Is Foreign Ownership Beneficial for Creating Value -Seminar in Finance Paper (1)

23

Is Foreign Ownership Beneficial for Creating Value? Is Foreign Ownership Beneficial for Creating Value? An Insight into Existing Literature for Developed and Emerging Markets Osama Abdeltawab Alvierweg 16, 9490 Vaduz, Liechtenstein +41762126256 [email protected] FS130212 Effrosyni Panagakou Fürst-Franz-Josef-Strasse 15, 9490 Vaduz, Liechtenstein +41766037422 [email protected] FS120284 Seminar paper University of Liechtenstein Graduate School Programme: MSc in Banking and Financial Management Course: Seminar in Finance Module: International Corporate Finance Assessor: Prof. Dr. Marco J. Menichetti Working period: 20.02.2014 to 09.06.2014 Date of submission: 09.06.2014

-

Upload

osama-elaish -

Category

Documents

-

view

42 -

download

0

Transcript of Is Foreign Ownership Beneficial for Creating Value -Seminar in Finance Paper (1)

Is Foreign Ownership Beneficial for Creating Value?

Is Foreign Ownership Beneficial for Creating Value?

An Insight into Existing Literature for Developed and Emerging Markets

Osama Abdeltawab

Alvierweg 16, 9490 Vaduz, Liechtenstein

+41762126256

FS130212

Effrosyni Panagakou

Fürst-Franz-Josef-Strasse 15, 9490 Vaduz, Liechtenstein

+41766037422

FS120284

Seminar paper

University of Liechtenstein

Graduate School

Programme: MSc in Banking and Financial Management

Course: Seminar in Finance

Module: International Corporate Finance

Assessor: Prof. Dr. Marco J. Menichetti

Working period: 20.02.2014 to 09.06.2014

Date of submission: 09.06.2014

Is Foreign Ownership Beneficial for Creating Value?

2

Table of Contents

Abstract 3

1 Introduction 4

2 Value Creation and Liability of Foreignness with Foreign Ownership 6

3 Literature Review 10

3.1 Supporting Evidence 10

3.2 Weak, Mixed or Opposing Evidence 14

4 Value Creation: Developed versus Emerging Markets 16

5 Conclusion 19

Reference List 20

Affidavit 23

Is Foreign Ownership Beneficial for Creating Value?

3

Abstract

This paper presents an overview of the existing literature on value creation for the stakeholders of

foreign-owned firms. The studies that are examined are systematically classified to developed and

emerging economies. The information obtained suggets that in both developed and emerging markets

there is a positive relationship between foreign ownership and value creation. However, this study

faces certain limitations and conclusively some recommendations for further research are outlined.

Is Foreign Ownership Beneficial for Creating Value?

4

1 Introduction

The globalization in combination with the increasing liberalization of the markets worldwide has facil-

itated the foreign direct investments (FDI). Foreign direct investments in comparison with investing in

securities listed or issued in another country, is an active way of investment with the objective of ob-

taining a lasting interest in an enterprise resident in another economy. Through FDI companies can

establish foreign ownership in another country. The basic criterion used to determine the existence of

foreign ownership is at least 10% ownership of the voting power of the foreign company.1 Foreign-

owned firms are affiliates owned by another company headquartered in a foreign country. Their mar-

ket entrance and subsequent growth create new labour demand. Furthermore, foreign-owned firms

may have access to new technologies provided by their parent company which increase their competi-

tiveness and, as a result, also their demand for labour. In addition, knowledge and technologies might

spill over to domestically owned firms and stimulate their growth as well.2 On the other hand, there are

cases where costs must be incurred so as to operate in foreign markets. This is known as “liability of

foreignness” (LOF) and it will be further examined in the second chapter.

The tendencies in FDI at a global level have been varying throughout years: until 2000 there was a

positive climate for FDI, also supported by favorable government legislation.3 Between 2001 and 2003

the FDI incurred a decrease mainly due to economical growth’s slowdown, while between 2003 and

2007 the FDI increased substantially.4 The negative climate that followed the financial crisis of 2007-

2008 resulted in decrease in FDI in North America and Europe. On the contrary, countries such as

Brazil, Russian Federation, India and China have been increasingly considered as attractive for the

investors.5

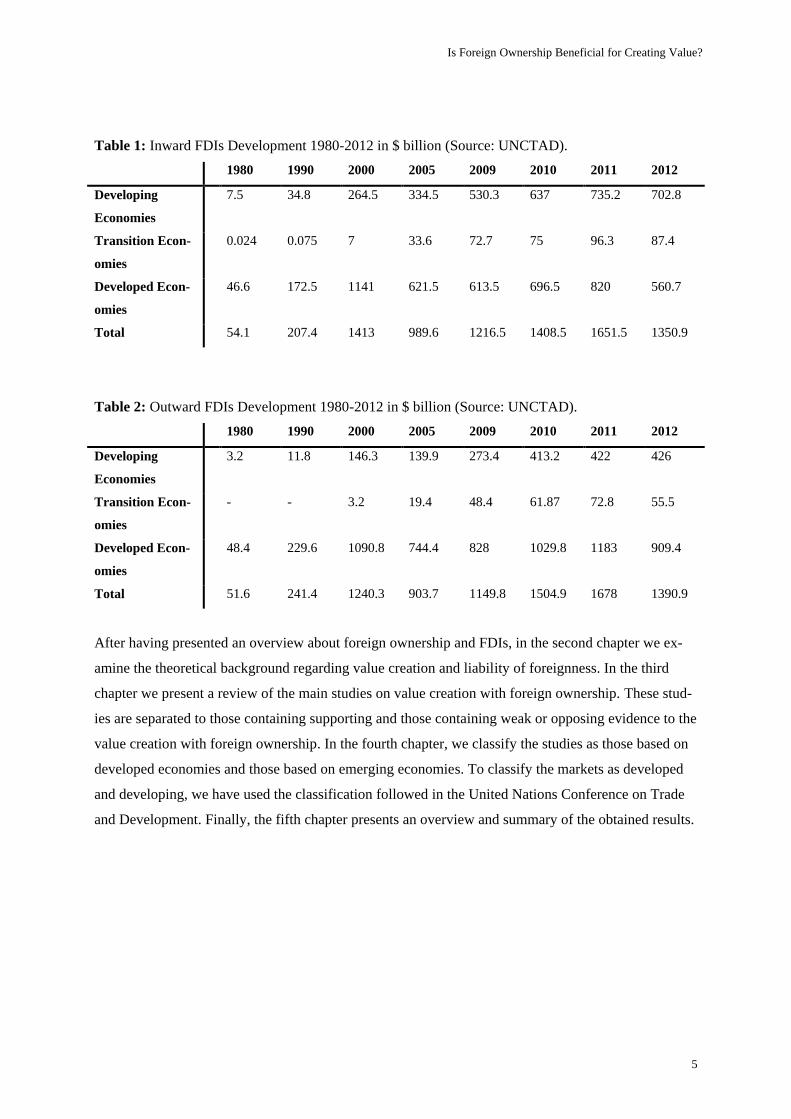

Table 1 and Table 2 show the development of inward and outward FDIs accordingly, where the coun-

tries are grouped in developing, transition and developed economies. It is to be observed that in the

recent years inward FDIs in emerging countries increased substantially and even overwhelmed those if

developed economies in 2012.

