Mechanism Design with Aftermarkets: On the Optimality...

63

Mechanism Design with Aftermarkets: On the Optimality of Cutoff Mechanisms PRELIMINARY AND INCOMPLETE Piotr Dworczak * January 2, 2017 Abstract I study a mechanism design problem of allocating a single good to one of several agents. The mechanism is followed by an aftermarket, that is, a post-mechanism game played be- tween the agent who acquired the good and a third-party market participant. The designer has preferences over final outcomes, but she cannot redesign the aftermarket. However, she can influence its information structure by disclosing information elicited by the mechanism, subject to providing incentives for agents to report truthfully. A companion paper (Dworczak, 2016) introduces a class of cutoff mechanisms, charac- terizes their properties, and derives the optimal mechanism within the class. In this paper, under the assumption that the aftermarket payoffs are determined by a binary decision of the third party, I provide sufficient conditions for optimality of cutoff mechanisms. I also analyze a version of the model in which cutoff mechanisms are sometimes suboptimal. I derive robust payoff bounds on their performance, and show that by using a cutoff mechanism the designer can often guarantee a large fraction of the payoff of the optimal (non-cutoff) mechanism. Keywords: Mechanism Design, Information Design, Auctions JEL codes: D44, D47, D82, D83. * Stanford University, Graduate School of Business, [email protected]. I would like to thank Darrell Duffie, Paul Milgrom, Michael Ostrovsky, Alessandro Pavan, and Andy Skrzypacz for helpful discussions.

Transcript of Mechanism Design with Aftermarkets: On the Optimality...

Mechanism Design with Aftermarkets:

On the Optimality of Cutoff Mechanisms

PRELIMINARY AND INCOMPLETE

Piotr Dworczak∗

January 2, 2017

Abstract

I study a mechanism design problem of allocating a single good to one of several agents.

The mechanism is followed by an aftermarket, that is, a post-mechanism game played be-

tween the agent who acquired the good and a third-party market participant. The designer

has preferences over final outcomes, but she cannot redesign the aftermarket. However, she

can influence its information structure by disclosing information elicited by the mechanism,

subject to providing incentives for agents to report truthfully.

A companion paper (Dworczak, 2016) introduces a class of cutoff mechanisms, charac-

terizes their properties, and derives the optimal mechanism within the class. In this paper,

under the assumption that the aftermarket payoffs are determined by a binary decision of the

third party, I provide sufficient conditions for optimality of cutoff mechanisms.

I also analyze a version of the model in which cutoff mechanisms are sometimes suboptimal.

I derive robust payoff bounds on their performance, and show that by using a cutoff mechanism

the designer can often guarantee a large fraction of the payoff of the optimal (non-cutoff)

mechanism.

Keywords: Mechanism Design, Information Design, Auctions

JEL codes: D44, D47, D82, D83.

∗Stanford University, Graduate School of Business, [email protected]. I would like to thankDarrell Duffie, Paul Milgrom, Michael Ostrovsky, Alessandro Pavan, and Andy Skrzypacz for helpfuldiscussions.

1 Introduction 1

1 Introduction

Real-life mechanisms rarely take place in a vacuum. Auctions are often embedded in

markets in which bidders can resell the items they bought. Procurement mechanisms

are followed by bargaining between winners of contracts and subcontractors. While

such post-mechanism interactions may be beyond the direct control of the mechanism

designer, the designer can nevertheless influence their outcome by disclosing information

elicited by the mechanism. For example, by revealing the price paid by the winning

bidder in a first price auction, an auctioneer changes the information structure of a

post-auction resale game. This can lead to a different level and split of surplus in

the aftermarket, and hence different behavior of bidders in the auction. In mechanism

design with aftermarkets, the designer chooses an ex-post information disclosure as part

of the mechanism.

This paper contains results that complement and extend the analysis of the pa-

per “Mechanism Design with Aftermarkets: Cutoff Mechanisms” (Dworczak, 2016). I

study the same model of mechanism design with aftermarkets, where the aftermarket

is defined as an interaction between the agent who acquired the object in the first-stage

mechanism and a third-party market participant. Instead of restricting attention to the

class of cutoff mechanisms, I impose a simplifying assumption on the structure of the

aftermarket: I assume that the outcome in the aftermarket is determined by a binary

decision of the third party. As a result, it is sufficient to look at binary signals in

the mechanism. This simplification allows me to characterize the set of implementable

allocation and disclosure rules, and then solve for optimal mechanisms.

The reader is referred to Dworczak (2016) for a discussion of the importance of

aftermarkets in real-life design problems. In this paper, I focus on the methodological

contribution, and on the economic intuitions underlying the results on optimality of

cutoff mechanisms. Cutoff mechanisms have a number of properties that were studied

extensively in Dworczak (2016). Here, I abstract away from those properties, and

focus solely on the issue of (Bayesian) optimality – when is it that a cutoff mechanism

achieves the highest value of the objective function of the mechanism designer among

all incentive-compatible mechanisms?

To answer this question, I first study an auxiliary problem of pure information

intermediation. This is a problem in which the designer does not control the allocation of

the physical good in the mechanism. That is, the designer acts only as a an information

mediator: Under commitment, she can send signals and exchange payments with the

1 Introduction 2

agent as a function of the agent’s report. After the signal is sent by the mechanism,

the agent interacts with the third party in the aftermarket. The question of interest is

whether the designer can influence the outcome of the aftermarket. The first result of

the paper (Theorem 1) provides conditions under which the answer is negative. The

condition requires that the agent’s and the third party’s preferences are misaligned:

When lower types of the agent have a higher willingness to pay for the high action of

the third party, the third party prefers to take the high action only if she believes that

the type of the agent is high. This is satisfied, for example, when the third party buys

a good from the agent (the high action corresponds to a high resale price).1 Formally,

the condition is expressed in terms of sub/supermodularity of the agent’s and the third

party’s utility functions in the type of the agent and the action of the third party. I

refer to the case of misaligned preferences as counter-modularity : When the agent’s

utility is submodular, the third party’s utility is supermodular (or vice versa). When

utilities of players are co-modular, the result is false: The designer can successfully

disclose information about the agent’s type to the aftermarket.

The analysis of pure information intermediation helps explain the main contribution

of the paper, that is, conditions for optimality of cutoff mechanisms (Theorems 2 - 4).

When the utility functions of the agent and the third party are counter-modular, and

certain additional conditions hold, a cutoff mechanism is optimal. (The additional

conditions restrict the set of possible objective functions of the mechanism designer,

and require that preferences of the agent take a strong form of sub/supermodularity.)

As shown in Dworczak (2016), cutoff mechanisms, which are mechanisms that only

disclose information about a cutoff (and not about the type of the agent directly), are

always feasible. That is, regardless of the form of the aftermarket, information about the

cutoff can be revealed without violating incentive constraints in the mechanism. When

preferences of the agent and the third party satisfy counter-modularity, as shown in

Theorem 1, it is hard to disclose information about the agent’s type directly. Therefore,

revealing information about the cutoff alone is optimal.

In the setting of pure information intermediation, the corresponding cutoff is a de-

generate random variable. Thus, a cutoff mechanism cannot disclose any non-redundant

information, consistent with Theorem 1. However, when the designer controls the al-

location, and allocates with different probabilities to different types (for example, by

running an auction), the cutoff becomes informative about the type of the winner, and

1 In a companion note, I extend this result to the case when the third party proposes an arbitrarymechanism in the aftermarket, without the restriction to binary actions.

1 Introduction 3

its disclosure influences the outcome of the aftermarket.

The results on optimality of cutoff mechanisms are illustrated with three examples,

where the aftermarket is, respectively, (i) a resale game in which the third party has

full bargaining power, (ii) a game in which the winner buys a complementary good

from a monopolist, and (iii) a resale game with adverse selection.

Finally, I consider cases when cutoff mechanisms fail to be optimal. In Theorem

5, I characterize optimal mechanisms for the case of co-modularity of the agent’s and

the third party’s preferences. I show that the optimal mechanism reveals information

about the type of the winner directly: The optimal (binary) signal partitions the type

space into low and high types, and discloses this information to the third party.

I also analyze a model in which preferences of the third party and the agent are

counter-modular, but the agent’s utility takes a more general form than that permitted

by Theorems 2 - 4. A cutoff mechanism is sometimes optimal, but is not optimal in

general. I derive robust payoff bounds on the performance of cutoff mechanisms. For

the case when the designer maximizes total surplus in the market, I show that a cutoff

mechanisms achieves nearly 90% of the payoff of the optimal mechanism in the worst

case. Similar (but weaker) bounds are established for revenue maximization, and for

an arbitrary objective function of the designer.

