MINUTES Meeting of the Investment Committee State … · 2019-10-22 · MINUTES . Meeting of the...

235

MINUTES Meeting of the Investment Committee of the Board of Trustees of the State Universities Retirement System September 12-13, 2019, 12:30 p.m. State Universities Retirement System Main Conference Room 1901 Fox Dr., Champaign, Illinois 61820 The following trustees were present: Mr. Aaron Ammons, Mr. John Atkinson, Mr. Richard Figueroa, Ms. Jamie-Clare Flaherty, Dr. Fred Giertz, Mr. John Lyons, Dr. Steven Rock, Mr. Collin Van Meter, Mr. Antonio Vasquez and Mr. Mitch Vogel. Others present: Mr. Martin Noven, Executive Director; Mr. Doug Wesley, Chief Investment Officer (CIO); Ms. Ellen Hung, Deputy CIO; Ms. Kimberly Pollitt, Mr. Joe Duncan and Mr. Shane Willoughby, Senior Investment Officers; Mr. Alex Ramos and Mr. Brian DeLoriea, Investment Officers; Ms. Kelly Valle and Mr. Akshay Patel, Investment Analysts; Ms. Bianca Green, General Counsel; Ms. Kristen Houch, Head of Legislative Affairs; Ms. Kelly Carson and Ms. Annette Ackerman, Executive Assistants; Mr. Neil Rue, Mr. Colin Bebee and Mr. Brandon Ross of Meketa; Mr. Anton Briton of Northern Trust; and Ms. Anna Willis and Ms. Courteney Keatinge of Glass Lewis. Investment Committee roll call attendance was taken. Trustee Vasquez, Chair, present; Trustee Ammons, present; Trustee Figueroa, present; Trustee Giertz, present; Trustee Rock, absent and Trustee Van Meter, present. Trustee Rock physically joined the meeting at 12:36 p.m. APPROVAL OF MINUTES Trustee Vasquez presented the minutes from the Investment Committee meeting of June 6, 2019. Trustee Ammons made the following motion: • That the minutes from the June 6, 2019 Investment Committee meeting be approved as presented. Trustee Van Meter seconded and the motion carried with all trustees present voting in favor. Trustee Giertz made the following motion: • That the closed session minutes from the June 6, 2019 Investment Committee meeting be approved as presented and remain closed. Trustee Rock seconded and the motion carried with all trustees present voting in favor.

Transcript of MINUTES Meeting of the Investment Committee State … · 2019-10-22 · MINUTES . Meeting of the...

MINUTES

Meeting of the Investment Committee of the Board of Trustees of the

State Universities Retirement System September 12-13, 2019, 12:30 p.m.

State Universities Retirement System Main Conference Room

1901 Fox Dr., Champaign, Illinois 61820 The following trustees were present: Mr. Aaron Ammons, Mr. John Atkinson, Mr. Richard Figueroa, Ms. Jamie-Clare Flaherty, Dr. Fred Giertz, Mr. John Lyons, Dr. Steven Rock, Mr. Collin Van Meter, Mr. Antonio Vasquez and Mr. Mitch Vogel. Others present: Mr. Martin Noven, Executive Director; Mr. Doug Wesley, Chief Investment Officer (CIO); Ms. Ellen Hung, Deputy CIO; Ms. Kimberly Pollitt, Mr. Joe Duncan and Mr. Shane Willoughby, Senior Investment Officers; Mr. Alex Ramos and Mr. Brian DeLoriea, Investment Officers; Ms. Kelly Valle and Mr. Akshay Patel, Investment Analysts; Ms. Bianca Green, General Counsel; Ms. Kristen Houch, Head of Legislative Affairs; Ms. Kelly Carson and Ms. Annette Ackerman, Executive Assistants; Mr. Neil Rue, Mr. Colin Bebee and Mr. Brandon Ross of Meketa; Mr. Anton Briton of Northern Trust; and Ms. Anna Willis and Ms. Courteney Keatinge of Glass Lewis. Investment Committee roll call attendance was taken. Trustee Vasquez, Chair, present; Trustee Ammons, present; Trustee Figueroa, present; Trustee Giertz, present; Trustee Rock, absent and Trustee Van Meter, present. Trustee Rock physically joined the meeting at 12:36 p.m.

APPROVAL OF MINUTES

Trustee Vasquez presented the minutes from the Investment Committee meeting of June 6, 2019. Trustee Ammons made the following motion:

• That the minutes from the June 6, 2019 Investment Committee meeting be approved as presented.

Trustee Van Meter seconded and the motion carried with all trustees present voting in favor. Trustee Giertz made the following motion:

• That the closed session minutes from the June 6, 2019 Investment Committee meeting be approved as presented and remain closed.

Trustee Rock seconded and the motion carried with all trustees present voting in favor.

Copies of staff’s memorandums titled “Investment Contracts Approved” and “Report from the June 2019 Investment Committee Meeting” are incorporated as part of these minutes as Exhibit 1 and Exhibit 2.

CHAIRPERSON’S REPORT Trustee Vasquez stated that he will attend the CII event in Minneapolis and an ESG event in Chicago the week of September 15, 2019. He also reminded trustees of a few upcoming investment events, if interested.

CHIEF INVESTMENT OFFICER REPORT Mr. Wesley provided an update on the fixed income restructuring that was approved during the June 2019 board meeting. Staff and the consultant completed the majority of contract negotiations. Staff retained a transition manager to coordinate the restructuring that was completed in early September. Mr. Wesley provided an update on the transition management contract with Loop Capital Markets (Loop). SURS’ external counsel provided a formal legal opinion that Loop cannot serve as a transition manager for SURS because they are not registered under the Federal Investment Advisers Act of 1940. Staff will discuss this opinion with Loop and terminate the contract. Finally, Mr. Wesley commented on the SURS inaugural Diverse Manager Week. SURS investment staff conducted one-hour meetings with 29 firms across different asset classes during the week of August 5, 2019. Representatives from Meketa, Callan, Progress and TorreyCove also attended relative to their specific asset classes.

CORPORATE GOVERNANCE OVERVIEW

Ms. Valle presented a historical review of Corporate Governance initiatives and discussed SURS’ current proxy voting standards and guidelines. Ms. Valle then introduced Ms. Anna Willis and Ms. Courteney Keatinge of Glass Lewis who provided a policy overview. Ms. Keatinge discussed the current proxy voting process, the management and shareholder proposals and SURS’ voting policy. She also addressed questions posed from the board. A copy of SURS memorandum titled “Corporate Governance Update” and the 2019 CII Conference Agenda are incorporated as part of these minutes as Exhibit 3 and Exhibit 4. The Glass Lewis Presentation titled “2019 Proxy Season Review” is incorporated as part of these minutes as Exhibit 5.

CLOSED SESSION

Trustee Van Meter moved that the Investment Committee go into closed session pursuant to §2(c)(7) of the Open Meetings Act to consider the sale or purchase of securities or investments or to consider an investment contract. Trustee Figueroa seconded and the motion carried in a roll call vote:

Trustee Ammons - aye Trustee Figueroa - aye Trustee Giertz - aye Trustee Rock - aye Trustee Van Meter - aye Trustee Vasquez - aye

RETURN TO OPEN SESSION

Upon a motion by Trustee Van Meter, seconded by Trustee Rock, the motion carried and the Investment Committee resumed its meeting in open session. Trustee Rock made the following motion:

• That based on the recommendation of SURS staff and Meketa, the Investment Committee approve retaining Aspect Capital, Campbell and Company, and LongTail Alpha, subject to successful contract negotiations.

Trustee Flaherty seconded and the motion carried with all trustees present voting in favor.

CONSIDERATION OF TRADITIONAL GROWTH INVESTMENT POLICY UPDATES

Meketa consultant, Mr. Rue, summarized the recently approved changes to the long-term investment strategy while also recognizing the policy decisions approved by the board. Mr. Rue explained that in order to continue the implementation process that incorporates the board’s prior directions to formalize and structure the Traditional Growth components of SURS’ newly created Broad Growth class; it is recommended that the Investment Committee approve the proposed changes to the Investment Policy. Trustee Van Meter made the following motion:

• That based on the recommendation of SURS staff and Meketa, the Investment Committee approve the revised defined benefit plan Investment Policy, as presented.

Trustee Ammons seconded and the motion carried with all trustees present voting in favor. The Meketa memorandum titled “09-2019 IPS Update Memo” is incorporated as part of these minutes as Exhibit 6.

CLOSED SESSION

Trustee Ammons moved that the Investment Committee go into closed session pursuant to §2(c)(7) of the Open Meetings Act to consider the sale or purchase of securities or investments or to consider an investment contract. Trustee Van Meter seconded and the motion carried in a roll call vote:

Trustee Ammons - aye Trustee Figueroa - aye Trustee Giertz - aye Trustee Rock - aye Trustee Van Meter - aye Trustee Vasquez - aye

RETURN TO OPEN SESSION

Upon a motion by Trustee Giertz, seconded by Trustee Van Meter, the motion carried and the Investment Committee resumed its meeting in open session.

Trustee Ammons made the following motion:

• That based on the recommendation of SURS staff and Meketa, the Investment Committee grant authority to staff to restructure the Traditional Growth portfolio to implement the Streamlined Structure (option 2) as presented, subject to successful completion of contract negotiations.

Trustee Rock seconded and the motion carried with all trustees present voting in favor.

PRESENTATION OF FY 2020 INVESTMENT PLAN

Due to time constraints, the board was directed to the 2020 investment plan information contained in the written materials and trustees were encouraged to reach out with any questions. A copy of the Compiled FY 2020 Investment Plan is incorporated as part of these minutes as Exhibit 7.