1 http://www.oecd-ilibrary.org/sites/factbook-2013-en/04/02/01/index.html?itemId=/content/chapter/factbook-

2013-34-en

2 Dachs, & Peters, 2014, p.214.

3 Mihai, & Cuza, 2012, p.123.

4 Mihai et al., 2012, p.124.

5 Mihai et al., 2012, pp.125-126.

Is Foreign Ownership Beneficial for Creating Value?

5

Table 1: Inward FDIs Development 1980-2012 in $ billion (Source: UNCTAD).

1980 1990 2000 2005 2009 2010 2011 2012

Developing

Economies

7.5 34.8 264.5 334.5 530.3 637 735.2 702.8

Transition Econ-

omies

0.024 0.075 7 33.6 72.7 75 96.3 87.4

Developed Econ-

omies

46.6 172.5 1141 621.5 613.5 696.5 820 560.7

Total 54.1 207.4 1413 989.6 1216.5 1408.5 1651.5 1350.9

Table 2: Outward FDIs Development 1980-2012 in $ billion (Source: UNCTAD).

1980 1990 2000 2005 2009 2010 2011 2012

Developing

Economies

3.2 11.8 146.3 139.9 273.4 413.2 422 426

Transition Econ-

omies

- - 3.2 19.4 48.4 61.87 72.8 55.5

Developed Econ-

omies

48.4 229.6 1090.8 744.4 828 1029.8 1183 909.4

Total 51.6 241.4 1240.3 903.7 1149.8 1504.9 1678 1390.9

After having presented an overview about foreign ownership and FDIs, in the second chapter we ex-

amine the theoretical background regarding value creation and liability of foreignness. In the third

chapter we present a review of the main studies on value creation with foreign ownership. These stud-

ies are separated to those containing supporting and those containing weak or opposing evidence to the

value creation with foreign ownership. In the fourth chapter, we classify the studies as those based on

developed economies and those based on emerging economies. To classify the markets as developed

and developing, we have used the classification followed in the United Nations Conference on Trade

and Development. Finally, the fifth chapter presents an overview and summary of the obtained results.

Is Foreign Ownership Beneficial for Creating Value?

6

2 Value Creation and Liability of Foreignness with Foreign Ownership

There are many authors and scholars that have engaged themselves in analyzing and defining the no-

tion of value. Haksever, Chaganti, and Cook (2004) stated that “Value is the capacity of a good, ser-

vice, or activity to satisfy a need or provide a benefit to a person or legal entity”. 6 In addition, Harvie

and Milburn (2010) stated that “For Marx, value is that which is created by human labour and, in par-

ticular, by human labour in the abstract—and whose measure is money”.7 “Value creation” can be

defined as the performance of actions that increases the value of goods, services and firms as a whole.8

Argandoña (2011) states that value creation cannot only refer to the shareholders, but should encom-

pass all the stakeholders.9 He defined the stakeholders as those who in their relationship with the firm

assume risk: Inside the firm these are the owners, managers and employees, outside the firm the con-

sumers and suppler. What is more in the stakeholders he includes also those who suffer the impact of

the firm’s externalities or misinformation such as the local community, the natural environment, future

generations and the society as a whole.10Firms are able to create value through increasing the abilities

for organizing and coordinating the activities of the company. Value creation can be achieved by

providing goods and services that are hard to produce or are valued for the society. In addition, value

creation can be achieved by focusing on marketing and competitive activities.11 It is crucial to clarify

that the concept of “value creation” by a firm goes beyond the economic value to encompass other

types of value which stakeholders need such as value stemming from corporate social responsibility

actions.12

The liability of foreignness concept comes originally from Hymer’s paper (1976) on disadvantage of

foreign firms in host markets. According to this paper, there are some costs the firms must incur to

establish a new business in a foreign market. First of all, foreign companies have information disad-

vantage as compared to the local companies because the local companies have advantages of better

information regarding the economic and political environment, the law and the language. Thus, the

foreign firms must incur costs to acquire new information inside the host market. Secondly, foreign

firms face risks related to the foreign exchange fluctuations because of the difference of currencies.

For example, an American company that must pay its dividends in dollars, must take this into consid-

eration when deciding to invest in Switzerland. Third, foreign firms may face discriminatory rules to

6 Haksever, Chaganti, & Cook, 2004, p.295.

7 Harvie and Milburn, 2010, p.631.

8 Kraaijenbrink, 2011, p.6.

9 Argandoña, 2011, p.1.

10 Argandoña, 2011, p.4.

11 Kraaijenbrink, 2011, pp.1-2.

12 Argandoña, 2011, p.9.

Is Foreign Ownership Beneficial for Creating Value?

7

establish a new foreign business in host market because the host government may try to protect the

local market from the high competition with foreign entities. Finally, home government may introduce

some restrictions for international activities of national firms by introducing rules. For example, the

