J.P. Morgan High Yield and Leveraged Finance Conference, Miami

26

J.P. Morgan High Yield and Leveraged Finance Conference, Miami February 2020

Transcript of J.P. Morgan High Yield and Leveraged Finance Conference, Miami

J.P. Morgan High Yield and Leveraged Finance Conference, MiamiFebruary 2020

Disclaimer

The information contained in these materials has been provided by ContourGlobal plc (“ContourGlobal” or the “Company”) and has not been independently verified.No representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of theinformation or opinions contained herein. It is not the Company’s intention to provide, and you may not rely on these materials as providing, a complete orcomprehensive analysis of the Company’s financial position or prospects. The information and opinions contained in these materials are provided as at the date ofthis presentation and are subject to change without notice. Neither the Company nor any of its affiliates, advisors or representatives shall have any liabilitywhatsoever (in negligence or otherwise) for any loss whatsoever arising from any use of this presentation or its contents or otherwise arising in connection with thispresentation.

Certain statements in this presentation are “forward-looking statements.” All statements other than statements of historical facts included in this presentation,including, without limitation, those regarding the Company’s financial position, business strategy, plans and objectives of management for future operations, areforward-looking statements. These statements involve a number of factors that could cause actual results to differ materially, including, but not limited to, changesin economic, business, social, political and market conditions, success of business and operating initiatives, and changes in the legal and regulatory environment andother government actions. Forward-looking statements contained in this presentation regarding past trends or activities should not be taken as a representation thatsuch trends or activities will continue in the future. Any forward-looking statement made during this presentation or in these materials speaks only as of the date onwhich it is made. The Company assumes no obligation to update or revise any forward-looking statements.

Information contained herein relating to markets, market size, market share, market position, growth rates, penetration rates and other industry data pertainingto the Company’s business is based on the Company’s estimates and is provided solely for illustrative purposes. In many cases, there is no readily available externalinformation to validate market-related analyses and estimates, thus requiring the Company to rely on internal surveys and studies. The Company has also compiled,extracted and reproduced market or other industry data from external sources, including third parties or industry or general publications, for the purposes ofits internal surveys and studies. Any such information may be subject to significant uncertainty due to differing definitions of the relevant markets and marketsegments described.

This presentation contains references to certain non-IFRS financial measures and operating measures. These supplemental measures should not be viewed in isolationor as alternatives to measures of the Company’s financial condition, results of operations or cash flows as presented in accordance with IFRS in its consolidatedfinancial statements. The non-IFRS financial and operating measures used by the Company may differ from, and not be comparable to, similarly titled measures usedby other companies. The non-IFRS adjustments for all periods presented are based upon information and assumptions available as of the date of this presentation.

2

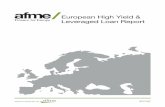

ARRUBAL

800 MW – SPAIN

CSP COMPLEX

250 MW – SPAIN

MARITSA

908 MW – BULGARIA

INKA

114 MW – PERU

BRAZIL WIND

598 MW

VOROTAN

404 MW – ARMENIA

Thermal Solar

Wind Hydro

High Efficiency Cogen / Energy Solutions business

CARIBBEAN

73 MW

BRAZIL HYDRO

167 MW

CHP COMPLEX

518 MW

AUSTRIA WIND

149 MW

Global Footprint: 4.8GW in 18 Countries

LEGEND

3

BRAZIL SOLUTIONS

76 MW

SOLAR ITALY

77 MW

SOLAR SLOVAKIA

35 MW

TOGO

100 MWKIVUWATT

26 MW

CAP DES BICHES

86 MW

SOLUTIONS EUROPE

34 MW

Colombia

405 MW

SOLUTIONS AFRICA

16 MW

0.2

0.060.03 0.03

2015 2016 2017 2018

4

Safety first: Commitment to Zero Harm With Best In Class Performance▪ Everyone goes home safe, everyday, everywhere

▪ “Target Zero” program sets the company-wide expectation that we will incur zero LTIs in all businesses for all people – employees, contractors and visitors

▪ Commitment to maintain the same high H&S standards in every country that we operate in. Proud to achieve globally consistent high H&S standards, which are significantly better than industry benchmarks

