It’s a Man’s World : Men’s Grooming Continues Robust...

58

IT’S A MAN’S WORLD : MEN’S GROOMING CONTINUES ROBUST PERFORMANCE August 2013

-

Upload

truongcong -

Category

Documents

-

view

214 -

download

0

Transcript of It’s a Man’s World : Men’s Grooming Continues Robust...

IT’S A MAN’S WORLD : MEN’S GROOMING CONTINUES ROBUST PERFORMANCE

August 2013

INTRODUCTION

INDUSTRY OVERVIEW

CATEGORY ANALYSIS

REGIONAL ANALYSIS

CHANNEL ANALYSIS

INNOVATION STRATEGIES

FUTURE PROSPECTS

© Euromonitor International PASSPORT 3 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

Disclaimer

Much of the information in this

briefing is of a statistical nature and,

while every attempt has been made

to ensure accuracy and reliability,

Euromonitor International cannot be

held responsible for omissions or

errors.

Figures in tables and analyses are

calculated from unrounded data and

may not sum. Analyses found in the

briefings may not totally reflect the

companies’ opinions, reader

discretion is advised.

Men’s grooming’s consistent

performance and resilience

during the recession has

brought the category to the

forefront of beauty companies’

strategies. While male

consumers in the West are

slowly adopting male-specific

products, in Asia Pacific, men

already have a regimented skin

care routine. As brand-owners

look to penetrate the market

further, Brazil and China are

becoming the next investment

markets to watch, with

deodorants and skin care

expected to fuel growth in the

future.

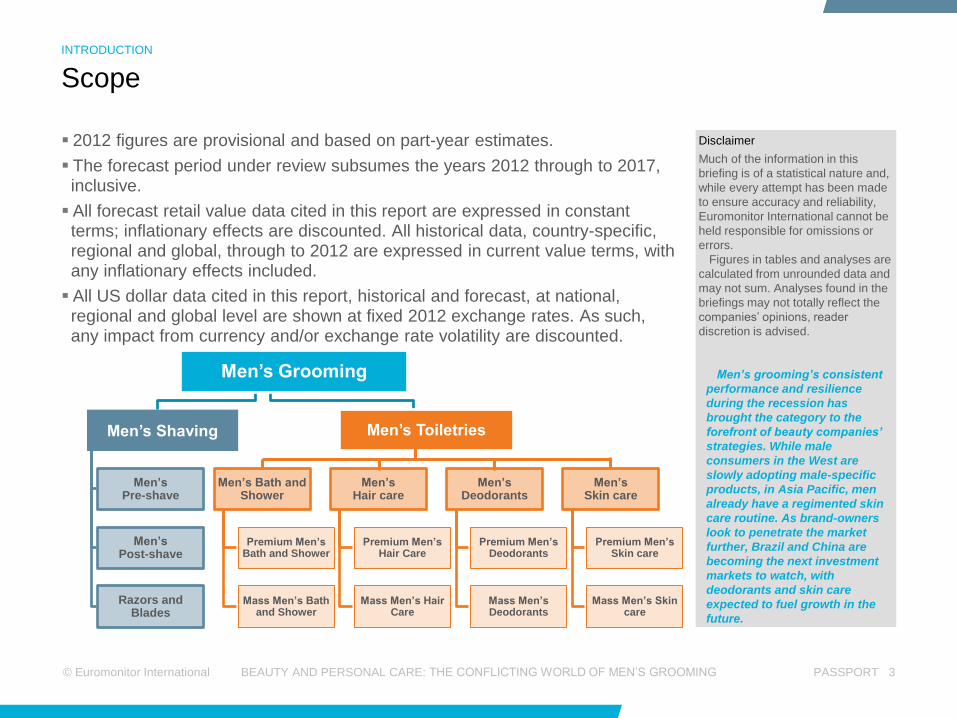

Scope

INTRODUCTION

2012 figures are provisional and based on part-year estimates.

The forecast period under review subsumes the years 2012 through to 2017, inclusive.

All forecast retail value data cited in this report are expressed in constant terms; inflationary effects are discounted. All historical data, country-specific, regional and global, through to 2012 are expressed in current value terms, with any inflationary effects included.

All US dollar data cited in this report, historical and forecast, at national, regional and global level are shown at fixed 2012 exchange rates. As such, any impact from currency and/or exchange rate volatility are discounted.

Men’s Grooming

Men’s Pre-shave

Men’s Post-shave

Razors and Blades

Men’s Toiletries

Men’s Bath and Shower

Premium Men’s Bath and Shower

Mass Men’s Bath and Shower

Men’s Hair care

Premium Men’s Hair Care

Mass Men’s Hair Care

Men’s Deodorants

Premium Men’s Deodorants

Mass Men’s Deodorants

Men’s Skin care

Premium Men’s Skin care

Mass Men’s Skin care

Men’s Shaving

© Euromonitor International PASSPORT 4 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

INTRODUCTION

Key findings

Men’s grooming

robust growth in

2012

Men’s grooming increased by 7% in 2012, the highest growth since 2005. This was

largely due to the strong performance of Latin America, which continued to grow by

double digits, with low but stable growth in Western Europe and North America.

Men’s shaving

performs strongly

Despite only slow growth in Western Europe and North America, men's shaving

registered a 7% increase in sales in 2012, on the back of its largest category, razors and

blades, with sales of US$13 billion.

Men’s toiletries to

overtake men’s

shaving

Men’s toiletries’ consistently stronger performance than men’s shaving over the past five

years helped it close the gap from US$1 billion in 2007 to just US$116 million in 2012,

and it is expected to overtake men’s shaving in 2013.

Innovation vital for

brands

As more men look for male-specific products, innovation that combines multiple benefits

as well as specialist solutions tailored to men’s problem-solving nature are becoming

more common not only in skin care but also in hair care and deodorants.

Asia Pacific leads

men’s skin care

With over 60% of the sales of men’s skin care coming from Asia Pacific, its importance

to men’s skin care brands is vital, while South Korea is the world’s leading premium

men’s skin care market.

Latin America key

region in the future

Latin America is set to lead absolute growth in both men’s shaving and men’s toiletries,

adding US$1.6 billion to and US$1.8 billion, respectively, over 2012-2017. Brazil, which

holds the lion's share of Latin America’s market value, is expected to replace the US as

the largest global market by 2017, accounting for 40% of global growth over the forecast

period.

INTRODUCTION

INDUSTRY OVERVIEW

CATEGORY ANALYSIS

REGIONAL ANALYSIS

CHANNEL ANALYSIS

INNOVATION STRATEGIES

FUTURE PROSPECTS

© Euromonitor International PASSPORT 6 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

0

1

2

3

4

5

6

7

8

9

10

0

20,000

40,000

60,000

80,000

100,000

120,000

Skin Care

Hair Care

Colour Cosmetics

Fra-grances

Oral Care

Bath and Shower

Men's Grooming

De-odorants

Sets/Kits

Baby/Child

Products

Sun Care

Depil-atories

% v

alu

e g

row

th

US

$ m

illio

n

Category Growth 2011 vs 2012

2012 US$mn 2010-11 % growth 2011-12 % growth

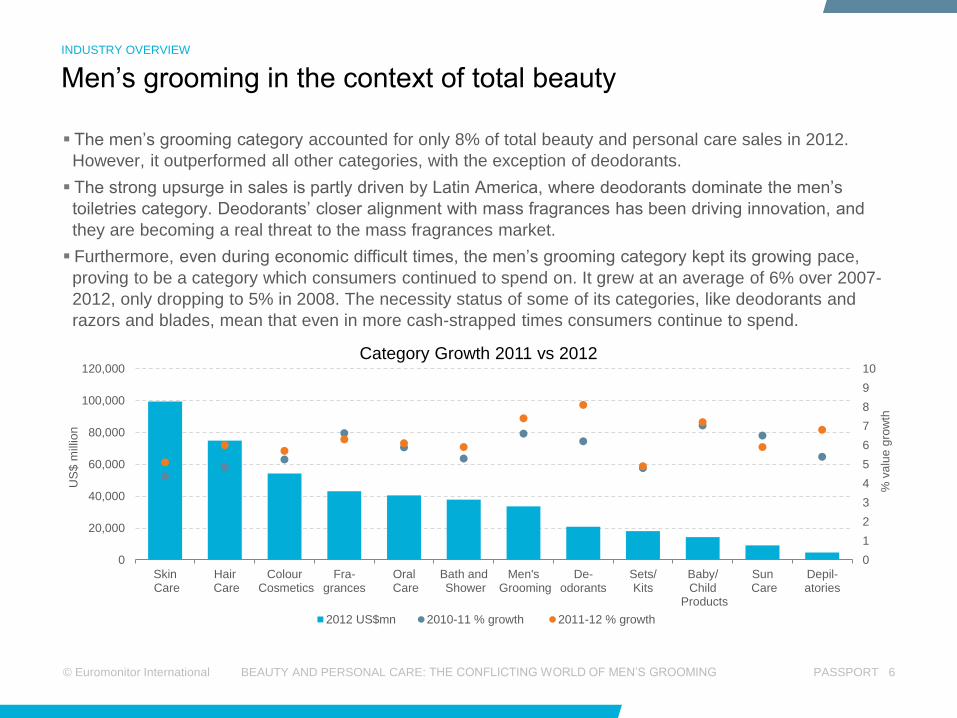

The men’s grooming category accounted for only 8% of total beauty and personal care sales in 2012.

However, it outperformed all other categories, with the exception of deodorants.

The strong upsurge in sales is partly driven by Latin America, where deodorants dominate the men’s

toiletries category. Deodorants’ closer alignment with mass fragrances has been driving innovation, and

they are becoming a real threat to the mass fragrances market.

Furthermore, even during economic difficult times, the men’s grooming category kept its growing pace,

proving to be a category which consumers continued to spend on. It grew at an average of 6% over 2007-

2012, only dropping to 5% in 2008. The necessity status of some of its categories, like deodorants and

razors and blades, mean that even in more cash-strapped times consumers continue to spend.

Men’s grooming in the context of total beauty

INDUSTRY OVERVIEW

© Euromonitor International PASSPORT 7 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

0

1

2

3

4

5

6

7

8

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2007-2008

2008-2009

2009-2010

2010-2011

2011-2012

% g

row

th

Va

lue

sa

les (

US

$ m

illio

n)

Men’s Grooming 2008-2012

Sales Growth

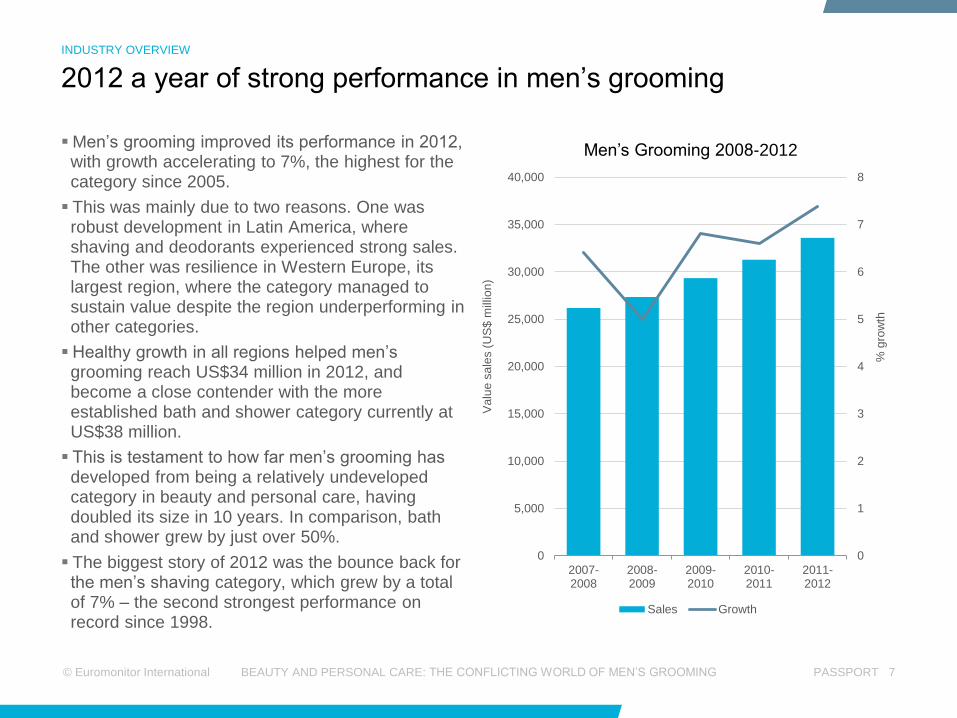

Men’s grooming improved its performance in 2012, with growth accelerating to 7%, the highest for the category since 2005.

This was mainly due to two reasons. One was robust development in Latin America, where shaving and deodorants experienced strong sales. The other was resilience in Western Europe, its largest region, where the category managed to sustain value despite the region underperforming in other categories.

Healthy growth in all regions helped men’s grooming reach US$34 million in 2012, and become a close contender with the more established bath and shower category currently at US$38 million.

This is testament to how far men’s grooming has developed from being a relatively undeveloped category in beauty and personal care, having doubled its size in 10 years. In comparison, bath and shower grew by just over 50%.

The biggest story of 2012 was the bounce back for the men’s shaving category, which grew by a total of 7% – the second strongest performance on record since 1998.

2012 a year of strong performance in men’s grooming

INDUSTRY OVERVIEW

© Euromonitor International PASSPORT 8 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

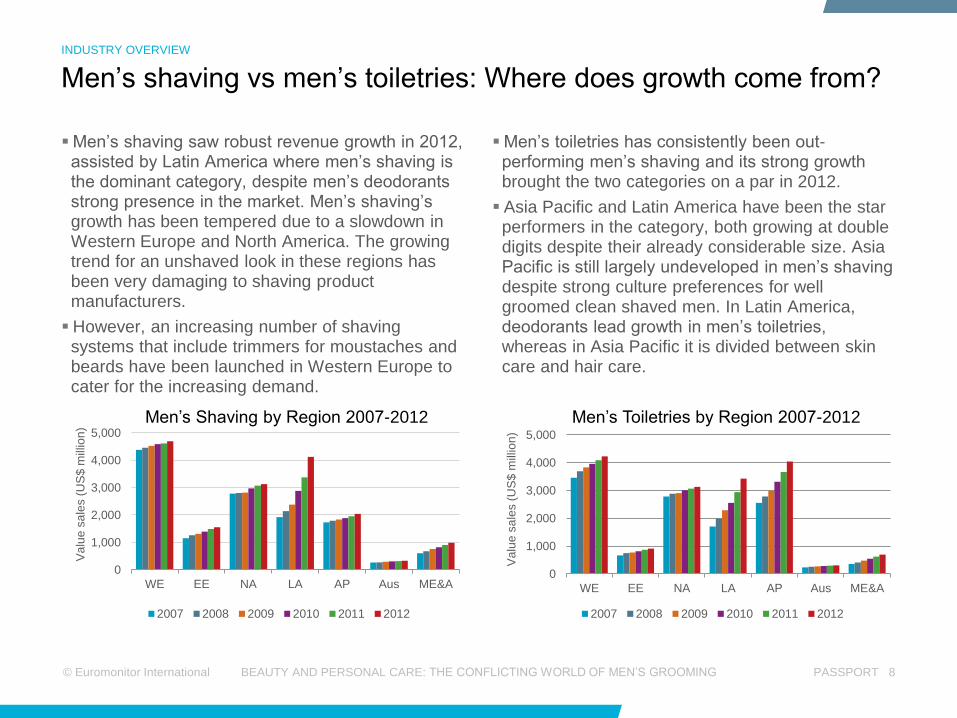

Men’s toiletries has consistently been out-performing men’s shaving and its strong growth brought the two categories on a par in 2012.

