Infographics: Bank Guarantee Issuance – Bank Guarantee Process

Upload

nguyendungCategory

view

214download

0

WORKING GROUP

Johanna Hietalahti (ed.), Municipal Guarantee Board, Communications Specialist, Master of Social

Sciences (economics), [email protected], tel. +358 (0)9 6227 2880

Jaakko Kiander, Ilmarinen Mutual Pension Insurance Company, Director, Doctor of Social Sciences

(economics), [email protected], tel. +358 (0)10 284 11

Sari Korento, The Association of Finnish Local and Regional Authorities, Development Manager,

Master of Administrative Sciences, [email protected], tel. +358 (0)9 771 2616,

mobile +358 (0)500 476 747

Heikki A. Loikkanen, University of Helsinki, Professor (emeritus) of Urban Economics,

Doctor of Social Sciences (economics), [email protected], tel. +358 (0)9 1912 8722,

mobile +358 (0)40 501 0156

Heikki Niemeläinen, Municipal Guarantee Board, CEO, Doctor of Social Sciences (economics),

[email protected], tel. +358 (0)9 6227 2880, mobile +358 (0)40 589 8348

Heikki Pukki, The Association of Finnish Local and Regional Authorities, Senior Adviser,

Bachelor of Science (mathematics), [email protected], tel. +358 (0)9 771 2190,

mobile +358 (0)50 324 3621

Tuukka Salminen, Municipal Guarantee Board, Director, Master of Social Sciences (economics),

[email protected], tel. +358 (0)9 6227 2880, mobile +358 (0)40 705 4824

Pekka Tiainen, the Ministry of Labor and the Economy, Special Advisor, Doctor of Social Sciences

(economics), [email protected], tel. +358 (0)10 604 8072

Juhani Turkkila, The Association of Finnish Local and Regional Authorities, Chief Economist,

Doctor of Social Sciences (economics), [email protected], tel. +358 (0)9 771 2095,

mobile +358 (0)50 667 47

Reijo Vuorento, The Association of Finnish Local and Regional Authorities, Deputy Director,

Master of Philosophy (economics), [email protected], tel. +358 (0)9 7712078,

mobile +358 (0)50 667 41

TRANSLATION FROM FINNISH TEXT Heikki A. Loikkanen

COVER DESIGN Leea Wasenius www.wasenius.fi ISBN 978-952-67511-3-9 (pdf) © Municipal Guarantee Board Helsinki 2012

1. CREDIT RATING PROCEDURES 1

2. MUNICIPAL ECONOMIES 2

2.1 Criteria for assessing municipal economies 2 2.2 Wealth and income 2 2.3 Diversification of the economic structure 3 2.4 Demographic profile 4

3. FINANCIAL MANAGEMENT OF MUNICIPALITIES 9

3.1 Assessment criteria for financial management 9 3.2 Transparency and disclosure 10 3.3 Budgeting 10 3.4 Long term capital and financial planning 11 3.5 Revenue and expenditure management 12 3.6 Debt management 13 3.7 Management of assets and liquidity 14 3.8 Management of local government related entities 15 3.9 Political strengths and leadership skills 15 3.10 External risk management 16

4. BUDGET FLEXIBILITY 17

4.1 Criteria for assessment of budget flexibility 17 4.2 Municipalities’ revenue adjustment 18 4.3 Cutting local government expenditure 23

5. BUDGET EXECUTION 25

5.1 Evaluation criteria for budget execution 25 5.2 Annual operating balance as a percentage of operating revenue 25 5.3 Balance after capital accounts 27

6. LIQUIDITY 29

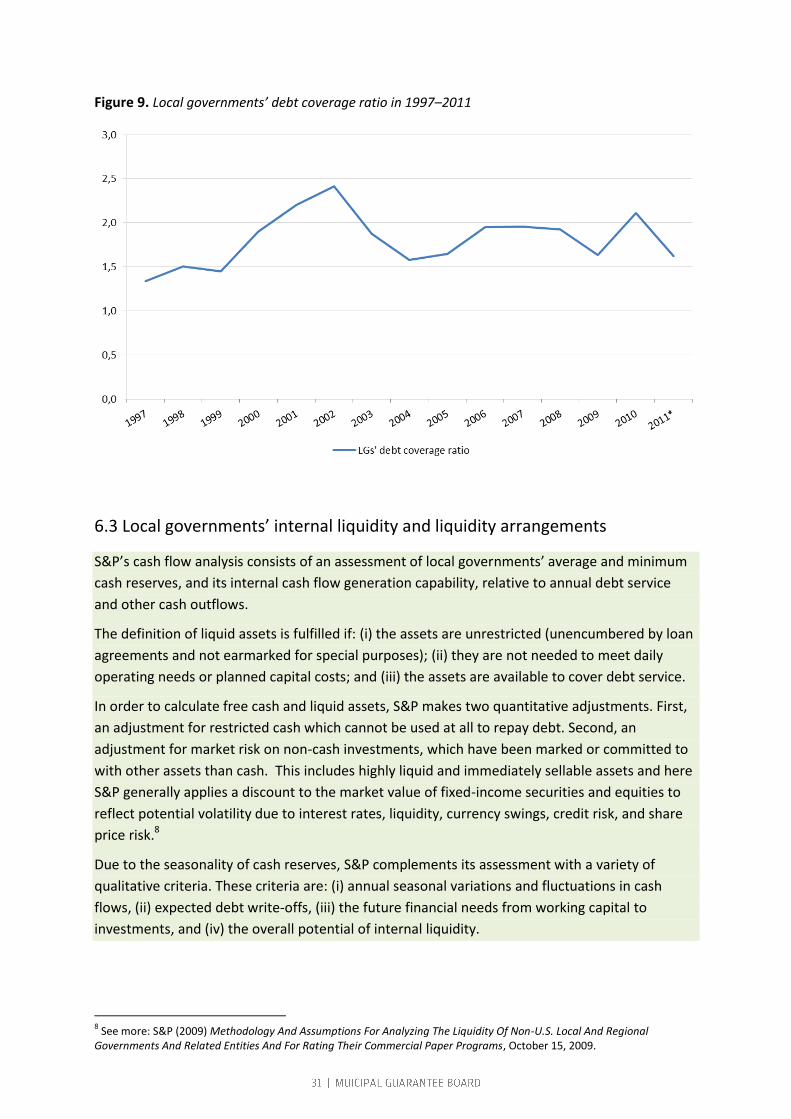

6.1 Assessment criteria for liquidity 29 6.2 Local governments’ debt servicing costs 30 6.3 Local govenrments’ internal liquidity and liquidity arrangements 31 6.4 External liquidity 32

7. INDEBTEDNESS 33

7.1 Indebtedness evaluation criteria 33 7.2 Local govenrment loans and cash equivalents 34 7.3 Local governments’ estimated indebtedness in the future 35 7.4 Exposure to market risks 36 7.5 Other long-term obligations 37

8. LIABILITIES 38

8.1 Assessment of liabilities 38 8.2 Local governments’ contingent liabilities 38

Standard & Poor's (S&P in the future) assesses the creditworthiness of municipalities in two

stages.1

In the first stage, the S&P evaluates municipal institutions from the view-point of (i)

predictability of systems, (ii) the adequacy of funding and resources to perform their duties and,

on the other hand, their liberties to adjust them; (iii) legality and transparency of budgetary

process and accounting systems, and (iv) system support, which is ultimately the responsibility of

the national government of the country.

In the second stage, the S&P estimates municipal activities from the view-point of their own

institutions. The following factors are evaluated (S&P 2010: 18): economy, financial management,

budgetary flexibility, budgetary performance, liquidity, debt burden and contingent liabilities.

What the above factors aim to measure in case of local and regional governments (LRG) is

defined as follows:

ECONOMY – score aims to measure how economic factors are likely to impact on LRG’s revenue

generation capability and spending needs, and ultimately its ability to service debt in the

medium to long term.

FINANCIAL MANAGEMENT – score aims to measure how the quality of an LRG’s financial

management and its political context are likely to affect its willingness and ability to service debt

over time.

BUDGETARY FLEXIBILITY – score aims to measure how much an LRG could increase its revenues

or reduce its expenditure in case of need, in order to maintain its debt service ability.