The rest of the paper is organized as follows. In Section 2, I formally introduce the

model. I study a version with one agent which is then extended to multiple agents in

Section 5. In Section 3, the results on pure information intermediation are presented.

Section 4 contains the main results on optimality of cutoff mechanisms, and Section 6

– the applications. In Section 7, I study optimal non-cutoff mechanisms, and derive

robust payoff bounds.

1.1 Related literature

A review of the literature on post-mechanism interactions is contained in the companion

paper Dworczak (2016), and I do not duplicate it here. I offer additional discussions

of related papers in the context of specific results throughout the paper. In particular,

my results on pure information intermediation are related to the model of Crawford

and Sobel (1982). I also compare my results to Calzolari and Pavan (2006) who study

an instance of a problem with one agent for which the unique optimal mechanism is

sometimes not a cutoff mechanism. I explain the relationship between their result and

my conditions for optimality in Section 7.

2 The baseline model 4

2 The baseline model

A mechanism designer is a seller who chooses a mechanism to sell an indivisible object

to an agent. The agent has a private type θ ∈ Θ. I normalize Θ = [0, 1], and assume

that θ is distributed according to a continuous full-support distribution F with density

f . If the agent acquires the good, she participates in the aftermarket which is an

interaction with a third party. The mechanism designer cannot contract with the third

party.

The market game consists of two stages: (1) implementation of the mechanism, and

(2) post-mechanism interaction between the agent and the third party (the aftermar-

ket). In the first stage, the seller chooses and publicly announces a direct mechanism

(x, π, t), where x : Θ→ [0, 1] is an allocation function, π : Θ→ ∆(S) is a signal func-

tion with some finite signal set S, and t : Θ → R is a transfer function.2 If the agent

reports θ, she receives the good with probability x(θ) and pays t(θ). Conditional on

selling the good, the designer draws and publicly announces a signal s ∈ S according to

distribution π(·| θ). For technical reasons, I assume that x(θ) must be right-continuous,

and π(s| θ) is measurable in θ. I call (x, π) a mechanism frame.

In the second stage, the third party observes the signal realization s, and Bayes-

updates her beliefs (knowing whether the agent acquired the good in the mechanism or

not). I let F s denote the updated belief over the agent’s type (conditional on the event

that the agent acquired the good and signal s was observed). The third party then takes

a binary decision a ∈ {l, h} to maximize the expectation of an upper semi-continuous

function va(θ) : Θ→ R,

a?(F s) = argmaxa∈{l, h}

ˆ 1

0

va(θ)dF s(θ).

When the third party is indifferent, it is assumed that the selection from the argmax

correspondence is made by the designer.

Although the aftermarket payoffs are formally determined by the decision of the

third party, this reduced-form specification allows for a non-trivial strategic interaction

between the agent and the third party. This is because the function va(θ) could be

determined endogenously in equilibrium. For example, if a denotes the price quoted by

the third party (high or low), the function va is derived from the optimal acceptance

2 Using a direct mechanism is without loss of generality, by the Revelation Principle, see for exampleMyerson (1982).

2 The baseline model 5

decision of the agent.

The agent’s payoff, net of transfers, conditional on acquiring the good in the mech-

anism is given by

Ua(θ) = ua θ + ca, (2.1)

where ua ≥ 0 and ca are constants. Linearity of Ua(θ) in θ is assumed for tractability.

The important assumption is that the action of the third party influences the slope of

the utility function of the agent. The agent’s payoff is normalized to zero if the agent

does not acquire the good. The agent’s final utility is quasi-linear in transfers, and the

agent is an expected-utility maximizer.

The mechanism designer’s ex-post utility is given by the function V a(θ) if the good

is allocated and the third party takes action a. If the good is not allocated, the payoff is

normalized to zero. For clarity of exposition, I assume that the designer always weakly

prefers the third party to take the high action, i.e.V h(θ) ≥ V l(θ), for all θ ∈ Θ. To

guarantee existence of solutions to all problems considered in this paper, I assume that

V h(θ), V l(θ), and V h(θ) − V l(θ) are all upper semi-continuous in θ. The mechanism

designer maximizes expected utility.3

To avoid trivial cases, unless explicitly stated, I assume that uh 6= ul, and that

vh(θ)−vl(θ) takes both strictly positive and strictly negative values, on sets of points of

non-zero measure (otherwise, the choice of the action by the third party is independent

of beliefs about θ).

2.1 Implementability

Because the action of the third party is binary, it is without loss of generality to assume

that the signal sent by the optimal mechanism is also binary (see for example Myer-

son, 1982). Moreover, the signal can be labeled by the action that it induces, that is,

S = {l, h}. I denote q(θ) = π(h| θ). From now on, a mechanism frame is represented

by the pair (x, q), where x is the allocation rule, and q(θ) is the conditional probabil-

ity of recommending the high action conditional on type θ acquiring the good in the

mechanism.

Definition 1. A mechanism frame (x, q) is implementable if there exist transfers t such

that the agent participates and reports truthfully in the first-stage mechanism, taking

3 The designer’s utility does not depend explicitly on transfers. However, under quasi-linear utility,transfers in the mechanism are uniquely pinned down by the final allocation of the good, and thereforethe setting allows for objectives such as expected revenue maximization.

2 The baseline model 6

into account the continuation payoff from the aftermarket,

Uh(θ)q(θ)x(θ) + U l(θ)(1− q(θ))x(θ)− t(θ) ≥ 0, (IR)

θ ∈ argmaxθ

{Uh(θ)q(θ)x(θ) + U l(θ)(1− q(θ))x(θ)− t(θ)}, (IC)

for all θ ∈ Θ, and the third party obeys the recommendations of the mechanism,

ˆ 1

0

[vh(θ)− vl(θ)]q(θ)x(θ)f(θ) ≥ 0, (OBh)

ˆ 1

0

[vh(θ)− vl(θ)](1− q(θ))x(θ)f(θ) ≤ 0. (OBl)

The tractability of the binary model stems from the fact that the (IR) and (IC)

constraints admit a simple representation (which is not typically the case in the presence

of an aftermarket). By a standard argument,4 it can be shown that there exists a

transfer function t such that (IR) and (IC) are satisfied if and only if

q(θ)x(θ)uh + (1− q(θ))x(θ)ul is non-decreasing in θ. (M)

Fact 1. A mechanism frame (x, q) is implementable if and only if conditions (M),

(OBh), and (OBl) all hold.

An interesting consequence of Fact 1 is that a decreasing allocation rule x may be

implemented (in contrast to the classical setting of Myerson, 1981) if information is

disclosed in an appropriate way. This is possible whenever uh 6= ul, that is, whenever

the agent’s types have differential preferences over the actions of the third party in the

aftermarket. For example when uh = 0 and ul > 0, implementability is equivalent to

monotonicity of (1 − q(θ))x(θ), and therefore x(θ) can be decreasing as long as this is

offset by a sufficient increase in 1− q(θ), the probability of sending the low signal.

I say that (x, q) reveals no information if the distribution of actions (conditional

on each θ) induced by (x, q) in the aftermarket could also be induced by a mechanism

(x, x) that sends a redundant (constant) message with probability one.

Note that a no-information-revealing mechanism may still influence the beliefs in

the aftermarket because the third party conditions on the event that the agent acquired

4 See for example Myerson (1981) or the companion paper.

2 The baseline model 7

the good. If x is non-constant, the posterior belief will be different from the prior f

even if the mechanism does not send any explicit signals.

2.2 Cutoff mechanisms

Cutoff mechanisms were defined and discussed in the companion paper Dworczak

(2016).5 I restate the definition in the context of the binary model.

Definition 2. A mechanism frame (x, q) is a cutoff rule if x is non-decreasing, and the

signal function q can be represented as

q(θ)x(θ) =

ˆ θ

0

γ(c)dx(c), (2.2)

(1− q(θ))x(θ) =

ˆ θ

0

(1− γ(c))dx(c), (2.3)

for each θ ∈ Θ, for some measurable signal function γ : Θ→ [0, 1].

A mechanism (x, π, t) is a cutoff mechanism if (x, π) is a cutoff rule.

