Message from the Director-General - Excise Department

40

Transcript of Message from the Director-General - Excise Department

Message from the Director-General “The Excise Department

has established

the excise laws consultation

service via the internet

so that the public and

industrial entrepreneurs”

0� 0�Annual Report 2009 0� 0�The Excise Department

Inthefirsthalfofthefiscalyear2009,theThaieconomyfacedwithregressionresultingfromworldwideeconomiccircumstance.Thishassubsequentlysloweddowntheexportofgoodsandservices.Nonetheless,theeconomyhadrecoveredandexpandedinthesecondhalfofthefiscalyear.Thishasled to further expansion of manufacturing industries for export; reduction of unemployment; andincreased demand for consumption. The Consumer Confidence Index had continuously improvedwhereintheConsumptionExpenditureIndexbythefiscalyearendwentupby4.5percent.Itwaspartlyaresultof theeconomicstimulationpolicy, to increase incomesandsubsidisethe livingexpensesoflowincomespopulation,togetherwiththeconsumer’sconfidenceontherecoveryoftheThaieconomy.Moreover,morestabilizedinternalpoliticalclimatehasboostedconfidenceofforeigntourists,henceanimprovement of their number. The Excise Department, therefore, managed to collect a total of THB291,221millioninexcisetaxrevenuewhichwasTHB12,909millionor4.64percenthigherthanthatofthe fiscalyear2008.TheExciseDepartment, in the fiscalyear2009,alsohadengaged innumerousactivitiessuchas:

The tax collection efficiency enhancement for financial stability, via the following measurements1) increase in beer and spirit tax rate; 2) increase in tax rate ceiling and actual for tobacco andcigarette;and3)increaseinfueltaxrateceiling,allofwhichenabledtheExciseDepartmenttocollectmoreexcisetaxatanaverageofTHB27,126permonth.Additionally,theDepartmentalsoexpeditedthesuppressionofexcisetaxoffenses.

Onthepromotionofbusinesssectorandindividuals,theExciseDepartmentexemptedexcisetaxonair-conditioningunitsforusewithinofficeandresidentialbuilding;exemptedexcisetaxforbathingor saunaandmassage forbeautysalonandhealthcarecentrebusiness;and issued theMinisterialAnnouncementonthecharacteristicsofpassengervehiclesproducedfrompick-uptruck,allofwhichhelped elevate cost burden of business sector and individuals and were in line with the economicstimulationpolicy.

Ontheservice front, theExciseDepartmenthasestablishedtheexcise lawsconsultationserviceviatheinternetsothatthepublicandindustrialentrepreneurscanclarifytheirquerieswithoutvisitingthe Department in person. The Department also introduced the ‘Smart Office’ concept deployingmodern technology to facilitate public service. The concert is to be piloted at the Bangkok Area 3Excise Office and will be expanded to other regional offices to ensure maximum satisfaction ofcustomers.

Onthehumanresourcedevelopmentaspect,theExciseDepartmenthasintroducedthe“S-M-I-L-E”value to all offices via public relations/publicize/communication activities, coupled with training andseminar-cum-workshoptoingrainsuchvaluewithanaimtowardsbecominganexcellentorganisationwithchangemanagementplanimplementation.

Onlawdevelopmentandrestructuring,theExciseDepartmenthasengagedinthedevelopmentoflaws toempower localadministrativeagencieswithadegreeofautonomyand increasedexcise taxcollectingability.TheDepartmentalsopublishedmanualentailingdetailsonapplication forpermit tosellspirit,tobaccoandplayingcardsforgeneralpublictoeducatethemontheproceduresaswellasmanualonworkingproceduresforthedepartmentalstafftoensureaccuracyandstandardtreatment.

On social responsibility, the Excise Department has implemented the CSR (Corporate SocialResponsibility) concept, initially designed for private sector. In line with that, the “FAMILY DAY SAYNO”wasorganisedtopromotepubliccollaborationtosuppressdangerfromillegalcigaretteandspirit,duringMarch31toJune30,2009.Theactivitywastosupportthegovernment’sinitiativetoreducetheconsumptionofspiritandcigarette,particularlyillegaloneswhichposemorehealthhazard.Thesaidactivitywascarriedoutcontinuouslycoveringallareasofthecountry.

In the fiscal year 2009, the Excise Department has worked under the continuous economicfluctuation circumstance which required the Department to be alert and responsive to such ever-changingenvironment.However, theDepartmenthasnotonly realised itsmission in taxcollection tomeetthegovernmentaltargetundertheconceptoftransparency,justandfairnessfortax-payersandwith efficiency, but also has placed importance on its responsibility to society and the environment.These practices and principles must be developed simultaneously to ensure a balance in countrydevelopment.

Dr. Areepong Bhoocha-oom Director-General

The Excise Department

0� 0�Annual Report 2009 0� 0�The Excise Department

Vision

DepartmentforThrivingEconomy,BetterSociety,andImprovedEnvironment.

Missions

1. Toincreaseefficiencyintaxcollectiontoensurethenation’sfinancialstability.

2.Towidenexcisetaxbasistoelevatesocialqualityandenergysaving.

Strategies

1.Todeveloptaxcollectionmanagementandtoincreaseprevention/suppressionefficiencytoensure

fiscalsustainability.

2.Toconductservicequalitysystembyappropriatetechnologyresponsivetomaximumpublicsatisfaction.

3.Toincreasehumanresourcecapacityandtomodernizeorganizationalculture.

4.Toimprovelawsandredesignorganizationalstructuretoincreaseoperationalefficiency.

Objectives

1.Toincreaseexcisetaxrevenue.

2.Towidenexcisetaxbasis.

3.Toincreaseefficiencyinpreventionandsuppression.

4.Toimproveservicequalitytointernationalstandard.

5.Toapplytechnologyandinnovationappropriatefortheservices.

6.Toimprovehumanresourcecapacityresponsivetothedepartmentaltasks.

7.Toestablishorganizationalcultureadaptivetochanges.

8.Toimprovelawsandregulationsaccommodatingtotheorganizationaloperation.

9.Torestructurethedepartmenttoaccommodatechanges.

Strategic Plan for the Fiscal Year 2009

0� 0�Annual Report 2009 0� 0�The Excise Department

The Excise Department’s Strategic Plan for the Fiscal Year 2009

TheExciseDepartmenthasdrawnupplans/projectsunder thedirectionto improvetaxcollectionefficiencywhichcanbecategorizedbystrategyasfollow:

Strategy 1 To develop tax collection management and to increase prevention/suppressionefficiencytoensurefiscalsustainability

1. OrganizationalRiskManagementPlan. 2. PreventionandSuppressionofExciseTaxEvasionPlan. 3. FieldAuditPlan. 4. OperationalVisittoincreaseTaxCollectionEfficiencyPlan. 5. LocalLiquorTaxCollectionControlPlan.

Strategy 2 Toconductservicequalitysystembyappropriatetechnologyresponsivetomaximumpublicsatisfaction.

1. DevelopmentandDeploymentofSmartOfficeSystemPlan. 2. DataExchangeandPerformancesImprovementforCoreApplicationPlan.

Strategy 3 Toincreasehumanresourcecapacityandtomodernizeorganizationalculture.

1. ParadigmShiftPlan. 2. TaxAuditor,ExciseAuditorandExciseInspectorDevelopmentPlan.

Strategy 4 To improve laws and redesign organizational structure to increaseoperationalefficiency.

- ExciseLawsDevelopmentinaccordancewithGoodGovernancePlan.

0� 0�Annual Report 2009 0� 0�The Excise Department

Excise Department Performance Results

Strategy 1: to develop tax collection management and to increase prevention/suppression efficiency to ensure fiscal sustainability

• Implementation Guideline 1 - Amount of Excise Tax Collected

TheExciseDepartmentcollectedatotalofTHB291,221millionagainstatargetofTHB 322,640 million, thus a sum of THB 31,419 million or 9.74 percent below target.Thiswasdue to theCabinet’s resolutiononJuly15,2008 introducing theSix (6)ReliefMeasuresforSix(6)MonthsthroughFinancialCrisis.Accordingly,theExciseDepartmentissuedtheMinistryofFinanceAnnouncementonReductionofExciseTaxRate(Issue2)dated July 23, 2008, effective from July 25, 2008 to January31, 2009.Resultantly, theexcisetaxongasoholwasreducedfromTHB3.3165/litretoTHB0.0165/litre;dieselwithsulphurnotexceeding25percentfromTHB2.305/litretoTHB0.005/litre;andbio-dieselfromTHB2.1898/litretoTHB0.0898/litre.

• Implementation Guideline 2 - Monitoring, Prevention and Prosecution

of Excise Tax Offenders

The Excise Department was able to prosecute a total of 42,608 cases of taxviolationagainsta targetof28,633case, thusasumof13,975casesor48.80percentabovethetarget.ThetotalofTHB378,878,912finewasreceivedcomparedtothetargetofTHB221,723,130,thusasumofTHB157,155,782or70.88percentabovethetarget.

