Mobile Telecom - · PDF fileMobile Telecom Building Connections ... Continuous decline in the...

18

Mobile Telecom Building Connections January 2016 Pakistan Cellular Industry Industry – Structure Regional Comparison Snapshot

Transcript of Mobile Telecom - · PDF fileMobile Telecom Building Connections ... Continuous decline in the...

Mobile TelecomBuilding Connections

January 2016

Pakistan Cellular Industry

Industry – Structure

Regional Comparison

Snapshot

Pakistan Cellular Industry

Industry – Structure Regional Comparison Snapshot

Year (Fixed + WLL) Mobile Total

2003-04 3 3 6

2004-05 4 8 12

2005-06 4 22 26

2006-07 4 40 44

2007-08 4 55 59

2008-09 4 58 62

2009-10 4 60 64

2010-11 4 65 68

2011-12 4 69 72

2012-13 4 71 75

2013-14 3 76 80

2014-15 2 61 63

Sep-15 2 63 65

Teledensity (%)

Teledensity in Pakistan

Pakistan Cellular Industry

Industry – StructureRegional

ComparisonSnapshot

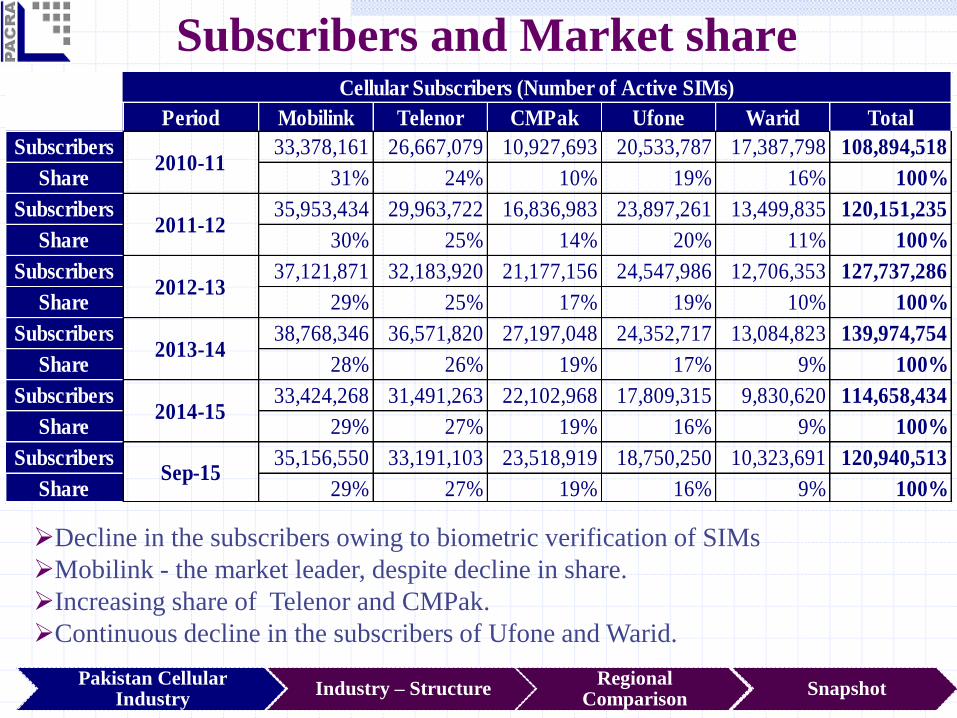

Decline in the subscribers owing to biometric verification of SIMs

Mobilink - the market leader, despite decline in share.

Increasing share of Telenor and CMPak.

Continuous decline in the subscribers of Ufone and Warid.

Subscribers and Market share

Period Mobilink Telenor CMPak Ufone Warid Total

Subscribers 33,378,161 26,667,079 10,927,693 20,533,787 17,387,798 108,894,518

Share 31% 24% 10% 19% 16% 100%

Subscribers 35,953,434 29,963,722 16,836,983 23,897,261 13,499,835 120,151,235

Share 30% 25% 14% 20% 11% 100%

Subscribers 37,121,871 32,183,920 21,177,156 24,547,986 12,706,353 127,737,286

Share 29% 25% 17% 19% 10% 100%

Subscribers 38,768,346 36,571,820 27,197,048 24,352,717 13,084,823 139,974,754

Share 28% 26% 19% 17% 9% 100%

Subscribers 33,424,268 31,491,263 22,102,968 17,809,315 9,830,620 114,658,434

Share 29% 27% 19% 16% 9% 100%

Subscribers 35,156,550 33,191,103 23,518,919 18,750,250 10,323,691 120,940,513

Share 29% 27% 19% 16% 9% 100%Sep-15

2010-11

2011-12

2012-13

2013-14

2014-15

Cellular Subscribers (Number of Active SIMs)