American government prohibited Ford of Canada to sell automobiles to China even though it might be

legal for Ford to do so.13

Gaur, Kumar and Sarathy (2011) explained the concept of liability of foreignness, which refers to the

social and economic costs when companies start operations in a foreign country. Further, the authors

state that there are two sources of LOF: Environmentally-derived LOF and firm-based LOF. The envi-

ronmentally-derived LOF comes from hosting and home markets. In contrast, firm-based LOF derives

from ownership structure and firm-specific characteristics.14 The authors argue that the LOF is differ-

ent from market to market. In addition, different structures and experiences result in different levels of

liability of foreignness even within the same market.15

The extent of LOF is moderated by factors such as institutional distance, industry competitiveness and

knowledge intensity, resource gap, internationalization motive, and governance structure. Firstly, the

foreign firm will experience different levels of the liability of foreignness depending on the differences

in institutional development in the home and host countries. In addition, the foreign company that

moves to similar environments- for example from developed to developed or from emerging to emerg-

ing market- will experience less LOF than a firm that moves to a different environment. Firms coming

from well-developed institutional environments may face less LOF as compared to firms coming from

less developed institutional environments. It can be seen that firms in developed markets have stronger

brands and more visibility in emerging market.16

There are several examples of such global brands coming from developed markets that need fewer

investments to operate in emerging markets: From Apple and Microsoft, to MTV, Nokia and McDon-

alds. On the other hand, firms in emerging markets face greater challenges when moving to operate in

developed markets. Firms such as Lenovo from China and Tata Motors from India (acquired the Jagu-

ar and Land Rover automobile brands) faced similar liabilities and attempted to overcome these by

acquiring well-established brands from firms coming from developed countries.17

13 Hymer, 1976, pp.32-35.

14 Gaur, Kumar , & Sarathy, 2011, p.2.

15 Gaur et al., 2011, p.26.

16 Gaur et al., 2011, pp.13-14.

17 Gaur et al., 2011, p.14.

Is Foreign Ownership Beneficial for Creating Value?

8

Secondly, foreign firms will experience different level of LOF depending on the industry they operate

in. Foreign firms in knowledge-intensive industries will experience higher LOF as compared to firms

in less knowledge-intensive industries. In addition, emerging markets are labor-intensive while many

developed market industries are knowledge-intensive so the emerging market firms that want to oper-

ate in developed market will carry a heavier baggage of LOF. To succeed in knowledge-intensive in-

dustries an emerging market firm will have to either acquire the knowledge-based asset or develop it

in-house. Both of these will result in high cost in terms of capital as well as time delays. Moreover,

foreign firms in local industries will experience higher LOF as compared to firms in global indus-

tries.18

Thirdly, the recourse gap between foreign companies and local companies will affect the liability of

foreignness. This means that firms with strong resources will experience low levels of liability of for-

eignness compared to firms with weak resources because the resource gap in assets-that are more dif-

ficult to be acquired from the market- will result in greater LOF than the resource gap in assets that are

less difficult to acquire. Consequently, firms in emerging markets will experience a high level of LOF

because they could not get an equal treatment from customers and other stakeholders in foreign mar-

kets. Fourthly, firms in emerging market with resources and capability seeking motive will experience

less LOF than firms in emerging markets that enter developed markets with market seeking motive.

For example, Industrial & Commercial Bank of China (ICBC) was the world’s largest bank by market

value and thereafter it acquired the US brokerage unit “Fortis Securities”, which was previously con-

trolled by France’s BNP Paribas S.A. This move was a foot-in-the-door approach for the Chinese bank

to tap the international markets of financial services in America.19

Finally, in addition to resource gap, the governance structure of a firm also affects LOF. Foreign firms

that adopt a network form of organization structure will experience less LOF compared to other firms.

In addition, firms in emerging markets with state ownership that want to operate in developed markets

will experience a high level of LOF compared to firms in emerging markets without state ownership.

For example, Chinese and German governments offer subsidies and incentives to providers of solar

power to decrease the cost of production. As a result, this is kind of subsidy may reduce the drive to

efficiency in state owned firms, establishing a competitive disadvantage when competing in foreign

markets, especially in developed markets.20

18 Gaur et al., 2011, pp.15-17.

19 Gaur et al., 2011, pp.19-21.

20 Gaur et al., 2011, pp.22-24.

Is Foreign Ownership Beneficial for Creating Value?

9

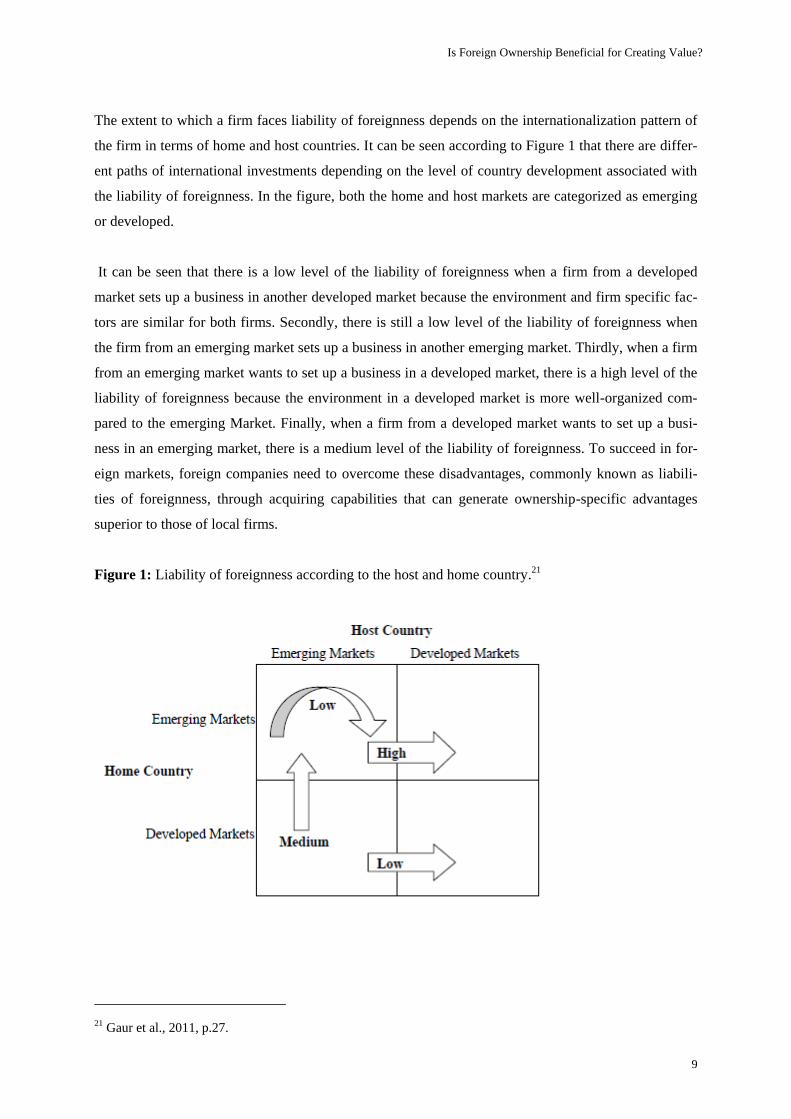

The extent to which a firm faces liability of foreignness depends on the internationalization pattern of

the firm in terms of home and host countries. It can be seen according to Figure 1 that there are differ-

ent paths of international investments depending on the level of country development associated with

the liability of foreignness. In the figure, both the home and host markets are categorized as emerging

or developed.