▪ Became member of the Campbell Institute at the National Safety Council

(1) Lost time incident rate (LTIR) is an industry standard reporting convention for calculating injuries in the workplace. LTIR measures recordable lost time incident (LTI) rates based on 200l working hrs

(2) Peers information as of 2018 reported in annual reports / sustainability reports published by companies normalized to basis of 200,000 workings hours. Selection of comparable peers from a CG sponsored study with all major US and European power generation companies

(3) Based on the 2018 US Bureau of Labor Statistics report(4) Total Recordable Incident Rate (TRIR) is an industry standard reporting convention for calculating recordable injuries in the

workplace. TRIR is the total lost time injuries, restricted workday cases and medical treatments on the basis of 200k working hrs

Lost Time Incident Rate (LTIR)1

On-going improvement in key H&S indicator

LTIR/TRIR Compared to Peers2 – Industry leader in H&S with KPIs significantly better than industry benchmarks

2018 Safety Scorecard5.7MMan hours worked without a lost time injury

85%Reduction in zero lost-time injuries in 4 years

63%Reduction in total recordable injuries in 4 years

95% less LTIR than US industry and 85% less than peers top quartile

(85%)

Total Recordable Incident Rate (TRIR)4

0.46

0.180.10

0.17

2015 2016 2017 2018

(63%)

0.6

0.9

0.2

0.43

0.030.17

LTIR TRIRUS Utilities -avg Peers - top quartile CG 2018

23

5

Business HighlightsWell-established power generation company with exceptional growth

Focused business model: acquire, develop and operate long-term contracted power generation assets

Diversified footprint by geography and technology: each asset category contributes less than 20% group EBITDA

High cashflow generation provides strong income protection while leaving significant liquidity for growth

Long term contracts and regulated tariffs with significant risk mitigation delivering stable and secure cash flows

Proven track record of value accretive growth through both operationally lead acquisitions and greenfield development, with attractive M&A and development pipeline

Efficient Capital Structure: primary use of non-recourse debt financing provides significant protection to equity investor

Long-term contracts with state-owned/supported utilities or large IG companies or stable regulatory regimes (avg. credit rating BBB-)

LimitedCredit Risk

Limited Duration and refinancing

Risk

NoCost Risk

Mitigated Political Risk

Negligible Volume Risk for Thermal

Limited /Mitigated Volume

Risk forRenewables

6

High-Quality and Stable BusinessesFixed-price, long-term contracts or regulated tariffs, with credit worthy off-takers

NoPrice Risk

(1) As of end of 2019

Long-term contracts, weighted average remaining contract life of 10 years1

Use of political risk insurance to limit exposure

Typical thermal PPAs virtually eliminate commodity risk via fuel and CO2 emission costs pass-throughs

• Thermal: no volume risk; plants receive full capacity payment irrespective of off-taker demand

• Renewables: diversification of portfolio limits resource risk

Fixed-price contracts that often contain inflation protection

7

M&A Strategy Demonstrates Ability to Improve Cost Structure While Increasing Operational Performance

Proven track-record of creating significant value in acquisitions through operational improvement

Asset Size Plant Type

908 MW LigniteMaritsa

800 MW Gas-firedArrubal

150 MW WindAustria Wind

65 MW Solar PVSolar Italy

28 MW Wind & HFOBonaire

250 MW Solar CSP Spanish CSP

Fixed Cost Reduction AvailabilityOther Operational Improvements

✓

✓

✓

✓

✓

✓

22%

20%

32%

16%

26%

12%

✓

✓

✓

✓

✓

✓

2%

2%

1%

3%

2%

4%

€2m fuel savings✓

✓ Insourced Operations: Zero LTI

✓ Repowering

O&M insourcedSell-down of 49% of asset for ~2x net equity value✓

Zero LTIs since 2015✓

Sell-down of 49% of asset for ~2x net equity value✓

Value Lever

92.6% 90.2% 93.3% 93.2%

2017 2018 H1 2018 H1 2019

92.7% 95.8% 95.8% 96.1%

2017 2018 H1 2018 H1 2019

97.8% 98.5% 98.5% 98.2%

2017 2018 H1 2018 H1 2019

99.2% 99.2% 99.7% 98.3%95.3% 96.7% 94.6%

2017 2018 H1 2018 H1 2019

Solar PV Solar CSP

Power Generation Operating PerformanceConsistently Strong Performance Across All Technologies