Pakistan Cellular Industry

Industry – Structure Regional Comparison Snapshot

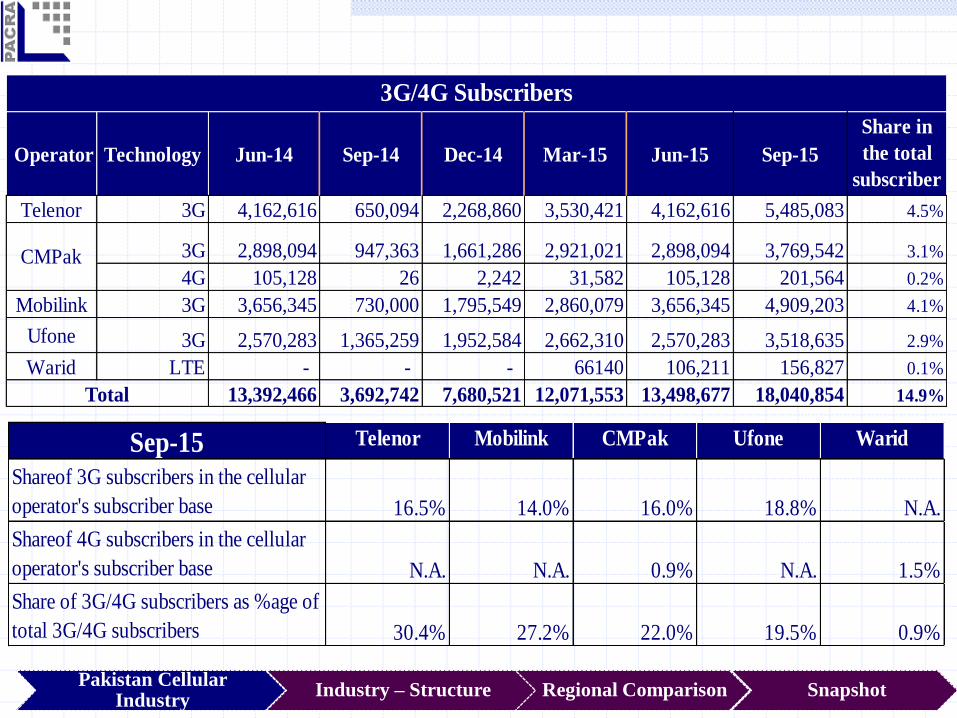

Operator Technology Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15

Share in

the total

subscriber

sTelenor 3G 4,162,616 650,094 2,268,860 3,530,421 4,162,616 5,485,083 4.5%

3G 2,898,094 947,363 1,661,286 2,921,021 2,898,094 3,769,542 3.1%

4G 105,128 26 2,242 31,582 105,128 201,564 0.2%

Mobilink 3G 3,656,345 730,000 1,795,549 2,860,079 3,656,345 4,909,203 4.1%

Ufone 3G 2,570,283 1,365,259 1,952,584 2,662,310 2,570,283 3,518,635 2.9%

Warid LTE - - - 66140 106,211 156,827 0.1%

13,392,466 3,692,742 7,680,521 12,071,553 13,498,677 18,040,854 14.9%

CMPak

Total

3G/4G Subscribers

Sep-15 Telenor Mobilink CMPak Ufone Warid

Shareof 3G subscribers in the cellular

operator's subscriber base 16.5% 14.0% 16.0% 18.8% N.A.

