our thesis

project. They always assisted us in best possible manner with their professional insights and

experience on the subject matter.

In last we are thankful to all the people at different organizational levels in companies. In

Zong Mr. Usman was very helpful in guiding and providing the information relevant to our

thesis and at government level Mr. Kashif from Pakistan Telecommunication Authority who

has been very helpful in providing valuable comments about the topic despite of his busy

schedule and to all of our friends who helped us to complete this thesis successfully through

their positive suggestions and inputs all the time.

_________________ ________________

Omar Waqqas Waseem Bahadur

3

ABBREVIATIONS

KPMG Klynveld Peat Marwick Goerdeler

CML China Moile Limited

SECP Securities and Exchange Commission of Pakistan

PTA Pakistan Telecommunication Authority

CMPak China Mobile Pakistan

CSR Corporate Social Responsibility

CG Corporate Governance

SOX Sarbanes-Oxley

NYSE New York Stock Exchange

CEO Chief Executive Officer

COSO Committee of Sponsoring Organizations

GSM Global System for Mobile Communications

ICT Information Communication Technology

HR Human Resource

HRSI Human Resource Solutions International

SIG Special Interest Groups

SSDL Sustainable Service Dominant Logic

GRI Global Reporting Initiatives

NGO Non-Governmental Organization

MD Managing Director

IFRS Financial Reporting Standards

WBCSD World Business Council for Sustainable Development

4

MOU Memorandum of Understanding

GIEs Globally Integrated Enterprises

TBL Triple Bottom Line

5

TABLE OF CONTENTS

CHAPTER 1 INTRODUCTION, RESEARCH BACKGROUND AND MOTIVATION 8

1.1 Introduction ................................................................................................................. 8

1.2 Research Background and Motivation ........................................................................ 8

1.3 Conceptual framework of Corporate Social Responsibility and Corporate

Governance .......................................................................................................................... 10

1.4 Research Purpose and Aim of study ......................................................................... 13

1.5 Research questions .................................................................................................... 13

CHAPTER 2 RESEARCH DESIGN AND METHODOLOGY ........................................ 14

2.1 Research Approach ................................................................................................... 14

2.1.1 Qualitative research method .............................................................................. 14

2.2 Research Method ....................................................................................................... 15

2.2.1 Case Study ......................................................................................................... 15

2.2.2 Data collection method ...................................................................................... 16

2.3 Reliability .................................................................................................................. 17

2.4 Limitations of research .............................................................................................. 17

CHAPTER 3 THEORETICAL FRAMEWORK ............................................................... 19

3.1 Sustainable development ........................................................................................... 19

3.2 Stakeholder Theory ................................................................................................... 20

3.3 Corporate Social Responsibility ................................................................................ 22

3.3.1 CSR Pyramid ..................................................................................................... 22

3.3.2 CSR and Corporate Image ................................................................................. 25

3.3.3 Tipple Bottom Line ............................................................................................ 25

3.4 Corporate Governance............................................................................................... 28

3.5 Integration of CSR and CG ....................................................................................... 30

3.6 Sustainable Service Business and Values Based Business ....................................... 31

3.6.1 Measuring internal service dimensions .............................................................. 31

6

3.6.2 Values Based Business ...................................................................................... 32

CHAPTER 4 EMPIRICAL STUDY .................................................................................... 34

4.1 Overview of Telecommunication Sector of Pakistan .............................................. 34

4.1.1 Subscriber wise- cellular market share .............................................................. 34

4.1.2 Telecom indicators ............................................................................................. 35

4.1.3 Economic Indicators .......................................................................................... 37

4.1.4 Cellular mobile infrastructure sharing ............................................................... 37

4.2 Company Profile ....................................................................................................... 39

4.2.1 CSR strategy and management .......................................................................... 41

4.2.2 CSR Strategy ...................................................................................................... 41

4.2.3 CSR Management .............................................................................................. 42

4.2.4 Stakeholder Engagement ................................................................................... 44

4.2.5 Corporate Governance ....................................................................................... 46

4.3 Comparative study of Zong with Telenor ...................................................................... 56

4.3.1 Offering mobile financial services ..................................................................... 56

4.3.2 Corporate Responsibility ................................................................................... 56

4.3.3 CSR Objective and strategy ............................................................................... 58

4.3.4 HR policies for employees at Zong: .................................................................. 59

4.3.5 Zong Initiatives regarding CSR development: .................................................. 60

4.3.6 Corporate Governance ....................................................................................... 61

4.4 Government‟s role in terms of CSR and CG............................................................. 61

CHAPTER 5 DISCUSSION AND ANALYSIS ......................................................................... 63

5.1 Stakeholder theory..................................................................................................... 63

5.2 Corporate Social Responsibility ................................................................................ 64

5.3 CSR Pyramid ............................................................................................................. 64

5.4 Triple Bottom Line .................................................................................................... 65

5.5 Corporate Governance............................................................................................... 66

5.6 Integration of CSR and CG ....................................................................................... 66

5.7 Sustainable Service Business and Values Based Business ....................................... 67

7

5.6.1 Measuring internal service dimensions of Zong ................................................ 67

5.6.2 Five principles for a sustainable values based service business ........................ 69

CHAPTER 6 CONCLUSION .................................................................................................... 73

Future research and recommendations................................................................................. 74

REFERENCES ....................................................................................................................... 76

Web sources ......................................................................................................................... 82

Annual Reports: ................................................................................................................... 83

Interviews ............................................................................................................................. 83

LIST OF FIGURES

Figure 1: Basic two-tier Stakeholder map 21

Figure 2: The Pyramid of Corporate Social Responsibility 24

Figure 3: Triple Bottom line 26

Figure 4: Subscriber wise- Cellular market share 35

Figure 5: History and Milestones: CSR Management at China Mobile 43

Figure 6: China Mobile Stakeholders 45

LIST OF TABLES

Table 1: Annual Cellular Subscribers 35

Table 2: Foreign Direct Investment in Telecom Sector 36

Table 3: Telecom Revenues 36

Table 4: Telecom Investment 36

APPENDIX .................................................................................................................................

8

CHAPTER 1 INTRODUCTION, RESEARCH BACKGROUND

AND MOTIVATION

1.1 Introduction

The paper will discuss about corporate social responsibility (CSR) and corporate governance

(CG) in telecom sector of Pakistan taking the case of Zong into the consideration. The first

chapter explains introduction, research background and motivation. It also includes

conceptual framework of CSR and CG, research purpose and aim of study and then research

questions. Chapter two contains research design and methodology which includes research

approach, research method, reliability and limitations of research. Chapter three is about

theoretical framework in which we discussed sustainable development, stakeholder theory,

corporate social responsibility, corporate governance, integration of CSR and CG, sustainable

service business and values based business. Chapter four relates to the empirical part in

which we have given overview of telecommunication sector of Pakistan, company profile,

comparative study of Zong with Telenor and government‟s role in terms of CSR and CG.

Chapter 5 consists of discussion and analysis of theories that were included in the research.

Chapter six is about conclusion whereas in last we discussed future research and

recommendations.

Business will play a pivotal role in meeting the sustainability challenges of the 21st century

(International Institute for Sustainable Development [IISD] 2010). For the business

community, sustainability is more than mere window dressing. By adopting sustainable

practices, companies can gain competitive edge, increase their market share and boost

shareholder value. The growing demand for green products has created many new markets in

which sharp eyed eco-entrepreneurs are reaping rewards (IISD 2010).

1.2 Research Background and Motivation

Presently businesses are facing competition while providing services to customers both

locally and internationally. At local and international level companies have to be concerned

about the standards and the competitors and about what they are providing to the customers.

