Italian Association for the Development of Biotechnology...

68

Blossom Associati - Assobiotec Report Italian Association for the Development of Biotechnology Biotechnology in Italy The Financial Perspective 2008

Transcript of Italian Association for the Development of Biotechnology...

Blossom Associati - Assobiotec Report

Italian Association for the Development of Biotechnology

Biotechnology in ItalyThe Financial Perspective

2008

blossomassociati.com

Leadership Finance Management

Companies and Individuals Development

Milan - Italy

MANAGEINNOVATION

Federica BottazziManaging Director

+39-02-80 50 50 [email protected]

BIOTECHNOLOGYIN ITALY 2008 Blossom Associati - Assobiotec Report

Blossom Associati srl. All rights reserved.

AUTHORISATION FOR DIVULGATION

All rights reserved for the divulgation and use of the data,information, translation, electronic storage, reproduction,and partial or total adaptation by any means(including microfilm and photocopies).

No data and information contained in this report maybe used or divulged without prior written authorisation.Blossom Associati may, at its own discretion, authorisesuch use upon request, on condition that the followingsource is cited:

Report by Blossom Associati - Assobiotec 2008

Data sheets, charts or tables must, instead, state thesource indicated within the document.

Request for the reproduction of the data and informationcontained herein should be made by email to:

Object:request for the reproduction - Biotechnology in Italy 2008

Massimo BorieroMaria Adelaide BottaroFederica BottazziAgostino CarloniMaria Grazia ChimentiMarina Del BueMaria Alessandra De LucaSergio DompéRita Nunzia FucciLaura GattoRoberto GradnikGianluigi LiberatiCorrado MaggiAlessandra ManciaLuca MartignoniNello MartiniStefano MilaniFrancesca MondelloMaria Luisa NolliCeleste Martina PenatiAlessia PisoniAlberto OnettiMarco RenoldiDeryck RhodesCarlo RicciniFederica RovidaAlessandro SidoliMarco TalaiaUmberto VattaniLeonardo VingianiAntonella Zucchella

BIOTECHNOLOGY IN ITALY 2008

Acknowledgements:

AIFA

Assobiotec

Blossom Associati

CCIAA Varese

CIBIE (Center for Researchin International Businessand Economics)University of Pavia

CrESITUniversità dell’Insubria di Varese

Farmindustria

ICE

This handbook 2008is available online:www.blossomassociati.com

3Blossom Associati 2008

Innovating the concept of businessDear Friends and Customers,

2008: the Italian biotechnological sector is consolidating aphase of successful development, thus demonstrating its capacityto meet the challenge posed by the knowledge economy.The sector is in a rare state of ferment and pursuing a clear strategicobjective: integrating biotechnological and pharmaceutical companies,financial institutions and research institutes; a phenomenontaking place in Italy, as elsewhere in the world, and which couldgive rise to one of Europe’s leading biotechnological clusters.

At the close of 2007, the sector comprised 228 companies, of whichno less than 24 – meeting Blossom Associati-CrESIT’s methodologicalselection criteria – were accredited in that sole year. The sectorremains dominated by companies dedicated to health care (74%).The overall turnover of accredited companies exceeded 10 billioneuros, of which 4.8 billion generated by biotechnological products,representing a 11% growth rate in 2007.Biotechnological R&D investments totalled 1.3 billion - a 9%year-on-year increase. The employees of accredited sector companiesnumbered more than 26,000 (14,543 if we exclude accreditedPharma companies) of which over 6,600 in R&D. Overall, equitycapital rose 56%, while at 213% the sector posted a particularlystrong EBIT growth. In conclusion, financial indebtedness decreased30%, shrinking to 1.6 billion euro.

All these indicators point to there being real growth prospects forsmall companies (75% of the accredited companies). However, theoverriding factor is the interest shown in the sector by medium-sizedand large companies, which generate 97% of the entire Biotech sector’ssales and are responsible for 84% of R&D biotechnological investments.

Stefano MilaniCEO Blossom Associati

Alberto OnettiDirector CrESIT

To achieve a better understanding of the futurepotentialities of biotechnologies in Italy, the mostobvious course of action is to analyse thefoundations upon which the so-called Italianchallenge to the knowledge economy rests. Assector operators appreciate, Italy ranks among theleading countries in the international arena of thelife sciences. Its total pharmaceutical sales(pharmacies + hospitals) at ex-works prices amountto E 16.5 billion (2006 data, source IMS).The overall value of the pharmaceutical market (atex-works prices denominated in Euro) shows thatItaly is the third market in Europe, after Germanyand France and the fifth in the world, with theUSA and Japan occupying the first two positions(source IMS). In terms of employment, the sectorhas over 70,000 workers on its payroll (June2006), of whom over 6000 occupied in R&D.

599 clinical studies were conducted in Italy between2001 and 2007 on biotechnologically deriveddrugs (source AIFA, National Observatory on clinicaltrials), of which the main part was Phase II (42.2%)and Phase III (49.8%) with the remaining trialsin Phase IV (7.46%). In terms of numbers,the first three therapeutic areas of clinical trialsare oncology (34.4%) immunology and infectivediseases (10.8%) and haematology (9.4%).

4

The first has the objective of raising E 150 millionfor investment in technological transfer, theweakest link in the value-creation chain of theItalian economy. The second fund, on the otherhand, has E 45 million of its own fundsthanks to the involvement of the Tuscan bankingsystem and is focusing on biotechnologies forthe development of innovative start-ups.Alongside these funds, there is the Fondo Next,considered the best European practice as regardsequity funds, which was set up thanks to thesupport of Finlombarda and the Lombardy Region.The fund has raised E 37 million and investedthe money in three biotechnology companies.

Listed Italian biotech companies, all situatedin Lombardy:> NicOx: Listed in

November 1999 - France(Nouveau Marché - Euronext)

> Cell Therapeutics: Listed inJanuary 2004 - Italy(Italian stock exchange)

> Gentium: Listed inJune 2005 - US (NASDAQ,American stock exchange)

> BioXell: Listed inJune 2006 - Switzerland(BXLN.SW, ZÜRICH),

> Newron Pharmaceuticals: Listed inDecember 2006 - Switzerland(SWX, ZÜRICH)

> Cosmo Pharmaceuticals: Listed inMarch 2007 - Switzerland(COPN.SW, ZÜRICH),

> DiaSorin: Listed inJuly 2007 - Italy(Italian stock exchange)

> MolMed: Listed inMarch 2008 - Italy(Italian stock exchange)

In addition, there are the companies Biosearchand Novuspharma.The first is a biopharmaceutical companyset up as a spin-off by the managers of theLepetit Research Centre. In 1998, the fund3i invested E 13.5 million in the company andtook out 39% of the company's share capital.In July 2000, Biosearch was listed on theNew Market with an equity capital of aboutE 350 million.

As regards the operations of private equity andventure capital in Italy as a whole, the markethas now reached a consolidated maturity interms of the investment operations conducted,although there is still a significant delay asconcerns investments in the specific sectorof biotechnologies, especially in comparisonwith the other main European countries.However, the delays have been compensated inItaly by the bank foundations, which, in part, playthe role that venture capital plays outside Italy.TT Venture owned by the Fondazione Cariploand Toscana Innovazione belonging to MontePaschi di Siena are two examples of bank-ownedfunds recently set up in Italy.

Year N. CT %2001 2 0.32002 10 1.82003 20 3.42004 87 14.52005 130 21.72006 195 32.52007 155 25.8Total 599 100.0

Total CT involving drugs of biotechnological origin

Source: AIFA

5Blossom Associati 2008

In Italy, the science and technological parks inwhich biotechnologies operate constitute animportant asset in terms of scientific, technologicaland organisational skills. Moreover, the networkprovided by such parks performs a fundamentalrole in the development of the innovation supplychain. According to the latest analyses conductedby Blossom Associati, there are 7 science parksin Italy where biotechnologies are operative:the AREA Science Park, the Canavese BioindustryPark, the Parco Tecnologico Padano, the RafScience Park, the TLS Science Park, SardinaRicerche and the Insubrias Biopark of Gerenzano.

The data confirm the findings documentedin the previous edition of the Report: i.e. thatthe localisation of the biotech industry is directlyrelated to the co-presence of a series of differentindustrial and institutional factors – pharmaceuticalcompanies, research centres and structures,scientific and technological parks and incubators,hospitals and clinics, and also investors – whichby functioning together as a system stimulatethe development of new companies.