• Implementation Guideline 3 - Efficiency Improvement Measure

TheExciseDepartmenthasissuedthefollowinglawsandregulations:

1. AmendmentRoyalOrdinanceB.E.2552ontheTobaccoActB.E.2509(Issue2),datedMay13,2009inthe64thyearundertheReignofKingRamaIX(MeasuretoRaiseCeilingTaxRateonTobaccoandCigarette).

WitheffecttocancelthetextinItemandRatecolumnsno13oftheTobaccoDutyandStampList(Issue7)B.E.2535andreplacewiththefollowing:

Thetobaccostampfortobaccoandcigaretteisatarateof90advaloremorTHB3pergramme,partialconsideredasawhole.

0� 0�Annual Report 2009 0� 0�The Excise Department

2. MinisterialRegulationonTobaccoStampRateB.E.2552datedJuly13,2009(MeasurestoRaiseCeilingTaxRateonTobaccoandCigarette)

1) Tobacco - 0.1 ad valorem or THB 0.01 per 10 gramme, partial thereof consideredaswhole.

2) Cigarette 2.1)Cigarette-85advalorem; 2.2) Cigar - 10 ad valorem or THB 0.50 per gramme, partial thereof consideredaswhole; 2.3) Othercigarette-0.1advaloremorTHB0.02perfivegramme,partial thereofconsideredaswhole; 2.4)Favouredtobacco-10advaloremorTHB0.02pergramme,partial thereofconsideredaswhole;and 2.5) Chewingtobacco-0.1advaloremorTHB0.09pergramme,partial thereofconsideredaswhole.

3. MinisterialRegulationonLiquorTypesandLiquorTaxRate(Issue4)B.E.2552datedMay6,2009(MeasuretoRaiseLiquorTaxRate)raisingthefollowingtaxrate:

Beerfrom55advaloremto60advalorem; WhiteSpiritfromTHB110perlitreofethanol(purealcohol)toTHB120; BlendedSpiritfromTHB280perlitreofethanoltoTHB300;and Brandyfrom45advaloremto48.

4.AmendmentRoyalOrdinanceB.E.2552ontheExciseTaxRateActB.E.2527(Issue7)andtheMinisterialAnnouncementonExciseTaxRateReductionandExemption(Issue85)datedMay13,2009(Measures toRaiseCeilingTaxRate,ExciseTaxRateReductionandExemption).

Witheffecttoraisetheceilingoftaxrateaccordingtopetroleumconditionandproducttypeandexcisetaxratereductionandexemption(Issue85).

5. Ministerial Announcement on Excise Tax Rate Reduction and Exemption(Issue86)onSeptember2,2009(MeasurestoExemptExciseTaxonAir-Condition).

Witheffect toexempt theexcisetaxonair-conditionunit forusewithinofficeandresidentialbuildingswithcapacitynotexceeding72,000BTU/hourwhiletheexcisetaxof vehicleair-conditioning unit with capacity not exceeding 72,000 BTU/hour is stilledcollectedatarateof15%advalorem.

6. Departmental Announcement on Terms and Conditions of Excise TaxExemptionforBathingBusinessorSaunaandMassageinBeautySalonorHealthCentreonOctober19,2009 (Measures toExemptExciseTaxonBathingBusinessorSaunaandMassageinBeautySalonorHealthCentre).

0� 0�Annual Report 2009 0� 0�The Excise Department

TheAnnouncementstipulatedthatabathingbusinessorsaunaandmassageinbeautysalonorhealthcentreawardedwithcertificationincompliancewiththeMinistryofPublicHealthAnnouncementonSpecificationofLocationforHealthCentreandBeautySalon;BusinessPlaceandServicingPersonnelStandards;RegulationsandExaminationGuidelinesforCertificationAwardinaccordingtothestandardofbeautysalonorhealthcentreundertheBusinessPlaceActB.E.2509orcertifiedsobythesaidAnnouncementis entitled to excise tax exemption on the incomes received from providing bathing orsaunaandmessageservicewithhealthserviceprovidersthroughoutaperiodunderthecertificationorbeingcertifiedaspassingthestandardtodoso.

7. MinisterialAnnouncementonSpecificationofAutomobileProducedfromPick-upTruckorChassiswithWindshieldofPick-upTruckorModifiedfromPick-upTruck(Issue2)onAugust20,2009.

TheAnnouncementstipulatedthatthewheelbasedistance,bothleftandright,mustnotdifferfromthemodelcodeandchassismodelofsuchparticularvehiclemodelwith the exception for modification of paramedic utility vehicle, communication utilityvehicle, other multi-utility vehicle and limousine of which the wheelbase could belengthenedfromwhatisspecifiedbythemodelcodeandchassismodel.

8. Ministerial Announcement on Excise Tax Rate Reduction (Issue 84) datedJanuary30,2009toincreasefueltax.

Strategy 2: To develop service excellence by appropriate technology responsive to maximum public satisfaction

• Implementation Guideline 1 – Information Technology System

Development

The Excise Department has established the Excise Laws Consultation Service(ELCS) System on the internet to increase accessibility of the general public andentrepreneurs who could clarity their queries at home or office without making officialinquiryorvisittheExciseDepartmentpersonally.Thesaidservicewouldassisttaxpayersto correctly make their tax payment, increase customer’s satisfaction and fairness forthoseconcernedwithexcisetax.

The excise tax laws consist of seven (7) acts namely the Excise Tax Act B.E.2527;theLiquorActB.E.2493;theTobaccoActB.E.2509;theExciseTaxRateAct2527;theExciseTaxIncomesAllocationActB.E.2527;andtheLiquorTaxIncomesAllocationB.E.2527andadditionalMinisterialRulesandRegulationsaswellasExciseDepartmentOrders.

0� 0�Annual Report 2009 0� 0�The Excise Department

• Implementation Guideline 2 – Development and Implementation of

Smart Office System

TheExciseDepartmenthasselected“BangkokAreaExciseOffice”asapilotingoffice for the development and implementation of the smart office system consisting ofthree(3)systematicaspectsnamely:

- Hardwarewithemphasisonfrontofficewithlessofficersandenergysaving; - Softwarewithemphasisonlessornonepaperformwhichisreplacedbycitizen IDcard; - Peoplewarewithemphasisonmodernizedworkforce,impressiveserviceunder theS-M-I-L-Evalue.

Strategy 3: To increase human resource capacity and to modernize organisational culture

• Implementation Guideline 1 – Modify Paradigm and Value of

Workforce towards Modernized Organisation

The Excise Department has introduced the S-M-I-L-E value into all offices viapublic relations/publicize/communicationactivities, coupled with training and seminar-cum-workshop to ingrain such value with an aim towards becoming an excellentorganisationwithinchangemanagementplanplementation.

Strategy 4: To Develop Laws and Organisational Restructure to Increase Operational Efficiency

• Implementation Guideline 1 – Laws Development Plan Execution

The Excise Department has executed the laws development plan following theCabinet’s resolution inwhich in the fiscalyear2009 the issuanceof liquorand tobaccosalepermitswas transferred to the localauthority.Suchpracticewas inaccordance totheGovernment’spolicytopromotedecentralisationoffinancialauthoritytoincreasethecapacityandautonomyoflocaladministrativeagencytothatofself-reliancelevel.Thelawswasamendedinsuchawaytosupportlocalauthority’sresponsebilityincollectingfee.

• Implementation Guideline 2 – Pubic Sector Management Quality

Development

The Excise Department has executed two (2) organisational development plansoutof thecompulsoryplans forservicingdepartmentsnamelyClause3: ImportanceonCustomerandStakeholderandClause6:WorkFlowOrganisation.

0� 0�Annual Report 2009 0� 0�The Excise Department

UnderClause3: ImportanceonCustomerandStakeholder, theExciseDepartmenthasproduced “Public Manual” entailed procedure on applying for permit to sell liquor,tobaccoandplayingcardaswellas their rightsasperstipulated in theExciseTaxActB.E. 2527 along with “Official Manual”. Additionally, the satisfaction survey wasconductedcoveringthefollowing:

- customer'sandstakeholder'ssatisfactiononself-learningchannels; - satisfaction on community relationship performance covering such activities as community education; monetary donation for juvenile equipment and public participationinactivitiesorganisedbytheExciseDepartment;and - customer'ssatisfactiononimprovedserviceproceduresandservices;

UnderClause6,theExciseDepartmenthasproducedmanualofindividualworkprocessandtraininginaccordancetothosemanualwhichwereasfollow:

(1)ValueCreatingProcessconsistingofthefollowingseven(7)procedures:

1. Tax Collection Management Procedure such as existence of manual on tax refund,exemptionandrelaxationinaccordancewiththeExciseTaxActB.E.2527; 2. PermitIssuanceProceduresuchasexistenceofmanualonliquorsalepermit issuanceprocedureforType1-7; 3. TaxMechanismStandardDevelopmentProceduresuchasexistenceofmanual onoperation,suppressionandexcisetaxbasisexpansionprocedures; 4. TaxAuditingProceduresuchasexistenceofmanualonexcisetaxaudit; 5. SuppressionandProsecutionofTaxOffenderProceduresuchasexistenceof manualonpreventionandsuppressionoperation; 6. ProductsandConfiscatedObjectExaminationProceduresuchasexistenceof manualonexaminationserviceonbeverage,liquor,petroleumandpetroleum products;and 7. Technical Examination for Tax Collection Procedure such as existence of manualoninstallationofflowmeter.

