MBTA Pension Update - MBTA - cdn.mbtace.com · MBTA Pension Update June 27, ... *Uses age rates for...

32

MBTA Pension Update June 27, 2016 FMCB

Transcript of MBTA Pension Update - MBTA - cdn.mbtace.com · MBTA Pension Update June 27, ... *Uses age rates for...

MBTA Pension Update

June 27, 2016

FMCB

Fiscal and Management Control Board

2

Draft for Discussion & Policy Purposes Only

• MBTA Retirement Fund is governed by the Pension Agreement between the MBTA and the L589 Carmen’s Union

› Agreement covers administration of the fund, contributions made to the fund, benefits paid to retirees, management of fund assets, and eligibility for retirement

› Latest agreement went in effect on 7/1/2014 and lasts until 6/30/2018

• MBTA Retirement Fund is independent and run by the MBTA Retirement Board

• MBTARF is governed by a 7 member board with union and management representation

› Makes decisions concerning the investment of funds, determination of benefits paid to members, level of required contributions by the MBTA, and the release of public information on the fund

› The MBTA management and employees have no direct control over these decisions

Overview of MBTA Retirement Fund:MBTA RF critical to the MBTA’s employees and its financial stability

Introduction

Fiscal and Management Control Board

3

Draft for Discussion & Policy Purposes Only

MBTA Main Fund pension assets have declined by 13% over the past 10 years

Main Fund – Asset Trend

0.0

0.5

1.0

1.5

$2.0B

Year-End Main Fund Pension Net Assets: Market Value

(not including unfunded liability)

CY05

1.71

CY06

1.86

CY07

1.92

CY08

1.31

CY09

1.42

CY10

1.49

CY11

1.39

CY12

1.48

CY13

1.61

CY14

1.59

CY15

1.50

-13%-13%

Note: As of 6/23/16, Buck (Actuaries) has received final 12/31/15 asset valuation of the Main Fund. Estimate is $1.498B.Source: MBTARF Annual Reports

Fiscal and Management Control Board

4

Draft for Discussion & Policy Purposes Only

While MBTA RF asset balance has declined, other state pensions have increased

Main Fund – Asset Trend

0.0

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

Market Value of Assets (2005=1)

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

-7%

+54%

+25%+32%

'05-'14Change

$1.7B

$3.7B

$20.0B$17.9B

$1.6B

$5.7B

$25.0B$23.6B

MA State Emp.

Retirement System MA Teacher's

Retirement System

State-Boston

Retirement System

MBTA Main Fund

2005

Assets2014

Assets

Source: MBTARF Annual Reports; PERAC

Fiscal and Management Control Board

5

Draft for Discussion & Policy Purposes Only

Why have MBTA Main Fund assets declined over past 10 years?

Main Fund – Asset Trend

• Two factors have driven the decline in MBTA Main Fund assets over past 10 years:

1. Fund is in a “net outflow” position (annual benefits paid to retirees exceed contributions by MBTA and members)

• MBTA has more retirees than active members

2. Fund net outflow % has exceeded fund investment return %

• Fund assets will decline in any year in which net outflow % exceeds investment return %

Fiscal and Management Control Board

6

Draft for Discussion & Policy Purposes Only

Definition of net outflow as a percentage of total assets

Main Fund – Net Outflows

Net Outflow as a percentage of net assets

=Net Outflow ( ) in year

Total Net Assets in fund at end of year

MBTA 2015:5.9%

Net Outflow = Total Contributions to pension (+$98M) – Total Benefits paid out to retirees (-$187M)

MBTA 2015:-$89M

A

BA

Fiscal and Management Control Board

7

Draft for Discussion & Policy Purposes Only

In 2015, total fund assets declined by $89M

Main Fund – Net Outflows

*As of 6/23/16, Buck (Actuaries) has received final 12/31/15 asset valuation of the Main Fund. Estimate is $1.498B.Source: MBTARF Annual Reports

0

1,500

1,550

1,600

1,650

$1,700M

Total Additions and Deductions from the Main

Fund, 2015

2014 Assets

(End of Year)

$1,588M

Investment

Return and

Income*

$3M

Contributions

$98M

Benefits Paid

-$187M

Admin.

