Journal of Emerging Issues in Economics, Finance and...

20

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X) Volume:1 No.4 April 2013 321 www.globalbizresearch.com An Assessment of Exchange Rate Volatility and Inflation in Nigeria BOBAI, Francis Danjuma, Economics Department, Ahmadu Bello University Zaria, Nigeria. E-mail: [email protected] UBANGIDA, Shuaibu Economics- Department, Federal College of Education, Zaria- Nigeria. E-mail: [email protected] UMAR, Yunusa Sa’id Economics- Department, Federal College of Education, Zaria- Nigeria. E-mail: [email protected] ________________________________________________________________________ Abstract This study examines the impact of exchange rate volatility on inflation in Nigeria economy. Annual time series data from 1986 to 2010 were employed for this study. The methodology employed in this study includes; VECM model (Vector Error Correction Mechanism), impulse response function, variance decomposition and ARCH and GARCH where the major tools of analysis. A stationary test was carried out using the Augmented Dickey-Fuller (ADF) and Phillip Perron (PP) test the variables were found to be stationary at first difference order at 5% level of significance. The VECM result indicated a negative shock between exchange rate and inflation that is a one percent increase in inflation rate leads to about 42 percent decrease in exchange rate. The major findings from the ARCH and GARCH results show the presence of volatility and the volatility is persistent. Therefore, the government should direct it expenditure to the key productive sectors of the economy such as agriculture and manufacturing this will go a long way in increasing the production of goods and services thereby stabilizing the prices and consequently exchange rate. ______________________________________________________________________ Keywords: Keywords: Exchange rate, inflation, Cointegration, Vector error correction, Mechanism ARCH and GARCH

Transcript of Journal of Emerging Issues in Economics, Finance and...

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

321

www.globalbizresearch.com

An Assessment of Exchange Rate Volatility and Inflation in Nigeria

BOBAI, Francis Danjuma,

Economics Department,

Ahmadu Bello University Zaria, Nigeria.

E-mail: [email protected]

UBANGIDA, Shuaibu Economics- Department,

Federal College of Education, Zaria- Nigeria.

E-mail: [email protected]

UMAR, Yunusa Sa’id Economics- Department,

Federal College of Education, Zaria- Nigeria.

E-mail: [email protected]

________________________________________________________________________

Abstract

This study examines the impact of exchange rate volatility on inflation in Nigeria economy.

Annual time series data from 1986 to 2010 were employed for this study. The methodology

employed in this study includes; VECM model (Vector Error Correction Mechanism), impulse

response function, variance decomposition and ARCH and GARCH where the major tools of

analysis. A stationary test was carried out using the Augmented Dickey-Fuller (ADF) and Phillip

Perron (PP) test the variables were found to be stationary at first difference order at 5% level of

significance. The VECM result indicated a negative shock between exchange rate and inflation

that is a one percent increase in inflation rate leads to about 42 percent decrease in exchange rate.

The major findings from the ARCH and GARCH results show the presence of volatility and the

volatility is persistent. Therefore, the government should direct it expenditure to the key

productive sectors of the economy such as agriculture and manufacturing this will go a long way

in increasing the production of goods and services thereby stabilizing the prices and consequently

exchange rate.

______________________________________________________________________ Keywords: Keywords: Exchange rate, inflation, Cointegration, Vector error correction, Mechanism ARCH and GARCH

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

322

www.globalbizresearch.com

1. Introduction

Exchange rate is an important macroeconomic policy instrument. Changes in exchange rates

have powerful effects on tradable and non-tradable of countries concerned through effects of

relative prices of goods and services. The importance of exchange rates in influencing inflation

rates cannot be overemphasized and this makes policy makers worry about the behavior of both

nominal and real exchange rates and also have active interest in their determination. (Obadan,

2007), states that the choice of an exchange rate regime coupled with the right level of the

exchange rate tends to be perhaps the most critical decision in an open economy because of the

impact of the exchange rate on economic performance, resource allocation, the wealth of citizens,

standard of living, income distribution, the balance of payment and other economic aggregates.

In line with the above, the important factors in the choice of an exchange rate regime

include: a country’s stage of development, structure of production (export reliance on primary

commodity production and exports in relation to manufactured goods), state of development of

the financial markets, openness of the economy, dependence on the external sector for essential

imports and so on. The more open the economy, the greater the importance of the exchange rate

in the policy process and the more important this variable becomes as an optional policy conduit.

For instance, it is expected that when exchange rate depreciates, inflation rate increases and vice

versa. The choice of exchange rate policy also determines the ability of a developing country to

take full advantage of international trade system.

Devaluation of currency ought to discourage imports and ostentatious consumption and also

encourage export but the experience in Nigeria is opposite. In Nigeria, devaluation of Naira has

resulted into increase in capital flight instead of inflow of foreign investment. It is well known

that Nigeria’s main exports remain crude oil which accounts for over 90% of its total exports.

Increased imports have been the experience of Nigeria throughout the post SAP period. Over the

years, there is always an excess demand for foreign exchange placing permanent pressure on the

value of Naira and encouraging transaction to speculate against the Naira resulting in serious

increase in capital flight. Sunusi (2007) shows that a stable exchange rate is crucial for

maintaining price stability and attracting foreign investment in Nigeria. Nigeria is an import

dependent country, importing most of its domestic fuel needs, foods and other items due to

neglect of agricultural and manufacturing sectors of the economy. Surely, this must have an effect

on the prices of goods and services in the country because our balance of payment will continue

to be unfavorable.