BUDGETARY PERFORMANCE – score aims to measure and forecast the level and the volatility of

an LRG’s expected cash flows from operations and capital activities, and its surplus available to

service debt.

LIQUIDITY – score aims to measure how LRG’s internal sources of liquidity, such as cash reserves

and cash flow generation, and external sources, namely bank lines and market access, are likely

to impact its debt servicing capability, primarily within the next 12 months.

DEBT BURDEN – aims to measure how our expectations for the level, structure, and

sustainability of an LRG’s debt are likely to affect its debt-service capacity.

CONTINGENT LIABILITIES – aims to measure to what extent off-balance sheet risks and their

relative size are likely to impair an LRG’s capacity to repay its debt in the medium-to-long term.

Note that in the Finnish two-tier system of government (central and local government or

municipalities) there are no regional governments. Thus our term local government (LG) refers

to municipalities and their joint organizations.

1 This report is written in a dialogue form. Our short interpretations and quotations of S&P's methodology and rating

criteria are highlighted in gray. They are based on the article: S&P (2010) Methodology For Rating International Local And Regional Governments, September 20, 2010 (available: http://www.standardandpoors.com/ratingsdirect).

2.1 Criteria for assessing municipal economies

In the assessment of local government finances, S&P considers how different economic factors

affects their revenue generation and consumption needs, as well as the ability of municipalities

to service their debt in the medium and long term.

In the assessment of municipalities, S&P reviews wealth and income levels, economic structure,

demographic profile, and the outlook for economic growth (S&P 2010: 18–19). The primary

measure is proportional to population size, namely Gross Domestic Product per capita. In order

to get the best score (a value of 1 point on a scale of 1–5) for the local government sector, GDP

per capita must be more than 35 000 USD.

Municipalities, which have better than average growth prospects and/or which have

exceptionally diversified economies can get an increase to their numerical (anchor) score (S&P

2010: 20).

Factors which reduce the anchor score include unfavourable demographic structure; poorly

diversified or unstable, and thus vulnerable economy that is dependent on individual or cyclically

sensitive industrial sectors; high level of unemployment, as well as structural problems, or poor

infrastructure, which are caused by weak growth outlook (S&P 2010: 20–21).

2.2 Wealth and income

S&P takes the view that wealth and income level, as measured by GDP per capita, is a key

indicator for local government sector. This is how it aims to form a picture of the strength of

municipalities’ revenue/tax base, as well as the need for social and other public service

provision, now and in the future. The level of services affects the decisions of municipalities to

raise taxes or reduce services, and it also tells about the stability of the local economic, social

and political situation. In general, S&P estimates that a high income level refers to good ability to

handle payment commitments. (S&P 2010: 19).

Finland's economic base and financial position

Finland has a good economic base. As for macroeconomic indicators, the economy is close to

external and internal balance; the current account is roughly in balance, inflation does not differ

significantly from the euro area average, and the unemployment rate is reasonable. While the

economic fundamentals are in good shape, the continuing euro zone debt crisis and the weak

economic development of the EU countries is detrimental for Finland. The long lasting weak

development of EU, which is a key export market, has reduced Finnish exports.

Finland's economic prospects may be, however, regarded as reasonably good. Competitiveness

of the economy is good. In addition to reasonable price competitiveness, it is strengthened by a

good operating environment for businesses, educated workforce, and high investments in

research and development.

The strong knowledge base reflects in innovativeness, and shows also in high amount of patents.

The Finnish economy also benefits from a strong industrial tradition, a high proportion of

industrial production in GDP, and a number of successful global companies.

The financial position of the public sector in Finland is strong compared to most other

industrialized countries. As a whole, the public sector is in financial balance, and public sector’s

financial wealth is far greater than its gross debt. The main reason for this is the partly funded

pension sector, which is regarded as a part of the public sector, as it has been on surplus.

Without the pension sector, the general government deficit in 2012 would be about three per

cent of GDP and the public debt about 50 per cent of GDP.

Finland's GDP per capita was 35 150 euro in 2011. Its volume grew by 2.7 per cent in 2011. The

increase is based on the above-mentioned factors.

2.3 Diversification of the economic structure

By considering the diversity of regional and local economic structures, S&P’s assesses the

potential volatility of their tax base and resilience to stress. The basic idea is that an economy,

whose strengths are divided to several sectors, is usually less exposed to downturns in individual

industries, and its tax base is more stable than economies that rely heavily on a single economic

sector or employer. Furthermore, concentrated and narrow economic economies have a

tendency to be more vulnerable to various exogenous factors. (S&P 2010: 19).

Tax base of municipalities and fragmentation of regional economies in Finland

Finland's economic structure is changing in many ways over the next 10–20 years. The most

important changes are expected to take place in the age structure of population, the regional

structure, and the structure of production.

The population share of pensioners and elderly people is growing rapidly in the period 2010–

2030. The weakening of the dependency ratio will increase expenditure pressures in the public

sector. The age structure dependent social and health spending’s share of GDP is expected to

grow by about 5 percentage points over the 2013–2030 period.

In addition to the age structure of the population, Finland is still undergoing a major change in its

regional economic structure. In this respect, Finland differs from many Western European

countries, where urbanization and the resulting concentration of the population took place

much earlier. In Finland, instead, a change in regional structure of population is still to be

expected as a result of migration within the country. The regional focus of population is

concentrating to the growing cities and their surroundings in Southern and Western Finland.

Population growth will be sustained by immigration, which mostly directs to large cities. Net

migration is expected to be around 0.3 per cent of the total population per year.

Finland's production structure has for long time been changing, and the change will continue.

Labour force participation rates in agriculture and forestry, as well as the in industry, continue to

decline. The economy continues to develop towards a post-industrial and service-intensive

structure. This does not mean the end of the traditionally strong industrial sectors.

It is probable that there will continue to be plenty of wood and metal using resource-based

industries. Areas that will remain in addition to forest industry will be mining, basic metal

industries as well as logistic sector serving these sectors. Selected energy policy, namely reliance

on extensive use of nuclear power, will support energy-intensive heavy industry in the future,

too.

Changes in the regional structure of population and production will change the local government

sector in different ways. Population and production will concentrate in university cities and their

surroundings. In these areas, as a result of their growth, there will be large-scale investment

needs, and due to migration, their age structure will remain favourable. It is expected that the

concentration of economic activities will also create agglomeration benefits, which reflect in

productivity growth.

Expected changes in demography are discussed in Section 2.4.

In the future, economic and demographic differences of municipalities are likely to increase

further. Therefore, also in the future, a tax revenue equalization system will be needed because

a large number of municipalities will be in a situation, where their own tax revenues, due to the

aging of the population, will not be sufficient to cover their expenditure. The need for

equalization cannot be removed by merging municipalities, because the differences remain large

even at the regional level.

Due to the change in age structure, local governments’ total expenditure are expected to grow

especially in the 2020s faster than GDP. This implies that there is a need to improve the cost-

effectiveness of local government and to strengthen its revenue base.

Municipal income tax may harden somewhat from current levels. Finnish income taxation is not

currently on average particularly hard, especially in comparison with other EU countries.

Therefore, it is possible that the average municipal tax rate may gradually increase close to 25

per cent. The tax base can also be amended by changing grants, income taxes and fees.

2.4 Demographic profile

By looking at the demographic profile of municipalities, S&P wants to find out how demographic

change will affect local governments, their opportunities to provide services and to collect tax

revenues.

Population growth typically contributes to the growth in tax revenues, while a loss of population

threatens the tax base. In general, S&P estimates that a 1–2 per cent per annum steady

population growth has a positive impact on the creditworthiness of municipalities, while a

decrease in population causes pressures to revenue development. On the other hand, a very

rapidly growing population may also be place an excessive burden to local public service and

industrial production.

Also, the age structure, particularly the share of dependents (other than 15–64 years of age) in

the population, is an important factor in assessing the need for a variety of public services and

the possibilities of local authorities to cover related expenditure with their own tax revenue.

(S&P 2010: 19).

The demographic dependency ratio in Finland

Finland’s demographic dependency ratio2 was 48.7 per cent in 1990 and 51.7 per cent in 2010.

This means that in 2010, Finland has three new dependent persons per one hundred people in

working age, as compared to 1990.