Today companies are moving towards internationalization and in that they have to meet the

9

international standards to compete and succeed in the market. They also need to be concerned

about environment, social and economic aspects if they want to meet the current market

challenges. Companies are moving from products to services and are facing the issues of

environment, social and economic those are termed as Corporate Social Responsibility

(CSR). These three elements or factors are very important for any company that wants to

compete internationally and locally within the country.

CSR is ―A concept whereby companies integrate social and environmental concerns in their

business operations and interact with their stakeholders on a voluntary basis (Commission of

the European Communities 2006). This trend is clearly visible globally as more and more

business owners have started to pay attention for social implications of their activities.

Corporate social responsibility is a commitment by business towards ethical behavior (Moir

2001), when it all begins. It is not only about how companies manage the business processes

to produce but an overall positive impact on the society (Baker 2008).

Today those companies that are concerned with the Corporate Social Responsibility through

its business are known around the world in service sector. H&M, IKEA, Starbucks, Lego and

many other companies are working on the CSR aspects from years and are laying the

foundations of CSR practices. Moreover, another term that is also important in today‟s

business world is Corporate Governance (CG). Companies are following CG rules and

implementing them in their daily business routines and activities. Selznick (1994) argues that

governance is more than management and has to take account of all the interests that affect

the viability, competence and moral character of an enterprise. Both CSR and CG are the part

of today‟s successful businesses that has integrated them in their operations.

We have studied Corporate Social Responsibility (CSR) and Corporate Governance (CG) and

understood their importance in today‟s business world. We developed our interest in CSR and

CG codes, their use and importance therefore wanted to study them further through practical

example. Like some other countries of the world Pakistan is also a good place for business

investment in services and other fields, we have seen investments by renowned companies

that are working and known internationally. Many local and international companies in

Pakistan are also working on CSR and CG concepts and adapted them as they started their

operations. We have undertaken our research on two companies that are Zong (China

Mobiles Pakistan) and Telenor providing telecom services to the people of Pakistan. In

10

addition this report will focus on existing CSR and CG practices in both companies i.e. Zong

and Telenor in Pakistan. And we will be taking the case of Zong as a case study of our paper

and comparing it with the Telenor practices in terms of CSR and CG. In this way a qualitative

comparative study will be done.

1.3 Conceptual framework of Corporate Social Responsibility and

Corporate Governance

According to Blowfield and Frynas (2005) Corporate Social Responsibility can be used as an

umbrella term for a number of theories and practices all of which accepts the following: (a)

that companies have a responsibility for their impact on society and the natural environment,

sometimes away from legal compliance and the responsibility of individuals; (b) that

companies have a liability for the behavior of others with whom they do business (e.g. within

supply chains); and (c) that business needs to manage its relationship with wider society,

whether for reasons of commercial viability or to add value to society. This definition also

gives the link between business and society through CSR.

The trend is clearly visible globally as more and more business owners have started to work

on social implications of their activities. Corporate social responsibility is a commitment by

business towards ethical behavior (Moir 2001), when it all begins. It is not only about how

companies manage the business processes to produce an overall positive impact on the

society (Baker 2008). But, as Carroll (1979) describes, it covers all the four kinds of

responsibilities namely economic, legal, ethical and discretionary, which companies have to

make a strategic decision. The development of the involvement of companies and the

emergence of sustainability thinking in business together can be seen as a pro-active driving

force (Edvardsson & Enquist 2009).

CSR„s role in tackling problems concerning corporate responsibilities of a company and its

link with the society and environment has been a very controversial subject (Enquist et al.

2007). It is normally professed that CSR is not what is written in company„s code of conduct

or annual reports. That is only one portion of total CSR plans used by the company. In

general social responsibilities of an organization have to include all the three bottom lines:

Ecological, Economic and Social.

11

The notion of CSR is not novel to business world as commonly determined. Corporate social

responsibility was not difficult to understand as we all know that the debate on ―polluting

organizations started at least in the 1970´s, which afterwards recycling, fair trade market

practices, good governance, safe packaging, sustainable development, and accountability

comes into view (Vogel 2005). In the past companies have been practicing CSR but most of

the time it has been sighted as something to fill annual reports and corporate public relation

statements or super facial. In fact, it has never been taken effectively so as to make it part of

corporate business strategy. And we don„t have enough business cases to argue for (Vogel

2005).

Corporate social responsibility is not only about Philanthropy. The under lying theme of

corporate social responsibility is that business and society are interlinked rather that distinct

entities (Wood 1991). CSR is also concerned with economic, social and environmental

aspects and philanthropy is only a small part of social aspect. Corporate social responsibility

is fast gaining importance as more and more firms are realizing its value (Chaudhry &

Krishnan 2007). Recently, business owners all over the world have started to think in terms

of integrating CSR activities into their core business strategies and started to assess its

repercussions gravely. Kotler and Lee (2005) mentioned CSR has to guarantee competitive

advantage and strategic gains.

Based on literature reviews, internet research and interviews with company stakeholders this

study attempts to draw a comparative analysis between two telecom companies operating in

Pakistan‟s cellular communications industry. The focus is on how these companies

themselves identify issues as their corporate social responsibility and how these companies

plan to deal with such issues. This study also explores how these companies integrate CSR in

their strategic planning and overall business model. Further, this study also investigates what

strategies these company apply in order to implement their CSR initiatives and how their

outcome can be measured.

According to Mallin (2007) corporate governance is the way the companies govern their

businesses and this depends on which stage of corporate governance development are they.

Corporate governance development depends on many underlying theories. The main

affecting theories of corporate governance development are as agency theory which points

out the agency relationship between principal and agent where the principal delegates work to

12

the agent so when it comes to the corporations, principals are the owners and agents are the

directors of the corporations. The other theory is transaction cost economics which

determines a corporation as a governance structure. So the selection of a better governance

structure will streamline the interests of directors and shareholders. Stakeholder theory not

only focuses on the shareholders but takes a wider view and takes the perspective of

stakeholders into consideration and the governance structure of the corporation may have

some direct involvement of stakeholder groups (Mallin 2007). In stewardship theory the

directors are treated as the stewards of the corporation‟s assets and are considered to act in

the best interest of the shareholders. In class hegemony theory the directors of the corporation

view themselves as an elite and remain at the top of the corporations and supposed to include

and promote new directors considering how well they are suited for and in this elite group. In

managerial hegemony theory the management of the corporation with their knowledge of

business operations of the corporation may reasonably dominate the directors as to reduce the

influence of the directors in the corporation.

The main theory in above discussed theories is the agency theory which affects the

development of the corporate governance most but nowadays it looks that stakeholder theory

is more in lime light as corporations now becoming more and more aware of the fact that they

cannot perform in isolation without the interaction with their stakeholders and giving the

shareholder its due position in the affairs of the business of the corporation who is a very

pivotal stakeholder of a corporation (Mallin 2007).

Sustainable Service Business and Values Based Business are discussed in the paper to better

understand the concept of CSR and dimensions to measure the internal service quality of the

business as: helpfulness, promptness, communication, tangibles, professionalism, reliability,

confidentiality, flexibility, preparedness and consideration were used to see how good Zong

is implementing and working on these dimensions. Five principles of sustainable value based

service business were also used that are: Strong values drive customer value, CSR as a

strategy for sustainable service business, Values based service experience for co-creating

value, Values based service brand and communication for values resonance and Values based

service leadership for living the values and these were analyzed with reference to Zong.

13

1.4 Research Purpose and Aim of study

The main aim of this study is to assess corporate social responsibility and corporate

governance from a service business perspective in the case of Zong Pakistan. The paper will

assess how the principles of sustainability and corporate governance are incorporated into

everyday business activities of Zong. Comparison of Zong Pakistan with the Telenor in terms

of CSR and CG practices has done for the case analysis. Moreover, we looked into China

Mobile Limited (CML); the parent company of Zong Pakistan for better understanding of

CSR and CG perspectives.

