MLC 个人总结

31

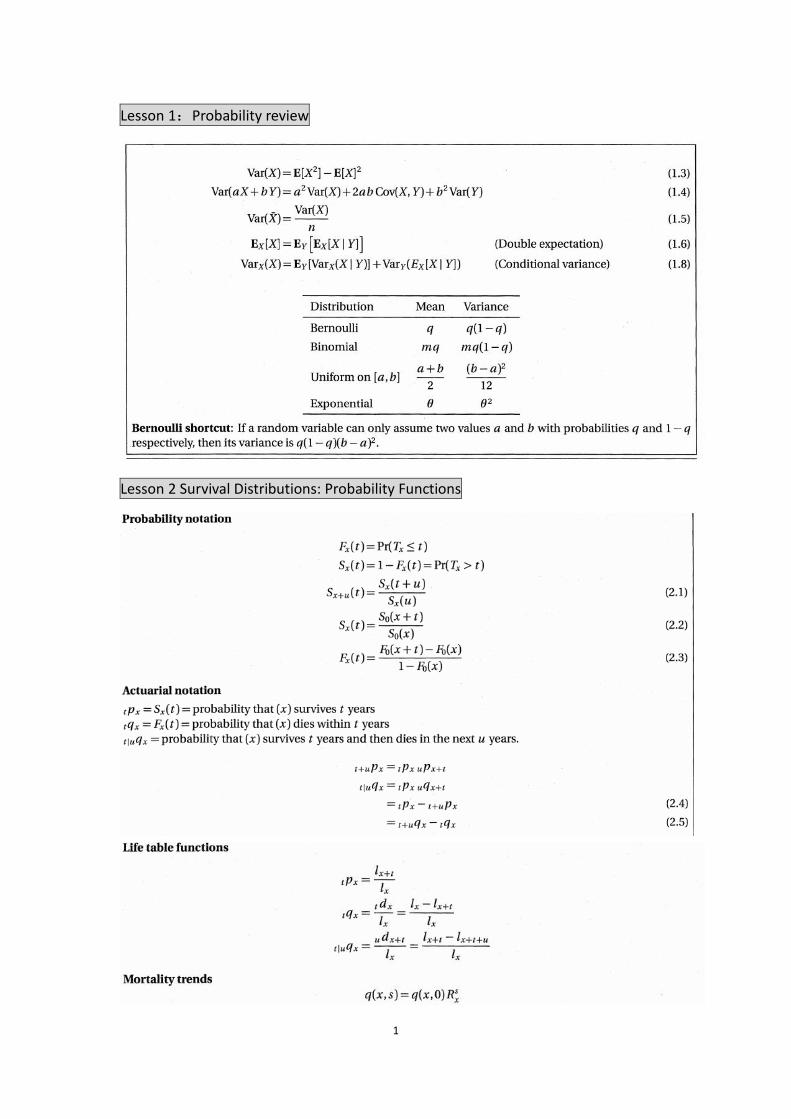

1 Lesson 1:Probability review Lesson 2 Survival Distributions: Probability Functions

-

Upload

danielchen -

Category

Documents

-

view

44 -

download

6

Transcript of MLC 个人总结

1

Lesson 1:Probability review

Lesson 2 Survival Distributions: Probability Functions

2

Lesson3 Surrvival Distributions: Force of Mortality

Lesson 4: Survival Distributions: Mortality Laws

3

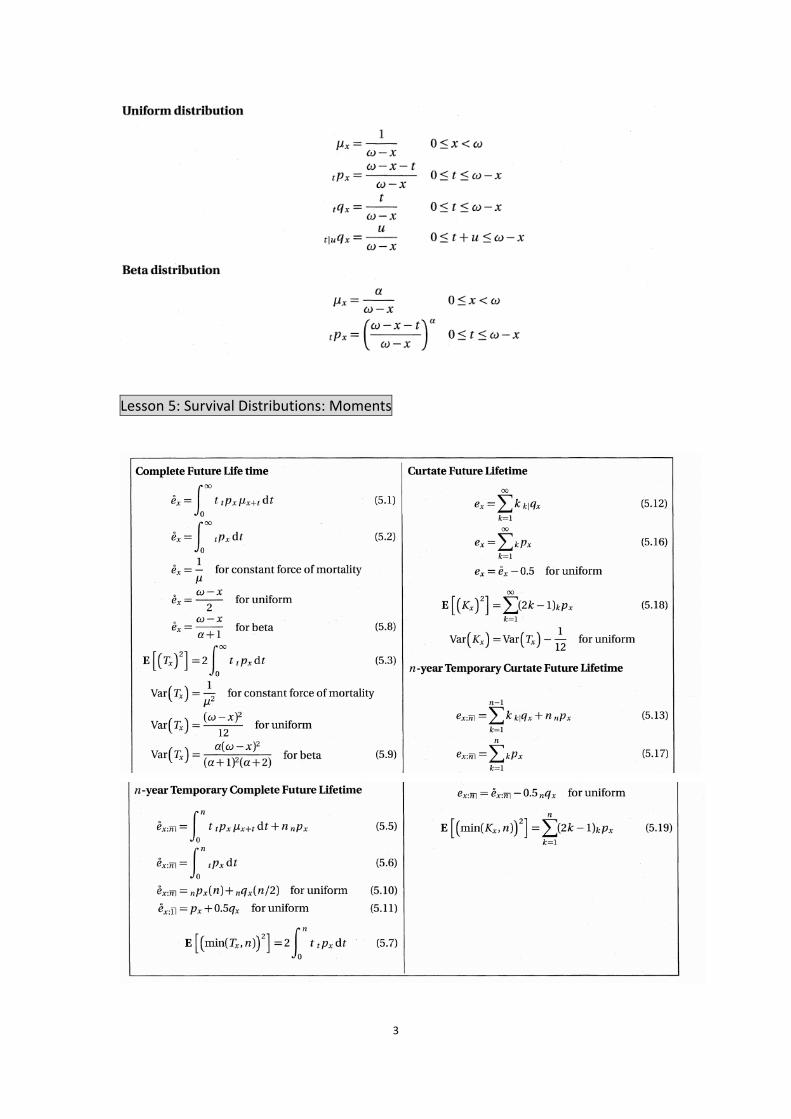

Lesson 5: Survival Distributions: Moments

4

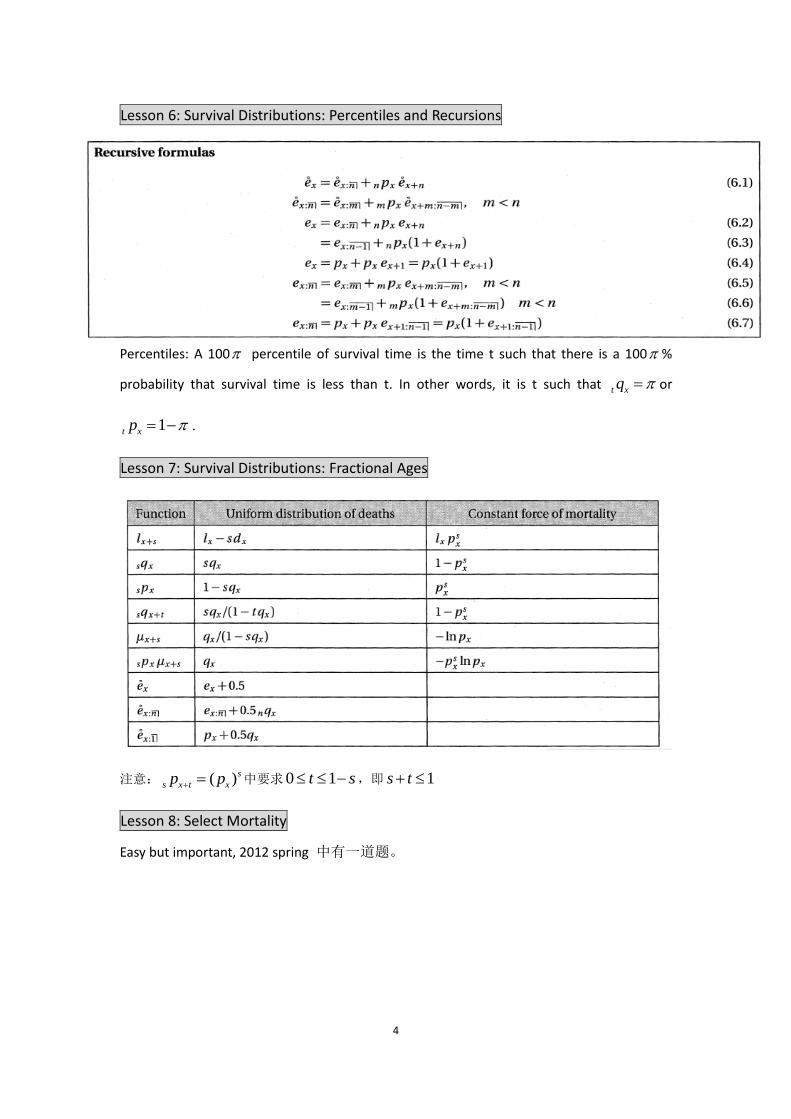

Lesson 6: Survival Distributions: Percentiles and Recursions

Percentiles: A 100 percentile of survival time is the time t such that there is a 100 %

probability that survival time is less than t. In other words, it is t such that t xq or

1t xp .

Lesson 7: Survival Distributions: Fractional Ages

注意: ( )s

s x t xp p 中要求0 1t s ,即 1s t

Lesson 8: Select Mortality

Easy but important, 2012 spring 中有一道题。

5

Lesson 9: Insurance: Continuous-Moments-Part 1

Shortcuts---Constant force of mortality:

/ ( )xA ( )

|

n

n x n x x nA E A e

Lesson 10: Insurance: Continuous-Moments-Part 2

The integral represents the present value of a continuously increasing

annuity-certain for u years at force of interest .

