Marcon International, Inc. Coupeville, WA 98239 U.S.A. · Marcon International, Inc. Vessels and...

77

Marcon International, Inc. Vessels and Barges for Sale or Charter Worldwide www.marcon.com Details believed correct, not guaranteed. Offered subject to availability. P.O. Box 1170, 9 NW Front Street, Suite 201 Coupeville, WA 98239 U.S.A. Telephone (360) 678 8880 Fax (360) 678-8890 E Mail: [email protected] http://www.marcon.com August 2016 Tug Market Report Following is a breakdown of available anchor handling coastal, ocean and harbor tugs. Separate reports available on inland river pushboats and anchor handling tug supply vessels. Horsepower Under 1,000 1,000 – 2,000 2,000 – 3,000 3,000 – 4,000 4,000 – 5,000 5,000 – 6,000 6,000 - 7,000 7,000 – 8,000 8,000 – 9,000 9,000 Plus Total Jan 2000 161 145 72 62 27 15 3 4 7 2 498 Jan 2001 138 133 81 72 34 20 5 7 8 2 500 Jan 2002 117 134 85 67 38 22 2 5 6 4 480 Jan 2003 152 176 96 71 40 21 2 4 6 5 573 Jan 2004 117 140 77 67 29 21 1 5 12 3 472 Jan 2005 117 141 71 69 28 21 1 11 9 2 470 Jan 2006 97 125 90 66 21 16 5 6 8 1 435 Jan 2007 77 114 97 68 25 10 5 4 7 0 407 Jan 2008 73 118 105 58 19 13 2 7 1 1 397 Jan 2009 73 94 95 76 29 19 6 5 2 3 402 Feb 2010 74 136 121 125 47 36 9 7 3 4 562 Feb 2011 66 111 137 142 80 47 10 15 8 5 621 Feb 2012 75 133 132 153 81 45 14 17 7 1 658 Feb 2013 92 166 167 153 73 34 17 15 8 2 727 Feb 2014 86 151 184 136 63 38 13 9 5 2 687 Aug 2014 78 117 170 131 69 34 11 6 6 1 623 Nov 2014 74 120 168 135 67 35 10 9 8 1 627 Feb 2015 74 117 163 134 66 38 15 8 7 0 622 May 2015 66 121 150 147 70 44 16 9 6 3 632 Aug 2015 65 123 168 133 64 46 17 8 6 5 635 Nov 2015 71 123 179 124 64 42 17 8 7 5 640 Feb 2016 66 114 164 127 69 41 17 6 4 6 614 May 2016 65 113 168 133 71 42 17 7 2 5 623 Aug 2016 55 108 161 153 79 43 19 10 4 5 637 Aug 2016 - U.S. 18 21 26 26 9 6 5 5 1 0 117 Aug 2016 - Foreign 37 87 135 127 70 37 14 5 3 5 520 Avg. Age - Worldwide 1980 1988 1989 1995 1999 2001 2002 1978 1999 1993 Avg. Age - U.S. 1959 1967 1967 1973 1981 1976 2006 1970 1991 0 Avg. Age - Foreign 1992 1993 1993 1999 2001 2006 2000 1985 2002 1993 Charter - Worldwide 19 47 56 63 38 21 9 6 9 17 285 Charter - U.S. 2 8 11 15 6 2 1 1 1 0 47 Charter - Foreign 17 39 45 48 32 19 8 5 8 17 238 Up Since Last Report Down Since Last Report Market Overview Of the 13,121 vessels and 3,816 barges that Marcon currently tracks, 4,945 are tugs with 637 currently officially on the market for sale worldwide, up 2.25% since May and 0.32% from August 2015. Of the tugs for sale, 55.19% of foreign and 96.58% of U.S. tugboats are direct from Owners. 217 or 34.07% of the tugs worldwide, primarily foreign flagged, were built within the last 10 years, are newbuilding re-sales or currently under construction – compared to 35.75% one year ago. 64 (10.05%) are over 50 years of age. Thirteen have no age listed. The oldest tug Marcon currently has listed was built in 1912 and is very last of over 1,000 first generation steam trawlers and halibut fishers. This “old lady” is balanced by 25 newbuildings up to 8,076HP scheduled for delivery in 2016.

Transcript of Marcon International, Inc. Coupeville, WA 98239 U.S.A. · Marcon International, Inc. Vessels and...

Marcon International, Inc. Vessels and Barges for Sale or Charter Worldwide

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

P.O. Box 1170, 9 NW Front Street, Suite 201

Coupeville, WA 98239 U.S.A.

Telephone (360) 678 8880

Fax (360) 678-8890

E Mail: [email protected]

http://www.marcon.com

August 2016

Tug Market Report Following is a breakdown of available anchor handling coastal, ocean and harbor tugs. Separate reports available on inland river pushboats and anchor handling tug supply vessels.

Horsepower Under

1,000

1,000 –

2,000

2,000 –

3,000

3,000 –

4,000

4,000 –

5,000

5,000 –

6,000

6,000 -

7,000

7,000 –

8,000

8,000 –

9,000

9,000

Plus Total

Jan 2000 161 145 72 62 27 15 3 4 7 2 498

Jan 2001 138 133 81 72 34 20 5 7 8 2 500

Jan 2002 117 134 85 67 38 22 2 5 6 4 480

Jan 2003 152 176 96 71 40 21 2 4 6 5 573

Jan 2004 117 140 77 67 29 21 1 5 12 3 472

Jan 2005 117 141 71 69 28 21 1 11 9 2 470

Jan 2006 97 125 90 66 21 16 5 6 8 1 435

Jan 2007 77 114 97 68 25 10 5 4 7 0 407

Jan 2008 73 118 105 58 19 13 2 7 1 1 397

Jan 2009 73 94 95 76 29 19 6 5 2 3 402

Feb 2010 74 136 121 125 47 36 9 7 3 4 562

Feb 2011 66 111 137 142 80 47 10 15 8 5 621

Feb 2012 75 133 132 153 81 45 14 17 7 1 658

Feb 2013 92 166 167 153 73 34 17 15 8 2 727

Feb 2014 86 151 184 136 63 38 13 9 5 2 687

Aug 2014 78 117 170 131 69 34 11 6 6 1 623

Nov 2014 74 120 168 135 67 35 10 9 8 1 627

Feb 2015 74 117 163 134 66 38 15 8 7 0 622

May 2015 66 121 150 147 70 44 16 9 6 3 632

Aug 2015 65 123 168 133 64 46 17 8 6 5 635

Nov 2015 71 123 179 124 64 42 17 8 7 5 640

Feb 2016 66 114 164 127 69 41 17 6 4 6 614

May 2016 65 113 168 133 71 42 17 7 2 5 623

Aug 2016 55 108 161 153 79 43 19 10 4 5 637

Aug 2016 - U.S. 18 21 26 26 9 6 5 5 1 0 117

Aug 2016 - Foreign 37 87 135 127 70 37 14 5 3 5 520

Avg. Age - Worldwide 1980 1988 1989 1995 1999 2001 2002 1978 1999 1993

Avg. Age - U.S. 1959 1967 1967 1973 1981 1976 2006 1970 1991 0

Avg. Age - Foreign 1992 1993 1993 1999 2001 2006 2000 1985 2002 1993

Charter - Worldwide 19 47 56 63 38 21 9 6 9 17 285

Charter - U.S. 2 8 11 15 6 2 1 1 1 0 47

Charter - Foreign 17 39 45 48 32 19 8 5 8 17 238

Up Since Last Report Down Since Last Report

Market Overview Of the 13,121 vessels and 3,816 barges that Marcon currently tracks, 4,945 are tugs with 637 currently officially on the market for sale worldwide, up 2.25% since May and 0.32% from August 2015. Of the tugs for sale, 55.19% of foreign and 96.58% of U.S. tugboats are direct from Owners. 217 or 34.07% of the tugs worldwide, primarily foreign flagged, were built within the last 10 years, are newbuilding re-sales or currently under construction – compared to 35.75% one year ago. 64 (10.05%) are over 50 years of age. Thirteen have no age listed. The oldest tug Marcon currently has listed was built in 1912 and is very last of over 1,000 first generation steam trawlers and halibut fishers. This “old lady” is balanced by 25 newbuildings up to 8,076HP scheduled for delivery in 2016.

Marcon International, Inc. Tug Boat Market Report – August 2016

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

2

The majority of tugs Marcon tracks for sale as of the time this report is being written are in Southeast Asia with 134 tugs officially on the market (131 last report), followed by 116 in the U.S. (123), 78 in the Mid-East (69), Europe with 71 (65), 69 in the Far East (66), 55 in the Mediterranean (55), 25 in the South Pacific (27), 23 in Latin America (21), 19 in the Caribbean (18), 15 in Africa (20), 15 in Canada (14), 9 where location unstated (6) and 8 in Southwest Asia (8). CAT diesels still power most tugs for sale with machinery in 150 or 23% of the tugs Marcon lists. This is followed by 90 Cummins, 63 EMD, 55 each Niigata and Yanmar, 24 each Deutz-MWM and Mitsubishi, 23 GM/DD and 19 Wartsila powered tugs. 134 tugs are powered by machinery from other manufacturers from ABC to Zibo with, as always seems, five Fairbanks Morse boats still on the market. In tugs listed for sale since August 2011, CAT and Yanmar powered vessels are up 5 percentage points each, Niigata is up 3 points, Mitsubishi and Wartsila are up 2 points each and EMD is down 3 points.

There has been a definite shift in the second-hand tug market over the last few years with newer boats, many of which are ASDs out of Southeast Asia and the Far East, being offered for sale. Five years ago, only 31.45% of the tugs worldwide, primarily foreign flag, were built within the previous ten years compared to 34.07% today. The United States also then had the largest selection of tugs listed for sale with 145 available (24.1%) tracked by Marcon (plus nine additional U.S. flag tugs overseas). 102 tugs were located in Southeast Asia (17.0%), 93 tugs in Europe (15.5%), Far East 87 (14.5%), Mediterranean 65 (10.8%), Mid-East 35 (5.8%) and Caribbean 24 (4.0%). Looking at types of tugs available for sale worldwide, conventional twin screw tugs still prevail today with 382 (60.0%). These are followed by 148 azimuthing tugs (23.2%) on the market, 92 single-screw tugs (14.4%), 12 Voith Schneider tractor tugs (1.9%) and three triple screw (0.5%). As a comparison and demonstrating the trend in propulsion, five years ago 20.0% of the 601 tugs for sale were single screw, 60.1% twin screw, 16.1% azimuthing and 3.3% were Voith Schneider. More ASD tugs are being listed for sale worldwide than single screw tugs. The scrapping of older single screw tugs continues as they are seldom able to be sold for further commercial trade. The greatest global changes in horsepower for sale in the last five years have been in the 2,000 – 2,999HP range with 40 tugs more available today with an average age of 27 years compared to August 2011 when the average age of the 121 vessels listed was 28 years. Tugs in the 3,000-3,999HP range increased by 21 from five years ago. Average age stayed at 21 years, with average build date now of 1995. There are also thirteen more 4,000 – 4,999HP tugs today (17 years vs. 19 years). There are 25 fewer under 1,999BHP and 13 fewer 7,000-7,999BHP tugs on the market today.

