LINK Global Holdings Financing 2013 PPT

11

Mark Dagel President and Co-Chairman Link Global Holdings, LLC FINANCING STRATEGIES

-

Upload

markdagel -

Category

Economy & Finance

-

view

688 -

download

0

Transcript of LINK Global Holdings Financing 2013 PPT

Mark Dagel

President and Co-Chairman

Link Global Holdings, LLC

FINANCING STRATEGIES

ALTERNATE CAPITAL SOURCE: PROJECT FINANCE

• Many companies are looking for secure financing options that can maximize returns & not tie-up liquidity.

• Project Finance can provide an alternate capital source for both public and private companies looking for construction financing. Debt provided for project development solely based on the

project’s perceived risks & expected cash flows

Debt providers have either no recourse or limited recourse to the parent company that develops or “sponsors” a project

ALTERNATE CAPITAL SOURCE: PROJECT FINANCE

Equity Investors

Debt Providers

Project Level Equity

InvestorsSponsors

Project Company (Borrower)

Off-take Agreements

O & M AgreementEPC Contract

Technology License

Agreements

Feedstock Agreements

BONDS AND PROJECT FINANCE

• Along with equity, traditional sources of capital for project finance include bank loans & personal investment.

• Market problems have led developers to seek new sources of capital for project finance.

• Bonds can either be a sole source of debt, or a complement to bank debt and offer structured advantages such as longer tenor, lower interest rate, and flexible amortization schedules that improve equity returns.

BOND CREDIT ENHANCEMENT MECHANISMS

• Currently, many projects reviewed by the rating agencies find themselves well below the investment grade threshold due to factors such as technology risk, scale-up risk, or feedstock risk.

• There are several credit enhancement mechanisms that can be employed to help mitigate these risks and allow the bonds to be priced at a more reasonable interest rate level.

• Third Party Insurance Highly tailored technology warranties that are able to support a

bond funded project financing. These third party insurers have both the technical expertise & balance sheet savvy to offer investment grade offerings. consider investment grade have begun offerings.

State and Local Governments Credit Enhancement Government support can range from accelerated permitting to

financial backing in the form of guaranteeing the debt through a “Moral Obligation”

BANK VS BOND MARKETIssue Banks Bonds

Large transactions Syndicators Access to incremental pool of investor Capital

Complex transactions Prefer “cookie cutter” deals Good for “story” credits in emerging markets

Timing Slow (9-12 months) Fast (4-6 months)

Cost Expensive Cheaper

Technology risk Less likely to accept Ability to mitigate some tech. risk and accept residual

Construction Risk Will assume with proper controls (IE) Will assume with “Bank like” controls

Capitalization interest None Raised at Financial/Transaction close

Drawdown's Timed to construction schedule Disbursed at closing (negative carry in steep curve environment)

Tenor Shorter (5-7 years) Longer (15-25 years)

Interest rate Higher/Floating Lower/Fixed rate

Covenants More restrictive Less restrictive

Amortization Usually straight line or mortgage style Flexible-can be sculptured to match cash flow and meet ratios

Cash sweeps Customary Not Customary

Prepayment Customary Make whole provisions (call premium)

BOND CREDIT ENHANCEMENT MECHANISMS(CONT’D)

• Export Finance Agency Loan Guarantees

• Most OECD member countries have an export finance agency whose goal is to support the export sales of goods and services from their country

• The majority have project finance programs that can guarantee loans. Many have a policy of supporting alterative energy and sustainability

• The amount of the loan guarantee from an export finance agency is based on percentage of domestic content (either goods or services) to be exported to a foreign buyer

• A loan guarantee becomes a 100% unconditional repayment obligation of the export finance agency whose credit rating is equivalent to its national governments credit rating

• Export finance agency financing require goods and services to move across borders

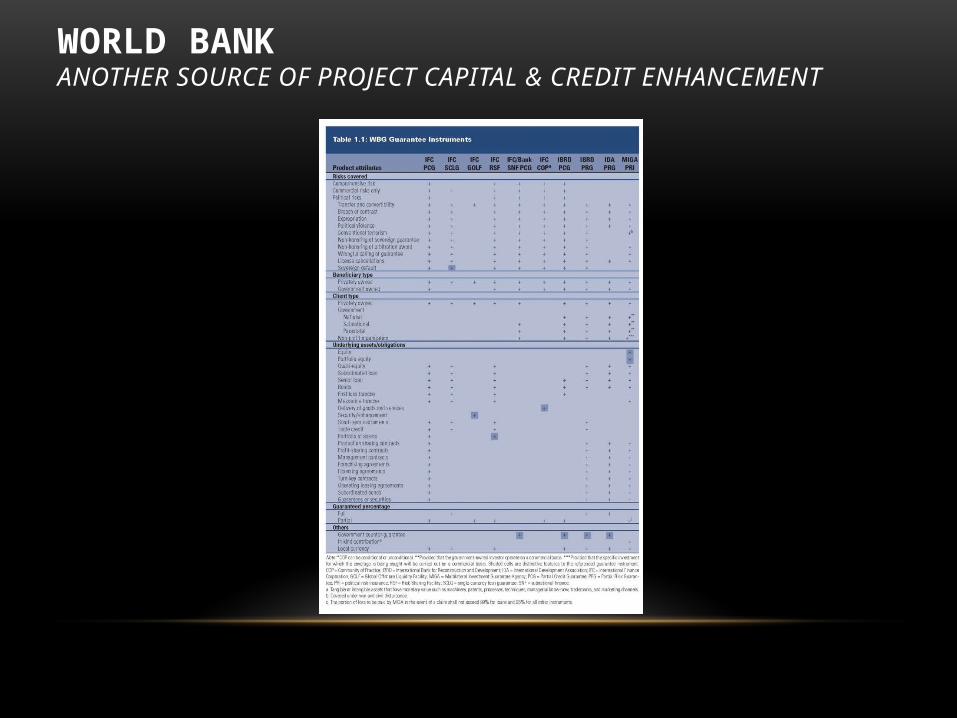

WORLD BANKANOTHER SOURCE OF PROJECT CAPITAL & CREDIT ENHANCEMENT

LINK GLOBAL HOLDINGS ACTIVITIES CHART

LINK GLOBAL HOLDINGS, LLC ACTIVITIES

CONTACT PAGELink Global Holdings, LLC Offices and Members Xcell Security House and Finance S.AAvenue de Béthusy 41005 Lausanne, SwitzerlandPhone : +41 21 312 57 07Fax : +41 21 312 57 15Attn: Lynnwood Farr Mark Richard Dagel Co- Chairman and PresidentLink Global Holdings, LLCDirect: 404-402-6761Fax: 888-909-4802Skype: MRDLink Conference line: 218-844-8230 (903784#) Offices: Lausanne, New York, Mexico, Dubai, Colombia, London, Atlanta Finance-Structure-Operations [email protected] Chairman of the Private Sector Committee Intergovernmental Renewable Energy Organizationwww.ireoigo.orgSpecial Adviser to Founder and CEO Pacific Rim Business Council (PRBC)www.aibc.us.com

Dr. Rand Neveloff, J.D., MBA, PhDCo-Chairman and CEOLINK Global GroupMobile: (646) 465-1692E-Mail: [email protected] of the Permanent Advisory Committee www.ireoigo.org Carl Williamson, J.D. Managing Director LINK Global Group Mobile: (919) 522-7063 E-Mail: [email protected] of the Permanent Advisory CommitteeIGO for Renewable Energywww.ireoigo.org