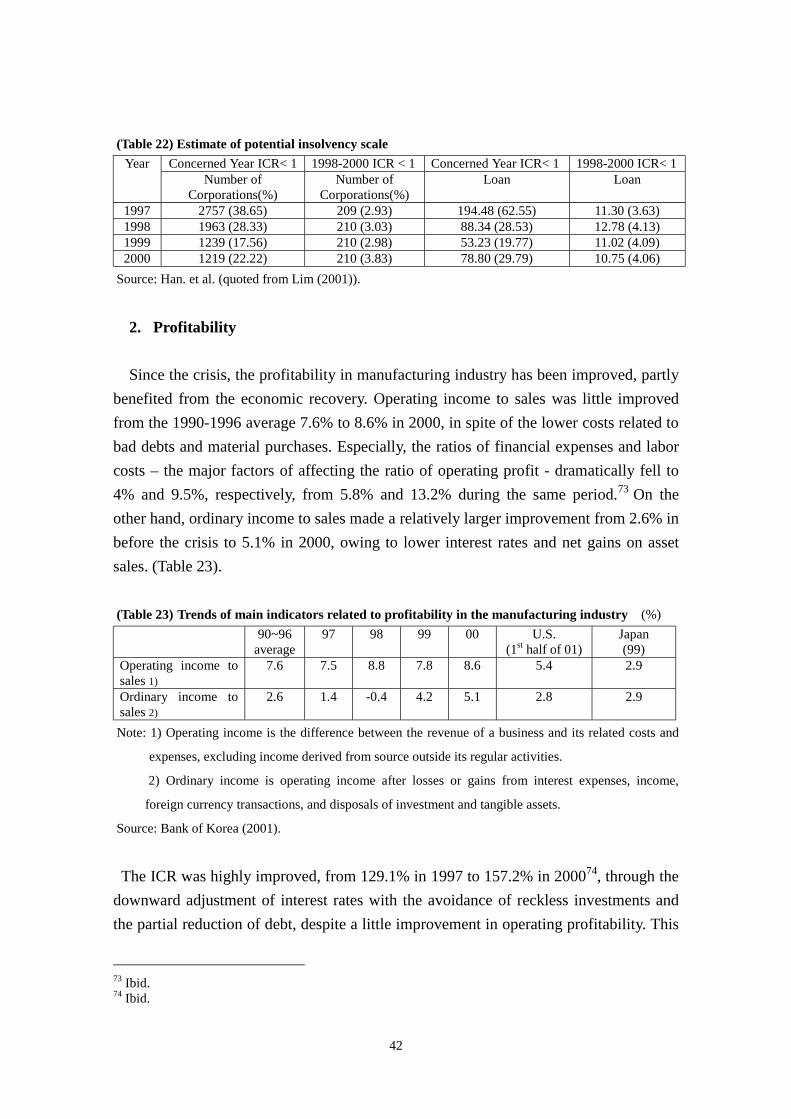

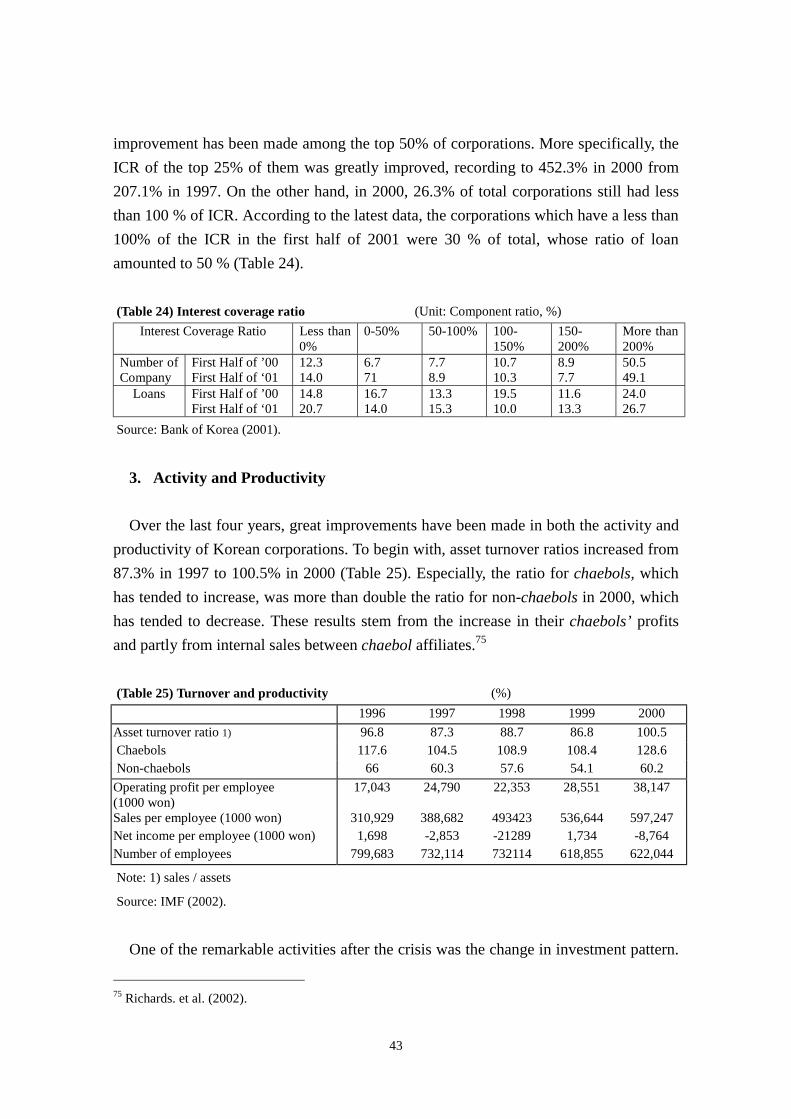

Measures and Assessment - CEPAL and Assessment April 2002 ... in 1998.1 The swift spread of this...

50

Korea’s Corporate Restructuring since the Financial Crisis: Measures and Assessment April 2002 Chan-Hyun Sohn Senior Fellow Korea Institute for International Economic Policy This draft paper is prepared for the seminar, “Promoting Growth and Welfare: Structural Changes and the Role of Institutions in Asia” jointly hosted by Economic Commission for Latin America and the Caribbean – United Nations, Institute of Developing Economies – Japan External Trade Organization, and Instituto de Economia – Universidade Federal do Rio de Janeiro between April 29 – May 3, 2002 at Santiago and Rio de Janeiro.

-

Upload

hoangquynh -

Category

Documents

-

view

214 -

download

1

Transcript of Measures and Assessment - CEPAL and Assessment April 2002 ... in 1998.1 The swift spread of this...

Korea’s Corporate Restructuring since the Financial Crisis:

Measures and Assessment

April 2002

Chan-Hyun Sohn

Senior Fellow Korea Institute for International Economic Policy

This draft paper is prepared for the seminar, “Promoting Growth and Welfare: Structural Changes and the Role of Institutions in Asia” jointly hosted by Economic Commission for Latin America and the Caribbean – United Nations, Institute of Developing Economies – Japan External Trade Organization, and Instituto de Economia – Universidade Federal do Rio de Janeiro between April 29 – May 3, 2002 at Santiago and Rio de Janeiro.

CONTENTS

I. Introduction

II. Evolution of the Financial Crisis and the Korean Government’s Initiatives III. First-stage of Corporate Restructuring

1. Corporate Restructuring (1) Management of Insolvency (2) Measures for the Facilitation of Corporate Restructuring

2. Corporate Governance

(1) Enhancement of Transparency of Corporate Management (2) Strengthening of the Minority Shareholder Rights (3) Strengthening of the Responsibility of Controlling Shareholders and Management

(4) Prohibition on Inappropriate Intra-group Transactions and Debt Guarantees

IV. Second-stage of Corporate Restructuring 1. Corporate Restructuring

(1) System for Corporate Restructuring System on a Regular basis (2) Measures for the Facilitation of Corporate Restructuring

V. Conclusion

Bibliography

2

��������Introduction

After the outbreak of the Asian financial crisis in 1997, Korea experienced severe

financial and economic distress. The country’s available foreign exchange reserves were almost exhausted by December 1998, and economic growth rate plummeted to its lowest-ever level, -6.7%, in 1998.1 The swift spread of this economic recession in Korea cast doubt on the true success of Korea’s economic development program, which had previously been credited for what was seen as Korea’s remarkable and rapid economic growth.2

This tumultuous situation revealed chronic structural weakness in the Korean economy – the underdeveloped financial sector and the government-business partnership. Although the crisis was initially sparked by contagion and currency speculation, its fundamental cause was the vicious circle of financial and corporate crises. In other words, a number of bankruptcies and ensuing problems of Korean conglomerates, following the Thailand’s financial crisis in 1997, stood at the core of the crisis. Therefore, in order to prevent the successive bankruptcies of banks and firms, due to the entangled correlation between the two sectors, the government undertook financial reform and corporate restructuring simultaneously from the initial stage.

This paper aims to make a diagnosis of major problems of Korean chaebols and to review the Korean government policies for corporate restructuring, including financial reform measures, and assess their performance.

The paper consists of six sections. Following this section, section II traces the evolution of the financial crisis in Korea and response of the Korean government to the crisis at the initial stage and discusses the major problems of Korean conglomerates. Section III reviews the government’s policy measures for corporate restructuring and governance at the first stage, from 1998 to the end of 2000. Section IV addresses the

1 OECD (1998). 2 There have been two main lines of argument as to the causes of the Asian financial crisis. The first line found the cause of the crisis from the fundamental weakness of the national development model of East Asian economies. This view was supported by Paul Krugman, an MIT economist. He suggested that the pace of economic growth in East Asia would gradually decline, because the growth was not driven by gains in knowledge or productivity but by an astonishing mobilization of resources (Krugman (1994)). The second line of argument views the massive, unpredictable movements of international speculative investment as the cause of the crisis. This view was supported by Steven Radelet and Jeffrey Sachs, who opposed Krugman’s critique of East Asia’s rapid growth. They argued that he was right in dispelling the notion that Asia’s “miraculous ” growth would continue at very high rates forever, but wrong about the solidity of Asia’s economic development. They asserted that the East Asian crisis resulted from vulnerability to financial panic, combined with a series of policy missteps and accidents that triggered the panic (Steven Radelet and Jeffrey Sachs (1998)).

3

government’s policy measures at the second stage, from 2001 to present. Then, section V assesses corporate performance, by examining corporate financial structure, profitability, and activity and productivity. This paper is concluded in section VI.

