Nigerian Bottling Company-FINAL - Nigeria’s No1 · PDF fileNigerian Bottling Company Plc...

19

0 | Page BC Nigeria Equity Research August 20, 2008 Nigerian Bottling Company Plc Initiation of Coverage Meristem Equity Research Saheed Bashir [email protected] +234-802-4546-575 Oluwakemi Adeneye kemi.ade[email protected] Abiodun Keripe [email protected] Ahmed Razaq [email protected] Kayode Tinuoye [email protected] Correspondence: info@meristemng.com

Transcript of Nigerian Bottling Company-FINAL - Nigeria’s No1 · PDF fileNigerian Bottling Company Plc...

0 | P a g e

BC

Nigeria Equity Research

August 20, 2008

Nigerian Bottling Company Plc

Initiation of Coverage

Meristem Equity Research

Saheed Bashir [email protected] +234-802-4546-575

Oluwakemi Adeneye [email protected]

Abiodun Keripe [email protected]

Ahmed Razaq [email protected]

Kayode Tinuoye [email protected]

Correspondence: [email protected]

1 | P a g e

Industry: Food/Beverages and Tobacco

FYE: December 31

Mkt Cap (N’bn): 64.11 (US$ 556.50m)

Executive Summary………………………………………………

Industry Background…………………………………………

Company Overview……………………………………………

Strategic Update…………………………………………………

Analysis of Financials…………………………………………

Stock Price Trajectory……………………………………………

Valuation Methodologies

Appendix……………………………………………………….………...

Historical Financial Statement…………………………………………

Abridged Financial Model a

Disclosures.……………………………………………………………

Content Highlight

Nigeria Equity Research August 6, 2008

M e r i s t e m R e s e a r c h

Nigeria Equity Research

August 19, 2008

Current Price (N): 49.92 Fair Price

52-Wk H/L (N): 70.00/40.00 Premium/ (Discount):

Volatility (β): 0.48 Upside/ (Downside):

ummary………………………………………………. ……..

round………………………………………….…………

erview………………………………………………………

date………………………………………………….……....

ncials………………………………………….…………

Stock Price Trajectory…………………………………………………....

and Results……………………….……….…

……………………………………………………….………...

l Statement…………………………………………

Financial Model and Forecasts……………………………...

ures.……………………………………………………………...

Highlights

M e r i s t e m R e s e a r c h

Fair Price (N): 65.77

Premium/ (Discount): -14.39%

Upside/ (Downside): 16.81%

2

3

5

6

8

14

15

17-19

17

18

19

2 | P a g e

Industry: Food/Beverages and Tobacco

FYE: December 31

Mkt Cap (N’bn): 64.11 (US$ 556.50m)

Executive Summary

• Nigerian Bottling Company Plc (NBC)

company and a sole franchisee of the

Coca-cola Inc. Spanning over six decades of operation, NBC is

a market leader in the production of non

• A softer than expected macro economic environment has

posed challenges to the manufacturing sector of which NBC, as

an integral part, has to come to grips with to stay ahead of the

pack. Major challenges facing the industry include weak

infrastructural support facilities (especially power), unfair

competition from cheaper imported products and rising cost of

fund among others.

• An analysis of the financial strength of NBC reveals an

above-par performance in 2007. H

retrospect, we observed abysmal operational

results in 2006. This was however reversed in 2007 with 13.91

percent ROE and 201.69 percent growth in PAT.

• Due to the FYE 2006 performance, NBC exhibited a very

risky financial profile, (based on Altman’s Z score). However, it

scaled through the gray areas to a health

2007 with a Z-score above the 4 year average. Q1 2008 results

show, respectively, turnover and PAT growth of 10.2 percent

and 11.7 percent. Our forecasts for FYE 2008

percent and 5.0 percent for turnover and PAT respectively

• In valuing NBC, we employed both the Discounted Cash

Flow (DCF) and relative valuation methodologies. We obtained

N13.57, N12.12 and N23.19 respectively from the Discounted

Dividend Method, Present Value of Growth Opportunities and

Residual Income valuations. Our relative v

of Price to Earnings (P/E), Price to Book Value (PBV) and

Price to Sales (P/S) yielded N55.75, N97.82 and N176.12

respectively.

• Attaching appropriate weights to each of the methodologies,

we arrived at a fair price of N65.77 with a dis

of 14.39 percent and an upside potential of 16.81 percent.

Nigeria Equity Research August 6, 2008

M e r i s t e m R e s e a r c h

Nigeria Equity Research

August 19, 2008

Current Price (N): 49.92 Fair Price

52-Wk H/L (N): 70.00/40.00 Premium/ (Discount):

Volatility (β): 0.48 Upside/ (Downside):

Nigerian Bottling Company Plc (NBC) is an indigenous

and a sole franchisee of the international brand;

Spanning over six decades of operation, NBC is

a market leader in the production of non-alcoholic beverage.

A softer than expected macro economic environment has

posed challenges to the manufacturing sector of which NBC, as

, has to come to grips with to stay ahead of the

pack. Major challenges facing the industry include weak

infrastructural support facilities (especially power), unfair

competition from cheaper imported products and rising cost of

of the financial strength of NBC reveals an

par performance in 2007. However, in a 4-year,

operational performance

reversed in 2007 with 13.91

percent ROE and 201.69 percent growth in PAT.

Due to the FYE 2006 performance, NBC exhibited a very

risky financial profile, (based on Altman’s Z score). However, it

scaled through the gray areas to a healthy financial status in

score above the 4 year average. Q1 2008 results

show, respectively, turnover and PAT growth of 10.2 percent

for FYE 2008 are 13.25

percent and 5.0 percent for turnover and PAT respectively

employed both the Discounted Cash

Flow (DCF) and relative valuation methodologies. We obtained

N13.57, N12.12 and N23.19 respectively from the Discounted

of Growth Opportunities and

Residual Income valuations. Our relative valuation techniques

of Price to Earnings (P/E), Price to Book Value (PBV) and

Price to Sales (P/S) yielded N55.75, N97.82 and N176.12

Attaching appropriate weights to each of the methodologies,

with a discount to valuation

of 14.39 percent and an upside potential of 16.81 percent.

Fig 2: NBC and NSE ASI Relative Trajectories

60

80

100

120

140

1-Aug-07 1-Dec-07

NSE ASI: 52-Wk Ret=

Source: NSE and Meristem

Key Metrics

Per Share data

Trailing EPS

Trailing SPS

BVPS*

Valuation Metrics

Trailing PE (x)

Tariling PS

P/BV (x)

Shares Outstanding (m)

Market Cap (Nb)**

Profitability

Net Profit Margin(%)

ROE (%)

ROA (%)

Earnings Yield %

* as @ last FYE

** Based on August 13 market price

Fig1: Summary of key investment statistics

M e r i s t e m R e s e a r c h

Fair Price (N): 65.77

Premium/ (Discount): -14.39%

Upside/ (Downside): 16.81%

: NBC and NSE ASI Relative Trajectories

07 1-Apr-08 1-Aug-08

Wk Ret=-3.08% NBC:52-Wk Ret=-4.91%

and Meristem Research

NBC Peer Avg

2.51 2.29

53.74 29.06

17.46 7.21

19.49 24.49

0.91 2.94

17.46 9.29

Shares Outstanding (m) 1.31 2.71

64.11 100.73

4.63% 10.54%

13.87% 38.99%

6.59% 16.04%

5.13% 4.85%

** Based on August 13 market price

Fig1: Summary of key investment statistics

3 | P a g e

Industry: Food/Beverages and Tobacco

FYE: December 31

Mkt Cap (N’bn): 64.11 (US$ 556.50m)

Price, Promotion and Branding

Industry Background

The Food/Beverage & Tobacco industry is one of the most

thriving and dynamic industries in the Nigerian economy. The

sector utilizes output from the agricultural sector as it main input

and contributes about 0.05 percent in turnover to Gross

Domestic Product (GDP) while its market capitalization of

N749.49bn* (US$6.41) relative to GDP at 1990 current basic

prices is estimated to be about 3.28 percent

in 2003. It captures an average of 31.4 percent share of the

manufacturing sector. The values index of the industry stock

tremendously increased from 32,763.3 in 2003 to 133,422.3 in

2007.

Major challenges facing the industry include the inadequate

supply of locally sourced raw materials,

facilities, unfair competition from smuggle

products, high cost of fund and product adulteration among

others.

In other to salvage the industry, the government formulated several

policy measures such as reduction in custom duty on machinery,

abolition of excise duty except for beers, wines, alcohol and

tobacco, ban on the importation of fruit juice, poultry products,

sugar confectionaries, sweets and chocolates to mention a few. The

re-structuring of National Agency for Food, Drug Administration

and Control (NAFDAC) and Standards Organization of Nigeria

(SON) has in no small measure contributed to the growth of the

industry by regulating and ensuring quality standards for local and

imported products.