Shareof 4G subscribers in the cellular

operator's subscriber base N.A. N.A. 0.9% N.A. 1.5%

Share of 3G/4G subscribers as %age of

total 3G/4G subscribers 30.4% 27.2% 22.0% 19.5% 0.9%

Pakistan Cellular Industry

Industry – Structure Regional Comparison Snapshot

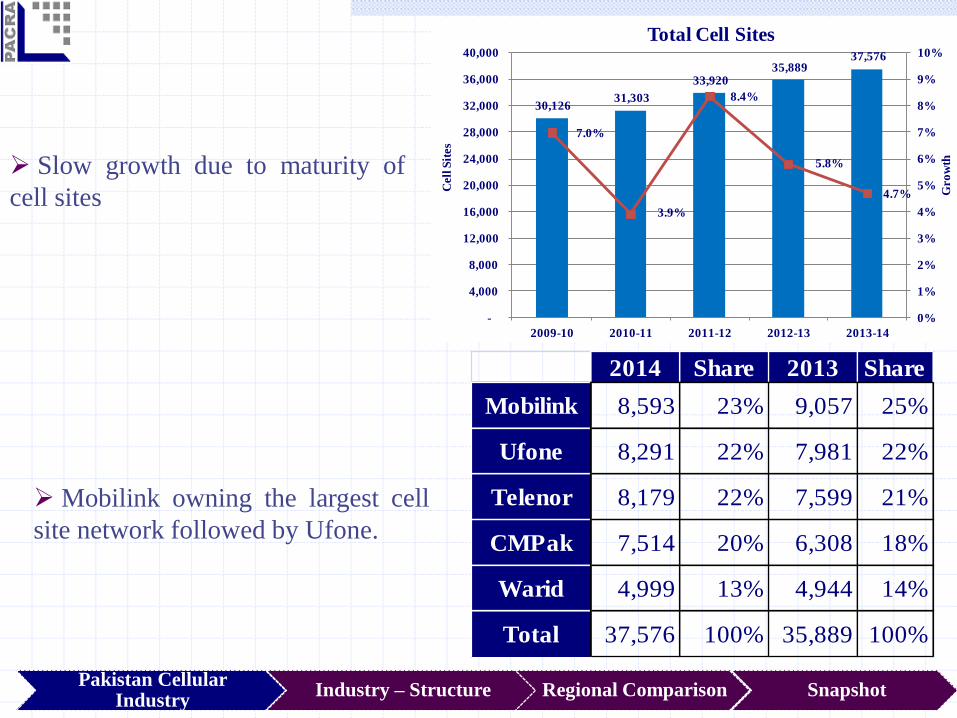

30,126 31,303

33,920 35,889

37,576

7.0%

3.9%

8.4%

5.8%

4.7%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

-

4,000

8,000

12,000

16,000

20,000

24,000

28,000

32,000

36,000

40,000

2009-10 2010-11 2011-12 2012-13 2013-14

Gro

wth

Cell

Sit

es

Total Cell Sites

Slow growth due to maturity of

cell sites

Mobilink owning the largest cell

site network followed by Ufone.

2014 Share 2013 Share

Mobilink 8,593 23% 9,057 25%

Ufone 8,291 22% 7,981 22%

Telenor 8,179 22% 7,599 21%

CMPak 7,514 20% 6,308 18%

Warid 4,999 13% 4,944 14%

Total 37,576 100% 35,889 100%

Pakistan Cellular Industry

Industry – Structure Regional Comparison Snapshot

Broadband Subscribers by Technology

Year DSL HFC WiMax FTTH EvDO Others Mobile BB Total

2009-10 476,722 49,110 257,616 5,002 111,194 1,004 0 900,648

2010-11 695,245 34,274 428,523 6,346 325,140 1,963 0 1,491,491

2011-12 880,071 35,520 589,887 8,444 584,459 2,934 0 2,101,315

2012-13 1,064,003 33,184 575,939 11,152 1,033,513 3,868 0 2,721,659

2013-14 1,346,817 37,011 530,889 14,848 1,861,118 5,240 0 3,795,923

2014-15 1,480,672 43,362 487,582 19,490 1,334,725 6,089 13,498,677 16,885,518

Sep-15* 1,563,321 43,929 245,284 20,549 1,273,184 6,160 18,040,854 21,193,281

*DSL, HFC, WiMax, FTTH, EvDo and others are As of August 15

After acquisition of 3G and 4G spectrum, wireless internet taken by the cellular

operators

Pakistan Cellular Industry

Industry – Structure Regional Comparison Snapshot

2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

Total FDI 3,720 2,199 1,574 821 1,576 2,641

Telecom FDI/(FD Outflow) 815 374 79 (361) (408) 903

Telecm FDI share in Total FDI 22% 17% 5% 0% 0% 34%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

(1,000)

(500)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

US

D in

mln

Foreign Direct Investment (FDI)