Definition 2 has the following interpretation. Any non-decreasing allocation rule x

can be extended to a cumulative distribution function on the type space Θ. Let cx be

the random variable (the cutoff) with realizations in Θ and with distribution x. Then,

the allocation rule x can be implemented by drawing a realization c of the random

cutoff cx, and giving the good to the agent if and only if the reported type exceeds

c. In a cutoff mechanism, the signal distribution is determined (through the function

γ) by the realization of the random cutoff cx representing the allocation rule x. That

is, conditional on the cutoff, the signal is independent of the report of the agent. The

signal in a cutoff mechanism can be an arbitrary garbling of cx. In the binary model, it

is without loss of generality to focus on binary signals. Therefore, the signal function γ

is one-dimensional: γ(c) is the probability of recommending the high action conditional

on cutoff realization c.

Using the results from the companion paper, I provide the following alternative

characterization of cutoff mechanisms, which is often easier to work with.

Fact 2. A mechanism frame (x, q) is a cutoff rule if and only if x(θ)q(θ) and x(θ)(1−q(θ)) are both non-decreasing in θ.

5 The reader is referred to the companion paper for a discussion of why cutoff mechanisms are aninteresting class to study. This paper takes the class as given, and analyzes conditions under whichcutoff mechanisms are optimal, without any reference to their additional desirable properties.

3 Pure information intermediation 8

2.3 Preferences

The properties of optimal mechanisms will depend primarily on monotonicity properties

of the objective function and the constraints. The following definitions play a key role

in the analysis.

Definition 3. A function Φ : {l, h} × Θ → R is submodular if Φh(θ) − Φl(θ) is non-

increasing in θ, and is supermodular if Φh(θ)− Φl(θ) is non-decreasing in θ.

Definition 4. The function Ua(θ) = ua θ + ca is strongly submodular if uh = 0 and

ul > 0, and is strongly supermodular if uh > 0 and ul = 0.

Strong submodularity implies submodularity because the former property only re-

quires that uh ≤ ul.

Definition 5. The preferences of two players are co-modular if their respective util-

ity functions are either both submodular or both supermodular. If one of the utility

functions is supermodular and the other one is submodular, the preferences of the two

players are called counter-modular.

Co-modularity is a notion of aligned preferences, in the sense that players with co-

modular preferences agree on the direction of the single crossing condition with respect

to the action a and the type θ. Counter-modularity is a notion of misaligned preferences.

Definition 6. The preferences of two players are strongly co-modular (strongly counter-

modular) if they are co-modular (counter-modular), one of the players is the agent, and

the agent’s utility is strongly submodular or strongly supermodular.

Strong counter-modularity differs from counter-modularity only in that the agent’s

utility is assumed to take the strong from of sub/supermodularity (see Definition 4).

3 Pure information intermediation

To understand the role that co-modularity and counter-modularity play in determining

how much information a mechanism can reveal in an incentive-compatible way, I study

an auxiliary problem. I assume that x(θ) is constant in the type θ so that the designer

engages in pure information intermediation: she elicits reports from the agent and sends

messages to the third party, without the possibility to influence the allocation.6 The

designer can still use transfers and has full commitment power.

6 It is without loss of generality to assume that x(θ) = 1, for all θ.

3 Pure information intermediation 9

Theorem 1. Suppose that x(θ) is constant, and the agent’s and the third party’s pref-

erences are counter-modular. Then, any implementable mechanism frame (x, q) reveals

no information.

The theorem implies that if the designer attempts to send non-redundant signals in

the mechanism, the agent will misreport making the signals uninformative. The only

mechanisms consistent with truth-telling are ones that reveal no information about the

type of the agent.

To gain intuition for Theorem 1, consider the case when the agent’s utility is super-

modular (then, the third party’s utility is submodular). High types of the agent have

a higher willingness to pay for signals that lead to a high action of the third party.

However, the third party has incentives to take a high action only when she believes

that the agent’s type is low, that is, after seeing a signal that is chosen more often

by low types. We get a contradiction: If the designer sets a relatively high price for

a signal that leads to a high action, then only high types want to choose that signal

but then that signal cannot lead to a high price. And if the price for the high signal is

relatively low, then all types choose it, and hence the signal is uninformative.

If counter-modularity is replaced with co-modularity, the incentives of the agent

and the third party become more aligned, and the mechanism designer can make a

non-trivial impact on the information structure of the aftermarket. An easy example is

the case in which the third party and the agent share the same supermodular objective

function – then, the mechanism designer can fully reveal the type of the agent in the

mechanism (by appropriately setting up transfers).7

Intuitively, the ability of the designer to release information in the model with a

constant allocation rule can come from two sources: commitment power and the use

of transfers. Commitment power means that the designer can commit to a signal

distribution as a function of the type of the agent. Transfers can be used to screen

types with different willingness to pay. The third party does not have these tools since

she simply takes a binary action. To understand the difference between counter- and

co-modularity, it is instructive to consider the (hypothetical) case in which the third

party is allowed to use commitment power and transfers. Formally, suppose that the

third party offers a mechanism with transfers to the agent. The mechanism is a menu of

distributions over actions of the third party offered at difference prices. The third party

7 Crawford and Sobel (1982) study a related model with cheap talk. That is, in their model,communication cannot be supported with transfers, and no player has commitment power. Theirresults on (im)possibility of communication have similar intuition.

4 Optimal mechanisms 10

maximizes the expectation of va(θ) but has no utility from the transfers (equivalently,

is required to run a budget-balanced mechanism).

When the preferences of the agent and the third party are counter-modular, it is easy

to show that the optimal mechanism elicits no information from the agent (hence, the

decision of the third party is constant). In other words, commitment power and transfers

are not useful in eliciting information in this case. However, when the preferences of

the agent and the third party are co-modular, the optimal mechanism divides the type

space into two intervals, and the high decision is taken when the type of the agent

lies in the high interval. In this case commitment power and transfers are effective in

eliciting information.

In the actual pure information intermediation problem, it is the designer who can use

commitment and transfers, rather than the third party. However, the intuition remains

the same: In the case of co-modularity, the mechanism can release information.

Theorem 1 can be extended to non-constant allocation rules that take the form of

a threshold rule.

Corollary 1. If the allocation rule x is a threshold rule, x(θ) = 1{θ≥θ?}, any imple-

mentable mechanism (x, q) reveals no information.

The corollary follows directly from Theorem 1 by considering the truncated type

space [θ?, 1]. Signals sent conditional on types in [0, θ?) play no role because these

types do not participate in the aftermarket.

The main conclusion of this section is that if the agent’s and the third party’s

preferences are counter-modular, then information disclosure is only possible when the

allocation rule is non-constant. This will be the crucial force behind optimality of cutoff

mechanisms.

4 Optimal mechanisms

Under the assumptions of Section 2, the mechanism designer solves

maxx, q

ˆ 1

0

(V h(θ)q(θ)x(θ) + V l(θ)(1− q(θ))x(θ)

)f(θ)dθ (4.1)

subject to (M), (OBl), and (OBh).

I introduce optimal mechanisms in two steps. In the first step, I consider a problem

in which the allocation rule x is fixed, and the designer optimizes over disclosure rules

4 Optimal mechanisms 11

(the crucial difference to Section 3 is that x is not necessarily constant in the type).

In the second step, I consider joint optimization. Throughout, I focus on sufficient

conditions for optimality of cutoff mechanisms. Alternative optimal mechanisms are

discussed in Section 7.

4.1 Optimal information disclosure

In this subsection, I fix a non-decreasing allocation rule x and optimize over disclosure

rules.8 The content of this subsection can be interpreted in two ways. First, solving

for the optimal disclosure rule q given an allocation rule x is an intermediate step

towards solving the full design problem. Second, x can be interpreted as an interim

expected allocation in a multi-agent mechanism. The results of this subsection will be

immediately applicable to designing optimal disclosure policies in auctions (see Sections

5 and 6).

When the allocation rule is fixed, the objective function (4.1) becomes (up to a

constant that does not depend on q)

maxq

ˆ 1

0

(V h(θ)− V l(θ)

)q(θ)x(θ)f(θ)dθ (4.2)

Theorem 2. Fix a non-decreasing allocation rule x. Suppose that (i) the agent’s and

the third party’s preferences are strongly counter-modular, and (ii) the designer’s and

the third party’s preferences are co-modular. Then, there exists a cutoff rule (x, q?)

such that q? is a solution to the problem (4.2) subject to (M), (OBl), and (OBh).

