January 18, 2016 Buy Godrej Industries - LKP Securities Ltd. · January 18, 2016 Buy Godrej...

16

Yashas Bhat [email protected] +91 22 6635 1220 January 18, 2016 Buy Godrej Industries Holding Company Initiating Coverage A conglomerate of market leaders Godrej Industries Limited (GIL) is one of the holding companies of the 119 year old Godrej group. It holds ~ 23.8% in Godrej Consumer Products (GCPL), ~56.7% in Godrej Properties (GPL), ~60.8% of Godrej Agrovet (GAVL) and 100% of Natures Basket (NBL). It also has its own oleochemical business, manufacturing and marketing over 100 chemicals for use in more than 24 industries. This consumer centric conglomerate has a significant exposure to emerging economies in Asia, Africa and Latin America either directly with its oleochemicals business with exports to over 80 countries or indirectly through its associates and subsidiaries. Group philosophy, brand moat, execution excellence to support consistent wealth creation The Godrej group practices the EVA philosophy, entering into those businesses where they believe they can achieve sustainable leading positions. We believe that a robust management, strong brand equity, consistent innovation and execution excellence would help Godrej to consistently create wealth for its stakeholders. Value unlocking in GAVL to be a potential upside trigger GAVL is a diversified agri-business with interests in animal feeds, agri-inputs, palm oil, poultry processing and value added foods. It is also looking to step up its expansion efforts with its recent acquisitions of Creamline Dairy and Astec Lifesciences. GAVL’s possible listing is expected to unlock value, offering a potential upside trigger. Exposure to emerging FMCG markets with GCPL stake GCPL follows a 3x3 strategy of strengthening presence in Asia, Latin America and Africa across hair care, personal wash and home care segments. A deeper focus on premiumisation of product offerings as well as widening its reach in underpenetrated rural markets is expected to help GCPL in continual growth. Unique business model, brand strength to help GPL sustain growth With a unique asset light business model, right mix of industry veterans for partners, and strong brand equity, GPL has exhibited resilience in a flat real estate market as seen in its BKC commercial asset deal and sales of 300 flats in a week in Vikhroli. Company Valuation (₹ mn) GIL Stake (%) Holding Company Discount Total (₹. mn) Per share (₹.) GCPL 4,93,773 24% 23% 91,076 271 GPL 69,830 57% 23% 30,685 91 GAVL 46,028 61% 0% 27,985 83 Oleochemicals 8,702 100% 0% 8,702 26 Others (NBL, Creamline, Astec) 5,746 100% 0% 5,746 17 Enterprise Value 6,24,079 1,64,194 489 Less: Debt -15,567 -46 Equity Value 1,48,627 442 Stock Data Current Market Price (₹) 343 Target Price (₹) 442 Potential upside (%) 29 Market Cap (₹ bn) 115 52-Week Range (₹) 412 / 286 Avg Daily Trading Value last 6 mts(₹.mn) 136 Reuters GODI.NS Bloomberg GDSP:IN BSE / NSE Code 500164 / GODREJIND Derivatives (F&O) Market Lot 1300 Shareholding Pattern Relative Price Performance One Year Indexed (%) 1 M 3 M 12 M GIL ( Absolute) -2% -3% 15% Nifty Relative 2% 6% 27% GCPL ( Absolute) -6% 1% 16% Nifty Relative -2% 10% 28% GPL ( Absolute) -5% -8% 20% Nifty Relative -2% 1% 32% Promoter 75% FII 13% DII 3% Others 9% 80 90 100 110 120 130 140 Jan-15 May-15 Sep-15 Jan-16 Godrej Industries Ltd. NIFTY 50

Transcript of January 18, 2016 Buy Godrej Industries - LKP Securities Ltd. · January 18, 2016 Buy Godrej...

Yashas Bhat

+91 22 6635 1220

January 18, 2016

Buy Godrej Industries Holding Company Initiating Coverage

A conglomerate of market leaders

Godrej Industries Limited (GIL) is one of the holding companies of the 119

year old Godrej group. It holds ~ 23.8% in Godrej Consumer Products (GCPL),

~56.7% in Godrej Properties (GPL), ~60.8% of Godrej Agrovet (GAVL) and

100% of Natures Basket (NBL). It also has its own oleochemical business,

manufacturing and marketing over 100 chemicals for use in more than 24

industries. This consumer centric conglomerate has a significant exposure to

emerging economies in Asia, Africa and Latin America either directly with its

oleochemicals business with exports to over 80 countries or indirectly

through its associates and subsidiaries.

Group philosophy, brand moat, execution excellence to support

consistent wealth creation

The Godrej group practices the EVA philosophy, entering into those businesses

where they believe they can achieve sustainable leading positions. We believe that

a robust management, strong brand equity, consistent innovation and execution

excellence would help Godrej to consistently create wealth for its stakeholders.

Value unlocking in GAVL to be a potential upside trigger

GAVL is a diversified agri-business with interests in animal feeds, agri-inputs, palm

oil, poultry processing and value added foods. It is also looking to step up its

expansion efforts with its recent acquisitions of Creamline Dairy and Astec

Lifesciences. GAVL’s possible listing is expected to unlock value, offering a potential

upside trigger.

