Liberalisation and competition in the European regional...

37

Liberalisation and competition in the European regional rail market. Page 1 Liberalisation and competition in the European regional rail market June 2013

Transcript of Liberalisation and competition in the European regional...

Liberalisation and competition in the European regional rail market. Page 1

Liberalisation and competition in

the European regional rail market

June 2013

Liberalisation and competition in the European regional rail market. Page 2

Executive Summary ............................................................................................................................. 3

1 Introduction .................................................................................................................................... 4

2 Arriva .............................................................................................................................................. 7

2.1 Arriva’s experience in European rail passenger markets............................................... 8

2.1.1 Denmark ........................................................................................................................ 8

2.1.2 Netherlands ................................................................................................................... 9

2.1.3 Portugal ........................................................................................................................ 10

2.1.4 Poland .......................................................................................................................... 11

3 Stakeholder needs ..................................................................................................................... 13

3.1 Challenges that Transport Authorities face .................................................................... 13

3.2 Why tender rail services? .................................................................................................. 14

3.3 Gross cost or Net cost contracts ...................................................................................... 16

3.4 Output based specifications.............................................................................................. 17

3.5 Bidding Arrangements ....................................................................................................... 17

3.6 Key Features of Best Practice Concession Contracts .................................................. 20

4 Preconditions for a successful competition ............................................................................ 21

4.1 Geographical perimeter (Size, Scope and Length of Concession) ............................ 21

4.2 Rolling Stock ....................................................................................................................... 22

4.3 Stations ................................................................................................................................ 23

4.4 Maintenance Workshops ................................................................................................... 23

4.5 Staff ...................................................................................................................................... 24

4.6 Performance Regimes ....................................................................................................... 25

5 Conclusion ................................................................................................................................... 26

Appendices ...................................................................................................................................... 27

Case studies of market liberalisation in Europe (UK, Germany, Sweden) ............................ 27

a) The UK experience (fully franchised since 1997) .............................................................. 27

b) The German Experience (since 1996) ................................................................................ 29

c) The Swedish Experience (since 2000) ............................................................................... 30

Annexe ............................................................................................................................................. 33

A possible route-map for a liberalised rail market in France by 2019 .................................... 33

Liberalisation and competition in the European regional rail market. Page 3

Executive Summary

Arriva is one of the largest and most successful transport services organisations in Europe

operating in 15 countries.

With rail passenger operations in 7 European countries Arriva has unrivalled experience of

the various passenger rail tendering models both in mature and emerging markets.

Effective rail passenger services are vitally important to socio-economic development and

growth and have a low environmental impact compared with other forms of transport.

Rail generates 403 billion passenger kilometres per annum but in overall terms its market of

passenger transport has stagnated and declined.

A European Commission Staff Working Document concluded that the fully liberalised rail

passenger markets of Sweden and the UK had improved more than other less liberalised

markets when considering a range of 10 key indicators.

European institutions are currently proposing the further liberalisation of rail markets.

Competitive tendering has delivered cost savings of typically 20% to 30%, increased

investment and improved service quality resulting in increased market share through better

customer orientation, better quality and performance and controlled costs through improved

efficiency.

Tendering Authorities retain control of key aspects of policy objectives through the tender

design.

Governments and Transport Authorities face a number of challenges with direct award

and tendering can allocate risks to the party best capable to manage them.

There are 3 types of contract each reflecting differing risk/reward characteristics.

It is absolutely necessary for processes and conditions to be totally transparent and equitable.

Effective design of the contract/concession is key to a successful outcome and there are a

significant number of relatively complex and interrelated aspects to be taken into account.

Adequate time needs to be provided for design, bidding and commissioning phases.

Evidence from throughout Europe shows that carefully conceived and implemented route

tendering can generate investment, significantly reduce subsidy requirements, improve

service quality and attract new passengers.

Arriva has successfully contributed to the opening of a number of Europe’s rail passenger

markets.

Arriva would be delighted to utilise this experience and to explore how a tendering model

could be developed to optimise delivery of Authorities’ financial and other objectives in new

markets.

Arriva is willing to consider working in partnership to establish pilot projects.

Liberalisation and competition in the European regional rail market. Page 4

1 Introduction

Effective rail passenger services are vitally

important to socio-economic development and

growth. They provide a sustainable, eco-friendly

and inclusive means of mobility giving access to

business, commerce, employment, social and

welfare needs. They impact our lives at a local,

regional, national and international level.

From an environmental perspective, rail (both

freight and passenger) has a relatively low

environmental impact compared with other forms of transport. Indeed within the EU it is the most

efficient producing only 0.6% of both Green House Gas and CO2 emissions when compared with

other modes (source: Eurostat). Modal shift to rail can further increase these advantages, and

produce major benefits for society and the environment.

Yet within the EU, whilst rail generates a staggering 403 billion passenger kilometres per annum, this

represents only some 7.0% of all land passenger transport kilometres and in overall terms its market

share in comparison with all other modes of passenger transport has stagnated and marginally

declined since the mid 1990’s (source Eurostat).

Economic cycles, growth of private transport, historical lack of investment and poor productivity have

certainly contributed to this situation and stakeholders need to address these issues in order to make

rail more competitive and the “first choice” of the consumer- the passenger.

A recent publication by the European

Commission, Staff working Document

(2013), Part 3, Impact Assessment (which

supported proposals for the opening of the

market for domestic passenger transport

services by rail) concluded that the fully

liberalised markets of Sweden and the UK

had improved more than less liberalised

markets when considering a full range of 10

key indicators. Furthermore, when

benchmarked on a range of

satisfaction/quality and efficiency indicators, the liberalised and mainly liberalised markets (which

include Germany) scored significantly higher than the other classifications of markets in all main

respects.

Liberalisation and competition in the European regional rail market. Page 5

However, the rail passenger sector is confronted with substantial challenges over the next decade

and to address these, the European Commission is proposing further widespread liberalisation of rail

markets.

Where competitive tendering for the procurement of Regional and Urban passenger rail

networks is established in such countries as Germany, the UK and Sweden it has delivered

better value for money, investment and improved service quality leading to:

Increase public transport market share through better customer orientation, better quality and

performance

Controlled costs through increased efficiency and reactivity.

Specific examples show that:

In Germany, Europe’s largest competitive rail transport market in terms of train kilometres,

approximately 32% of the annual volume of 629 million train kilometres per year was put out

to public tender by the end of 2008. The previously high subsidies were thereby reduced

by an average of 26 per cent enabling authorities to increase the amount of train kilometres

offered to passengers;

In the UK, successive reviews of franchising in have concluded that the franchising system

has helped deliver better services, more passengers and lower subsidies than would

have been possible under British Rail, and;

In Sweden passenger transport authorities systematically use competitive tendering for rail

PSCs, although they are not required to do so. This demonstrates that there are clear

benefits from the competitive process.

Liberalisation of markets together with competitive tendering has

demonstrably led to:

•the development of services, in terms of both quality (passenger

comfort, on board services, punctuality, reliability) and volume;

•High levels of safety and security;

•A stimulus to innovation and thereby organic growth of services;

•Customer-orientated strategy leading to rail market share increase (e.g. improved information,

service frequency, intra-modal and inter-modal integration); and,

•Transparency of contractual relations between rail undertakings and authorities.

Liberalisation and competition in the European regional rail market. Page 6

With rail passenger operations in 7 European countries Arriva has unrivalled experience of the

various passenger rail tendering models that have been adopted in Europe and operate both in

mature and emerging markets. Additionally, as part of the Deutsche Bahn Group we have access to

their extensive knowledge, experience and resources. In this paper we share some of our

experiences and set out what we consider are the key elements of a successful rail passenger tender

model.

Liberalisation and competition in the European regional rail market. Page 7

2 Arriva

Arriva is one of the largest and most successful transport

services organisations in Europe with almost 56,000 employees

operating almost 19,900 buses and more than 750 trains (as well

as metros, trams, funiculars, waterbuses and paramedic

transport) in 15 European countries to carry more than 1.5Bn

passengers each year. Our scale and expertise mean that we

can operate a range of transport modes across our business, in

a variety of markets.