Venture Capitalists

Banks

IstitutionalInvestors

Stock Market

Business Angels

INVESTORS

Advisory

Financial

Legal

Human Resources

SERVICESPROVIDERS

Consortia

Hospital

Science Park

Universities

Bio-incubator

FUNDAMENTALRESEARCH

Related Companies

Applied Companies

COMPANIES

Istitutions

Local Istitutions

IndustrialAssociations

European Union

ISTITUTIONS

Biotechnologycompanies

CLUSTER

CapitalProfessional

Services

Fees

Fees

HumanResources

Interest,dividends

Legislative Support

EconomicDevelopmentEmployment

Know how Investments

In December 2003, Biosearch merged withVersicolor, a Californian company listed onNasdaq and the resulting company was calledVicuron, a fully integrated, global, pharmaceuticalcompany that was subsequently taken overby Pfizer in September 2005.Novuspharma, instead, started life as abiopharmaceutical company specialised in R&Don antitumour drugs. The group BoehringerMannheim sold it as a spin-off from its Monzadivision. The fund 3i invested E 18 millionin the company together with two other investorsand the management and employees ofNovuspharma became shareholders in thecompany through a stock option plan.Roche continued to act as strategic partner tothe company, guaranteeing the transfer andlicensing of important research project patents onwhich it retained option rights. In November 2002,it was listed on the New Market witha pre-money capital valuation of about E 360million and raised around E 160 million incapital subscriptions. In June 2003, the companymerged with the American Cell Therapeutics.

Listed Italian biotech companies (up to 2008)

Profile: Blossom Associati Corporate Finance

That these are particularly exciting times forItalian biotech companies is also demonstratedby the international agreements they haveentered into. Examples of these developments arethe agreement reached between Nerviano MedicalSciences and the American Genentech for 316million euros, the acquisition of Hunter-Flemingby Newron and the merger between Amgen andDompé which will lead to a biotech company witha strong research orientation and investments in2008 estimated at E 10.5 million.

Company Year of Listing Stock exchangeNicOx 1999 France - Nouveau

TrademarksEuronext

Biosearch 2000 Italian stock exchangeNovuspharma 2000 Italian stock exchangeCell Therapeutics 2004 Italian stock exchangeGentium 2005 USA - NASDAQ

Americanstock exchange

BioXell 2006 SwitzerlandSWX Zurich

Newron 2006 SwitzerlandSWX Zurich

Cosmo 2007 SwitzerlandSWX Zurich

DiaSorin 2007 Italian stock exchangeMolMed 2008 Italian stock exchange

Source: Blossom Associati - CrESIT

Discovery Preclinical Phase I Phase II Phase IIIPipeline Italy 2008 99 63 33 35 16

Source: Blossom Associati - Assobiotec

Furthermore, the sector’s characteristically strong territorialconcentration is also a local phenomenon. Thus, biotech companiesapart from polarising on a limited number of regions (Lombardy,Piedmont, Tuscany and Friuli Venezia Giulia), also tend to concentratein certain specific territorial areas within them. If we limit ourselvesto the case of Lombardy alone, we find that accredited companiesare principally situated in the area of Milan, with ramifications inComo, Varese, Lodi and Pavia, although all are situated within amaximum radius of 50 kilometres from the regional capital.

If we consider international empirical analyses, on the one hand,and, on the other, our accumulated experience of cooperation withmany companies as strategic advisor, we can illustrate some featuresthat characterise the managerial DNA of all the companies thatwe can define as “emergent companies”:> they invest in business ideas and products that do not

set limits upon their own growth potential or value(Business Innovation);

> they sustain the implementation of new ideas – innovationunderstood as the task of all persons within the organisation(Corporate Innovation);

> they demonstrate managerial capacity through the adoptionof strategic options and financially sustainable exit strategies(Managerial Innovation).

Finally, we would like to emphasise three structural problem areasthat in, our opinion, call for serious remedy, in Italy as elsewhere:> Corporate renovation to be understood as a crucial phase in the

innovation of not only products, processes and systems butalso corporate objectives and missions in order to guaranteethe attractiveness and ongoing advantage of companies if theyare to be able to compete at a global level (The Innovation of theBusiness Concept, Corporate Innovation, and Managerial Innovation).

> Certainty of the timeline to obtain authorisations and clinicaltrial permits, which can be achieved by borrowing the systemsand operating arrangements in use in other European countries.

> Rigour and the application of selective sector models in theprovision of financing while bearing in mind the universal needfor a new class of financial advisors and operators, as they havethe capacity to interpret and valuate such new business types.

These are the considerations that we would recommend our readersremember when they read the 2009 edition of the Report evaluatingthe operations conducted in the course of the year and describingthe performances of the best-accredited “emergent companies”.

6

7Blossom Associati 2008

The growth and consolidation of Italian biotech

The fourth edition of the report “Biotechnologies in Italy” provides expertswith an updated overview of the sector and a chance to critically appraise thedevelopmental process of the Italian biotech industry in recent years.

The phases through which the industry has developed as well as the objectiveshitherto reached in terms of the critical mass of companies, employees and salestestifies to the fact that the sector – comprising companies, scientific parks andresearch centres – has by now acquired the characteristics of a mature industry.The process is well known as other countries have passed through the same phases.Italian biotechnologies are undergoing a specific developmental phase characterisedby the ongoing growth of new corporate ventures but also, and more importantly, bythe consolidation of established companies, and the elimination of the weakest.

The undeniable maturity of the biotech sector is also demonstrated by a seriesof important factors. First the sector’s capacity to produce value has been reinforced,as testified by its sizeable pipeline, which, in a pharmaceutical context,translates into a constant increase in the number of products undergoing clinicaldevelopment (Phases I-II-II), and which are all the result of Italian research.The number of such products has practically tripled in only two years, rising from30 in March 2006 to 84 in March 2008 (a 280% growth rate). In particular,of the 84-biotech products undergoing clinical development, 33 are in Phase I,35 in Phase II, and 16 in Phase III. Moreover, 8 have received “orphan drugdesignation” (3 by EMEA and 5 by both EMEA and the FDA). These are mainlyproducts for use in the field of oncology. The remaining products refer to cardiovascularapplications. Italian biotech research, furthermore, can boast 63 products at apre-clinical developmental phase and 99 molecules at a discovery phase, whichaltogether constitute a solid foundation for the sector in the coming years.

A second element demonstrating the maturity of the sector is the progressivecapitalisation of the companies. A strong growth in capitalisation goeshand-in-hand with the increase in companies’ project development activities.Similarly, R&D investments are increasing and some important agreementscan be read in the light of these investments, as they bring Italian companies andinternational partners increasingly closer together.

In conclusion, there is the contribution made by the stock exchange. In a six-yearperiod, since 2001, five Italian biotechnological companies achieved a listingon the principal international markets. In March 2008, a sixth company managedto be listed on the Milan stock exchange. This is not an insignificant achievementif it is considered that the first listings – and for considerable time the onlylistings – go back to the period 1999-2000, the time of the ‘new economy’ boom.

Certainly, the path is still long and major investments in biotechnological innovation,which has shown itself capable of generating wealth, jobs and wellbeing, is stillnecessary. In terms of the national economy the challenge is, therefore, to sustainand realise the potentialities of the Italian sector through strong and strategicindustrial policy decisions, in both the medium and the long term, capable ofattracting ever-higher investment flows. In the same manner, it is necessary tosupport whoever has an original idea and transform it into a corporate reality.For this purpose, Assobiotec has launched “Sportello Biotech”, (the Biotech Desk)a new area of its internet site, offering free information for the creation ofstart-ups and spin-offs in the biotechnology sector. Similarly, we also promotedthe exhibition BioInItaly (April 2008), where fifteen companies (chosen from about30 applicants) were able to present their research projects to over forty internationalfinancial investors.

Now it is necessary to improve the country’s capacity to attract investment –for whoever has an original idea and for whoever wants to invest.Therefore, it is necessary that the Finance Act fully implements all the taxfacilities for “new innovative companies”, and increases tax relief on corporateR&D expenditure from 10 to 20%.

Roberto GradnikPresident Assobiotec

8

Within a fast changing framework characterised by increases in R&D spendingand the reduction in the number of active principles discovered each year, biotechnologieshave long since come to play an important and integral role in the life sciences.

Ever-closer relationships between pharmaceutical companies and the new technologies(in various forms such as co-operation, co-promotion, and co-development) meanthat many advanced scientific paths can now be explored to meet hitherto unsatisfiedtherapeutic needs. Furthermore, through closer working relations the necessaryskills, resources and instructions are forthcoming for the development of themolecules and expertise that will make the new therapeutic instruments available.

Thanks to possessing a number of unique qualities, Italy has demonstrated itsleading international role in the life sciences (the third country in Europe and thefifth in the world in terms of employees), and its capacity to attract foreign capital.

Furthermore, Italy has acquired an international specialisation in the pharmaceuticalfield as demonstrated by its foreign trade surplus in pharmaceuticals (E 1,229million in 2007). The intensity of research and development is growing in thesector, as proxied not only by the ratio of researchers to total employees (whichrose from 8.3% in 2006 to 8.7% in 2007) but also by the ratio of R&D investmentto turnover (which grew from 9.4% to 10.1%).The biotechnologies deployed for health care are making an important contributiontowards such results.

At present 147 projects are being conducted by Red Biotech in Italy, of which63 in the pre-clinical phase and 84 in the clinical development phase.Total R&D investments are rising as well as the value of red biotechnologicalproduction (estimated at E 4.6 billion), corresponding to 20% of the total valuegenerated by the pharmaceutical sector as a whole.

Apart from large Italian-and foreign owned companies, the companies dedicatedto biotech research in Italy are becoming ever more numerous: 42 pharmaceuticalcompanies have recently oriented their R&D effort towards the new technologies.