Actual sale prices of all vessels and barges sold by Marcon to-date has averaged 95.49% of asking prices. In 2015 actual sales prices averaged 84.95% of asking prices, compared to 2014’s 85.65%, 2013’s 87.07% and 2012’s average 81.79%. Five tugs were sold so far in 2016 with an average price per BHP of $291.94 and average age of 36 years. Five tugs were sold in 2015 with an average price of $243.20 and average age of 34 years. Seven tugs were sold in 2014 with an average price per BHP of $282.55 and average age of 41 years. These are lower than 2013’s average price per BHP for a “generic” 33 year old twin screw tug of US$ 324.78. 2014 sales included both foreign and domestic tugs and actual

ages covered a relatively narrow range from 32 to 47 years of age, whereas 2015’s sales included one foreign and four U.S. sales with ages ranging from 8 to 50 years and 2016’s to date include one foreign and four U.S. sales with ages ranging from 19 to 50 years. We continue to see updates about vessels scrapped or repossessed and we believe that 2016’s uptick in $/BHP is temporary due to the specific vessels and that prices, especially for older vessels, will continue to decline for the next few years.

Marcon International, Inc. Tug Boat Market Report – August 2016

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

3

Recent Marcon Tug Sales & Charters Out of thirteen sales so far this year, Marcon has sold five tugs totaling 7,690HP and one 1,360HP inland river pushboat. Two additional tugs are under offer and expected to close within the next 45 days. Three 5,000+ HP twin screw and ASD tugs continue to be fixed on previously arranged long-term charters in the U.S. and Latin America. Since 1981, Marcon has sold or chartered 318 tugs totaling 986,875BHP and hoping to break the 1,000,000BHP mark by the end of this year.

Olympic Tug & Barge of Seattle, Washington has sold their U.S. flag, harbor tug “Catherine Quigg” (ex-Swanee) to U.S. East Coast buyers to support marine construction and dredging operations in that region. The 65.0’ x 23.0’ x 11.0’ depth, twin screw tug was built by Jones Tug & Barge of Long Beach, California in 1977 for local service and originally powered by a pair of 455HP GM16V71s. Hull is welded steel with an aluminum two-level deck house fitted with an upper pilot station. The tug was later acquired by Olympic Tug & Barge who upgraded and repowered her with the current GM12V149s developing a total of 1,350BHP at 1,650RPM, Twin Disc MG520 5.04:1 gears and 59” x 59” 4-blade Kaplan fixed pitch props in stainless steel lined

kort nozzles. ABS certified bollard pull is 18.85 short tons ahead, free running speed 10.5kn and range abt. 4,000nm. Towing gear consists of a Tulsa hydraulic double drum side-by-side tow winch with a capacity of 2,000’ of ½” tow wire plus a soft-line on the second drum, an “H” bitt and three manual tow pins. “Catherine Quigg” worked mostly as a day boat, packing just under 20,000g of fuel. She has a small crew cabin, galley and mess area. Electrical power is provided by a pair of 30kW / GM4-71 generators. Tug is fully fendered. This is the fifth tug Marcon has sold this year, totaling 7,690HP and 318

th tug sold or chartered, totaling 986,857HP, over the last 35 years. Marcon

acted as sole broker in the sale.

Marcon International, Inc. is pleased to announce the sale of a U.S. flag 52,000 barrel capacity, ocean single hull tank barge on private & confidential terms. The ABS +A1 Oil Tank Barge classed barge, measuring 300' loa x 64.1' beam x 21.8' depth, was built in 1970 at Bollinger Gretna, LLC. The barge will be converted to deck service by the buyers. This is the third ocean tank barge Marcon has sold this year, totaling 110,000bbl capacity and the 90

th ocean tank barge, totaling

6,836,987bbl, over the last 35 years. Marcon acted as sole broker. The U.S. flag, ABS coastal loadline, deck barge “Islander” was sold between U.S. West Coast interests. The 128‘ x 38‘ x 7’8” barge was built in 1964 at Southern Oregon Marine, carries around 532 tonnes of cargo and is fitted with a 26’ long x 12.5’ – 18’ wide aft ramp. Until recent times, “Islander” served as a freight barge to Santa Catalina Island off the southern Californian coast, but was deemed excess to requirements after the contract changed hands. New owner intends to convert the barge to trade outside of deck freight service. Marcon was sole broker in the transaction and has handled a number of previous purchases and sales over the years for the buyer. Marcon has sold 244 deck barges, totaling over one million deadweight tons capacity, over the last thirty-five years.

The U.S. flag, inland deck barge “Lockwood 2001” was sold to U.S. Mid-West interests. Built in 1991 by Conrad Industries, Inc. of Morgan City, Louisiana, the single raked barge measures 200’ x 48’ x 12’ depth and has a cargo capacity of 2,350 short tons on a draft of abt. 10.5’ and a deck strength of abt. 1,800PSF. A 44’ long x 24’ wide sloped ramp is set into the stern. Marcon acted as seller’s broker in this transaction, for whom we have sold numerous barges in the past.

Marcon International, Inc. Tug Boat Market Report – August 2016

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

4

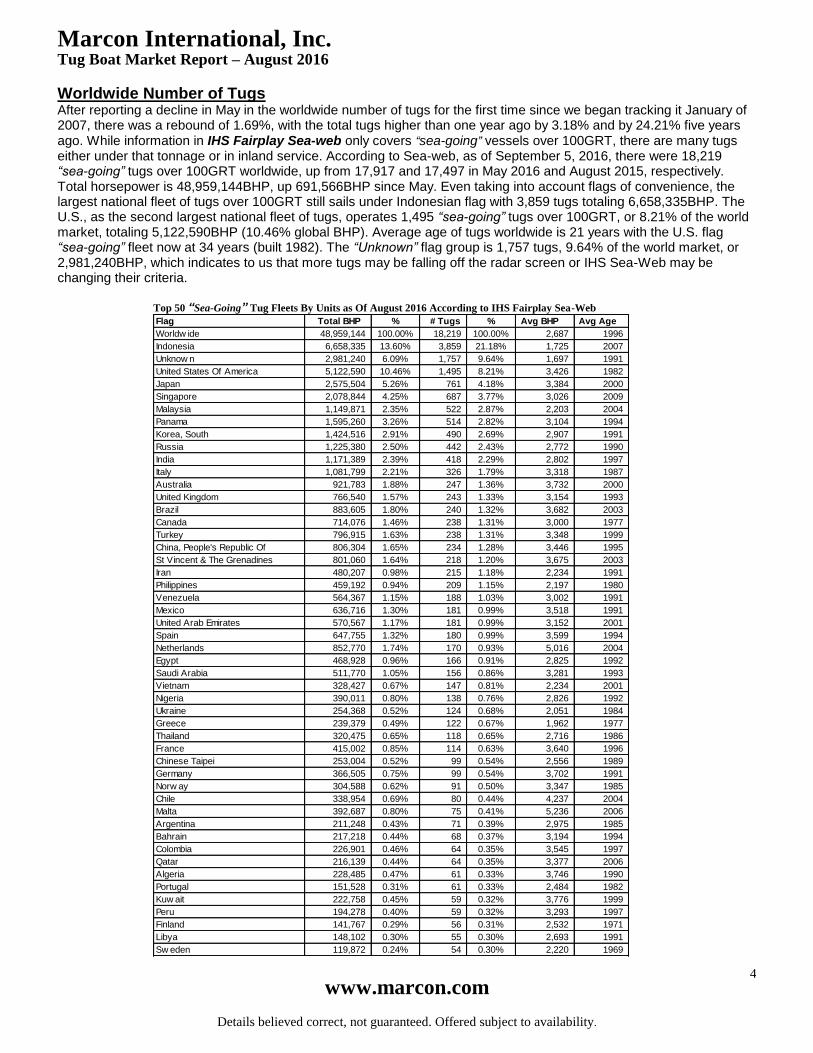

Worldwide Number of Tugs After reporting a decline in May in the worldwide number of tugs for the first time since we began tracking it January of 2007, there was a rebound of 1.69%, with the total tugs higher than one year ago by 3.18% and by 24.21% five years ago. While information in IHS Fairplay Sea-web only covers “sea-going” vessels over 100GRT, there are many tugs either under that tonnage or in inland service. According to Sea-web, as of September 5, 2016, there were 18,219 “sea-going” tugs over 100GRT worldwide, up from 17,917 and 17,497 in May 2016 and August 2015, respectively. Total horsepower is 48,959,144BHP, up 691,566BHP since May. Even taking into account flags of convenience, the largest national fleet of tugs over 100GRT still sails under Indonesian flag with 3,859 tugs totaling 6,658,335BHP. The U.S., as the second largest national fleet of tugs, operates 1,495 “sea-going” tugs over 100GRT, or 8.21% of the world market, totaling 5,122,590BHP (10.46% global BHP). Average age of tugs worldwide is 21 years with the U.S. flag “sea-going” fleet now at 34 years (built 1982). The “Unknown” flag group is 1,757 tugs, 9.64% of the world market, or 2,981,240BHP, which indicates to us that more tugs may be falling off the radar screen or IHS Sea-Web may be changing their criteria.

Top 50 “Sea-Going” Tug Fleets By Units as Of August 2016 According to IHS Fairplay Sea-Web

Flag Total BHP % # Tugs % Avg BHP Avg Age

Worldw ide 48,959,144 100.00% 18,219 100.00% 2,687 1996

Indonesia 6,658,335 13.60% 3,859 21.18% 1,725 2007

Unknow n 2,981,240 6.09% 1,757 9.64% 1,697 1991

United States Of America 5,122,590 10.46% 1,495 8.21% 3,426 1982

Japan 2,575,504 5.26% 761 4.18% 3,384 2000

Singapore 2,078,844 4.25% 687 3.77% 3,026 2009

Malaysia 1,149,871 2.35% 522 2.87% 2,203 2004

Panama 1,595,260 3.26% 514 2.82% 3,104 1994

Korea, South 1,424,516 2.91% 490 2.69% 2,907 1991

Russia 1,225,380 2.50% 442 2.43% 2,772 1990

India 1,171,389 2.39% 418 2.29% 2,802 1997

Italy 1,081,799 2.21% 326 1.79% 3,318 1987

Australia 921,783 1.88% 247 1.36% 3,732 2000

United Kingdom 766,540 1.57% 243 1.33% 3,154 1993

Brazil 883,605 1.80% 240 1.32% 3,682 2003

Canada 714,076 1.46% 238 1.31% 3,000 1977

Turkey 796,915 1.63% 238 1.31% 3,348 1999

China, People's Republic Of 806,304 1.65% 234 1.28% 3,446 1995

St Vincent & The Grenadines 801,060 1.64% 218 1.20% 3,675 2003

Iran 480,207 0.98% 215 1.18% 2,234 1991

Philippines 459,192 0.94% 209 1.15% 2,197 1980

Venezuela 564,367 1.15% 188 1.03% 3,002 1991

Mexico 636,716 1.30% 181 0.99% 3,518 1991

United Arab Emirates 570,567 1.17% 181 0.99% 3,152 2001

Spain 647,755 1.32% 180 0.99% 3,599 1994

Netherlands 852,770 1.74% 170 0.93% 5,016 2004

Egypt 468,928 0.96% 166 0.91% 2,825 1992

Saudi Arabia 511,770 1.05% 156 0.86% 3,281 1993

Vietnam 328,427 0.67% 147 0.81% 2,234 2001

Nigeria 390,011 0.80% 138 0.76% 2,826 1992

Ukraine 254,368 0.52% 124 0.68% 2,051 1984

Greece 239,379 0.49% 122 0.67% 1,962 1977

Thailand 320,475 0.65% 118 0.65% 2,716 1986

France 415,002 0.85% 114 0.63% 3,640 1996

Chinese Taipei 253,004 0.52% 99 0.54% 2,556 1989

Germany 366,505 0.75% 99 0.54% 3,702 1991

Norw ay 304,588 0.62% 91 0.50% 3,347 1985

Chile 338,954 0.69% 80 0.44% 4,237 2004

Malta 392,687 0.80% 75 0.41% 5,236 2006

Argentina 211,248 0.43% 71 0.39% 2,975 1985

Bahrain 217,218 0.44% 68 0.37% 3,194 1994

Colombia 226,901 0.46% 64 0.35% 3,545 1997

Qatar 216,139 0.44% 64 0.35% 3,377 2006

Algeria 228,485 0.47% 61 0.33% 3,746 1990

Portugal 151,528 0.31% 61 0.33% 2,484 1982

Kuw ait 222,758 0.45% 59 0.32% 3,776 1999

Peru 194,278 0.40% 59 0.32% 3,293 1997

Finland 141,767 0.29% 56 0.31% 2,532 1971

Libya 148,102 0.30% 55 0.30% 2,693 1991

Sw eden 119,872 0.24% 54 0.30% 2,220 1969

Marcon International, Inc. Tug Boat Market Report – August 2016

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

5

At the time of our August 2015 tug market report, the average horsepower for the world’s 17,658 “sea-going” tugs was 2,662BHP with an average year built of 1992. Today’s 18,219 tugs have an average horsepower of 2,687BHP, with an average year built of 1996 – a slight improvement in both HP and age. The U.S. fleet in August 2015 included 1,474 “sea-going” tugs with an average horsepower of 3,385BHP and an average year built of 1979. Today’s U.S. fleet has increased to 1,495 tugs with an average horsepower of 3,426BHP and a year built of 1982, i.e. an average age of 34 years, which also shows a very gradual replacement of the older, lower horsepower tugs - most notably with higher horsepower and more efficient twin screw AT/B tugs and azimuthing shipdocking and escort tugs.