Exposure to emerging FMCG markets with GCPL stake

GCPL follows a 3x3 strategy of strengthening presence in Asia, Latin America and

Africa across hair care, personal wash and home care segments. A deeper focus on

premiumisation of product offerings as well as widening its reach in underpenetrated

rural markets is expected to help GCPL in continual growth.

Unique business model, brand strength to help GPL sustain growth

With a unique asset light business model, right mix of industry veterans for partners,

and strong brand equity, GPL has exhibited resilience in a flat real estate market as

seen in its BKC commercial asset deal and sales of 300 flats in a week in Vikhroli.

Company Valuation

(₹ mn) GIL Stake

(%)

Holding Company Discount

Total (₹. mn)

Per share (₹.)

GCPL 4,93,773 24% 23% 91,076 271

GPL 69,830 57% 23% 30,685 91

GAVL 46,028 61% 0% 27,985 83

Oleochemicals 8,702 100% 0% 8,702 26

Others (NBL, Creamline, Astec) 5,746 100% 0% 5,746 17

Enterprise Value 6,24,079 1,64,194 489

Less: Debt

-15,567 -46

Equity Value

1,48,627 442

Stock Data

Current Market Price (₹) 343

Target Price (₹) 442

Potential upside (%) 29

Market Cap (₹ bn) 115

52-Week Range (₹) 412 / 286

Avg Daily Trading Value last 6 mts(₹.mn) 136

Reuters GODI.NS

Bloomberg GDSP:IN

BSE / NSE Code 500164 / GODREJIND

Derivatives (F&O) Market Lot 1300

Shareholding Pattern

Relative Price Performance

One Year Indexed

(%) 1 M 3 M 12 M

GIL ( Absolute) -2% -3% 15%

Nifty Relative 2% 6% 27%

GCPL ( Absolute) -6% 1% 16%

Nifty Relative -2% 10% 28%

GPL ( Absolute) -5% -8% 20%

Nifty Relative -2% 1% 32%

Promoter 75%

FII 13%

DII 3%

Others 9%

80

90

100

110

120

130

140

Jan-15 May-15 Sep-15 Jan-16

Godrej Industries Ltd. NIFTY 50

Godrej Industries

LKP Research 2

Company Profile

GIL is one of the holding companies of the 119 year old Godrej group with a majority

stake in GPL, GAVL, NBL and a significant minority stake in GCPL. It also has its

own oleochemical business, manufacturing and marketing over 100 chemicals for

use in more than 24 industries. GIL, the residual of a demerger in 2001 which led to

the formation of what is now GCPL, is primarily levered to the consumption story of

emerging markets through its associates and subsidiaries. The Godrej group has

shown a significant appetite for chasing growth through the inorganic route both in

India and overseas, especially over the past decade, which has helped GIL attain

exposure in different product categories and geographies. Thus the combination of

EVA philosophy with diligent expansion has led to the Godrej name being cemented

as one of the most recognizable and trusted brands in India.

Holding Structure of GIL

Source: Company, LKP Research

GCPL

(23.8%)

GPL

(56.7%)

GAVL

(60.8%)

(Unlisted)

NBL

(100.0%)

(Unlisted)

Chemical Division

(Standalone)

Godrej Industries

LKP Research 3

International operations firming up

and a renewed rural focus to drive

growth in GCPL

Investment Argument

GCPL – Emerging markets FMCG play

GCPL, in which GIL holds a ~ 23.8 % stake, is the stalwart of the Godrej group with

interests in personal care, hair care and home care. Starting out as the manufacturer

of the world’s first animal fat free soap in 1918, GCPL is currently the market leader

in hair color, household insecticides and liquid detergents and 2nd in soaps in India.

This ~ ₹ 84 bn revenue company follows a 3x3 strategy of strengthening presence in

3 key emerging markets of Asia, Latin America and Africa across 3 segments of hair

care, personal wash and home care. It has a perennial focus on innovation as

illustrated by its recognition as the highest ranked Indian company in the Forbes' list

of “The World's 100 Most Innovative Growth Companies-2015” at rank 24. Over the

period of its existence, the company has demonstrated its ability to identify niche

markets and capture a significant market share both in India and overseas through

green-field and brown-field investments.

Product wise market leadership of GCPL across geographies

Source: Company, LKP Research

Good corporate culture translating to great business

Source: Company, LKP Research

Godrej Industries

LKP Research 4

Indian Brands of GCPL

Source: Company, LKP Research

Godrej Industries

LKP Research 5

From its humble roots in 1918, GCPL has grown to the 2nd largest soap

manufacturer behind HUL with its marquee No. 1 and Cinthol brands. It has

expanded its offerings by making a foray into the ~ ₹ 16 bn face wash segment

on the back of its No. 1 Brand. It has also introduced the face wash in a sachet

format which is a first in India. We believe that this face wash foray would auger

well for GCPL as it tries to establish itself in a market that has penetration levels

as low as ~ 13% -14%.