Assumption (i) of Theorem 2 is essential for the result. Its informal meaning is that

the structure of the aftermarket makes it “hard” to disclose information in the mech-

anism. Theorem 1 states that under counter-modularity of the agent’s and the third

party’s preferences, no information can be revealed by a mechanism with a constant

allocation rule. In a cutoff mechanism with a constant allocation rule, no information

can be revealed either because the cutoff corresponding to a constant allocation rule is

8 The results of this section easily generalize to the case of allocation rules that are not non-decreasing. The optimal solution in this case can be obtained by replacing x(θ) in the monotonicityconstraint (derived from condition M) by its lower monotone envelope, denoted x(θ), and defined as

x(θ) = sup{χ(θ) : χ(θ) ≤ x(θ), ∀θ, χ is non-decreasing}.

Because I give conditions for optimality of using a non-decreasing allocation rule in the next subsection,there is no need for me to consider this more general case.

4 Optimal mechanisms 12

a degenerate (deterministic) random variable. For a general allocation, a cutoff mech-

anism uses the allocation rule x as a “leverage” to elicit and reveal information about

the corresponding cutoff cx. As shown in the companion paper, this implies that a

cutoff rule is implementable regardless of the form of the aftermarket, that is, even if

the misaligned preferences in the aftermarket make it “hard” to disclose information in

the mechanism. In other words, information about the cutoff can always be disclosed

without violating incentive-compatibility of the mechanism.

Theorem 2 states that for counter-modular aftermarkets no information other than

the information about the cutoff is used at the optimal mechanism. When assumption

(i) fails, it is typically possible to reveal more information. Therefore, an optimal

mechanism may reveal more information than just information about the cutoff. Section

7 analyzes the structure of optimal mechanisms without assumption (i).

Assumption (ii), on the other hand, is a technical condition that simplifies solving

the problem. When the preferences of the third party and the mechanism designer are

co-modular, it is possible to improve any suboptimal mechanism by shifting probability

mass under q in the direction that increases the objective function (4.2) and preserves

the obedience constraint (OBh). This allows me to solve the problem by defining an

order (similar to first-order stochastic dominance) on the set of feasible mechanisms,

and arguing that the optimal mechanism must be a maximal point in that order. When

the preferences of the designer and the third party are counter-modular, the problem

becomes more difficult because no such order can be defined. Optimal control theory

can be used but the problem is intractable in many cases. This is because, unlike in

traditional mechanism design, the monotonicity constraint (M) will typically bind at

the optimal solution. In Section 6, I analyze several optimization problems in which

assumption (ii) is violated but a cutoff mechanism is nevertheless optimal.

4.2 Joint optimization

I turn attention to joint optimization over allocation and disclosure rules. Using The-

orem 2, I can provide the following sufficient conditions for optimality of cutoff mech-

anisms.

Theorem 3. Suppose that either

• the agent’s utility is strongly supermodular, the third party’s and the designer’s

utilities are submodular, and V l(θ) is non-decreasing, or

5 Multi-agent mechanisms 13

• the agent’s utility is strongly submodular, the third party’s and the designer’s

utilities are supermodular, and V h(θ) is non-decreasing.

Then, a cutoff mechanism is optimal for the problem (4.1) subject to (M), (OBl), and

(OBh).

Examples satisfying the assumptions of Theorem 3 are provided in Section 6 which

considers applications of the model.

The companion paper Dworczak (2016) establishes a general result about optimality

of no information disclosure in the class of cutoff mechanisms, when there is one agent in

the mechanism, and the designer optimizes jointly over allocation and disclosure rules.9

Thus, a corollary of Theorem 3 is that the optimal mechanism reveals no information

(in the sense defined in Subsection 2.1).

Corollary 2. Under the assumptions of Theorem 3, there always exists an optimal

mechanism that reveals no information.

The result should be properly interpreted. The definition of a no-information-

revealing mechanism is that the mechanism does not send informative signals. However,

even in the absence of explicit signaling, the choice of the allocation rule and the fact

that the trade took place will influence the aftermarket beliefs. Thus, the aftermarket

will in general impact the structure of the optimal mechanism.

Corollary 2 does not extend to the multi-agent setting. An optimal cutoff mechanism

often sends explicit signals when there are multiple agents. I consider this case in the

next subsection.

5 Multi-agent mechanisms

In this section, I extend the model to multi-agent symmetric settings. I maintain the

assumption that only the agent who acquires the object in the mechanism interacts in

the aftermarket.

There are N ex-ante identical agents, indexed by i = 1, 2, ..., N . Each agent i has a

privately observed type θi ∈ Θ. Types are distributed i.i.d. according to a full-support

distribution f on Θ ≡ [0, 1]. The payoff of the designer and the third party may depend

9 This result does not depend on the objective function and the form of the aftermarket, so it isimmediately applicable here.

5 Multi-agent mechanisms 14

on the type of the agent in the aftermarket but not on the agent’s identity. Therefore,

the utility functions V a(θ) and va(θ) take the same form as in the one-agent model.

Under these assumptions, it is without loss of generality to look at symmetric mech-

anisms. I consider Bayesian implementation.10 Symmetric N -agent mechanisms can be

represented by their reduced forms (x, π, t), where x : Θ → [0, 1], π : Θ → ∆(S),

and t : Θ → R are all one-dimensional functions, subject to the constraint that x is

feasible under f for some joint N -dimensional allocation rule x with∑N

i=1 xi(θ) = 1

for all θ ∈ ΘN :

x(θ) =

ˆ

ΘN−1

xi(θ, θ−i)∏j 6=i

f(θj)dθj. (5.1)

For non-decreasing interim allocation rules x, condition (5.1) is equivalent to the so-

called Matthews-Border condition:

ˆ 1

τ

x(θ)f(θ)dθ ≤ 1− FN(τ)

N, ∀τ ∈ [0, 1], (MB)

If the allocation rule x is not non-decreasing, condition (MB) is necessary but no longer

sufficient (see Matthews, 1984, and Border, 1991). I will consider the relaxed problem

with constraint (MB). Thus, the obtained solution is guaranteed to be feasible only if

the optimal x turns out to be non-decreasing (which will be the case in all subsequent

results).

As before, it is without loss of generality to look at binary signal spaces, S = {l, h}.Then, letting q(θ) denote the probability of sending the high signal conditional on type

θ and allocating the object, any mechanism can be represented by its reduced form

(x, q, t).

Under Bayesian implementation, conditions for implementability of (x, q) are for-

mally identical to those from the one-agent model. That is, equations (M), (OBl),

(OBh) together with (MB) fully characterize all implementable pairs (x, q).

Finally, the objective function of the mechanism designer is given by

N

ˆ 1

0

(V h(θ)q(θ)x(θ) + V l(θ)(1− q(θ))x(θ)

)f(θ)dθ (5.2)

which only differs from the one-agent objective function in that it is multiplied by N .

A symmetric mechanism in the multi-agent setting is defined as a cutoff mechanism

10 Under sufficient conditions for optimality of cutoff mechanisms, the optimal mechanism will bedominant-strategy incentive-compatible, by the results in the companion paper Dworczak (2016).

6 Applications 15

if its reduced form is a one-agent cutoff mechanism.

For a fixed interim allocation rule, we obtain a problem that is formally identical

to the one-agent problem considered in the previous sections (the additional constraint

MB only pertains to the allocation rule). Therefore, Theorem 2 applies without any

modifications (with x interpreted as an interim allocation rule). Theorem 3 can be

extended as well, although this requires a proof.

Theorem 4. Suppose that either

• each agent’s utility is strongly supermodular, the third party’s and the designer’s

utilities are submodular, and V l(θ) is non-decreasing, or

• each agent’s utility is strongly submodular, the third party’s and the designer’s

utilities are supermodular, and V h(θ) is non-decreasing.

Then, a cutoff mechanism is optimal for the problem (5.2) subject to (M), (OBl),

(OBh), and (MB).

6 Applications

In this section, I present three applications. In the first application, I explicitly solve

for optimal mechanisms. In the second and third application, I only show that the

optimal mechanism is a cutoff mechanism. Optimization in the cutoff class can then

be performed in a way analogous to that in the first application.

6.1 Resale

In the first example, the aftermarket is a resale game. Resale after auctions (or bilat-

eral trade) is a common phenomenon in financial over-the-counter markets, treasury

auctions, spectrum auctions, or art auctions.

