LNG$BUNKERING - Platts · LNG$BUNKERING $ Manuel$Carlier$ Member$of$the$Board$of$Directors$...

45

LNG BUNKERING Manuel Carlier Member of the Board of Directors European Community Shipowners’ AssociaDons ECSA

-

Upload

trannguyet -

Category

Documents

-

view

226 -

download

0

Transcript of LNG$BUNKERING - Platts · LNG$BUNKERING $ Manuel$Carlier$ Member$of$the$Board$of$Directors$...

LNG BUNKERING

Manuel Carlier Member of the Board of Directors

European Community Shipowners’ AssociaDons -‐ ECSA

Established in 1965, ECSA comprises the naDonal shipowners’ associaDons of the EU plus Norway

Aims:

promoDng the interests of European shipping so that the industry can best serve European and internaDonal trade and commerce

in a compeDDve free-‐enterprise environment to the benefit of shippers and consumers

European Community Shipowners’ Associa7ons ECSA

European shipping

controlling over 40% of the world merchant fleet

European Community Shipowners’ Associa7ons ECSA

European Community Shipowners’ Associa7ons Manuel Carlier PhD in Naval Architecture and Marine Engineering

CEO -‐ Spanish Shipowners’ AssociaDon (ANAVE) Member of ECSA’s Board of Directors since 1996 Chairman -‐ ECSA’s Shipping Policy CommiTee

(up to June 2011) President -‐ Shortsea PromoDon Center-‐Spain Assistant Professor of Shipping Economics

Polytechnic University Madrid – Since 1986

Embracing LNG as a clean and economical fuel for shipping EvaluaDng the economic viability of LNG as a shipping fuel

Is universal conversion feasible?

Overcoming the barriers to developing LNG bunker supply infrastructure

References Trending topic Some recent studies Greenship.org (2012): Green ship of the future. ECA retrofit study. Det Nosrke Veritas (2012): Shipping 2020. Danish Mari7me Administra7on (2012): North European LNG Infrastructure Project. Feasibility Study.

TRI-‐ZEN (2012): LNG market perspecEve. Wär7lä (2012): Turning gas to ship power

Germanischer Lloyd (2011): MSC.285(86) and Code for gas-‐fuelled ships

Marintek (2008): MAGALOG – MariEme Gas Fuel LogisEcs.

Main drivers

REGULATORY PRESSURE SOx/Nox:

MARPOL Annex VI

EU Direc7ve

CO2: EEDI -‐ Future Market Based Measures

BUNKER MARKET PRICE Record year-‐average bunkers prices in 2011

and 2012

LNG price lower than oil bunkers

CO2 Other SOx NOx Balast

A 7ght environmental agenda (source: DNV)

Crude Oil Price Evolu7on Brent ($/barrel)

Source: Bunkerworld

“2012: record of annual average price of crude oil”

27 Nov: 634 $/t 27 Nov: 986 $/t Heavy Fuel Oil Marine Gas Oil

Year Average HFO price Average MGO price MGO/HFO

2010 461 716 +55%

2011 632 978 +55%

2012 658 1003 +53%

Distillates about 55% more expensive than HFO

The ECA regulatory dilemma (source: DNV)

Dis/llates? Scrubbers? LNG as bunker?

LNG environmental advantages

LNG / Oil prices In 2012, energy from HFO is 48% more expensive than from LNG

0

2

4

6

8

10

12

14

16

18

20 $/MMBtu

European LNG imports

HFO Gibraltar

LNG / Oil prices Forecast future evolu7on (DNV study)

?

LNG / Oil import prices Scenarios considered at DMA study

MGO price/HFO price between 1.6 and 2.2

LNG price/HFO price between 0.5 and 0.9 LNG price/MGO price between 0.36 and 0.65

LNG / MGO prices (delivered on board) Scenarios considered at DMA study

Including es7mated distribu7on costs: LNG price on board expected to be between 0,40 and 0,84 of MGO price

MGO/LNG

0,55

0,69

0,84

0,40

0,50

0,61

LNG drawbaks Larger bunker storage on-‐board space: double for LNG than for HFO, triple space in case of dual fuel.

Higher investment cost for newbuildings (10 %to 20%, possibly lower in the future).

Higher maintenance costs (some studies say about 20%).

Trade restric7ons depending on availability of bunkering infrastructure.