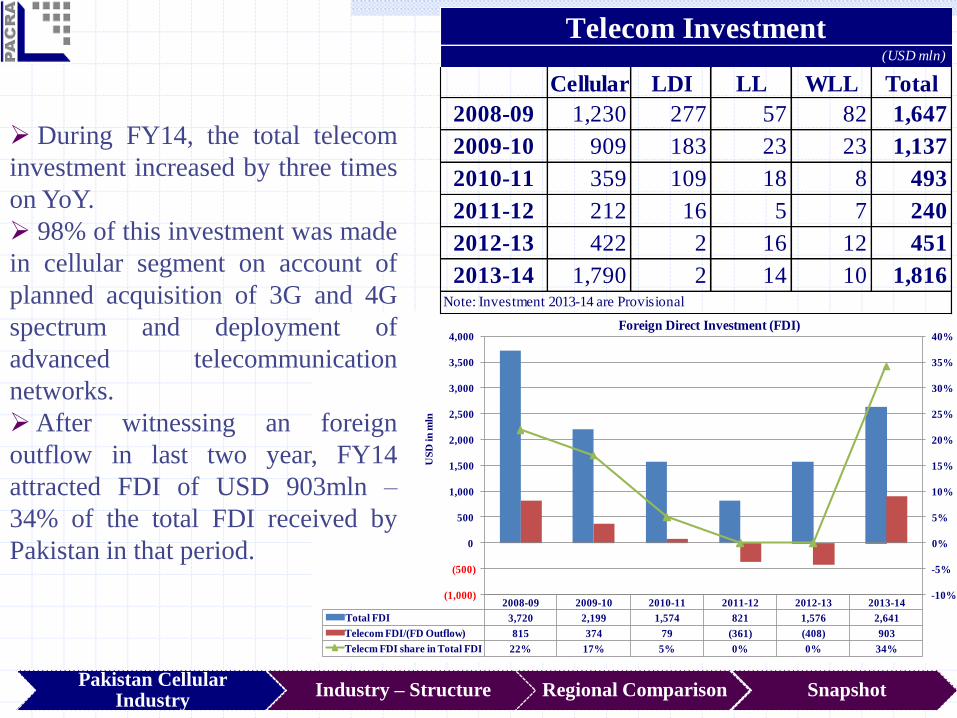

During FY14, the total telecom

investment increased by three times

on YoY.

98% of this investment was made

in cellular segment on account of

planned acquisition of 3G and 4G

spectrum and deployment of

advanced telecommunication

networks.

After witnessing an foreign

outflow in last two year, FY14

attracted FDI of USD 903mln –

34% of the total FDI received by

Pakistan in that period.

Cellular LDI LL WLL Total

2008-09 1,230 277 57 82 1,647

2009-10 909 183 23 23 1,137

2010-11 359 109 18 8 493

2011-12 212 16 5 7 240

2012-13 422 2 16 12 451

2013-14 1,790 2 14 10 1,816

Telecom Investment(USD mln)

Note: Investment 2013-14 are Provisional

Pakistan Cellular Industry

Industry – Structure Regional Comparison Snapshot

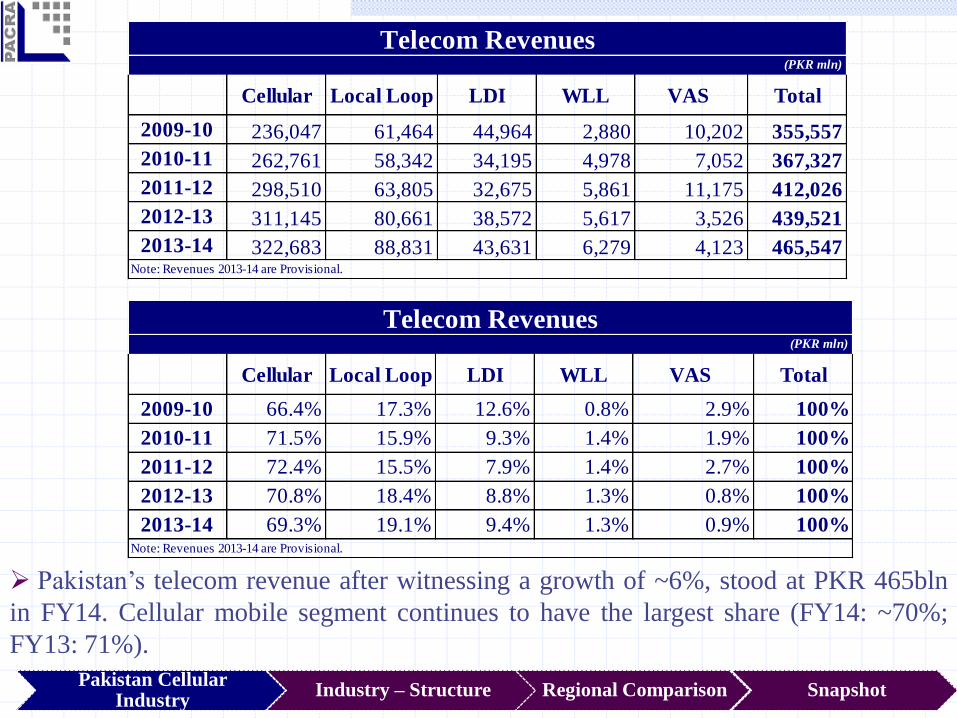

Pakistan’s telecom revenue after witnessing a growth of ~6%, stood at PKR 465bln

in FY14. Cellular mobile segment continues to have the largest share (FY14: ~70%;

FY13: 71%).

Cellular Local Loop LDI WLL VAS Total

2009-10 236,047 61,464 44,964 2,880 10,202 355,557

2010-11 262,761 58,342 34,195 4,978 7,052 367,327

2011-12 298,510 63,805 32,675 5,861 11,175 412,026

2012-13 311,145 80,661 38,572 5,617 3,526 439,521

2013-14 322,683 88,831 43,631 6,279 4,123 465,547Note: Revenues 2013-14 are Provisional.

Telecom Revenues(PKR mln)

Cellular Local Loop LDI WLL VAS Total

2009-10 66.4% 17.3% 12.6% 0.8% 2.9% 100%

2010-11 71.5% 15.9% 9.3% 1.4% 1.9% 100%

2011-12 72.4% 15.5% 7.9% 1.4% 2.7% 100%

2012-13 70.8% 18.4% 8.8% 1.3% 0.8% 100%

2013-14 69.3% 19.1% 9.4% 1.3% 0.9% 100%Note: Revenues 2013-14 are Provisional.

