Journal of Internet Banking and Commerce · 2017-03-27 · Journal of Internet Banking and...

12

Journal of Internet Banking and Commerce An open access Internet journal (http://www.icommercecentral.com) Journal of Internet Banking and Commerce, Jan 2017, vol. 22, no. S7 Special Issue: Global Strategies in Banking and Finance Edited By: Mihail N. Dudin USERS’ LOYALTY TOWARDS MOBILE BANKING IN MALAYSIA YUN MIN LOW Faculty of Management, Universiti Teknologi Malaysia, 81310 Johor Bahru, Malaysia, Tel: 60167420987; Email: [email protected] CHIN FEI GOH Faculty of Management, Universiti Teknologi Malaysia, 81310 Johor Bahru, Malaysia OWEE KOWANG TAN Faculty of Management, Universiti Teknologi Malaysia, 81310 Johor Bahru, Malaysia AMRAN RASLI Faculty of Management, Universiti Teknologi Malaysia, 81310 Johor Bahru, Malaysia Abstract Electronic banking emerges as perhaps the most prominent development trend in the Malaysian internet economy. Thus, it is vital to explore customer loyalty in using electronic banking industry. The study is aimed to investigate the determinants of

Transcript of Journal of Internet Banking and Commerce · 2017-03-27 · Journal of Internet Banking and...

Journal of Internet Banking and Commerce

An open access Internet journal (http://www.icommercecentral.com)

Journal of Internet Banking and Commerce, Jan 2017, vol. 22, no. S7

Special Issue: Global Strategies in Banking and Finance Edited By: Mihail N. Dudin

USERS’ LOYALTY TOWARDS MOBILE BANKING IN MALAYSIA

YUN MIN LOW

Faculty of Management, Universiti Teknologi Malaysia, 81310 Johor

Bahru, Malaysia, Tel: 60167420987;

Email: [email protected]

CHIN FEI GOH

Faculty of Management, Universiti Teknologi Malaysia, 81310 Johor

Bahru, Malaysia

OWEE KOWANG TAN

Faculty of Management, Universiti Teknologi Malaysia, 81310 Johor

Bahru, Malaysia

AMRAN RASLI

Faculty of Management, Universiti Teknologi Malaysia, 81310 Johor

Bahru, Malaysia

Abstract

Electronic banking emerges as perhaps the most prominent development trend in the Malaysian internet economy. Thus, it is vital to explore customer loyalty in using electronic banking industry. The study is aimed to investigate the determinants of

JIBC Jan 2017, Vol. 22, No.S7 - 2 -

customer loyalty of mobile banking. A survey questionnaire approach is adopted in this study. Our findings show that subjective norms, perceived convenience and perceived usefulness positively and significantly influencing loyalty. The findings offer important implications to policy makers to understand customer loyalty on mobile banking in Malaysia. Keywords: Mobile banking, Loyalty, Consumer behaviour, Malaysia © Yun Min Low, 2017

INTRODUCTION

With the proliferation of informational technologies and the internet, online banking has become an important element in the Malaysian economy. Currently, it is reported that there are 31 banks are offering online banking services to their customers although online banking was introduced less than a decade in Malaysia. Central Bank of Malaysia reported that there were 19.8 million internet banking subscribers and 7,279,000 mobile banking subscribers in December 2015. These figures show that percentage of penetration of mobile banking to reach 63.7% of the total population. While the number of mobile banking subscribers has grown rapidly in Malaysia, but the understanding of customer loyalty on mobile banking remain inadequate. The empirical evidence of customer loyalty on mobile banking is relatively scarce compared to the behavioral intention literature. This knowledge gap is important because subscribers to mobile banking may not be active users. Such problem remains a significant challenge to establish pure online banks in Malaysia. Some pure online banks try to complement their online services by establishing branch services. However, they cannot sustain main business operation, i.e. online banking, if lacking customer loyalty on online banking [1]. Furthermore, mobile banking service is a source of competitive advantage in the banking industry [2]. Therefore, this study seeks to investigate the determinants of customer loyalty of online banking in the Malaysian context. This study adapts technology acceptance model (TAM) to investigate customer loyalty of online banking [3-5]. This study is expected to generate new insights on the factors that influence mobile banking loyalty.