Breakdown of U.S. “Sea-Going” Fleet Following is a breakdown of the U.S. sea-going tug fleet as of August

2016, according to IHS Fairplay Sea-web, compared with May 2016. As of August 2016, the U.S. domestic tug fleet consisted of 1,495 “sea-going” tugs totaling 5,122,590BHP. The U.S. flag fleet increased by six and total horsepower by 27,758BHP. High horsepower and large tugs are easy to track, but Sea-web has data on only 50 U.S. tugs under 999BHP. As most “under 1,000HP” U.S. tugs are below 100 GRT, they are not included in the Registry. Not counting pushboats, there are eight to nine hundred additional small tugs within U.S. coastal waters.

U.S. Sea-Going Tug Fleet Over 100GRT By BHP According to Lloyd’s Register as of August 2016

Unknown

BHP

Under

999

1000-

1999

2000-

2999

3000-

3999

4000-

4999

5000-

5999

6000-

6999

7000-

7999

8000-

8999

9000

Plus Total

Total # 119 50 262 209 281 255 128 85 49 10 47 1,495

Avg. BHP 782 1,504 2,365 3,410 4,353 5,431 6,368 7,171 8,066 11,270

Avg. LOA 88 81 87 96 104 106 110 112 136 137 142

Avg. Beam 28 23 26 29 32 34 36 38 39 41 47

Avg. Depth 11 9 11 13 15 15 17 18 20 20 25

Avg. Year Built 1976 1951 1965 1976 1981 1993 1996 2002 1986 1996 2005

Previous U.S. Sea-Going Tug Fleet Over 100GRT By BHP According to Lloyd’s Register as of May 2016

Unknown

BHP

Under

999

1000-

1999

2000-

2999

3000-

3999

4000-

4999

5000-

5999

6000-

6999

7000-

7999

8000-

8999

9000

Plus Total

Total # 115 50 264 210 282 257 122 83 49 10 47 1,489

Avg. BHP 782 1,504 2,364 3,412 4,351 5,428 6,375 7,171 8,066 11,265

Avg. LOA 88 81 87 96 105 106 110 112 136 137 142

Avg. Beam 28 23 26 29 32 34 36 38 39 42 47

Avg. Depth 12 9 11 13 15 15 17 17 19 21 24

Avg. Year Built 1974 1951 1965 1975 1981 1993 1995 2002 1986 1996 2005

Of the 1,495 U.S. tugs in Sea-web’s, 188 have unknown engines. 499, or 38% where type is known, are powered by EMDs, 422 (32%) by CATs, 107 (8%) by General Motors / Detroit Diesels, Alco and Cummins have 4%, Fairbanks Morse and M.T.U. (Rolls Royce) are tied with 3% each and Wartsila has 2% of the market share. 370 (25%) and 800 (53%) are conventional single and twin screw, respectively. The remaining 22% are 264 azimuthing, 38 triple screw and 23 Voith tractor tugs. Five years ago, of 1,500 U.S. flag tugs, 498 or 40% were powered by EMDs, 369 (30%) by CATs and 112 (9%) by General Motors / DD. We can see that CATs and EMDs gained two percentage points each, while GM/DDs fell by one from five years ago. In regards to propeller types, today there are 81 fewer single screw, 15 more twin screw and 61 more azimuthing U.S. flag tugs today compared to the fleet statistics in May 2011.

Marcon International, Inc. Tug Boat Market Report – August 2016

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

6

New Construction, Shipyard and Conversion News According to “Fairplay Newbuildings”, as of 5

th September, there

were 6,017 ships over 299GRT on the World Orderbook, down 352 from May and down 574 from newbuildings one year ago. Of the total number on today’s orderbook, 556, or 9.24%, are tugs or “towing / pushing” vessels, down from 604 in May. This is, of course, down from a peak of 768 in October 2008. 602 of today’s total newbuildings, down 72 from May, are OSVs and 289 (no change) are “Offshore – Other”.

Of 556 tugs listed by Fairplay under construction, China PR leads the order book with 134 tugs being built, down 11 from May. They are followed by Malaysia at 69 (down 4) tugs, Vietnam 54, Turkey 38, Indonesia 36, 26 Egypt, 17 each Japan, Spain, the UAE and the USA, 14 Mexico, 13 each Poland and Romania, 11 Singapore, Brazil 9, South Africa 8, 7 each India and Russia, 6 each Qatar and South Korea, Canada, Cuba and Netherlands 5 each, 4 Italy, 3 each Argentina, Iran and Thailand, 2 each Germany and Philippines and 1 each Bangladesh, Chile, Serbia, Ukraine and Venezuela.

Of 604 reported tugs being built the end of April, abt. 84.0% were scheduled to be delivered in the remainder of 2016, 14.4% in 2017, 1.4% 2018 and 0.2% each during 2019 and 2021. It would not surprise me to see a few delivery dates slip, but nowhere near the percentage of delays and cancellations of jack-up rigs, OSVs, container and dry bulk vessels due to today’s market conditions, which are nowhere as rosy as when the vessels were initially ordered. Many Owners today find themselves postponing, or even cancelling, selected deliveries in order to mitigate their financial exposure while restructuring. According to BIMCO, across the board, 2016 looks like it will set the record for the lowest newbuilding contracts in more than 20 years.

CAT power once again leads in popularity for propulsion in newbuilding sea-going tugs with main engines in 198 tugs - as they have since July 2007 when Marcon first started tracking this data. This is followed by Niigata diesels in 67 boats, Yanmar in 38, Cummins in 35, 28 Mitsubishi, 22 MTU, 20 ABC, 14 MaK (i.e. CAT), 9 Chinese “Standard Type”, 8 each MAN/MAN-B&W and Wartsila, 4 EMD, 2 each Daewoo and GE Marine and 1 each with Daihatsu and Deutz. Engines were not listed for 99 tugs. Only 35 tugs below 1,000BHP are shown under construction. As discussed earlier, many lower horsepower tugs are under 299GRT. 26.8% of the tugs on order are in the 3,000-3,999HP range, followed by 17.6% in the 2,000-2,999HP range and 11.0% in the 1,000-1,999HP range.

Summary of Horsepower – Fairplay Worldwide Tug Orderbook Over 299GRT

Under 1,000 – 2,000- 3,000- 4,000- 5,000- 6,000- 7,000- 8,000- 9,000- Over Unk. Total

1,000HP 1,999HP 2,999HP 3,999HP 4,999HP 5,999HP 6,999HP 7,999HP 8,999HP 9,999HP 10,000HP

Tugs 35 61 98 149 55 29 2 1 0 2 5 119 556

As in August 2011, the greatest number of tugs worldwide under construction are in the 3,000 – 3,999HP range. The greatest shift in horsepower over the last five years is 56 fewer 1,000 – 1,999HP and 38 fewer under 1,000HP tugs on today’s orderbook.

Marcon International, Inc. Tug Boat Market Report – August 2016

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

7

As of the beginning of September, Fairplay reported 17 “sea-going” U.S. flag tugs

on the books in U.S. shipyards. Colton Co. reports on recent deliveries from U.S. shipyards. As of August 17, 2016, Colton Co. reported 17 tugs delivered year-to-date in 2016. This compares to 2015, which saw the delivery of 26 tugs over the year and to 2014, when Colton reported 13 tug deliveries.