Telecom Revenues(PKR mln)

Pakistan Cellular Industry

Industry – Structure Regional Comparison Snapshot

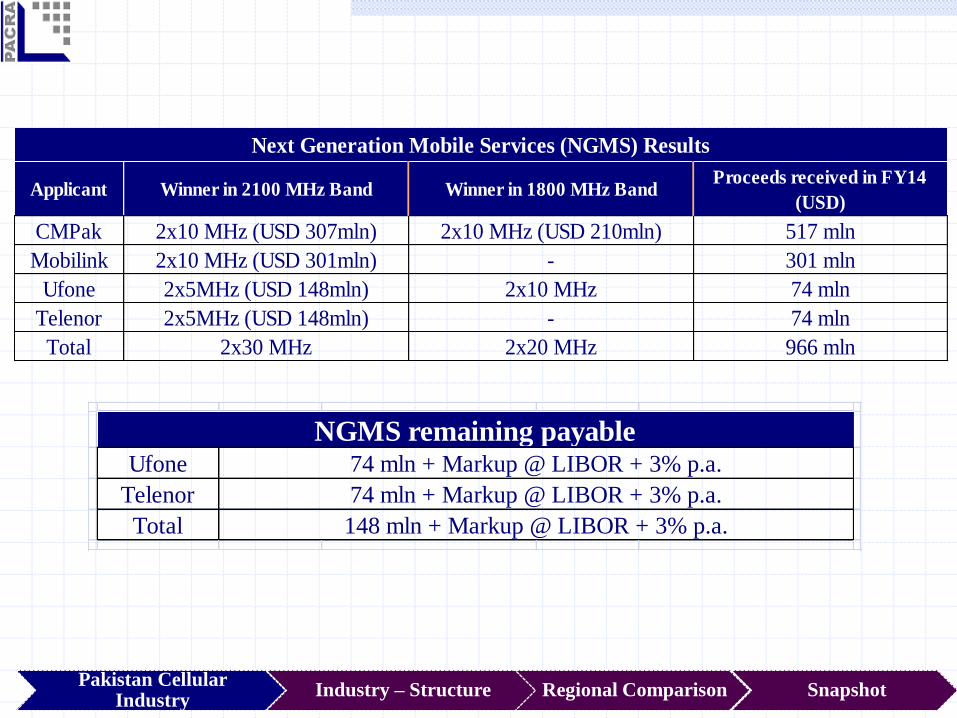

Ufone

Telenor

Total

74 mln + Markup @ LIBOR + 3% p.a.

74 mln + Markup @ LIBOR + 3% p.a.

148 mln + Markup @ LIBOR + 3% p.a.

NGMS remaining payable

ApplicantProceeds received in FY14

(USD)

CMPak 517 mln

Mobilink 301 mln

Ufone 74 mln

Telenor 74 mln

Total 966 mln

Next Generation Mobile Services (NGMS) Results

2x5MHz (USD 148mln) -

2x10 MHz (USD 301mln) -

2x30 MHz 2x20 MHz

2x10 MHz (USD 210mln)

2x5MHz (USD 148mln) 2x10 MHz

Winner in 2100 MHz Band Winner in 1800 MHz Band

2x10 MHz (USD 307mln)

Oligopoly

Few firms dominate the

industry

High barriers to entry

Price makers –Mutually

interdependent (react to rival’s

actions)