(2)SupportingProcessconsistingofthefollowingfour(4)procedures:

1. Human Resource Management Procedure such as existence of manual on individualassessmentintheselectionprocesstofulfillacademicposition; 2. Financial Management Procedure such as existence of manual on GFMIS operation; 3. InformationTechnologyManagementProceduresuchasexistenceofmanual oninformationtechnologymanagement;and 4. PublicRelationsMediaProductionProceduresuchaspublicationofnewsvia massmedia.

010 011Annual Report 2009 010 011The Excise Department

Type(Case)

TypeofFine

FineTotalFine

NumberofCases CourtFine Fines

NoOffender

LiquorActB.E.2493 27,617 97,895,315.56 4,754,426.00 558,176.68 103,207,918.24TobaccoActB.E.2509 12,796 214,922,029.42 171,710,927.55 23,454,696.25 410,087,653.22exciseTaxActB.E.2486 45 1,514,251.36 37,664.00 1,551,915.36exciseTaxActB.E.2527 2,461 64,753,423.06 10,745.00 - 64,764,168.06

Total 42,919 377,570,768.04 177,990,349.91 24,050,536.93 579,611,654.88

Office ClosedCase(Case)

TaxEstimation(Case)

Total(Case)

Amount(THB)

Central 40 59 99 93,148,719.65

Regional 33 59 92 7,095,583.62

TotalNationwide 73 118 191 100,244,303.27

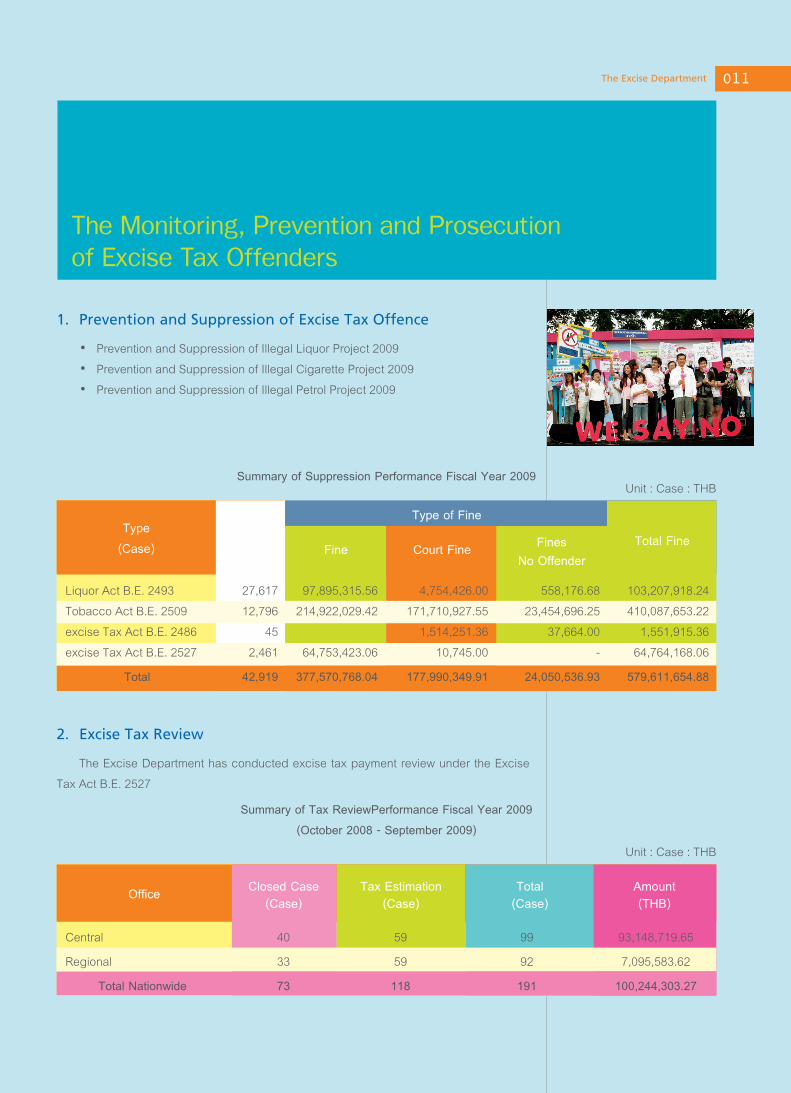

The Monitoring, Prevention and Prosecution of Excise Tax Offenders

1. Prevention and Suppression of Excise Tax Offence

• PreventionandSuppressionofIllegalLiquorProject2009 • PreventionandSuppressionofIllegalCigaretteProject2009 • PreventionandSuppressionofIllegalPetrolProject2009

SummaryofSuppressionPerformanceFiscalYear2009Unit:Case:THB

2. Excise Tax Review

TheExciseDepartmenthasconductedexcisetaxpaymentreviewundertheExciseTaxActB.E.2527

SummaryofTaxReviewPerformanceFiscalYear2009(October2008-September2009)

Unit:Case:THB

010 011Annual Report 2009 010 011The Excise Department

Amount(Case)

ImpoundedEvidentNumberOfOffender

(Person)Methamphetamine

(Pill)

Ecstasy(“E”)(Pill)

K-tamine(Bottle)

CrystalMethamphetamine

(“Ice”)(Gramme)

Heroin(Gramme)

Marijuana

Fresh(Gramme) Dried(Gramme)

23 33 6,044.00 - 20 0.6 - 7,000 -

3. Narcotic Suppression

SummaryofNarcoticSuppressionPerformanceFiscalYear2009

Source:BureauofAudit,PreventandSuppress

Excise Tax Offence Suppression Performance Fiscal Year 2009

Source:BureauofAudit,PreventandSuppress

01� 01�Annual Report 2009 01� 01�The Excise Department

Human Resource Management System Development

• Human Resource Management System Development by HR Scorecard

TheExciseDepartmenthas implemented thehumanresourcemanagementsystemfollowingtheHRScorecardframeworkinaccordancewithitscommitmentgivenwiththeOffice of Public Sector Development Commission (OPDC) for the fiscal year 2007.Consequently, the Department has drawn up the Human Resource DevelopmentStrategic Plan, 2008 - 2010 and has been selected as one from 10 organizations toquotedas“PublicSectorwithGoodPracticeonHumanResourceDevelopmentStrategicPlanExercise”.

The Human Resource Management System by HR Scorecard is coupled with theDepartment’s strategies on human resource development which indicated significanttargetandactivities todevelophumanresourcewithefficiencyandethics; tocreateanorganizational knowledge management to promote individual’s capacity and theDepartment as ‘Learning Organization’. The core objective of the practice was for theDepartmenttobecomeamodernizedorganizationwithworkingstandardincompliancewithgoodgovernanceideology.

Finally, TheHumanResourceManagementDivisionhasdrawnup thecorehumanresourceprojects/activitiesforthefiscalyear2009inthefollowingfive(5)dimensions:

Dimension 1: Strategic Compliance with strategic objectives to promote theacceptance of the SMILE value to become an on-going organizational culture; and toincreaseprominentcareerpathsinvariousdisciplines.

Dimension 2: Human Resource Management Efficiency with strategic objectiveto develop work systems along with personnel’s knowledge on such system to ensureefficiency,standardandtransparency.

Dimension 3: Human Resource Management Effectiveness with strategicobjective to pilot the Individual Development Plan (IDP) leading to develop workforcecapacityinaccordancetotheirworkline.

Dimension 4: Human Resource Management Accountability with strategicobjective to encourage good governance in the selection process concretely andtransparently.

01� 01�Annual Report 2009 01� 01�The Excise Department

Dimension 5: Quality of Life and Balanced Personal and Professional Life withstrategicobjective toprovideadditionalwelfare fromstatutoryprovisionand to improveworkingenvironment.

• Knowledge Management: KM

TheExciseDepartmenthasengagedinknowledgemanagementactivitiestosupportitsstrategies.Thefour(4)bodyofknowledgeidentifiedwere-KnowledgeonPetroleumProduct-HydrocarbonSolvent;KnowledgeonTaxPaymentbyInternetforEntrepreneurs;KnowledgeonIncomesDataLinkagewithGFMISSystemvia Interface;andKnowledgeonCriticalStudyontheDraftonAmendmentof theExciseTaxAuditB.E.2527andtheNew Forms. The experts in both tacit and explicit knowledge, both internally andexternally,wereinvitedtoconductthelearningsessionstoensureaccuracyandsharingof knowledge. The practice aimed to pursue excellence in the operation of the ExciseDepartment.Interestedindividualscanalsoseefurtherathttp://km.excise.go.th.

• Performance Management System: PMS

The Excise Department has prepared its readiness to adopt the PerformanceManagement System (PMS), specified by OPDC, which relied on two followingcomponents:

1) Work Accomplishment - with key performance indicators (KPK.) and targets of publicsectorwork,weightingatleast70percent.

2) WorkingCapability-followingtheframeworkidentifiedbyOPDC.