The paper has analyzed how Zong is incorporating sustainable service research into their

business strategies and daily practices. This report will provide a chance to study the CSR

and CG in the telecom sector of Pakistan and their future will be discussed.

1.5 Research questions

The paper will try to look into the CSR and CG practices in Zong, compare it with Telenor

and will try to answer following questions through qualitative case study research:

What are the CSR and CG practices in Zong and its comparison with Telenor?

How CSR and CG practices can benefit the organization like Zong in providing better

services to their customers?

What are internal service dimensions and how they can be measured?

14

CHAPTER 2 RESEARCH DESIGN AND METHODOLOGY

2.1 Research Approach

This thesis is structured to follow a qualitative comparison of two case companies which have

a successful image of Corporate Social Responsibility (CSR) and Corporate Governance

(CG). We will be demonstrating and comparing their CSR and CG activities starting from

their intended strategies to their realized strategies.

Bryman and Bell (2007) describes that it is a research strategy that usually emphasizes words

rather than quantification in the collection and analysis of data. Also Maxwell (2005)

mentions that qualitative research approach emphasizes words rather than numbers and

focuses on specific situations or people.

Many researchers as Carroll (1999) in article Corporate Social Responsibility Evolution of a

Definitional Construct, Edvardsson, B. and Enquist B. in their article Values-based Service

for Sustainable Business: Lessons from IKEA (2009) and Sebhatu, S.P. in his paper

Corporate Social Responsibility for Sustainable Service Dominant Logic (2010) has used

qualitative research method for case study analysis. Therefore we have used the qualitative

research method in our research. This helped us to better understand about the

implementation of CSR and CG in the case study of Zong and Telenor because implications

of these practices are difficult to quantify. As we used the qualitative method, we used data

available through annual reports, online data on company‟s websites and through the

interviews and secondary data from different articles on the subject matter.

2.1.1 Qualitative research method

Bryman and Bell (2007) explains that the question of how well the case study fares in the

context of the research design criteria cited early, measurement validity, internal validity,

external validity, ecological validity, reliability and replicability - depends in large part on

how far the researcher feels that these are appropriate for the evaluation of case study

research. Therefore we considered the case study approach for our research paper.

15

2.2 Research Method

2.2.1 Case Study

A case study is one which investigates specific research questions that may be fairly loose to

begin with and which seeks a range of different kinds of evidence, evidence which is there in

the case setting, and which has to be abstracted and collated to get the best possible answers

to the research questions (Gillham 2000) further (Gerring 2004) argues that case study is a

thorough study of a lone component with an aim to simplify across a larger set of units

therefore case study is just not the way to analyze or model but it is a particular way of

defining cases.

Case study can be seen to satisfy three tenets of the qualitative method: describing,

understanding, and explaining. The literature contains numerous examples of applications of

the case study methodology. The body of literature in case study research is "primitive and

limited" (Yin 1994), in comparison to that of experimental or quasi-experimental research.

Case study evaluations can cover both process and outcomes, because they can include both

quantitative and qualitative data (Tellis 1997). Case studies can be theoretically exciting and

data rich (Cassell & Saymon 2004) and further it is mentioned that the case study is suited to

the research questions that are designed to analyze and study the organization in particular

context. Therefore case study method is used to study a particular example and gives the

results in that context.

Johnson (2007) in his paper “Stakeholder Dialogue for Sustainable Service”, Edvardsson and

Enquist (2009) in their book Values-based Service for Sustainable Business: Lessons from

IKEA and Sebhatu (2010) in his paper Corporate Social Responsibility for Sustainable

Service Dominant Logic, (Enquist et al. 2007) in the paper values-based service quality for

sustainable business have used the case study approach for the analysis in their research

papers.

Our research study is based on exploratory research that is mainly used in qualitative

approaches and involves the use of primary and secondary data through interviews,

observations, focus groups, articles, journals, periodicals to get up to date information.

Secondly, for our research we have used the deductive reasoning approach which states that

we start with theory then make the hypothesis which is followed by the observations and in

the last confirmation is made about the research (Bryman & Bell 2007). In our case the

16

research questions are made instead of hypothesis as we are using the qualitative research

methodology.

We have used the case study approach in our thesis and will try to come up with results to

support our questions. We feel that this approach is relevant to our research as it requires

deep insights into certain situation and also for studying the concepts of CSR and CG. In our

case we have taken two companies operating in same industry which are selected as case

studies with huge activity across diversified value added services range but with similar end

user base that are Zong (China Mobile Pakistan) and Telenor Pakistan.

2.2.2 Data collection method

Qualitative research method involves the interviewing, participant observations and

unstructured interviewing, because these methods are viewed as particularly helpful in the

generation of an intensive, detailed examination of a case (Bryman & Bell 2007).

According to Merriam (1988), qualitative data obtained from documents, interviews and

observations is based on qualitative case study method that is mostly relied on the above

methods of data collection. In this regard the data may come from different sources through

structuring the case studies that can be: participant-observation, physical artifacts, archival

records, documentation, interviews and direct observations. These are sources that can be

used to collect data and help in case study but all these sources are not relevant in every case

study. They change as per the case and requirement of study and available data to the

researcher (Yin 2002).

To make a study on these two case companies, we gathered the data by using primary and

secondary data. Mainly documented data in the form of written materials such as annual

reports, case studies in the similar filed, literature reviews, CSR annual reports of Zong and

Telenor and companies websites were used. Through comparative research design we will

focus on objects that are similar in some contexts and different in some contexts.

To find answers for research questions, analysis of data will be done by using comparative

research method. Mainly focus will be established to expose orderly structure and would be

on general findings to our topic which will be based on rational framework. We have used

deductive research approach for our case study analysis. Moreover we conducted several

interviews of both the company officials as well as government representatives from telecom

17

regulatory authority in Pakistan. These interviews were the basis of our case study which

gives an overall view of CSR and CG practices in both under discussion companies. In

interviews observation method was used and questions posed were open ended to have

maximum information from the respondents. The concepts of CSR and CG were introduced

to respondents before the start of interview so that they may answer the questions relevant to

our topic.

2.3 Reliability

One of the necessary requirement for a research paper is that it should be trustworthy and the

viewer may see it steady and dependable (Gummesson, 2000; Alvesson and Sköldberg,

2008).We have tried our best in collecting the data from reliable sources. We relied on

interviews for our analysis which are mainly based on our previous knowledge on the subject

matter. In interviews we tried to put open ended questions, to get maximum information

about our research areas. The information gathered through interviews was then validated

through different theories regarding CSR and CG.

2.4 Limitations of research

Information regarding CSR and CG normally is not well defined, explained and available in

not consistent formats over the company‟s websites and online sources. There are

internationally agreed formats like Global Reporting Initiatives (GRI) and International

Financial Reporting Standards (IFRS) used for CSR reporting but these are still not in vogue

and very few companies are using them in their annual reports.

Companies in general have less knowledge and awareness about CSR and CG; as a result we

were not able to get deep information through company representatives. As far as our case

study is concerned, Telenor and China Mobile both are big companies but Telenor is working

in Pakistan since 2005 and Zong (CM Pak) started its business in 2008. Both the companies

involve many external stakeholders including direct customers, indirect customers,

government, NGOs, suppliers and etc. that lead to difficulty in collecting data. At first we

intended to collect the secondary data over the internet from company‟s websites and primary

data by making qualitative research (interviews and discussions) but Zong has not given

anything relevant to CSR and CG on its website and no proper reports were available for this

purpose so we have to rely more on other sources.

18

As the result, we conducted the interviews of company officials and Pakistan

Telecommunication Authority (PTA) officials. Therefore to make our research more reliable,

we have focused on existing interview available online of Chief Executive Officer (CEO) and

Managing Director (MD) of Zong. Findings from our research would be based on our two

focused companies that may not depict the whole picture of entire population of telecom

sector of Pakistan.