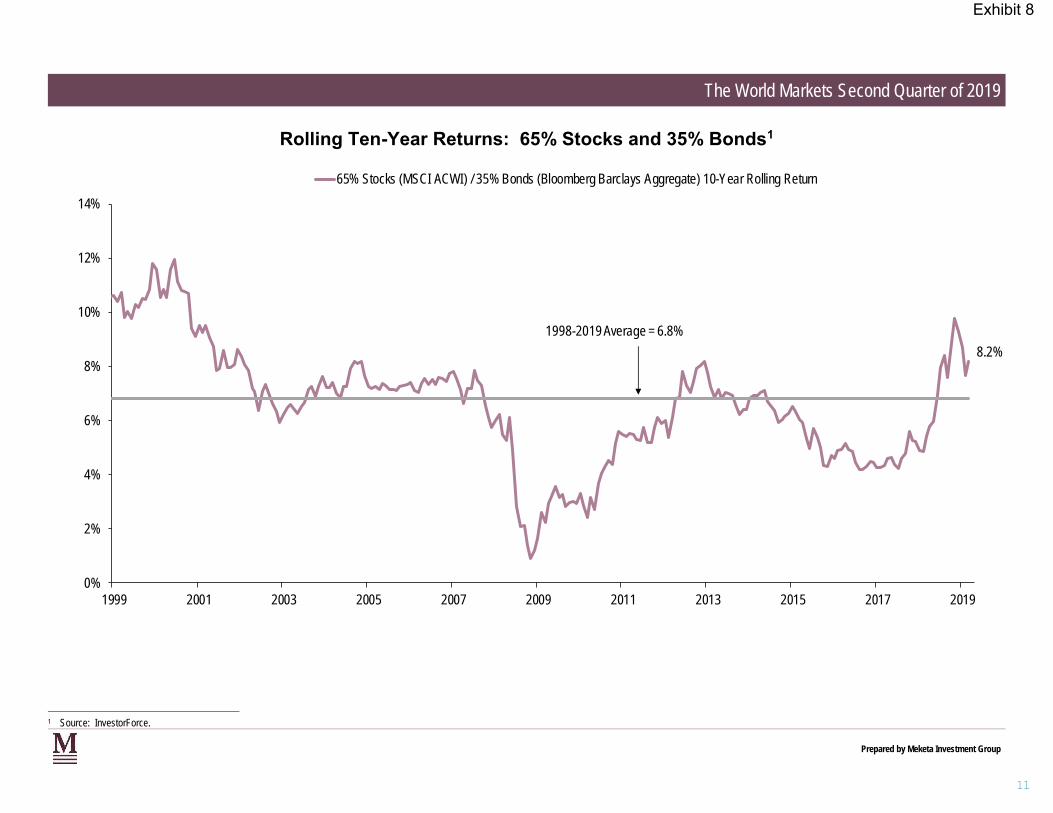

MEKETA PERFORMANCE REPORT AND MANAGER PERFORMANCE

DASHBOARDS

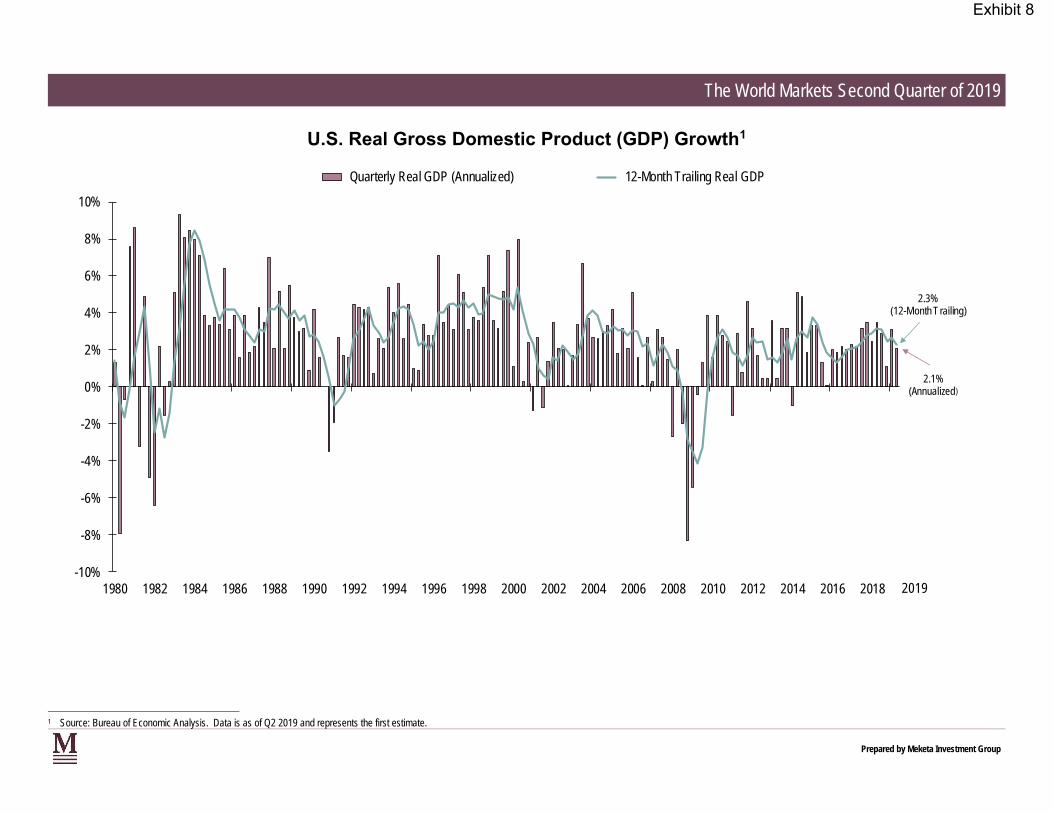

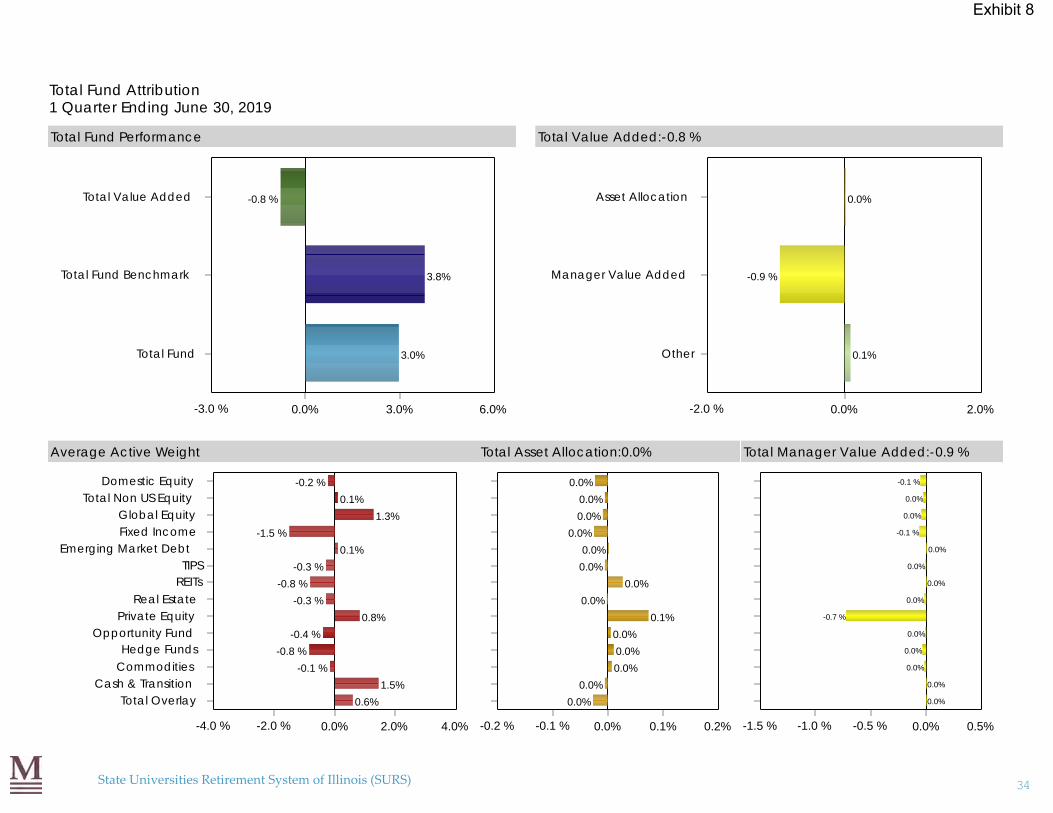

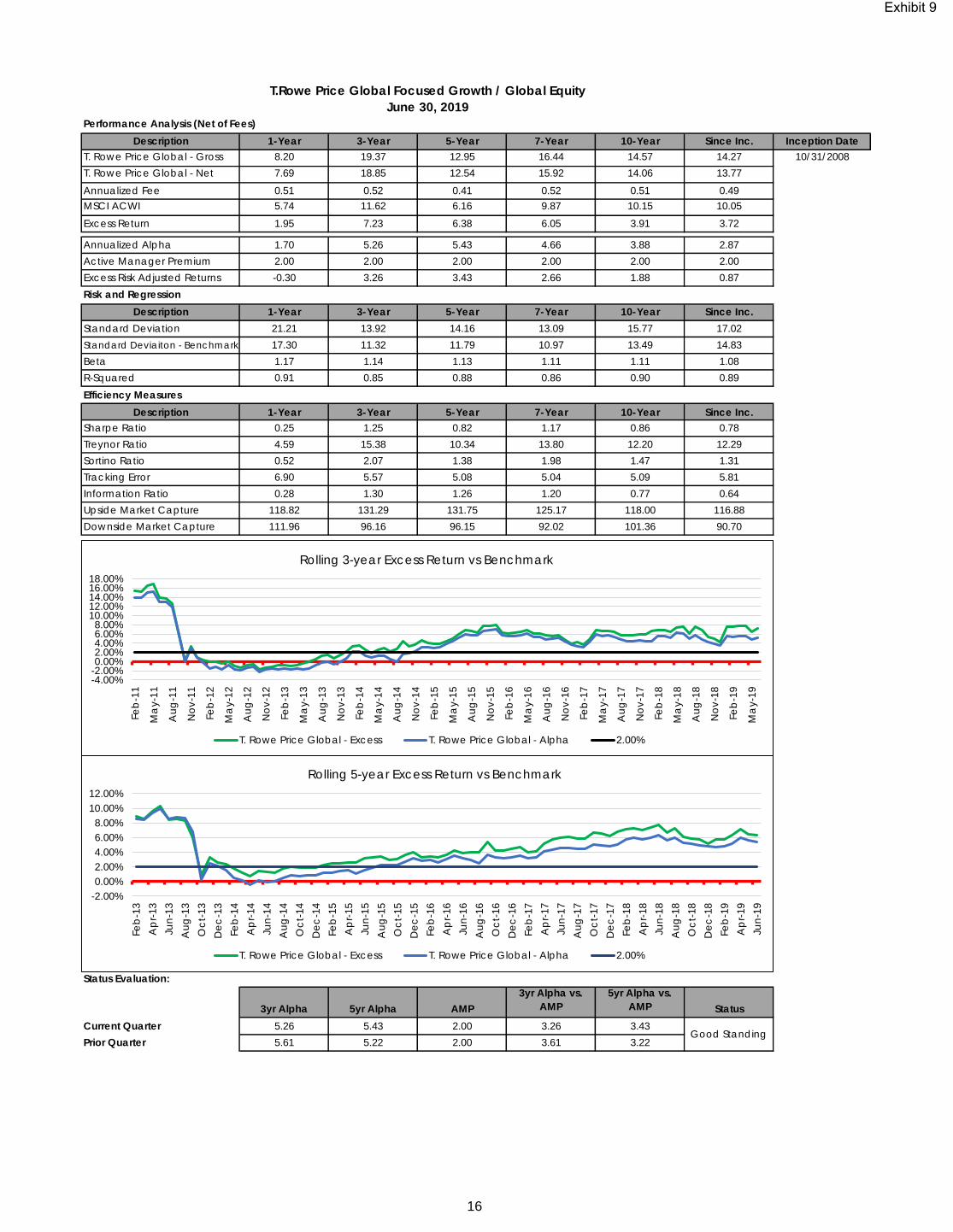

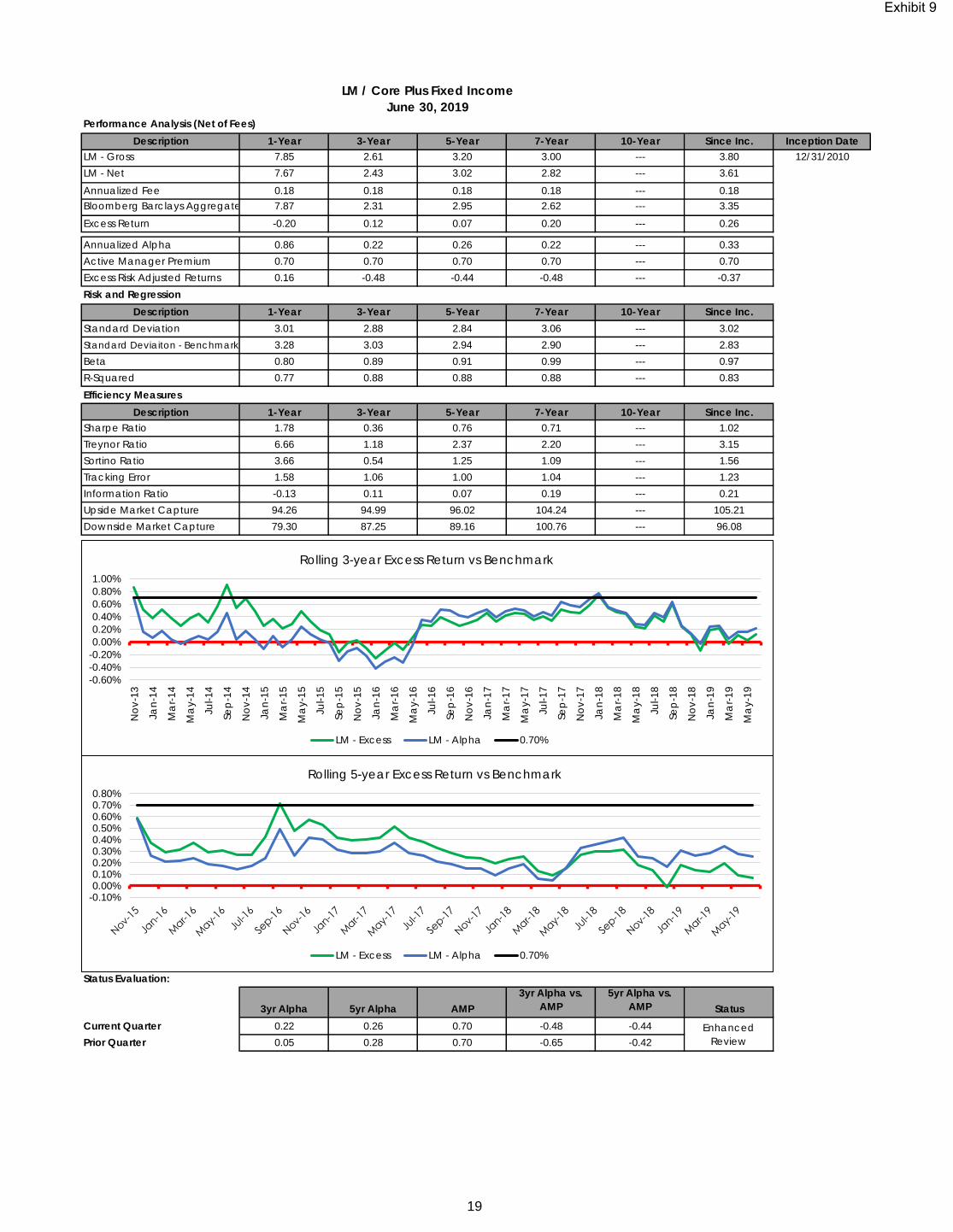

Due to time constraints, the board was directed to the manager performance dashboards contained in the written materials and trustees were encouraged to reach out with any questions. A copy of Meketa’s presentations titled “Q2 2019 Board Report” and “SURS Manager Status Review” are incorporated as part of these minutes as Exhibit 8 and Exhibit 9.