According to the 2009 population forecast, the dependency ratio rises to 65 per cent by 2020,

after which the age structure of the population will stabilize. The dependency ratio in 2030–

2040's will be about 75 per cent.

The dependency ratio increases as the post-World War II baby boom generation reaches the age

of 65 years. The ratio was also high in the childhood of these age groups: the average ratio in the

2010’s is one percentage point lower than in the 1950’s. At the beginning of 2030’s, however,

the dependency ratio is already 15 percentage points higher than the average for 1950’s.

The difference to the post-war quarter century is that the dependency ratio will not only

continue to climb higher, but it will also stay more permanently at a high level. Previously, high

dependency ratios were due to a large proportion of children, whereas in the future the reason

is a large proportion of aging and old population. The challenge of municipalities will be in their

responsibility to provide care for the elderly, and a rapid rise in related expenditure during the

2020’s, as the number of more than 80 years of age population is rising rapidly.

The rapid growth in pension expenditure, in turn, takes place in the 2010’s. But that does not

burden local government finances - not even in respect of municipal pensions, because the

pension system has prepared for this change in the form of advance funding.

Demographic dependency ratio at the municipal level

The demographic dependency ratio varies greatly between municipalities: in 2010, municipal

dependency ratios ranged from 40 to 90 per cent. By 2020, the ratios go up across the board so

that the range will be from 50 to over 100 per cent. While in 2010, there were no municipalities

with higher than 90 per cent dependency ratio, already in the year 2020, there will be 71 of

them (Figure 1). In 2020, the lowest ratio (47.8 per cent) will be in Helsinki. For a total of 20

municipalities, the ratio will exceed the 100 per cent limit in 2020.

In 2010, the municipalities, whose dependency ratio was less than 60 per cent, had a total

population which accounted for 80 per cent of the whole country's population. In 2020, the

corresponding figure is 36 per cent. In 2020, the municipalities with a dependency ratio of less

than 65 per cent will have 47 per cent of the country's total population. In 2020, the

municipalities for which the dependency ratio is less than 70 per cent, will have 60 per cent of

the country's population.

2 The dependency ratio measures over 65 year old plus under 15 year old population relative to 15–64 old population.

Figure 1. Demographic dependency ratios at municipal level in 2010 and 2020

© Municipal borders: Statistics Finland | © Municipal Guarantee Board 2012

Non-employed relative to employed people in the different municipalities

Thinking of municipal service delivery and the collection of tax revenue, in addition to

dependency ratio, it is essential to look at local economic dependency ratio, that is, how dig

share of the population is employed.

Throughout the first decade of 2000’s, the ratio of non-employed and employed was 120 per

cent.3 This means that for every hundred employed people, there were 120 persons outside the

labour force.

In the future, this figure will be 130 per cent during 2010–2020's; during 2030–2040's it is 140

per cent, and during 2050's it is 150 per cent. The ratio of non-employed to employed is thus

growing to the same level as it was between the wars.

At the municipal level, the ratio between non-employed and employed varied between

municipalities from 95 per cent to nearly 250 per cent in 2010. In 1990, the range was from just

above 70 per cent to over 190 per cent (Figure 2).

3 Employment rates are defined according to employment statistics.

Figure 2. Ratio of non-employed to employed persons at municipal level in 1990 and 2010, per cent

© Municipal borders: Statistics Finland | © Municipal Guarantee Board 2012

By applying employment rates of 2010, proportion of non-employed to employed ranges across

municipalities from 106 to 309 per cent in 2020 (Figure 3). By applying the 1990 employment

rates, the respective range for 2020 is 92–292 per cent.

By applying employment rates of 2010 to make estimates for 2020, and considering

municipalities where the ratio of non-employed to employed is over 200 per cent, their

population will be 590 000 people, which is 10.4 per cent of the country's population. By

applying the 1990 employment, the corresponding figure is 280 000 people, which id 5 per cent

of total population.

FIGURE 3. Ratio of non-employed to employed in 2020 calculated (i) with 1990 employment levels, and

(ii) with 2010 employment levels, per cent

© Municipal borders: Statistics Finland | © Municipal Guarantee Board 2012

In Finland, the deterioration in the dependency ratio over the long term, is a country-wide

problem, and it has to be solved as a problem concerning the whole country. What matters, is

not changing the administrative size of municipalities, but improving the employment rate.

Better employment would effectively negate the effect of increase in the dependency ratio for a

long time by preventing the growth in the number of non-employed in relation to employed

people. Also later, the increase in this ratio would be limited to low figures. Better employment

and concomitant overall increase in productivity can completely eliminate the effect of the

increase in dependency ratio.

3.1 Assessment criteria for financial management

As a central part of credit rating, S&P evaluates the practices and measures of municipal

management, as well as the municipality's ability and readiness to meet its financial obligations

on time. The assessment is based on economic documents of municipalities and discussions with

senior management.

S&P examines municipal management, policies, procedures, culture, and political characteristics

using the following nine categories (S&P 2010: 23–27): transparency and disclosure, budgeting,

long-term capital and financial planning, revenue and expenditure management, debt management,

reserve and liquidity management, management of government-related entities, political and

managerial strength (formerly referred to as "institutional and management legitimacy"), and

external risk management.

Each category gets a score on scale of 1–5, with 1 being very positive and 5 very negative (S&P

2010: 22–23). Scoring criteria are presented in Table 1.

Table 1. Scoring criteria for local governments’ financial management (S&P 2010: 22–23)

SCORING CRITERIA

1 VERY

POSITIVE

The LRG has very prudent fiscal targets backed by widespread political support and implemented by sophisticated management. It has transparent and well-defined financial policies reflected in reliable and public long-term planning and very good reporting. The management demonstrates a high degree of expertise, through very good planning and monitoring, prudent and well-defined debt and liquidity management, and active external risk management.

2 POSITIVE The LRG has prudent financial policies and practices that ensure a good degree of transparency and fiscal discipline through the electoral cycles. The management demonstrates relevant expertise, through good planning and monitoring, prudent debt and liquidity management, and some monitoring of external risks.

3 NEUTRAL The LRG has generally prudent financial policies, but they are frequently changed and may lack precision. The management is transparent and has adequate expertise, with good though not detailed planning and monitoring and generally prudent debt and liquidity management. But it may lack a comprehensive strategy to manage external risks.

4 NEGATIVE The LRG's financial management is underdeveloped in some areas. In a stress scenario, the government may lack the political strength to impose fiscal discipline. Reporting meets the legal standard but is not very detailed and timely. Planning and monitoring are limited. The management of debt and liquidity may be unpredictable to a degree, while any external risk mitigation is minimal.

5 VERY

NEGATIVE

The LRG has a weak financial and credit culture, including poor monitoring and reported information that meets just the minimum requirements to maintain a rating. A lack of political stability makes it difficult to impose fiscal discipline. The management lacks the relevant skills for planning and monitoring. The management of debt and liquidity is unpredictable and sometimes aggressive, while key external risks have not been identified.

3.2 Transparency and disclosure

To get the highest score (value 1) requires that local governments’ financial management is very

transparent. The financial report must be detailed and timely, and it must be published several

times a year. Financial reporting must be based on clear accounting standards and its

implementation must be flawless. The auditor must be an independent firm (S&P 2010: 23–24).

Local governments’ financial reporting

Municipal financial reporting and the checking of its legal accuracy are defined in Act. Municipal

accounts must be compiled in compliance with the Local Government Act and with the

Accounting Act and Regulation (Local Government Act, § 68).

The municipality's financial statements include balance sheet, income statement, cash flow

statement and the accompanying information, as well as budget comparison and annual report.

The annual accounts shall give a true and fair view of the results of municipality’s operations and

financial position. Needed additional information must be disclosed in notes. In addition, when a

municipality together with its subsidiaries forms a group, it must prepare and include in its

financial statements also a consolidated financial statement for the group (Local Government

Act § 68).

Financial statement and annual report must be drawn up in accordance with the Local

Government Act once a year. Municipalities usually monitor the implementation of the budget

2–3 times a year with interim reports or similar reviews. These describe the achievement of

operational and financial objectives, as well as an assessment of the whole year's events.

Municipalities monitor the achievement of economic goals continuously. Audit is done by an

independent auditor, who has official responsibility in carrying out auditing.