19

CHAPTER 3 THEORETICAL FRAMEWORK

3.1 Sustainable development

The real meaning of sustainable development is a constant affiliation among human actions,

including the desires to get better their way of life and the sentiment of well being on one

hand, and the natural world‟s resources and ecosystem on the other. This concept aims not to

reduce the prospects for future generations to enjoy a quality of life at least as good as our

generations (Mintzer 1992).

According to The Bruntland Report (1987) economic development, social development and

environmental protection are the three dimensions that are concerned with the sustainable

development. As per World Business Council for Sustainable Development (WBCSD) “The

continuing commitment by business to behave ethically and contribute to economic

development while improving the quality of life of the workforce and their families as well as

the local community and society at large” 1

In 1981 Freer Spreckley first articulated the triple bottom line in a publication called 'Social

Audit - A Management Tool for Co-operative Working' as he described what Social

Enterprises should include in their performance measurement. The phrase was coined by

John Elkington in his 1998 book Cannibals with Forks: the Triple Bottom Line of 21st

Century Business (Brown et al. 2006).

This concept aims to not diminish the prospects for future generations to enjoy a quality of

life at least as good as our generations (Mintzer 1992). In our opinion sustainable

development is for the people itself, for everybody who uses the nature and wants to make

nature long lasting for next generation. Nowadays people are using the nature in both direct

and indirect ways which they may do not even know that they are going to destroy the

environment, nature which finally will reverse to harm human itself, if the people in this

generation do nothing. The influence of sustainable development is growing and accepted

1 www.wbscd.org

20

from all people. Moreover, due to the environmental issue, many researchers are concerning

about environment that many natural resources can be run out if we do not use it wisely.

According to social, environment and sustainability reporting and organizational value

creation by Gray (2006), organization can create value to the planet to be sustainable based

on the logic of economic development. That mentions about the value creation in

organization, we should consider the one who can cooperate together, that are the

stakeholders. It can be a group or individual affiliated to the organization, who perceive the

value, share interest that can be both internal and external of the organization. However

business sustainable society has complexity in implementing but it is the best solution to

persuade the organization into better ways.

3.2 Stakeholder Theory

Freeman (1984, pp. 25) explains about stakeholder as “any group or individual who can

affect or is affected by the achievement of the firm‟s objectives”. He also explains in his

article that those groups or individuals if not support the organization then the organization

will not be able to survive. Stakeholder theory not only concerns about maximizing the

shareholders profit but all other people who are concerned with the organization directly or

indirectly (Freeman 1984).

Further Freeman (1984) in his effort, Strategic Management: A Stakeholder Approach has

laid very fine ground for the stakeholder theory. Key (1999) mentions about the observable

fact that Freeman tries to clarify is the relationship with its external environment and

behavior within this environment of firm. Stakeholders are mainly distributed among two

groups as internal and external. Internal stakeholders mean the people within the firm while

external stakeholders refer to people or organizations outside of firm.

Donaldson and Preston (1995) developed stakeholder model although this model did not

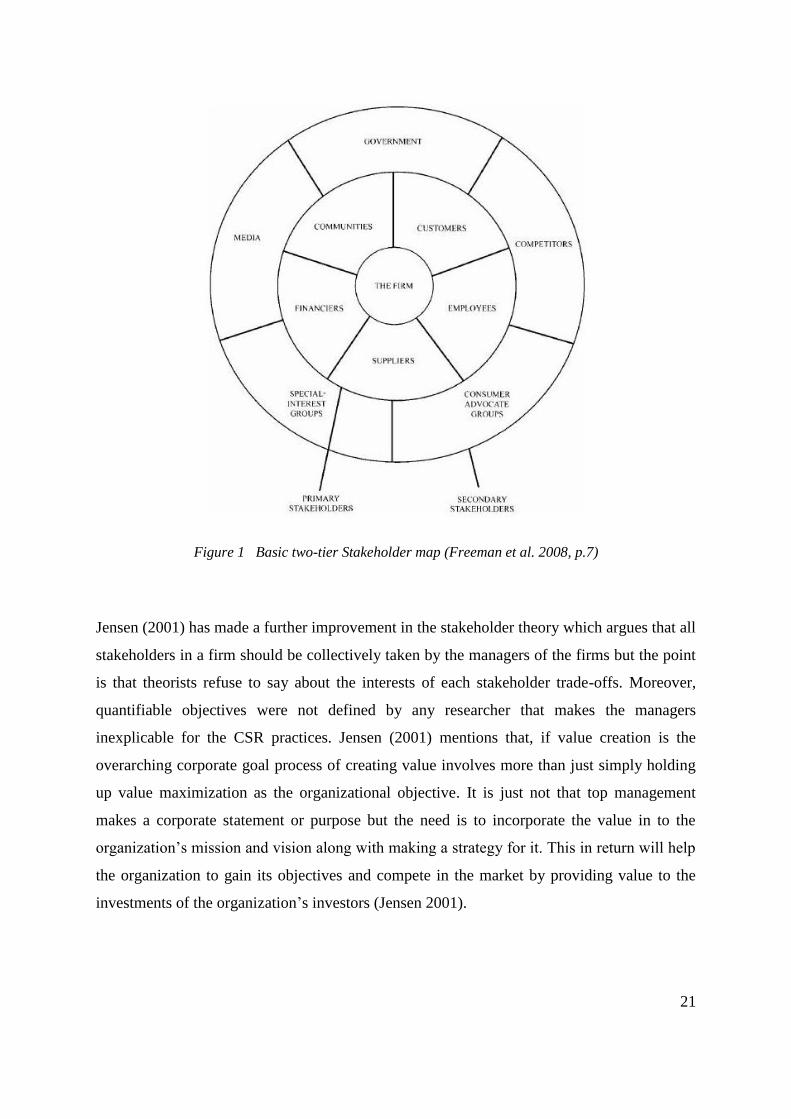

mention an important stakeholder which is media. In figure 1 we can see media is also a

stakeholder of a firm given by (Freeman et al. 2008) where they talked about several

stakeholders instead of talking about only shareholders. They have distributed the model in

two circles one with external stakeholders that are government, competitors, consumer

advocate groups, special interest groups and media and internal stakeholders that influence a

company as suppliers, financiers, communities, customers and employees. Company must

identity its key stakeholders for the long term sustainability and profitability.

21

Figure 1 Basic two-tier Stakeholder map (Freeman et al. 2008, p.7)

Jensen (2001) has made a further improvement in the stakeholder theory which argues that all

stakeholders in a firm should be collectively taken by the managers of the firms but the point

is that theorists refuse to say about the interests of each stakeholder trade-offs. Moreover,

quantifiable objectives were not defined by any researcher that makes the managers

inexplicable for the CSR practices. Jensen (2001) mentions that, if value creation is the

overarching corporate goal process of creating value involves more than just simply holding

up value maximization as the organizational objective. It is just not that top management

makes a corporate statement or purpose but the need is to incorporate the value in to the

organization‟s mission and vision along with making a strategy for it. This in return will help

the organization to gain its objectives and compete in the market by providing value to the

investments of the organization‟s investors (Jensen 2001).

22

3.3 Corporate Social Responsibility

It is being noticed that Corporate Social Responsibility (CSR) has turn into an appealing

topic; so far there is no accurate definition for this term. With regard to its nature it is a multi-

disciplinary subject covering a broad range of issues in operating business. Different authors

have introduced different definitions; some of them are as follows:

Carroll (1991) argues that these four categories as economic, legal, ethical and philanthropic

of corporate social responsibilities can be represented as a pyramid, in which economic

responsibilities are the foundations upon which all other responsibilities are based and

without which they cannot be accomplished and philanthropic responsibilities are on the top

of the pyramid.