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

323

www.globalbizresearch.com

Thus, the stability of exchange rate is important for price stabilization. In order to sustain

price stability, most central banks intervene in the foreign exchange market to smoothen short run

fluctuations of the exchange rate. However, the effects of the central bank intervention in the

foreign exchange market are not straightforward though the efficiency and depth of the foreign

exchange market coupled with the nature and credibility of the interventions matter most

(Adebayo, 2009).

Exchange rate being one of the main macroeconomic indicators, its changes affects exports

and imports through changes in their relative prices. (Dornbush, 1976), indicate that the exchange

rate is identified with the relative prices of goods and thus is a determinant of the allocation of

world expenditure between domestic and foreign goods. Appreciations of exchange rate cause

any trade balance deficit and it affects particularly agricultural products. Therefore the

importance of the study is to search the real exchange rate volatility and monetary policy on

exportation. The liquidity of foreign exchange market is vital for managing exchange rate in a

way that is consistent with inflation targeting framework to ensure exchange rate stability.

Presently, the Central Bank has as its target to achieve a single digit inflation through liquidity

tightening (raising the cash reserve requirement and liquidity ratio for banks) in order to reduce

lenders’ ability to create more money. In terms of the relationship between exchange rates and

inflation, the most frequently explored issues are how inflation rates react to changes in exchange

rates. Other questions that are crucial to this study are: Is the exchange rate fluctuations a major

cause of inflation in Nigeria? From the experience of Nigeria, what kind of relationship (the short

and long run) is between exchange rates and inflation over the post SAP period? What effects do

the prices of our exports have on the value of exchange rates?

These issues will be addressed in this paper and the paper is structured as follows: section

one is the introduction comprising the problems/ research questions the paper aims at

investigating, Section 2 provides the literature review and the theoretical background and briefly

discusses the stylized facts on exchange rates and inflation in Nigeria, Section 3 the methodology

highlighting the econometric models (vector autoregressive approach and ARCH and GARCH

models). The empirical analysis is conducted in Section 4 while section five contains the

summary, conclusions and recommendation.

2. Literature Review and Theoretical Framework

Fitzpatrick et al., (1976), however maintained that though an increase in money supply is a

necessary condition for the rise in the overall level of prices, it is not a sufficient condition. Some

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

324

www.globalbizresearch.com

other notable studies that have applied alternative inflationary models that include the exchange

rate as a determinant of inflation other than VAR methodology are: (Chhibber and Shafi, 1990);

(Egwaikhide, Chete and Falokun, 1994); (Gross and Schmitt, 2000), and (Omotor, 2005a) among

others.

Undoubtedly, the search for a realistic exchange rate in a depressed economy like Nigeria at

that time through currency devaluation was bound to generate inflationary pressures as most of

the imported goods had no close domestic substitute. Soludo (1993:54) in reference to Singh

(1986:87) emphatically stated that even the Chicago and Cambridge Schools of Economics,

though differ over their views on the functioning of economic systems, they however agreed that

deliberate adjustments of exchange rate is not a suitable method of structural change since such

generate inflation.

However, exchange rate adjustment and the inflation nexus have been discussed in some

studies (see, Weir, 1986; Shapiro, 1988; Edwards, 1989; Agenor, 1991; Rogers and Warg, 1995;

Kamin and Rogers, 1997; Kamin and Klau, 1998; Zhang, 2000; Odusola and Akinlo, 2001;

Phylaktis and Girardin, 2001; Kara and Nelson, 2002 and Lu and Zhang, 2003). At the core of

this discussion is the determination of the inflationary costs of devaluation. It is thus critical to

assess the extent to which exchange rate adjustment and reforms would have affected Nigeria’s

domestic prices.

Focusing on Uganda, (Elbadawi's, 1990) research revealed that rapid monetary expansion

and the precipitous depreciation of the parallel exchange rate were the principal determinants of

inflation during 1988-89. He concluded from the comprehensive review of exchange rate and

price movements that devaluation of the official exchange rate is not inflationary. Obviously, this

conclusion is consistent with the findings of (Chhibber and Shafik, 1990a) and (Sowa and

Kwakye, 1991) with respect to Ghana.

While Chhibber, (1991) posits that there is no one and-only-one relationship between

exchange rate and price inflation. Basing his argument on empirical studies of some African

countries, one of his main conclusions is that devaluation could exert upward pressure on the

general price level through its increased cost of production in the short-run. For Chhibber, the

extent to which devaluation of a local currency engenders inflation is largely a function of the

impact of such policy measures on the revenues and expenditures (budget) of government,

together with the monetary policy that is simultaneously pursued.

Most of the causality studies on developing countries’ inflation focus on Latin America

rather than inflationary episodes in sub-Saharan Africa. However, (Canetti and Greene,1991),

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

325

www.globalbizresearch.com

using vector autoregression analysis to separate the influence of money supply growth from

exchange rate changes on prevailing and predicted rates of inflation in Africa, find that both

exchange rate movements and monetary expansion affect consumer price changes in a number of

sub-Saharan African countries. In particular, the authors find a significant causal impact of

exchange rates on prices in Sierra Leone, Tanzania, and the Congo (then Zaire).