II. Evolution of the Financial Crisis and the Korean Government’s Initiatives

1. Evolution of the Financial Crisis and Revealed Problems

The Asian financial crisis was triggered by the Thailand’s financial crisis in mid-1997. Following the sudden devaluation of the baht of Thailand, the financial turmoil spread to its neighboring countries, the Philippines, Singapore, Malaysia and finally Korea. On the surface, the crisis seemed to be a liquidity crisis, resulting from low foreign reserves and excessive short-term foreign debts. Actually, the Korea’s short-term foreign debts were more than six times of its foreign reserves.3 However, at the core of the Korea’s crisis, stood the accumulated inefficiencies during its high growth period, mainly reflected in a series of bankruptcies of Korean conglomerates.

The number of bankruptcies of Korean corporations, near the outburst of the crisis, jumped by about 50%, to over 17,000 in 1997 from less than 12,000 in 1996.4 The situation seemed all the more severe because those figures included some of the largest-scale bankruptcies in Korean history, including the collapse of several chaebols. Specifically, seven of the thirty-largest Chaebols, accounting for 4% of the assets of non-farm and non-financial businesses, failed in 1997: the first insolvency of Hanbo Steel, Korea’s 14th largest chaebol, in January 1997; Sammi Steel in March, 1997; and Kia, the third largest carmaker in Korea in July, 1997. These successive bankruptcies of conglomerates and consequent financial market uncertainties shook investors’ confidence in the Korean economy, which eventually brought about currency and bank crises in Korea.

In these collapses of Korean corporations, their excessive investment and diversification through debt financing played notorious roles, backed by the government-administered credit allocation. Their external liabilities trended to increase especially in the 1990s. Gross external liability had been increased greatly until 1996, and external liabilities/GDP increased to 33.16% in 1997 from 19.99% in 1992. Short-

3 Lim (2001). 4 KERI (2001).

4

term external liabilities/total remained above 60% between 1993 and 1995, and short-term external liabilities/official foreign reserves reached the level of 300 % in 19975 (Table 1). (Table 1) External liabilities (Unit: 100million US $, %) 1992 1993 1994 1995 1996 1997 Gross external liab.1

(y-o-y growth rate) - Financial Inst.2

- Corporations

629.0 436.0 137.0

670.0 (6.52) 475.0 156.0

887.0 (32.39) 651.0 200.0

1,197.0 (34.95) 905.0. 261.0

1,643.4 (37.29) 1,165.3 417.5

1,580.6 (-3.82) 896.0 462.0

External liab./ GDP 19.99 19.38 22.04 24.46 31.60 33.16 Short-term ext.liab. /Total ext.liab.

58.82 60.15 65.84 65.75 56.58 40.00

Short-term ext. liab. / FX reserves3

215.69 198.89 227.48 240.58 279 309.82

Note: 1) External liabilities include external debts as defined by the IBRD, plus offshore borrowings of

Korean banks and overseas borrowings of Korean banks’ overseas branches.

2) Including foreign bank branches operating in Korea.

3) External liabilities and foreign exchange reserves are year end values.

Source: Ministry of Finance and Economy (1998).

On the other hand, Korea had the declining profitability during the 1990s. Overall, indicators of corporate profitability plummeted in 1996: return on assets, 0.8%; return on equity, 2.7%; Y-to Y operating income rate, -14.4%. In 1997, the first two rates had negative values, -0.7% and –2.9%, respectively (Table 2).

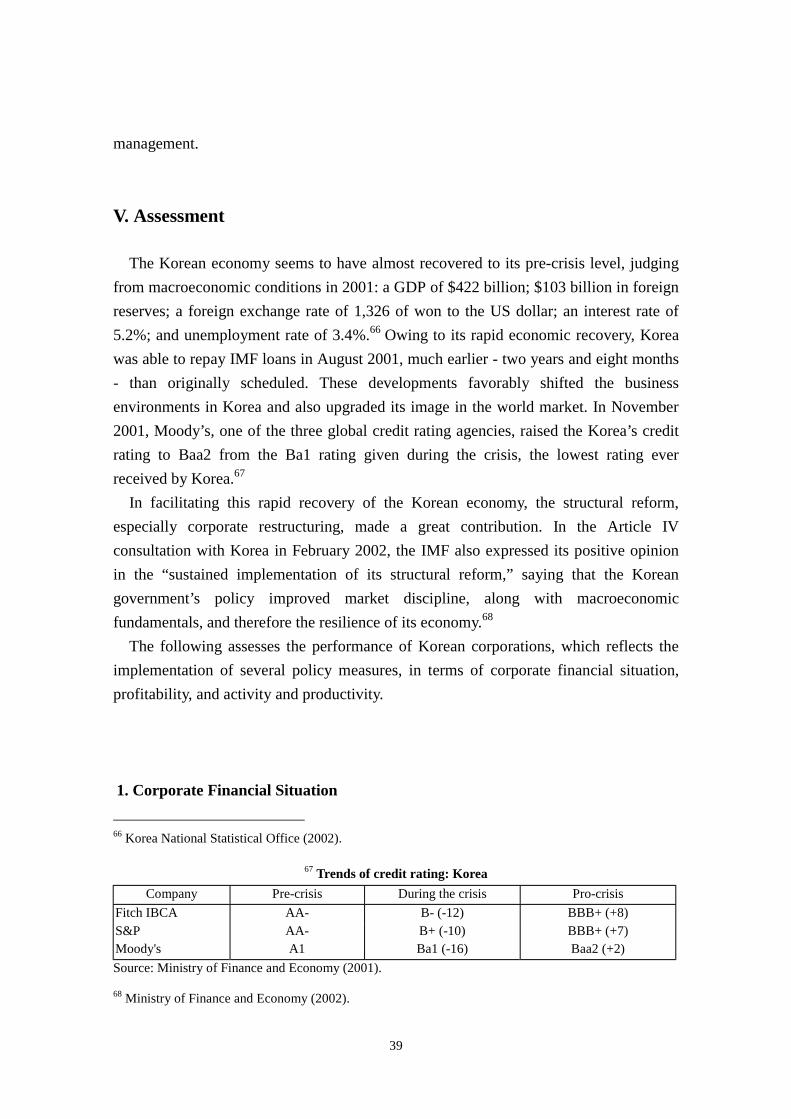

(Table 2) Indicators of Corporate Sector Profitability (%) 1991 1992 1993 1994 1995 1996 1997 Return on Assets 1.8 1.5 1.1 2.0 2.5 0.8 -0.7 Return on Equity 6.0 5.1 4.0 6.9 8.7 2.7 -2.9 Y-to Y operating Income rate

29.1 11.9 16.7 21.1 26.0 -14.4 22.9

Note: listed companies, excluding financial institutions

Source: Monthly financial statistics Bulletin (1999) and Financial Supervisory Service.

As a result, these excessive borrowings and low profitabilities could not cover their

5 Short-term debts accounted for two-thirds of total corporate debt, of which a quarter were from foreign financial institutions. The level of debt to equity ratio of Korean firms was at a very high level. For example, it was 396.3% in 1997, much higher than that of other countries such as the US and Japan whose ratios were 153.8% and 186.4%, respectively.5 Particularly, by the end of 1997, the average debt to equity ratio of Korea’s thirty-largest chaebols had risen to over 500%, 100 points higher than the five previous years (OECD (1998)).

5

interest expenses in 1990’s, which finally resulted in the negative profit growth in 1997 (figure 1).

(Figure 1) Profitability and opportunity cost of capital for Korean manufacturing firms

Source: Bank of Korea (quoted from Lim (2001)).

The Chaebols’ ambitious strategy of rapid growth on a global scale was successful in the 1970s and 1980s, when Korea enjoyed a favorable business climate and its firms achieved scale economies. However, as global economic condition changed and competition got fiercer in both domestic and world markets in the late 1980s, their debt-financed growth became riskier than the past, facing falling profitability.6

Here, the collusive relationship between the government and business groups was deeply involved. The government guaranteed the loans of large conglomerates, chaebols, through the control of the financial sector. This credit allocation often resulted in the excessive lending by financial and non-financial institutions without prudential rules. It finally brought about the inefficient allocation of capital and the fragile financial system in Korea. Actually, non-performing loans of banks amounted to W87.26 trillion ($63 billion) at the end of March 1998, which accounted for 16.89% of total bank loans, and 20.72% of Korea’s GDP in 1997 (Table 3).

6 The warning signs of bankruptcy and high systematic risk started to appear in mid-1996: 1) the problem of over-capacity emerged in key export sector investment - semiconductors, cars, steel and petrochemicals; 2) the low level of corporate liquidity magnified the negative effects of cash flow shocks on firms’ needs; 3) quick asset ratios declined to above 60 % from 100%.

-10

-5

0

5

10

15

20

25

30

35

67 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97

net profit/net worth financial expenses to to tal borrowing

6

(Table 3) Non-performing loans, end of March 1998 (trillion won) Total loans Non-performing loans (% of total)

Banks 516.6 87.3 (16.89) Other financial institutions 256.9 24.8 (9.64) Total 773.6 112 (14.48)

Source: F SC (quoted from Ahn (2001) ).

In consequence, the demise of the corporate and financial sectors was interwined, and therefore financial institutions became burdened with bad debt and were no longer able to roll over their domestic and foreign liabilities as corporate bankruptcies rose.

In addition, irrational corporate governance was another reason for the insolvent operation. Namely, the absence of mechanisms that check and discipline management in Korea, for example, M&As, prudential supervision in the financial market, and competition through entry and withdrawal, allowed to the traditional type of ownership in Korea, “controlling shareholder-managerialsm”.7 The concept means that controlling shareholders got deeply involved in the management of their firms. Korean chaebols, running businesses in almost every sector, controlled their affiliates with relatively small amounts of capital, through a centralized hierarchy system known as the “control pyramid system.”8 Actually, the number of affiliates of the top 30 chaebols increased from 16 in 1983 to 27 in 1997 (per group), while the percentage of shareholdings decreased from 15.8% to 8.5% during the same period. 2. Korean Government’s Response at the Initial Stage

As the Korean government could not find a way to break out of the crisis, despite its

attempts to support the won and implement an emergency program, 9 it sought emergency support from the IMF in November 1997. On 3 December, a $57 billion IMF stand-by agreement was announced, and the IMF provided a financial assistance package on the condition that Korea undertake economic reforms. The main objective of the program was to stabilize the exchange rate and stem another inflation effect from

7 “Controlling shareholder-managerialsm” is the concept of ‘controlling shareholder-manager meaning that a large shareholder participates in management and ‘managerialsm’ indicating that there’s no the appropriate checking system for exercising the right of managing (KERI (2000)). 8 ‘Control pyramid system’ indicates the leverage effect which the certain shareholder has control over the management of main business and this main business becomes the large shareholder of other business by controlling the assets of other business with its small amount of assets. This is phenomenon occurring in many countries except U.S and U.K (Ghemawat (1998) quoted from KERI (2000)). 9 The program included several measures to clean up the bad loan problem (by reactivating the resolution fund) and widened the won’s daily trading range to 10%, but it proved too little too late.

7

currency depreciation. However, its central focus was on speeding up the financial reform and corporate restructuring in order to break the vicious circle.