2016 Deliveries of Tugs Sorted by Owner/Operator

O.N. Name Builder Owner/Operator Type of Vessel GT Date

1267830 Zyana K Eastern SB Bay Houston Towing 5,150-hp Escort Tug 199 28-Apr-16

1265978 H Douglas M Eastern SB Bay Houston Towing 5,150-hp Escort Tug 319 03-Feb-16

1265316 Frederick E. Bouchard VT Halter Marine Bouchard Transportation 6,000-hp ATB Tug 713 06-Jun-16

1265315 Morton S. Bouchard, Jr. VT Halter Marine Bouchard Transportation 6,000-hp ATB Tug 713 28-Jan-16

1257374 Donna J. Bouchard VT Halter Marine Bouchard Transportation 10,000-hp ATB Tug 1,457 13-Jan-16

1258773 Gulf Venture Conrad Shipyard C-Stone LLC Tug 420 11-Mar-16

1254223 Denise Foss Foss Shipyard Foss Maritime 7,268-hp Tug 714 02-Jun-16

1263069 Dale R. Lindsey Vigor Seattle Harley Marine 3,000-hp ATB Tug 454 07-Jul-16

839992 Ocean Catatug 2 C.N. Ocean Location TMO Ocean 50' Tug 40 09-Jun-16

1268013 Jack T. Moran Washburn & Doughty Moran Towing 6,000-hp Tug 351 21-Jun-16

1267675 Barbara Carol Ann Moran Bay Shipbuilding Moran Towing 5,100-hp ATB Tug 297 16-May-16

1266268 Jonathan C. Moran Washburn & Doughty Moran Towing 6,000-hp Tug 283 27-Apr-16

1268860 David B Eastern SB Suderman & Young 5,150-hp Escort Tug 319 15-Jun-16

1267257 Neptune Eastern SB Suderman & Young 5,150-hp Escort Tug 319 03-Mar-16

840066 Iron Guppy Hike Metal Prods. Toronto Port Authority 66' Tug 87 23-Mar-16

1258328 Fort McHenry Chesapeake SB Vane Bros. Towing 3,000-hp Escort Tug 271 28-Jun-16

1264941 Hudson St. Johns Shipbuilding Vane Brothers 4,200-hp Escort Tug 103 07-Apr-16

2015 Deliveries of Tugs Sorted by Owner/Operator

O.N. Name Builder Owner/Operator Type of Vessel GT Date

1257372 Kim Bouchard VT Halter Marine Bouchard Transportation 4,000-hp ATB Tug 299 10-Jul-15

1258129 Finli Ryanne Leevac Shipyards Devall Towing Tug 145 13-Oct-15

1261999 Edward Julian Leevac Shipyards ETC Marine Tug 112 14-Oct-15

1254222 Michele Foss Foss Shipyard Foss Maritime 7,268-hp Tug 295 16-Apr-15

839086 Inlet Crusader Sylte Shipyard Gowlland Towing 65' Tug 142 05-Jun-15

1255672 Barry Silverton Conrad Shipyard Harley Marine 4,070-hp Tug 261 15-Oct-15

1255668 Jake Shearer Conrad Shipyard Harley Marine 4,070-hp Tug 261 14-Jul-15

1258229 Lela Franco Diversified Marine Harley Marine 2,000-hp Tug 175 15-Jun-15

1256369 Nancy Peterkin Nichols Bros. Kirby Ocean Tptn. ATB Tug 266 30-Oct-15

839530 Ocean Catatug I CN Ocean Location TMO Ocean 50' Tug 40 15-Dec-15

838896 Jessica Coy CN Ocean Manitoba Hydro 45' Tug 98 30-Mar-15

1264623 JRT Moran Washburn & Doughty Moran Towing 6,000-hp Tug 351 29-Dec-15

1261986 Leigh Ann Moran Bay Shipbuilding Moran Towing 5,100-hp ATB Tug 297 20-Oct-15

1261647 James D. Moran Washburn & Doughty Moran Towing 6,000-hp Tug 283 26-Aug-15

1259958 Kirby Moran Washburn & Doughty Moran Towing 6,000-hp Tug 283 03-Aug-15

1257668 Mariya Moran Patti Marine Moran Towing 6,000-hp ATB Tug 297 09-Jun-15

1258193 Payton Grace Moran Washburn & Doughty Moran Towing 5,000-hp Tug 283 07-Apr-15

1258627 Dylan Cooper SENESCO Reinauer Transportation 4,720-hp ATB Tug 199 27-Jul-15

1264552 Triton Eastern Shipbuilding Suderman & Young 5,150-hp Escort Tug 319 30-Nov-15

1260103 James E. Brown Rodriguez SB Thomas J. Brown & Sons 1,000-hp Tug 98 23-Apr-15

839194 Tuugaalik CN Forillon Transport Umialaarik 32' Tug 11 21-Jul-15

839193 Tuulik CN Forillon Transport Umialaarik 32' Tug 11 21-Jul-15

1265305 Sarah Diversified Marine Unknown Tug 169 04-Nov-15

1257138 Fort Schuyler Chesapeake Shipbuilding Vane Bros. Towing 3,000-hp Tug 99 24-Sep-15

1253729 Kings Point Chesapeake Shipbuilding Vane Bros. Towing 3,000-hp Tug 99 02-Mar-15

1262419 Elizabeth Anne St. Johns Shipbuilding Vane Brothers 4,200-hp Escort Tug 332 04-Dec-15

According to an 8th August 2016 SteelBenchMaker report, standard steel

plate in the US, East of the Mississippi was $699/mt down 1% from the previous month, while standard plate in China was $330/mt, up 4%.

Marcon International, Inc. Tug Boat Market Report – August 2016

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

8

At the end of June, two Damen ASD Tugs 2810 set sail from Galati in Romania to Puerto General de San Martin (Argentina) for towing, mooring and firefighting operations in the Argentinian region around Rosario on the

Paraná river by Damen Galati Shipyards (Romania), the vessels will be

delivered on time, having met expectations of Cooperativa De Trabajos

Portuarios Limitada de San Martín. This was a first-time order for the Argentinian company who also purchased a Cutter Suction Dredger 500 from Damen Dredging, which is also on its way by means of a cargo vessel. Alex Westendarp Knol, Damen Area Manager South-America, explains: “Our short delivery time together with the cooperation of Argentinian authorities, allowed us to meet the requirements for arranging this departure at short notice. This has been a great way to start a long-lasting relationship with Cooperativa. We hope to be able to provide the client with more vessels in the future, either built locally or at our shipyards.” The company’s current large rescue center will be able to expand its Maritime Division with the tugboats “Estibador I” and “Estibador II”. The ASD 2810 tugboats can perform emergency and firefighting activities should fire break out at a terminal or on a vessel. The tugs will also be used for vessel maneuvering operations. The 28.67m ASD Tugs have a beam of 10.43m

and are equipped with state-of the-art Fire Fighting 1 capability. Fitted with Rolls Royce US 205 azimuth thrusters, these compact tugs have a maximum bollard pull of 60.2 tonnes and are easy to maneuver at speeds of 13 knots. The CSD 500 dredger, “La Portuaria”, will be used for dredging operations in the Argentinian terminal region. “La Portuaria” has a modular design which makes it easy to transport almost anywhere. Damen Services will continue to provide Cooperativa De Trabajos Portuarios with proper operation and maintenance of the vessels as well as crew familiarization and

training…… Fratelli Neri S.p.A., the family-owned, Livorno-based harbor towage company (highlighted on page 9 in our May 2016 Tug Market Report), has ordered three new Damen vessels; an ASD Tug 2913, a Stan Tug 1606 and a

Stan Launch 1305, the last for its subsidiary company Labromare, which is 50% owned by Tripmare S.p.A. All three vessels will operate in and around the port of Livorno, one of the busiest in the Mediterranean Sea. Delivery will take place in November this year. This order takes to six the number of Damen vessels ordered by Fratelli Neri in the past year. In January 2016 the company took delivery of an ASD Tug 3212, the first in the Mediterranean to be fitted with a render recovery winch. Several months earlier it also purchased two used Stan Tugs 2608 via Damen Trading. The three latest vessels are all being purchased from stock. As well as its positive experience with its existing Damen vessels, the ability to guarantee rapid delivery was a significant factor in Damen winning this latest order. The ASD 2913 is currently in build at Damen Shipyards Galati, Romania and will now undergo modifications to ensure full compliance with Italian flag requirements. This will include FiFi1, oil recovery capability and an aft bridge. Fratelli Neri selected the ASD 2913 based on its powerful yet compact design. 80 tonnes of bollard pull will give it all the power it will need for operations in the busy port of Livorno on Italy’s Tuscany coast and the excellent maneuverability will also be a valuable asset. The Stan Tug 1606 has been ordered for operations on coastal and inland waters around Livorno. This proven design is both robust and compact making it ideal for restricted waterways. Currently being held in stock at Damen Shipyards Gorinchem, the Netherlands, the vessel will be brought up to Italian flag standard with modifications including fire-fighting apparatus and an aft towing winch. The last vessel, a Stan Launch 1305 is also currently in stock at Gorinchem. This will be used by Labromare S.r.l. Livorno to deliver a range of environmental services in Italy and will be fitted with a bow thruster and an aft towing hook. Andrea Trevisan, Damen Sales Manager North, West and South Europe, commented: “We are honored to be serving Fratelli Neri again and so quickly. It is always a pleasure to work with another successful and prestigious Italian family business with values very similar to our own. Once again, Damen’s policy of building for stock has enabled a vessel operator to obtain customized, high quality vessels in substantially shorter time frames than is possible when building to order. These three vessels also represent a cross section of the various capabilities that that the group can provide its clients and we are confident that each will give many years of efficient service.” Piero Neri, owner of Fratelli Neri, stated: “We are delighted to have again chosen Damen for their ability and readiness to respond to our demand for tugs that can be deployed across a range of different operations. We have recently experienced excellent cooperation with Damen, from the earliest discussions right up to the delivery of the vessels, with the personnel on both sides working together as a team. This way of working is a reflection of our shared values and reliability that lead to technical solutions lasting long into the future.”

Marcon International, Inc. Tug Boat Market Report – August 2016

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

9

SAFEEN, the subsidiary of Abu Dhabi Ports formerly known as Abu Dhabi Marine

Services, took delivery in June of a Damen Shoalbuster 2609 named “Maqtaa” to join its existing fleet. Like all the vessels in Damen’s Shoalbuster range she is a multi-purpose, shallow draught workboat capable of undertaking a wide range of roles including towing, mooring, pushing, anchor handling, dredge support, supplying and other support activities. The 26.0m x 9.1m x 3.6m vessel is powered by a pair of CAT 3508TA/Cs with 1,800mm Promarin fixed pitch props in kort nozzles and develops a total of 2,200BHP at 1,600RPM, bollard pull of 28 tonnes ahead and speed of 11kn free running. “Maqtaa’s” maneuverability is assisted by a 200HP bow thruster. Towing

gear consists of a 90 tonne brake Ridderinkhof AHW-H-400 anchor handling / towing winch, triple hydraulic tow pins, a 5T capstan and 8T tugger. Tug is classed BV I +Hull, +Mach Tug Unrestricted Navigation, AUT-UMS…… Damen

congratulates Reylaver of Veracruz, Mexico on the safe arrival and naming ceremony of the new 5,632BHP ASD Tug 2411 “Jesus” (Hull 512283). In order to reach her owners, the 24.55m x 10.70m x 4.60m vessel undertook, on her own keel, a significant voyage covering 10.500 nautical miles. Reylaver ordered the new vessel from Damen Shipyards Group in April 2015. After a successful construction phase at Damen Shipyards Changde, she made a major journey starting in Shanghai, via Japan to Dutch Harbor in Alaska, through the Panama Canal, all under her own keel, finally arriving Veracruz, Mexico on 9

th June.

Following her arrival, the 70 tonne bollard pull vessel was named “Jesus” on 18

th July. The well organized and festive ceremony took place in the afternoon in the presence

of owners and personnel of Reylaver, the local authorities, guests, press and representatives of Damen. The vessel, a standard design from the Damen portfolio powered with 1,641bkW CAT 3516Bs, received a number of custom features in order to meet the needs of the client, including adaptations to her accommodation……. In an official handover

ceremony at the Den Helder Naval Base, the Royal Netherlands Navy took formal delivery of three Damen ASD 2810 Hybrid tugs. In addition to providing an increase in ship handling capacity, the new vessels are also installed with hybrid propulsion systems. This will contribute to Dutch Ministry of Defense ambitions regarding sustainable operations of the Navy. The acquisition of the three Damen tugs is part of the Royal Netherlands Navy’s ongoing fleet renewal program. The hybrid vessels, named “Noordzee”, “Waddenzee” and “Zuiderzee”, can sail under diesel-direct, diesel-electric or fully-electric power. This will result in a significant increase in fuel

efficiency and reduction of exhaust emissions. For example, when sailing in fully-electric mode – possible for up to one hour at a speed of 4 knots – the tugs will have zero emissions. This is highly relevant to the Ministry of Defense Operational Energy Strategy. Recently presented to the Dutch government, this concerns future emissions targets and dependence on diesel as a principle fuel. When sailing under diesel power, the Damen ASD 2810 Hybrid can store any electrical energy that is not immediately used in its battery pack. This can subsequently be used to sustain vessel operating systems or for use in electric sailing mode. In addition to hybrid capabilities, the new tugs are also more powerful than the vessels that they are replacing. The Damen ASD 2810 Hybrid packs a 60-tonne bollard pull: considerably more than the 22-tonne bollard pull of the ongoing Linge-class tug. This increase in bollard pull will support safe and efficient ship handling operations of the largest vessels of the Royal Netherlands Navy

fleet, such as HNLMS “Johan de Witt”, HNLMS “Rotterdam” and 204m

Joint Support Ship HNLMS “Karel Doorman” in all weather conditions.

Tugs are powered by two MTU 16V4000M63R main diesels developing a total of 4,935BHP and one MTU 12V2000M41B 800kVA 440vAC 60Hz propulsion generator providing power to two Rolls Royce US205 2,400mm props. Now that the tugs are in active service, Damen Shipyards Den Helder will perform an ongoing maintenance program for all three vessels, a task is normally undertaken by the Royal Netherlands Navy itself.