The system was applied for the performance appraisal starting from October 1st,2009onwardsandusedasbasisforsalaryraiseonApril1st,2009.Withinthepastyear,the Human Resource Management Division has selected Regional Excise Office atAyudhaya1,SupanburiandAng-thongprovincialofficesaspilotingareas for individualKPIpractice.Furthermore,aseminar-cum-workshoponIndividualKPIsforcentralofficesandanexplanatorymeetingonKPIs for headsofdivisions/bureauswereorganizedbycollaboration from the OPDC consultant agency. The Human Resource ManagementDivision has also compiled and made available KPIs of all offices together withperformance appraisal details and related rules, regulations and memos at http://hrm.excise.go.th.

01� 01�Annual Report 2009 01� 01�The Excise Department

by

Dr.Kontee Nuchsuwan

Economist, Fiscal Policy Office, Ministry of Finance Thailand

Introduction

Fordevelopinganddevelopedcountriesalike,theglobalizationoffreetradedoctrinehas played a major role in today international trade. For small-open economy likeThailand,suchfreertradepoliciesleadtoastreamlineofcountry’stariffstructures,whichresults inamajor reductionofoverall tax revenue.Asa result, the reformof theexcisetax, at least in the short run, has received vigorous attention in Thailand as “revenueneutralization”mechanism.Atthesametime,theexcisetaxesalsohavesomeadditionalobjectives such as discouraging consumption of immoral goods and reflecting theexternalitycostasameanstocollecttheenvironmentaltax.Thus,ourresearchquestioniswhat is theoptimaldirectionsofexcise taxesdesign forThailand thatstrike the rightbalancebetweenrevenuemaximizingandwelfaremaximizingobjectives.

This paper uses the Marginal Tax Reform model pioneered by Ahmad and Stern(1984: AS Model) that explores the directions of optimal tax reform at the margin.TheMarginalTaxReformModeluses themeasurementcalled theMarginalSocialCost(MSC) of raising revenue via an increase in the tax on a specific good, which can beexpressedastheratioofmarginalchangeinwelfaretothemarginalchangeinrevenue.Toreachtheoptimalitycondition,theMSCofeachcommoditymustbeequalbecauseatthispoint it reaches theParetooptimalitywhen there is no possibility of furtherwelfareimprovementwith taxadjustment. If theMSCarenotequal, themodelcansuggest thedirectionoftheoptimaltaxreform.

Thecommodity taxreformstudiesarenotnew.Themethodologyhasbeenusedinmanycountries includedAhmadandStern (1984)on India,Madden (1995)on Ireland,Madden (1996) on UK, Ray (1999) for Australia. For Thailand, however, there is noliterature using the Marginal Tax Reform model. The closest approach comes from astudybySarntisartI,etal(2002)thatsuggeststhedirectionofthetaxlevelthatreflectscost of externality (Pigouvian Tax). Their study focuses on a single commodity (theTobacco industry) rather than the comparison of the different commodities that the ASmodelallowed.Thus,ourmaincontributionsarenotonlylookatmultiplecommoditiesatthesametime,butthispaperalsoprovidesthedirectionofwelfareimprovingtaxreform.

Optimal Excise Tax from Theory to Practice: A Case Study of Sin Related Products

01� 01�Annual Report 2009 01� 01�The Excise Department

Thispaperisorganizedasfollows.Insection2,wepresentourMarginalTaxReformmodel.Insection3,wedescribethedataanditsconstruction.Section4willpresentthecountryexcisetaxstructureonsin-relatedproducts. Insection5,weexplaintheresultsfromourASmodel.Then,wepresentourconclusion.

1. The Marginal Tax Reform Model (The Ahmad-Stern model)

Thetraditionaloptimaltaxapproachattemptstoderivethetaxratesthatminimizethewelfare loss for the collection of given revenue. This may be appealing from thetheoretical point of view but it requires quite severe information on the explicit utilityfunction and the distribution of income. In additions, the demand responses at theindividualhouseholdmustbeevaluated,whichareusuallyverydifferentfromthecurrentpositionof the economy. Thus, the calculationof optimal tax rates using the traditionalapproaches may compromise the relevance of the optimal tax design with our policyimplication.

Unlike the traditionaloptimal taxapproachthat tries toderive taxrate thatminimizedeadweight loss, the marginal tax reform approach, pioneered by Ahmad and Stern(1984),takestheexistingtaxrateasgivenandidentifiesthedirectionoftaxreformatthemargin.ThemarginaltaxapproachusesameasurethattheycalledtheMarginalSocialCost (MSC)of raising revenue through tax increased.TheMSC is the ratioofawelfareeffecttoarevenueeffect.

Most importantly, the optimality condition requires the MSC to be identical for allgoods,otherwiseaParetoimprovementcouldbeimplementedbyloweringthetaxonthegoodwithhighermarginalcost,andbyraising the taxon thegoodwith lowermarginalcost.

Model Specification

On theproductionside,pricesare fixed,andall firmsexhibit theconstant return toscaleinproduction.Theseassumptionsimplythatthechangeinindirecttaxwillreflectintheconsumerprice.Wecanwritetheconsumerpricevectorastheproducerpricevectorplusthevectorofspecifictaxespricevectorasq=p+t.First,eachhouseholdh,theconsumption bundle that maximizes utilityuh (xh) subject the corresponding budgetconstraint can be denoted as xh (q‚mh). Such consumption bundle will lead to theassociateindirectutilityfunction,whichcanexpressasvh (q, mh)Byassumption,thereis a social welfare function W (u1‚...‚uH) that can be rewritten in terms of pricesandincomesas:

01� 01�Annual Report 2009 01� 01�The Excise Department

V (q‚m1‚...‚mH) = W (v1(q‚m1)‚..., vH (q‚mH)) (1)

The aggregate demand vector is given by X (q‚m1‚...‚mh) = Σ xh (q‚mh) andgovernmenttaxrevenueisgivenby

R =Σ ti Xi (2)

Now,suppose that theexcise taxofgood i is tobe increasedat themargin.Given theequation(1)and(2),themarginalsocialcost(MSC)oftaxincreasecanbedefinedasthecorrespondingmarginaldecreaseinsocialwelfarerelativetothecorrespondingincreaseingovernmentrevenue.

(3)

Theinsertionofnegativesignin(3)intendstomakethesignofMSCtobepositive.Thereasonisthattheimpactoftaxonwelfare( )usuallycarriesapositiverelationship,whiletherelationshipbetweentaxandrevenue()tendstobepositive.

Weknowthatwemayrewriteλiandexpressintheelasticitytermsas

(4)

From(4),qicanbedefinedasretailpriceofgoodI(inclusiveoftax).τkistheproportionof the tax relative to price And, is the cross-price elasticity of theaggregateddemandforgoodkwithrespecttopricei.

In addition,we interpret that each βh provides informationon thewelfareweight.Households are assumed to have ordered according to their ascending income totalexpenditures. Thus, the welfare weight for household h is given byβh = m1 ewhere e indicates the parameter of inequality aversion. As e is increased, the relativeweightofthepooresthouseholdrise.

2. Data

From the model derived in the previous section, we need the data on householdexpenditure of goods i, retail price, tax rate, and the estimation of aggregate demandresponse (cross-price elasticities). This study aggregated the consumption goods into4 categories: tobacco, alcohol, gambling, and other goods. The expenditure data iscalculated from the Household Socio Economic Survey (SES) 2000 from NationalStatistics Office (NSO), which divided households into 10 separate income groups

01� 01�Annual Report 2009 01� 01�The Excise Department

e=0 e=1 e=2

Alcohol 1.087 0.260 0.069

Tobacco 0.892 0.333 0.147

Gambling 1.484 0.262 0.0528

Others(nonsin-relatedgoods) 2.821 0.406 0.0724

Mean 1.571 0.315 0.085

Products DegreeofInequalityAversion

accordingtotheincomelevel.Itisassumedthatinthisstudytheexpenditureproportionsbetweeneachgoodarethesamein2000asin2003.

The estimation of price and demand responses, both own-price elasticity andcross-priceelasticity,come fromSarntisart I,KaluntakaphanN,andChuensukkasemkulK.(2002).

3. Results

By applying above data in to equation (4), we obtain the marginal social cost ofraising 1 unit of tax revenue across 4 commodities and across different degree ofinequality.Theresultscanbesummarizedasreportedintable1.

Table1MarginalSocialWelfareCostof2003taxstructure

AssumingthatThaigovernmentchoosesthetaxreformpoliciesthatminimizesocialwelfare cost. When there is no special concern regarding the poor (e=0), our resultssuggest that Thai government should increase the excise tax on tobacco since themarginalsocialcostofincreasingtaxisthelowest.Theresultsalsoimplythattheoverallindirecttaxfornon-sinrelatedproductsshouldbelowertoreachtheoptimaltaxlevel.

Once the government concerns more about the poor, as reflected in high welfareweightforthepoor(e=1),thealcoholandgamblingbecomesthebestandsecondbestoption to increase tax respectively. Interestingly, when government put even higherwelfareweight for thepoor (e=2), themarginal socialcostsuggests thegovernment toincreasetaxonalcoholinsteadofcigaretteasanoptimaltaxdirectionthatcanminimizethewelfarecost.Ourmodelconsistentlyprovidesaclearmessagethatregardlessofthewelfareweighttothepoorthemodelindicatesthereductionofexcisetaxesonallothergoodsisadesirabledirectiontogainthetaxoptimalityintermsofsocialwelfare.