It can be seen that there is a low level of the liability of foreignness when a firm from a developed

market sets up a business in another developed market because the environment and firm specific fac-

tors are similar for both firms. Secondly, there is still a low level of the liability of foreignness when

the firm from an emerging market sets up a business in another emerging market. Thirdly, when a firm

from an emerging market wants to set up a business in a developed market, there is a high level of the

liability of foreignness because the environment in a developed market is more well-organized com-

pared to the emerging Market. Finally, when a firm from a developed market wants to set up a busi-

ness in an emerging market, there is a medium level of the liability of foreignness. To succeed in for-

eign markets, foreign companies need to overcome these disadvantages, commonly known as liabili-

ties of foreignness, through acquiring capabilities that can generate ownership-specific advantages

superior to those of local firms.

Figure 1: Liability of foreignness according to the host and home country.21

21 Gaur et al., 2011, p.27.

Is Foreign Ownership Beneficial for Creating Value?

10

3 Literature Review

In the two following sections, the evidence from studies on value creation with foreign ownership is

presented. The studies are sorted to those illustrating supporting evidence for value creation through

foreign ownership and those illustrating weak, mixed or opposing evidence.

3.1 Supporting Evidence

In their paper of 1995, Aitken, Harrison and Lipsey examined the relationship between foreign in-

vestments and wages in Mexico (for the period 1984 though 1990), Venezuela (for the period 1977

through 1989) and the United States (for the period 1988-1991). They acquired robust results indicat-

ing that foreign ownership is associated with higher wages for foreign-owned firms, while in the U.S.

the wages spillovers that lead to higher wages are not only limited to the foreign-owned firms, but

further expand to domestically firms.22

Djankov and Hoekman (1999) examined the impact of foreign investments on productivity perfor-

mance of firms in the Czech Republic during the initial post-reform period of 1992-1996. They distin-

guished between firms that established partnerships with foreign firms either through a joint venture or

through direct sale of majority equity stake and those that did not, and ask whether total

factor productivity (TFP) growth rates of these groups of firms differ.23 After corrections for selection

bias, they obtained robust results that foreign investments have a positive impact on the TFP growth of

recipient firms. In addition, FDIs appeared to have a greater impact on TFP growth than joint ventures,

suggesting that parent firms transfer more know-how to their international affiliates than joint venture

firms do.24

Ramachandran and Shah (2000) examined the influence of foreign ownership on firm performance in

Zimbabwe, Ghana and Kenya using data from the World Bank.The data for Ghana were collected in

1991, while for Kenya and Zimbabwe in 1992. They concluded that there is an effect in the form of

value addition, but only for foreign ownership greater than 55%. This study controls for many of the

key inputs into the production, namely quantities of labour, capital in the production process, the level

of worker training and other industry specific effects. They attributed this positive relationship be-

tween foreign ownership and firm value to factors such as timely access to inputs, finance, mainte-

nance personnel, and sources of information about technology and markets.25

22 Aitken, Harrison, & Lipsey, 1996, p.22.

23 Djankov, & Hoekman, 1999, p.2.

24 Djankov et al., 1999, p.20.

25 Ramachandran, & Shah, 2000, pp.15-16.

Is Foreign Ownership Beneficial for Creating Value?

11

Evenett and Voicu in their paper of 2001 examined the effects of FDIs on firm performance in pub-

licly-traded Czech firms for the period 1994-1998- a period following a time of substantial privatiza-

tion and foreign investments. It was found that there is evidence suggesting that benefits from FDIs to

the recipient firms, are sizeable, widespread and robust. However, there is some restraint in this con-

clusion, because there is an inclarity as per the representativeness of the selected sample, due to the

fact that it is more possible that foreign investors pick up larger and more productive companies.26

In their paper of 2002, Conyon, Girma, Thompson and Wright studied the impact of foreign ownership

on productivity and wages in the United Kingdom manufacturing industry for the period 1989-1994.

This study finds a significant labour productivity difference between foreign- and domestically owned

firms, which results in higher wage levels for foreign-owned companies.27

In his paper of 2004, Hao conducted a study on the Japanese market for the period from 1990 to 2001.

He found out that the level of foreign ownership is positively correlated with future stock returns

mainly due to the increase in stock demand from foreign investors.28

Wei, Xie and Zhang (2005) conducted a study on Chinese partially privatized former state-owned

enterprises for the period 1991-2001 using a sample of 5284 firm years.29 They obtained results show-

ing that for eight out of the nine years examined, foreign ownership is significantly related to the firm

value. They attributed this result to better monitoring of the firm by foreign managers, possibly to the

fact that the presence of foreign ownership forces management to act more consistently with the value

maximization and finally to the higher access to international capital markets, as well as advanced

technology and international managerial talents.30

In their study of 2009 on Indonesian manufacturing plants, Arnold and Javorcik investigated the rela-

tionship between foreign ownership and plant performance covering the period 1983-2001. In particu-

lar, they aimed to clarify whether the superior performance of foreign affiliates stems from the strate-

gies the foreign parent company follows to make the foreign affiliates successful or from the fact that

foreign parent companies are successful in selecting the right acquisition targets.31 The study focuses

26 Evenett, & Voicu, 2001, pp.15-17.

27 Conyon, Girma, Thompson, & Wright, 2002, p.100.

28 Javorcik, 2004, p.625.

29 Wei, Xie, & Zhang, 2005, p.87.

30 Wei et al., 2005, p.96.

31 Arnold & Javorcik, 2009, p.2.

Is Foreign Ownership Beneficial for Creating Value?