Marcon International, Inc. Tug Boat Market Report – August 2016

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

10

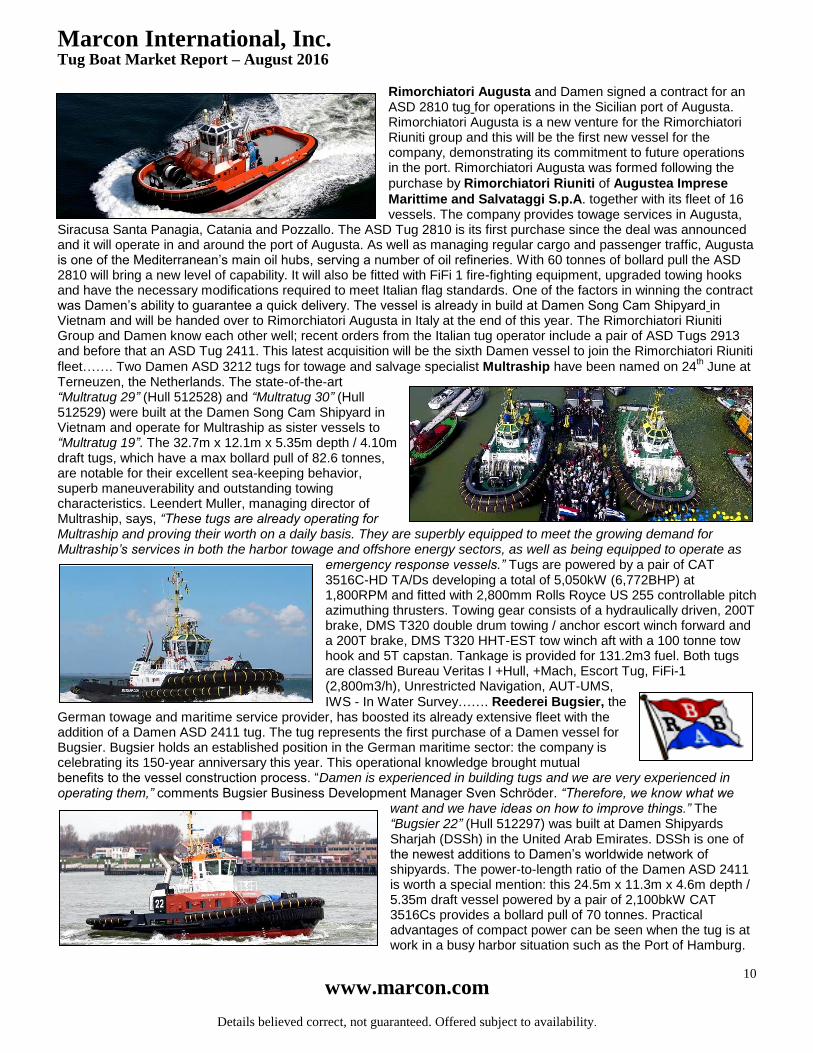

Rimorchiatori Augusta and Damen signed a contract for an ASD 2810 tug for operations in the Sicilian port of Augusta. Rimorchiatori Augusta is a new venture for the Rimorchiatori Riuniti group and this will be the first new vessel for the company, demonstrating its commitment to future operations in the port. Rimorchiatori Augusta was formed following the

purchase by Rimorchiatori Riuniti of Augustea Imprese

Marittime and Salvataggi S.p.A. together with its fleet of 16 vessels. The company provides towage services in Augusta,

Siracusa Santa Panagia, Catania and Pozzallo. The ASD Tug 2810 is its first purchase since the deal was announced and it will operate in and around the port of Augusta. As well as managing regular cargo and passenger traffic, Augusta is one of the Mediterranean’s main oil hubs, serving a number of oil refineries. W ith 60 tonnes of bollard pull the ASD 2810 will bring a new level of capability. It will also be fitted with FiFi 1 fire-fighting equipment, upgraded towing hooks and have the necessary modifications required to meet Italian flag standards. One of the factors in winning the contract was Damen’s ability to guarantee a quick delivery. The vessel is already in build at Damen Song Cam Shipyard in Vietnam and will be handed over to Rimorchiatori Augusta in Italy at the end of this year. The Rimorchiatori Riuniti Group and Damen know each other well; recent orders from the Italian tug operator include a pair of ASD Tugs 2913 and before that an ASD Tug 2411. This latest acquisition will be the sixth Damen vessel to join the Rimorchiatori Riuniti

fleet……. Two Damen ASD 3212 tugs for towage and salvage specialist Multraship have been named on 24th June at

Terneuzen, the Netherlands. The state-of-the-art “Multratug 29” (Hull 512528) and “Multratug 30” (Hull 512529) were built at the Damen Song Cam Shipyard in Vietnam and operate for Multraship as sister vessels to “Multratug 19”. The 32.7m x 12.1m x 5.35m depth / 4.10m draft tugs, which have a max bollard pull of 82.6 tonnes, are notable for their excellent sea-keeping behavior, superb maneuverability and outstanding towing characteristics. Leendert Muller, managing director of Multraship, says, “These tugs are already operating for Multraship and proving their worth on a daily basis. They are superbly equipped to meet the growing demand for Multraship’s services in both the harbor towage and offshore energy sectors, as well as being equipped to operate as

emergency response vessels.” Tugs are powered by a pair of CAT 3516C-HD TA/Ds developing a total of 5,050kW (6,772BHP) at 1,800RPM and fitted with 2,800mm Rolls Royce US 255 controllable pitch azimuthing thrusters. Towing gear consists of a hydraulically driven, 200T brake, DMS T320 double drum towing / anchor escort winch forward and a 200T brake, DMS T320 HHT-EST tow winch aft with a 100 tonne tow hook and 5T capstan. Tankage is provided for 131.2m3 fuel. Both tugs are classed Bureau Veritas I +Hull, +Mach, Escort Tug, FiFi-1 (2,800m3/h), Unrestricted Navigation, AUT-UMS,

IWS - In Water Survey……. Reederei Bugsier, the German towage and maritime service provider, has boosted its already extensive fleet with the addition of a Damen ASD 2411 tug. The tug represents the first purchase of a Damen vessel for Bugsier. Bugsier holds an established position in the German maritime sector: the company is celebrating its 150-year anniversary this year. This operational knowledge brought mutual benefits to the vessel construction process. “Damen is experienced in building tugs and we are very experienced in operating them,” comments Bugsier Business Development Manager Sven Schrӧder. “Therefore, we know what we

want and we have ideas on how to improve things.” The “Bugsier 22” (Hull 512297) was built at Damen Shipyards Sharjah (DSSh) in the United Arab Emirates. DSSh is one of the newest additions to Damen’s worldwide network of shipyards. The power-to-length ratio of the Damen ASD 2411 is worth a special mention: this 24.5m x 11.3m x 4.6m depth / 5.35m draft vessel powered by a pair of 2,100bkW CAT 3516Cs provides a bollard pull of 70 tonnes. Practical advantages of compact power can be seen when the tug is at work in a busy harbor situation such as the Port of Hamburg.

Marcon International, Inc. Tug Boat Market Report – August 2016

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

11

The second of two Damen Shoalbuster 3009 multi-purpose workboats for SMIT Amandla Marine has been named in a

ceremony at Damen Shipyards Cape Town, South Africa. With

De Beers Group Services the end client, the Lady Sponsor for the occasion was Mrs. Adri Nelson, Supply Chain Centre Manager for De Beers Group Services in Port Nolloth. Mrs. Nelson has been integral to the newbuild program in her role of managing the Northern Cape based supply chain center for De Beers. Named “Aogatoa” (Hull 571719), the vessel is the second of two CAT C32

powered Shoalbuster 3009s ordered by Smit Amandla Marine for the De Beers contract and built at Damen Shipyards Cape Town (DSCT). The first, “Aukwatowa” (Hull 571718), was delivered in December 2015. Throughout both builds, DSCT had the full cooperation of Damen Shipyards Hardinxveld. The Dutch yard transferred the necessary technology and provided full support to ensure a top quality end result. The Shoalbuster range of multi-purpose, shallow draught workboats is designed for all types of operations in inland and coastal waters. The 30m 3009S has a bollard pull of 24.5 tonnes and fitted with a crane with a lifting capacity of up to 1.7 tonnes, making it suitable for towage, buoy-laying, pushing and all-round support duties. These new vessels will carry out supply and support work for the De Beers Group’s offshore diamond mining activities out of Port Nolloth in the Northern Cape. With the shallow waters of the port making it accessible only to vessels with draughts of 2.8m or less, the minimal draught of the Shoalbuster was an important factor in selecting the class. During their time at the yard the construction of the two vessels made a significant contribution to the local economy with 180 employees employed locally working on the projects and with many materials also sourced locally. In addition, 13 apprentices, both male and female, also played an important part in the build, between them accumulating over 30,000 hours of on the job training. This was delivered by DSCT’s acclaimed merSETA-accredited training school. In expressing appreciation to De Beers Group and Smit Amandla, Sam Montsi, Chairman of DSCT, said: “I am confident that the delivery of this, the second of the two shoalbusters, will conclusively demonstrate to the regional shipping industry that, given the opportunity, DSCT can build and deliver

quality vessels at a fair price.”…….Van der Velden Marine Systems (VDVMS), part of Damen Shipyards Group, in conjunction with its US representative Ships Machinery International, Inc. (SMI) is pleased to announce the launching of a new state-of-the-art Jones Act ATB Tug with Barke ® high-lift flap rudders for coastal services. This new designed vessel brings increased maneuvering to the fleet of ATBs plying the US coastal waters. Tank tests prove that for this type of vessel this is the most effective rudder design. The new ATB will have enhanced maneuverability and excellent course-keeping stability. The efficiency provided by this high technology rudder solution will result in significant savings over the life of the vessel, hence reduced total cost of ownership. The “Sea Power” (Hull 259), built

by BAE Systems Southeast Shipyards in Jacksonville, Florida, was handed over to its owner Seabulk Tankers of

Fort Lauderdale, Florida in August. This modern 12,000BHP A/TB tug is designed by Guido Perla and Associates,

Inc. of Seattle, Washington to the following characteristics: length 43.0m, breadth 14.0m and a draft of 6.75m. Power is via two 4,640bkW Wartsila main engines and three main generators of 250ekW each with a standby emergency generator of 150ekW. The vessel uses a pin connector system between the tug and the barge and fully complies with ABS Under 90m Rules, Maltese Cross A1 AMS ACCU Towing Vessel, SOLAS, USCG Subchapter I. “We are pleased that our client selected this state of the art rudder system for their new vessel” said Arthur Dewey Vice President of SMI. “We are confident that their faith in Van der Velden rudders will be rewarded.” Independent Proportional Steering will allow the rudders to be actuated either independently or synchronized. Van der Velden has done a lot of work to facilitate the installation of these rudders into a hull and works closely with the designer and shipyard to ensure a

smooth transition from initial design to final installation. Guido Perla commented, “Van der Velden provided excellent technical support and on time delivery of design documents that helped us develop the engineering and design for the installation of their steering system. Their coordination with our staff was prompt and to the point. We appreciated their support.” The tug will work in tandem with a high-spec 30,000dwt chemical tank barge as an AT/B unit in Sea Tankers’ Jones Act coastal operation transporting chemical and petroleum products between U.S. ports. Another set of Barke® high-lift rudders will be installed on another ATB before this summer.