Thermal – Equivalent Availability Factor1 (%)

Hydro – Equivalent Availability Factor1 (%)

Wind – Equivalent Availability Factor1 (%)

Solar – Equivalent Availability Factor1 (%)

(1) Equivalent Availability factor refers to the actual amount of time a plant or group of plants is available to produce electricity

• Technical performance is in line with previous periods and well above minimum PPA required threshold

• Ongoing improvement in Brazil Wind operations driving EAF improvements

8

• Excellent hydro availability; plants primarily rewarded on capacity or regulatory payments as opposed to individual plant generation

• Decrease in H12019 availability due to blade failure in CSP and forced outages and maintenance at Solar Italy

• Strong production performance at CSP despite lower H1 2019 EAF

74% weighted average PPA minimum availability requirement

Our Principles: Going Beyond Power with Key ESG Commitments

Grow Well

Implementing “Next

Generation”

technologies such as

Bonaire battery

storage and Quad-Gen

technology

Providing power in

underserved countries

such as Togo, Senegal,

Rwanda

Operate Safely & Efficiently and Minimize

Impacts

Manage our Businesses Responsibly

Enhance the Operating Environment

Supplier Code of Conduct

and incentive program for

adherence to UNGC

principles

Top decile and quartile

operational KPIs and

robust benchmarking

Programs to

strengthen

Institutional and

Private Sector Capacity

Effective Social Investment

and Community

Engagement

Air Emissions, Waste and

Water Management

Plans

H&S Target Zero for all

employees, contractors

and visitors

Adhere to Highest Standards

of Corporate Governance

and Business Ethics and

Uphold Human Rights and

Labor Principles

Governmental support

to improve Policy and

the Regulatory

Environment

Partnerships to

increase Power

Accessibility and

Affordability

Worker Exchange

Program and global

training plans

9

10

Commitment to CommunityWe strive to make positive impact on the communities where we operate

ContourGlobal 2018 Social Responsibility Performance

122Social investment projects

+31% on 2017

~ 996,000Beneficiaries from social projects

+109% on 2017

$ 2.4 MillionTotal investment+102% on 2017

283ContourGlobal employees dedicated to social

investment initiatives

▪ More than 20,500 hours dedicated to social investment initiatives

▪ Around 2,800 hours devoted to social volunteering activities in our communities

Social Investment Projects

Europe 45%

Latam 40%

Africa 14%

America 1%

Community Education & Engagement

19,000 hours

16,000 hours Community education activities

Community engagement activities

122Projects

21

21

17

16

16

16

16

15

14

11

10

6

6

6

4

4

4

4

2

2

KivuWatt

Vorotan

Hydro Brazil

Cap des Biches

Spain CSP

Chapada Complex

Togo

Inka

Asa Branca

Mexico

Solar Italy

Solar Slovakia

Austria Wind

Bonaire

Maritsa

Sochagota

Termoemcali

Solutions

French Carribbean

Arrubal

11

Stable Long Term Contracted / Regulated Revenues Delivering Robust Cash FlowsWeighted Average Remaining Contracted / Regulated Term of 10 Years

(1) For assets with multiple PPAs, numbers shown based on midpoint of the expiration dates for such PPAs; data as of 30-Jun-2019.(2) Weighted by adjusted EBITDA before corporate and holding company costs.

Maintaining Long Weighted Average Remaining Contracted / Regulated Term2 (Years)

Remaining Contracted / Regulated Life by Asset (Years)1,2

% of Total Estimated Adjusted Revenues in 2019E-2024E

>90%

<10%

Contracted / Regulated Revenue Uncontracted / Unregulated Revenue

Current contracts / regulated revenues

have a weighted average remaining

term ofc.10 years

12 11

12 11

2015 2016 2017 2018

17%

15%

6%

17%

14%

23%

8%

Coal Natural Gas

Fuel oil High Efficiency Cogen

Wind Solar

Hydro

Diversification Across Geographies and TechnologiesAdj. EBITDA

LTM H1 2019 PF EBITDA by Technology1

LTM H1 2019 PF EBITDA by Currency1

LTM H1 2019 PF EBITDA by Geography1

(1) PF for full year EBITDA of Mexican CHP acquisition completed in November 2019 ($110m) and Solar InterPorto acquisition completed in June 2019 ($6m). Split excludes Thermal and Renewable HoldCo expenses and gain on CSP and Solar Italy and Slovakia farm downs