However, the effectiveness of the policy thrust will be determined

by the unfolding realities in the economy.

Industry Background

*as at August 4, 2008

Nigeria Equity Research August 6, 2008

M e r i s t e m R e s e a r c h

Nigeria Equity Research

August 19, 2008

Current Price (N): 49.92 Fair Price

52-Wk H/L (N): 70.00/40.00 Premium/ (Discount):

Volatility (β): 0.48 Upside/ (Downside):

The Food/Beverage & Tobacco industry is one of the most

thriving and dynamic industries in the Nigerian economy. The

sector utilizes output from the agricultural sector as it main input

out 0.05 percent in turnover to Gross

Domestic Product (GDP) while its market capitalization of

relative to GDP at 1990 current basic

prices is estimated to be about 3.28 percent up from 2.01 percent

31.4 percent share of the

manufacturing sector. The values index of the industry stock

tremendously increased from 32,763.3 in 2003 to 133,422.3 in

Major challenges facing the industry include the inadequate

supply of locally sourced raw materials, weak infrastructural

facilities, unfair competition from smuggled cheaper foreign

high cost of fund and product adulteration among

salvage the industry, the government formulated several

policy measures such as reduction in custom duty on machinery,

abolition of excise duty except for beers, wines, alcohol and

tobacco, ban on the importation of fruit juice, poultry products,

fectionaries, sweets and chocolates to mention a few. The

structuring of National Agency for Food, Drug Administration

and Control (NAFDAC) and Standards Organization of Nigeria

(SON) has in no small measure contributed to the growth of the

regulating and ensuring quality standards for local and

However, the effectiveness of the policy thrust will be determined

by the unfolding realities in the economy.

M e r i s t e m R e s e a r c h

Fair Price (N): 65.77

Premium/ (Discount): -14.39%

Upside/ (Downside): 16.81%

4 | P a g e

Industry: Food/Beverages and Tobacco

FYE: December 31

Mkt Cap (N’bn): 64.11 (US$ 556.50m)

Company Overview

Nigerian Bottling Company, the largest bottler of non

beverage in Nigeria, has its operations dated

November 1951 when it was incorporated as a subsidiary of A.G

Leventis Group and given the franchise to bottle and sell Coca

cola products in Nigeria. In 1972, it became a public company

with its shares listed on the floor of the Exchange.

off as a family business and has metamorphosised into a

soft drinks Company. It is a subsidiary of the Coca

Hellenic Bottling Company (CCHBC), the emerging company in

the merger of Hellenic Bottling Company S.A and CC Beverage

Company Plc in 2000. NBC is capitalized to the tune of

N65.33bn with outstanding shares of N1.31bn and accounts for

8.72 percent of industry market capitalization.

Analysis of shareholdings reveals that CCHBC has a controlling

equity stake of 55.81 percent through Molino Soft Drinks S.A,

Luxembourg and 10.62 percent through CCBC Services Limited,

Ireland while the remaining holdings (33.57 percent)

directors and other shareholders.

From a single manually operated bottling facility with a

production capacity of a few dozen cases per day within

basement of Mainland hotel in Oyingbo, Lagos in 1953, NBC

currently operates 13 bottling plants with over 80 distribution

warehouses, 250,000 sales outlets and a staff strength of over

6,000 employees across the country.

inception has continued to soar above board and has remained

the largest bottler in Nigeria and the second largest in the

African continent commanding average a

billion bottles up from 1.0 million cases in 1960.

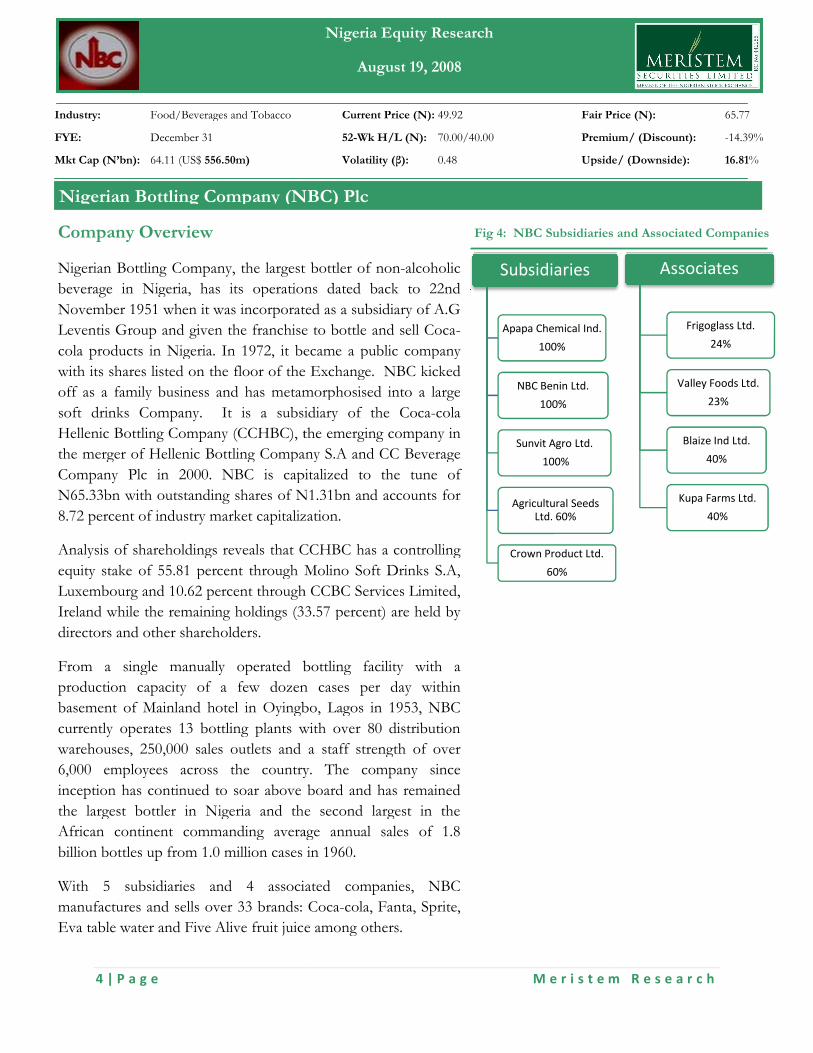

With 5 subsidiaries and 4 associated companies, NBC

manufactures and sells over 33 brands: Coca

Eva table water and Five Alive fruit juice among others.

Nigerian Bottling Company (NBC) Plc

Nigeria Equity Research August 6, 2008

M e r i s t e m R e s e a r c h

Nigeria Equity Research

August 19, 2008

Current Price (N): 49.92 Fair Price

52-Wk H/L (N): 70.00/40.00 Premium/ (Discount):

Volatility (β): 0.48 Upside/ (Downside):

Fig 4: NBC Subsidiaries and Associated Companies

largest bottler of non-alcoholic

Nigeria, has its operations dated back to 22nd

November 1951 when it was incorporated as a subsidiary of A.G

Leventis Group and given the franchise to bottle and sell Coca-

ducts in Nigeria. In 1972, it became a public company

with its shares listed on the floor of the Exchange. NBC kicked

off as a family business and has metamorphosised into a large

. It is a subsidiary of the Coca-cola

Company (CCHBC), the emerging company in

the merger of Hellenic Bottling Company S.A and CC Beverage

NBC is capitalized to the tune of

N65.33bn with outstanding shares of N1.31bn and accounts for

lization.

Analysis of shareholdings reveals that CCHBC has a controlling

equity stake of 55.81 percent through Molino Soft Drinks S.A,

Luxembourg and 10.62 percent through CCBC Services Limited,

(33.57 percent) are held by

From a single manually operated bottling facility with a

production capacity of a few dozen cases per day within

basement of Mainland hotel in Oyingbo, Lagos in 1953, NBC

currently operates 13 bottling plants with over 80 distribution

ales outlets and a staff strength of over

6,000 employees across the country. The company since

inception has continued to soar above board and has remained

the largest bottler in Nigeria and the second largest in the

African continent commanding average annual sales of 1.8

billion bottles up from 1.0 million cases in 1960.

With 5 subsidiaries and 4 associated companies, NBC

manufactures and sells over 33 brands: Coca-cola, Fanta, Sprite,

Eva table water and Five Alive fruit juice among others.

Nigerian Bottling Company (NBC) Plc

Subsidiaries

Apapa Chemical Ind.