01� 01�Annual Report 2009 01� 01�The Excise Department

4. Conclusion

The design of appropriate tax reform is inevitable for Thailand. The optimal taxapproach via the Marginal Tax Reform Model (AS model) seems to be the mostappropriatechoiceofinstrumentsincetheimplicationsofthemodelaremuchinrelevantto the realworldapplication.Our results suggest that the2003excise tax structureonsin-related products is not optimal. It is recommended that the optimal direction of taxreform should be toward lowering excise tariffs on tobacco and alcohol respectively.Moreover, the choice of commodities is sensitive to the welfare weight. As welfarefunctionfocusingmoreonthepoor,thegamblingseemstobethefirstchoicefortaxrateincreaseandalcoholcomescloselythesecond.

01� 01�Annual Report 2009 01� 01�The Excise Department

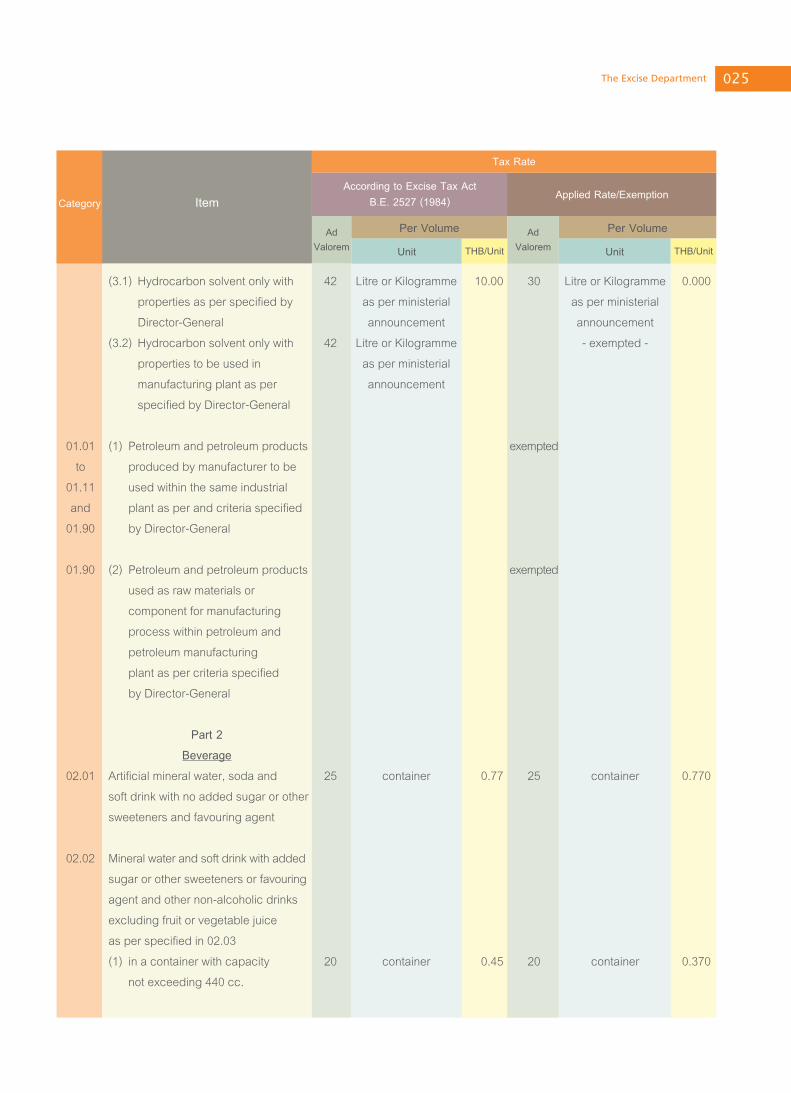

Excise

Tax Rate

0�0 0�1Annual Report 2009 0�0 0�1The Excise Department

TaxRate

AccordingtoExciseTaxActB.E.2527(1984)

Unit THB/Unit

PerVolumeAdValorem

Category Item

Unit

PerVolumeAdValorem THB/Unit

AppliedRate/Exemption

Asof29October2009

Part1 PetroleumandPetroleumProducts 01.01 -GasolineandSimilarProducts (1) UnleadedGasoline 42 Litre,partialthereof 10.00 0 Litre,partialthereof 7.000 consideredaswhole consideredaswhole (2) Gasolineotherthan(1) 42 Litre,partialthereof 10.00 0 Litre,partialthereof 7.000 consideredaswhole consideredaswhole (3) UnleadedGasolinesoldto 42 Litre,partialthereof 10.00 -exempted- privilegedindividualasper consideredaswhole criteriaspecifiedbyMinister (4) E10Gasohol 42 Litre,partialthereof 10.00 0 Litre,partialthereof 6.300 aspercriteriaspecifiedbyMinister consideredaswhole consideredaswhole (5) E20Gasohol 42 Litre,partialthereof 10.00 0 Litre,partialthereof 5.600 aspercriteriaspecifiedbyMinister consideredaswhole consideredaswhole (6) E85Gasohol 42 Litre,partialthereof 10.00 0 Litre,partialthereof 1.050 aspercriteriaspecifiedbyMinister consideredaswhole consideredaswhole 01.02 Naphtareformate,Pyrolysis,Gasoline 42 Litre,partialthereof 10.00 36 Litre,partialthereof 7.000 andotherfluidswithsimilarproperties consideredaswhole consideredaswhole 01.03 KeroseneandSimilarLightingOil 34 Litre,partialthereof 4.00 0 Litre,partialthereof 3.055 consideredaswhole consideredaswhole 01.04 FueloilforJetPlane (1) Fuelforjetplanenotusedfor 34 Litre,partialthereof 4.00 23 Litre,partialthereof 3.000 anaircraft consideredaswhole consideredaswhole (2)Fuelforjetplaneusedfordomestic 34 Litre,partialthereof 4.00 1 Litre,partialthereof 0.200 aircraftaspercriteriaspecified consideredaswhole consideredaswhole byDirector-General (3)Fuelforjetplaneusedfor 34 Litre,partialthereof 4.00 -exempted- outboundaircraftaspercriteria consideredaswhole specifiedbyDirector-General

0�0 0�1Annual Report 2009 0�0 0�1The Excise Department

TaxRate

AccordingtoExciseTaxActB.E.2527(1984)

Unit THB/Unit

PerVolumeAdValorem

Category Item

Unit

PerVolumeAdValorem THB/Unit

AppliedRate/Exemption

01.05 DieselandSimilarProducts (1)Dieselwithsulphuriccontent 34 Litre,partialthereof 10.00 0 Litre,partialthereof 5.310 exceeding0.25percentbyweight consideredaswhole consideredaswhole (2)Dieselwithsulphuriccontent 34 Litre,partialthereof 10.00 0 Litre,partialthereof 5.310 notexceeding0.25percent consideredaswhole consideredaswhole byweight (3)Dieselsoldwithinseaboundary 34 Litre,partialthereof 10.00 -exempted- oftheKingdomaspercriteria consideredaswhole specifiedbyDirector-General (4)Dieselrefilledwithinseaboundary 34 Litre,partialthereof 10.00 -exempted- oftheKingdombyvesselregistered consideredaswhole undertheThaiVesselActB.E. 2481andremainedintankwhen returningintotheKingdom (5)DieselwithMethylEatersbio-diesel 34 Litre,partialthereof 10.00 0 Litre,partialthereof 5.040 notlessthan4percentasper consideredaswhole consideredaswhole termsandcondition specifiedbytheCabinet 01.06 NaturalGasLiquid(N.G.L)and similarproducts (1) NaturalGasLiquid(N.G.L) 42 Litre,partialthereof 10.00 36 Litre,partialthereof 5.310 andsimilarproducts consideredaswhole consideredaswhole (2)NaturalGasLiquid(N.G.L) 42 Litre,partialthereof 10.00 -exempted- andsimilarproductstobeused consideredaswhole inrefiningprocessofarefinery 01.07 LiquidPetroleumGas(L.P.G), Propaneandsimilarproducts (1) LiquidPetroleumGas(L.P.G), 34 Kilogramme, 9.00 0 Kilogramme, 2.170 Propaneandsimilarproducts partialthereof partialthereof consideredaswhole consideredaswhole (2) LiquidPropaneandsimilar 34 Kilogramme, 9.00 23 Kilogramme, 2.170 products partialthereof partialthereof consideredaswhole consideredaswhole

0�� 0��Annual Report 2009 0�� 0��The Excise Department

TaxRate

AccordingtoExciseTaxActB.E.2527(1984)