We are currently active in the following countries:

Croatia- 260 employees, 120 buses

Czech Republic- 3,000 employees, 1,860 buses, 4

trains

Denmark- 4,095 employees, 1,220 buses, 43 trains,

3 waterbuses

Italy- 3,340 employees, 2,320 buses, 6 trams,

2 waterbuses

Hungary- 945 employees, 405 buses

Malta- 1,120 employees, 285 buses

Netherlands- 2,955 employees, 880 buses, 99 trains, 10 waterbuses

Poland- 1,965 employees, 845 buses, 27 trains

Portugal- 7,015 employees, 3,400 buses, 18 trains, 126 trams

Serbia- 580 employees, 250 buses

Slovakia- 1,560 employees, 840 buses

Slovenia- 520 employees, 275 buses

Spain- 900 employees, 480 buses

Sweden- 3,095 employees, 920 buses, 165 trains, 37 trams

UK- 24,550 employees, 5,800 buses, 403 trains, 375 ambulances/cars

Liberalisation and competition in the European regional rail market. Page 8

2.1 Arriva’s experience in European rail passenger markets

Arriva operates rail passenger services in 7 European countries; these are:

Czech Republic

Denmark

The Netherlands

Portugal

Poland

Sweden

United Kingdom.

We also operated rail passenger services in Germany (until 2010).

Four of our rail passenger operations are described below and more detailed case studies can be

found within the Appendices.

2.1.1 Denmark

2.1.1.1 Rail market

The Danish rail market is regulated, having opened to public tendering in 2000. The Danish

parliament is responsible for the regulatory framework for transport provision and setting fares.

Contracts are typically net cost, with bonus and/or penalty regimes for punctuality and customer

satisfaction.

The market is dominated by the public sector, with Danish State Railways operating approximately 75

per cent of train kilometres in Denmark, under direct award from the Ministry for Transport.

2.1.1.2 Arriva in Denmark

In 2001 Arriva won the first competitive tender in Denmark for approximately 7.5m train km per annum

covering diesel operations in mid Jutland. This was a net

cost contract for 7 years (from 2003) including commercial

activities at stations. The specification was framed to give

bidders the opportunity to develop timetables that would

both grow the market and reduce costs. The state

incumbent was required to lease the existing fleet to other

bidders on non-discriminatory terms and key staff would

transfer to the new concession. The Arriva solution was

extremely resource efficient, included replacement of two-thirds of the fleet (29 trains) with new

Alstom Lints, and targeted investment in station improvements and other quality initiatives despite

saving the client body €11m a year. Increased frequency, shorter journey-times, better connections

and better quality (Arriva Tog services were repeatedly top of the national performance league with

very high levels of customer satisfaction) reversed the long-term decline in patronage on these routes

and generated a 15% growth in passengers during the contract period.

Liberalisation and competition in the European regional rail market. Page 9

The tender process for franchise replacement started in 2008. The tender was for 8 years (with an

optional 2-year extension) and the process was broadly similar to the previous one but with the

service specification and bid evaluation criteria (50% price, 30% quality and 20% deliverability) more

clearly expressed and detail alterations to the draft contract. Five expressions of interest were

received and three of these were shortlisted to prepare full bids. The result was that the service was

again awarded to Arriva with an offer that included renewing the remainder of the fleet, further

timetable enhancements and significant investment. The Trafikstyrelsen (client body) announcement

stated that the contract would further reduce the subsidy requirement by 10% (€20m) annually and

the independent panel assembled to confirm the award recorded that the successful offer was some

15% cheaper than that submitted by the incumbent (in association with First Group) and had the best

quality rating.

The service continues to operate with excellent standards of reliability and customer satisfaction.

2.1.2 Netherlands

2.1.2.1 Rail market

Very little of the rail market has been competitively tendered to date and only around six per cent of

the market is operated by the private sector.

Regional authorities have responsibility for regional rail services. Contract conditions differ widely

between the regions, and by contract.

Contracts are typically net cost and up to 15 years in length.

2.1.2.2 Arriva in Netherlands

The process of passenger rail liberalisation started in 1998 when responsibility for procurement of

local rail services was devolved to 19 Regional

Authorities and started to accelerate around 5 years

later encouraged by institutional reform and the

success of initial trial tenders.

Arriva was an early mover in the market winning

(through a joint venture with the state owned

incumbent) one of the trial net cost contracts to

operate 5.3m train km on rural lines in the Friesland

and Groningen Regions from 1995-2005. This was a

low investment concession (the existing fleet was retained) but the Arriva offer included some

timetable enhancements and a key focus was improving customer service and integration with other

public transport modes. It also delivered a modest cost saving to the client body.

When the service was re-tendered in 2004-5 for a longer 15-year period, Arriva (acting alone) won

with a bid that included significant timetable enhancements (to 7m train km), major investment

Liberalisation and competition in the European regional rail market. Page 10

(procurement of 43 new Stadler DMUs and construction of a train maintenance depot) while reducing

the subsidy requirement by almost 50%.

In 2006 Arriva won another small concession providing electric services between Dordrecht and

Geldermaisen. This is a 12-year net cost contract of 1.4m train km for which a fleet of 10 new trains

were procured.

Three further contracts (5 lines) have now been won some of these commenced operations in

December 2012 and the remainder will start in December 2013. A total of 38 new diesel and electric

multiple units have been purchased for these services.

So far only around 15% of the Dutch network has been tendered but the results have been impressive

in terms of new investment, service enhancements and reduced subsidy (typically by around 25%).

Most concessions are net cost (providing a real incentive to grow the patronage) and of sufficient

duration (10-15 years) that depot investment can be justified and rolling-stock residual value does not

add too significantly to costs. On the negative side though, some tenders are for just a single route –

often less than a million train km and requiring just a handful of trains. The mobilisation and start-up

costs can therefore be disproportionately significant. Furthermore some regions lay down very tightly

defined specifications which can stifle timetable and resource efficiency improvements.

2.1.3 Portugal

2.1.3.1 Rail market

There has been only one instance of a concession awarded to a private operating company to date

(Fertagus), but there are now signs of moves towards more widespread competitive tendering.

Urban and regional rail services are operated under concessions allocated by the state, to state-

owned Comboios de Portugal (CP). State funding provides for loss-making regional and urban

services

2.1.3.2 Arriva in Portugal

Through a substantial shareholding in Barraquiero

Group, Arriva has an interest in Fertagus, the only

heavy rail network to have been tendered in

Portugal. This very busy route linking suburbs south

of Lisbon with the city centre is 54km in length and

2.2m train km per annum are operated using a fleet

of 18 4-car double-deck trains that are leased

(heavy maintenance included) from the client body.

It is a net cost contract with some freedom to vary

service levels and fares and, under a contract extension agreement covering the period December

2010 to 2019, now operates without public subsidy.

Liberalisation and competition in the European regional rail market. Page 11

Barraquiero Group are also part of the consortium that won the Design, Build, Operate and Maintain

contract for the Metro sul do Tejo (also south of Lisbon). It is a 30-year concession that commenced

in 2002.

Both Arriva and Barraquiero Group are also in the consortium that holds the Metro do Porto

concession. It is a 5-year gross cost contract from 2010 that covers both maintenance (infrastructure

and trains) and operation of this 54km network of light rail (underground in the city centre) and tram

services. There are 5 lines with 70 stations and the fleet comprises 102 Light Rapid Transit units.

Contract evaluation criteria were 80% price and 20% technical quality and it is understood that the

client saved around €10m pa (over 20%) through the tender.

2.1.4 Poland

2.1.4.1 Rail market

The rail market in Poland is dominated by state and region-owned operators, however it is opening

slowly to competitive tendering.

Regional rail provision has been devolved to the regions, while state-owned PKP remains responsible

for Inter-City and long-distance rail operations.

Przewozy Regionalne (PR) is owned by the 16 Voivodships (provinces), which decide whether to

direct award rail services to PR or put services out to tender in their regions.

Contracts are typically net cost contracts. Where previously they were between one and three years,

there has been a recent move, in some regions, towards longer 10-year contracts.

2.1.4.2 Arriva in Poland

In 2007 Arriva (through a joint venture with a freight operator) became the first private passenger rail

operator in Poland by winning a tender in Kujawsko Pomorskie Region for 1.75m train km per annum

around Bydgoszcz and Torun. It was a short net cost concession and while the client provided 13

modern diesel units, the rest of the fleet had to be provided by the bidder. There was considerable

flexibility to design a new resource efficient timetable with improved connections but no staff would

transfer to the new operator and new train maintenance facilities had to be provided – all during a six-

month mobilisation. Tender evaluation criteria were price (70%) and committed reliability (30%).