The effect of the exchange rate in the inflationary process can be exacerbated under

conditions in which the money supply reacts passively to any inflationary pressures. In this case,

exchange rate depreciation can play a key role in sustaining the inflationary spiral regardless of

whether the process is initiated by internal rather than external factors (Burdekin and Burketi

1996).

In some other studies, the relationship between exchange rates and inflation has been

investigated along the synthesis of monetarist and structuralist theories. The monetarists regard

inflation as a purely monetary phenomenon, caused and sustained by expansionary money supply.

The structuralists on the other hand argue that structural rigidities such as food prices and wage or

exchange rate changes in developing economies create structural vulnerability (Barungi, 1997).

As regards the inflation and exchange rate dynamics literature, (Agenor and Montiel, 1999)

observe that under purchasing power parity (PPP), the domestic price level appears to be

determined by the exchange rate. Thus, inflation stabilization would seemingly require that the

rate of depreciation be slowed to that of the exchange rate-thereby assigning it the task of

ensuring price stability and external balance be achieved through restrictive aggregate demand

policies.

Kara et al., (2002), in their study of the UK found that neither of the above extremes had

justification in empiricism. Rather, in line with (Campa and Goldberg, 2002) analysis of the UK,

the data reported a close and high correspondence between exchange rate changes and rates of

change in prices of products labeled as imported consumer goods. (Kara and Nelson, 2002)

observed that whereas, there is low correlation between domestic price (inflation) and nominal

exchange rate changes, the correlation between ‘import price inflation’ and nominal exchange

rate changes is however high.

Apkan (2009) was able to the dynamic relationship between oil price shocks and major

macroeconomic variables in Nigeria by applying a VAR approach. The study pointed out the

asymmetric effects of oil price shocks; it was found from their study that a strong positive

relationship between positive oil price changes and real government expenditures. Unexpectedly,

the result identified a marginal impact of oil price fluctuations on industrial output growth.

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

326

www.globalbizresearch.com

Furthermore, the “Dutch Disease” syndrome is observed through significant real effective

exchange rate appreciation.

Abwaku et al., (2010) examined the effects of oil price volatility, demand for foreign

exchange, and external reserves on exchange rate volatility in Nigeria using monthly data for the

period 1999:1 to 2009:12. The results showed that a 1.0 per cent permanent increase in oil price

at the international market increases exchange rate volatility by 0.54 per cent in the long-run,

while in the short-run by 0.02 per cent. Also a permanent 1.0 per cent increase in demand for

foreign exchange increases exchange rate volatility by 14.8 per cent in the long-run. Therefore,

recommends that demand for foreign exchange should be closely monitored and exchange rate

should move in tandem with the volatility in crude oil prices bearing in mind that Nigeria remains

an oil-dependent economy.

2.1 Macro Economic Variables

The exchange rate is a key macroeconomic variable in the context of general economic

policy making, and of economic reform programmes. Exchange rate plays a role in connecting

the price systems in different countries, thus enabling traders to compare prices directly. This

paper evaluates the trends exhibited by exchange rate in Nigeria in relation to other

macroeconomic variables considered in this paper.

With the introduction of market based exchange rate system in 1986, the naira exchange rate

has exhibited the features of continuous instability, for most of the period, reflecting

unidirectional depreciation in the official, bureau de change and parallel market for foreign

exchange. (Ibanda, 2006)

Figure 1: Exchange Rate trend in Nigeria

020406080

100120140160180

1980 1990 2000 2010 2020

Exch

ange

rat

e

years

chart showing the trend of exchange rate in Nigeria (1986-

2010)

exchange rate

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

327

www.globalbizresearch.com

Source: The Authors

The graph above (figure 1) shows the exchange rate trend in Nigeria from 1986 to 2010. The

graph indicated an upward movement in exchange rates from 1986 to 1993 after which the

exchange rates became stable up to 1998. In 1998, there was a sharp rise in exchange rate from

approximately 22 Naira per Dollar to 92 Naira per Dollar and continued to rise steadily up to

2004 and started decreasing from 2005. This downward trend continued for three years where in

2007 the exchange rate of Naira was 118 per one Dollar. From 2008 to 2010 exchange rates rose

from 147 to 154 Naira (approximately) respectively per one Dollar. Thus, generally, exchange

rates in Nigeria show an upward trend throughout the post SAP period with the exception of

2005, 2006 and 2007 when the country experienced decrease in exchange rates.