Second hand ship market value (?)

Time being, lack of binding IMO regula7on (to be solved soon)

LNG drawbaks Higher investment costs AddiDonal costs for a newbuilding:

Fuel storage tanks Gas engine Safety systems

Approval Building costs differenDal:

Marintek: Ro-‐Pax 35,000 GT: +10%

Is universal conversion feasible?

Technically surely YES

Economically, indeed NO, depending on:

Ship’s age (remaining operaDng life up to recycling)

Trade (% Dme in ECAs)

Ship type, bunker costs share in total costs (funcDon of speed)

Retrofiing Main technical elements

Engine change or adapta7on: Easier and less expensive in ships with ME (electronic controlled) engines

LNG storage on board: Two main opDons: inside hull or on deck.

Vaccum/perlite insulated tanks at about 10 bar.

greenship.org ECA retrofit study

Large consorDum: Maersk, DSA, Man, LRS, DNV, etc.

2 retrofit soluDons compared: scrubber and LNG 2 scenarios: 2015-‐2019 and 2020-‐2024 Ship analyzed: 38,500 dwt products tanker

greenship.org ECA retrofit study

Conclusions: Investment cost of the LNG soluDon: 7.56 mUSD (including 40 days off-‐hire: 0.68 mUSD)

LNG soluDon 1.7 mUSD more expensive than scrubber

LNG soluDon payback period of 3 years for 100% operaDon in ECA

Investment costs

Payback 7mes

Retrofiing First Experience (2011) Bit Viking: 25.000 dwt product tanker

Retrofiing First Experience (2011) Bit Viking: 25.000 dwt product tanker Conversion of 2 engines from Wärsilä 46 to Wärsilä 50 DF (dual) with 2 x 5700 kW at 500 rpm

Wärtsilä’s new LNGPac onboard storage system: 2 x 500 m3 C type (cilindrical presurized) storage tanks at 9 bar isolated by perlite/ vacuum, mounted on the deck, 400 t each tank (full). 33 x 7,5 m

Bunkering LNG rate: 430 m3 / hour (less than 2,5 h). Sufficient for 12 days of autonomous operaDon at 80 % load, with the opDon of switching to MGO if an extended range is required.

When in EU ports (0.1 % sulphur limit), the vessel operates on gas. Retrofinng duraDon: 6 weeks.

Retrofiing First Experience (2011) Bit Viking: 25.000 dwt product tanker

Retrofiing First Experience (2011) Bit Viking: 25.000 dwt product tanker

LNG Storage on board (source Wärtsilä)

Retrofiing, a Spanish proyect by BALEARIA and COTENAVAL Fast ferries, monohull and catamaran.

Speed between 32 and 40 knots.

81 m – 4305 GT – 17280 kW 83 m – 2616 GT – 14800 kW

82 m – 5517 GT – 6500 kW 81 m – 4305 GT – 17280 kW

Retrofiing, a Spanish experiencie by BALEARIA and COTENAVAL

Shipping company Engineering company

www.balearia.com www.cotenaval.es

LNG Bunkering supply infrastructure 4 possibili7es Based on Danish MariDme AdministraDon study

STS

TPS TTS

LNG Bunkering supply infrastructure 4 possibili7es Based on Danish MariDme AdministraDon study

Possible infrastructure arrangement Source: Danish MariDme AdministraDon study

Possible infrastructure arrangement Small LNG feeder tanker loading in large terminal

LNG Bunkering supply infrastructure Bunkering barge (source Wärsilä)

