Meaningful & mutually beneficial trading relationship ... · 94 95 96 97 98 99 '00 '01 '02 '03 '04...

32

Is there a meaningful and mutually beneficial trading relationship between the USA and South Africa. Any opportunities for Agribusiness? John Purchase South Africa Protein Seminar 3 March 2011

Transcript of Meaningful & mutually beneficial trading relationship ... · 94 95 96 97 98 99 '00 '01 '02 '03 '04...

Is there a meaningful and mutually beneficial trading relationship

between the USA and South Africa. Any opportunities for Agribusiness?

John Purchase

South Africa Protein Seminar

3 March 2011

Content

• Background

• South Africa’s agriculture

• South Africa’s agricultural trade

• SA/US Agricultural trade

• Opportunities for agribusiness?

• Conclusion

Background • Trade relations between US and SA governed

by AGOA and TIDCA

• AGOA I to AGOA IV – runs out Sept 2012 and up for revision

• AGOA has encouraged substantial new investments, trade and job creation in Africa

• Helped to integrate SSA’s integration into multi-lateral trading system

• Contributed to economic and commercial reforms, making African countries attractive

• commercial partners

Background AGOA Implementation:• Determination of country eligibility• Determination of products eligible for zero

tariff under expansion of GSP• Determinations of compliance with the

conditions of apparel benefits• Establishment of US-SSA Trade & Economic

Forum• Provisions for technical assistance to help

countries qualify for benefits

Background

• US-SACU TIDCA signing in Washington in July 2008

• Promotes an attractive investment climate expands and diversifies trade between SACU (incl. SA) and US

• Consultative Group to ensure fulfilment of above objectives

• Consultation and Cooperation provisions

Content

• Background

• South Africa’s agriculture

• South Africa’s agricultural trade

• SA/US Agricultural trade

• Opportunities for agribusiness?

• Conclusion

Role of Agriculture in

SA Economy• Strategic sector – provides food, fiber, wine & beer,

satisfying two basic needs of man (+ others!)

• Has provided national food security since the start

of the 20th century (Pop: ~4,0 million), right

through to the 21st century (Pop: ~49,0 million,

~60% in urban areas)

Contribution of Primary Agriculture to GDP (Source: Statssa)

2

3

4

5

94 95 96 97 98 99 '00 '01 '02 '03 '04 '05 06 07 08 09

%

SA economic growth: Tradable goods sectors lag the non-tradable goods sectors

Source: StatsSA

0

50

100

150

200

250

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

IND

EX

GDP Index per Sector of Economy

GDP

Agric

Mining

Manufacturing

Construction

Trade

Transport

Finance

Inflation

Source: AMT, 2010

Commercial Agric Census 2007

Indicator 1993 2002 2007

Farming units 57 980 45 818 39 982

Gross Farm income (R x1 000 000) 19 620 53 329 79 544

Employees Remuneration (R X1 000 000) 3 637 6 216 8 611

Paid employees 1 093 265 940 820 796 806

Expenditure (R X1 000 000) (Current & Cap) 16 377 45 038 54 072

Market value of assets (R X1 000 000) 66 905 98 428 178 647

Farming debt (R X1 000 000) 15 295 30 857 37 090

Ratio between Farming Debt and GFI (%) 78,0 57,9 46,6

Source: StatsSA

OIL SEED & GRAIN CROP PRODUCTION IN THE RSA (TON)(2006/2007-2010/2011 MARKETING SEASONS)