53%

11%

36%

Europe Africa Latin America

54%31%

13%

2%

EUR USD BRL Other

Renewable45%

HE Cogen17%

Thermal38%

12

10%

16%

5%

17%

4%

40%

8%

Coal Natural Gas

Fuel Oil High Efficiency Cogen

Wind Solar

Hydro

Diversification Across Geographies and TechnologiesCFADS

LTM H1 2019 PF CFADS by Technology1

LTM H1 2019 PF CFADS by Currency1

LTM H1 2019 PF CFADS by Geography1

(1) PF for full year EBITDA of Mexican CHP acquisition completed in November 2019 ($45m)

Renewable52%

HE Cogen17%

Thermal31%

13

63%7%

30%

Europe Africa Latin America

66%

26%

8%

EUR USD BRL

49%

28%

37%

16%

74%

51%

CG PeersAverage

CG Thermal PeersAverage

CGRenewable

PeersAverage

Sector Leading Operational and Financial Delivery

31.0%

27.7%

28.8%

2016 2017 2018 2019E

27 – 28%

✓Continued focus on strong margins and efficient cost structures through streamlined operations – EBITDA margins on average approx. 20% higher than peers

✓~350bps decrease in Fixed Cost / Variable Margin vs. 2016 levels on a run-rate basis

✓100bps increase in 2018 partially partially caused by increased overhead as a result of public listing

14

Resilient Cost Structure and EBITDA Margins1

(1) Thermal and Renewable margins include corporate SG&A fully allocated proportionately to each division

Fixed Costs to Variable Margin (%)

~ 350 bps.

+21%

+20%

+22%

7.1%7.7%

5.1%4.5%

3.7% 3.4%(2023)

3.0%(2025)

4.1% (2025)

$400m $100m Tap €500m €50m €100m €750m €100m Tap

Yiel

d t

o M

atu

rity

ContourGlobal HoldCo Bond Issuances

May 2014 Nov 2015 Jun 2016 July 2018Feb 2017Jul 2016 July 2019

BB- / BB-BB- BB / BB- BB / BBBB / BB BB / BBBB / BB-

Our business model is well attuned to the debt capital markets and debt investors value the credit

15

✓ €100m tap on the 4.125% senior secured notes due 2025 Notes priced on 30 July 2019 at 106.0% of par corresponding to a yield to maturity of 3.024%, the lowest recorded for the Company

SSN Rating:(S&P / Fitch)

Spread (bps) 599.2547.5 514.5311.9-360.7

366.3 339.5463

1,196 1,132

1,587 1,712

2,399 2,222

2,029

345 341 456 476

614 580 567

3.5x 3.3x

3.5x 3.6x 3.9x 3.8x

3.6x

(0.5x)

0.5x

1.5x

2.5x

3.5x

4.5x

5.5x

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Dec-18 Jun-19

NGPTI Prop. Adj. EBITDA (LTM)

Leverage Ratio Incurrence Level (5x max)

Leverage Ratio1 DSCR1

In $m or multiple In $m or multiple

Continued Strong Bond Credit Metrics7.4x DSCR & 3.6x Non-Guarantor Combined Leverage Ratio as of June 2019

16

(1) DSCR and Leverage Ratio (Non-guarantor combined leverage ratio) as defined in Bond Indenture. Please see slide 31 for calculation of Bond Indenture Leverage Ratio, including Proportionate Adjusted EBITDA and NGPTI (Non-Guarantor Proportionate Total Indebtedness) .