Blowfield and Frynas (2005) defines CSR, as an umbrella term for a variety of theories and

practices all of which recognize the following: (a) that companies have a responsibility for

their impact on society and the natural environment, sometimes beyond legal compliance and

the liability of individuals; (b) that companies have a responsibility for the behavior of others

with whom they do business (e.g. within supply chains); and that (c) business needs to

manage its relationship with wider society, whether for reasons of commercial feasibility, or

to add value for the society.

Corporate social responsibility (CSR) is a citizenship function with social, ethical and moral

responsibility among a company and its customers (Maignan & Ferrell, 2001).

These definitions are used to explain and understand the concept of CSR with other

definitions by other authors and are used in terms of action and responsibilities to society and

environment. This also explains about how an organization should apply social and

environmental implication in their business procedures.

3.3.1 CSR Pyramid

The development of CSR is widely spread around the world. Many companies are interested

in adopting CSR, From “Doing Good to Do Good” is the old style of CSR (Vogel 2005) ,

using CSR to build good reputations to the community, such as charity. So, this was more

into the top of the CSR pyramid called as philanthropic activities. And adopt into new CSR

practice from “Doing Good to Do Good” to be “Doing Good to Do Well” which are under

the core values of sustainable business by emphasizing on balancing between economical,

23

social, and environmental perspectives into the business. Therefore, CSR can be understood

as the voluntary integration of social and environmental concerns into business operations

and interactions with stakeholders (Enquist et al. 2006).

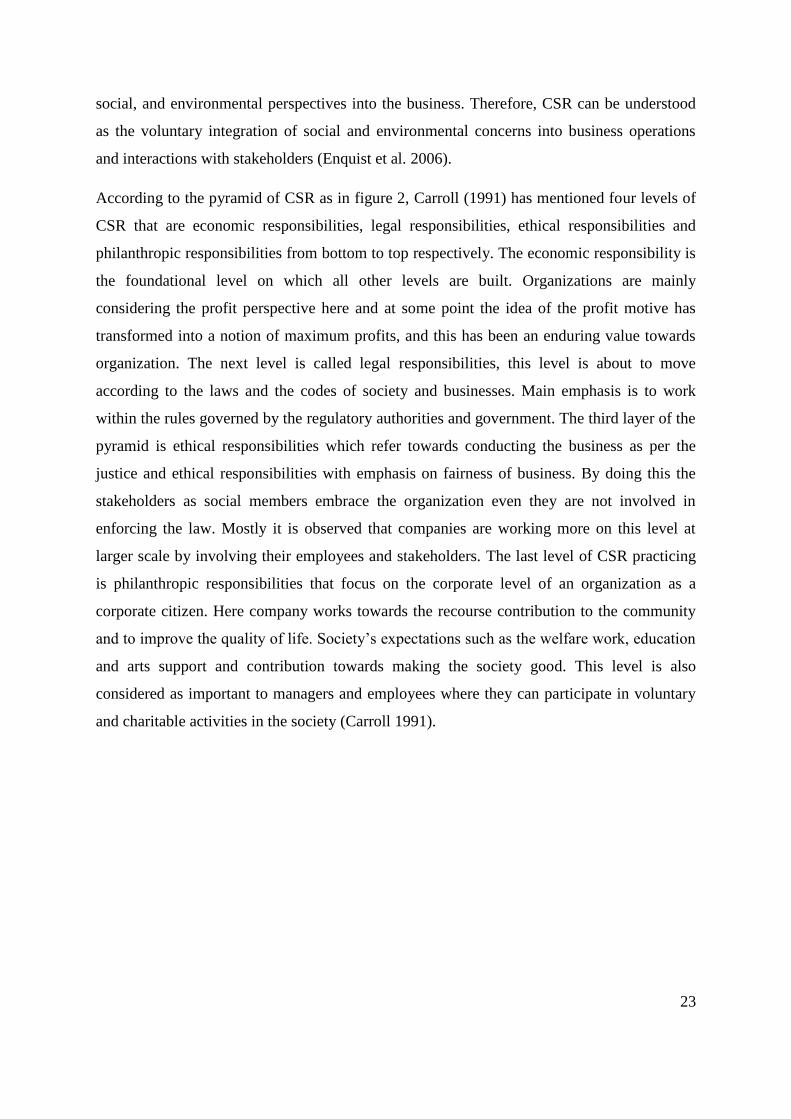

According to the pyramid of CSR as in figure 2, Carroll (1991) has mentioned four levels of

CSR that are economic responsibilities, legal responsibilities, ethical responsibilities and

philanthropic responsibilities from bottom to top respectively. The economic responsibility is

the foundational level on which all other levels are built. Organizations are mainly

considering the profit perspective here and at some point the idea of the profit motive has

transformed into a notion of maximum profits, and this has been an enduring value towards

organization. The next level is called legal responsibilities, this level is about to move

according to the laws and the codes of society and businesses. Main emphasis is to work

within the rules governed by the regulatory authorities and government. The third layer of the

pyramid is ethical responsibilities which refer towards conducting the business as per the

justice and ethical responsibilities with emphasis on fairness of business. By doing this the

stakeholders as social members embrace the organization even they are not involved in

enforcing the law. Mostly it is observed that companies are working more on this level at

larger scale by involving their employees and stakeholders. The last level of CSR practicing

is philanthropic responsibilities that focus on the corporate level of an organization as a

corporate citizen. Here company works towards the recourse contribution to the community

and to improve the quality of life. Society‟s expectations such as the welfare work, education

and arts support and contribution towards making the society good. This level is also

considered as important to managers and employees where they can participate in voluntary

and charitable activities in the society (Carroll 1991).

24

Figure 2 The Pyramid of Corporate Social Responsibility (Carroll 1991, p.42)

The pyramid of corporate social responsibility as in figure 2 and mentioned above is divided

into four levels. Starting from foundation step about economic performance, at the same time

business is expected to obey by law as the social codification of acceptable behavior. And

come to next level is the ethic responsible which is at its most fundamental level, this is the

obligation to do what is right, just and fair, and to avoid or minimize harm to stakeholder.

And the last step is the philanthropic that about the charitable expectation from social

responsibility wherein business in this time is expected to add financial and human resources

to the community and to improve the quality of life.

There are five key areas to focus on corporate activities to implement for good CSR, which

are financial performance, the treatment of the workforce, impact on the market place, impact

on environment, and commitment to promoting human rights. Furthermore, media as an

important stakeholder is focusing more on the environmental issues as fundamental. So if

firm is not able to fulfill the environmental and social responsibility, then the media acts by

25

spreading the news to the people. The response of the people towards the firm would be

negative that will harm the company‟s profit. The best way in the interest of the firm would

be to reduce the conflicts and increase confidence about the firm among their stakeholders as

a result this will protect their brands (Waddock & Bodwell 2007). Porter and Kramer (2006),

mentions about the philanthropic activities that is in decline but can be of competitive

advantage to the organization when used in a positive way that can lead towards long-term

sustainability. By using the CSR perspectives and considering it while providing at the same

time products in markets it can be beneficial to the company as well as to its stakeholders.

3.3.2 CSR and Corporate Image

This part will illustrate that how CSR and corporate image are interrelated. Morsing and

Beackmann (2006) agreed on adopting CSR actions so companies tries to focus on the

capability of value to make their company‟s identity and name by building its brand image or

building trust of stakeholders including customers, supplier, business partners and others.

Moreover, companies that are working and incorporating CSR practices in their business are

reporting the payback into their name and their bottom line. Therefore, in most of the big

corporations, it is seen as an essential tool for developing and improving the image of the

corporation in public. Also, annual reports highlighted with explanation of companies'

attempts to be fair, green and responsible which can be referred to as “Sustainable

Development Report” As the result, people who viewed annual reports will have positive

image about the company (Mattila 2009).