In early 1998, the newly elected Kim Dae-jung administration, in conformity with the IMF conditions, started to reform the inefficient financial and corporate sectors. In January 13, 1998, president Kim and the leaders of the top five chaebols established five tasks for the corporate sector to accomplish. The tasks were as follows: 1) to enhance the transparency of management; 2) to eliminate mutual debt guarantees; 3) to improve the financial structure of corporations; 4) to focus the conglomerates on core activities; and 5) to strengthen the responsibility of controlling shareholders and management. Considering changed conditions and new problems, the government added the three following tasks on August 15, 1999: 1) to improve the managerial governance of the second financial institution; 2) to eliminate cross-financing and illegal intra-transaction; 3) to prevent irregular inheritances and donations.

In addition to the above eight tasks, proposed by the president to form the fundamental principles of corporate restructuring, three accompanying principles were added to promote them. First, financial institutions, who provide loan to corporations, were to take a leading role in promoting corporate restructuring. This was aimed at preventing inefficiencies that could be brought about by the government’s intervention in restructuring. For this purpose, leading banks and the top 64 business groups concluded the Capital Structure Improvement Plans (CSIPs) in 1998.

Second, the principle of burden-sharing was to be applied in the process of corporate restructuring. This principle aimed to prevent excessive burdens from being transferred to financial institutions, in case losses due to the unilateral relief loans disbursed under the corporate rehabilitation policy could not be shared properly.

Third, the workout program was to be used as the main tool for corporate restructuring. Viable firms should be rehabilitated through self-restructuring efforts and financial support, while non-viable firms should be eliminated through the corporate restructuring process. The workout plan was designed as a way to accomplish this objective, through close deliberations between credit financial institutions and corporations.

To facilitate corporate restructuring, the government also amended 10 bills. More specifically, the following laws were revised in order to expedite the bankruptcy system—Corporate Reorganization Act, Composition Act and Bankruptcy Act; the financial and accounting system—Banking Act, Securities and Exchange Law, Law Concerning External Auditing of Joint Stock Corporations; and the foreign investment system—Tax Exemption Law, Corporate Tax Law, Foreign Investment and Capital

8

Inducement Law, Fair Trade Act. The problems of chaebols were incorporated into the Korean government’s policies

for restructuring corporate financial structure and governance. The weak financial structure, related to corporate restructuring, was dealt with in conformity with two tasks established at the initial stage of economic reform — improving the financial structure of corporations and ensuring that conglomerates focus only on core activities. The monopoly of management, related to corporate governance, was dealt with the remaining three tasks — the enhancing the transparency of management, the eliminating cross-debt guarantees and strengthening the responsibility of controlling shareholders and management. Important measures for corporate governance were mostly completed in the first stage, and therefore are mentioned only in section III.

III. First Stage of Corporate Restructuring

The first stage of corporate restructuring can be characterized as a stage of a government-led reform. Since few systems existed, at the outset of the financial crisis, to deal with the large-scale of insolvency and to discipline the corporate governance, the Korean government had to play a leading role in preparing the foundations of a market-based corporate restructuring system.

In this stage, financial reform was active, which became a cornerstone for corporate restructuring both in the first and second stages. While no longer viable financial institutions (including banks), due to excessive non-performing loans (NPLs), were shut down, the First Bank of Korea and Seoul Bank were recapitalized. By the end of 1997, Financial Supervisory Commission (FSC) made accounting firms inspect 12 banks that had failed to meet BIS’s capital adequacy ratio, which is closely related to the measure - the reduction in the debt-to-equity ratio of corporations. 10 In 1998, provision requirements and loan classification standards were strengthened based on forward-looking criteria,11 which was effective in 2000. Non-bank Financial Institutions (NBFIs),

10 The exit of non-viable banks through this measure is based on the ‘purchase and assumption (P&A) formula, whereby each acquiring banks purchased the sound assets and assumed the liabilities of those acquired banks. 11 Provision requirements and loan classification standards based on forward-looking criteria regarding future cash flows were strengthened in July 1998. According to the criteria, loans in areas of three months or more are considered precautionary loans. Therefore, most of the emergency loans made to bankrupt companies instead of precautionary loans are now reclassified as standard loans. The provision requirement for precautionary loans were raised from 1% to 2%. Eventually, this system under the global

9

on which firms have depended their debt financing before the crisis, were overhauled. Through these series of financial reforming measures, the foundation for the establishment of sound financial structure of corporations were prepared.

1. Corporate Restructuring

Faced the successive and sudden insolvencies, the government prepared

comprehensive measures for handling insolvent corporations and for facilitating corporate restructuring.

(1) Management of Insolvencies To begin with, in need of a systematic means of managing insolvencies, the Korean

government improved the existing court-based supervision and introduced an out-of-court workout program. During this period, insolvent companies were liquidated or rehabilitated through these two main mechanisms of court-based insolvency and out-of-court workout (Figure 2).

asset quality standard enlarged the size of NPLs (Ahn 2001).

10

(Figure 2) The Management Procedure of Insolvent Corporations in Korea

No

Yes

Court-based procedure Out-of-court procedure

No Yes

Yes No

Source: Bank of Korea

Insolvent Corporation

Is it viable?

Court-based procedure or

out-of-court procedure?

Composition Disposition

Rehabilitation procedure

Normalization

Removal of Disposition or

Completion of Composition

Workout

Normalization Bankruptcy

CRV

Sale

M&

A

Spinoff

Continuation

Com

pletionof

Workout

Bankruptcy

Dissolution

Liquidation

Dissolution

Liquidation

Rehabilitation procedure

11

1) Improvement of Court-Based Insolvency Procedures12 The court-based insolvency system before the crisis was not functional. For example, out of more than 17,000 insolvency cases reported by the Bank of Korea in 1997, only 492 cases were filed before the court.13 Court procedures were inefficient; Only 41 judges, some of whom were not specialists in commercial law, were assigned to deal with bankruptcy cases, and the lengthy proceedings, taking several years sometimes, were not attractive to creditors.

The government reformed the court-based insolvency system while revising the bankruptcy law in February 1998: it became easier for a court to accept and hear cases even when the file was not complete; the consolidation of related cases under the same court was facilitated; deadlines for the approval and submission of re-organization plans were shortened to between 12 and 18 months; and it became possible to switch from the composition or re-organization options to bankruptcy proceedings.

Also, the former management was under more harsh punishment in re-organization procedure, such as the compulsive retirement of shares and the deprivation of managerial rights. It was for former management to take responsibility for insolvency. However, the procedure has been used much less than before, from 148 cases in 1998 to 37 cases in 1999 (Table 4). (Table 4) Trends of Bankruptcy, Composition and Re-organization

Bankruptcy Composition Re-organization 1994 18 - 68 1995 12 13 79 1996 18 9 52 1997 38 322 132 1998 467 728 148 1999 733 140 37 2000 461 78 32

Source: KERI (2001).

12 The court-based insolvency system in Korea is composed of three: bankruptcy; composition; re-organization. Bankruptcy is a procedure that liquidates debtors’ assets by a court-appointed liquidator. Composition is a settlement procedure between the debtor and creditors, in which a debtor possesses its estates. It is available to enterprises that owe less than W250 billion, for it offers very few guarantees to the creditors. In Re-organization procedure, the court directs the creditors to handle the debtor, and the latter’s estate is administered by an external administrator under the influence of the debtor. Creditors and debtor can start any of the procedures, if there is evidence of cash flow insolvency (OECD (1998)). 13 KERI (2001).

12

2) Out–of–Court Debt Workouts14 The Korean government started its debt workout program, following the London Approach,15 in July 1998. The debt workout is an out-of-court settlement process for creditors and debtors, which is based on the principle of burden-sharing with financial institutions, through the firm’s own efforts for rehabilitation as well as debt adjustments. A Corporate Restructuring Accord (CRA) was signed in June 1998, in which 200 banks and non-bank financial institutions committed themselves to following the agreed workout procedure. Problems between financial institutions and a debtor were resolved through the Corporate Restructuring Co-ordination Committee (CRCC), an arbitration committee. In this bank-led voluntary workout, eight major creditor banks - leading banks – were responsible for renegotiating workouts with the 64 major corporate groups. Each bank established its own workout unit. In the process of corporate restructuring, the Korean Asset Management Company (KAMCO)16 played an important role by purchasing non-performing loans from commercial banks.

Workout plans included various tools for adjusting debts, through the analysis of mid- and long-term cash flows 17 , which contained debt/equity swaps, term extensions, deferred payment of principal or interest, interest rate cuts, and provision of new credits.

14 Workout is a procedure of eliminating non-viable firms and supporting the rehabilitation of insolvent but viable firms, through close cooperation with credit financial institutions. It is distinguished from a bailout, in which insolvent and non-viable firms remain afloat through support from the government or financial institutions. While the decision to carry out a bailout is made informally and does not entail any effort on the part of the firms, a workout plan is prepared through a transparent process and objective judgement on the viability of firms. 15 There are three corporate restructuring approaches in the world: centralized approach; decentralized approach; London approach. Under the centralized approach, the government leads the corporate restructuring - this method is appropriate for small companies with a simple governance structure (Sweden and Hungary). On the other hand, under the decentralized approach, appropriate for large companies (the U.S. and Poland), the involved parties attempt to narrow the difference in their interests. The London approach is a mixture of the first two approaches, in which corporate restructuring is overseen by an arbitrator mediating between the companies and financial institutions (UK and Korea) (Shin. et al (2000)). 16 KAMCO also played a fundamental role in financial sector restructuring by managing the bailout fund and purchasing non-performing assets from the banks. The loans purchased by KAMCO, by the end of September 1997, amounted to W37 trillion at a cost of W17.2 trillion (Ahn (2001)). 17 The amount of sustainable debt for a firm is determined by its cash flow. Usually, an interest coverage ratio (ICR) of less than 1.0 means a firm cannot meet its interest payments. According to an IMF study (Richards. et al (2001), about one in four firms were found to be unable to generate enough cash flow to meet their interest payments, in spite of the improvement in their operating performance in 1999. The average ICR for the companies in 1999 was 2.3, higher than the 1.4 recorded in 1998. However, 23% of the affiliates of the top 64 chaebols had an ICR below 1.0. In addition, the financial position of the medium-size chaebol affiliates was much weaker than the affiliates of the top 4 chaebols. The average ICR for the medium-sized chaebols was 1.6 compared to 2.9 for the affiliates of the top-4 chaebols. The medium-sized chaebols also had a larger share of companies with an ICR of below 1.0 and a larger share of precautionary debt.

13

For some cases, favorable tax treatments were available: a bank acquiring shares was exempt from the acquisition tax in a debt/equity swap; taxes were not imposed on firms selling real estate holdings to reduce its debts. In addition, to accelerate the workout process, a three-month time limit was imposed, with a one-month extension.