The model is stylized to keep the binary structure assumed in this paper. There

are N agents, where N ≥ 1. The type θi of agent i is interpreted as the probability of

an initially unknown value for the object. The value can be high (vh) or low (vl), and

is learned by the agent upon acquiring the object. The third party has a value v for

holding the object, with v > vh > vl ≥ 0, and makes a take-it-or-leave-it offer to the

agent in the aftermarket.

Because of the binary value of the agent in the aftermarket, it is without loss of

generality to assume that the third party will offer a price vh or vl. Thus, this setting

6 Applications 16

admits the structure of the baseline binary model. Any agent i always accepts the

offer vh, and accepts offer vl only if her ex-post value is low, i.e. with ex-ante interim

probability 1 − θi. Thus, in equation (2.1) we have uh = 0, ch = vh, ul = (h − l),

cl = vl, i.e. agent’s utility is strongly submodular. The third party has vh(θ) = v − vhand vl(θ) = (1− θ)(v − vl), i.e. the third party’s utility is supermodular.

I will consider two objective functions of the mechanism designer: efficiency and

revenue. Under the assumption that V h(θ) is non-decreasing in θ, let γh be the smallest

number on [0, 1] such that V h(θ) ≥ 0 for all θ ≥ γh. To avoid trivial cases, I assume

that, ˆ 1

γh(vh(θ)− vl(θ))FN−1(θ)f(θ)dθ < 0. (6.1)

If condition (6.1) fails, it is optimal for the third party to take the high action under the

“myopically optimal” allocation rule – allocate to the agent with the highest type (or

to the only agent if N = 1) as long as that type exceeds the threshold γh above which

the objective function is non-negative. Because the high action is always preferred by

the designer to the low action, the mechanism that implements this myopically optimal

allocation rule and discloses no information achieves the upper bound on the payoff to

the mechanism designer, and is hence trivially optimal. Assumption (6.1) implies that

this upper bound is not achievable.

6.1.1 Socially optimal mechanisms

Suppose that the mechanism designer maximizes efficiency in the market. When the

resale price is high, the total surplus (conditional on allocating the good) is v, and

otherwise it is (1− θ)v+ θvh because only low-value agents resell for a low price. Thus,

V h(θ) = v, and V l(θ) = (1 − θ)v + θvh, i.e. the designer’s utility is supermodular. By

Theorem 2, a cutoff mechanism is optimal for any fixed non-decreasing allocation rule.

By Theorem 3, because V h(θ) is non-decreasing in θ, a cutoff mechanism is also optimal

for the joint optimization problem. By Corollary 2, the optimal mechanism reveals no

information when N = 1.

The rest of this subsection describes the optimal cutoff mechanism (which is also

the optimal mechanism overall) in three cases: optimization over disclosure rules, joint

optimization with one agent, and joint optimization with multiple agents.

Optimal information disclosure.

6 Applications 17

Claim 1. For a fixed non-decreasing (interim) allocation rule x, suppose that

ˆ 1

0

(θ(v − vl)− (vh − vl))x(θ)f(θ)dθ ≥ 0. (6.2)

Then, the socially optimal mechanism that implements x reveals no information. If

condition (6.2) fails, define xres as the smallest solution to the equation

ˆ 1

0

(θ(v − vl)− (vh − vl)) max{x(θ)− xres, 0}f(θ)dθ = 0. (6.3)

Then, the socially optimal mechanism is given by q(θ) = max{1− xres/x(θ), 0}.

When condition (6.2) holds, it is optimal not to send any signals in the mechanism

because in the absence of additional information, the third party takes the high action.

To understand the case when (6.2) fails, define θ?res by

θ?res = sup{θ ∈ Θ : x(θ) ≤ xres}. (6.4)

When x is continuous, xres = x(θ?res). The optimal mechanism recommends the low

action with conditional probability one when the good is allocated to a type θ below

θ?res, and with conditional probability xres/x(θ) when the good is allocated to a type

θ above θ?res. The intuition is that the mechanism has to exclude enough low types

from the high signal to induce the high action of the third party. This is possible when

x(θ) is non-constant and non-decreasing: The unconditional probability of sending a

high signal for type θ ≥ θ?res is equal to x(θ)− xres, so that higher types have a higher

probability of receiving a high price in the aftermarket. The unconditional probability of

sending the low signal is constant and (in general) non-zero for all types above θ?res. This

is necessary to keep the mechanism incentive-compatible. If the highest type received

the high price with probability one, low types would deviate and report a high type.

The non-zero probability of a low signal provides the necessary separation between low

and high types (only when the low signal is sent, high types have a strictly higher value

for winning the object).

Suppose that N ≥ 2, and x(θ) is the interim allocation rule FN−1(θ) corresponding

to an auction that allocates to the highest type. Then, the optimal disclosure rule is

to announce whether the second highest type was above or below θ?res. The optimal

mechanism is indeed a cutoff mechanism because the second highest type (the highest

competing type from the perspective of the winner) is the cutoff representing x. The

6 Applications 18

mechanism can be implemented by running a second price auction and announcing

whether or not the price paid by the winner exceeded a threshold p?res, where p?res is the

bid made by type θ?res in a monotone equilibrium of the auction.

Optimal mechanism for N = 1. When N = 1, joint optimization over allocation and

disclosure rules yields a mechanism that reveals no information, by Corollary 2.

Claim 2. When N = 1, one of the following two mechanisms is optimal:

(a) x(θ) = 1 and q(θ) = 0, for all θ,

(b) x(θ) = 1{θ≥θ}, and q(θ) = 1, where θ is defined by

Ef [θ| θ ≥ θ] =vh − vlv − vl

.

Mechanism (a) is optimal if and only if

Ef [θ] ≤v

v − vhF (θ).

The intuition for Claim 2 is straightforward given Corollary 2. The optimal mecha-

nism releases no information, so it either always induces the low price (case a) or always

induces the high price (case b). If the designer is not trying to affect the default price

in the aftermarket (which is low under assumption 6.1), it is optimal to always allocate

the object because the objective function is non-negative. To induce the high price, the

designer excludes low types from trading: The threshold θ is chosen so that the third

party is exactly indifferent between the high and the low price (and quotes the high

price).

Optimal mechanism for N > 1. Finally, I present results about optimal mechanisms

for the case of multiple agents.

Claim 3. Under assumption (6.1) which takes the form Ef [θ(1)N ] < (vh − vl)/(v −

vl), where θ(1)N denotes the first order statistic of (θ1, ..., θN), one of the following two

mechanisms is optimal when N > 1 :

6 Applications 19

(a) For some type θ? ∈ (0, 1)11

x(θ) =

(1/N)FN−1(θ?) θ < θ?

FN−1(θ) θ ≥ θ?

and

q(θ) = max

{1− (1/N)FN−1(θ?)

FN−1(θ), 0

},

(b) x(θ) = FN−1(θ)1{θ≥r?} and q(θ) = 1, where r? is defined by

Ef [θ(1)N | θ

(1)N ≥ r?] =

vh − vlv − vl

.

Mechanism (a) is optimal whenever the regularity condition (A.42) defined in Ap-

pendix A.7 holds.12

I focus on case (a) in the discussion. (Appendix A.7 contains the discussion of case

b.) The following indirect implementation of the optimal mechanism from case (a) is

possible. The designer names a price p?, and agents simultaneously accept or reject.

If all agents reject, the object is allocated uniformly at random. If exactly one agent

accepts, she gets the object at price p?. If more than one agent accept, the designer runs

a tie-breaking auction with reserve price p? among agents who accepted. The designer

only reveals whether the auction took place or not.

Intuitively, in order to induce a high price with positive probability, the designer

runs a two-step procedure, and announces whether the second step (the auction) was

reached. The auction is a signal of high value of the winner of the object. The price

p? is set in such a way that conditional on announcing that the auction took place, the

third party is indifferent between the high and low price (and quotes the high price).

To gain intuition for the optimal design of the allocation rule, suppose that no

agent accepts the initial price p?. Conditional on this event, the low price vl will be

offered in the second stage. To maximize the probability of resale (which is consistent

with social surplus maximization because the third party has a higher value than the

agent), the designer should allocate to the lowest type. However, incentive-compatibility

constraints make it impossible to allocate to low types more often than to high types.

Therefore, the mechanism allocates the object by a uniform lottery.

11 See equation (A.39) in Appendix A.7.12 The regularity condition is satisfied, for example, by all distributions F (θ) = θκ for κ > 0.