INFORMATIONAL ITEMS NOT REQUIRING COMMITTEE ACTION The following items were provided for reference and are incorporated as a part of these minutes:

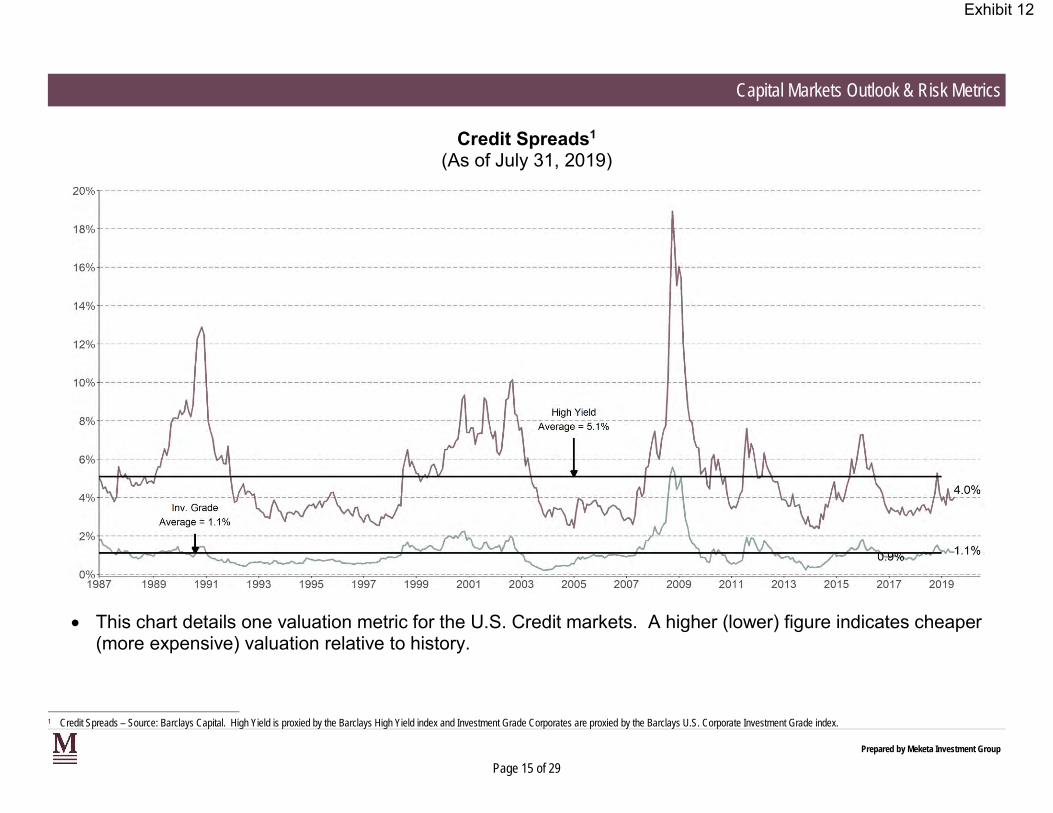

1. Exhibit 10 – SURS Projected Funding Status 2. Exhibit 11 – Alternative Risk Premia Search Update Memo 3. Exhibit 12 – Capital Market Outlook and Risk Metrics – August 2019 4. Exhibit 13 – SURS Risk Memo 5. Exhibit 14 - SURS Risk Report

PUBLIC COMMENT

There were no public comments presented to the Investment Committee.

RECESS At 6:00 p.m. on September 12, 2019, the Investment Committee recessed the meeting.

RECONVENE

At 11:00 a.m. on September 13, 2019, the Investment Committee reconvened the meeting.

The following trustees were present: Mr. Aaron Ammons, Mr. Richard Figueroa, Ms. Jamie-Clare Flaherty, Dr. Fred Giertz, Mr. John Lyons, Dr. Steven Rock, Mr. Collin Van Meter, Mr. Antonio Vasquez and Mr. Mitch Vogel. Others present: Mr. Martin Noven, Executive Director; Mr. Doug Wesley, Chief Investment Officer; Ms. Ellen Hung, Deputy CIO; Ms. Kimberly Pollitt, Mr. Joe Duncan and Mr. Shane Willoughby, Senior Investment Officers; Mr. Alex Ramos and Mr. Brian DeLoriea, Investment Officers; Ms. Kelly Valle and Mr. Akshay Patel, Investment Analysts; Ms. Bianca Green, General Counsel; Ms. Suzanne Mayer, Chief Benefits Officer; Ms. Tara Myers, Chief Financial Officer; Ms. Brenda Dunn, Chief Human Resource Officer; Ms. Kristen Houch, Head of Legislative Affairs; Ms. Kelly Carson and Ms. Annette Ackerman, Executive Assistants; Mr. Michael Sanders and Ms. Emily Wrightson of Cammack Retirement Group. Investment Committee roll call attendance was taken. Trustee Vasquez, Chair, present; Trustee Ammons, present; Trustee Figueroa, present; Trustee Giertz, present; Trustee Rock, present and Trustee Van Meter, present.

DEFINED CONTRIBUTION SEARCH UPDATE

Mr. Joe Duncan along with Cammack representatives Mr. Mike Saunders and Ms. Emily Wrightson provided an update on the Self-Managed Plan and supplemental plan provider search. Ms. Suzanne Mayer discussed the feedback she and Mr. Noven received from SURS employers and members regarding the proposed plan changes.

CLOSED SESSION

Trustee Van Meter moved that the Investment Committee go into closed session pursuant to §2(c)(7) of the Open Meetings Act to consider the sale or purchase of securities or investments or to consider an investment contract. Trustee Rock seconded and the motion carried in a roll call vote:

Trustee Ammons - aye Trustee Figueroa - aye Trustee Giertz - aye Trustee Rock - aye Trustee Van Meter - aye Trustee Vasquez - aye

RETURN TO OPEN SESSION

Upon a motion by Trustee Rock, seconded by Trustee Van Meter, the motion carried and the Investment Committee resumed its meeting in open session. Trustee Giertz made the following motion:

• That based on the recommendation from SURS staff and Cammack, the Investment Committee approve the retention of Voya Financial as the sole recordkeeper for the existing Self-Managed Plan and the new supplemental plan, subject to successful contract negotiations.

Trustee Ammons seconded and the motion carried with all trustees present voting in favor.

Trustee Giertz made the following motion:

• That based on the recommendation from SURS staff and Cammack, the Investment Committee approve the retention of AllianceBernstein as the income solution provider for the existing Self-Managed Plan and the new supplemental plan, subject to successful contract negotiations.

Trustee Van Meter seconded and the motion carried with all trustees present voting in favor.

RECOMMENDATION FOR LONG-DURATION MANDATE

Ms. Hung provided background information regarding the asset allocation approved in September 2018 for the CRO class, which will include long duration investments. Ms. Hung discussed the current RFI and provided staff’s recommendation and guidelines for the Quiet Period Policy. Trustee Giertz made the following motion:

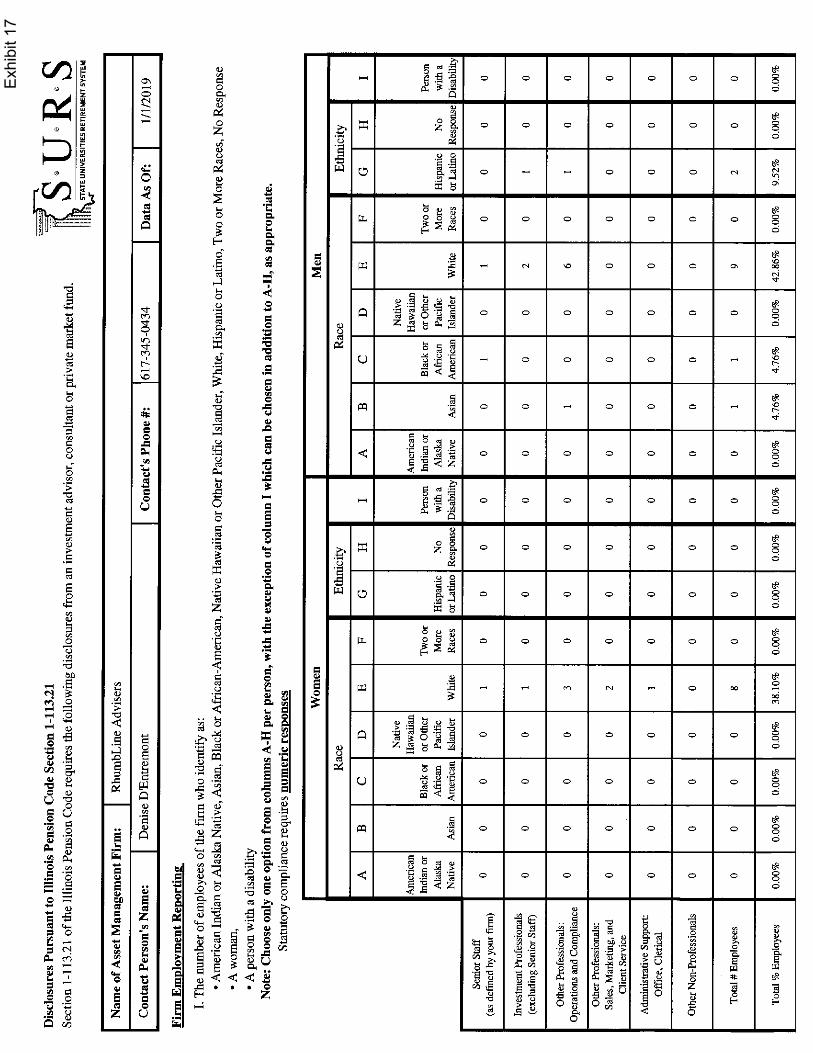

• That based on the recommendation of SURS staff and Meketa, the Investment Committee approve RhumbLine to be retained to manage a U.S. Long Government passive strategy with an initial allocation of 1.75 percent of the SURS total portfolio, subject to successful completion of contract negotiations.

Trustee Ammons seconded and the motion carried with all trustees present voting in favor. A copy of SURS memorandum titled “Long Duration Recommendation Memo” and the “Long Duration RFO Response Matrix” are incorporated as part of these minutes as Exhibit 15 and Exhibit 16. The “Rhumbline Diversity Disclosure Form” is also incorporated as part of these minutes as Exhibit 17.

PROCUREMENT POLICY UPDATE

Mr. Wesley provided a summary of proposed revisions to the Investment Procurement Policy. Trustee Giertz made the following motion:

• That based on the recommendation of SURS staff, the Investment Committee approve the Investment Procurement Policy as presented.

No one seconded the motion; the motion failed. Discussion ensued regarding the proposed amendment to section 6d of the policy. It was then determined that the group would approve the proposed policy amendment without including the section six change that would allow SURS staff to authorize specialty consultants to invest in commitments of $50 million or less. Trustee Van Meter made the following motion:

• That based on the recommendation of SURS staff, the Investment Committee approve the Investment Procurement Policy as amended.

Trustee Lyons seconded and the motion carried with all trustees present voting in favor. A copy of SURS memorandum titled “Procurement Policy Revision Summary” and a copy of the proposed Investment Procurement Policy are incorporated as part of these minutes as Exhibit 18 and Exhibit 19. There was no further business brought before the committee and Trustee Van Meter moved that the meeting be adjourned. The motion was seconded by Trustee Figueroa and carried with all trustees present voting in favor.