Industry Structure

Pakistan Cellular Industry

Industry – Structure Regional Comparison Snapshot

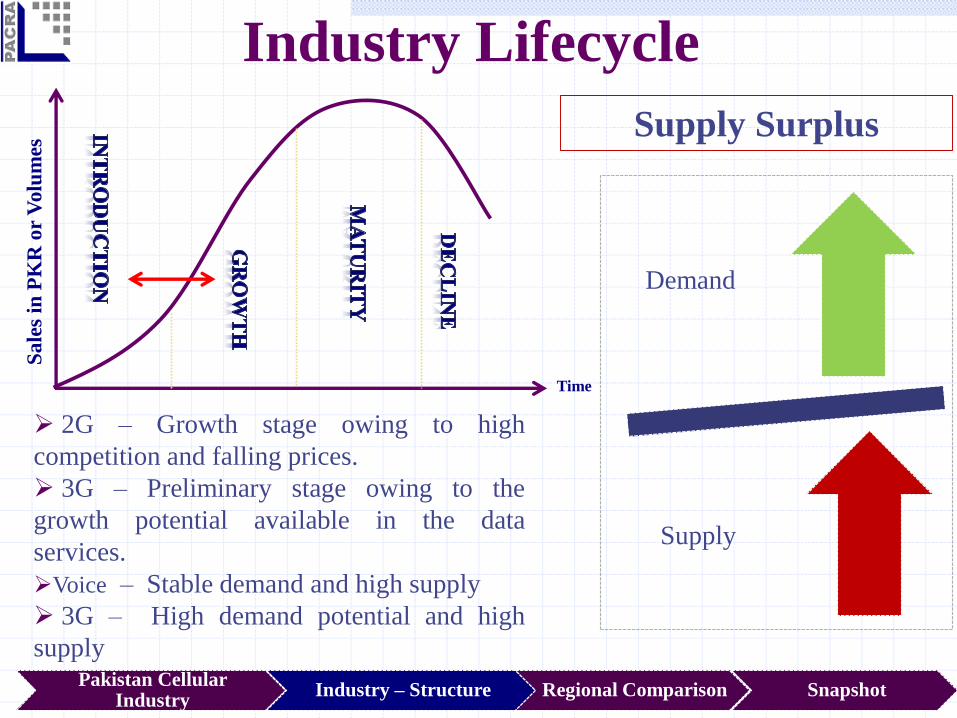

Industry Lifecycle

Time

Sa

les

in P

KR

or

Vo

lum

es

Pakistan Cellular Industry

Industry – Structure Regional Comparison Snapshot

2G – Growth stage owing to high

competition and falling prices.

3G – Preliminary stage owing to the

growth potential available in the data

services.

Voice – Stable demand and high supply

3G – High demand potential and high

supply

Supply Surplus

Demand

Supply

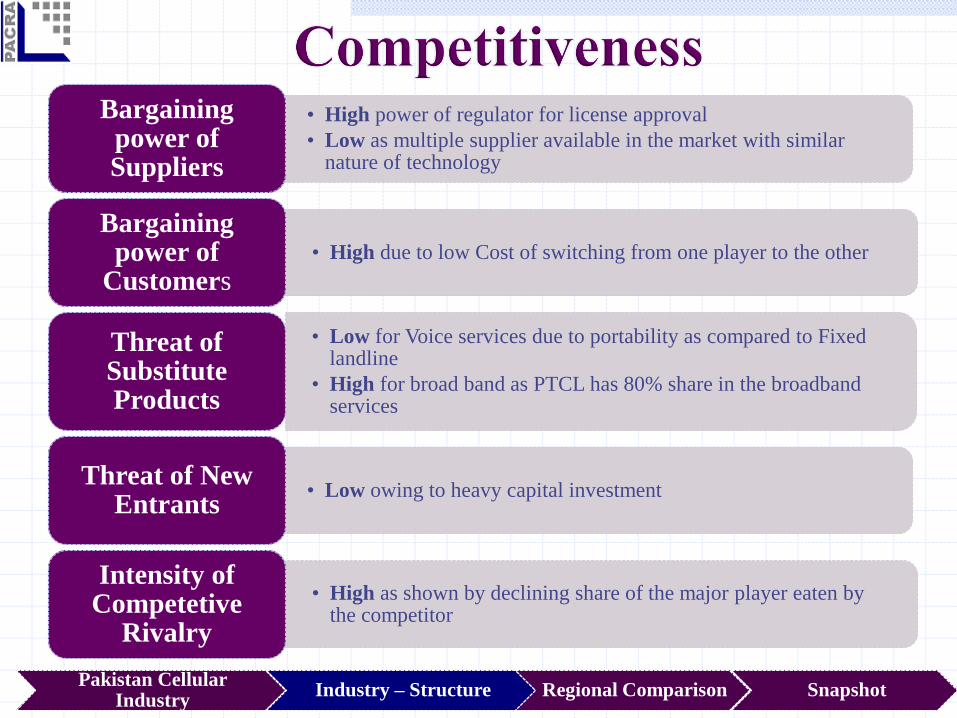

• High power of regulator for license approval

• Low as multiple supplier available in the market with similar nature of technology