6 Applications 20

6.1.2 Profit-maximizing mechanisms

In this subsection, I derive the profit-maximizing mechanisms for the resale model. I

let J(θ) ≡ θ − (1 − F (θ))/f(θ) denote the virtual surplus function. I say that the

distribution F is regular when J(θ) is non-decreasing in θ. I denote

J = max{J ′(θ) : θ ∈ Θ},

and assume that J is well defined and finite.

Using the envelope formula, I can express information rents of an agent with type

θ as

U(θ) = U(0) + (vh − vl)ˆ θ

0

(1− q(τ))x(τ)dτ.

In the revenue-maximizing mechanism, U(0) = 0. Thus, transfers are uniquely pinned

down and the objective function of the designer can be shown to be

ˆ 1

0

[vhx(θ) + (vh − vl)(J(θ)− 1)(1− q(θ))x(θ)]f(θ)dθ.

Thus, we can take V h(θ) = vh and V l(θ) = vh − (vh − vl)(1− J(θ)). If the distribution

F is regular, V a(θ) is submodular.

Optimal information disclosure. I cannot apply Theorem 2 directly because the pref-

erences of the mechanism designer and the third party are not co-modular. However,

under additional regularity assumptions, the problem can be solved by applying optimal

control techniques.

Claim 4. Fix a non-decreasing and absolutely continuous (interim) allocation rule x.13

Further, suppose that F is regular, and that

vh − vlv − vl

≤ E[θ| θ ≥ θ?res] +1− θ?resJ

, (6.5)

where θ?res was defined in (6.4). Then, the highest expected revenue over all mechanisms

implementing x can be obtained by using a cutoff mechanism. Moreover, in this case, the

profit-maximizing mechanism coincides with the welfare-maximizing mechanism from

Claim 1. If F is the uniform distribution on [0, 1], condition (6.5) holds.

13 It is enough if x is absolutely continuous on {θ ∈ [0, 1] : x(θ) > 0}, i.e.x can be equal to zero insome initial interval.

6 Applications 21

Optimal mechanism for N = 1 Because the joint optimization problem is an optimal

control problem with two control variables and a monotonicity constraint, it is in general

difficult to solve. I focus on the case in which I can solve the problem by relaxing the

monotonicity constraint.14 I do not have to assume regularity of the distribution F but

instead (for technical reasons) I assume that the virtual surplus function J(θ) is convex.

Claim 5. Suppose that J is convex. Define θ by

Ef [θ| θ ≥ θ] =vh − vlv − vl

. (6.6)

If vl + (vh − vl)J(θ) ≤ 0 for all θ ≤ θ, then the profit-maximizing mechanism is given

by x(θ) = 1{θ≥θ}, and q(θ) = 1.

The optimal mechanism under the assumption of Claim 5 is a cutoff mechanism, and

thus, by Corollary 2, reveals no information. The allocation rule excludes just enough

low types from trading so that a high price is quoted in the aftermarket conditional on

trade in the mechanism.

Suppose for example that F is the uniform distribution on [0, 1], and vl = 0. Then, θ

defined by (6.6) is given by θ = 2vh/v − 1, and is contained in (0, 1] under assumption

(6.1). When vh/v ≤ 3/4, it is optimal to sell to all types above θ and reveal no

information. When vh/v > 3/4, so that θ > 1/2, it becomes harder to induce a high

price in the aftermarket, in the sense that the mechanism has to exclude even relatively

high types from trading. At some point, it becomes optimal not to induce a high price

at all, in which case the aftermarket has no influence on the agent’s value – the optimal

mechanism is identical to the one that would arise in the absence of an aftermarket (i.e.

the seller sells to all types with non-negative virtual surplus).

Optimal mechanism for N > 1 The optimal mechanism for the case N > 1 can be

quite complicated, and I only offer an informal discussion based on numerical solutions.

If the value of the third party v is relatively large relative to vh (fixing vl), so that it

is relatively easy to induce a high price in the aftermarket, the optimal mechanisms

will often take the form analogous to that in Claim 5. The seller runs an auction in

which the good is allocated to the highest type subject to a reserve price. The reserve

price is chosen in such a way that conditional on allocating the object the third party

14 In other cases, the monotonicity constraint will bind at the optimal solution, and standard optimalcontrol techniques cannot be applied, especially that one needs to allows for jumps in the variables.

6 Applications 22

is indifferent between offering a high and a low price (and offers a high price). No

additional information is revealed.

However, when vh is relatively close to v (fixing vl), the reserve price would have

to be very high in order to induce a high price in the aftermarket. There are cases

in which the optimal mechanism is still a cutoff mechanism but sends explicit (binary

signals). The optimal allocation rule in this case is similar to that from point (a) of

Claim 3 but can feature multiple regions of either (i) exclusion from trade, (ii) uniform

randomization, and (iii) allocation to the highest type.

6.2 Acquiring a complementary good

In this subsection, I consider a different example of an aftermarket game. After the

agent acquires the object in the mechanism, she can buy a complementary good from

a monopolist (third party). The combined value for holding both objects is high (vh)

or low (vl), with ex-ante probability αθ+ β, and 1−αθ− β, respectively, where α > 0,

β ≥ 0 and α + β ≤ 1. If the agent fails to acquire the complementary good in the

aftermarket, she gets a reservation value r ≥ 0. It is assumed that r < vl < vh. The

monopolist quotes an optimal monopoly price given the information revealed by the

first-stage mechanism.

In this setting, the third party quotes either a price vl−r or vh−r. The high action

corresponds to high probability of trade in the aftermarket, i.e. a low price quoted by

the third party. Thus, uh = α(vh − vl), ch = r+ β(vh − vl), ul = 0, and cl = r. Agent’s

utility is strongly supermodular. Moreover, vh = vl − r and vl = (αθ + β)(vh − r), so

the third party’s utility is submodular.

Socially optimal mechanisms Efficiency maximization corresponds to V l(θ) = (αθ+

β)vh + (1−αθ−β)r, and V h(θ) = (αθ+β)vh + (1−αθ−β)vl. The designer’s utility is

submodular. Theorem 2 implies that a cutoff mechanism is optimal when the designer

optimizes over disclosure rules for any fixed allocation rule. Theorem 3 and Theorem

4 imply that a cutoff mechanism is optimal for the joint design problem, regardless of

the number of participating agents.

Profit-maximizing mechanisms By an analogous derivation as in Subsection 6.1, we

obtain V h(θ) = r+β(vh−vl)+α(vh−vl)J(θ), V l(θ) = r. Thus, utility is supermodular as

long as the distribution F is regular. I cannot directly apply Theorems 2 - 4. However,

7 Counterexamples and robust payoff bounds 23

under regularity conditions similar to those in Claim 4 and Claim 5, a cutoff mechanism

can be shown to be optimal.

6.3 Lemons market

Suppose that the third party has value v(θ) for holding the asset, where v(θ) is a

continuous non-decreasing function. I assume that v(θ) ≥ θ, i.e. it is always socially

efficient for the third party to be the final holder of the good. For simplicity, and to

keep the binary structure of the model, I assume that the price in the aftermarket is

fixed at p. It is without loss of generality for a model with fixed allocation x to assume

that p = 1.15 The third party decides whether to trade or not, taking into account the

adverse selection problem.

In this setting, the high action corresponds to the decision of the third party to

trade. For the agent, we have uh = 0, ch = 1, ul = 1, and cl = 0 – utility is strongly

submodular. The utility of the third party is given by vh(θ) = v(θ)− p, vl(θ) = 0, and

is thus supermodular.

Socially optimal mechanisms If the mechanism designer wants to maximize effi-

ciency, we have V h(θ) = v(θ), V l(θ) = θ. If v(θ)− θ is non-decreasing (this is case for

example when v(θ) = κθ for some κ > 1, or when v(θ) = θ + δ for some δ > 0), then a

cutoff mechanism is optimal, by Theorems 2 - 4.

Profit-maximizing mechanisms To maximize revenue, the designer would set V h(θ) =

p, V l(θ) = J(θ). Theorem 2 cannot be applied directly but sufficient conditions can be

derived for a cutoff mechanism to be optimal, in a fashion similar to Claims 4 and 5.

7 Counterexamples and robust payoff bounds

In this section, I analyze cases in which the assumption of strong counter-modulairty of

the agent’s and the third party’s preferences fails. First, I consider the effects of relaxing

counter-modularity altogether, and show that when the preferences of the agent and

the third party are co-modular, more information about the agent can be revealed by

the mechanism, compared to a cutoff mechanism. Second, I consider the consequences

of relaxing strong counter-modularity to counter-modularity.