The client body published the results of the tender and the Arriva offer was PLN 12.93 per train km

with 90.5% punctuality while the incumbent offered PLN 18.36 per train km with 95% performance. In

actual fact the real saving to the Marshall was greater than the 30% suggested by these figures since,

according to press reports the lowest figure that had been quoted in negotiations for direct award had

been over PLN 20. Although not evaluated by the client, our bid also included timetable

improvements, the introduction of two new and 6 second-hand but refurbished trains from Denmark

and customer service benefits.

Liberalisation and competition in the European regional rail market. Page 12

After some initial problems the concession

delivered better reliability than contracted, not

least because we were able to improve the

reliability and daily availability of the Marshall’s

owned fleet by over 30% compared with that

which had been achieved by the incumbent. We

were also able to win some small add-on routes

bringing the annual train km to 2.5m

When the network was re-tendered in 2010

under broadly similar conditions but with the concession period extended to 10 years the Arriva offer

was PLN 17.99 per train km with 91.17% punctuality and the incumbent’s offer was PLN 35.48 with

90% performance guarantee. The Arriva winning bid also included replacing the 2nd

-hand trains with

new ones (to provide a 100% modern low-floor fleet) and further customer service benefits.

Other concessions have been offered in Poland but generally these have been too short – often just

1-2 years (the current legal framework only allows contracts with a maximum duration of 3-years in

most cases) and with inadequate bidding and mobilisation time so Arriva has been unable to bid and

other private operators have not yet entered the market.

Liberalisation and competition in the European regional rail market. Page 13

3 Stakeholder needs

The main driver of tender design will always be the policy objectives of the client body.

Within the EU regulatory framework client bodies remain free (if they so wish) to:

establish social and qualitative criteria;

determine fares policy and tariffs;

define the public service obligations and the geographical areas

concerned;

establish the parameters on the basis of which the compensation

payment, if any, is to be calculated, and the nature and extent of any

exclusive rights granted;

determine the arrangements for the allocation of costs connected with

the provision of services;

define levels of information, coordination and ticketing integration with

other transport modes and operators.

However, it should be remembered that the more prescriptive a tender is, the less flexibility

there will be to capture the operator’s innovative and entrepreneurial skills.

Whereas a national client body will generally wish to adopt a single model across the whole country

and be keen to attract private investment for new trains and other facilities, a Regional Authority will

more often want a bespoke structure that delivers on local objectives – be these releasing funds for

other essential projects, visibly improved quality, or delivering on challenging modal-change and

environmental targets. Again though access to “off the Public Accounts” investment is likely to be

attractive.

3.1 Challenges that Transport Authorities face

Increasingly, Governments and Transport Authorities face a number of challenges with direct

award for the procurement of public transport, these include:

Pressure on scarce financial resources;

Capital tied up in fleet, property and other assets;

Significant future capital investment requirements;

Historic conditions may make operational efficiencies difficult to achieve;

Significant liabilities may apply;

Employee guarantees;

Historic concessions may not represent value for money or allow improved quality;

Revenue risk may lay with the client body;

Transport is always a political and social issue;

Tough budgets may force difficult choice;

Achievement of multi-modal solutions; and,

Growing customer expectations.

Liberalisation and competition in the European regional rail market. Page 14

3.2 Why tender rail services?

The driving-force behind the move to competitive tendering of services has generally been the wish of

client bodies (whether National or Regional) to achieve some or all of:

Reduction in the (perceived to be un-justifiably high) subsidy requirement for Regional and

Suburban rail services and delivery of better value-for-money;

Through competition to force the incumbent operator to improve efficiency to the levels achieved

by “best in class” operators elsewhere in Europe;

An end to annual (and possibly difficult…)

renegotiation of service levels and subsidy

requirements;

Transfer of cost (and, more often than not, revenue)

forecasting, management and delivery risks from the

client to a third-party;

Innovation and the development of new cost-effective

services/products;

Improved service delivery (punctuality and other quality attributes) and more effective marketing

to deliver growth in patronage; and finally,

Unlocking timely and effective private-sector investment (e.g. new trains and maintenance

facilities, station car parks and passenger service facilities, ease of bus/metro/bike/pedestrian

interchange, marketing and employee development, environmental protection etc.).

The extent to which each of these is delivered will depend critically on the detailed design of the

tendering process and the nature of the client specification. Nevertheless there is overwhelming

evidence that where the tender structure is well thought through and appropriate, and where risks and

rewards are sensibly allocated to the contracting parties, competition through tendering does deliver

substantial benefits.

The exhaustive research, previously referred to, which was undertaken on behalf of the European

Commission shows clearly that route and network tendering really does deliver these benefits and

more. Specific findings included:

Higher absolute and evolving levels of productivity and efficiency in liberalised markets with

tendering typically delivering a 20-30% cost reduction along with higher levels of passenger

growth;

Significantly higher satisfaction and quality of service

(e.g. punctuality) indicators in liberalised markets. Also

higher growth in the level of services offered (measured

by train km) and patronage (normalised passenger km);

Higher service frequency;

Greater growth in the number of staff employed and

some evidence that employment conditions (principally salaries) are better;

Liberalisation and competition in the European regional rail market. Page 15

Liberalised markets typically have the highest safety standards (but, quite rightly, no causal link

is claimed).

The study concluded that

“Evidence of competition for PSCs in Germany, Sweden and the Netherlands has shown

that tendering accrues savings for Client Authorities, sometimes up to 20-30%, which can

be re-invested to improve services or be used elsewhere. Experience in other liberalised

markets such as Sweden and the UK has shown improvements in quality and availability

of services with passenger satisfaction rising year on year and passenger growth of over

50% over ten years. Improved services would bring clear benefits to passengers and

savings of some €30-40bn to taxpayers if competitive tendering was extended across the

whole of the EU”.

The finding that staff numbers (and pay) have grown faster in liberalised markets than in closed ones

is, perhaps, at first sight surprising. Private operators win concessions through their constant pursuit

of resource efficiency as demonstrated by the table below, which compares the staff numbers per

million train km of the main operators in Poland:

Carrier Annual Train km

(million)

Number of

employees

Staff per million

train km

Arriva RP 2.4 200* 83

Koleje Śląskie** 3.0 320 107

Koleje Mazowieckie 16.5 2,600 158

Przewozy Regionalne 70.0 12,900 184

* includes contractors

** half-year 2012

It is, however, the case that lower unit costs enable client bodies to affordably increase the level of

service leading to greater employment opportunities.

The European Commission report does not fully address the benefits of investment by private

operators but it should be noted that in the UK, for

example, subsidiaries of Arriva are investing to re-open

previously closed routes, to construct completely new lines

and to open new stations as well as spending massive

amounts to regenerate existing stations and improve

customer facilities. It is also worth noting that across the

whole of mainland Europe the average age of the Arriva

train fleet is just 10 years and that over three-quarters of

Liberalisation and competition in the European regional rail market. Page 16

the trains that we run have been built since 2000.

The report’s findings align closely with Arriva’s own experiences details of which may be found in the

case studies attached as appendices.

3.3 Gross cost or Net cost contracts

Historically there have been two main types of contracts- these are:

Gross cost contracts, of which the main features are:

Tendering authority pays an operator a specified sum to provide a specified service

Tendering authority keeps passenger revenue and often sets routes and vehicle specifications

Gross cost contracts may be considered easier to manage and, perhaps as a result of this, the

approach is often adopted by client bodies in markets that are in the early stages of liberalisation.

Such contracts can, however, end up being very inflexible (effectively the timetable is frozen) or very

complex with subsidy variations based on changes in vehicle km, vehicle hours and peak vehicle

requirement with separate rates for additional staff hours ordered and complex performance regimes.

Net cost contracts, of which the main features are:

The operator takes on revenue and cost risks

Operator keeps passenger revenue

Tendering authority can provide a contribution where cost of providing service would not be

commercially viable

In reality a net cost approach may be simpler to introduce and to manage and gives the operator a

strong incentive to meet the needs of end customers without recourse to complex performance

regimes. The key requirement for a net cost contract is a transparent revenue allocation system. This

does not necessarily need to be 100% accurate, merely to broadly reflect travel patterns and to

respond to changes in patronage.

Either approach is acceptable from a bidder’s perspective.

Hybrid solutions are also possible. In some Swedish and German gross cost contracts part of the

subsidy is based on the quantum of services provided but the remainder is related directly or indirectly

to passenger usage. Other contracts migrate from gross cost to net cost once a track record of

financial performance has been established after, for example, two years of operation.

