Kig Hir 2015

20

Jour nal of Financial Reporti ng and Accoun ting Corporate cash flow and dividends smoothing: a panel data analysis at Bursa Malaysia Apedzan Emmanuel Kighir Normah Haji Omar No rhayati Mohamed A r t i c le inf or m at ion: To cite this document: Apedzan Emmanuel Kighir Normah Haji Omar No rhayati Mohamed , (2015),"Corpor ate cash flow an d dividends smoothing: a panel data analysis at Bursa Malaysia", Journal of Financial Reporting and Accounting, V ol. 13 Iss 1 pp. 2 - 19 Permanent link to this document: http://dx.doi.org/10.1108/JFRA-09-2013-0072 Downloaded on: 04 February 2016, At: 00:27 (PT) References: this document contains references to 28 other documents. T o copy this document: [email protected] The fulltext of this document has been downloaded 368 times since 2015* Users wh o down loaded thi s article also downl oaded: Awad E lsayed Awad Ibrahim, (2015), "Economic grow th and cost stick iness: evidence from Egypt", Journal of Financial Reporting and Accounting, Vol. 13 Iss 1 pp. 119-140 http://dx.doi.org/10.1 108/ JFRA-06-2014-0052 Anis Maaloul, Daniel Zéghal, (2015),"Financial s tatement informativeness and intellectual c apital disclosure: An empirical analysis", Journal of Fi nancial Reporting and Accounting, Vol. 13 Iss 1 pp. 66-90 http://dx.doi.or g/10.1 108/JFRA-04-2014-0023 Philip Kamau, Eno L. Inanga, Kami Rwegasira, (2015),"Currency risk impact on the financial performance of multilateral banks", Journal of Financial Reporting and Accounting, V ol. 13 Iss 1 pp. 91-118 http://dx.doi.org/10.1108/JFRA-11-2013-0076 Access to this document was granted through an Emerald subscription provided by emerald- srm:272736 [] For A uth o rs If you would like to write for this, or any other Emerald publication, then please use our Emerald for Authors service information about how to choose which publication to write for and submission guidelines are available for all. Please visit www .emeraldinsight.com/authors for more information. A bout Emerald w w w.em eraldinsi gh t .c o m Emerald is a global publisher linking research and practice to t he benefit of society . The company manages a portfolio of more than 290 journals and over 2,350 books and book series volumes, as well as providing an extensive range of online products and additional customer resources and services. Emerald is both COUNTER 4 and TRANSFER compliant. The organization is a partner of the Committee on Publication Ethics (COPE) and also works with Portico and the LOCKSS initiative for digital archive preservation. D o w n l o a d e d b y F L I N D E R S U N I V E R S I T Y O F S O U T H A U S T R A L I A A t 0 0 : 2 7 0 4 F e b r u a r y 2 0 1 6 ( P T )

-

Upload

markhaidir -

Category

Documents

-

view

221 -

download

0

Transcript of Kig Hir 2015

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 120

Journal of Financial Reporting and AccountingCorporate cash flow and dividends smoothing a panel data analysis at Bursa

MalaysiaApedzan Emmanuel Kighir Normah Haji Omar Norhayati Mohamed

Article information

To cite this documentApedzan Emmanuel Kighir Normah Haji Omar Norhayati Mohamed (2015)Corporate cash flow anddividends smoothing a panel data analysis at Bursa Malaysia Journal of Financial Reporting andAccounting Vol 13 Iss 1 pp 2 - 19Permanent link to this documenthttpdxdoiorg101108JFRA-09-2013-0072

Downloaded on 04 February 2016 At 0027 (PT)

References this document contains references to 28 other documents

To copy this document permissionsemeraldinsightcom

The fulltext of this document has been downloaded 368 times since 2015

Users who downloaded this article also downloaded

Awad Elsayed Awad Ibrahim (2015)Economic growth and cost stickiness evidence from EgyptJournal of Financial Reporting and Accounting Vol 13 Iss 1 pp 119-140 httpdxdoiorg101108JFRA-06-2014-0052

Anis Maaloul Daniel Zeacuteghal (2015)Financial statement informativeness and intellectual capitaldisclosure An empirical analysis Journal of Financial Reporting and Accounting Vol 13 Iss 1 pp

66-90 httpdxdoiorg101108JFRA-04-2014-0023Philip Kamau Eno L Inanga Kami Rwegasira (2015)Currency risk impact on the financialperformance of multilateral banks Journal of Financial Reporting and Accounting Vol 13 Iss 1 pp91-118 httpdxdoiorg101108JFRA-11-2013-0076

Access to this document was granted through an Emerald subscription provided by emerald-

srm272736 []

For Authors

If you would like to write for this or any other Emerald publication then please use our Emeraldfor Authors service information about how to choose which publication to write for and submissionguidelines are available for all Please visit wwwemeraldinsightcomauthors for more information

About Emerald wwwemeraldinsightcom

Emerald is a global publisher linking research and practice to the benefit of society The companymanages a portfolio of more than 290 journals and over 2350 books and book series volumes aswell as providing an extensive range of online products and additional customer resources andservices

Emerald is both COUNTER 4 and TRANSFER compliant The organization is a partner of theCommittee on Publication Ethics (COPE) and also works with Portico and the LOCKSS initiative for digital archive preservation

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 220

Related content and download information correct at time of

download

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 320

Corporate cash 1047298ow and

dividends smoothing a paneldata analysis at Bursa MalaysiaApedzan Emmanuel Kighir

Department of Financial Reporting Accounting Research InstituteShah Alam Malaysia and

Normah Haji Omar and Norhayati Mohamed Accounting Research Institute Universiti Teknologi MARA

Shah Alam Malaysia

Abstract

Purpose ndash The purpose of this paper is to contribute to the debate and 1047297nd out the impact of cash 1047298ow

on changes in dividend payout decisions among non-1047297nancial 1047297rms quoted at Bursa Malaysia as

compared to earnings There has been renewed debate in recent 1047297nance and accounting literature

concerning the key determinants of changes in dividends payout policy decisions in some jurisdictions

The conclusion in some is that 1047297rms base their dividend decisions on cash 1047298ows rather than published

earnings

Designmethodologyapproach ndash The research made use of panel data from 1999 to 2012 at Bursa

Malaysia using generalized method of moments as the main method of analysis

Findings ndash The research 1047297nds that Malaysia non-1047297nancial 1047297rms consider current earnings more

important than current cash 1047298ow while making dividends payout decisions and prior year cash 1047298owsare considered more important in dividends decisions than prior year earnings We also found support

for Jensen (1986) in Malaysia on agency theory that managers of 1047297rms pay dividends from free cash

1047298ow to reduce agency con1047298icts

Practical implications ndash The research concludes that Malaysian non-1047297nancial 1047297rms use current

earnings and less of current cash 1047298ow in making changes in dividends policy The policy implication is

that current earnings are dividends smoothing agents and the more they are considered in dividends

payout decisions the less of dividends smoothing

Social implications ndash If dividends smoothing is encouraged it could lead to dividends-based

earnings management

Originalityvalue ndash The research is our novel contribution of assisting investors and government in

making informed decisions regarding dividends policy in Malaysia

Keywords Bursa Malaysia Cash 1047298ow from operations Dividends smoothing Free cash 1047298owSpeed of adjustment Target payout ratio

Paper type Research paper

1 IntroductionLintner (1956) de1047297ned dividends smoothing as the variation in dividends that isdifferent from the variation in earnings Dividend smoothing according to

The researchers gratefully acknowledge 1047297nancial support from the Ministry of EducationMalaysia through Accounting Research Institute Universiti Teknologi MARA Malaysiatowards the research

The current issue and full text archive of this journal is available on Emerald Insight at

wwwemeraldinsightcom1985-2517htm

JFRA131

2

Received 26 September2013Revised18 April 2014Accepted 8 August2014

Journal of Financial Reporting and

Accounting

Vol 13 No 1 2015

pp 2-19

copy Emerald GroupPublishing Limited

1985-2517

DOI 101108JFRA-09-2013-0072

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 420

Guttman et al (2001) is keeping the dividends per share constant over two or moreconsecutive years ie stability of dividends Managers are said to smooth dividendsif they follow a constant nominal dividend payment policy with a partial adjustment

strategy Dividends smoothing involves setting a dividend payout policy that doesnot necessarily conform to earnings

Lintner (1956) in his seminal work on partial adjustment hypothesis held that 1047297rmsrealizing the transitory nature of current earnings adjust only partially to its desiredlevel of dividend with a time lag Lintner (1956) observed that 1047297rms are primarilyconcerned with the stability of dividends Instead of setting dividends each quarter1047297rms 1047297rst consider whether they need to make any changes from the existing rate Onlywhen they have decided that a change is necessary do they consider how large it shouldbe These views were later supported with an addition by Miller and Modigliani (1961)Miller and Modigliani in their classic argued that changes in dividends depend largelyon managementrsquos expectations of future earnings and cash 1047298ows Lee (1983) points out

that dividend payment should be based on cash 1047298ows not on earnings because cash1047298ows better re1047298ect the position of the 1047297rm Healy (1985) conducted his research on theimpact of bonus schemes on the selection of accounting principles and argued that cash1047298ows are more reliable in determining 1047297rm value than earnings because the latter caneasily be manipulated by managers to maximise their own compensation

There has been a renewed debate in recent 1047297nance and accounting literature similarto that of Lee (1983) concerning the key determinants of dividends payout policydecisions in some jurisdictions Andres et al (2009) concluded that German 1047297rms basetheir dividend decisions on cash 1047298ows rather than published earnings Al-Najjar andBelghitar (2012) argue that UK 1047297rms rely more on their cash 1047298ows to pay dividends andthat Lintnerrsquos (1956) partial adjustment model seems not to work very well in the UK

The main objective of this research is to contribute to the above debate and 1047297nd outthe impact of cash 1047298ow on changes in dividend payout decisions among non-1047297nancial1047297rms quoted at Bursa Malaysia as compared to earnings The study is unique asresearch on the association between cash 1047298ows and dividends changes has been limitedin Malaysia In addition unlike others who combined cash 1047298ow we separate free cash1047298ow (FCF) from cash 1047298ow from operations (CFOs) to determine speci1047297cally which of them have much impact on changes in dividends decisions in Malaysia using a muchmore advanced econometric technique the generalized method of moments (GMMs)

The remaining part of this paper covers hypothesis development in Section 2research methodology adopted in Section 3 and we take on data presentation andanalysis in Section 4 while summary conclusions and recommendations is in Section 5

2 Hypothesis development and literature reviewWe hypothesized that earnings are the key determinants of changes in dividendsdecisions among Malaysian 1047297rms

Lintner (1956) in his seminal work on partial adjustment hypothesis held that 1047297rmsrealizing the transitory nature of current earnings adjust only partially to its desiredlevel of dividend with a time lag Lintner (1956) surveyed managers on their attitudestowards dividend policy and concluded that managers target a long-term payout ratioHe also found that dividends are sticky tied to long-term sustainable earnings paid bymature companies and is smoothed from year to year

3

Corporatecash 1047298ow

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 520

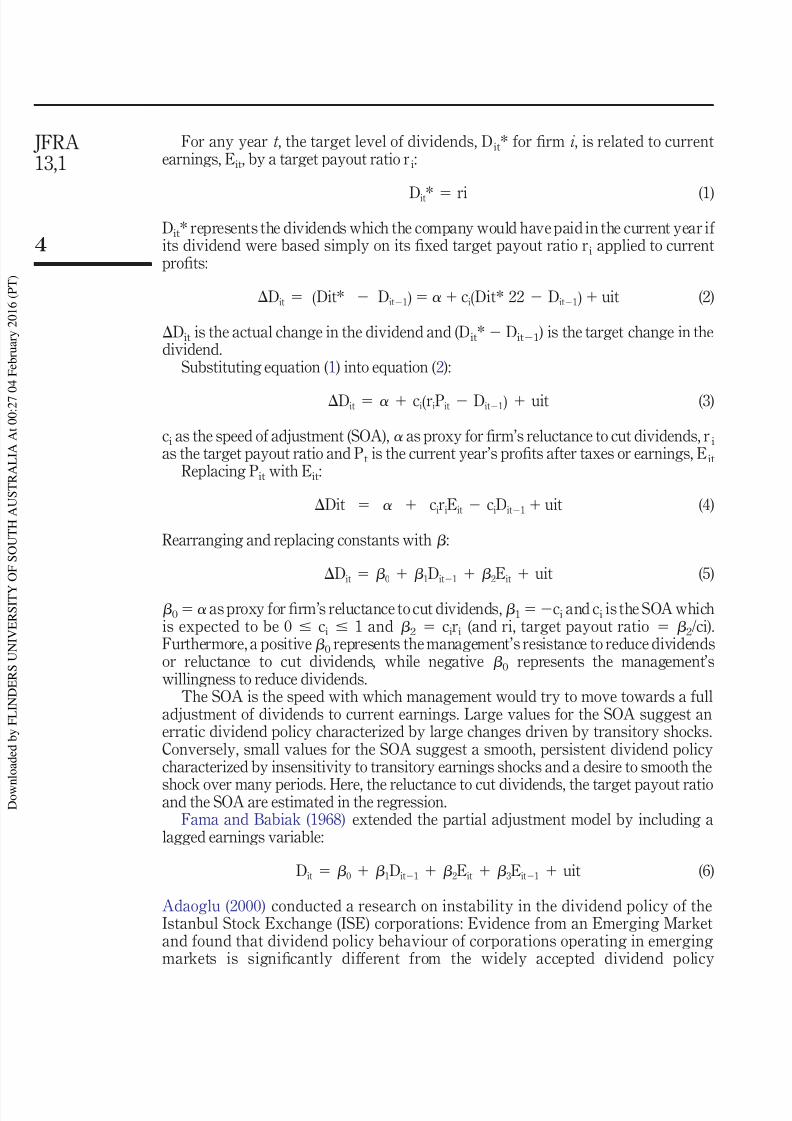

For any year t the target level of dividends Dit for 1047297rm i is related to currentearnings Eit by a target payout ratio ri