GCPL has ~ 50% of market share in terms of value in the Indian household

insecticides market with its Good Knight and Hit brands. GCPL compliments

strong brand equity of its brands with consistent innovation and R&D such as

the introduction of Good Knight Fast Card priced at ₹ 1 in FY15 which grew into

a ~ ₹ 1 bn brand within 11 months of its introduction. Neem Activ+ Low Smoke

Coil and Good knight Xpress liquid vaporizer has also been well received by

consumers.

It is also the market leader in the ~ ₹ 29 bn Indian hair color industry with

product offerings both in powdered and crème variants. Its flagship Expert

brand has a loyal consumer base of over ~ 40 mn users and available in ~ 2.3

mn outlets across India. Its other brands like Nupur and Renew also are doing

well in their respective product categories.

It has demonstrated a deeper focus in the underpenetrated rural market with its

One Rural and E-Cube pilot projects to accelerate growth rates going forward.

One Rural includes setting up of a separate rural organization structure and

focuses on demand generation and demand fulfilment. E-Cube pertains to

extracting more demand from rural areas, expanding distribution in urban areas

and effectively implementing go-to market strategy. Currently, only ~ 15% of its

consolidated revenues come from rural markets, and thus we believe that

further rural penetration would offer a potential upside trigger.

With significant overseas acquisitions over the past decade, GCPL has placed

itself as an emerging markets FMCG player with a strategic presence in Asia,

Africa and Latin America. It has diligently acquired market leaders and

significant players in niche foreign markets, deriving synergetic and cross

pollination benefits like the introduction of Crème hair color sachet in India

whose technology was brought over from its Argentina business. We believe

that this geographic exposure and synergies would help GCPL effectively

participate in the emerging markets FMCG growth story.

GCPL enjoys strong brand equity, strategic presence in major emerging markets,

and leading positions in each of the markets and product categories it operates in.

With its international operations firming up and a renewed focus on domestic rural

market, we expect GCPL to exhibit a comfortable pace of growth. We estimate

GCPL to be valued at ~ 35XFY17E earnings at ~ ₹1,450 per share which takes GILs

~ 23.8% stake at ~ ₹ 117.4 bn.

Godrej Industries

LKP Research 6

GCPL- A true emerging markets FMCG player

Source: Company, LKP Research

Godrej Industries

LKP Research 7

Quarterly trends in GCPL’s top-line and bottom-line

Source: Company, LKP Research

Financial performance of GCPL as on FY15

Source: Company, LKP Research

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

17,000

18,000

19,000

20,000

21,000

22,000

23,000

Q3F

Y14

Q4F

Y14

Q1F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Operational Revenues (₹ mn) PAT Margin (%)

Personal Wash 33%

Hair Care 13%

Home Care 48%

Others 6%

Indonesia 37%

Africa 30%

LatAm 16%

UK 13%

Others 4%

Raw Materials

54%

Employee Benefits

11%

Ad, Publicity

and Sales Promotion

17%

Others 18%

Product wise break-up of domestic sales Geographical break-up of International sales

Break up of Costs

Godrej Industries

LKP Research 8

A unique joint development business

model, strong brand, right mix of

industry veterans and marketing

strength to aid growth

GCPL Financials

YE Mar (₹ Mn) FY14 FY15 FY16E FY17E

Total Revenues 76,024 82,764 90,626 1,00,958

Materials Cost 35,547 38,415 41,987 46,743

Employee Benefits 7,424 7,770 8,158 8,566

Ad, Publicity and Sales Promotion 11,065 12,066 13,005 14,057

Selling & Dist. Expenses 1,324 1,373 1,446 1,506

Power and Fuel 1,032 1,099 1,178 1,312

Freight 2,444 2,539 2,719 3,029

Others 5,620 5,849 6,163 6,865

EBITDA 11,568 13,653 15,971 18,879

EBITDA Margin (%) 15.2% 16.5% 17.6% 18.7%

Depreciation 819 908 931 928

Other Income 627 915 943 1020

EBIT 11,376 13,660 15,983 18,971

EBIT Margin (%) 14.8% 16.3% 17.5% 18.6%

Interest 1074 1002 1017 1025

PBT 10,302 12,659 14,965 17,946

PBT Margin (%) 13.4% 15.1% 16.3% 17.6%

Exceptional Items -6 -172 - -

Tax 2,104 2,723 3,255 3,903

PAT 8,193 9,764 11,710 14,042

PAT Magin (%) 10.7% 11.7% 12.8% 13.8%

Share of prof in ass comp -0.5 0.4 - -

MI -595 -694 -855 -1025

PAT 7,597.3 9,071.2 10,855.5 13,017.2

PAT Margin (%) 9.9% 10.8% 11.9% 12.8%

EPS 24.1 28.7 34.4 41.3

PE 51.3 42.8 35.7 29.7

GPL – Unique business model, brand strength

Established in 1990, GPL is the real estate arm of the Godrej group where GIL

would hold a majority ~ 56.7 % stake. It is a pan India real estate player with an

estimated developable area of ~ 109.4 mn sq ft as on Q2FY16 and a focus on tier I

and tier II cities. It follows a unique joint development business model where it either

enters into a profit/ revenue/ area sharing (PRAS) or development manager (DM)

agreement with land owners. This unique business model keeps GPL asset light and

capital efficient enabling it to be lower levered in comparison to its peers which

resulted in a moderate debt equity ratio of ~ 1.1 as on Q2FY16.