These include those start-ups that in short space of time conquered the front pagesof prestigious international scientific journals, attracted investments into Italy andreached cooperation agreements with large companies. Gentium, which is specialisedin research activities, especially in the field of orphan drugs, is the only Italiancompany to be listed on NASDAQ; Axxam works in the San Raffaele Scientific Park;Nerviano Medical Science has commenced cooperation with Bristol Myers Squibbfor the development of oncological drugs; Layline Genomics, a spin-off from theScuola Internazionale Superiore di Studi Avanzati (SISSA) in Trieste, is part of anetwork with BioXell for the development of a monoclonal antibody; MolMed hasbeen recently listed on the Milan stock exchange; Newron has reached an agreementwith Merck Serono for the development of products for Parkinson’s and Alzheimer’sdisease; Philogen, from which Bayer-Schering AG has acquired the developmentof marketing rights for a new anticancerogenic molecule will soon be listed on theMilan stock exchange; NicOx, listed on Euronext, has reached agreements withPfizer and Merck & CO.

That Italy offers numerous competitive advantages is a fact recognized by themanagers who work here. Such advantages include the presence of many outstandingpublic biomedical research centres, in which some of the most prestigious internationalnames work, highly qualified personnel and a skilled management, the productivity,flexibility and creativity of the human resources, solid skills and a long industrialtradition and a widespread and strongly innovative entrepreneurial spirit.

The Life Sciences in Italy:the pharmaceutical companies’ biotech effort

by Sergio DompéPresident Farmindustria

9Blossom Associati 2008

Moreover, this salient position has been furtherconsolidated in recent years by incentives providedfor sector companies: the programmatic agreementsto promote investment in production and R&D inItaly; the fund for the promotion of research andadvanced training in biotechnologies and, veryimportantly, tax credits for research activities.

And nor should we forget the 0.5 percent allocation,a mechanisms that allows the taxpayer toearmark a part of his or her income tax towardsassociations that undertake socially relevant activities(non-profit, scientific and health-care research).Moreover, we can also cite other forms of assistance:the EU’s 7th framework programme, the reductionin the Ires (corporate income tax) rate, and financingfrom bank foundations.

These measures have created the premises foran ever closer co-operation between companiesand public centres of excellence, for examplein the field of rare illnesses – a particular fieldof biotechnological application – which areindispensable if significant results are to be achieved.Genetic engineering and pharmaceutical/biotechnological research constitute the maincontributions for the cure of rare illnesses while manyof the orphan drugs are, in fact, biotech drugs.

Such pathologies (which are mostly genetic inorigin) call for a new approach on account of theircomplexity in therapeutic and ethical terms; anapproach that can bring public and private skillstogether in the name of social solidarity and theobservation of the principle of subsidiarity.

The commitment of companies to the researchnetwork on rare diseases needs the support of anad hoc network created for information and training.This was the premise that led to the agreementon the protocol of understanding betweenFarmindustria and the UNIAMO Association.The protocol is a tool aimed at promoting theadoption in Italy of legislative instrumentsdesigned to encourage the development of orphandrugs by providing financing for research andimproving the welfare and social assistance aspectsof such pathologies.

The biotech sector is an extremely high valueindustry in terms of its therapeutic potentiality andhigh innovative profile.Italy has been able to participate successfully inthis process thanks to its mix of industrial skills,the excellence of its research and the entrepreneurialvitality exhibited by the biotechnological sector,which is generating not only important scientificresults but also ever larger numbers of companiesand, consequently, overall sector growth.

Pharmaceutical andBiotech companies

Public R&D:istitutions and

universitiesPatient andnon-profit

associations

Commitmentto industrial

research

Circulation ofintellectual

resourses andinformation

Incentivesfor R&D andnetworking

New andmore-focused

therapies

Information,prevention,diagnosis,

and treatment

The network of research, information and training

Biotechnologies in Italy 2008

At the end of 2007, the sector comprised 228 companies,of which 24 accredited in that year insofar as they met theBlossom Associati-CrESIT methodological selection criteria.The sector remains dominated by companies dedicated tohealthcare (74%).The overall turnover of accredited companies exceeded 10 billioneuros of which 4.8 billion generated by biotechnological productswhose 2007 growth rate was 11%. Biotechnological R&Dinvestments totalled 1.3 billion, which represents a 9% increaseon the previous year.The employees of accredited sector companies numbered over26,000 (14,543 if we exclude accredited Pharma companies)of which over 6,600 active in R&D. Equity capital rose overallby 56%, with a strongly growing EBIT of 213%, and a 30%decline in financial debt, which shrank to 1.6 billion euro.

Although the Italian biotechnological industry is, largely, arecent development, interesting information can be obtainedfrom the growth in the number of companies over time.Of the 222 companies almost 60% were set up or located inItaly in the last ten years and of these 87 (40% of the total)were only founded in the last six years. The number of companiesin the industry has grown constantly, especially since 2000when the development rate intensified significantly. Since 2000,the average annual registration rate of new companies has been13 (representing an approximate annual new entrant rate of 10%)However, alongside the new entrants there are a group of companieswith a long history and tradition. 63 companies were foundedprior to beginning of the 1990s, and 20 before 1970. These arecompanies whose consolidated market positions were achievedby developing traditional technologies and which have tended todiversify into new biotech-derived technologies in recent years.

Numerically, the Italian industry is mainly made up of smallcompanies. 170 of the 228 certified companies (75%)employ fewer than 50 employees and generate total sales ofless than 10 million euros. 27 of the remaining companies (12%)are medium-sized concerns (i.e. employing less than 250,with annual sales of less than 50 million euros) and 30 (13%)are large companies employing over 250, whose sales exceed50 million euros.

by Stefano Milani, Alberto Onetti, Federica Bottazzi, Federica Rovida

Blossom Associati Management Consulting

CrESIT - University of Insubria of Varese

befo

re 1

970

2229

40

63

94

132

228

20

1971

- 19

75

1976

- 19

80

1981

- 19

85

1986

- 19

90

1991

- 19

95

1996

- 20

00

2001

- 20

07

Number of biotechcompanies in Italy:temporal growth

Source: Blossom Associati - CrESIT 2008

159 178 199 211 223 228

149

2002

2003

2004

2005

2006

2007

2001

Source: Blossom Associati - CrESIT 2008

Number of newly set upbiotech companies:temporal growth (2001-2007)

Large 13%

Medium 12%

Small 75%

Source: Blossom Associati - CrESIT 2008

Breakdown of Italian biotech companiesby size

10

11Blossom Associati 2008

Red 73%

White 9%Bioinfo 5%

Green 13%

Source: Blossom Associati - CrESIT 2008

Classification of biotech companies in Italyby area of application

Red 95,36%

White 0,54%Bioinfo 0,07%

Green 4,04%

Source: Blossom Associati - CrESIT 2008

Breakdown of biotech turnover by area

Green 11,76%

Red 86,28%

White 1,60% Bioinfo 0,36%

Source: Blossom Associati - CrESIT 2008

Breakdown of R&D investments inbiotech activities by area

An analysis of the 228 companies shows that 168 work inthe health care area (the so-called “Red Biotech Companies”),30 in the field of biotechnologies for agricultural, animal husbandryand veterinary applications (the so-called “Green BiotechCompanies”), 19 in industrial and environmental fields(“White Biotech Companies”) and 11 are oriented to R&D inthe field of bioinformatics.

It should also be noted that 31 subsidiaries, or branches ofmultinationals, figure among these 228 companies, of which18 belong to the “Pharma- industry” category. In numericalterms, therefore, the industry reveals a prevalence ofItalian-owned companies.

Apart from estimating the overall economic value created bythe sector, we are also in a position to quantify the revenuesgenerated by companies from the sale of biotech-derived products.The figure constitutes a subset of the aggregate revenues postedby the 228 recognised companies and was obtained by applyinga percentage – representative of the share of revenue from thesales of biotechnological products in Italy and on internationalmarkets1 – to the revenues of each company.

Although this figure is important, and now places Italy amongthe leading European countries, it should be stressed that, today,sales revenues are certainly not the principal indicator for assessingthe development potential and growth opportunities of the industry.The analysis of investments and pipelines allows us to determinethe potential future of the business, which, in view of theextreme volatility of the sector, can undergo strong (positive)variations from one year to another.

This is the case of certain small companies that, thanks tothe development of innovative products, were able to increasetheir market share within the space of a few years until theyreached a position of global leadership with levels of capitalisationon a par with the main multinational companies operating intraditional sectors.

95% of the foregoing 4,805 million euros is accounted for bythe “Red” sub-sector. The remaining 5% is produced bycompanies operating in other areas, with a clear predominanceof the “Green” sub-sector.

1 This percentage was calculated in the course of a qualitative analysis of theinformation provided by the companies.

It would also be useful to supplement the foregoing data withinformation on the aggregate sales of which the foregoing biotechrevenues form part. In terms of total turnover (thus not singlingout the biotech component) in 2006 the 228 companies surveyedposted revenues of over 10.8 billion euros2. Obviously, the datalargely reflect the revenues obtained by the 42 red biotechcompanies with a pharmaceutical derivation, which alone accountedfor over 7.9 of the 10,8 billion in question.

