Liability in Securities Offerings Underwriter and accountant due diligence Last updated 06 Feb 12.

15

Liability in Securities Offerings Underwriter and accountant due diligence Last updated 06 Feb 12

-

Upload

amberly-singleton -

Category

Documents

-

view

220 -

download

3

Transcript of Liability in Securities Offerings Underwriter and accountant due diligence Last updated 06 Feb 12.

Liability in Securities Offerings

Underwriter and accountant

due diligence

Last updated 06 Feb 12

Securities Class Action

Software Toolworks(Issuer)

Deloitte & Touche(auditor)

DirectorsOfficers

Investors• Plaintiffs• Defendants • Claims

– ’33 Act § 11

– ’34 Act Rule 10b-5

• Defenses

Montgomery SecuritiesPaineWebber

(lead underwriters)

Section 11 Liability(’33 Act)

Prospectus• Issuer – strict• Ds / Os / UWs – due

diligence defense (reasonable investigation + reasonable belief true)

• Auditor (expert) – no liability

Financials• Issuer – strict• Ds / Os / UWs – not

believe false• Auditor (expert) – due

diligence defense (reasonable investigation + reasonable belief true)

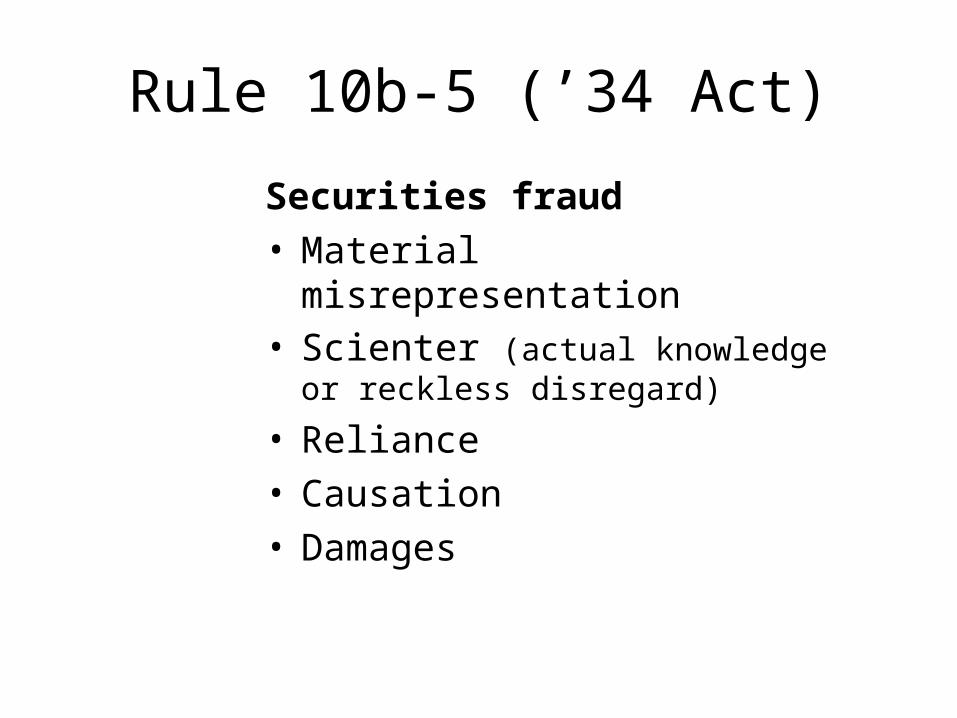

Rule 10b-5 (’34 Act)

Securities fraud• Material misrepresentation • Scienter (actual knowledge or reckless

disregard)

• Reliance• Causation• Damages

Securities Class Action• Underwriters (Montgomery

Securities and PaineWebber)– granted summary judgment on

Section11 and Rule 10b-5– what does this mean? – What do plaintiffs appeal?

