IRPC Investor Update - listed company

44

INVESTOR UPDATE May 2020

Transcript of IRPC Investor Update - listed company

INVESTOR UPDATE

May 2020

2

AGENDA

Strategic Direction

Performance Highlight

Projects Update

Company Profile

Industry Outlook

Appendix

47.55%

5.19%

8.95%

38.30%

Others

Introduction to IRPCIntegrated Petrochemical Complex

3

Shareholding Structure*

PTT secures 100% crude procurement for IRPC at the market price

Receive 90 days credit term from PTT

Petroleum Product off-take and swap agreement with PTT group on arm-length basis

Strong support of credit facilities from PTT thru Intercompany Borrowing & Lending (ICBL) program

IRPC are under umbrella of PTT group’s centraltreasury management framework

PTT

Crude Procurement &

Credit Term

Product Swaps and Off-takes

Financial and Risk Control

Systems

Operational & Strategic Relationships with PTT Group

Complex & Facilities

*Note: as of Feb 2020

• Integrated petrochemical complex: Upstream to downstream in a single complex

• Locate in Industrial Area: Eastern Seaboard Area of Thailand, 200 km. from Bangkok and 30 km. from Map Ta Phut Industrial Area

• Facility Support:- Deepest sea port- Tank Farm and Power Plant- Thailand’s main coastal highway

Market Cap. : 59,260 MB

(as of May 19, 2020)

Credit Rating

A-(tha) Stable Outlook

Thai NVDR

Foreign

4

Petroleum and Petrochemical Capacity

Petroleum

Port and Tank Services

Utilities307 MW Power plant

Facilities & Utilities

Refinery• LPG• Naphtha• Gasoline• Diesel• Fuel Oil

Lube Base• Lube Base Oil• Asphalt

Olefins• Ethylene• Propylene• Butadiene

Aromatics• Benzene• Toluene• Mixed Xylene

Styrenics• EBSM

Polyolefins• HDPE• PP

Polystyrenics• ABS• PS• EPS

Petrochemical Capacity• Monomer 1,848 KTA• Polymer 1,267 KTA

3,115 KTA

Crude Refining Capacity

215 KBD

Freehold Land~4,000 Acres

(~10,000 Rais)

1,221

367

915

352

920

215

Unit: KTA

Unit: KBD

Unit: KTA260

5 Depots

Petrochemical

5

IRPC’s Profile

Refinery Capacity : 215 KBD (crude distillation unit)

Petrochemical Capacity : 3,115 KTA (Olefins, Aromatics, Styrenics,

Polyolefins, Polystyrenics)

1

PP’s leading producer in South-East Asia: 775 KTA

HDPE pipe grade 140 KTA

ABS 179 KTA: The Largest producer in Thailand

2

Lube base oil : 320 KTA

Asphalt : 600 KTA

3

55% of specialty petrochemical portfolio

PPC to add more specialty Petrochemical Products

Specialty : 10-20% higher margin vs Commodity

5

Integrated

Petrochemical Complex &

Product Diversification

Remarkable Position

in ASEAN

Polymer Market

The largest lube base oil capacity

in Thailand

Power & Utility business : ~ 1.0 $/bbl to GIM

Additional contribution from utility JV starting from 2018

Stable income from Port and Tank business

4 Sustained earnings

from facility

and utility businesses

Specialty Petrochemical

to capture

higher margin

6

Petroleum and Petrochemical Value Chain Optimized Configuration & Product Diversification

Olefins Plant PropyleneEthyleneAcetylene Butadiene

180 KTA360 KTA6 KTA56 KTA

Vacuum Gas Oil (VGO)

PP

PS

ABS/SAN

EPS

CCM

Acetylene Black

HDPEEthylene

Acetylene

Propylene

Benzene

TolueneMixed Xylene

Butadiene

CD1

Ethylene

EBSM

4 KTA

140 KTA

775 KTA

Ethylene Rich Gas

DCC

Propylene 132 KTA

ADU1 65 KBD

ADU2 150 KBD

215 KBD

Naphtha

Reformate

UHV

Ethylene Propylene 320 KTA

73 KTA

Lube BaseLube Base Oil Asphalt

320 KTA600 KTA

BTX Benzene TolueneMixed Xylene

114 KTA132 KTA121 KTA 31 KTA

57 KTA

179 KTA

125 KTA

48 KTA

260 KTAStyrene Monomer

Acrylonitrile

Feed (Crude Oil / Condensate)Transportation FuelDiesel/JetGasolineFuel Oil

PRP

HS ATB

Propylene 100 KTA

Pyrolysis Gasoline Raffinate

Styrene Monomer

LS ATB

For sale

HS ATB

68% 17% 6% 9%

2019 Crude/Condensate Portfolio

Middle east Far east Domestic Others

Polyolefins Products

7

PP Polypropylene has medium transparency. It features such significant properties as high stiffness, high surface hardness, high heat and medium impact strength. It can be used for the manufacture of kitchenware, household items, stretch tape, electrical parts, fertilizer bags, sugar bags, woven bags, hot fill bags, etc.