Although there are detailed instructions for municipal accounting, the comparison between

municipalities is somewhat challenging because, inter alia, municipal services are organized in a

variety of ways. A municipality can have, for example, shareholdings in energy companies. If

their shares are below 20 per cent, they need not be combined to the consolidated financial

statements. Dividends received may, however, be relatively significant, especially in revenues of

small municipalities. When comparing and assessing municipal financial statements, one should

also know how the results have been formed.

As a result of the above mentioned circumstances, consideration of municipal groups as a whole

has been continuously increasing, and municipal accounting is developing to the direction of

reviewing municipal groups.

3.3 Budgeting

In order to get the highest score for budgeting, it must be done on a fully consolidated basis,

including government-related entities where relevant. According to criteria, budgets must reflect

goals defined in long-term financial plan, and they must be based on realistic assumptions.

Budgeting must be efficient and continuous. This requires stability in the application of

administration’s measures and clearly formalized budgetary procedures. The budget must be

approved before the start of each fiscal year and eventual – only limited budget revisions – must

be done during the fiscal year. (S&P 2010: 24).

The municipality's activities and finances are directed by at least a three-year financial plan, in

which the first year is the budget year.

The Local Government Act requires municipalities to ensure adequacy of income financing and

liquidity preservation. The budget and the plan must allocate adequate resources to implement

the objectives set, and they must indicate how the activities and investments will be financed.

Planned activities and projects have to be realistic in relation to available resources.

The budget of a municipality and a joint organization of municipalities must have an income

statement and profit and loss statement as well as an investment and financing statement (Local

Government Act, § 65.4). In the budget of a municipal enterprise, there must be an income

statement, and investment and financing statements (Local Government Act 87.2 e § and 87.2 f

§). Entities in municipal groups prepare their own budgets, and they cannot be combined to

municipal figures.

Financial plan must describe the measures how to cover accumulated or current fiscal year’s

deficits. A formal annual income and expenditure balance is not required. The budget and the

plan bind municipal institutions and personnel, and at the same time they are tools of control

and supervision. Amendments to their budgets are decided by municipal councils and councils or

boards of joint municipal organizations. (Local Government Act, § 65.5). Amendments to budgets

of municipal enterprises are decided by their Executive Boards (Local Government Act 87.5 e §

and 87.5 f §).

3.4 Long term capital and financial planning

According to credit rating criteria local governments’ economic policy should be sensible,

thoroughly defined and stable: it should remain largely unchanged over the individual

legislatures. This requires a detailed long-term plan, which defines the main revenue targets.

Income and expenditure assessment has to be realistic and documented in detail. Political actors

must be committed to implement financial discipline. (S&P 2010: 24).

Basic Service Procedure and Basic Services Programme4

Economic policies of local governments are outlined by basic service procedure as stated in

Local Government Act. According to the Local Government Act, municipal administration, as well

as central government and local public finance issues are dealt with in a negotiation procedure

of state and local authorities. The outcome of the negotiating procedure is a basic service

program and an annual budget of basic services. The basic service procedure is led by a group of

ministers. The Association of Local and Regional Authorities represents municipalities.

The basic service program assesses changes in the tasks of municipalities, municipal economic

development as part of the public finances, as well as local government funding. On this basis, a

proposal of measures to balance expenditure and revenues is made. If the current account

deficit cannot be covered during the planning period, an action plan is made on measures to

cover the deficit. On the basis of the principle of balance, the commitments and risks of

municipalities must not exceed their capacity. A particular risk is associated, for example, with

loan guarantees and –collateral to entities that are not controlled by the municipality.

4 The basic service procedure is described in detail in Part I of Finnish local government institutions and creditworthiness.

3.5 Revenue and expenditure management

The credit rating criteria require from municipalities successful economic forecasts, as well as a

steady income and expenditure control. Municipalities must also ensure that units receiving

eventual state grants use this funding effectively. Only insignificant overrun of the budget is

possible, and it must be corrected within a year. (S&P 2010: 25).

Comparison of the budget and actual results

According to the Local Government Act § 68 the municipality's financial statements must include

a comparison on how the budget has realized. Budget monitoring in municipalities is ongoing,

and it takes place both at the level of municipal bodies and public servants. A broader type of

interim report, which examines the fulfilment of functional objectives and evaluates the budget

outcome for the whole year, is normally prepared 2–3 times a year, in addition to annual

financial statements.

Goals are part of the budget and binding in the sense that they are to be implemented. If the

goals are not achievable because of fundamental economic changes, the council must also

approve changes in the objectives.

Sometimes, the municipality may incur expenditure the amount of which is difficult to estimate

in advance. For example, particularly expensive treatments in specialized medical care may

affect the individual municipality’s economy unpredictably. In this case, the budget may need to

be adjusted during the fiscal year.

State grants to municipalities and the tax base equalization system

The above-described basic service procedure and, as part of it, state grants to municipalities

account for about 19 per cent of Finnish municipalities expenditure (in 2011 figures). Most of

local government revenue (81 per cent), especially tax and fee income, are based on local

conditions, which the above-described procedure does not take into account systematically.

To correct for this defect, there is a tax equalization system. The equalization system is designed

to ensure that municipalities operating in different economic conditions are able to provide basic

services to their residents equally.

State grants are determined by using formulas, and they are granted to municipalities without

application. The majority of grants are based on factors, which include population, quantities of

services, evaluated needs for services, and on costs of service provision in various circumstances.

State grants are not based on actual expenditure or costs of municipalities and they cannot

affect the amount of grant received. The state contributes in the financing of services in

accordance with state’s percentage share. The municipal part of costs (self-financed share) is

equal to all municipalities in terms of per capita costs.

Central government grants are lump sum grants. They are not earmarked for any specific

services, but the municipalities can direct the use of grants to whatever purposes they desire.

Preparatory work to amend the state grant system has been initiated in 2012. The aim of the

reform is to increase the computational nature of the system in order to encourage

municipalities to greater efficiency.

Municipalities in particularly difficult economic situation

In principle, the basic service procedure should ensure a balance to the economies of all Finnish

municipalities, for each and every one of them. Since individual municipalities may face special

economic difficulties, which the basic service procedure does not recognize, it has been

complemented by a procedure designed for municipalities in particularly difficult circumstances

(framework law 169/2007 § 9).

There is an evaluation process, which is applied to municipalities, in which the adequacy of

funding and solvency ratios are substantially and consistently weaker than the corresponding

national figures, and have for two consecutive years been below the limit values laid down in a

related government decree.

The thresholds are undercut, if in two years in a row (i) the accumulated deficit as €/inhabitant

in the last approved financial statement was at least € 1 000 and year before at least 500 €, or

(ii) all of the following criteria are met:

the operating balance of the municipality is without discretionary financial assistance < 0

the municipal income tax rate is at least 0.5 percentage points higher than the weighted

average income tax rate of all municipalities

the loan amount (€/inhabitant) exceeds the average loan amount of municipalities by at least

50 per cent

there is accumulated deficit in the balance of the municipality

the equity ratio of the municipality is less than 50 per cent

the relative indebtedness of the municipality is at least 50 per cent

The evaluation procedure was carried out in 25 municipalities during 2007–2010. In all 13

municipalities merged to another municipality. Many municipalities, which have been on the list

of problem municipalities, have applied for and received the so-called discretionary assistance.

By increasing the state discretionary aid to problem municipalities, the government has aimed to

ensure that, even in the toughest financial position being municipalities are able to provide basic

services and they have been able to improve their financial balance. There are also

amalgamation subsidies which aim to give an incentive to amalgamate on a voluntary basis. The

funds for these purposes are determined annually in the state budget.

3.6 Debt management

To get the highest score, S&P requires that municipalities conduct very sensible debt

management. Long-lasting debt must be targeted to investments, not to operating expenses.

The debt ratio must be clearly lower than the national figure. Highest score calls for advanced,

proactive and risk-averse economic policies, where the primary aim should be to minimize the

risks, and cost reduction should be a secondary target. Currencies must be protected against

exchange rate fluctuations, interest rate risk must be restricted to a minimum, and the share of

short-term loans must be small. (S&P 2010: 25).

Financial balance and indebtedness of municipalities

In Finland, municipalities have the right, independently from central government, to use debt to

fund their activities. In addition to the amount of debt, also the choice of debt instruments can

be determined locally.