100%

NBC Benin Ltd.

100%

Sunvit Agro Ltd.

100%

Agricultural Seeds

Ltd. 60%

Crown Product Ltd.

60%

M e r i s t e m R e s e a r c h

Fair Price (N): 65.77

Premium/ (Discount): -14.39%

Upside/ (Downside): 16.81%

NBC Subsidiaries and Associated Companies

Associates

Frigoglass Ltd.

24%

Valley Foods Ltd.

23%

Blaize Ind Ltd.

40%

Kupa Farms Ltd.

40%

5 | P a g e

Industry: Food/Beverages and Tobacco

FYE: December 31

Mkt Cap (N’bn): 64.11 (US$ 556.50m)

In August 2006, it re-acquired Schweppes franchise which hitherto

bottled Bitter Lemon, Club Soda and Tonic Water under the Krest

brand. NBC has in recent times re-launched and re

of products such as the 50cl PET bottles

additional products- Burn energy drink, can coke,

NBC like many other firms in the manufacturing sector continues to

grapple with challenges of dilapidating basic infrastructure with

particular reference to power and transport (given the brittle nature of

their products).

Strategic Updates

In an environment with low income and high marginal propensity to

consume, soaring food prices have increasingly restricted consumer

discretionary spending and to a large extent re

commodity basket in favour of necessities. This could have an adverse

effect on sales volume. In the light of this, NBC has initiated

processes and products to mitigate attendant threats likely to be posed

in the nearest future ranging from operational to economic

challenges.

In early August 2008, NBC re-launched

Eva water as part of its innovative manageme

maintain market leadership. The company

meet consumer requirement and with tamper proof and greater

resilience to prevent adulteration. In addition, the attractiveness of the

package, the ease of carriage and quality integrity is expected to boost

revenue for the firm.

Among the Company’s recent strategic moves is the product

portfolio expansion to provide quality and wider range of

products to the whole gamut of consumers across the country

while also initiating processes to enhance

working capital management.

Nigeria Equity Research August 6, 2008

M e r i s t e m R e s e a r c h

Nigeria Equity Research

August 19, 2008

Current Price (N): 49.92 Fair Price

52-Wk H/L (N): 70.00/40.00 Premium/ (Discount):

Volatility (β): 0.48 Upside/ (Downside):

acquired Schweppes franchise which hitherto

bottled Bitter Lemon, Club Soda and Tonic Water under the Krest

launched and re-branded a number

of products such as the 50cl PET bottles and also introduced

can coke, etc to the market

NBC like many other firms in the manufacturing sector continues to

with challenges of dilapidating basic infrastructure with

particular reference to power and transport (given the brittle nature of

In an environment with low income and high marginal propensity to

prices have increasingly restricted consumer

discretionary spending and to a large extent re-ordered their choice of

commodity basket in favour of necessities. This could have an adverse

effect on sales volume. In the light of this, NBC has initiated

esses and products to mitigate attendant threats likely to be posed

in the nearest future ranging from operational to economic-wide

launched one of its flagship products,

Eva water as part of its innovative management and decision to

The company re-packaged the product to

meet consumer requirement and with tamper proof and greater

resilience to prevent adulteration. In addition, the attractiveness of the

uality integrity is expected to boost

Among the Company’s recent strategic moves is the product

portfolio expansion to provide quality and wider range of

products to the whole gamut of consumers across the country

to enhance its supply chain and

Nigerian Bottling Company (NBC) Plc

M e r i s t e m R e s e a r c h

Fair Price (N): 65.77

Premium/ (Discount): -14.39%

Upside/ (Downside): 16.81%

Nigerian Bottling Company (NBC) Plc

6 | P a g e

Industry: Food/Beverages and Tobacco

FYE: December 31

Mkt Cap (N’bn): 64.11 (US$ 556.50m)

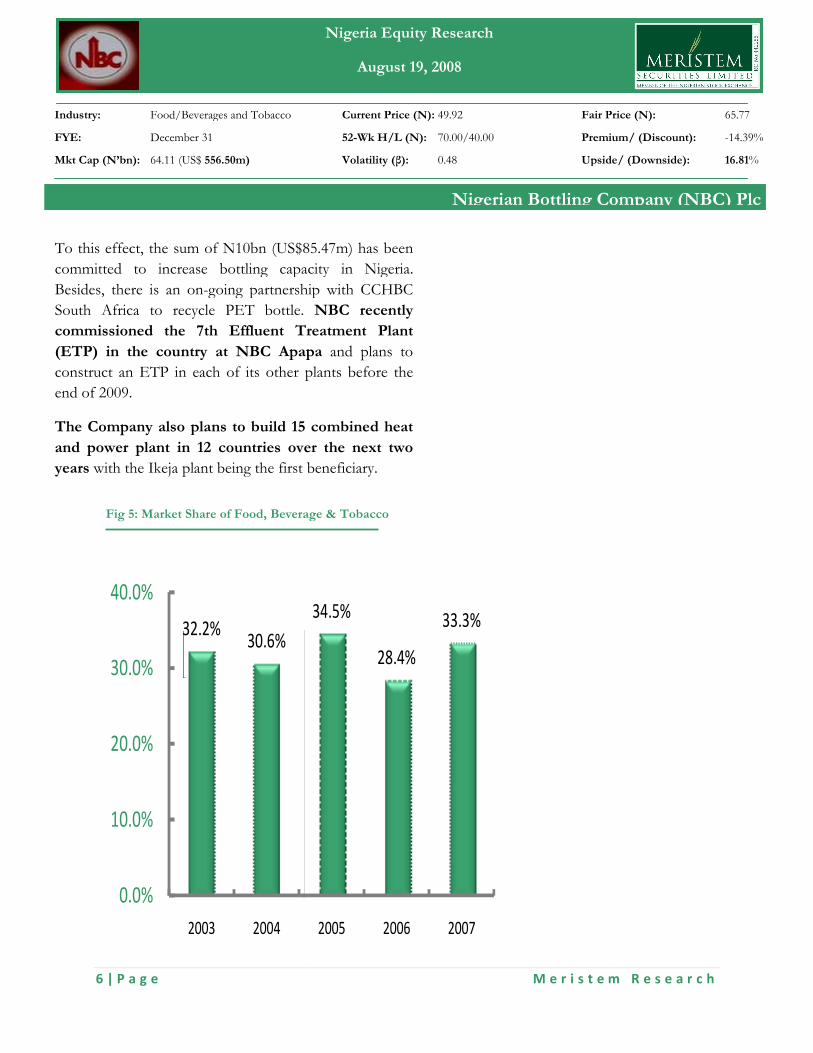

32.2%30.6%

0.0%

10.0%

20.0%

30.0%

40.0%

2003 2004

Fig 5: Market Share of Food, Beverage & Tobacco

To this effect, the sum of N10bn (US$85.47m)

committed to increase bottling capacity in Nigeria.

Besides, there is an on-going partnership with CCHBC

South Africa to recycle PET bottle.

commissioned the 7th Effluent Treatment Plant

(ETP) in the country at NBC Apapa

construct an ETP in each of its other plants before the

end of 2009.

The Company also plans to build 15 combined heat

and power plant in 12 countries over the next two

years with the Ikeja plant being the first beneficiary.

Nigeria Equity Research August 6, 2008

M e r i s t e m R e s e a r c h

Nigeria Equity Research

August 19, 2008

Current Price (N): 49.92 Fair Price

52-Wk H/L (N): 70.00/40.00 Premium/ (Discount):

Volatility (β): 0.48 Upside/ (Downside):

34.5%

28.4%

33.3%

2005 2006 2007

Nigerian Bottling Company (NBC) Plc

Share of Food, Beverage & Tobacco

(US$85.47m) has been

committed to increase bottling capacity in Nigeria.

going partnership with CCHBC

NBC recently

commissioned the 7th Effluent Treatment Plant

(ETP) in the country at NBC Apapa and plans to

construct an ETP in each of its other plants before the

plans to build 15 combined heat

and power plant in 12 countries over the next two

with the Ikeja plant being the first beneficiary.