Resin Appearance Sample

PE High Density Polyethylene (HDPE) has an opaque appearance. Products exhibit high tensile, impact strength and high chemical resistance.

Styrenics Products

8

Acrylonitrile Butadiene Styrene (ABS) features such significant properties as high impact strength, high heat and chemical resistance, high stiffness and high gloss including weather resistance. It is mainly used for the manufacturing of electrical parts, automotive parts, bicycle parts, household items, kitchenware, office supplies, toy, etc

Polystyrene (PS) can be divided into 2 types as follows; General Purpose Polystyrene (GPPS) has significant properties of transparency, rigidity, and process ability which are ideal for production of products, such as electrical parts, cassette tapes, CD boxes, household items, including foam boxes, food tray, etc. High Impact Polystyrene (HIPS) has significant properties of high impact strength, and process ability which are suitable for producing electrical parts, frame of TV, air conditioner, computers, toys, sanitary wares, office suppliers, plastic cup and tray, etc.

ABS

PS

Resin Appearance Sample

9

AGENDA

Strategic Direction

Performance Highlight

Projects Update

Company Profile

Industry Outlook

Appendix

QoQ 24%

30

31

32

33

10

Key DriversCrude oil price collapse amid Saudi Arabia – Russia price war & COVID-19 pandemic

30

40

50

60

70

80

Brent Dubai

Crude Oil Price (avg)

Gross Refining Margin (GRM)

Foreign Exchange (avg)

Product to Feed Margin (PTF)

Unit: $/bbl Unit : THB/USD

Unit: $/bbl Unit: $/bbl

YoY 56%

QoQ 52%

YoY 18%

31.8

Dubai QoQ 18%

Dubai YoY 20%

QoQ depreciated 3%

YoY appreciated 1%

31.8

1Q19 2Q19 3Q19 4Q19 1Q20

Brent 63.2 68.8 61.9 63.2 50.3

Dubai 63.5 67.4 61.2 62.1 50.71Q19 2Q19 3Q19 4Q19 1Q20

30.9 30.5 31.5

5.2 5.2

2.5 1.9 1.7

0.8

2017 2018 2019 1Q19 4Q19 1Q20

8.3 7.3

5.1 5.7

3.8 4.7

2017 2018 2019 1Q19 4Q19 1Q20

YoY 52% YoY 30%

53.269.4 63.5 63.5 62.1

50.7

11

Key Performance

20,420 18,344

5,940 2,355 543

(6,436)

Net Sales (net excise tax)

Unit: MB

EBITDA

Unit: MB

Performance by Business

Net ProfitUnit: MB

Petroleum Petrochemical Utilities & Others

Net Sales(net excise tax)

Dubai (Avg.)Unit: $/bbl

197,594 258,919

216,577

54,274 50,337 43,617

Crude Run (KBD)

EBITDA

Net Profit

Market GIM ($/bbl)

Acct. GIM ($/bbl)

Net Stock G/(L)($/bbl)

YoY 115%

YoY 68%

YoY 16%

Operating NINet Income

8,621 8,859

(2,982)(780)

(2,330)(43)

11,354 7,735

(1,174)

153

(513)

(8,905)

2017 2018 2019 1Q19 4Q19 1Q20

1Q20 VS 4Q19200 190 188

QoQ 13%

YoY 20%

QoQ, YoY – n.a.

180 208 197

14.48 13.60 8.70

1.01 (0.50) 0.27

15.49 13.10 8.97

QoQ , YoY – n.a.

QoQ 98%

YoY 94%

8.68 6.76 6.82

1.26 1.38 (12.66)

9.94 8.14 (5.84)

(107%) (95%)

102%

(83%)(20%)

3%

5%

(20%)

115%

(93%)

(17%)

10%

72%

27%

1%

69%

29%

2%

4Q19 1Q20 4Q19 1Q204Q19 1Q20

4Q19 1Q20 4Q19 1Q204Q19 1Q20

4Q19 1Q20 4Q19 1Q204Q19 1Q20

12

Net Profit: 1Q20 VS 4Q19Net Stock loss & unrealized loss on derivatives resulted in a drop of Net Profit

60

Net Loss 4Q19

Margin Net Stock loss

OPEX & Selling

Exp.