Municipalities and their joint organizations have used debt finance mainly to finance

investments. Financing of operating expenditure by debt has been exceptional.5 The gross debt

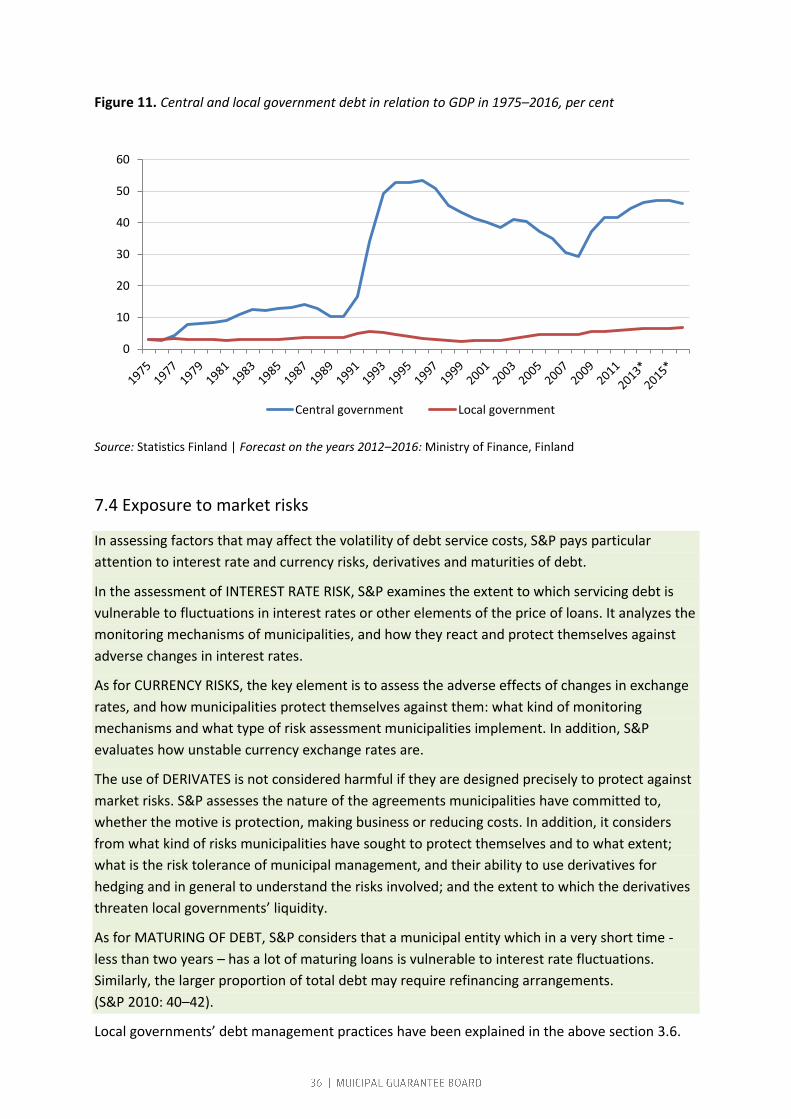

of Finnish municipalities and their joint organizations at end of year 2010 was 11.7 billion euro,

which is about 6.5 per cent of Finland's GDP. Current debt-equity ratio is close to the average for

the years 1971–2010.

Finnish municipalities’ right to decide about their indebtedness has effectively prevented moral

hazard that would be obviously present, if indebtedness could only take place within limits

regulated by the central government. State or central government regulation would constitute a

tacit promise that the state or the central government bodies would take responsibility of debts

if the debts would be subject to regulation.

In case of moral hazard type behaviour, the central government imposed limit would, in actual

fact, become the lower bound for indebtedness. This development has been blocked in Finland

by the autonomy of municipalities to determine their indebtedness.

3.7 Management of assets and liquidity

S&P's rating criteria require that the municipality has clear procedures for maintaining liquidity. Cash

balances and other similar funds must have a minimum level. Assets should be a wise combination of

liquid items and own cash. Highest scoring also requires a detailed annual plan and corresponding

plan based cash-flow management, and accurate daily monitoring. Cash and debt management must

be integrated and managed by experts. All administrative units must have centralized cash

management. (S&P 2010: 25–26).

The sufficiency of municipalities’ funding is shown by the annual cash flow statement, which

municipalities prepare in connection of the budget and financial report. There are no binding

guidelines for liquidity or cash management plans. In practice, municipalities make monthly cash

plans and daily cash budgets.

Minimum cash level requirements are not nationally defined. For securing sufficient liquidity in

municipalities, usually cash money to cover 10–15 days expenses is sufficient. Investment

related expenses, however, may temporarily require larger cash reserves. On average,

municipalities’ cash is sufficient to cover 40 days’ expenditure.

When taking a loan, interest rate development is usually monitored. When interest rates are

falling, it may be advantageous to postpone taking a long-term loan and to finance the

investment initially with a short-term loan. As a rule, long-term loan is taken to finance an

investment, and by the use of short-term loans, liquidity is maintained.

Local authorities have organized their liquidity through the joint municipal funding system

formed by Municipality Finance Plc and Municipal Guarantee Board.

5 The amount of operating expenses, which municipalities have been forced to finance by debt or selling property, was

approximately 40 million euros for the period 1997–2010.

3.8 Management of local government related entities

According to the credit rating criteria, there must be a reasonable cause for the existence of each

municipality related entity or company. The reason may be, for example, more efficient organization

of services, or access to private funding. It also requires that the nomination process of the

company's board of directors is transparent, and that the CEO’s selection process is open. The action

plans of municipal enterprises must be in-depth and linked with the municipal financial plans.

Companies need to cover their costs from their own revenue sources or from fees and payments

received from the municipality. The companies shall provide public services according to an

agreement with the municipality. (S&P 2010: 26).

The Association of Finnish Local and Regional Authorities has prepared recommendations for

municipal ownership policy and good management and governance practices. This guidance is

intended to harmonize practices, improve the transparency of subsidiary entities and to ensure

that organizations comply with good corporate governance and management practices, as well

as to protect the interests of the owner municipality.

The annual report of the municipality must consider shortly, how the control of the whole group

of entities is organized in the municipality. In addition, it must include information on such key

issues of group that is not directly visible in consolidated financial statements.

3.9 Political strengths and leadership skills

According to credit rating criteria, the municipalities must be capable of complying with strict fiscal

discipline. A prerequisite for this is that the dominant political party has wide decision making power

or alternatively that there is widely accepted joint view on local economic policy. Authorities must be

able to implement structural changes, approve the budget and make unpopular decisions, too.

Highest score requires a very strong management team, which has very relevant experience and

qualifications. (S&P 2010: 26–27).

Municipalities’ political and other control in cooperation with other joint organizations

A significant part of local government functions is realized outside the municipality in various

joint organizations. In this context, we can speak of political guidance, owners’ control and

corporate governance. The most significant form of cooperation between municipalities

according to the Local Government Act is a joint organization. Statutory joint organizations

consisting of all municipalities are of three types. They include hospital districts (20), special

service districts (16) and Regional Councils (18). In addition, Finland has 82 voluntary joint

organizations of municipalities, including joint organizations in the fields of education and public

health. Three-quarters of all joint organizations’ expenditure are related to the provision of

health care.

In the conduct of business type activities, suitable forms of cooperation are limited liability

companies, cooperatives and foundations. Local authorities have set up joint companies in such

areas as waste management, business services and travel. In a limited liability company, the

owner is represented by the General Meeting. The Corporation Board must act pursuing the

interest of the company and its owners.

Finland does not have a system which monitors systematically municipal companies.

3.10 External risk management

A good external risk management requires that the most significant external risks have been clearly

identified, and they are followed by a comprehensive and credible risk management strategy. Top

management should receive regular updates on political decisions. Highest score also requires that in

financial stress situations municipalities have financial flexibility. Local authorities must be prepared

to reduce public services, if economic viability is at risk. (S&P 2010: 27).

In line with general guidelines concerning financial statements and annual reports, municipalities

must assess significant risks and uncertainties and other factors affecting the development of

their activities in their financial statements. In addition, there must be a description of how the

municipality's internal control and risk management is organized in each municipality: whether

deficiencies were found, and how internal control is designed to be developed during the

current economic planning period.