• Accountant (Deloitte & Touche)– granted summary judgment on

Section 11 and 10b-5– What do plaintiffs appeal? – Why don’t plaintiffs appeal Section

11 judgment for defendants?Software Toolworks

(Issuer)

Deloitte & Touche(auditor)

DirectorsOfficers

Montgomery SecuritiesPaineWebber

(lead underwriters)

Investors

Underwriter defense …

Underwriter defense’33 Act § 11

•“after reas investigation, believed true”

OR(2) “no reason believe false”

’34 Act Rule 10b-5

No “actual knowledge” AND

No “recklessness (extreme departure ordinary care)”

Business – price reductions

• “Nintendo not subject to price reductions”• “customers do not have return rights”

Recognition of OEM revenue

• Korean manufacturer backdates contract• Law firm not give comfort letter on OEM contracts• Contracts were contingent

Contingent sales • Barron’s says slumping sales and bad accounting• SEC told that data not available• Late June sales were bogus

Underwriter defense’33 Act § 11

•“after reas investigation, believed true”

OR(2) “no reason believe false”

’34 Act Rule 10b-5

No “actual knowledge” AND

No “recklessness (extreme departure ordinary care)”

Business – price reductions

• “Nintendo not subject to price reductions”• “customers do not have return rights”

Recognition of OEM revenue

• Korean manufacturer backdates contract• Law firm not give comfort letter on OEM contracts• Contracts were contingent

Contingent sales • Barron’s says slumping sales and bad accounting• SEC told that data not available• Late June sales were bogus

Underwriter defense’33 Act § 11

•“after reas investigation, believed true”

OR(2) “no reason believe false”

’34 Act Rule 10b-5

No “actual knowledge” AND

No “recklessness (extreme departure ordinary care)”

Business – price reductions

• “Nintendo not subject to price reductions”• “customers do not have return rights”

Recognition of OEM revenue

• Korean manufacturer backdates contract• Law firm not give comfort letter on OEM contracts• Contracts were contingent

Contingent sales • Barron’s says slumping sales and bad accounting• SEC told that data not available• Late June sales were bogus

Underwriter defense’33 Act § 11

•“after reas investigation, believed true”

OR(2) “no reason believe false”

’34 Act Rule 10b-5

No “actual knowledge” AND

No “recklessness (extreme departure ordinary care)”

Business – price reductions

• “Nintendo not subject to price reductions”• “customers do not have return rights”

Recognition of OEM revenue

• Korean manufacturer backdates contract• Law firm not give comfort letter on OEM contracts• Contracts were contingent

Contingent sales • Barron’s says slumping sales and bad accounting• SEC told that data not available• Late June sales were bogus

Auditor defense …

Auditor defense’33 Act § 11

(1)“after reas investigation, believed true”

Not appealed

’34 Act Rule 10b-5

(1) No “actual knowledge”(2) No “recklessness – no extreme

departure ordinary care”

Recognition of OEM revenue

• OEM agreements poorly documented• Management under “extraordinary pressure” • Deloitte only got oral assurances on some

contracts• No information on return policies

SEC letters • SEC told that June data not available• Sample OEM contract differed from actual

contracts

Auditor defense’33 Act § 11

(1)“after reas investigation, believed true”

Not appealed

’34 Act Rule 10b-5

(1) No “actual knowledge”(2) No “recklessness – no extreme

departure ordinary care”

Recognition of OEM revenue

• OEM agreements poorly documented• Management under “extraordinary pressure” • Deloitte only got oral assurances on some

contracts• No information on return policies

SEC letters • SEC told that June data not available• Sample OEM contract differed from actual

contracts

Auditor defense’33 Act § 11

(1)“after reas investigation, believed true”

Not appealed

’34 Act Rule 10b-5

(1) No “actual knowledge”(2) No “recklessness – no extreme

departure ordinary care”

Recognition of OEM revenue

• OEM agreements poorly documented• Management under “extraordinary pressure” • Deloitte only got oral assurances on some

contracts• No information on return policies

SEC letters • SEC told that June data not available• Sample OEM contract differed from actual

contracts

The end(mercifully)