M e r i s t e m R e s e a r c h

Fair Price (N): 65.77

Premium/ (Discount): -14.39%

Upside/ (Downside): 16.81%

Company (NBC) Plc

7 | P a g e

Industry: Food/Beverages and Tobacco

FYE: December 31

Mkt Cap (N’bn): 64.11 (US$ 556.50m)

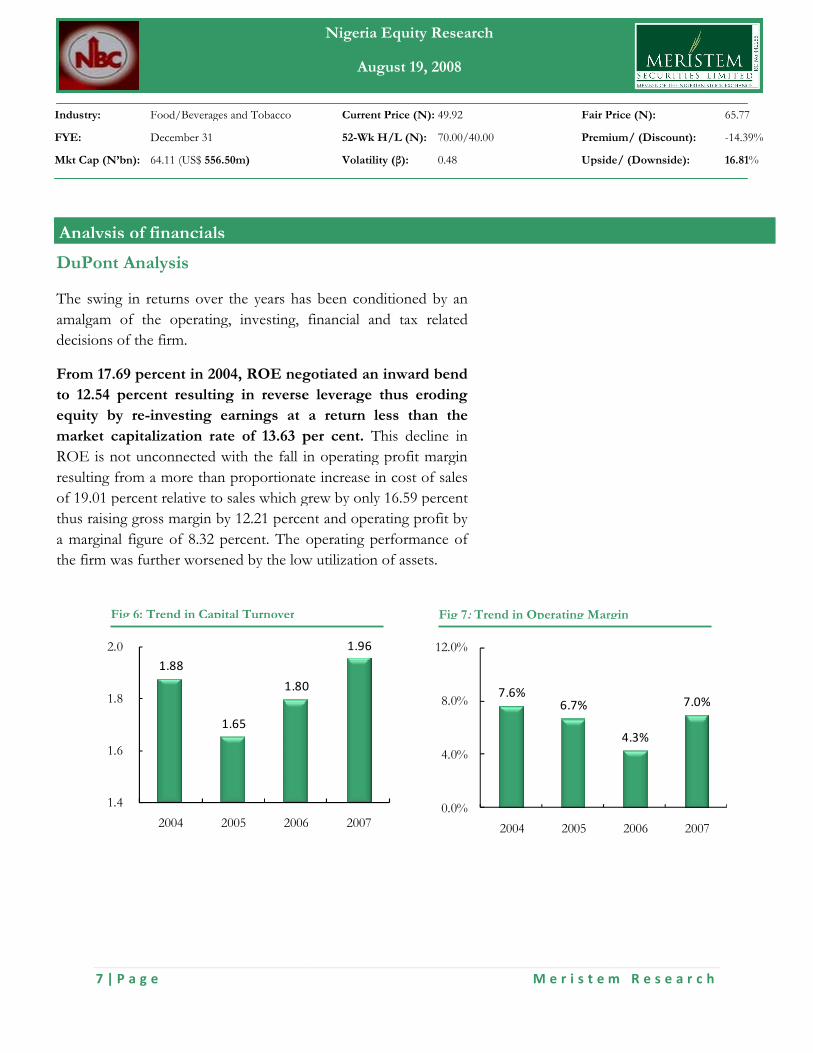

DuPont Analysis

The swing in returns over the years has been conditioned by an

amalgam of the operating, investing, financial and tax related

decisions of the firm.

From 17.69 percent in 2004, ROE negotiated an inward bend

to 12.54 percent resulting in reverse leverage thus erodin

equity by re-investing earnings at a return less than the

market capitalization rate of 13.63 per cent.

ROE is not unconnected with the fall in operating profit margin

resulting from a more than proportionate increase in cost of sales

of 19.01 percent relative to sales which grew by only 16.59 percent

thus raising gross margin by 12.21 percent

a marginal figure of 8.32 percent. The operating performance of

the firm was further worsened by the low utilization of asse

Analysis of financials

Fig 6: Trend in Capital Turnover

1.88

1.65

1.80

1.4

1.6

1.8

2.0

2004 2005 2006

Nigeria Equity Research August 6, 2008

M e r i s t e m R e s e a r c h

Nigeria Equity Research

August 19, 2008

Current Price (N): 49.92 Fair Price

52-Wk H/L (N): 70.00/40.00 Premium/ (Discount):

Volatility (β): 0.48 Upside/ (Downside):

in returns over the years has been conditioned by an

amalgam of the operating, investing, financial and tax related

From 17.69 percent in 2004, ROE negotiated an inward bend

to 12.54 percent resulting in reverse leverage thus eroding

investing earnings at a return less than the

market capitalization rate of 13.63 per cent. This decline in

ROE is not unconnected with the fall in operating profit margin

resulting from a more than proportionate increase in cost of sales

19.01 percent relative to sales which grew by only 16.59 percent

percent and operating profit by

of 8.32 percent. The operating performance of

the firm was further worsened by the low utilization of assets.

1.80

1.96

2006 2007

Fig 7: Trend in Operating Margin

7.6%6.7%

0.0%

4.0%

8.0%

12.0%

2004 2005

M e r i s t e m R e s e a r c h

Fair Price (N): 65.77

Premium/ (Discount): -14.39%

Upside/ (Downside): 16.81%

Trend in Operating Margin

4.3%

7.0%

2006 2007

8 | P a g e

Industry: Food/Beverages and Tobacco

FYE: December 31

Mkt Cap (N’bn): 64.11 (US$ 556.50m)

In which case, capital turnover, a measure of asset efficiency shows

a decline from 1.88 to 1.65 as a result of a lower sales growth of

16.59 percent relative to growth in invested capital of 32.39

percent. Considerations for the management of operating asset and

liabilities informed the preference for invested capital over total

asset turnover. In addition to the abo

jump in taxation capped up the low operating margin.

NBC was able to salvage the overall performance by improved

financial decisions as seen in the upward movement in

financial cost and financial structure ratios.

1.48

1.81 1.66

-0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8 2.0

2004 2005 2006

Fig 8: Trend in Financial Structure Ratio

Nigeria Equity Research August 6, 2008

M e r i s t e m R e s e a r c h

Nigeria Equity Research

August 19, 2008

Current Price (N): 49.92 Fair Price

52-Wk H/L (N): 70.00/40.00 Premium/ (Discount):

Volatility (β): 0.48 Upside/ (Downside):

Analysis of fiunancials

In which case, capital turnover, a measure of asset efficiency shows

a decline from 1.88 to 1.65 as a result of a lower sales growth of

growth in invested capital of 32.39

. Considerations for the management of operating asset and

liabilities informed the preference for invested capital over total

asset turnover. In addition to the above factors, 318.81 percent

ed up the low operating margin. However,

NBC was able to salvage the overall performance by improved

financial decisions as seen in the upward movement in

financial cost and financial structure ratios.

Fig 9: Trend in Financial Cost Ratio

0.92 0.96

-

0.2

0.4

0.6

0.8

1.0

1.2

2004 2005

1.54

2007

Trend in Financial Structure Ratio

M e r i s t e m R e s e a r c h

Fair Price (N): 65.77

Premium/ (Discount): -14.39%

Upside/ (Downside): 16.81%

Analysis of fiunancials

Trend in Financial Cost Ratio

0.24

0.91

2006 2007

9 | P a g e

Industry: Food/Beverages and Tobacco

FYE: December 31

Mkt Cap (N’bn): 64.11 (US$ 556.50m)

This downward trend perpetuated itself till

low as 5.25 percent. Tax overprovision in prior year coupled with

improved asset utilization slightly compensated for operational

inefficiencies but could not raise ROE bey

Provided FYE 2007 performance is sustained, we expect ROE to

further improve to 15.32 percent in 2008. However, a better

performance can be achieved given more efficient cost and working

capital management. The debt composition of the firm is skewed

towards short term financing and as a consequence, NBC has not

been able to achieve a current ratio of 1.0 in the last 4 years. By

implication it could not meet its short term obligations with its level

of current assets.

0.91

0.65

1.71

-

0.6

1.2

1.8

2004 2005 2006

Fig 10: Trend in Tax Effect Ratio

Nigeria Equity Research August 6, 2008

M e r i s t e m R e s e a r c h

Nigeria Equity Research

August 19, 2008

Current Price (N): 49.92 Fair Price

52-Wk H/L (N): 70.00/40.00 Premium/ (Discount):

Volatility (β): 0.48 Upside/ (Downside):

This downward trend perpetuated itself till FYE 2006 dropping as

low as 5.25 percent. Tax overprovision in prior year coupled with

improved asset utilization slightly compensated for operational

inefficiencies but could not raise ROE beyond 5.25 percent.

performance is sustained, we expect ROE to

further improve to 15.32 percent in 2008. However, a better

e can be achieved given more efficient cost and working

capital management. The debt composition of the firm is skewed

towards short term financing and as a consequence, NBC has not

been able to achieve a current ratio of 1.0 in the last 4 years. By

ation it could not meet its short term obligations with its level

17.69%

12.54%

0.0%

6.0%

12.0%

18.0%

24.0%

2004 2005 2006

Fig 11: Trend in ROE

0.73

2007

M e r i s t e m R e s e a r c h

Fair Price (N): 65.77

Premium/ (Discount): -14.39%

Upside/ (Downside): 16.81%

Analysis of financials

5.25%

13.91%

2006 2007

10 | P a g e

Industry: Food/Beverages and Tobacco

FYE: December 31

Mkt Cap (N’bn): 64.11 (US$ 556.50m)