All municipalities do not have in use a comprehensive and documented risk management

system, which would enable reliable collection of information that could be presented in the

annual report. Municipal risk management and internal control has been boosted by an

amendment to the Local Government Act. As a result of the reform, the municipal council must

decide and report on principles of internal control and risk management in the municipality and

the related group in its financial statements by 2014. The auditor should check that the internal

control and risk management of the municipality and the group are properly organized.

The main risk is associated with the municipal economy, especially with financing of service

provision. Although local authorities have increased efficiency in their operations, curbed the

growth in expenditure and increased their taxes, the basic problem is that local government

spending rises faster than income. Expenditure growth is explained by the economic slowdown,

the increase in the number of municipalities’ tasks and high costs, and particularly by the growth

of health care expenditure as the number of elderly people increases.

Municipalities have varying ability to meet the economic challenges and finance the service

provision, which has been delegated to be their duty by national law, at reasonable burden of

local (mainly income) taxation. Flexibility of municipal budgets is discussed in more detail in

Chapter 4.

4.1 Criteria for assessment of budget flexibility

Budget flexibility measures how much local governments can increase their revenues or reduce

their costs in order to service their costs of debt.

Budgetary flexibility is emphasized especially at a time when public finances are under external

pressure. If the municipal budget is flexible, it will be better able to adjust revenues and

expenditures when faced with external economic shocks, and to ensure their ability to cope with

debt-servicing costs. The shocks can be economic downturns or administrative changes. (S&P

2010: 31).

S&P assesses flexibility both qualitatively and numerically from two perspectives: by looking at

municipal economies’ ability and the possibility to strengthen their revenue base, on the one

hand, and on the other hand, to cut expenditure. In its assessment, S&P examines these two

elements using three different criteria.

According to S&P REVENUE FLEXIBILITY depends on (i) municipalities’ possibility of increasing

the tax rate, fees or tariffs; (ii) sufficient political will and economic limits that could curb the use

of flexibility, and (iii) potential revenue from the sale of assets.

As for EXPENDITURE, S&P examines the relationship between investment and total expenditure

and assesses (i) operating expenditure flexibility, (ii) capital expenditure flexibility, and (iii)

potential sources of pressure to make cuts. (S&P 2010: 27–29).

In order to get the highest score (value of 1) requires that the share of modifiable revenues in

adjusted operating revenue is more than 70 per cent, and that the share of modifiable

investment expenditure in total expenditure is more than 15 percent (S&P 2010: 30).

In addition to numerical assessment, S&P also considers qualitative factors that may affect the

evaluation of budget flexibility.

If the municipality considered shows that it can and it is ready to cut operating spending, in the

S&P's assessment, this can increase the numerical score of the municipality. Other factors

include the ability to increase operating revenues, postpone investments, and get more than the

average income by selling assets.

Factors which lower the score include very limited room for manoeuvre in increasing operating

revenue - for example, due to already high tax rates - and in general a weak ability to cut

expenditure. (S&P 2010: 29–30).

4.2 Municipalities’ revenue adjustment

According to S&P's definition, municipalities’ adaptable revenues include taxes, fees and rents:

they are of such a nature that the municipalities can adjust their level if necessary. By calculating

the ratio of adaptable revenue to total revenue S&P evaluates the municipalities’ tax base

flexibility. It seeks to explore, what is municipalities’ current level of taxation in relation to the

statutory maximum level, and how much municipalities have room for maneuver in terms of

taxation.

Budget flexibility or lack of flexibility can also be affected by political priorities and the

competitive situation. For example, is a significant departure of municipal tax rate from the

national or regional average may be a sign that the municipality is under pressure to cut tax rate.

A restriction on revenue growth may also be a political decision. In general, factors forming

financial constraints may include low income of the population, or a weak tax base.

Local governments’ property that can be liquidated typically means shareholdings in commercial

companies or residential and other properties. The sale of such property can produce large-scale

non-recurring revenue to the municipality. On the other hand, such an asset sale can be difficult

because of political resistance. Selling may also have legal obstacles, and finding buyers is not

necessarily easy. (S&P 2010: 28).

Economic flexibility of Finnish municipalities

Flexibility of municipal economies can be viewed from many angles. The starting point is that

each municipality is a financially independent entity, which is responsible for its own finances.

Municipal economic development is affected by many external factors, which are beyond the

control of local governments. On the other hand, municipalities have a high degree of

independence concerning their functions and financing.

Looking at local government as a whole, one boundary condition for municipalities is the overall

economic development, which the central government seeks to influence, inter alia, by

measures that affect local revenue and expenditure. Local revenue is affected mainly through

the tax system and grants. Local expenditure, in turn, is mainly influenced by legislation.

The state also takes measures which affect personnel expenditure at local government level.

Economically, the most important decisions on personnel expenditure, however, are made by

the public sector related trade unions and local government units.

In addition, the European Union has become more active in fiscal governance of the whole

public sector in recent times. The financial targets of the Stability and Growth Pact concern also

municipalities as part of the general government. In 2011, came into force a Budget Framework

Directive which requires that member states strengthen the management of entire public sector,

and take note of the Stability and Growth Pact rules. The basic service procedure is one of the

tools to promote stability in the local government sector.

Local government (municipalities and their joint organizations) revenues

S&P's concept of OPERATING REVENUES consist of local government (here municipalities and

their joint organizations) operating income, tax revenue, state subsidies, and interest and other

financial income. In all, their total amount in Finland was approximately EUR 38.5 billion in the

year 2011. During the time interval 1997–2011 operating revenue grew by an average of 4.6

percent per year, or about 1.9-fold (Table 2, Figure 4).

Local governments’ OPERATING INCOME includes the sale of goods and services, sales, customer

payments and fees, subsidies and aid from other sectors, as well as rental income from

apartments, buildings, and land and water areas. In 2011, operating income amounted to EUR

11.2 billion, or about 29 percent of total operating revenue. Operating income increased by an

average of 4.8 percent per year, slightly faster than total operating revenue.

Table 2. Local government revenues during 1997–2011, at current prices (billion €)

Source: Statistics Finland, Finances and activities of municipalities and joint municipal boards

Figure 4. Local government revenues during 1997–2011 (1997=100)

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011* AVG annual

percentage

change

Operating revenue 5,80 5,97 6,16 6,39 6,64 6,99 7,45 7,89 8,30 8,81 9,12 9,75 10,07 10,90 11,21 4,8

Tax revenue 11,00 11,80 12,11 12,92 14,10 14,08 13,50 13,68 14,26 15,17 16,30 17,53 17,61 18,35 19,07 4,0

State grants 3,33 3,18 3,19 3,35 3,67 3,89 4,29 4,74 5,07 5,50 5,76 6,43 6,91 7,43 7,66 6,1

Interest and other

financial revenue 0,38 0,39 0,42 0,39 0,40 0,36 0,36 0,39 0,43 0,48 0,55 0,55 0,53 0,55 0,57 2,8

(1) Total revenue 20,51 21,34 21,87 23,05 24,82 25,31 25,61 26,70 28,04 29,95 31,73 34,26 35,12 37,23 38,51 4,6

LOCAL GOVERNMENT TAX REVENUES include local income tax, property tax, and a share of

corporate income tax revenue, as well as an economically marginal dog tax. According to

financial statements in 2011, local tax revenues were nearly 19.1 billion euros, or almost exactly

half of total revenue. Tax revenues have increased on average by 4 percent per year.

Municipalities have a broad right to collect taxes, and in particular this applies to earned income.

Municipalities decide independently their tax rate for earned income. The weighted average of

municipal earned income tax rates was 19.16 per cent in 2011 and 19.25 percent in 2012. The

range of tax rates in 2012 is from 16.5 to 21.5 per cent.

Municipal income tax is affected, besides the development of earned income, as well as by

various deductions which are decided by the state. In recent years, deductions both from earned

income and directly from taxes have significantly increased, and this has slowed down the

growth of municipal tax revenue.

Municipalities decide upon their tax rates in November for the forthcoming budget year. The tax

percentages cannot be changed during the fiscal year, and thus local governments’ must react to

unexpected economic changes in other ways.

There is no upper limit to municipal earned income tax rate: in principle, municipalities can raise

the tax rate at their discretion. The barriers are mainly related to local politics. Residents may

perceive the tax rate or even the property tax level to be too high. This is known as the so-called

political tax ceiling.