Brief snapshot of GPL

Source: Company, LKP Research

Ahmedabad 21%

Mumbai 18%

Pune 17%

Bangalore 12%

Hyderabad 9%

NCR 7%

Kolkata 7%

Others 9%

PRAS 70%

DM 21%

Owned Land 9%

Focus on capital efficient projects Target markets -Tier 1 and 2 cities

Godrej Industries

LKP Research 9

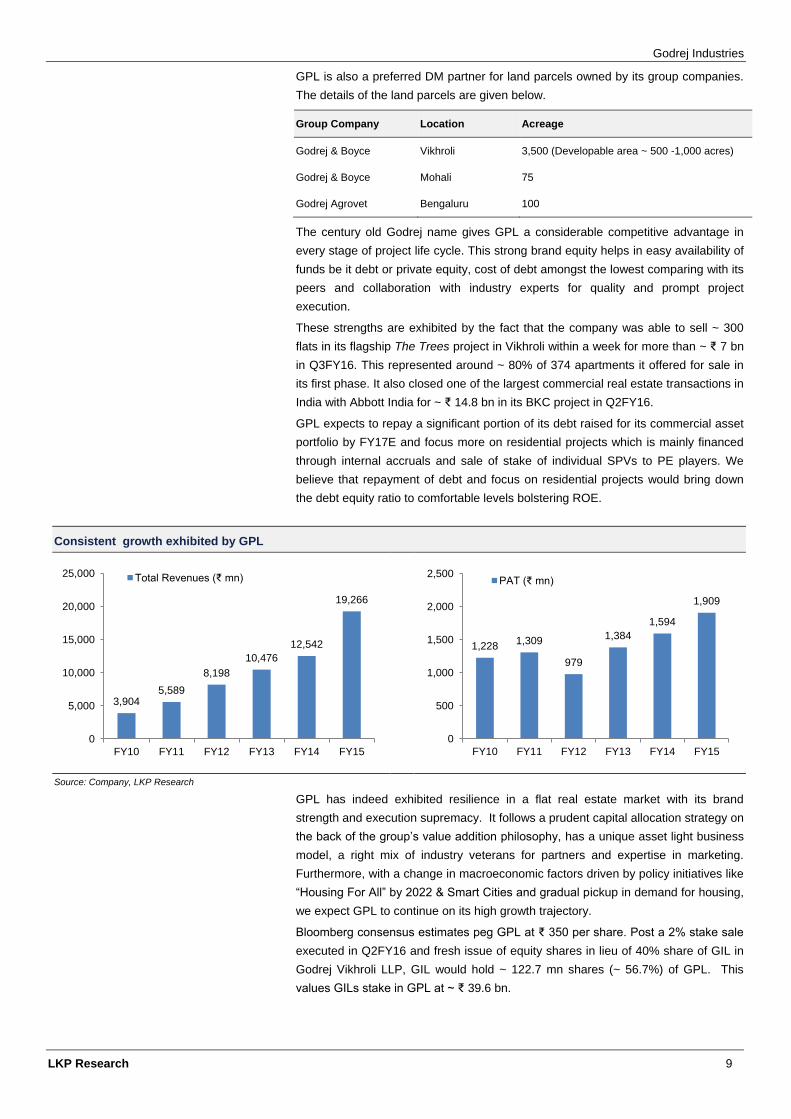

GPL is also a preferred DM partner for land parcels owned by its group companies.

The details of the land parcels are given below.

Group Company Location Acreage

Godrej & Boyce Vikhroli 3,500 (Developable area ~ 500 -1,000 acres)

Godrej & Boyce Mohali 75

Godrej Agrovet Bengaluru 100

The century old Godrej name gives GPL a considerable competitive advantage in

every stage of project life cycle. This strong brand equity helps in easy availability of

funds be it debt or private equity, cost of debt amongst the lowest comparing with its

peers and collaboration with industry experts for quality and prompt project

execution.

These strengths are exhibited by the fact that the company was able to sell ~ 300

flats in its flagship The Trees project in Vikhroli within a week for more than ~ ₹ 7 bn

in Q3FY16. This represented around ~ 80% of 374 apartments it offered for sale in

its first phase. It also closed one of the largest commercial real estate transactions in

India with Abbott India for ~ ₹ 14.8 bn in its BKC project in Q2FY16.

GPL expects to repay a significant portion of its debt raised for its commercial asset

portfolio by FY17E and focus more on residential projects which is mainly financed

through internal accruals and sale of stake of individual SPVs to PE players. We

believe that repayment of debt and focus on residential projects would bring down

the debt equity ratio to comfortable levels bolstering ROE.

Consistent growth exhibited by GPL

Source: Company, LKP Research

GPL has indeed exhibited resilience in a flat real estate market with its brand

strength and execution supremacy. It follows a prudent capital allocation strategy on

the back of the group’s value addition philosophy, has a unique asset light business

model, a right mix of industry veterans for partners and expertise in marketing.