Expenses*

-$4M

2015 Assets

(End of

Year)*

$1,498M

Net Outflow: $89MA

Fiscal and Management Control Board

8

Draft for Discussion & Policy Purposes Only

0

2

4

6%

2015 net outflow as a % of total assets

(not including investment return)

MBTARF

5.9%

State-Boston

Retirement

System

(SBRS)

1.2%

Mass.

Teachers'

Retirement

System

(MTRS)

3.4%

Mass. State

Employees'

Retirement

System

(MSERS)

2.5%

MBTA RF net outflow % is higher than other MA pension funds

Main Fund – Required Returns

• MBTARF has net outflow of (-$89M) on net assets of $1.5B in CY15 before investment returns

• SBRS had net outflow of (-$67M) on assets of $5.7B in FY14 before investment returns

• MTRS had net outflow of (-$865M) on assets of $25B in FY15 before investment returns

• MSERS had net outflow of (-$595M) on assets of $23.8B in FY15 before investment returns

Net Outflow as a %of net assets =

Net Outflow

Total Fund Assets

B

Source: MBTA Pension Fund Data; PRIM Annual Report

Fiscal and Management Control Board

9

Draft for Discussion & Policy Purposes Only

MBTA RF’s lower active-to-retired ratio is driven by younger age of eligibility for full benefits

Comparison of MBTA and State Employee Plans

0.0

0.5

1.0

1.5

2.0

Active-to-Retired Member Ratio

MBTARF

0.9X

State-Boston

Retirement

System (SBRS)

1.4X

Massachusetts

Teachers'

Retirement

System (MTRS)

1.4X

Massachusetts

State Employees'

Retirement

System (MSERS)

1.6X

6,478 14,341 62,873 58,454Retired Members

69.2 73.1 71.3 72.1Average Age

of Retirees*

5,868 20,278 88,814 91,298Active Members

Active-to-Retired

Ratio

*Normal retirement only; disability and beneficiaries/survivors excludedNote: MBTARF figures as of 12/31/2015; MTRS, MSERS figures as of 6/30/2015; SBRS figures as of 12/1/2014Source: MSTERS, SBRS, MTRS Annual Reports

Fiscal and Management Control Board

10

Draft for Discussion & Policy Purposes Only

MBTA calculation uses higher rate of benefit for younger retirees than state

Comparison of MBTA and State Employee Plans

Years of service

Age at retirement Employer Annual multiplier*

Pension % of highest wages

25 55MBTA 2.46% 61.5%

State 1.50% 37.5%

25 60MBTA 2.46% 61.5%

State 2.00% 50.0%

25 65MBTA 2.46% 61.5%

State 2.50% 62.5%

32 65MBTA 2.46% 75%^

State 2.50% 80%

*Uses age rates for state employees hired before 4/2/2012^Calculation produces result >75%, which is adjusted down to maximum benefitNote: MBTARF benefits do not get automatic COLAs; retirees in State systems do (those covered by Chapter 32)

Years of service x Annual Multiplier = Pension % of Highest Wages

Because MBTA pension multiplier does not grow with age, benefits for early retirees are significantly higher than those for state employees

Fiscal and Management Control Board

11

Draft for Discussion & Policy Purposes Only

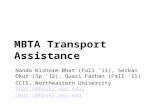

0

5

10

15%

Employee pension contribution rate

FY16 MBTA

employee

contribution

Pension

contribution

rate

5.8%

5.8%

State employees (all

other employees)

Pension

contribution

rate

9%

Additional

contribution*

11.0%

MA Teachers

Pension

contribution

rate

11%

11.0%

MA State police and

inspectors

Pension

contribution

rate

12%

Additional

contribution*

14.0%

MBTA employees contribute 5.8% of payroll to their pension – state employees contribute anywhere from 11-14%

Comparison of MBTA and State Employee Plans

*An additional 2% of all income over $30K is contributed to the fund†Rates cover most state employeesNote: State contribution rates shown are for state police and inspectors and state employees hired after 7/1/1996 and teachers

hired after 7/1/2001

Fiscal and Management Control Board

12

Draft for Discussion & Policy Purposes Only

Average retiring MBTA employee (hired before 12/2012) Total projected lifetime benefits: $1.65M; Total career contributions: $47K