The overall size of the investments in R&D in biotechnologicaltechnologies and processes in 2006 in Italy has been estimatedat 1,331 million euros: of which 1,149 million (over 86%)invested by Red companies, 155 million euros (12%) by companiesin the Green area and the remaining 26 million (2%), in theWhite Biotech sub-sector.

The significance of these data once again demonstrates theunderestimates of the research effort of Italian industry bymost studies with an international circulation. The principalreason for this under-estimate is to be found in the difficultyof procuring and identifying pertinent data during analysis.As stated in the methodological notes, the foregoing data concerningthe size of biotech investments are based solely on the valuesof R&D investments in technology and processes referring tobiotechnological type platforms carried out by the 228 companiesmaking up the industry.

However, it would be appropriate to supplement the foregoingfigures with data on the overall volumes of investments inR&D (and thus not just limited to biotech activities). In 2006,the 228 recognised companies made investments for over2,345 million euros in R&D. The data, however, are stronglyinfluenced by the value of investments referring to companiesfrom the pharmaceutical sector that mainly tend to investin traditional technology and products, especially the 14“Pharma Oriented” companies.

2 Aggregate sales data proxy the economic value generated by the biotech sector.However, it should be noted that this value is necessarily an over- or under-estimateas it not possible to “map” situations that sometimes can have a major impact onthe results presented. A frequent case is that of spin-offs or branches of foreigncompanies with marketing agreements for the products of their parent companies.In this case, the sales data refer to R&D activities performed outside Italy.However, the same argument applies to diversified companies that occupy marketsother than biotech. For this reason, the turnover should be rectified to excludesales referring to other business. In all these cases, an analysis that takes accountof the sales data of Italian companies is structurally inclined to over-estimate thesize of the sector. On the other hand, there are subsidiaries of foreign companiesdedicated to R&D whose products are marketed by other companies of the group.In this case, their operating revenue will not reflect the actual value of theoperations performed in our country. However, such simplifications are unavoidablein an analysis on aggregate data. Nevertheless, they also mean that we should makea careful and prudent use of the results presented.

12

13Blossom Associati 2008

The data used (number of employees declared by the companiesand found by qualitative analysis or by analysing the notes tothe financial statements) nevertheless tend to underestimate thesize of the industry. Thus, it can be presumed that the industryincludes, especially in the case of smaller companies, a significantnumber of self-employed professional workers and other freelancers.

In terms of territorial location, the Italian biotechnological sectoris characterised by its strong geographical concentration.If, on the one hand, almost all the regions (17) of our countryhost biotech companies, at present only a few have attractednumerically and economically significant concentrations ofcompanies. The regions that exhibit strong concentrations areLombardy, where 78 companies are situated (35% of the total),Piedmont with 31 companies (12% of the total), Tuscanywith 22 (10% of the total), Friuli Venezia Giulia with 16(7% of the total) followed by Lazio with 15 (6% of the total)and Sardina with 13 (6% of the total). 76% of the Italianbiotechnological companies are concentrated in these six regions.

Furthermore, strong territorial concentrations also emergewhen we examine each region. Thus, biotech companiesapart from being concentrated in a limited number of regions(Lombardy, Piedmont, Tuscany and Friuli Venezia Giulia), alsotend to cluster in certain specific territorial areas within them.We can take the case of Tuscany to illustrate this phenomenon.In this region, the companies are not evenly distributed throughoutthe region but localised in areas around Florence, Siena and Pisa,where all the basic factors for their development can be found.

Breakdown of R&D employees and overall totals by area

Scope of application Total R&Demployees employees

Bioinfo 205 162Green 477 149Red 25,303 6,233White 172 108Overall total 26,157 6,652

Source: Blossom Associati – CrESIT 2008

The overall number of employees performing R&D activities is6,652 (57% of all employees surveyed in the framework ofbiotech companies). The data take account of researchers activein Green (3%), White (2%), Bioinformatics (3%) and Red Biotech(92%) companies.

If the analysis is extended to cover all the employees of the228 Italian biotechnological companies (of which 14 arethe direct expression of the pharmaceutical industry) the resultingfigure is 26,157 employees, hence all the employees of Green(3.3%), White (1.2%), Bioinformatics (1.4%) and Red Biotech(94%) companies. The latter two categories include not onlyauthentically red biotech companies but also pharmaceuticallyderived companies.

14

Lazi

o

Tosc

ana

Emili

a Ro

mag

na

Piem

onte

Cam

pani

a

Friu

li Ve

nezi

a Gi

ulia

Vene

to

0

8000

7000

6000

5000

4000

3000

2000

1000

Lom

bard

ia

Sard

egna

Altre

ALL EMPLOYEESR&D EMPLOYEES

Empirical evidence shows that the extreme volatility of the sectorand the facility of transferring intellectual capital and financialresources, means that foreign companies tend to invest financialcapital and attract intellectual capital where the prospectsof a functional system and the creation of value have alreadybeen found to operate, in terms of internationally consolidatedpositions and relations.

If we reflect on the analysis of the 228 companies, net of the13 Pharma oriented companies, we find confirmation of theforegoing considerations, and also as regards employment data,even though their national ranking in this respect may be slightlydifferent. At a national level, the number of employees engagedon R&D amounts to 6,652 while the overall number of allemployees of biotechnological companies (including the dataon accredited pharmaceutical companies) is around 26,157.

Source: Blossom Associati – CrESIT 2008

Lombardy certainly detains a leading position. 11,555 employeeswork in the region, of whom 3,472 engaged in R&D (44% ofthe national total and 52% of all employees in the industryengaged on R&D, on a national basis). In terms of total and R&Demployees, Lazio emerges as the second most important region,where there is a strong prevalence of Big Pharma or large biotechoriented companies. After these we find regions with a strongpropensity towards investment such as Piedmont, with 9,5%of all the industry's employees and 8,7% of all R&D employeeson a national basis, Emilia Romagna with 1,5% of all employeesand 4,5% of employees engaged on R&D on a national basis,followed by Tuscany and Friuli Venezia Giulia.

The geographic distribution of all employees in the industry and R&D employees

15Blossom Associati 2008

An analysis of the distribution of turnover by region underlinesthe territorial polarisation mentioned earlier. Two regions (Lombardyand Lazio) alone account for 76% (in almost equal proportions)of national sales, while demonstrating profoundly differentorientations and morphological characteristics with respect tocompany structure.

An examination of other regions reveals important contributionsfrom Tuscany (which accounts for 11% of biotech operatingrevenue), Emilia Romagna and Friuli (which jointly account foranother 7%)

The analysis of biotech investments in R&D reveals a partiallydifferent picture, which tends to correspond to the map of thedistribution of the companies. In this case, the followingaspects emerge. Lombardy plays a predominant role, with 73%of all investments carried out in Italy in biotechnological R&D.

However, the importance of Tuscany in the panorama of the Italianmarket diminishes as it accounts for only 2% of all investments.On the other hand, the contributions of Emilia Romagna (8%)and Piedmont (4%) are found to be significant, as well as thatof Friuli (3%). Lazio, on the other hand, has a much more limitedR&D role (6%) in relation to the foregoing indicators.

The analysis of the asset structures of biotech companiesreveals a very clear competitive position attributable to eachof the Italian regions.

Geographical distribution

Region # Companies # R&D # Overall Biotechemployees employees Turnover

Campania 9 212 265 9,314,027Emilia Romagna 14 581 2,500 174,589,188Friuli Venezia Giulia 16 135 206 37,712,805Lazio 15 1,069 7,721 1,685,686,182Lombardy 78 3,472 11,555 2,386,039,818Piedmont 31 299 385 130,489,461Sardinia 13 75 93 2,384,617Tuscany 22 637 3,169 315,197,226Trentino Alto Adige 4 7 40 42,020Veneto 11 98 138 52,210,292Other 15 66 85 12,215,073Total 228 6,652 26,157 4,805,880,708

Source: Blossom Associati – CrESIT 2008

The strong territorial concentration of the sector, which weunderlined earlier, now appears even more pronounced.The first six regions that account for 76% of all Italian companiesemploy over 96% of all employees and over 79% of the employeesengaged on R&D.

Lombardy is the region with the highest concentration of R&Dactivities, as well as displaying a uniform distribution of large,medium-size and small companies, all sharing the same strongvocation for innovation and investment in technologies and products.In addition, the system includes the presence in the territory ofnot only scientific parks such as, for example, Science Park Raf(as described in detail below), but also internationally importantuniversities, clinical institutes with a strong vocation forexperimentation and attracting investors (the latter favoured bythe proximity of Milan, the nation’s most important financialcentre). In addition, to these advantages there is the supportprovided by local institutions. These are increasingly committedto sustaining the development of biotechnologies and attractingforeign investments by streamlining bureaucratic formalitiesfor company growth and developing specific packets to sustainintellectual capital and help set up new companies.