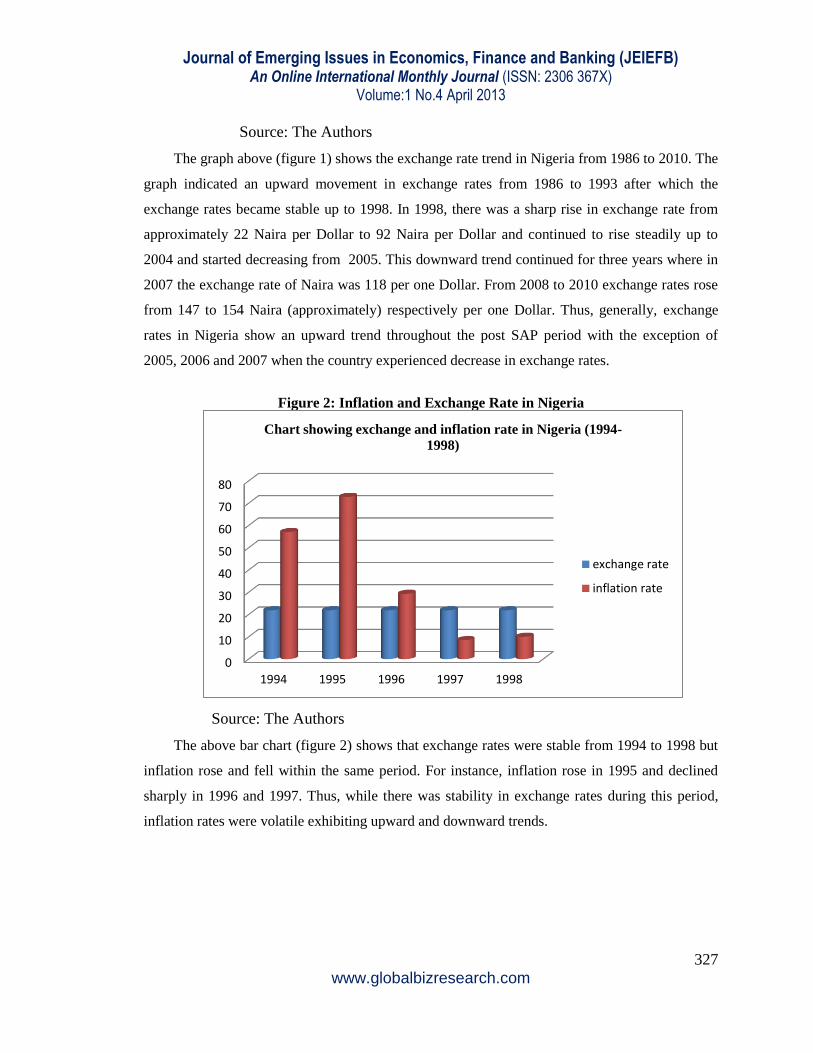

Figure 2: Inflation and Exchange Rate in Nigeria

Source: The Authors

The above bar chart (figure 2) shows that exchange rates were stable from 1994 to 1998 but

inflation rose and fell within the same period. For instance, inflation rose in 1995 and declined

sharply in 1996 and 1997. Thus, while there was stability in exchange rates during this period,

inflation rates were volatile exhibiting upward and downward trends.

0

10

20

30

40

50

60

70

80

1994 1995 1996 1997 1998

Chart showing exchange and inflation rate in Nigeria (1994-

1998)

exchange rate

inflation rate

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

328

www.globalbizresearch.com

Figure 3: Exchange Rate and Inflation Rate in Nigeria 1998 - 2004

Source: The Authors

Taking the cross section of exchange rates and inflation from 1998 to 2004, the graph above

shows persistent increases in exchange rates for the whole period while, inflation appeared to

fluctuate within the period. In 1999 inflation declined relative to 1998 and in 2000 there was a

slight increase in inflation; inflation rose significantly in 2001, dropped in 2002, rose again in

2003 and then declined in 2004.

Figure 4: Inflation and Exchange Rate in Nigeria 2004 - 2010

Source: The Authors

0

20

40

60

80

100

120

140

1998 1999 2000 2001 2002 2003 2004

Chart showing exchange and inflation rate in Nigeria (1998-

2004)

exchange rate

inflation rate

0

20

40

60

80

100

120

140

160

2004 2005 2006 2007 2008 2009 2010

Chart showing exchange and inflation rate in Nigeria (2004-2010)

exchange rate

inflation rate

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

329

www.globalbizresearch.com

The bar chart above shows a cross section of exchange rates and inflation in Nigeria from

2004 to 2010. It can be seen from the bar chart that while exchange rate decreased from 2004 to

2005 there was a slight increase in inflation from 2004 to 2005. However, exchange rates and

inflation moved in the same direction from 2005 to 2008 as shown above, exchange rates and

inflation declined from 2005 to 2007. In 2008, there was an increase in exchange rates and same

was experienced with regards to inflation. Nevertheless, rise in exchange rates in 2009 did not

lead to rise in inflation rather there was a decline in inflation compared to 2008. Similarly, there

was a rise in exchange rates in 2010 but inflation declined in the same period. From the above bar

charts, it will be very difficult to establish a particular type of relationship between inflation and

exchange rates in Nigeria. Although, both seem to be volatile, inflation seems to be more volatile

than exchange rate.

Figure 5: Inflation and Interest Rates in Nigeria 2004 to 2010

Source: The Authors

Looking at inflation and exchange rates from the graph above, there was a decline in interest

rate between 2004 and 2005 but inflation showed an increase from 10% to almost 12 in the same

period. However, from 2005 to 2007 inflation and interest rates moved in the same direction.

Between 2007 and 2008 Nigeria experienced sharp increase in inflation with slight increase in

interest rates compared to that of inflation. Again, between 2008 and 2009, inflation declined but

interest rates rose significantly. Generally, one can deduce that inflation and interest rates in

Nigeria between 2004 and 2010 have no specific (positive/direct or negative/indirect)

relationship.

0

10

20

30

40

50

60

70

80

90

100

2004 2005 2006 2007 2008 2009 2010

Chart showing inflation and exchange rate in

Nigeria (2004-2010)

inflation rate

interest rate

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

330

www.globalbizresearch.com

Figure 6: Inflation and Money Supply in Nigeria 2004 - 2010

Source: The Authors

Quantity of money supplied is one of the variables that affect inflation. From 2004 to 2005

there was a significant increase in money supply (M2) with slight increase inflation this trend

continued for money supply (M2) up to 2006 but for inflation it declined from 2005 to 2006 and

continued declining until 2007 when it began to rise and stood at 15.1 in 2008. For money supply

(M2), the graph shows that there was a decline in2007 and slight increase in 2008. In 2009 and

2010, inflation and money supply moved in a uniform direction both showing decline. Thus,

based on this, a direct relation relationship exists between inflation and broad money supply (M2)

in Nigeria.