6

10.3 Variance of endowment insurance

For n-pure endowment 2

2 2

0 ( ) Var( )= ( )

( )

n x n

n x n xn

n x

qZ Z p q v

v p

Lesson 11: Insurance: Annual and mthly Moments

7

注意: ,(2 5

5 45 5 45E v E )

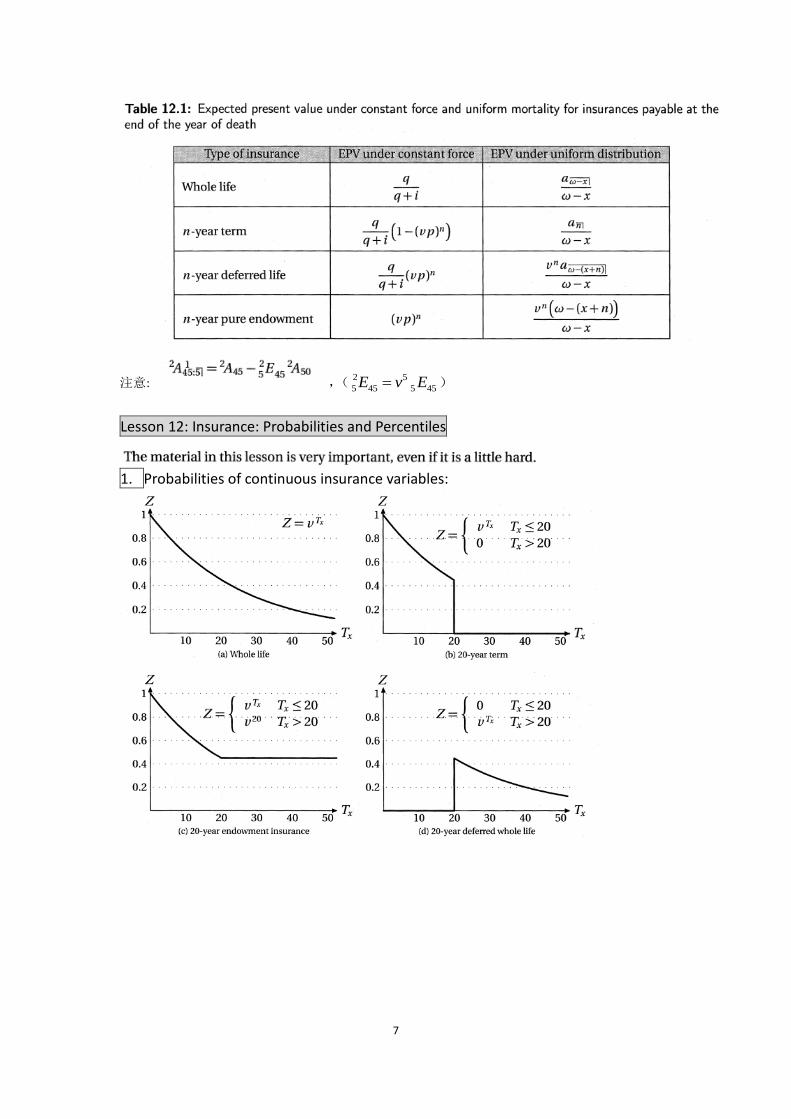

Lesson 12: Insurance: Probabilities and Percentiles

1. Probabilities of continuous insurance variables:

8

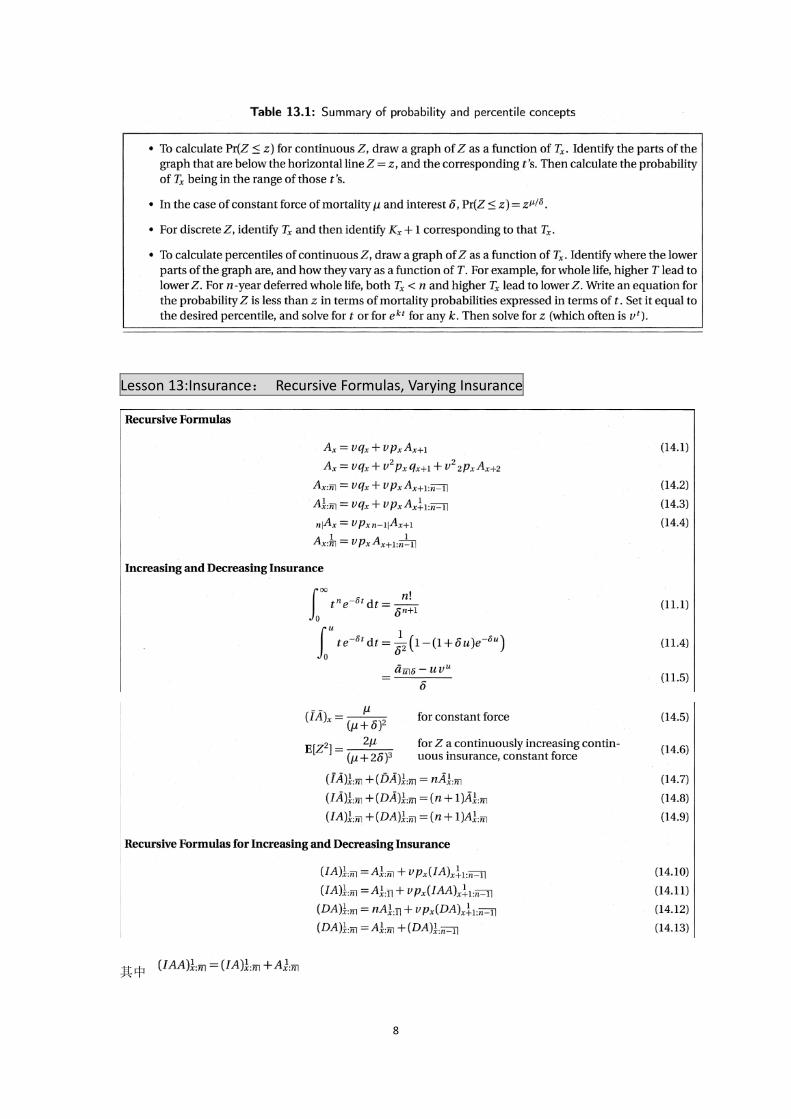

Lesson 13:Insurance: Recursive Formulas, Varying Insurance

其中

9

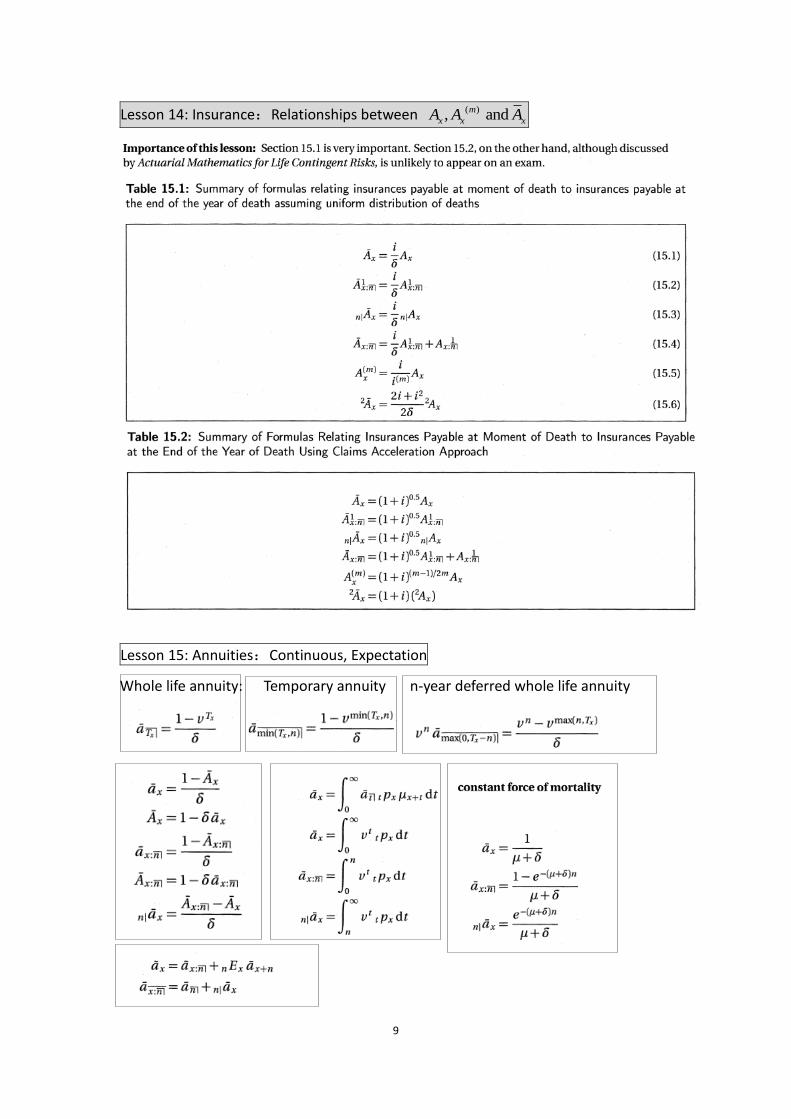

Lesson 14: Insurance:Relationships between ( ), and m

x x xA A A

Lesson 15: Annuities:Continuous, Expectation

Whole life annuity: Temporary annuity n-year deferred whole life annuity

10

t0

= dt E(Y),t

x xa v p

注意: 只能用于求 不能用于求高阶期望。

Lesson 15: Annuities:Annual and mthly, Expectation

Very important since discrete annuities are emphasized in the new syllabus.

1.定义:whole life annuity-due n-year temporary life annuity-due

n year deferred whole life n year certain and life

2. Relationships between annuity-due

and annuity-immediate:

3、Relationships between annuities and

insurances:

4、Relationships between annuities:

5、Other annuity equations:

6、Actuarial accumulated value

7、mthly annuities:

11

Lesson 17: Annuities: Variance

2、Combinations of annuities and insurances with no variance

Y—annuity;Z—insurance

Continuous:

Discrete(due):

Discrete(immediate):

Lesson 18: Annuities: Probabilities and Percentiles (very important)