Retiree Benefits and Member Contributions

Note: Medical and life includes Retiree Life Insurance, Retiree Medical (provided through the GIC, with premium-sharing between MBTA and retirees), Retiree Part B premium reimbursement; See backup for details on post-retirement healthcare

*Main Fund only, does not include deferred compensation^None of the figures have been discounted† MBTA average annual cost over retirement for retiree medical and life is $19.8K p.a. for Medical Insurance, $3.7K p.a. for Part B, $0.5K p.a. for Life InsuranceAs of 2014, annual retiree medical costs are $9.3K p.a. for Medical Insurance, $2.1K p.a. for Part B, $0.3K p.a. for Life InsuranceSource: Buck Consulting Actuaries

0

500

1,000

1,500

$2,000K

MBTA retirement contributions and benefits

(excluding social security)^

Employee and MBTA

Lifetime Contributions

$161K

Employee Lifetime

Retirement Benefits

$1,651K

Employee Pension ContributionMBTA Pension Contribution Pension*

Medical and Life

U

For the average employee who is currently eligible to retire:

• Employee will have contributed $47K over their career to the pension fund (MBTA contributes the rest)

• They will receive $1.1M in pension benefits

o $43.6K in pension benefits per year for 24.4 years (actuarially estimated pension benefit duration)

• They will receive $583K in medical and life benefits

• $23.9K† in medical and life benefits per year for 24.4 years (actuarially estimated medical and life benefit duration)

• Difference is funded by MBTA contributions ($114K), unvested employees’ contributions, and investment returns on both MBTA’s and employee’s contributions

• However, an unfunded liability exists because

A. Investment returns have not been high enough to cover future pension payments to the employee; and

B. Changes in actuarial assumptions to reflect longer lives and other changes in MBTA retiree population have increased the total liability

Unfunded (pay as you go)

Fiscal and Management Control Board

13

Draft for Discussion & Policy Purposes Only

MBTA Main Fund recent annual returns compared to target return rate

Main Fund – Investment Returns

0

5

10

15

20%

Main Fund Annual Rate of Net Return

7.75%

CY2011

0.8%

CY2012

14.0%

CY2013

16.4%

CY2014

4.8%

CY2015*

0.5%

YTD CY2016

(Jan-May)*

1.5%

7.75%

Net Annual

Return Below

Target

Target Rate of

Return (as of

2/19/2016)Net Annual

Return Above

Target

Target rate of returnis the rate at which a fund is expected to return over the long

term; fund is not expected to beat target

rate each year

*CY15 is an estimate and won’t be complete until the audit is finalized; CY16 returns are for the first 5 months, January to May; CY16 includes 1-3 month valuation lag of alternative investmentsSource: MBTA Pension Fund Data

Fiscal and Management Control Board

14

Draft for Discussion & Policy Purposes Only

0

1,000

2,000

$3,000M

3%

4%

5%

6%

6.75%

7.75%

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

211 215 219 223 227 230 234 237 240 243187 244 244 244 243 241 238189 193 195 199 201 204 208

122 125 128 132 135 139 143 147 151 15598 159 163 167 172 177 18196 104 106 109 112 115 118

-90 -90 -91 -92 -92 -91 -91 -90 -90 -88-89 -85 -81 -76 -71 -64 -56-93 -89 -89 -89 -89 -89 -89

Main Fund Pension Assets

2%

Outflow

Contribution

Net ($M)

7.75%6.75%6.00%5.00%4.00%3.00%2.00%

Sensitivity Analysis: MBTA Main Fund asset base at various levels of investment return

PROJECTION: Main Fund Assets in a 4% return environment

Assumed Rate of Return

MBTA Pension Sensitivity

$1.5BValue on12/31/15

Note: Model used is preliminary has not undergone actuarial peer reviewSource: MBTA Main Fund Asset and Contribution Projection Model

DRAFT FOR DISCUSSION

Key Assumptions

• Contribution rate as a percentage of payroll remains constant at 24%−MBTA rate

17.7%• Payroll grown at 2.7%, the ten year historic avg.