Asia Pacific and Latin America have been the star performers in the category, both growing at double digits despite their already considerable size. Asia Pacific is still largely undeveloped in men’s shaving despite strong culture preferences for well groomed clean shaved men. In Latin America, deodorants lead growth in men’s toiletries, whereas in Asia Pacific it is divided between skin care and hair care.

Men’s shaving saw robust revenue growth in 2012, assisted by Latin America where men’s shaving is the dominant category, despite men’s deodorants strong presence in the market. Men’s shaving’s growth has been tempered due to a slowdown in Western Europe and North America. The growing trend for an unshaved look in these regions has been very damaging to shaving product manufacturers.

However, an increasing number of shaving systems that include trimmers for moustaches and beards have been launched in Western Europe to cater for the increasing demand.

0

1,000

2,000

3,000

4,000

5,000

WE EE NA LA AP Aus ME&A

Va

lue

sa

les (

US

$ m

illio

n)

Men’s Shaving by Region 2007-2012

2007 2008 2009 2010 2011 2012

0

1,000

2,000

3,000

4,000

5,000

WE EE NA LA AP Aus ME&A

Va

lue

sa

les (

US

$ m

illio

n)

Men’s Toiletries by Region 2007-2012

2007 2008 2009 2010 2011 2012

Men’s shaving vs men’s toiletries: Where does growth come from?

INDUSTRY OVERVIEW

INTRODUCTION

INDUSTRY OVERVIEW

CATEGORY ANALYSIS

REGIONAL ANALYSIS

CHANNEL ANALYSIS

INNOVATION STRATEGIES

FUTURE PROSPECTS

© Euromonitor International PASSPORT 10 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

0

5

10

15

0

5,000

10,000

15,000

Men's Post-Shave Men's Pre-Shave Men's Razors andBlades

Men's Bath andShower

Men's Deodorants Men's Hair Care Men's Skin Care

MEN'S SHAVING MEN'S TOILETRIES

% g

row

th

Va

lue

sa

les (

US

$ m

illio

n) Category Value Sales 2007/2012 and % Growth

2007 2012 2011/12

Men’s skin care showed the most robust growth between 2007 and 2012, with a CAGR of 12%, albeit from a small base. This was largely due to the Asia Pacific region, where the majority of sales come from. The growing appeal of men’s skin care has been damaging to the men’s post-shave industry, as many young men view such products as harsh for their skin and old-fashioned, preferring skin care products.

Men’s razor and blades continued their strong growth, due largely to the Latin America region. However, difficult economic conditions in Western Europe have caused many consumers to trade down, and this, coupled with a new trend of a slightly unshaved look, called the “three-day beard” have played an important role as men minimise their shaving and their spending.

Men’s deodorants have been the star performer within men’s toiletries in terms of actual growth, with a CAGR of 8% between 2007 and 2012 corresponding to a value increase of US$2.5 billion – over half of the growth in men’s toiletries.

Deodorants, skin care and razors and blades are the categories to watch, as they are expected to shape the balance between men’s shaving and men’s toiletries.

Men’s toiletries close down on men’s shaving

CATEGORY ANALYSIS

© Euromonitor International PASSPORT 11 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

0

5

10

15

20

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Western Europe Eastern Europe North America Latin America Asia Pacific Australasia Middle East andAfrica

% g

row

th

Va

lue

sa

les (

US

$ m

illio

n)

Razors and Blades Value and Growth 2011-2012

2011 2012 % CAGR 2007-12

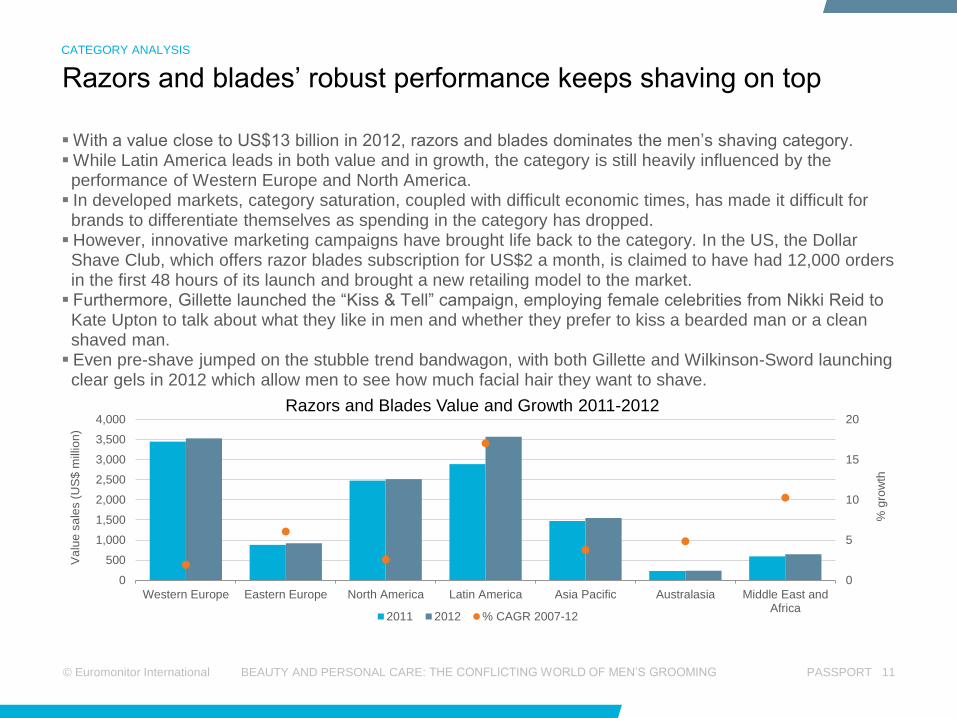

With a value close to US$13 billion in 2012, razors and blades dominates the men’s shaving category. While Latin America leads in both value and in growth, the category is still heavily influenced by the performance of Western Europe and North America.

In developed markets, category saturation, coupled with difficult economic times, has made it difficult for brands to differentiate themselves as spending in the category has dropped.

However, innovative marketing campaigns have brought life back to the category. In the US, the Dollar Shave Club, which offers razor blades subscription for US$2 a month, is claimed to have had 12,000 orders in the first 48 hours of its launch and brought a new retailing model to the market.

Furthermore, Gillette launched the “Kiss & Tell” campaign, employing female celebrities from Nikki Reid to Kate Upton to talk about what they like in men and whether they prefer to kiss a bearded man or a clean shaved man.

Even pre-shave jumped on the stubble trend bandwagon, with both Gillette and Wilkinson-Sword launching clear gels in 2012 which allow men to see how much facial hair they want to shave.

Razors and blades’ robust performance keeps shaving on top

CATEGORY ANALYSIS

© Euromonitor International PASSPORT 12 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

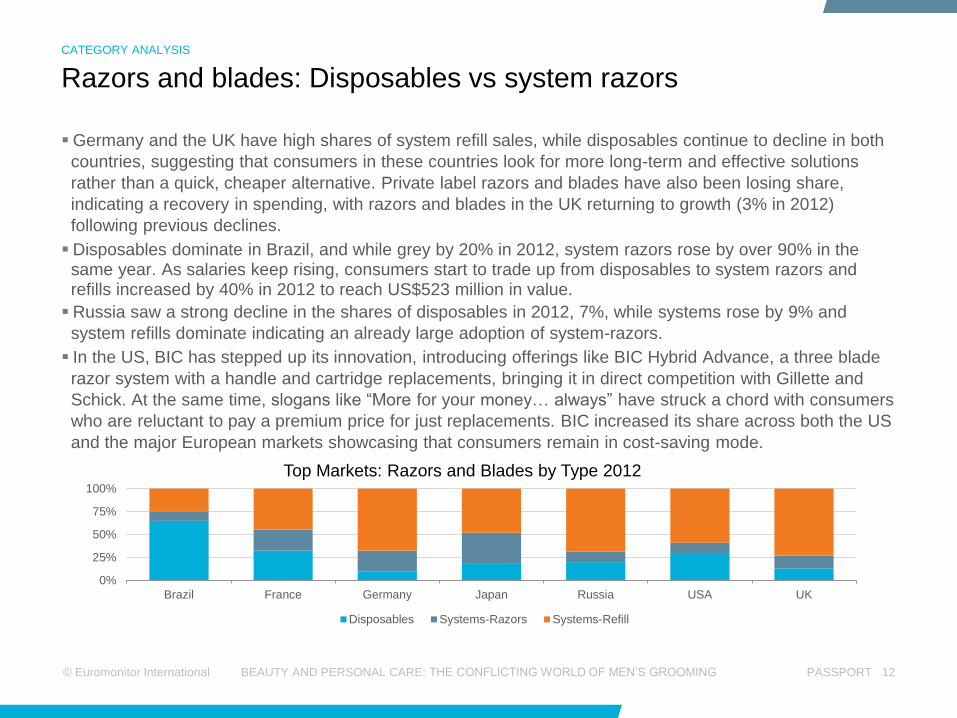

Germany and the UK have high shares of system refill sales, while disposables continue to decline in both

countries, suggesting that consumers in these countries look for more long-term and effective solutions

rather than a quick, cheaper alternative. Private label razors and blades have also been losing share,

indicating a recovery in spending, with razors and blades in the UK returning to growth (3% in 2012)

following previous declines.

Disposables dominate in Brazil, and while grey by 20% in 2012, system razors rose by over 90% in the same year. As salaries keep rising, consumers start to trade up from disposables to system razors and refills increased by 40% in 2012 to reach US$523 million in value.

Russia saw a strong decline in the shares of disposables in 2012, 7%, while systems rose by 9% and

system refills dominate indicating an already large adoption of system-razors.

In the US, BIC has stepped up its innovation, introducing offerings like BIC Hybrid Advance, a three blade

razor system with a handle and cartridge replacements, bringing it in direct competition with Gillette and

Schick. At the same time, slogans like “More for your money… always” have struck a chord with consumers

who are reluctant to pay a premium price for just replacements. BIC increased its share across both the US

and the major European markets showcasing that consumers remain in cost-saving mode.

0%

25%

50%

75%

100%

Brazil France Germany Japan Russia USA UK

Top Markets: Razors and Blades by Type 2012

Disposables Systems-Razors Systems-Refill

Razors and blades: Disposables vs system razors

CATEGORY ANALYSIS

© Euromonitor International PASSPORT 13 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

0

5

10

15

20

USA France Germany Greece Ireland Netherlands Portugal Spain

% v

alu

e

Private Label Share in Razors and Blades

2007 2012

In France, disposables grew from 29% to 33% of razors and blades sales over 2007-2012, at the expense of system razors. BIC’s sales rose by 4% in 2012, while Gillette’s declined for a second year in a row. A further indicator of the quest for cheaper alternatives in France is the rise of private label, the share of which rose to 8% of total razors and blades sales in 2012.

The economically troubled southern European countries of Greece, Portugal and Spain saw even bigger gains in private label share, especially in Greece, where private label was negligible prior to 2007. Growing on average at double digits, private label in Western Europe added more in sales than any individual manufacturer between 2007 and 2012.

Gillette holds over 60% of razors and blades sales in Western Europe, but has had to fight disposable brands and private label, as well as the trend for stubble. It launched a new product in 2012, the Gillette Fusion ProGlide Styler, a three in one battery operated razor which gives the option of trimming not just shaving. The higher price of new launches like Gillette Fusion ProGlide Styler, which retails at over US$20, shows how brands are putting up prices to cope with lower demand as well as less frequent repurchases.

Private label benefits in Southern Europe

CATEGORY ANALYSIS

© Euromonitor International PASSPORT 14 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

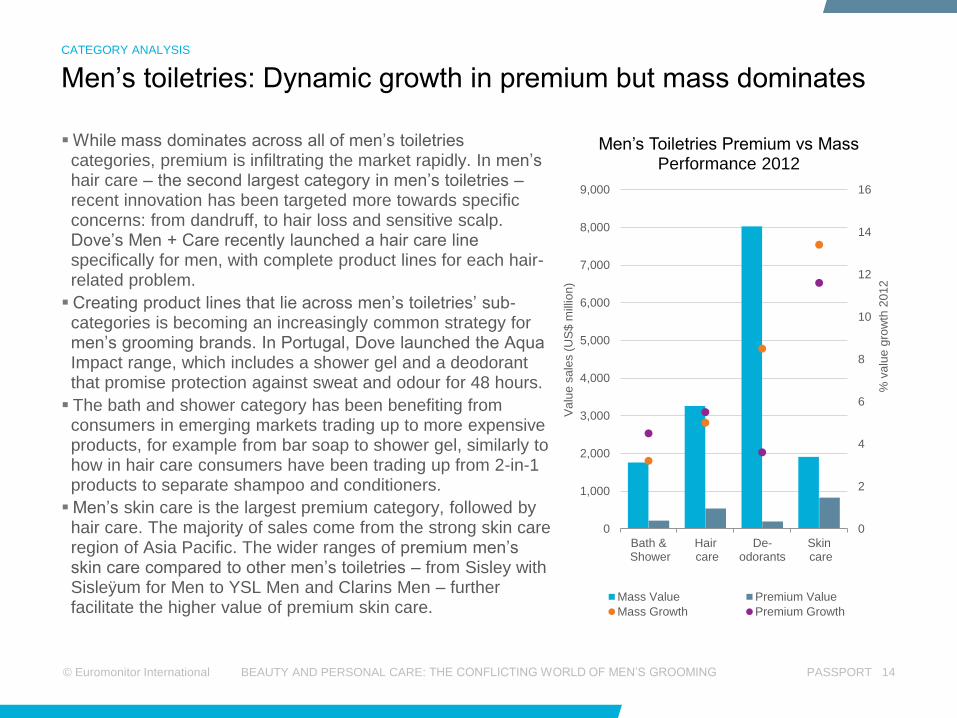

While mass dominates across all of men’s toiletries categories, premium is infiltrating the market rapidly. In men’s hair care – the second largest category in men’s toiletries – recent innovation has been targeted more towards specific concerns: from dandruff, to hair loss and sensitive scalp. Dove’s Men + Care recently launched a hair care line specifically for men, with complete product lines for each hair-related problem.

Creating product lines that lie across men’s toiletries’ sub-categories is becoming an increasingly common strategy for men’s grooming brands. In Portugal, Dove launched the Aqua Impact range, which includes a shower gel and a deodorant that promise protection against sweat and odour for 48 hours.

The bath and shower category has been benefiting from consumers in emerging markets trading up to more expensive products, for example from bar soap to shower gel, similarly to how in hair care consumers have been trading up from 2-in-1 products to separate shampoo and conditioners.

Men’s skin care is the largest premium category, followed by hair care. The majority of sales come from the strong skin care region of Asia Pacific. The wider ranges of premium men’s skin care compared to other men’s toiletries – from Sisley with Sisleÿum for Men to YSL Men and Clarins Men – further facilitate the higher value of premium skin care.