Three Different Approaches

Under the broad framework of debt workout, the Korean government created three different approaches to corporate restructuring, which were applied according to the firm’s restructuring capacity: the top five chaebols, with the capacity to absorb the resulting losses, were allowed to pursue ‘self-directed restructuring:’ The Daewoo Group and the 6th to 64th largest conglomerates, with the inability to restructure successfully on their own, entered into “workouts” with financial institutions; the SMEs, too weak to bear the costs of restructuring, were supported by their creditor financial institutions.

a. Top Five Chaebols

The self-directed financial structure restructuring of the top five chaebols was not only based on their own restructuring plans, but also on the Capital Structure Improvement Plans (CSIPs). The CSIPs were established through an agreement between the top 64 Korean business groups and their lead creditor banks in early 1998. According to the plan, the chaebols were required to reduce their debt-to-equity ratios to 200%, sell off non-viable affiliates, and reduce intra-group debt guarantees under the supervision of the lead banks.

The Korean government also directed the chaebols to identify their core businesses and to divest from peripheral businesses. 18 To strengthen the competitiveness of the core businesses, it also required the inclusion of the restructuring plans into CISPs and the supervision of their implementation. However, as the larger conglomerates progressed relatively slower in their restructuring than the smaller conglomerates and SMEs, a December 1998 Agreement19 was concluded between the conglomerates, the government and their creditor

18 The Korean conglomerates, under the government’s protection, diversified their affiliates and business areas. The average number of affiliates for the 30 largest conglomerates continued to increase, growing from 19.7 in 1992 to 27.3 in 1997; meanwhile, the average number of business areas also increased from 16 to 20 during the same period (OECD (1998)). 19 The agreement also emphasized the reduction of debt-to-equity ratios. Other points included the exit of non-viable firms, independent management of chaebol affiliates, the elimination of intra-group debt

14

banks. The Agreement emphasized two aspects – detailing restructuring plans and ‘Big Deals,’ which were also incorporated into the revised CSIPs.

Big Deals, an industrial adjustment program, was conducted as a part of the solution to excessive competition, excess capacity, and high debt-to-equity ratios. In 1998, the Ministry of Trade, Industry, and Energy identified ten industries that were in need of restructuring to reduce excess capacity and combined major producers in each industry (Table 5).

(Table 5) Big Deals

Industry Plan Controlling body Semiconductors Power-generating equipment Petrochemicals Aircraft manufacturing Railroad vehicles Ship engines Oil refining Cars1

Samsung Electronic Co. ! Hyundai Electronics Ind. Combine ! LG Semiconductor Co. Hyundai Heavy Industries Co. Korea Heavy Industries & Construction Co. Combine ! Samsung Heavy Industries Co. SK,LG, Daelim, Lotte, Hanwha ! Hyundai Petro-chemical Co. Combine ! Samsung General Chemical Co. Samsung Aerospace Industries Co. Daewoo Heavy Industries Co. Combine ! Hyundai Space & Aircraft Co. Hyundai Precision & Ind. Co. Daewoo Heavy Industries Co. Combine ! Hanjin Heavy Industries Co. Hyundai Heavy Industries Co. ! Korea Heavy Industries & Construction Co. Combine ! Samsung Heavy Industries Co. SK, LG, Ssangyong ! Hyudai Oil Co. Combine ! Hanwha Energy Co. Hyundai Motors2 !

Daewoo Motors3 Combine ! Samsung Motors

Samsung Electronics Co. Hyundai Electronics Ind. (Agreement reached in January 1999) Korea Heavy Industries & Construction Co. SK, LG, Daelim, Lotte, Hanwha New entity New entity Third-party professional manager Hyundai Heavy Industries Co. Korea Heavy Industries & Construction Co. Sk, LG, Ssangyoung Hyundai Oil Co. Hyundai Motors2

Daewoo Motors

1. Added in December 1998.

2. Hyundai Motors acquired Kia Motors earlier in 1997.

3. Daewoo Motors acquired Ssangyong Motors in 1997.

Source: Yoo (quoted from OECD (1999)).

guarantees and the transparency of corporate management.

15

To facilitate the program, the government reduced or exempted taxes resulting from

the deals, e.g., transactions and acquisition taxes were exempted for major shareholders. However, unlike the top four chaebols, the workout program was applied to the

Daewoo Group. The Daewoo Group started its financial restructuring relatively later than the other conglomerates, and therefore could not achieve satisfactory performance. In addition, they had financial difficulty due to a fall in their credit rating from 1999. They, again, announced a supplementary restructuring program in April and a plan for accelerating corporate restructuring in July 1999. However, Daewoo group could not overcome its short-term liquidity problem, and finally entered into a workout program in August 1999. The Group was loaded with an excessive debt burden of W60 trillion, including nearly $10 billion in foreign debt. The nearly complete dismantling of Korea’s second largest chaebol was the most dramatic example of corporate restructuring – namely, it caused the collapse of the traditional belief of “too big to fail” in Korea.20

Following the dissolution of the Daewoo Group in 1999, the existing self-restructuring plans were implemented by the remaining four chaebols. By the end of 1999, they had succeeded in keeping their plans as agreed in the restructuring Memorandum of Understanding (MOU) with the government. In accordance with their 1998 plan, the top four chaebols reduced their debt-equity ratios to less than 200%, dropping them from 352 % to 173.9% by the end of 1999 (Table 6). (Table 6) Improvement of financial structure

End-1998 June, 1999 Implemen Tation (A) (B) End- 1999 Chan Ges Plans

(C) Achievement

(D) (D-A) (D-B)

Debt/equity ratio 352 254.6 197.7 173.9 178.1 180.7 Debt 165.1 160.9 128.3 139.6 25.5 21.3 Equity 46.9 63.2 64.9 80.3 33.4 17.1

Source: FSC (quoted from Shin. et al. (2000)).

They also implemented their financial restructuring plans as they had announced – with an implementation rate of over 100% (Table 7). They implemented their self-restructuring plans with W15 trillion of asset sale and W22.7 trillion won of raising capital. As well, they induced foreign capital, spun off non-core firms, improved 20 Analysts saw the Daewoo case as a manifestation of the government’s determination to reform chaebols under the “convey management practice” (OECD (2000)).

16

corporate governance and reduced affiliates. (Table 7) Implementation of restructuring plans of the top four chaebols

Plan Accomplishment Implementation rate 1998 (A) 1999 (B) (B/A, %)

Self-restructuring effort (Trillion won)

33 37.7 114.4

Asset sales 13.7 15 109.6 Raising capital 19.3 22.7 117.8 Inducement of foreign capital (Billion won)

71.9 84.3 117.2

Prohibition of Cross debt guarantee ( Trillion won)

2.7 3.1 116.7

Spin-offs 173 442 255.5 Improvement of corporate governance

136 143 105.1

Reduction of affiliates 84 94 111.9

Source: FSC (quoted from Shin. et al. (2000)).

b. Daewoo Group and the 6th to 64th Largest Conglomerates

In the corporate restructuring process, the 6th to 64th largest conglomerates, including Daewoo Group, entered into the workout program.

As of the end of 2000, 104 firms, including Daewoo Group affiliates, have been nominated for the workout process. Of the 104 companies nominated, 36 firms have graduated and 34 remained in the program. Among the remaining 34 firms, 8 dropped out, 11 were ejected, and 15 were merged with other companies. Ten of the remaining companies were affiliated with the Daewoo Group, while 15 were affiliates of the 6-64 conglomerates and 9 were medium-sized firms. The companies in the program received a total of 71.5 trillion won of concessions as of December 2000. 60 trillion won out of the total consisted of interest rate cuts or exemptions, while debt-equity swaps and the conversion of bonds to equity accounted for less than 6 trillion won21 (Table 6).

21 OECD (2001).

17

(Table 6) Selection of firms under the workout program and their progress Nominated Excluded Pre Sent (A) Total (B) Dropped out Merged Ejected Graduated

(C) Remaining (A-B-C)

Daewoo Companies

12 1 0 0 1 1 10

Affiliates of 6-64 Con-glomerates

49 22 5 12 5 12 15

Medium-sized firms

43 11 3 3 5 23 9

Total 104 34 8 15 11 36 34

Source: OECD (2001).

The face value of bonds for affiliates under the workout program (including 12 affiliates of Daewoo) reached 98.5742 trillion won in June 2000. Among them, the face value of bonds for the 12 affiliates of Daewoo accounts for 66.5767 trillion won (67.5%) and the face value of bonds of leading corporations below the top six accounts for 31.9975 trillion won (32.5%). Among the total of W98.6 trillion, W72.3 trillion benefited from the interest rate cut. Transfer financing reached W15.8 trillion. Deferred payments amounted to W70.2 trillion, and debt transferred to W3.4238 trillion. Moreover, corporations under the workout program were supported by W4.9 trillion with new credit for management funds and trade finance (Table 8).

(Table 8) Workout plans and implementation (hundred million won, %) Classification Debt Adjustment New

Deferred Payment Debt/equity swaps

Others Total Credits

Interest rate cut

Normal interest rate

Non-Daewoo Plan 189,277 47,950 72,401 10,347 319,975 10,982 56 Achievement 171,696 34,627 28,572 37,591 272,486 11,313

Implementation ratio(%) 90.7 72.2 39.5 363.3 85.2 103 Daewoo Plan 533,641 11,888 85,849 34,389 665,767 56,110

12 Achievement 530,744 11,888 5,666 35,257 583,555 37,209 Implementation ratio(%) 99.5 100 6.6 102.5 87.7 66.3

Total Plan 722,918 59,838 158,250 44,736 985,742 67,092 68 Achievement 702,440 46,515 34,238 72,848 856,742 48,522

Implementation ratio(%) 97.2 77.7 21.6 162.8 86.8 72.3

Source: FSC (quoted from Shin. et al. (2000)).

18

c. Small and Medium-Sized Enterprises (SMEs)

SMEs were hard hit by the 1998 recession, especially by the credit crunch as banks reduced loans to them, which resulted in the upsurge of their bankruptcy rate. At the initial stage, before 2000, the Korean government support SMEs with several measures. First of all, the government directed banks to roll over loans to SMEs. A special task force was established in each bank in May 1998, and classified firms into three groups: priority support (38.9%); conditional support (55.6%); other (5.5%). For the firms in the first two categories, accounting for almost 95% of SMEs, banks were instructed to roll over loans maturing by December 1998.22 In addition, the government provided W33 trillion of guarantees for loans to small firms and additional budgetary support of W2.2 trillion through a variety of programs – the Guarantee Fund and the Enterprise Promotion Fund for Software. Twenty-five financial institutions also established the Corporate Restructuring Fund and raised W1.6 trillion to assist small companies. The central bank changed its criteria for setting credit ceilings to encourage banks to support small firms. Lastly, small firms were granted tax benefits: income tax or corporate tax was reduced by half for newly established SMEs during their first five years; tax benefits associated with facility investments were made more generous.