Marcon International, Inc. Tug Boat Market Report – August 2016

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

12

The retractable flanking rudder system is an in-house innovation of

Van der Velden Marine Systems (VDVMS). The system brings new efficiency to the inland shipping industry and will first be used

in Paraguay. At request of Dutch shipbuilder Veka Shipbuilding of Werkendam, VDVMS developed the system and had it tested independently by the Development Centre for Ship Technology and Transport Systems (DST) in Duisburg. Flanking rudders are often used for inland river tow boats. They are located forward of the propellers in order to provide maneuverability during astern operations, giving the convoy control when backing or flanking. In practice flanking rudders are only required during a small percentage of the sailing time and when not in use produce drag and creating turbulence to inflow of water to the main propellers. Retractable flanking rudders

increase water flow to the propellers, reduce vessel drag and increase efficiency, directly resulting in increased fuel savings. In close cooperation with the customer and end-client VDVMS designed, engineered and manufactured the retractable flanking units in less than 6 months. Imperial Shipping’s new pushers, the 43.5m x 17.56m x 3.0m depth, triple screw “Herkules XVII” and “Herkules XVIII”, will operate on the Parana river in Paraguay with a maximum of twelve approx. 62 x 17m barges, providing a total loading capacity of 35,000 tons. (Contact Marcon for further details). Including the towboat, the entire convoy will measure 290 x 50 meters. Vessels are powered by three 1,350bkW CAT 3512Cs developing a total of 5,500HP Mcr

at 1,600RPM. In addition to delivery of two retractable flanking units (each with two high lift rudders and asymmetric steering gears) VDVMS also supplied the main rudder system consisting of three HD240S high lift fishtail rudders with stainless steel reinforced leading edges. The vessels have five independently operating hydraulic power packs, three units which operate the three main rudders (3 x 1DW65/60) and two to retract and operate the flanking rudders (2 x 2DWK 4060/35). All main rudders are operated independently and controlled by the VDVMS Triple SP2700 control panel, the flanking rudders are operated by two SP2700 NFU control panels. To operate the flanking rudder lift units, 2 HDMI touch screens (retractable flanking rudder operation and control system RET2700) have been installed. In addition, VDVMS supplied a proprietary follow up steering system to operate each rudder independently and one FU2700 steering lever to operate all three main rudders synchronized…… On 10

th

August a keel-laying ceremony was held at Great Lakes Shipyard in Cleveland, Ohio for the first of 10 Damen Stan Tugs 1907 ICE. The tugs will be Ice Class and operated by the yard’s

affiliate company, The Great Lakes Towing Company, replacing existing vintage tonnage. Damen’s Houston-based manager for North America, confirmed that under the license, Great Lakes Shipyard will receive full construction, design and engineering support from Damen. The ten 1907 tugs will be the first in the USA to be designed and built to comply with the US Coast Guard Subchapter M regulations under ABS

classification. These came into effect in June this year and set new standards of seaworthiness for the towage industry and also establish new rules for safety management, including protocols and inspection requirements. Stan Tugs 1907 were chosen based on fact-finding visits made by the management of

The Great Lakes Towing Company to Damen in the Netherlands. In addition to Ice Class, they will be treated with special, high endurance paint capable of withstanding the abrasion that comes with moving through ice. Stan Tugs 1907 can be found operating in locations around the world including Russia, Qatar and the Netherlands. The partnership with Damen provided Great Lakes Shipyard with a portfolio of proven vessel designs for customers in the United States. Most of the designs have been refined to meet the needs of US operators.

Marcon International, Inc. Tug Boat Market Report – August 2016

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

13

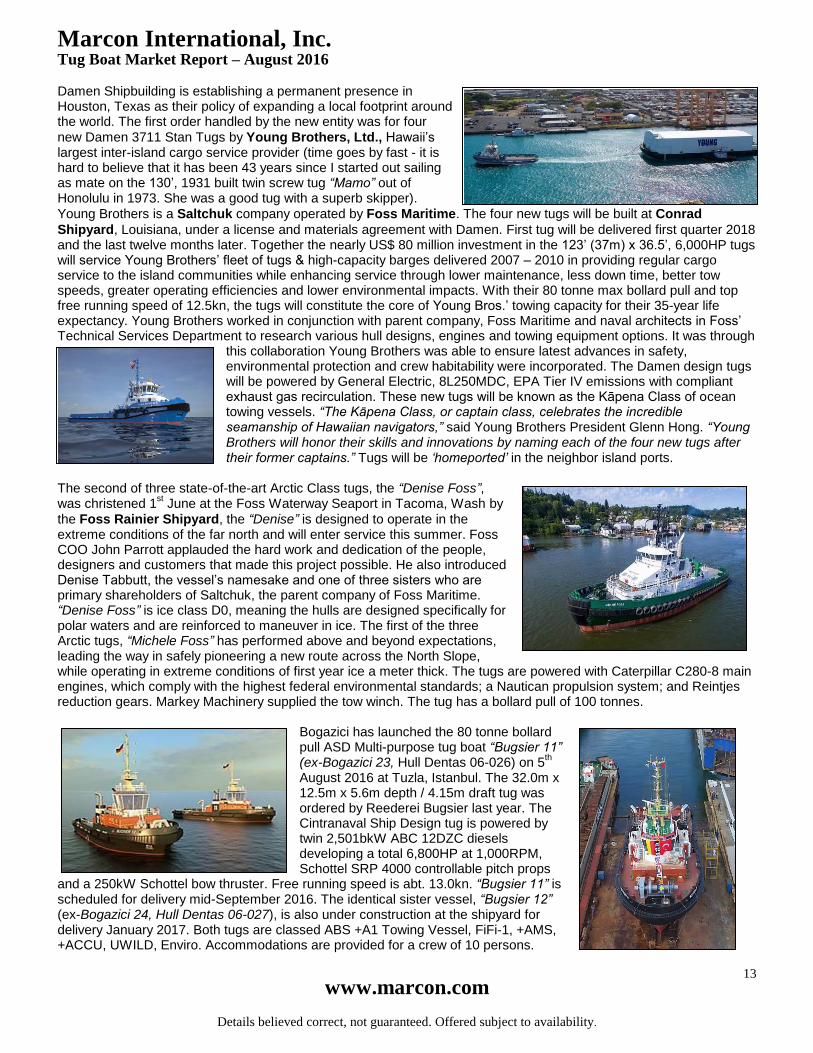

Damen Shipbuilding is establishing a permanent presence in Houston, Texas as their policy of expanding a local footprint around the world. The first order handled by the new entity was for four

new Damen 3711 Stan Tugs by Young Brothers, Ltd., Hawaii’s largest inter-island cargo service provider (time goes by fast - it is hard to believe that it has been 43 years since I started out sailing as mate on the 130’, 1931 built twin screw tug “Mamo” out of Honolulu in 1973. She was a good tug with a superb skipper).

Young Brothers is a Saltchuk company operated by Foss Maritime. The four new tugs will be built at Conrad

Shipyard, Louisiana, under a license and materials agreement with Damen. First tug will be delivered first quarter 2018 and the last twelve months later. Together the nearly US$ 80 million investment in the 123’ (37m) x 36.5’, 6,000HP tugs will service Young Brothers’ fleet of tugs & high-capacity barges delivered 2007 – 2010 in providing regular cargo service to the island communities while enhancing service through lower maintenance, less down time, better tow speeds, greater operating efficiencies and lower environmental impacts. With their 80 tonne max bollard pull and top free running speed of 12.5kn, the tugs will constitute the core of Young Bros.’ towing capacity for their 35-year life expectancy. Young Brothers worked in conjunction with parent company, Foss Maritime and naval architects in Foss’ Technical Services Department to research various hull designs, engines and towing equipment options. It was through

this collaboration Young Brothers was able to ensure latest advances in safety, environmental protection and crew habitability were incorporated. The Damen design tugs will be powered by General Electric, 8L250MDC, EPA Tier IV emissions with compliant exhaust gas recirculation. These new tugs will be known as the Kāpena Class of ocean towing vessels. “The Kāpena Class, or captain class, celebrates the incredible seamanship of Hawaiian navigators,” said Young Brothers President Glenn Hong. “Young Brothers will honor their skills and innovations by naming each of the four new tugs after their former captains.” Tugs will be ‘homeported’ in the neighbor island ports.

The second of three state-of-the-art Arctic Class tugs, the “Denise Foss”, was christened 1

st June at the Foss Waterway Seaport in Tacoma, Wash by

the Foss Rainier Shipyard, the “Denise” is designed to operate in the extreme conditions of the far north and will enter service this summer. Foss COO John Parrott applauded the hard work and dedication of the people, designers and customers that made this project possible. He also introduced Denise Tabbutt, the vessel’s namesake and one of three sisters who are primary shareholders of Saltchuk, the parent company of Foss Maritime. “Denise Foss” is ice class D0, meaning the hulls are designed specifically for polar waters and are reinforced to maneuver in ice. The first of the three Arctic tugs, “Michele Foss” has performed above and beyond expectations, leading the way in safely pioneering a new route across the North Slope, while operating in extreme conditions of first year ice a meter thick. The tugs are powered with Caterpillar C280-8 main engines, which comply with the highest federal environmental standards; a Nautican propulsion system; and Reintjes reduction gears. Markey Machinery supplied the tow winch. The tug has a bollard pull of 100 tonnes.

Bogazici has launched the 80 tonne bollard pull ASD Multi-purpose tug boat “Bugsier 11” (ex-Bogazici 23, Hull Dentas 06-026) on 5

th

August 2016 at Tuzla, Istanbul. The 32.0m x 12.5m x 5.6m depth / 4.15m draft tug was ordered by Reederei Bugsier last year. The Cintranaval Ship Design tug is powered by twin 2,501bkW ABC 12DZC diesels developing a total 6,800HP at 1,000RPM, Schottel SRP 4000 controllable pitch props

and a 250kW Schottel bow thruster. Free running speed is abt. 13.0kn. “Bugsier 11” is scheduled for delivery mid-September 2016. The identical sister vessel, “Bugsier 12” (ex-Bogazici 24, Hull Dentas 06-027), is also under construction at the shipyard for delivery January 2017. Both tugs are classed ABS +A1 Towing Vessel, FiFi-1, +AMS, +ACCU, UWILD, Enviro. Accommodations are provided for a crew of 10 persons.

Marcon International, Inc. Tug Boat Market Report – August 2016

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

14

On 22nd

July, Harley Marine Services’ newest ATB tug, “Dale R. Lindsey” was christened in Seattle. The “Dale R. Lindsey” (Hull 54143), a 95.0’ x 38.0’ x 16.9’ ATB tug, will be paired with the 28,450bbl double hull tank barge “Petro Mariner” using an Articouple FRM043 system. The 3,000HP tug is powered by twin 1,500HP Caterpillar 3512C Tier 3 diesel main propulsion engines at 1,600RPM. Reintjes WAF 675 7.091:1 reduction gears turn a pair of five-blade, 96” x 85” stainless steel propellers. A Markey TYS-32 towing winch operates on the aft deck. Accommodations include six staterooms for 11 crew. Fuel capacity is 65,000 gallons. The raised aluminum upper pilothouse

has a 50’ height of eye. The tug was designed by Elliott Bay Design Group in Seattle and built locally by Vigor Fab. LLC on Harbor Island in Seattle, Washington. This is the first tug Vigor has built for Harley Marine. Both the “Dale R. Lindsey” and the 222.0’ x 64.6’ x 23.6’ ““Petro Mariner” will be servicing Petro Marine Services’ fuel supply business in Southeastern Alaska. The company is Alaska's largest independent petroleum marketing firm, with operations throughout South Central and Southeast Alaska, as well as Northwestern Canada.