Fiscal and Management Control Board

15

Draft for Discussion & Policy Purposes Only

0

500

1,000

$1,500M

Main Fund Pension Assets

(not including unfunded liability)

2015

$1,498M

2020

$1,325M

2025

$1,117M

2030

$856M

2035

$576M

Sensitivity Analysis: What is the trend on asset balance of MBTA Main Fund if future investment returns averaged 4%?

PROJECTION: Main Fund Assets in a 4% return environment

Note: Model used is preliminary has not undergone actuarial peer reviewSource: MBTA Main Fund Asset and Contribution Projection Model

Key Assumptions

• Fund returns 4% annually

• Contribution rate % of pay roll remains constant: 24% (of which MBTA pays 17.7%)

• Annual payroll grows at 2.7% (10 year historic avg.)

DRAFT FOR DISCUSSION

Fiscal and Management Control Board

16

Draft for Discussion & Policy Purposes Only

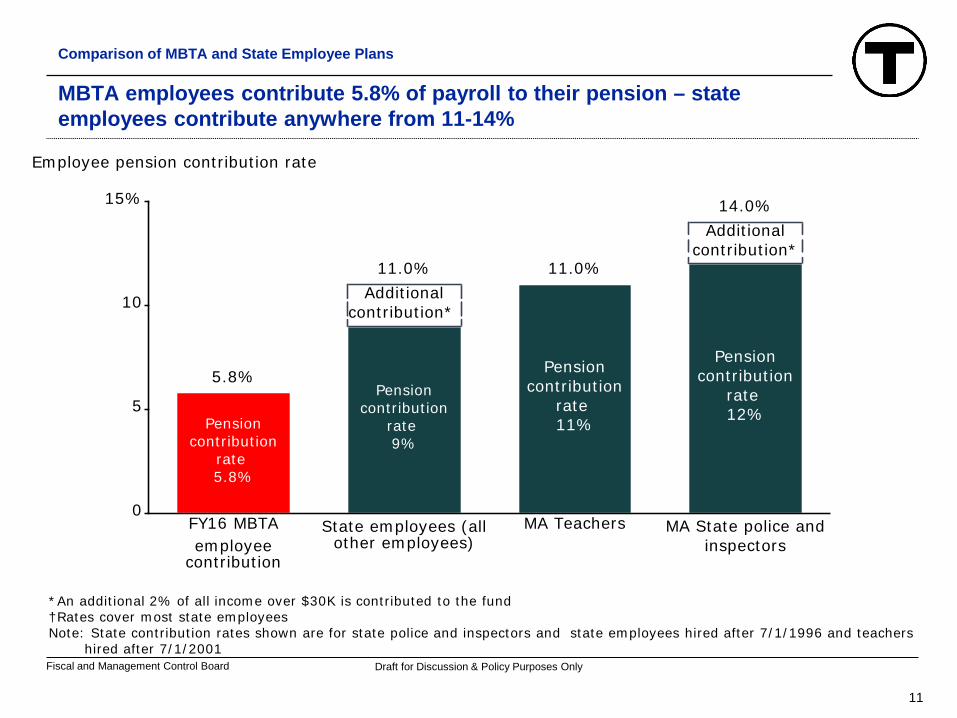

Main Fund – Unfunded Liability

0

1

2

$3B

Year-End Main Fund Pension Net Assets and Liability: Actuarial Value

CY05

1.71

0.16$1.87B

CY06

1.83

0.11$1.94B

CY07

1.90

0.19$2.09B

CY08

1.73

0.41

$2.14B

CY09

1.67

0.55

$2.22B

CY10

1.65

0.69

$2.34B

CY11

1.55

0.73

$2.28B

CY12

1.46

0.86

$2.31B

CY13

1.61

0.76

$2.36B

CY14*

1.63

0.87

$2.50B

CY15*^

1.63

0.94

$2.57B

Actuarial Value of Pension AssetsUnfunded Liability

*Assumed rate of return decreased from 8.00% to 7.75% in 2016; CY14, CY15 shown with 7.75% rate^ Actuarial Value of Assets as estimated by MBTA; As of 6/23/16, Buck (Actuaries) has received final 12/31/15 asset valuation of the Main Fund

and is in process of producing the valuation. Market Value of Assets Estimate is $1.498B. Preliminary Actuarial Accrued Liability is $2.572B. This figure was $2.447 in 2014.