Respectfully submitted,

Mr. Martin Noven

Secretary, Board of Trustees MMN/kc

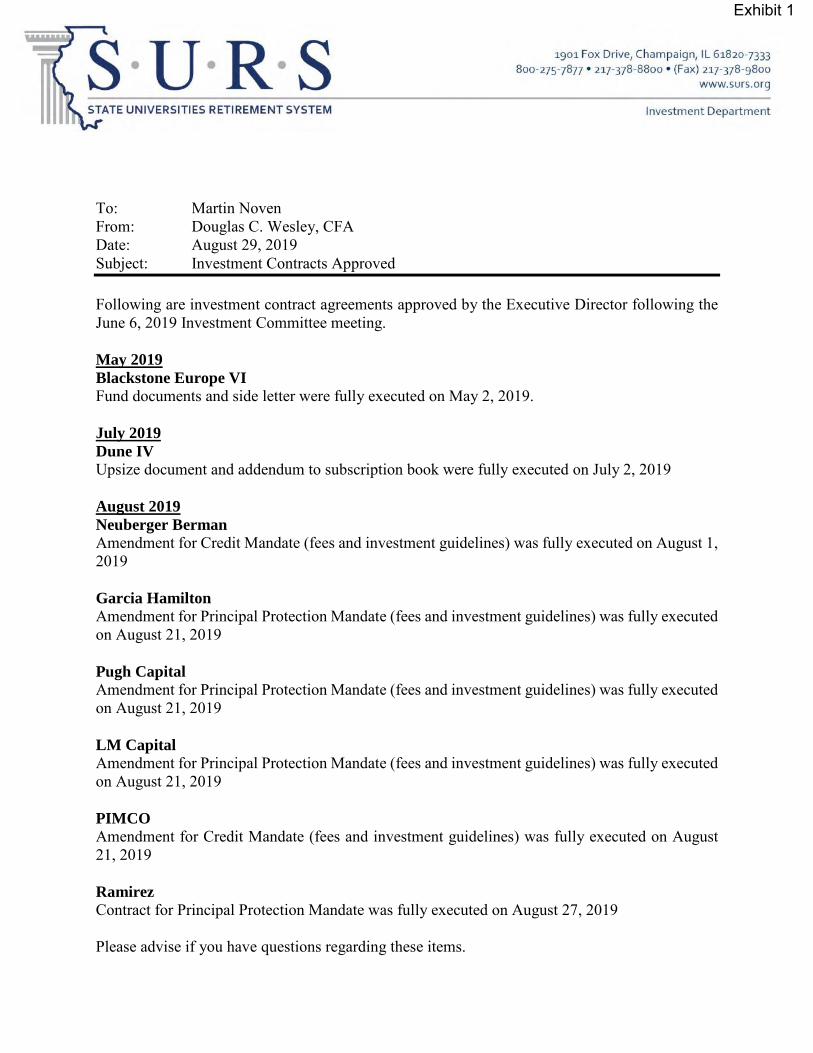

To: Martin Noven From: Douglas C. Wesley, CFA Date: August 29, 2019 Subject: Investment Contracts Approved Following are investment contract agreements approved by the Executive Director following the June 6, 2019 Investment Committee meeting. May 2019 Blackstone Europe VI Fund documents and side letter were fully executed on May 2, 2019. July 2019 Dune IV Upsize document and addendum to subscription book were fully executed on July 2, 2019 August 2019 Neuberger Berman Amendment for Credit Mandate (fees and investment guidelines) was fully executed on August 1, 2019 Garcia Hamilton Amendment for Principal Protection Mandate (fees and investment guidelines) was fully executed on August 21, 2019 Pugh Capital Amendment for Principal Protection Mandate (fees and investment guidelines) was fully executed on August 21, 2019 LM Capital Amendment for Principal Protection Mandate (fees and investment guidelines) was fully executed on August 21, 2019 PIMCO Amendment for Credit Mandate (fees and investment guidelines) was fully executed on August 21, 2019 Ramirez Contract for Principal Protection Mandate was fully executed on August 27, 2019 Please advise if you have questions regarding these items.

Exhibit 1

To: Investment Committee From: Douglas C. Wesley, CFA Date: August 29, 2019 Subject: Report from the June 6, 2019 Investment Committee Meeting Enclosed are the Minutes of the June 6, 2019 Board Meeting. The purpose of this memorandum is to provide a status report on the action items for Investments. Six motions were approved during the Investment Committee Meeting. These included the approval of the minutes from the March 7, 2019 Investment Committee Meeting and a motion that the closed session minutes from the March 7, 2019 Investment Committee Meeting be approved and be opened. The remaining motions were approved by the SURS Board of Trustees and required further action by SURS staff. Open motions requiring further action by SURS Staff are listed below. 1. That based on the recommendation of SURS staff and Meketa, the Investment

Committee approve TorreyCove as the discretionary private equity advisor for a five-year term, subject to successful completion of contract negotiations.

Staff is in process of finalizing contract and side letter with TorreyCove.

2. That based on the recommendation of SURS staff and Meketa, the Investment

Committee approve the proposed amendments to the Investment Policy, as presented.

The Investment Policy for the defined benefit plan has been revised and posted on the SURS website.

3. That based on the recommendation of SURS staff and Meketa, the Investment

Committee grant authority to staff to restructure the fixed income portfolio to implement the agreed upon goals for the principal protection and credit portfolios, subject to successful completion of contract negotiations.

The fixed income restructure is in progress with Northern Trust acting as the transition manager.

4. That based on the recommendation of SURS staff and Callan, the Investment Committee

approve an add-on commitment of $30 million to Dune Real Estate Fund IV, subject to successful completion of contract negotiations.

Upsize commitment and subscription documents with Dune Real Estate Fund IV were fully executed.

Exhibit 2

Open item from April 18, 2018 5. That based on the recommendation of SURS staff and Callan, the Board of Trustees

approve a commitments of the lesser of $40 million or 10% of total fund commitments to Long Warf Real Estate Partners Fund VI, contingent on successful contract negotiations.

Staff is in process of completing the negotiations for the commitment.

6. That based on the recommendation of SURS staff, Progress Investment Management,

and Meketa, the Board of Trustees approve the graduation of Ramirez Asset Management from the Progress Portfolio to a direct SURS relationship.

Contract with Ramirez was fully executed on August 27, 2019.

Open item from March 7, 2018 7. That based on the recommendation of staff and SURS real assets consultant, that a

commitment $75 million Euros to Blackstone Fund 6 be approved, contingent on successful contract negotiations.

Subscription documents and side letter with Blackstone Fund 6 were fully executed.

8. That based on the recommendation of staff and PCA, that a commitment of no more than

1.75 percent of SURS total portfolio (35 percent of the initial 5 percent target to CRO) to long duration strategy be authorized, contingent on successful bidding among the approved slate of passively managed liquid fixed income providers.

The RFI for long duration strategy was issued on May 6, 2019 and responses were due on May 31, 2019. Staff and Meketa will be making a recommendation to the Board at the September 2019 meeting.

9. That based on the recommendation of staff and PCA, that a search be conducted to

identify qualified firms to manage a trend following strategy.

The trend following strategy RFP was issued on April 1, 2019. Thirty responses were received on May 2, 2019. Staff and Meketa reviewed the RFP responses and gave an update at the June Board meeting. Semi-finalist meetings were held on July 31 and August 1, 2019. Staff and Meketa will be making a recommendation to the Board at the September 2019 meeting.

10. That based on the recommendation of staff and PCA, that a search be conducted to

identify qualified firms to manage an alternative risk premia strategy.

The alternative risk premia strategy RFP was issued on April 1, 2019. Thirty-seven responses were received on May 2, 2019. Staff and Meketa reviewed the RFP responses and will be having semi-finalist meetings on September 4-5, 2019. Recommendations to the Board will be made at the October 2019 meeting.

Exhibit 2

Open item from December 6, 2018 11. That based on the recommendation from staff and PCA, the Investment Committee

approve that proceeds from the hedge fund of funds redemption be allocated to AQR (25 percent), Gladius (25 percent) and Neuberger Berman (50 percent), and used to fund benefit payments if needed.

As stated in item 16 below, SURS has received a total of $476.5 million from the hedge fund of funds. A portion of the redemption was reallocated to options strategies ($225 million) with the remaining used for benefit payments. Prior to the additional allocation, Staff negotiated a lower fee schedule with Neuberger Berman and AQR. The reduced fee schedule with Neuberger Berman resulted in annual savings of $90,000 on the additional $150 million allocation. The annual savings with AQR was $82,500 on $75 million of additional allocation.

Open item from October 18, 2018 12. That based on the recommendation from staff and PCA, the Investment Committee

approve the selection of transition managers for the transition manager bench and/or interim management services: BlackRock, Citigroup, Loop Capital, Northern Trust, Penserra and Russell.

Staff has been negotiating contracts with the six managers approved to be on SURS transition bench. Staff continues to work with BlackRock on contract negotiations.

Open item from September 13, 2018 13. That based on the recommendation from SURS staff and SURS investment consultant,

that SURS coordinate full redemption from the KKR Prisma Codlin Fund and from the Newport Monarch Fund. At either the October or December 2018 Investment Committee meeting, staff will recommend where proceeds will be invested.

The notifications for full redemption were submitted to KKR Prisma Codlin Fund and Newport Monarch Fund on September 19, 2018. A total of $332.5 million has been received from Prisma and $144.0 million from PAAMCO. As stated in item 11 above, Staff has reallocated $225 million to options strategies managers as approved by the Board at the December 2018 meeting.

Open item from December 7, 2017

14. The Investment Committee recommends that based on the recommendation of staff and

SURS investment consultant, that staff be able to coordinate a full redemption from the UBS Trumbull Property Fund and use proceeds to invest $300 million in core-plus, open-end real estate fund(s).

The notification was submitted on December 21, 2017. SURS has received a total distribution of $275 million. As the exit queue has significantly increased, it may take a few years before the remaining proceeds, approximately $103 million, are returned.

Please advise if you have any questions prior to the September 12, 2019 Investment Committee meeting.

Exhibit 2

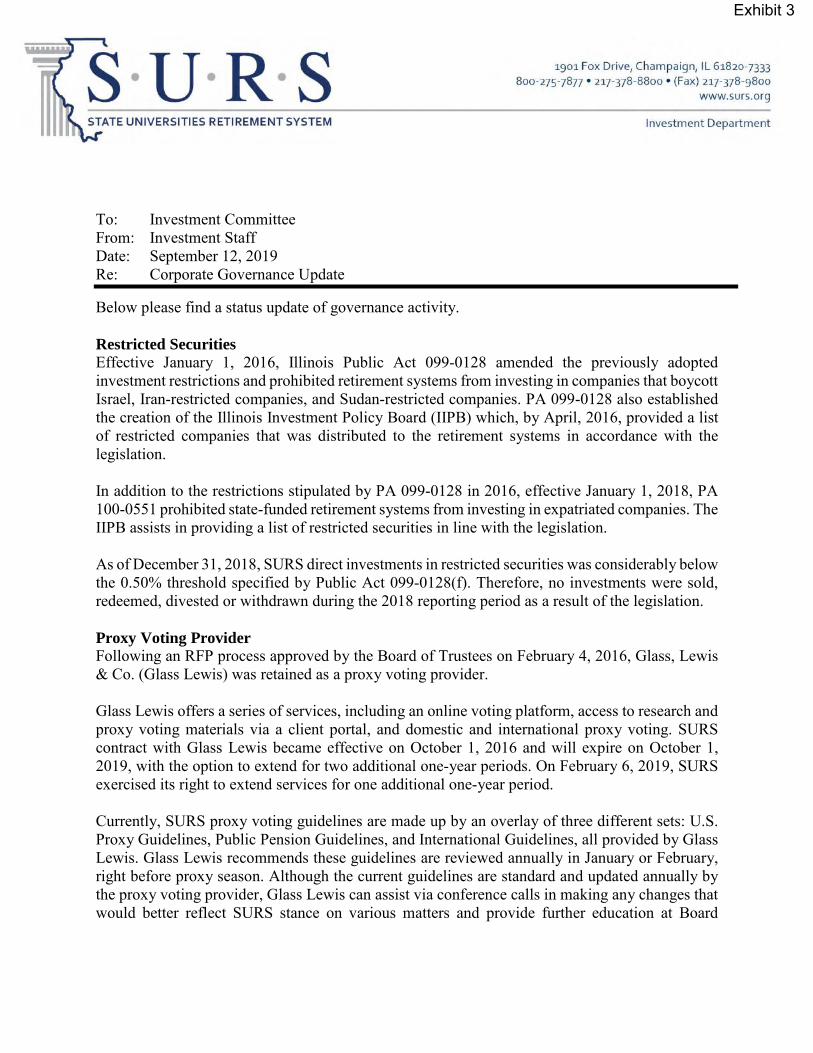

To: Investment Committee From: Investment Staff Date: September 12, 2019 Re: Corporate Governance Update Below please find a status update of governance activity. Restricted Securities Effective January 1, 2016, Illinois Public Act 099-0128 amended the previously adopted investment restrictions and prohibited retirement systems from investing in companies that boycott Israel, Iran-restricted companies, and Sudan-restricted companies. PA 099-0128 also established the creation of the Illinois Investment Policy Board (IIPB) which, by April, 2016, provided a list of restricted companies that was distributed to the retirement systems in accordance with the legislation. In addition to the restrictions stipulated by PA 099-0128 in 2016, effective January 1, 2018, PA 100-0551 prohibited state-funded retirement systems from investing in expatriated companies. The IIPB assists in providing a list of restricted securities in line with the legislation. As of December 31, 2018, SURS direct investments in restricted securities was considerably below the 0.50% threshold specified by Public Act 099-0128(f). Therefore, no investments were sold, redeemed, divested or withdrawn during the 2018 reporting period as a result of the legislation. Proxy Voting Provider Following an RFP process approved by the Board of Trustees on February 4, 2016, Glass, Lewis & Co. (Glass Lewis) was retained as a proxy voting provider. Glass Lewis offers a series of services, including an online voting platform, access to research and proxy voting materials via a client portal, and domestic and international proxy voting. SURS contract with Glass Lewis became effective on October 1, 2016 and will expire on October 1, 2019, with the option to extend for two additional one-year periods. On February 6, 2019, SURS exercised its right to extend services for one additional one-year period. Currently, SURS proxy voting guidelines are made up by an overlay of three different sets: U.S. Proxy Guidelines, Public Pension Guidelines, and International Guidelines, all provided by Glass Lewis. Glass Lewis recommends these guidelines are reviewed annually in January or February, right before proxy season. Although the current guidelines are standard and updated annually by the proxy voting provider, Glass Lewis can assist via conference calls in making any changes that would better reflect SURS stance on various matters and provide further education at Board