Oil Hedging

Unrealized

Financial Derivatives

FX Tax & Others

Net Loss 1Q20

Operating Income 98%

Net Income – n.a.(513) (8,905)

(2,330) (43)

Unit: MB

13

AGENDA

Strategic Direction

Performance Highlight

Projects Update

Company Profile

Industry Outlook

Appendix

14

Projects UpdatedFloating Solar Project with Electricity 12.5 MW ABS Expansion: Increasing ABS specialty by 6,000 MTA

Construction ProgressABS Expansion

Project Objective : Increase 6,000 MTA of Specialty

ABS Powder. Recovery Vapor Butadiene

278 MTA from Flare.

CAPEX : ~ 430 MB

IRR : ~ 17%Project Progressas of April 2020

: 80% of Target

Installing equipment and

Piping work under

progression

MC : 3Q20

COD : 3Q20

Project Progressas of April 2020

Project Objective : To produce electricity 12.5 MW Floating Support material by

own HDPE BOI Privilege

Area: Reservoir in Industrial Park

Usage: Internal use at PP Plant

CAPEX : ~ 550 MB

IRR : ~ 17%

Floating Solar

: 99% of Target

Construction Progress

MC : April 2020

COD : 2Q20

15

UHV project : Major CAPEXImprove product yield and earnings

IRPC’s refined Production Yield

Upstream project for Hygiene & Value-added Products

Objective : Upgrade low value to high valued-added products

Investment : $ 1.1 bn

COD : Jul. 2016

Benefit : GIM 1.5-2.0 $/ bblAssumption : Spread propylene to FO ~ 500-600 $/ton

RDCC unit Feed Cut-in

@ Jun 16 COD @ Jul 16

HYVAHL unit Feed Cut-in

HS-ATB @ Jul 16 COD @ Jul 16

Performance Guarantee Test RDCC run 100%

@ Oct 2016

Plant Acceptance

(PAC)

Jan 2017

43%

80%

99%

2016A 2017A 2018A

Upgrade to High Valued-Added products

131

123

163

367

220

326

74

HSFO

LPG

Ethylene

HYVAHL

Propylene

Naphtha

FO/FG

Middle Distillates

RDCC

C4 Raffinate III

Internal use & Loss

Unit : KTA

16%

5%

23%

9%

9%

26%

12%

Flow Diagram

LSFO

UHV

Designed Yield

23%8% 11%

4%2%

2%

14%

10%15%

11% 11%

40%

38%

45%

47% 47%

5%

10%

8%12% 12%

16%

21%

16%16% 16%

2%

5%3% 5% 5%6%1% 4% 4%

2% 1% 1%

IRPC IRPC+UHV IRPC2015A

IRPC2018A

IRPC2019A

Ethylene

Propylene

LPG

Naphtha

Gasoline

Diesel/Jet Fuel

Lube Oil

LSFO 0.5%S

HSFO

Designed Yield

CompoundingHouse

PP inline compound

16

PPE&PPC Benefit EnhancementFulfill UHV benefits thru higher margin on PPE & PPC

Random PP• Pipe grade• Hygiene

Super Clear PP• Container box• Medical Device

Block-CO PP• Household Material• Heavy-duty

HOMO PP• Film application• Fiber grade

PP Specialty•Frozen food packaging•Lamination•Health care

PP Compound• Automotive:

pumper, instrument panel, etc

PPE 160 KTA PPC 140 KTA

Total PP 775 KTA in 2017

PP Existing 475 KTA

PP Expansion and PP Compound Project

Lower cost : PPC production by Inline process technology

Note: Cost Saving • No Packing & Logistic• No 2nd Extruder Process

PP Marketing Strategy : Sales Plan

Y2017

Volume: 600 Ktons

Y2022

Volume: 760 Ktons

PP Expansion Project (PPE) Licensor : Novolen Capacity : 160 KTA PMC : Foster Wheeler EPC : Sinopec

• CAPEX : $ 236 mn• GIM 0.8-1.0 $/bbl• COD : 4Q17

Random PP4%

Homo PP

75%

Block-CO PP21%

PP Compound11%

Random PP10%

Homo PP

58%

Block-CO PP21%

PP Compound & Specialties (PPC) Licensor : JPP Capacity : 140 KTA PMC : Foster Wheeler EPC : Sinopec