3. Research Methodology

3.1 Types and Sources of Data

Annual data on exchange rate (Ex), inflation rate (Inf), interest rate (Int), broad money

supply, (Ms), and gross domestic product (GDP) were used for this research work. Data for the

variables are mainly secondary source from the central bank of Nigeria.

3.2 Model Specification

3.2.1 Vector Autoregressive Model

The theoretical link between exchange rate and inflation is quite complex as the literature

reviewed in the previous section. They are both potentially endogenous. This makes the use of

VAR modelling more appropriate. VAR can also be used to analyze the dynamic nature of the

0

20

40

60

80

100

2004 2005 2006 2007 2008 2009 2010

Chart showing inflation rate and money supply

in Nigeria (2004-2010)

inflation rate

money supply

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

331

www.globalbizresearch.com

inter-relationship between exchange rate and inflation which the static OLS modelling will not

allow. The VAR model assumes that the economy can be described by the following:

The VAR model with expected signs is specified as follows:

inft = Ex, int, ms, gdp, ••• ••• ••• ••• ••• ••• 1

(+) (+) (+) (-)

Where Inf t = Inflation Rate at time t

Ex t = Exchange Rate at time t

Intt = Interest rate at time t

Ms t = Broad money supply at time t Gdpt = Gross domestic product at time t

The structural form is:

inft = o + 1Ext-i + 2int t-i + 3ms t-i + 4gdp t-i + Uti ••• ••• ••• 2

3.2.2 Arch and Garch Models

Like most other financial data, exchange rate and inflation in Nigeria are known to be

volatile. It may not be appropriate to model it with ordinary least square; OLS which is the

commonest modeling technique because the basic assumptions concerning the means and

variance of stochastic term. (The white noise assumption) for which the estimates of this

technique will be accepted as robust may not hold. Besides, this problem may also make one to

cast doubt on the inferential procedure because it may cause incorrect rejection of the null

hypothesis i.e. type 1 error. As a result of this, this study consider two different but unique

models that take into consideration the volatile nature of financial data like exchange rate and

inflation into consideration. The models are ARCH AND GARCH.

The GARCH is respectively made up of the mean equation (3) and conditional variance

equation (4) below. Except the inclusion of last period’s forecast variance (λδ2t-1), the GARCH

model is the same as the ARCH. The mean equation of the inflation rate model and conditional

variance of inflation rate are therefore specified as follows:

Inft = α0 + α1Ext-1 + µt ••• ••• ••• ••• ••• ••• ••• 3

δ2

t = β1 + β2µ2t-1 + λ1δ

2t-1 ••• ••• ••• ••• ••• ••• ••• 4

Where inft and Ext-1 are the current inflation rate and previous session of exchange rate. α1 is

the coefficient of exchange rate while µt is the stochastic term of the model. In the conditional

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

332

www.globalbizresearch.com

variance equation, the news about volatility from previous period is denoted by µ2

t-1 and its

coefficient is β2.

The mean equation of the exchange rate model and the conditional variance of the exchange

rate are therefore specified as follows:

Ext = π0 + π1inft-1 + µ1 ••• ••• ••• ••• ••• ••• ••• 5

δ2

t = β1 + β2µ2t-1 + λ1δ

2t-1 ••• ••• ••• ••• ••• ••• ••• 6

The expected signs are α1 <0 and π1>o

4. Empirical Results and Discussions

4.1 The Estimation of Vector Autoregressive Model

4.1.1 Unit Root Test

A necessary but not sufficient condition for cointegration and VECM is that all series should

share the same integrational properties in a univariate sense. Prior to testing for cointegration, we

investigated the integrational properties of each of the variables by applying unit-root testing

procedure. This study makes use of Philips-Perron (PP) tests. The result shows that all variables

are not stationary in levels. After first difference, the PP test of unit root indicates that all

variables employed are stationary at one percent level and their use would not lead to spurious

regression. Therefore, all the series are stationary or integrated of the same order one, that is, I(1)

as expected.

Table (A): Results of Unit Root Tests: Using Philip-Perron (PP) Tests

Critical value: 1%=-4.4167, 5%=-3.6219, 10%=-3.2474 * 1% significance level

**5% significance level

***10% significance level (GDP and INT were logged)

Source: Author’s Estimation using E-views 4.0.

Variable Level, 1st difference With drift & trend Conclusion

INF Level First diff

-2.699044 -4.308325**

I(1)

EX

Level First diff

-2.187464 -.4.668140*

I(1)

INT Level First diff

-3.135162 -5.681758*

I(1)

M2 Level First diff

-2.166620 -4.750200*

I(1)

GDP Level First diff

-2.166820 -3.251937***

I(1)

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

333

www.globalbizresearch.com

4.1.2 Cointegration Test

Having established that the variables are integrated of the same order, we proceed to testing

for cointegration. The Johansen-Juselius maximum likelihood procedure was applied in

determining the cointegrating rank of the system and the number of common stochastic trends

driving the entire system. We reported the trace and maximum eigen-value statistics and its

critical values at both one per cent (1%) and five per cent (5%) in the table below. The result of

multivariate cointegration test based on Johansen and Juselius cointegration technique reveal that

there are three cointegrating equations at 5% and two cointegration equation at 1% level of

significant as indicated by the trace statistic while the max-eigien statistic only indicated three

cointegrating equation at 5% significant level. These results suggest that the appropriate model to

use is the VECM specification with more than one cointegrating vector in the model.