Bargaining power of Suppliers

• High due to low Cost of switching from one player to the other

Bargaining power of

Customers

• Low for Voice services due to portability as compared to Fixed landline

• High for broad band as PTCL has 80% share in the broadband services

Threat of Substitute Products

• Low owing to heavy capital investmentThreat of New

Entrants

• High as shown by declining share of the major player eaten by the competitor

Intensity ofCompetetive

Rivalry

Pakistan Cellular Industry

Industry – Structure Regional Comparison Snapshot

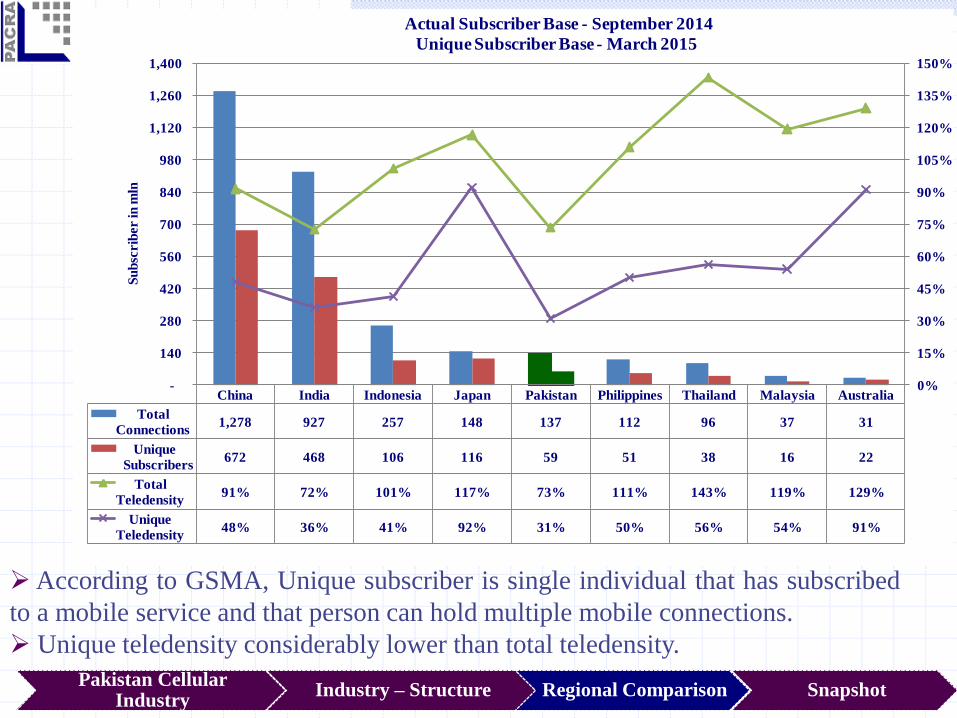

According to GSMA, Unique subscriber is single individual that has subscribed

to a mobile service and that person can hold multiple mobile connections.

Unique teledensity considerably lower than total teledensity.