Dit ri (1)

Dit represents the dividends which the company would have paid in the current year if its dividend were based simply on its 1047297xed target payout ratio ri applied to currentpro1047297ts

Dit ( Dit Dit1 ) ci( Dit 22 Dit1 ) uit (2)

Dit is the actual change in the dividend and (Dit Dit1 ) is the target change in thedividend

Substituting equation ( 1 ) into equation ( 2 )

Dit ci( riPit Dit1 ) uit (3)

ci as the speed of adjustment (SOA) as proxy for 1047297rmrsquos reluctance to cut dividends r i

as the target payout ratio and Pt is the current yearrsquos pro1047297ts after taxes or earnings Eit

Replacing Pit with Eit

Dit ciriEit ciDit1 uit (4)

Rearranging and replacing constants with

Dit 0 1Dit1 2Eit uit (5)

0 as proxy for 1047297rmrsquos reluctance to cut dividends1ci and ci is the SOA whichis expected to be 0 ci 1 and 2 ciri (and ri target payout ratio 2ci)Furthermore a positive0 represents the managementrsquos resistance to reduce dividendsor reluctance to cut dividends while negative 0 represents the managementrsquoswillingness to reduce dividends

The SOA is the speed with which management would try to move towards a fulladjustment of dividends to current earnings Large values for the SOA suggest anerratic dividend policy characterized by large changes driven by transitory shocksConversely small values for the SOA suggest a smooth persistent dividend policycharacterized by insensitivity to transitory earnings shocks and a desire to smooth the

shock over many periods Here the reluctance to cut dividends the target payout ratioand the SOA are estimated in the regression

Fama and Babiak (1968) extended the partial adjustment model by including alagged earnings variable

Dit 0 1Dit1 2Eit 3Eit1 uit (6)

Adaoglu (2000) conducted a research on instability in the dividend policy of theIstanbul Stock Exchange (ISE) corporations Evidence from an Emerging Marketand found that dividend policy behaviour of corporations operating in emergingmarkets is signi1047297cantly different from the widely accepted dividend policy

JFRA131

4

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 620

behaviour of corporations operating in developed markets His empirical resultsshow that the ISE corporations follow unstable cash dividend policies and the mainfactor that determines the amount of cash dividends is the earnings of the

corporation in that yearBrav et al (2005) 1047297nd that managers are willing to raise external capital or even

forego positive net present value (NPV) investments to avoid cutting dividendsAl-Yahyae et al (2011) conducted their research in Oman a developing economy on

ldquoDividend smoothing when 1047297rms distribute most of their earnings as dividendsrdquo Theresearch found that Omani 1047297rms have unstable dividend policies and target payoutratios and they adjust their dividend policies very quickly and are willing to cut theirdividends

In Malaysia prior studies in the area of determinants of dividend policy changeshave been limited A study by Mohamed et al (2005) on determinants of dividendspayments pro1047297tability and liquidity and Normah et al (2006) on dividends survey

revealed that Malaysian 1047297rms payout a large proportion of their earnings individends Appannan and Sim (2011) examines the leading determinants affectingthe dividend payment decision by company management in Malaysia listedcompanies for food industries under the consumer products sector and concludedthat debt equity ratio and past dividend per share were the important determinantsof dividend payment

H1 Earnings are the key determinants in explaining dividends smoothing amongMalaysian 1047297rms

We expect a positive coef1047297cient A signi1047297cant impact would support our hypothesis andthe SOA compared with that of CFO or FCF

We hypothesized that cash 1047298ows are the key determinants of changes individends decisions among Malaysian 1047297rms Our hypothesis would be supportedwhere cash 1047298ow is signi1047297cant on partial adjustment model Lee (1983) points outthat dividend payment should be based on cash 1047298ows not on earnings because cash1047298ows better re1047298ect the position of the 1047297rm Andres et al (2009) conducted theirresearch in Germany and found that German 1047297rms payout a lower proportion of their cash 1047298ows but a higher proportion of their published pro1047297ts than UK and US1047297rms They estimated partial adjustment models and report two major 1047297ndingsFirst German 1047297rms base their dividend decisions on cash 1047298ows rather thanpublished earnings as published earnings do not correctly re1047298ect performancebecause German 1047297rms retain parts of their earnings to build up legal reserves and

as published earnings are subject to more smoothing than cash 1047298ows Second to theopposite of UK and US 1047297rms German 1047297rms have more 1047298exible dividend policies asthey are willing to cut the dividend when pro1047297tability is only temporarily downAl-Najjar and Belghitar (2012) conducted their research on ldquoThe information contentof cash 1047298ows in the context of dividend smoothingrdquo using a modi1047297ed dividendpartial adjustment model In their model they replaced current yearrsquos earnings withFCF as according to them UK 1047297rms rely more on their cash 1047298ows to pay dividendsand that Lintnerrsquos (1956) partial adjustment model seems not to work very well inthe UK That their results were consistent across the different models and show thatcash 1047298ows are superior to earnings in dividend smoothing suggesting that cash1047298ows are the key determinant of dividend payments This is because their proposed

5

Corporatecash 1047298ow

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 720

dividend partial adjustment model has a lower adjustment coef1047297cient than Lintnerrsquosmodel suggesting that their estimates are much closer to reality They concludedthat the modi1047297ed version of Lintnerrsquos model explains better the smoothing process

of dividends for UK 1047297rms H2 CFOs are the key determinants in explaining dividends smoothing among

Malaysian 1047297rms

We expect a positive coef1047297cient of CFO A signi1047297cant impact would support ourhypothesis and would also indicate that 1047297rms make use of cash generated fromoperations to pay dividends The SOA would also be compared with that of earnings orFCF to determine which better explains dividends smoothing A higher SOAbetter explains the impact of a variable on dividends as it reduces dependence on prioryear dividends (Dit1 ) which is a smoothing agent The higher the Dit1 coef1047297cient thelower the SOA and the more dividends smoothing a 1047297rm is tagged

H3 FCFs are the key determinants in explaining dividends smoothing amongMalaysian 1047297rms

We expect a positive coef1047297cient of FCF A signi1047297cant impact would support ourhypothesis and would also indicate that 1047297rms make use of FCF to pay dividends Thiswill also support Jensen (1986) that managers try to reduce agency con1047298ict by payingdividends to shareholders out of FCFs The SOA is compared with that of earnings orCFO to determine which better explains dividends smoothing

Finally we hypothesized that both earnings and cash 1047298ows are equally consideredby 1047297rms as key determinants of changes in dividends decisions Our hypothesis issupported where both earnings and cash 1047298ow are signi1047297cant on partial adjustment

model Miller and Modigliani (1961) in their classic argued that changes in dividendsdepend largely on managementrsquos expectations of future earnings and cash 1047298owsSimonsrsquo (1994) study tried to provide evidence on the incremental information content of cash 1047298ow numbers over pro1047297ts and previous yearrsquos dividends (Lintnerrsquos model) inexplaining changes in cash dividends The study was however inconclusive Charitouand Vafeas (1998) conducted a study on association between operating cash 1047298ows anddividend changes given earnings and argue that a positive relationship between cash1047298ows and dividend changes should exist due to liquidity and accruals managementconsiderations Their study found empirical evidence that the dividend changesndashcash1047298ow relationship is signi1047297cantly positive when operating cash 1047298ows are low comparedto earnings and when 1047297rm growth is moderate Andres et al (2009) and Adelegan (2003)

re-evaluate the incremental information content of cash 1047298ows in explaining dividendchanges given earnings in Nigeria and found a signi1047297cant relationship betweendividend changes and cash 1047298ow unlike previous studies The empirical results revealthat the relationship between cash 1047298ows and dividend changes depends substantiallyon the level of growth the capital structure choice size of each 1047297rm and economic policychanges

H4 Earnings are better determinants than CFOs in explaining dividends smoothingamong Malaysian 1047297rms

H5 Earnings are better determinants than FCF in explaining dividends smoothingamong Malaysian 1047297rms

JFRA131

6

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 820

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 920

We therefore use the GMM technique developed by Arellano and Bond (1991) (GMM(diff)[1] Arellano and Bover (1995)Blundell and Bond (1998) (GMMsys)[2] in additionto the estimated generalized least squares random effects model and least squares FEM

to estimate dividends and earnings panel data We make use of Hausmanrsquos (1978)con1047297rmatory test for correlated random effects and BreuschndashPagan Lagrangemultiplier(1980) to decide between a panel random effects regression and a pooled OLSregression

The models for this research are therefore

LogDit 0 1LogDit1 2LogEit 3LogEit1 ϒi ui eit (8)

Where LogDit is dividend per share as dependent variable Dit1 lagged dividend pershare Eit earnings per share and Eit-1 lagged earnings per share as regressors withias cross-sectional effect coef1047297cient and it is a 1047297rm-speci1047297c effect for unobserved

in1047298uences on the dividend behaviour of each 1047297rm and is assumed to remain constantover time i as time period effect coef1047297cient and they are time dummies that control forthe impact of time on the dividend behaviour of all sampled 1047297rms The eit is a whitenoise

Our modi1047297ed versions of the model is as follows

LogDit 0 1LogDit1 2LogCFOit 3LogCFOit1 ϒi ui eit (9)

Where CFO is cash 1047298ow from operations per year

LogDit 0 1LogDit1 2LogFCFit 3LogFCFit1 ϒi ui eit (10)

Where FCF is free cash 1047298ow per share

LogDit 0 1LogDit1 2LogEit 3LogCFOit ϒi ui eit (11)

LogDit 0 1LogDit1 2LogEit 4LogFCFit ϒi ui eit (12)

This research adopts 5 per cent signi1047297cant level as its maximum level of rejection or notrejecting any hypothesis

4 Data presentation and analysis41 Analysis results

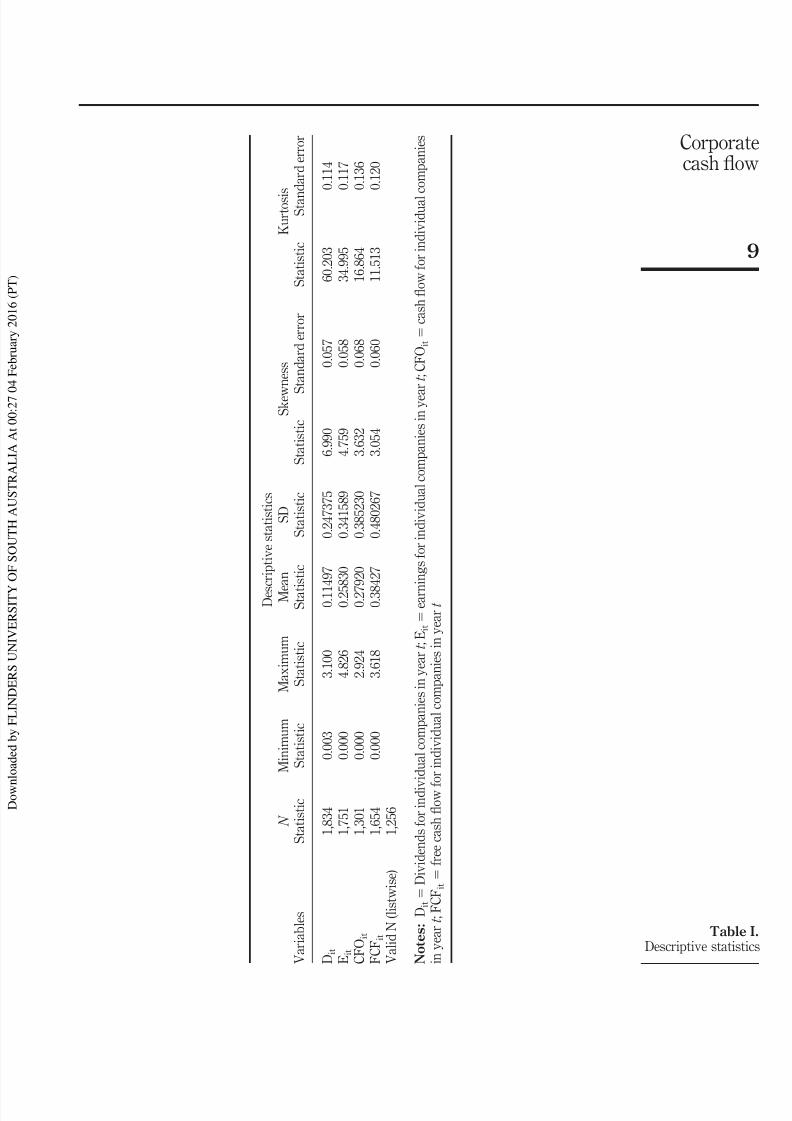

Table I shows an average dividends payout ratio relative to earnings of 0445 0441relative to CFOs and 0299 relative to FCF This means Malaysian 1047297rms use 445 per centof their current earnings to pay dividends 441 per cent of cash generated for the currentperiod to pay dividends and about 30 per cent of current yearrsquos FCF to pay dividendsThe zero values in the minimum column are companies that reported negative earningsor CFOs or FCFs