Possible infrastructure arrangement Source: Danish MariDme AdministraDon study

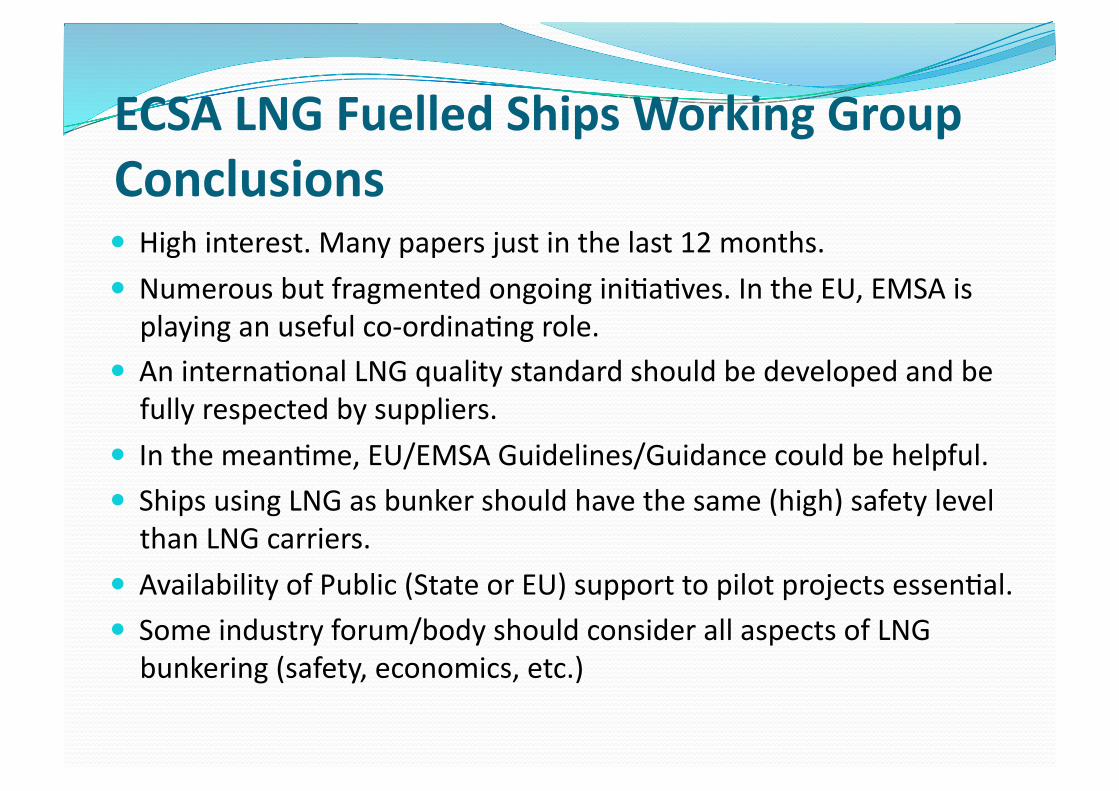

ECSA LNG Fuelled Ships Working Group Conclusions High interest. Many papers just in the last 12 months.

Numerous but fragmented ongoing iniDaDves. In the EU, EMSA is playing an useful co-‐ordinaDng role.

An internaDonal LNG quality standard should be developed and be fully respected by suppliers.

In the meanDme, EU/EMSA Guidelines/Guidance could be helpful.

Ships using LNG as bunker should have the same (high) safety level than LNG carriers.

Availability of Public (State or EU) support to pilot projects essenDal. Some industry forum/body should consider all aspects of LNG bunkering (safety, economics, etc.)

Conclusions Environmental aspects LNG has significant environmental advantages with regard to: NOx: 80% lower emissions

SOx: Virtually no emissions PM: Virtually no emissions CO2: 25% lower emissions

All basic technology elements necessary for engine conversion and for on board storing are available and proved.

First key-‐in-‐hand on-‐board storing solu7ons already available. Safety:

Normally no higher risk with LNG. IMO specific regulaDons are s7ll under way.

Some safety procedures for bunkering operaDons are sDll to be developed.

Retrofiing:

Technically viable in most cases. Easier and less expensive in ships with ME engines

Conclusions Technical aspects

Conclusions Economic aspects The LNG soluDon is very aTracDve for newbuildings in medium/ long term.

A high % of operaDon inside ECA is key But retrofinng can also be economically aTracDve in some special cases (e.g. high speed craps).

Conclusions Infrastructure development • Partnerships (shipowner, LNG and equipment suppliers, port) are key for development of LNG supply infrastructure.

• Bunkering infrastructure developing should start based on regular services operaDng 100% in ECAs.

• SSS and Motorways of the Sea lines could be the starDng point.

• Possible use of EU TEN-‐T funds for developing the bunkering net?

Co-‐opera7on is essen7al

Port

Authority

LNG

supplier

Shipping Co.

Equipment supplier

Conclusions, DNV Study

For 2020, about 1,000 ships will be fuelled by pure LNG or dual LNG/HFO

About 10/15% of expected newbuildings

Thank you

ECSA