0

2

4

6

8

10

12

14

16

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Bath & Shower

Hair care

De-odorants

Skin care

% v

alu

e g

row

th 2

01

2

Va

lue

sa

les (

US

$ m

illio

n)

Men’s Toiletries Premium vs Mass Performance 2012

Mass Value Premium Value

Mass Growth Premium Growth

Men’s toiletries: Dynamic growth in premium but mass dominates

CATEGORY ANALYSIS

© Euromonitor International PASSPORT 15 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

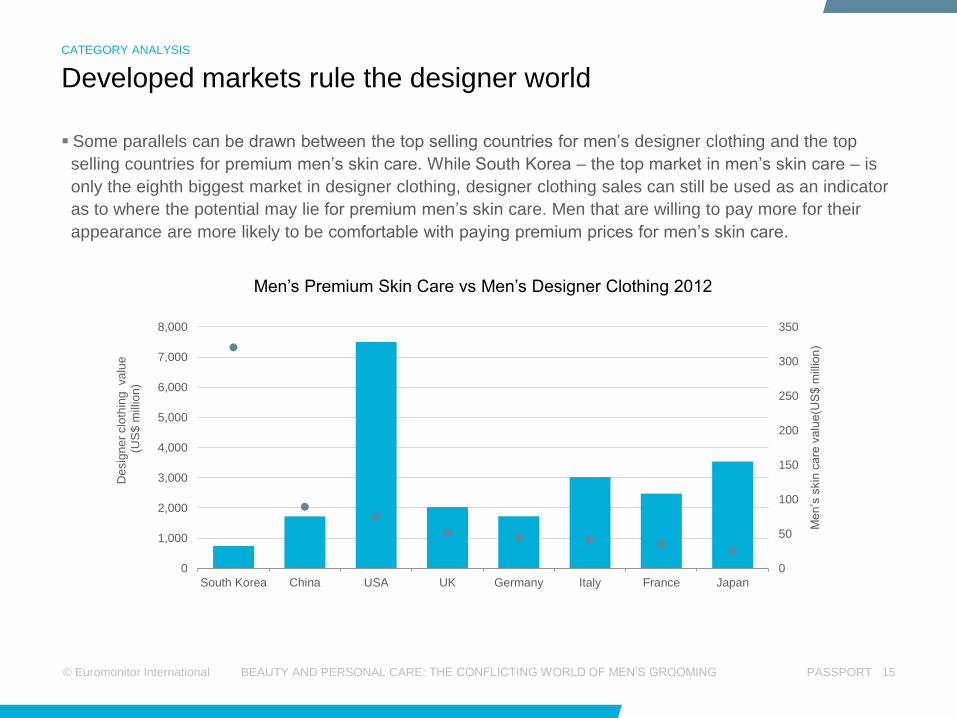

Some parallels can be drawn between the top selling countries for men’s designer clothing and the top

selling countries for premium men’s skin care. While South Korea – the top market in men’s skin care – is

only the eighth biggest market in designer clothing, designer clothing sales can still be used as an indicator

as to where the potential may lie for premium men’s skin care. Men that are willing to pay more for their

appearance are more likely to be comfortable with paying premium prices for men’s skin care.

Developed markets rule the designer world

CATEGORY ANALYSIS

0

50

100

150

200

250

300

350

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

South Korea China USA UK Germany Italy France Japan

Me

n’s

skin

ca

re v

alu

e(U

S$ m

illio

n)

Desig

ne

r clo

thin

g va

lue

(

US

$ m

illio

n)

Men’s Premium Skin Care vs Men’s Designer Clothing 2012

© Euromonitor International PASSPORT 16 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

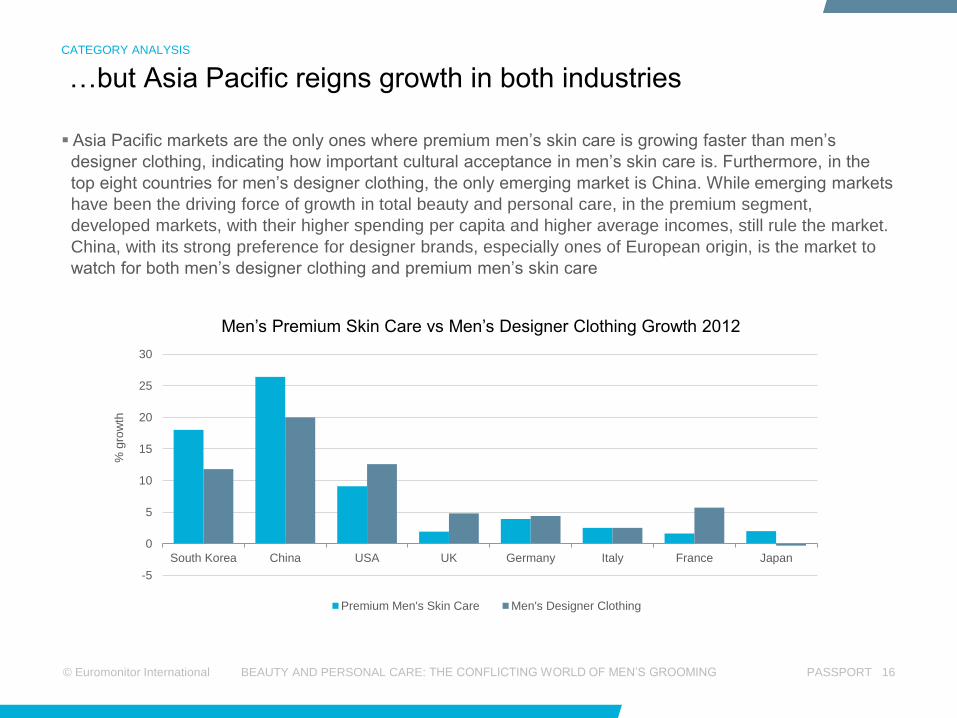

Asia Pacific markets are the only ones where premium men’s skin care is growing faster than men’s

designer clothing, indicating how important cultural acceptance in men’s skin care is. Furthermore, in the

top eight countries for men’s designer clothing, the only emerging market is China. While emerging markets

have been the driving force of growth in total beauty and personal care, in the premium segment,

developed markets, with their higher spending per capita and higher average incomes, still rule the market.

China, with its strong preference for designer brands, especially ones of European origin, is the market to

watch for both men’s designer clothing and premium men’s skin care

…but Asia Pacific reigns growth in both industries

CATEGORY ANALYSIS

-5

0

5

10

15

20

25

30

South Korea China USA UK Germany Italy France Japan

% g

row

th

Men’s Premium Skin Care vs Men’s Designer Clothing Growth 2012

Premium Men's Skin Care Men's Designer Clothing

© Euromonitor International PASSPORT 17 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

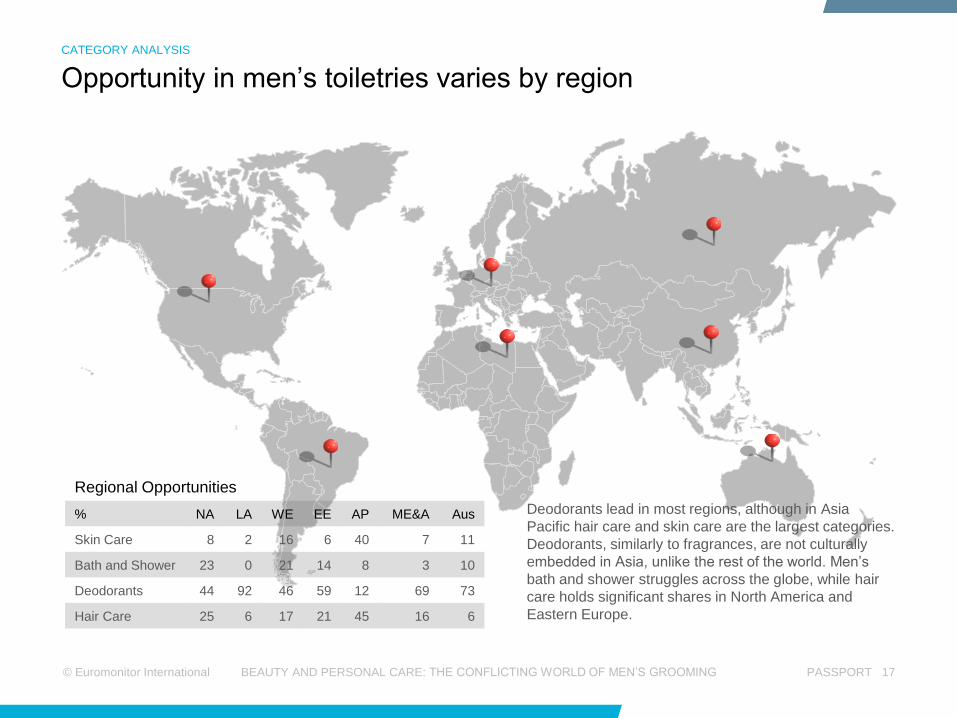

Opportunity in men’s toiletries varies by region

CATEGORY ANALYSIS

Deodorants lead in most regions, although in Asia

Pacific hair care and skin care are the largest categories.

Deodorants, similarly to fragrances, are not culturally

embedded in Asia, unlike the rest of the world. Men’s

bath and shower struggles across the globe, while hair

care holds significant shares in North America and

Eastern Europe.

Regional Opportunities

% NA LA WE EE AP ME&A Aus

Skin Care 8 2 16 6 40 7 11

Bath and Shower 23 0 21 14 8 3 10

Deodorants 44 92 46 59 12 69 73

Hair Care 25 6 17 21 45 16 6

© Euromonitor International PASSPORT 18 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

0

1

2

3

4

5

6

7

8

9

0

500

1,000

1,500

2,000

2,500

3,000

3,500

AP Aus EE LA ME&A NA WE

Va

lue

pe

r ca

pita

(U

S$)

Va

lue

sa

les (

US

$ m

illio

n)

Men’s Deodorants 2012

Value Sales Per Capita Spending

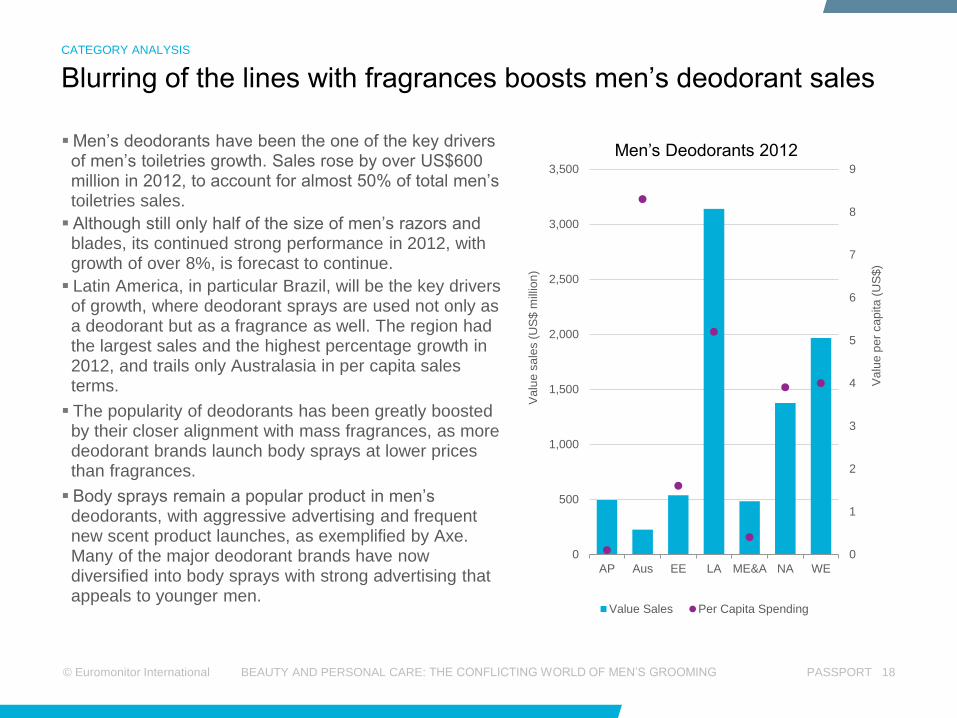

Men’s deodorants have been the one of the key drivers of men’s toiletries growth. Sales rose by over US$600 million in 2012, to account for almost 50% of total men’s toiletries sales.

Although still only half of the size of men’s razors and blades, its continued strong performance in 2012, with growth of over 8%, is forecast to continue.

Latin America, in particular Brazil, will be the key drivers of growth, where deodorant sprays are used not only as a deodorant but as a fragrance as well. The region had the largest sales and the highest percentage growth in 2012, and trails only Australasia in per capita sales terms.

The popularity of deodorants has been greatly boosted by their closer alignment with mass fragrances, as more deodorant brands launch body sprays at lower prices than fragrances.

Body sprays remain a popular product in men’s deodorants, with aggressive advertising and frequent new scent product launches, as exemplified by Axe. Many of the major deodorant brands have now diversified into body sprays with strong advertising that appeals to younger men.

Blurring of the lines with fragrances boosts men’s deodorant sales

CATEGORY ANALYSIS

© Euromonitor International PASSPORT 19 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

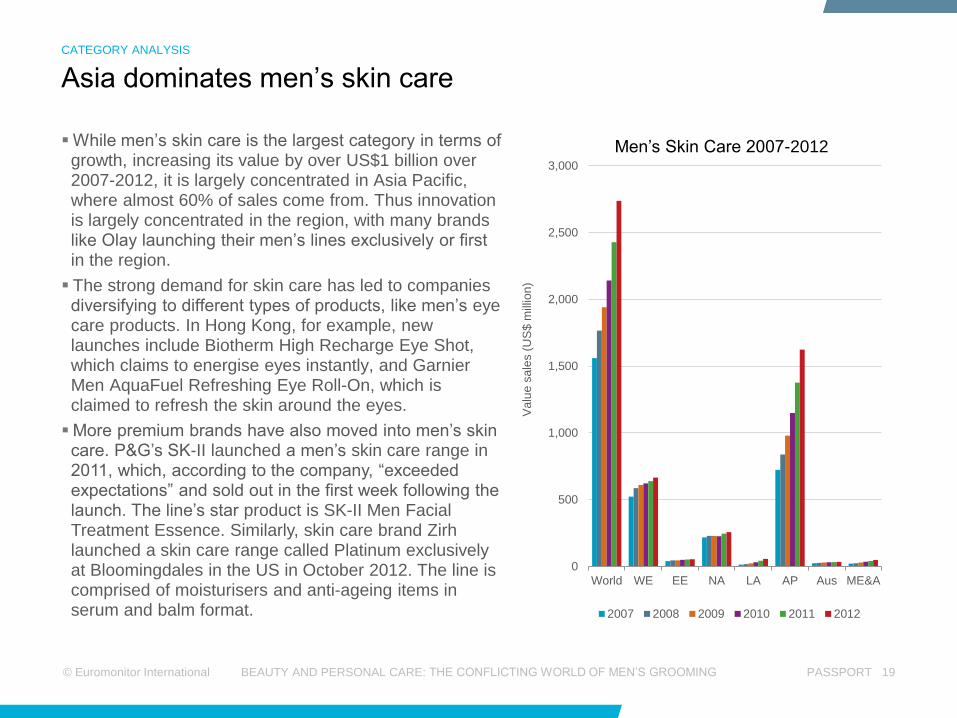

While men’s skin care is the largest category in terms of growth, increasing its value by over US$1 billion over 2007-2012, it is largely concentrated in Asia Pacific, where almost 60% of sales come from. Thus innovation is largely concentrated in the region, with many brands like Olay launching their men’s lines exclusively or first in the region.

The strong demand for skin care has led to companies diversifying to different types of products, like men’s eye care products. In Hong Kong, for example, new launches include Biotherm High Recharge Eye Shot, which claims to energise eyes instantly, and Garnier Men AquaFuel Refreshing Eye Roll-On, which is claimed to refresh the skin around the eyes.

More premium brands have also moved into men’s skin care. P&G’s SK-II launched a men’s skin care range in 2011, which, according to the company, “exceeded expectations” and sold out in the first week following the launch. The line’s star product is SK-II Men Facial Treatment Essence. Similarly, skin care brand Zirh launched a skin care range called Platinum exclusively at Bloomingdales in the US in October 2012. The line is comprised of moisturisers and anti-ageing items in serum and balm format.