Liberalisation and competition in the European regional rail market. Page 17

3.4 Output based specifications

By specifying the outputs required rather than the precise timetable to be operated client bodies can

create the freedom for bidders to develop more resource efficient (and, often, more customer friendly)

solutions. Such a specification will normally include the following parameters:

Time band for first and last trains;

Minimum frequency required at each station;

Regularity (e.g. strict clock-face, or every hour +/- 3 minutes)

Required connections

Capacity requirement

Permitted variations at weekends and on Public Holidays etc.

A fixed timetable leaves the bidder with few opportunities to either reduce costs or respond to

changing customer needs. In the UK, Denmark and elsewhere, flexibility in the service specification

has enabled operators such as Arriva to provide more capacity by running a more frequent service

at lower cost.

Similarly, issues of service quality above a minimum level defined in the ITT are better addressed

through the tender award criteria (typically 70% price and 30% quality, but this can be varied

according to the client body’s objectives) and bonus/malus regimes than through detailed

specification (e.g. specified ticket office opening hours, frequency of ticket checks etc.) in the ITT.

3.5 Bidding Arrangements

If a number of bidders are expected then a prequalification process is beneficial to shortlist those with

the best approach and qualifications.

These are major long-term contracts and bidders will need to fully understand the existing

performance together with the risks and opportunities before committing to an offer.

Liberalisation and competition in the European regional rail market. Page 18

Comprehensive bidding information should therefore be provided including extensive current and

time-trend data for the concession. At the very least this should include:

Passenger counts;

Passenger flow and ticketing sales/income data;

Performance (punctuality and reliability);

Details of known or expected future developments;

Details of any contracts and/or other obligations that will transfer to the new operator;

Copy of the draft concession contract;

If the existing fleet is to transfer and the operator is to be responsible for train maintenance then

maintenance schedules and detailed cost/contract data;

Employment conditions and summary personal record details for any staff that are expected to

transfer to the new concession.

The invitation to tender should also give a clear view of what the client-body is seeking to achieve

through the tender and the methodology that will be used to evaluate the offers received (the award

criteria.)

A simple process for clarification questions and answers should be laid down (normally with the

answers published to all shortlisted bidders) and also, to the extent appropriate, arrangements that

allow some meetings with the client body, site visits and meetings with existing management.

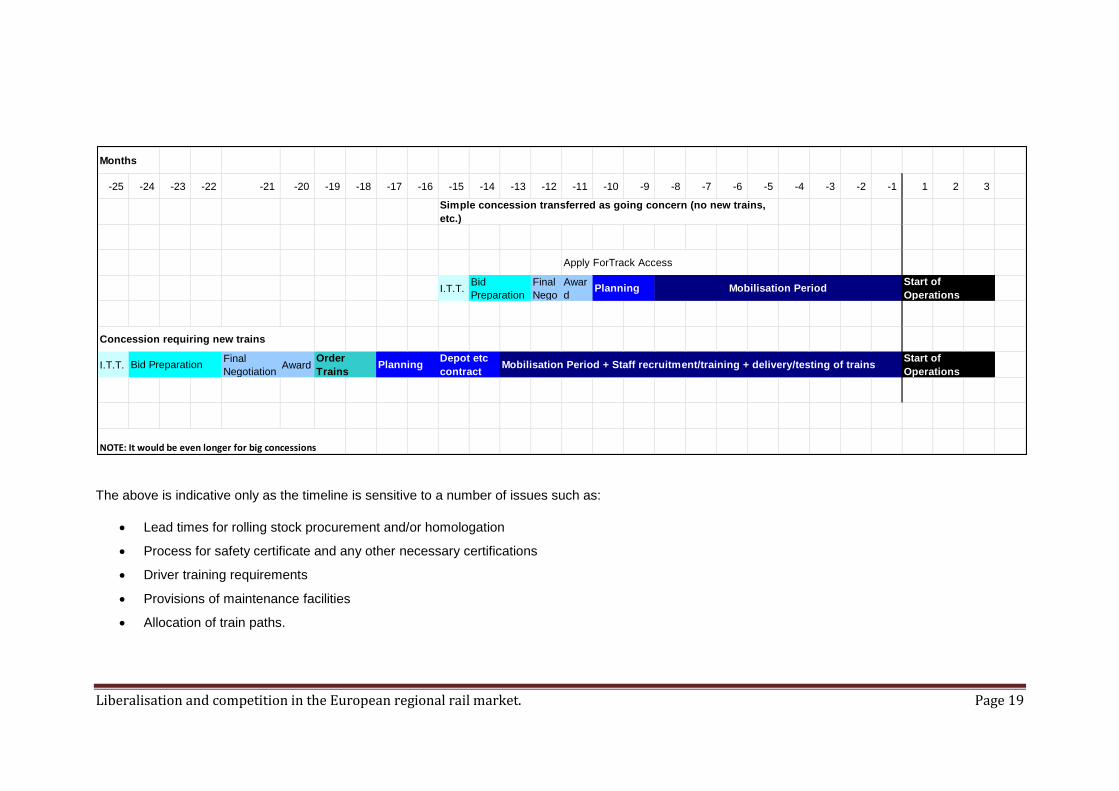

Bearing in mind the complexity of bid preparation and the fact that many bidders will have to obtain

Company Board approval of their offer, at least 3 months should be allowed for bid preparation and

adequate time will also be required for tender evaluation and award and for mobilisation. These

considerations mean that even for a modestly sized “transfer as a going concern” concession

the tender process should start perhaps 2 years before the proposed commencement of

operations. More complex concessions, especially those requiring construction of new trains

will typically require perhaps three years or even longer in extreme cases.

Liberalisation and competition in the European regional rail market. Page 19

The above is indicative only as the timeline is sensitive to a number of issues such as:

Lead times for rolling stock procurement and/or homologation

Process for safety certificate and any other necessary certifications

Driver training requirements

Provisions of maintenance facilities

Allocation of train paths.

-25 -24 -23 -22 -21 -20 -19 -18 -17 -16 -15 -14 -13 -12 -11 -10 -9 -8 -7 -6 -5 -4 -3 -2 -1 1 2 3

I.T.T.Final

Nego

Awar

d

I.T.T.Final

NegotiationAward

NOTE: It would be even longer for big concessions

Start of

Operations

Concession requiring new trains

Bid PreparationOrder

TrainsPlanning

Depot etc

contract

Start of

Operations

Mobilisation Period

Mobilisation Period + Staff recruitment/training + delivery/testing of trains

Months

Simple concession transferred as going concern (no new trains,

etc.)

Bid

PreparationPlanning

Apply ForTrack Access

Liberalisation and competition in the European regional rail market. Page 20

3.6 Key Features of Best Practice Concession Contracts

These can be summarised as being:

Financial and other risks allocated to the party best able to manage them;

Adequate indexation to cover inflation;

Focus on defined outputs and processes rather than a prescriptive list of inputs;

Periodic reporting requirements focussed on what is really necessary – avoidance of costly and

innovation stifling micro-management of concession activities;

Proportionate and graduated process to address contract infringements by either party;

Independent dispute resolution process;

Contract variation and client specification change process (usually best-endeavours to agree will

suffice).

It follows that an appropriately structured contract should provide the operator with enough

commercial freedom to apply innovative solutions and focus on the delivery of a quality service.

Liberalisation and competition in the European regional rail market. Page 21

4 Preconditions for a successful competition

4.1 Geographical perimeter (Size, Scope and Length of Concession)

The minimum size of concession that should be considered is around 15 trains and 1m+ train km. as

bidding and mobilisation costs will have a disproportionate impact on the price per km of anything

smaller than this.

If a significant number of new trains are required and/or existing staff do not transfer from the

incumbent then the maximum practical size is around 8-10m train km but even then only the largest

international players will be able to participate in a tender of this magnitude. A concession of 4-5m

train km is probably more realistic for effective competition.

If the concession transfers to the new operator as a “going concern” with the existing fleet and staff

(even if a new depot is required) then there is no real limit on the size of concession that can be

offered.

Whatever the number of train km it is generally beneficial (and costs will be

lower) if the selected routes form a “natural network” having proximity to a

depot and opportunities to inter-work trains and crews between routes to

optimise resource efficiency.

Ideally the concession holder should also be responsible for all customer-

facing activities including station operation and retailing (ticket sales), and

on-train customer service, revenue protection etc. This is particularly

beneficial in the case of net cost concessions as it enables the operator to

ensure consistent standards of customer service across the whole journey and to focus investment

and management attention on initiatives that have the greatest impact on the customer experience.

