Negotiating Contractual Indemnity in M&A Deals:...

31

Negotiating Contractual Indemnity in M&A Deals: Transactional and Litigation Considerations Structuring Terms to Minimize Financial Risks, Measuring Damages in the Event of Breach Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10. THURSDAY, MAY 1, 2014 Presenting a live 90-minute webinar with interactive Q&A Lisa S. Lathrop, Partner, Jones Day, Chicago Adam R. Schaeffer, Partner, Jones Day, Chicago

-

Upload

phungquynh -

Category

Documents

-

view

220 -

download

3

Transcript of Negotiating Contractual Indemnity in M&A Deals:...

Negotiating Contractual Indemnity in M&A Deals: Transactional and Litigation Considerations Structuring Terms to Minimize Financial Risks, Measuring Damages in the Event of Breach

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

THURSDAY, MAY 1, 2014

Presenting a live 90-minute webinar with interactive Q&A

Lisa S. Lathrop, Partner, Jones Day, Chicago

Adam R. Schaeffer, Partner, Jones Day, Chicago

Tips for Optimal Quality

Sound Quality If you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection. If the sound quality is not satisfactory, you may listen via the phone: dial 1-888-450-9970 and enter your PIN when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem. If you dialed in and have any difficulties during the call, press *0 for assistance. Viewing Quality To maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

For CLE purposes, please let us know how many people are listening at your location by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of attendees at your location

• Click the SEND button beside the box

If you have purchased Strafford CLE processing services, you must confirm your participation by completing and submitting an Official Record of Attendance (CLE Form).

You may obtain your CLE form by going to the program page and selecting the appropriate form in the PROGRAM MATERIALS box at the top right corner.

If you'd like to purchase CLE credit processing, it is available for a fee. For additional information about CLE credit processing, go to our website or call us at 1-800-926-7926 ext. 35.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Negotiating Contractual Indemnity in M&A Deals

May 1, 2014

Lisa Lathrop and Adam Schaeffer, Jones Day

Goals

• Talk about recent experience and trends in negotiating indemnification provisions in M&A deals.

• Highlight most negotiated and “trendy” indemnification issues and provisions.

• Assuming basic understanding of indemnification provisions (i.e., what they generally do / how they work).

• Happy to answer questions, basic or complicated, at the end or offline.

6

I. Indemnification Generally

7

Indemnity – Generally

• A contractual remedy for specified items (e.g., breaches of contract; specified liabilities)

• Absence of an indemnification provision doesn’t mean that a contracting party doesn’t have a remedy; rather you would have a breach of contract claim

• Indemnification provisions not only help the injured party recover, they limit the indemnifying party’s obligations

8

• Indemnified / indemnifying parties • Subject of indemnification • Limitations on indemnity

• Survival • Caps, baskets, etc. • Other carveouts and limitations

• Procedures for making indemnity claims (third-party; direct)

9

Key Components

• Seller(s) / Buyer • Escrows • Holdbacks • Setoff • Is recovery limited to a particular source?

10

Source of Indemnification

Indemnification in Multi-Seller Transactions • Joint vs. several liability

• Joint: “The Sellers will, on a joint and several basis, indemnify the Buyer Parties from and against any Losses arising from any breach of any representation of the Company . . . ”

• Several: “Each Seller will, on a several and not joint basis, indemnify the Buyer Parties from and against any Losses arising from any breach of such Seller’s representations . . . ”

• Pro rata share of each claim • “Each Seller will indemnify the Buyer Parties up to its Pro

Rata Share from any Losses arising from any breach of any representation of the Company . . . ”

• Individual caps • Consider applicability among various indemnity provisions

• Indemnification through ancillary agreements

11

Items Typically Subject to Indemnification

• Breaches of reps/warranties • Breaches of covenants • Excluded liabilities

• Pre-closing liabilities (asset deal or quasi- asset deal)