Tuscany possesses a mature system made up of 22 companiescharacterised by a strong R&D vocation for biotechnologicalresearch (such as, for example, Novartis Vaccines ex Chiron)while important investments are being carried out within theterritory by pharmaceutical companies. For example, we findnational pharmaceutical companies (such as Abiogen Pharmaor Menarini), small biotech companies strongly oriented toinnovation, as well as scientific parks such as the Tuscany LifeSciences (see following data sheet), universities oriented tothe setting up of academic spin-offs such as the University ofFlorence, clinical institutes oriented to experimentation andinstitutional investors willing to support the sector (the Montedei Paschi Foundation).

Piedmont, Friuli, Sardinia and other regions are meeting thedevelopmental challenge by an increased commitment to innovation.Although the number of companies on their territories is stillsmall, they exhibit a strong vocation for innovation and a strongorientation towards innovation in biotechnological R&D. Moreover,it should be noted that for years regional institutions have beensupporting the creation of systems and structures able to hostnew innovative biotechnological companies with a stronginternational character. This is demonstrated by the scientificparks to be discussed in further detail below (the CanaveseBioindustry Park in Piedmont, the Science Park Area in Friuliand the Scientific and Technological Park in Sardinia), that functionas reference points for the sector in each territorial area.

On the other hand, Lazio shows that its vocation is to host maturecompanies with a predominant interest in production andsales, as confirmed by the high concentration of employees,and significant levels of turnover as also by the average EBITposted by the companies situated in the region, which is a suresign of operational maturity.

16

17Blossom Associati 2008

2008: Red biotechnologiesin Italyby Stefano Milani, Alberto Onetti, Federica Bottazzi

Blossom Associati Management Consulting

CrESIT – University of Insubria of Varese

Competitive Positioning.An overall view of the national context.

By the end of 2007, the segmentof the Italian biotechnology industryspecialised in biotech for health carecomprised 168 companies. The datapresented are based on a list certifiedby Blossom Associati and CrESIT.For further information, readers arereferred to the methodologicalappendix for the sample selectionprocedure. However, we would liketo point out that, in line with themethodologies adopted by the mostauthoritative international studies,the most rigorous criteria werefollowed in our selection procedure.Thus, we excluded pharmaceuticalcompanies that do not performin- house R&D activities onbiotechnological platforms within Italy.

Although the Italian biotechnologicalindustry is a quite recent development,some interesting information emergeson the numerical growth of companiesover time. Of the 168 companiesalmost 58% were set up or locatedin Italy in the last ten years and ofthese 70 (42% of the total) were onlyfounded in the last six years. Theparticularly intense development thatthe Red biotech sub-sector has beenexperiencing since the start of thenew millennium is also reflected inthe constant growth in its numberswithin the sector. Last year, 24new Red biotech companies wereaccredited, as they were found tocomply with the criteria used forinclusion in the biotech sector, while18 were removed from the sector, asrequired by the application of therigorous Blossom Associati-Cresitmethodology.

Alongside these recently establishedcompanies, there is a group ofpharmaceutical companies with along history and tradition: 42pharmaceutical companies that inrecent years have been directingresearch and development towardsbiotechnologies. These are nationaland multinational companies thathave been able to consolidate theirmarket positions by developing and/ormarketing traditional technologies andwhich in recent years intend todiversify their pipeline with the newproducts derived from biotechnologies.

18

Numerically, the Italian red biotech sub-sector is made up ofsmall companies. 114 of the 168 accredited companies (68%)employ fewer than 50 employees and their total annual salesare less than 10 million euros. Of the remaining companies,26 (16%) are medium-sized concerns (i.e. employing up to250 with annual sales of under 50 million euros) and 27(16%) are large companies employing over 250 with sales ofover 50 million euros.

It should also be noted that of the 168 companies, 29 aresubsidiaries (the reduction in their number with respect to2007 – minus 30 subsidiaries – is mainly due to importantacquisitions and mergers). 18 of these subsidiaries belong to the“Pharma-industry” category. In numerical terms, therefore, theindustry reveals a prevalence of Italian-owned companies.

From the analysis of the business models of the 168companies, we can classify them as belonging to one of thefollowing two segments:

> a “Born Biotech” segment that accounts for 126 companies.These are mainly small to medium-sized companies witha strong orientation to research and development within abiotechnological environment;

> “Pharma-Biotech” a macro-segment, made up of 42companies with important ties to the pharmaceutical sector.These 42 break down as follows:– 28 are “Biotech Oriented” companies, in other words,companies with a pharmaceutical derivation but whoseoperations are mainly focused upon biotech R&D activities.These companies tend to have a business model mainlyor exclusively based on strong ties with pharmaceutical firms,from which, as stated, they mainly derive. Good examplesare, first, Biosearch, created as a spin-off by the managersof the Lepetit research centre and, second, Novuspharma,a spin-off from a division of the German BoehringerMannheim Group.– 14, instead, are “Pharma Oriented” i.e., Italian or multinationalpharmaceutical companies that, in line with their own strategicplans are investing in R&D in order to extend their ownpipelines with innovative products, which, inter alia, enablethem to extend the period of patent protection.

befo

re 1

970

1971

- 19

75

1976

- 19

80

1981

- 19

85

1986

- 19

90

1991

- 19

95

1996

- 20

00

2001

- 20

07168

98

71

52

33272120

Number of Red Biotech companiesin Italy:temporal growth

Source: Blossom Associati - CrESIT 2008

2002

2003

2004

2005

2006

2007

108

2001

115

128

145152

163 168

Number of newly set up biotechcompanies: temporal growth(2001-2007)

Source: Blossom Associati - CrESIT 2008

19Blossom Associati 2008

3 Aggregate sales data proxy the economic value generated by the biotech sector.However, it should be noted that this value is necessarily over- or under-estimatedas it not possible to “map” situations that can sometimes have a major impacton the results presented. A frequent case in point is that of the spin-offs or subsidiariesof foreign companies that have marketing agreements for products of the parentcompany. In this case, the sales data refer to R&D operations conducted outside Italy.However, the same argument applies for diversified companies that occupy marketsother than biotech. For this reason, the turnover should be rectified to excludesales referring to other business. In all these cases, an analysis that takes accountof the sales data of Italian companies is structurally inclined to over-estimate the sizeof the sector. On the other hand, there may be subsidiaries of foreign companiesdedicated to R&D whose products are marketed by other companies of the group.In this case, their operating revenue will not reflect the actual value of theoperations performed in our country. Such simplifications cannot, unfortunately,be eliminated at an aggregate level analysis. Nevertheless, they counsel us to considerthe results presented with due prudence.

Small 68%

Large 16%

Medium 16%

Breakdown of Red Biotech companiesin Italy by size

Source: Blossom Associati - CrESIT 2008

Pharma 25%

Biotech 75%

Breakdown of Red Biotech companiesby category

Source: Blossom Associati - CrESIT 2008

Revenue trend and macro indicators

The overall value of biotechnological production (referring tothe sole area of health care) is estimated at E 4.6 billion, or20% of the total value of the production generated by thepharmaceutical sector, with a 12% year-on-year growth rate.

Broken down into its component parts, the value of Italianbiotechnological production derives 34% from 126 “Born Biotech”companies, and 47% from 28 pharmaceutically derivedcompanies that focus primarily on biotech (“Biotech Oriented”).The remaining 19% of biotechnological production value isproduced by 14 “Pharma Oriented” companies. The marketshare of the 32 foreign-capital companies amounts to 77%.

It would be useful to supplement the foregoing data withinformation on the financial aggregate of which the foregoingbiotech revenues form part. We have determined that total turnover(thus not singling out the biotech component) in 2006 of the168 companies surveyed amounted to over 9.8 billion euros3.

An historical analysis of sales trends shows that after areduction in biotech production values in 2005, a strong recovery(+12%) took place in 2006.The growth in production revenue was mainly attributable tothe 28 pharmaceutically derived biotechnological companies(+15%) which accounted for E 2.2 billion. This performancewas matched – in percentage terms – by the 14 pharmaceuticalcompanies (+14%) that generated E 0.9 billion in sales whilethe born biotech companies, with a +8% growth generated1.5 billion in sales revenues from biotechnological derived products.

If we analyse the companies by size we that find a strongsales increase took place in the past year as regards 54 largeand medium-sized companies (+13%), while the 112 smallsized-companies, after a 55% growth in 2005, recorded adrop-off in sales (- 14%) in 2006.

The 168 red companies have a total market capitalisation ofE 2.2 billion with R&D biotech investments for E 1.1 billionand significant growth performance with respect to thepreceding year (+11%).

