January 27–28, 2009 Authorized for Public Release 218 … · Appendix 1: Materials used by Ms....

50

Appendix 1: Materials used by Ms. Mosser and Mr. Hilton January 27–28, 2009 218 of 267 Authorized for Public Release

Transcript of January 27–28, 2009 Authorized for Public Release 218 … · Appendix 1: Materials used by Ms....

Appendix 1: Materials used by Ms. Mosser and Mr. Hilton

January 27–28, 2009 218 of 267Authorized for Public Release

(1) U.S. Libor–OIS Spreads July 1, 2007 – January 23, 2009

Source: Bloomberg

Class II FOMC – Restricted FR

0

50

100

150

200

250

300

350

400

07/01/07 09/01/07 11/01/07 01/01/08 03/01/08 05/01/08 07/01/08 09/01/08 11/01/08 01/01/09

BPS

0

50

100

150

200

250

300

350

400BPS

1-Week1-Month3-Month

Sept.14: Lehman Brothers Holdings files for bankruptcy

Oct.13: Euro Area AnnouncementOct.14: Treasury Capital Purchase Program, FDIC Debt Guarantee, and

further details of Federal Reserve CPFF Program Announced

Page 1 of 16

(2) Three-Month Commercial Paper Rates August 1, 2008 – January 23, 2009

Source: Federal Reserve Board

0

1

2

3

4

5

6

7

8

08/01/08 09/01/08 10/01/08 11/01/08 12/01/08 01/01/09

Percent

0

1

2

3

4

5

6

7

8Percent

AA-Rated Non-Financial CPAA-Rated Financial CPAA-Rated ABCPA2/P2 Non-Financial CP

Oct.7: CPFF announced (effective Oct.27)

Sept.19: AMLF announced

Sept.14: Lehman Brothers Holdings files for bankruptcy

Oct.21: MMIFF announced

-100

-50

0

50

100

150

200

250

08/01/08 09/01/08 10/01/08 11/01/08 12/01/08 01/01/09

BPS

5.00

5.25

5.50

5.75

6.00

6.25

6.50

6.75Percent

Fannie 5Y Debt Spread to TSY Yield (LHS)Mortgage OAS to Treasury (LHS)30Y Fixed Conforming Mortgage Rate (RHS)

Sept.14: Lehman Brothers Holdings files for bankruptcySept.7: Fannie Mae and Freddie Mac enter conservatorship

Nov.25: Agency Coupon and Agency-MBS Purchases Announced

Jan.5: First Agency-MBS Purchase

Dec.30: Agency-MBS FAQ Released

(3) Mortgages and AgenciesAugust 1, 2008 – January 23, 2009

Source: Bloomberg, Lehman Brothers/Barclays

January 27–28, 2009 219 of 267Authorized for Public Release

Class II FOMC – Restricted FR

Source: Merrill Lynch/Bank of America

0

200

400

600

800

1000

08/01/07 10/01/07 12/01/07 02/01/08 04/01/08 06/01/08 08/01/08 10/01/08 12/01/08

BPS

0

500

1000

1500

2000

2500BPS

Investment Grade (LHS)

High Yield (RHS)

(4) Corporate Debt Cash Spreads Narrow RecentlyAugust 1, 2007 – January 23, 2009

(5) Monthly Investment Grade Bond IssuanceJanuary 2008 – January 2009

0

20

40

60

80

100

120

140

Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08 Jan-09 (2wks)

$ Billions

0

20

40

60

80

100

120

140$ Billions

GuaranteedNot Guaranteed

Source: JPMorgan Chase

Page 2 of 16

January 27–28, 2009 220 of 267Authorized for Public Release

Source: JPMorgan Chase

(6) Asset-Backed Security Spreads Narrow After Year EndAugust 1, 2008 – January 23, 2009

Class II FOMC – Restricted FR

(7) Commercial Mortgage-Backed and Leveraged Loan Prices Deteriorate August 1, 2008 – January 23, 2009

Source: Lehman Brothers/Barclays, JPMorgan Chase

556065707580859095

100

08/01/08 09/01/08 10/01/08 11/01/08 12/01/08 01/01/09

Dollar

556065707580859095100

Dollar

CMBX Series 2 (2006)CMBX Series 4 (2007)LCDX

0

100

200

300

400

500

600

700

08/01/08 09/01/08 10/01/08 11/01/08 12/01/08 01/01/09

BPS

0

100

200

300

400

500

600

700BPS

3-Year Auto (AAA-Rated)5-Year Credit Card (AAA-Rated)3-Year FFELP Student Loan (AAA-Rated)

Sept.14: Lehman Brothers Holdings files for bankruptcy

Dec.19: TALF announced

Page 3 of 16

January 27–28, 2009 221 of 267Authorized for Public Release

Class II FOMC – Restricted FR

(8) Average Daily Bid-Ask Spread: Euro-Dollar FX RateJanuary 1, 2007 – January 22, 2009

Source: ICAP FX

0.000

0.005

0.010

0.015

0.020

0.025

0.030

01/01/07 04/01/07 07/01/07 10/01/07 01/01/08 04/01/08 07/01/08 10/01/08 01/01/09

Percent

0.000

0.005

0.010

0.015

0.020

0.025

0.030Percent

10-Day Moving Average

Average Percent

Source: Broker Tec

(9) Trade Quote Sizes in the Treasury Market ShrinkAverage Daily, 2008 - 2009

0

50

100

150

200

250

2-year 5-year 10-year 30-year

$ Millions

0

50

100

150

200

250$ Millions

2008

Dec. 2008

Jan. 2009

Page 4 of 16

January 27–28, 2009 222 of 267Authorized for Public Release

Class II FOMC – Restricted FR(10) Average Absolute Price Error between Treasury Yields and FRB Model

January 1, 2007 – January 21, 2009

0

5

10

15

20

25

01/01/07 05/01/07 09/01/07 01/01/08 05/01/08 09/01/08 01/01/09

BPS

0

5

10

15

20

25BPS

Source: Federal Reserve Board*Calculated from securities with two to ten years until maturity, excluding on-the-run and first off-the-run securities.

-800

-600

-400

-200

0

200

01/01/08 03/01/08 05/01/08 07/01/08 09/01/08 11/01/08 01/01/09

Percent

-800

-600

-400

-200

0

200Percent

Investment Grade

High Yield

Sept.14: Lehman Brothers Holdings files for bankruptcy

(11) Corporate CDS Bond Basis January 1, 2007 – January 23, 2009

Source: JPMorgan Chase(12) Hedge Fund Returns Decline* January 1, 1998 – December 30, 2008

Source: CS/Tremont, Bloomberg, Lehman Brothers/Barclays

-30

-20

-10

0

10

20

30

40

01/01/98 01/01/00 01/01/02 01/01/04 01/01/06 01/01/08

Percent

-30

-20

-10

0

10

20

30

40Percent

Sept.14: Lehman Brothers Holdings files for bankruptcy

*12-Month rolling returns

Page 5 of 16

January 27–28, 2009 223 of 267Authorized for Public Release

Class II FOMC – Restricted FR

Source: Bloomberg

(13) Bank Earnings Disappoint Expectations Q3 2008 – Q4 2008

*U.K. banks report semi-annually**Expected to report Q4 earning on 1/28/09

Source: Goldman Sachs

(14) Bank Capital RatiosQ3 2008

3.4%

11.5%

6.1%

11.1%

0

3

6

9

12

15Percent

0

3

6

9

12

15Percent

8 Large Banks

14 Regional Banks

Tier 1 Ratio Tangible Common Equity Ratio

Earnings Estimate ($bln)