CROP 2006/2007 2007/2008 2008/2009 2009/2010 2010/2011

White maize 4,187,400 4,315,000 7,480,000 6,775,000 7,822,400

Yellow maize 2,430,600 2,810,000 5,220,000 5,275,000 5,220,600

Sorghum 96,000 176,000 255,000 276,500 220,093

Groundnuts 74,000 58,000 88,800 99,500 87,880

Sunflower 520,000 300,000 872,000 801,000 516,265

Soybeans 424,000 205,000 282,000 516,000 560,950

Cotton seed 25,962 19,525 17,378 15,658 14,576

Wheat 2,105,000 1,905,000 2,130,000 1,958,000 1,570,980

Canola 36,500 38,150 30,800 40,350 39,650

Source: NCEC, PRF

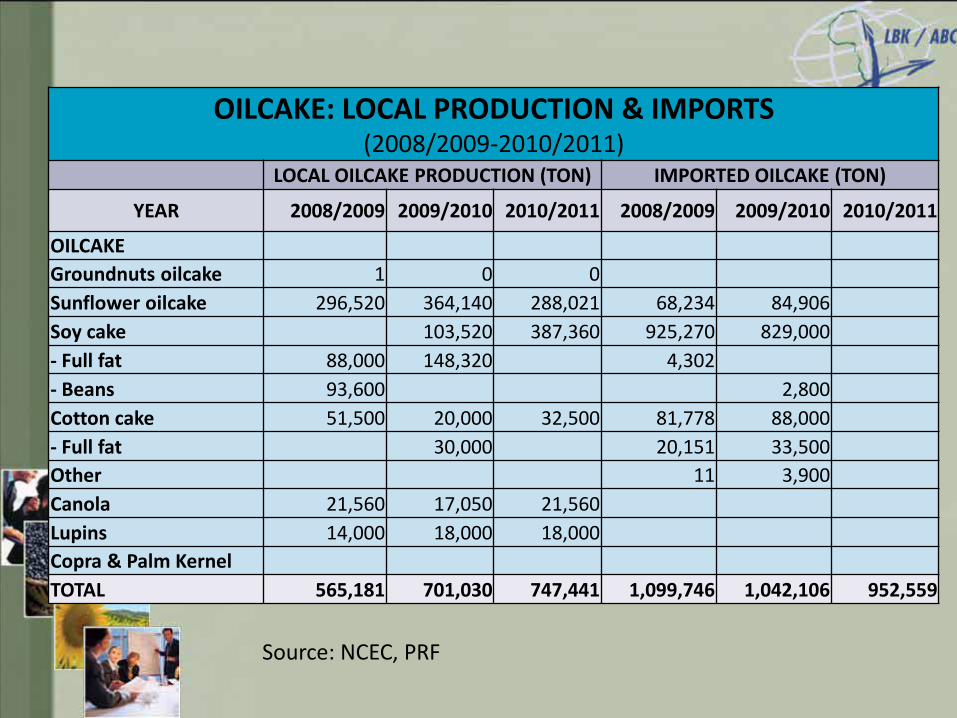

OILCAKE: LOCAL PRODUCTION & IMPORTS(2008/2009-2010/2011)

LOCAL OILCAKE PRODUCTION (TON) IMPORTED OILCAKE (TON)