Unit THB/Unit

PerVolumeAdValorem

Category Item

Unit

PerVolumeAdValorem THB/Unit

AppliedRate/Exemption

(3) LiquidPetroleumGas(L.P.G) 34 Kilogramme, 9.00 -exempted- Propane,andsimilarproducts partialthereof usedinpowergeneratingprocess, consideredaswhole tobewhollysoldtotheElectricity GeneratingAuthorityofThailand aspercriteriaspecifiedby Director-General 01.08 LiquidMethane,LiquidEthane, LiquidButane,Butaneisomerinliquid formandgasorsimilarproducts (1)LiquidMethane,LiquidButane 34 Kilogramme, 13.00 -exempted- Butaneisomerinliquidform partialthereof andgasorsimilarproducts consideredaswhole (2) LiquidEthane 34 Kilogramme, 13.00 23 Kilogramme, 2.170 partialthereof partialthereof consideredaswhole consideredaswhole 01.09 LiquidEthylene,LiquidPropylene, LiquidButylene,Bytyleneisomerin liquidform,LiquidButadieneand similarproducts (1) LiquidEthylene,LiquidPropylene, 34 Kilogramme, 9.00 23 Kilogramme, 2.170 LiquidButylene,Bytyleneisomerin partialthereof partialthereof liquidform,LiquidButadieneand consideredaswhole consideredaswhole similarproducts (2)LiquidEthyleneandsimilar 34 Kilogramme, 9.00 -exempted- productsonlywithpurity partialthereof exceeding95percent consideredaswhole (3) LiquidPropylene,LiquidButylene 34 Kilogramme, 9.00 -exempted- Butyleneisomerinliquidform, partialthereof LiquidButadieneandsimilar consideredaswhole productsonlywithpurity exceeding90percent

0�� 0��Annual Report 2009 0�� 0��The Excise Department

TaxRate

AccordingtoExciseTaxActB.E.2527(1984)

Unit THB/Unit

PerVolumeAdValorem

Category Item

Unit

PerVolumeAdValorem THB/Unit

AppliedRate/Exemption

01.10 MethaneGas,EthaneGas, PropaneGas,ButaneGas,Butane isomeringasformandsimilarproducts (1) EthaneGas 34 Kilogramme, 13.00 23 Kilogramme, 2.170 partialthereof partialthereof consideredaswhole consideredaswhole (2)PropaneGas 34 Kilogramme, 13.00 23 Kilogramme, 2.170 partialthereof partialthereof consideredaswhole consideredaswhole (3)MethaneGas,EthaneGas 34 Kilogramme, 13.00 -exempted- Butaneisomeringasform partialthereof andsimilarproducts consideredaswhole 01.11 Ethylene,Propylene,Butylene, 42 Kilogramme, 9.00 -exempted- Butyleneisomeringasformand partialthereof similarproducts consideredaswhole 01.90 (1) Fueloilorsimilarproducts 42 LitreorKilogramme 10.00 5 LitreorKilogramme 0.000 asperministerial asperministerial announcement announcement (2) Productwhichismixtureof bitumenusedasfuel (2.1) Productwhichismixtureof 42 LitreorKilogramme 10.00 12 LitreorKilogramme 0.000 bitumenusedasfuel asperministerial asperministerial announcement announcement (2.2)Productwhichismixtureof 42 LitreorKilogramme 10.00 1 LitreorKilogramme 0.000 bitumenusedasfuelfor asperministerial asperministerial electricitygeneratingtobesold announcement announcement whollytotheElectricityGenerating AuthorityofThailandasper criteriaspecifiedby Director-General (3)Hydrocarbonsolventonlywith propertiesasperspecifiedby Director-General

0�� 0��Annual Report 2009 0�� 0��The Excise Department

TaxRate

AccordingtoExciseTaxActB.E.2527(1984)

Unit THB/Unit

PerVolumeAdValorem

Category Item

Unit

PerVolumeAdValorem THB/Unit

AppliedRate/Exemption

(3.1) Hydrocarbonsolventonlywith 42 LitreorKilogramme 10.00 30 LitreorKilogramme 0.000 propertiesasperspecifiedby asperministerial asperministerial Director-General announcement announcement (3.2)Hydrocarbonsolventonlywith 42 LitreorKilogramme -exempted- propertiestobeusedin asperministerial manufacturingplantasper announcement specifiedbyDirector-General 01.01 (1) Petroleumandpetroleumproducts exempted to producedbymanufacturertobe 01.11 usedwithinthesameindustrial and plantasperandcriteriaspecified 01.90 byDirector-General 01.90 (2) Petroleumandpetroleumproducts exempted usedasrawmaterialsor componentformanufacturing processwithinpetroleumand petroleummanufacturing plantaspercriteriaspecified byDirector-General Part2 Beverage 02.01 Artificialmineralwater,sodaand 25 container 0.77 25 container 0.770 softdrinkwithnoaddedsugarorother sweetenersandfavouringagent 02.02 Mineralwaterandsoftdrinkwithadded sugarorothersweetenersorfavouring agentandothernon-alcoholicdrinks excludingfruitorvegetablejuice asperspecifiedin02.03 (1) inacontainerwithcapacity 20 container 0.45 20 container 0.370 notexceeding440cc.

0�� 0��Annual Report 2009 0�� 0��The Excise Department

TaxRate

AccordingtoExciseTaxActB.E.2527(1984)

Unit THB/Unit

PerVolumeAdValorem

Category Item

Unit

PerVolumeAdValorem THB/Unit

AppliedRate/Exemption

(2) inacontainerwithcapacity 20 capacity440cc., 0.45 20 capacity440cc., 0.370 Exceeding440cc. partialthereof partialthereof consideraswhole consideraswhole (3) producedorpackedorpumped 20 capacity440cc., 0.45 20 capacity440cc., 0.370 fromdrinkvendingmachine partialthereof partialthereof consideraswhole consideraswhole 02.03 Fruitjuice(incl.Grapemust)and vegetablejuice,withoutfermentation andaddedalcohol,whetherornot withsugarorothersweeteners (1) inacontainerwithcapacity 20 container 0.45 20 container 0.370 notexceeding440cc. (2)inacontainerwithcapacity 20 capacity440cc., 0.45 20 capacity440cc., 0.370 Exceeding440cc. partialthereof partialthereof consideraswhole consideraswhole (3) producedorpackedorpumped 20 capacity440cc., 0.45 20 capacity440cc., 0.370 fromdrinkvendingmachine partialthereof partialthereof consideraswhole consideraswhole Fruitjuice(incl.Grapemust)and vegetablejuice,withoutfermentation andaddedalcohol,whetherornotwith sugarorothersweeteners,andwith Ingredientsasspecifiedbythe Director-Generalandwithprior permissionfromtheDirector-General (1) inacontainerwithcapacity 20 container 0.45 -exempted- notexceeding440cc. (2) inacontainerwithcapacity 20 capacity440cc., 0.45 -exempted- Exceeding440cc. partialthereof consideraswhole (3) producedorpackedorpumped 20 capacity440cc., 0.45 -exempted- fromdrinkvendingmachine partialthereof consideraswhole

0�� 0��Annual Report 2009 0�� 0��The Excise Department

TaxRate

AccordingtoExciseTaxActB.E.2527(1984)

Unit THB/Unit

PerVolumeAdValorem

Category Item

Unit

PerVolumeAdValorem THB/Unit

AppliedRate/Exemption

Part3 ElectricalAppliances 03.01 -Air-conditioningunitwithmotor-driven fanandthermostat,whetherornot withhumiditycontrolunitwithcapacity ofnotexceeding 72,000BTU/hour (1) forusedinvehicle 30 - - 15 - - (2)othersfrom(1) 30 - exempted (AccordingtotheMinisterial AnnouncementonExciseTaxRate ReductionandExemption(Issue86) datedSeptember2,2009) 03.02 -Lightingandchandelierforceilingor 15 - - 15 - - wall,excludingthoseforpublicopen spaceorpublicroad (1)Lighting 15 - -exempted - - (2) Chandeliersotherthanthose 15 - -exempted - - madefromorcontainpartiallead crystalorothertypeofcrystal (AccordingtotheMinisterial AnnouncementonExciseTaxRate ReductionandExemption (Issue41)datedMay21,1997 furtheramendedbytheMinisterial AnnouncementonExciseTax Exemption(Issue43)dateJune3, 1997effectivefromMay22, 1997onwards. (3) Chandeliermadefromorcontain 15 - - 15 - - partialleadcrystalorothertype ofcrystal

0�� 0��Annual Report 2009 0�� 0��The Excise Department

TaxRate

AccordingtoExciseTaxActB.E.2527(1984)

Unit THB/Unit

PerVolumeAdValorem

Category Item

Unit

PerVolumeAdValorem THB/Unit

AppliedRate/Exemption

Part4 CrystalandGlassware 04.01 -Leadcrystalandothertypeofcrystal (1)forusedastableware,kitchen 30 - - 15 - - ware,Inbathroom,office,interior decorationorothersimilarpurposes (2)Beads,imitationpearls,imitation 30 - - 15 - - gemsorsemiimitationgemsand crystalmadeintosimilarsmall objectsandproductsmadefrom suchmaterialsexceptimitation jewelryandjewel,glasseyeother thanprosthesissmallfigureand otherornamentmadefromglass andmoldedbyblowlampexcept imitationjewelryandjewelin sphericalshapewithnominal diameternotexceeding1mm. (AccordingtotheMinisterial AnnouncementonExciseTaxRate ReductionandExemption (Issue41)datedMay21,1997) (3) Productsin(1)or(2)tobeused 30 - -exempted - - asrawmaterialsorpartsofother productsorartifactsaccording tothetermsandConditions specifiedbytheDirector-General (4)Others 30 - -exempted - - (AccordingtotheMinisterial AnnouncementonExciseTax Exemption(Issue52)dateMarch 11,1998)