LITERATURE REVIEW Mobile Banking In general, mobile banking refers to the use of mobile banking application to perform online financial transactions. Other mobile banking services include online fund transfer, account management, bill payment, PIN changes and balance inquiry [5]. The mobile banking user may use those services when the mobile devices are connected to a server through internet. Mobile devices and communications networks are two preconditions for mobile banking services. That is, users need to install mobile banking

JIBC Jan 2017, Vol. 22, No.S7 - 3 -

application on their mobile devices, such as mobile phones or tablets [6]. TAM Perceived usefulness and perceived ease of use are the key components of technology acceptance model (TAM) [3]. Technology acceptance refers to an observable willingness to use the information technology in accomplishing a task. However, numerous people are not willing to make real use of technology in daily lives. Therefore, there is a phenomenon in investigating the factors of influencing individual’s technology adopttion [6]. In addition, Theory of Reasoned Action (TRA) from Ajzen et al. [7] is the origins of TAM. In TRA, a person's beliefs and attitudes are assumed to influence on the individual’s intention to perform a specific task [8]. Whereas in TAM, user acceptance of technology is assumed to determine by perceived usefulness and perceived ease of use. The model is shown in Figure 1. Figure 1: TAM (Davis, 1989).

Loyalty Loyalty is a customer’s intention to repurchase a product or service from the same seller, brand or service provider [9]. Hence, the user’s loyalty of mobile banking may refer to continuous or repeating use of mobile banking service. In other words, customer’s loyalty can be interpreted as the higher value provided by the specify seller, brand or service provider compared to others [10]. Therefore, customer’s loyalty is considered as a key success factor for a seller or brand over a time [11,12]. Loyalty can be measured by psychological component and behavioral component, where psychological component depends on customer’s feeling to rely on a person, products or services of an organization [10], whereas the latter one is based on customer’s frequency of visiting a certain shop or customer’s expenses on the brand or product [13]. Besides, loyalty may also be known as e-loyalty. E-loyalty is defined as the customer’s intention to revisit a website or to repurchase from same online vendor [11].

JIBC Jan 2017, Vol. 22, No.S7 - 4 -

Research Model and Hypotheses The research model of this study includes 4 variables, which are subjective norms, perceived ease of use, convenience and loyalty. As shown in Figure 2, the subjective norms are acting as an independent variable which influencing the convenience and perceived ease of use. Convenience and perceived ease of use are mediating between the relationship of subjective norms and user’s loyalty. Figure 2: Research Model.

Subjective Norms and Convenience Subjective norms happened when someone’s thought; action or feeling is influenced by other people such as family and friends. It is also refer to social influence or social norm [14]. Subjective norms are defined as the “perceived pressures on a person to perform a given behaviour and the person’s motivation to comply with those pressures” [15]. In this study, the external variable is subjective norm. Therefore, the relationship between subjective norms and convenience is the first hypothesis. Empirical evidences that social influence positively on convenience [16-18]. In Gu et al. [19] study, subjective norms are found have insignificance relationship with convenience. H1: Subjective norms have a positive impact on user’s perceived convenience of mobile banking. Subjective Norms and Perceived Ease of Use From the research model shown in Figure 2, subjective norms are also influencing perceived ease of use (PEOU). In TAM, PEOU is assumed to influence by external variable. As stated in previous section, the external variable is subjective norms. From previous studies, subjective norms are investigated to have a significant and positive relationship with PEOU [17]. From the finding of Montazemi et al. [20], subjective norms proved to significant and positively influencing user’s PEOU in their pre-adoption stage of using online banking. Hypothesis 2 is developed below.