Table B: Unrestricted Cointegration Rank Test Trace Statistic and Max- Eigen Statistic

Hypothesized

No. of CE(s) Eigenvalue Trace

Statistic Max-Eigen

Statistic 5 Percent

Critical Value 1 Percent

Critical Value None** (*) 0.791824 98.29300 36.09554 68.52(33.46) 76.07(38.77) At most1**(*) 0.730775 62.19746 30.18079 47.21(27.07) 54.46(32.24) At most 2*(*) 0.612107 32.01666 21.78157 29.68(20.07) 35.65(25.52) At most 3 0.354929 10.23510 10.08307 15.41(14.07) 20.04(18.63) At most 4 0.006588 0.152026 0.152026 3.76 (3.76) 6.65(6.65)

*(**) denotes rejection of the hypothesis at the 5%(1%) level,Trace test indicates 3 cointegrating

equation(s) at the 5% level. Trace test indicates 2 cointegrating equation(s) at the 1% level.

Max-eigenvalue test indicates 3 cointegrating equation(s) at the 5% level

The parenthesis ( ) represent the max-eigen values

Source: Author’s Estimation using E-views 4.0.

4.1.3 Vector Error Correction Model

We proceed to estimate the VECM that is designed for use with non-stationary series that

are known to be cointegrated. The VECM has cointegration relations built into the specification

so that it restricts the long run behaviour of the endogenous variables to converge to their

cointegrating relationship while allowing for short-run adjustment dynamics. The cointegration

term is known as the error correction term (ECT) since the deviation from long-run equilibrium

is corrected gradually through a series of partial short-run adjustments. The results are presented

in the table (C) below. It shows that only some macroeconomic variables are crucial in

influencing the performance of the inflation rate as only few of the test statistics are significant.

The results were evaluated using the conventional diagnostic tests. The estimated VECM satisfy

the stability condition, that is, the vector error correction term in each of the models should have

the required negative sign and lie within the accepted region of less than unity.

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

334

www.globalbizresearch.com

Table C: Vector Error Correction Model Result

Error Correction: D(INF) D(EX) D(INT) D(M2) D(LOG(GDP

)) CointEq1 -0.683173 -0.147675 0.053005 0.062699 -0.000328

[-5.66075] [-0.61651] [ 0.86646] [ 0.23141] [-0.62153]

D(INF(-1)) 0.190928 0.058378 0.068880 -0.013992 0.000405

[ 1.45396] [ 0.22399] [ 1.03482] [-0.04746] [ 0.70558]

D(EX(-1)) -0.425316 -0.148701 0.017867 0.383242 0.000331

[-2.87991] [-0.50731] [ 0.23868] [ 1.15589] [ 0.51372]

D(INT(-1)) -2.942840 -0.226006 -0.170923 1.087247 0.001877

[-5.39242] [-0.20866] [-0.61788] [ 0.88740] [ 0.78722]

D(M2(-1)) 0.120849 -0.094345 0.011810 -0.082693 -0.000212

[ 1.01582] [-0.39956] [ 0.19585] [-0.30961] [-0.40767]

D(LOG(GDP(-

1))) -277.0014 -61.98458 -15.04484 68.33057 0.388603

[-4.60865] [-0.51960] [-0.49382] [ 0.50639] [ 1.48003]

C 11.56178 9.667702 0.576702 -2.704415 0.021353

[ 3.72360] [ 1.56875] [ 0.36642] [-0.38796] [ 1.57424]

R-squared 0.760774 0.042971 0.268235 0.152407 0.302742 Adj. R-squared 0.671065 -0.315915 -0.006177 -0.165440 0.041270 F-statistic 8.480416 0.119735 0.977491 0.479499 1.157839

Source: Author’s Estimation using E-views 4.0.

The error correction term in column two has the expected negative sign and is statistically

significant and it shows a low speed adjustment towards equilibrium. The results of the

estimation show that the explanatory variables account for about 76 percent variation in inflation

rate in Nigeria. The estimation also shows a negative relationship between inflation rate and

exchange rate in Nigeria and statistically significant (being our variables of interest). For instance

a one (1) percent increase in inflation rate ratio reduces exchange rate by about 0.42 percent. This

is consistent with the works of Burdekin and Burketi (1996), Elbadawi (1990) and Kara and

Nelson (2002), who discovered that increase in inflation leads to a decrease in exchange rate. The

negative relations between inflation and interest rate shows that interest rate have significant

relation with inflation in Nigeria. A 1 percent increase in inflation leads to approximately 2.9

percent decrease in interest rate and the estimation revealed that interest rate is statistically

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

335

www.globalbizresearch.com

significant. Moreover, a 1 percent increase in inflation rate in the previous year increases money

supply (M2) by approximately 0.12 percent though it is not statistically significant. Finally, it

shows that the log value of GDP is negative but has a significant influence on current inflation.