• Pre-closing taxes • Specified matters

• Environmental items • Litigation items • Items disclosed during diligence

12

Definition of Losses • Key seller concepts:

• Opportunity to embed exclusions of consequential and punitive damages

• Opportunity to resist “diminution of value” claims or losses based on a multiple

• Opportunity to embed “de minimis” concept • Key buyer concepts:

• Resist seller’s request for exclusions • Try to cover costs of bringing indemnification claims

• Example: “Loss” means to the extent actually paid or incurred: all losses, liabilities, damages (including excluding consequential, incidental and indirect damages and lost profits), judgments, interest, Taxes, deficiencies, demands, payments, fines, costs, penalties, amounts paid in settlement, assessments or awards and reasonable out-of-pocket costs and expenses incurred in connection therewith (including costs and expenses of suits and Legal Proceedings) and investigation and defense thereof, and reasonable costs and expenses of enforcing a Party’s rights hereunder.

13

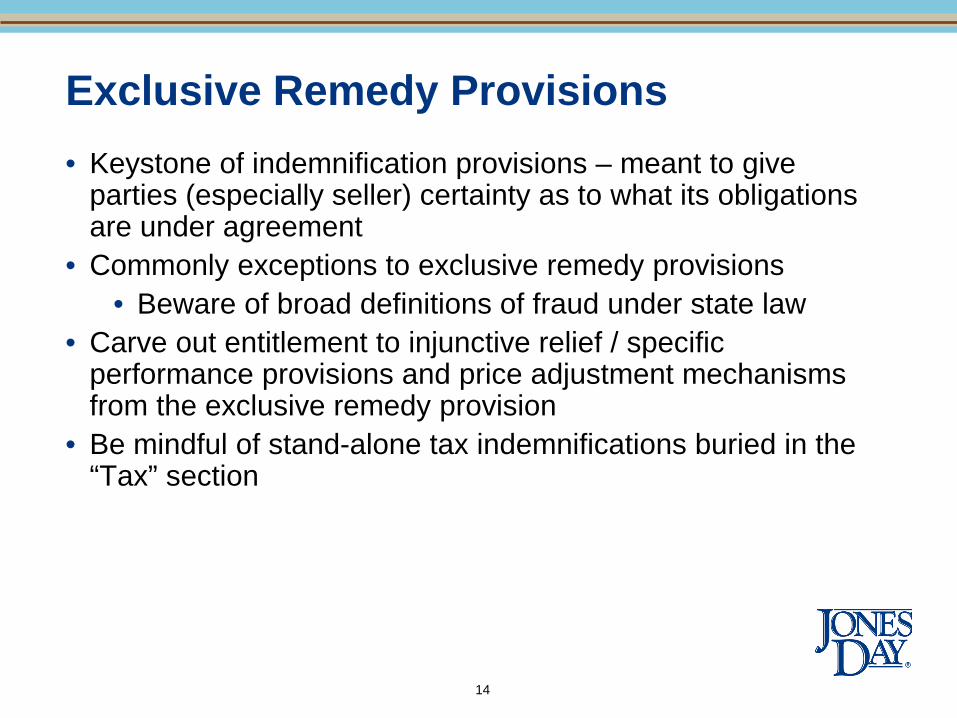

Exclusive Remedy Provisions • Keystone of indemnification provisions – meant to give

parties (especially seller) certainty as to what its obligations are under agreement

• Commonly exceptions to exclusive remedy provisions • Beware of broad definitions of fraud under state law

• Carve out entitlement to injunctive relief / specific performance provisions and price adjustment mechanisms from the exclusive remedy provision

• Be mindful of stand-alone tax indemnifications buried in the “Tax” section

14

II. Limitations on Indemnification

15

• Monetary: caps / baskets / mini-baskets • Time periods • Types of losses • Net losses • Subjective limitations and “gotchas”