JIBC Jan 2017, Vol. 22, No.S7 - 5 -

H2: Subjective norms have a positive impact on user’s perceived ease of use on mobile banking. Convenience and Loyalty In Oxford dictionary, convenience is defined as “the state of being able to proceed with something without difficulty or the quality of being useful, easy, or suitable for someone.” Convenience can also be known as perceived usefulness in TAM theory. According to Davis et al. [3] perceived usefulness refer to the user’s belief in using a technology or system to increase his or her performance. Moreover, perceived usefulness can also be referred as time saving, effectiveness at work and the significance of the system for individuals work [21]. As basic technology and service have already been tested and standardized, convenience has become an important factor for user’s acceptance of certain technology when similar products and services exist [22]. To enhance customer loyalty, high level of convenience of online shopping has become more significant for driving force a brand [23]. Numerous researches found the convenience and loyalty has a positive and significant relationship [14,24-27]. Therefore, the hypothesis of convenience and loyalty is developed. H3: Convenience has a positive impact on user’s loyalty in mobile banking. Perceived Ease of Use and Loyalty Perceived ease of use is one of the important variables in TAM. The definition of perceived ease of use (PEOU) by Davis et al. [3] is “the degree to which a person believes that using a particular system would be free of effort”. In other words, PEOU refer to the easiness for user to understand and use the system. PEOU is affecting the customer’s intention to use mobile banking due to the requirement to have a certain level of knowledge and skill for the users [28]. Besides, it is related to the effort of involve in utilizing a technology [29]. In previous research, perceived ease of use was found positively influence user’s intention to adopt smartphone apps .In other words, user’s loyalty will be higher as they perceived the technology is easy to use [30]. From previous researches, PEOU has positive and significant relationship with the user’s loyalty [24,31-34]. Therefore, the last hypothesis is shown below. H4: Perceived ease of use has a positive impact on user’s loyalty in mobile banking.

METHODOLOGY Survey Instrument In this study, a questionnaire was developed to collect empirical data. The questionnaire consisted 3 parts. In the first part of the questionnaire, questions regarding demographic characteristic were asked such as gender, age, education level and income. For the second part, respondents were asked to indicate their level of agreement to the statement which related to the research constructs. On the other hand, the third part of the questionnaire is questions about the period of respondents using mobile banking

JIBC Jan 2017, Vol. 22, No.S7 - 6 -

and the frequency they use mobile banking in a month. In second part questionnaire, all statements are measuring by seven-point Likert scale ranging from ‘strongly disagree’ to ‘strongly agree’. Sampling The study use convenience sampling strategy to select the sample. Paper questionnaire was distributed in a total of 300 copies. In a month period, 183 copies were returned back. The response rate was achieved at 56%. The questionnaire also distributed in another form which is an online questionnaire. The online questionnaire was randomly sent to 150 mobile banking users and 78 questionnaires were answered. The response rate is successfully achieving 52%. The total responses are 261. Data Analysis Technique After the survey was completed, all the raw data were edited, recorded and coded in Microsoft excel and data input into SmartPLS for processing. Before process the data with SmartPLS, the data was checked for outliers and missing values. There are 251 cases as valid sample and retained for measurement analysis. Partial least squares (PLS) path modeling technique was used using the SmartPLS 2.0 M3 software. PLS was chosen to use in this study because it is not requiring the distributional assumption of normality, needed less demand on measurement scales and not limit with small as well as large samples [35].