12

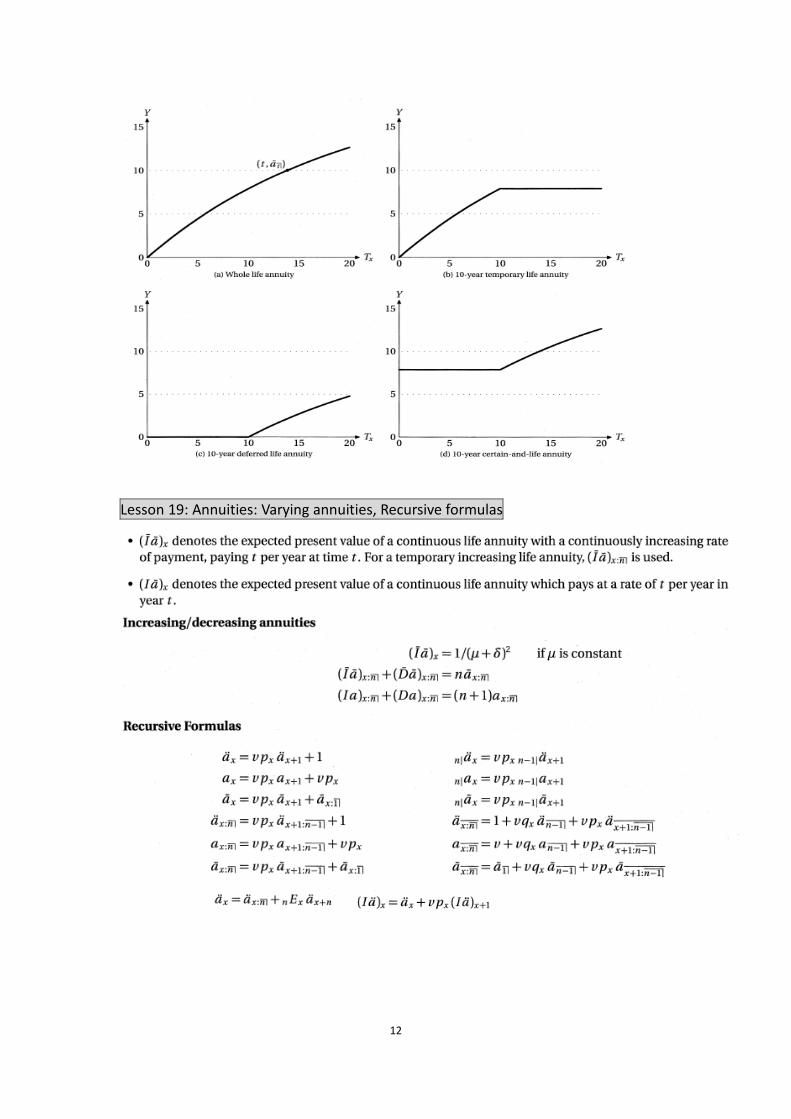

Lesson 19: Annuities: Varying annuities, Recursive formulas

13

Lesson 20: Annuities: m-thly payments

Lesson 21: Premiums: Net Premiums for fully Continuous Insurances

14

Lesson 22: Premiums: Net Premiums for Discrete Insurances calculated from life tables.

Lesson 23: Premiums: Net Premiums for Discrete Insurances calculated from Forlulas