Actual Earnings ($bln)

Tangible Common Equity

to Assets

Tier 1 Capital Ratio

U.S. Bank Holding CompaniesJPMorgan Chase 0.4 0.7 3.8 8.9Citigroup -5.0 -8.3 1.8 8.2Bank of America 1.6 -1.8 2.6 7.6Merrill Lynch -1.9 -15.3 8.7Wells Fargo** 1.6 5.4 8.6State Street 0.0 0.1 2.4 16.0Bank of New York-Mellon 0.7 0.1 2.1 9.3Goldman Sachs -1.7 -2.1 11.6Morgan Stanley 0.5 -2.3 12.7

Foreign Banks (in local currency)UBS -3.1 1.6 10.8Credit Suisse -3.0 2.0 10.4Deutsche Bank -4.4 -4.8 1.2 7.6HSBC 4.2 3.4 8.2Barclays* 1.1 1.0 7.9RBS* -4.2 2.7BNP Paribas 0.7 2.1Societe Generale 0.6 2.7 8.2

Q4 Earnings Q3 Capital Ratios

Page 6 of 16

January 27–28, 2009 224 of 267Authorized for Public Release

Source: Bloomberg

0

20

40

60

80

100

120

140

08/01/08 09/01/08 10/01/08 11/01/08 12/01/08 01/01/09

Index to 100 on 8/1/08

0

20

40

60

80

100

120

140Index to 100 on 8/1/08

Morgan StanleyGoldman SachsS&P 500 Sept.22: Goldman and Morgan Stanley become bank holding companies

Sept.14: Lehman Brothers Holdings files for bankruptcy

Source: Bloomberg

(16) Commercial Bank Equity PricesAugust 1, 2008 – January 23, 2009

0

20

40

60

80

100

120

140

08/01/08 09/01/08 10/01/08 11/01/08 12/01/08 01/01/09

Index to 100 on 8/1/08

0

20

40

60

80

100

120

140Index to 100 on 8/1/08

JPMorgan ChaseCitigroupBank of AmericaWells FargoS&P 500 Sept.14: Lehman Brothers Holdings files for bankruptcy

(15) Former Investment Bank Equity PricesAugust 1, 2008 – January 23, 2009

Class II FOMC – Restricted FR

(17) European Bank Equity PricesAugust 1, 2008 – January 23, 2009

0

20

40

60

80

100

120

140

08/01/08 09/01/08 10/01/08 11/01/08 12/01/08 01/01/09

Index to 100 on 8/1/08

0

20

40

60

80

100

120

140Index to 100 on 8/1/08

BarclaysRBSHSBCDeutscheSociete GeneraleUBSCredit Suisse Sept.14: Lehman Brothers Holdings files for bankruptcy

Source: Bloomberg

Page 7 of 16

January 27–28, 2009 225 of 267Authorized for Public Release

Class II FOMC – Restricted FR

(18) Former Investment Bank CDS Spreads August 1, 2008 – January 23, 2009

Source: Markit

0200400600800

10001200140016001800

08/01/08 09/01/08 10/01/08 11/01/08 12/01/08 01/01/09

BPS

020040060080010001200140016001800

BPS

Morgan Stanley

Goldman Sachs

Sept.22: Goldman and Morgan Stanley become bank holding companies

Sept.14: Lehman BrothersHoldings files for bankruptcy

Oct.13: Euro Area AnnouncementOct.14: Treasury Capital Purchase Program, FDIC Debt Guarantee, and further details of Federal Reserve CPFF Program Announced

(19) Commercial Bank CDS SpreadsAugust 1, 2008 – January 23, 2009

Source: Markit

0

100

200

300

400

500

600

08/01/08 09/01/08 10/01/08 11/01/08 12/01/08 01/01/09

BPS

0

100

200

300

400

500

600BPS

JPMorgan ChaseCitigroupBank of AmericaWells Fargo

Sept.14: Lehman Brothers Holdings files for bankruptcy & Bank of America announced purchse of Merrill Lynch

Nov.23: US government provides a package of gurantees, liquidity access, and capital to Citigroup

Oct.13: Euro Area AnnouncementOct.14: Treasury Capital Purchase Program, FDIC Debt Guarantee, and further details of Federal Reserve CPFF Program Announced

(20) European Bank CDS SpreadsAugust 1, 2008 – January 23, 2009

Source: Bloomberg

050

100150200250300350400450

08/01/08 09/01/08 10/01/08 11/01/08 12/01/08 01/01/09

BPS

050100150200250300350400450BPS

BarclaysRBSHSBCDeutscheSociete GeneraleUBSCSFB

Sept.14: Lehman Brothers Holdings files for bankruptcy & Bank of America announced purchse of Merrill Lynch

Nov.23: US government provides a package of gurantees, liquidity access, and capital to Citigroup

Oct.13: Euro Area AnnouncementOct.14: Treasury Capital Purchase Program, FDIC Debt Guarantee, and further details of Federal Reserve CPFF Program Announced

Page 8 of 16

January 27–28, 2009 226 of 267Authorized for Public Release

Class II FOMC – Restricted FR

Source: Bloomberg

(21) Sovereign CDS Spreads WidenAugust 1, 2008 – January 23, 2009

050

100150200250300350400450

08/01/08 09/01/08 10/01/08 11/01/08 12/01/08 01/01/09

BPS

050100150200250300350400450BPS

USUKGermanySpainJapanIrelandAustraliaKorea

Source: Bloomberg

(22) Treasury Yield Curve Steepens ModestlyAugust 1, 2007 – January 23, 2009

0.51.01.52.02.53.03.54.04.55.05.5

08/01/07 10/01/07 12/01/07 02/01/08 04/01/08 06/01/08 08/01/08 10/01/08 12/01/08

Percent

0.51.01.52.02.53.03.54.04.55.05.5

Percent

2-Year5-Year10-Year30-Year

(23) Distribution of Expected Policy Target Rate Among Primary Dealers Prior to January 28 FOMC Meeting

Source: Dealer Policy Survey

-1.0-0.50.00.51.01.52.02.53.03.54.0

Percent

Survey Response -size indicates freq

January Average Forecast

Market Rates as of 1/20

Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010

Page 9 of 16

January 27–28, 2009 227 of 267Authorized for Public Release

Source: Federal Reserve Bank of New York

(24) Federal Reserve Balance Sheet Assets August 2007 – January 2009

Class II FOMC – Restricted FR

0250500750

1000125015001750200022502500

8-Aug-07 12-Sep-08 22-Oct-08 17-Dec-08 31-Dec-08 23-Jan-09

$ Billions

02505007501000125015001750200022502500

$ Billions

All Other LendingPCF+PDCFAMLFCPFFFX SwapsTAFOutright Agency HoldingsSingle Tranche RepoConventional RPsOutright Treasury HoldingsAutofactors

(25) Market Rates Corresponding to Liquidity Facilities July 1, 2008 – January 23, 2009