Furthermore, with a change in macroeconomic factors driven by policy initiatives like

“Housing For All” by 2022 & Smart Cities and gradual pickup in demand for housing,

we expect GPL to continue on its high growth trajectory.

Bloomberg consensus estimates peg GPL at ₹ 350 per share. Post a 2% stake sale

executed in Q2FY16 and fresh issue of equity shares in lieu of 40% share of GIL in

Godrej Vikhroli LLP, GIL would hold ~ 122.7 mn shares (~ 56.7%) of GPL. This

values GILs stake in GPL at ~ ₹ 39.6 bn.

3,904 5,589

8,198

10,476

12,542

19,266

0

5,000

10,000

15,000

20,000

25,000

FY10 FY11 FY12 FY13 FY14 FY15

Total Revenues (₹ mn)

1,228 1,309

979

1,384

1,594

1,909

0

500

1,000

1,500

2,000

2,500

FY10 FY11 FY12 FY13 FY14 FY15

PAT (₹ mn)

Godrej Industries

LKP Research 10

Possible listing of GAVL would lead

to value unlocking thus offering a

potential upside trigger

GAVL - Potential value unlocking in a diversified agri-business

GAVL, where GIL holds ~ 60.8% stake, is a diversified agri-business company with

interests in animal feeds, agri-inputs, palm oil, poultry processing and value added

foods. The company is the largest commercial animal feeds manufacturer and seller

in India. It has cattle, poultry, fish and specialty feed categories in its product

portfolio and clocked feed sales volumes of over ~ 1.1 mn tonnes in FY15. It has ~

55,000 hectares of smallholder palm oil palm plantations over 7 states and

manufactures crude palm oil, palm kernel oil and palm kernel cake. It is also a niche

player in select agrochemicals like insecticides, fungicides, soil conditioners and

organic manure with a pan-India network of ~ 6,500 distributors. GAVL is in 2

strategic joint ventures that help leverage its core strengths of brand, R & D and

marketing expertise to gain a firm foothold in its target markets.

Feeds business: A substantial contributor to GAVLs top-line and bottom-line

Source: Company, LKP Research

Details of Joint Ventures of GAVL

Joint Venture Details

ACI Godrej Agrovet Amongst top 3 across all feed categories in Bangladesh.

Godrej Tyson Foods Processed poultry and other value added foods with Yummiez and So Good brands.

India’s animal feed industry, which is currently at ~ $15 bn, is poised to double and

touch ~ $30 bn in the next five years to cater to the growing protein requirements of

the country. With changing income levels and more people eating fish, meat and

chicken, there will be a higher requirement of processed dairy, aqua and poultry

products, which in turn will result in higher feed requirement. The demand for animal

protein and dairy products in India is estimated to increase the compound feed

consumption volumes by a stable CAGR of 8% to 28 mn tonnes by FY18E. This

gives organised feed players like GAVL a significant growth driver in the

underpenetrated feed industry, where only ~ 11 %, ~ 14 % and ~ 55% requirements

are met by the organised segment for compound feed, aqua feed and poultry feed

respectively.

Animal Feed

77.6%

Veg Oil 11.4%

Agri 10.7%

Others 0.3% Animal

Feed 55.4%

Veg Oil 19.6%

Agri 24.8%

Others -0.2%

Top-line Bottom-line

Godrej Industries

LKP Research 11

Sales volume breakup of GAVL

Source: Company, LKP Research

GAVL is also expanding diligently with strategic brown field acquisitions. It made a

foray into the dairy industry with an increase of its stake from ~ 26% to ~ 51% in

Creamline Dairy, a South India based dairy company, for ~ ₹ 1.5 bn. Creamline

Dairy owns the Jersey brand of milk and its derivatives and has a market presence

in Telangana, Andhra Pradesh, Tamil Nadu, Karnataka and Maharashtra. It also

operates dedicated Jersey milk parlors in South India. The company is expecting to

close FY16E with a top-line of ~ ₹ 10 bn and plans to double its revenues over the

next 3 - 4 years. We believe that this acquisition is a logical forward integration move

by GAVL, as Creamline would stand to benefit from the strong brand recall enjoyed

by Godrej Agrovet amongst dairy farmers on the back of its feeds business. We

estimate GAVLs stake in Creamline dairy to be ~ ₹ 3.1 bn.

GAVL is looking to strengthen its agri-inputs offerings with a majority ~ 52.3% stake

in Astec Lifesciences (ASL) for ~ ₹1.9 bn as on December 2015. ASL is a leading

manufacturer of triazole fungicides, herbicides and intermediaries mainly used in

pesticides, insecticides and pharmaceuticals. It has 2 production facilities in

Dombivali and Mahad, Maharashtra and has over 214 product registrations across

32 countries including 139 in India. It carries out contract manufacturing for global

giants like Syngenta, Nufarm, Dow, Biostadt, etc and has an impressive track record

of 100% client retention since its inception in 1994. Through its wholly owned

subsidiary Astec Crop Care Pvt. Ltd, ASL markets and distributes branded

agrochemical formulations in in Gujarat, Maharashtra, Karnataka Himachal Pradesh,

Punjab and Haryana. Its list of customers includes reputed multinational companies

in USA, Japan, Europe and Asia.