16

Limitations Generally

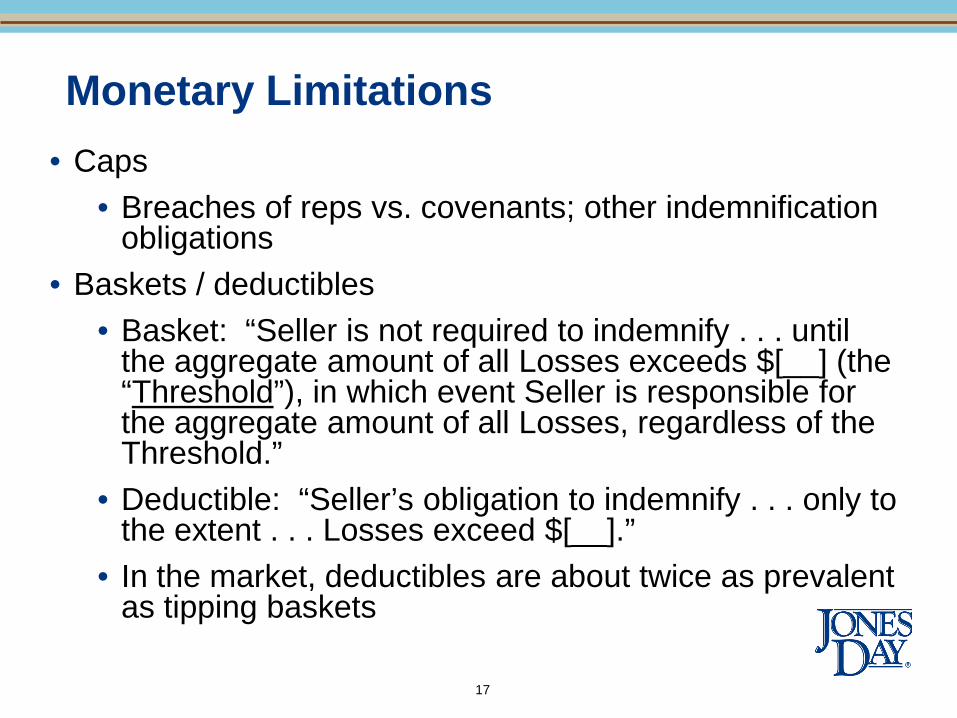

• Caps • Breaches of reps vs. covenants; other indemnification

obligations • Baskets / deductibles

• Basket: “Seller is not required to indemnify . . . until the aggregate amount of all Losses exceeds $[__] (the “Threshold”), in which event Seller is responsible for the aggregate amount of all Losses, regardless of the Threshold.”

• Deductible: “Seller’s obligation to indemnify . . . only to the extent . . . Losses exceed $[__].”

• In the market, deductibles are about twice as prevalent as tipping baskets

17

Monetary Limitations

• Common Basket carveouts • Fundamental representations • Taxes • Benefits • Environmental • Title to assets

• Most frequently, indemnification claims other than those arising from breaches of representations are not subject to basket