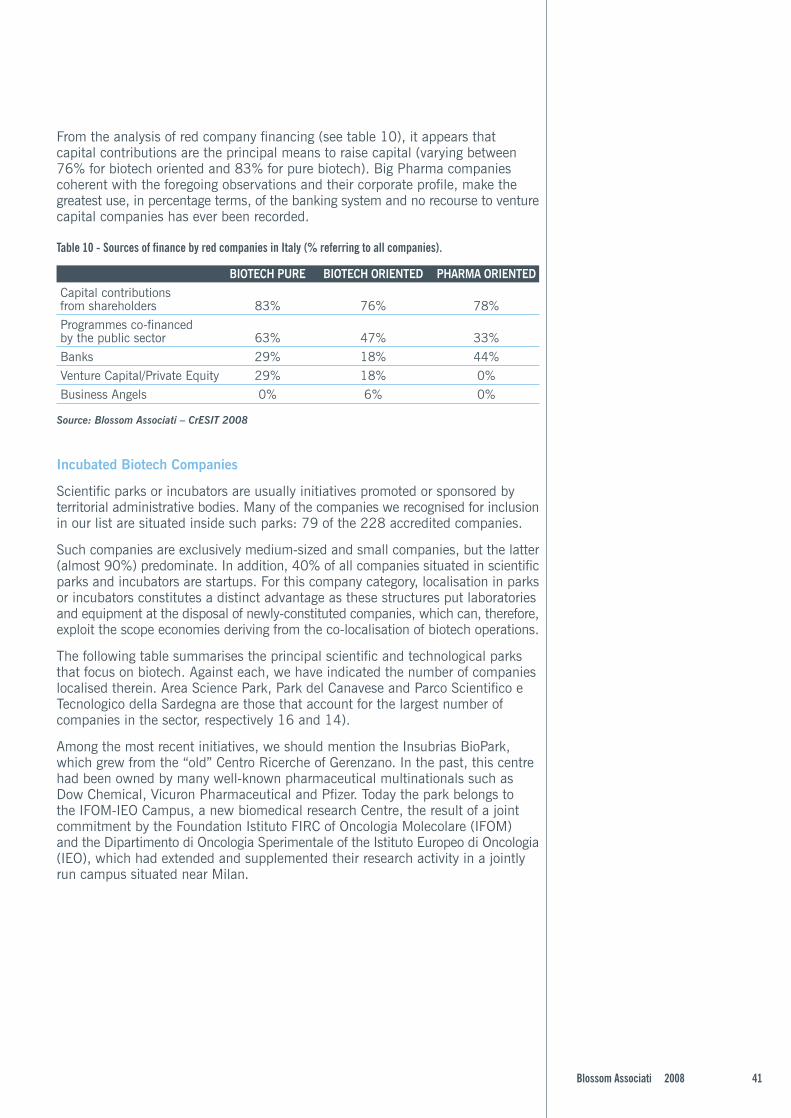

The companies' net indebtedness amounts to E 1.6 billion.This is a major reduction (-30%) with respect to the precedingyear and demonstrates a significant increase in their net worth(+79%), mainly through important capitalisation operations;mainly more capital injections. And, in fact, the most commonform of financing, for all companies, is constituted by majorcapital contributions from shareholders. In 28% of the cases,banks intervened in the operations to provide an additionalguarantee for the success of the operations, but almost exclusivelyon behalf of medium-sized and large companies.

A central role is played by programmes co-financed by thepublic sector (mainly functioning as seed and pre-seed money,otherwise virtually absent from the national financial market)which – through mostly national and regional financialschemes – intervened in 61% of the operations and mainly tosupport small companies, which are normally more exposed toenterprise risk. Local programmes, on the other hand, offeredonly marginal assistance. Venture capital, mainly originatingoutside Italy, accounted for 19.5% of the capitalisation operationsof accredited companies, which is an index of the dynamism inthe sector and the interest it arouses. The contribution fromBusiness Angels was practically nil as they are virtually absentfrom the sector. Our analysis has shown only one case of theirhaving operated in Italy. It should be emphasised that the limitedimpact of this type of operation reflects the virtual absence ofsuch operators from the Italian market.

An assessment of the companies’ 2006 operating marginsshows an operating income (EBITDA) of E 768 million, of which142 million accounted for by biotech companies, with theremaining E 626 million generated by Pharma companies.Furthermore, after a breakdown by size, the analysis uncoversa strong diversification in relation to the maturity and sustainabilityof the business of biotech companies. Thus if, on the one hand,the overall level of operating income would seem to indicatethat the sector has grown beyond the first development stage,on the other, we must distinguish three different “moving spirits”that ideally comprise the totality of the accredited biotechcompanies covered by this analysis, if we are to comprehend thenature of the growth.

20

Medie 50%

Piccole 14%

Grandi 36%

Breakdown of R&D investmentsRed Biotech by size

Source: Blossom Associati - CrESIT 2008

An EBIT analysis (i.e. net of the depreciation charges on investments)yields an overall figure of over E 338 million for the 168 accreditedbiotech companies, which break down as follows:

> 114 small companies that against overall investments ofE 158 million posted a negative EBIT in 2006 of E 69 million;

> 26 medium-sized companies that against E 578 millionin overall investments posted an EBIT of slightly overE 12.5 million;

> 28 large companies that against overall biotech investmentsof just over E 403 million posted an EBIT in excess ofE 395 million.

The performance of the 29 subsidiaries of foreign companiesis significant. These invested slightly less than E 250 millionin biotech technology (22% of total national investment)and posted an EBIT of almost E 250 million.

In making international comparisons we must always bear inmind that the real potential of the Italian pharmaceutical market(which is one of the main drivers for the future development ofthe biotech market) puts Italy in the fifth position among worldmarkets with total pharmaceutical sales (pharmacies + hospitals),at ex works prices, of E 16.5 billion (2006 data: Source IMS).The global value of the pharmaceutical market (expressedin Euro at ex-works prices) confirms that Italy is the third largestmarket in Europe, after Germany and France and the fifth inthe world, with the USA and Japan occupying the first two places(Source IMS).

Biotech investments in R&D

The overall size of R&D investments in biotechnological technologiesand processes in 2006 in Italy was estimated at 1.149 millioneuros (an 11% year-on-year growth rate). The size of suchinvestment confirms that significant R&D activities are takingplace in Italy directed at both the development of authenticallyoriginal products (research conducted in Italy, but largely underthe auspices of foreign multinationals) and the development ofproducts able to improve the clinical effectiveness of knownmolecules by the development of innovative release applicationsand/or systems. As stated in the methodological notes, theforegoing data concerning the size of biotech investments aresolely based on the values of R&D investments in technology andprocesses referring to biotechnological type platforms carried outby the 168 accredited companies that meet the selection criteriaof Blossom Associati-CrESIT.

21Blossom Associati 2008

However, to supplement the foregoing figures it would beuseful to provide data on the overall volumes of investments inR&D (and thus not just limited to biotech activities). In 2006,the 168 accredited red biotech companies made investmentsfor over 2,160 million euros in R&D. These data directlyeflect the value of investments made by the 14 companiesclassified as pharmaceutical, which mainly make investmentsin innovative technologies and products (53% of the overallvalue of the investments).

Of the E 1,149 million in total investments in biotech technologiesand processes, E 413 million (with a 14% year-on-yeargrowth rate) were accounted for by large companies, while 578million (with a 7% year-on-year growth rate) were made bymedium-sized companies. Small companies made overallinvestments for 158 million (representing a 16% year-on-yeargrowth rate).

Moreover, extremely interesting considerations emerge fromthe analysis of the origin of the investments. Thus of theE 1,149 million in total investments, 555 million (with a 31%year-on-year growth rate) were accounted for by biotech derivedcompanies, while 517 million stemmed from biotech companieswith a pharmaceutical derivation. In conclusion, traditionalpharmaceutical companies tended to limit their internal investmentsand only accounted for a modest 67 million (representing a22% year-on-year decrease). In general, instead of internaldevelopment such companies prefer a risk diversification strategyaimed at the setting up of Newco Biotechs which they canendow with capital, licensing contracts and expertise.Of such investments, the 29 branches of multinationals accountedfor 250 million (22%).

Biotech products under development in Italy *by Assobiotec

Research & Development taking place in Italy has given rise toan extremely interesting pipeline.The principal area of activity, in which 74% of the Italian biotechcompanies operate, is pharmaceuticals.Thus, in Italy there are, overall, no less than 147 biotechnologicalproducts under development, the results of research being carriedout by 35 companies. Of these 147 products, 63 are in thepreclinical development phase while 84 are already in the clinicalphase (Phases I-II-III). In particular, of the 84-biotech productsundergoing clinical development, 33 are in Phase I, 35 in PhaseII, and 16 in Phase III.Italian biotech research, furthermore, can boast 63 productsat a pre-clinical developmental phase and 99 molecules at adiscovery phase, which altogether constitute a promising foundationfor the sector in the coming years.

If we consider all R&D activities (therefore also including moleculesin the discovery phase), the analysis shows a strong orientationof overall investments towards the area of oncological therapy(33%), the central nervous system (15%) and the areas ofdermatology (3%) and antimicrobials for systemic use (3%).Moreover, these data are even more significant if we take accountof the fact that the activities performed by R&D centres of themultinationals operating in our country have not been considered.