Regardless of who runs the stations, there need to be arrangements that ensure non-discriminatory

station access by any operator and provision of seamless, convenient and attractive services and

assistance to all passengers.

Experience has shown that for “transfer as going concerns” concessions requiring little or no

investment, duration as short as 5 years can generate attractive bids but even in these circumstances

better value will be achieved by a period of 7 years or longer. More generally though for concessions

with modest investment and staff recruitment/training requirements 7-10 years will be appropriate

whilst if significant fleet renewal is proposed 12-15 years should be the norm.

It is also common practice to provide for an extension (typically of 3 years) if the concession holder

delivers on franchise service delivery and quality commitments.

Liberalisation and competition in the European regional rail market. Page 22

The tendering authority needs to facilitate:

The availability to bidders of transparent, detailed and recent market and operational data

including passenger flows and ticket income, track and facility access charges etc. If existing staff

are expected to transfer to the new operator then employee details (numbers by function,

employment conditions, seniority etc.) also need to be provided.

A Clearly defined requirement specification (minimum level of service, minimum frequency etc.).

A precise time line for the expected bid/start of operation/mobilisation

A good level of flexibility especially on timetabling

Fair, open and transparent prequalification

Availability of all aspects of customer care service and information to passengers

Thus the optimal duration depends on the complexity, the risk/reward structure and the level of

investment.

4.2 Rolling Stock

There are a number of different models for the provision and

ownership of rolling stock. Normally the operator provides the rolling

stock but in some concessions, for example in Sweden, the rolling

stock is a concession asset owned by the client body and then

leased to the operator whilst in other cases the operator may be

required to take over existing fleets at an agreed value.

However, a key consideration is what the concession and client’s finances can sustain in terms of

new or second-hand rolling stock. Trains typically have a useful working life of around 30 years or

more so with appropriate refurbishment second-hand vehicles will often be the most customer-friendly

and cost effective solution, particularly in the case of short duration concessions.

If new rolling stock is a requirement the initial investment together with any residual value

considerations (possibly exacerbated by any non-standard features of the train specification) will

necessitate a long concession, typically of 12-15 years. Value for money can be further enhanced if

the client body commits to either “buying-back” the trains at the end of the concession or requiring the

next concession-holder to take-on the assets book value based on a predetermined formula.

Rolling stock procurement is one of the key dynamics determining the timeline for delivering a

concession.

Liberalisation and competition in the European regional rail market. Page 23

4.3 Stations

There is a preference, particularly in respect of regional rail concessions, for the train operator to

operate and manage the stations. Otherwise they are unable to manage (and upgrade) the “whole-

journey experience” to maximise patronage. There may also be significant cost-reduction benefits

from being able to develop station-trading etc. opportunities.

Where stations are served by a number of train operators it is normal practice for operator with the

largest number of departures to take the management role.

If stations are not included then access and other unavoidable facility charges should be determined

on a transparent and equitable basis and ideally be regulated.

4.4 Maintenance Workshops

It is desirable that train maintenance is included in the tender of the operations but the train operator

should have the commercial freedom to decide whether to undertake the work in-house or to

subcontract it.

For all except the smallest concessions – and even then

only if new trains are an absolute requirement - best-

value is achieved by transferring the existing staff, depots

and trains to the franchise.

Start-up costs (particularly construction of a maintenance

depot) are significant and will be reflected in the tender

prices. It is not sensible use of public money to pay for

construction of new buildings etc. when adequate facilities (that were originally subsidised by tax-

payers) already exist.

This will also reduce the lead-time between concession award and commencement of operation to the

minimum possible. Train procurement, recruitment and training of staff and building construction etc.

typically take a minimum of 18 months.

Where the facilities are provided by the incumbent operator these need to be provided on a

transparent and equitable basis.

For longer duration contracts Arriva is prepared to invest in building new facilities but the

infrastructure manager will have to facilitate connections from the depot site to the mainline.

If a new depot is required, an option is for the client body to offer suitable sites to all bidders, on non-

discriminatory terms, for them to develop.

Liberalisation and competition in the European regional rail market. Page 24

4.5 Staff

Staffing a concession is always a key issue and will be determined by whether the incoming operator

is required to employ new or existing personnel - or a combination of both.

In some countries, such as Germany, the existing employees do not transfer with their work to the

new concession and it is necessary to recruit and train new service delivery teams (drivers,

conductors etc.). Across Europe driver training typically takes between 6 and 12 months (3 months+

classroom and 3 months+ practical train handling and general/route familiarisation) so even if

adequate and accessible training facilities exist (which is not the case everywhere), this has very real

cost and timescale consequences for mobilisation and effectively puts a limit on the size of

concessions that can be tendered.

The largest tenders that have been offered in Germany are for around 8m train km requiring about

100 drivers. In this mature market bidders would generally expect around half of their new employees

to be trained staff who resign from the incumbent to “follow their work” to the new entrant while the

other 50% have to be recruited “off the street” and receive full training.

In most countries where we operate either the staff transfer automatically to the new operator or each

individual has the right to transfer if he or she wishes and in these circumstances there is generally

significantly less requirement for recruiting and training new staff so concessions can be larger and/or

mobilisation periods shorter.

Flexibility to negotiate terms and conditions applicable to the concession and local market conditions

is to be preferred. However, Arriva also has considerable experience in staff transferring on existing

terms and conditions but this may limit innovation in some areas and will be reflected in the bid.

Indeed as previously mentioned staff transferring can in certain circumstances see an improvement in

terms through achieving increased productivity.

Arriva aims to provide a supportive, respectful working environment and works develops meaningful,

professional relationships with our employees, trades unions and work councils. This is underpinned

by an annual group-wide survey to benchmark employee satisfaction across a range of measures.

Surveys and other regular communications such as company newsletters, open forums, road shows

and websites help us to listen to our employees. The majority of our workforce is covered by collective

arrangements on working conditions.

Health & Safety is a key consideration throughout Arriva and particularly within the safety critical

environment of rail operation.

Liberalisation and competition in the European regional rail market. Page 25

4.6 Performance Regimes

Reputation considerations and, for net cost contracts, revenue risk, will generally ensure that private

operators maintain high quality standards. Nevertheless contracts invariably include performance

(bonus/malus) regimes. Typically these cover punctuality and reliability, station and train condition

(repairs) and cleanliness, provision of committed staffing, customer satisfaction and, particularly for

gross cost contracts, patronage levels.

It is important that all such arrangements are simple/understandable (avoiding perverse incentives),

proportionate and based on realistic targets. If bidders regard them as representing extraordinary

risks then these will be reflected in a higher price offer. Experience suggests that the most successful

service punctuality and reliability regimes are based on arrival time at destination with the benchmark

set at the actual level of punctuality (normally 0-5 minutes late) achieved historically by the incumbent.

Unless arrangements exist for the regime to be “back-to-back” with the Infrastructure Manager the

operator should only be penalised for delays and cancellations that are its own fault.

Penalties normally take the form of a percentage reduction of the subsidy for delayed services (full

loss for cancelled trains) but these levels are normally reduced if the alterations are pre-advertised

and/or alternative road transport is provided. Bonus payment levels should, in order to incentivise and

reward investment to achieve high standards of performance, mirror the penalties.

Other regimes will be based on customer surveys, spot checks and recorded passenger flows as

appropriate.

Liberalisation and competition in the European regional rail market. Page 26

5 Conclusion

Evidence from throughout Europe shows that carefully conceived and

implemented route tendering can generate investment, significantly reduce

subsidy requirements, improve service quality and attract new passengers.

By focusing tender design on the Best Practice outlined above it is possible

to maximise delivery of these benefits.

Arriva has successfully contributed to the opening of a number of Europe’s

rail passenger markets and would be delighted to utilise this experience and

to explore how a tendering model could be developed to optimise delivery of

Authorities’ financial and other objectives in other markets. A possible first step maybe to have a pilot

project in advance of the opening of a market and once again Arriva is willing to consider working in

partnership to achieve this.

Ends.

Arriva plc.

June 2013.

Liberalisation and competition in the European regional rail market. Page 27

Appendices

Case studies of market liberalisation in Europe (UK, Germany, Sweden)

Most European countries adopt a tendering model that is based on one of the following:

a) UK

b) Germany

c) Sweden

a) The UK experience (fully franchised since 1997)

An independent Infrastructure Manager (IM) was established in the early 1990s. Originally this

was privatised as Railtrack plc but it was taken back into public ownership following

insolvency. Variable Track Access charges were set at a low level (reflecting the marginal

costs of additional operations) to incentivise timetable enhancements.

