Nedim Baruh

20

Framework Nedim Baruh Director

Transcript of Nedim Baruh

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 1/20

Framework

Nedim Baruh

Director

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 2/20

Agenda

¾ Operational Risk Elements

Strengths & Weaknesses

¾ External Data 101 Types of External Data

Key Considerations

Case Study

¾ Approaches to Uses

Inclusion into Capital Model

Direct & Indirect

¾ Conclusion

©2010 Algorithmics Incorporated. All rights reserved. 2

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 3/20

Pillar 1 AMA Requirements

Capital model must consider the four data elements

,

The Chief Executive must sign off on a comprehensive waiver application

Internal Loss Data¾ Losses arising from operational

risk events

¾ Collected via an

External Loss Data¾ Losses arising from operational risk events

occurring in other organizations

Collected by external providers or

internal lossreporting process

above a certain

threshold

“An institution must demonstrate that it

has appropriate internal loss

event data , relevant external loss event data ,

consortiums— External databases contain

publicly reported data

— Consortium data contain data

from participating firms

internal controls factors , and results from

scenario analysis to support its operational

risk management and

measurementframework.”

Scenarios

¾ Potential

operational risk

Business Environment &

Control Factors

events could occur

based on business expertise

¾ Collected via a facilitated

workshop

A collection of risk and controls based

on an organization’s processes

A collection of key indicators that aims to proactively

©2010 Algorithmics Incorporated. All rights reserved. 3

ent y potent a areas o r s

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 4/20

Challenges to Modeling Operational Risk Capital

Understanding the strengths and weaknesses of elements allows for their appropriate use within thecapital modeling methodology and overall management of operational risk

Internal

Data

External

DataScenario RCSA

Can be used to trackaggregateperformance

Can “sum” loss

StrengthsEasily available

from publicandconsortium

Used to identifypotentialevents

Engages business

Used to escalaterisk concernsand controldeficiencies

events both up

and across anorganization

a a ase

providersUsed to inform

aboutotential

units Can be used as

an incentive

Takes a long time to

collect sufficientWeaknesses

events

Relevance

Subjective

Can be difficult to“sum”

Difficult to “sum”

risks,

especially

Lags business andenvironmentalchanges

Scaling issues

Reporting bias

because of overlaps/gaps in scenariogeneration

qualitativerankings

Subjective

Time intensive

©2010 Algorithmics Incorporated. All rights reserved. 4

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 5/20

Types of External Loss Data

Publically Available Database

FIRST OpData:

Consortium Data

ABA ORX IRST, OpData:losses

ABA, ORX: on-pu c poo e op r s osses

Accurate & Verifiable Provides a wider range of loss

Qualitative & Quantitative: Providesdescriptive info about the loss and the

sever es

More complete loss profile of giveninstitution

• Allows for meaningful data selection & scaling

Analysis of control breakdowns and lessons

Emerging patterns, warning signs, implicationsfor industry

Reporting & control bias;overrepresentation of extreme losses

Relevance; lack of completeness

Lack of detailed event information

©2010 Algorithmics Incorporated. All rights reserved. 5

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 6/20

Key Considerations

“Reading an article in isolation is not as powerful as reading 40-50 case studies, or being

able to see the whole universe of problems, losses and frauds”

Establishing Relevance

¾Post-mortem analysis – identifying an event trigger , as well as control failings and

contributory factors that allow users to analyze whether it could happen to MY BANK

Risk identification – ’isk identification

an accurate reflection of MY BANK’s which means that risk identification needs to be lookedat in a context broader than one company’s direct loss experience

New product analysis – ew product analysis

integration of risk concerns within the new product approval process so as to help establish

proper controls against identified risks when a new product is brought to market

©2010 Algorithmics Incorporated. All rights reserved. 6

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 7/20

Asking the right questions

1. Could this type of event happen to me?

. ,

3. If yes, how? What could the impact be?

4. What can I learn from this event?

5. Are there lessons that can help my business become more effective?

6. Can we see any patterns and trends across different events that indicate a growing

concern?

7. Were there any warning signs? Indicators?

.

9. How did management respond to the event?

10. How would our mana ement res ond if this event ha ened to us?

The key is making an event one’s own!

©2010 Algorithmics Incorporated. All rights reserved. 7

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 8/20

Analyzing Impact

¾ Analyze other organizations’ exposure to the same risks and use that information to.