18

Monetary Limitations

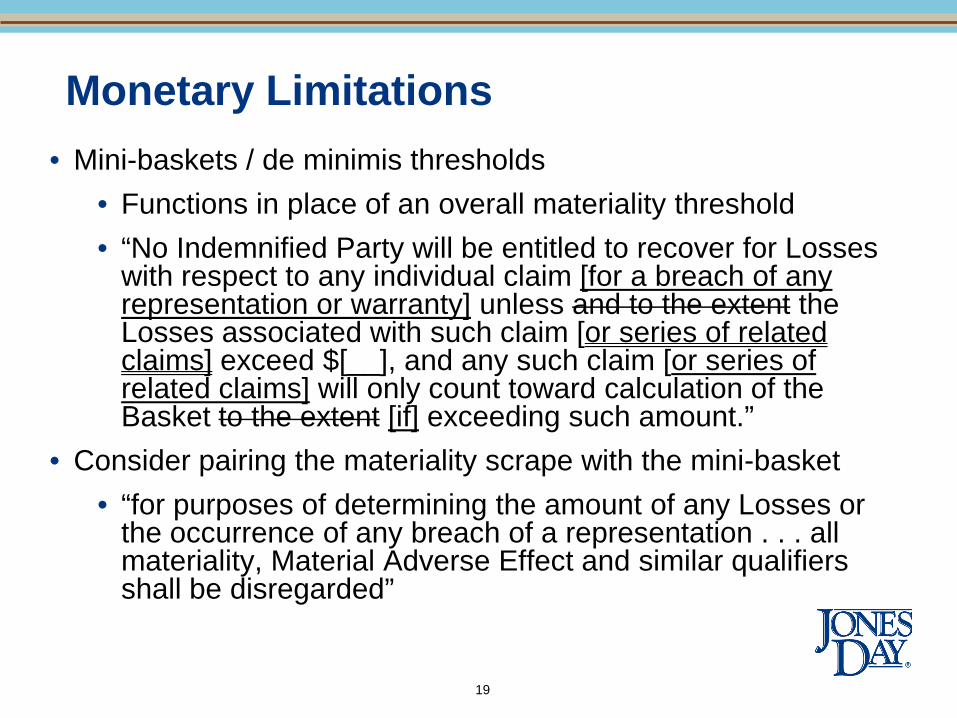

• Mini-baskets / de minimis thresholds • Functions in place of an overall materiality threshold • “No Indemnified Party will be entitled to recover for Losses

with respect to any individual claim [for a breach of any representation or warranty] unless and to the extent the Losses associated with such claim [or series of related claims] exceed $[__], and any such claim [or series of related claims] will only count toward calculation of the Basket to the extent [if] exceeding such amount.”

• Consider pairing the materiality scrape with the mini-basket • “for purposes of determining the amount of any Losses or

the occurrence of any breach of a representation . . . all materiality, Material Adverse Effect and similar qualifiers shall be disregarded”

19

Monetary Limitations

Time Periods to Bring Claims • Time limitations on claims for breaches of reps and

warranties vs. covenants • Carveouts

• Statute of limitations considerations • Delaware: Marathon; proposed amendments • I/MX Information Management Solutions

– Must provide that claim survives if notice is given – Sample: “to the extent any claim for indemnification

. . . is made on or before the date on which such representation expires, such representation will survive until the resolution of such claim.”

20

• The trend has been to adopt “boilerplate” consequential damages waivers: “Notwithstanding anything to the contrary herein, no party shall be liable for special, punitive, exemplary, incidental, consequential or indirect damages, lost profits or lost benefits, loss of enterprise value, diminution in value of any business, damage to reputation, loss to goodwill or any damages calculated based on a multiple, whether based on contract, tort, strict liability, other law or otherwise and whether or not arising from any other party’s sole, joint or concurrent negligence, strict liability or other fault.”

• Recent market studies show that consequential damages were expressly excluded in 54% of transactions; incidentals excluded in 17%; punitives in 75%*

21 *Source: ABA’s 2013 Private Target Mergers & Acquisitions Deal Points Study.

Limiting Types of Recoverable Damages

• What do these terms mean? • “Punitive” and “Exemplary” damages are essentially the same thing –

a measure to penalize an actor • “Incidental” damages – a term from the UCC that means damages

incurred in correcting breach (i.e., a specialty tool to fix a damaged product)

• “Direct” and “General” damages – damages that naturally and necessarily flow from a breach

• “Consequential” damages – inconsistent meanings, but interpreted to mean damages that ensue because of special circumstances of the buyer (and are not the natural result of the breach)

• “Special” damages – essentially synonymous with consequential damages

• “Lost profits,” “diminution in value,” “losses based on a multiple” – these are all valid measurements of lost value in the right circumstance

22

Exclusions of “Consequential” and Other Damages

• Law school: Hadley v. Baxendale

• Direct damages v. consequential damages

• Consequential: losses arising from the non-breaching party’s special circumstances

• Generally recoverable if reasonably foreseeable or contemplated by the parties at the time the contract was entered into as a probable result of the breach

• Compare to remote or speculative damages, which are damages that were not contemplated by the parties and are not recoverable under general contract law

• Negotiating tactics

23

What are “Consequential” Damages?