Source: MBTARF Annual Reports; Buck Consultants Actuarial Valuations

Total pension liability was $2.6B at 12/31/15Funded actuarial value is 63%

Actuarial value of assets equals market value less a five-year phase-in of the differences between actual

and assumed investment return

DRAFT FOR DISCUSSION

Fiscal and Management Control Board

17

Draft for Discussion & Policy Purposes Only

Pension unfunded liability:Actuarial value of assets vs. Market value of assets

Main Fund – Unfunded Liability

0

20

40

60

80

100%

Total pension liability

(based on 2015 actual assets and total pension liability)

Actuarial Asset Value*

2015 Actuarial Value of

Assets ($1.628B)

$1,628M - (63%)

Unfunded Actuarial

Liability (based

on 2015 Pension Liability

at 7.75% discount rate)

$944M - (37%)

$2,572M (2015)

Market Asset Value*

2015 Market Value of

Assets ($1.498B)

$1,498M - (58%)

Implied Unfunded

Liability (based

on 2015 Pension Liability

at 7.75% discount rate)

$1,074M - (42%)

$2,572M (2015)

*Actuarial Value of Assets as estimated by MBTA; As of 6/23/16, Buck (Actuaries) has received final 12/31/15 asset valuation of the Main Fund and is in process of producing the valuation. Market Value of Assets Estimate is $1.498B. Preliminary Actuarial Accrued Liability is $2.572B. This figure was $2.447 in 2014.

**Total Liability assumed to be constant from 2014 to 2015Source: MBTA Analysis; Buck Consultants Actuarial Valuations

DRAFT FOR DISCUSSION

Fiscal and Management Control Board

18

Draft for Discussion & Policy Purposes Only

Where do we go from here?MBTA contributions to Main Fund have more than doubled over past 10 years

MBTA Pension Future Outlook

0

20

40

60

80

$100M

MBTA contribution to Main Fund

FY07

$37M

FY17 Budget

$87M

Note: $7.0M in contributions during FY07 were retroactive ‘catch-up’ payments for previous years in which not enough had been contributed compared with contractual obligations; these have been removedSource: MBTA Financials

MBTA contribution has risen from 9.5% to 17.7%

Fiscal and Management Control Board

19

Draft for Discussion & Policy Purposes Only

0

25

50

75

100

$125M

Estimated annual MBTA contribution to

pension fund at 4% annual investment return

FY17E

$87M

FY18E

$92M

FY19E

$96M

FY20E

$101M

FY21E

FY16 Base

Estimated

Contribution

Growth

$107M

5%

FY17-FY21CAGR

17.7% 18.2% 18.6% 19.1% 19.6%MBTA

Contribution

Rate

In a 4% return environment, MBTA annual required contribution will likely exceed $100M within the next 5 years

PROJECTION: Main Fund Assets in a 4% return environment

Note: Does not include contributions made based on back pay; Contribution rate estimates produced have undergone peer review by actuaries; dollar estimates have not been reviewed

Source: Buck Consultants; MBTA analysis

DRAFT FOR DISCUSSION

Key Assumptions

• Contribution rate as a percentage of payroll recalculated each year to reflect a 4% annual investment return from FY16-FY21

• Payroll grown at 2.7%, the ten year historic avg.

Fiscal and Management Control Board

20

Draft for Discussion & Policy Purposes Only

• Eligibility, benefits, contribution rates (for MBTA and employees) and board governance rules for the MBTA Pension are set forth in a Pension Agreement negotiated between the MBTA and the L589 Boston Carmen’s Union› Current Pension Agreement was signed on July 1, 2014 and is in effect

for 4 years› All existing contractual terms of current Pension Agreement expire on

June 30, 2018 and are open to negotiation in the next contract cycle (or sooner – if the parties so choose)