0

500

1,000

1,500

2,000

2,500

3,000

World WE EE NA LA AP Aus ME&A

Va

lue

sa

les (

US

$ m

illio

n)

Men’s Skin Care 2007-2012

2007 2008 2009 2010 2011 2012

Asia dominates men’s skin care

CATEGORY ANALYSIS

INTRODUCTION

INDUSTRY OVERVIEW

CATEGORY ANALYSIS

REGIONAL ANALYSIS

CHANNEL ANALYSIS

INNOVATION STRATEGIES

FUTURE PROSPECTS

© Euromonitor International PASSPORT 21 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

Latin America outperforms all regions globally

REGIONAL ANALYSIS

Regionally, Western Europe remains the largest market, at US$9 billion,

followed by Latin America, at US$7.5 billion. Latin America and the Middle

East and Africa were the only regions growing in double digits in 2012. While

North America and Western Europe saw sluggish growth of 2-3%, Latin

America’s 19% growth added US$1.2 billion to the market ,accounting for

over half of the industry’s growth in 2012.

2012 Value Growth

■ <10%

■ 7-8%

■ 4-6%

■ 1-3%

© Euromonitor International PASSPORT 22 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

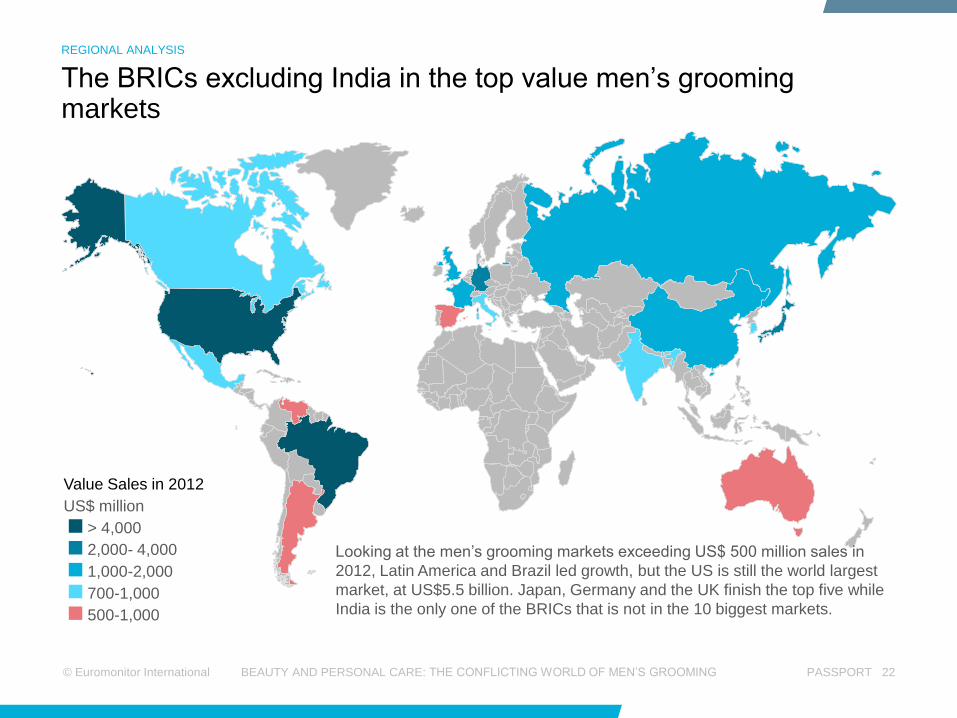

The BRICs excluding India in the top value men’s grooming markets

REGIONAL ANALYSIS

Value Sales in 2012

US$ million

> 4,000

2,000- 4,000

1,000-2,000

700-1,000

500-1,000

Looking at the men’s grooming markets exceeding US$ 500 million sales in

2012, Latin America and Brazil led growth, but the US is still the world largest

market, at US$5.5 billion. Japan, Germany and the UK finish the top five while

India is the only one of the BRICs that is not in the 10 biggest markets.

© Euromonitor International PASSPORT 23 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

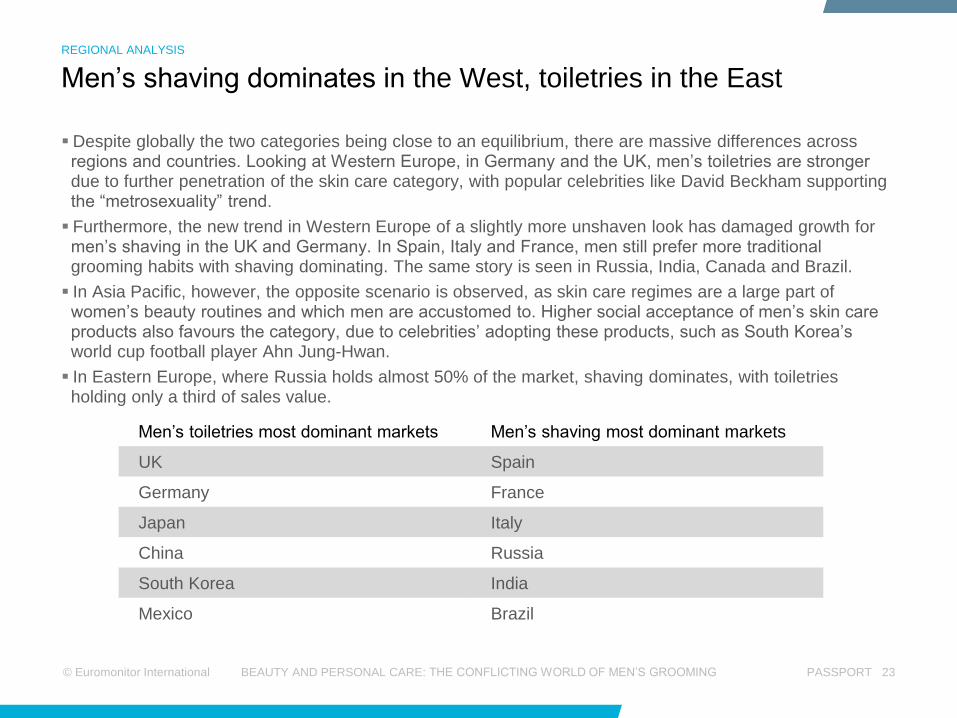

Men’s toiletries most dominant markets Men’s shaving most dominant markets

UK Spain

Germany France

Japan Italy

China Russia

South Korea India

Mexico Brazil

Despite globally the two categories being close to an equilibrium, there are massive differences across regions and countries. Looking at Western Europe, in Germany and the UK, men’s toiletries are stronger due to further penetration of the skin care category, with popular celebrities like David Beckham supporting the “metrosexuality” trend.

Furthermore, the new trend in Western Europe of a slightly more unshaven look has damaged growth for men’s shaving in the UK and Germany. In Spain, Italy and France, men still prefer more traditional grooming habits with shaving dominating. The same story is seen in Russia, India, Canada and Brazil.

In Asia Pacific, however, the opposite scenario is observed, as skin care regimes are a large part of women’s beauty routines and which men are accustomed to. Higher social acceptance of men’s skin care products also favours the category, due to celebrities’ adopting these products, such as South Korea’s world cup football player Ahn Jung-Hwan.

In Eastern Europe, where Russia holds almost 50% of the market, shaving dominates, with toiletries holding only a third of sales value.

Men’s shaving dominates in the West, toiletries in the East

REGIONAL ANALYSIS

© Euromonitor International PASSPORT 24 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

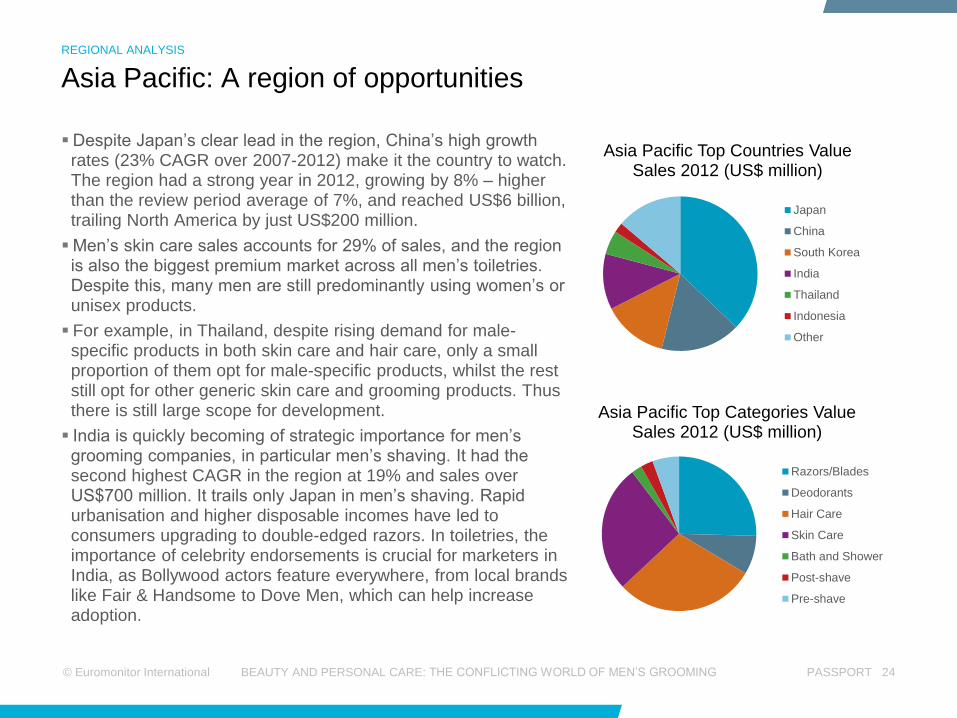

Despite Japan’s clear lead in the region, China’s high growth rates (23% CAGR over 2007-2012) make it the country to watch. The region had a strong year in 2012, growing by 8% – higher than the review period average of 7%, and reached US$6 billion, trailing North America by just US$200 million.

Men’s skin care sales accounts for 29% of sales, and the region is also the biggest premium market across all men’s toiletries. Despite this, many men are still predominantly using women’s or unisex products.

For example, in Thailand, despite rising demand for male-specific products in both skin care and hair care, only a small proportion of them opt for male-specific products, whilst the rest still opt for other generic skin care and grooming products. Thus there is still large scope for development.

India is quickly becoming of strategic importance for men’s grooming companies, in particular men’s shaving. It had the second highest CAGR in the region at 19% and sales over US$700 million. It trails only Japan in men’s shaving. Rapid urbanisation and higher disposable incomes have led to consumers upgrading to double-edged razors. In toiletries, the importance of celebrity endorsements is crucial for marketers in India, as Bollywood actors feature everywhere, from local brands like Fair & Handsome to Dove Men, which can help increase adoption.

Asia Pacific Top Categories Value Sales 2012 (US$ million)

Razors/Blades

Deodorants

Hair Care

Skin Care

Bath and Shower

Post-shave

Pre-shave

Asia Pacific Top Countries Value Sales 2012 (US$ million)

Japan

China

South Korea

India

Thailand

Indonesia

Other

Asia Pacific: A region of opportunities

REGIONAL ANALYSIS

© Euromonitor International PASSPORT 25 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

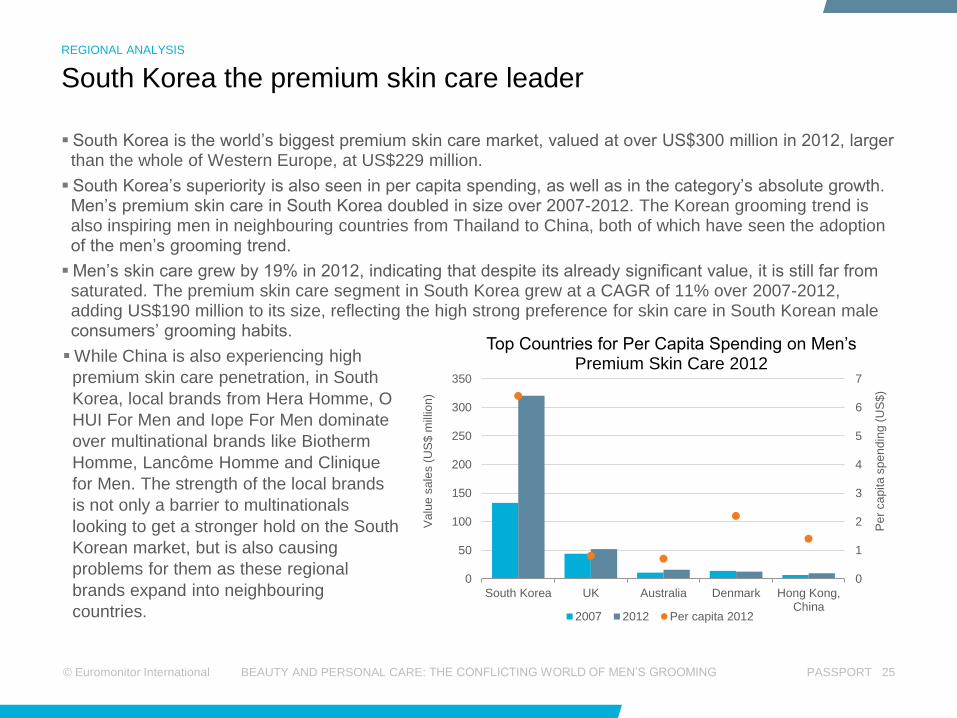

South Korea is the world’s biggest premium skin care market, valued at over US$300 million in 2012, larger than the whole of Western Europe, at US$229 million.

South Korea’s superiority is also seen in per capita spending, as well as in the category’s absolute growth. Men’s premium skin care in South Korea doubled in size over 2007-2012. The Korean grooming trend is also inspiring men in neighbouring countries from Thailand to China, both of which have seen the adoption of the men’s grooming trend.

Men’s skin care grew by 19% in 2012, indicating that despite its already significant value, it is still far from saturated. The premium skin care segment in South Korea grew at a CAGR of 11% over 2007-2012, adding US$190 million to its size, reflecting the high strong preference for skin care in South Korean male consumers’ grooming habits.

While China is also experiencing high

premium skin care penetration, in South

Korea, local brands from Hera Homme, O

HUI For Men and Iope For Men dominate

over multinational brands like Biotherm

Homme, Lancôme Homme and Clinique

for Men. The strength of the local brands

is not only a barrier to multinationals

looking to get a stronger hold on the South

Korean market, but is also causing

problems for them as these regional

brands expand into neighbouring

countries.

South Korea the premium skin care leader

REGIONAL ANALYSIS

0

1

2

3

4

5

6

7

0

50

100

150

200

250

300

350

South Korea UK Australia Denmark Hong Kong,China

Pe

r ca

pita

sp

en

din

g (

US

$)

Va

lue

sa

les (

US

$ m

illio

n)

Top Countries for Per Capita Spending on Men’s Premium Skin Care 2012

2007 2012 Per capita 2012

© Euromonitor International PASSPORT 26 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

China continues to chase… …While Japan continues to decline

China has continued its chase for the top market

spot, breaking US$1 billion in sales in 2012. 80% of

this was in toiletries, and over half of from the skin

care category.

Despite only three categories experiencing double

digit growth in 2012, the sizeable size of skin care

and hair care pushed growth for total men’s

grooming category to 17%.

While premium skin care only made up 16% of the

total men’s skin care market in 2012, its consistently

higher growth rates, as well as the increasing

number of multinationals entering the market,

indicate that the segment is booming.

While traditionally there were three main functions

dominating the Chinese men’s skin care market:

cleansing, oil control and moisturising, new

innovation appears to be increasingly targeted to

anti-ageing.

Both local and international brands have been

launching anti-ageing lines specifically designed for

men.

Despite economic improvement in Japan, the

category still declined in 2012.

Deodorants experienced the largest decline, as high

temperatures in summer 2011, coupled with efforts to

save energy, caused sales to surge in 2011, by 17%.