15 Types above p are irrelevant because they never resell. It is thus without loss of generality toassume that all types are below p, or that p = 1.

7 Counterexamples and robust payoff bounds 24

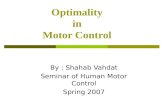

Fig. 7.1: A Cutoff Mechanisms versus a Partitional Mechanism

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 10

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

θ

A Binary Cutoff Mechanism

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 10

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

θ

A Binary Partitional Mechanism

q(θ)x(θ)(1-q(θ))x(θ)x(θ)

High Action

HighAction

Low Action Low Action

7.1 Relaxing counter-modularity

The following definition introduces a class of mechanisms that will emerge as optimal

under co-modularity of the agent’s and third party’s preferences.

Definition 7. A mechanism frame (x, q) is a partitional mechanism if the signal is a

deterministic function of the type: q(θ) ∈ {0, 1}, for all θ ∈ Θ.

A partitional mechanism defines a binary partition of the type space, with the two

sets in the partition corresponding to the two possible actions of the third party. In

an implementable partitional mechanism, the partition consists of two intervals. A

partitional mechanism is typically not a cutoff mechanism, and vice versa (the only

exceptions are boundary cases, for example, a mechanism that makes no announcements

is both a partitional and a cutoff mechanism). Figure 7.1 contrasts a typical shape of

a cutoff and a partitional mechanism.

Co-modularity of the agent’s and the third party’s utilities can be interpreted as a

notion of aligned preferences. It is thus easier to support information disclosure in the

aftermarket. As a result, the optimal mechanism reveals more information about the

type of the agent, in the sense that the posterior belief is a partition.

Theorem 5. Fix any allocation rule x. If (i) the agent’s and the third party’s prefer-

ences are strongly co-modular and (ii) the designer’s and the third party’s preferences

are co-modular, then the optimal mechanism is a partitional mechanism.

7 Counterexamples and robust payoff bounds 25

Because Theorem 5 applies to any allocation rule (including allocation rules that

are not non-decreasing), its assumptions are also sufficient for optimality of partitional

mechanisms in the joint design problem, with one or multiple agents. Conditions (sim-

ilar to those in Theorems 3 and 4) can be provided under which a non-decreasing

allocation rule is optimal for the joint design problem.

The following example illustrates Theorem 5.

Example 1. A mechanism designer allocates a license that the agent must have in

order to pursue a project. Moreover, for the project to succeed, the agent needs to

receive external funding from the third party. If both of these elements are provided,

then the project succeeds with probability θ equal to the type of the agent. Otherwise,

the project fails for sure. If the project succeeds, it generates a payoff of 1.

In the mechanism, the designer allocates the license to the agent. In the aftermarket,

the third party takes a binary decision: invest or not. Investing incurs a sunk cost c but

in the event of a success, the third party receives a fraction β of the generated surplus.

The remaining fraction 1− β goes to the agent.

The designer maximizes the profit of the agent (or, equivalently, tax revenues for a

fixed tax rate τ) conditional on allocating the license, and receives a (possibly negative)

payoff π if the license is not allocated.

In this setting, uh = 1 − β, ul = 0, so the agent’s utility is strongly supermodular.

The designer’s objective is thus also supermodular. For the third party, vh(θ) = βθ− cand vl(θ) = 0, so the utility is supermodular. Theorem 5 implies that a partitional

mechanism is optimal.

Suppose that π is sufficiently negative so that the designer always allocates the

license. Then, the optimal mechanism charges a fee for the license to agents above a

threshold type α? but, in exchange, sends a message that induces the third party to

invest in the project. Agents below α? receive the license for free but the mechanism

sends a message that induces the third party not to invest. This simple communication

mechanism is possible because, unlike in the case of counter-modularity, higher types

of the agent have a higher willingness to pay for the high signal. At the same time, the

third party’s preferences are aligned – she is willing to take the high action when the

agent’s type is high.

7 Counterexamples and robust payoff bounds 26

7.2 Relaxing strong counter-modularity

In this section, I relax the assumption that the agent’s utility is strongly counter-

modular. Using an example, I show that the optimal mechanism may sometimes lie

outside of the cutoff class. However, I show that a cutoff mechanism is typically close

to optimal, in the sense that it achieves a large fraction of the optimal payoff in the

worst case.

The model I study is a simple variation of the resale model of Subsection 6.1 with

one agent. The only difference is that the aftermarket takes place with probability

λ ≤ 1. That is, with probability 1− λ, the third party is absent, and the agent enjoys

the utility of being the final holder of the asset. This may seem to be an innocuous

difference but it actually changes the structure of the optimal solution. In particular,

with λ = 1, it is never necessary to reveal information in the optimal mechanism but

with λ < 1 this is no longer true – sometimes the optimal mechanism will send explicit

signals.

With λ < 1, agent’s utility is still submodular but no longer strongly submodular.

To simplify notation, I will denote by E(θ) = θvh + (1 − θ)vl the expected value of

the agent in the absence of the aftermarket. We have Uh(θ) = (1− λ)E(θ) + λvh, and

U l(θ) = E(θ). Therefore, Uh(θ)−U l(θ) is non-increasing, as required by the definition

of submodularity, but because uh = (1− λ)(vh − vl) and ul = vh − vl, the utility is not

strongly submodular.

The mechanism designer maximizes the expectation of some generic function V a(θ),

for a ∈ {l, h} (which will typically depend on λ). I assume that V l(θ) and V h(θ) are

both non-decreasing. I define γa ∈ [0, 1] as the (largest) point at which V a(θ) = 0, for

a ∈ {l, h}.16 I assume that

ˆ 1

γh

(vh(θ)− vl(θ))f(θ)dθ < 0. (7.1)

If assumption (7.1) fails, the optimal mechanism is trivial: Allocate to all types above

γh and reveal no information (this is a special case of condition 6.1 with N = 1). I

define α? as the smallest solution to

ˆ 1

α

(vh(θ)− vl(θ))f(θ)dθ = 0. (7.2)

16 If V a(θ) does not cross zero at all, then γa = 0 if V a(θ) ≥ 0, and γa = 1 if V a(θ) ≤ 0.

7 Counterexamples and robust payoff bounds 27

That is, when the good is allocated only to types above α?, it is optimal for the third

party to offer a high price (assumption 7.1 implies that γh < α?).

Proposition 1. Under the above assumptions, the optimal mechanism takes one of the

two possible forms:

1. x(θ) = 1{θ≥γl}, q(θ) = 0 (no information is revealed and a low price is quoted in

the aftermarket),17

2.

x(θ) =

0 θ < γl,

1− λ γl ≤ θ < α?,

1 α? ≤ θ,

and q(θ) = 1{θ≥α?}.

Mechanism 1 is optimal if and only if

ˆ 1

γl

V l(θ)f(θ)dθ ≥ (1− λ)

ˆ α?

γl

V l(θ)f(θ)dθ +

ˆ 1

α?V h(θ)f(θ)dθ.

Mechanisms 1 is a cutoff mechanism but mechanism 2 is not (in fact, mechanism

2 is a partitional mechanism). In mechanism 2, types below γl do not get the object,

types in [γl, α?] receive the object with probability 1− λ and always face a low resale

price in the aftermarket (whenever it takes place), and types in [α?, 1] receive the object

with probability 1 and always face a high resale price in the aftermarket (whenever it

takes place).

To better understand the intuition for optimality of mechanism 2, it is useful to

compare it to the optimal cutoff mechanism. In one one-agent settings, optimal cutoff

mechanisms reveal no information (see Corollary 2). Therefore, it is easy to derive the

structure of the optimal cutoff mechanism (I omit the proof).

Proposition 2. Under the above assumptions, the optimal cutoff mechanism is either

mechanism 1 from Proposition 1, or mechanism 3: x(θ) = 1{θ≥α?}, q(θ) = 1 (no

information is revealed and a high price is quoted in the aftermarket) with α? defined

by (7.2).

17 For some parameters this mechanism is not feasible because a high price is optimal for the thirdparty when γl > α?. However, in this case mechanism 1 is going to be dominated by mechanism 2.