This is also indicating that a 1 percent increase in inflation rate in the previous year’s leads to a

decrease in the GDP by about 277 percent.

4.1.4 Impulse Response Analysis

Having estimated the VECM, the analysis proceeds to use those properties in analyzing the

short run dynamic properties of the economy using impulse response function. An impulse

response function (IRF) using the accumulated response to cholesky one S.D. innovations

measures the time profile of the effect of a shock on the behavior of time series. It is used to

investigate the time profile of the effect of a shock hitting the individual variables in the core

model at any time. Thus, for every VEC model we are able to compute the accumulated impulse

response functions for short-term exchange rate (EX), interest rate (INT), money supply (M2) and

output (GDP) that follow from a shock to inflation indicator. The analysis of accumulated

impulse responses of economic variables under consideration to inflation shock are presented

below.

Source: Author’s Estimation using E-views 4.0.

From the above diagram shock in inflation shows no relationship exist from the 1st via the

2nd

period however, from the 2nd

to the 10th period indicated that a positive response existed

throughout the period from inflation to exchange rate within the period of study. The accumulated

response of inflation to interest is similar with that of inflation to exchange rate. The accumulated

response of inflation to money supply from the first to the last quarter shows a positive effect

-100

-50

0

50

100

1 2 3 4 5 6 7 8 9 10

Accumulated Response of INF to EX

-100

-50

0

50

100

1 2 3 4 5 6 7 8 9 10

Accumulated Response of INF to INT

-100

-50

0

50

100

1 2 3 4 5 6 7 8 9 10

Accumulated Response of INF to M2

-100

-50

0

50

100

1 2 3 4 5 6 7 8 9 10

Accumulated Response of INF to LOG(GDP)

Accumulated Response to Cholesky One S.D. Innovations

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

336

www.globalbizresearch.com

throughout the horizon. However, the accumulated response of inflation to log (GDP) is negative

throughout the period. This indicated that the shock of inflation on GDP is negative both in the

short run and in the long run.

4.1.5 Variance Decomposition of Inflation

We now proceed to examine the relative strength of various processes through which

inflation impulses are transmitted to exchange rate. This is accomplished by carrying out a

decomposition of INF, EX, INT, M2 and GDP with a view to determining the size of the

fluctuation in a given variable that are caused by different shocks. The results are reported in the

table below, indicating the percentages of variance of the variable forecast as attributed to each

variable at a 10 quarter horizon. The first column list the periods, whereas the second column

refers to standards error (SE), which is the forecast error of the variable at different periods. The

third column refers to INF, the fourth EX, the fifth INT, the six M2 and the last GDP.

Table D: Variance Decomposition of Inflation

Period S.E. INF EX INT M2 LOG(GDP)

1 9.076819 100.0000 0.000000 0.000000 0.000000 0.000000 2 17.58423 58.06438 0.198957 0.124877 3.034296 38.57749 3 24.68259 40.29454 8.591895 8.463545 3.949481 38.70054 4 30.00269 36.58181 13.57599 12.29381 3.493765 34.05463 5 34.36845 35.97543 14.33206 12.16826 3.336181 34.18807 6 38.52859 34.48006 15.02361 12.51768 3.354020 34.62463 7 42.28941 33.43616 15.91688 13.16056 3.310044 34.17635 8 45.66252 32.97933 16.38931 13.38936 3.263681 33.97833 9 48.82666 32.57145 16.67415 13.51285 3.247429 33.99412 10 51.81528 32.19500 16.95926 13.68317 3.234009 33.92855 Source: Author’s Estimation using E-views 4.0.

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

337

www.globalbizresearch.com

Source: Author’s Estimation using Eviews 4.0.

Variance decomposition of INF has shown that in the first period none of the other variables

EX, INT, M2 and log (GDP) could explain any variability on INF; while the other variables like

EX, INT and M2 were gradually increasing inflation and log (GDP) were declining. However, in

the fifth quarter shocks in log (GDP), EX, INT, and M2 explain about 34 percent, 14 percent, 12

percent and 3 percent respectively on INF. while in the 10th period even though shocks log (GDP)

explain about 33.9 percent being the highest but is still declining about 17 percent, 14 percent and

3 percent shocks in EX, INT and M2 were explained by variability in INF.

4.2 The Estimation of Arch and Garch Models

The ARCH and GARCH models were used in testing the volatility of the exchange rate in

Nigeria from 1986 to 2010 and the results of the estimation indicate that the effect of exchange

rate during the previous period have significant effects on inflation rate in Nigeria at 5% level of

significance. The coefficient of exchange rate of the mean equation of the inflation function is -

0.099. Not as expected, the exchange rate is negatively related to inflation rate as presented

below:

inft = 26.99865 - 0.099Ext ••• ••• ••• ••• ••• ••• ••• 7

0

20

40

60

80

100

1 2 3 4 5 6 7 8 9 10

Percent INF variance due to EX

0

20

40

60

80

100

1 2 3 4 5 6 7 8 9 10

Percent INF variance due to INT

0

20

40

60

80

100

1 2 3 4 5 6 7 8 9 10

Percent INF variance due to M2

0

20

40

60

80

100

1 2 3 4 5 6 7 8 9 10

Percent INF variance due to LOG(GDP)

Variance Decomposition

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

338

www.globalbizresearch.com

The result of the estimation of conditional variance equation for inflation rate shows that

inflation rate is volatile because the coefficient of the ARCH component is significant at 5%.