5x

202

301

237 232

291

203

251

32 33 41 41 43 34 34

6.3x

9.2x

5.7x 5.6x

6.8x

6.1x

7.4x

(0.5x)

0.5x

1.5x

2.5x

3.5x

4.5x

5.5x

6.5x

7.5x

8.5x

9.5x

-

50

100

150

200

250

300

350

400

450

500

Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Dec-18 Jun-19

CFADS (LTM) Annualized Debt Service

DSCR Incurrence Level (2x min)

2x

513

610 695

447 532

650

2017A 2018A 9M19LTM

Q3 YTD2018

Q3 YTD2019

High Growth and Robust Financial PerformanceHighly cash generative business with natural deleveraging

(1) Adjusted EBITDA is a non-IFRS measure as defined in IPO Prospectus(2) Pro forma numbers: Adjusted to reflect full year contribution of Spanish CSP(3) Growth based on 2017 to 9M19 LTM (CAGR)(4) EBITDA includes net gains from farm down transactions of $46m(5) Includes full year earnings of Spanish CSP, which was acquired in May 2018 (+$40m of Adjusted EBITDA based on FY Earnings)

Adjusted EBITDA1

($m)

+19%3

Net debt / EBITDA(x)

2

CFADS($m)

+19%

4 4

17

232

203

251

2017A 2018A LTM H1 2019

4.1x

4.4x

4.0x

2017A 2018A LTM H1 20195

USDm 2017 2018 LTM H1 2019Cash 781 697 744 Debt 2,890 3,560 3,601 Net debt 2,109 2,863 2,857

Target leverage ratio of 4.5x

Mexican Cogeneration Business Acquisition Signed in Jan 2019; closed November 2019

• Acquisition of natural-gas fired combined heat & power assets with518MW of operational capacity at completion, potential for afurther 414MW in development

• More than 98% contracted revenues including heat and steam withseller

• Integration of Mexico CHP¹ is progressing as planned with all keyintegration workstreams on track

• Made both internal and external appointments to supportthe new acquisition

• CG operational and H&S standards were developed inadvance of closing and are in the process of beingimplemented

• The plants have successfully transitioned to all of ouroperational and IT systems

• Acquired for $724m in cash with an additional VAT payment atclosing estimated at $77 million expected to be refunded in fullwithin 12 months of closing. $535m project financing underwrittenby Scotiabank and being syndicated to international banks

• Estimated Adj. EBITDA of $110m in first full year of operations

Transaction Highlights and Update Geographic Footprint

Altamira, TamaulipasCGA

Cosoleacaque, VeracruzCELCSA

(1) CHP – Combined Heat and Power 18

2019 key updates

Austria Wind Repowering

• Phase 1 (21 MW): Repowering of Velm reached COD in Jan 2019. Repowering of 3 of 5 Scharndorf turbines reached COD in November 2019. Both received a FIT of 13 years

Vorotan Refurbishment

• Electro-mechanical refurbishment and modernization program started in 2017 to improve operational performance, safety, reliability and efficiency of Vorotan. Initial phase has been completed and the project is on track with completion expected in 2020, ahead of original schedule and on budget

• Total $71.5m investments: electrical part funded by a €51m loan with a Development Finance Institution and additional civil works at $13.5m are funded by company’s operating cash flow

• Civil works to be entitled to a reimbursement and a regulated unlevered return through an adjustment to the tariff

19

• In February 2020 we inaugurated an innovative battery replacement and hybrid expansion project, which has enabled us to integrate more wind energy into the system and further reduce costs to the island customers

• Phase 01: Successfully implemented 6 MW/MWh Battery upgrade project in Q1 2019. 7.7 GWh production increase

• Phase 02: COD achieved in November 2019 on time and on budget. Replaced rented engines and ensured security of supply and grid stability, while reducing end user tariffs through avoidance of usage of rental diesel engines.