0.000.501.001.502.002.503.003.504.004.505.00

07/01/08 09/01/08 11/01/08 01/01/09

Percent

0.000.501.001.502.002.503.003.504.004.505.00

Percent

1M GC Treasury Repo1M Agency-MBS Repo1M USD Libor3M USD Libor3M Financial CP

Sept.14: Lehman Brothers Holdingsfiles for bankruptcy

Year End

Source: Federal Reserve Bank of New York

Page 10 of 16

January 27–28, 2009 228 of 267Authorized for Public Release

(26) TSLF Loans Outstanding March 28, 2008 – January 23, 2009

0255075

100125150175200225250

03/28/08 05/28/08 07/28/08 09/28/08 11/28/08

$ Billions

0255075100125150175200225250

$ Billions

TOP (Schedule 2)Schedule 2Schedule 1

Year End

Source: Federal Reserve Bank of New York(27) Demand at TSLF Auctions

March 27, 2008 – January 22, 2009

0.00.51.01.52.02.53.03.54.04.5

3/28/08 5/9/08 6/20/08 8/1/08 9/12/08 10/3/08 10/31/08 11/28/08 12/26/08 1/23/09

Percent

0102030405060708090

$ Billions

Sch1: Auction Size (RHS)Sch1: Amount Awarded (RHS)Sch2: Auction Size (RHS)Sch2: Amount Awarded (RHS)Sch1: Stop-Out Rate (LHS)Sch2: Stop-Out Rate (LHS)

Source: Federal Reserve Bank of New York

Class II FOMC – Restricted FR

(28) Total Outstanding FX Swap Draw-Downs Decline December 1, 2007 – January 23, 2009

0

100

200

300

400

500

600

12/01/07 02/01/08 04/01/08 06/01/08 08/01/08 10/01/08 12/01/08

$ Billions

0

100

200

300

400

500

600$ Billions

Norges Bank Danmark NBBOK Riksbank RBA BOJ BOE SNB ECB

Year End

Source: Federal Reserve Bank of New York

Page 11 of 16

January 27–28, 2009 229 of 267Authorized for Public Release

(29) Term Auction Facility Loans Outstanding December 20, 2007 – January 23, 2009

050

100150200250300350400450500

12/20/07 02/20/08 04/20/08 06/20/08 08/20/08 10/20/08 12/20/08

$ Billions

050100150200250300350400450500

$ Billions

Forward84-Day28-Day

Year End

Source: Federal Reserve Bank of New York(30) Demand at TAF Auctions

December 20, 2007 – January 15, 2009

0

25

50

75

100

125

150

175

200

12/20/07 2/28/08 5/8/08 7/17/08 9/11/08 11/6/08 12/23/08

BPS

0

25

50

75

100

125

150

175

200$ Billions

Auction Size (RHS)Amount Awarded (RHS)Stop-Out Rate Spread to Minimum Bid Rate (LHS)

84-Day Term

Forward Settling Auctions

Source: Federal Reserve Board

Class II FOMC – Restricted FR

0255075

100125150175200225250

01/01/08 02/12/08 03/25/08 05/06/08 06/17/08 07/29/08 09/09/08 10/21/08 12/02/08 01/13/09

$ Billions

0255075100125150175200225250

$ Billions

PDCF

PCFSept.14: Lehman Brothers Holdings files for bankruptcy

Year End

(31) PCF and PDCF BorrowingJanuary 1, 2008 – January 23, 2009

Source: Federal Reserve Bank of New York

Page 12 of 16

January 27–28, 2009 230 of 267Authorized for Public Release

Source: Federal Reserve Bank of New York

Class II FOMC – Restricted FR

(33) AMLF Loans Outstanding September 22, 2008 – January 23, 2009

0

25

50

75

100

125

150

175

09/22/08 10/07/08 10/22/08 11/06/08 11/21/08 12/06/08 12/21/08 01/05/09 01/20/09

$ Billions

0

25

50

75

100

125

150

175$ Billions

Source: Federal Reserve Bank of New York

(32) Amount of CPFF Loans Outstanding October 27, 2008 – January 23, 2009

0

50

100

150

200

250

300

350

400

10/27/08 11/11/08 11/26/08 12/11/08 12/26/08 01/10/09

$ Billions

0

50

100

150

200

250

300

350

400$ Billions

CPFDIC Guaranteed CPABCP

(34) Assets in Prime Money Market Funds August 1, 2008 – January 23, 2009

Source: iMoneyNet

1400

1600

1800

2000

2200

2400

08/01/08 09/01/08 10/01/08 11/01/08 12/01/08 01/01/09

$Billions

0

200

400

600

800

1000$Billions

Prime (LHS)Treasury Only (RHS)Treasury & Repo (RHS)Treasury & Agency (RHS)

Oct.7: CPFF announced (effective Oct.27)

Sept.19: AMLF announced

Sept.14: Lehman Brothers Holdings files for bankruptcySept.16: Reserve Fund breaks the buck

Oct.21: MMIFF

Jan.5: MMIFF eligibility expanded

Page 13 of 16

January 27–28, 2009 231 of 267Authorized for Public Release

0

10

20

30

40

50

60

5-Jan 6-Jan 7-Jan 8-Jan 9-Jan 12-Jan 13-Jan 14-Jan 15-Jan 16-Jan 20-Jan 21-Jan 22-Jan 23-Jan

$ Billions

0

10

20

30

40

50

60$ Billions

Cummulative Amount PurchasedAgency-MBS Purchase Size

Source: Federal Reserve Bank of New York

(35) Purchases of Agency-MBS January 5, 2009 – January 23, 2009

0

5

10

15

20

25

5-Dec-08 12-Dec-09 18-Dec-08 19-Dec-08 23-Dec-08 9-Jan-09 13-Jan-09 22-Jan-09

$ Billions

0

5

10

15

20

25$ Billions

Cumulative Amount PurchasedAgency Coupon Purchase Size

(37) Purchases of Agency Coupon Debt December 5, 2008 – January 22, 2009

Source: Federal Reserve Bank of New York

0

100

200

300

400

500

01/01/08 03/01/08 05/01/08 07/01/08 09/01/08 11/01/08 01/01/09

Index=100 on 1/1/08

0

100

200

300

400

500Index=100 on 1/1/08

Mortgage Application IndexMortgage Refinance Application Index

Nov.25: Agency Coupon and Agency-MBS Purchases Announced

Jan.5: First Agency-MBS Purchase

Dec.30: Agency-MBS FAQ Released

(36) Mortgage Refinance Applications January 1, 2008 – January 16, 2009

Source: Bloomberg

Class II FOMC – Restricted FR Page 14 of 16

January 27–28, 2009 232 of 267Authorized for Public Release

Source: Bloomberg

(38) Three-Month Libor and Expectations for Three-Month Libor Decline July 1, 2007 – January 23, 2009

Class II FOMC – Restricted FR

0

1

2

3

4

5

6

07/01/07 09/01/07 11/01/07 01/01/08 03/01/08 05/01/08 07/01/08 09/01/08 11/01/08 01/01/09