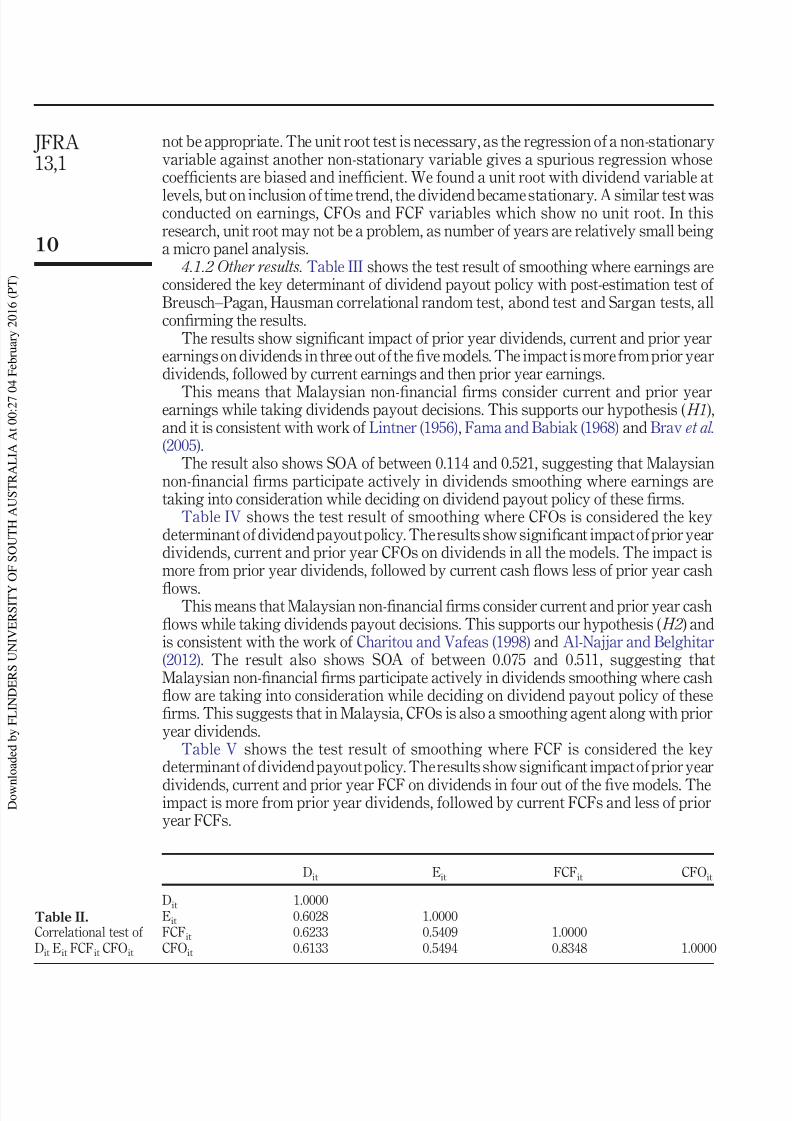

Table II shows correlations between the variables The strongest is between CFOsand FCFs This indicates that these variables cannot be regressors in the same test toavoid multicollinearity

411 Unit root test unit root (common unit root process) We used Levin et al (2002)test for unit root as our data are a panel data and normal time series unit root tests will

JFRA131

8

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 1020

Table IDescriptive statistics

D e s c r i p t i v e s t a t i s t i c s

V a r i a b l e s

N

M i n i m u m

M a x i m u m

M e

a n

S D

S k e w

n e s s

K u r t o s i s

S t a t i s t i c

S t a t i s t i c

S t a t i s t i c

S t a t i s t i c

S t a t i s t i c

S t a t i s t i c

S

t a n d a r d e r r o r

S t a t i s t i c

S t a n

d a r d e r r o r

D i t

1 8 3 4

0 0 0 3

3 1 0 0

0 1 1

4 9 7

0 2 4 7 3 7 5

6 9 9 0

0 0 5 7

6 0 2 0 3

0 1 1 4

E i t

1 7 5 1

0 0 0 0

4 8 2 6

0 2 5

8 3 0

0 3 4 1 5 8 9

4 7 5 9

0 0 5 8

3 4 9 9 5

0 1 1 7

C F O i t

1 3 0 1

0 0 0 0

2 9 2 4

0 2 7

9 2 0

0 3 8 5 2 3 0

3 6 3 2

0 0 6 8

1 6 8 6 4

0 1 3 6

F C F i t

1 6 5 4

0 0 0 0

3 6 1 8

0 3 8

4 2 7

0 4 8 0 2 6 7

3 0 5 4

0 0 6 0

1 1 5 1 3

0 1 2 0

V a l i d N ( l i s t w i s e )

1 2 5 6

N o t e s D i t

D i v i d e n d s f o r i n d i v

i d u a l c o m p a n i e s i n y e a r t E i t

e a r n

i n g s f o r i n d i v i d u a l c o m p a n i e s i n y e a

r t C F O i t

c a s h 1047298 o w f o r i n d i v i d u a l c o m p a n i e s

i n y e a r t F C F i t

f r e e c a s h 1047298 o w f o r i n d i v i d u a l c o m p a n i e s i n y e a r t

9

Corporatecash 1047298ow

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 1120

not be appropriate The unit root test is necessary as the regression of a non-stationaryvariable against another non-stationary variable gives a spurious regression whosecoef1047297cients are biased and inef1047297cient We found a unit root with dividend variable at

levels but on inclusion of time trend the dividend became stationary A similar test wasconducted on earnings CFOs and FCF variables which show no unit root In thisresearch unit root may not be a problem as number of years are relatively small beinga micro panel analysis

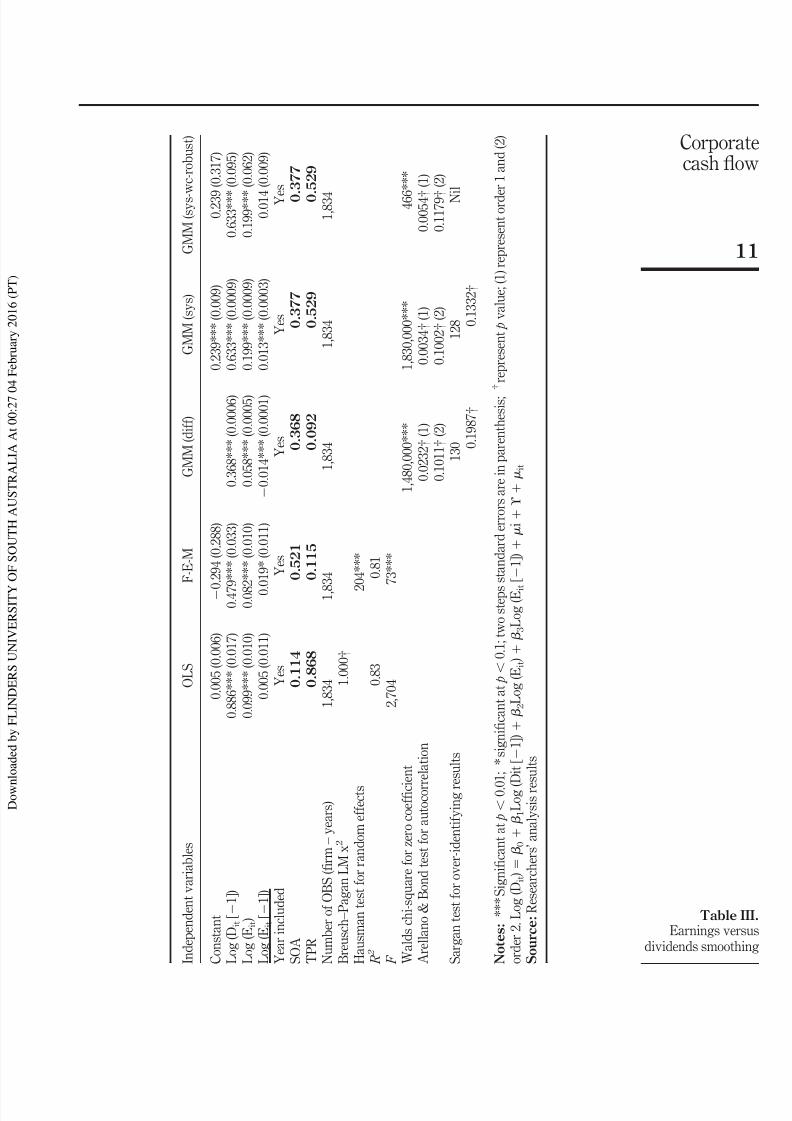

412 Other results Table III shows the test result of smoothing where earnings areconsidered the key determinant of dividend payout policy with post-estimation test of BreuschndashPagan Hausman correlational random test abond test and Sargan tests allcon1047297rming the results

The results show signi1047297cant impact of prior year dividends current and prior yearearnings on dividends in three out of the 1047297ve models The impact is more from prior yeardividends followed by current earnings and then prior year earnings

This means that Malaysian non-1047297nancial 1047297rms consider current and prior yearearnings while taking dividends payout decisions This supports our hypothesis ( H1 )and it is consistent with work of Lintner (1956) Fama and Babiak (1968) and Brav et al(2005)

The result also shows SOA of between 0114 and 0521 suggesting that Malaysiannon-1047297nancial 1047297rms participate actively in dividends smoothing where earnings aretaking into consideration while deciding on dividend payout policy of these 1047297rms

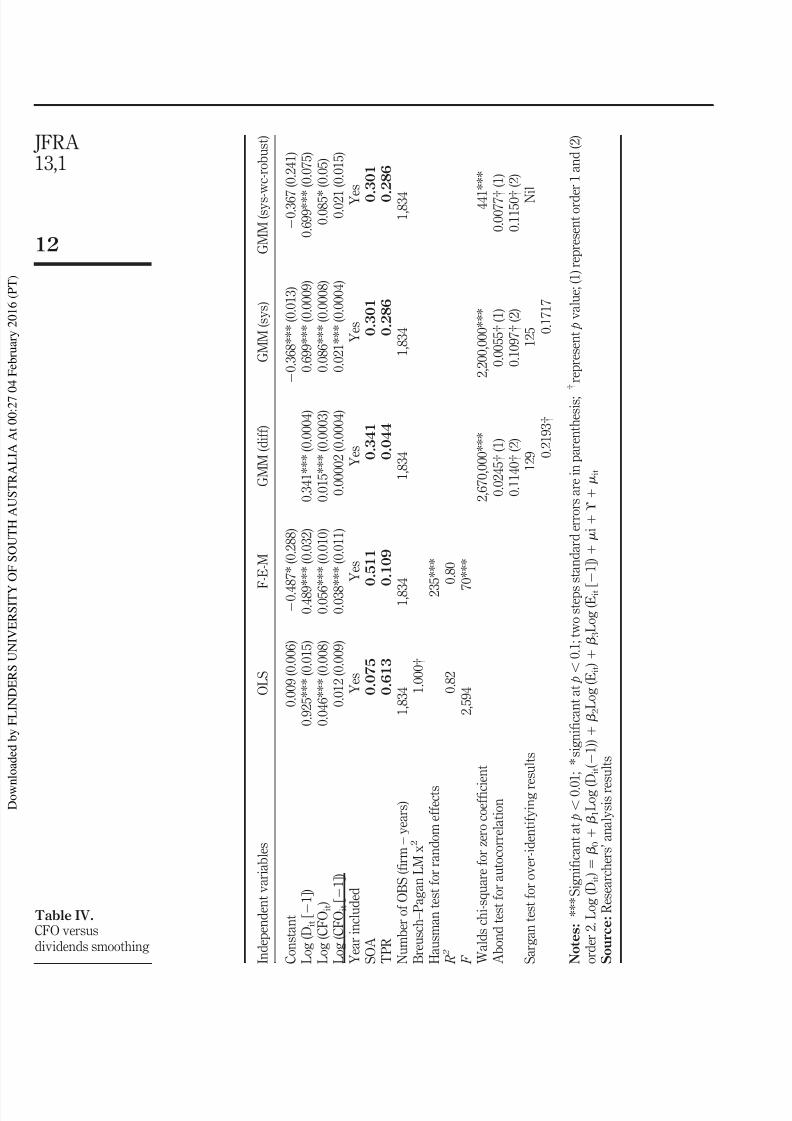

Table IV shows the test result of smoothing where CFOs is considered the keydeterminant of dividend payout policy The results show signi1047297cant impact of prior yeardividends current and prior year CFOs on dividends in all the models The impact ismore from prior year dividends followed by current cash 1047298ows less of prior year cash