Also, the summation of the coefficients of the ARCH and GARCH component (0.59 and 0.46) is

about 1. We therefore say the volatility is persistent.

The result of the estimation of the mean equation of exchange rate shows that there is

negative significant relationship between exchange rate and inflation rate in Nigeria at 5%. The

coefficient of inflation rate is -1.63. The ARCH component of the conditional variance equation

shows that there is evidence of volatility at 5% level of significance. Also the summation of the

coefficient of ARCH and GARCH components (0.72 and -0.26) gives less than 1. This indicates

that the volatility is not persistent as indicated below:

Ext = 119.0024 – 1.630inft ••• ••• ••• ••• ••• ••• 8

5. Conclusion and Recommendations

The study has attempted to assess the impact of exchange rate volatility on inflation rate in

Nigeria over the past 24 years through vector autoregressive analysis. A relatively large set of

factors that can potentially influence exchange rate volatility in Nigeria such as inflation rate,

broad money supply, interest rate and real gross domestic product are considered in the

econometric analysis. The paper also made use of ARCH and GARCH model in the test of

exchange rate volatility in Nigeria.

The results obtained from the vector error correction suggest that inflation and exchange

rates in Nigeria are negatively related which means that an increase in inflation rate leads to a

decrease in exchange rate. The result also shows that interest rate have significant relationship

with inflation in Nigeria. Moreover, inflation rate in the previous year increases money supply

(M2) by approximately 0.12 percent. Finally, the result shows that the log value of GDP is

negatively related but has a significant influence on current inflation. The results obtained from

the ARCH and GARCH model shows the evidence of volatility but the volatility is not persistent.

Finally, from the results of the empirical study, the following recommendations are proposed

to encourage and improve the exchange rate stability in Nigeria. There is the need to put in place

appropriate policies and strategies that will ensure the maintenance of a very stable inflation rate

as this has been an important factor influencing exchange rate. The government should direct it

expenditure to the key productive sectors of the economy such as agriculture and manufacturing

this will go a long way in increasing the production of goods and services thereby stabilizing the

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

339

www.globalbizresearch.com

prices and consequently exchange rate. The issue of country’s budget should be adequately

addressed as more of the country’s budget is recurrent than capital. It is not healthy for a country

with 70% recurrent expenditure because it shows that, the country’ expenditure is more of

consumption than investment which will definitely spark up inflation rate in the country. Further

efforts should therefore be geared towards reducing prime lending rate in such a manner that it

would boost the credit facilities for the productivity in the country.

Reference

Adebayo A. (2009). An Empirical Analysis of the effectiveness of foreign exchange intervention

in Nigeria. A paper presented at the 50th annual conference of the Nigerian economic society

(NES) Heal at Nicon Luxury Hotel Abuja.

Akanji O.A. (2007), Exchange Rates Policy Design: Choosing the right exchange Response in a

changing Environment.

Agenor, Pierre and Peter Montiel (1999), Development Macroeconomics, 2nd ed., Princeton

University Press, Princeton, NJ.

Barungi, B. Mbire (1997), Exchange Rate Policy and Inflation: The Case of Uganda. AERC

Research Papers, No. 59. Nairobi: African Economic Research Consortium.

Burdekin, RichardC.K. and Paul Burketi (1996), Hyperinflation, the Exchange Rate and

Endogenous Money: Post-World War I Germany Revisited, Journal of International Money

and Finance, Vol. 15, pp. 599–621.

CBN (2007), Economic and Financial Review, Volume 45 no 4.

Canetti, Elia and Joshua Greene (1991), Monetary Growth and Exchange Rate Depreciation as

Causes of Inflation in African Countries: An Empirical Analysis. Center for Economic Research

on Africa Research Monograph Series. School of Business-Montclair State University, New

Jersey.

Chhibber, A. and N. Shafi k (1991). The Infl ationary Consequences of Devaluation with P

arallelMarkets: The Case of Ghana. Chhibber, A. and S. Fischer (eds.) Economic Reform in sub

Saharan Africa. The World Bank, Washington, D.C., 39-49.

Egwaikhide, F.O., L.N. Chete and G.O. Falokun. (1994). Exchange Rate Depreciation, Budget

Def cit and Inflation: The Nigerian Experience. AERC Research Paper No. 26. Nairobi:African

Research Consortium.

Elbadawi, l.A., 1990, 'Inflationary Process, Stabilisation and the role of Public Expenditure in

Uganda', Mimeo, July, World Bank, Washington DC.

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306 367X)

Volume:1 No.4 April 2013

340

www.globalbizresearch.com

Fitzpatrick, C.H. and F.I. Nixson (1976), The origins of Inflation in Less Developing Countries:A

Selective Review, in: Parking M. and G. Zis (eds.), Inflation in Open Economies,

Manchester: Manchester University Press, pp. 126 – 74.

Kara, A. and F. Nelson (2002). “The Exchange Rate and Inflation in the UK”. External MPC

Unit Discussion Paper. No. 11.

Obadan M.I (2007), Exchange Rates Policy Design: Choosing the right exchange Response in a

changing Environment.

NBF News (2011), The Raging Debate over valuation of Naira. Business/Finance.

Soludo, C.C. (1993). “Theoretical Basis for the Structural Adjustment Programme in Nigeria:

Two Alternative Critiques”. The Nigerian Journal of Economic and Social Studies. 35 (1): 49-63.