Existing train fleets were allocated to three leasing Companies (ROSCOs) which were then

privatised. These have invested heavily in new trains and some 45% of the current fleet has

been built since the year 2000

The former British Railways (state-owned incumbent) passenger Divisions were reorganised

into 25 self-contained regionally or sector-based Train Operating Companies (TOCs), each

with their own trains, stations and maintenance depots etc. (leased from the ROSCOs and the

Infrastructure Manager respectively). To enable the development of a financial track record for

these Companies all trading relationships with other parts of the former British Railways were

made arms-length and fully contractual.

Comprehensive contract and enforcement (Regulatory) arrangements were put in place to

ensure that network benefits were maintained. These included mandatory non-discriminatory

ticket sales and customer service, cross acceptance of tickets, guaranteed non-discriminatory

access to stations and train maintenance depots by third-party operators etc. The

independent Rail Regulator was also given extensive powers to protect public interest,

oversee the value-for-money of the IM and ensure that competition was “fair.”

A minimum service level (PSO) was established for each route along with arrangements that

capped increases in key fares according to an RPI formula. Highly complex Performance

Regimes (Bonus/Malus) were also implemented to ensure that service quality would be

maintained and improved.

The 25 TOCs were then tendered as “going concerns” by Central Government. All bar one

franchise were net-cost (i.e. the franchisee bore the revenue risk) and were for around 7

years except on a small number of networks requiring major investment which were for longer

periods of up to 15 years. Although award was to be based largely on the basis of price

(lowest subsidy or highest premium) bidders were encouraged to commit to service

improvements, new trains and other investments that would grow the market.

Liberalisation and competition in the European regional rail market. Page 28

Since British Railways had, effectively, been abolished, only new-entrant private companies

were permitted to bid for the franchises.

Competition for the franchises was fierce and several bidders had unrealistic expectations

concerning their ability to reduce costs and attract additional patronage. As a result a few

operators got into financial difficulties (particularly during the hiatus following the insolvency of

Railtrack) and required government bail-outs to maintain services until their franchises could

be re-tendered.

In the succeeding years the UK model has been refined to reflect real and perceived

weaknesses. These adjustments have included increasing the importance of quality plans and

incorporation of a deliverability test in the award criteria, some re-mapping of franchises (there

are now 19), inclusion of a revenue “cap and collar” (sharing of risk/reward between the

franchisee and the Government), simplification of the various performance regimes, a move

towards longer franchises and more prescriptive franchise specifications. Responsibility for

some franchises has also been devolved from Central Government to Regional Authorities.

However the overall structure has changed little.

Franchisees have also become more expert and realistic in the way that they compile their

bids but nevertheless (and despite the “cap and collar”) one franchisee has terminated a

contract early as a result of the current economic downturn.

UK rail concessions are very large and complex businesses (several perform in excess of

40m train km pa and have turnovers in excess of €1 Bn) and with service/quality levels fixed

(so few levers are available for franchisees to reduce the cost base), the expected scale of

cost reductions has not been achieved. Indeed, a recent report prepared for the UK

Government found that the real (inflation adjusted) cost per unit of output has barely changed

during the 15-years since franchising started.

In other respects though the UK model has delivered significant benefits. Patronage (annual

passenger km) has increased by almost 65% and there has been a 24% increase in the train

km operated. Service quality and customer satisfaction have improved significantly (with more

staff in customer facing roles and better training) and there has been very significant private

sector investment in new trains and passenger facilities etc.

A further review of the UK rail franchising process and procedures is currently being

undertaken following the discovery of anomalies in the evaluation of bids for the West Coast

Main Line tender during summer 2012.

Arriva operates around 14% of UK rail services - approximately 80m train km each year

through 4 franchises, one open-access Inter-City operation and a city metro network.

Liberalisation and competition in the European regional rail market. Page 29

UK-Rail

1995-2008: 800 m → 1,232bn passengers/year

1995-2006: 200 m £/year → 1bn £/year invested

South West Trains / Stagecoach

Passenger increase 1997-2009: + 45%

Reliability + punctuality:

o 2005 76% → 89%

o 2009 96%

b) The German Experience (since 1996)

In 1996 responsibility for the specification and financial support of local rail services was

devolved from Central to Regional Government (Länders) who perform this role through 27

Regional Passenger Authorities (Aufgabenträger des SPNV). Long-distance services (not

requiring subsidy) may be provided by DB (the state-owned incumbent) or any other operator.

Initially most Regional Passenger Authorities (RPAs) entered into direct award or negotiated

contracts with the incumbent operator but some initiated open tenders for small service

groups.

Following the success of this early involvement by non-incumbent operators, around half of

the Regional market has now been the subject of an open tender (in 2011, approximately

23% of Regional train km were provided by new-entrants) and, following a Federal Court

ruling in 2011 (and in the light of reducing levels of funding from Central Government) it

seems likely that the remainder will also be tendered over the next few years as existing

contracts expire.

Arriva was active in the German market prior to 2010, operating some 22m train km annually

(with further large concessions being mobilised) but the Competition Authorities required

these to be disposed of as a condition of the take-over by DB.

Germany, development in regional rail in 10 years

Tendering, performance contracting and regionalisation lead to:

+ 28% train-km

- 26% in public subsidy for tendered services

+ 43% passengers

Liberalisation and competition in the European regional rail market. Page 30

c) The Swedish Experience (since 2000)

Vertical separation between railway operations and infrastructure management was

introduced in 1988 as part of reforms intended to improve the financial performance of the

state-owned incumbent operator (SJ). The same legislation transferred responsibility for the

provision of unprofitable regional rail services (as well as associated funding and ownership of

the rolling-stock) to 21 County Public Transport Authorities (CPTAs) that are also responsible

for procuring local bus services.

Subsequent legislation (principally in 2000) made it easier for new entrants to participate in

the market by establishing a central office for the procurement of subsidised inter-regional

services and creating new arms-length companies within SJ (later to be privatised) to provide

support services such as train maintenance and cleaning. Since 2010 network management

and procurement of inter-regional services have been transferred to Trafikverket – a new

authority responsible for the infrastructure of all transport modes.

Initially most CPTAs simply negotiated contracts with the incumbent but others tried to

encourage interest from new-entrant operators and the perceived success of an early

competitive tender (services in Jönköping County in 1990) which delivered improved quality

despite a 21% reduction in subsidies encouraged other Regions to follow the same route.

Market-entry barriers in Sweden are very low as the trains for Regional services are generally

provided by the CPTA (several have pooled their fleets and expertise in a ROSCO “Transitio”)

and trains are also available for lease from a hived-off former division of SJ (Affärsverket

Statens Järnvägar, which is still state-owned). Investment requirements are minimal, train

maintenance is available from the privatised former SJ maintenance division (now called

Euromaint) and from other providers while the existing train-crew and other key staff normally

transfer from the previous to the new operator. As a result some of the initial tenders in the

early 1990s were won by small local companies with limited financial resources and a very

small number of these were over optimistic in their bid forecasts and had to be bailed-out.

Nevertheless the significant cost reductions (typically 20%+ in the first round of tendering) and

quality improvements were such that the experiment was considered a success and now just

about all subsidised services (including loss-making inter-regional services procured by

Central Government) have been tendered. In most cases the second round of tendering has

seen a further significant reduction in subsidy requirements.

Provision of trains by the client is particularly beneficial in Sweden as trains are typically wider

than can be accommodated elsewhere in mainland Europe and it is likely that commercial

leasing companies would price this lack of alternative markets into their residual value

calculations.

There is no standard form of tender or contract arrangements for Regional services as each

CPTA determines a structure suited to local needs but typical features are:

o Gross cost but with a bonus/malus scheme related to the level of patronage;

o Between 2m and 8m train km annually on a “natural network”;

Liberalisation and competition in the European regional rail market. Page 31

o Of 7 to 10 years duration with a modest extension for good performance

o Trains to be used specified by and leased from the client body;

o Some clients also rent a maintenance depot to the operator and/or include Heavy

Maintenance (undertaken by Euromaint or the vehicle constructor) in the lease-charge;

o Some contracts include station operation but there are also examples of this being

undertaken by the client body and other examples of this being the object of a separate

tender;

o Staff have the right to transfer to the new operator on their existing employment terms

and conditions (in accordance with Swedish employment law) but are not compelled to

do so;

o Timetable and total train km to be operated are specified by client but often bidders are

encouraged to submit alternative proposals that will provide an equivalent or better

service at lower cost;

o Offer price expressed as a cost per train km for the specified service but with a menu of

prices to cover possible variations in service level and annual indexation based on a

basket of appropriate indices for staff-cost, energy etc. Track Access charges are

normally paid by the client direct or as a contract “pass-through”;

o High quality standards with bids evaluated 25-40% on quality plans and 60-75% on price.