1047298owsThis means that Malaysian non-1047297nancial 1047297rms consider current and prior year cash

1047298ows while taking dividends payout decisions This supports our hypothesis ( H2 ) andis consistent with the work of Charitou and Vafeas (1998) and Al-Najjar and Belghitar(2012) The result also shows SOA of between 0075 and 0511 suggesting thatMalaysian non-1047297nancial 1047297rms participate actively in dividends smoothing where cash1047298ow are taking into consideration while deciding on dividend payout policy of these1047297rms This suggests that in Malaysia CFOs is also a smoothing agent along with prioryear dividends

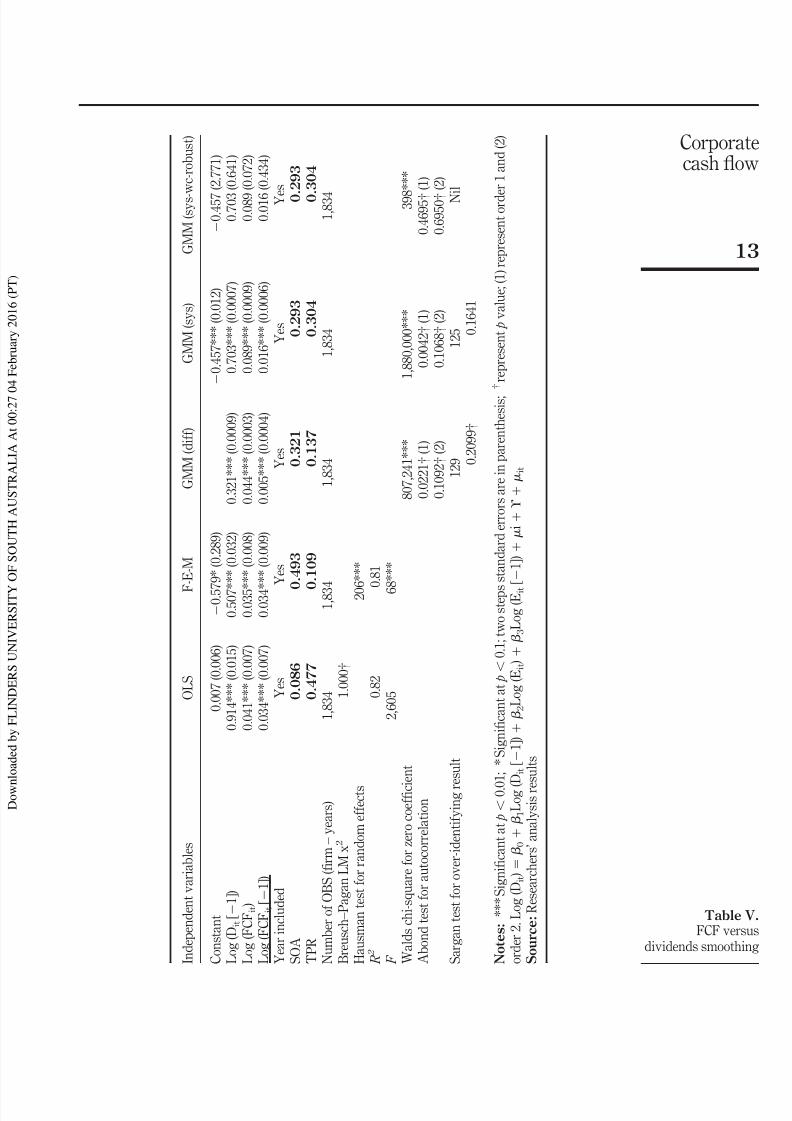

Table V shows the test result of smoothing where FCF is considered the keydeterminant of dividend payout policy The results show signi1047297cant impact of prior year

dividends current and prior year FCF on dividends in four out of the 1047297ve models Theimpact is more from prior year dividends followed by current FCFs and less of prioryear FCFs

Table IICorrelational test of

Dit Eit FCFit CFOit

Dit Eit FCFit CFOit

Dit 10000

Eit 06028 10000

FCFit 06233 05409 10000

CFOit 06133 05494 08348 10000

JFRA131

10

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 1220

Table IIIEarnings versus

dividends smoothing I n d e p e n d e n t v a r i a b l e s

O L S

F - E - M

G M M ( d i f f )

G M M ( s y s )

G M M ( s y s - w c - r o b u s t )

C o n s t a n t

0 0 0 5 ( 0 0 0 6 )

0 2 9 4 ( 0 2 8 8 )

0 2 3 9 ( 0 0 0 9 )

0 2 3 9

( 0 3 1 7 )

L o g ( D i t [ 1 ] )

0 8 8 6 ( 0 0 1 7 )

0 4 7 9 ( 0 0 3 3 )

0 3 6 8 ( 0 0 0 0 6 )

0 6 3 3 ( 0 0 0 0 9 )

0 6 3 3

( 0 0 9 5 )

L o g ( E i t )

0 0 9 9 ( 0 0 1 0 )

0 0 8 2 ( 0 0 1 0 )

0 0 5 8 ( 0 0 0 0 5 )

0 1 9 9 ( 0 0 0 0 9 )

0 1 9 9

( 0 0 6 2 )

L o g ( E i t

[ 1 ] )

0 0 0 5 ( 0 0 1 1 )

0 0 1 9 ( 0 0 1 1 )

0 0 1 4 ( 0 0 0 0 1 )

0 0 1 3 ( 0 0 0 0 3 )

0 0 1 4

( 0 0 0 9 )

Y e a r i n c l u d e d

Y e s

Y e s

Y e s

Y e s

Y e s

S O A

0 1 1 4

0 5 2 1

0 3 6 8

0 3 7 7

0 3 7 7

T P R

0 8 6 8

0 1 1 5

0 0 9 2

0 5 2 9

0 5 2 9

N u m b e r o f O B S ( 1047297 r m ndash y e a r s )

1 8 3 4

1 8

3 4

1 8 3 4

1 8 3 4

1 8 3 4

B r e u s c h ndash P a g a n L M x

2

1 0 0 0 dagger

H a u s m a n t e s t f o r r a n d o m e f f e c t s

2

0 4

R 2

0 8 3

0 8 1

F

2 7 0 4

7 3

W a l d s c h i - s q u a r e f o r z e r o c o e f 1047297 c i e n t

1 4 8 0 0 0 0

1 8 3 0 0 0 0

4 6 6

A r e l l a n o amp B o n d t e s t f o r a u t o c o r r e l a t i o n

0 0 2 3 2 dagger ( 1 )

0 0 0 3 4 dagger ( 1 )

0 0 0 5 4 dagger

( 1 )

0 1 0 1 1 dagger ( 2 )

0 1 0 0 2 dagger ( 2 )

0 1 1 7 9 dagger

( 2 )

S a r g a n t e s t f o r o v e r - i d e n t i f y i n g r e s u l t s

1 3 0

1 2 8

N i l

0 1 9 8 7 dagger

0 1 3 3 2 dagger

N o t e s S i g n i 1047297 c a n t a t p 0 0

1 s i g n i 1047297 c a n t a t p

0 1 t w o s t e p s

s t a n d a r d e r r o r s a r e i n p a r e n t h e s i s dagger

r e p r e s e n t p v a l u e ( 1 ) r e p r e s e n t o r d e r 1 a n d ( 2 )

o r d e r 2 L o g ( D i t )

0

1 L o g ( D i t [ 1 ] )

2 L o g ( E i t )

3 L o g ( E i t

[ 1 ] )

i

ϒ

i t

S o u r c e R e s e a r c h e r s rsquo a n a l y s i s r e

s u l t s

11

Corporatecash 1047298ow

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 1320

Table IVCFO versus

dividends smoothing I n d e p e n d e n t v a r i a b l e s

O L S

F - E - M

G M M ( d i f f )

G M M ( s y s )

G M M ( s y s - w c - r o b u s t )

C o n s t a n t

0 0 0 9 ( 0 0 0 6 )

0 4

8 7 ( 0 2 8 8 )

0 3 6 8 ( 0 0 1 3 )

0 3 6 7

( 0 2 4 1 )

L o g ( D i t

[ 1 ] )

0 9 2 5 ( 0 0 1 5 )

0 4 8 9

( 0 0 3 2 )

0 3 4 1 ( 0 0 0 0 4 )

0 6 9 9 ( 0 0 0 0 9 )

0 6 9 9

( 0 0 7 5 )

L o g ( C F O i t )

0 0 4 6 ( 0 0 0 8 )

0 0 5 6

( 0 0 1 0 )

0 0 1 5 ( 0 0 0 0 3 )

0 0 8 6 ( 0 0 0 0 8 )

0 0 8 5

( 0 0 5 )

L o g ( C F O i t

[ 1 ] )

0 0 1 2 ( 0 0 0 9 )

0 0 3 8

( 0 0 1 1 )

0 0 0 0 0 2 ( 0 0 0 0 4 )

0 0 2 1 ( 0 0 0 0 4 )

0 0 2 1

( 0 0 1 5 )

Y e a r i n c l u d e d

Y e s

Y e s

Y e s

Y e s

Y e s

S O A

0 0 7 5

0 5 1 1

0 3 4 1

0 3 0 1

0 3 0 1

T P R

0 6 1 3

0 1 0 9

0 0 4 4

0 2 8 6

0 2 8 6

N u m b e r o f O B S ( 1047297 r m ndash y e a r s )

1 8 3 4

1 8 3

4

1 8 3 4

1 8 3 4

1 8 3 4

B r e u s c h ndash P a g a n L M x

2

1 0 0 0 dagger

H a u s m a n t e s t f o r r a n d o m e f f e c t s

2 3

5

R 2

0 8 2

0 8 0

F

2 5 9 4

7

0

W a l d s c h i - s q u a r e f o r z e r o c o e f 1047297 c i e n t

2 6 7 0 0 0 0

2 2 0 0 0 0 0

4 4 1

A b o n d t e s t f o r a u t o c o r r e l a t i o n

0 0 2 4 5 dagger ( 1 )

0 0 0 5 5 dagger ( 1 )

0 0 0 7 7 dagger

( 1 )

0 1 1 4 0 dagger ( 2 )

0 1 0 9 7 dagger ( 2 )

0 1 1 5 0 dagger

( 2 )

S a r g a n t e s t f o r o v e r - i d e n t i f y i n g r e s u l t s

1 2 9

1 2 5

N i l

0 2 1 9 3 dagger

0 1 7 1 7

N o t e s S i g n i 1047297 c a n t a t p 0 0

1 s i g n i 1047297 c a n t a t p

0 1 t w o s t e p s

s t a n d a r d e r r o r s a r e i n p a r e n t h e s i s dagger

r e p r e s e n t p v a l u e ( 1 ) r e p r e s e n t o r d e r 1 a n d ( 2 )

o r d e r 2 L o g ( D i t )

0

1 L o g ( D i t ( 1 ) )

2 L o g ( E i t )

3 L o g ( E i t

[ 1 ] )

i

ϒ

i t

S o u r c e R e s e a r c h e r s rsquo a n a l y s i s r e

s u l t s

JFRA131

12

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 1420

Table VFCF versus

dividends smoothing I n d e p e n d e n t v a r i a b l e s

O L S

F

- E - M

G M M ( d i f f )

G M M ( s y s )

G M M ( s y s - w c - r o b u s t )

C o n s t a n t

0 0 0 7 ( 0 0 0 6 )

0 5 7 9 ( 0 2 8 9 )

0 4 5 7 ( 0 0 1 2 )

0 4 5 7

( 2 7 7 1 )

L o g ( D i t [ 1 ] )

0 9 1 4 ( 0 0 1 5 )

0 5 0 7 ( 0 0 3 2 )

0 3 2 1 ( 0 0 0 0 9 )

0 7 0 3 ( 0 0 0 0 7 )

0 7 0 3

( 0 6 4 1 )

L o g ( F C F i t )

0 0 4 1 ( 0 0 0 7 )

0 0 3 5 ( 0 0 0 8 )

0 0 4 4 ( 0 0 0 0 3 )

0 0 8 9 ( 0 0 0 0 9 )

0 0 8 9

( 0 0 7 2 )

L o g ( F C F i t [ 1 ] )

0 0 3 4 ( 0 0 0 7 )

0 0 3 4 ( 0 0 0 9 )

0 0 0 5 ( 0 0 0 0 4 )

0 0 1 6 ( 0 0 0 0 6 )

0 0 1 6

( 0 4 3 4 )

Y e a r i n c l u d e d

Y e s

Y e s

Y e s

Y e s

Y e s

S O A

0 0 8 6

0

4 9 3

0 3 2 1

0 2 9 3

0 2 9 3

T P R

0 4 7 7

0

1 0 9

0 1 3 7

0 3 0 4

0 3 0 4

N u m b e r o f O B S ( 1047297 r m ndash y e a r s )