Brief financial snapshot of ASL

Impressive Growth both on top-line and bottom-line (₹ mn)

Source: Company, LKP Research

Cattle Feed 45%

Poultry 45%

Aqua Feed 10%

1,128

1,747

2,070

2,665

0

500

1,000

1,500

2,000

2,500

3,000

FY12 FY13 FY14 FY15

Revenues from operations

15

59

87

148

0

20

40

60

80

100

120

140

160

FY12 FY13 FY14 FY15

PAT

Godrej Industries

LKP Research 12

Sales Mix

Source: Company, LKP Research

We believe that the acquisition of Astec Lifesciences would further strengthen

GAVLs agrochemicals retail presence in the country. The agri input business will

also have access to the export market with Astec having registered in over 32

countries. GAVL’s holding is estimated to be ~ ₹ 2.5 bn.

GAVL has faced a slight decline on its top-line from ~ ₹ 2.17 bn to ~ ₹ 2.14 bn and

bottom-line from ~ ₹ 150 mn to ~ ₹ 146 bn in H1FY15 and H1FY16 respectively.

This is on account of 2 consecutive sub -par monsoons and a significant fall in

prices of agri-commodities, affecting its animal feeds, oil palm, agri inputs and seeds

businesses. But it has been able to adjust its strategy and deliver sustained earnings

despite a weak macroeconomic scenario.

We value GAVL at 20XFY17E earnings at ~ ₹83 per share to arrive at a valuation of

GILs ~ 60.8% stake at ~ ₹ 28 bn. A brief snapshot of GAVLs profitability is given

below.

₹ mn FY13 FY14 FY15 FY16E FY17E

Op. Revenues 28,526 32,388 34,651 34,224 38,057

Material Cost 22,687 25,292 26,397 25,891 28,372

Employee Expenses 1,020 1,231 1,282 1,371 1,454

Other Expenses 3,121 3,722 4,204 4,175 4,567

Op. Expenses 26,828 30,246 31,882 31,437 34,392

EBITDA 1,698 2,142 2,768 2,787 3,665

EBITDA % 6.0% 6.6% 8.0% 8.1% 9.6%

PAT 1,001 1,439 2,031 1,640 2,301

Institututional Sales

75%

CMO 16%

Branded Sales 9%

A 19%

B 12%

C 8%

D 8% E

7%

Others 46%

India 65%

Europe 22%

Americas 7%

Asia Pacific 5%

Others 1%

By Product

By Geography Share of top 5 clients

Godrej Industries

LKP Research 13

Better product mix, improved

procurement and energy efficiency to

auger well for the oleochemical

business

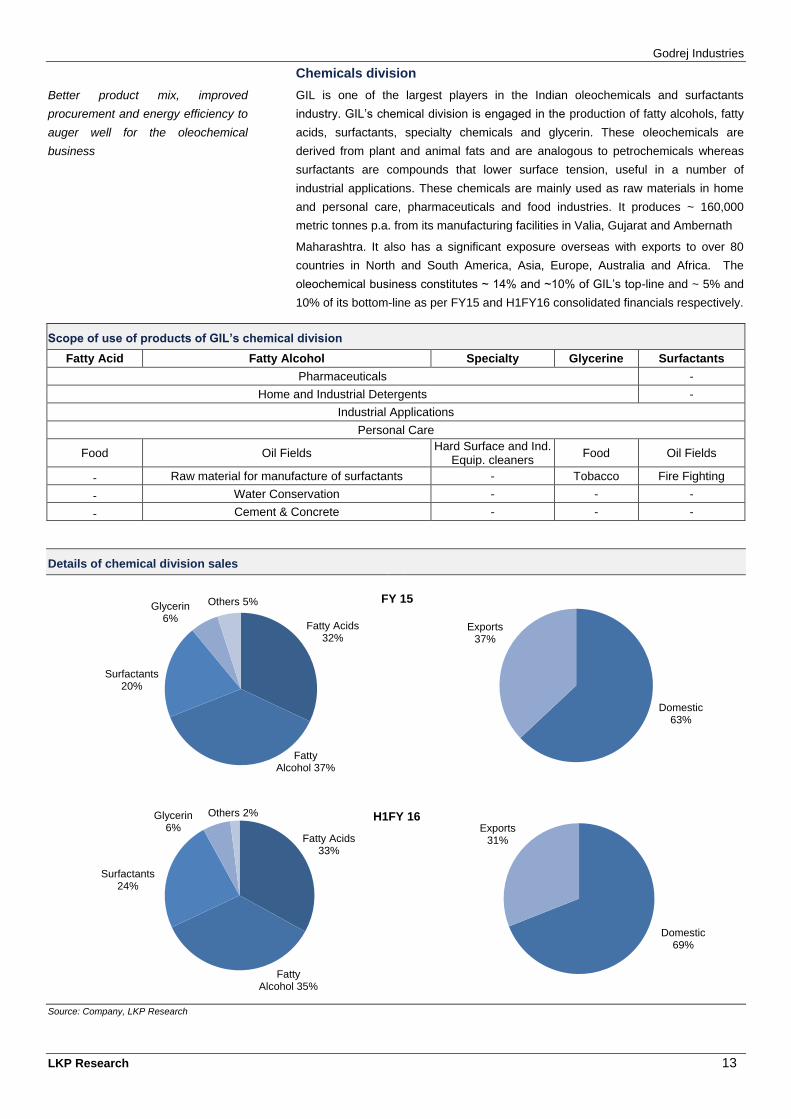

Chemicals division

GIL is one of the largest players in the Indian oleochemicals and surfactants

industry. GIL’s chemical division is engaged in the production of fatty alcohols, fatty