12

on the causal relationship between the foreign ownership and the plant performance. By implementing

the difference-in-difference method and the method of propensity match scoring to control for selec-

tion bias, the researchers aimed to construct the missing counterfactual of how the acquired plants

would have behaved had they not been acquired.32 In this study 297 acquisition cases are considered

and the data is collected for two years before the acquisition, the acquisition period and two years after

the acquisition.33 The results suggest that the Total Factor Productivity (TFP) increases under foreign

ownership and also the labor productivity does the same. Moreover, the acquired plants produce a

higher output year after year and also pay higher average wages. Furthermore, according to the results,

acquired plants invest in general or just in the machinery between twice and more than three times as

much as plants remaining in domestic hands. What is more, foreign ownership was found to increase

the participation of the acquired plants in international markets, as well as an increase in the volume of

exports. On the contrary, it was found that FDIs do not appear to induce any considerable changes in

the intensity of the labor force. Moreover, the fact that foreign owners may lessen the credit con-

straints of the acquisition targets was not found to be related with the FDIs. Finally, the higher mark-

ups that acquired plants may enjoy as a result of entering export markets does not appear as a possible

explanation for the higher productivity of the plants.34

Usually in literature researchers examine the acquisitions of firms in emerging markets by foreign

firms located in the developed countries. In their paper of 2009, Chari, Chen and Dominguez adopted

a different scope from what is commonly done by looking at the foreign acquisitions of U.S. firms by

firms located in emerging markets and particularly Hong Kong, Singapore, Mexico, South Korea and

Taiwan.35 They examined the period 1980-2007 and similarly to other studies presented in this paper,

they employed a difference-in-difference approach together with a propensity match score with an

intention to examine “how U.S. firms that are acquired by firms from emerging markets fare relative

to their non-acquired counterparts”.36 To do this, they implemented an analysis with two axes: First,

the stock market performance so as to get “a forward-looking estimate of expected shareholder value

creation” and secondly the accounting measures so as to evaluate the after-acquisition performance by

using accounting measures of profitability, investment, sales and employment.37 They further aspired

to figure out the criteria that the acquiring companies consider when selecting a target. The results

suggest that the selection of the acquired companies is not random, but rather based on the level of

32 Arnold et al., 2009, p.7.

33 Arnold et al., 2009, p.11.

34 Arnold et al., 2009, pp.15-21.

35 Chari, Chen & Dominguez, 2009, p.6.

36 Chari et al., 2009, p.1.

37 Chari et al., 2009, p.2.

Is Foreign Ownership Beneficial for Creating Value?

13

sales, employment and total assets. Moreover, the performance of the acquired firm increases both

around the time of the acquisition announcement and the after-acquisition period as indicated by the

return on assets (ROA). At the same time, the firm is undergoing restructuring as indicated by de-

creased employment, sales and capital.38

Romalis (2011) used firm data on cross-border mergers and acquisitions and share prices to examine

whether foreign ownership increases the profitability of firms in emerging markets. The author states

that cross-border acquisitions add more value than the purely domestic acquisitions. In crisis condi-

tions there is evidence of a higher premium for target firms acquired by foreign firms especially in

developed economies.39

In a recent study of 2013, Chang, Chung and Moon aspired to investigate the conditions under which

foreign subsidiaries outperform comparable local firms by employing the propensity score matching

and the difference-in-difference method to control for the endogeneity. They examined 151,192 local

manufacturing firms in China for the period from 1998 to 2007. The analysis period expands to four

consecutive years including one year before the acquisition, the year of the acquisition and two years

after the acquisition.40 The results show that after the acquisition the ROA of the foreign-acquired local

firms increases more than the corresponding ROA of the remaining local firms.41 Moreover, the results

indicate that the acquisitions result in enhanced performance of the local target firms which is higher

for firms with higher intangible assets and modernized processes.42

Another category of papers focus on examining the effect of productivity spillovers in domestic firms

as a result of the presence of multinational potential customers, potential suppliers or even potential

competitors in the local market. In her article of 2003, Javorcik adopted a research question focusing

on whether the productivity of domestic firms is correlated with the presence of multinationals in

downstream sectors or upstream industries (vertical spillovers) and also examines the determinants of

vertical spillovers.43 The study is based on the Lithuanian market and it covers the period 1996-2000.

The results identify positive spillovers from FDI associated with multinational customers, but do not

find enough evidence regarding the effect on multinational companies in the same industry or multina-

38 Chari et al., 2009, p.17.

39 Romalis, 2011, p.117.

40 Chang, Chung & Moon, 2013, p.855.

41 Chang et al., 2013, p.858.

42 Chang et al., 2013, p.859.

43 Javorcik, 2004, pp.606-607.

Is Foreign Ownership Beneficial for Creating Value?

14

tional suppliers. Moreover, the productivity spillovers are mainly detected in investments with joint

foreign and domestic ownership and not with purely foreign ownership.44

3.2 Weak, Mixed or Opposing Evidence

It is not only Hymer (1976) who showed that the disadvantages of foreign companies in host markets

are the costs of doing business abroad (liability of foreignness as described in the second chapter), but

also Buckley and Casson (1976) and Hennart (1982) referred to the costs that companies incur when

they start their foreign operations. In addition, Buckley and Casson (1976) suggested that the addition-

al costs for foreign firms include communication costs, resource costs, host government discrimination

costs, and governance costs. Hennart’s (1982) list of the relevant costs included costs associated with

communication, travel, foreign exchange, and unfamiliarity with the cultural, legal and institutional

aspects of doing business in a foreign country.45

In addition, Zaheer and Mosakowski (1997) showed the impact of the foreign ownership on firm per-

formance by studying the impact of foreignness on survival in inter-bank currency trading worldwide

over the period 1974-1993. The results show that there is a liability of foreignness and changes over

time. Furthermore, they found out that foreign firms must acquire superior competitive advantages

over local firms to compensate for the liability of foreignness. For instance, Zaheer (1995) examined

the probability of foreign firms to have a competitive disadvantage relative to local firms by using

across sectional study of a small sample of paired subsidiaries in the U.S. and Japan and showed that

foreign firms were less profitable than comparable local firms.46

Smarzynska (2002) used firm-level data from Lithuania obtained by the annual enterprise survey over

the period 1996-2000 to examine the correlation between firm productivity spillovers and foreign

ownership within the same industry. The author finds that local firms seem to benefit from the activi-

ties of foreign firms and that greater productivity benefits are related to local companies rather than the

foreign companies. Furthermore, it is shown that there is no difference between the effects of fully-

owned foreign firms and those with joint domestic and foreign ownership. 47

Kronborg and Thomsen (2009) studied the relative survival of foreign firms and local firms in Den-

mark over the period 1985-2005. The outcome of the study shows that there is an evidence of signifi-

44 Javorcik, 2004, p.607.

45 Hennart, 1982, pp.144-145.

46 Zaheer, 1995, p.341.

47 Smarzynska, 2002, p.1.

Is Foreign Ownership Beneficial for Creating Value?