As the category returned to normal demand in 2012,

it contracted by 9%. Deodorants still do not have a

high penetration in the region and there is still a large

untapped market.

Skin care was the only category to experience strong

growth in 2012, of 5%, as men’s skin care companies

launched new gentler formulas with moisturising the

skin as a key focus. This was also seen among pre-

shave products like Schick Hydro and Gillette Pure

and Sensitive.

Whitening skin care products are very popular

among female consumers and are now being

launched by men’s skin care brands, for example

Rohto Pharmaceutical Co Ltd’s whitening series

under its Oxy brand.

The powerhouses of Asia: China vs Japan

REGIONAL ANALYSIS

© Euromonitor International PASSPORT 27 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

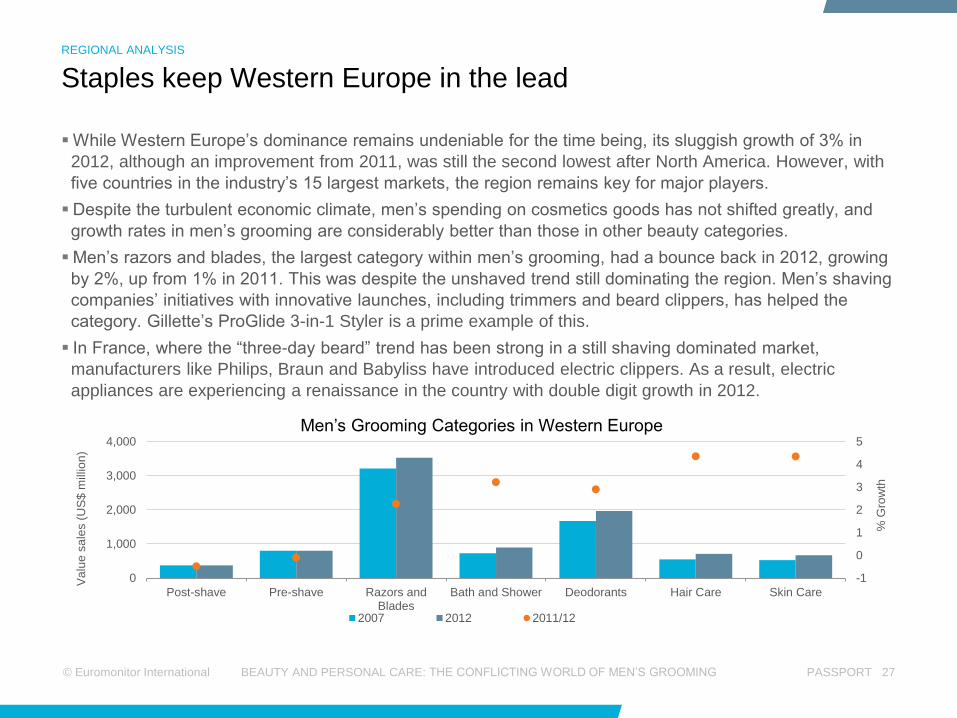

While Western Europe’s dominance remains undeniable for the time being, its sluggish growth of 3% in

2012, although an improvement from 2011, was still the second lowest after North America. However, with

five countries in the industry’s 15 largest markets, the region remains key for major players.

Despite the turbulent economic climate, men’s spending on cosmetics goods has not shifted greatly, and

growth rates in men’s grooming are considerably better than those in other beauty categories.

Men’s razors and blades, the largest category within men’s grooming, had a bounce back in 2012, growing

by 2%, up from 1% in 2011. This was despite the unshaved trend still dominating the region. Men’s shaving

companies’ initiatives with innovative launches, including trimmers and beard clippers, has helped the

category. Gillette’s ProGlide 3-in-1 Styler is a prime example of this.

In France, where the “three-day beard” trend has been strong in a still shaving dominated market,

manufacturers like Philips, Braun and Babyliss have introduced electric clippers. As a result, electric

appliances are experiencing a renaissance in the country with double digit growth in 2012.

Staples keep Western Europe in the lead

REGIONAL ANALYSIS

-1

0

1

2

3

4

5

0

1,000

2,000

3,000

4,000

Post-shave Pre-shave Razors andBlades

Bath and Shower Deodorants Hair Care Skin Care

% G

row

th

Va

lue

sa

les (

US

$ m

illio

n)

Men’s Grooming Categories in Western Europe

2007 2012 2011/12

© Euromonitor International PASSPORT 28 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

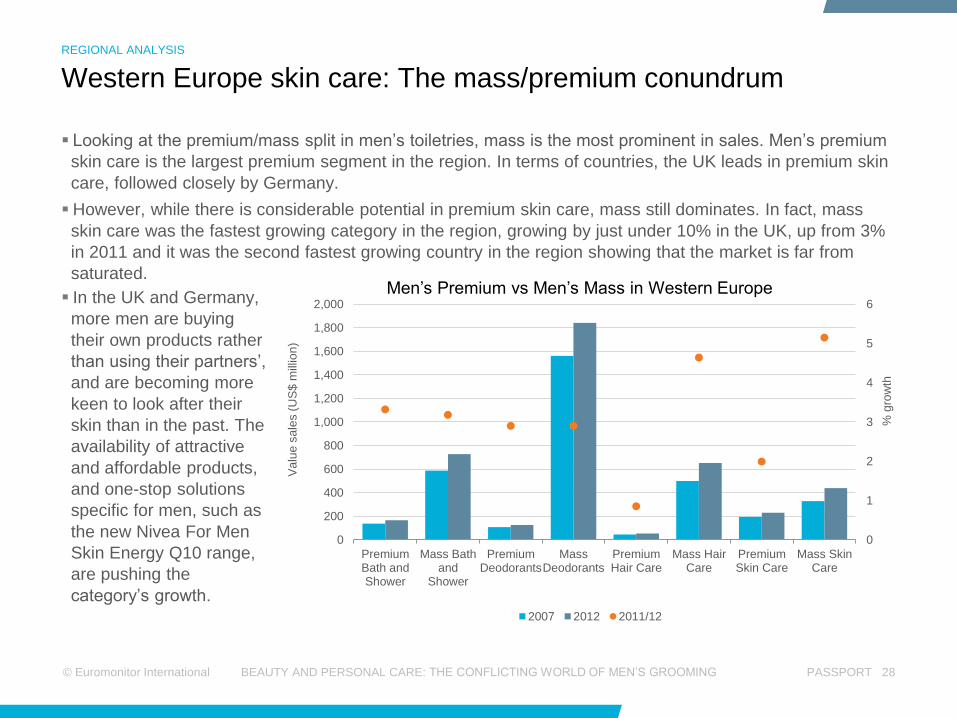

Looking at the premium/mass split in men’s toiletries, mass is the most prominent in sales. Men’s premium

skin care is the largest premium segment in the region. In terms of countries, the UK leads in premium skin

care, followed closely by Germany.

However, while there is considerable potential in premium skin care, mass still dominates. In fact, mass

skin care was the fastest growing category in the region, growing by just under 10% in the UK, up from 3%

in 2011 and it was the second fastest growing country in the region showing that the market is far from

saturated.

In the UK and Germany,

more men are buying

their own products rather

than using their partners’,

and are becoming more

keen to look after their

skin than in the past. The

availability of attractive

and affordable products,

and one-stop solutions

specific for men, such as

the new Nivea For Men

Skin Energy Q10 range,

are pushing the

category’s growth.

Western Europe skin care: The mass/premium conundrum

REGIONAL ANALYSIS

0

1

2

3

4

5

6

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

PremiumBath andShower

Mass Bathand

Shower

PremiumDeodorants

MassDeodorants

PremiumHair Care

Mass HairCare

PremiumSkin Care

Mass SkinCare

% g

row

th

Va

lue

sa

les (

US

$ m

illio

n)

Men’s Premium vs Men’s Mass in Western Europe

2007 2012 2011/12

© Euromonitor International PASSPORT 29 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

Southern Europe remains more traditional… …While the UK and Germany lead in toiletries

While Italy, Spain and France have traditionally

been dominated by shaving, changing consumer

perceptions, coupled with a trend for an unshaved

look are shifting the balance between the two major

categories.

In France, for example, men’s shaving continued to

decline in 2012, while men’s toiletries grew by 3%. A

similar trend was seen in Italy and Portugal. Difficult

economic climates have been affecting the

Eurozone countries in the south more strongly, with

consumers cutting back on their spending across all

categories. Furthermore, private label penetration in

countries like Spain is becoming increasingly strong.

In both Spain and Portugal, there is evidence of the

old perceptions of masculinity fading. UK men’s skin

care brand Bulldog entered the Spanish market in

summer 2012 through department store Corte

Inglés, while studies by the Spanish “Men’s Health”

magazine indicate that Spanish men are adopting

more sophisticated and purpose-specific grooming

products.

In the UK, the biggest category in 2012, after

razors and blades, was men’s deodorants, as

these two product types are seen as a standard

part of their hygiene regime. While some men are

happy to use unisex shampoo or unisex shower

gel, fewer are willing to use unisex deodorant, as

their fragrances are often too feminine. However,

there is evidence showing that this is changing.

In Germany, similarly to the UK, the market is

skewed towards men’s toiletries, with men’s

shaving accounting for around 40% of the market.

Within men’s toiletries in Germany, deodorants

lead, but sales of men’s hair care are also

considerable, at over US$300 million.

Men’s hair care is also the fastest growing

category in men’s grooming in both the UK and

Germany, indicating the change towards more

male-specific products.

Western Europe: A divided continent

REGIONAL ANALYSIS

© Euromonitor International PASSPORT 30 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

While the US remains the number one market in men’s grooming, valued at US$5.5 billion, many of its

categories have been in decline or are static.

The fastest growing categories, men’s hair care and men’s skin care are less than half the size of men’s

razor and blades which has been heavily influenced by the trend towards a more bearded look for men.

Despite men becoming more sophisticated in their grooming habits and looking for more premium male-

specific products, private label penetration has been increasing, with CVS, Wal-Mart and Walgreen private

label brands all featuring in the top 20 brands in men’s grooming.

The average unit price for men’s toiletries has dropped as a result of this.

-10

-8

-6

-4

-2

0

2

4

6

8

0

500

1,000

1,500

2,000

2,500

Men's Post-shave

Men's Pre-shave

Men's Razors and Blades

Men's Bath and Shower

Men's Deodorants

Men's Hair Care

Men's Skin Care

% g

row

th

Va

lue

(U

S$ m

illio

n)

US Men’s Grooming Market

2011 2012 2011/12 % CAGR 2007-12

North America: The US still the world’s largest market

REGIONAL ANALYSIS

© Euromonitor International PASSPORT 31 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

Men’s grooming in Latin America is largely concentrated in two categories, men’s razors and blades, and men’s deodorants.

Despite their already considerable size, men’s razor’s and blades grew by an impressive 23% in 2012, while sales of deodorants increased by 16%.

The small categories of bath and shower and skin care were the fastest growing overall in percentage terms. Bath and shower grew by over 50%, as men in Latin America are starting to look more for male-specific products. This is in line with the total bath and shower market where Brazil is the world’s second largest market and Latin America is expected to add another US$1 billion in value by 2017.

Innovations like the latest bar soap line by Procter & Gamble’s Old Spice, a top 10 men’s deodorant brand in Latin America, is slowly changing the landscape, bringing the humour factor and spark from the deodorants’ category into men’s bath and shower.

The popularity of deodorants in

Latin America has given

deodorant brands from Axe/Lynx

to Old Spice a good base to

work from. Consumers trust

these brands, and their unusual

and assertive campaigns appear

to appeal to men and translate to

sales. Axe/Lynx has now

expanded into skin care, after

having expanded into hair care a

couple of years ago.

Deodorants and razors generate largest revenues in Latin America

REGIONAL ANALYSIS

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Men's Post-Shave

Men's Pre-Shave

Men'sRazors and

Blades

Men's Bath andShower

Men'sDeodorants

Men's HairCare

Men's SkinCare

Va

lue

(U

S$ m

illio

n)

Men’s Grooming in Latin America 2011-2012

2011 Absolute growth in 2012

© Euromonitor International PASSPORT 32 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

0

2

4

6

8

10

12

0

500

1,000

1,500

2,000

2,500

Argentina Brazil Mexico Peru Venezuela

US

$

US

$ m

illio

n

Men’s Razors and Blades in Latin America: Top Five Markets 2012

Value Per Capita Spending

0

10

20

30

40

50

60

70

80

90

Argentina Brazil Mexico Venezuela

% v

alu

e 2

01

2

Men’s Razors and Blades Breakdown in Top Markets 2012

Disposables Systems-Razors Systems-Refills

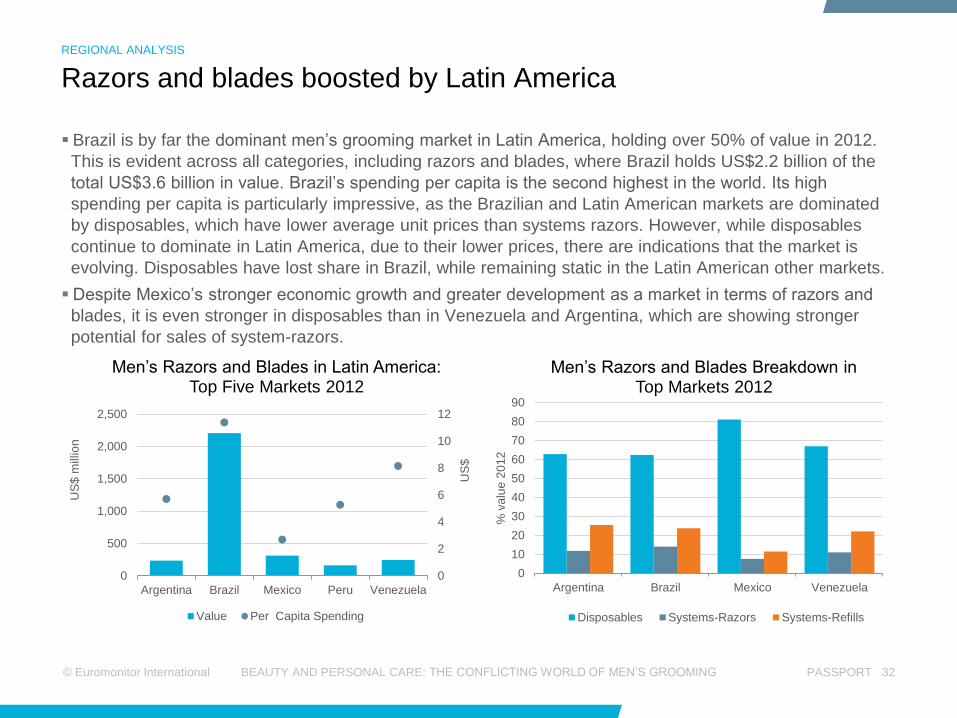

Brazil is by far the dominant men’s grooming market in Latin America, holding over 50% of value in 2012.

This is evident across all categories, including razors and blades, where Brazil holds US$2.2 billion of the

total US$3.6 billion in value. Brazil’s spending per capita is the second highest in the world. Its high

spending per capita is particularly impressive, as the Brazilian and Latin American markets are dominated

by disposables, which have lower average unit prices than systems razors. However, while disposables

continue to dominate in Latin America, due to their lower prices, there are indications that the market is

evolving. Disposables have lost share in Brazil, while remaining static in the Latin American other markets.

Despite Mexico’s stronger economic growth and greater development as a market in terms of razors and

blades, it is even stronger in disposables than in Venezuela and Argentina, which are showing stronger

potential for sales of system-razors.