With the favorable turn in financial market conditions - easier access to bank loans and to other financial sources, e.g., KOSDAQ and the bond market,23 the government reduced its support for SMEs from full to partial guarantees in 2000. Namely, with abundant liquidity, the rate on bank loans to SMEs recorded to 7.8% at the end of 2000, compared to financing in government programs with rates of 5.5% ~ 8.25%24. The government cut its support for facility investment and operating expenditure, but increased it for technology development and venture businesses instead. The number of business lines reserved for SMEs, which totalled 237 in 1989, was reduced to 88 in 2000 and further lowered to 45 in 2001. In addition, the requirement of the government procurement of certain items solely from cooperatives organized by SMEs was eliminated in compliance with the WTO’s rules, and the number of designated goods decreased from 258 items in 1998 to 154 items in 2000.

22 Firms in the category of conditional support were required to reduce their debt-to-equity ratios and to improve their capital structure by disposing of real estate holdings (OECD (1999)). 23 Financial market conditions for SMEs improved in 2000. Firstly, their access to bank loans increased with the reduction of chaebols’ borrowing from banks due to the lowering of their debt-to-equity ratios below 200% (The new bank loans to SMEs accounted for 97% of total loans in 1999 and 84% in 2000). Secondly, other financial sources, such as KOSDAQ and the bond market, were increasingly accessible to SMEs. 24 OECD (2000).

19

(2) Measures for the Facilitation of Corporate Restructuring In order to support the new restructuring systems, the government took several market-friendly measures: the development of restructuring intermediates, the elimination of regulation on M&A, and the establishment of the Bond Recycling System.

1) Development of Restructuring Intermediates

For the formation of the restructuring market, the function of Korean Asset Management Corporation (KAMCO) was widened, and new restructuring intermediates, Corporate Restructuring Fund (CRF), Corporate Restructuring Company (CRC), and Corporate Restructuring Vehicle (CRV), were established.

a. Korean Asset Management Corporation (KAMCO) The Korean Asset Management Corporation (KAMCO), which was established as a subsidiary of the Korea Development Bank (KDB) to resolve the non-performing loans (NPLs) of the KDB in 1962, was reorganized into a specialized resolution agency under the Act on Efficient Management of NPLs of Financial Institutions and Establishment of KAMCO, and set up the Non-Performing Asset Management Fund. The KAMCO Act was amended in 1999 directing KAMCO to function as a bad bank.

KAMCO, as a bad bank, manages and operates the Non-Performing Asset Management Fund and, under the government’s debt guarantees, purchases non-performing assets25 from banks and other financial institutions (Figure 3). At the same time, it provides assistance for the recovery of transferred insolvent companies. Next, for the revulsion of the Non-Performing Asset Management Fund, KAMCO resells them to investors through individual corporate loan sales (ICLS) and merger & acquisition (M&A)26.

25 The basic rule of purchasing price assessment for NPLs is as follows: secured loans are priced by adding or subtracting price fluctuations of collateral assets from the recent average foreclosure action rate; unsecured loans are priced at 3% of the face value. 26 KAMCO pools and sells the loans of particular companies to interested investors through two methods: through ICLSs, investors take over KAMCO’s position as a creditor through open competitive bidding; through M&As, investors take over the stake and managerial rights of subject companies by reviving the reorganization plans.

20

(Figure 3)- KAMCO’s procedure of acquisition and disposition of distressed assets>

Debt-Guarantee

ICLS Sales of loan Revulsion of capital.

Underwriting charge M&A

(cash, bond) Revulsion of capital

Source: KERI (1998).

The Non-Performing Asset Management Fund collected a total of W20.5734 trillion in 1998, of which bond issues accounted for W17 trillion. With the basis of book value, the fund purchased W13.8607 trillion and had W12.0712 trillion as available capital (Table 9).

(Table 9) Accomplishments of the NPA Management Fund The fund’s Scale

Supplier Sum of money Cost of

Collecting fund Acquisition of

NPLS Available Fund

Bond Issue 17.0 Tril. 11.55-12.14% BOK loaning 2.0 Tril. 5% KDB loaning 0.5 Tril. 8.35%

Financial instituions’s contribution (��)

0.5734 Tril. -

Total 20.5734 Tril. Average 10.72%

Book value: 13.8607 Tril.

Acquisition 7.5522 Tril.

12.0712 Tril.

Source: KERI (1998).

KAMCO introduced a joint venture partnership as one disposition method, given the necessity of specialized and systematic asset management techniques (Figure 5). The government enacted the Corporate Restructuring Company (CRC) Act and the Ministry of Finance and Economy has given loans to KAMCO. With these loans, KAMCO established three joint venture corporate restructuring companies and built joint venture

Government

KAMCO

Investors

Investors

Financial Institutions

21

relationships 27 with foreign investment companies such as Lehman Brothers, Sonnenblick Goldman & Colony Capital and Morgan Stanley Dean Witter.

b. Corporate Restructuring Fund (CRF)

The Corporate Restructuring Fund (CRF) is a paper company, a form of mutual fund created under the Securities and Investment Trust Law. It was established with an investment of W1.6 trillion by financial institutions in 1998 to relieve the financial difficulties of SMEs and some leading companies. The CRF’s substantial asset management was supposed to entrust asset management company (AMC) but was left to foreign investment companies on the policy authorities’ judgment that Korea companies were unable to manage the asset.

The CRF is divided into an equity fund and debt restructuring fund. The former was established to invest in newly issued stock for the expansion of SMEs and leading companies’ capital and the latter was established to support debt-equity swaps of short- term debt to long-term debt for the improvement of corporate financial structure. In 1998, a debt fund, Seoul Debt, and three mutual funds, Arirang, Mugoongwha, and Hangang, were established (Table 10). The CRF has also performed the pre and post management for the normalization of corporations in addition to providing support through funds.28 (Table 10) Registration of CRF

Classification Form Scale (hundred million) Management company Seoul Debt Debt fund 6,000 Rothschild Inc.

Arirang Mutual fund 3,334 State Street Bank & Trust Co. Mugoongwha Mutual fund 3,333 Scudder Kemper Investments Inc.

Hangang Mutual fund 3,333 Templetion Asset Management Ltd.

Source: FSC (quoted from KERI (2001).

c. Corporate Restructuring Company (CRC) and Vulture Fund 27 The strength of having the equity partnerships is to maximize the returns by introducing the incentive system for general partners (the investors) while minimizing the holding period of the assets. Another advantage is that KAMCO does not have to bear the full burden of collection expenses. On the other hand, there are some weaknesses in equity partnerships. For example, KAMCO has to bear the risk of trusting foreign investors who may make poor business decisions. 28 CRF has the limits on substantial business management for subject companies because it is restricted to

22

CRCs and Vulture Fund were established under the Industrial Development Law in

February 1999 for the facilitation of market-induced corporate restructuring. CRCs are a joint-stock corporation based on commercial law, whose main function is to carry out corporate restructuring through takeovers, management restructuring, and sales of insolvent corporations.29 The restructuring corporations include companies that are in needs of restructuring as well as in insolvency. CRCs also invest in and purchase the assets of restructuring companies, mediates M&As, and handle business for composition, reorganization, and bankruptcies. In addition, CRCs, as asset owners, issue ABS via SPC and manages assets.

For investment funds, CRCs use Vulture Funds (association based on civil law) as well as their own capital. Vulture Funds are applicable to civil law, and their functions, such as the management of assets and the management restructuring of insolvent companies, are carried out by the CRC. Vulture Funds are supervised more strictly than the CRCs, within two years after registration, they are obliged to use 20% of paid-in capital for the takeover, management restructuring, and sale of insolvent corporations (cf. 10% in case of the CRC).

By June 2000, 42 CRCs have been registered, among which pure companies numbered to thirty-seven, while investment corporations30 and new technology credit business were four and one, respectively. Most of them, 80%, were small and medium sized CRCs with less than W 5 billion of paid-in capital; only eight CRCs had a paid-in-capital of more than W 5 billion (Table 11).

(Table 11) Registration of CRC

Registration Year

Paid-in capital 1)

Listing or unlisting Shareholder Investor

Classification

‘ 99 ‘ 00 More than 5

Bil.

Less than 5

Bil

Exchange

KOSDAQ

Unlisting Corp. Private Native

Foreigner

No. 20 22 8 34 1 1 40 31 11 37 5 1) Total paid-in capital: W 500.9 billion

Source: Lee, C. (2000).

the management of securities. 29 Insolvent corporations are taken over through the acquisition of stock and share or through merger and divestiture. Then their management is restructured through a group of managers or a board of directors from the CRC. Finally, investment funds are paid back within five years through sales of stock, management, and assets. 30 This is a kind of venture capital to support and invest in enterprises who have an outstanding business program but less capital.

23

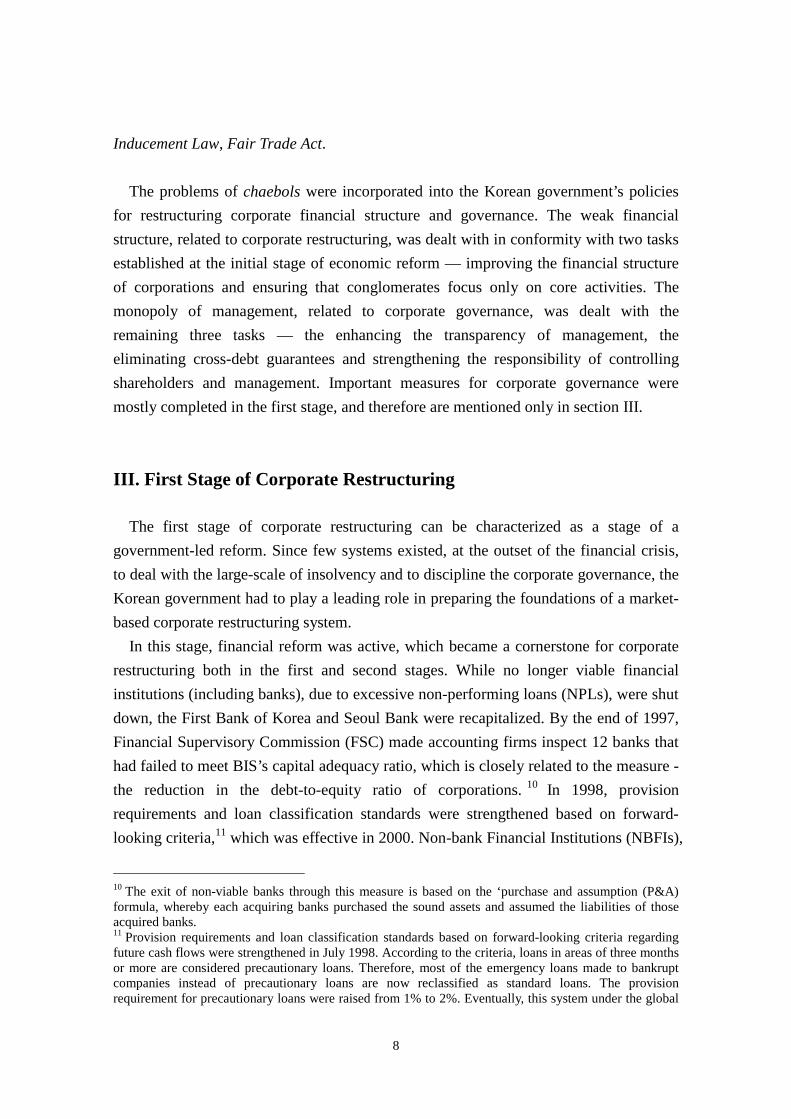

Six Vulture funds were registered by June 2000, with W351.8 billion in total investment (Table 12).