¾ Develop a catalogue of key “what-if” scenarios:

What will happen if:

a fall in demand for services occurs

em lo ee turnover increases dramaticall

regulations change how services can be priced

certain business practices come under attack by regulators, customers and the media

©2010 Algorithmics Incorporated. All rights reserved. 8

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 9/20

Public Data: Dispelling the Myths

¾ External events are not relevant to my bank because they occurred to someone elseand in a different control environmentnd in a different control environment

• External events provide the content and context to fully dissect potential problems

• Control breakdowns can be used as a benchmark ‘ ’• an e use o per orm ea -c ec o your an

¾ Only events that occurred to institutions in my same sector and geography arerelevant to meelevant to me

• All firms, no matter their sector, are exposed to national regulations, such as anti-trust andanti-discrimination laws

• – ,

¾

External events occurred in the past and are not relevant to an analysis of whatcould happen in the futureould happen in the future

Similar control breakdowns occur frequently

Patterns can be observed that become predictive of future events

©2010 Algorithmics Incorporated. All rights reserved. 9

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 10/20

Case Study: Dwelling House S&L (Pittsburgh, PA)

Dwelling House closed on August 14, 2009 by OTS

assume . m on n epos s

Bank had $13.4 million in assets when closed

...and poor bookkeeping that failed to detect crime formore than one year

Criminals transferred proceeds into accounts held with62 financial institutions

Bank’s capital base was depleted by the time the crimewas discovered

opening accounts for prisoners

©2010 Algorithmics Incorporated. All rights reserved. 10

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 11/20

Case Study: Dwelling House S&L -- Questions

Could such a fraud occur within our organization?

capital base?

Could a smaller fraud occur over a period of timew t ou etect on ou sma w t rawa s o un sby employees or fraudsters add up to somethingsubstantial over time?

What control breakdowns could occur for money to besiphoned out of the bank for over one year withoutdetection?

What is the state of these controls? Are they currently being attended to?

-practices?

Could such practices result in reputational issues?