Actual Damages - “Benefit of the Bargain” Damages

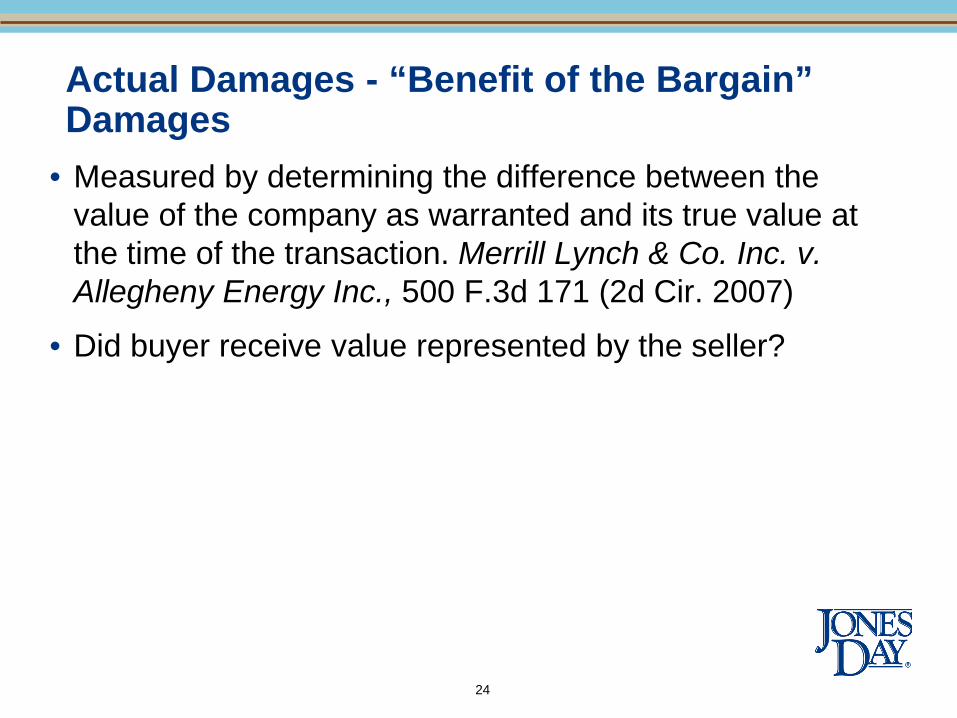

• Measured by determining the difference between the value of the company as warranted and its true value at the time of the transaction. Merrill Lynch & Co. Inc. v. Allegheny Energy Inc., 500 F.3d 171 (2d Cir. 2007)

• Did buyer receive value represented by the seller?