Razors and blades boosted by Latin America

REGIONAL ANALYSIS

© Euromonitor International PASSPORT 33 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

While Brazil’s dominance is unquestionable, the possibility of slower

growth in the country has increased the importance of building

stronger positions in smaller but potentially faster growing emerging

markets.

Despite Venezuela’s high inflation issues, the market has potential,

given rising disposable incomes and the increasing sophistication of

the market. This is exemplified by the healthy real terms growth of

men’s skin care in 2012, of nearly 8%, as well as the return to growth

of both men’s pre- and men’s post shave.

Mexico has a more developed economy than Argentina and

Venezuela, and in 2012 its economy grew four times faster than

Brazil’s. This strong performance is expected to continue in the short

to medium term future, at least. In 2012, Mexico’s retail spending on

men’s grooming increased by 14%, and Argentina’s by 26%. Looking

ahead, in absolute real terms spending between 2012 and 2017, they

are forecast to increase by US$198 million and US$114 million,

respectively.

Evidence of the mushrooming middle class in these two countries is

seen in category growth rates, which show how consumers are

becoming more sophisticated in their choices. In Mexico, men’s skin

care (although still a niche) grew from US$7 million in 2007 to US$42

million in 2012. Similarly, in Argentina, men’s pre-shave grew from

US$15 million in 2007 to 42 million in 2012.

Men’s Grooming Absolute Growth 2007-2012

Argentina

Brazil

Mexico

Venezuela

Others

Beyond Brazil? Mexico, Argentina and Venezuela

REGIONAL ANALYSIS

© Euromonitor International PASSPORT 34 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

0

5

10

15

20

25

0

50

100

150

200

250

300

350

Algeria Cameroon Egypt Iran Israel Kenya Morocco Nigeria SaudiArabia

SouthAfrica

Tunisia UnitedArab

Emirates

% C

AG

R

US

$ m

illio

n

Men’s Grooming in the Middle East and Africa

Value % CAGR 2007-12

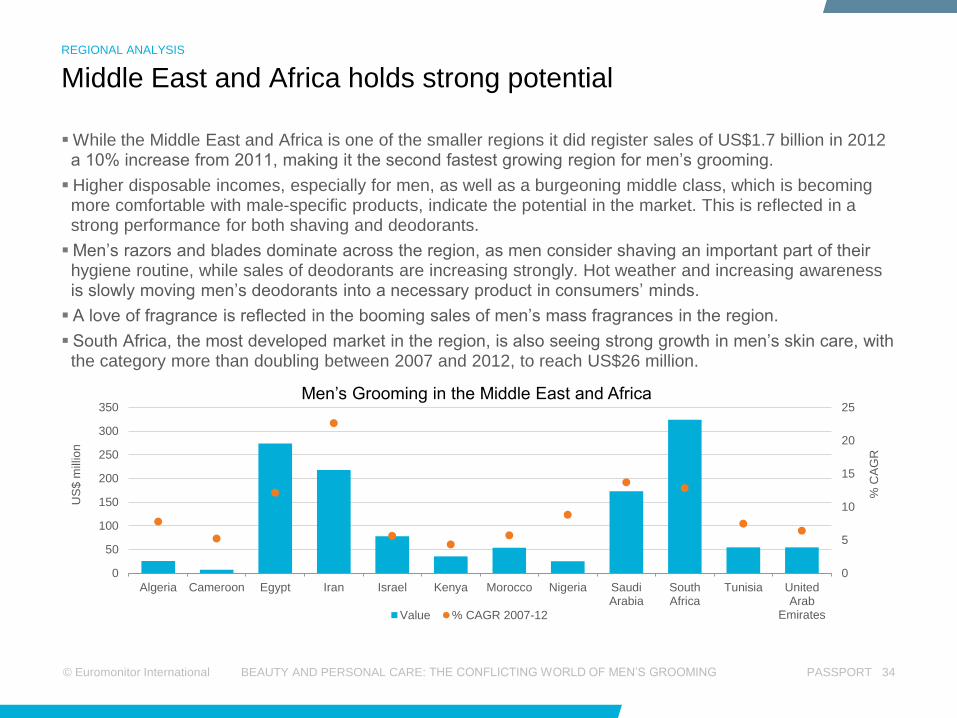

While the Middle East and Africa is one of the smaller regions it did register sales of US$1.7 billion in 2012 a 10% increase from 2011, making it the second fastest growing region for men’s grooming.

Higher disposable incomes, especially for men, as well as a burgeoning middle class, which is becoming more comfortable with male-specific products, indicate the potential in the market. This is reflected in a strong performance for both shaving and deodorants.

Men’s razors and blades dominate across the region, as men consider shaving an important part of their hygiene routine, while sales of deodorants are increasing strongly. Hot weather and increasing awareness is slowly moving men’s deodorants into a necessary product in consumers’ minds.

A love of fragrance is reflected in the booming sales of men’s mass fragrances in the region.

South Africa, the most developed market in the region, is also seeing strong growth in men’s skin care, with the category more than doubling between 2007 and 2012, to reach US$26 million.

Middle East and Africa holds strong potential

REGIONAL ANALYSIS

INTRODUCTION

INDUSTRY OVERVIEW

CATEGORY ANALYSIS

REGIONAL ANALYSIS

CHANNEL ANALYSIS

INNOVATION STRATEGIES

FUTURE PROSPECTS

© Euromonitor International PASSPORT 36 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

Supermarkets lead sales in men’s grooming, as men tend to pick up their necessary grooming products as part of their weekly shopping trip. However, they saw only slow growth in 2012, as beauty specialists and drugstores upped their offerings in men grooming products. There have been larger retail spaces dedicated to men’s products, and men’s products have also been moved to the front of the store so they are more visible.

Exclusive launches are becoming increasingly common, like Coty’s new adidas personal care for men collection (a range of deodorants, body washes, antiperspirants and body sprays) available exclusively at Wal-Mart. Exclusive launches are becoming a more widely used strategy for men’s grooming retailers as a way to increase footfall.

Despite the internet’s dynamic growth, it still holds only a very small share of the market. While the internet has maintained its strong momentum, department stores declined in 2012, as premium brands are becoming increasingly available in drugstores, beauty specialists and online.

The online channel has been detrimental to department stores, since value for money is a big factor for men. Blogs like “Men’s grooming review” provide not only reviews on products, but also state where the particular product is sold at the lowest price.

Supermarkets continue to lead while department stores decline

CHANNEL ANALYSIS

-10

0

10

20

30

0

10

20

30

Hyper-markets

Super-markets

Beauty Specialists

Chemists/Pharmacies

Parapharmacies/Drugstores

Department Stores

Direct Selling

Internet Retailing

% g

row

th

% v

ale

Distribution Channels in Men’s Grooming 2007/2012

2007 2012 2011-12

© Euromonitor International PASSPORT 37 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

0

1,000

2,000

3,000

4,000

5,000

Hypermarkets/Supermarkets

Beauty Specialists

Chemists/Parapharmacies

Department Stores

DirectSelling

Internet

US

$ m

illio

n

Distribution by Region 2012

Asia Pacific Australasia Eastern Europe Latin America Middle East and Africa North America Western Europe

Both Asia Pacific and Latin America have significant sales through direct selling, while Asia Pacific is also the most important region for department stores. This impacts brand strategies. UK men’s skin care brand Bulldog normally sells through supermarkets, but in South Korea it chose to enter the market through department stores. This puts it in competition against premium skin care brands, such as Clarins for Men and Clinique for Men.

Latin America continues to be a strong region for direct sellers, as is Asia Pacific. Direct seller Natura’s strength in Latin America in men’s deodorants has elevated it to the sixth largest brand in the world in men’s deodorants.

Internet sales are of particular importance in North America, Western Europe and Asia Pacific. For men’s skin care companies in particular, it is a significant medium through which they can educate, as well as sell their products to consumers. More retailers are tapping into the lucrative men’s grooming market, such as mr-porter.com, an online luxury men’s e-retailer, which has recently added Aesop grooming sets as part of its offering, while also collaborating with the Australian brand for a set that is exclusively made for the e-retailer.

Asia leads department stores and internet sales in men’s grooming

CHANNEL ANALYSIS

© Euromonitor International PASSPORT 38 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

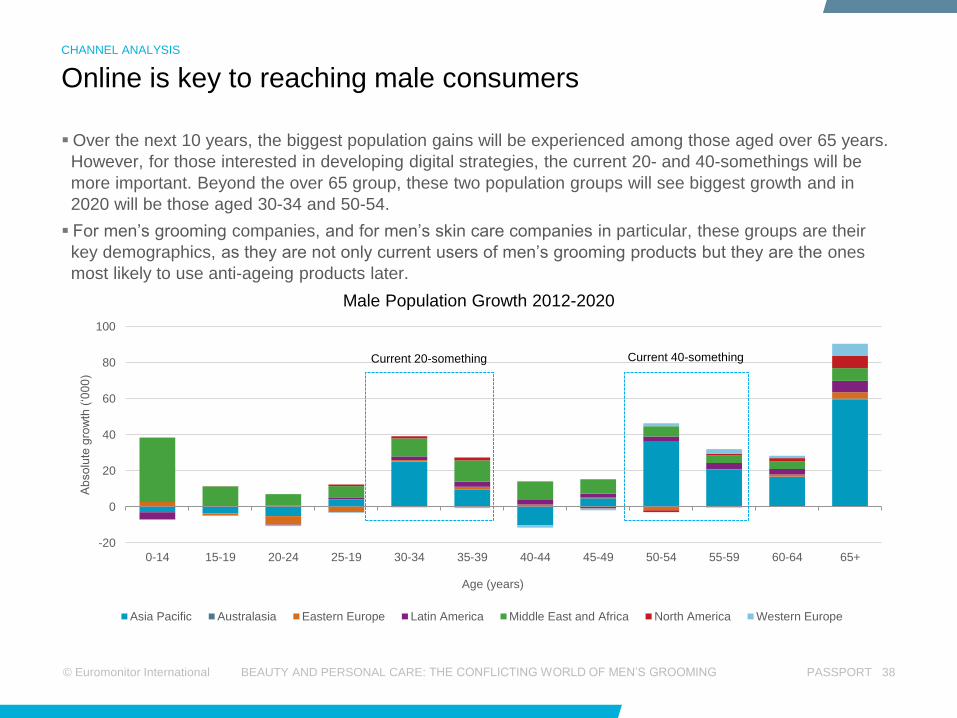

Over the next 10 years, the biggest population gains will be experienced among those aged over 65 years.

However, for those interested in developing digital strategies, the current 20- and 40-somethings will be

more important. Beyond the over 65 group, these two population groups will see biggest growth and in

2020 will be those aged 30-34 and 50-54.

For men’s grooming companies, and for men’s skin care companies in particular, these groups are their

key demographics, as they are not only current users of men’s grooming products but they are the ones

most likely to use anti-ageing products later.

-20

0

20

40

60

80

100

0-14 15-19 20-24 25-19 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65+

Ab

so

lute

gro

wth

(‘0

00

)

Age (years)

Male Population Growth 2012-2020

Asia Pacific Australasia Eastern Europe Latin America Middle East and Africa North America Western Europe

Current 20-something Current 40-something

Online is key to reaching male consumers

CHANNEL ANALYSIS

© Euromonitor International PASSPORT 39 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

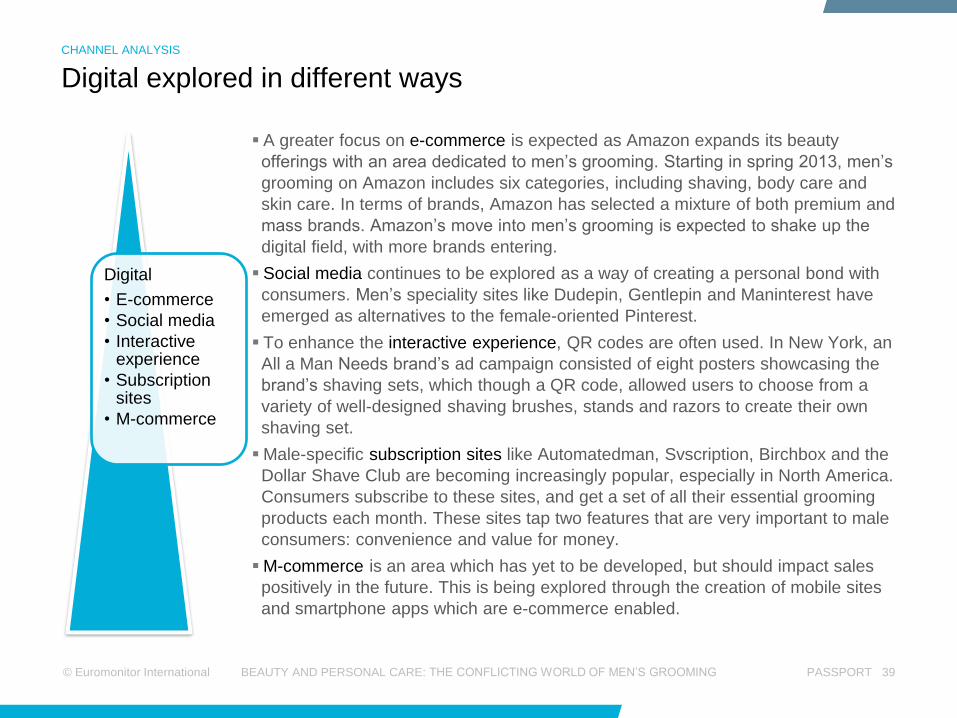

Digital

• E-commerce

• Social media

• Interactive experience

• Subscription sites

• M-commerce

A greater focus on e-commerce is expected as Amazon expands its beauty

offerings with an area dedicated to men’s grooming. Starting in spring 2013, men’s

grooming on Amazon includes six categories, including shaving, body care and

skin care. In terms of brands, Amazon has selected a mixture of both premium and

mass brands. Amazon’s move into men’s grooming is expected to shake up the

digital field, with more brands entering.

Social media continues to be explored as a way of creating a personal bond with

consumers. Men’s speciality sites like Dudepin, Gentlepin and Maninterest have

emerged as alternatives to the female-oriented Pinterest.

To enhance the interactive experience, QR codes are often used. In New York, an

All a Man Needs brand’s ad campaign consisted of eight posters showcasing the

brand’s shaving sets, which though a QR code, allowed users to choose from a

variety of well-designed shaving brushes, stands and razors to create their own

shaving set.

Male-specific subscription sites like Automatedman, Svscription, Birchbox and the

Dollar Shave Club are becoming increasingly popular, especially in North America.

Consumers subscribe to these sites, and get a set of all their essential grooming

products each month. These sites tap two features that are very important to male

consumers: convenience and value for money.

M-commerce is an area which has yet to be developed, but should impact sales

positively in the future. This is being explored through the creation of mobile sites

and smartphone apps which are e-commerce enabled.

Digital explored in different ways

CHANNEL ANALYSIS

INTRODUCTION

INDUSTRY OVERVIEW

CATEGORY ANALYSIS

REGIONAL ANALYSIS

CHANNEL ANALYSIS

INNOVATION STRATEGIES

FUTURE PROSPECTS

© Euromonitor International PASSPORT 41 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

0

10

20

30

40

50

60

70

80

Good health Supportivefamily

Rewarding job Financialsecurity

Friends Long-termgoal

Status Being wealthy Children Spiritualbeliefs

% M

en

ag

ed

15

-29

Euromonitor International Annual Study: Young Men’s Attitudes Towards Health, Fitness and Wellbeing. What is the Most Important Factor to a Happy Life?