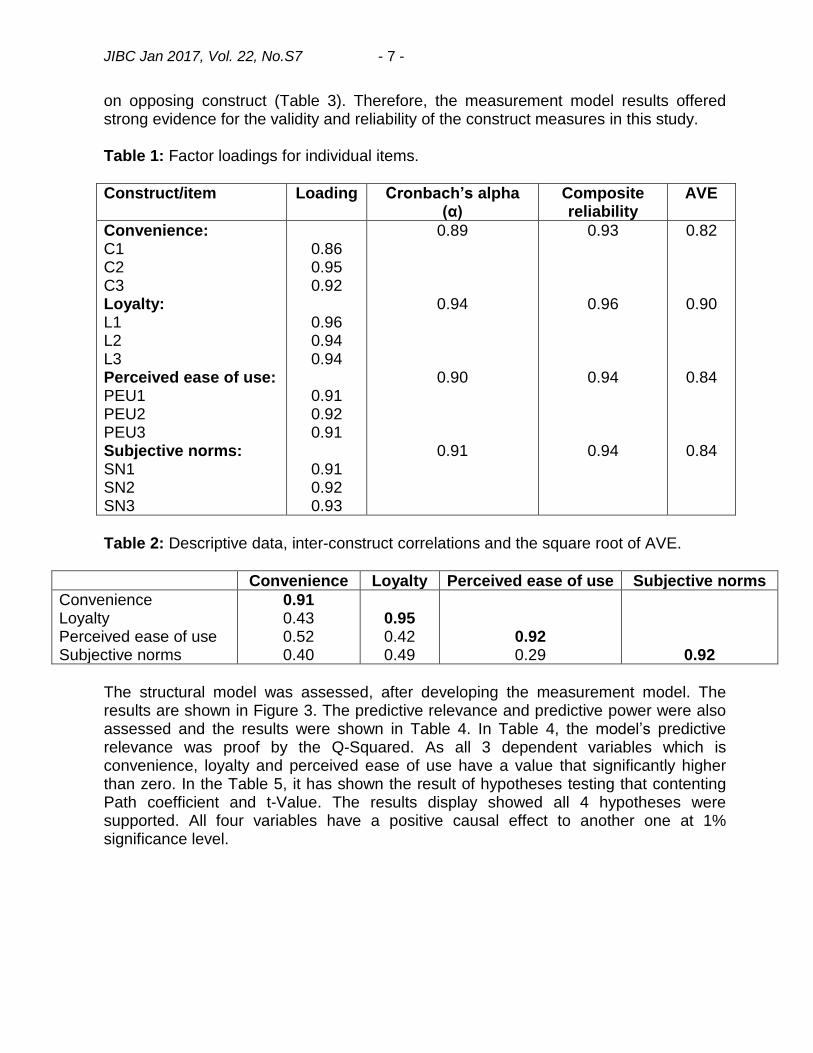

RESULTS Respondents’ Profile In the survey, majority of the respondents are female (69%). Most of the respondents are between 18 to 25 years-old. Their educational level, mostly at the college and university level. As most of them are university students, therefore 59% of them have no monthly income, whereas for those who have a job mostly has RM2, 001 to RM3, 000 monthly incomes. Besides, the majority of the respondents have over 2 years’ experiences for using mobile banking. Lastly, there are 80% of them using mobile banking between 1 to 5 times in a month. Evaluation of the Measurement Model To assess the adequacy of the measurement model, PLS factorial validity tests were conducted and shown in Table 1. Convergent and discriminant validity were considered for validating the measures and PLS factorial validity test provided evidence for the convergent validity. The outer loadings were all exceeded 0.7 and significant. The Chronbach’s alpha value and composite reliability value were both greater than 0.7. Besides, the AVE were also all greater than 0.50. In Table 2, the discriminant validity of the measurement model was built. Each of the variable’s square roots of AVE was greater than the correlation between the variable and other variable. Moreover, the indicators’ cross loading was also accessed and found there is no indicator loads higher

JIBC Jan 2017, Vol. 22, No.S7 - 7 -

on opposing construct (Table 3). Therefore, the measurement model results offered strong evidence for the validity and reliability of the construct measures in this study. Table 1: Factor loadings for individual items.

Construct/item Loading Cronbach’s alpha (α)

Composite reliability

AVE

Convenience: C1 C2 C3 Loyalty: L1 L2 L3 Perceived ease of use: PEU1 PEU2 PEU3 Subjective norms: SN1 SN2 SN3

0.86 0.95 0.92

0.96 0.94 0.94

0.91 0.92 0.91

0.91 0.92 0.93

0.89

0.94

0.90

0.91

0.93

0.96

0.94

0.94

0.82

0.90

0.84

0.84

Table 2: Descriptive data, inter-construct correlations and the square root of AVE.