0�� 0��Annual Report 2009 0�� 0��The Excise Department

TaxRate

AccordingtoExciseTaxActB.E.2527(1984)

Unit THB/Unit

PerVolumeAdValorem

Category Item

Unit

PerVolumeAdValorem THB/Unit

AppliedRate/Exemption

Part5 Automobile 05.01 -PassengerCar (1) PassengerCar (1.1) withcylindricalvolumenot 50 - - 30 - - exceeding2,000cc.andengine powernotexceeding220horse power(HP) (1.2)withcylindricalvolumeexceeding 50 - - 35 - - 2,000cc.butnotexceeding 2,500cc.andenginepowernot exceeding220horsepower(HP) (1.3)withcylindricalvolumeexceeding 50 - - 40 - - 2,500cc.butnotexceeding 3,000cc.andenginepowernot exceeding220horsepower(HP) (1.4)withcylindricalvolumeexceeding 50 - - 50 - - 3,000cc.orwithenginepower exceeding220horsepower(HP) (2) Pick-upPassengerVehicle:PPV withspecificationsasperspecified bytheMinisterofFinance (2.1) withcylindricalvolumenot 50 - - 20 - - exceeding3,250cc. (2.2) withcylindricalvolume 50 - - 50 - - exceeding3,250cc. (3) DoubleCabVehiclewith specificationsasperspecified bytheMinisterofFinance (3.1)withcylindricalvolume 50 - - 12 - - notexceeding3,250cc. (3.2) withcylindricalvolume 50 - - 50 - - exceeding3,250cc.

0�� 0��Annual Report 2009 0�� 0��The Excise Department

TaxRate

AccordingtoExciseTaxActB.E.2527(1984)

Unit THB/Unit

PerVolumeAdValorem

Category Item

Unit

PerVolumeAdValorem THB/Unit

AppliedRate/Exemption

(4) Passengercarwithspecification asperspecifiedbytheMinister ofFinancewhichismadefrom pick-uptruckorchassiswith windshieldofpick-uptruckor modifiedfrompick-uptruck (4.1) producedormodifiedby industrialentrepreneurasper qualifiedbytheMinister ofFinance (4.1.1) withcylindricalvolume 50 - - 3 - - notexceeding3,250cc. (4.1.2)withcylindricalvolume 50 - - 50 - - exceeding3,250cc. (4.2) modifiedbymodifierasper 50 - -exempted - - clause144,third,taxable asper(1) accordingtoclause144.fifth. passenger car(1.1) to(1.4) 05.02 Passengercarwithseatingnot exceeding10seats (1) withcylindricalvolume 50 - - 30 - - notexceeding2,000cc.and enginepowernotexceeding220 horsepower(HP) (2)withcylindricalvolumeexceeding 50 - - 35 - - 2,000cc.butnotexceeding 2,500cc.andenginepowernot exceeding220horsepower(HP) (3)withcylindricalvolumeexceeding 50 - - 40 - - 2,500cc.butnotexceeding 3,000cc.andenginepowernot exceeding220horsepower(HP)

0�0 0�1Annual Report 2009 0�0 0�1The Excise Department

TaxRate

AccordingtoExciseTaxActB.E.2527(1984)

Unit THB/Unit

PerVolumeAdValorem

Category Item

Unit

PerVolumeAdValorem THB/Unit

AppliedRate/Exemption

(4) withcylindricalvolumeexceeding 50 - - 50 - - 3,000cc.orenginepower exceeding220horsepower(HP) 05.01 Passengercarorpublictransport vehiclewithandseatingnotexceeding 10seats 05.02 (1)Passengercarorpublictransport 50 - -exempted - - vehiclewithseatingnotexceeding 10seatsusedasambulanceof governmentalagency,hospital orcharitableorganisationasper termsandconditionandnumber specifiedbytheMinistryofFinance (2) Passengercarorpubictransport vehiclewithseatingnotexceeding 10seatinenergysavingmodel (2.1) HybridElectricVehicle (2.1.1) withcylindricalvolume 50 - - 10 - - notexceeding3,000cc. (2.1.2)withcylindricalvolume 50 - - 50 - - exceeding3,000cc. (2.2) ElectricPoweredVehicle 50 - - 10 - - (2.3)FuelCellPoweredVehicle 50 - - 10 - - (2.4) EcoCar (2.4.1) Gasolineenginewithcylindrical 50 - - 17 - - volumenotexceeding1,300cc. (2.4.2) Dieselenginewithcylindrical 50 - - 17 - - volumenotexceeding1,400cc. (AccordingtotheMinisterial AnnouncementonExciseTax RateReduction(Issue81) datedJanuary18,2008)

0�0 0�1Annual Report 2009 0�0 0�1The Excise Department

TaxRate

AccordingtoExciseTaxActB.E.2527(1984)

Unit THB/Unit

PerVolumeAdValorem

Category Item

Unit

PerVolumeAdValorem THB/Unit

AppliedRate/Exemption

(3) Passengercarorpublictransport vehiclewithseatingnotexceeding 10seatsusingalternativeenergy withcylindricalvolumenotexceeding 3,000cc.withspecificationasper specifiedbytheMinisterofFinance (3.1) abletousepetrolwithnotless than20percentofethanolas mixture (3.1.1) withcylindricalvolume 50 - - 25 - - notexceeding2,000cc.and enginepowernotexceeding 220horsepower(HP) (3.1.2) withcylindricalvolume 50 - - 30 - - exceeding2,000cc.butnot exceeding2,500cc.and enginepowernotexceeding 220horsepower(HP) (3.1.3)withcylindricalvolume 50 - - 35 - - exceeding2,500cc.butnot exceeding3,000cc.and enginepowernotexceeding 220horsepower(HP) (3.1.4)withcylindricalvolume 50 - - 50 - - exceeding3,000cc.orengine powerexceeding220horse power(HP) (3.2)abletousenaturalgasasfuel 50 - - 20 - - (AccordancetotheMinisterial AnnouncementonExciseTax RateReduction(Issue80)dated November9,2007) (4)Motortricycleandpassengercar producedwithmotorcycleengine withenginepowernotexceeding 250cc.

0�� 0��Annual Report 2009 0�� 0��The Excise Department

TaxRate

AccordingtoExciseTaxActB.E.2527(1984)

Unit THB/Unit

PerVolumeAdValorem

Category Item

Unit

PerVolumeAdValorem THB/Unit

AppliedRate/Exemption

(4.1) MotorTricycle 50 - - 5 - - (4.2) Passengercarproducedwith 50 - - 5 - - motorcycleenginewithpower notexceeding250cc. 05.90 (1) Pick-uptruckdesignedtohave totalweightincludingloading weightnotexceeding4,000 kilogramme (1.1) withcylindricalvolume notexceeding3,250cc. (1.1.1) withspecificationasper 50 - - 3 - - specifiedbytheMinistryof Finance (1.1.2) withspecificationother 50 - - 18 - - than(1.1.1) (1.2) withcylindricalvolume 50 - - 50 - - exceeding3,250cc. (AccordingtotheMinisterial AnnouncementonExciseTax RateReductionandExemption (Issue72)dateJuly27,2004) Part6 Boat 06.01 -Yachtandboatusedforleisure purpose (1) Yachtandboatusedforleisure 50 - -exempted - - purposeexceptthosein(2)and(3) (AccordingtotheMinisterial AnnouncementonCancellation ofExciseTaxRateReduction (Issue70)dateFebruary13,2004) (2) Rowboat,yawlandinflatableraft 50 - -exempted - -

0�� 0��Annual Report 2009 0�� 0��The Excise Department

TaxRate

AccordingtoExciseTaxActB.E.2527(1984)

Unit THB/Unit

PerVolumeAdValorem

Category Item

Unit

PerVolumeAdValorem THB/Unit

AppliedRate/Exemption

(3) boatforsportpurposeasperterms 50 - -exempted - - andconditionsspecifiedbythe Director-General (AccordingtotheMinisterial AnnouncementonExciseTaxRate ReductionandExemption(Issue27) dateDecember30,1991) Part7 PerfumeandCosmatic 07.01 -Perfume,fragrantessenceand essentialoil” (1) Essentialoilandfragrantessence, 20 - - 15 - - excludingofperfumeandfragrant essencein(3) (AccordingtotheMinisterial AnnouncementonExciseTaxRate ReductionandExemption(Issue41) dateMay21,1997) (2)Essentialoil 20 - -exempted - - (3)Perfumeandfragrantessence 20 - -exempted - - whichislocalproductand produceddomestically (AccordingtotheMinisterial AnnouncementonExciseTaxRate ReductionandExemption(Issue27) dateDecember30,1991) Part8 OtherProducts 08.90 (1)Carpetandotherfloorcovering textile - carpetandanimalhairfloorcovering 30 - - 20 - - materials -othersfromabove 30 - -exempted - -

0�� 0��Annual Report 2009 0�� 0��The Excise Department

TaxRate

AccordingtoExciseTaxActB.E.2527(1984)