• Phase 03: 6 MW PV plant, 11-16 MW wind farm expansion and additional battery capacity

• Starting from October 2019, ContourGlobal is again the sole power producer on the island

Bonaire Hybrid Concept, a 24

MW integrated Wind, Diesel and Battery Power Plant

Appendices

Sao Domingos II Hydro Power Plant (Brazil) 20

Contributors to Adj. EBITDA

(1) EBITDA is calculated by asset excluding corporate costs and thermal and renewable holdcos(2) Includes Solutions Europe and Africa and Solutions Brazil(3) Includes Solar Italy, Solar Slovakia, Solar Romania and Biogas Italy

Top Contributors to Adj. EBITDA1 2016 2017 2018 LTM H1 2019

Top contributors from Thermal fleet

Maritsa East III 117 125 120 122

Arrubal 62 61 63 63

KivuWatt 22 24 26 29

Cap des Biches 12 26 27 27

Togo 21 25 25 26

CG Solutions2 12 27 27 24

Caribbean 21 27 24 24

Colombia 21 22 21 19

Top contributors from Renewable fleet

Spanish CSP - - 89 135

Brazil Wind 79 82 59 57

Solar Europe, excl. CSP3 31 31 41 42

Brazil Hydro 9 28 41 39

Peru Wind 31 25 29 32

Austria Wind 23 25 20 24

Vorotan 22 23 23 24

Total 485 553 638 687

21

Top Contributors to CFADS(Before Corporate and Other Costs)1 2016 2017 2018 LTM H1 2019

Spanish CSP - - 35 75

Solar Europe excl. CSP2 22 55 38 61

Maritsa 118 30 65 34

Arrubal 19 28 18 29

Brazil Hydros (1) 55 14 23

CG Solutions3 28 41 15 15

Cap des Biches - 7 17 12

Peru Wind 23 5 15 12

Colombia 4 8 4 12

KivuWatt - - 4 8

Vorotan 111 13 9 5

Austria Wind 7 8 4 5

Others5 18 20 11 7

Total 349 270 249 298

Contributors to CFADS1

(1) CFADS (Cash Flows Available for (Corporate) Debt Service) as defined in Bond Indenture(2) Includes Solar Italy, Solar Slovakia, Solar Romania and Biogas Italy(3) Includes Solutions Europe and Africa and Solutions Brazil(4) $84m second instalment of acquisition payment not deducted from CFADS(5) Other include Togo, Caribbean and Brazil Wind

4

22

Segment Facility / Project Name LocationGross Cap.

(MW)Number of

Assets Fuel Type1ContourGlobal

Ownership COD Power Purchaser PPA Expiration

Maritsa Bulgaria 908 1 Coal 73% 1978 NEK 2024

Arrubal Spain 800 1 Natural Gas 100% 2005 Gas Natural Fenosa 2021

TermoemCali Colombia 240 1 Natural Gas / Diesel 37% 1999 Various N/A

Sochagota Colombia 165 1 Coal 49% 1999 Gensa 20192

Togo Togo 100 1 Natural Gas / HFO / Diesel 80% 2010 CEET 2035

Cap des Biches Senegal 86 1 Oil /Natural Gas 100% Q2 2016 / Q4 2016

Senelec 2036

Energies Antilles / Energies St Martin

French Caribbean 35 2 HFO / LFO 100% 2000; 2003 EDF 2020; 2023

Bonaire Dutch Antilles 38 1 HFO / Wind 100% 2010 WEB 2025

KivuWatt Rwanda 26 1 Natural Gas 100% Q4 2015 EWSA (ex-Electrogaz & REC) 2040 (expected)

Total Thermal 2,398 10

Mexican CHP assets Mexico 518 2 Natural Gas cogeneration 100% 2014/19 Mexican industrial/commercial N/A

ContourGlobal Solutions Europe – Nigeria –Brazil

126 10 Natural Gas / Diesel / LFO 100%;100%; 80% 1995-2015 Investment grade global industrial companies

2018-2032

Total Cogen 644 12

Chapada Complex Brazil 438 3 Wind 51%, 51%, 100% 2015; Q1 2016 CCEE; distribution companies 2035

Vorotan Armenia 404 1 Hydro 100% 1970 AEN 2040

CSP Portfolio Spain 250 5 CSP 100% 2010 CNMC 2034-2037

Hydro Brazil Brazil 167 9 Hydro 79%3 1963; 1992; 2009-2012

Distribution companies 2027-2042

Asa Branca Brazil 160 1 Wind 100% 2013 Distribution companies 2033

Austria Wind Austria 149 10 Wind 94% 2003-2014 OeMAG 2016-2027

Inka Peru 114 2 Wind 100% 2014 Distribution companies 2034

Solar Europe Italy, Slovakia, Romania

121 54 Solar 51% / 100% 2007-2013 Distribution companies 2027-2033

Total Renewable 1,803 85

Total portfolio 4,845 107

ContourGlobal Portfolio

Thermal Renewables(1) HFO refers to heavy fuel oil, and LFO to light fuel oil. (2) CES has already signed 4 contracts to replace existing PPA, extending expiration to 2024, with an additional 5 year extension expected(3) Capacity weighted