Convenience Loyalty Perceived ease of use Subjective norms

Convenience Loyalty Perceived ease of use Subjective norms

0.91 0.43 0.52 0.40

0.95 0.42 0.49

0.92 0.29

0.92

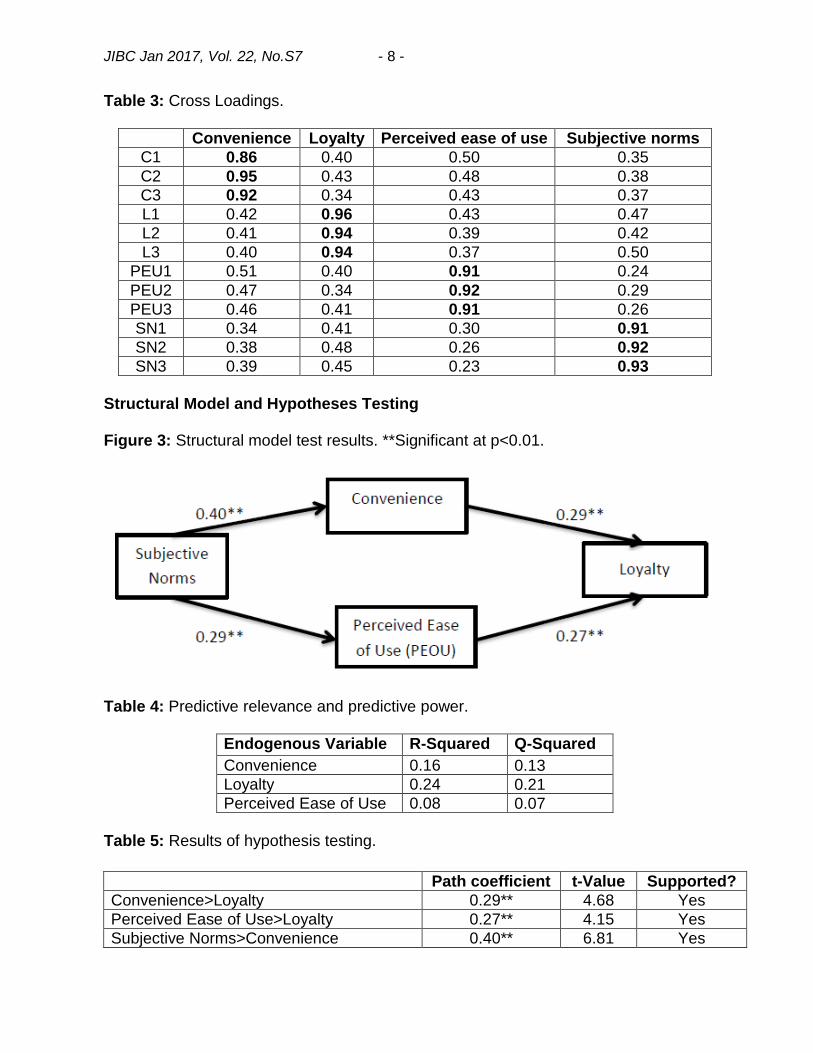

The structural model was assessed, after developing the measurement model. The results are shown in Figure 3. The predictive relevance and predictive power were also assessed and the results were shown in Table 4. In Table 4, the model’s predictive relevance was proof by the Q-Squared. As all 3 dependent variables which is convenience, loyalty and perceived ease of use have a value that significantly higher than zero. In the Table 5, it has shown the result of hypotheses testing that contenting Path coefficient and t-Value. The results display showed all 4 hypotheses were supported. All four variables have a positive causal effect to another one at 1% significance level.

JIBC Jan 2017, Vol. 22, No.S7 - 8 -

Table 3: Cross Loadings.