Exhibit 3

meetings annually. SURS current proxy guidelines can be found in the supplemental materials folder. • 2019 U.S. Proxy Guidelines • 2019 Public Pension Guidelines • 2019 International Guidelines Investor Stewardship Group and Principles for Responsible Investment On October 19, 2017, SURS became a signatory to the Investor Stewardship Group (ISG), joining more than 60 U.S. and international investors with combined assets in excess of $31 trillion. The ISG establishes a framework comprised of a set of stewardship principles for institutional investors and corporate governance principles for U.S. listed companies. Prior to ISG, SURS was a signatory to the Principles for Responsible Investment (PRI) from 2009 to late 2017. At time of signing, ISG had a larger U.S. base and no membership fees, the latter remains true for ISG, giving ISG an advantage over PRI. In recent years, PRI U.S.-based membership has increased and currently, 48 asset owners, 64 service providers, and 372 investment managers have joined. Although ISG has no membership fees, its focus is particularly strong on Governance at the investor and public company level. In contrast, PRI is an all-encompassing framework that incorporates the various aspects of ESG into the investment practice. Whether ISG or PRI frameworks are utilized will directly depend on the level and scope of involvement SURS would like to achieve. Legislation On August 23, 2019, House Bill 2460 – Illinois Sustainable Investing Act, was signed into law as Public Act 101-0473. This Public Act will require SURS to “adopt a written investment policy that must include material, relevant, and decision-useful sustainability factors to be considered by the board, within the bounds of financial and fiduciary prudence, in evaluating investment decisions. Such factors must include, but are not limited to: (1) corporate governance and leadership factors; (2) environmental factors; (3) social capital factors; (4) human capital factors; and (5) business model and innovation factors, as provided under the Illinois Sustainable Investing Act.” General and specialty consultants, as well as, Glass Lewis, and staff have begun preliminary work to implement this legislation. Council of Institutional Investors (CII) 2019 Conference The 2019 Council of Institutional Investors (CII) will take place September 16-18, in Minneapolis, MN. The conference agenda is attached to this memo. Ms. Kelly Valle and a few members of the Board of Trustees will attend the 2019 CII meeting. Ms. Valle will provide an update to the Board of Trustees at the December meeting. Additionally, a General Member’s business meeting will take place on September 17. During the business meeting, members will have the opportunity to vote on two items: approval of CII 2020 budget and approval of a revised CII policy on executive compensation. SURS staff has recommended to vote FOR on both items. Analysis of the recommendations is presented on Appendix A.

Exhibit 3

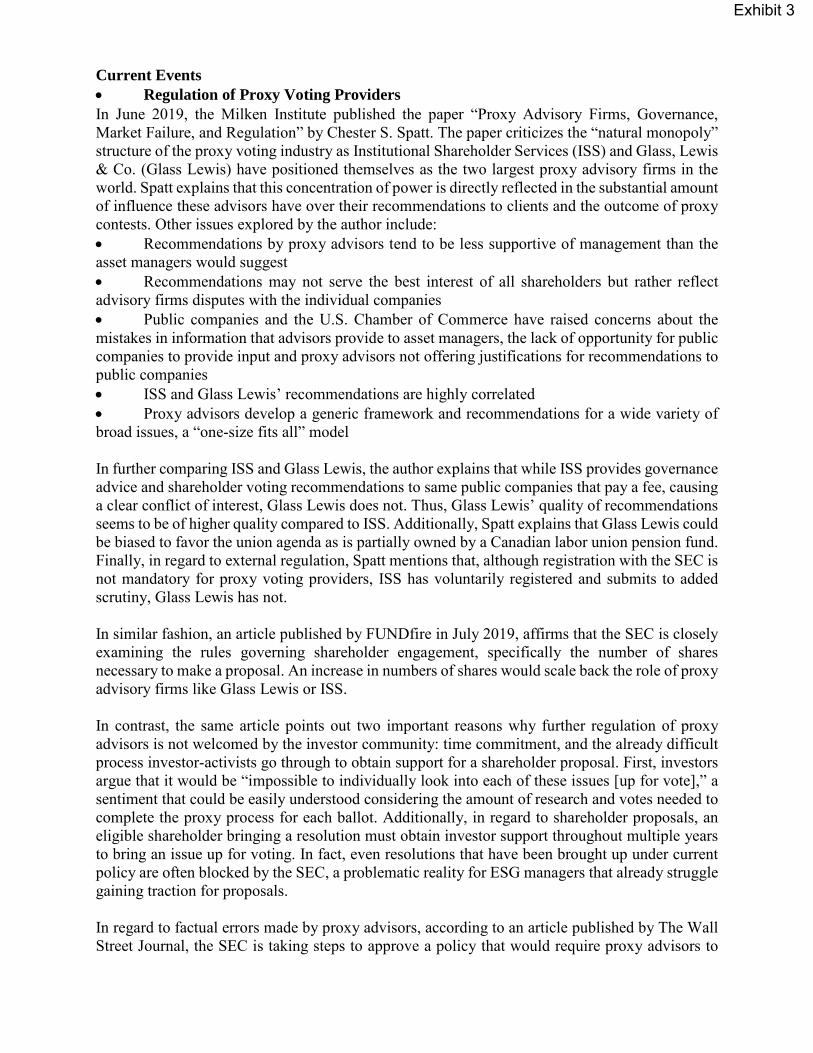

Current Events • Regulation of Proxy Voting Providers In June 2019, the Milken Institute published the paper “Proxy Advisory Firms, Governance, Market Failure, and Regulation” by Chester S. Spatt. The paper criticizes the “natural monopoly” structure of the proxy voting industry as Institutional Shareholder Services (ISS) and Glass, Lewis & Co. (Glass Lewis) have positioned themselves as the two largest proxy advisory firms in the world. Spatt explains that this concentration of power is directly reflected in the substantial amount of influence these advisors have over their recommendations to clients and the outcome of proxy contests. Other issues explored by the author include: • Recommendations by proxy advisors tend to be less supportive of management than the asset managers would suggest • Recommendations may not serve the best interest of all shareholders but rather reflect advisory firms disputes with the individual companies • Public companies and the U.S. Chamber of Commerce have raised concerns about the mistakes in information that advisors provide to asset managers, the lack of opportunity for public companies to provide input and proxy advisors not offering justifications for recommendations to public companies • ISS and Glass Lewis’ recommendations are highly correlated • Proxy advisors develop a generic framework and recommendations for a wide variety of broad issues, a “one-size fits all” model In further comparing ISS and Glass Lewis, the author explains that while ISS provides governance advice and shareholder voting recommendations to same public companies that pay a fee, causing a clear conflict of interest, Glass Lewis does not. Thus, Glass Lewis’ quality of recommendations seems to be of higher quality compared to ISS. Additionally, Spatt explains that Glass Lewis could be biased to favor the union agenda as is partially owned by a Canadian labor union pension fund. Finally, in regard to external regulation, Spatt mentions that, although registration with the SEC is not mandatory for proxy voting providers, ISS has voluntarily registered and submits to added scrutiny, Glass Lewis has not. In similar fashion, an article published by FUNDfire in July 2019, affirms that the SEC is closely examining the rules governing shareholder engagement, specifically the number of shares necessary to make a proposal. An increase in numbers of shares would scale back the role of proxy advisory firms like Glass Lewis or ISS. In contrast, the same article points out two important reasons why further regulation of proxy advisors is not welcomed by the investor community: time commitment, and the already difficult process investor-activists go through to obtain support for a shareholder proposal. First, investors argue that it would be “impossible to individually look into each of these issues [up for vote],” a sentiment that could be easily understood considering the amount of research and votes needed to complete the proxy process for each ballot. Additionally, in regard to shareholder proposals, an eligible shareholder bringing a resolution must obtain investor support throughout multiple years to bring an issue up for voting. In fact, even resolutions that have been brought up under current policy are often blocked by the SEC, a problematic reality for ESG managers that already struggle gaining traction for proposals. In regard to factual errors made by proxy advisors, according to an article published by The Wall Street Journal, the SEC is taking steps to approve a policy that would require proxy advisors to

Exhibit 3

disclose how recommendations are crafted. The policy would also include guidance for investors on how to approach a situation in which the proxy advisors had made factual errors in their recommendations. Opponents to this regulation argue that added disclosures would add financial burden to advisors and as a result barriers to entry to the industry would be much higher, deepening the influence of already existing firms. Furthermore, higher cost for voting guidance could stop smaller managers from voting, causing control to be concentrated on the hands of the bigger investors. Glass Lewis Response In response to concerns raised by Spatt and echoed by other news outlets, Glass Lewis shared its Proxy Advisor Regulation Overview with SURS staff. Glass Lewis’ Proxy Advisor Regulation Overview argues that “proxy advisors do not have undue influence on voting” because investors retain control of decisions at all times. As part of the voting process, investors have access to research and the opportunity to manually vote via the online platform. Glass Lewis also mentions that large investors have custom policies that may differ from advisor’s recommendations or buy research from other advisors. Furthermore, the Overview argues that “investors universally oppose additional regulation,” based to investor opposition to two House Bills introduced in 2016 and 2017, respectively. According to Glass Lewis, opponents included CII, Investment Company Institute, International Corporate Governance Network, CalSTRS, Florida State Board of Administration, and the Ohio PERS. Overall, Glass Lewis believes that further regulation is not necessary and affirms that appropriate safeguards to avoid conflicts of interest have been put in place, including not consulting for issuers, shareholder proposals or proxy contest initiatives, and antifraud provisions of federal securities laws. • Companies Have Obligations to Society CEOs of some of America’s biggest companies voted to change the purpose statement of a corporation to reflect that decisions should not only be based on whether they yield higher profits for shareholders but also to take into account “all stakeholders,” writes David Benoit in an article published by The Wall Street Journal. The proposed stance by members of the Business Roundtable states that “companies should work to deliver value to customers, invest in employees, deal fairly with suppliers and support communities, as well as generate long-term shareholder value,” according to Benoit. Although many supported the proposal, seven CEOs, including Larry Culp of General Electric, declined to endorse the statement fearing the effects it could have on the company’s investors. The statement as presented was an effort to formalize individual stances taken by a number of executives in recent years, possibly as to challenge the narrow focus of the decades-old theory by Milton Friedman that states that “companies only obligation is to maximize value for shareholders,” affirms Benoit. In response to this initiative, CII believes that “the statement gives CEOs cover to dodge shareholder oversight.” In fact, changing the current purpose of a corporation to an all-encompassing, blanket statement to include “all stakeholders,” could be used to signal that the company is complying with their obligations as part of day-to-day business practices and that further oversight is not necessary.

Exhibit 3

Voting at CII APPENDIX A On September 17, CII will conduct the General Member’s business meeting. During the meeting, members will vote on various matters related to CII. SURS staff has made the following voting recommendations: 1. Approve CII 2020 budget: FOR From CII’s proposal: • The budget includes revenue of $4,142,000 (4% higher than projected 2019 revenue) and expenses of $4,119,000 (3% higher than projected 2019 expenses). The operating gain in the budget is $23,000. • General Member dues are unchanged, except the caps for larger funds will have an inflation adjustment of 1.3%. • Associate Member dues will be unbundled from conference attendance fees, which will be charged separately. Associate Member dues levels will be lower, but the budget anticipates that total revenue from Associate Members will be marginally greater.