Also, the state tries to act so that the tax rates would no rise significantly as a result of local

measures. The national overall tax rate has, as a matter of fact, decreased in recent years. Local

tax revenue as a share of GDP has remained roughly constant, around ten percent.

As already explained in Section 2.3, the municipal earned income tax has some room for

maneuver: the average municipal part of the tax rate may be increased close to 25 per cent. In

addition to earned income tax, the municipalities have the opportunity to tighten property

taxation and special taxes, and impose various mandatory fees.

LOCAL SALES PROCEEDS are revenues from sale of goods and services; they are meant to be

offered for sale usually at a price that covers the cost of production. Proceeds from the sale will

be affected, in addition to the measures taken by municipalities, also by the market situation.

MUNICIPAL FEE REVENUE refers to user fees and payments for goods and services in cases

where pricing is not intended to cover the full costs of production, or the prices are determined

taking into account the customers’ ability to pay. Typically, these fees are laid down by law or

regulation. Examples of such fees are social and health care payments (Law on the Social and

Health Care Fees), gate fees (Waste Act), environmental and land use fees (Land Use and

Building Act), as well as education payments (basic education, upper secondary and vocational

education of the Act).

Out of all local government expenditure, approximately 20 percent is covered by fees (5%) and

revenues from sales (15%). Charges levied by the municipalities are either based on private law

and as such subject to contracts or they are based on the laws concerning public entities.

The latter include building inspection and supervision fees, gate fees, as well as social and health

care fees. Private litigation fees include such as water and waste water charges, electricity,

heating and other energy charges, various entrance fees, mooring fees, as well as tuition fees

which are not regulated by the law.

A number of charges have a legally regulated upper limit, which local governments

(municipalities and their joint organizations) cannot exceed. Such payments include, among

other things, the clients’ fees for social and healthcare services and other fees which are

regulated by an Act on clients’ fees.

STATE GRANTS TO LOCAL GOVERNMENTS include grants based on agreements between the

State and municipalities about cost-sharing of basic service provision. Grants from central

government were according to local government accounts 7.7 billion euros in 2011. They have

increased rapidly, on average by 6.1 per cent per year, partly also because the central

government has compensated for local tax revenue reductions caused by increases of

deductions in taxation. Without these compensations, which amounted to EUR 1.8 billion in

2011, the average annual increase in grants would have been about four per cent a year. As

indicated below, municipalities cannot really affect the amount of grants they get from central

government.

INTEREST AND OTHER FINANCIAL REVENUES amounted to about half a billion euro in 2011. Their

changes are influenced, among other things, by the amount of financial resources and the level

of interest rates.

Local government-owned enterprises and their turnover

The local government sector's consolidated financial statements do not have information about

total revenue of local government and companies owned or controlled by municipalities in such

a way that their interim transactions would be cleaned away. Therefore, in Table 3 and Figure 5,

there is only time series concerning the turnover of municipal-owned enterprises in the period

1997–2010.

The time series is based on Statistics Finland's annual Business Register’s statistics. It includes

firms and offices that have been operating for more than half a year annually, and their annual

turnover has exceeded a specified statistical threshold.

Published statistics do not make it possible to estimate the percentage of turnover which has

occurred with other municipal actors like municipalities and their joint organizations.

In the future, attempts to assess business transactions between municipalities and their firms

will be made. Local governments own, for example, a number of energy companies, which

supply energy to municipalities. These energy operators' share of total turnover has been about

two-thirds.

Table 3. Local government revenues and the turnover of government related enterprises during 1997–2011, at current prices (billion €)

Source: Statistics Finland, Finances and activities of municipalities and joint municipal boards, Statistics on Finnish Enterprises

FIGURE 5. Local government revenues and the turnover of government related enterprises in 1997–

2011 (1997=100)

Turnover of local government related companies increased over the 1997–2010 period on

average by 11 percent a year. Their turnover has tripled during the term. The reason for this has

been the rapid growth of industries, and the number of such companies has doubled. Also, the

number of employees of these companies has increased rapidly, inter alia, because of

incorporations.

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011* AVG annual

percentage

change

LGs:

Total revenue 20,51 21,34 21,87 23,05 24,82 25,31 25,61 26,70 28,04 29,95 31,73 34,26 35,12 37,23 38,51 4,6

GREs:

Turnover 1,95 2,09 1,83 1,89 2,10 1,91 2,17 2,23 2,45 2,87 3,30 4,04 4,87 5,72 10,9

incl.

-electricity, gas and heat services 1,26 1,23 1,43 1,25 1,44 1,42 1,48 1,88 2,16 2,60 3,21 3,76

-other fields of operation 0,57 0,66 0,68 0,66 0,74 0,81 0,97 0,99 1,14 1,43 1,66 1,96

Number of GREs 625 659 847 904 944 959 993 1 007 1 030 1 049 1 063 1 250 1 290 1 428 4,9

Personnel (*1 000) 12,52 12,71 14,05 14,08 13,51 12,36 12,52 12,96 14,32 15,50 17,31 19,79 21,79 27,14 6,2

4.3 Cutting local government expenditure

S&P notes that cutting of municipal operating expenditures is generally challenging. Often, the

expenditure are of such a nature that they cannot be cut - such as interest expenses, pension

contributions or other statutory expenditures for which municipalities are responsible. In case of

some expenditure items, in theory, there is flexibility, but cuts can be difficult to make for

political reasons. These include, for example, employees' salaries or education and health care

expenditure.

Also, capital expenditures are generally difficult to cut- especially if they result from a

construction project in progress or, if there are necessary investments in infrastructure ahead.

On the other hand, often investments also represent a positive impulse on the economy,

especially in recovering markets, and municipal tax revenues typically increase over the long

term.

Expenditure-cutting can lead to challenges, especially in situations where expenditure should

rather be increased: for example, when population increases, the municipality is under pressure

to increase services or to invest in infrastructure. According to S&P, municipalities’ expenditure

elasticity depends in part on how the most important service responsibilities of municipalities

have been defined. Cutting expenditure in education and health is generally more difficult than

for street lighting, for example. (S&P 2010: 28–29).

Local governments’ operating expenditure

Local governments’ operating expenditure include personnel costs, services and material

purchases from outsiders, grants and subsidies to households and communities, as well as other

operating costs. These include, for example, rental costs, eventual taxes or sales losses. When

the above-mentioned operational expenditure items and financing costs are summed up, this

corresponds to S&P's concept of operating expenditure (Table 4). They amounted to

approximately EUR 36 billion in 2011. This is 2.5 billion less than operating income in the

corresponding year, see Table 2.

Table 4. Local governments’ operating expenditure during 1997–2011, at current prices (billion €)

Source Statistics Finland, Finances and activities of municipalities and joint municipal boards

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011* AVG annual

percentage

change

Operating expenditure 18,14 18,67 19,20 20,20 21,64 22,75 23,78 25,01 26,30 27,52 28,90 31,18 32,48 33,85 35,48 4,9

incl.

-Personnel expenditure 11,63 11,96 12,26 12,78 13,58 14,24 14,85 15,49 16,17 16,78 17,55 18,60 19,05 19,48 20,32 4,1

-Purchases of services 2,48 2,66 2,86 3,23 3,59 3,87 4,11 4,55 4,88 5,28 5,78 6,55 7,29 7,99 8,59 9,3

-Other operating expenditure 4,02 4,04 4,08 4,19 4,47 4,64 4,82 4,97 5,25 5,46 5,57 6,02 6,14 6,37 6,58 3,6

Interest and other financial

expenditure 0,43 0,43 0,32 0,34 0,34 0,31 0,24 0,25 0,26 0,33 0,44 0,68 0,34 0,36 0,48 0,8

(3) Total expenditure 18,57 19,09 19,52 20,54 21,98 23,05 24,02 25,26 26,57 27,85 29,34 31,86 32,82 34,21 35,96 4,8

Figure 6. Local governments’ operating expenditure during 1997–2011 (1997=100)

PERSONNEL EXPENDITURE was the most significant expenditure item for the reporting period.

They accounted for nearly 60 percent of all operating expenditure. Personnel expenditure

increased on average by 4.1 percent per year. Earnings in local government sector increased on

average by 3.5 percent per year, which explains most of the increase in personnel expenditure.