› The Pension Agreement is posted online at www.mbtarf.com

• In addition to the benefits negotiated under the Pension Agreement, MBTA and its employees pay into, and receive Social Security Benefits. MA does not pay Social Security and MA state workers do not receive Social Security Benefits

The Pension Agreement is a contract between the MBTA and the Boston Carmens Union (L589)

MBTA Pension Future Outlook

Fiscal and Management Control Board

21

Draft for Discussion & Policy Purposes Only

• Age required for retirement• Annual multiplier applied per year of service• Value of sick days in relation to pensionable years of service• Terms on which pensions can be passed onto beneficiaries (other

than spouses) and on which pensions are paid for retirees who pass early

• Overall pension operating expenses (investment and administrative expenses)

• Approach to investment strategy and asset allocation decisions• Level of access to top managers (particularly for private equity) and

ability, given scale, to negotiate best rates for investment mgmt• Contribution split between MBTA and employees• Breadth of eligibility and availability of the current 401K plan, which

is offered to management union and EXE employees

Key terms that impact long term sustainability of the pension, future required MBTA contributions and total pension returns

MBTA Pension Future Outlook

Fiscal and Management Control Board

22

Draft for Discussion & Policy Purposes Only

MBTRF Governance: Retirement Board Structure

MBTA Pension Future Outlook

Retirement Board MembershipA. 3 people appointed by AuthorityB. 1 Member of the Fund elected by vote by Members of the Fund who are not members of the

Carmen’s Union L589C. 2 Members of the Fund to be designated by the Carmen’s Union L589D. 1 honorary member selected by the board, who does not have regular voting powers

Voting on decisions by the Retirement Board• At least 4 votes from elected members are required to make a decision including:

− At least two out of three members from (A)− AND at least two out of three members from (B) and (C)

• If no decision can be made, the rules are as follows:− Vote of the honorary member− AND at least two out of three members from (A)− OR at least two out of three members from (B) and (C)

Key Responsibilities of the Retirement Board• Investing the Fund’s money• Setting the annual contribution rate, with the aid of Actuaries• Annual report on operations, assets, and liabilities of the Fund, available to all members of

the Fund• Decisions on retirement of active members and distribution of benefits• Providing public information on MBTA pension benefits paid to retired members• Choosing the Executive Director of the MBTA Retirement Fund

Fiscal and Management Control Board

23

Draft for Discussion & Policy Purposes Only

Where do we go from here?

1. Pensions are the fastest growing operating expense• MBTA pension expense fastest growing portion of operating budget at ~17% in

FY17

2. Sustainability of the pension fund is dependent on overall market performance and investment returns• If the MBTARF does not produce returns close to target rate of 7.75%, the fund

will face significant shortfalls • Filling the gap will place significant pressure on MBTA operating budget

3. This is the time to pursue reform that addresses the sustainability of the pension and protects all stakeholders: employees, retirees and taxpayers