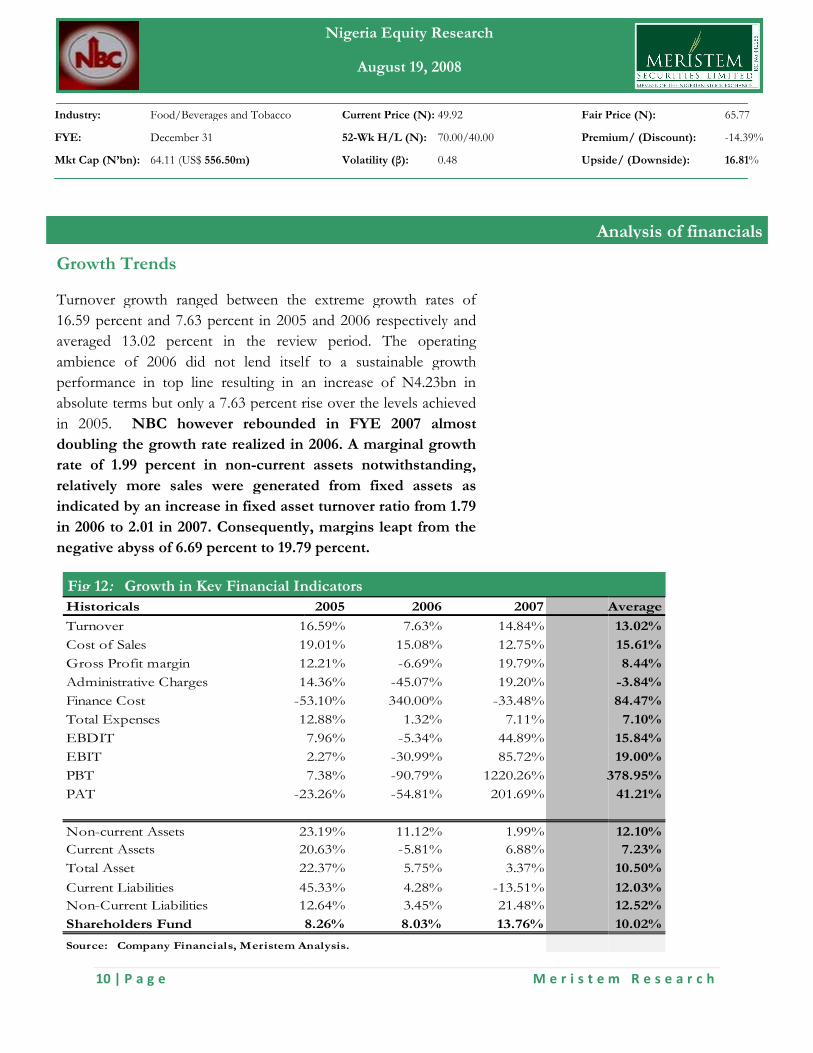

Growth Trends

Turnover growth ranged between the extreme growth rates of

16.59 percent and 7.63 percent in 2005 and 2006 respectively

averaged 13.02 percent in the review period. The operating

ambience of 2006 did not lend itself to a sustainable growth

performance in top line resulting in an

absolute terms but only a 7.63 percent rise over the levels achieved

in 2005. NBC however rebounded in FYE

doubling the growth rate realized in 2006. A marginal growth

rate of 1.99 percent in non-current assets notwithstanding,

relatively more sales were generated from fixed assets as

indicated by an increase in fixed asset turnover ratio from 1.79

in 2006 to 2.01 in 2007. Consequently, margins leapt from the

negative abyss of 6.69 percent to 19.79 percent.

Fig 12: Growth in Key Financial Indicators

Historicals

Turnover 16.59%

Cost of Sales 19.01%

Gross Profit margin 12.21%

Administrative Charges 14.36%

Finance Cost -53.10%

Total Expenses 12.88%

EBDIT

EBIT

PBT

PAT -23.26%

Non-current Assets 23.19%

Current Assets 20.63%

Total Asset 22.37%

Current Liabilities 45.33%

Non-Current Liabilities 12.64%

Shareholders Fund

Source: Company Financials, Meristem Analysis.

Nigeria Equity Research August 6, 2008

M e r i s t e m R e s e a r c h

Nigeria Equity Research

August 19, 2008

Current Price (N): 49.92 Fair Price

52-Wk H/L (N): 70.00/40.00 Premium/ (Discount):

Volatility (β): 0.48 Upside/ (Downside):

Analysis of financial

Turnover growth ranged between the extreme growth rates of

in 2005 and 2006 respectively and

averaged 13.02 percent in the review period. The operating

ambience of 2006 did not lend itself to a sustainable growth

performance in top line resulting in an increase of N4.23bn in

absolute terms but only a 7.63 percent rise over the levels achieved

NBC however rebounded in FYE 2007 almost

doubling the growth rate realized in 2006. A marginal growth

current assets notwithstanding,

relatively more sales were generated from fixed assets as

n fixed asset turnover ratio from 1.79

in 2006 to 2.01 in 2007. Consequently, margins leapt from the

negative abyss of 6.69 percent to 19.79 percent.

Growth in Key Financial Indicators

2005 2006 2007 Average

16.59% 7.63% 14.84%

19.01% 15.08% 12.75%

12.21% -6.69% 19.79%

14.36% -45.07% 19.20%

-53.10% 340.00% -33.48%

12.88% 1.32% 7.11%

7.96% -5.34% 44.89%

2.27% -30.99% 85.72%

7.38% -90.79% 1220.26% 378.95%

-23.26% -54.81% 201.69%

23.19% 11.12% 1.99%

20.63% -5.81% 6.88%

22.37% 5.75% 3.37%

45.33% 4.28% -13.51%

12.64% 3.45% 21.48%

8.26% 8.03% 13.76%

Source: Company Financials, Meristem Analysis.

M e r i s t e m R e s e a r c h

Fair Price (N): 65.77

Premium/ (Discount): -14.39%

Upside/ (Downside): 16.81%

Analysis of financials

Average

13.02%

15.61%

8.44%

-3.84%

84.47%

7.10%

15.84%

19.00%

378.95%

41.21%

12.10%

7.23%

10.50%

12.03%

12.52%

10.02%

11 | P a g e

Industry: Food/Beverages and Tobacco

FYE: December 31

Mkt Cap (N’bn): 64.11 (US$ 556.50m)

The expenses profile of the company improved in 2006 grew

slightly by 1.32 percent despite a 340 per cent increase in finance

charges. Operational efficiencies in administration

the associated expenses by 45.07 percent. Efficient asset utilization

and cost management translated into 85.72 per cent growth in

EBIT.

Nevertheless, this improvement could not birth a positive growth

in PBT as a result of the negative impact

overprovision in the prior year could only assuage negative earnings

as PAT growth rate could have been worse than

recorded in 2006. However, there was a phenomenal rebound

translating to 1,220.26 percent and 201.69 per

and PAT respectively in 2007.

Total assets have grown at an average of 10.50 percent over the

past 4 years. Both current and non-current liabilities grew at an

average of about 12 percent over the years. Current assets which in

absolute terms fell short of current liabilities was not able to meet

up with the pace of the latter save for 2007. Indeed, 2007 witnessed

a remarkable performance in most financial metrics as NBC was

able to improve on operations, finances and investments.

On the average, NBC performed comparatively fair relative to

the industry. With regards to its most recent results it

outperformed the industry in major indices with earning

yields of 5.04 percent, a P/E lower than half

average and sales per share of 53.74 relative to an industry

average of 44.31. As an income stock, NBC has consistently paid

dividend at an average payout of 38.43 percent over the past 10

years save for 2000.