Convenience Loyalty Perceived ease of use Subjective norms

C1 0.86 0.40 0.50 0.35

C2 0.95 0.43 0.48 0.38

C3 0.92 0.34 0.43 0.37

L1 0.42 0.96 0.43 0.47

L2 0.41 0.94 0.39 0.42

L3 0.40 0.94 0.37 0.50

PEU1 0.51 0.40 0.91 0.24

PEU2 0.47 0.34 0.92 0.29

PEU3 0.46 0.41 0.91 0.26

SN1 0.34 0.41 0.30 0.91

SN2 0.38 0.48 0.26 0.92

SN3 0.39 0.45 0.23 0.93

Structural Model and Hypotheses Testing Figure 3: Structural model test results. **Significant at p<0.01.

Table 4: Predictive relevance and predictive power.

Endogenous Variable R-Squared Q-Squared

Convenience 0.16 0.13

Loyalty 0.24 0.21

Perceived Ease of Use 0.08 0.07

Table 5: Results of hypothesis testing.

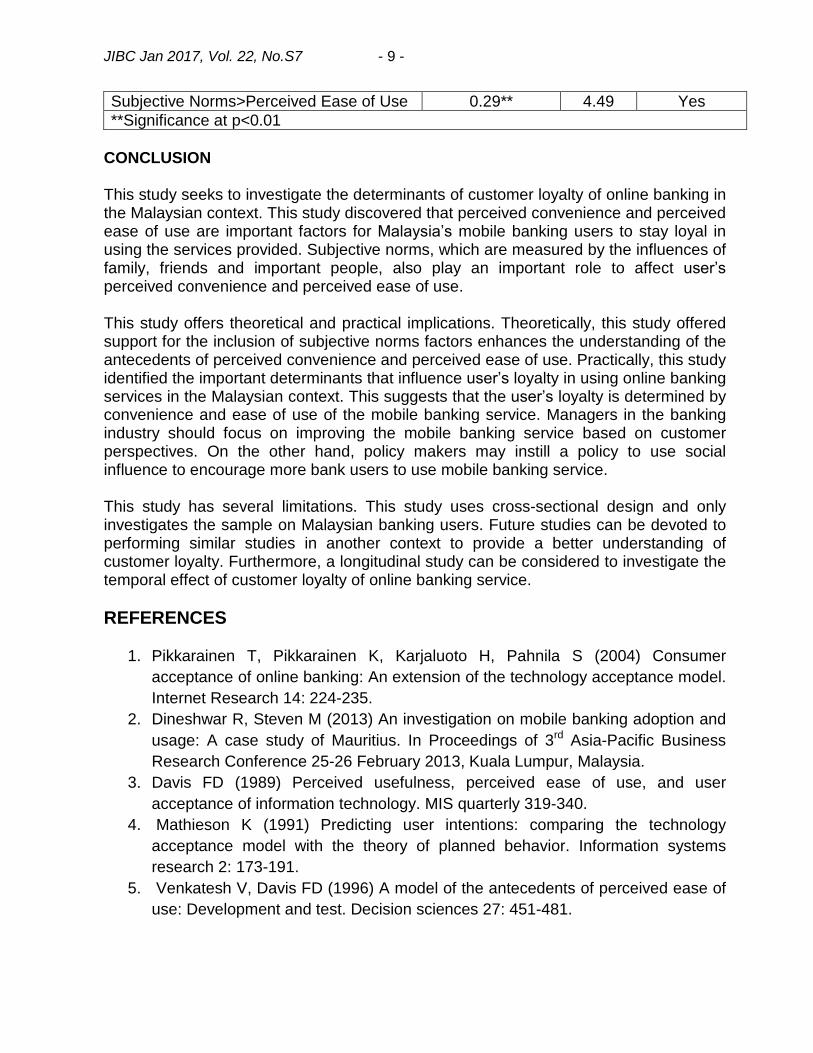

Path coefficient t-Value Supported?