Spin off pharma 45%

Pharma 7%

Biotech 48%

Breakdown of R&D investmentsRed Biotech by class of company

Source: Blossom Associati - CrESIT 2008

Discovery 40%

Preclinic 26%

Phase I 13%

Phase II 14%

Phase III 7%

Table 1 - Pipeline referring to the R&Dactivities conducted in Italy (2008)

Fonte: Blossom Associati - Assobiotec 2008

22

Discovery 99Preclinic 63Phase I 33Phase II 35Phase III 16

Chart 1 - Pipeline referring to the R&Dactivities conducted in Italy (2008)

Source: Blossom Associati - Assobiotec 2008

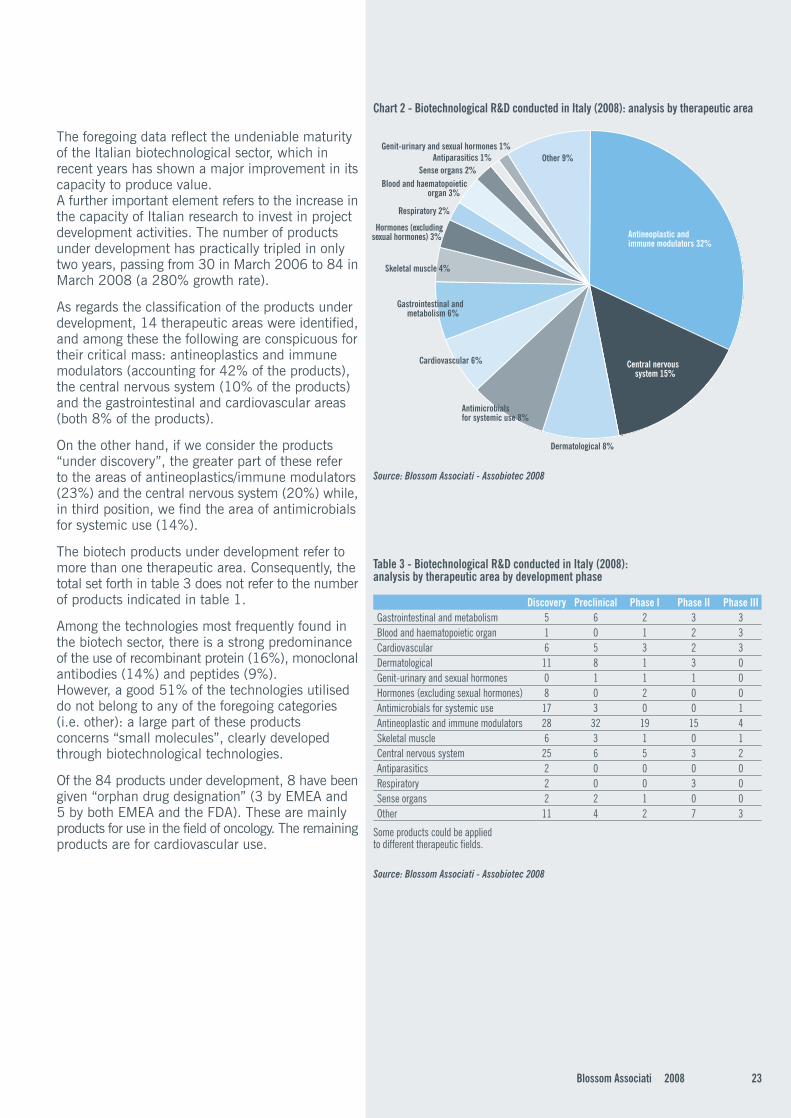

The foregoing data reflect the undeniable maturityof the Italian biotechnological sector, which inrecent years has shown a major improvement in itscapacity to produce value.A further important element refers to the increase inthe capacity of Italian research to invest in projectdevelopment activities. The number of productsunder development has practically tripled in onlytwo years, passing from 30 in March 2006 to 84 inMarch 2008 (a 280% growth rate).

As regards the classification of the products underdevelopment, 14 therapeutic areas were identified,and among these the following are conspicuous fortheir critical mass: antineoplastics and immunemodulators (accounting for 42% of the products),the central nervous system (10% of the products)and the gastrointestinal and cardiovascular areas(both 8% of the products).

On the other hand, if we consider the products“under discovery”, the greater part of these referto the areas of antineoplastics/immune modulators(23%) and the central nervous system (20%) while,in third position, we find the area of antimicrobialsfor systemic use (14%).

The biotech products under development refer tomore than one therapeutic area. Consequently, thetotal set forth in table 3 does not refer to the numberof products indicated in table 1.

Among the technologies most frequently found inthe biotech sector, there is a strong predominanceof the use of recombinant protein (16%), monoclonalantibodies (14%) and peptides (9%).However, a good 51% of the technologies utiliseddo not belong to any of the foregoing categories(i.e. other): a large part of these productsconcerns “small molecules”, clearly developedthrough biotechnological technologies.

Of the 84 products under development, 8 have beengiven “orphan drug designation” (3 by EMEA and5 by both EMEA and the FDA). These are mainlyproducts for use in the field of oncology. The remainingproducts are for cardiovascular use.

Discovery Preclinical Phase I Phase II Phase IIIGastrointestinal and metabolism 5 6 2 3 3Blood and haematopoietic organ 1 0 1 2 3Cardiovascular 6 5 3 2 3Dermatological 11 8 1 3 0Genit-urinary and sexual hormones 0 1 1 1 0Hormones (excluding sexual hormones) 8 0 2 0 0Antimicrobials for systemic use 17 3 0 0 1Antineoplastic and immune modulators 28 32 19 15 4Skeletal muscle 6 3 1 0 1Central nervous system 25 6 5 3 2Antiparasitics 2 0 0 0 0Respiratory 2 0 0 3 0Sense organs 2 2 1 0 0Other 11 4 2 7 3

Some products could be appliedto different therapeutic fields.

Table 3 - Biotechnological R&D conducted in Italy (2008):analysis by therapeutic area by development phase

Source: Blossom Associati - Assobiotec 2008

Antineoplastic andimmune modulators 32%

Central nervous system 15%

Dermatological 8%

Antimicrobialsfor systemic use 8%

Cardiovascular 6%

Gastrointestinal and metabolism 6%

Skeletal muscle 4%

Hormones (excludingsexual hormones) 3%

Respiratory 2%

Blood and haematopoietic organ 3%

Sense organs 2%Antiparasitics 1%

Genit-urinary and sexual hormones 1%Other 9%

Chart 2 - Biotechnological R&D conducted in Italy (2008): analysis by therapeutic area

23Blossom Associati 2008

Source: Blossom Associati - Assobiotec 2008

Human resources and employment.An overview of the national context

The overall number of employees performing R&Dactivities is 6,233 (25% of all employees surveyedin the framework of biotech companies)*.

However, we can break this figure down stillfurther into two sub-categories based on themethodological approach indicated in this Report.

> 50% (equivalent to 3,133 employees to R&Doperations) is accounted for by 126 companiesthat can be described as authentically

biotechnological.

> The remaining 50% (equivalent to 3,100employees) refers to 42 pharmaceutical companiesor spin offs from pharmaceutical companies.

A more in-depth analysis reveals that 58% of thetotal number of R&D employees is employed by largecompanies, 29% by medium-sized companies and13% by small companies. These figures illustratethe enormous importance played by medium-sizedand small enterprises in the employment of researchpersonnel. If the large companies generally assign16% of their personnel to R&D, the medium-sizedand small companies appear much more focused,declaring 66% of all employees engaged on R&D work.

The data used (number of employees disclosedby the companies through either qualitative analysisor the analysis of the notes to the financial statements)nevertheless tend to underestimate the size of theindustry. Thus, it can be presumed that the industryincludes, especially in the case of smaller companies,a significant number of self-employed professionalworkers and other freelancers.

Competitive regional positioningTerritorial distribution

For many years, the Blossom Associati-Cresitmethodology has been pursuing the objective ofdefining a unique and objective approach fordetermining the comparative importance ofbiotechnologies as between the Italian regions.With respect to 2005, the biotech companiesperforming R&D operations within Italy display ahigh level of geographical clustering.

Monoclonal Recomb. Cell Gene Fermen-Anti Protein Pept. Therapy Therapy Vacc. tation Other

Discovery 5% 6% 5% 2% 1% 1% 0% 22%Preclinic 3% 4% 1% 2% 0% 0% 1% 14%Phase 1 3% 2% 0% 1% 0% 0% 0% 6%Phase 2 2% 3% 2% 1% 0% 0% 0% 7%Phase 3 1% 1% 1% 1% 0% 0% 0% 2%

Table 5 - Biotechnological R&D conducted in Italy (2008):analysis of biotechnological technologies by development phase

Source: Blossom Associati - Assobiotec 2008

Other 51%

RecombinantProtein 16%

MonoclonalAnti 14%

Peptides 9%

Cell Therapy 7%

Gene Therapy 1%Fermentation 1%

Vaccines 1%

Chart 4 - Biotechnological R&D conducted in Italy (2008):analysis of biotechnological technologies

24

Fonte: Blossom Associati - Assobiotec 2008

* The overall number of R&D employees in Italy in the lifesciences amounts to 9,383 of whom 3,133 accountedfor by biotech companies, 3,100 by pharmaceutical companiesthat invest in biotechnologies and a further 3,150 bytraditional pharmaceutical companies.