Nigeria Equity Research August 6, 2008

M e r i s t e m R e s e a r c h

Nigeria Equity Research

August 19, 2008

Current Price (N): 49.92 Fair Price

52-Wk H/L (N): 70.00/40.00 Premium/ (Discount):

Volatility (β): 0.48 Upside/ (Downside):

The expenses profile of the company improved in 2006 grew

slightly by 1.32 percent despite a 340 per cent increase in finance

charges. Operational efficiencies in administration brought down

the associated expenses by 45.07 percent. Efficient asset utilization

and cost management translated into 85.72 per cent growth in

Nevertheless, this improvement could not birth a positive growth

in PBT as a result of the negative impact of gross margin. Tax

overprovision in the prior year could only assuage negative earnings

as PAT growth rate could have been worse than –54.81 percent

recorded in 2006. However, there was a phenomenal rebound

translating to 1,220.26 percent and 201.69 percent growths in PBT

Total assets have grown at an average of 10.50 percent over the

current liabilities grew at an

average of about 12 percent over the years. Current assets which in

terms fell short of current liabilities was not able to meet

2007. Indeed, 2007 witnessed

a remarkable performance in most financial metrics as NBC was

able to improve on operations, finances and investments.

average, NBC performed comparatively fair relative to

the industry. With regards to its most recent results it

outperformed the industry in major indices with earning

lower than half the industry

of 53.74 relative to an industry

As an income stock, NBC has consistently paid

dividend at an average payout of 38.43 percent over the past 10

Analysis of financials

M e r i s t e m R e s e a r c h

Fair Price (N): 65.77

Premium/ (Discount): -14.39%

Upside/ (Downside): 16.81%

Analysis of financials

12 | P a g e

Industry: Food/Beverages and Tobacco

FYE: December 31

Mkt Cap (N’bn): 64.11 (US$ 556.50m)

Solvency and Debt Management

The risk profile of NBC reveals that it has dotted the regions of

financial health, caution and ‘bankruptcy possibilities’ over the

review period. A careful analysis of events unfold that a low

current ratio of 0.67 in 2006, (unfavorable working capital

condition), a high proportion of short term fund relative to

long term debt in funding operations and plummeting EBIT

accounted for the shift in credit worthiness of the firm into the

bankruptcy region in 2006.

This is further supported by a decline in int

25.85 to 4.05 in the same year. However, the downward trend was

partly offset by an increased return on equity relative to asset; by

implication a higher financial leverage index. The unimpressive

performance recorded in 2006 took its toll on the share price with a

year return of –43.39 percent. The strategic positioning of NBC

in 2007 brought it back to a level surpassing the 2005

performance.

0.00

1.50

3.00

4.50

2004 2005 2006

Z score

Fig 13: NBC’s Key Risk Metrics and ChartKey Ratio 2004

Long term debt ratio 0.16

Short term debt ratio 0.36

Debt/Equity 1.10

Finnancial Leverage Index 2.10

Current Ratio 0.89

Interest Coverage 11.85Z score 3.95

Nigeria Equity Research August 6, 2008

M e r i s t e m R e s e a r c h

Nigeria Equity Research

August 19, 2008

Current Price (N): 49.92 Fair Price

52-Wk H/L (N): 70.00/40.00 Premium/ (Discount):

Volatility (β): 0.48 Upside/ (Downside):

Analysis of financials

Solvency and Debt Management

The risk profile of NBC reveals that it has dotted the regions of

financial health, caution and ‘bankruptcy possibilities’ over the

A careful analysis of events unfold that a low

(unfavorable working capital

ondition), a high proportion of short term fund relative to

long term debt in funding operations and plummeting EBIT

accounted for the shift in credit worthiness of the firm into the

This is further supported by a decline in interest coverage from

25.85 to 4.05 in the same year. However, the downward trend was

partly offset by an increased return on equity relative to asset; by

implication a higher financial leverage index. The unimpressive

toll on the share price with a

The strategic positioning of NBC

in 2007 brought it back to a level surpassing the 2005

2007

Bankruptcypossibilities(within 2 yrs)

High probability of financial embarrassment

Healthy

Gray Area

and Chart 2005 2006 2007 Anual Avrg.

0.15 0.15 0.17 0.16

0.43 0.42 0.35 0.39

1.37 1.32 1.11 1.22

2.37 2.32 2.11 2.22

0.74 0.67 0.83 0.78

25.85 4.05 11.32 13.27

3.46 2.41 3.51 3.33

M e r i s t e m R e s e a r c h

Fair Price (N): 65.77

Premium/ (Discount): -14.39%

Upside/ (Downside): 16.81%

Analysis of financials

13 | P a g e

Industry: Food/Beverages and Tobacco

FYE: December 31

Mkt Cap (N’bn): 64.11 (US$ 556.50m)

Stock Price Trajectory

NBC stock price has demonstrated pendulum swings in the past 4 years

undulating between successive highs and lows.

reference of a year, price movement has been gravitating upwards

with the RSI within band for most months

volumes traded in late July 2007, NBC price continued to soar high

reaching N57.75 before trending downwar

During this period the RSI fell in the overbought region but

continued to decline until it came within band and was sustained

till late June 2008 before momentarily nose

region. However, this time around it was characterized by moderate

volumes but with falling prices. NBC stock price trailed an upward path

from August 2007 to reach its all-time high of N70.00 on March 3rd,

2008. It thereafter exhibited a step-movement to stabilize at N49.92 with

an RSI of 29.03.

0

25

50

75

100

2-Jul-07 2-Oct-07 2-Jan

RSIOverbought

Fig 14: 12-Month Price-Volume and RSI Charts

0

20

40

60

80

2-Jul-07 2-Nov-07

Volume

Nigeria Equity Research August 6, 2008

M e r i s t e m R e s e a r c h

Nigeria Equity Research

August 19, 2008

Current Price (N): 49.92 Fair Price

52-Wk H/L (N): 70.00/40.00 Premium/ (Discount):

Volatility (β): 0.48 Upside/ (Downside):

NBC stock price has demonstrated pendulum swings in the past 4 years

undulating between successive highs and lows. However, within a time

reference of a year, price movement has been gravitating upwards

with the RSI within band for most months. With unusually high

volumes traded in late July 2007, NBC price continued to soar high

reaching N57.75 before trending downwards to N44.00 in early August.

During this period the RSI fell in the overbought region but

continued to decline until it came within band and was sustained

till late June 2008 before momentarily nose-diving into the oversold

nd it was characterized by moderate

volumes but with falling prices. NBC stock price trailed an upward path

time high of N70.00 on March 3rd,

movement to stabilize at N49.92 with

Jan-08 2-Apr-08 2-Jul-08

Oversold

RSI(14)= 29.03

Volume and RSI Charts

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

2-Mar-08 2-Jul-08

Volume Price

M e r i s t e m R e s e a r c h

Fair Price (N): 65.77

Premium/ (Discount): -14.39%

Upside/ (Downside): 16.81%

14 | P a g e

Industry: Food/Beverages and Tobacco

FYE: December 31

Mkt Cap (N’bn): 64.11 (US$ 556.50m)

A combination of Discounted Cash flow methodology and

relative valuations were adopted in valuing NBC. The former

was utilized to determine the intrinsic worth of the firm while

the later gives a valuation methodology based on its competitive

stance in the industry. In using the discounted cash flows, we

employed the 2-stage Dividend Discount Method (DDM),

Present Value of Growth Opportunities (PVGO) and the

Residual Income Model (RI). Due to high investment in fixed

capital, NBC has not been able to generate a positive free cash

flow informing the exclusion of Free Cash Flow to Equity

(FCFE) based valuation in determining NBC’s fair

We used a risk free rate of 10.75 percent based on the current

rate on 10-year Federal Government of Nigeria (FGN) bond.

Other input variables include a risk premium of 6 percent and

2-year beta of 0.48 resulting in a market capitalization rate or

cost of equity of 13.63 percent.

The intrinsic share price of NBC based on the DDM, assuming

a terminal growth rate of 7.60 percent, was estimated at N

The PVGO, assuming a growth rate based on the return on

equity of 12.68 percent and retention rate

in a negative franchise factor of 0.55 but a positive growth

factor of 1.32 culminating in a projected share price of N12.1

Similarly, we derive a price of N26.87

valuation methodology taking into consideration n

items and violations of clean surplus accounting.

A sensitivity analysis of the discounted cash flow

methodologies reveals a maximum price of N

growth rate of 12 percent based on DDM and a minimum

value of N15.46 at 5 percent growth

DDM as well.

Valuation Methodologies and Summary

Nigeria Equity Research August 6, 2008

M e r i s t e m R e s e a r c h

Nigeria Equity Research

August 19, 2008

Current Price (N): 49.92 Fair Price

52-Wk H/L (N): 70.00/40.00 Premium/ (Discount):

Volatility (β): 0.48 Upside/ (Downside):

A combination of Discounted Cash flow methodology and

relative valuations were adopted in valuing NBC. The former

determine the intrinsic worth of the firm while

the later gives a valuation methodology based on its competitive

stance in the industry. In using the discounted cash flows, we

stage Dividend Discount Method (DDM),

ortunities (PVGO) and the

Residual Income Model (RI). Due to high investment in fixed

capital, NBC has not been able to generate a positive free cash

flow informing the exclusion of Free Cash Flow to Equity

(FCFE) based valuation in determining NBC’s fair value.