Percent

0

1

2

3

4

5

6Percent

3-Month U.S. Libor

3-Month Forward 3-Month Libor

Sept.14: Lehman Brothers Holdings files for bankruptcy

Oct.13: Euro Area AnnouncementOct.14: Treasury Capital Purchase Program, FDIC Debt Guarantee,

and further details of Federal Reserve CPFF Program Announced

APPENDIX: Reference Exhibits

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

01/01/08 04/01/08 07/01/08 10/01/08 01/01/09

Percent

0

30

60

90

120

150

180

210BPS

Conforming Mortgage Rates (LHS)Jumbo Mortgage Rates (LHS)Spread (RHS)

Sept.14: Lehman Brothers Holdings files for bankruptcySept.7: Fannie Mae and Freddie Mac enter conservatorship

Nov.25: Agency Coupon and Agency-MBS Purchases Announced

Jan.5: First Agency-MBS Purchase

Dec.30: Agency-MBS FAQ Released

(39) Spread between Jumbo and Conforming Mortgage Rates Remains WideJanuary 1, 2008 – January 23, 2009

Source: Bloomberg

0.75

1.00

1.25

1.50

1.75

2.00

2.25

08/01/08 09/01/08 10/01/08 11/01/08 12/01/08 01/01/09

Ratio

0.75

1.00

1.25

1.50

1.75

2.00

2.25Ratio

10-Year

30-Year

(40) Ten- and Thirty- Year AAA–Rated Municipal Debt Yields Decline* August 1, 2008 – January 23, 2009

Source: Bloomberg

Page 15 of 16

January 27–28, 2009 233 of 267Authorized for Public Release

Class II FOMC – Restricted FR

(41) Distribution of Expected Policy Target Rate Among Primary Dealers Prior to December 16 FOMC Meeting

Source: Dealer Policy Survey Q1 2009 Q2 2009 Q3 2009 Q4 2009

-0.25

0.00

0.25

0.50

0.75

1.00

1.25Percent

Survey Response -size indicates freq

December Average Forecast

Market Rates as of 12/08

Page 16 of 16

January 27–28, 2009 234 of 267Authorized for Public Release

Appendix 2: Materials used by Mr. Sichel, Ms. Dynan, and Mr. Reeve

January 27–28, 2009 235 of 267Authorized for Public Release

CLASS II FOMC - Restricted (FR)

Material for

Staff Presentation on the

Economic Outlook

January 27, 2009

January 27–28, 2009 236 of 267Authorized for Public Release

January 27–28, 2009 237 of 267Authorized for Public Release

January 27–28, 2009 238 of 267Authorized for Public Release

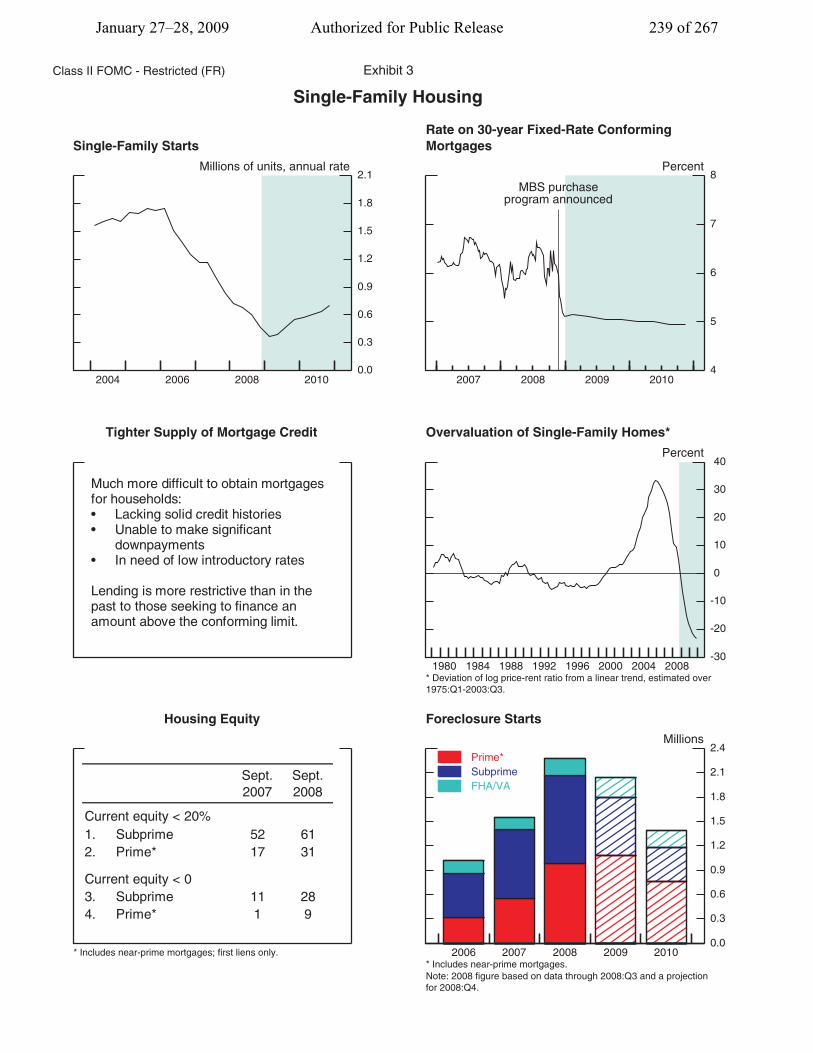

January 27–28, 2009 239 of 267Authorized for Public Release

January 27–28, 2009 240 of 267Authorized for Public Release

January 27–28, 2009 241 of 267Authorized for Public Release

January 27–28, 2009 242 of 267Authorized for Public Release

January 27–28, 2009 243 of 267Authorized for Public Release

January 27–28, 2009 244 of 267Authorized for Public Release

January 27–28, 2009 245 of 267Authorized for Public Release

Class II FOMC - Restricted (FR) Exhibit 10

Global Financial Markets

30

40

50

60

70

80

90

100 110

Jul Sep Nov Jan

Equity PricesIndex, Jun. 3, 2008 = 100

Weekly

Emergingmarkets

UnitedKingdom

Euroarea

Japan

Dec.FOMC

2008

30

40

50

60

70

80

90

100 110

Jul Sep Nov Jan

Bank Equity PricesIndex, Jun. 3, 2008 = 100

Weekly

Emergingmarkets

UnitedKingdom

Euroarea

Japan

Dec.FOMC

2008

0

100

200

300

400

500

600

700

Jul Sep Nov Jan

Outstanding Central Bank Swap DrawsBillions of dollars

Weekly

3-monthOther

2008

0

50

100

150

200

250

300

350

400

Jul Sep Nov Jan

3-Month LIBOR-OIS SpreadsBasis points

Daily Dec.FOMCDollar

Sterling

Euro

2008

70

75

80

85

90

2006 2007 2008 2009 2010

Broad Real DollarIndex, Feb. 2002 = 100

Monthly

Dec. GB

95

100

105

110

115

120

125

Jul Sep Nov Jan

U.S. Dollar Exchange RatesIndex, Jun. 3, 2008 = 100

Daily Dec.FOMC

2008

OITP index*

Majorcurrencies

index

*Other important trading partners.

January 27–28, 2009 246 of 267Authorized for Public Release

Class II FOMC - Restricted (FR) Exhibit 11

Foreign Growth Outlook

-30

-20

-10

0

10

20

2007 2008

Japan12-month percent change

Real household spending

Real exports

Nov.

Dec.