17

AGENDA

Strategic Direction

Performance Highlight

Projects Update

Company Profile

Industry Outlook

Appendix

Impact of the outbreak of COVID-19 and mitigation strategies

Spunbond

Face Shield

Alcohol

Key Actions for supporting the COVID-19 outbreak Our Survival Mode

Modular room

Negative-pressure Bed

Business Continuity Management (BCM)

Employees Protection

Social Contribution

Liquidity management

Production and marketing strategies alignment

Tighten Operating expenses (OPEX)

Capital spending plan (CAPEX) Reconsideration

Strengthen IRPC projects

18

19

Survival Mode

1. Maintain Market Position

2. CAPEX & OPEX Reduction

3. Strengthen IRPC

20

1. Maintain Market PositionRelationship-based strategies and Portfolio management

Key challenges and mitigation: Protect domestic market share and search for new territories

Petrochemical ProductsPetroleum Products

-1.0 -0.5 0.0

Diesel

Gasoline

Jet

Lube

IRPC MKT

-30%

-20%

Overall reduction in demand, decline across Petroleum products portfolio especially gasoline and jet

-100%

-50%

-40%

-30%

-10%

Impact across petrochemical, some sectors harder hit especially automotive, electronic and industrial while packaging and consumer remains strong

Key challenges and mitigation: Closely monitor customer’s inventory & adjust proportion export

%Market demand decline (2Q20F)

▪ Keep contract of domestic demand based on market decline to maintain market share

▪ Export sales to countries those are not lockdown or partial lockdown

▪ Jet is only 4-5% of refinery portfolio, swap to diesel pool

▪ Lube products group : maintain South East Asia and China customers

▪ Demand decline both domestic and export

▪ Demand decline both domestic and export

Key challenges Mitigation Key challenges Mitigation

No impact

▪ Secure order with contract customer

▪ Review and negotiate with strategic partner to ensure order

▪ Spot order move to focus area

▪ Closely monitor and follow up customer’s inventory to immediate response after lock down

-0.5 -0.3 0.0

Polystyrenics

Polyolefins

IRPC MKT

-30%

-20%

-30%

-25%

%Market demand decline (2Q20F)

Stress case Stress case

21

2. CAPEX & OPEX ReductionTotal 5 years CAPEX plan decreased ̴ 48% and OPEX decreased ̴ 13% after review

41,598

15,009

12,355

10,870

2,176

2020-2024Plan

2020-2024Review

53,953

28,055

-48%

Strengthen IRPC

General CAPEX

4,010 2,159

2,952

2,367

254

2020 Plan

6,962

254

2020 Review

4,780-31%

CAPEX Reduction 2020-2024 (MB)

CAPEX 2020 (MB)

OPEX Reduction 2020 (MB)

2020 Plan 2020 Review2020 Plan 2020 Review

Projects

-13%

22

3. Strengthen IRPCDriven performance by “Strengthen IRPC” program to deliver benefit

Significant EBITDA impact (total value estimated at 4,600+ MB)

▪ “Strengthen core business IRPC”

▪ Cross functional team from Operation , Commercial , Business development , ISC M&R and RD to

– Safety

– Reliability

– Productivity

– Increase specialties products

– Conversion cost reduction

– Enhance value of idle asset

– Inventory management

– Increase distribution channel

▪ Project governance by IRPC ourselves

Benefit Forecasted for 2020 ≈ 1,904 MB (Off PL 640 MB)

MB

Overview of impact and capital required

254

1,530

392

2,1761,904

7731,069

855

4,600

20222020 2021 2023 total

CAPEX

Benefit

886

1,904

329

E4E

Breakthrough Project

IRPC 4.0

total

MB

689

23

3.1 Inventory ManagementMinimize inventory and keep less

Spare Part Management:Minimize stock and more cooperation with partner / supplier

Total Spare Part2,200 MB

Fast Move200 MB

Min - Max500 MB

Non/Slow Move1,500 MB

Method

Challenge reason to stock

Co-develop strategy with supplier

Co-develop strategy with group

Crude & Product Inventory:Reduce product and intermediate

2020 2021 2022

200

400 400

3 Phases development during 2020 – 2022

Targetsaving ~ 1,000 MB

11.010.6

0.0

5.0

10.0

0.0

5.0

10.0

15.0

Existing Target Y20

Reduce product & intermediate inventory ~400K Barrels

-4%

Million bbl

Unit: MB

24

3.2 STARGATE

Project description :

