Managing Finance and Budgets Seminar 5. Seminar Five - Activities Preparation: read M & A Chapters...

34

Managing Finance and Budgets Seminar 5

-

Upload

wade-bunyan -

Category

Documents

-

view

214 -

download

0

Transcript of Managing Finance and Budgets Seminar 5. Seminar Five - Activities Preparation: read M & A Chapters...

Managing Finance and Budgets

Seminar 5

Seminar Five - Activities

Preparation: read M & A Chapters 8, 9 and 10 Describe key concepts:

Objectives of cost analysis

Cost definitions

Cost behaviour & Break-even analysis

Full (absorption) costing Exercises 10.4 (page 337) and 10.8 (page 340)

Starting Points (1)

Define what is meant by the following: Historic Cost Past Cost Opportunity Cost Sunk Cost Committed Cost Outlay Cost

.When and in what circumstances can costs be regarded as relevant or irrelevant?.

Summary of the relationship between relevant and irrelevant costs

Costs which are the same irrespective

of which decision is made

Relevant costs

Irrelevant costs

Future costs which vary with the

decision under consideration

Past costs

Costs which were incurred as a result of a past decision

Opportunity costs

The cost of being deprived

of the next best option

Outlay costs

Future cash outflows which vary with the

decision

Future cash outflows which do not vary with

the decisionOutlay costs

Starting Points (2)

Define what is meant by the following: Fixed Cost Variable Cost

Consider a Hairdressing Salon.

Can you give some examples of: Fixed costs Variable costs

The behaviour of costs

Those that stay fixed (the same) when changes occur to the

volume of activity

Those that vary according to the volume of activity

Costs may be broadly classified as:

Fixed

Variable

Starting Points (3)

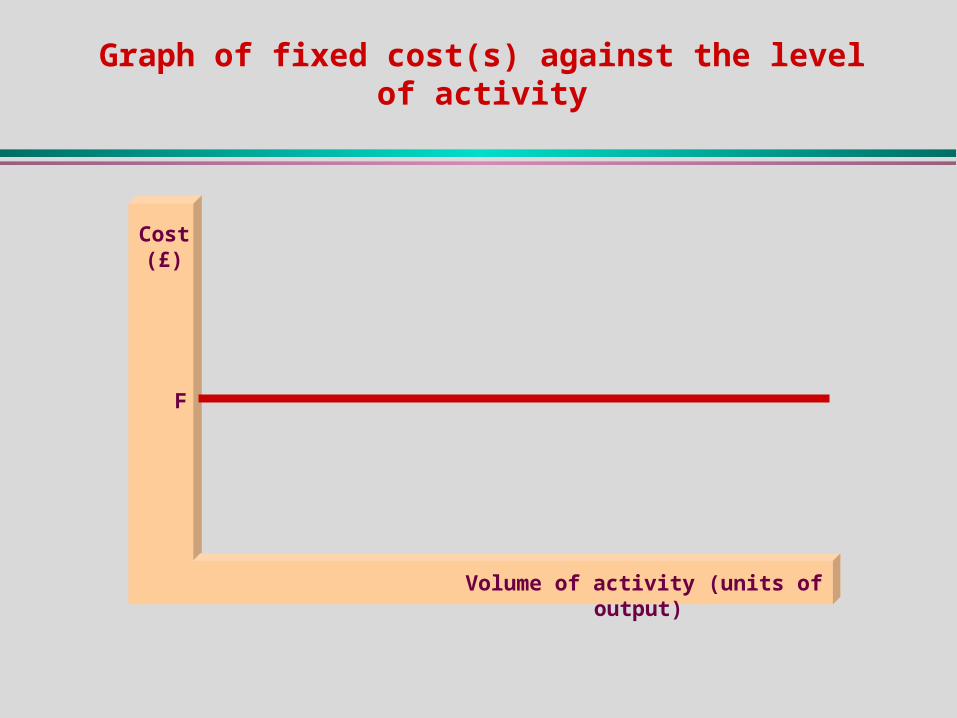

Interpreting Graphs The next three slides show the level of cost against volume

of activity for different types of costs. Explain what the graph shows in each case.