20

25

30

35

40

45

50

55

60

2007 2008

Global PMIsDiffusion index

New exportorders

Manufacturingoutput

Dec.

Source: Haver Analytics.

0

5

10

15

20

2007 2008

China12-month percent change

Retail salesvolume

Industrial productionNov.

Dec.

-10.0

-7.5

-5.0

-2.5

0.0

2.5

5.0

2007 2008

Euro Area12-month percent change

Retail salesvolume

Industrial production

Nov.

Nov.

Real GDP* Percent change, annual rate**

2007 2008 2009p 2010p

Q1-Q3 Q4e Q1 Q2 H2

1. Total 4.2 1.4 -3.8 -2.8 -0.8 1.5 2.82. December Greenbook 4.2 1.4 -1.6 -1.2 0.1 1.5 2.8

3. Advanced Foreign Economies 2.6 0.2 -2.8 -3.4 -1.9 0.6 1.94. Japan 2.0 -1.1 -5.2 -3.7 -1.5 0.0 1.15. Euro area 2.1 0.4 -2.0 -2.0 -1.0 0.7 1.96. United Kingdom*** 3.0 -0.4 -5.9 -4.0 -2.2 0.3 1.77. Canada 2.8 0.4 -2.4 -4.4 -2.8 0.7 2.1

8. Emerging Market Economies 6.4 3.0 -5.0 -1.9 0.8 2.6 4.19. Emerging Asia 7.8 4.0 -6.5 -0.8 1.8 4.3 5.710. China 11.4 9.1 0.3 4.0 6.5 7.5 8.811. Latin America 4.8 1.8 -4.1 -3.5 -0.4 0.9 2.512. Mexico 4.2 0.9 -5.0 -4.0 -1.0 0.4 2.2

*GDP aggregates weighted by shares of U.S. merchandise exports.**Change from final quarter of preceding period to final quarter of period indicated.***Updated since January Greenbook.

January 27–28, 2009 247 of 267Authorized for Public Release

Class II FOMC - Restricted (FR) Exhibit 12

U.S. Trade

70

90

110

130

150

170

190

2002 2003 2004 2005 2006 2007 20080

20

40

60

80

100

120

Nominal TradeBillions of dollarsBillions of dollars

Monthly

Q1p

Non-oil imports

Oil imports

Exports

5

10

15

20

25

2002 2003 2004 2005 2006 2007 2008

Automotive TradeBillions of dollars

Monthly

Exports

Imports

Q1p

-100

-80

-60

-40

-20

0

20

2002 2003 2004 2005 2006 2007 2008

Trade BalanceBillions of dollars

Monthly

Q1pEx. oil imports

Total

0

2

4

6

8

10

2002 2003 2004 2005 2006 2007 2008

Aircraft ExportsBillions of dollars

MonthlyQ1p

Trade in Real Goods and Services

2007 2008 2009p 2010p

Q1-Q3 Q4e Q1 Q2 H2

Growth Rates (percent, annual rate*)

1. Exports 8.9 6.7 -19.9 -5.1 -2.7 -0.1 2.4

2. Imports 1.1 -3.9 -15.4 -11.7 -1.9 5.8 5.4

Contribution to Real GDP Growth (percentage points, annual rate*)

3. Net Exports 0.8 1.6 -0.1 1.2 -0.1 -0.8 -0.5

4. December Greenbook 0.8 1.6 0.4 0.9 0.1 -0.5 -0.4

*Change from final quarter of preceding period to final quarter of period indicated.

January 27–28, 2009 248 of 267Authorized for Public Release

Class II FOMC - Restricted (FR) Exhibit 13

Cyclical Comparisons

-4

-2

0

2

4

6

8

10

1975 1980 1985 1990 1995 2000 2005 2010

Real GDPPercent change, Q4/Q4

United States

Foreign*

NBERpeak

*Weighted by shares of U.S. merchandise exports.

70

80

90

100

110

120

130

140

1975 1980 1985 1990 1995 2000 2005 2010

Broad Real DollarIndex, historical average = 100

NBERpeak

Note: Gray shading represents U.S. recessions as dated by the NBER. Blue shading represents the forecast period.

-3

-2

-1

0

1

2

3

1975 1980 1985 1990 1995 2000 2005 2010

Contribution of Trade to U.S. GDP GrowthPercentage points, Q4/Q4

ExportsImportsNet exports

NBERpeak

January 27–28, 2009 249 of 267Authorized for Public Release

Class II FOMC - Restricted (FR) Exhibit 14

Commodity Prices

20

40

60

80

100

120

140

160

2007 200820

40

60

80

100

120

140

160

Recent Price DevelopmentsDollars per barrelIndex, Jan. 3, 2007 = 100

Daily

WTI oil

CRB nonfuel

Peak oil price

-50

-25

0

25

50

2007 2008

U.S. Crude Oil InventoriesMillions of barrels

Weekly

Deviation fromhistorical average

Peak oil price

-100

-50

0

50

100

150

Jan Apr Jul Oct Jan200

250

300

350

400

450

Financial Investors’ Net Oil Futures PositionsThousands of contractsThousands of contracts

Noncommercialtraders

Indexinvestors

2008

Peak oil price

Source: CFTC.

24

26

28

30

32

2007 200844

46

48

50

52

Oil ProductionMillions of barrels per dayMillions of barrels per day

OPEC*

Non-OPEC

JanuaryOPEC target

Peak oil price

*Excluding Indonesia and Iraq.

-6

-4

-2

0

2

4

6

2007 2008

Oil DemandFour-quarter percent change

World

Advancedeconomies

Emergingeconomies

Peak oil price

20

40

60

80

100

120

140

160

2007 2008 2009 201020

40

60

80

100

120

140

160

Commodity Price OutlookDollars per barrelIndex, Jan. 2007 = 100

Oil importprice

Nonfuelindex

January 27–28, 2009 250 of 267Authorized for Public Release

Class II FOMC - Restricted (FR) Exhibit 15 (Last Exhibit)

Prices

-4

-2

0

2

4

6

8

2007 2008 2009 2010

Consumer Price IndexesFour-quarter percent change

Canada

UnitedKingdomEuro

area

Japan

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2006 2007 2008

CPI Excluding Food and Energy*12-month percent change

Euroarea

UnitedKingdom

Canada

Japan Nov.

Dec.

Dec.

Dec.

*Staff estimates.

-4

-2

0

2

4

6

8

2007 2008 2009 2010

Consumer Price IndexesFour-quarter percent change

Emerging Asia

Latin America

-1

0

1

2

3

4

5

6

2007 2008 2009 2010

Policy RatesPercent

United Kingdom

Euro area

Canada

Japan

0

2

4

6

8

2006 2007 2008

CPI Excluding Food*12-month percent change

EmergingAsia

LatinAmerica

Dec.

Nov.

*Staff estimates.