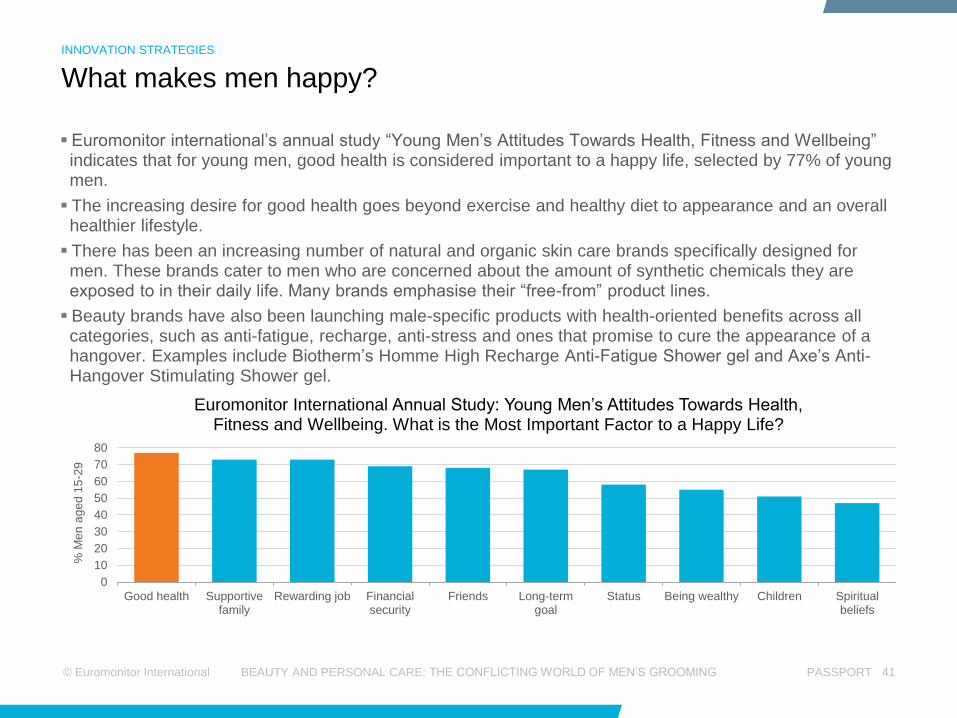

Euromonitor international’s annual study “Young Men’s Attitudes Towards Health, Fitness and Wellbeing” indicates that for young men, good health is considered important to a happy life, selected by 77% of young men.

The increasing desire for good health goes beyond exercise and healthy diet to appearance and an overall healthier lifestyle.

There has been an increasing number of natural and organic skin care brands specifically designed for men. These brands cater to men who are concerned about the amount of synthetic chemicals they are exposed to in their daily life. Many brands emphasise their “free-from” product lines.

Beauty brands have also been launching male-specific products with health-oriented benefits across all categories, such as anti-fatigue, recharge, anti-stress and ones that promise to cure the appearance of a hangover. Examples include Biotherm’s Homme High Recharge Anti-Fatigue Shower gel and Axe’s Anti-Hangover Stimulating Shower gel.

What makes men happy?

INNOVATION STRATEGIES

© Euromonitor International PASSPORT 42 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

Extra benefits boost men’s

skin care

Skin care becomes multi-functional

INNOVATION STRATEGIES

Moisturising

Anti-acne

Anti-ageing

Self-tanning

Skin lightening

Sensitive skin

Natural ingredients

Oil control

Sun protection

Men’s skin care was the most dynamic category in 2012, experiencing double-digit growth. Fuelling growth was the increase in features in men’s skin care, which have been replicated from women’s skin care, for example skin lightening, oil control and anti-ageing.

With almost 60% of total men’s skin care sales derived from Asia Pacific, the region’s dominance is influencing innovation, with skin lightening featuring as a key benefit in men’s skin care due to the regional preference for fair skin. The success of both Unilever’s Fair & Lovely and Emami’s Fair & Handsome in India exemplifies this.

As more men are learning about their skin, many are looking for male-specific products. This has helped the men’s skin care category to grow more strongly than men’s bath and shower and men’s hair care, where more men are still using unisex products and find it harder to see the added benefits of using a male-specific product. Problem-solvers by nature, men prefer products that can solve all their skin care problems in one easy step. This has led to the rise of roll-ons for eye creams and multi-purpose products like Lab Series BB tinted moisturiser for men.

The fact that men are typically reluctant to use sunscreen or to care for their skin at all can be a challenging combination, and men’s skin care brands’ main focus is to get men to start using skin care products, as adoption is still low in most of the world. The addition of sun protection in men’s skin care products provides both convenience and extra value to men, and can be an area of further development.

© Euromonitor International PASSPORT 43 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

Increasing sophistication in

men’s skin care is exemplified

by Estée Lauder-owned

Clinique now offering a Dark

Spot Corrector in its Skin

Supplies for Men range, as well

as two items to treat the eye-

contour area. Aramis Lab

Series’ Max LS, the brand’s anti-

ageing range, includes an

overnight anti-ageing serum,

while P&G’s premium The Art of

Shaving range now offers a

hydrating toner and a camomile

essential oil-based Eye Gel.

L’Oréal-owned Kiehl’s range for

men has a string of products

that are claimed to combat loss

of density in the skin, age spots

and deep wrinkles.

More sophisticated lines

Packaging in men’s skin care

has traditionally played a key

role in how companies position

themselves. In terms of colours,

blue, silver, grey and black are

dominant.

Nivea changed its packaging a

couple of years ago from white

to blue, to look more “manly”.

A more recent example is Dove,

with Dove Men and Care in grey

packaging instead of the

traditional white.

There is likely to be more

diversification in application

formats, similar to those in the

female market, such as roll-ons

and stick formats.

Packaging a key factor

L’Oréal Paris Men Expert is

among the brands using

celebrity spokespeople,

including the actors Pierce

Brosnan, known from the Bond

Films, and Gerald Butler.

Celebrity endorsements are

particularly popular in countries

like India where Bollywood is

almost like a religion. Brands

like Fair and Handsome have

been using Bollywood actors to

promote their skin lightening

products.

Celebrity endorsements

Inspiration from female skin care

INNOVATION STRATEGIES

© Euromonitor International PASSPORT 44 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

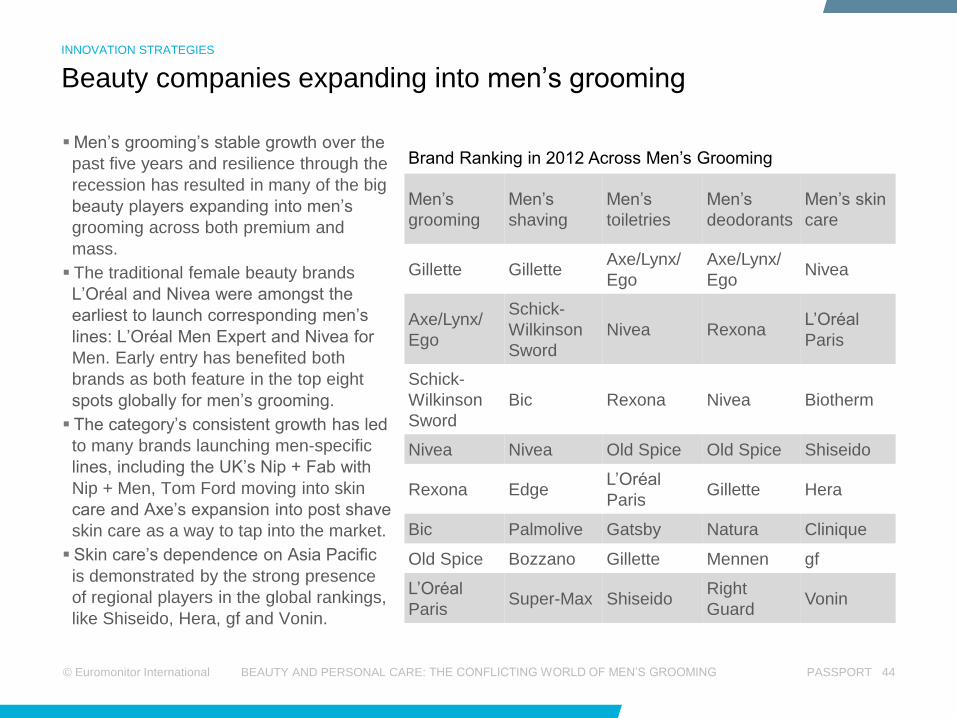

Men’s grooming’s stable growth over the

past five years and resilience through the

recession has resulted in many of the big

beauty players expanding into men’s

grooming across both premium and

mass.

The traditional female beauty brands

L’Oréal and Nivea were amongst the

earliest to launch corresponding men’s

lines: L’Oréal Men Expert and Nivea for

Men. Early entry has benefited both

brands as both feature in the top eight

spots globally for men’s grooming.

The category’s consistent growth has led

to many brands launching men-specific

lines, including the UK’s Nip + Fab with

Nip + Men, Tom Ford moving into skin

care and Axe’s expansion into post shave

skin care as a way to tap into the market.

Skin care’s dependence on Asia Pacific

is demonstrated by the strong presence

of regional players in the global rankings,

like Shiseido, Hera, gf and Vonin.

Brand Ranking in 2012 Across Men’s Grooming

Men’s

grooming

Men’s

shaving

Men’s

toiletries

Men’s

deodorants

Men’s skin

care

Gillette Gillette Axe/Lynx/

Ego

Axe/Lynx/

Ego Nivea

Axe/Lynx/

Ego

Schick-

Wilkinson

Sword

Nivea Rexona L’Oréal

Paris

Schick-

Wilkinson

Sword

Bic Rexona Nivea Biotherm

Nivea Nivea Old Spice Old Spice Shiseido

Rexona Edge L’Oréal

Paris Gillette Hera

Bic Palmolive Gatsby Natura Clinique

Old Spice Bozzano Gillette Mennen gf

L’Oréal

Paris Super-Max Shiseido

Right

Guard Vonin

Beauty companies expanding into men’s grooming

INNOVATION STRATEGIES

© Euromonitor International PASSPORT 45 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

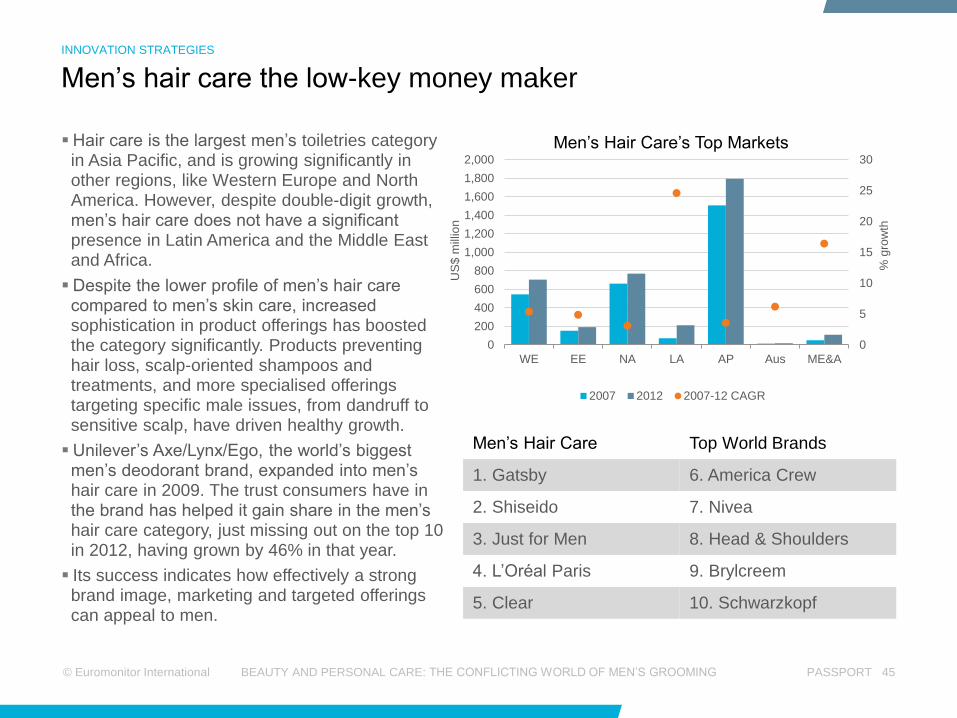

Hair care is the largest men’s toiletries category in Asia Pacific, and is growing significantly in other regions, like Western Europe and North America. However, despite double-digit growth, men’s hair care does not have a significant presence in Latin America and the Middle East and Africa.

Despite the lower profile of men’s hair care compared to men’s skin care, increased sophistication in product offerings has boosted the category significantly. Products preventing hair loss, scalp-oriented shampoos and treatments, and more specialised offerings targeting specific male issues, from dandruff to sensitive scalp, have driven healthy growth.

Unilever’s Axe/Lynx/Ego, the world’s biggest men’s deodorant brand, expanded into men’s hair care in 2009. The trust consumers have in the brand has helped it gain share in the men’s hair care category, just missing out on the top 10 in 2012, having grown by 46% in that year.

Its success indicates how effectively a strong brand image, marketing and targeted offerings can appeal to men.

Men’s Hair Care Top World Brands

1. Gatsby 6. America Crew

2. Shiseido 7. Nivea

3. Just for Men 8. Head & Shoulders

4. L’Oréal Paris 9. Brylcreem

5. Clear 10. Schwarzkopf

0

5

10

15

20

25

30

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

WE EE NA LA AP Aus ME&A

% g

row

th

US

$ m

illio

n

Men’s Hair Care’s Top Markets

2007 2012 2007-12 CAGR

Men’s hair care the low-key money maker

INNOVATION STRATEGIES

© Euromonitor International PASSPORT 46 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

Colour cosmetics tapping into the men’s grooming market

INNOVATION STRATEGIES

Following the trend from women’s skin care, as well as due to

greater acceptance of cosmetics in Asia Pacific, there has been

an increasing number of colour cosmetics products targeted at

men.

BB creams, like Lab Series for Men, a hybrid product between

skin care, sun care and colour cosmetics, provide a good

testing platform for men’s propensity for colour. If BB creams

manage to become successful in men’s grooming, then they

will be a stepping stone into introducing men to colour

cosmetics. Hybrid products that lie in between three categories

offer an all-in-one solution to the perfect skin, thus adding value

and providing convenience. Although in Asia Pacific, and in

particular in South Korea, it is considered more of a norm to

wear facial make-up, there is still a long way to go before this

category is seen in a similar way in Western Europe and North

America.

In the US, in 2009, Blakk Cosmetics launched Alpha nail paint

which is a nail polish line for men, with colours called Burning

Rubber and Gasoline. While this is a very niche category, many

male celebrities have embraced it, such asJohnny Depp and

Zac Efron. More niche players are moving into this category,

describing their nail polishes as temporary tattoos and as a way

for men to express their individuality.