Fiscal and Management Control Board

24

Draft for Discussion & Policy Purposes Only

Backup

Fiscal and Management Control Board

25

Draft for Discussion & Policy Purposes Only

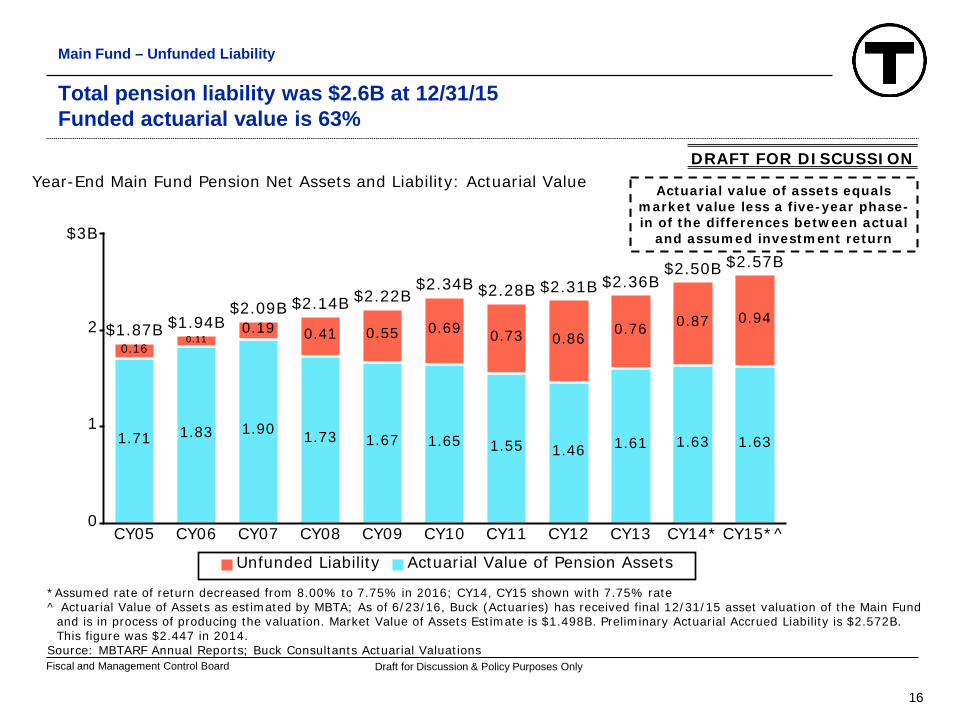

Over ten years, Mass PRIM fund assets have increased by 48%

Main Fund – Asset Trend

0

20

40

60

$80B

Year-End Main Fund Pension Net Assets: Market Value

(not including unfunded liability)

CY05

40.2

CY06

46.7

CY07

53.7

CY08

37.8

CY09

42.6

CY10

48.3

CY11

47.1

CY12

52.0

CY13

57.9

CY14

60.7

CY15

59.6

+48%+48%

Source: Massachusetts PRIM CAFRs, 2005-2015

Note: PRIM serves as an investment manager for multiple retirement systems in Massachusetts

• Since 2005, the number of systems with assets managed by PRIM has risen from 54 to 95

• Growth in PRIM assets under management a result of both investment returns and increased allocation of assets by those systems into PRIM

• For systems other than State Employees (MSERS) and MA Teachers (MTRS), contributions to PRIM have exceeded redemptions paid from PRIM by $6.2B since 2005 due to shift of assets into the system

Fiscal and Management Control Board

26

Draft for Discussion & Policy Purposes Only

MBTA Pension Main Fund benefits paid + admin expenses exceed total investment returns + active member contributions over past 10 years

Main Fund – Net Outflows

0

1,000

2,000

3,000

$4,000M

Total Additions and Deductions from the Main

Fund, 2004-2014

2004 Assets

(End of Year)

$1,670M

Investment

Return and

Income

$918M

Contributions

$626M

Benefits Paid

-$1,575M

Admin.

Expenses

-$51M

2014 Assets

(End of Year)

$1,588M

Note: Administrative Expenses includes RefundsSource: MBTARF Annual Reports

Net Outflow: $949MA

Fiscal and Management Control Board

27

Draft for Discussion & Policy Purposes Only

Asset smoothing defers recognition of fund underperformance: actuarial value of assets was $44M higher at end-of-year 2014

Main Fund – Unfunded Liability

0

500

1,000

1,500

$2,000M

Market-to-Actuarial Asset Value, 2014

2013 Market

Value of Assets

$1,607M

Net Outflow

-$92M

Net Market

Return*

$74M

2014 Market

Value of Assets

$1,588M

Actuarial

Deferred

Losses (2014)

$44M

2014 Actuarial

Value of Assets

$1,632M

*Net Market Return includes investment expenses, fund administrative expenses and refundsNote: Asset smoothing is a common practice used by pension funds to reduce volatility in contribution levels. MBTARF, State-

Boston Retirement System, Mass Teachers’ Retirement System and Mass State Employees’ Systems all use the same method to defer realization of gains/losses (although use different values for maximum deviation from market value)

Source: Buck Consultants Actuarial Valuations

80% Deferred

In 2013, actuarial value of assets was reset to equal market value of assets

Fiscal and Management Control Board

28

Draft for Discussion & Policy Purposes Only

0

500

1,000

1,500

2,000

Market-to-Actuarial Asset Value, 2015

2014 Market

Value of

Assets

$1,588M

2015 Net

Outflow

-$89M

2015 Net

Market

Return**

-$1M

2015 Market

Value of

Assets

$1,498M

Actuarial

Deferred

Losses (2014

vintage)