Lesson 24: Premiums: Net Premiums paid on an mthly Basis

15

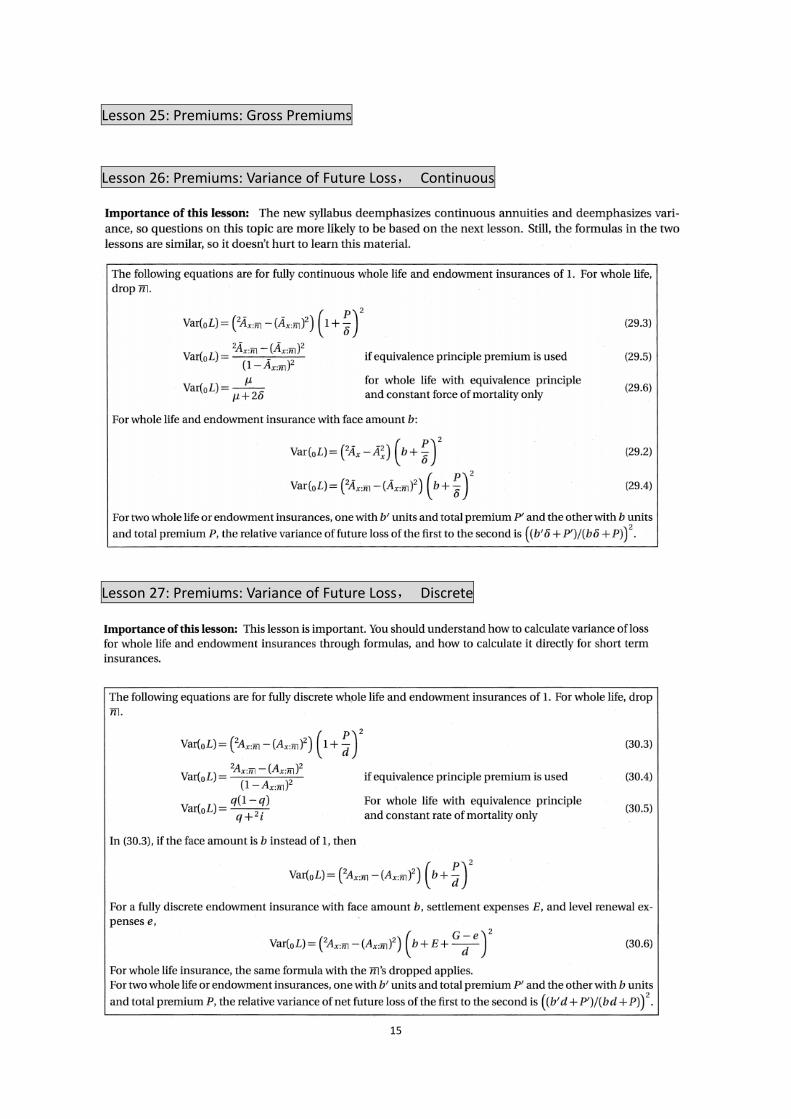

Lesson 25: Premiums: Gross Premiums

Lesson 26: Premiums: Variance of Future Loss, Continuous

Lesson 27: Premiums: Variance of Future Loss, Discrete

16

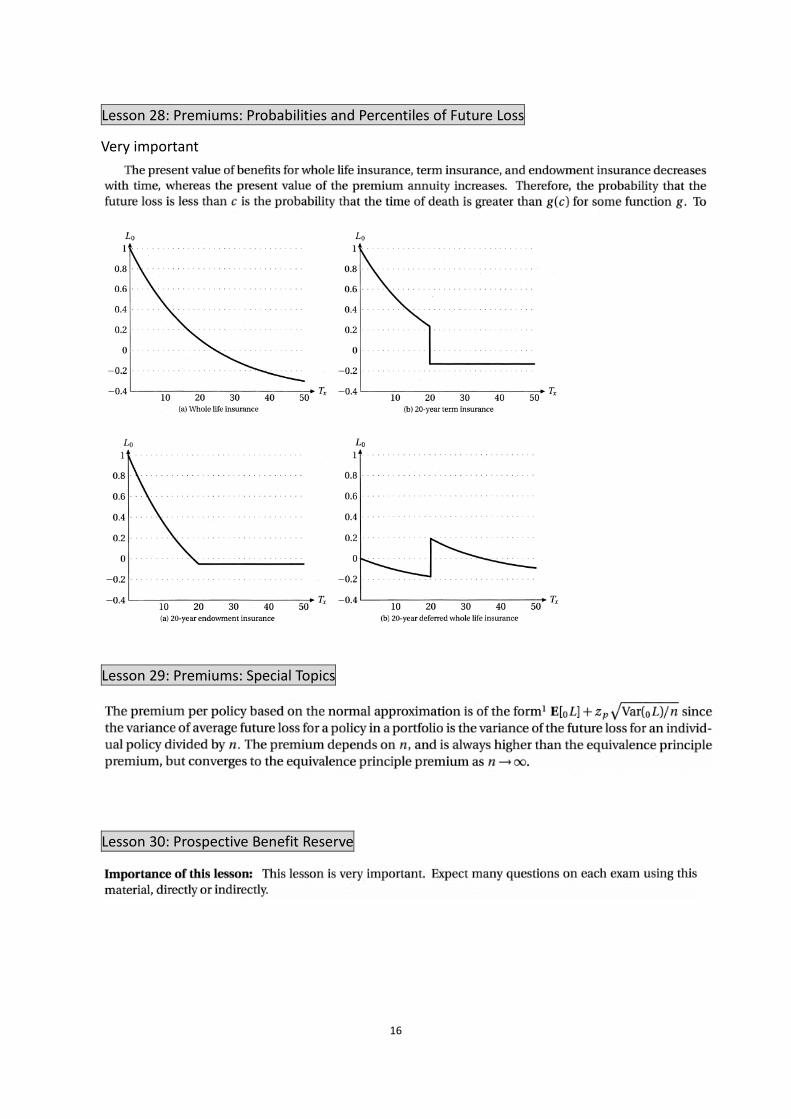

Lesson 28: Premiums: Probabilities and Percentiles of Future Loss

Very important

Lesson 29: Premiums: Special Topics

Lesson 30: Prospective Benefit Reserve

17

Lesson 31: Reserves: Gross Premium and Expense Reserve

Expense reserve:

When the gross premium is calculated using the equivalence principle and the premium

basis is the same as the reserve basis, the g

0V 0

(Gross premium) (benefit premium) (expense premium)g n eP P P

The expense reserve is usually negative because expenses are front-loaded.

Lesson 32: Retrospective Formula

Relationships between premiums:

图形 32.8 和 32.9.

Lesson 33: Reserves: Special Formulas for Whole Life and Endowment Insurance

注意是:fully discrete and fully continuous

18

Lesson 34: Reserves: Variance of Loss

Lesson 35: Reserves: Recursive Formulas

35.1 Benefit reserves:

35.2 Insurances or annuities with refund of reserve

Net amount at risk: j jb V

19

Deferred annuities and insurances:

Constant mortality:

35.3 Gross premium reserve:

Lesson 36: Reserves: Other Topics

1、 Reserves on semi-continuous topics(Premiums are payable annually and benefit

is payable at the moment of death)

(1)semi-whole life (2) semi-endowment

2、 Gain by source

Total profit:

20

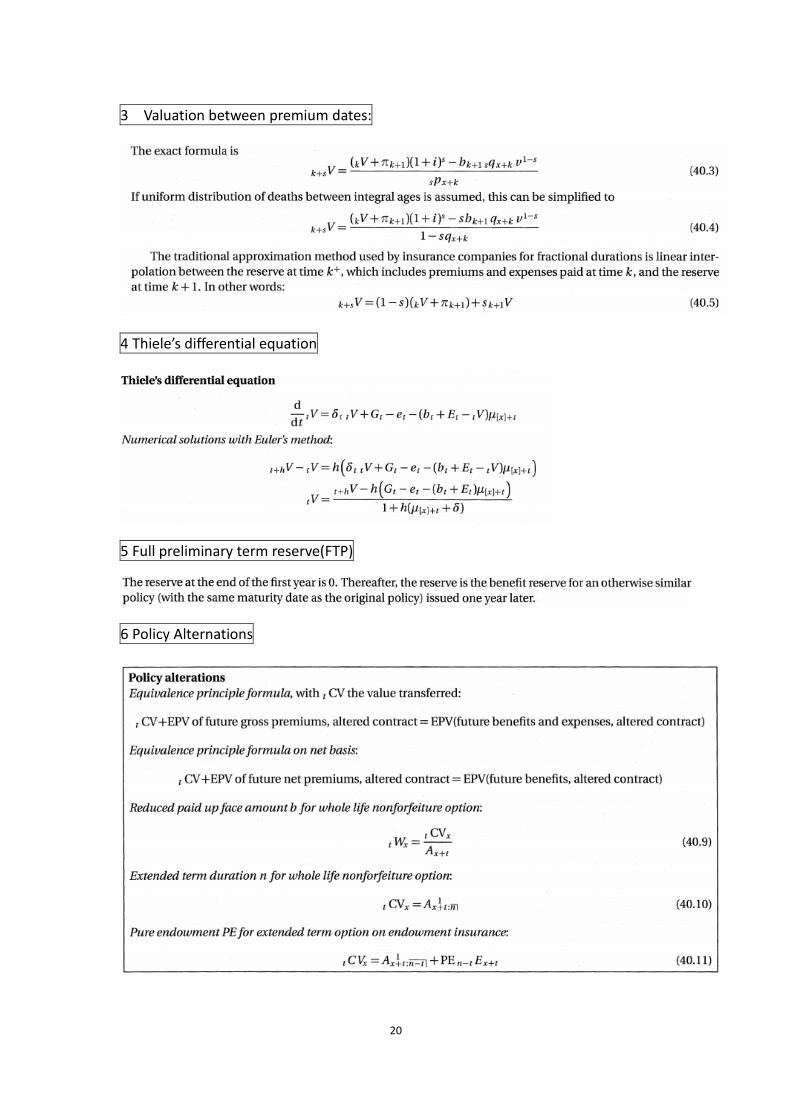

3 Valuation between premium dates:

4 Thiele’s differential equation

5 Full preliminary term reserve(FTP)

6 Policy Alternations

21

Lesson 37: Markov Chains: Discrete—Probabilities

Lesson 38: Markov Chains: Continuous—Probabilities

22

Lesson 39: Markov Chains: Premiums and Reserves

An insurance pays a benefit upon transition to a different state.

An annuity pays a benefit as long as one is in a state.