Pakistan Cellular Industry

Industry – Structure Regional Comparison Snapshot

China India Indonesia Japan Pakistan Philippines Thailand Malaysia Australia

Total

Connections1,278 927 257 148 137 112 96 37 31

Unique

Subscribers672 468 106 116 59 51 38 16 22

Total

Teledensity91% 72% 101% 117% 73% 111% 143% 119% 129%

Unique

Teledensity48% 36% 41% 92% 31% 50% 56% 54% 91%

0%

15%

30%

45%

60%

75%

90%

105%

120%

135%

150%

-

140

280

420

560

700

840

980

1,120

1,260

1,400

Su

bsc

rib

er in

mln

Actual Subscriber Base - September 2014

Unique Subscriber Base - March 2015

392 365

287 270

217 215

136

62

-

50

100

150

200

250

300

350

400

450

Min

utes

Average Minutes of Usage per Subscriber per

Month

Pakistan Cellular Industry

Industry – Structure Regional Comparison Snapshot

0.07

0.06

0.02 0.02 0.02

0.01 0.01 0.01

-

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

USD

Call Charges per Minute

Pakistan Cellular Industry

Industry – Structure Regional Comparison Snapshot

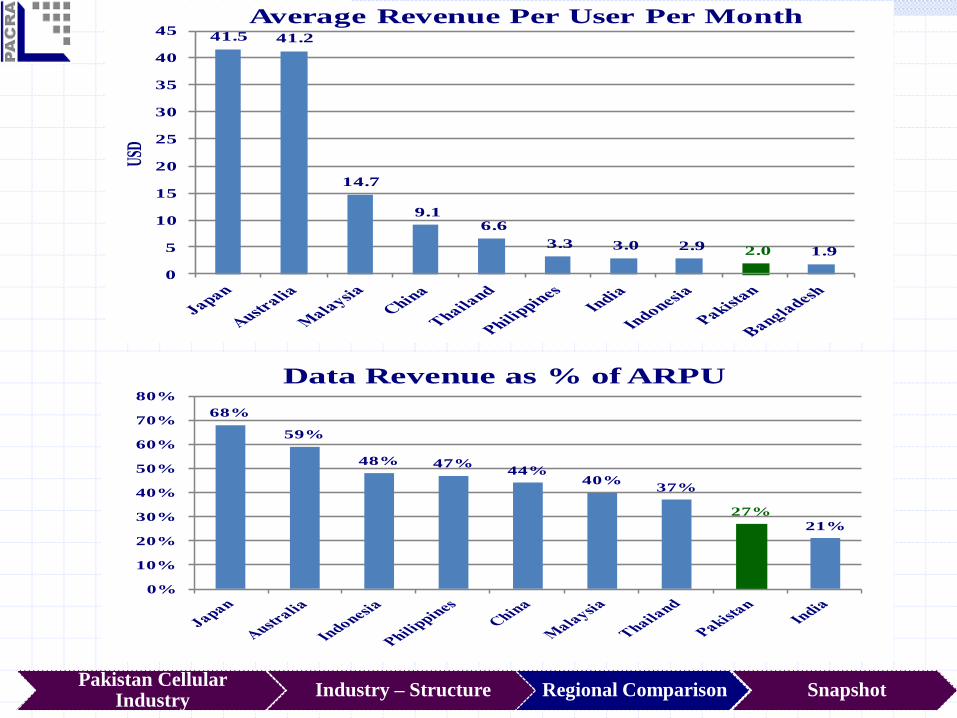

41.5 41.2

14.7

9.1 6.6

3.3 3.0 2.9 2.0 1.9

0

5

10

15

20

25

30

35

40

45

USD

Average Revenue Per User Per Month

68%

59%

48% 47%44%

40%37%

27%

21%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Data Revenue as % of ARPU

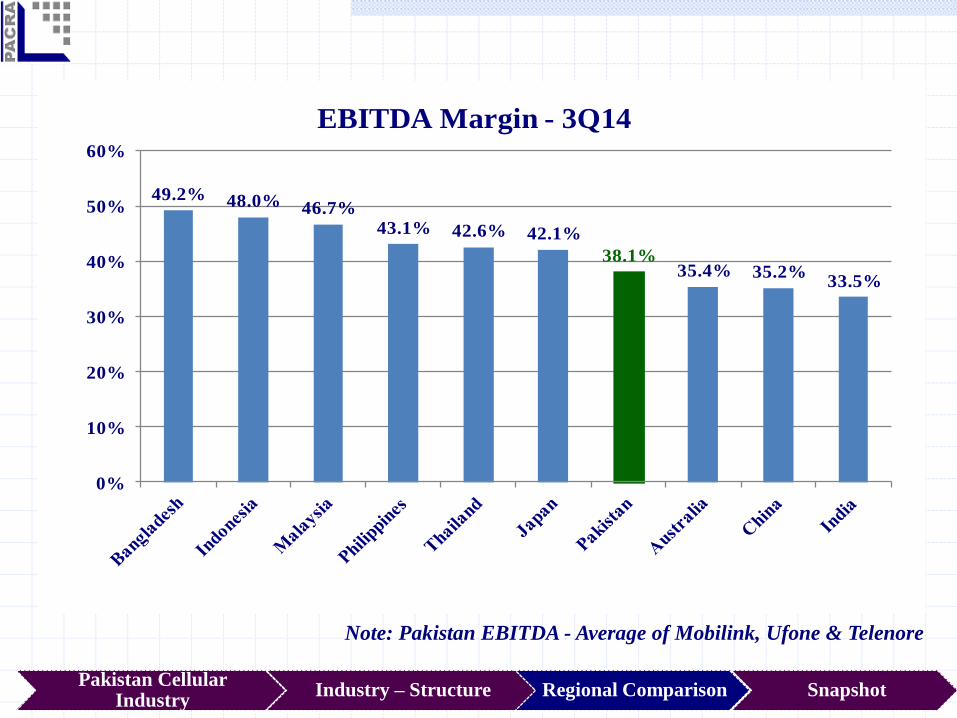

49.2% 48.0% 46.7%43.1% 42.6% 42.1%

38.1%35.4% 35.2%

33.5%

0%

10%

20%

30%

40%

50%

60%

EBITDA Margin - 3Q14

Note: Pakistan EBITDA - Average of Mobilink, Ufone & Telenore

Pakistan Cellular Industry

Industry – Structure Regional Comparison Snapshot

Snapshot

Pakistan Cellular Industry

Industry – Structure Regional Comparison Snapshot

As competitive landscape exists, average revenues per user

(ARPUs) have yet to stabilize.

Business potential in value added services is expected to

provide impetus to revenue growth to the market players,

though time-line is uncertain.

Intense competition among players is expected to keep

EBITDA margin under pressure.

After acquisition of 3G and 4G spectrum, wireless internet

taken by the cellular operators

Bibliography

1. Pakistan Telecommunication Authority (PTA) : http://www.pta.gov.pk/index.php?Itemid=1

2. PTA Annual Reports :

http://www.pta.gov.pk/index.php?option=com_content&view=article&id=361&Itemid=590

3. Cellular Operators Association of India: http://www.coai.com/reports-and-papers/coai-annual-

report

Analysts

Rana Nadeem

Unit Head Ratings

Aisha Khalid

Manager Ratings

Abdul Sami

Senior Financial Analyst

Contact Number: +92 42 3586 9504

DISCLAIMER

PACRA has used due care in preparation of this document. Our information

has been obtained from sources we consider to be reliable but its accuracy

or completeness is not guaranteed. The information in this document may

be copied or otherwise reproduced, in whole or in part, provided the source

is duly acknowledged. The presentation should not be relied upon as

professional advice.