(Table 12) Registration of Vulture Fund

Fund name Registration date Fund operator Total investment

First Comet M&A fund ’99.9.9 Comet Investment Corp. W 23.8 Bil First KTIC fund ’99.10.8 Korea Technology Investment Corp. W 208 Bil First KTB fund ’99.12.9 KTB Network Co., Ltd. W 13.5 Bil First QCP fund ’00.1.25 Q Capital W 1.5 Bil Second KTB fund ’00.3.3 KTB Network Co., Ltd. W 55 Bil Third KTB fund ’00.4.10 KTB Network Co., Ltd. W 50 Bil Source: Lee, C. (2000).

CRC and Vulture Fund has made W 991.6 billion in investments in restructuring

companies by May 2000. By types, 76 purchase of assets and bonds were made with W 763.6billion, which is more than underwriting, with W 227.2 billion (Table 13).

(Table 13) Investment accomplishment (Unit: W Billion)

Classification Underwriting Purchase of assets & bonds

Total

Amount of money 167 135.8 302.8 1999. 6-12 Number of cases 49 cases 14 cases 63 cases

Amount of money 60.2 627.8 688.8 2000. 1-5 Number of cases 3 cases 62 cases 65 cases

Amount of money 227.2 763.6 991.6 Total Number of cases 52 cases 76 cases 128 cases

Source: Lee, C. (2000).

Recently, the registration of large-sized CRCs established through the collaboration of domestic and foreign financial institutions has been increasing. In particular, three very large CRCs, affiliates of KAMCO, were established in early 2000 through a collaboration with $1 billion of foreign capital. In June 2000, the KDB Lone Star was established as an affiliate of Korea Development Bank through the collaboration with the Lone Star, one of American corporate restructuring company, which plans to invest W1000 billion within 5 years.31 In addition, the CRCs taking charge of a specific industry tended to increase, such as the Sun & Moon, registered in 1999, specialized in the hotel and restaurant business and the Investor United, registered in 2000, specialized in car components. d. Corporate Restructuring Vehicle (CRV)

31 Lee, C. (2000).

24

The Corporate Restructuring Vehicle (CRV) was started with the establishment of the

Corporate Restructuring Vehicle Act legalized CRF’s structure with six years validity from October 2000. The CRV was established as a device for market induced restructuring because corporate restructuring was not progressing swiftly enough due to the problem of the Daewoo crisis.

The Corporate Restructuring Vehicle (CRV) is a paper company that is a type of mutual fund for a limited period of time. CRV is to normalize the management of the subject corporation and then to distribute the profits among shareholders by separating and gathering the insolvent assets of corporations, and then concluded the contract and entrusting this asset to AMC specialized in restructuring business (this asset possessed by bond financial institutions). 32 CRV do not have the disadvantages of CRCs and Vulture Funds which are not financial institutions and therefore have difficulty in taking over large conglomerates with little capital. The CRC’s minimum capital is W500 million and its duration is less than 5 years. A company can borrow loan within two times of equity capital and issue corporate bonds within ten times of capital and reserve. Bond financial institutions can own corporate shares exceeding the capital limit prescribed by business relevant law like the Bank law33.

CRVs did not get satisfactory results in corporate restructuring contrary to the expectations. Only three corporations, Shinwoo, Dynast Club Korea and Orion Electronics are registered to establish CRVs with the Financial Supervisory Committee.

2) Elimination of Regulations on M&A As a way of activating corporate takeovers, the Korean government tried to prepare

measures to develop the capital market. Before the financial crisis, hostile M&As were not allowed and even friendly M&As were limited to cases where the total assets of the companies involved did not exceed W2 trillion. However, all forms of M&As, including hostile takeovers, were fully liberalized by May 1998.

More specifically, foreign direct investment (FDI) in Korean enterprises was allowed. 32 There are differences between CRV and AMC as follow. First, CRV is fundamentally a holding company while AMC works as the executive office of a holding company. Second, CRV does a loan business itself while AMC does substantial business. Third, CRV gets tax benefits such as exemption from securities transaction tax, exemption from registration transaction tax, tax-free marginal profit from transfer, dividend exclusion and tax-free for private investment (KERI(2001)). 33 CRV has the advantage as a legal organization because financial institution can do debt-equity swap free from legal restriction if financial institution use CRV after the determination of debt settlement.

25

Recently, several industries have been opened up to FDI, including construction, leasing, securities, and futures brokerage, but FDI is still prohibited in 31 business lines.34 In addition, the ceiling on total foreign shareholdings in individual companies was abolished in May 1998. Moreover, the rule that limited holdings acquired without the approval of the board of directors to only 10% was revoked, enabling foreign investors to acquire 100% of a company without approval by the board.

The government abolished two important stock market rules: the rule requiring statutory tender offers in the case of a purchase of 25% or more was abolished; and disclosure of incremental acquisitions of stakes larger than 5% was no longer required. 3) Introduction of ‘Bond Recycling System’

Following the collapse of Daewoo in mid-1999 and the shift to non-guaranteed bonds following the crisis, a significant number of firms faced difficulty in rolling over maturing bonds in 2000. While 85% of bonds issued in 1997 were guaranteed, 95% of bonds in 1999 had no guarantees. In addition, for the newly-introduced exposure limits, an investor holding the bonds of a company could not purchase an equivalent amount of new bonds to roll over the existing debt. In response to the situation in the bond market, the government created a primary Collateralised Bond Obligation (CBO) program35 in August 2000.

This approach involves bundling maturing bonds, providing a partial government guarantee and selling securities backed by those bonds to investors. The guarantee is provided by the Korean Credit Guarantee Fund (KCGF), which charges a 1.5% fee for this service and screens the companies wishing to participate in this program. By the end of 2000, 17 different consortiums had put together CBOs, which were sold by securities companies. This approach was extended in December 2000 to loans with the creation of collateralised loan obligations (CLOs), which are sold by banks.

Given the bunching of maturities, bonds worth 65 trillion won – 42% higher than in 2000 – were due in 2001, which amounted to three-fourths of the total stock of outstanding corporate bonds, excluding asset-backed securities. While the CBO program was expected to handle much of this amount, some companies had large 34 The effort raised M&A by foreign companies sevenfold, which accounted for a fifth of all such deals in Korea in 1998 (OECD (1999)). 35 The companies using this scheme have to have a bond rating of at least BB. The size of individual CBOs issued to date has ranged between W100 billion and W1.5 trillion of corporate bonds. The amount of bonds from an individual company is between 5 and 10% of the total CBO in order to reduce risks. Thus, the amount of bonds from an individual company in a CBO issue is between W5 billion and W150 billion (OECD (2001)).

26

amounts of maturing debts, making them unsustainable for the CBO program. To prevent a large number of major bankruptcies, the authorities established a “quick underwriting” program using the Korean Development Bank (KDB),36 a government owned institution, to roll over maturing bonds by partially using government guarantees.

2. Corporate Governance

The term “corporate governance structure” can be defined as a system to command

and control a corporation. 37 A good corporate governance structure prevents the management from investing in unprofitable businesses and enabling shareholders to get their fair share of profits.

Korea companies were plagued by numerous problems in corporate governance structure, especially, the disparity between the ownership and control rights of founding families and the potential for expropriation of minority shareholder value that resulted.38 Recognized the need of the fair and transparent governance, the reform of corporate governance focused on four areas: improving the transparency of corporate management, strengthening minority shareholder rights, strengthening the responsibility of controlling shareholders and management, and improving intra-group relationships.

(1) Enhancement of Transparency of Corporate Management

Transparency is at the core of good governance as it allows shareholders and creditors to monitor management and to prevent managers and controlling shareholders from taking actions in their own interest at the expense of the company. 39 Enhanced transparency can guarantee good corporate governance. Especially in Korea, enhancing transparency was designed to address the “arbitrary imperial rule” of the chaebol bosses, who exercised complete control over their firms with low ownership stakes and in some

36 Under this programme, the KDB purchases 80% of the maturing bonds and divides it into three categories: 1) 20% are sold to banks that are already creditors of the issuing company; 2) 70% are sold to CBOs or CLOs within three months by bundling the bonds from different companies, which are partially guaranteed by the Korean Credit Guarantee Fund (KCGF); and 3) the remaining 10% are held by the KDB. The repackaged bonds mature in one year, by which time it is expected that the capital market is functioning better and the company has implemented its restructuring plan, allowing the scheme to end. 37 Cadbury Committee Report (1992) gives this definition. Normally, corporate governance structure means systematic relationship between an owner and the management. In a broad sense, it means systematic process to maintain and manage the clear or implied contract among the persons concerned of corporate, such as shareholders, creditors, employees and so on. 38 Haggard, Lim and Kim (eds.) (2001). 39 OECD (1999).

27

cases without even being registered as the chief executive.40 To increase transparency, the government demanded the improvement and internationalization of the corporate accounting standards, the enhancement of credibility in the accounting auditing, the introduction of combined financial statements and corporate public disclosure.

1) Improvement of the Corporate Account Auditing Procedure

Under the agreement with the IMF, the Korean government set corporate accounting standards to conform to international standards by October 1998. Korea has long been noted as a country with low comparability with international standards.41 Although the Korean Generally-Accepted Accounting Practices (GAAP) is generally consistent with international accounting standards, important loopholes remained in terms of accuracy, timeliness, and depth and veracity of the reported information.42 The introduction of the international accounting standards is sure to boost the credibility of accounting information, and further encourage foreign investment and acquisitions. Major changes include: the elimination of deferred assets and liabilities; the introduction of new rules for the accounting of derivatives; the adoption of limits on asset revaluation; and a reduction in the scope for shifting between different accounting standards in corporate accounts.43

The government also enhanced the credibility of auditing procedures by guaranteeing the independence of certified public accountants. In addition, the Law Concerning External Auditing of Joint Stock Corporations, which was passed in February 1998, and effective since April 1998, requires corporations to create an Auditor Selection Committee which includes outside directors and major creditors and shareholders. This law was aimed at enhancing public confidence in the external auditing of the listed companies and affiliates within conglomerates, and at increasing penalties on external audits and company accounts, so that trustworthiness of the financial statements and transparency of the business management would be enhanced.44 Furthermore, listed companies with assets of more than W1 trillion must now appoint a full-time statutory auditor. In addition, the government extended the minimum contract for an auditor to three years and restricted shareholders with more than 3% of common stock from executing their voting power above that level in the appointment of auditors.