1 8 3 4

1 8 3 4

1 8 3 4

1 8 3 4

1 8 3 4

B r e u s c h ndash P a g a n L M x

2

1 0 0 0 dagger

H a u s m a n t e s t f o r r a n d o m e f f e c t s

2 0 6

R 2

0 8 2

0 8 1

F

2 6 0 5

6 8

W a l d s c h i - s q u a r e f o r z e r o c o e f 1047297 c i e n t

8 0 7 2 4 1

1 8 8 0 0 0 0

3 9 8

A b o n d t e s t f o r a u t o c o r r e l a t i o n

0 0 2 2 1 dagger ( 1 )

0 0 0 4 2 dagger ( 1 )

0 4 6 9 5 dagger

( 1 )

0 1 0 9 2 dagger ( 2 )

0 1 0 6 8 dagger ( 2 )

0 6 9 5 0 dagger

( 2 )

S a r g a n t e s t f o r o v e r - i d e n t i f y i n g r e s u l t

1 2 9

1 2 5

N i l

0 2 0 9 9 dagger

0 1 6 4 1

N o t e s S i g n i 1047297 c a n t a t p 0 0

1 S i g n i 1047297 c a n t a t p

0 1 t w o s t e p s

s t a n d a r d e r r o r s a r e i n p a r e n t h e s i s

dagger

r e p r e s e n t p v a l u e ( 1 ) r e p r e s e n t o r d e r 1 a n d ( 2 )

o r d e r 2 L o g ( D i t )

0

1 L o g ( D i t

[ 1 ] )

2 L o g ( E i t )

3 L o g ( E i t

[ 1 ] )

i

ϒ

i t

S o u r c e R e s e a r c h e r s rsquo a n a l y s i s r e

s u l t s

13

Corporatecash 1047298ow

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 1520

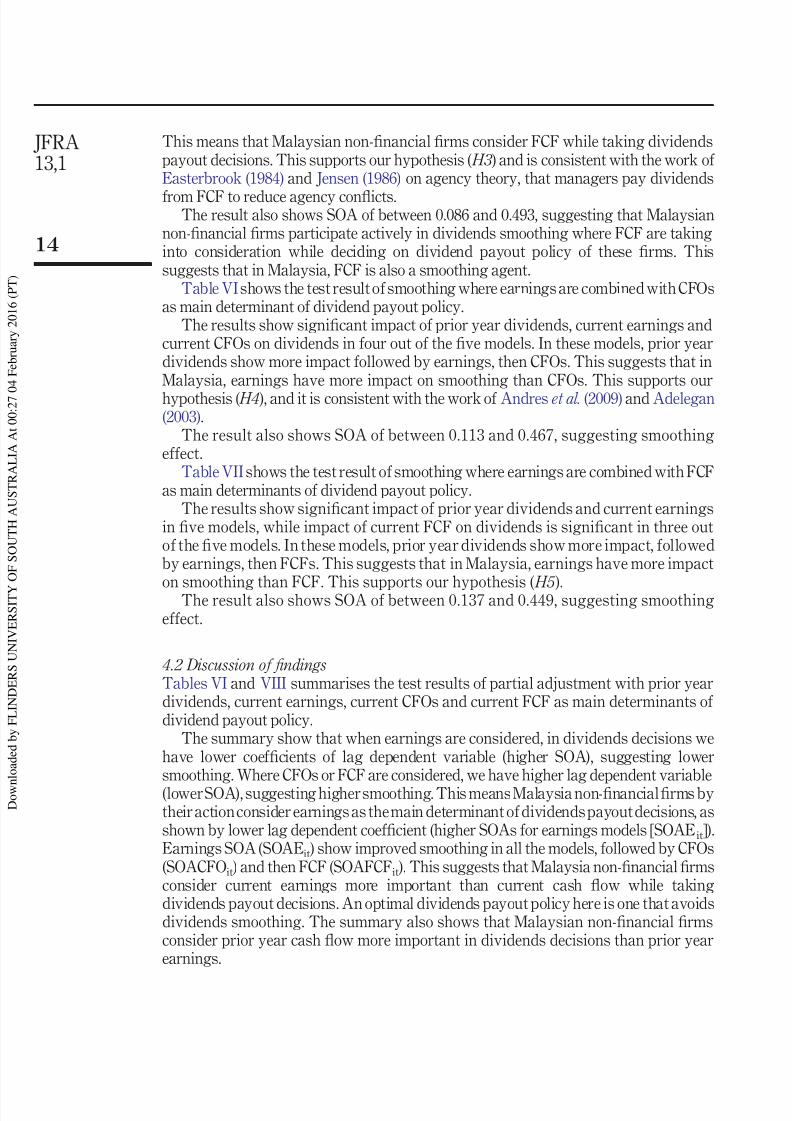

This means that Malaysian non-1047297nancial 1047297rms consider FCF while taking dividendspayout decisions This supports our hypothesis ( H3 ) and is consistent with the work of Easterbrook (1984) and Jensen (1986) on agency theory that managers pay dividends

from FCF to reduce agency con1047298ictsThe result also shows SOA of between 0086 and 0493 suggesting that Malaysian

non-1047297nancial 1047297rms participate actively in dividends smoothing where FCF are takinginto consideration while deciding on dividend payout policy of these 1047297rms Thissuggests that in Malaysia FCF is also a smoothing agent

Table VI shows the test result of smoothing where earnings are combined with CFOsas main determinant of dividend payout policy

The results show signi1047297cant impact of prior year dividends current earnings andcurrent CFOs on dividends in four out of the 1047297ve models In these models prior yeardividends show more impact followed by earnings then CFOs This suggests that inMalaysia earnings have more impact on smoothing than CFOs This supports our

hypothesis ( H4 ) and it is consistent with the work of Andres et al (2009) and Adelegan(2003)

The result also shows SOA of between 0113 and 0467 suggesting smoothingeffect

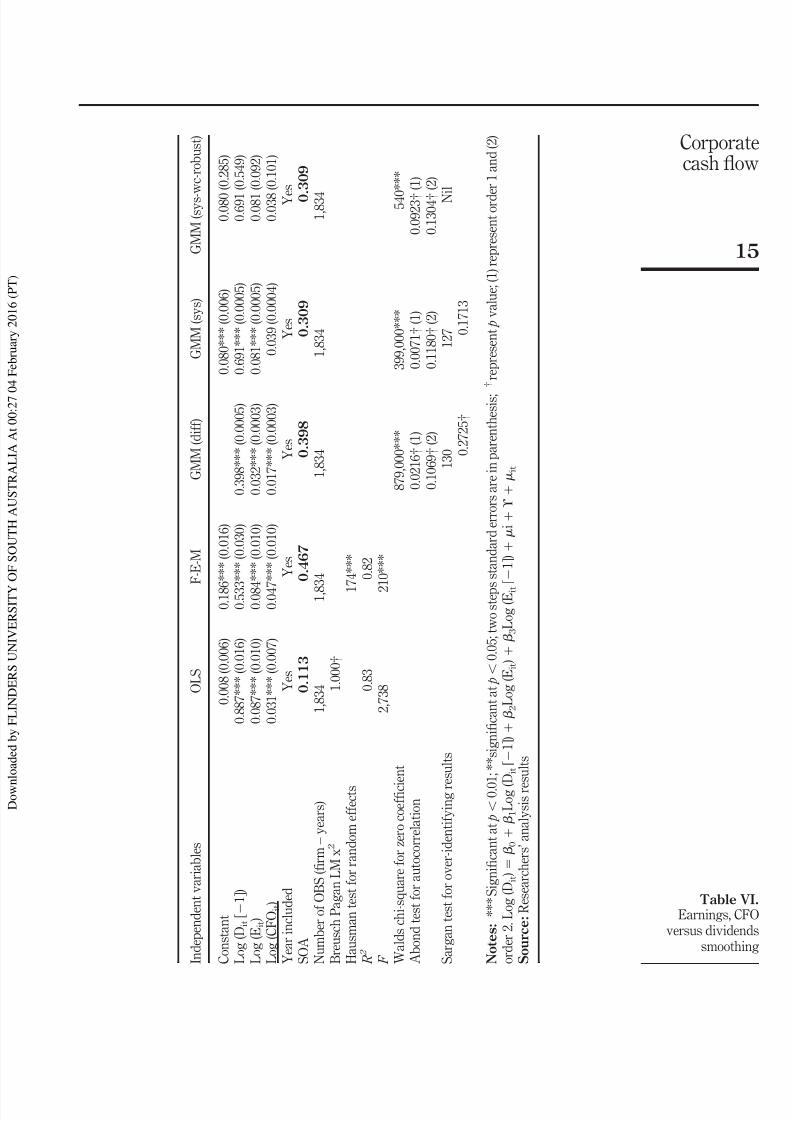

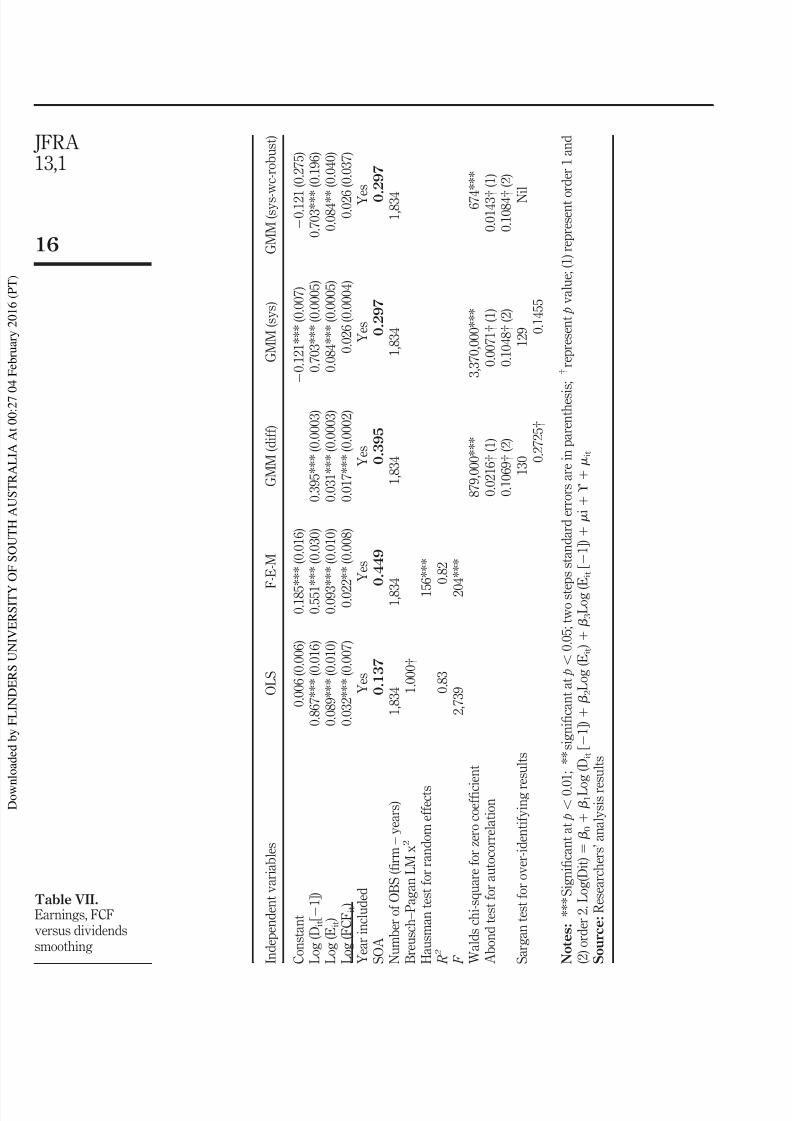

Table VII shows the test result of smoothing where earnings are combined with FCFas main determinants of dividend payout policy

The results show signi1047297cant impact of prior year dividends and current earningsin 1047297ve models while impact of current FCF on dividends is signi1047297cant in three outof the 1047297ve models In these models prior year dividends show more impact followedby earnings then FCFs This suggests that in Malaysia earnings have more impact

on smoothing than FCF This supports our hypothesis ( H5 )The result also shows SOA of between 0137 and 0449 suggesting smoothingeffect