15

cant survival premium for foreign companies but the premium declines over time and disappears at the

end of 2005. The reason of the foreign survival premium decline might be caused due to the corre-

sponding decline of the advantage of the foreign direct investments over time as a result of interna-

tionalization. There are many limitations of this research, for example the authors study a single coun-

try which may not be representative of large strategically important host country markets, so they can-

not confirm the existence of a liability of foreignness.48

In 2009, Petkova examined the relationship between foreign shareholding and firm operating perfor-

mance as measured by firm productivity in the context of a detailed panel dataset of Indian manufac-

turing companies for the period 1988-2008. The results showed that there is no significant difference

between the operating performance of foreign companies and non-foreign companies. In addition,

there is no significant difference between the operating performance of foreign-divested firms and

firms that remain foreign-invested.49

Ferragina, Pittiglio and Reganati (2009) examined the impact of foreign direct investments on Italian

manufacturing and services firms’ survival during the period 2005-2007. First, they distinguished be-

tween foreign multinationals, domestic multinationals and domestic non-multinationals. Secondly,

they distinguished between the impact of foreign presence on Italian-owned multinationals, non-

multinational firms and other foreign-owned firms. The results suggest that during the period 2005-

2007, manufacturing and services firms owned by foreign multinationals are more likely to exit the

market than local companies. Moreover, domestic multinationals have a higher probability to survive

compared to the foreign multinationals.50

Recently, Le and Phung (2013) conducted a research on Vietnamese listed firms by examining the

relationships among foreign ownership, capital structure and firm value on data of all listed companies

in Hochiminh Stock Exchange during the period of 2008-2011 excluding financial firms and banks.

The outcome of the research shows that foreign ownership has negative impact on firm value, but a

positive effect on leverage. However, in the case of the Vietnamese stock market, the foreign owner-

ship is low and monitoring the activities of the foreign ownership faces certain limitations because

foreign investors are not allowed to hold more than 49% of a local firm, so they cannot invest and

influence at their maximum potential.51

48 Kronborg et al., 2009, p.217.

49 Petkova, 2009, p.27.

50 Ferragina, Pittiglio, & Reganati , 2009, p16.

51 Le et al., 2013, pp.25-26.

Is Foreign Ownership Beneficial for Creating Value?

16

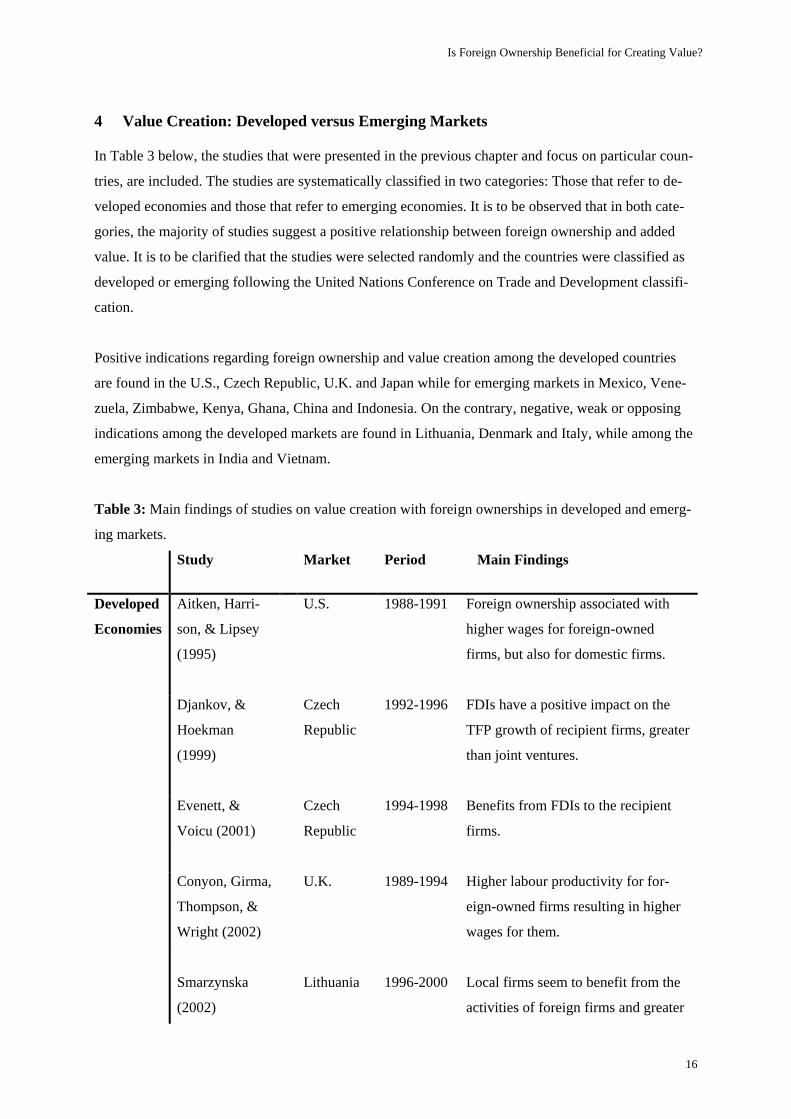

4 Value Creation: Developed versus Emerging Markets

In Table 3 below, the studies that were presented in the previous chapter and focus on particular coun-

tries, are included. The studies are systematically classified in two categories: Those that refer to de-

veloped economies and those that refer to emerging economies. It is to be observed that in both cate-

gories, the majority of studies suggest a positive relationship between foreign ownership and added

value. It is to be clarified that the studies were selected randomly and the countries were classified as

developed or emerging following the United Nations Conference on Trade and Development classifi-

cation.

Positive indications regarding foreign ownership and value creation among the developed countries

are found in the U.S., Czech Republic, U.K. and Japan while for emerging markets in Mexico, Vene-

zuela, Zimbabwe, Kenya, Ghana, China and Indonesia. On the contrary, negative, weak or opposing

indications among the developed markets are found in Lithuania, Denmark and Italy, while among the

emerging markets in India and Vietnam.

Table 3: Main findings of studies on value creation with foreign ownerships in developed and emerg-

ing markets.

Study Market Period Main Findings

Developed

Economies

Aitken, Harri-

son, & Lipsey

(1995)

U.S. 1988-1991 Foreign ownership associated with

higher wages for foreign-owned

firms, but also for domestic firms.

Djankov, &

Hoekman

(1999)

Czech

Republic

1992-1996 FDIs have a positive impact on the

TFP growth of recipient firms, greater

than joint ventures.

Evenett, &

Voicu (2001)

Czech

Republic

1994-1998 Benefits from FDIs to the recipient

firms.