We used a risk free rate of 10.75 percent based on the current

year Federal Government of Nigeria (FGN) bond.

Other input variables include a risk premium of 6 percent and

year beta of 0.48 resulting in a market capitalization rate or

The intrinsic share price of NBC based on the DDM, assuming

a terminal growth rate of 7.60 percent, was estimated at N20.23.

The PVGO, assuming a growth rate based on the return on

equity of 12.68 percent and retention rate of 61 percent resulted

in a negative franchise factor of 0.55 but a positive growth

in a projected share price of N12.12.

6.87 from the Residual

valuation methodology taking into consideration non-recurring

items and violations of clean surplus accounting.

A sensitivity analysis of the discounted cash flow

methodologies reveals a maximum price of N62.92 at a

growth rate of 12 percent based on DDM and a minimum

at 5 percent growth rate derived from the

Valuation Methodologies and Summary

M e r i s t e m R e s e a r c h

Fair Price (N): 65.77

Premium/ (Discount): -14.39%

Upside/ (Downside): 16.81%

15 | P a g e

Industry: Food/Beverages and Tobacco

FYE: December 31

Mkt Cap (N’bn): 64.11 (US$ 556.50m)

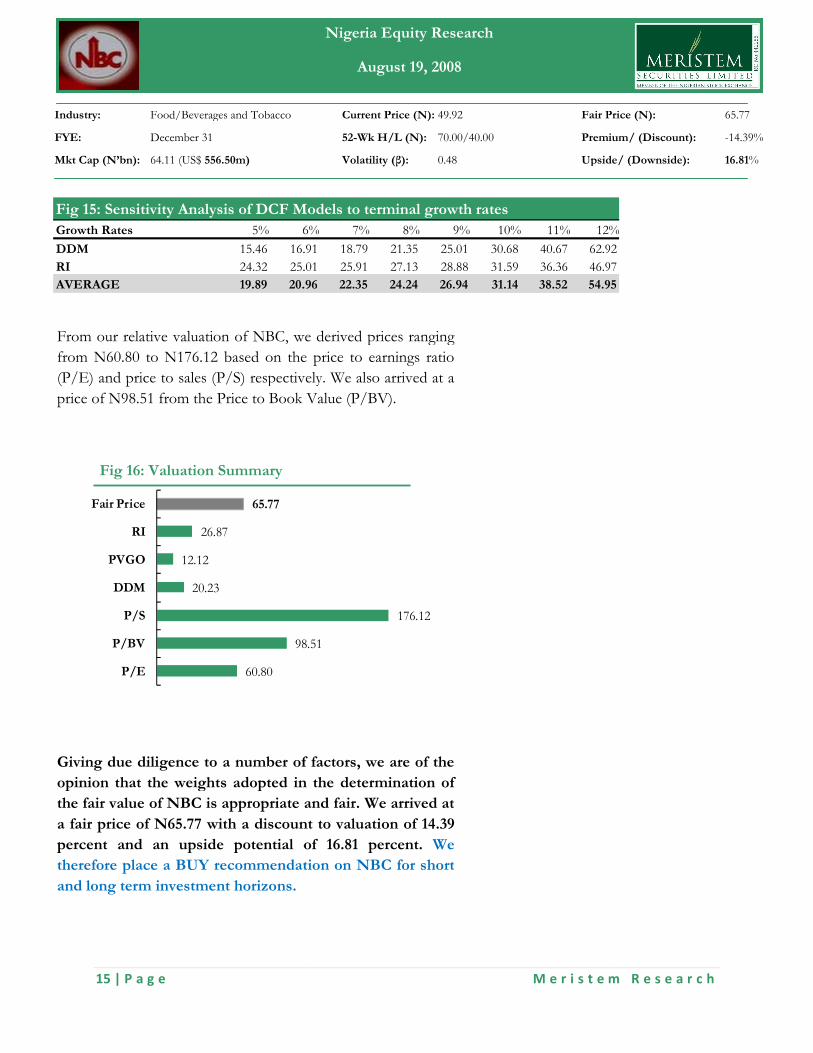

From our relative valuation of NBC, we derived prices ranging

from N60.80 to N176.12 based on the price to earnings ratio

(P/E) and price to sales (P/S) respectively. We

price of N98.51 from the Price to Book Value (P/BV).

Giving due diligence to a number of factors, we are of the

opinion that the weights adopted in the determination of

the fair value of NBC is appropriate and fair. We arrived at

a fair price of N65.77 with a discount to valuation of 14.39

percent and an upside potential of 16.81 percent.

therefore place a BUY recommendation on NBC for short

and long term investment horizons.

60.80

98.51

20.23

12.12

26.87

65.77

P/E

P/BV

P/S

DDM

PVGO

RI

Fair Price

Fig 16: Valuation Summary

Fig 15: Sensitivity Analysis of DCF Models to terminal growth rates

Growth Rates 5% 6%

DDM 15.46 16.91 RI 24.32 25.01 AVERAGE 19.89 20.96

Nigeria Equity Research August 6, 2008

M e r i s t e m R e s e a r c h

Nigeria Equity Research

August 19, 2008

Current Price (N): 49.92 Fair Price

52-Wk H/L (N): 70.00/40.00 Premium/ (Discount):

Volatility (β): 0.48 Upside/ (Downside):

From our relative valuation of NBC, we derived prices ranging

to N176.12 based on the price to earnings ratio

ales (P/S) respectively. We also arrived at a

he Price to Book Value (P/BV).

Giving due diligence to a number of factors, we are of the

opinion that the weights adopted in the determination of

the fair value of NBC is appropriate and fair. We arrived at

with a discount to valuation of 14.39

percent and an upside potential of 16.81 percent. We

therefore place a BUY recommendation on NBC for short

98.51

176.12

: Sensitivity Analysis of DCF Models to terminal growth rates

6% 7% 8% 9% 10% 11% 12%

16.91 18.79 21.35 25.01 30.68 40.67 62.92 25.01 25.91 27.13 28.88 31.59 36.36 46.97 20.96 22.35 24.24 26.94 31.14 38.52 54.95

M e r i s t e m R e s e a r c h

Fair Price (N): 65.77

Premium/ (Discount): -14.39%

Upside/ (Downside): 16.81%

12%

62.92

46.97

54.95

16 | P a g e

Industry: Food/Beverages and Tobacco

FYE: December 31

Mkt Cap (N’bn): 64.11 (US$ 556.50m)

Historical Financial Summary

Turnover

Cost of Sales

Gross Profit

Other operating incomes

Share of profit from associated companies

Expenses

Administrative(Actual)

Administrative(adjusted)

Selling and distribution

Operating Profit

Finance Charges

Total expenses

Total expenses(Actual)

EBDIT

Depreciation

EBIT

Interest

Profit before taxation and exceptional items

Exceptional Items

PBT

Taxation

PAT before Extra-Ordinary items

Extra-ordinary items

PAT

Earnings Per Share

Dividend Per Share

Appendix I

Source: Company Financials, Meristem Research

Nigeria Equity Research August 6, 2008

M e r i s t e m R e s e a r c h

Nigeria Equity Research

August 19, 2008

Current Price (N): 49.92 Fair Price

52-Wk H/L (N): 70.00/40.00 Premium/ (Discount):

Volatility (β): 0.48 Upside/ (Downside):

2004 2005 2006

47,553,874 55,444,504 59,674,516

30,638,654 36,464,205 41,963,985

16,915,220 18,980,299 17,710,531

175,758 75,247 41,729

202,880 282,825 151,233

17,293,858 19,338,371 17,903,493

5,052,354 5,778,049 3,173,637

2,353,787 2,657,661 (734,514)

8,604,025 9,840,136 12,162,588

3,434,599 3,437,361 2,416,035

306,885 143,929 633,286

10,957,812 12,497,797 11,428,074

13,963,264 15,762,114 15,969,511

6,336,046 6,840,574 6,475,419

2,698,567 3,120,388 3,908,151

3,637,479 3,720,186 2,567,268

306,885 143,929 633,286

Profit before taxation and exceptional items 3,330,594 3,576,257 1,933,982

- - (1,604,741)

3,330,594 3,576,257 329,241

298,272 1,249,197 (437,007)

3,032,322 2,327,060 766,248

- - 285,248

3,032,322 2,327,060 1,051,496

2.33 1.78 0.80

1.20 0.60 0.30 Source: Company Financials, Meristem Research.