0

5

10

15

2007 2008 2009 2010

Policy RatesPercent

Korea

Mexico

China

Brazil

January 27–28, 2009 251 of 267Authorized for Public Release

Appendix 3: Materials used by Mr. Madigan

January 27–28, 2009 252 of 267Authorized for Public Release

Class I FOMC – Restricted Controlled (FR)

Material for Briefing on FOMC Participants’ Economic Projections

Brian Madigan January 27, 2009

January 27–28, 2009 253 of 267Authorized for Public Release

2

1

+_0

1

2

3

4

5

Percent

Figure 1. Central tendencies and ranges of economic projections, 2009–11 and over the longer run

Change in real GDP

Range of projections

Actual

2004 2005 2006 2007 2008 2009 2010 2011 LongerRun

Central tendency of projections

5

6

7

8

9

Percent

Unemployment rate

2004 2005 2006 2007 2008 2009 2010 2011 LongerRun

+_0

1

2

3

Percent

PCE inflation

2004 2005 2006 2007 2008 2009 2010 2011 LongerRun

+_0

1

2

3

Percent

Core PCE inflation

2004 2005 2006 2007 2008 2009 2010 2011

NOTE: Definitions of variables are in the notes to table 1. The data for the actual values of the variables are annual.

Exhibit 1: Economic Projections of FOMC Participants for 2009 to 2011 and over the Longer Run

January 27–28, 2009 254 of 267Authorized for Public Release

Exhibit 2: Economic Projections of FOMC Participants for 2009 to 2011 and over the Longer Run

Real GDP Growth

2009 2010 2011 Longer-Run

Central Tendency -1.3 to -0.5 2.5 to 3.3 3.8 to 5.0 2.5 to 2.7 October projections -0.2 to 1.1 2.3 to 3.2 2.8 to 3.6 2.5 to 2.7

Range -2.5 to 0.2 1.5 to 4.5 2.3 to 5.5 2.4 to 3.0 October projections -1.0 to 1.8 1.0 to 4.5 2.0 to 5.0 2.0 to 2.9

Memo: Greenbook -0.8 2.6 4.9 2.7 October Greenbook -0.1 2.3 4.5 2.7

Unemployment Rate

2009 2010 2011 Longer-Run

Central Tendency 8.5 to 8.8 8.0 to 8.3 6.7 to 7.5 4.8 to 5.0 October projections 7.1 to 7.6 6.5 to 7.3 5.5 to 6.6 4.8 to 5.0

Range 8.0 to 9.2 7.0 to 9.2 5.5 to 8.0 4.5 to 5.5 October projections 6.6 to 8.0 5.5 to 8.0 4.9 to 7.3 4.5 to 5.8

Memo: Greenbook 8.4 8.1 6.7 4.8 October Greenbook 7.2 7.2 6.4 4.8

PCE Inflation

2009 2010 2011 Longer-Run

Central Tendency 0.3 to 1.0 1.0 to 1.5 0.9 to 1.7 1.7 to 2.0 October projections 1.3 to 2.0 1.4 to 1.8 1.4 to 1.7 1.7 to 1.8

Range -0.5 to 1.5 0.7 to 1.8 0.2 to 2.1 1.5 to 2.0 October projections 1.0 to 2.2 1.1 to 1.9 0.8 to 1.8 1.5 to 2.0

Memo: Greenbook 0.6 1.1 0.8 ----- October Greenbook 1.4 1.4 1.1 -----

Core PCE Inflation

2009 2010 2011

Central Tendency 0.9 to 1.1 0.8 to 1.5 0.7 to 1.5 October projections 1.5 to 2.0 1.3 to 1.8 1.3 to 1.7

Range 0.6 to 1.5 0.4 to 1.7 0.0 to 1.8 October projections 1.3 to 2.1 1.1 to 1.9 0.8 to 1.8

Memo: Greenbook 1.0 0.8 0.6 October Greenbook 1.5 1.3 1.1

January 27–28, 2009 255 of 267Authorized for Public Release

Exhibit 3: Risks and Uncertainty in Economic Projections

Uncertainty about GDP Growth Risks to GDP Growth

0

4

8

12

16

Lower Similar Higher

OctoberJanuary

0

4

8

12

16

Downside Balanced Upside

Uncertainty about PCE Inflation Risks to PCE Inflation

0

4

8

12

16

Lower Similar Higher

OctoberJanuary

0

4

8

12

16

Downside Balanced Upside

January 27–28, 2009 256 of 267Authorized for Public Release

2

4

6

8

10

12

Number of participants

Figure 2.A. Distribution of participants’ projections for the change in real GDP, 2009–11 and over the longer run

2009

October projections

-2.6--2.5

-2.4--2.3

-2.2--2.1

-2.0--1.9

-1.8--1.7

-1.6--1.5

-1.4--1.3

-1.2--1.1

-1.0--0.9

-0.8--0.7

-0.6--0.5

-0.4--0.3

-0.2--0.1

0.0-0.1

0.2-0.3

0.4-0.5

0.6-0.7

0.8-0.9

1.0-1.1

1.2-1.3

1.4-1.5

1.6-1.7

1.8-1.9

2.0-2.1

2.2-2.3

2.4-2.5

2.6-2.7

2.8-2.9

3.0-3.1

3.2-3.3

3.4-3.5

3.6-3.7

3.8-3.9

4.0-4.1

4.2-4.3

4.4-4.5

4.6-4.7

4.8-4.9

5.0-5.1

5.2-5.3

5.4-5.5

Percent range

January projections

2

4

6

8

10

12

Number of participants

2010

-2.6--2.5

-2.4--2.3

-2.2--2.1

-2.0--1.9

-1.8--1.7

-1.6--1.5

-1.4--1.3

-1.2--1.1

-1.0--0.9

-0.8--0.7

-0.6--0.5

-0.4--0.3

-0.2--0.1

0.0-0.1

0.2-0.3

0.4-0.5

0.6-0.7

0.8-0.9

1.0-1.1

1.2-1.3

1.4-1.5

1.6-1.7

1.8-1.9

2.0-2.1

2.2-2.3

2.4-2.5

2.6-2.7

2.8-2.9

3.0-3.1

3.2-3.3

3.4-3.5

3.6-3.7

3.8-3.9

4.0-4.1

4.2-4.3

4.4-4.5

4.6-4.7

4.8-4.9

5.0-5.1

5.2-5.3

5.4-5.5

Percent range

2

4

6

8

10

12

Number of participants

2011

-2.6--2.5

-2.4--2.3

-2.2--2.1

-2.0--1.9

-1.8--1.7

-1.6--1.5

-1.4--1.3

-1.2--1.1

-1.0--0.9

-0.8--0.7

-0.6--0.5

-0.4--0.3

-0.2--0.1

0.0-0.1

0.2-0.3

0.4-0.5

0.6-0.7

0.8-0.9

1.0-1.1

1.2-1.3

1.4-1.5

1.6-1.7

1.8-1.9

2.0-2.1

2.2-2.3

2.4-2.5

2.6-2.7

2.8-2.9

3.0-3.1

3.2-3.3

3.4-3.5

3.6-3.7

3.8-3.9

4.0-4.1

4.2-4.3

4.4-4.5

4.6-4.7

4.8-4.9

5.0-5.1

5.2-5.3

5.4-5.5

Percent range

2

4

6

8

10

12

Number of participants

Longer Run

-2.6--2.5

-2.4--2.3

-2.2--2.1

-2.0--1.9

-1.8--1.7

-1.6--1.5

-1.4--1.3

-1.2--1.1

-1.0--0.9

-0.8--0.7

-0.6--0.5

-0.4--0.3

-0.2--0.1

0.0-0.1

0.2-0.3

0.4-0.5

0.6-0.7

0.8-0.9

1.0-1.1

1.2-1.3

1.4-1.5

1.6-1.7

1.8-1.9

2.0-2.1

2.2-2.3

2.4-2.5

2.6-2.7

2.8-2.9

3.0-3.1

3.2-3.3

3.4-3.5

3.6-3.7

3.8-3.9

4.0-4.1

4.2-4.3

4.4-4.5

4.6-4.7

4.8-4.9

5.0-5.1

5.2-5.3

5.4-5.5

Percent range

NOTE: Definitions of variables are in the general note to table 1.