©2010 Algorithmics Incorporated. All rights reserved. 11

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 12/20

Approaches to Using Public External Data

Direct Role

Indirect Role

¾ Statistical comparisons identify areas where

external data could be used to ‘fill in’ gaps in

internal data

¾Used to benchmark internal loss data and data

models assuming certain characteristics such as

nature and details - size of loss, categorization

¾ Statistical comparisons identify ways in which

external data could be directly combined with

internal data

¾Techni ues includes

o even are compara e

Informing Scenario Analysis

¾Provide depth of information to ensure

sufficient context for scenario eneration

−EVT Analysis, Body & Tail, Credibility Theory

− Synthetic Data Points

¾Use the event detail as content to build theirown internally relevant scenarios

Assessin Business Control & Environmental Factors− Scaling

• Conventional vs. Statistical

Homogeneity Scaling

¾ Identify potential areas of risk and control

failures by analyzing how similar failures

would occur in one’s own organization• Bayes an Approac to er ve sever ty

distributions

©2010 Algorithmics Incorporated. All rights reserved. 12

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 13/20

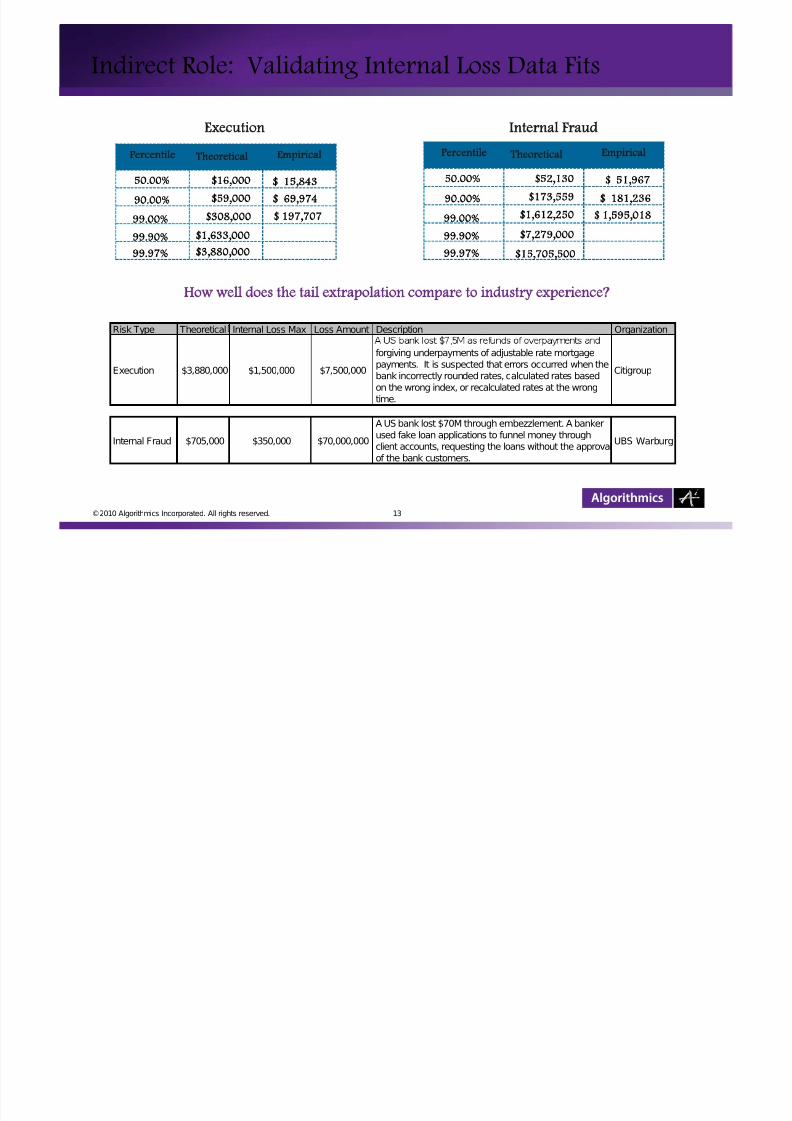

Indirect Role: Validating Internal Loss Data Fits

E i i ll

Execution Internal Fraud

Empiricalercentile Th ti lmpiricalercentile

$16,000

$59,000

$308 000

50.00%

90.00%

$ 15,843

$ 69,974

$ 197 707

Theoretical Empiricalercentile

$52,130

$173,559$1 612 250

50.00%

90.00%

$ 51,967

$ 181,236

$ 1 595 018

Theoretical

$308,000

$1,633,000

$3,880,000

99.00%

99.90%

99.97%

$ 197,707 $1,612,250

$7,279,000

$15,705,500

99.00%

99.90%

99.97%

$ 1,595,018

Risk Type Theoretical Internal Loss Max Loss Amount Description Organization

How well does the tail extrapolation compare to industry experience?

Execution $3,880,000 $1,500,000 $7,500,000

.

forgiving underpayments of adjustable rate mortgage

payments. It is suspected that errors occurred when the

bank incorrectly rounded rates, calculated rates based

on the wrong index, or recalculated rates at the wrong

time.

Citigroup

Internal Fraud $705,000 $350,000 $70,000,000

A US bank lost $70M through embezzlement. A banker

used fake loan applications to funnel money through

client accounts, requesting the loans without the approval

of the bank customers.

UBS Warburg

©2010 Algorithmics Incorporated. All rights reserved. 13

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 14/20

Indirect Role: Validating Internal Loss Data Fits

Comparing External and Internal LossData Distributions

Severity Distribution

Data Distributions

¾Conduct a qualitative analysis of the external

1.0

a a y assess ng even ca egor a ons,reviewing event details, and analyzing datapatterns and trends

¾Compare the shape of the distributions and

0.9

r o b a b i l i t y

Fitted

size of the losses between internal and externaldata

Plot losses for the internal business unit againstthe CDF of the corres ondin external usiness

0.8

FittedLoss Data (Algo)

unit

QQ-plots

Compare percentiles

0.7

$10,000 $100,000 $1,000,000 $10,000,000 $100,000,000

Loss Amount

xam ne stat st ca measures o goo ness-o - t(KS test, etc)

©2010 Algorithmics Incorporated. All rights reserved. 14

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 15/20

Indirect Role: Informing Scenario Analysis

Examples: Scenario Analysisuses external data to

Business Unit

Severity Buckets

$100k - $1M $1M - $10M $10M - $20M $20M - $50M $50M - $100M $100M+Risk Type

Max Single

generate scenario examplesof potential losses that

‘could happen’

Internal Fraud 11 11 0.15 0.05 0.05 0.05 100M

External Fraud 0.67 2 0.2 0.1 0.02 0.01 250M

CPBP 1.33 0.67 0.1 0.05 0.67 0.02 30M

EPWS 5 2 0.2 0.1 1.33 0.02 50MBDSF 0.67 0.1 0.05 0.15 5 0.05 500M

Max Loss: External data isused to determine the

EDPM 2 0.2 0.1 0.2 0.67 0.05 100M

DPA 11 0.5 0.1 0.2 0.2 0.15 20M

appropr ate s ze o a s ng emaximum loss event for a given event type Distribution of losses