40 Haggard, Lim and Kim,(eds.) (2001). 41 Whang. et al. (1999). 42 OECD (1998). 43 OECD (1999). 44 Whang. et al. (1999).

28

2) Introduction of Combined Financial Statements

The second effort to enhance transparency was the introduction of the mandatory combined financial statement.45 The Korean government agreed with the IMF to set the standards for combined financial statements by October 1998, introduce them in 1999 and require quarterly reporting in 2000. In the absence of combined financial statements, the extremely complicated web of intra-group loans, guarantees and other transactions remained opaque to most investors. 46 Thus the new combined financial statements system will make it easier to control reckless management by unifying the chaebols’ financial statements, which used to be under the control of the powerful owners, and clarifying intra-group transactions, shares held among affiliates, cross debt guarantees and credit trading.

A unique aspect of Korea’s approach is the broad definition given to the concepts of joint control or common management by the Fair Trade Commission in the combined statements.47 At the same time, the combined statements are to include disclosure of intra-group transactions and individual affiliate information in the footnotes, as well as segmented reporting (also known as business-line accounting).48

3) Improvement of Corporate Public Disclosure

The purpose of corporate public disclosure is to enable investors to bring reasonable judgement and to conduct fair business in the securities market by giving fast and accurate information on corporations, such as past, current, and future management and financial affairs, and business plans, and so on.49 Thus, corporate public disclosure activates a checking of the management and establishment of an efficient corporate governance structure by making public the important information on matter related to the corporations.

In the sixth Letter of Intent, the government agreed with the IMF to publish biannual financial statements, prepared and reviewed by external auditors in accordance with international standards by the end of August 1998; and to publish quarterly the non- 45 Combined financial statements are similar to consolidated financial statements, as their main purpose is to net out intro-group transactions (OECD1999). In Korea, the consolidated financial statements is usually substituted for the combined financial statement as the same. 46 OECD (1998). 47 OECD (1999). 48 Ibid. 49 KERI (2000).

29

audited financial statements beginning January 1, 2000. And in the case of Korean business conglomerates, publication of the combined financial statements for their affiliate companies is also required.

(2) Strengthening Minority Shareholder Rights

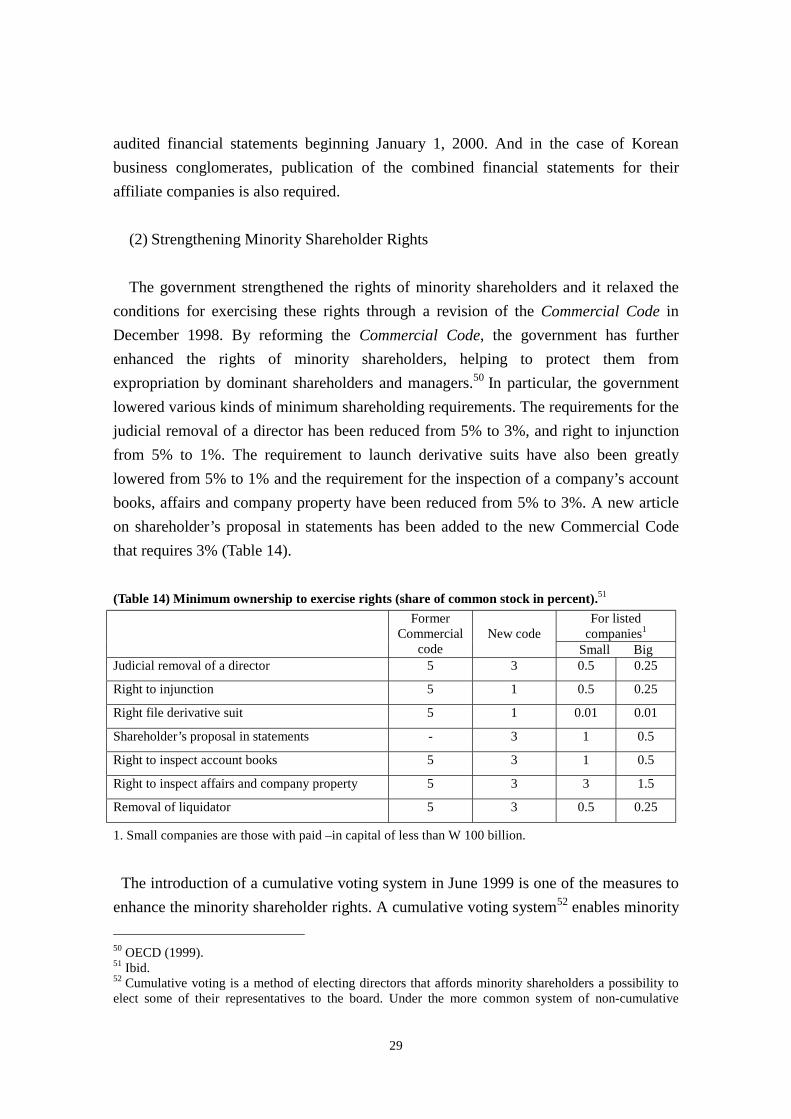

The government strengthened the rights of minority shareholders and it relaxed the conditions for exercising these rights through a revision of the Commercial Code in December 1998. By reforming the Commercial Code, the government has further enhanced the rights of minority shareholders, helping to protect them from expropriation by dominant shareholders and managers.50 In particular, the government lowered various kinds of minimum shareholding requirements. The requirements for the judicial removal of a director has been reduced from 5% to 3%, and right to injunction from 5% to 1%. The requirement to launch derivative suits have also been greatly lowered from 5% to 1% and the requirement for the inspection of a company’s account books, affairs and company property have been reduced from 5% to 3%. A new article on shareholder’s proposal in statements has been added to the new Commercial Code that requires 3% (Table 14).

(Table 14) Minimum ownership to exercise rights (share of common stock in percent).51

For listed companies1

Former Commercial

code

New code

Small Big Judicial removal of a director 5 3 0.5 0.25

Right to injunction 5 1 0.5 0.25

Right file derivative suit 5 1 0.01 0.01

Shareholder’s proposal in statements - 3 1 0.5

Right to inspect account books 5 3 1 0.5

Right to inspect affairs and company property 5 3 3 1.5

Removal of liquidator 5 3 0.5 0.25

1. Small companies are those with paid –in capital of less than W 100 billion.

The introduction of a cumulative voting system in June 1999 is one of the measures to enhance the minority shareholder rights. A cumulative voting system52 enables minority 50 OECD (1999). 51 Ibid. 52 Cumulative voting is a method of electing directors that affords minority shareholders a possibility to elect some of their representatives to the board. Under the more common system of non-cumulative

30

shareholders to appoint a director. And, institutional investors have been allowed to vote freely on mergers, business transfers and the election of directors and auditors with the removal of the “shadow voting” requirement. In addition, there has been a surge of investor activism in the wake of the crisis. Minority shareholders, led by citizen’s groups, such as the People’s Solidarity for Participatory Democracy, have prompted many long and animated discussions at annual general meetings, which were typically brief, and mere formalities in the past. By actively participating in the annual meetings of chaebol flagships and other major companies, minority shareholders have managed to prevent some moves by the groups to reassign assets to the detriment of shareholders and have scrutinized management proposals and intentions thoroughly.

(3) Strengthening the Responsibility of Controlling Shareholders and Management The important measure to strengthen the responsibility of controlling shareholders and management was to introduce the appointment outsider directors. The introduction of outside directors normalized the role of the board of directors by breaking from former practice of the board merely serving as a “rubber stamp” for management decisions.53 The controlling shareholders exercised enormous power over the appointment of directors so that it was very difficult for directors to secure their independence from the management and to check the management until now.

The government required the listed companies to appoint and authorize outside directors with the amendment of the Securities and Futures Commission from February 1998. Thereafter, all listed companies were required to have at least one outside director on their boards. Furthermore, since 1999, most listed companies have been required to appoint outside directors to fill one fourth of their board seats. In order for outside directors to fully fulfill their function, individual companies need to formulate and make public the operational guidelines for their executive boards to demonstrate their commitment to transparent management. 54

Another measure to strengthen the responsibility of controlling shareholders and management is to systemize the voting rights of institutional investors with the Securities Investment Trust Law. Before the crisis, the role of institutional investors in voting, the election of each individual direct-elect all of its candidates. In cumulative voting, in contrast, the number of votes one shareholder may cast corresponds to the number of his/her common stock shares multiplied by the number of seats on the board. The entire board is elected in one round of voting, allowing the votes to be concentrated on one candidate and giving the minority the possibility of electing directors (OECD (1999)). 53 KERI (2000). 54 Whang. et al. (1999).

31

supervising the controlling shareholders and management was severely curtailed because of the severe restrictions on their voting rights. Institutionalizing the voting rights of institutional investors would force the management to make their business decisions on the basis of profitability.

(4) Prohibition of Inappropriate Intra-Group Transactions and Debt Guarantees

1) Inappropriate Intra-Group Transactions

The Korea Fair Trade Commission has investigated inappropriate intra-group transactions55 since 1997 and has the authority to demand the submission of financial statements from the thirty largest conglomerates.

The rate of intra-group transactions of the listed companies of the top thirty groups in 1997 was 27.74% with the bigger groups showing a higher rate of such transactions as shown in Table 15. Also, the rate of these types of transactions had been on an upward swing since 1987. A provision added to the Fair Trade Act in 1996 made the “undue provision of money,” illegal, with “undue” defined as “a substantial deviation from the expected result of an arm’s length relationship in the market.”56 The Korea Fair Trade Commission can impose fines of up to 2% of the amount of the inappropriate intra-group transaction.

(Table 15) The rate of intra-group transactions among the top thirty groups.57 Group ‘86 ‘87 ‘88 ‘89 ‘96 ‘97 Top 5th 28.25 25.52 27.71 29.62 29.80 35.77

Top 10th 26.27 24.36 25.55 26.37 29.16 32.77 Top 20th 24.17 22.61 24.14 24.42 27.14 29.85 Top 30th 23.14 21.98 23.39 23.73 26.94 27.74 Source: KERI (2000).