YEAR 2008/2009 2009/2010 2010/2011 2008/2009 2009/2010 2010/2011

OILCAKE

Groundnuts oilcake 1 0 0

Sunflower oilcake 296,520 364,140 288,021 68,234 84,906

Soy cake 103,520 387,360 925,270 829,000

- Full fat 88,000 148,320 4,302

- Beans 93,600 2,800

Cotton cake 51,500 20,000 32,500 81,778 88,000

- Full fat 30,000 20,151 33,500

Other 11 3,900

Canola 21,560 17,050 21,560

Lupins 14,000 18,000 18,000

Copra & Palm Kernel

TOTAL 565,181 701,030 747,441 1,099,746 1,042,106 952,559

Source: NCEC, PRF

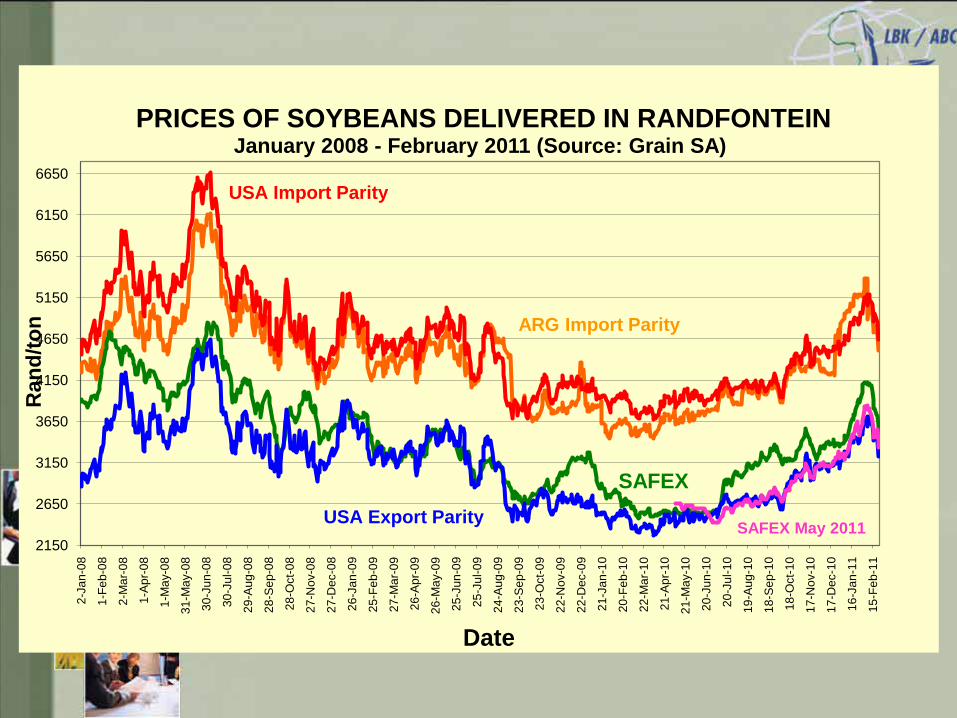

2150

2650

3150

3650

4150

4650

5150

5650

6150

6650

2-J

an

-08

1-F

eb

-08

2-M

ar-

08

1-A

pr-

08

1-M

ay-0

8

31

-Ma

y-0

8

30

-Ju

n-0

8

30

-Ju

l-0

8

29

-Au

g-0

8

28

-Se

p-0

8

28

-Oct-

08

27

-Nov-0

8

27

-Dec-0

8

26

-Ja

n-0

9

25

-Fe

b-0

9

27

-Ma

r-0

9

26

-Ap

r-0

9

26

-Ma

y-0

9

25

-Ju

n-0

9

25

-Ju

l-0

9

24

-Au

g-0

9

23

-Se

p-0

9

23

-Oct-

09

22

-Nov-0

9

22

-Dec-0

9

21

-Ja

n-1

0

20

-Fe

b-1

0

22

-Ma

r-1

0

21

-Ap

r-1

0

21

-Ma

y-1

0

20

-Ju

n-1

0

20

-Ju

l-1

0

19

-Au

g-1

0

18

-Se

p-1

0

18

-Oct-

10

17

-Nov-1

0

17

-Dec-1

0

16

-Ja

n-1

1

15

-Fe

b-1

1

Ran

d/t

on

Date

PRICES OF SOYBEANS DELIVERED IN RANDFONTEINJanuary 2008 - February 2011 (Source: Grain SA)

ARG Import Parity

USA Import Parity

SAFEX

USA Export ParitySAFEX May 2011

Content

• Background

• South Africa’s agriculture

• South Africa’s agricultural trade

• SA/US Agricultural trade

• Opportunities for agribusiness?

• Conclusion

Agricultural trade trends

16

Source: DAFF/NAMC, 2009.