Work continues on Harley Marine’s new 120.0’ x 35.0’ x 19.25’ depth, 5,350HP, ASD line-haul boat, the “Earl W Redd” (Hull 34) which is being built by

Kurt Redd at Diversified Marine, Inc. in Portland, Oregon and powered with the first Caterpillar Tier IV engines in a tug. To meet the more stringent Tier 4 Final emissions standards coming in 2016, each of the two continuous duty 3516E engines - individually rated with a 10% horsepower increase

of 2,682HP at 1,600RPM - is paired with a selective catalytic reduction (SCR) after treatment system. SCR uses a urea-based solution to reduce the oxides of nitrogen (NOx) contained in diesel exhaust down to nitrogen and water vapor. Just as important, it does so efficiently.

Astilleros Armon SA of Vigo, Spain currently has three tugs on their orderbook, the 32.5m x 11.0m, 6,700HP “Armon Navia 763” being built for Ocean Srl, Italy / Adria Tow doo, Slovenia, the 40.0m x 8.1m, CAT 3508C powered, twin screw “Armon Navia 781” under construction for yet unnamed operators and the 24.4m x 11.25m x 4.38m, CAT 3516C powered “Ponga” (Hull Armon Navia 775) being built for Remolques Gijoneses SA of Gijon, Spain. Recently delivered to Remolques Unidos SL of Santander, Spain were the Bureau Veritas classed, 31.5m x 11.2m x 5.4m depth, ASD escort, FiFi-1 (2,700m3/h) tugs “Trheintayuno” (Hull 767) and “Trheinta” (Hull 766). Both tugs (photo left) are powered by twin 1,492bkW CAT 3516Cs with Schottel azimuthing drives and Schottel bow thruster providing abt. 90 tonnes of bollard pull.

On April 26, 2016, Cheoy Lee Shipyards of Hong Kong launched at their Hin Lee (Zhuhai) Shipyard the 100th

vessel it has built to a Robert Allan Ltd. design, becoming the second shipyard worldwide to do so, after Sanmar’s initial achievement of this milestone in 2013. This 32.0m x 12.8m x 5.37m depth epic tug, Hull Number 5098 at Cheoy Lee, is a RAstar 3200 class ASD tug, with completion expected in August 2016. Tug will be classed LR 100A1. At present Cheoy Lee’s Hin Lee yard in China is very busy with a flotilla of Robert Allan Ltd. tugs at various stages of completion. The cooperation between Robert Allan Ltd. and Cheoy Lee dates back to 2003, with the construction of the first of the Z-Tech® series tugs for PSA Marine.

Marcon International, Inc. Tug Boat Market Report – August 2016

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

15

OAO Astrakhan Sudoverf of Russia has launched the 24.5m x 8.0m x 3.7m depth, twin screw tugs “Mars” (Hull 703) and “Saturn” (Hull 704) as the last of a

five tug order being built for OMS Shipping LLP of Aqtau, Mangghystau oblysy, Kazakhstan. The tugs are powered by twin Daewoo V180TIH 4-stroke diesels developing a total of 1,200HP at 1,800RPM. These five tugs, all named after planets, join three, ice-strengthened, 2012 built, 1,958HP, 30.7m Nanjing East Star built tugs – the “Phoenix”, “Orion” and “Hercules”. In all, OMS Shipping reportedly is planned to purchase sixteen ancillary and special vessels to delivery stone for artificial islands being built in Kazakhstan’s sector of the Caspian Sea. Tugs are being classed under the Russian Maritime Register.

Eastern Shipbuilding Group, Inc., of Panama City, Florida

launched the escort tug “Laura B” (Hull 254) for Bay-Houston

Towing Co. on 1st July. The tug is scheduled to deliver later this

year. “Laura B” is the last of a series of four Z-Tech Class Terminal & Escort Tugs designed by Robert Allan Ltd. being constructed for Bay-Houston Towing Co. The “H. Douglas M” (Hull 236), “Zyana K” (Hull 238) and “David B” (Hull 239) delivered earlier this year. Eastern is also constructing simultaneously an identical series, of the same design for

Suderman & Young Towing Company. The escort tug “Oceanus” (Hull 240) was delivered to Suderman & Young Towing Company in July 2016 and the “Poseidon” (Hull 255), the fourth in the series being built for Suderman & Young, was launched on 15

th August and scheduled for

delivery later this year. G&H Towing Company is the Owners’ onsite Representative and Agent during the engineering, construction and delivery for both Bay-Houston and Suderman & Young Towing companies. In addition to various types of offshore support / supply vessels and two factory stern trawlers, Eastern Shipbuilding also has the

158.3’ x 52.0’ x 32’.8 deep, 14,000HP ATB pusher tug “Douglas B. Mackie” (Hull 252) powered with twin MaK 12M32Cs and the 433’ x 92’ x 36’, 15,000yd3, ATB trailing suction hopper dredge barge “Ellis Island” (Hull 253)

being built for Great Lakes Dredge & Dock Co. and designed by Ocean Tug

& Barge Engineering, Inc. The state-of-the-art Great Lakes ATB hopper dredge will be a key tool in performing restoration of the eroded land mass in the Gulf Coast States. Additionally, the vessel’s ability to cost effectively deepen and maintain navigable waterways will bolster the United States’ competitive position in world trade, as the nation’s ports move forward with deepening plans to accommodate larger vessels, sailing through the expanded Panama Canal.

Chesapeake Shipbuilding Corp. of Salisbury, Maryland successfully

delivered another ocean going tugboat to Vane Brothers of Baltimore, Maryland. The boat, named “Fort McHenry” (Hull 122), marks the 12th “Sassafras” class tugboat that Chesapeake Shipbuilding has built for Vane. Chesapeake Shipbuilding has 5 additional tugboats under construction for the company. The “Fort McHenry” is equipped with twin Caterpillar 3512 Tier 3 main engines producing a combined 3,000BHP and a single drum Series

“500” hydraulic winch from JonRie of New Jersey. The tug measures 94’ long with a 32’ beam and a 13’ depth. Her name pays homage to the Baltimore-based fort that was instrumental in America's defense against the British during the War of 1812 and inspired the writing of "The Star-Spangled Banner." Chesapeake Shipbuilding and Vane Brothers also signed contracts for three additional ocean-going tugs, which will be the 18

th, 19

th and 20

th similar design tugs built for Vane in the last

eight years. All Chesapeake Shipbuilding tugs are built in a controlled indoor environment prior to being moved and launched into Maryland’s Wicomico River. Chesapeake Shipbuilding has recently made significant upgrades to its facility to increase its production capacity and efficiency. Vane Brothers operates more than 50 tug boats, two articulated tug and barge units (AT/Bs) and two freight boats in North America.

Marcon International, Inc. Tug Boat Market Report – August 2016

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

16

As of late June, Vane Brothers were not only looking forward to the delivery of the “Fort McHenry” above, but the 4,200HP, 100’ x 34’ x 15’ depth “Baltimore” (Hull 60), tug number three in the “Elizabeth Anne” (Hull 58 built in 2015 &

delivered January 2016) class coming out of St. Johns Ship Building of Palatka, Florida, with several more vessels ready to launch. The 4,200HP “Hudson” (Hull

59 built 2016 photo left) had joined Vane’s Philadelphia-based fleet in early May after picking up the 55,000bbl tank barge “Double

Skin 601” completed at the Conrad Deepwater

South Shipyard in Amelia, Louisiana. The “Double Skin 602” was launched in early June and soon headed to Crescent Consolidated Services in Gibson, Louisiana for tank lining installation. Delivery of the completed barge is expected in October. Meanwhile, the tug “Oyster Creek” picked up the “Double Skin 317”, the last of seven 35,000bbl bunker barges built by Conrad’s Orange, Texas operation. Currently under construction at Conrad Deepwater South is the 55,000bbl asphalt barge “Double Skin 510A”, a modified version of last year’s “Double Skin 509A”, but with enlarged machinery & accommodations houses, an Ian-Conrad Bergan cargo monitoring

system and the ability to handle asphalt cargoes loaded at even higher temperatures up to 360 deg. F. Each of the ten pipe coil heat exchangers in the cargo tanks are comprised of nearly one mile of 2.5” diameter pipe. Conrad Deepwater South is also beginning to fabricate panels for the “Double Skin 801”, the first of three 80,000bbl barges to be matched with tugs as AT/B units. “DS-801” is slated for delivery in Fall 2017, about a month after the 110’ x 38’ AT/B tug

“Assateague” is delivered by Conrad Orange. Each of the new tugs being built are ready for Subchapter “M”.

VT Halter Marine, Inc. delivered the 6,000HP twin screw ATB tug “Frederick E. Bouchard” at their Pascagoula, Mississippi facility on 9

th June. The delivery culminates the two-vessel

contract awarded by Bouchard Transportation Co. of New York to VT Halter in August 2014. The first vessel of the contract, “Morton S. Bouchard Jr.”, was delivered 1

st February

and is currently in service. “Frederick E. Bouchard”, named after another Bouchard family member, the brother of Morton S. Bouchard, Jr., will be joining Bouchard Transportation’s coastwise fleet. These two vessels are equipped with Intercon coupler systems, measure 130’ x 38’ x 22’ depth and are classed ABS +A1, Towing Vessel, +AMS, Dual Mode ATB, Unrestricted Service. Tugs are powered by twin EMD 12-710G7C diesels with Lufkin gears driving fixed pitch propellers and develop a bollard pull of 60.91 short tons.

Fincantieri Marine Group’s Fincantieri Bay Shipbuilding delivered the 5,300HP ATB tug “Barbara Carol Ann Moran” (Hull 776) and the 468’ x 78’ x 34’, 122,000bbl, double hull,

chemical barge “Louisiana” (Hull 775) to Moran Towing Corporation. The 5,300HP, 123.0’ x 36.1’ x 18.0’ vessel is classed ABS +A-1 Towing Vessel, +AMS, CPS, RRDA, UWILD (Underwater Inspection In Lieu of Drydocking), Unrestricted Service and equipped with state-of-the-art navigation and communications technology. Tug is powered by twin EMD 12-710G7C diesels, Lufkin gears and fixed pitch props. ABS certified bollard pull is 53.7 tonnes ahead. The ATB unit was delivered on the exact day called for by the contract and will work the East Coast of the United States and the Gulf of Mexico. This is the third delivery to Moran under a 2014 contract, with a tank barge

delivered in May of 2015 and another Intercon coupler fitted ATB - the tug “Leigh Ann Moran” (Hull 778) and the 495’ x 78’ x 41’ depth, 160,0815bbl double hull, coiled petroleum barge “Mississippi” (Hull 777) delivered 1

st December 2015.