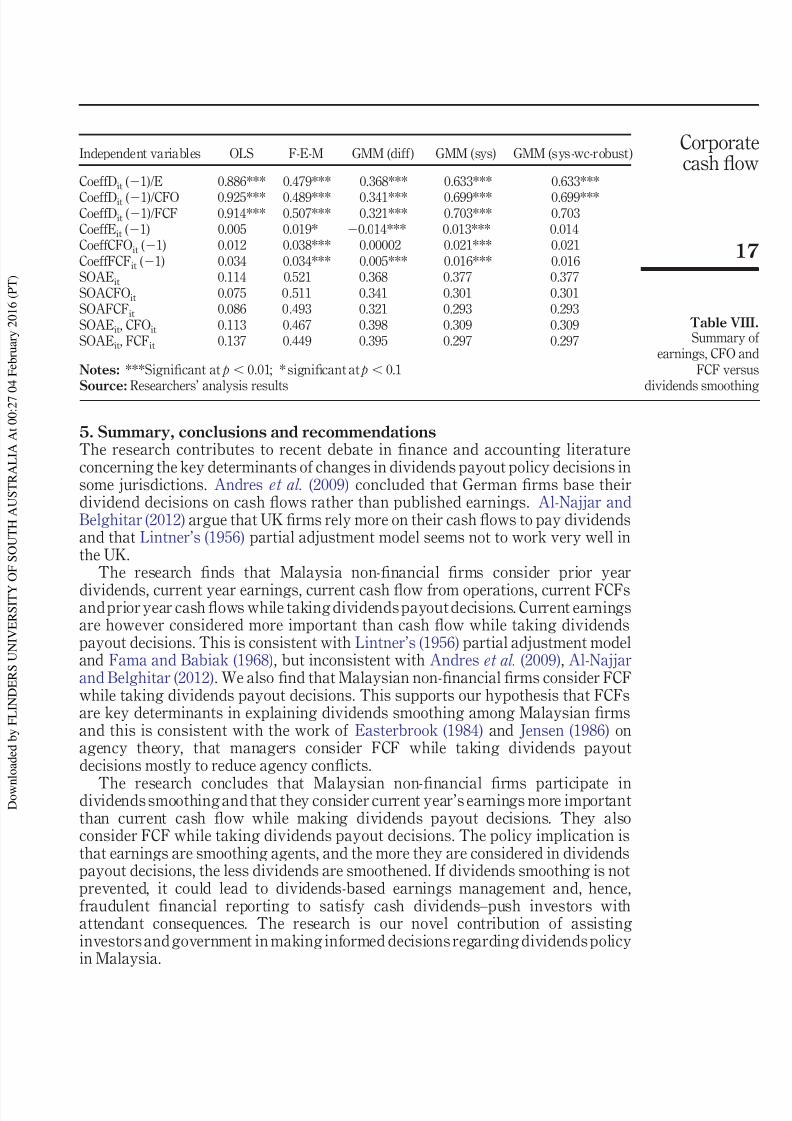

42 Discussion of 1047297ndingsTables VI and VIII summarises the test results of partial adjustment with prior yeardividends current earnings current CFOs and current FCF as main determinants of dividend payout policy

The summary show that when earnings are considered in dividends decisions wehave lower coef1047297cients of lag dependent variable (higher SOA) suggesting lowersmoothing Where CFOs or FCF are considered we have higher lag dependent variable(lower SOA) suggesting higher smoothing This means Malaysia non-1047297nancial 1047297rms bytheir action consider earnings as the main determinant of dividends payout decisions asshown by lower lag dependent coef1047297cient (higher SOAs for earnings models [SOAEit])Earnings SOA (SOAEit ) show improved smoothing in all the models followed by CFOs(SOACFOit ) and then FCF (SOAFCFit ) This suggests that Malaysia non-1047297nancial 1047297rmsconsider current earnings more important than current cash 1047298ow while takingdividends payout decisions An optimal dividends payout policy here is one that avoidsdividends smoothing The summary also shows that Malaysian non-1047297nancial 1047297rmsconsider prior year cash 1047298ow more important in dividends decisions than prior yearearnings

JFRA131

14

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 1620

Table VIEarnings CFO

versus dividends

smoothing I n d e p e n d e n t v a r i a b l e s

O L S

F - E - M

G M M ( d i f f )

G M M ( s y s )

G M M ( s y s - w c - r o b u s t )

C o n s t a n t

0 0 0 8 ( 0 0 0 6 )

0 1 8 6 ( 0 0 1 6 )

0 0 8 0 ( 0 0 0 6 )

0 0 8 0

( 0 2 8 5 )

L o g ( D i t

[ 1 ] )

0 8 8 7 ( 0 0 1 6 )

0 5 3 3 ( 0 0 3 0 )

0 3 9 8 ( 0 0 0 0 5 )

0 6 9 1 ( 0 0 0 0 5 )

0 6 9 1

( 0 5 4 9 )

L o g ( E i t )

0 0 8 7 ( 0 0 1 0 )

0 0 8 4 ( 0 0 1 0 )

0 0 3 2 ( 0 0 0 0 3 )

0 0 8 1 ( 0 0 0 0 5 )

0 0 8 1

( 0 0 9 2 )

L o g ( C F O i t )

0 0 3 1 ( 0 0 0 7 )

0 0 4 7 ( 0 0 1 0 )

0 0 1 7 ( 0 0 0 0 3 )

0 0 3 9 ( 0 0 0 0 4 )

0 0 3 8

( 0 1 0 1 )

Y e a r i n c l u d e d

Y e s

Y e s

Y e s

Y e s

Y e s

S O A

0 1 1 3

0 4 6 7

0 3 9 8

0 3 0 9

0 3 0 9

N u m b e r o f O B S ( 1047297 r m ndash y e a r s )

1 8 3 4

1 8

3 4

1 8 3 4

1 8 3 4

1 8 3 4

B r e u s c h P a g a n L M x

2

1 0 0 0 dagger

H a u s m a n t e s t f o r r a n d o m e f f e c t s

1

7 4

R 2

0 8 3

0 8 2

F

2 7 3 8

2

1 0

W a l d s c h i - s q u a r e f o r z e r o c o e f 1047297 c i e n t

8 7 9 0 0 0

3 9 9 0 0 0

5 4 0

A b o n d t e s t f o r a u t o c o r r e l a t i o n

0 0 2 1 6 dagger ( 1 )

0 0 0 7 1 dagger ( 1 )

0 0 9 2 3 dagger

( 1 )

0 1 0 6 9 dagger ( 2 )

0 1 1 8 0 dagger ( 2 )

0 1 3 0 4 dagger

( 2 )

S a r g a n t e s t f o r o v e r - i d e n t i f y i n g r e s u l t s

1 3 0

1 2 7

N i l

0 2 7 2 5 dagger

0 1 7 1 3

N o t e s S i g n i 1047297 c a n t a t p

0 0

1 s i g n i 1047297 c a n t a t p

0 0 5 t w o s t e p s s t a n d a r d e r r o r s a r e i n p a r e n t h e s i s

dagger

r e p r e s e n t p v a l u e ( 1 ) r e p r e s e n t o r d e r 1 a n d ( 2 )

o r d e r 2 L o g ( D i t )

0

1 L o g ( D i t

[ 1 ] )

2 L o g ( E i t )

3 L o g ( E i t

[ 1 ] )

i

ϒ

i t

S o u r c e R e s e a r c h e r s rsquo a n a l y s i s r e

s u l t s

15

Corporatecash 1047298ow

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 1720

Table VIIEarnings FCF

versus dividends

smoothing I n d e p e n d e n t v a r i a b l e s

O L S

F - E - M

G M M ( d i f f )

G M M ( s y s )

G M M ( s y s - w c - r o b u s t )

C o n s t a n t

0 0 0 6 ( 0 0 0 6 )

0 1 8 5

( 0 0 1 6 )

0 1 2 1 ( 0 0 0 7 )

0 1 2 1

( 0 2 7 5 )

L o g ( D i t [ 1 ] )

0 8 6 7 ( 0 0 1 6 )

0 5 5 1

( 0 0 3 0 )

0 3 9 5 ( 0 0 0 0 3 )

0 7 0 3 ( 0 0 0 0 5 )

0 7 0 3

( 0 1 9 6 )

L o g ( E i t )

0 0 8 9 ( 0 0 1 0 )

0 0 9 3

( 0 0 1 0 )

0 0 3 1 ( 0 0 0 0 3 )

0 0 8 4 ( 0 0 0 0 5 )

0 0 8 4

( 0 0 4 0 )

L o g ( F C F i t )

0 0 3 2 ( 0 0 0 7 )

0 0 2

2 ( 0 0 0 8 )

0 0 1 7 ( 0 0 0 0 2 )

0 0 2 6 ( 0 0 0 0 4 )

0 0 2 6

( 0 0 3 7 )

Y e a r i n c l u d e d

Y e s

Y e s

Y e s

Y e s

Y e s

S O A

0 1 3 7

0 4 4 9

0 3 9 5

0 2 9 7

0 2 9 7

N u m b e r o f O B S ( 1047297 r m ndash y e a r s )

1 8 3 4

1 8 3

4

1 8 3 4

1 8 3 4

1 8 3 4

B r e u s c h ndash P a g a n L M x

2

1 0 0 0 dagger

H a u s m a n t e s t f o r r a n d o m e f f e c t s

1 5

6

R 2

0 8 3

0 8 2

F

2 7 3 9

2 0

4

W a l d s c h i - s q u a r e f o r z e r o c o e f 1047297 c i e n t

8 7 9 0 0 0

3 3 7 0 0 0 0

6 7 4

A b o n d t e s t f o r a u t o c o r r e l a t i o n

0 0 2 1 6 dagger ( 1 )

0 0 0 7 1 dagger ( 1 )

0 0 1 4 3 dagger

( 1 )

0 1 0 6 9 dagger ( 2 )

0 1 0 4 8 dagger ( 2 )

0 1 0 8 4 dagger

( 2 )

S a r g a n t e s t f o r o v e r - i d e n t i f y i n g r e s u l t s

1 3 0

1 2 9

N i l

0 2 7 2 5 dagger

0 1 4 5 5

N o t e s S i g n i 1047297 c a n t a t p 0 0

1 s i g n i 1047297 c a n t a t p

0 0 5 t w o s t e

p s s t a n d a r d e r r o r s a r e i n p a r e n t h e s i s

dagger

r e p r e s e n t p v a l u e ( 1 ) r e p r e s e n t o

r d e r 1 a n d

( 2 ) o r d e r 2 L o g ( D i t )

0

1 L o

g ( D i t

[ 1 ] )

2 L o g ( E i t )

3 L o g (

E i t

[ 1 ] )

i

ϒ

i t

S o u r c e R e s e a r c h e r s rsquo a n a l y s i s r e

s u l t s

JFRA131

16

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 1820

5 Summary conclusions and recommendationsThe research contributes to recent debate in 1047297nance and accounting literatureconcerning the key determinants of changes in dividends payout policy decisions insome jurisdictions Andres et al (2009) concluded that German 1047297rms base theirdividend decisions on cash 1047298ows rather than published earnings Al-Najjar andBelghitar (2012) argue that UK 1047297rms rely more on their cash 1047298ows to pay dividendsand that Lintnerrsquos (1956) partial adjustment model seems not to work very well inthe UK

The research 1047297nds that Malaysia non-1047297nancial 1047297rms consider prior year

dividends current year earnings current cash 1047298ow from operations current FCFsand prior year cash 1047298ows while taking dividends payout decisions Current earningsare however considered more important than cash 1047298ow while taking dividendspayout decisions This is consistent with Lintnerrsquos (1956) partial adjustment modeland Fama and Babiak (1968) but inconsistent with Andres et al (2009) Al-Najjarand Belghitar (2012) We also 1047297nd that Malaysian non-1047297nancial 1047297rms consider FCFwhile taking dividends payout decisions This supports our hypothesis that FCFsare key determinants in explaining dividends smoothing among Malaysian 1047297rmsand this is consistent with the work of Easterbrook (1984) and Jensen (1986) onagency theory that managers consider FCF while taking dividends payoutdecisions mostly to reduce agency con1047298icts

The research concludes that Malaysian non-1047297nancial 1047297rms participate individends smoothing and that they consider current yearrsquos earnings more importantthan current cash 1047298ow while making dividends payout decisions They alsoconsider FCF while taking dividends payout decisions The policy implication isthat earnings are smoothing agents and the more they are considered in dividendspayout decisions the less dividends are smoothened If dividends smoothing is notprevented it could lead to dividends-based earnings management and hencefraudulent 1047297nancial reporting to satisfy cash dividendsndashpush investors withattendant consequences The research is our novel contribution of assistinginvestors and government in making informed decisions regarding dividends policyin Malaysia

Table VIIISummary of

earnings CFO and

FCF versus

dividends smoothing

Independent variables OLS F-E-M GMM (diff) GMM (sys) GMM (sys-wc-robust)

CoeffDit ( 1)E 0886 0479 0368 0633 0633

CoeffDit ( 1)CFO 0925 0489 0341 0699 0699CoeffDit ( 1)FCF 0914 0507 0321 0703 0703

CoeffEit ( 1) 0005 0019 0014 0013 0014

CoeffCFOit ( 1) 0012 0038 000002 0021 0021

CoeffFCFit ( 1) 0034 0034 0005 0016 0016

SOAEit 0114 0521 0368 0377 0377

SOACFOit 0075 0511 0341 0301 0301

SOAFCFit 0086 0493 0321 0293 0293

SOAEit CFOit 0113 0467 0398 0309 0309

SOAEit FCFit 0137 0449 0395 0297 0297

Notes Signi1047297cant at p 001 signi1047297cant at p 01

Source Researchersrsquo analysis results

17

Corporatecash 1047298ow

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 1920

Notes

1 Arellano-Bond (1988 1991 ) developed a linear 1047297rst difference GMM estimator to deal with

such problems The estimators are designed for situations with ldquosmall T large Nrdquo panels

meaning few time periods and many individuals with independent variables that are notstrictly exogenous