24

Damages Using “Multiple of Earnings” as a Measure

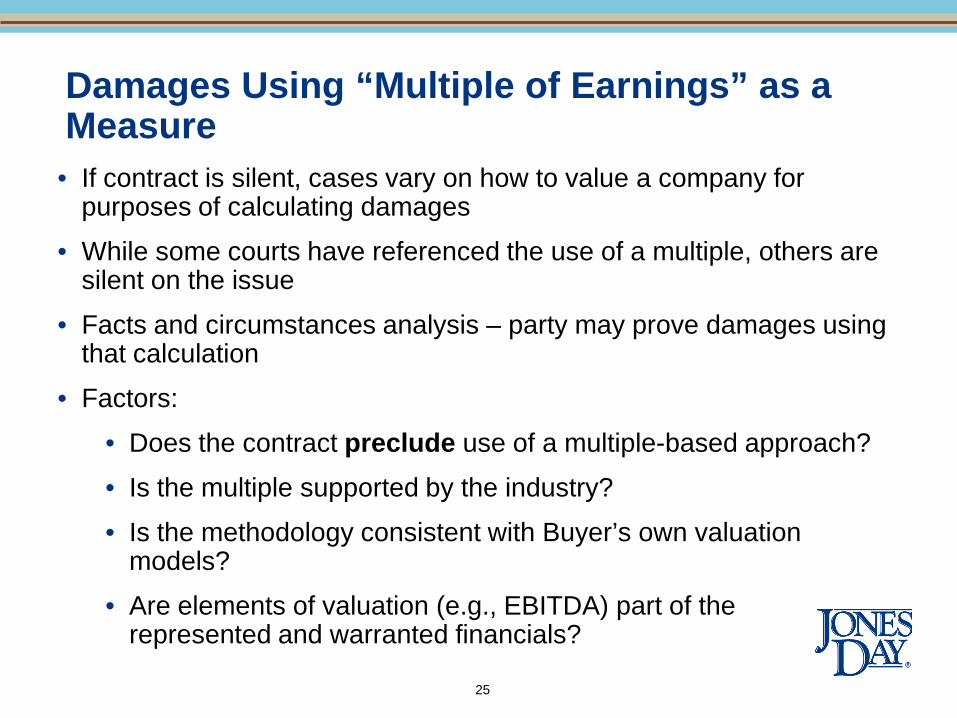

• If contract is silent, cases vary on how to value a company for purposes of calculating damages

• While some courts have referenced the use of a multiple, others are silent on the issue

• Facts and circumstances analysis – party may prove damages using that calculation

• Factors:

• Does the contract preclude use of a multiple-based approach?

• Is the multiple supported by the industry?

• Is the methodology consistent with Buyer’s own valuation models?

• Are elements of valuation (e.g., EBITDA) part of the represented and warranted financials?

25

• Using this term to mean limitations on recoveries where third party claims, insurance claims and tax benefits may be available to offset a loss

• Third party and insurance claims

• “The right to indemnification for a particular claim will be reduced by the amount [payable by / actually recovered from] a third party (including an insurance company) with respect to such claim, less any costs or expenses incurred by in connection with its collection of such amount (including any increased premiums)”

• Is the indemnified party required to pursue?

• Tax benefits

• Difficult to measure

• May extend several years 26

Net Losses

Subjective Limitations and “Gotchas” • Limitations on indemnification that are not necessarily cut

and dry

• Duty to mitigate

• Required under most state laws

• Always provides the indemnifying party with a subjective argument that the indemnified party didn’t do everything possible to stem a loss

• Exacerbation provisions

• Specific notice periods

• Exclude delays that do not result in material prejudice to the indemnifying party