Also robust bonus/malus regimes;

o Mobilisation periods are shorter than in Germany (not tied to new train delivery

timescales) but, at typically around 15 months+ are adequate bearing in mind that neither

extensive recruitment nor training of new staff nor construction of major new facilities are

generally required.

Very little data about detail of tender bids is published and with improved quality being such a

key element of the evaluation criteria, it is difficult to be specific about the financial and other

benefits that competitive tendering has delivered. However a report prepared for the

European Conference of Ministers of Transport and published by OECD in 2007 concludes

the following:

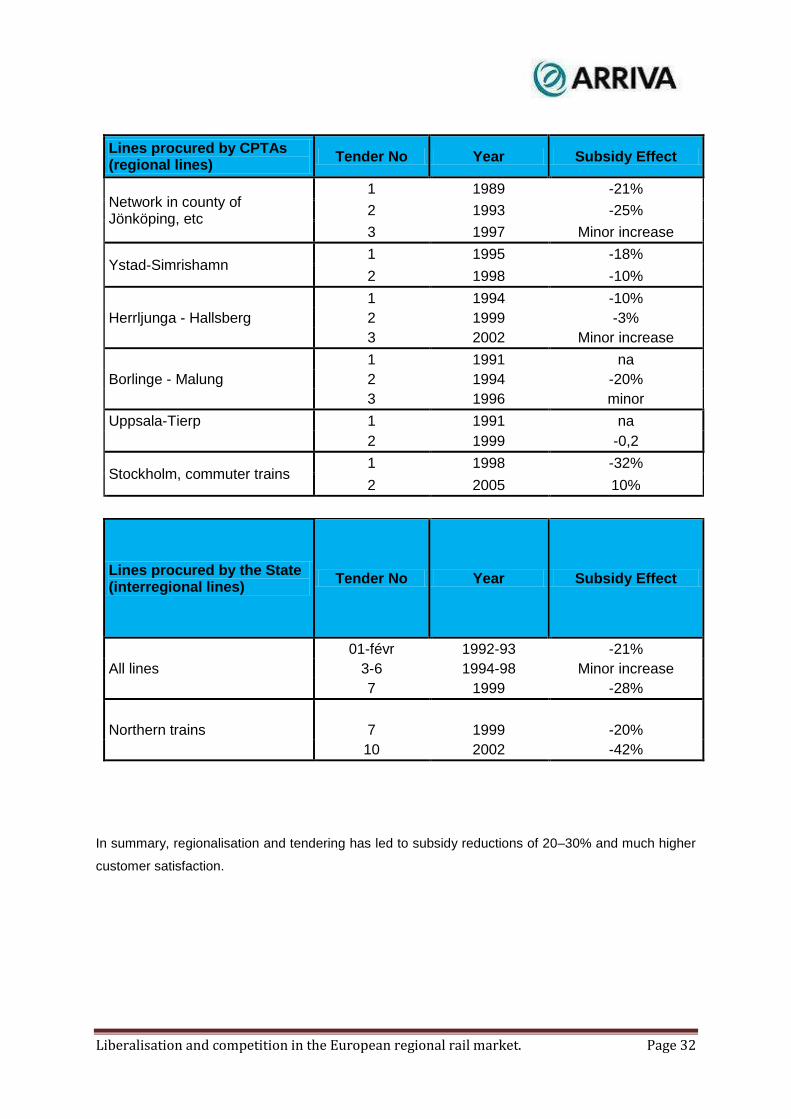

Data on subsidy reductions caused by tenders carried out by CPTA’s is somewhat scarce,

partly due to difficulties when comparing subsidy levels under different conditions. Currently

available examples are listed in the following table. Typically there have been subsidy

reductions in the magnitude of 20% in the first round of tendering. For services procured by

the state, substantial reductions were accomplished during the first two years of tendering,

despite the lack of new market entry. After that a period of tenders implying stable subsidies

followed. When several new firms finally were able to win these tenders in 1999, additional

large subsidy reductions (28%) were achieved.

Liberalisation and competition in the European regional rail market. Page 32

Lines procured by CPTAs (regional lines)

Tender No Year Subsidy Effect

Network in county of Jönköping, etc

1 1989 -21%

2 1993 -25%

3 1997 Minor increase

Ystad-Simrishamn 1 1995 -18%

2 1998 -10%

1 1994 -10%

Herrljunga - Hallsberg 2 1999 -3%

3 2002 Minor increase

1 1991 na

Borlinge - Malung 2 1994 -20%

3 1996 minor

Uppsala-Tierp 1 1991 na

2 1999 -0,2

Stockholm, commuter trains 1 1998 -32%

2 2005 10%

Lines procured by the State (interregional lines)

Tender No Year Subsidy Effect

01-févr 1992-93 -21%

All lines 3-6 1994-98 Minor increase

7 1999 -28%

Northern trains 7 1999 -20%

10 2002 -42%

In summary, regionalisation and tendering has led to subsidy reductions of 20–30% and much higher

customer satisfaction.

Liberalisation and competition in the European regional rail market. Page 33

Annexe

A possible route-map for a liberalised rail market in France by 2019

A specimen timeline showing a possible approach that would facilitate an orderly transition to

competitive tendering in France is shown below. It includes a suggestion of four small pilot projects

intended to enable client bodies and potential new-entrant operators to gain experience (and deliver

some early cost and quality benefits) in advance of the main programme of tendering which would

extend these benefits to the rest of the network progressively from December 2018.

It is based upon the knowledge and experience gained during the opening of the UK rail passenger

market as well as the other 7 European markets in which Arriva operates and/or participated in the

market opening. Inevitably a number of assumptions have had to be made, perhaps the most

significant of which are that the tendering authority will be a Region but working to a nationally agreed

template and that, at least initially, sufficient vehicles from the existing rolling stock fleet will be made

available to all bidders on a non-discriminatory basis (by, for example, the Regions, one or more

ROSCOs and/or SNCF.)

It is also assumed that the main programme of route tendering will be spread over a number of years

from 2018 to (say) 2022, thereby enabling maximum participation by potential bidders.

Liberalisation and competition in the European regional rail market. Page 34

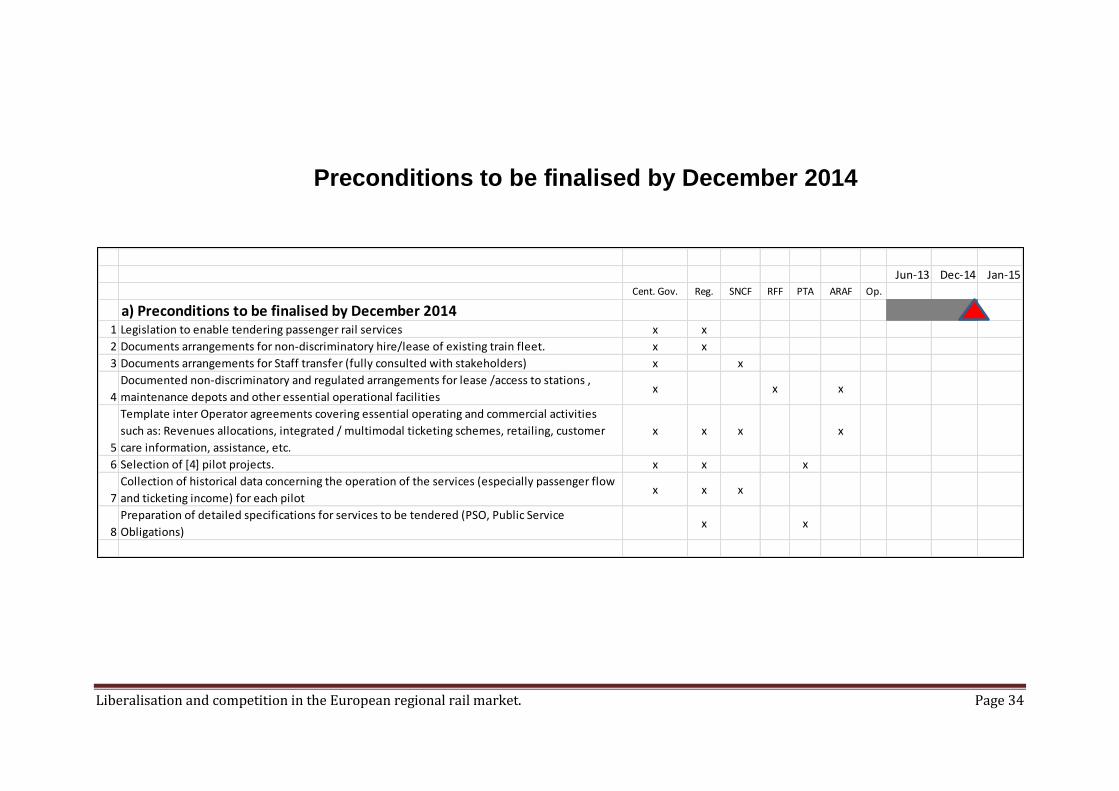

Preconditions to be finalised by December 2014

Jun-13 Dec-14 Jan-15

Cent. Gov. Reg. SNCF RFF PTA ARAF Op.