M e r i s t e m R e s e a r c h

Fair Price (N): 65.77

Premium/ (Discount): -14.39%

Upside/ (Downside): 16.81%

2007 Average

68,529,128 57,800,506

47,313,777 39,095,155

21,215,351 18,705,350

76,719 92,363

159,737 199,169

21,451,807 18,996,882

3,782,905 4,446,736

(831,492) 861,361

12,900,844 10,876,898

4,608,321 3,474,079

421,232 376,333

12,069,352 11,738,259

17,104,981 15,699,968

9,382,455 7,258,624

4,614,397 3,585,376

4,768,058 3,673,248

421,232 376,333

4,346,826 3,296,915

- (401,185)

4,346,826 2,895,730

1,174,562 571,256

3,172,264 2,324,474

- 71,312

3,172,264 2,395,786

2.42 1.83

0.75 0.71

17 | P a g e

Industry: Food/Beverages and Tobacco

FYE: December 31

Mkt Cap (N’bn): 64.11 (US$ 556.50m)

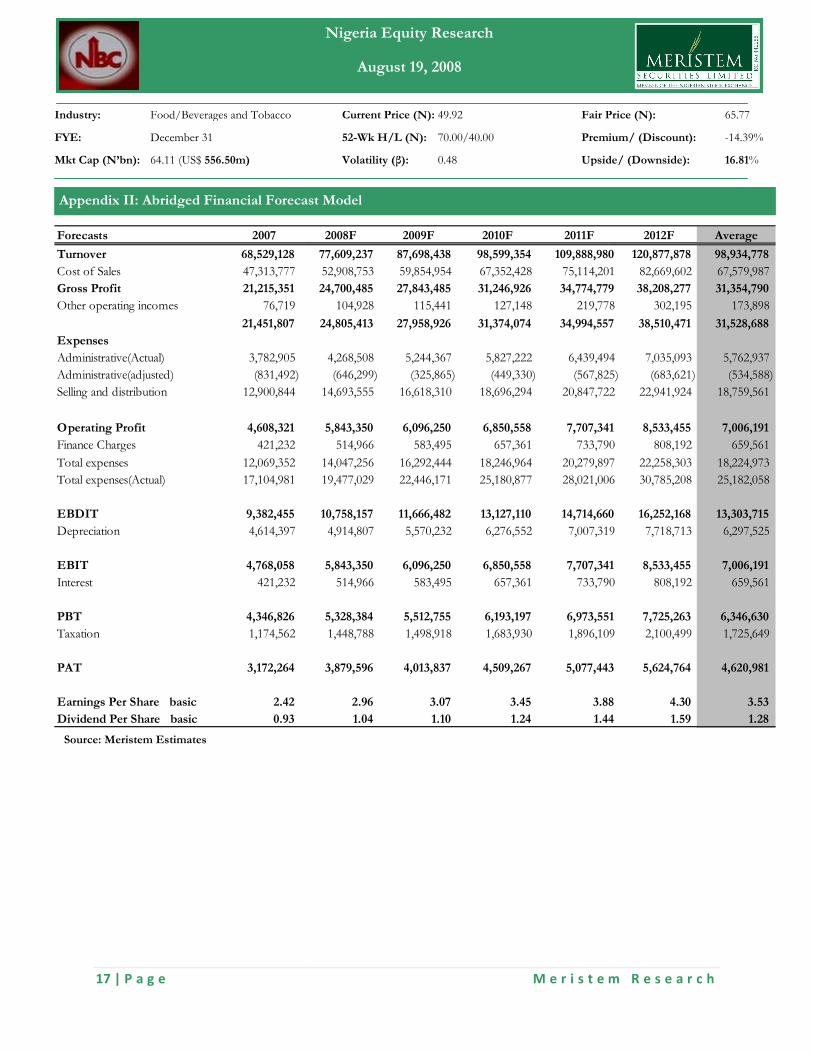

Appendix II: Abridged Financial Forecast Model

Forecasts 2007

Turnover 68,529,128

Cost of Sales 47,313,777

Gross Profit 21,215,351

Other operating incomes 76,719

21,451,807

Expenses

Administrative(Actual) 3,782,905

Administrative(adjusted) (831,492)

Selling and distribution 12,900,844

Operating Profit 4,608,321

Finance Charges 421,232

Total expenses 12,069,352

Total expenses(Actual) 17,104,981

EBDIT 9,382,455

Depreciation 4,614,397

EBIT 4,768,058

Interest 421,232

PBT 4,346,826

Taxation 1,174,562

PAT 3,172,264

Earnings Per Share basic 2.42

Dividend Per Share basic 0.93

Source: Meristem Estimates

Nigeria Equity Research August 6, 2008

M e r i s t e m R e s e a r c h

Nigeria Equity Research

August 19, 2008

Current Price (N): 49.92 Fair Price

52-Wk H/L (N): 70.00/40.00 Premium/ (Discount):

Volatility (β): 0.48 Upside/ (Downside):

: Abridged Financial Forecast Model

2008F 2009F 2010F 2011F

77,609,237 87,698,438 98,599,354 109,888,980

52,908,753 59,854,954 67,352,428 75,114,201

24,700,485 27,843,485 31,246,926 34,774,779

104,928 115,441 127,148 219,778

24,805,413 27,958,926 31,374,074 34,994,557

4,268,508 5,244,367 5,827,222 6,439,494

(646,299) (325,865) (449,330) (567,825)

14,693,555 16,618,310 18,696,294 20,847,722

5,843,350 6,096,250 6,850,558 7,707,341

514,966 583,495 657,361 733,790

14,047,256 16,292,444 18,246,964 20,279,897

19,477,029 22,446,171 25,180,877 28,021,006

10,758,157 11,666,482 13,127,110 14,714,660

4,914,807 5,570,232 6,276,552 7,007,319

5,843,350 6,096,250 6,850,558 7,707,341

514,966 583,495 657,361 733,790

5,328,384 5,512,755 6,193,197 6,973,551

1,448,788 1,498,918 1,683,930 1,896,109

3,879,596 4,013,837 4,509,267 5,077,443

2.96 3.07 3.45 3.88

1.04 1.10 1.24 1.44

M e r i s t e m R e s e a r c h

Fair Price (N): 65.77

Premium/ (Discount): -14.39%

Upside/ (Downside): 16.81%

2012F Average

109,888,980 120,877,878 98,934,778

75,114,201 82,669,602 67,579,987

34,774,779 38,208,277 31,354,790

219,778 302,195 173,898

34,994,557 38,510,471 31,528,688

6,439,494 7,035,093 5,762,937

(567,825) (683,621) (534,588)

20,847,722 22,941,924 18,759,561

7,707,341 8,533,455 7,006,191

733,790 808,192 659,561

20,279,897 22,258,303 18,224,973

28,021,006 30,785,208 25,182,058

14,714,660 16,252,168 13,303,715

7,007,319 7,718,713 6,297,525

7,707,341 8,533,455 7,006,191

733,790 808,192 659,561

6,973,551 7,725,263 6,346,630

1,896,109 2,100,499 1,725,649

5,077,443 5,624,764 4,620,981

3.88 4.30 3.53

1.44 1.59 1.28

18 | P a g e

Industry: Food/Beverages and Tobacco

FYE: December 31

Mkt Cap (N’bn): 64.11 (US$ 556.50m)

IMPORTANT DISCLOSURES

Meristem Research equity analysis stock report and its attendant

recommendations are prepared based on publicly available

information and are meant for general informative purposes.

Meristem Research can neither guarantee the accuracy nor

completeness of the information as they are an expression of

our analysts’ views and opinions. Meristem Research cannot be

held responsible for any loss suffered by relying on the said

information as this information as earlier stated is based on

estimates and opinions and is meant for general information

purposes and not as solicitation to buy securities and financial

instrument.

© Meristem Research

MERISTEM SECURITIES LTD

124, Norman William Street,

Ikoyi, Lagos.

Phone: 234-01-2717350-5, Fax: 2717356

E-mail: [email protected]

Website: www.meristemng.com

Nigeria Equity Research August 6, 2008

M e r i s t e m R e s e a r c h

Nigeria Equity Research

August 19, 2008

Current Price (N): 49.92 Fair Price

52-Wk H/L (N): 70.00/40.00 Premium/ (Discount):

Volatility (β): 0.48 Upside/ (Downside):

Meristem Research equity analysis stock report and its attendant

recommendations are prepared based on publicly available

information and are meant for general informative purposes.

Meristem Research can neither guarantee the accuracy nor

he information as they are an expression of

our analysts’ views and opinions. Meristem Research cannot be

held responsible for any loss suffered by relying on the said

information as this information as earlier stated is based on

is meant for general information

purposes and not as solicitation to buy securities and financial

5, Fax: 2717356

M e r i s t e m R e s e a r c h

Fair Price (N): 65.77

Premium/ (Discount): -14.39%

Upside/ (Downside): 16.81%