27

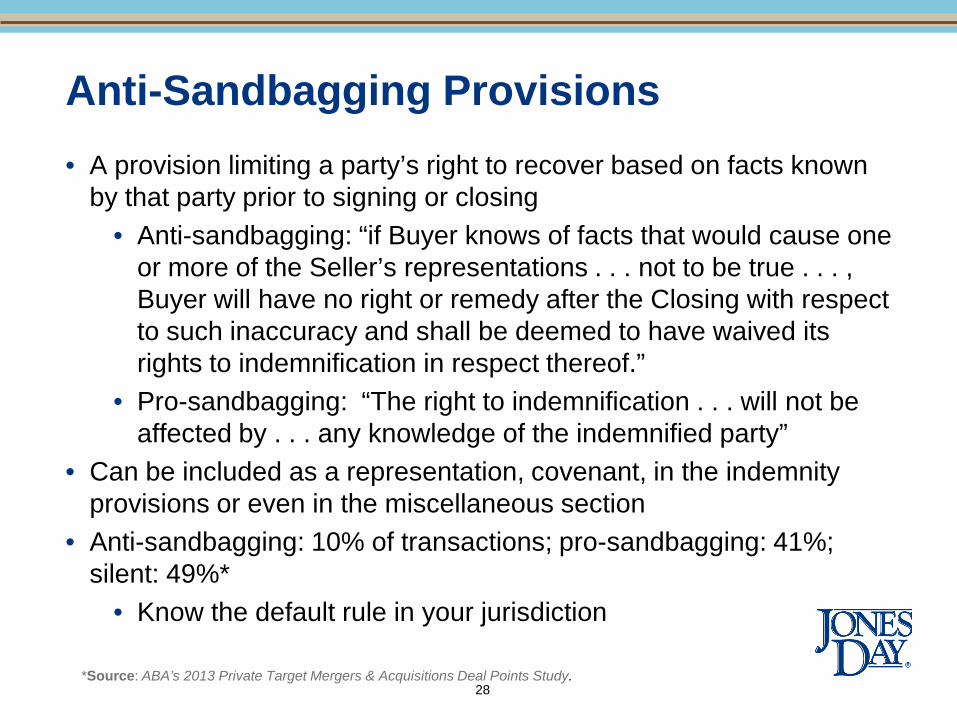

Anti-Sandbagging Provisions • A provision limiting a party’s right to recover based on facts known

by that party prior to signing or closing • Anti-sandbagging: “if Buyer knows of facts that would cause one

or more of the Seller’s representations . . . not to be true . . . , Buyer will have no right or remedy after the Closing with respect to such inaccuracy and shall be deemed to have waived its rights to indemnification in respect thereof.”

• Pro-sandbagging: “The right to indemnification . . . will not be affected by . . . any knowledge of the indemnified party”

• Can be included as a representation, covenant, in the indemnity provisions or even in the miscellaneous section

• Anti-sandbagging: 10% of transactions; pro-sandbagging: 41%; silent: 49%*

• Know the default rule in your jurisdiction

28 *Source: ABA’s 2013 Private Target Mergers & Acquisitions Deal Points Study.

Indemnification Claim Procedures • Requirements to give notice • Control of third-party litigation

• Litigation conditions –Competent defense –Conflicts of interest –Coverage of cost of indemnified party’s counsel

• No settlement without consent of indemnified party • Indemnifying part covers all amounts payable • Unconditional release of liability

29

Environmental Indemnification • No-dig • Cleanup standards • Control of remediation

30

31

Adam Schaeffer concentrates his practice in the areas of mergers and acquisitions, leasing transactions, and general corporate matters. He represents buyers, sellers, and management teams in public and private acquisitions and divestitures, restructurings, joint ventures, and other strategic alliances, including those in distressed and non-distressed settings. He regularly advises clients regarding general corporate matters, including corporate governance, fiduciary issues, and strategic planning, and in connection with the negotiation of commercial contracts. Adam has represented clients in a wide range of industries, including manufacturing, mining, aerospace, agriculture, health care, pharmaceuticals, logistics, and software. Adam is a frequent speaker on M&A and transactional topics.

Adam R. Schaeffer Partner, Mergers & Acquisitions Telephone: 312.269.1565 Facsimile: 312.782.8585 Email: [email protected]

Lisa Lathrop has acted as the principal lawyer in a wide variety of transactions involving privately held companies, with a focus on representing private equity funds and their portfolio companies. In doing so, she has experience working with a variety of deal structures in a wide range of industries. Lisa has extensive experience in leveraged buyout transactions, corporate restructurings, equity financings, mergers and acquisitions, and general corporate counseling. She leads the Private Equity Practice in the Chicago Office. Clients Lisa has represented include Baird Capital, Brockway Moran & Partners, High Road Capital Partners, Industrial Growth Partners, Kirtland Capital Partners, Primus Capital Partners, and The Riverside Company.

Lisa S. Lathrop Partner, Private Equity Telephone: 312.269.1528 Facsimile: 312.782.8585 Email: [email protected]

Biographies