Men’s skin care

Men’s BB creams

Men’s colour

cosmetics

INTRODUCTION

INDUSTRY OVERVIEW

CATEGORY ANALYSIS

REGIONAL ANALYSIS

CHANNEL ANALYSIS

INNOVATION STRATEGIES

FUTURE PROSPECTS

© Euromonitor International PASSPORT 48 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

US

$ m

illio

n, co

nsta

nt rs

p

Value Sales 2000-2017

Men's toiletries

Men's shaving

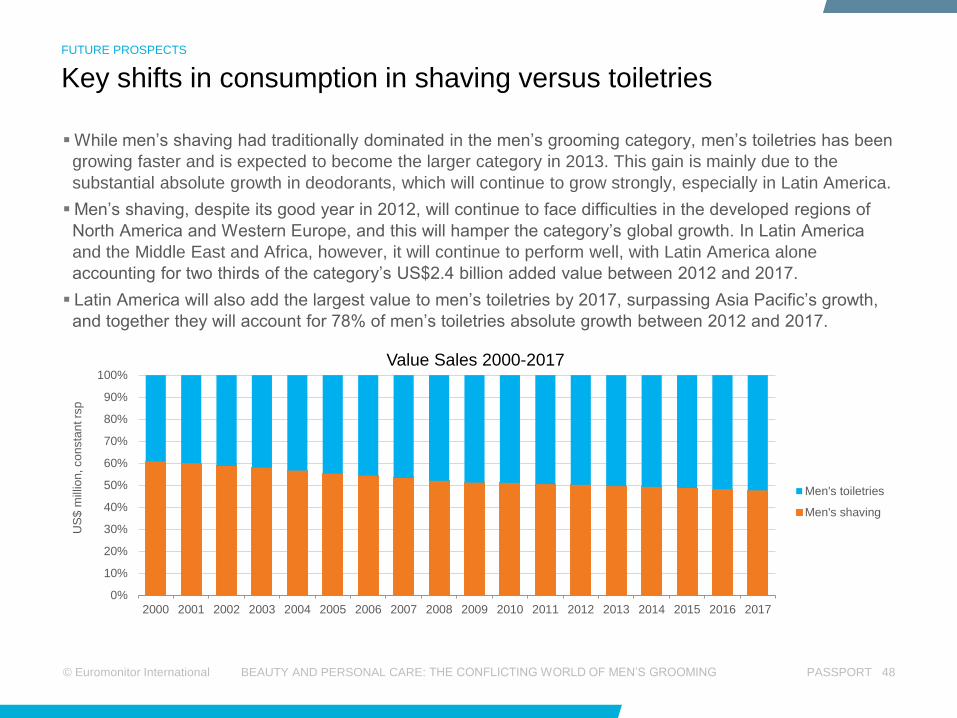

While men’s shaving had traditionally dominated in the men’s grooming category, men’s toiletries has been

growing faster and is expected to become the larger category in 2013. This gain is mainly due to the

substantial absolute growth in deodorants, which will continue to grow strongly, especially in Latin America.

Men’s shaving, despite its good year in 2012, will continue to face difficulties in the developed regions of

North America and Western Europe, and this will hamper the category’s global growth. In Latin America

and the Middle East and Africa, however, it will continue to perform well, with Latin America alone

accounting for two thirds of the category’s US$2.4 billion added value between 2012 and 2017.

Latin America will also add the largest value to men’s toiletries by 2017, surpassing Asia Pacific’s growth,

and together they will account for 78% of men’s toiletries absolute growth between 2012 and 2017.

Key shifts in consumption in shaving versus toiletries

FUTURE PROSPECTS

© Euromonitor International PASSPORT 49 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Men's shaving Men's post-shave

Men's pre-shave

Men's razorsand blades

Men's toiletries Men's bathand shower

Men'sdeodorants

Men's haircare

Men's skincare

Ab

so

lute

gro

wth

(U

S$

mill

ion

, co

nsta

nt 2

01

2 r

sp

)

Category Value Growth 2012-2017

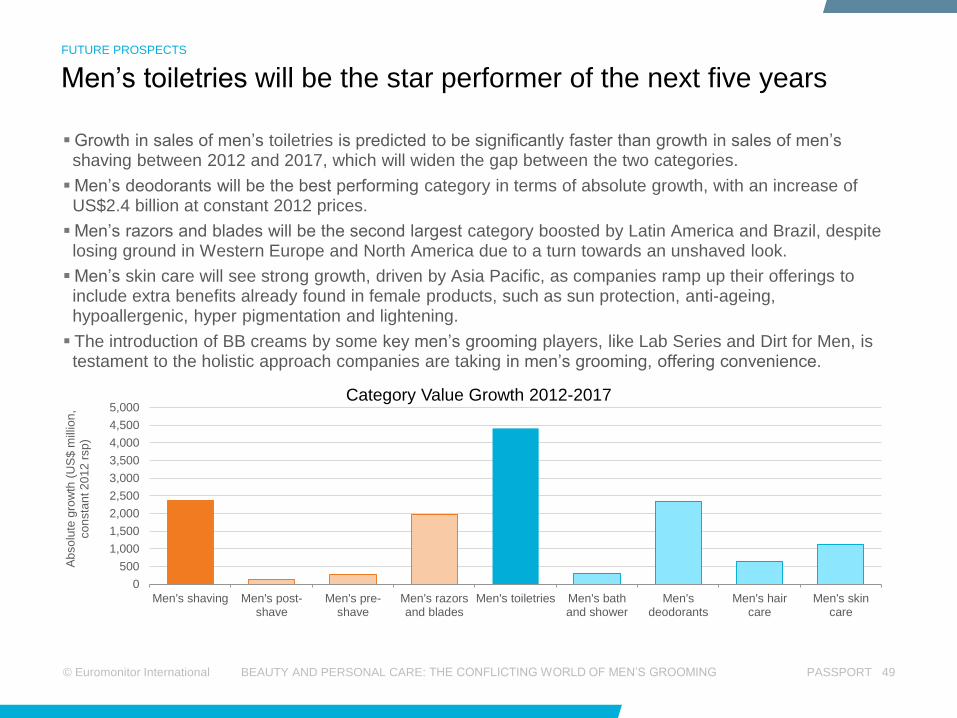

Growth in sales of men’s toiletries is predicted to be significantly faster than growth in sales of men’s shaving between 2012 and 2017, which will widen the gap between the two categories.

Men’s deodorants will be the best performing category in terms of absolute growth, with an increase of US$2.4 billion at constant 2012 prices.

Men’s razors and blades will be the second largest category boosted by Latin America and Brazil, despite losing ground in Western Europe and North America due to a turn towards an unshaved look.

Men’s skin care will see strong growth, driven by Asia Pacific, as companies ramp up their offerings to include extra benefits already found in female products, such as sun protection, anti-ageing, hypoallergenic, hyper pigmentation and lightening.

The introduction of BB creams by some key men’s grooming players, like Lab Series and Dirt for Men, is testament to the holistic approach companies are taking in men’s grooming, offering convenience.

Men’s toiletries will be the star performer of the next five years

FUTURE PROSPECTS

© Euromonitor International PASSPORT 50 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

With men’s toiletries growing at almost double

the pace of men’s shaving, companies will

continue to concentrate on innovation, as

competition intensifies

Innovation in men’s toiletries will continue to

centre around benefits and claims associated

with:

– Health, such as dry scalp, sensitive skin and

hair loss, which will drive sales of both men’s

hair care and men’s skin care, as men continue

to look for more health benefits in their products.

– Products providing specific solutions for acne

prone skin, oil control or skin lightening, which

will be more concentrated in men’s skin care.

– Offerings which provide a basic and simple

skin care routine. The success of UK brand

Bulldog and its recent entry in the South Korean

market indicate that men find a simple and

straightforward positioning appealing, both in

terms of marketing message and packaging.

Innovation focus becomes more targeted in men’s toiletries

FUTURE PROSPECTS

Health

Simple Solutions

Focus

© Euromonitor International PASSPORT 51 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

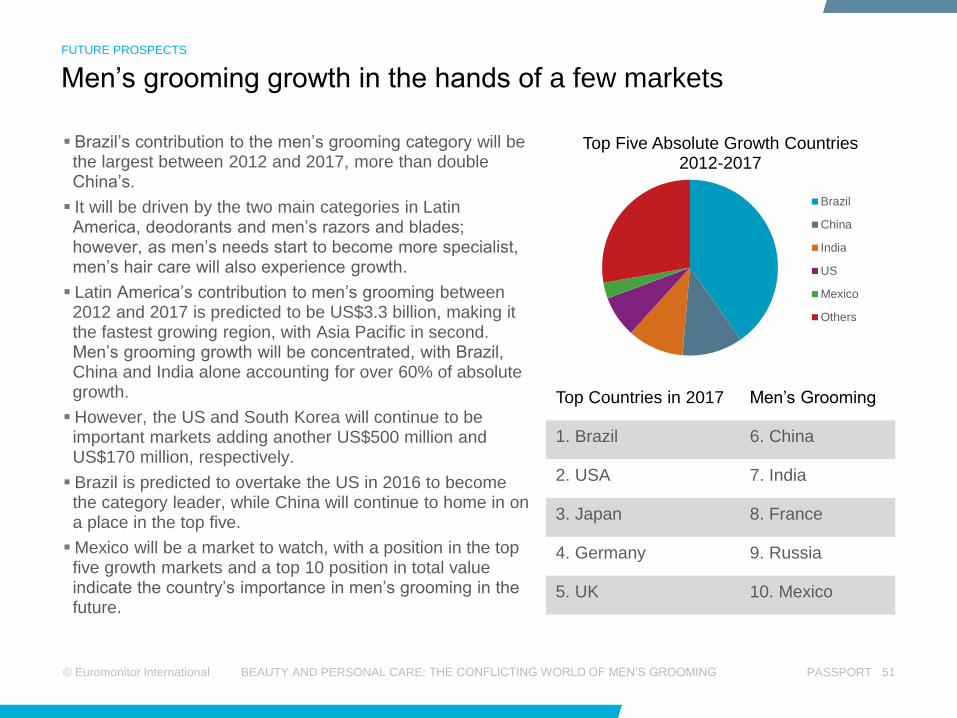

Brazil’s contribution to the men’s grooming category will be the largest between 2012 and 2017, more than double China’s.

It will be driven by the two main categories in Latin America, deodorants and men’s razors and blades; however, as men’s needs start to become more specialist, men’s hair care will also experience growth.

Latin America’s contribution to men’s grooming between 2012 and 2017 is predicted to be US$3.3 billion, making it the fastest growing region, with Asia Pacific in second. Men’s grooming growth will be concentrated, with Brazil, China and India alone accounting for over 60% of absolute growth.

However, the US and South Korea will continue to be important markets adding another US$500 million and US$170 million, respectively.

Brazil is predicted to overtake the US in 2016 to become the category leader, while China will continue to home in on a place in the top five.

Mexico will be a market to watch, with a position in the top five growth markets and a top 10 position in total value indicate the country’s importance in men’s grooming in the future.

Top Countries in 2017 Men’s Grooming

1. Brazil 6. China

2. USA 7. India

3. Japan 8. France

4. Germany 9. Russia

5. UK 10. Mexico

Top Five Absolute Growth Countries 2012-2017

Brazil

China

India

US

Mexico

Others

Men’s grooming growth in the hands of a few markets

FUTURE PROSPECTS

© Euromonitor International PASSPORT 52 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

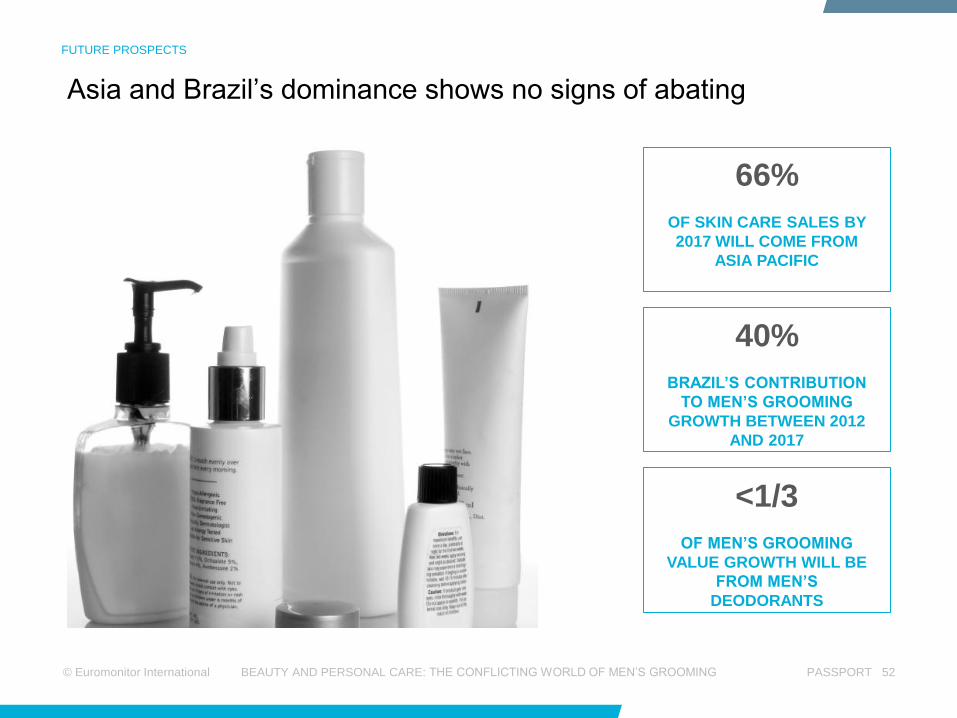

Asia and Brazil’s dominance shows no signs of abating

FUTURE PROSPECTS

66%

OF SKIN CARE SALES BY

2017 WILL COME FROM

ASIA PACIFIC

40%

BRAZIL’S CONTRIBUTION

TO MEN’S GROOMING

GROWTH BETWEEN 2012

AND 2017

<1/3

OF MEN’S GROOMING

VALUE GROWTH WILL BE

FROM MEN’S

DEODORANTS

© Euromonitor International PASSPORT 53 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

Men’s shaving loses domination to men’s

toiletries

Deodorants lead growth despite low penetration

in Asia Pacific

As Western Europe and North America continue to

struggle, men’s shaving will lose share to men’s

toiletries, which is experiencing faster growth in

these regions. Brazil will continue to lead growth in

men’s shaving, while India, Russia and Mexico will

also be vital markets for this category.

The recent trend which favours the unshaven look

opens new opportunities for innovation, such as

male-specific products ranging from manual/battery

trimmers, like Gillette’s Pro-Glider 3-in-1 Trimmer,

to colourants for facial hair, conditioning

gels/foams/lotions, styling gels, etc. The electric

hair appliances market is also expected to benefit

from the trend for facial hair.

As disposable brands like BIC and SuperMax

launch more sophisticated products, such as

double edge razors and three razor disposable

systems, system razor brands like Gillette and

Schick are expected to keep moving upwards in

the price range to compensate for volume losses.

While deodorants will lead in absolute growth

terms between 2012 and 2017, men’s deodorants

still remain largely undeveloped in the Middle East

Africa, Eastern Europe and Asia Pacific, where

awareness of such products is still low. Given

Brazil’s expected saturation and slowdown, more

focus is expected to be given to raising awareness

in other emerging regions.

Further alignment with fragrances will be beneficial

for the Middle East market, while incorporating skin

care benefits may increase penetration in Asia

Pacific.

Saudi Arabia and UAE, where both men’s

fragrances and men’s deodorants are growing

strongly, are likely to get more attention from

companies in these product categories.

Key opportunities and recommendations

FUTURE PROSPECTS

© Euromonitor International PASSPORT 54 BEAUTY AND PERSONAL CARE: THE CONFLICTING WORLD OF MEN’S GROOMING

Hair care becomes more specialised Skin care’s challenges in Asia

The US and China are predicted to be the leading

markets in absolute growth terms for hair care

between 2012 and 2017.

In particular, the US, the world’s largest premium

hair care market, is of the highest importance to

premium men’s hair care players, with over two

thirds of all sales in 2017 coming from the US

alone.

Further specialisation, with more products

targeting specific concerns from dandruff, hair

volume and scalp treatments, should boost the

category further.

Asia Pacific will continue to dominate men’s skin

care, with over 60% of sales in 2017 coming from

this region.

However, there are challenges for international

men’s skin care players, as many of the fastest

growing markets, such as Thailand, Indonesia and

South Korea, are strongly dominated by local

players.

While some international brands are already strong

players in China, local and regional brands are

major competitors. Local brands benefit from

specialisation in whitening skin care products

and/or natural ingredients, as well as higher

awareness from the female version of the brands,

coupled with lower prices.

With men’s skin care penetration still very low,

companies should look to educate men on the

advantages of such products. Increasing sampling