3.3.3 Tipple Bottom Line

Literature review shows that Triple Bottom Line (TBL) was first phrased by John Elkington

in 1994 and subsequently in 1997 in his book Cannibals with Forks: the Triple Bottom Line

of 21st Century Business (Elkington 2004). TBL term was used by Elkington in public,

together with an article in the California Management Review on „win–win–win‟ business

strategies (Elkington 1994), Sustainability‟s 1996 report Engaging Stakeholders and 1997

book Cannibals with Forks: The Triple Bottom Line of 21st Century Business (Elkington

1997). TBL focuses on three aspects namely economic, ecological and social. TBL notion

requires the responsibility of stakeholders rather than shareholders in order to increase the

organization‟s value. This also consists of its profitability, shareholder values and its social,

human and environmental capital (Savitz & Weber 2006). Moreover, it attempts to put

together not only the environmental and social aspects, but also the economic factors. TBL is

26

a complicated approach; many companies are only in start to discover the real repercussions

of its use and implementation. Also, it discusses about three important fundamentals together

as environmental responsibility, social equity and economic performance. By implementing

the TBL concept, several companies expect to be able to take more efficient and sustainable

method to manage business risks, handle the concerns of society and to identify new business

opportunities, as well as likely obstacles (Henriques & Richardson 2004).

Figure 3: Triple Bottom line (Source: Sustainability Assessment and Reporting

for the University of Michigan's 2002, p.8)

TBL is mainly divided into three spheres that are also interlinked together as shown in figure

3 and discussed below:

i. Economic

TBL refers to both economic and financial bottom lines. Financial is concerning about money

which is tangible, distributed and shared. On the other hand, economic is a concept that

embraces the relationships between policies decision, institution, theories and choices that

27

affects the production. Economic and social aspects cannot be separated and it is hard to

reject the vital relationships that guide the economic institutions (Porter 1998). The Economic

refers to the profits, cost savings, economic growth, research and development in an

organization. The profit characteristic needs to be considered by a firm as the real economic

benefit of the society. When economic aspect is integrated in social aspect (economic-social

aspects) they come up with business ethics, fair trade and worker rights as per figure 3. TBL

approach does not believe only in the organizational advantages but also the social profits

where the ethics, behaviors and practices are reflecting the profit maximization to maintain

the social and economic accountability and have a balance between economic and social

elements.

ii. Social

Social aspect of Triple Bottom Line refers to standard of living, education, community and

equal opportunity for all in the society. Furthermore the sustainable business helps towards

the development of community and the region. This also take account of monitoring the

labor, comply human rights, enhancing working conditions and making relationships with

and among labor, as well as considering any indications of social responsibility which is

achieved in the civil society movement (Bob 2002). In figure 3, the social-environmental

aspect discusses about environmental justice, natural resources stewardship locally &

globally in the sphere of TBL.

iii. Environmental

Environmental aspect includes natural resource use, environmental management, and

pollution prevention of air, water, land and waste as shown in figure 3. This element is

related to the advantages of nature in order to uphold the available resources. The aim is to do

no damage to environment and restrain environmental conditions as well as supervising and

cautiously utilizing energy and resources at the same time decreasing manufacturing waste

and contaminated materials before disposal so that the environment is safe and it is done in a

lawful way (Schaltegger et al. 2003). As in figure 3 environmental-economic aspect covers

energy efficiency, subsidies or incentives for use of natural resources that can help the

environmental resources to be sustainable and usable for the generations to come.

28

3.4 Corporate Governance

Mallin points out that there have been a number of high profile corporate collapses that have

arisen despite the fact that the annual reports of the firms showed true and fair view of the

business. These collapses have negative impacts on all stakeholders and on the society at

large. Why have such collapses occurred? What might be done to prevent such collapses

happening again? How can investor confidence be restored? The answers to all these

questions lie in good corporate governance; it can help prevent such collapses happening

again and restore investor‟s confidence (Mallin 2010). The importance of corporate

governance cannot be denied. It helps to ensure the reasonable and proper system of control

which works within a company so that the company‟s assets can be protected. It prevents any

one person to have too much power or influence which can hurt the business operations.

Corporate governance is concerned with the relationship between company‟s management,

the board of directors, shareholders and other stakeholders; stakeholder groups consists of

employees including coworkers, provider of credit, suppliers, customers, local communities,

non government organizations and government. It aims to ensure that the company is run for

the best interest of shareholders and stakeholders. Corporate governance encourages both

transparency and accountability which investors want in corporate management and in

corporate performance.

Cadbury states corporate governance is concerned with holding the balance between

economic and social goals and between individual and communal goals (Cadbury 1992).

There are two perspectives of CG mainly categorized as narrow and the broad point of view

of CG. The narrow perspective is related to governing the interactions between the

shareholders and the top management inside a corporation. These interactions are intervened

through the board of directors (Bradley, Schipani, Sundaram, & Walsh, 1999; Hart, 1995;

cited in Mehmood & Riaz, 2008, p.1). The other perspective that is broader reflection of CG

sights it other than the affiliation among shareholders and management of corporation. This

perspective of CG explains the interaction among various constituencies. These

constituencies consist of different stakeholders such as employees, shareholders, business

partners and host societies and the inter-relationships of all these entities (Bradley et al.,

1999; cited in Mehmood & Riaz, 2008, p.1). The broader view presents CG as a complex

phenomenon and this complexity increases with the series of corporate collapse of the current

29

decade across the world on the whole in Anglophone countries (Adams et al., 2001; Clarke,

2004b; Niskanen, 2005; cited in Mehmood & Riaz, p.1). Further Mehmood and Riaz (2008,

p.1) mentions that these types of collapses of the corporations not only affect the shareholders

and investors in monetary terms but also to employees resulting in their loss of jobs who were

directly or indirectly associated with these large corporations. This in return shows the bad

governance of collapsed corporations.

Governance is about steering and stewardship. It is an essential mechanism to help the

company attain its corporate objectives and monitoring performance. CG, specifically, more

concerned with the structures and processes associated with management, decision making

and control in organizations. To govern is to accept responsibility for the whole life of the

institution. Governance takes account of all the interests that affect the viability, competence

and moral character of an enterprise (Selznick 1994). Selznick (1996) in his Admin Science

Quarterly article argues on the structure of institutions and institutionalism.

Corporate governance is the system by which business corporations are directed and

controlled. It specifies the rights and responsibilities of the different participants in the

corporation, such as the board, managers, shareholders and other stakeholders. The term

corporate governance has become everyday‟s use in the financial press for a little more than a

decade but the theories underlying it are of much earlier date and from several disciplines

including finance, economics, accounting, law, management and organizational behavior

(Enquist 2010).

Selznick states that the two functions, management and governance, coexist and interact. To

govern is to accept responsibility for the whole life of the institution. Governance takes

account of all the interests that affect the viability, competence and moral character of an

enterprise (Selznick 1994).

Socially responsible investment involves taking into consideration the ethical, social and

environmental performance of companies selected for investment as well as their financial

performance. The basic strategies for socially responsible investment are engagement,

preference and screening (Mallin 2010).

30

3.5 Integration of CSR and CG

According to Palmisano (2006), businesses are changing in fundamental ways- structurally,

operationally, and culturally- in response to globalization and new technology; as a result, the

larger companies are no longer „multinational corporations‟ (MNCs), but globally integrated

enterprises (GIEs). He also suggests „global collaboration‟, whereby various stakeholders

interact in development and learning processes.