Cost (£)

Volume of activity (units of output)

F

Graph of fixed cost(s) against the level of activity

Rent cost (£)

Volume of activity

R

Graph of rent cost against the level of activity

Cost (£)

Volume of activity 0

Graph of cost of lotions and other materials against the level of activity

Electricity cost (£)

Volume of activity 0

The slope of this line gives the variable cost

per unit of activity

Graph of electricity cost against the level of activity

Fixed cost

element

Break-Even Analysis (1)

Explain what is meant by the ‘Break-Even’ point. The next two slides show various components required to

calculate the ‘Break-Even’ point. What do the slides show? Interpret what is happening.

State the Break-Even Formula. Where does this formula come from?

Cost (£)

Volume of activity (units of output)0

F

Total cost

Fixed costs

Variable costs

Graph of total cost against the level of activity

Cost (£)

Volume of activity (units of output)0

F

Total cost

Fixed costs

Variable costs

Break even point

Total sales service

Break-even chart

Calculating the break - even point

Fixed costs________________ Sales revenue per unit – Variable costs per unit

b =

Profit (£)

Volume of activity0

Loss

Profit

Break even point

Loss (£)

Fixed cost

Profit-volume chart

Break-Even Analysis (2)

Cottage Industries sells 500 baskets per month. Fixed costs are £500 Each basket costs £2 in materials and £10 labour. Baskets are sold at £14 each.

Calculate the ‘Break-Even’ point, in terms of ‘baskets per month.

What is the total profit each month?

Break-even chart for Cottage Industries’ basket making without the machine

Cost (£000)

Volume of activity (number of baskets)

0

1Fixed costs

Totalrevenue5

4

3

2

Totalcosts

100 400300200 500

Break-Even Analysis (2)

A machine costing £3000 per month is available, but reduces the other costs to: Fixed costs are £500 Each basket costs £2 in materials and £5 labour.

Calculate the new ‘Break-Even’ point, in terms of ‘baskets per month.

What is the new total profit each month?

Break-even chart for Cottage Industries’ basket making with the machine

Cost (£000)

1

Fixed costs

Totalrevenue5

4

3

2

Totalcosts

Volume of activity (number of baskets)

0100 400300200 500

Operational Gearing

The Basket-making example highlights the issue of ‘Operational (or Operating) Gearing’. Explain, using the example what this means.

Fill in the blanks, using the words high and low:

If the volume of trade is ____, a company with ___ operational gearing will tend to have ____ profit compared to a company with ____ operational gearing.

The effect of operating gearing

Break-Even Analysis

Describe some of the weaknesses of Break-Even Analysis

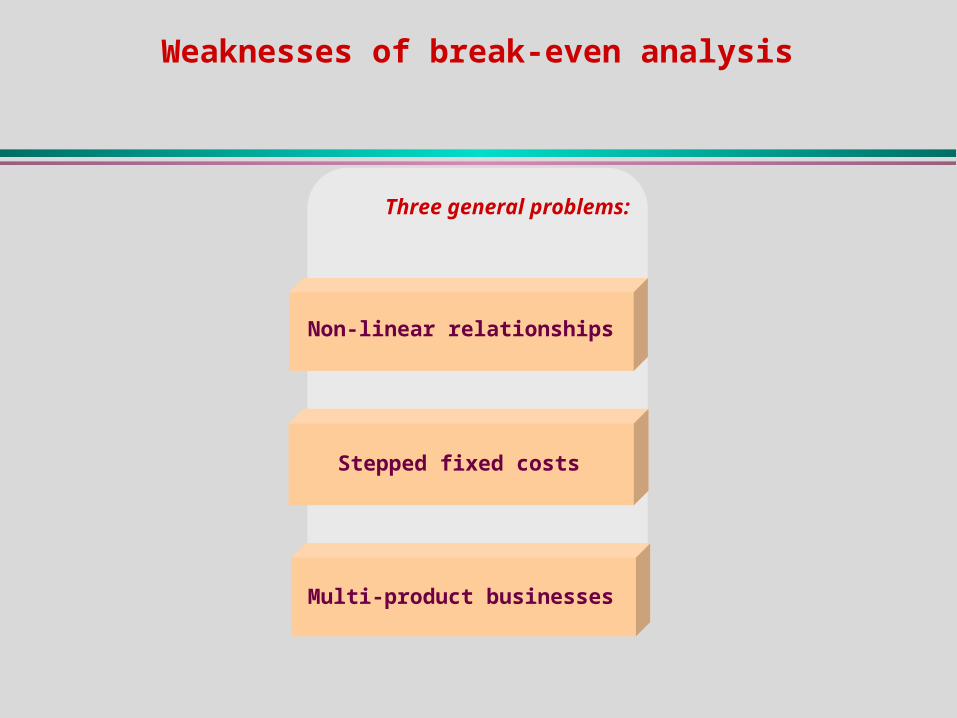

Weaknesses of break-even analysis

Three general problems:

Non-linear relationships

Stepped fixed costs

Multi-product businesses

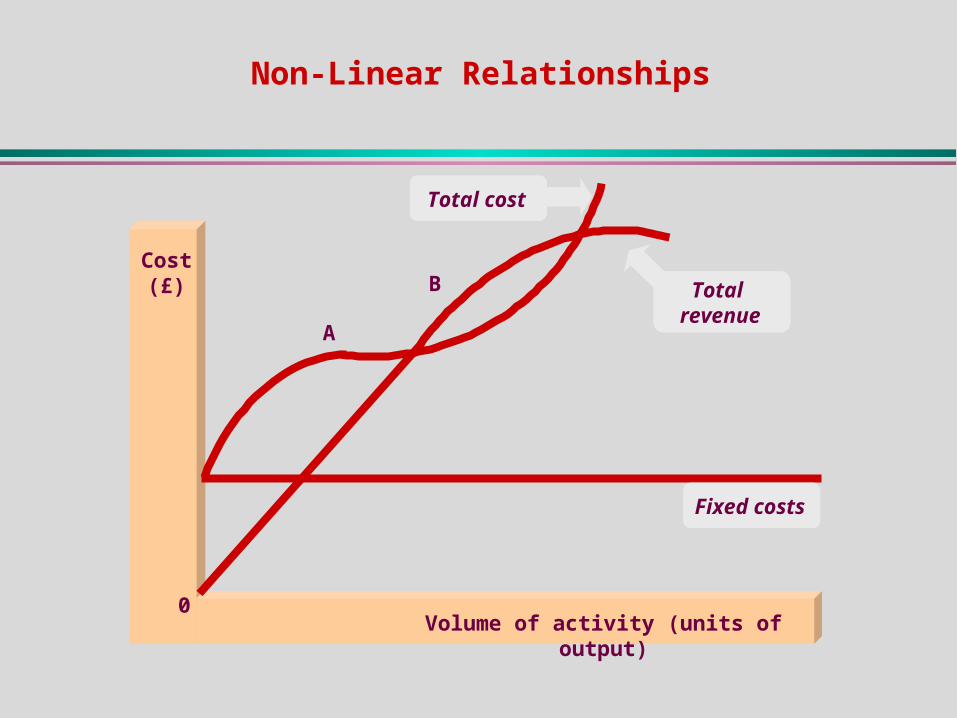

Non-Linear Relationships

Cost (£)

Volume of activity (units of output)0

Fixed costs

A

B

Total cost

Total revenue

Fixed cost (£)

Duration of activity

R

Stepped Fixed Costs

Full Costing

What is ‘Full Costing’? What is it used for? Explain the relationships between Full Costs and:

Direct and Indirect Costs Fixed and Variable Costs

How would you deal with overheads on a departmental basis?

Uses of full cost information

Two main uses:

For pricing purposes

For income measurement purposes

Direct and indirect costs

These are all other costs: That is, those that cannot be directly

measured in respect of each particular unit of output.

Two categories of costs:

Direct costs

Indirect costs or (overheads)

Costs that can be identified with specific cost units – the effect of

the cost can be measured in respect of each particular output.

The relationship between direct costs and indirect costs

Full cost of the unit

Direct costs of the unit

Fair share of indirect costs (overheads)

The relationship between fixed costs, variable costs and total costs

Total (or full) costs

Fixed costsVariable

costs

The relationship between direct, indirect, variable and fixed costs of a particular job

Total (or full) cost of a

particular job

Indirect costs (overheads)

Fixed costs

Direct costs

Variable costs

Preparation department

Finished goods store

Finishing department

Machining department

* Direct materials * Direct labour * A share of thePreparation Department’s overheads

Job A

A cost unit passing through the production process

Costing Jobs

M & A Exercise 10.4 M & A Exercise 10.8