2 Arellano and Bover (1995)Blundell and Bond (1998) further re1047297ned Arellano and Bondrsquos

(1991) model Their analysis show that in dynamic panel data models where the

autoregressive parameter is moderately large and the number of time series observations is

moderately small the GMM 1047297rst-differences IV estimator is poorly behaved They therefore

developed the GMMsys

References

Adaoglu C (2000) ldquoInstability in the dividend policy of the Istanbul Stock Exchange (ISE)

Corporations evidence from an emerging marketrdquo Emerging Markets Review Vol 1 No 3pp 252-270

Adelegan OJ (2003) ldquoAn empirical analysis of the relationship between cash 1047298ow anddividend changes in Nigeriardquo African Development Review Vol 15 No 1 pp 35-49

Al-Najjar B and Belghitar Y (2012) ldquoThe information content of cash1047298ows in the context of dividend smoothingrdquo Economic Issues Vol 17 No 2 pp 57-70

Al-Yahyaee KH Pham TM and Walter TS (2011) ldquoDividend smoothing when 1047297rmsdistribute most of their earnings as dividendsrdquo Applied Financial EconomicsVol21No16pp 1175-1183

Andres C Betzer A Goergen M and Renneboog L (2009) ldquoDividend policy of German 1047297rmsa panel data analysis of partial adjustment modelsrdquo The Journal of Empirical Finance

Vol 16 No 2 pp 175-187Appannan S and Sim LW (2011) ldquoA study on leading determinants of dividend policy in

Malaysia listed companies for food industry under consumer product sectorrdquo Proceeding of 2nd International Conference on Business and Economic Research Holiday Villa Beach Resort and Spa Langkawi Kedah Vol 2 pp 945-976

Arellano M and Bond SR (1988) ldquoDynamic panel data estimation using DPD-A guide for usersrdquoWorking Paper 8815 Institute for Fiscal Studies London

Arellano M and Bond S (1991) ldquoSome tests of speci1047297cation for panel data Monte Carlo evidenceand an application to employment equationsrdquo Review of Economic Studies Vol 58 No 2pp 277-297

Arellano M and Bover O (1995) ldquoAnother look at the instrumental variable estimation of error

component modelsrdquo Journal of Econometrics Vol 68 No 1 pp 29-51

Blundell R and Bond S (1998) ldquoInitial conditions and moment restrictions in dynamic panel datamodelsrdquo Journal of Econometrics Vol 87 No 1 pp 115-143

Brav A Graham J Harvey C and Michaely R (2005) ldquoPayout policy in the 21st centuryrdquo Journal of Financial Economics Vol 77 No 3 pp 483-527

Charitou A and Vafeas N (1998) ldquoThe association between operating cash 1047298ows and dividendchanges an empirical investigationrdquo Journal of Business Finance and Accounting Vol 25Nos 12 pp 225-249

Easterbrook F (1984) ldquoTwo agency-cost explanations of dividendsrdquo American Economic ReviewVol 74 No 4 pp 650-659

JFRA131

18

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 2020

Fama EF and Babiak H (1968) ldquoDividend policy an empirical analysisrdquo Journal of the American Statistical Association Vol 63 No 324 pp 1132-1161

Guttman I Kadan O and Kandel E (2001) ldquoA theory of dividend smoothing 1rdquo Working Paper

Graduate School of Business Stanford University available at httpsscholargooglecomscholarhlenampqaccordingtoGuttman28200129iskeepingthedividendsper-shareconstantovertwoormoreconsecutiveyears2CampbtnGampas_sdt12C5ampas_sdtp

Hausman JA (1978) ldquoSpeci1047297cation tests in econometricsrdquo Econometrica Vol 46 No 6pp 1251-1273

Healy P (1985) ldquoThe impact of bonus schemes on the selection of accounting principlesrdquo Journal of Accounting and Economics Vol 7 No 1 pp 85-107

Jensen MC (1986) ldquoAgency cost of free cash 1047298ow corporate 1047297nance and takeoversrdquo American Economic Review Vol 76 No 2 pp 323-329

Lee TA (1983) ldquoFunds statements and cash 1047298ow analysisrdquo Investment Analyst pp 13-21

Levin A Lin CF and Chu CSJ (2002) ldquoUnit root tests in panel data asymptotic and1047297nite-sample propertiesrdquo Journal of Econometrics Vol 108 No 1 pp 1-24

Lintner J (1956) ldquoDistribution of incomes of corporations among retained earnings and taxesrdquo American Economic Review Vol 46 No 2 pp 97-113

Miller MH and Modigliani F (1961) ldquoDividend policy growth and valuation of sharesrdquo Journal of Business Vol 34 No 4 pp 411-433

Mohamed N Shu Hui W Omar N Abdul Rahman R and Norrsquoazam M (2005) ldquoEmpiricalanalysis of determinants of dividends payments pro1047297tability and liquidityrdquo available atwbiconprocom145B15DHuipdf

Nickell S (1981) ldquoBiases in dynamic models with 1047297xed effectsrdquo Econometrica Vol 49 No 6pp 1417-1426

Normah O Rashidah AR Wee SH Norrsquoazam M Norhayati M Wan Azmimi WM andMaz Ainy AA (2006) Dividend Survey 2006 MSWG UiTM Kuala Lumpur

Simons K (1994) ldquoThe relationship between dividend changes and cash 1047298ow an empiricalanalysisrdquo Journal of Business Finance and Accounting Vol 21 No 4 pp 577-587

Further reading

Crum R Jensen D and Ketz E (1988) ldquoAn investigation of managementrsquos dividend policy modeland cash 1047298ow measuresrdquo Working Paper PA State University PA

Leary M and Michaely R (2011) ldquoDeterminants of dividend smoothing empirical evidencerdquo Review of Financial Studies Vol 24 No 10 pp 3197-3294

Corresponding authorApedzan Emmanuel Kighir can be contacted at apedzankighir2007yahoocom

For instructions on how to order reprints of this article please visit our websitewwwemeraldgrouppublishingcomlicensingreprintshtmOr contact us for further details permissionsemeraldinsightcom

19

Corporatecash 1047298ow

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 220

Related content and download information correct at time of

download

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 320

Corporate cash 1047298ow and

dividends smoothing a paneldata analysis at Bursa MalaysiaApedzan Emmanuel Kighir

Department of Financial Reporting Accounting Research InstituteShah Alam Malaysia and

Normah Haji Omar and Norhayati Mohamed Accounting Research Institute Universiti Teknologi MARA

Shah Alam Malaysia

Abstract

Purpose ndash The purpose of this paper is to contribute to the debate and 1047297nd out the impact of cash 1047298ow

on changes in dividend payout decisions among non-1047297nancial 1047297rms quoted at Bursa Malaysia as

compared to earnings There has been renewed debate in recent 1047297nance and accounting literature

concerning the key determinants of changes in dividends payout policy decisions in some jurisdictions

The conclusion in some is that 1047297rms base their dividend decisions on cash 1047298ows rather than published

earnings

Designmethodologyapproach ndash The research made use of panel data from 1999 to 2012 at Bursa

Malaysia using generalized method of moments as the main method of analysis

Findings ndash The research 1047297nds that Malaysia non-1047297nancial 1047297rms consider current earnings more

important than current cash 1047298ow while making dividends payout decisions and prior year cash 1047298owsare considered more important in dividends decisions than prior year earnings We also found support

for Jensen (1986) in Malaysia on agency theory that managers of 1047297rms pay dividends from free cash

1047298ow to reduce agency con1047298icts

Practical implications ndash The research concludes that Malaysian non-1047297nancial 1047297rms use current

earnings and less of current cash 1047298ow in making changes in dividends policy The policy implication is

that current earnings are dividends smoothing agents and the more they are considered in dividends

payout decisions the less of dividends smoothing

Social implications ndash If dividends smoothing is encouraged it could lead to dividends-based

earnings management

Originalityvalue ndash The research is our novel contribution of assisting investors and government in

making informed decisions regarding dividends policy in Malaysia

Keywords Bursa Malaysia Cash 1047298ow from operations Dividends smoothing Free cash 1047298owSpeed of adjustment Target payout ratio

Paper type Research paper

1 IntroductionLintner (1956) de1047297ned dividends smoothing as the variation in dividends that isdifferent from the variation in earnings Dividend smoothing according to

The researchers gratefully acknowledge 1047297nancial support from the Ministry of EducationMalaysia through Accounting Research Institute Universiti Teknologi MARA Malaysiatowards the research

The current issue and full text archive of this journal is available on Emerald Insight at

wwwemeraldinsightcom1985-2517htm

JFRA131

2

Received 26 September2013Revised18 April 2014Accepted 8 August2014

Journal of Financial Reporting and

Accounting

Vol 13 No 1 2015

pp 2-19

copy Emerald GroupPublishing Limited

1985-2517

DOI 101108JFRA-09-2013-0072

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 420

Guttman et al (2001) is keeping the dividends per share constant over two or moreconsecutive years ie stability of dividends Managers are said to smooth dividendsif they follow a constant nominal dividend payment policy with a partial adjustment

strategy Dividends smoothing involves setting a dividend payout policy that doesnot necessarily conform to earnings

Lintner (1956) in his seminal work on partial adjustment hypothesis held that 1047297rmsrealizing the transitory nature of current earnings adjust only partially to its desiredlevel of dividend with a time lag Lintner (1956) observed that 1047297rms are primarilyconcerned with the stability of dividends Instead of setting dividends each quarter1047297rms 1047297rst consider whether they need to make any changes from the existing rate Onlywhen they have decided that a change is necessary do they consider how large it shouldbe These views were later supported with an addition by Miller and Modigliani (1961)Miller and Modigliani in their classic argued that changes in dividends depend largelyon managementrsquos expectations of future earnings and cash 1047298ows Lee (1983) points out

that dividend payment should be based on cash 1047298ows not on earnings because cash1047298ows better re1047298ect the position of the 1047297rm Healy (1985) conducted his research on theimpact of bonus schemes on the selection of accounting principles and argued that cash1047298ows are more reliable in determining 1047297rm value than earnings because the latter caneasily be manipulated by managers to maximise their own compensation

There has been a renewed debate in recent 1047297nance and accounting literature similarto that of Lee (1983) concerning the key determinants of dividends payout policydecisions in some jurisdictions Andres et al (2009) concluded that German 1047297rms basetheir dividend decisions on cash 1047298ows rather than published earnings Al-Najjar andBelghitar (2012) argue that UK 1047297rms rely more on their cash 1047298ows to pay dividends andthat Lintnerrsquos (1956) partial adjustment model seems not to work very well in the UK

The main objective of this research is to contribute to the above debate and 1047297nd outthe impact of cash 1047298ow on changes in dividend payout decisions among non-1047297nancial1047297rms quoted at Bursa Malaysia as compared to earnings The study is unique asresearch on the association between cash 1047298ows and dividends changes has been limitedin Malaysia In addition unlike others who combined cash 1047298ow we separate free cash1047298ow (FCF) from cash 1047298ow from operations (CFOs) to determine speci1047297cally which of them have much impact on changes in dividends decisions in Malaysia using a muchmore advanced econometric technique the generalized method of moments (GMMs)

The remaining part of this paper covers hypothesis development in Section 2research methodology adopted in Section 3 and we take on data presentation andanalysis in Section 4 while summary conclusions and recommendations is in Section 5

2 Hypothesis development and literature reviewWe hypothesized that earnings are the key determinants of changes in dividendsdecisions among Malaysian 1047297rms

Lintner (1956) in his seminal work on partial adjustment hypothesis held that 1047297rmsrealizing the transitory nature of current earnings adjust only partially to its desiredlevel of dividend with a time lag Lintner (1956) surveyed managers on their attitudestowards dividend policy and concluded that managers target a long-term payout ratioHe also found that dividends are sticky tied to long-term sustainable earnings paid bymature companies and is smoothed from year to year

3

Corporatecash 1047298ow

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 520

For any year t the target level of dividends Dit for 1047297rm i is related to currentearnings Eit by a target payout ratio ri

Dit ri (1)

Dit represents the dividends which the company would have paid in the current year if its dividend were based simply on its 1047297xed target payout ratio ri applied to currentpro1047297ts

Dit ( Dit Dit1 ) ci( Dit 22 Dit1 ) uit (2)

Dit is the actual change in the dividend and (Dit Dit1 ) is the target change in thedividend

Substituting equation ( 1 ) into equation ( 2 )

Dit ci( riPit Dit1 ) uit (3)

ci as the speed of adjustment (SOA) as proxy for 1047297rmrsquos reluctance to cut dividends r i

as the target payout ratio and Pt is the current yearrsquos pro1047297ts after taxes or earnings Eit

Replacing Pit with Eit

Dit ciriEit ciDit1 uit (4)

Rearranging and replacing constants with

Dit 0 1Dit1 2Eit uit (5)