Unit THB/Unit

PerVolumeAdValorem

Category Item

Unit

PerVolumeAdValorem THB/Unit

AppliedRate/Exemption

(AccordingtotheMinisterial AnnouncementonExciseTaxRate Reduction(Issue27)dateDecember 30,1991) (2) Motorcycle (2.1) 2strokeengine 30 - - 5 (fromJanuary1, 2002onwards) (2.2)4strokeengine 30 - - 3 (fromdateof announcement) (2.3)others 30 - -exempted - - (AccordingtotheMinisterial AnnouncementonExciseTaxRate ReductionandExemption(Issue62) datedFebruary6,2001) (3) Marbleandgranite 30 - -exempted - - (AccordingtotheMinisterial (fromMay23, AnnouncementonExciseTaxRate 1997onwards) ReductionandExemption(Issue45) datedJune25,1997) (4)Battery 30 - - 10 - - (AccordingtotheMinisterial AnnouncementonExciseTaxRate ReductionandExemption(Issue42) datedMay21,1997)” - batteryusingrawmaterialsor 30 - - 5 - - manufacturingcomponentfrom batterywhoseexcisetaxhasbeen paidaccordingtothetermsand conditionsspecifiedbytheDirector- General (AccordingtotheMinisterial AnnouncementonExciseTaxRate ReductionandExemption(Issue45) datedJune25,1997andthe DepartmentalAnnouncementon CancellationofTermsandConditions

0�� 0��Annual Report 2009 0�� 0��The Excise Department

TaxRate

AccordingtoExciseTaxActB.E.2527(1984)

Unit THB/Unit

PerVolumeAdValorem

Category Item

Unit

PerVolumeAdValorem THB/Unit

AppliedRate/Exemption

forBatteryusingRawMaterialsor ManufacturingComponentEntitledto ExciseTaxRateReductiondated November22,2005) (5) OzoneDepletingHalogenated HydrocarbonAcrylic (5.1) CarbonTetrachloride 30 - - 30 - - (5.2) Trichloroethane 30 - - 30 - - (5.3) Trichlorofluoromethane 30 - - 30 - - (5.4)Dichlorodifluoromethane 30 - - 30 - - (5.5) Trichlorotrifluoroethane 30 - - 30 - - (5.6)Dichlorotetrafluoroethane 30 - - 30 - - (5.7) Chloropentafluoroethane 30 - - 30 - - (5.8)Bromochlorodifluoromethane 30 - - 30 - - (5.9)Bromotriflufluoromethane 30 - - 30 - - (5.10)Dibromotetrafluoroethane 30 - - 30 - - (5.11)Othersfrom(5.1)to(5.10) 30 - -exempted - - Part9 EntertainmentorRecreationalActivities 09.01 -NightclubandDiscotheque (1)Incomesofbusinessproviding 20 - - 10 - - foodanddrinkanddancewithlive musicoraudioequipmentorother performanceforentertaining purpose (2) Otherincomes 20 - -exempted - - 09.02 -TurkishBathorSaunaandMassage (1) Incomesfromprovidingbathing orsaunaandmassageservices -Incomesfromprovidingbathingor 20 - - 10 - - saunaandmassageservicewith serviceprovider

0�� 0��Annual Report 2009 0�� 0��The Excise Department

TaxRate

AccordingtoExciseTaxActB.E.2527(1984)

Unit THB/Unit

PerVolumeAdValorem

Category Item

Unit

PerVolumeAdValorem THB/Unit

AppliedRate/Exemption

- Incomesfromprovidingbathingor 20 - -exempted - - saunaandmassageservicein educationalinstituteortempleor religiousplace - Incomesfromprovidingbathingor 20 - -exempted - - saunaandmassageservicein hospitalorclinicaccordingtoClinical Laws - Incomesfromprovidingbathingor 20 - -exempted - - saunaandmassageserviceinbeauty salonorhealthcarecentreaccording tothetermsandconditionsspecified bytheDirector-General (2) Otherincomes 20 - -exempted - - Part10 Gamble 10.01 - HorseRacingCourse (1) AdmissionFee 20 - - 20 - - (2) Incomesfromgamblingafter 20 - - 20 - - deductionofprizemoneyforwinners fromsuchgambling (3) Otherincomes 20 - -exempted - - 10.02 -Incomesfromlotteryissuance 20 - -exempted - - Part11 ActivitywithAdverseEffect ontheEnvironment 11.01 -GolfCourse (1) MembershipFee 20 - - 10 - - (2) CourseUsageFee 20 - - 10 - - (3) Otherincomes 20 - -exempted - -

0�� 0��Annual Report 2009 0�� 0��The Excise Department

TaxRate

AccordingtoExciseTaxActB.E.2527(1984)

Unit THB/Unit

PerVolumeAdValorem

Category Item

Unit

PerVolumeAdValorem THB/Unit

AppliedRate/Exemption

Part12 BusinessbyGovernmentPermission orConcession 12.01 - TelecommunicationBusiness (1) LandLineTelephoneService - Incomesfromprovidingdomestic 50 - - 0 - - telephoneservice - Incomesfromprovidinginternational 50 - - 0 - - telephoneservice,onlyfromincomes occurdomestically - Otherincomes 50 - -exempted - - (2)MobilePhoneorCellularRadio CommunicationService - Incomesfromprovidingdomestic 50 - - 0 - - telephoneservice - Incomesfromprovidinginternational 50 - - 0 - - telephoneservice,onlyfromincomes occurdomestically - Otherincomes (3) Others 50 - -exempted - - (AccordingtotheMinisterial AnnouncementonExciseTaxRate ReductionandExemption(Issue79) datedFebruary26,1997)

UpdateMay29,2008

0�� 0��Annual Report 2009 0�� 0��The Excise Department

Spirit Tax Rate TaxRate

ByVolumeItemAdValorem

Unit THB/Unit

1. BrewedBeverageTaxRateCeiling 60 Litreofpurealcohol 100 1.1 Beer 60 Litreofpurealcohol 100 1.2 WineandSparkingWinefromGrape 60 Litreofpurealcohol 100 1.3 LocalBrewedbeverage 25 Litreofpurealcohol 70 1.4 Othersfrom1.11.2and1.3 25 Litreofpurealcohol 70 2. DistilledBeverageExciseTaxRateCeiling 50 Litreofpurealcohol 400 2.1 WhiteSpirit 50 Litreofpurealcohol 120 2.2 BlendedSpirit 50 Litreofpurealcohol 300 2.3 SpecialBlendSpirit 50 Litreofpurealcohol 400 2.4 PremiumSpirit (1) Brandy 48 Litreofpurealcohol 400 (2)Whiskey 50 Litreofpurealcohol 400 (3)Othersfrom(1)and(2) 50 Litreofpurealcohol 400 (AccordingtotheMinisterialAnnouncementonTypeofSpirit andSpiritExciseTaxRate(Issue4)B.E.2009dateMay6,2009) 2.5 Ethanol(Spiritwithover80degreeofpurealcohol) (1)forusedinindustryorbeingconversed 2 Litre 1.00 accordingtothemethodsspecifiedbythe Director-General (2)forusedinmedicalorscientific 0.1 Litre 0.05 purposeaccordingtothemethodsspecifiedbythe Director-General (3)Othersfrom(1)and(2) 10 Litreofpurealcohol 6.00

0�� 0��Annual Report 2009 0�� 0��The Excise Department

Tobacco Stamp Rate TaxRate

ByVolumeItem AdValorem Unit THB/Unit

Playing Card Levy TaxRate

ByVolumeItem AdValorem

Unit THB/Unit

TobaccoandCigaretteExciseTaxRateCeilingconsideraswhole 90 Gramme,partialthereof 0.60 consideraswhole 1.PipeTobacco 0.1 10gramme,partialthereof 0.01 (AccordingtotheMinisterialAnnouncementconsideraswhole onTobaccoStampB.E.2552datedMay13,2009) 2.Cigarette 2.1 Cigarette 85 - - (AccordingtotheMinisterialAnnouncementonTobacco StampRateB.E.2552datedMay13,2009) 2.2Cigar 10 Gramme,partialthereof 0.50 (AccordingtotheMinisterialAnnouncementonTobaccoStamp RateB.E.2552datedMay13,2009) 2.3 OtherCigarette 0.1 5gramme,partialthereof 0.02 (AccordingtotheMinisterialAnnouncementonTobaccoStamp consideraswhole RateB.E.2552datedMay13,2009) 2.4FavouredPipeTobacco 10 Gramme,partialthereof 0.50 (AccordingtotheMinisterialAnnouncementonTobaccoStamp consideraswhole RateB.E.2552datedMay13,2009) 2.5ChewingTobacco 0.1 Gramme,partialthereof 0.09 (AccordingtotheMinisterialAnnouncementonTobaccoStamp consideraswhole RateB.E.2552datedMay13,2009)

PlayingCardLevyExciseTaxRateCeiling - 100Cards 30.00 1) PokerCard,allsizesandtypes - 100Cards 30.00 2) OtherCards,allsizesandtypes - 100Cards 2.00 (AccordingtotheMinisterialAnnouncementIssue7B.E.2534 datedDecember30,1991)

0�0 0PBAnnual Report 2009