23

24

Robust continuous improvement process Our value to “embrace excellence” means that we commit to continuously improve in all aspects of business performance

Operating as a high-growth company in a complex and diverse environment, we understand that failures are inevitable. Embracing failure, openly discussing it at all levels of management, and taking action to prevent the failure in the future is the way to operate safely and efficiently

Tools

▪ Internal and third party Health, Safety and Environmental audits▪ The Power for HSE Excellence Manual▪ Benchmarking▪ Five why’s, Lessons learned, Case study, other root-cause methodologies

Continuous Improvement

Committee

Timely and Transparent

▪ Responsible for reviewing operational aspects of our global Continuous Improvement program and developing strategy to further the culture of learning from failure across our organization

▪ The 2 Ts, timely transparency, is a specific initiative to encourage that successes and failures are communicated in a timely, open and honest way

▪ This creates and environment of trust without blame, allowing us to honor our commitments and improve performance

322 24

35

2015 2016 2017 2018

# of 5 why’s solely HSE related

Correction and Prevention

▪ Corrective and Preventive Action Tracker to ensure all inspection actions are timely closed

▪ Company stand downs, Company bulletins, injuries alerts▪ Hazard identification, hazard awareness and safety inspections (incl by

Senior Management)▪ Job safety analysis for each task▪ Utilization of predictive maintenance (“PdM”) and condition-based

maintenance (“CBM”), as well as centralized pool of experts to reduce unplanned failures

Leading indicator strategy

▪ Combination a series of interlinked KPIs to identify and remove hazards from the work environment in a timely manner, reducing workers’ exposure to hazardous conditions.

▪ Assignation of target values to our leading indicators.

0.0033

0.0023

0.0024

0.0026

2015

2016

2017

2018

SAFETY INSPECTIONS PER WORKING HOURS

96%

94%

91%

83%

2018

2017

2016

2015CORRECTIVE AND PREVENTIVE ACTIONS CLOSURE RATE

23%

44%

64%

74%

2015

2016

2017

2018

HAZARD IDENTIFICATION RATE

2.77%2.89%

2.16%1.10%

2018201720162015

% OF WORKING HOURS DEDICATED TO H&S TRAINING

25

Strong environmental performance We are actively managing and minimizing environmental impacts

ContourGlobal 2018 Environmental Performance

CO₂ emissions includes emissions from combustion of fuel, purchase of electricity, heat, steam and cooling, including a power plant’s own use

8.17 7.51

8.14

6.48

2015 2016 2017 2018

CO2 Emissions (tonnes)

0.630.61

0.58

0.56

2015 2016 2017 2018

Net CO2 tonnes/MWH

One of the most significant environmental impacts of our Thermal portfolio is our CO₂ emissions.

We set a target in 2014 to maintain or reduce our intensity of carbon emissions, i.e. the carbon emissions in tonnes/MWh.

We have achieved this through growth in our Renewable portfolio and promoting efficiency in power plant operations

We have the ongoing dedication to minimizing our environmental impact as much as possible at all our sites.

Our social and environmental governance is centered around our Policy on Social Responsibility and Environmental Sustainability, a policy aligned with the International Finance Corporation Performance Standards. The policy, and accompanying frameworks set out how we are working to achieve social and operational excellence and include:

• Compliance with regulations and legislation and alignment to global best practice

• Maintaining or decreasing our carbon, air and waste footprint

• Training and development for our human talent

• Launching targeted social investments aligned to our core business objectives

In 2018,our carbon intensity was at its lowest level since our baseline year 2011

88%

2.7t hazardous waste recycled+60% y-o-y

246 SO2 emissions-45% y-o-y

198k seedings planted+34% y-o-y

246 SO2 emissions-45% y-o-y

No Environmental grievances and 1 Environmental sanction in 2018