a) Preconditions to be finalised by December 20141 Legislation to enable tendering passenger rail services x x

2 Documents arrangements for non-discriminatory hire/lease of existing train fleet. x x

3 Documents arrangements for Staff transfer (fully consulted with stakeholders) x x

4

Documented non-discriminatory and regulated arrangements for lease /access to stations ,

maintenance depots and other essential operational facilitiesx x x

5

Template inter Operator agreements covering essential operating and commercial activities

such as: Revenues allocations, integrated / multimodal ticketing schemes, retailing, customer

care information, assistance, etc.

x x x x

6 Selection of [4] pilot projects. x x x

7

Collection of historical data concerning the operation of the services (especially passenger flow

and ticketing income) for each pilotx x x

8

Preparation of detailed specifications for services to be tendered (PSO, Public Service

Obligations)x x

Liberalisation and competition in the European regional rail market. Page 35

PILOT PROJECTS

PILOT PROJECTS Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Dec-16 Jan-17

b) Tender Procedure Cent. Gov. Reg. SNCF RFF PTA ARAF Op.

1 Invitation for expression of interest (prequalification) x

2 Finalisation of ITT x

3 Issue Template Concession Agreement x

4 Short List Bidders x

5 Issueing of ITT to Short List Bidders x

6 Bidding period x

7 Tender Evaluation x

8 Final Negotiation and tender award x

c) Mobilisation Period Cent. Gov. Reg. SNCF RFF PTA ARAF Op.

1

Consultation and finalisation of timetable with client and

stakeholdersx x

2 Application of Track Access x x

3 Final negotiation of arrangements for staff transfer x x

4 Appointments/ Confirmation Senior Management x

5 Real Estate (Depots, offices, etc.) x

6 Third party and supplier contracts x

7 IT / Equipment supply and maintenance contracts x

8 Membership of industry schemes x

9

If not already held: obtaining operating licenses and safety

certification, etc.x

10 Implementation of Safety Management Systems x

11 Insurance x

12 Business Transfer Agreements x

13 Service Delivery and Contingency Plans x

14 Communication Plan for Employee, Stakeholders, etc x

d) Start of Services (Pilot Projects) x

Liberalisation and competition in the European regional rail market. Page 36

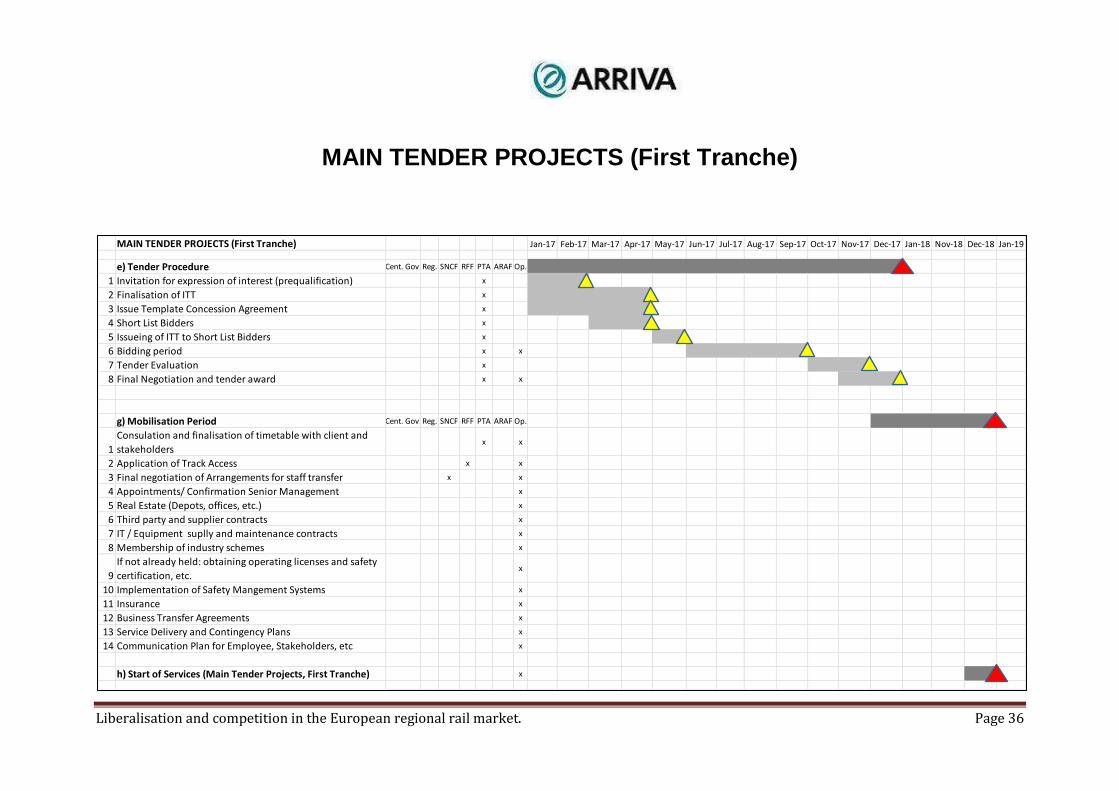

MAIN TENDER PROJECTS (First Tranche)

MAIN TENDER PROJECTS (First Tranche) Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Nov-18 Dec-18 Jan-19

e) Tender Procedure Cent. Gov. Reg. SNCF RFF PTA ARAF Op.

1 Invitation for expression of interest (prequalification) x

2 Finalisation of ITT x

3 Issue Template Concession Agreement x

4 Short List Bidders x

5 Issueing of ITT to Short List Bidders x

6 Bidding period x x

7 Tender Evaluation x

8 Final Negotiation and tender award x x

g) Mobilisation Period Cent. Gov. Reg. SNCF RFF PTA ARAF Op.

1

Consulation and finalisation of timetable with client and

stakeholdersx x

2 Application of Track Access x x

3 Final negotiation of Arrangements for staff transfer x x

4 Appointments/ Confirmation Senior Management x

5 Real Estate (Depots, offices, etc.) x

6 Third party and supplier contracts x

7 IT / Equipment suplly and maintenance contracts x

8 Membership of industry schemes x

9

If not already held: obtaining operating licenses and safety

certification, etc.x

10 Implementation of Safety Mangement Systems x

11 Insurance x

12 Business Transfer Agreements x

13 Service Delivery and Contingency Plans x

14 Communication Plan for Employee, Stakeholders, etc x

h) Start of Services (Main Tender Projects, First Tranche) x

Liberalisation and competition in the European regional rail market. Page 37

Assumptions

1 Initial pilot project concessions will be for 7 years each covering just a small network with about 30 train sets and ideally 2.5 and 3.5 million of train km. Later concessions can, of course (as discussed above) be rather larger than this.

2 The pilot concessions will not require new trains, the existing fleet will be made available to the new operator.

3 The necessary staff required for the services covered by the pilot will be transferred from the incumbent operator

4 The incumbent operator is committed to and cooperates with the process.

5 Best practice tendering procedures developed in Europe (as described above) are adopted.

6 Adequate historical information is made available to bidders by the incumbent.

7 Non-discriminatory access to all essential operational facilities.

8 The mobilisation period shown here is the absolutely minimum. If any new trains and/or significant staff recruitment (eg drivers) is required then mobilisation period will need to be extended accordingly.

9 For the main programme it is assumed that the network will be split into around 40+ concessions and that 7 to 10 of these will be tendered each year thereby ensuring the maximum participation by potential bidders.