Conyon, Girma,

Thompson, &

Wright (2002)

U.K. 1989-1994 Higher labour productivity for for-

eign-owned firms resulting in higher

wages for them.

Smarzynska

(2002)

Lithuania

1996-2000

Local firms seem to benefit from the

activities of foreign firms and greater

Is Foreign Ownership Beneficial for Creating Value?

17

productivity benefits are related to

local companies rather than the for-

eign companies.

Hao (2004)

Japan

1990-2001

Foreign ownership is positively corre-

lated with future stock returns mainly

due to the increase in stock demand

from foreign investors.

Chari, Chen,

&Dominguez

(2009)

U.S. 1980-2007 Performance of the acquired firms

increases both around the time of the

acquisition announcement and the

after-acquisition period as indicated

by ROA.

Kronborg,

&Thomsen

(2009)

Denmark 1985-2005 Evidence of significant survival pre-

mium for foreign companies but the

premium declines over time and dis-

appears at the end of 2005.

Ferragina,

Pittiglio, &

Reganati (2009)

Italy 2005-2007 Manufacturing and services firms

owned by foreign multinationals are

more likely to exit the market than

local companies.

Emerging

Economies

Aitken, Harri-

son, & Lipsey

(1995)

Mexico 1984-1990 Foreign ownership associated with

higher wages for foreign-owned

firms.

Aitken, Harri-

son, & Lipsey

(1995)

Venezuela 1977-1989 Foreign ownership associated with

higher wages for foreign-owned

firms.

Ramachandran,

& Shah (2000)

Zimbabwe

1992

There is an effect in the form of value

addition, but only for foreign owner-

ship greater than 55%.

Ramachandran,

& Shah (2000)

Kenya 1992 There is an effect in the form of value

addition, but only for foreign owner-

ship greater than 55%.

Is Foreign Ownership Beneficial for Creating Value?

18

Ramachandran,

& Shah (2000)

Ghana 1991 There is an effect in the form of value

addition, but only for foreign owner-

ship greater than 55%.

Wei, Xie, &

Zhang (2005)

China 1991-2001 Foreign ownership is significantly

related to the firm value.

Arnold, &

Javorcik (2009)

Indonesia

1983-2001

Under foreign ownership TFP and

labor productivity increases. Moreo-

ver, the acquired plants produce a

higher output year after year, pay

higher average wages, invest more in

general or just in the machinery and

increase the participation in interna-

tional markets, as well as the volume

of exports.

Petkova (2009)

India 1988-2008 No significant difference between the

operating performance of foreign

companies and non-foreign compa-

nies.

Chang, Chung,

& Moon (2013)

China 1998-2007 The ROA of foreign-acquired local

firms increases more than the corre-

sponding ROA of the remaining local

firms. Moreover, acquisitions result in

enhanced performance.

Le, & Phung

(2013)

Vietnam 2008-2011 The outcome of the research shows

that foreign ownership has negative

impact on firm value, but a positive

effect on leverage

Is Foreign Ownership Beneficial for Creating Value?

19

5 Conclusion

In the scholar literature there are many studies that aspire to establish a relationship between foreign

ownership of firms and value creation. As already described, value creation should not only refer to

shareholders, but also to all the stakeholders of the firm in both the internal and external environment.

Some studies find a beneficiary impact of foreign ownership for the acquired firms due to transfer of

know-how, productivity improvements, access to international capital markets and other factors. On

the contrary, other studies argue that foreign ownership has a negative effect due to the costs firms

must incur to establish a new business in a foreign country, which is known as “liability of foreign-

ness”.

The studies examined are sorted according to the market where they are implemented. The two catego-

ries of markets that are examined are the developed and emerging markets. The information obtained

suggests that in both developed and emerging markets there is a positive relationship between foreign

ownership and value creation. However, no safe conclusion could be drawn given the fact that the

number of studies examined is limited and also there is no consistency regarding the time frame. There

is need for further comprehensive research that encompasses a considerable number of countries from

both the developed and the emerging markets and extends to a statistically significant time span.

Is Foreign Ownership Beneficial for Creating Value?

20

Reference List

Aitken, B., Harrison, A, & Lipsey, R. (1997). Wages and Foreign Ownership: A Comparative Study of

Mexico, Venezuela and the United States. NBER Working Paper 5102, 40 (3), 345-371. doi:

10.3386/w5102. Retrieved from: http://www.nber.org/papers/w5102

Argandoña, A. (2011). Stakeholder Theory and Value Creation.IESE Business School Working Paper

922. Retrieved from: http://ssrn.com/abstract=1947317

Arnold, J., & Javocik, B. (2009). Gifted Kids or Pushy Parents?: Foreign Direct Investment and Plant

Productivity in Indonesia. University of Oxford: Department of Economics Discussion Paper

Series, 1-48. Retrieved from: http://www.economics.ox.ac.uk/Department-of-Economics-

Discussion-Paper-Series/gifted-kids-or-pushy-parents-foreign-direct-investment-and-plant-

productivity-in-indonesia

Buckley, P., & Casson, M. (1976). The International Operations of National Firms: The future of the

Multinational Enterprise. Macmillan.

Chang, S-J., Chung, J., & Moon, J. (2013). When Do Foreign Subsidiaries Outperform Local Firms?

Journal of International Business Studies, 44 (8), 853-860, 2013. doi: 10.1057/jibs.2013.35.

Retrieved from: http://ssrn.com/abstract=2341026

Chari, A., Chen, W., & Dominguez, K. (2009). Foreign Ownership and Firm Performance: Emerging-

Market Acquisitions in the United States. NBER Working Paper 14786, 1-38. doi:

10.3386/w14786. Retrieved from: http://www.nber.org/papers/w14786

Conyon, M., Gima, S., Thompson, S., & Wright, P. (2002). The Productivity and Wage Effects of

Foreign Acquisition in the United Kingdom. The Journal of Industrial Economics, 50 (1), 85-

102. Retrieved from: http://www.jstor.org/stable/3569775

Dachs, B., & Peters, B. (2014). Innovation, Employment Growth, and Foreign Ownership of Firms: A

European Perspective. Research Policy, 43 (1), 214-232. doi: 10.1016/j.respol.2013.08.001.