Exhibit 4: GDP Growth Projections of FOMC Participants for 2009 to 2011 and over the Longer Run

January 27–28, 2009 257 of 267Authorized for Public Release

2

4

6

8

10

12

Number of participants

Figure 2.B. Distribution of participants’ projections for the unemployment rate, 2009–11 and over the longer run

2009

October projections

4.4-4.5

4.6-4.7

4.8-4.9

5.0-5.1

5.2-5.3

5.4-5.5

5.6-5.7

5.8-5.9

6.0-6.1

6.2-6.3

6.4-6.5

6.6-6.7

6.8-6.9

7.0-7.1

7.2-7.3

7.4-7.5

7.6-7.7

7.8-7.9

8.0-8.1

8.2-8.3

8.4-8.5

8.6-8.7

8.8-8.9

9.0-9.1

9.2-9.3

Percent range

January projections

2

4

6

8

10

12

Number of participants

2010

4.4-4.5

4.6-4.7

4.8-4.9

5.0-5.1

5.2-5.3

5.4-5.5

5.6-5.7

5.8-5.9

6.0-6.1

6.2-6.3

6.4-6.5

6.6-6.7

6.8-6.9

7.0-7.1

7.2-7.3

7.4-7.5

7.6-7.7

7.8-7.9

8.0-8.1

8.2-8.3

8.4-8.5

8.6-8.7

8.8-8.9

9.0-9.1

9.2-9.3

Percent range

2

4

6

8

10

12

Number of participants

2011

4.4-4.5

4.6-4.7

4.8-4.9

5.0-5.1

5.2-5.3

5.4-5.5

5.6-5.7

5.8-5.9

6.0-6.1

6.2-6.3

6.4-6.5

6.6-6.7

6.8-6.9

7.0-7.1

7.2-7.3

7.4-7.5

7.6-7.7

7.8-7.9

8.0-8.1

8.2-8.3

8.4-8.5

8.6-8.7

8.8-8.9

9.0-9.1

9.2-9.3

Percent range

2

4

6

8

10

12

Number of participants

Longer Run

4.4-4.5

4.6-4.7

4.8-4.9

5.0-5.1

5.2-5.3

5.4-5.5

5.6-5.7

5.8-5.9

6.0-6.1

6.2-6.3

6.4-6.5

6.6-6.7

6.8-6.9

7.0-7.1

7.2-7.3

7.4-7.5

7.6-7.7

7.8-7.9

8.0-8.1

8.2-8.3

8.4-8.5

8.6-8.7

8.8-8.9

9.0-9.1

9.2-9.3

Percent range

NOTE: Definitions of variables are in the general note to table 1.

Exhibit 5: Unemployment Projections of FOMC Participants for 2009 to 2011 and over the Longer Run

January 27–28, 2009 258 of 267Authorized for Public Release

2

4

6

8

10

12

Number of participants

Figure 2.C. Distribution of participants’ projections for PCE inflation, 2009–11 and over the longer run

2009

October projections

-0.5--0.4

-0.3--0.2

-0.1-0.0

0.1-0.2

0.3-0.4

0.5-0.6

0.7-0.8

0.9-1.0

1.1-1.2

1.3-1.4

1.5-1.6

1.7-1.8

1.9-2.0

2.1-2.2

Percent range

January projections

2

4

6

8

10

12

Number of participants

2010

-0.5--0.4

-0.3--0.2

-0.1-0.0

0.1-0.2

0.3-0.4

0.5-0.6

0.7-0.8

0.9-1.0

1.1-1.2

1.3-1.4

1.5-1.6

1.7-1.8

1.9-2.0

2.1-2.2

Percent range

2

4

6

8

10

12

Number of participants

2011

-0.5--0.4

-0.3--0.2

-0.1-0.0

0.1-0.2

0.3-0.4

0.5-0.6

0.7-0.8

0.9-1.0

1.1-1.2

1.3-1.4

1.5-1.6

1.7-1.8

1.9-2.0

2.1-2.2

Percent range

2

4

6

8

10

12

Number of participants

Longer Run

-0.5--0.4

-0.3--0.2

-0.1-0.0

0.1-0.2

0.3-0.4

0.5-0.6

0.7-0.8

0.9-1.0

1.1-1.2

1.3-1.4

1.5-1.6

1.7-1.8

1.9-2.0

2.1-2.2

Percent range

NOTE: Definitions of variables are in the general note to table 1.

Exhibit 6: PCE Inflation Projections of FOMC Participants for 2009 to 2011 and over the Longer Run

January 27–28, 2009 259 of 267Authorized for Public Release

2

4

6

8

10

12

Number of participants

Figure 2.D. Distribution of participants’ projections for core PCE inflation, 2009–11 and over the longer run

2009

October projections

-0.1-0.0

0.1-0.2

0.3-0.4

0.5-0.6

0.7-0.8

0.9-1.0

1.1-1.2

1.3-1.4

1.5-1.6

1.7-1.8

1.9-2.0

2.1-2.2

Percent range

January projections

2

4

6

8

10

12

Number of participants

2010

-0.1-0.0

0.1-0.2

0.3-0.4

0.5-0.6

0.7-0.8

0.9-1.0

1.1-1.2

1.3-1.4

1.5-1.6

1.7-1.8

1.9-2.0

2.1-2.2

Percent range

2

4

6

8

10

12

Number of participants

2011

-0.1-0.0

0.1-0.2

0.3-0.4

0.5-0.6

0.7-0.8

0.9-1.0

1.1-1.2

1.3-1.4

1.5-1.6

1.7-1.8

1.9-2.0

2.1-2.2

Percent range

NOTE: Definitions of variables are in the general note to table 1.

Exhibit 7: Core PCE Inflation Projections of FOMC Participants for 2009 to 2011

January 27–28, 2009 260 of 267Authorized for Public Release

Appendix 4: Materials used by Mr. Madigan

January 27–28, 2009 261 of 267Authorized for Public Release

Class I FOMC – Restricted Controlled (FR)

Material for FOMC Briefing on Monetary Policy Alternatives Brian Madigan January 27-28, 2009

January 27–28, 2009 262 of 267Authorized for Public Release

Exhibit 1 Unconventional Policy Tools

1. Policy communications • About the federal funds rate

o Quantitative expectations o Qualitative expectations o Conditional expectations

• About other policy tools o Amounts and time frame

• About inflation outlook and objectives o Explicit numerical inflation objective o Longer-term projections o Express concern about undesirably low inflation

2. Credit policies

• Supporting or substituting for dysfunctional markets 3. Transactions under open market authority