Abela and Murphy (2008) have found that S-D logic can be a positive development for

marketing ethics because it facilitates the seamless integration of ethical accountability into

marketing decision-making. Freeman et al. (2004) conclude that business and ethics should

be seen as connected. Selznick (1994) also argues that governance is more than management

and has to take account of all the interests that affect the viability, competence and moral

character of an enterprise.

As per Tricker (1984) in his book “International corporate governance” mentions the term

governance that is not only concerned with managing the business of the company but it is

giving an overall direction to the organization, with overseeing and controlling executive

actions of management and with satisfying legal expectations for accountability and

regulation through the interests that goes beyond the corporate boundaries. Here beyond the

corporate boundaries needs the integration of CG with other organizational goals like CSR.

According to Lusch and Vargo (2006), “Organizations exist to integrate and transform micro

specialized competences into complex services that are demanded in the marketplace but

becomes more apparent in its almost immediate restatement. All economic actors i.e.

individuals, households, firms, nations, etc. are resource integrators” (Lusch & Vargo 2006).

It is also apparent that the customers are the co-creators of value so CSR and CG are also

integrated like any other resource of the firm to give value to its stakeholders. According to

van den Berghe and Louche (2005), CG and CSR can work jointly to bring transparency,

honesty, and accountability in the organizational processes.

Marsigla and Falautano (2005) have recommended that corporate governance and corporate

social responsibility ideas are progressing from philanthropic activities to valid strategies to

recover the confidence of both society and clients at large. Jamali et al. (2008) discusses that

both CG and CSR are supposed to give ongoing benefits and ensures the continued existence

of the business. Further they mention that with respect to CG, when implemented in

31

organization helps to gain the interests of employees, managers, owners and other

stakeholders that in return gives long-lasting affects to the organizational profits (Jamali et al.

2008).

3.6 Sustainable Service Business and Values Based Business

According to Enquist et al. (2008) a value based business is based on different aspects of core

company values and basic values that lead a company in producing customer value and a

sustainable service business. To see how much a business is a sustainable service business we

need to measure its internal service dimensions.

3.6.1 Measuring internal service dimensions

Reynoso and Moores (1995) used internal service dimensions to measure the service quality

with the perspective of internal dynamics of an organization as an interrelation of customers

and suppliers working together to satisfy customers. These dimensions can be used to

measure service quality of any service oriented business like in our case it is Zong. According

to Reynoso and Moores (1995) internal service dimensions to measure the quality of a service

are as follows:

i. Helpfulness:

This is the willingness of the unit to help in a courteous, approachable manner. A group of

items originally assigned to responsiveness were segmented in three parts. The first

containing items about helpfulness appeared together with items of courtesy.

ii. Promptness:

It is the ability to provide the service promptly responding rapidly to service requests. The

second group of items from responsiveness was clearly related to this dimension.

iii. Communication:

To keep the internal customer informed and consult it about progress, problems or changes

which may impact upon its activities.

iv. Tangibles:

Tangibles are the condition and physical appearance of facilities, equipment, materials and

written information of the unit.

32

v. Professionalism:

These are skills, knowledge and experience that members of the unit require to provide the

service and to give advice.

vi. Reliability:

The ability of the unit to provide the internal service required on time and correctly, including

the provision of accurate information.

vii. Confidentiality:

The unit‟s handling of confidential information and delicate situations.

viii. Flexibility:

This is the willingness of the unit to respond flexibly to unexpected situations. This was

represented by a unique, highly loaded item originally assigned to responsiveness.

ix. Preparedness:

The internal organization and resources required by the unit to be able to provide the service.

x. Consideration:

It is the understanding, recognition, trust, and honesty of the unit towards internal customer.

3.6.2 Values Based Business

A value based business is a business which depends upon the core company values and takes

guidance from basic values to make the value for the customers through its operations

(Edvardsson & Enquist 2009).

3.6.2.1 Five principles for a sustainable values based service business

According to Edvardsson and Enquist (2009) in their book Values- based Service for

Sustainable Business: lessons from IKEA have mentioned that many companies are now well

aware of the repercussions of sustainable development and the important of values based

services when it comes to environment and social responsibility. Customer value focuses on

positive service experience, well recognized brand and proactive marketing way of

interaction. For this purpose companies has to remain near to their customers, understand

their needs and provide the solutions of their needs which are in-line with the values and

living standards of customers. Five principles for sustainable values based business are:

33

i. Strong values drive customer value

Values are dynamic and should be integrated in the business model. Values are used by

customers and other stakeholders when value is accessed. The values create relationships

with customers and so represent an important loyalty driver (Edvardsson and Enquist 2009).

ii. CSR as a strategy for sustainable service business

CSR is important for rethinking the role of any company in any industry. By using CSR in a

proactive way, companies think „laterally‟ in searching for „smart‟ solutions. The logic of

values thus drives the logic of value creation (Edvardsson and Enquist 2009).

iii. Values based service experience for co-creating value

Customers‟ experiences are formed during consumption of a service. When a customer‟s

basic requirements are met, other issues make a difference. These issues are often

understated, affective and values based (Edvardsson and Enquist 2009).

iv. Values based service brand and communication for values resonance

Brands are living expressions of what a company stands for. They communicate what its

products or services can do for people. However if a company overstates what its products

can do and fails to deliver as perceived by customers, this creates unfavorable reactions both

in the market and among the company‟s employees. Using CSR to secure a values based

service brand is more than only communication about CSR with the customers; rather it is

about using CSR as basis for strategy and insuring that the service brand and communication

with all stakeholders is in resonance with the company‟s values, the customers‟ values and

the values of the whole society (Edvardsson and Enquist 2009).

v. Values based service leadership for living the values

Leaders communicate through their interactions with employees, partners, suppliers and

customers. Authentic leaders spend time with customers and employees and learn from them

(Edvardsson and Enquist 2009).

34

CHAPTER 4 EMPIRICAL STUDY

4.1 Overview of Telecommunication Sector of Pakistan

4.1.1 Subscriber wise- cellular market share

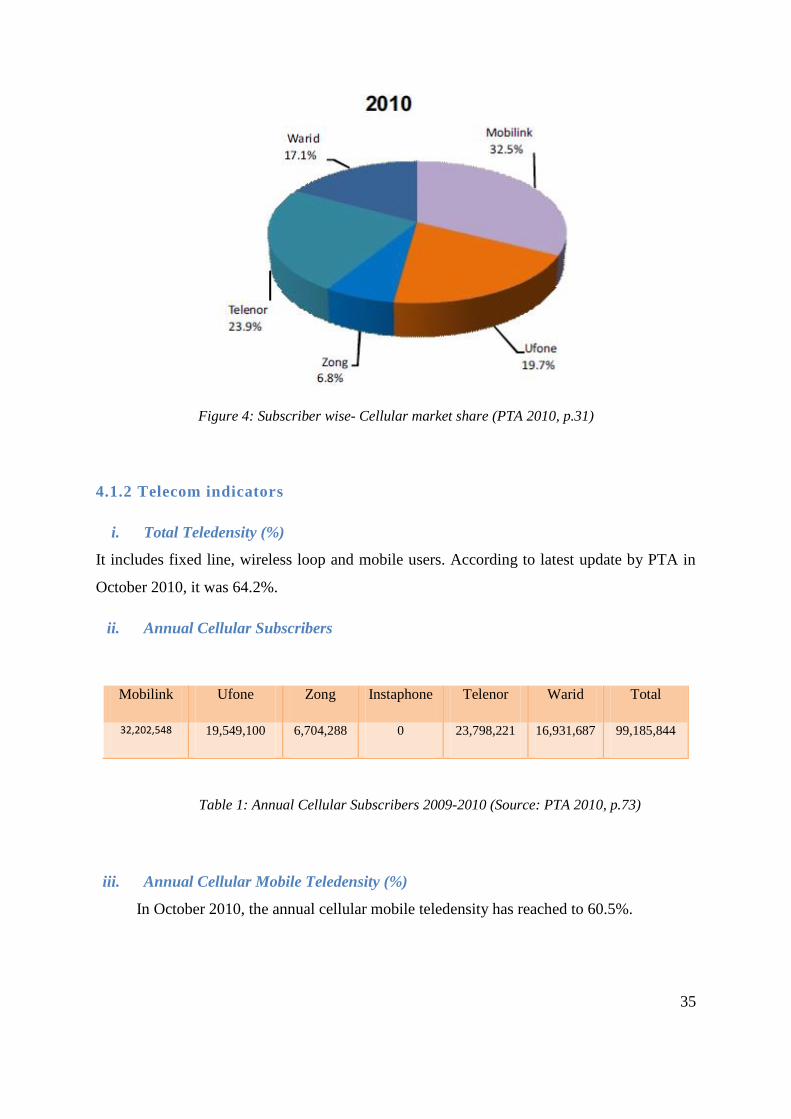

As per the PTA annual report for the year 2010 the market share of different cellular