Analysis: SURS staff recommends to vote FOR CII’s 2020 budget. The proposed budget will allow CII to cover expenses caused by increases in retirement contributions, and expanded staff and pay. Approval will also serve in supporting CII to continue operations as they project new member revenue to drop to 2016 and 2017 levels, support marketing efforts that have been previously under-budgeted, and an increase in legal fees related to analysis of new legislation. 2. Approve revised CII policy on executive compensation: FOR From CII’s proposal: • The proposed new policy lifts up two important objectives for the next decade: simplifying executive pay design, so that both investors and executives can reasonably understand how it works; and lengthening periods of performance measurement with respect to variable pay. • The CII board adopted the language under consideration on August 1. The Policies Committee adopted the draft on May 28 following an 18-month inquiry, which included two roundtables and two comment periods, all of which contributed to the committee’s careful consideration, and in several cases, substantive revisions. • A legacy section of the policy addressing executive stock sales will be replaced by a separate statement currently under development.

Analysis: SURS staff recommends to vote FOR CII’s revised policy on executive compensation. According to CII, policy on executive compensation had not been revised in nearly a decade. The proposed text is a step forward in providing guidance and clarity to a topic that has gained traction in the past few years. The reviewed policy requires boards to disclose forms or compensation, metrics and goals, a comprehensive compensation structure, and guidelines for cost-effective and equitable pay. Additionally, the proposed document provides a revised view of governance of compensation, transparency, peers, and elements of compensation, stock ownership guidelines, compensation recovery, and poor pay practices.

Exhibit 3

2019 CII Conference Agenda

Registration Open 9/16/2019 10:00 AM CT

Master Class: Evaluating Pay for Performance (Additional Fees Apply) Education Courses (additional fees apply)

9/16/2019 11:00 AM CT

Engagement Exchange (Invite Only, Prior Registration Required) 9/16/2019 1:00 PM CT

The New Focus on Stakeholder Interests: Considerations for Public Pension Funds (Invite Only)

9/16/2019 1:00 PM CT

Member-Hosted Panel: Transformation to a Low-Carbon Economy - Board Accountability & Investor Roles

Member-Hosted Meetings 9/16/2019 3:15 PM CT

Member-Hosted Panel: Contested M&A Activity and Trends Member-Hosted Meetings 9/16/2019 3:15 PM CT

Member-Hosted Panel: Artificial Intelligence and Its Role and Impact on Investor Relations

Member-Hosted Meetings 9/16/2019 3:15 PM CT

Welcome & CII Updates Plenary Sessions 9/16/2019 4:30 PM CT

Dual Class Stock and the Future of Corporate Governance Plenary Sessions 9/16/2019 4:45 PM CT

Evolving the Board Plenary Sessions 9/16/2019 5:30 PM CT

Cocktail Reception Networking Event 9/16/2019 6:15 PM CT

Trustee Roundtable & Dinner (Invite Only) 9/16/2019 7:30 PM CT

Registration Open 9/17/2019 7:00 AM CT

Member Lounge Open 9/17/2019 7:00 AM CT

Breakfast Food/Meals 9/17/2019 7:30 AM CT

Welcome from Minnesota Governor Tim Walz Plenary Sessions 9/17/2019 8:05 AM CT

Fiduciary Duty and ESG in Investment: CIO Perspectives Plenary Sessions 9/17/2019 8:15 AM CT

Public Company Accounting Oversight: Key Issues and Developments Plenary Sessions 9/17/2019 9:00 AM CT

Gender Pay Equity Plenary Sessions 9/17/2019 9:30 AM CT

Lessons from the Front Lines: Challenges in Renewable Energy Deployment & Transitions

Plenary Sessions 9/17/2019 10:00 AM CT

Networking Break Networking Event 9/17/2019 10:45 AM CT

Member-Hosted Panel: RiskyRX - Investor Views on Opioid Risks & Anticompetitive Practices in Pharma

Member-Hosted Meetings 9/17/2019 11:15 AM CT

Member-Hosted Panel: Forced Arbitration Clauses & the Repercussions for Institutional Investors

Member-Hosted Meetings 9/17/2019 11:15 AM CT

Member-Hosted Panel: The Growing Risk of Private Prisons for Long-term Investors

Member-Hosted Meetings 9/17/2019 11:15 AM CT

Luncheon Keynote: Dan Ariely, Author of The Secret and Benefits of Understanding Motivation at Work

Food/Meals 9/17/2019 12:30 PM CT

Breakout: Auditing Issues and Proxy Voting Breakout Sessions 9/17/2019 2:15 PM CT

Breakout: Sustainability Reporting Standards Breakout Sessions 9/17/2019 2:15 PM CT

Exhibit 4

Breakout: Bankruptcy Process and Corporate Governance Breakout Sessions 9/17/2019 2:15 PM CT

Corporate Members Constituency Meeting Constituency Meetings 9/17/2019 3:30 PM CT

Public Pension Fund Members Constituency Meeting Constituency Meetings 9/17/2019 3:30 PM CT

Labor Union Members Constituency Meeting Constituency Meetings 9/17/2019 3:30 PM CT

Associate Members Constituency Meeting Constituency Meetings 9/17/2019 3:30 PM CT

General Members Business Meeting Business Meeting 9/17/2019 4:30 PM CT

Cocktail Reception Networking Event 9/17/2019 5:30 PM CT

Registration Open 9/18/2019 8:00 AM CT

Member Lounge Open 9/18/2019 8:00 AM CT

Continental Breakfast Food/Meals 9/18/2019 8:15 AM CT

International Governance Developments hosted by the International Governance Committee

Plenary Sessions 9/18/2019 9:00 AM CT

Policy Outlook: Proxy Advisory Firm Regulation Plenary Sessions 9/18/2019 9:45 AM CT

Networking Break 9/18/2019 10:45 AM CT

ESG Priorities and Director Accountability Followed by Roundup of CII Members’ Initiatives

Plenary Sessions 9/18/2019 11:00 AM CT

Networking Buffet Lunch Food/Meals 9/18/2019 12:15 PM CT

Exhibit 4

PRESENTATION TO ILLINOIS STATE UNIVERSITIES RETIREMENT SYSTEM

2019 PROXY SEASON REVIEW

POLICY OVERVIEW

SEPTEMBER 12th, 2019

Exhibit 5

AGENDA

• Introduction to Glass Lewis

• Introduction to Corporate Governance

• Institutional Investors: Proxy Voting Process

• 2019 Proxy Season Review

• SURS Proxy Voting Policy

2

Exhibit 5

INTRODUCTION TO GLASS LEWIS

3

Exhibit 5

GLASS LEWIS & CO.

Founded in 2003, Glass Lewis is the leading independent provider of global governance services. Glass Lewis helps institutional investors understand and connect with the companies in which they invest.

4

1,300+Institutional Clients

20,000+Research Reports Annually

360+Employees

We produce Proxy Papers to provide analysis and voting recommendations to our clients (Institutional Investors) on how to vote at a public company’s (Issuer) annual and special meetings.

Exhibit 5

PROXY RESEARCH PROCESS

Team Approach

Analysis varies based upon market, issue, complexity and company size

All reports reviewed by two or more people; varies by report profile

Accuracy and lead times are monitored to ensure client satisfaction

Executive Compensation

Analyze executive compensation quantitatively and qualitatively

Incorporate multiple performance factors into Pay-for-Performance analysis

Mergers & Acquisitions / Proxy Contests

Specialized team and experience

Proposed offers are evaluated versus the returns to shareholders

Approach to proxy contests aligns well with most institutional investors

ESG / Shareholder Proposals

Viewpoint’s proprietary rules engine interprets complex policies

Unmatched nuance and cascading rules minimize noise and focus your attention on the most important issues

5

Exhibit 5

PROXY PAPER

Guaranteed global coverage; complete report for all companies

More than 20,000 meetings across 100 markets

Independent and contextual analysis with a focus on economic impact

Direct access to research team

Board presentations, white papers, Proxy Talks, data feeds

Issuer Engagement Policy:

Designed to empower clients and investors

6

Exhibit 5

VIEWPOINT

Flexible, configurable user interface

Responsive search; workflow updates dynamically

In-application user collaboration; also streamlines communication between non-users

Nuanced custom policy implementation

Transparent and compliant; audits, reconciliation and activity logs

Extensive permissioning controls

Myriad reporting options

Secure and reliable:99.9%+ uptime; round the clock support

7

Exhibit 5

INTRODUCTION TO CORPORATE GOVERNANCE

8

Exhibit 5

• Corporate governance is the system of rules, practices and processes by which a company is directed and controlled

– A framework that promotes accountability and transparency

– Involves balancing the interests of the company’s many stakeholders: management, board of directors, shareholders, customers, the environment and everyone effected.

– More attention on corporate governance following the collapse of Enron and similar scandals (Glass Lewis was founded in 2003)

• Recent examples: Wells Fargo; Uber; Equifax; Volkswagen; Boeing; Tesla

WHAT IS CORPORATE GOVERNANCE?

9

Exhibit 5

• Management Proposals: Governance– Election of Directors (“EOD”)– Ratification of Auditors (“ROA”)– Misc. proposals

• Amendments to articles/bylaws• Board size, company name change, transaction of other business• Reverse stock splits & changes to authorized capital• Issuances of securities

• Management Proposals: Compensation– Advisory Vote on Executive Compensation (“Say-on-Pay”)

• Mandated by Dodd Frank Act, July 2010.– Equity Plans and other Pay-Related Proposals

• Stock Option Plans; Bonus 162(m) Plans; ESPP’s; Director Comp. Plans;

• Shareholder Proposals– Governance topics; Environmental Reporting; Gender Pay Equity;

Corporate Political Spending; Corporate Practices, etc.• Mutual Fund Advisory/Sub-advisory Agreements, Fund Reorganizations• Approval of Mergers & Acquisitions (“M&A”)

TYPES OF PROPOSALS

10

Exhibit 5

INSTITUTIONAL INVESTORS: PROXY VOTING PROCESS

11

Exhibit 5

PROXY VOTING PROCESS

12

1. Annual or special meeting is called by a company whose shares they own

2. Institutional Investor is required to vote on the proposals– Outsource to proxy advisors (such as Glass Lewis)– In-house resources expanding in recent years

3. Institutional Investor votes their shares4. Vote results help drive change and ongoing dialogue

between investors and companies

• Clients use GL/proxy advisors in different ways– Implement custom policies based on data collection – Use analysis as input to their in-house policies and decisions

• “Research only” clients– Implement proxy advisor’s standard policy

Exhibit 5

2019 PROXY SEASON REVIEW

13

Exhibit 5

2019 PROXY SEASON REVIEW- MANAGEMENT PROPOSALS

• Increased opposition to directors– Sixty-eight directors failed to receive majority support from shareholders in the 2019 proxy

season, up from fifty-one in 2018 and sixty in 2017

– Issues such as ongoing compensation concerns, failure to attend enough board meetings, overboarding and responsiveness to majority supported shareholder proposals appear to be some of the top reasons for shareholder discontent

• Board composition is still a key issue, and is driving change in the boardroom– Board diversity a significant concerns for investors

– 27% of companies in the S&P 500 disclosed a board skills matrix

– 43% of companies in the S&P 500 have explicit board oversight of environmental and social issues

• There is increased opposition to executive compensation– Average support for say on pay proposals dropped from 90% to 89% in 2019

– Failed proposals decreased by 10% from 2018 while the number of companies receiving significant opposition increased by 5.5%.

– The proportion of failed Golden Parachute proposals more than doubled year over year.

14

Exhibit 5

2019 SHAREHOLDER PROPOSALS BY CATEGORY

15

Exhibit 5

2019 PROXY SEASON REVIEW- SHAREHOLDER PROPOSALS

• Although ESG issues continue to become more mainstream, the number of proposals going to a vote has been on a continuous decline: Glass Lewis reviewed 426 shareholder proposals in 2019, down from 585 in 2015.

– Average support for shareholder proposals was 32.5% in both 2018 and 2019. However, we saw a notable increase in the average support for environmental and social initiatives (24.8% to 27% in 2019).

• There has been an increased focus on human capital management, with new proposals on issues related to sexual harassment, mandatory arbitration and inequitable employment practices, all going to a vote during the 2019 proxy season.

– Despite many of these proposals being submitted to tech companies with dual class shares (and therefore depressed shareholder support), these proposals received average support of 26%. Further, a number of these proposals, on issues ranging from executive diversity to reporting on workforce composition, received majority shareholder support.