acids, surfactants, specialty chemicals and glycerin. These oleochemicals are

derived from plant and animal fats and are analogous to petrochemicals whereas

surfactants are compounds that lower surface tension, useful in a number of

industrial applications. These chemicals are mainly used as raw materials in home

and personal care, pharmaceuticals and food industries. It produces ~ 160,000

metric tonnes p.a. from its manufacturing facilities in Valia, Gujarat and Ambernath

Maharashtra. It also has a significant exposure overseas with exports to over 80

countries in North and South America, Asia, Europe, Australia and Africa. The

oleochemical business constitutes ~ 14% and ~10% of GIL’s top-line and ~ 5% and

10% of its bottom-line as per FY15 and H1FY16 consolidated financials respectively.

Scope of use of products of GIL’s chemical division

Fatty Acid Fatty Alcohol Specialty Glycerine Surfactants

Pharmaceuticals -

Home and Industrial Detergents -

Industrial Applications

Personal Care

Food Oil Fields Hard Surface and Ind.

Equip. cleaners Food Oil Fields

- Raw material for manufacture of surfactants - Tobacco Fire Fighting

- Water Conservation - - -

- Cement & Concrete - - -

Details of chemical division sales

Source: Company, LKP Research

Fatty Acids 32%

Fatty Alcohol 37%

Surfactants 20%

Glycerin 6%

Others 5%

Domestic 63%

Exports 37%

Fatty Acids 33%

Fatty Alcohol 35%

Surfactants 24%

Glycerin 6%

Others 2%

Domestic 69%

Exports 31%

FY 15

H1FY 16

Godrej Industries

LKP Research 14

Increasing acceptability of gourmet

and healthy foods, high street

locations of stores and online focus

to bode well for gourmet business

There was a decline witnessed in the division’s revenue from ~ ₹ 7.1 bn in H1FY15

to ~ ₹ 5.9 bn in H1FY16 which is largely attributable to benign commodity prices. In

spite of this, GIL managed to grow its PBIT by ~ 94% from ~ ₹ 290 mn to ~ ₹ 560

mn on account of better product mix, improved procurement and energy efficiency

efforts in both their factories.

GIL has been able to withstand the headwinds of weak commodity prices and

dramatically improve on its profitability with respect of its oleochemicals business.

We expect the chemicals division to earn an EBITDA of ~ ₹ 1.2 bn by FY17E. We

value the chemicals division at 7XFY17E EBITDA at ~ ₹ 8.7 bn.

NBL- A gourmet food retail play

Starting out in 2005 as a single fresh food store, NBL is now one of the largest

gourmet food retail chains. It has over 36 premium gourmet stores at high street

locations in over 5 metros of Delhi/NCR, Mumbai, Pune, Hyderabad and Bengaluru.

NBL- a leading player in the niche gourmet market

Source: Company, LKP Research

NBL has renewed its focus on building a robust online platform with a series of

moves since FY15. It acquired EkStop, a grocery e-store for ~ ₹ 350 mn in Feb-15

to spearhead its online gourmet ordering platform. It has partnered with online

marketplaces such as Snapdeal and Amazon to widen its reach. From stores and

online operations in five cities, the products are now available in ~ 125 cities across

the country including all metros, state capitals and major Tier 1 and 2 cities. Under

this, over ~ 10,000 products are available for delivery across close to 3,000+ pin

codes over a period of time.

We believe that NBL is at an inflection point with premium gourmet and healthy

foods finding increased acceptability of over the last half decade, strategic store

locations and a renewed online focus that can drive it to a high growth phase. We

value NBL at book value which stood at ~ ₹ 146 mn as on FY15.

Godrej Industries

LKP Research 15

Risks

India continues to face a tepid rural demand scenario on account of 2

consecutive deficit monsoons in FY15 and FY16. This may hamper GCPLs

efforts to gain a firm foothold in in this underpenetrated market in spite of new

rural-centric products launches. GAVL also faced significant headwinds in its

agribusiness on account of a below par monsoon. We believe a situation of

weak rural demand on account of monsoon deficiencies may serve as a

deterrent to the growth prospects of GCPL and GAVL.

The US dollar index has risen more than 20% since mid-2014 on the back of a

relatively robust US economy attracting investor flows from other regions. The

Federal Reserve's first increase in U.S. interest rates in a decade in December

and the prospect for further rises are expected to continue underpinning the

greenback going forward. GIL, through its subsidiaries and associates, has a

material exposure to emerging markets that are facing a significant downward

currency pressure. This exposes GIL to material forex risks.