Retrieved from: http://www.sciencedirect.com/science/article/pii/S0048733313001418

Djankov, S., & Hoekman, B.(1999). Foreign Investment and Productivity Growth in Czech Enterpris-

es. Working Paper, 1-24. doi: 10.1596/1813-9450-2115. Retrieved from:

http://elibrary.worldbank.org/doi/book/10.1596/1813-9450-2115

Evenett, S., & Voicu, A. (2001). Picking Winners or Creating them?: Revising the Benefits of FDI in

the Czech Republic. Working Paper, 1-28. Retrieved from:

http://webcache.googleusercontent.com/search?q=cache:bN_YmHIn7QwJ:https://www.alexan

dria.unisg.ch/export/dl/22271.pdf+&cd=1&hl=el&ct=clnk&gl=de

Ferragina, A., Pittiglio, R., & Reganati, F. (2009). The impact of FDI on firm survival in Italy. FIW

Working Paper 35.Retrieved from:

http://www.fiw.ac.at/fileadmin/Documents/Publikationen/Working_Paper/N_035-

FERRAGINA_PITTIGLIO_REGANATI.pdf

Is Foreign Ownership Beneficial for Creating Value?

21

Gaur, A., Kumar, V., & Sarathy, R. (2011). Liability of Foreignness and Internationalization of

Emerging Market Firms. Emerald, 24, 211-233. Retrieved from:

http://ssrn.com/abstract=1763328

Haksever, C., Chaganti, R., & Cook, R. (2004). A Model of Value Creation: Strategic View. Journal

of Business Ethics, 49 (3), 295-307. Retrieved from: http://www.jstor.org/stable/25123172

Harvie, D., and Milburn, K. (2010). Speaking out: How Organizations Value and how Value Organiz-

es. Organization, 17 (5), 631-636. Retrieved from: http://hdl.handle.net/2381/8506

Hennart, J.F. (1982). A Theory of Multinational Enterprise. University of Michigan Press.

Hymer, S. (1976). The International Operations of National Firms: A Study of Direct Foreign Invest-

ment. MIT Press. Retrieved from:

http://teaching.ust.hk/~mgto650p/meyer/readings/1/01_Hymer.pdf

Javorcik, B. (2004). Does Foreign Direct Investment Increase the Productivity of Domestic Firms?: In

Search for Spillovers through Backward Linkages. The American Economic Review, 94 (3),

605-627. Retrieved from: http://www.jstor.org/stable/3592945

Kraaijenbrink, J. (2011). A Value-Oriented View of Strategy. Working paper. Retrieved from:

http://kraaijenbrink.com/wp-content/uploads/2012/06/A-value-oriented-view-of-strategy-

Kraaijenbrink-15-04-2011.pdf

Kronborg, D., & Thomsen, S. (2009). Foreign Ownership and Long-term Survival. Strategic Man-

agement Journal, 30 (2), 207-219. Retrieved from: http://www.docin.com/p- 57737336.html

Le, T., & Phung, D. (2013). Foreign Ownership, Capital Structure and Firm Value: Empirical

Evidence from Vietnamese Listed Firms. University of Economics Hochiminh City. Re-

trieved from: http://ssrn.com/abstract=2196228

Mihai, C., & Cuza, A. (2012). The Context and New Trends of Foreign Direct Investment Flows. The

USV Annals of Economics and Public Administration, 12 (15), 121-129. Retrieved from:

http://seap.usv.ro/annals/ojs/index.php/annals/article/viewFile/463/470

OECD iLibrary. Foreign Direct Investment. Retrieved April 15, 2014, from: http://www.oecd-

ilibrary.org/sites/factbook-2013-en/04/02/01/index.html?itemId=/content/chapter/factbook-

2013-34-en

Petkova, N. (2009). Does Foreign Shareholding Improve Firm Operating Performance?: Financial

Management Association International. Retrieved from:

http://www.fma.org/Reno/Papers/FDI_and_firm_performance.pdf

Ramachandran, V., & Shah, M. (2000). Foreign Ownership and Firm Performance in Africa: Evidence

from Zimbabwe, Ghana and Kenya. RPED Discussion Paper 81, DC:World Bank, 1-36. Re-

trieved from: http://documents.worldbank.org/curated/en/2000/01/12827495/foreign-

ownership-firm-performance-africa-evidence-zimbabwe-ghana-kenya

Romalis, J. (2011). The Value of Foreign Ownership. Economic and Business Review Journal,

13, (1-2), 107-118. Retrieved from:

Is Foreign Ownership Beneficial for Creating Value?

22

http://www.ebrjournal.net/ojs/index.php/ebr/article/download/81/pdf

Smarzynska, K. (2002). Does Foreign Direct Investment Increase the Productivity of Domestic

Firms: In Search of Spillovers through Backward Linkages. The World Bank, Policy Re-

search Working Paper Series 2923. Retrieved from:

http://elibrary.worldbank.org/doi/pdf/10.1596/1813-9450-2923

United Nations Conference on Trade and Development. (2013). UNCTAD Handbook of Statistics

2013. Retrieved from:

http://unctad.org/en/pages/PublicationWebflyer.aspx?publicationid=759

Wei, Z., Xie, F., & Zhang, S. (2005). Ownership Structure and Firm Value in China's Privatized Firms:

1991–2001. Journal of Financial and Quantitative Analysis, 40, 87-108.

doi:10.1017/S0022109000001757. Retrieved from:

http://journals.cambridge.org/action/displayAbstract?fromPage=online&aid=4200740&fileId=

S0022109000001757

Zaheer, S. (1995). Overcoming the Liability of Foreignness. Academy of Management Journal, 38 (2),

341-363. Retrieved from:

http://winfobase.de/lehre%5Clv_materialien.nsf/intern01/A86A0DB8DE3B7D22C12577B500

308A01/$FILE/14%20Liability%20of%20Foreignness.pdf

Zaheer, S., & Mosakowski,E. (1997). The Dynamics of the Liability of Foreignness: A Global Study

of Survival in Financial Services. Strategic Management Journal, 18 (6), 439-463. Retrieved

from: http://www.business.uconn.edu/ciber/documents/thedynamicsliabilityofforeignness.pdf

Is Foreign Ownership Beneficial for Creating Value?

23

Affidavit

Is Foreign Ownership Beneficial for Creating Value?: An Insight into Existing Literature

for Developed and Emerging Markets

We hereby declare under penalty of perjury that the present paper has been prepared independently by

us and without unpermitted aid. Anything that has been taken verbatim or paraphrased from other

writings has been identified as such. This paper has hitherto been neither submitted to an examining

body in the same or similar form, nor published.

Vaduz, 09.06.2014

Signature:

Osama Abdeltawab Effrosyni Panagakou