Provide strategic gateway for domestic market via pipeline system

Support UCF project

Scope:

Margin improvement

Increase competitive advantage in domestic oil market

CAPEX : Minimal or none

Margin Improvement : 500 - 600 MB

COD : 2Q2023

STARGATE

Future Opportunity

25

AGENDA

Strategic Direction

Performance Highlight

Projects Update

Company Profile

Industry Outlook

Appendix

26

Crude Oil Outlook

Source: Platts

2Q20 oil demand growth heavily fall to 18.9 MMB/D due to coronavirus triggered lockdown but will be getting better in 2H20 amid concern on economic activities

So far, 13.2 MMB/D of shut ins announced from core OPEC (6.1), Russia (2.1), Canada (1.0), US (1.7) and Other International (2.3)*

* As of 12/5/2020

Remark : Additional cut in Jun 1.18 from Saudi, UAE and Kuwait and US estimate to cut up to 3 MMB/D (Total reduction in Jun ~17.38 MMB/D)

27

Singapore Crack Spread on Dubai

Source: FGE

$/bbl

Weak demand of Gasoline and Kero/Jet drive lower crack spread while lifting of lockdown help crack move up slowly

Huge drop in demand but now see positive growth sign

Source: Platts

28

IMO 2020

Weekly worldwide demand for marine fuels YoY change 2020 vs 2019

Source: IHS

Tanker demand support from storage opportunities for

crude oil and refined products as contango market

Increase of Middle Distillate demand blend into bunkers

Source: Platts

Share of Bunker Sales by Product

Notes: * Tanker includes crude, refined products, LPG and chemicals ** Cruise ships and other passenger vessels under other

29

Petrochemical Outlook : Polypropylene

Polypropylene world operating rate

Previous forecast

World : Addition Capacity

Regional Polypropylene Net Trade Polypropylene Per Capita Consumption

>80%

World’s per capita Consumption at 9.9 kg up from 9.6 kg in 2018Is expected to reach 11.6 kg by 2024

World

Mainly export from ME to Asia

Global operating rates averaged 86% for 2019-2024Strong demand by NEA, SEA, India due to continued urbanization

30

Petrochemical Outlook : HDPE

HDPE world operating rate World : Addition Capacity

Regional HDPE Net Trade Southeast Asia : HDPE Trade

>80%

Mainly export from ME to Asia

Global operating rates averaged 84% for 2019-2024Low-cost producers MDE, NAM is pressuring high-cost producers

Southeast Asia : Net import

31

Petrochemical Outlook: ABS

World : ABS Supply & Demand

World: 2019 ABS Demand by Region

World : ABS Capacity Addition by Region

World : ABS Demand by Application

32

AGENDA

Strategic Direction

Performance Highlight

Projects Update

Company Profile

Industry Outlook

Appendix

0.31

0.19

-0.04

0.04

-0.26

0.46 0.48

0.56

0.38

-0.06

0.08 0.10 0.08

0.22 0.230.29

0.10

0.08 0.08 0.10

0.100.04

0.09

0.180.12

0.19

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

EPS

Year Dividend

1H Dividend

2H Dividend

33

Dividend Policy & PaymentIRPC is firmly committed to pay dividend at no less than 25% of net income

58% 63%

25% 25% 25%

48% 48% 52% 50%

25%

Dividend Yield 2.8% 2.9% 1.9% 3.1% 2.6% 5.1% 4.8% 4.1% 3.3% 2.7%

Share Price 1 6.50 4.08 4.12 3.26 3.06 4.30 4.80 7.05 5.75 3.68

IRPC pay at 48-63% payout ratio with average dividend yield of 3.3%

Dividend Payout

Unit: THB

Div. Policy ≥ 25%

Note: 1 Closing price at the end of period

N.A.N.A.N.A. N.A.