Although almost all the regions (14) of our country host companiesfrom this sector, at present only a few have attracted economicallyand numerically significant concentrations of companies.These are: Lombardy, where 64 companies are situated (38%of the total), Piedmont with 17 companies (10% of the total),Tuscany with 17 (10% of the total), Piedmont with 17(10% of the total), Lazio with 11 (8% of the total) and FriuliVenezia Giulia with 11 (7% of the total) followed by EmiliaRomagna with 10 and Sardinia with 10. These seven regionsaccount for 85% of the Italian biotechnological companies.

The analysis of the 168 companies shows that the foregoingconsiderations also apply to employment data, even thoughtheir actual national ranking may differ slightly. The overall numberof employees performing R&D activities at a national level,and employed by the accredited companies, is 6,233.

Lombardy certainly detains a leading position. 11,294 employeeswork in the region, of whom 3,398 engaged in R&D (45%of the national total and 55% of all employees in the industryengaged on R&D, on a national basis).

In terms of total employees and R&D employees Lazio emergesas the second most important region, with a strong Big Pharmapresence and important pharmaceutically derived biotechoriented companies employing 7,714 employees of whom1,065 dedicated to R&D activities. The other regions with astrong innovative propensity are Piedmont, with 4% of totalemployees in R&D Emilia Romagna with 9% of total employeesin R&D and Tuscany with 10%.

Geographical distribution Red Biotech

Region # Companies # Overall # R&D Biotechemployees employees turnover

Campania 6 70 56 5,179,505Emilia Romagna 10 2,487 571 173,982,633Friuli Venezia Giulia 11 105 85 20,220,158Lazio 14 7,714 1,065 1,685,221,761Lombardy 64 11,294 3,398 2,251,047,836Piedmont 17 304 252 121,859,191Sardinia 10 74 63 662,763Tuscany 17 3,045 614 308,787,222Veneto 7 122 87 12,501,057Other 12 88 42 3,187,616Overall total 168 25,303 6,233 4,582,649,741

Source: Blossom Associati – CrESIT 2008

25Blossom Associati 2008

The strong territorial concentration of the sector, which weunderlined earlier, now appears even more pronounced.The first seven regions, where 85% of Italian biotechnologicalcompanies are situated, employ over 97% of the total employeesdedicated to R&D operations.

The analysis of the distribution of turnover by regiondemonstrates the territorial polarisation mentioned previously.Two regions (Lombardy and Lazio), while demonstrating profoundlydifferent orientations and morphological characteristics inrespect of company structure, alone account for 86% of nationalsales of biotechnological products for health care with growthrates of, respectively, 16% for Lombardy and 9% for Lazio.

If we turn our attention to the other regions, we can identifyan important contribution from Tuscany (which accountsfor 7% of biotech sales with a 3% year-on-year growth rate)followed by Emilia Romagna (4% with a 9% year-on-year growthrate) and Piedmont (3% and substantially stable with respectto the preceding year).

The analysis of biotech investments in R&D reveals a partiallydifferent picture, which tends to correspond to the map ofthe distribution of the companies. In this case, the followingaspects emerge:

> Lombardy plays a predominant role, accounting for 73%of all investments carried out in Italy in biotechnological R&Dand biotech processes for health care;

> With 9% of all investments Emilia Romagna's new and importantrole in the Italian panorama is confirmed;

> Lazio at 7% confirms its position in the national panorama,while also characterised by a strong propensity on the partof companies to localise headquarters and marketing officesin the region, as well as important production facilities.

> At 3% of all overall national investments in Tuscany plays aless important role in the Italian scenario;

> On the other hand, the contribution made by Piedmont (4%),as also that of Friuli Venezia Giulia and Veneto (3%) is important.

26

Helping companies improvetheir financial results

The art ofbusinessinnovationis differentfor everycountry

blossomassociati.com

The art ofmanagementinnovationis differentfor everyindustry

Helping companies improvetheir financial results

blossomassociati.com

Structure, characteristics and developmental dynamicsof biotech companies in Italyby Alberto Onetti, Stefano Milani, Alessia Pisoni and Marco TalaiaCrESIT - University of Insubria of VareseBlossom Associati - Management Consulting

The 2008 Report contains an important novelty.By processing the data collected for the preparationof the reports in past years, we are now ableto trace out the sector's historical developmentaltrend. We have dedicated special attention tothe growth of the sector in the three-yearperiod 2003-2006 by making reference toturnover growth rates and new entrants/leavers(following the start-up of new companies orthe winding up of existing ones).

In addition, thanks to the qualitative informationcollected through questionnaires we were ableto indicate the “sentiments”, i.e. the evaluationsof biotech companies concerning the developmentprospects of the sector in the immediate future.

Information on the trends and developmentaldynamics of the sector was subsequentlysupplemented by a qualitative analysis designedto highlight the specific features of the biotechcompanies comprising the reference populationat the end of 2007. The sector is made up ofdifferent “moving spirits” in terms of not only sizeand strategic positioning, but also corporategovernance and relationships with institutionalactors; a sector in which small, medium-sizedand large companies are all active. Thesecompanies include the subsidiaries ofmultinationals as well as start-ups and spin-offs,with either academic or corporate origins.

Some companies are located in science andtechnological parks. For these reasons, wehave chosen to provide detailed studies designedto fathom the characteristics of these differentcategories of company and the differentcorporate structures and performance capacitiesthat connote them.

The developmental trends of the biotech sectorin Italy

In this section, we would like to make someconsiderations regarding the developmentaldynamics of the turnover exhibited by biotechcompanies in the period 2003 -2006.Therefore, we have reconstructed the historicaldevelopmental trends of the turnover of thecompanies in our sector from two temporal,but complementary, standpoints:

> the medium-term, represented by averageturnover growth rate in the three-year period2003-2006;

> a more recent standpoint, focusing uponvariations in turnover in the last year of ourhistorical data series (2006).

Figure 1 - Developmental growth matrix

Source: Blossom Associati - CrESIT 2008

29Blossom Associati 2008

Ave

rage

turn

over

gro

wth

rat

e in

the

thre

e-ye

ar p

erio

d 20

03-2

006

Variations in turnover in the last year of our historical data series (2006)

Average

Based on the cross-classification of the foregoingdata it was possible to construct a matrix(see Figure 1) and thus represent the developmentalpattern of biotech companies for the period inquestion. Each company is identified in the matrixby a dot that represents its annual averagegrowth in the three-year period and in the lastfiscal year considered. Hereinafter we proposethe principal keys with which to read the matrixof the development dynamics of the biotech sector.

> The companies in the top right quadrant ofthe matrix (quadrant A) were those that grewin the period in question and whose growthpropensity was confirmed in the last yearexamined. These are companies that exhibitstable and lasting signs of development andwhich can reasonably be seen as constitutingthe backbone of the biotech sector.

> The companies in the bottom right quadrant(quadrant B) despite exhibiting a positiveaverage growth in the three-year period inquestion, recorded a sales slowdown in thelast year (2006). For such companies ourevaluation, albeit positive, remains suspended.In other words, we must understand if 2006’sslowdown is to be attributed to externaleconomic circumstances and therefore likelyto be reversed or if it represents the signalof a possible company crisis.

> The companies situated in the top left-handquadrant (quadrant D) are companies thatdespite having undergone a negative trendin the three-year period were able to recoverin the last year under examination.Consequently, also for them our judgementremains suspended. It must be determinedif the growth exhibited constitutes a structuralinversion in the sales trend or simply atemporary phenomenon.

> The companies situated in the bottom rightquadrant (quadrant C), on the other hand,are companies undergoing structural decline.They exhibited a decline in sales in both thethreeyear period and in the last year studied.It is not unrealistic to expect that all thesecompanies will disappear from the sector inthe near future.

However, these evaluations must take accountof the positioning of the dots within the singlequadrants.

> For companies situated near to the origin ofthe axes the foregoing trends are clearly lesspronounced. Consequently, the evaluationof a company in quadrant A, situated closeto the axes although positive must obviouslybe qualified. Similarly, for those companiesin quadrant C and D, the negative evaluationsexpressed need to be qualified in the eventthat the dots are situated near to the axisof the abscissas.

> The further from the axes the more markedthe situations of growth or decline become.In such cases, evaluations are more definitivein either a positive or a negative sense.

In order to give objective references to theevaluations we have also indicated averagesector values within the matrix in figure 1(represented by broken lines). Thus, the biotechcompanies exhibited a 10.4% average annualgrowth three-year period 2003-2006, while in2006 (the latest year with an available data)they recorded an annual growth of 24.2%.Such values should be regarded as proxies;a help to the analyst in his or her evaluationsof the performance of individual companies.

> Companies situated to the right and abovethe broken lines are companies, which can bedefined as over-performers, insofar as theiraverage growth is greater than the sectoraverage with reference to both the three-yearperiod and the latest year examined.

> On the other hand, companies to the left ofor below the broken lines are, instead,underperformers. They exhibit more pronouncedreductions than the average of the companiesin the sector.