companies operating in Pakistan varies since their operations. Figure 4 shows the market

share of different cellular companies operating in Pakistan in year 2010, where Zong has

6.8% of market share that is very less as compared to the other companies. Mobilink is

market leader with 32.5 % of market share, Telenor has the 2nd

largest market share of 23.9%,

Ufone is having the market share of 19.7% and Warid is having 17.1% of total market share.

The least market share of Zong is mainly attributed to its newness in the market as we know

they started their operations in year 2008 (Zong 2010). So we think it will catch up to other

companies with passage of time if CSR strategies are adopted according to the company‟s

values.

Mr. Usman while mentioning about the market share of the company, says that as we are new

company in the market and it just passed couple of years of operations in Pakistan. We are

committed to increase the market share in coming years to compete with Ufone and Telenor.

He again stated that it takes time to come at the same level as other companies are but they

are ambitious and expecting to increase their market share with an increase of 5 to 8 percent

in coming couple of years.

He emphasized that they are marketing out products and branding the image of Zong in a

very result oriented way. They have allocated separate budgets for the branding of Zong and

are hoping to get positive results from it.

35

Figure 4: Subscriber wise- Cellular market share (PTA 2010, p.31)

4.1.2 Telecom indicators

i. Total Teledensity (%)

It includes fixed line, wireless loop and mobile users. According to latest update by PTA in

October 2010, it was 64.2%.

ii. Annual Cellular Subscribers

Mobilink Ufone Zong Instaphone Telenor Warid Total

32,202,548 19,549,100 6,704,288 0 23,798,221 16,931,687 99,185,844

Table 1: Annual Cellular Subscribers 2009-2010 (Source: PTA 2010, p.73)

iii. Annual Cellular Mobile Teledensity (%)

In October 2010, the annual cellular mobile teledensity has reached to 60.5%.

36

iv. Foreign Direct Investment in Telecom Sector:

(US $ million)

Year FDI in Telecom Total FDI Telecom (%) Share

2009-10 373.62 2,199.44 17.0

Table 2: Foreign Direct Investment in Telecom Sector 2009-2010 (PTA 2010, p.71)

v. Telecom Revenues:

(PKR Millions)

Year Cellular Local Loop LDI WLL VAS (Estimated) Total

2009-10 236,047 61,464 47,067 2,880 10,202 357,712

Table 3: Telecom Revenues 2009-2010 (Source: PTA 2010, p.70)

vi. Telecom Investment:

(US $ million)

Year Cellular LDI LL WLL Total

2009-10 908.8 183.1 22.5 23 1,137.4

Table 4: Telecom Investment 2009-2010(Source: PTA 2010, p.24)

37

4.1.3 Economic Indicators

According to the PTA annual report for the year 2010:

i. Telecom Sector shares in GDP (%)

The latest figure available is for year 2005-06 which shows 2 % share in GDP by the telecom

sector.

ii. GST/CED Collection from Telecom sector

The GST and CED collected from only mobile phone companies in year 2007-08 was PKR.

36.80 billion.

iii. Foreign Direct Investment

The total foreign direct investment in the country in the year 2007-08 was USD 5151.80

million out of which USD 1438.60 million was in telecom sector which comes to be 27.92 %

of the total foreign direct investment.

4.1.4 Cellular mobile infrastructure sharing

Tower/infrastructure sharing has long been a priority matter by Pakistan Telecommunication

Authority (PTA) and it strived hard to reach a workable agreement between all the operators.

Currently in Pakistan, tenancy ratio is 1.02 which means out of every 100 towers only two are

shared by operators. For this particular reason PTA and Cellular Mobile Operators (CMOs)

signed memorandum of understanding (MOU) for infrastructure sharing on August 2010 in

Karachi. It is expected that this cooperation will serve to support mutual interests resulting in

less human resource requirement for maintenance, lower fuel expenses, quality maintenance,

lower power consumption, an environmentally friendly appearance, better opportunities for

new service providers, public convenience and expanded coverage in line with international

best practices (PTA 2010).

Mr. X2 mentioned about the company‟s response towards the memorandum of understanding

(MOU) that focuses on the network sharing agreement between all network operators

2 Mr. X representative of Zong Pakistan, identity concealed due to confidentiality and anonymity reasons.

.

38

working in Pakistan. He mentioned that they are happy to do that and have participated in

signing the memorandum. He further said that this is a great initiative by PTA which will

reduce the number of network towers in country, will reduce costs to the company, helps

towards environment saving and is also important from the perspective of social

responsibility and development that the company is committed towards.

As per the requirement of Securities and Exchange Commission of Pakistan (SECP),

Companies (Corporate Social Responsibility) General Order, 2009, “every company shall

provide descriptive as well as monetary disclosures of the corporate social responsibility

activities undertaken by it during each financial year” (SECP 2010). So now it is regulatory

requirement for the companies to disclose CSR activities done in a financial year although it

is not mandatory.

The order also states, “The disclosure, wherever required, shall include but shall not be

limited to the following:

i. Corporate philanthropy

ii. Energy conservation

iii. Environmental conservation

iv. Community investment and welfare schemes

v. Consumer protection measures

vi. Welfare spending for under privileged classes

vii. Industrial relations

viii. Employment of special persons

ix. Occupational safety and health

x. Business ethics and anti corruption measures

xi. National cause donations

xii. Contribution to national exchequer

xiii. Rural development programs (SECP, 2010)

39

Full text of the order can be found in the Appendix.

When asked from the company representative regarding the Corporate Social Responsibility

general order, 2009 by SECP. He (MR. X3) mentioned that this law is not compulsory to

implement and follow and the SECP and PTA are not forcing the companies to implement it

in the company‟s policies and activities. But Zong is already working on the social

development of the country from the start of its business in Pakistan. As the parent company

China Mobiles is using CSR and is part of its policies, we are also working on it. We also

hope that in coming years we will also make it part of our policy.

4.2 Company Profile

China mobile is world‟s largest telecom operator with over 300 million customer base. The

company networks route 700 million text messages and handles 250 million calls every hour.

The company claims “one of the unique features of China mobile servicing excellence is to

customize its products, services and tariffs to suit the individual needs of its huge subscriber

base. There are hundreds of payment/tariff options to choose from according to one‟s usage

pattern, budgetary limitations and nature of use” (Zong 2010).

China mobile Pakistan (CM Pak) is first overseas subsidiary of China mobile

communications corporation (CMCC) that has the license to offer and operate voice, data and

all value added services across Pakistan (Zong 2010). China mobile Pakistan which is a

100% subsidiary of China mobile acquired the license from Millicom to operate GSM

network in Pakistan. CM Pak started with USD 700 million and so far invested additional

USD 800 million till the end of year 2008. CM Pak believes that their competitive edge