Probability

Control Breakdowns:

Interviews, an important UnexpectedExpected,

used to determine wherecontrol breakdowns couldoccur - an o erational loss

LossesLosses

©2010 Algorithmics Incorporated. All rights reserved. 15

. percen eAnnual aggregate

loss ($)

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 16/20

Indirect Role: Max Loss Example

• “Sample Bank” has Structured ScenarioEvent Type

10K -

50K

50K -

100K

100K -

250K

250K -

500K

500K -

1MM

1MM + Max Loss

• Workshop participants provided incomplete

Risk Scenario 1 0.2 0.1 0.1 0.05 0.02

Risk Scenario 2 0.1 0.05

Risk Scenario 3 0.1 0.05 0.04 0.04 0.04 0.04 100k

Risk Scenario 4 0.05 0.05 0.05 0.05 0.05 0.2Risk Scenario 5 0.05 0.02 1mm

max oss a a po n s an max oss es ma es

that were low compared to industry data

Sample BankExternal Data

Max Loss

• “Sample Bank” can directly incorporate loss

amounts from external data that could

represent the max loss

Risk Scenario 11mm

Risk Scenario 2 25mm

Risk Scenario 3 100k

Risk Scenario 4 2.5mm

• Step1: Perform qualitative analysis

• Step 2: Map relevant BU/ETs

• Ste 3: Review size of relevant losses

s cenar o mm

• Step 4: Generate frequency/severity dist.

• Step 5: …………….

©2010 Algorithmics Incorporated. All rights reserved. 16

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 17/20

Indirect Role: Assessing BC&E Factors

Risk & Control Self-Assessments

Provides content and context for events used

to compare whether an organization is

¾ exposed to similar risks

¾ vulnerable to similar control weaknesses

Key Indicatorsey Indicators

Used to find commonalities among events

¾ Identifying commonalities help uncover

characteristics of a specific type of event

¾These indicators could be monitored over time to

identify the trends that would trigger a similarevent to appen

¾Indicators could be internal as well as external

(e.g., Cyclicality of Operational Risk: The Tracking

©2010 Algorithmics Incorporated. All rights reserved. 17

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 18/20

Direct Role: Addressing the Paucity of Internal Data

External data is necessary here e r o f e v e n t

N u m

Size of loss

Prerequisite:Good internal data but missing tail, good external data to describe tail

Assumption:External data comes from identified eers and relevance to same external data set

Modeling Approaches:

¾Extreme Value Theory principles applied to external data used to complete the loss distribution

¾Body & Tail combination modeling to complete risk profile, with internal data for the body and external data

as for the tail of the distribution

¾Use Credibility Theory to combine components of the severity distribution

©2010 Algorithmics Incorporated. All rights reserved. 18

− Useful in stress testing impact of use of external data

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 19/20

Direct Role: ‘Filling Out’ the ‘Fat Tail’

External data is necessary here e r o f e v e n t

N u m

Size of loss

Prerequisite:Available internal data but with gaps

Assumption:External data comes from identified eers and direct relevance to same external data set

Modeling Approaches:

¾Synthetic Data Point methodology by utilizing external data with assigned likelihoods, incorporate intointernal data set and fit a severity distribution across data set

¾Max Loss helps address the max loss question by directly incorporating loss amounts that could represent

the max loss

©2010 Algorithmics Incorporated. All rights reserved. 19

7/28/2019 Nedim Baruh

http://slidepdf.com/reader/full/nedim-baruh 20/20

Conclusion

¾ External data can be used either directly in operational risk capital models to address gaps or

¾ It is important to understand the drawbacks of external data and to use it in the most effective

¾ In deciding how to incorporate external data, it is important to evaluate the “inventory” of

n erna a a ava a e o an ns u on – s w e erm ne ow es o u ze ex erna a a

Industry best practice and the most effective way is to use external data is in a supporting

ro e o n erna a a, scenar os an us ness con ro env ronmen a ac ors

Using external data directly in capital modeling opens up additional questions aboutassumptions t at may e i icu t to support an e en ot interna y to usiness managers

and externally to regulators

©2010 Algorithmics Incorporated. All rights reserved. 20