Total

-

5

10

15

20

25

2004 2005 2006 2007 2008

R b

illi

on

Year

Primary exports Primary imports Primary trade balance

Primary

-10

-5

-

5

10

15

20

25

30

35

2004 2005 2006 2007 2008

R b

illi

on

Year

Processed exports Processed imports Processed trade balance

Processed

Agricultural trade

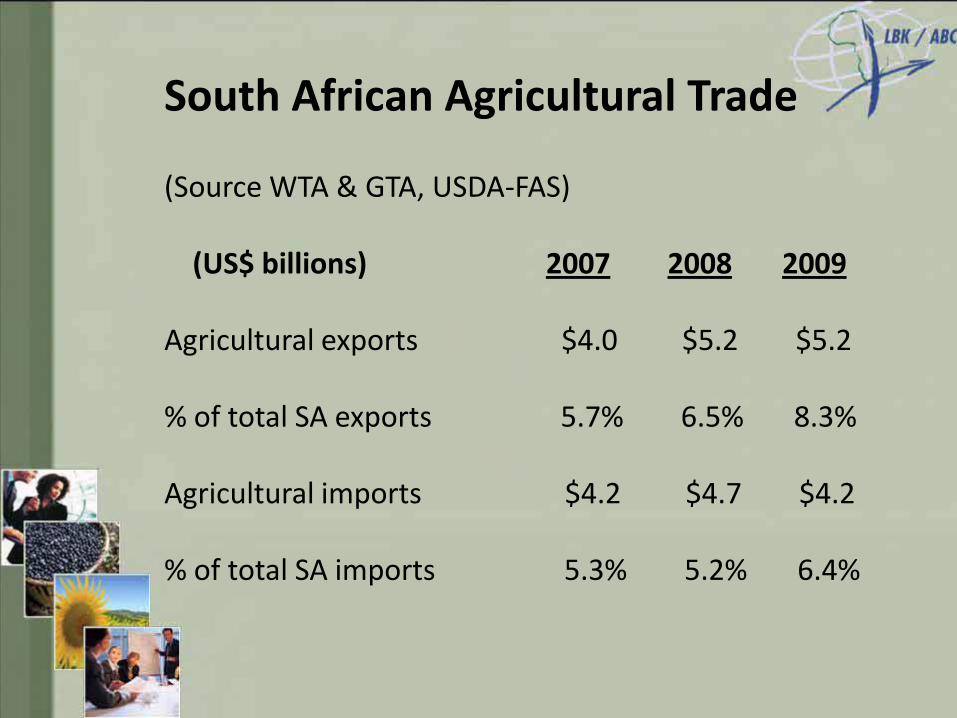

South African Agricultural Trade

(Source WTA & GTA, USDA-FAS)

(US$ billions) 2007 2008 2009

Agricultural exports $4.0 $5.2 $5.2

% of total SA exports 5.7% 6.5% 8.3%

Agricultural imports $4.2 $4.7 $4.2

% of total SA imports 5.3% 5.2% 6.4%

Major agricultural products exported:

(US$ millions) 2007 2008 2009

Wine $673.6 $753.9 $727.5

Citrus $613.1 $711.4 $667.1

Corn $32.1 $510.3 $444.6

Table grapes $364.5 $387.6 $379.7

Apples $329.5 $367.3 $364.7

Sugar $276.1 $217.9 $386.7

Major export destinations (2009)

United

Kingdom

Netherlands

Zimbabwe

Kenya

Mozambique

Germany

United States

China

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0%

Major agricultural products imported:

(US$ millions) 2007 2008 2009

Rice $302.1 $463.9 $458.8

Wheat $261.6 $444.6 $282.0

Soybean cake $209.8 $311.9 $297.1

Palm oil $195.7 $299.3 $232.1

Soybean oil $212.0 $288.5 $106.9

Whisky $212.5 $202.9 $201.6

Major countries imported from (2009)

Argentina

Brazil

Thailand

Germany

Malaysia

China

Netherlands

Indonesia

United States

0% 2% 4% 6% 8% 10% 12% 14% 16%

Content

• Background

• South Africa’s agriculture

• South Africa’s agricultural trade

• SA/US Agricultural trade

• Opportunities for agribusiness?

• Conclusion

US – SA Agricultural trade

(US$ millions) 2007 2008 2009 2010

SA ag-exports to US $174.8 $174.6 $173.5 $223.6

% of total exports to US 2.1% 1.9% 3.2% N/A

SA ag-imports from US $290.6 $393.2 $161.7 $291.9

% of total imports from US 4.8% 4.3% 3.1% N/A

Major agricultural products exported

to the US:

(US$ millions) 2007 2008 2009 2010

Wine & Beer $41.7 $44.5 $39.9 $45.1

Fresh fruit $46.7 $41.8 $40.3 $50.5

Sugar $10.2 $0.0 $21.1 $25.1

Tree nuts $11.1 $14.2 $15.9 $28.5

Fruit juice $10.8 $14.7 $11.9 $15.8

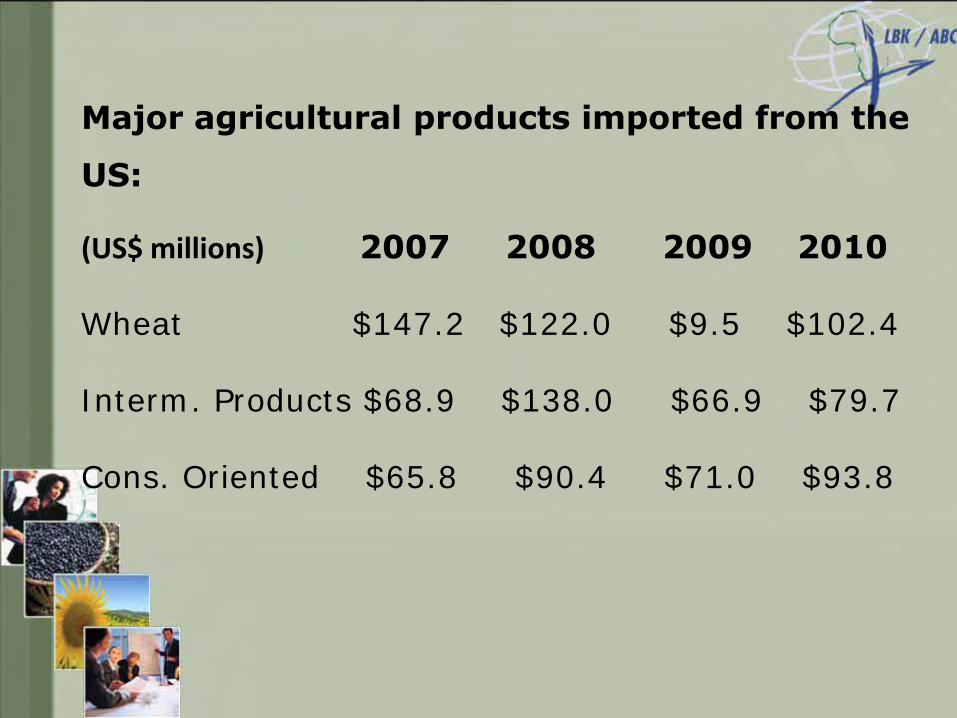

Major agricultural products imported from the

US:

(US$ millions) 2007 2008 2009 2010

Wheat $147.2 $122.0 $9.5 $102.4

Interm. Products $68.9 $138.0 $66.9 $79.7

Cons. Oriented $65.8 $90.4 $71.0 $93.8

Content

• Background

• South Africa’s agriculture

• South Africa’s agricultural trade

• SA/US Agricultural trade

• Opportunities for agribusiness?

• Conclusion

SAARF LSM Segments: Proportion of SA adult population and average monthly household

income in 2009

Source: SAARF (2010a) & BFAP, 2010

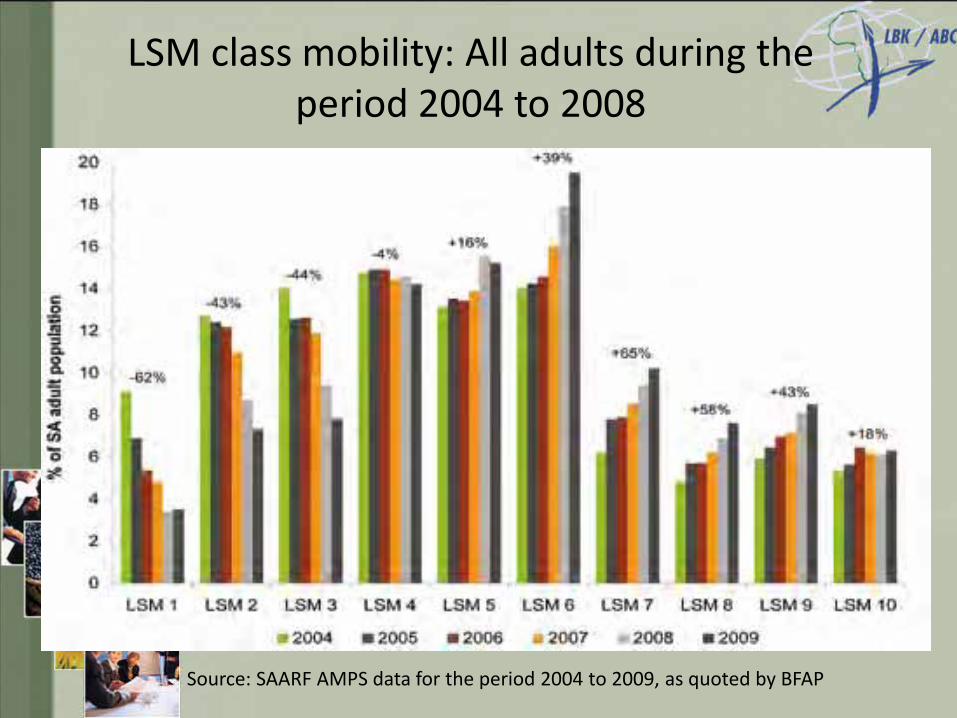

LSM class mobility: All adults during the period 2004 to 2008

Source: SAARF AMPS data for the period 2004 to 2009, as quoted by BFAP

Opportunities for agribusiness?

• SA population: ~49.8 million, and growing.

• Growing SA middle class – market expansion

• Consumer behaviour patterns changing

• Value added and processed products, e.g. dairy & processed veg & fruit

• Niche markets developing faster, e.g. Organics, etc.

• Wheat

Content

• Background

• South Africa’s agriculture

• South Africa’s agricultural trade

• SA/US Agricultural trade

• Opportunities for agribusiness?

• Conclusion

Conclusion

• Is there a meaningful and mutually beneficial trading relationship between the USA and South Africa?

Yes, most certainly, and growing.

• Any opportunities for Agribusiness?Yes, but need to look for specific opportunities and do good market research.

Thank you

www.agbiz.co.za