• Swap arrangements • MBS purchases • Treasury purchases

January 27–28, 2009 263 of 267Authorized for Public Release

Alternative A 1. The Federal Open Market Committee decided today to keep its target range for the federal funds rate at 0 to 1/4 percent. The Committee continues to anticipate that economic conditions are likely to warrant exceptionally low levels of the federal funds rate for some time. 2. Information received since the Committee met in December suggests that the economy has weakened somewhat more than anticipated. Industrial production, housing starts, and employment have declined steeply, as consumers and businesses have cut back spending. Furthermore, global demand appears to be slowing significantly. Conditions in some financial markets have improved, in part reflecting government efforts to provide liquidity and strengthen financial institutions; nevertheless, credit conditions for households and firms remain extremely tight. The Committee anticipates that a gradual recovery in economic activity will begin later this year, but the downside risks to that outlook are sizable significant. 3. In light of the declines in the prices of energy and other commodities in recent months and the prospects for an extended period of economic slack, the Committee expects that inflation pressures will remain subdued. Moreover, the Committee sees some risk that inflation could persist for a time below rates that best foster economic growth and price stability in the longer term. 4. The Federal Reserve will employ all available tools to promote the resumption of sustainable economic growth and to preserve price stability. The focus of the Committee’s policy is to support the functioning of financial markets and stimulate the economy through open market operations and other measures that are likely to keep the size of the Federal Reserve's balance sheet at a high level. [Alt. 1: To provide further support to activity in housing markets, the Committee decided to expand its purchases of agency mortgage-backed securities to $750 billion this year from its previously announced total of $500 billion. The Committee anticipates completing these purchases by the end of the third quarter. The Committee also is prepared to purchase longer-term Treasury securities as needed to improve overall financial conditions.] [Alt. 2: To help improve overall financial conditions, the Committee decided to purchase up to $250 billion of longer-term Treasury securities this year. The Federal Reserve continues to purchase large quantities of agency debt and mortgage-backed securities to provide support to the mortgage and housing markets, and it stands ready to expand such purchases as conditions warrant.] Next month, the Federal Reserve will implement the Term Asset-Backed Securities Loan Facility to facilitate the extension of credit to households and small businesses. The Committee will continue to monitor carefully the size and composition of the Federal Reserve’s balance sheet in light of evolving financial market developments and to assess whether expansions of or modifications to lending facilities would serve to further support credit markets and economic activity and help to preserve price stability.

January 27–28, 2009 264 of 267Authorized for Public Release

Alternative B 1. The Federal Open Market Committee decided today to keep its target range for the federal funds rate at 0 to 1/4 percent. The Committee continues to anticipate that economic conditions are likely to warrant exceptionally low levels of the federal funds rate for some time. 2. Information received since the Committee met in December suggests that the outlook for the economy remains weak. Industrial production, housing starts, and employment have continued to decline steeply, as consumers and businesses have cut back spending. Furthermore, global demand appears to be slowing significantly. Conditions in some financial markets have improved, in part reflecting government efforts to provide liquidity and strengthen financial institutions; nevertheless, credit conditions for households and firms remain extremely tight. The Committee anticipates that a gradual recovery in economic activity will begin later this year, but the downside risks to that outlook are significant. 3. In light of the declines in the prices of energy and other commodities in recent months and the prospects for considerable economic slack, the Committee expects that inflation pressures will remain subdued in coming quarters. 4. The Federal Reserve will employ all available tools to promote the resumption of sustainable economic growth and to preserve price stability. The focus of the Committee’s policy is to support the functioning of financial markets and stimulate the economy through open market operations and other measures that are likely to keep the size of the Federal Reserve's balance sheet at a high level. The Federal Reserve continues to purchase large quantities of agency debt and mortgage-backed securities to provide support to the mortgage and housing markets, and it stands ready to expand the quantity of such purchases and the duration of the purchase program as conditions warrant. The Committee also is prepared to purchase longer-term Treasury securities as needed to improve if evolving circumstances indicate that such transactions would be particularly effective in improving conditions in private credit markets. Next month, the Federal Reserve will implement the Term Asset-Backed Securities Loan Facility to facilitate the extension of credit to households and small businesses. The Committee will continue to monitor carefully the size and composition of the Federal Reserve’s balance sheet in light of evolving financial market developments and to assess whether expansions of or modifications to lending facilities would serve to further support credit markets and economic activity and help to preserve price stability.

January 27–28, 2009 265 of 267Authorized for Public Release

Alternative C 1. The Federal Open Market Committee decided today to keep its target range for the federal funds rate at 0 to 1/4 percent. The Committee continues to anticipate that economic conditions are likely to warrant exceptionally low levels of the federal funds rate for some time. 2. Information received since the Committee met in December suggests that the outlook for the economy remains weak. Industrial production, housing starts, and employment have continued to decline steeply, as consumers and businesses have cut back spending. Conditions in some financial markets have improved, in part reflecting government efforts to provide liquidity and strengthen financial institutions; nevertheless, credit conditions for households and firms remain tight. The Committee anticipates that a recovery in economic activity will begin later this year, supported in part by additional fiscal measures and the monetary and liquidity policies already in place. 3. The declines in the prices of energy and other commodities in recent months have significantly reduced overall price inflation. With economic slack likely to persist, the Committee expects that both overall and core consumer price inflation will remain low. 4. The Federal Reserve will employ all available tools to promote the resumption of sustainable economic growth and to preserve price stability. The focus of the Committee’s policy is to support the functioning of financial markets and stimulate the economy through open market operations and other measures that are likely to keep the size of the Federal Reserve's balance sheet at a high level. The Federal Reserve continues to purchase large quantities of agency debt and mortgage-backed securities to provide support to the mortgage and housing markets. Next month, the Federal Reserve will implement the Term Asset-Backed Securities Loan Facility to facilitate the extension of credit to households and small businesses. The Committee will continue to monitor carefully the size and composition of the Federal Reserve’s balance sheet in light of evolving financial market developments.

January 27–28, 2009 266 of 267Authorized for Public Release

December FOMC Statement The Federal Open Market Committee decided today to establish a target range for the federal funds rate of 0 to 1/4 percent. Since the Committee's last meeting, labor market conditions have deteriorated, and the available data indicate that consumer spending, business investment, and industrial production have declined. Financial markets remain quite strained and credit conditions tight. Overall, the outlook for economic activity has weakened further. Meanwhile, inflationary pressures have diminished appreciably. In light of the declines in the prices of energy and other commodities and the weaker prospects for economic activity, the Committee expects inflation to moderate further in coming quarters. The Federal Reserve will employ all available tools to promote the resumption of sustainable economic growth and to preserve price stability. In particular, the Committee anticipates that weak economic conditions are likely to warrant exceptionally low levels of the federal funds rate for some time. The focus of the Committee's policy going forward will be to support the functioning of financial markets and stimulate the economy through open market operations and other measures that sustain the size of the Federal Reserve's balance sheet at a high level. As previously announced, over the next few quarters the Federal Reserve will purchase large quantities of agency debt and mortgage backed securities to provide support to the mortgage and housing markets, and it stands ready to expand its purchases of agency debt and mortgage-backed securities as conditions warrant. The Committee is also evaluating the potential benefits of purchasing longer-term Treasury securities. Early next year, the Federal Reserve will also implement the Term Asset-Backed Securities Loan Facility to facilitate the extension of credit to households and small businesses. The Federal Reserve will continue to consider ways of using its balance sheet to further support credit markets and economic activity.

January 27–28, 2009 267 of 267Authorized for Public Release