7 Counterexamples and robust payoff bounds 28

Mechanism 3 from Proposition 2 and mechanism 2 from Proposition 1 coincide

when λ = 1. However, mechanism 2 dominates when λ < 1. Both mechanisms induce

a high resale price for types above α?. It is not possible to induce a high resale price for

types below α? because, by definition, α? is the smallest threshold that still induces a

high resale price. However, mechanism 2 allocates to types below α? and recommends

a low price, while the cutoff mechanism 3 does not allocate at all.

To understand the difference, suppose first that λ = 1. Both mechanisms allocate

to types above α? and reveal no information. When the aftermarket takes place with

probability one, and the high price is always quoted by the third party, the agent’s

endogenous value for acquiring the object is equal to the resale price vh. In particular,

the value no longer depends on the agent’s type θ. As a consequence, the designer has to

charge exactly vh for reporting a type above α?, leaving the agent with no information

rents (if the agent received a positive information rent, types below α? would have

an incentive to misreport to also receive a positive rent). It follows that it is not

incentive-compatible to offer the good and recommend the low price to agents below

α?. Otherwise, higher types would have to be offered a strictly positive information

rent, contradicting the above reasoning.

Suppose now that λ < 1. In this case, even when a high resale price is quoted in the

aftermarket, higher types of the agent have a strictly higher value for the object (driven

by the event that the aftermarket does not take place and the agent is the final holder

of the good). Thus, types in [α?, 1] receive a positive information rent, proportional

to the probability of the aftermarket not taking place, 1 − λ. As a consequence, the

designer can sell the good to types below α? but only with sufficiently small probability

so that higher types do not want to deviate to reporting a type below α?. In the optimal

mechanism 2, the good is offered exactly with probability 1− λ (the probability of the

aftermarket not taking place) to types below α?. A low price is recommended for these

types, so it remains optimal for the third party to quote a high price for types above

α?.18

Intuitively, the slope of the agent’s utility (as a function of the type) determines

the ability of the designer to screen types by offering the good with different probabil-

ities. When the utility is flat, it is impossible to screen, but as it gets steeper, more

information can be elicited and revealed. The slope is determined by the action of

18 This would not be possible in a cutoff mechanism because the probability of recommending thelow price would have to be non-decreasing in the type, by Fact 2. It is not non-decreasing: the lowprice is never recommended for types above α?.

7 Counterexamples and robust payoff bounds 29

the third party. When λ = 1, the utility function can sometimes have a zero slope

(when the high price is offered) making screening impossible. When λ < 1, the slope

is bounded from below by (1− λ)(vh − vl). The optimal mechanism fully exploits this

lower bound to screen the agent’s type by offering the good with different probabili-

ties. Cutoff mechanisms, by design, reveal information about the cutoff, and are hence

incentive-compatible regardless of the slope of the agent’s utility in the aftermarket.

However, this also means that cutoff mechanisms do not fully exploit the lower bound

on the slope when λ < 1, and are hence suboptimal.

Calzolari and Pavan (2006) consider a similar model to the one above, with three

differences: (i) they assume that the agent’s type is binary (I model it as a continu-

ous variable), (ii) they consider revenue maximization (I allow an arbitrary objective

function), and (iii) they consider a stochastic binary value of the third party but as-

sume that the aftermarket always happens (I assume that the third party has a fixed

value which is higher than the value of the agent but the aftermarket happens with

interior probability). The effect of a stochastic value of the third party is similar to

the effect of an interior probability of the aftermarket: Instead of assuming that the

aftermarket does not take place, I could assume that the value of the third party is

below the value of the agent. As a result, the optimal mechanisms from Proposition

1 have similar structure to the optimal mechanisms from Calzolari and Pavan (2006)

(with some differences stemming from the discrete versus continuous types space).

One interesting insight from Propositions 1 and 2 relative to Calzolari and Pavan

(2006) is that the optimal mechanism reveals information only when there is non-zero

probability that there will be no gains from trade after the mechanism: either because

the aftermarket does not happen (as in my model), or because the third party has a

low value (as in the model of Calzolari and Pavan, 2006).

7.2.1 Robust payoff bounds

Propositions 1 and 2 imply that a cutoff mechanism may sometimes be suboptimal.

They do not directly show how much value the designer may lose by using a mechanism

in this class instead of the optimal mechanism. Under the assumptions of the previous

subsection, I provide robust payoff bounds on the performance of cutoff mechanisms.

Proposition 3a. If the objective is to maximize total expected surplus, then for any

7 Counterexamples and robust payoff bounds 30

fixed λ ∈ [0, 1] the optimal cutoff mechanism achieves at least a fraction

1

1 + 12(√λ− λ)

of the social surplus of the optimal mechanism.

In particular, regardless of λ, f , l, h, v, a cutoff mechanism is guaranteed to yield

more than 88% of the optimal surplus. Moreover, a cutoff mechanism is optimal at

λ = 0 and at λ = 1 (see Figure 7.2).

Proposition 3b. If the objective is to maximize expected revenue, and r ≡ vh/vl, then

for any fixed λ ∈ [0, 1] the optimal cutoff mechanism achieves at least a fraction

max

{1

2− λ,

1

1− λ(1− r)

}.

of the expected revenue of the optimal mechanism.

For example, if r = 1.5, then a cutoff mechanisms achieves at least 75% of the

optimal expected revenue in all cases. For any finite r, the gap disappears close to

λ = 0 and λ = 1 (see Figure 7.2).

For a general objective function of the designer, a weaker bound can be provided.

Proposition 3c. For a general objective function of the mechanism designer, a cutoff

mechanisms achieves at least a fraction

1

2− λ

of the value of the optimal mechanism.

A cutoff mechanism is always optimal when the probability λ of the aftermarket

is 1. As the probability of the aftermarket vanishes, the optimal cutoff mechanism

achieves at least half of the value of the optimal mechanism. This bound is driven by

cases in which the value from the optimal mechanism goes to zero as λ → 0. If the

payoff of the optimal mechanism is bounded away from zero, then cutoff mechanisms

are trivially optimal in the limit as λ → 0 because when there is no aftermarket,

information disclosure does not influence the outcomes in the mechanism.

7 Counterexamples and robust payoff bounds 31

Fig. 7.2: Robust payoff guarantees from using a cutoff mechanism: social surplus (solidline), revenue for vh/vl ≤ 1.5 (thick dotted line) and arbitrary objective (thindotted line)

0 0.2 0.4 0.6 0.8 150%

60%

70%

80%

90%

100%

Probability of aftermarket λ

References

Border, Kim C., “Implementation of Reduced Form Auctions: A Geometric Ap-

proach,” Econometrica, 1991, 59 (4), 1175–1187.

Calzolari, Giacomo and Alessandro Pavan, “Monopoly with resale,” RAND Jour-

nal of Economics, 06 2006, 37 (2), 362–375.

Crawford, Vincent P and Joel Sobel, “Strategic Information Transmission,”

Econometrica, November 1982, 50 (6), 1431–51.

Dworczak, Piotr, “Mechanism Design with Aftermarkets: Cutoff Mechanisms,”

Working Paper 2016.

Matthews, Steven A., “On the Implementability of Reduced Form Auctions,” Econo-

metrica, 1984, 52 (6), 1519–1522.

Myerson, Roger B., “Optimal Auction Design,” Mathematics of Operations Research,

1981, 6 (1), 58–73.

, “Optimal coordination mechanisms in generalized principal-agent problems,” Jour-

nal of Mathematical Economics, June 1982, 10 (1), 67–81.

A Proofs 32

Seierstad, A. and Knut Sydsaeter, Optimal Control Theory with Economic Appli-

cations, Elsevier, North-Holland, 1987. Advanced Textbooks in Economics, volume

24.

A Proofs

A.1 Proof of Theorem 1

Since x is constant, constraint (M) becomes

q(θ)(uh − ul) is non-decreasing in θ.

Take for concreteness the case when the agent’s utility is submodular, ul > uh (the

other case is fully analogous, and uh = ul is ruled out by assumption). Then, q has to

be non-increasing. By condition (OBh), the mean value theorem for integrals, and the

assumption that v is supermodular,

0 ≤ˆ 1

0

(vh(θ)− vl(θ))q(θ)f(θ)dθ = q(0+)

ˆ α

0

(vh(θ)− vl(θ))f(θ)dθ,

for some α ∈ [0, 1]. If q(0+) = 0, then q ≡ 0 because q is non-increasing. Otherwise,

we have ˆ α

0

(vh(θ)− vl(θ))f(θ)dθ ≥ 0

which, by the fact that v is supermodular, implies that