0 as proxy for 1047297rmrsquos reluctance to cut dividends1ci and ci is the SOA whichis expected to be 0 ci 1 and 2 ciri (and ri target payout ratio 2ci)Furthermore a positive0 represents the managementrsquos resistance to reduce dividendsor reluctance to cut dividends while negative 0 represents the managementrsquoswillingness to reduce dividends

The SOA is the speed with which management would try to move towards a fulladjustment of dividends to current earnings Large values for the SOA suggest anerratic dividend policy characterized by large changes driven by transitory shocksConversely small values for the SOA suggest a smooth persistent dividend policycharacterized by insensitivity to transitory earnings shocks and a desire to smooth the

shock over many periods Here the reluctance to cut dividends the target payout ratioand the SOA are estimated in the regression

Fama and Babiak (1968) extended the partial adjustment model by including alagged earnings variable

Dit 0 1Dit1 2Eit 3Eit1 uit (6)

Adaoglu (2000) conducted a research on instability in the dividend policy of theIstanbul Stock Exchange (ISE) corporations Evidence from an Emerging Marketand found that dividend policy behaviour of corporations operating in emergingmarkets is signi1047297cantly different from the widely accepted dividend policy

JFRA131

4

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 620

behaviour of corporations operating in developed markets His empirical resultsshow that the ISE corporations follow unstable cash dividend policies and the mainfactor that determines the amount of cash dividends is the earnings of the

corporation in that yearBrav et al (2005) 1047297nd that managers are willing to raise external capital or even

forego positive net present value (NPV) investments to avoid cutting dividendsAl-Yahyae et al (2011) conducted their research in Oman a developing economy on

ldquoDividend smoothing when 1047297rms distribute most of their earnings as dividendsrdquo Theresearch found that Omani 1047297rms have unstable dividend policies and target payoutratios and they adjust their dividend policies very quickly and are willing to cut theirdividends

In Malaysia prior studies in the area of determinants of dividend policy changeshave been limited A study by Mohamed et al (2005) on determinants of dividendspayments pro1047297tability and liquidity and Normah et al (2006) on dividends survey

revealed that Malaysian 1047297rms payout a large proportion of their earnings individends Appannan and Sim (2011) examines the leading determinants affectingthe dividend payment decision by company management in Malaysia listedcompanies for food industries under the consumer products sector and concludedthat debt equity ratio and past dividend per share were the important determinantsof dividend payment

H1 Earnings are the key determinants in explaining dividends smoothing amongMalaysian 1047297rms

We expect a positive coef1047297cient A signi1047297cant impact would support our hypothesis andthe SOA compared with that of CFO or FCF

We hypothesized that cash 1047298ows are the key determinants of changes individends decisions among Malaysian 1047297rms Our hypothesis would be supportedwhere cash 1047298ow is signi1047297cant on partial adjustment model Lee (1983) points outthat dividend payment should be based on cash 1047298ows not on earnings because cash1047298ows better re1047298ect the position of the 1047297rm Andres et al (2009) conducted theirresearch in Germany and found that German 1047297rms payout a lower proportion of their cash 1047298ows but a higher proportion of their published pro1047297ts than UK and US1047297rms They estimated partial adjustment models and report two major 1047297ndingsFirst German 1047297rms base their dividend decisions on cash 1047298ows rather thanpublished earnings as published earnings do not correctly re1047298ect performancebecause German 1047297rms retain parts of their earnings to build up legal reserves and

as published earnings are subject to more smoothing than cash 1047298ows Second to theopposite of UK and US 1047297rms German 1047297rms have more 1047298exible dividend policies asthey are willing to cut the dividend when pro1047297tability is only temporarily downAl-Najjar and Belghitar (2012) conducted their research on ldquoThe information contentof cash 1047298ows in the context of dividend smoothingrdquo using a modi1047297ed dividendpartial adjustment model In their model they replaced current yearrsquos earnings withFCF as according to them UK 1047297rms rely more on their cash 1047298ows to pay dividendsand that Lintnerrsquos (1956) partial adjustment model seems not to work very well inthe UK That their results were consistent across the different models and show thatcash 1047298ows are superior to earnings in dividend smoothing suggesting that cash1047298ows are the key determinant of dividend payments This is because their proposed

5

Corporatecash 1047298ow

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 720

dividend partial adjustment model has a lower adjustment coef1047297cient than Lintnerrsquosmodel suggesting that their estimates are much closer to reality They concludedthat the modi1047297ed version of Lintnerrsquos model explains better the smoothing process

of dividends for UK 1047297rms H2 CFOs are the key determinants in explaining dividends smoothing among

Malaysian 1047297rms

We expect a positive coef1047297cient of CFO A signi1047297cant impact would support ourhypothesis and would also indicate that 1047297rms make use of cash generated fromoperations to pay dividends The SOA would also be compared with that of earnings orFCF to determine which better explains dividends smoothing A higher SOAbetter explains the impact of a variable on dividends as it reduces dependence on prioryear dividends (Dit1 ) which is a smoothing agent The higher the Dit1 coef1047297cient thelower the SOA and the more dividends smoothing a 1047297rm is tagged

H3 FCFs are the key determinants in explaining dividends smoothing amongMalaysian 1047297rms

We expect a positive coef1047297cient of FCF A signi1047297cant impact would support ourhypothesis and would also indicate that 1047297rms make use of FCF to pay dividends Thiswill also support Jensen (1986) that managers try to reduce agency con1047298ict by payingdividends to shareholders out of FCFs The SOA is compared with that of earnings orCFO to determine which better explains dividends smoothing

Finally we hypothesized that both earnings and cash 1047298ows are equally consideredby 1047297rms as key determinants of changes in dividends decisions Our hypothesis issupported where both earnings and cash 1047298ow are signi1047297cant on partial adjustment

model Miller and Modigliani (1961) in their classic argued that changes in dividendsdepend largely on managementrsquos expectations of future earnings and cash 1047298owsSimonsrsquo (1994) study tried to provide evidence on the incremental information content of cash 1047298ow numbers over pro1047297ts and previous yearrsquos dividends (Lintnerrsquos model) inexplaining changes in cash dividends The study was however inconclusive Charitouand Vafeas (1998) conducted a study on association between operating cash 1047298ows anddividend changes given earnings and argue that a positive relationship between cash1047298ows and dividend changes should exist due to liquidity and accruals managementconsiderations Their study found empirical evidence that the dividend changesndashcash1047298ow relationship is signi1047297cantly positive when operating cash 1047298ows are low comparedto earnings and when 1047297rm growth is moderate Andres et al (2009) and Adelegan (2003)

re-evaluate the incremental information content of cash 1047298ows in explaining dividendchanges given earnings in Nigeria and found a signi1047297cant relationship betweendividend changes and cash 1047298ow unlike previous studies The empirical results revealthat the relationship between cash 1047298ows and dividend changes depends substantiallyon the level of growth the capital structure choice size of each 1047297rm and economic policychanges

H4 Earnings are better determinants than CFOs in explaining dividends smoothingamong Malaysian 1047297rms

H5 Earnings are better determinants than FCF in explaining dividends smoothingamong Malaysian 1047297rms

JFRA131

6

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 820

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 920

We therefore use the GMM technique developed by Arellano and Bond (1991) (GMM(diff)[1] Arellano and Bover (1995)Blundell and Bond (1998) (GMMsys)[2] in additionto the estimated generalized least squares random effects model and least squares FEM

to estimate dividends and earnings panel data We make use of Hausmanrsquos (1978)con1047297rmatory test for correlated random effects and BreuschndashPagan Lagrangemultiplier(1980) to decide between a panel random effects regression and a pooled OLSregression

The models for this research are therefore

LogDit 0 1LogDit1 2LogEit 3LogEit1 ϒi ui eit (8)

Where LogDit is dividend per share as dependent variable Dit1 lagged dividend pershare Eit earnings per share and Eit-1 lagged earnings per share as regressors withias cross-sectional effect coef1047297cient and it is a 1047297rm-speci1047297c effect for unobserved

in1047298uences on the dividend behaviour of each 1047297rm and is assumed to remain constantover time i as time period effect coef1047297cient and they are time dummies that control forthe impact of time on the dividend behaviour of all sampled 1047297rms The eit is a whitenoise

Our modi1047297ed versions of the model is as follows

LogDit 0 1LogDit1 2LogCFOit 3LogCFOit1 ϒi ui eit (9)

Where CFO is cash 1047298ow from operations per year

LogDit 0 1LogDit1 2LogFCFit 3LogFCFit1 ϒi ui eit (10)

Where FCF is free cash 1047298ow per share

LogDit 0 1LogDit1 2LogEit 3LogCFOit ϒi ui eit (11)

LogDit 0 1LogDit1 2LogEit 4LogFCFit ϒi ui eit (12)

This research adopts 5 per cent signi1047297cant level as its maximum level of rejection or notrejecting any hypothesis

4 Data presentation and analysis41 Analysis results

Table I shows an average dividends payout ratio relative to earnings of 0445 0441relative to CFOs and 0299 relative to FCF This means Malaysian 1047297rms use 445 per centof their current earnings to pay dividends 441 per cent of cash generated for the currentperiod to pay dividends and about 30 per cent of current yearrsquos FCF to pay dividendsThe zero values in the minimum column are companies that reported negative earningsor CFOs or FCFs

Table II shows correlations between the variables The strongest is between CFOsand FCFs This indicates that these variables cannot be regressors in the same test toavoid multicollinearity

411 Unit root test unit root (common unit root process) We used Levin et al (2002)test for unit root as our data are a panel data and normal time series unit root tests will

JFRA131

8

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 1020

Table IDescriptive statistics

D e s c r i p t i v e s t a t i s t i c s

V a r i a b l e s

N

M i n i m u m

M a x i m u m

M e

a n

S D

S k e w

n e s s

K u r t o s i s

S t a t i s t i c

S t a t i s t i c

S t a t i s t i c

S t a t i s t i c

S t a t i s t i c

S t a t i s t i c

S

t a n d a r d e r r o r

S t a t i s t i c

S t a n

d a r d e r r o r

D i t

1 8 3 4

0 0 0 3

3 1 0 0

0 1 1

4 9 7

0 2 4 7 3 7 5

6 9 9 0

0 0 5 7

6 0 2 0 3

0 1 1 4

E i t

1 7 5 1

0 0 0 0

4 8 2 6

0 2 5

8 3 0

0 3 4 1 5 8 9

4 7 5 9

0 0 5 8

3 4 9 9 5

0 1 1 7

C F O i t

1 3 0 1

0 0 0 0

2 9 2 4

0 2 7

9 2 0

0 3 8 5 2 3 0

3 6 3 2

0 0 6 8

1 6 8 6 4

0 1 3 6

F C F i t

1 6 5 4

0 0 0 0

3 6 1 8

0 3 8

4 2 7

0 4 8 0 2 6 7

3 0 5 4

0 0 6 0

1 1 5 1 3

0 1 2 0

V a l i d N ( l i s t w i s e )

1 2 5 6

N o t e s D i t

D i v i d e n d s f o r i n d i v

i d u a l c o m p a n i e s i n y e a r t E i t

e a r n

i n g s f o r i n d i v i d u a l c o m p a n i e s i n y e a

r t C F O i t

c a s h 1047298 o w f o r i n d i v i d u a l c o m p a n i e s

i n y e a r t F C F i t

f r e e c a s h 1047298 o w f o r i n d i v i d u a l c o m p a n i e s i n y e a r t

9

Corporatecash 1047298ow

8162019 Kig Hir 2015

httpslidepdfcomreaderfullkig-hir-2015 1120

not be appropriate The unit root test is necessary as the regression of a non-stationaryvariable against another non-stationary variable gives a spurious regression whosecoef1047297cients are biased and inef1047297cient We found a unit root with dividend variable at

levels but on inclusion of time trend the dividend became stationary A similar test wasconducted on earnings CFOs and FCF variables which show no unit root In thisresearch unit root may not be a problem as number of years are relatively small beinga micro panel analysis

412 Other results Table III shows the test result of smoothing where earnings areconsidered the key determinant of dividend payout policy with post-estimation test of BreuschndashPagan Hausman correlational random test abond test and Sargan tests allcon1047297rming the results

The results show signi1047297cant impact of prior year dividends current and prior yearearnings on dividends in three out of the 1047297ve models The impact is more from prior yeardividends followed by current earnings and then prior year earnings

This means that Malaysian non-1047297nancial 1047297rms consider current and prior yearearnings while taking dividends payout decisions This supports our hypothesis ( H1 )and it is consistent with work of Lintner (1956) Fama and Babiak (1968) and Brav et al(2005)

The result also shows SOA of between 0114 and 0521 suggesting that Malaysiannon-1047297nancial 1047297rms participate actively in dividends smoothing where earnings aretaking into consideration while deciding on dividend payout policy of these 1047297rms

Table IV shows the test result of smoothing where CFOs is considered the keydeterminant of dividend payout policy The results show signi1047297cant impact of prior yeardividends current and prior year CFOs on dividends in all the models The impact ismore from prior year dividends followed by current cash 1047298ows less of prior year cash

1047298owsThis means that Malaysian non-1047297nancial 1047297rms consider current and prior year cash