• Technology companies were arguably the focus of investors during the 2019 proxy season. Alphabet had the highest number of shareholder proposals (13) followed by Amazon (12) and Facebook (8).

– This highlights the increasing importance of technology companies in society. Shareholder proposals on technology-related issues, such as facial recognition technology and content governance, received 21% average support.

16

Exhibit 5

SURS VOTING POLICY

17

Exhibit 5

SURS PROXY VOTING GUIDELINES

• SURS follows Glass Lewis’ Public Pension Guidelines

• The Public Pension Guidelines overlay on top of Glass Lewis’ standard guidelines, where we evaluate each company on a case-by-case basis

– Will take the Glass Lewis approach for a number of issues, including M&A and contested meetings and other unique situations

• The Public Pension guidelines are designed to ensure compliance with the special fiduciary responsibilities of public pension plan sponsors in voting proxies on behalf of public employees. These guidelines are designed for investors with extremely long-term investment horizons.

18

Exhibit 5

SURS PROXY VOTING GUIDELINES

• Board diversity, tenure and refreshment– Vote against members of the nominating committee in the event that the board has an

average tenure of over ten years and the board has not appointed a new nominee to the board in at least five years;

– Vote against the male members of the nominating committee in instances where the board is comprised of fewer than 30% female directors for large-cap companies, or against the nominating committee when there is not at least one woman on the board at mid- and small-cap companies.

• Overboarding– Vote against directors who sit on more than five corporate boards (or for directors who are

also executives, two total boards)

– Vote against the nominating and governance committee when companies have adopted a virtual-only shareholder meeting format and have not provided disclosure of shareholder protections

• Tax Havens– Vote against company proposals to redomicile in known tax havens.

• Auditor Ratification– Vote against auditor ratification proposals i n instances where it is clear that a company’s

auditor has not been changed for 20 or more years.

19

Exhibit 5

SURS PROXY VOTING GUIDELINES

• Compensation

– Largely follows the Glass Lewis recommendations

– In instances where a company has received a Pay-for-Performance grade of “D” or “F” and Glass Lewis’ standard policy has recommended in favor of the plan, vote against say-on-pay proposals where sustainability is not an explicit consideration for companies when awarding executive compensation.

• Shareholder Proposals

– Vote for most governance shareholder proposals

– Vote for all environmental and social proposals aimed at increasing a company’s disclosure of environmental or social issues

– Vote against resolutions requesting that companies take specific actions or adopt specific policies, unless Glass Lewis has recommended in favor of the resolution

20

Exhibit 5

M E M O R A N D U M

M E K E T A I N V E S T M E N T G R O U P 411 PARK AVENUE SUITE 401 PORTLAND, OR 97209

503 226 1050 fax 503 226 3304 www.meketagroup.com

To: State Universities Retirement System (SURS) Board of Trustees

From: Neil Rue, CFA; Colin Bebee, CFA; David Sancewich Meketa Investment Group (MIG)

Cc: Doug Wesley, CFA – CIO Ellen Hung, CFA – Deputy CIO

Date: September 12, 2019

Re: Recommendations to Rename SURS’ Public Equity class “Traditional Growth,” Modify the Traditional Growth Policy, and Make Additional Updating Edits to SURS’ Investment Policy Statement

SUMMARY & RECOMMENDATION

Over the last several months, extending back into mid-2018, the SURS Board has approved several material changes to its long-term investment strategy. The first major decision, in September 2018, was the Board approving a new long-term strategic allocation policy.

As a result of the allocation policy decision, the Board has approved (i) a strategic plan and revised policy language for the SURS Real Assets classes (December 2018), (ii) a structural blueprint and policy language for the new Crisis Risk Offset class (March 2019), (iii) revised policy language and structural changes for the Principal Protection class and the Credit component of Stabilized Growth (June 2019), and (iv) selected a new Private Equity advisor who will provide key guidance in developing an expanded Non-Traditional Growth portfolio (June 2019). All these decisions provide important direction and guidance to Staff and its consultants to implement the Board’s earlier major policy decision.

This memo continues the implementation process by recommending policy language changes that incorporate the Board’s prior direction on formalizing and structuring the Traditional Growth component of SURS’ newly-created Broad Growth class. Both Staff and MIG recommend that the Investment Committee/Board approve the requested changes to the SURS IPS.

DISCUSSION

The attached changes to the IPS incorporate and memorialize all of the above prior Board approvals while also directly highlighting requested changes to the Traditional Growth component that reflects Board direction in June 2019 (See Attachment 1 – Clean Copy and Attachment 2 – Red Line Copy). In summary, the latest redline requests to the IPS are:

Exhibit 6

Memorandum Page 2 of 3 September 12, 2019

Renaming the Public Equity Structure section to “Traditional Growth” and revising policy language pertaining to this class. The key change are to (i) provide Staff with flexibility to allocate assets across U.S., Non-U.S., and Global regional mandates and (ii) to adopt a broad Global Equity benchmark, as presented in Appendix 5. These changes reflect Board deliberation and direction during the June 2019 Investment Committee meeting.

Re-organizing Section VI of the IPS to completely reflect the new strategic allocation structure. Prior versions of Section VI of the IPS were evolutions toward the new allocation structure, which the Board approved and adopted in September 2018. Section VI’s format now fully reflects that structural decision. Such a change is largely shifting/re-organizing of content and not necessarily making substantive changes to the content itself. Importantly, Appendix 4 now fully reflects implementation of the new strategic structure, which is to begin at the outset of 4Q 2019 (i.e., 10/1/2019).

Updating Appendices 6-8 of the IPS to reflect updated diversity goals. Based on recent deliberations, diversity goals have been updated to (i) address desired level of fees paid to diverse managers and (ii) adjusting goals for minority broker activity, primarily to account for new strategic structure.

Housecleaning items. Minor changes and edits that help make policy language more consistent across all sections. Also updating Appendix 5 to include previously approved benchmarks for the relevant classes, components, sub-components, and classes.

These updates to the IPS represent a key phase in incorporating the Board’s prior strategic decisions into the current SURS investment portfolio. In particular, the Traditional Growth component is SURS portfolio’s largest segment. Approving the changes related to the Traditional Growth component will likely have a material impact on future investment results.

PLANS FOR THE TRADITIONAL GROWTH COMPONENT

The most impactful recommended IPS language changes relates to the Traditional Growth component. Here are a few key points related to Traditional Growth implementation (most were discussed and reviewed in June):

Based on the strategic allocation, Traditional Growth (as a percent of assets) is slated to decline materially over time. In keeping with this implementation trend, Staff is expecting to withdraw roughly $1B from Traditional Growth over the next few months.

A key to a successful Traditional Growth class is allocating appropriately to a spectrum of passive and active management. The new manager structure for Traditional Growth will likely incorporate a broader spectrum of approaches than in the past.

Exhibit 6

Memorandum Page 3 of 3 September 12, 2019

The new policy language provides heightened implementation flexibility to Staff. Allocation weights to U.S., Non-U.S., and Global mandates were previously hard-coded. Staff will now be allowed to determine the appropriate weights as long as they remain in-line with the global equity benchmark. This should allow Staff to migrate to global mandates over time, where the ability to add value appears to be strongest.

A BRIEF COMMENT ON IMPLEMENTATION

As discussed earlier, Appendix 4 in the IPS has now been updated to fully reflect the new strategic allocation structure. The Appendix in prior versions of the IPS showed an allocation structure that was an evolving hybrid of both the historical and new policy structures. With the new structure now in place, the overarching objective is to achieve the long-term class weighting targets highlighted in Appendix 4 in a deliberate, yet timely manner. Shown below is a preliminary allocation plan for achieving the long-term target by Fiscal 2023:

Interim Strategic Allocation Targets

SURS Actual 6/30/2019

(%)* 10/1/2019

(%)** 7/1/2020

(%) 7/1/2021

(%) 7/1/2022

(%)

Long-Term Target

(%)

Broad Growth 86 81 76 66 66 66

Non-Traditional Growth 10 10 11 12 13 15

Traditional Growth 54 47 41 28 27 25

Stabilized Growth 22 24 24 26 26 26

Inflation Sensitive 6 6 6 6 6 6

Principal Protection 7 8 8 8 8 8

CRO 0 5 10 20 20 20

Total 100 100 100 100 100 100

*May not sum to 100% due to rounding **Preliminary

As the table highlights, as of 6/30/2019, Staff has made some incremental progress toward the new strategic allocation since the end of 2018. However, significant implementation remains. October 2019 is indicated as “Preliminary” as it is a challenge to precisely determine starting percentages with various tasks currently in process. That being the case, Staff and MIG are working closely together to execute various implementation tasks in a deliberate yet timely manner in order to maintain the spirit of the implementation schedule highlighted above. To date, Principal Protection and Credit transitions should be completed by October 1st. In addition, Crisis Risk Offset class implementation is proceeding on schedule, with manager searches expected to be completed in or near October 2019. NAR/CB/DPS/hls Attachments

Exhibit 6

Investment Policy April 2019

Page 11

VI. Portfolio Construction and Performance Benchmarks The Board has adopted Target Allocation Percentages in accordance with its Strategic Allocation and Rebalancing strategy described in Section V. Within each Strategic Class, the Board will determine the amount of such class that will be (i) managed internally vs. externally; (ii) managed actively vs. passively; (iii) allocated to a particular sub-class, sector or style, if any, and (iv) allocated to each approved Manager. Strategic Class allocations will be reviewed annually in connection with the Target Allocation Percentage review. The choice of internal vs. external management shall be based on a periodic comparison of (i) the cost and availability of qualified Staff and systems support and (ii) the cost and availability of Managers. Currently, the Board makes exclusive use of external Managers. Active Management shall be considered for Strategic Classes, sub-classes and styles of Marketable Securities (actively traded public Equity, public Fixed-income and Alternative markets), where empirical evidence shows that (i) a significant percentage (e.g. 25%) of Managers in such category (adjusted for survivorship) have consistently outperformed applicable Benchmarks for such category (net of fees) over a three (3), five (5) and ten (10) year period and (ii) that outperformance has been significant (e.g. greater than 50 basis points). For categories not meeting this threshold, and subject to SURS’ MFDB Manager Utilization Goals and Manager Diversity Program, Passive Management will be followed. For all non-actively traded public Equity, public Fixed-income and Alternative markets, Active Management will be used. Amounts allocated to a particular sector or style shall also be based on empirical evidence showing that (i) a significant percentage (e.g. 25%) of Managers in such sub-sector or style (adjusted for survivorship) have consistently outperformed applicable Benchmarks for such sub-sector or style (net of fees) over a three (3), five (5) and ten (10) year period and (ii) that outperformance has been significant (e.g. greater than 50 basis points). If such threshold is not met, no allocation to such sub-sector or style will be made. Amounts allocated to each Manager, within a Strategic Class, sub-class, sector or style shall be based on: (i) the total dollar amount to be allocated to such category; (ii) the relative ongoing performance of applicable Managers; (iii) the unique attributes of such Manager’s investment style and potential benefits from diversification; and (iv) the overhead cost of managing the number of Managers within such category. Subject to SURS’ MFDB Manager Utilization Goals and Manager Diversity Program, the Board has a bias toward fewer Managers and more meaningful allocations. Managers selected by the Board will be given specific roles within each Strategic Class, sub-class, sub-sectors, and styles, as applicable. These roles are specifically set forth for each firm as Manager Guidelines, established at the beginning of the relationship with SURS as part of the contract negotiation process. These guidelines cover such items as Benchmarks, permissible investments, use of leverage, obligor concentrations, currency denomination, etc. Staff and Consultant will be responsible for implementation of these guidelines, supervision of the Managers, performance monitoring and reporting. Updates will be provided to the Board or Investment Committee as requested, or as deemed necessary by Staff and Consultant.