Lesson 40: Multiple Decrement Models: Probabilities

23

Lesson 41: Multiple Decrement Models: Forces of Decrement

24

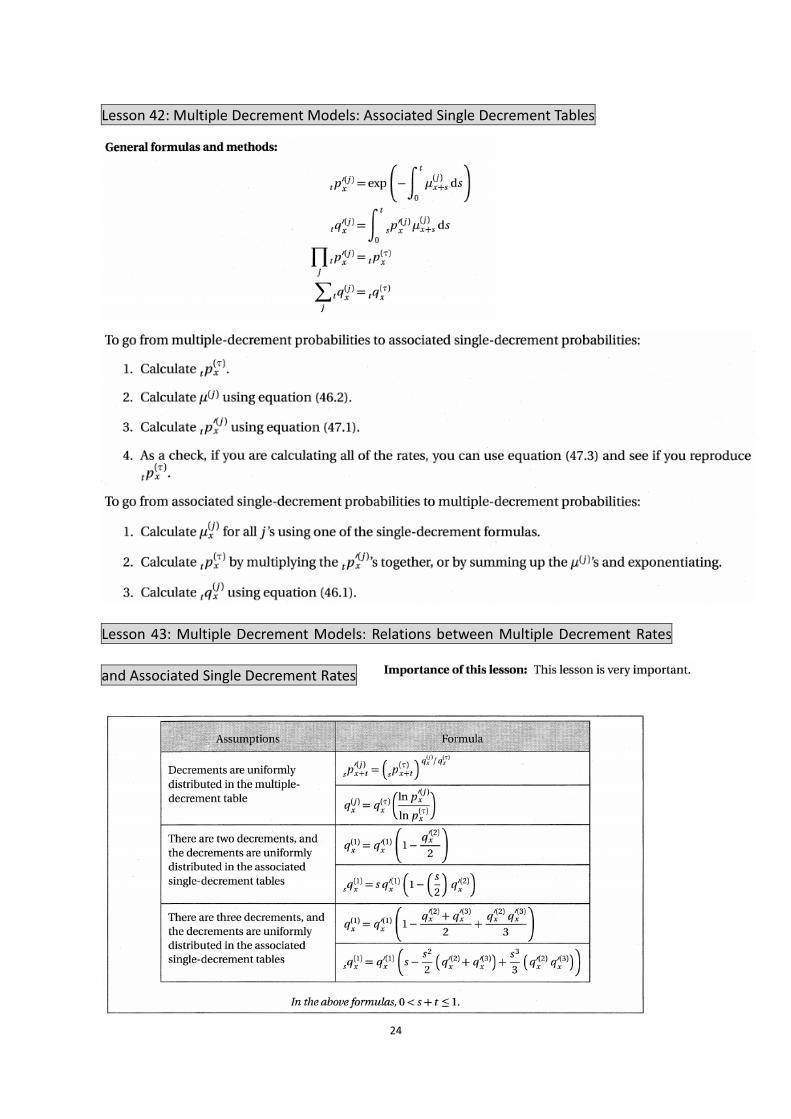

Lesson 42: Multiple Decrement Models: Associated Single Decrement Tables

Lesson 43: Multiple Decrement Models: Relations between Multiple Decrement Rates

and Associated Single Decrement Rates

25

Lesson 44: Multiple Decrement: Discrete Decrements

看例题和部分习题

Lesson 45: Multiple Decrement Models: Continuous Insurance

Lesson 46: Asset Shares

26

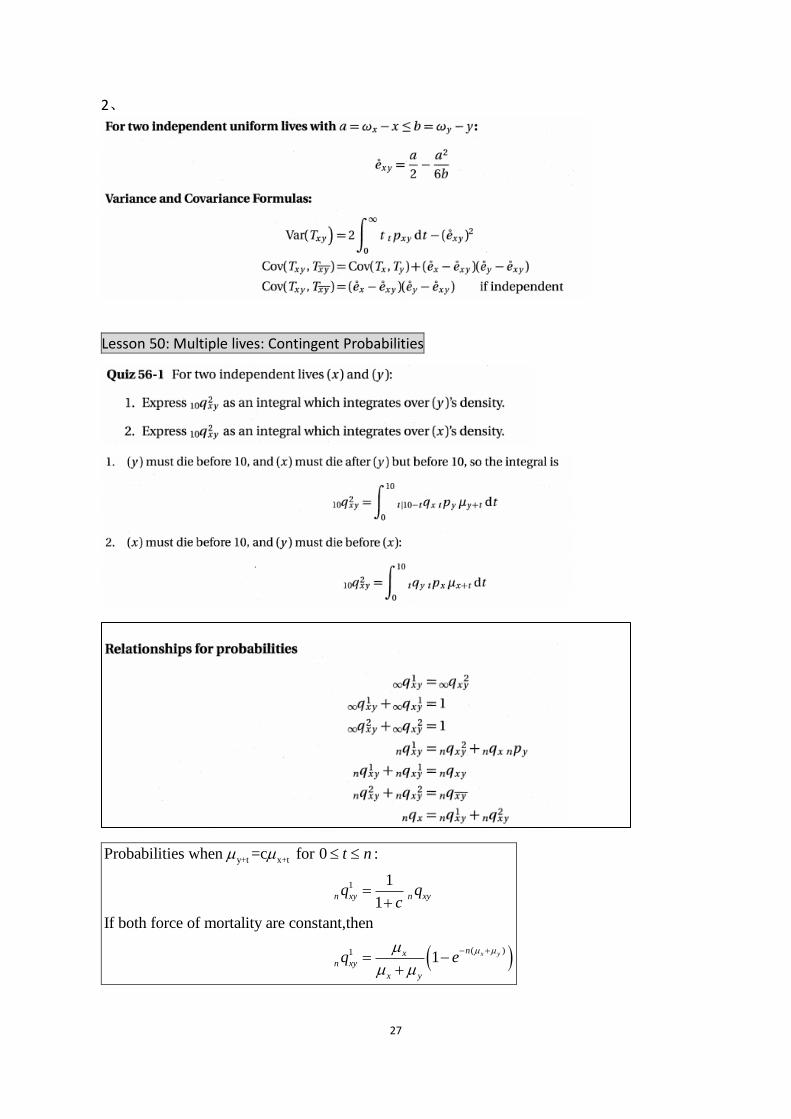

Lesson 47: Joint Life Probabilities

Lesson 48: Multiple Lives: Last Survivor Probabilities

Last survivor status: a status that fails only when every member of the status fails.

1t txy xyp q

:t u t uxy xy x t y tp p p

( ) is the force of mortality of the last survivor.xy

u t

Lesson 49: Multiple Lives: Moments

1、Expected value formulas:

27

2、

Lesson 50: Multiple lives: Contingent Probabilities

y+t x+t

1

Probabilities when =c for 0 :

1

1

If both force of mortality are constant,then

n xy n xy

t n

q qc

( )1 1 x ynxn xy

x y

q e

28

Lesson 51: Multiple lives: Common Shock

Lesson 52: Multiple lives: Insurance

Importance: 52.1 and 52.2 is important, and 52.3 is unlikely to be tested on.

1 1

2 2

2 2

2 2

(All the A's in either equality may be barred, and the equalities works

for term insurance as well.)

For term insurance as an example:

(discrete/

xy xy xy

xy xy xy

n xy n xy n xy

xy xy x

A A A

A A A

A A A

A A A

1 2

continuous/ whole or term)

(discrete/ continuous/ whole life only)xy xy x xy yxyA A A A A A

注意:

29

Lesson 53: Multiple lives: Annuities

Lesson 54: Pension Mathematics

Lesson 55: Interest Rate Risk: Replicating Cash Flows

30

Lesson 56: Interest Rate Risk: Diversifiable and Non-Diversifiable Risk

Lesson 57: Profit Measures—Traditional Products

57.2 Profit measures

—the expected value of future profit, better known as the net present value(NPV)

The profit margin is the ratio of the NPV to the expected present value of future gross

premiums.

31

Lesson 58: Profit Measures—Universal Life