Convenience>Loyalty 0.29** 4.68 Yes

Perceived Ease of Use>Loyalty 0.27** 4.15 Yes

Subjective Norms>Convenience 0.40** 6.81 Yes

JIBC Jan 2017, Vol. 22, No.S7 - 9 -

Subjective Norms>Perceived Ease of Use 0.29** 4.49 Yes

**Significance at p<0.01

CONCLUSION This study seeks to investigate the determinants of customer loyalty of online banking in the Malaysian context. This study discovered that perceived convenience and perceived ease of use are important factors for Malaysia’s mobile banking users to stay loyal in using the services provided. Subjective norms, which are measured by the influences of family, friends and important people, also play an important role to affect user’s perceived convenience and perceived ease of use. This study offers theoretical and practical implications. Theoretically, this study offered support for the inclusion of subjective norms factors enhances the understanding of the antecedents of perceived convenience and perceived ease of use. Practically, this study identified the important determinants that influence user’s loyalty in using online banking services in the Malaysian context. This suggests that the user’s loyalty is determined by convenience and ease of use of the mobile banking service. Managers in the banking industry should focus on improving the mobile banking service based on customer perspectives. On the other hand, policy makers may instill a policy to use social influence to encourage more bank users to use mobile banking service. This study has several limitations. This study uses cross-sectional design and only investigates the sample on Malaysian banking users. Future studies can be devoted to performing similar studies in another context to provide a better understanding of customer loyalty. Furthermore, a longitudinal study can be considered to investigate the temporal effect of customer loyalty of online banking service.

REFERENCES

1. Pikkarainen T, Pikkarainen K, Karjaluoto H, Pahnila S (2004) Consumer

acceptance of online banking: An extension of the technology acceptance model.

Internet Research 14: 224-235.

2. Dineshwar R, Steven M (2013) An investigation on mobile banking adoption and

usage: A case study of Mauritius. In Proceedings of 3rd Asia-Pacific Business

Research Conference 25-26 February 2013, Kuala Lumpur, Malaysia.

3. Davis FD (1989) Perceived usefulness, perceived ease of use, and user

acceptance of information technology. MIS quarterly 319-340.

4. Mathieson K (1991) Predicting user intentions: comparing the technology

acceptance model with the theory of planned behavior. Information systems

research 2: 173-191.

5. Venkatesh V, Davis FD (1996) A model of the antecedents of perceived ease of

use: Development and test. Decision sciences 27: 451-481.

JIBC Jan 2017, Vol. 22, No.S7 - 10 -

6. Yucel UA, Gulbahar Y (2013) Technology acceptance model: A review of the

prior predictors. Egitim Bilimleri Fakultesi Dergisi 46: 89.

7. Ajzen I (1987) Attitudes, traits, and actions: Dispositional prediction of behavior in

personality and social psychology. Advances in experimental social psychology

20: 1-63.

8. Van Schaik P, Teo T (2013) Understanding technology acceptance in pre-service

teachers: A structural-equation modeling approach.

9. Sirdeshmukh D, Singh J, Sabol B (2002) Consumer trust, value, and loyalty in

relational exchanges. Journal of marketing 66: 15-37.

10. Hallowell R (1996) The relationships of customer satisfaction, customer loyalty,

and profitability: An empirical study. International journal of service industry

management 7: 27-42.

11. Flavián C, Guinalíu M, Gurrea R (2006) The role played by perceived usability,

satisfaction and consumer trust on website loyalty. Information andManagement

43: 1-14.

12. Keating B, Rugimbana R, Quazi A, Differentiating between service quality and

relationship quality in cyberspace. Managing Service Quality: An International

Journal, 2003. 13(3): 217-232.

13. Thakur R (2016) Understanding Customer Engagement and Loyalty: A Case of

Mobile Devices for Shopping. Journal of Retailing and Consumer Services 32:

151-163.

14. Yoon HS, Barker Steege LM (2013) Development of a quantitative model of the

impact of customers’ personality and perceptions on Internet banking use.

Computers in Human Behavior 29: 1133-1141.

15. Douglass RB, Fishbein M, Ajzen I (1977) Belief, Attitude, Intention, and

Behavior: An Introduction to Theory and Research.