A lot of volatility has been noticed with the commodities market worldwide, even

more so in agri-commodities. This would have a spill-over effect on various

businesses that GIL has exposure in, like soaps, oleochemicals, agri-inputs etc

leading to margin pressure.

Valuation and Outlook

Company Valuation

(₹ mn) GIL Stake

(%)

Holding Company Discount

Total (₹. mn)

Per share (₹.)

GCPL 4,93,773 24% 23% 91,076 271

GPL 69,830 57% 23% 30,685 91

GAVL 46,028 61% 0% 27,985 83

Oleochemicals 8,702 100% 0% 8,702 26

Others (NBL, Creamline, Astec) 5,746 100% 0% 5,746 17

Enterprise Value 6,24,079 1,64,194 489

Less: Debt

-15,567 -46

Equity Value

1,48,627 442

Godrej Industries

LKP Securites Ltd, 13th Floor, Raheja Center, Free Press Road, Nariman Point, Mumbai-400 021. Tel -91-22 - 66351234 Fax- 91-22-66351249. www.lkpsec.com

DISCLAIMERS AND DISCLOSURES

LKP Sec. ltd. (CIN-U67120MH1994PLC080039, www. Lkpsec.com) and its affiliates are a full-fledged, brokerage and financing group. LKP was established in

1992 and is one of India's leading brokerage and distribution house. LKP is a corporate trading member of Bombay Stock Exchange Limited (BSE), National

Stock Exchange of India Limited(NSE), MCX Stock Exchange Limited (MCX-SX).LKP along with its subsidiaries offers the most comprehensive avenues for

investments and is engaged in the businesses including stock broking (Institutional and retail), merchant banking, commodity broking, depository participant,

insurance broking and services rendered in connection with distribution of primary market issues and financial products like mutual funds etc.

LKP hereby declares that it has not defaulted with any stock exchange nor its activities were suspended by any stock exchange with whom it is registered in

last five years. However, SEBI and Stock Exchanges have conducted the routine inspection and based on their observations have issued advice letters or levied

minor penalty on LKP for certain operational deviations in ordinary/routine course of business. LKP has not been debarred from doing business by any Stock

Exchange / SEBI or any other authorities; nor has its certificate of registration been cancelled by SEBI at any point of time.

LKP offers research services to clients. The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal

views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related

to specific recommendations or views expressed in this report.

Other disclosures by LKP and its Research Analyst under SEBI (Research Analyst) Regulations, 2014 with reference to the subject company(s) covered in this

report-:

Research Analyst or his/her relative’s financial interest in the subject company. (NO)

LKP or its associates may have financial interest in the subject company.

LKP or its associates and Research Analyst or his/her relative’s does not have any material conflict of interest in the subject company. The research Analyst or

research entity (LKP) has not been engaged in market making activity for the subject company.

LKP or its associates may have actual/beneficial ownership of 1% or more securities of the subject company at the end of the month immediately preceding

the date of publication of Research Report.

Research Analyst or his/her relatives have actual/beneficial ownership of 1% or more securities of the subject company at the end of the month immediately

preceding the date of publication of Research Report: (NO)

LKP or its associates may have received any compensation including for investment banking or merchant banking or brokerage services from the subject

company in the past 12 months.

LKP or its associates may have received compensation for products or services other than investment banking or merchant banking or brokerage services from

the subject company in the past 12 months.

LKP or its associates may have received any compensation or other benefits from the Subject Company or third party in connection with the research report.

Subject Company may have been client of LKP or its associates during twelve months preceding the date of distribution of the research report and LKP may

have co-managed public offering of securities for the subject company in the past twelve months.

Research Analyst has served as officer, director or employee of the subject company: (NO)

LKP and/or its affiliates may seek investment banking or other business from the company or companies that are the subject of this material. Our salespeople,

traders, and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to

the opinions expressed herein, and our proprietary trading and investing businesses may make investment decisions that may be inconsistent with the

recommendations expressed herein.

In reviewing these materials, you should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest

including but not limited to those stated herein. Additionally, other important information regarding our relationships with the company or companies that

are the subject of this material is provided herein. This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or

resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or

regulation or which would subject LKP or its group companies to any registration or licensing requirement within such jurisdiction. Specifically, this document

does not constitute an offer to or solicitation to any U.S. person for the purchase or sale of any financial instrument or as an official confirmation of any

transaction to any U.S. person.

Unless otherwise stated, this message should not be construed as official confirmation of any transaction. No part of this document may be distributed in

Canada or used by private customers in United Kingdom.

All trademarks, service marks and logos used in this report are trademarks or registered trademarks of LKP or its Group Companies. The information contained

herein is not intended for publication or distribution or circulation in any manner whatsoever and any unauthorized reading, dissemination, distribution or

copying of this communication is prohibited unless otherwise expressly authorized. Please ensure that you have read “Risk Disclosure Document for Capital

Market and Derivatives Segments” as prescribed by Securities and Exchange Board of India before investing in Indian Securities Market. In so far as this report

includes current or historic information, it is believed to be reliable, although its accuracy and completeness cannot be guaranteed.

All material presented in this report, unless specifically indicated otherwise, is under copyright to LKP. None of the material, nor its content, nor any copy of it,

may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of LKP