ATTACHMENT 1 - CleanExhibit 6

Investment Policy April 2019

Page 12

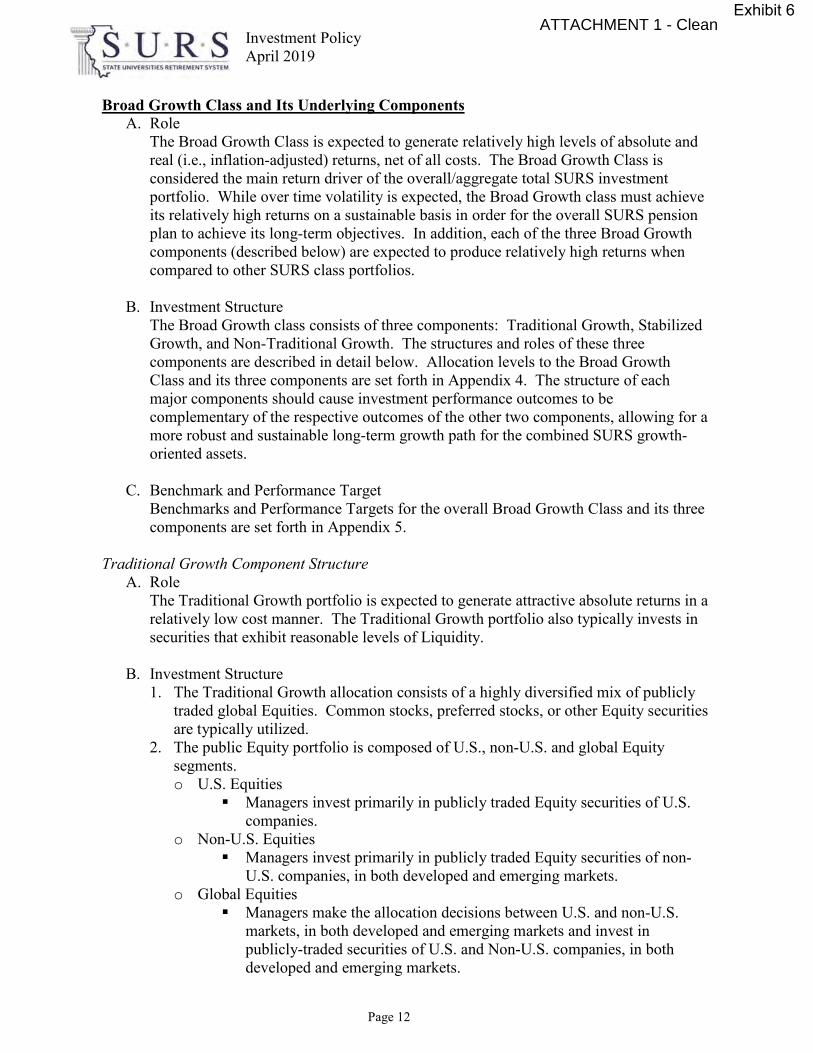

Broad Growth Class and Its Underlying Components A. Role

The Broad Growth Class is expected to generate relatively high levels of absolute and real (i.e., inflation-adjusted) returns, net of all costs. The Broad Growth Class is considered the main return driver of the overall/aggregate total SURS investment portfolio. While over time volatility is expected, the Broad Growth class must achieve its relatively high returns on a sustainable basis in order for the overall SURS pension plan to achieve its long-term objectives. In addition, each of the three Broad Growth components (described below) are expected to produce relatively high returns when compared to other SURS class portfolios.

B. Investment Structure The Broad Growth class consists of three components: Traditional Growth, Stabilized Growth, and Non-Traditional Growth. The structures and roles of these three components are described in detail below. Allocation levels to the Broad Growth Class and its three components are set forth in Appendix 4. The structure of each major components should cause investment performance outcomes to be complementary of the respective outcomes of the other two components, allowing for a more robust and sustainable long-term growth path for the combined SURS growth-oriented assets.

C. Benchmark and Performance Target Benchmarks and Performance Targets for the overall Broad Growth Class and its three components are set forth in Appendix 5.

Traditional Growth Component Structure

A. Role The Traditional Growth portfolio is expected to generate attractive absolute returns in a relatively low cost manner. The Traditional Growth portfolio also typically invests in securities that exhibit reasonable levels of Liquidity.

B. Investment Structure

1. The Traditional Growth allocation consists of a highly diversified mix of publicly traded global Equities. Common stocks, preferred stocks, or other Equity securities are typically utilized.

2. The public Equity portfolio is composed of U.S., non-U.S. and global Equity segments. o U.S. Equities

Managers invest primarily in publicly traded Equity securities of U.S. companies.

o Non-U.S. Equities Managers invest primarily in publicly traded Equity securities of non-

U.S. companies, in both developed and emerging markets. o Global Equities

Managers make the allocation decisions between U.S. and non-U.S. markets, in both developed and emerging markets and invest in publicly-traded securities of U.S. and Non-U.S. companies, in both developed and emerging markets.

ATTACHMENT 1 - Clean

ATTACHMENT 1 - CleanATTACHMENT 1 - CleanATTACHMENT 1 - Clean

Exhibit 6

Investment Policy April 2019

Page 13

3. Allocation The allocations to the above subcomponents of the Traditional Growth portfolio are overseen and managed by Staff. To ensure consistency with investment policy, overall regional allocations (e.g., the allocation proportion to the U.S. versus non-U.S. regions and/or developed vs. emerging markets, etc.) of the Traditional Growth portfolio will be assessed versus the commensurate proportional allocation levels exhibited within the MSCI ACWI IMI Index, the benchmark for the overall Traditional Growth portfolio. Taking these considerations into account, Staff has discretion to manage the allocation levels among the above three portfolio segments.

4. Assets may be held in Commingled Funds or privately managed Separate Accounts.

5. Use of leverage will be controlled as appropriate in the Manager’s Guidelines. 6. Implementation of the Traditional Growth portfolio is via a combination of Active

Management and Passive Management. Allocation to active and passive mandates takes market efficiency into account across and/or within the above three major Traditional Growth segments.

C. Benchmarks and Performance Targets

Benchmarks and Performance Targets for the Traditional Growth portfolio and its three subcomponents are set forth in Appendix 5. Benchmarks and Performance Targets for specific subcomponent, sector, style, and/or manager portfolios will be established to ensure consistency with both the overall Traditional Growth benchmark as well as the specific subcomponent benchmark under which the portfolio resides.

Stabilized Growth Component and Its Underlying Sub-Components

D. Role The Stabilized Growth Component is expected earn Risk-Adjusted returns in excess of the Traditional Growth Component, primarily as a result of (i) achieving absolute return levels that are near-or-equivalent to those achieved by the Traditional Growth component while also (ii) achieving lower volatility (risk) over a full investment cycle, particularly during Traditional Growth bear markets.

E. Investment Structure The Stabilized Growth component consists of three sub-components: Options Strategies, Credit, and Real Assets. The structures of these three sub-components are described below. Allocation levels to the Stabilized Growth component and its three sub-components are set forth in Appendix 4.

F. Benchmark and Performance Target Benchmarks and Performance Targets for the overall Stabilized Growth component and its three sub-components are set forth in Appendix 5.

ATTACHMENT 1 - CleanExhibit 6

Stabilized Growth Sub-Components: I. Options Strategies Structure

A. Role The Options Strategies portfolio is expected to provide similar, but higher Risk-Adjusted Returns than public equity. This expectation should be due to these strategies (i) producing compound returns that are modestly below traditional long-only public equities over a full investment cycle while (ii) also incurring significantly lower volatility than long-only public equity. In addition, Options Strategies produce a return pattern that is significantly different from traditional public equity over time – specifically, periodic outlying returns should be reduced. In summary, Options Strategies are utilized to achieve downside protection and risk mitigation to the overall SURS Portfolio (and, in particular the traditional public equity portfolio).

B. Investment Structure

1. SURS has implemented its initial Options Strategies through direct allocations to multiple managers that exhibit specific expertise in this strategy.

2. The aggregate Options Strategies portfolio consists of managers that apply a limited range of collateral-supported options selling programs (i.e., (i) writing call options associated with a specified long position in an equity index fund or long positions of specified equity securities or (ii) writing index put options associated with a commensurate level of cash or very-near-cash collateral).

3. The Options Strategies portfolio may seek to invest globally across U.S. and non-U.S. markets, replicating the general risk characteristics of industry-standard equity market indices.

4. Within the portfolio, the account structure utilized may be a blend of separate account(s) and fund(s), depending on the assigned strategy/mandate.

5. Leverage is not typically employed in Options Strategies. Any degree of leverage requires SURS Board approval.

6. Implementation of the Options Strategies portfolio is via Active Management.

C. Benchmarks and Performance Targets Benchmarks and Performance Targets for the Hedged Strategies portfolio are set forth in Appendix 5.

II. Credit Structure

A. Role The public credit portfolio is expected to provide income, yield and diversification to the total Portfolio due to a moderate correlation with other Asset Classes. In addition, the public Credit portfolio is expected to provide return, a source of Liquidity, and positive returns relative to an appropriate performance Benchmark.

ATTACHMENT 1 - CleanExhibit 6

B. Investment Structure 1. The Credit allocation consists of a diversified mix of publicly traded Credit

securities, invested across multiple asset types. o Quality standards, such as credit, concentration, duration, liquidity, etc., will be

specifically set forth in each Manager’s Guidelines, as applicable. In the event a security no longer meets the quality standards referenced above, the Manager may continue to hold such security if it believes doing so is in the best interest of SURS. The Manager shall provide written justification of the action to Staff [and Consultant] as soon as practicable.

2. The public credit portfolio is composed of Global Investment Grade, High Yield, Global Bank Loans and Emerging Market Debt (“EMD”) segments. o Global Investment Grade

Managers may invest primarily in global investment grade securities of corporation and governmental agencies.

Global Investment Grade is defined as those with a rating of at least “BBB-” or equivalent by two or more of the credit rating agencies.

o High Yield Managers are permitted to invest in high yield bonds with an

understanding that these bonds provide greater risk, potential for capital loss but with greater potential yield/return.

High Yield bonds are defined as those that are rated lower than “BBB-” by at least one of the credit rating agencies.

o Global Bank Loans Managers may invest in global bank loan debt

o EMD Managers invest in Investment Grade corporate and high yield debt

securities of emerging market countries, in both U.S. dollar and local currency terms, providing additional diversification and opportunities for higher yield.

3. Allocation o The policy targets for the subcomponents of the portfolio are set forth in

Appendix 4. 4. Assets may be held in Commingled Funds or privately managed Separate

Accounts. 5. Use of leverage and short sales will be controlled as appropriate in the Manager’s

Guidelines. 6. Implementation of the Credit portfolio is via Active Management.

C. Benchmarks and Performance Targets

Benchmarks and Performance Targets for subcomponents of the Fixed Income portfolio are set forth in Appendix 5.

III. Real Assets Structure

A. Role The Real Asset portfolio is expected to generate attractive Risk-Adjusted Returns through stable income and the opportunity for capital appreciation, while providing diversification to the overall Portfolio.

ATTACHMENT 1 - Clean

ATTACHMENT 1 - Clean

Exhibit 6

Investment Policy April 2019

Page 16

B. Investment Structure 1. The Real Asset allocation consists of Core Real Estate and Core/Core-Plus

Infrastructure.

o Core Real Estate Core Real Estate Managers typically invest in properties that are well

located and well leased with strong quality tenants. Core investments provide stable income with lower volatility.

o Core Infrastructure Funds typically invest in a variety of assets in the transportation,

power/utilities, midstream energy, ports, communications, and waste management sectors globally. Core investments should exhibit low-to-moderate levels of leverage, both income and appreciation return orientation, emphasis on return/investment stability, etc.

o Core-Plus Infrastructure Funds typically invest in a variety of assets in the transportation,

power/utilities, midstream energy, ports, communications, and waste management sectors, but may exhibit some level of sector-specific expertise or capability. Core-plus investments typically exhibit moderate levels of leverage, both income and appreciation return orientation, emphasis on return/investment stability, etc. Core-plus infrastructure may have modestly higher return expectations than core infrastructure.

2. Allocation o The minimum policy allocation for the Core Real Estate and Infrastructure

subcomponents is 50% of Real Assets component. 3. The account structure for Core Real Estate and Infrastructure is typically either

Open-end Funds or Closed-end Funds. SURS may also participate through Fund-of-Funds structures, which provide further Manager diversification and the opportunity for co-investment and secondary fund opportunities.

4. Leverage is an inherent component of Real Assets investing and levels are generally determined on a fund-level basis. Leverage levels in Real Assets are typically lower than those for Non-Core Real Assets.

5. The Real Assets portfolio is implemented via Active Management. SURS will seek to diversify the portfolio by utilizing various Managers and limiting a Manager’s concentration within the portfolio. Subject to Emerging Investment Manager and MFDB Utilization Goals and Board exception, concentration limits are set forth in Appendix 4. The optimal number of investment vehicles in the portfolio and their vintage year exposure varies with market opportunities and will be evaluated as part of the Real Assets Strategic Plan and Pacing Model developed by Staff and Consultants.

C. Benchmarks and Performance Targets Benchmarks and Performance Targets for subcomponents of the Real Assets portfolio are set forth in Appendix 5.

ATTACHMENT 1 - CleanExhibit 6

Non-Traditional Growth Component and Its Underlying Components A. Role