16. Kesharwani A, Bisht SS (20120 The impact of trust and perceived risk on internet

banking adoption in India: An extension of technology acceptance model.

International Journal of Bank Marketing 30: 303-322.

17. Rodrigues LF, Oliveira A, Costa CJ (2016) Does ease-of-use contributes to the

perception of enjoyment? A case of gamification in e-banking. Computers in

Human Behavior 61: 114-126.

18. Al-Somali SA, Gholami R, Clegg B (2009) An investigation into the acceptance of

online banking in Saudi Arabia. Technovation 29: 130-141.

19. Gu JC, Lee SC, Suh YH (2009) Determinants of behavioral intention to mobile

banking. Expert Systems with Applications 36: 11605-11616.

20. Montazemi AR, Qahri-Saremi H (2015) Factors affecting adoption of online

banking: A meta-analytic structural equation modeling study. Information and

Management 52: 210-226.

21. Aldás‐Manzano J, Lassala‐Navarré C, Ruiz‐Mafé C, Sanz‐Blas S (2009) Key

drivers of internet banking services use. Online Information Review 33: 672-695.

JIBC Jan 2017, Vol. 22, No.S7 - 11 -

22. Yang HD, Lee J, Park CI, Lee K (2014) The Adoption of Mobile Self-Service

Technologies: Effects of Availability in Alternative Media and Trust on the

Relative Importance of Perceived Usefulness and Ease of Use. International

Journal of Smart Home 8: 165-178.

23. Jiang L, Yang Z, Jun M (2013) Measuring consumer perceptions of online

shopping convenience. Journal of Service Management 24: 191-214.

24. Ozturk AB (2016) What keeps the mobile hotel booking users loyal?

Investigating the roles of self-efficacy, compatibility, perceived ease of use, and

perceived convenience. International Journal of Information Management 36:

1350-1359.

25. Yiu CS, Grant K, Edgar D (2007) Factors affecting the adoption of Internet

Banking in Hong Kong—implications for the banking sector. International Journal

of Information Management 27: 336-351.

26. Koenig‐Lewis N, Palmer A, Moll A (2010) Predicting young consumers' take up of

mobile banking services. International Journal of Bank Marketing 28: 410-432.

27. Fung Chiu S (2012) International Conference on Asia Pacific Business

Innovation and Technology Management The Effects of Computer Self-Efficacy

and Technology Acceptance Model on Behavioural Intention in Internet Banking

Systems. Procedia - Social and Behavioral Sciences 57: 448-452.

28. Alalwan AA (2016) Consumer adoption of mobile banking in Jordan: Examining

the role of usefulness, ease of use, perceived risk and self-efficacy. Journal of

Enterprise Information Management 29: 118-139.

29. Venkatesh V (2000) Determinants of perceived ease of use: Integrating control,

intrinsic motivation, and emotion into the technology acceptance model.

Information systems research 11: 342-365.

30. Lee D (2015) Antecedents and consequences of mobile phone usability: Linking

simplicity and interactivity to satisfaction, trust, and brand loyalty. Information and

Management 52: 295-304.

31. Luarn P, Lin HH (2005) Toward an understanding of the behavioral intention to

use mobile banking. Computers in Human Behavior 21: 873-891.

32. Sinha I, Mukherjee S (2016) Acceptance of technology, related factors in use of

off branch e-banking: An Indian case study. The Journal of High Technology

Management Research 27: 8-100.

33. Guriting P, Ndubisi NO (2006) Borneo online banking: evaluating customer

perceptions and behavioural intention. Management Research News 29: 6-15.

34. Karasavvoglou AG (2014) The Economies of Balkan and Eastern Europe

Countries in the Changed World (EBEEC 2013) Investigating the Determinants of

Internet Banking Adoption in Greece. Procedia Economics and Finance 9: 501-

510.

JIBC Jan 2017, Vol. 22, No.S7 - 12 -

35. Ayeh JK (2015) Travellers’ acceptance of consumer-generated media: An

integrated model of technology acceptance and source credibility theories.

Computers in Human Behavior 48: 173-180.