$33M

Actuarial

Deferred

Losses

(2015)*

$97M

2015

Actuarial

Value of

Assets*

$1,628M

Asset smoothing defers recognition of fund underperformance: actuarial value of assets estimated to be ~$130M higher than market value in 2015

Main Fund – Unfunded Liability

*Actuarial Value of Assets as estimated by MBTA**Net Market Return includes investment expenses, fund administrative expenses and refundsNote: As of 6/14/16, Buck (Actuaries) had not received final 12/31/15 asset valuation of the Main Fund. Estimate is $1.498BSource: MBTA Analysis; Buck Consultants Actuarial Valuations

80% Deferred60% Deferred

DRAFT FOR DISCUSSION

Fiscal and Management Control Board

29

Draft for Discussion & Policy Purposes Only

Actuarial smoothing defers recognition of losses; currently, actuarial funding ratio 5% higher than market value of assets

Main Fund – Unfunded Liability

0

20

40

60

80

100%

Ratio of Assets to Pension Liability, 2005-2014

CY05 CY06 CY07 CY08 CY09 CY10 CY11 CY12 CY13 CY14 CY15*

68% 63% 58%92% 96% 92% 61% 64% 64% 61% 64%Market Value

Funded Ratio

68% 65% 63%91% 94% 91% 81% 75% 70% 68% 63%Actuarial

Funded Ratio

Market Value

Funded RatioActuarial

Funded Ratio

Actuarial value of assets set equal to

market value of assets in 2013

*Actuarial Value of Assets as estimated by MBTA; As of 6/14/16, Buck (Actuaries) had not received final 12/31/15 asset valuationof the Main Fund. Market Value of Assets Estimate is $1.498B. Preliminary Actuarial Accrued Liability is $2.572B.

Source: MBTA Analysis; Buck Consultants Actuarial Valuations

DRAFT FOR DISCUSSION

Fiscal and Management Control Board

30

Draft for Discussion & Policy Purposes Only

Where do we go from here?Annual required contribution rate (% of payroll) has doubled over past 10 years

MBTA Pension Future Outlook

0

10

20

30%

Contribution rates to the MBTA Retirement Fund

(Percentage of eligible wages)

FY07

4.0%

9.5%

13.5%

FY17 Preliminary*

6.5%

18.1%

24.6%

Employee Contribution Rate MBTA Contribution Rate

MBTA contribution to pension fund

Employee contribution to pension fund

Total contribution

rate

*FY17 contribution rate subject to revision pending final FY17 Buck Consulting actuarial valuation; Original estimate was 24.0%,updated to 24.6% as of 6/24/2016

Source: MBTA Historical Contribution Rates

Fiscal and Management Control Board

31

Draft for Discussion & Policy Purposes Only

0

200

400

600

800

$1,000M

Cumulative MBTA contributions to the Main Fund

(Calendar Year)

Ten Years: CY2006-2015

$495M

Ten Years: CY2016-2025E

$877M

1.8X1.8X

Where do we go from here?At current cont. %, MBTA contribution will nearly double over next 10 years

MBTA Pension Future Outlook

Source: MBTA Main Fund Asset and Contribution Projection Model

DRAFT FOR DISCUSSION

Fiscal and Management Control Board

32

Draft for Discussion & Policy Purposes Only

$1.76B in benefits paid by MBTARF 2005-2015

Main Fund Benefits and Contributions

0

50

100

150

$200M

CY05

126

CY06

132

CY07

142

CY08

149

CY09

157

CY10

165

CY11

170

CY12

175

CY13

177

CY14

182

CY15

187

4%

'05-'15CAGR

Benefits

![MBTA Commuter Rail System - cdn.mbtace.com€¦ · South Acton W t o r d ^ ] o À , ] o o ... run express to/from Boston weekdays Grove Hall Union Square Powder House Square Hotel](https://static.fdocuments.net/doc/165x107/5aedf5117f8b9ac62b8b5706/mbta-commuter-rail-system-cdn-south-acton-w-t-o-r-d-o-o-o-run-express.jpg)