According to National accounts, the number of employees in local government increased from

1997 to 2011 by about 42 000 people (on average by 0.7 percent per year). The number of

employees was about 464 000 in 2011.

In mid-1990s, municipalities and their joint organizations resorted to temporary lay-offs, and

even dismissals of municipal personnel. During so called PARAS-reform project (ends by the end

of 2012), such measures have been relatively rare. In the local government sector, personnel

expenditure is largely determined by collective agreements between labor market organizations.

Municipalities and their joint organizations have as employers the opportunity to make local

agreements.

PURCHASES OF SERVICES include purchases of customer services from other producers, as well

as services which the municipalities use in their own service production as input. Purchases of

customer services have grown particularly rapidly in recent years. Mutual purchases between

local government units have been eliminated in the calculation.

The value of purchased services increased on average by 9.3 percent per year, becoming 3.5-fold

during the period considered. This represents about 5.5 per cent annual quantitative growth,

when increases in earnings and other cost increases have been taken into account. Other

operating expenditure grew moderately during the review period.

INTEREST AND FINANCIAL EXPENDITURE has remained at less than half a billion euros over the

period considered. An exception is the year 2008. At that time, as a result of rising interest rates

and increase in borrowing, interest and financial expenditure increased exceptionally close to

700 million euro. As a result of low interest rate the nominal amount of interest and financial

expenditure in 2011 was at the same level as at the beginning of the period considered.

5.1 Evaluation criteria for budget execution

In the evaluation of budget execution S&P examines in particular the two key figures: (i) the

operating balance6 as a percentage of adjusted operating revenues and (ii) the balance after

capital accounts as a percentage of total adjusted revenues.

The highest score (value 1) requires that the operating balance is not negative, and that the

annual balance as a percentage of adjusted operating revenues is at least 5 percent.

In addition, S&P considers qualitative factors that can increase or decrease the score for budget

execution.

Expected structural reforms compared to the average and significant cash reserves of local

government may increase the numerical score.

Expected structural declines and volatility of functions, which are associated with high inflation,

excessive income seasonality, dependence on state grants or exposure to risks, in turn, reduce

the numerical score. The score also is also reduced if there is underestimation of disbursements,

resulting from significant under-consumption, unpaid debt or financing through public

undertakings, which does not appear in the municipal budget. (S&P 2010: 31–33).

5.2 Annual operating balance as a percentage of operating revenue

Annual operating balance in proportion to the operating revenue reflects the extent to which a

municipality can finance its expenses and public services with recurring revenues, typically with

tax revenue, operating income and subsidies.

High operating balance (more than 5 per cent of operating revenue) indicates that the

municipality has self-financing capacity that it can use to partially or fully fund its capital

investments. Low operating balance (less than 5 per cent), in turn, indicates less self-financing

capacity, and suggests that the municipality is more vulnerable to prolonged recession or to

unexpected economic shocks.

Persistent operating deficits indicate that a municipality would normally need to use debt to

fund every day operations. We note that such a situation is generally not sustainable in the long

term and could indicate that the municipality’s revenue base may not be sufficient to sustain its

range of services, or it can indicate management's lack of willingness to address structural

imbalances.

S&P also analyses the accrual operating balance because indicates whether the municipality’s

revenues can also cover the accumulation of noncash liabilities and the maintenance of capital

stock. (S&P 2010: 31–33).

6 S&P's operating balance corresponds (almost) to the annual operating balance in the Finnish accounts. The difference to

Finnish balance concept is the item "production for own use" and previously relevant item "VAT recovery." Note also that according to S&P operating balance = adjusted operating revenues [minus] adjusted operating expenditures; but here operating balance = operating revenues [minus] operating expenditures.

Local governments’ annual balance, depreciation and investments

According to S&P, the operating balance can be obtained as the difference between adjusted

operating revenues and adjusted operating expenditures. It corresponds approximately to the

Finnish municipalities’ operating balance based on their profit and loss account.

The operating balance tells about sufficiency of internal financing. It shows the cash flow, which

after payment of current expenditure is left available for investments and repayments of loans.

Typically, the annual balance can vary from one year to another.

Finnish municipal sector actors relate the annual balance to municipalities’ depreciations and

depreciable investments. In this thinking, the basic assumption is that the operating revenue is

sufficient, if the operating balance is at least equal to the depreciation of fixed assets. If the

operating balance covers depreciation, the municipality does not need to incur debt, liquidate

fixed assets or reduce its margin.

On the national level the operating balance has been enough for depreciations throughout most

of the period, with the exception of a few years (Table 5, Figure 7).

Table 5. Local governments’ operating balance, depreciation and investments during 1997–2011, at current prices (billion €)

Source: Statistics Finland, Finances and activities of municipalities and joint municipal boards

Local government investment expenditures are mainly related to maintenance and renewal of

the municipal infrastructure. Depreciable investments include inter alia day care centers,

schools, hospitals, elderly care facilities, and other buildings, streets and cable networks, as well

as machinery and equipment. Non-depreciable investments include acquisition of land and

water areas, as well as stocks and shares.

In the period under review, investment expenditure increased on average by nearly 5 percent a

year. The exceptionally high level of investment expenditure and income in 2010 is explained by

the transactions of municipalities in the Helsinki metropolitan area when they organized their

environmental administration. Investment income accounts between 20 and 50 per cent of the

financing of investment expenditures.

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011* AVG 97-11 or

AVG annual

percentage

change

(4) Operating balance 1,25 1,49 1,58 1,70 1,95 2,26 1,58 1,44 1,48 2,10 2,39 2,40 2,31 3,03 2,54 1,97

Depreciations 1,22 1,27 1,36 1,42 1,45 1,56 1,61 1,69 1,76 1,78 1,84 1,94 2,04 2,16 2,23 4,4

Operating balance/depreciations % 103 117 116 119 135 145 98 85 84 118 130 124 113 140 114 116

(5) Total capital expenditures 2,28 2,50 2,33 2,85 3,04 3,00 3,20 3,29 3,23 3,55 3,79 4,13 3,99 5,69 4,31 4,7

(5a) Depreciative investments 2,00 2,09 2,03 2,29 2,53 2,63 2,78 2,89 2,88 3,09 3,25 3,70 3,47 4,45 3,53 4,2

Operating balance/

depreciative investments 63 71 78 74 77 86 57 50 51 68 73 65 66 68 72 68

(6) Total capital revenue 0,57 0,80 0,99 1,17 0,70 0,89 0,87 0,84 1,14 1,78 1,11 1,12 0,91 2,67 0,99 4,0

Capital expenditure/Capital revenue % 25 32 43 41 23 30 27 26 35 50 29 27 23 47 23 32

Figure 7. Local governments’ operating balance relative to depreciations and depreciable investments, and the ratio of capital revenue to capital expenditure, %

5.3 Balance after capital accounts

By considering the annual balance after capital accounts, S&P seeks to determine (i) the extent

to which local authorities are able to generate revenue to maintain their ability to function

without relying to any outside sources of funding, and (ii) the amount of cash flow that goes to

investments (S&P 2010: 32).

Local governments’ annual balance after capital accounts operations and cash flow from investments7

Annual balance after capital accounts is an item of cash flow statement, which is obtained by

subtracting from the operating balance net investments and by taking into account

extraordinary items in net terms, and adjustments to operating revenue (Table 6). Extraordinary

revenue and expenses are those, which are based on events that are extraordinary, non-

recurring and essential for the municipality. Adjustments to operating revenue include

corrections to operating balance, such as capital gains or losses which have been included on

revenue or expenditure side.

7 This series describes the balance, which is obtained by subtracting Table 5, according to the functional being stranded in

the [operating balance], the annual margin capital expenditure [capital Expenditure] and increasing income from capital [capital revenues]. The table below shows the time series is constructed municipal accounts based on the concepts.

Table 6. Local governments’ operating balance after capital accounts operations, and cash flow related to investment activities during 1997–2011, at current prices (billion €)

Source: Statistics Finland, Finances and activities of municipalities and joint municipal boards, Annual national accounts

In Figure 8 time series for local governments’ annual balance after capital accounts operations is

compared to changes in their debt portfolio. During the time interval, the time series’ average

absolute values are almost identical, i.e. the fifteen-year averages of the absolute values are a