The FTC launched three rounds of investigations between 1998 and 1999 on intra-group transactions among the top five chaebols. Eighty companies had provided a total of 4 trillion won of support to 35 affiliates and were fined W72.2 billion as a result of 55 Intra-group transactions mean business transactions between affiliates of one chaebol. All intra-group transactions can not regard as illegal because there can be necessary transaction between affiliates in any case. There are four types of illegal intra-group transaction; to give an advantage of prices of manufactured goods and terms and conditions of business to affiliate, to put pressure on executives and employees to buy or sell manufactures of affiliates, to force suppliers to buy manufactures of affiliates, and to avoid business transactions with non-affiliates without a good reason. 56 OECD (2000). 57 KERI (2000).

32

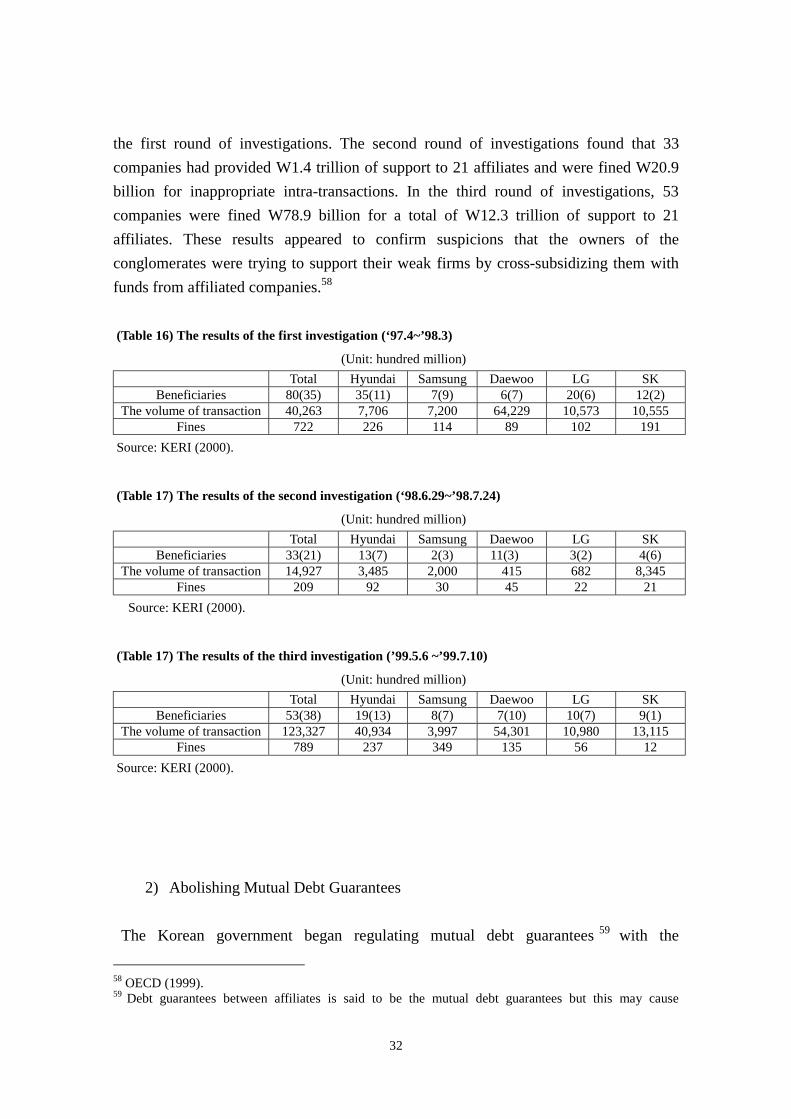

the first round of investigations. The second round of investigations found that 33 companies had provided W1.4 trillion of support to 21 affiliates and were fined W20.9 billion for inappropriate intra-transactions. In the third round of investigations, 53 companies were fined W78.9 billion for a total of W12.3 trillion of support to 21 affiliates. These results appeared to confirm suspicions that the owners of the conglomerates were trying to support their weak firms by cross-subsidizing them with funds from affiliated companies.58

(Table 16) The results of the first investigation (‘97.4~’98.3)

(Unit: hundred million) Total Hyundai Samsung Daewoo LG SK

Beneficiaries 80(35) 35(11) 7(9) 6(7) 20(6) 12(2) The volume of transaction 40,263 7,706 7,200 64,229 10,573 10,555

Fines 722 226 114 89 102 191 Source: KERI (2000).

(Table 17) The results of the second investigation (‘98.6.29~’98.7.24)

(Unit: hundred million) Total Hyundai Samsung Daewoo LG SK

Beneficiaries 33(21) 13(7) 2(3) 11(3) 3(2) 4(6) The volume of transaction 14,927 3,485 2,000 415 682 8,345

Fines 209 92 30 45 22 21 Source: KERI (2000).

(Table 17) The results of the third investigation (’99.5.6 ~’99.7.10)

(Unit: hundred million) Total Hyundai Samsung Daewoo LG SK

Beneficiaries 53(38) 19(13) 8(7) 7(10) 10(7) 9(1) The volume of transaction 123,327 40,934 3,997 54,301 10,980 13,115

Fines 789 237 349 135 56 12 Source: KERI (2000).

2) Abolishing Mutual Debt Guarantees The Korean government began regulating mutual debt guarantees 59 with the

58 OECD (1999). 59 Debt guarantees between affiliates is said to be the mutual debt guarantees but this may cause

33

amendment of the Fair Trade Act in 1993. As a result, the ratio of debt guarantees greatly decreased from 342% to 47.7% in 1997. However, the bankruptcies caused by excessive borrowing and affiliate expansion using debts as in the cases of Hanbo, Jinro, and Kia raised questions about the effectiveness of the regulations, so finally the Korean government decided to strengthen the limits on debt guarantees between affiliates of the top thirty groups to 100% beginning April 1998. And new debt guarantees among chaebol affiliates were prohibited and required to be eliminated by March 2000. Debt guarantees scheduled to expire in 2001 or beyond are to be negotiated with banks for extensions. (Table 18) Trends of Debt Guarantees of the Top 30 Groups

(Unit: Trillion Won, %) Debt Guarantee Net Worth to Total Assets Date Equity

(A) Total(B) Restricted Companies(C)

Excluded Companies(D)

B/A C/A

1993.4.1 35.2 165.5 120.6 44.9 469.8 342.4 1994.4.1 42.8 110.7 72.5 38.2 258.1 169.3 1995.4.1 50.7 82.1 48.3 33.8 161.9 95.2 1996.4.1 62.9 67.5 35.2 32.3 107.3 55.9 1997.4.1 70.4 64.9 33.6 31.3 92.2 47.7 1998.4.1 68.1 63.5 26.9 36.6 93.1 39.5 1999.4.1 100.1 22.4 9.8 12.6 22.3 9.7 Source: FTC (2000).

(Table 19) Financial Structure of Insolvent Companies

(%) Hanbo Sammi Jinro Kia 30 Largest Debt Ratio(End of 1996) 675 3,244 3,746 517 387 Debt Guarantee Ratio (April 1997)

309.4 740.7 473.3 110.8 91.3

Dependency on Loans 57.7 62.7 78.2 51.3 48.4 Financial cost rate 5.8 14.5 21.4 7.0 4.9 Increase Rate of Affiliates(Past 3 Years)

262.5 - 200 200 31.5

Net Income (in KRW billion) -46 -125 -138.1 -125.1 12.3 Source: FTC (2000).

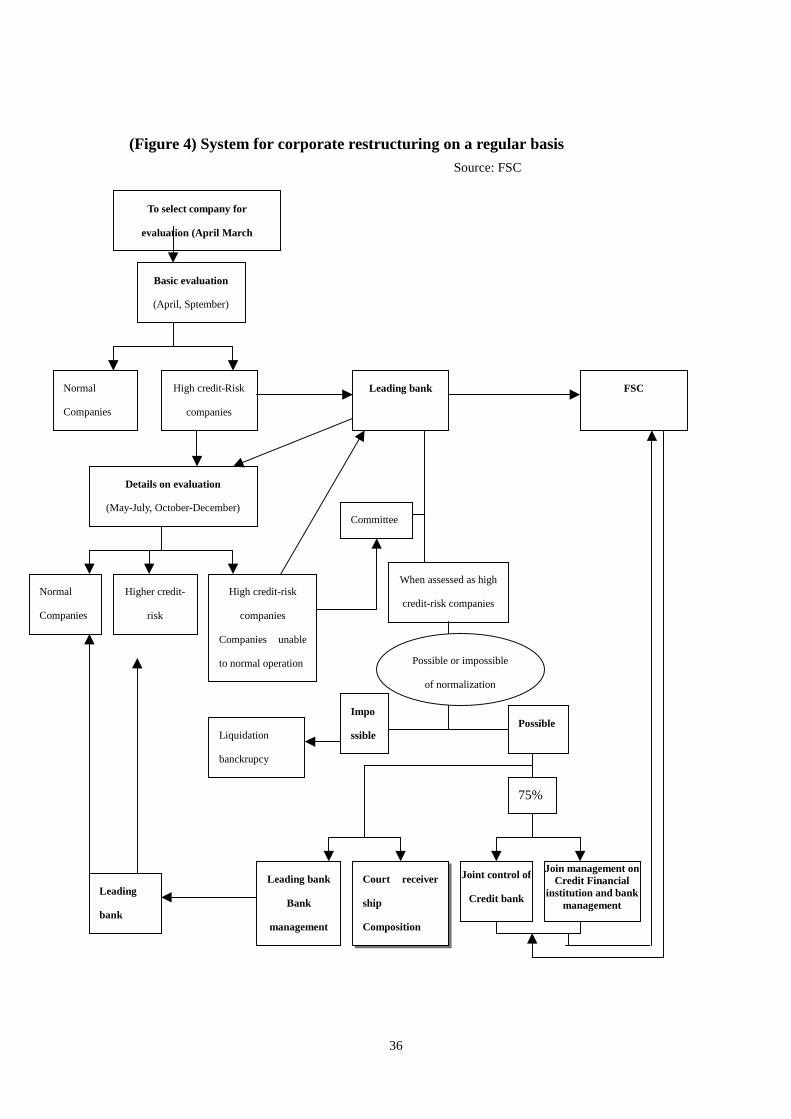

III. Second-Stage of Corporate Restructuring

The second-stage of corporate restructuring is characterized as a trial towards a market-based system. The first-stage reforms greatly contributed to the restoration of

misunderstanding. Statistically, most of debt guarantees between affiliates assume the form that a few competent affiliates guarantee debt of affiliates which start a new business and have difficulty in lending because they lost the credit standing of a firm. Thus, there has been no dent guarantees between affiliate A and B.

34

confidence in Korea and its economic recovery beginning in the third quarter of 1998. However, by mid-2000, the pace of reform had slowed, reflecting complacency in the

high rate of output growth and the politicization of economic issues in the national election in April 2000. The slowdown in growth in late 2000 exacerbated the underlying weakness in the corporate sector. In addition, the credit risks in the sector continued to threaten the viability of many financial institutions, and vise versa. In this situation, the government launched a second round of reforms to address the problems and restore confidence in the Korean economy.