Marcon International, Inc. Tug Boat Market Report – August 2016

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

17

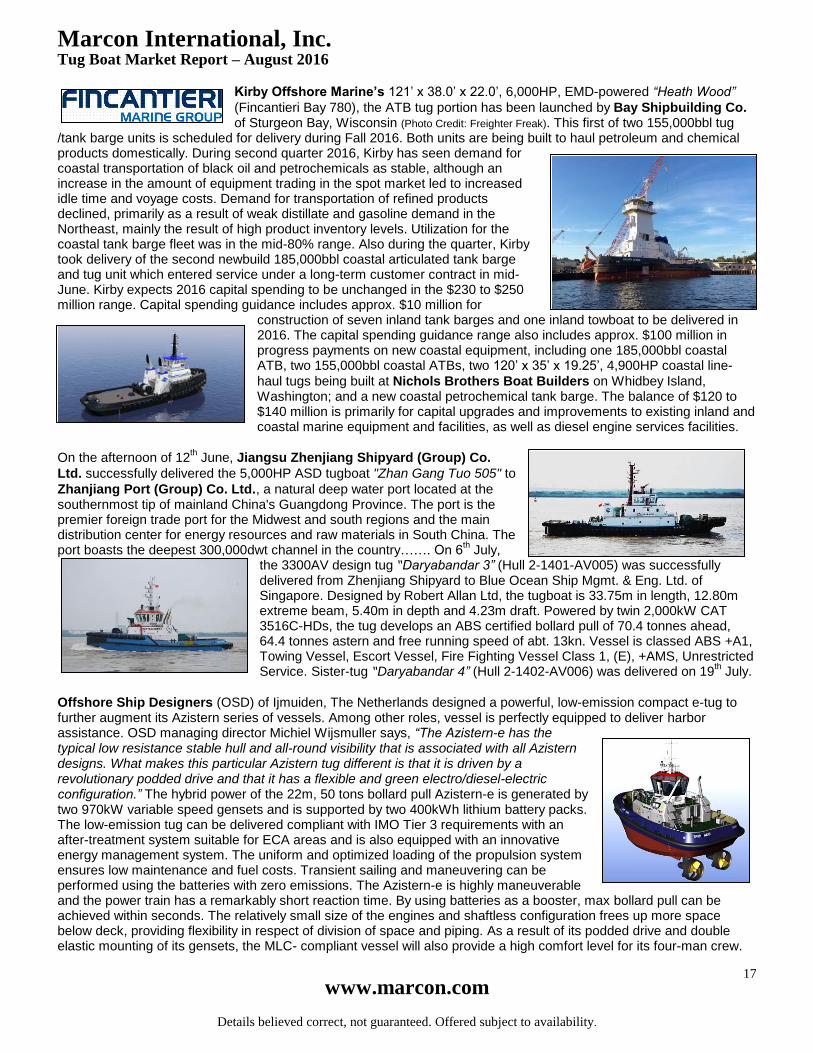

Kirby Offshore Marine’s 121’ x 38.0’ x 22.0’, 6,000HP, EMD-powered “Heath Wood”

(Fincantieri Bay 780), the ATB tug portion has been launched by Bay Shipbuilding Co. of Sturgeon Bay, Wisconsin (Photo Credit: Freighter Freak). This first of two 155,000bbl tug

/tank barge units is scheduled for delivery during Fall 2016. Both units are being built to haul petroleum and chemical products domestically. During second quarter 2016, Kirby has seen demand for coastal transportation of black oil and petrochemicals as stable, although an increase in the amount of equipment trading in the spot market led to increased idle time and voyage costs. Demand for transportation of refined products declined, primarily as a result of weak distillate and gasoline demand in the Northeast, mainly the result of high product inventory levels. Utilization for the coastal tank barge fleet was in the mid-80% range. Also during the quarter, Kirby took delivery of the second newbuild 185,000bbl coastal articulated tank barge and tug unit which entered service under a long-term customer contract in mid-June. Kirby expects 2016 capital spending to be unchanged in the $230 to $250 million range. Capital spending guidance includes approx. $10 million for

construction of seven inland tank barges and one inland towboat to be delivered in 2016. The capital spending guidance range also includes approx. $100 million in progress payments on new coastal equipment, including one 185,000bbl coastal ATB, two 155,000bbl coastal ATBs, two 120’ x 35’ x 19.25’, 4,900HP coastal line-

haul tugs being built at Nichols Brothers Boat Builders on Whidbey Island, Washington; and a new coastal petrochemical tank barge. The balance of $120 to $140 million is primarily for capital upgrades and improvements to existing inland and coastal marine equipment and facilities, as well as diesel engine services facilities.

On the afternoon of 12th June, Jiangsu Zhenjiang Shipyard (Group) Co.

Ltd. successfully delivered the 5,000HP ASD tugboat "Zhan Gang Tuo 505" to

Zhanjiang Port (Group) Co. Ltd., a natural deep water port located at the southernmost tip of mainland China's Guangdong Province. The port is the premier foreign trade port for the Midwest and south regions and the main distribution center for energy resources and raw materials in South China. The port boasts the deepest 300,000dwt channel in the country……. On 6

th July,

the 3300AV design tug “Daryabandar 3” (Hull 2-1401-AV005) was successfully delivered from Zhenjiang Shipyard to Blue Ocean Ship Mgmt. & Eng. Ltd. of Singapore. Designed by Robert Allan Ltd, the tugboat is 33.75m in length, 12.80m extreme beam, 5.40m in depth and 4.23m draft. Powered by twin 2,000kW CAT 3516C-HDs, the tug develops an ABS certified bollard pull of 70.4 tonnes ahead, 64.4 tonnes astern and free running speed of abt. 13kn. Vessel is classed ABS +A1, Towing Vessel, Escort Vessel, Fire Fighting Vessel Class 1, (E), +AMS, Unrestricted Service. Sister-tug “Daryabandar 4” (Hull 2-1402-AV006) was delivered on 19

th July.

Offshore Ship Designers (OSD) of Ijmuiden, The Netherlands designed a powerful, low-emission compact e-tug to further augment its Azistern series of vessels. Among other roles, vessel is perfectly equipped to deliver harbor assistance. OSD managing director Michiel Wijsmuller says, “The Azistern-e has the typical low resistance stable hull and all-round visibility that is associated with all Azistern designs. What makes this particular Azistern tug different is that it is driven by a revolutionary podded drive and that it has a flexible and green electro/diesel-electric configuration.” The hybrid power of the 22m, 50 tons bollard pull Azistern-e is generated by two 970kW variable speed gensets and is supported by two 400kWh lithium battery packs. The low-emission tug can be delivered compliant with IMO Tier 3 requirements with an after-treatment system suitable for ECA areas and is also equipped with an innovative energy management system. The uniform and optimized loading of the propulsion system ensures low maintenance and fuel costs. Transient sailing and maneuvering can be performed using the batteries with zero emissions. The Azistern-e is highly maneuverable and the power train has a remarkably short reaction time. By using batteries as a booster, max bollard pull can be achieved within seconds. The relatively small size of the engines and shaftless configuration frees up more space below deck, providing flexibility in respect of division of space and piping. As a result of its podded drive and double elastic mounting of its gensets, the MLC- compliant vessel will also provide a high comfort level for its four-man crew.

Marcon International, Inc. Tug Boat Market Report – August 2016

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

18

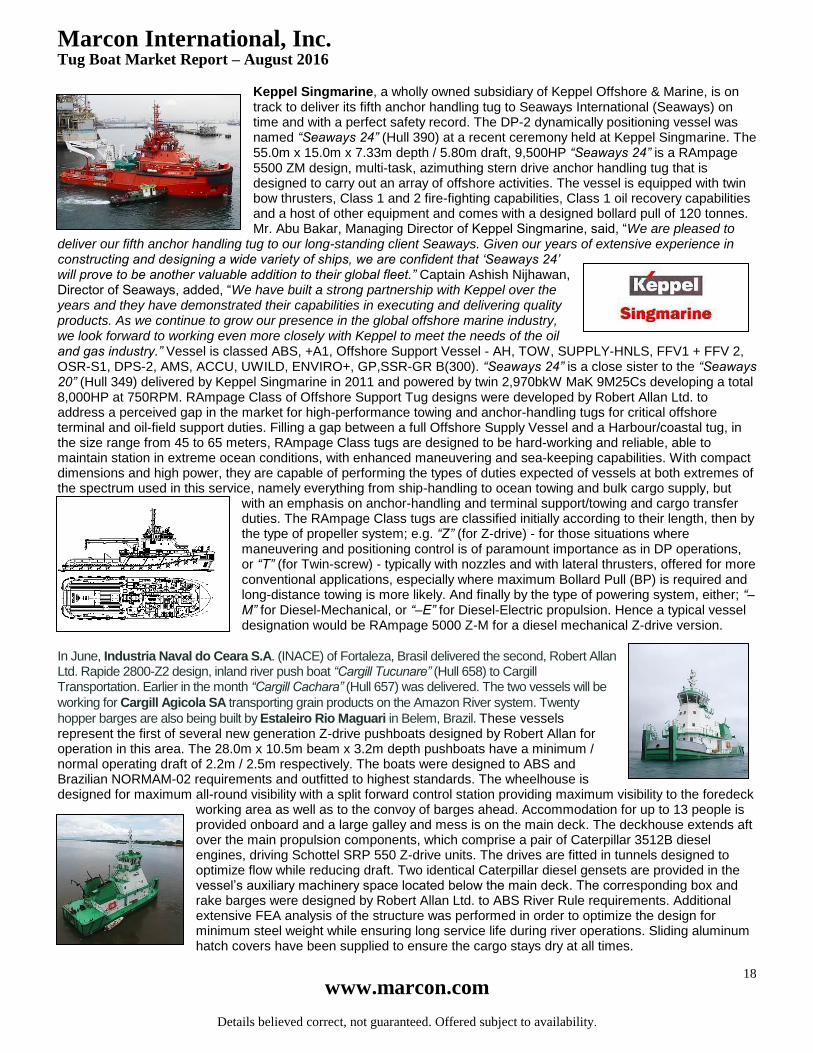

Keppel Singmarine, a wholly owned subsidiary of Keppel Offshore & Marine, is on track to deliver its fifth anchor handling tug to Seaways International (Seaways) on time and with a perfect safety record. The DP-2 dynamically positioning vessel was named “Seaways 24” (Hull 390) at a recent ceremony held at Keppel Singmarine. The 55.0m x 15.0m x 7.33m depth / 5.80m draft, 9,500HP “Seaways 24” is a RAmpage 5500 ZM design, multi-task, azimuthing stern drive anchor handling tug that is designed to carry out an array of offshore activities. The vessel is equipped with twin bow thrusters, Class 1 and 2 fire-fighting capabilities, Class 1 oil recovery capabilities and a host of other equipment and comes with a designed bollard pull of 120 tonnes. Mr. Abu Bakar, Managing Director of Keppel Singmarine, said, “We are pleased to

deliver our fifth anchor handling tug to our long-standing client Seaways. Given our years of extensive experience in constructing and designing a wide variety of ships, we are confident that ‘Seaways 24’ will prove to be another valuable addition to their global fleet.” Captain Ashish Nijhawan, Director of Seaways, added, “We have built a strong partnership with Keppel over the years and they have demonstrated their capabilities in executing and delivering quality products. As we continue to grow our presence in the global offshore marine industry, we look forward to working even more closely with Keppel to meet the needs of the oil and gas industry.” Vessel is classed ABS, +A1, Offshore Support Vessel - AH, TOW, SUPPLY-HNLS, FFV1 + FFV 2, OSR-S1, DPS-2, AMS, ACCU, UWILD, ENVIRO+, GP,SSR-GR B(300). “Seaways 24” is a close sister to the “Seaways 20” (Hull 349) delivered by Keppel Singmarine in 2011 and powered by twin 2,970bkW MaK 9M25Cs developing a total 8,000HP at 750RPM. RAmpage Class of Offshore Support Tug designs were developed by Robert Allan Ltd. to address a perceived gap in the market for high-performance towing and anchor-handling tugs for critical offshore terminal and oil-field support duties. Filling a gap between a full Offshore Supply Vessel and a Harbour/coastal tug, in the size range from 45 to 65 meters, RAmpage Class tugs are designed to be hard-working and reliable, able to maintain station in extreme ocean conditions, with enhanced maneuvering and sea-keeping capabilities. With compact dimensions and high power, they are capable of performing the types of duties expected of vessels at both extremes of the spectrum used in this service, namely everything from ship-handling to ocean towing and bulk cargo supply, but