34

CAPEX Plan in 2020 – 2024(Business Plan)

264 194

88

3,675

14,428

11,315

2,965 1,570

2,164

3,797

1,392

1,632 1,255

225

-

-

-3,785

2,839

2,365

6,962

9,097

20,590

12,707

4,597

2020 2021 2022 2023 2024

E4E, IRPC 4.0

MARS project

General & Maintenance Project

Others

UCF Project

Unit: MB

10,555 ,

19%

458 , 1%

32,472 ,

60%

8,989 ,

17%

1,480 , 3%

IRPC 5 year CAPEX Plan

General & Maintenance Project

E4E, IRPC 4.0

Others

Total *

53,953 MB

UCF Project

MARS Project

* Excluding study projects for investment opportunities of 14,108 MB

Remark: Data as of Dec, 2019

ST Loan21%

LT Loan (USD)10%LT Loan (THB)

59%

Bond (THB)10%

Leasing0.4%

5,694 6,443 6,942 6,765 12,652 1,957 - 1,305 1,305

1,957

-6,889

- -

-

7,652

13,332

8,247 8,070

14,609

2020 2021 2022 2023 >2023

THB Bond

USD Loan

THB Loan

35

Financial PositionSecuring liquidity in response to COVID-19

121,991 121,362

12,212 14,523

40,611 32,681

3,036 12,273

83,402 73,008

4,860 5,217

52,071 51,910

37,517 50,705

Maturity of Long-term Borrowing

Debt ProfileStatements of Financial Position

Cash Flow

Unit : MB

Remark: Long-term debt as at 31 March 2020

Unit: MB

PP&E(incl.

investment properties and ROU)

Other Non-CA

CashOther CurrentLiabilities

LT Borrowing incl. current port.

Shareholders’Equity

Mar. 2020Dec. 2019

Other CA

Other Non-CurrentLiabilities

Beginning Cash

1 Jan 2020

Ending Cash31 Mar 2020

Cash Flow from

Operating

Unit: MB

Cash Flow from

Investing

Cash Flow from

Financing

Net Debt = 53,589 MB

Ex. Rate = 32.83 Baht/$

Financial Ratios

< 1.0x

Net D/E CA/CL

177,850 180,839Interest Rate Currency

Float 80% THB 90%

Fixed 20% USD 10%

2%

(31)(46)

13

(40)

98

27

2017 2018 2019 1Q19 4Q19 1Q20

36

Petroleum Spread

602 518 490 482 553 536

2017 2018 2019 1Q19 4Q19 1Q20

498 447 321 330 384 370

2017 2018 2019 1Q19 4Q19 1Q20

(2.3) (2.6) (4.9)

0.6

(18.7)(7.4)

2017 2018 2019 1Q19 4Q19 1Q20

12.5 14.6 13.7 12.8 14.3 11.0

2017 2018 2019 1Q19 4Q19 1Q20

14.9 10.5 9.0

3.7

12.9

6.7

2017 2018 2019 1Q19 4Q19 1Q20

500SN – FO 180 3.5%S Spread

150 BS – FO 180 3.5%S Spread

Asphalt – FO 180 3.5%S Spread

$/BBL

$/BBL

$/BBL

Lube Base SpreadRefinery Spread

Gas oil - Dubai

ULG 95 - Dubai

HSFO - Dubai

0.7

(2.4)(6.6) (7.5)

(2.2) (2.9)

2017 2018 2019 1Q19 4Q19 1Q20

Naphtha - Dubai$/BBL

$/TON

$/TON

$/TON

YoY 28%

YoY 5%

YoY 128%

YoY 88%

YoY 6%

YoY 14% QoQ 48%

QoQ 23%

QoQ 60%

QoQ 4%

QoQ 3%

QoQ 72%

YoY – N/A QoQ 48%

52.4 60.8 58.0

14.2 14.0 13.4

6.4 7.0

6.9

1.8 1.7 1.7

58.8 67.8 64.9

16.0 15.7 15.2

2017 2018 2019 1Q19 4Q19 1Q20

Lube Base

Refinery

1Q20 Market GRM was $0.8/bbl: QoQ & YoY: declined as a decrease in products spread & higher crude

premium

37

Petroleum Business2019: Dropping products spread led to lower GRM1Q20: Falling Gasoline & Diesel spreads plus high crude premium led to negative refinery margin

Refinery ProductionCrude Intake

Unit : Mbbl

3.1 3.5 1.1 0.8

0.1 (0.9)

2.1 1.7

1.3 1.1 1.6 1.7

5.2 5.2

2.5 1.9 1.7 0.8

2017 2018 2019 1Q19 4Q19 1Q20

Lube Base

Refinery

Crude intake (Mbbl)

Market GRMSales Volume & Revenue

Unit : $/bbl

Sales Volume

Revenue

65.576.1 72.0

67% 66% 69% 66% 68% 72%

33% 34% 31% 34% 32% 28%

2017 2018 2019 1Q19 4Q19 1Q20

Sweet Crude

Sour Crude

180 208 197

119,015 163,724 136,670

33,336 32,193 26,384

16,110

19,229 16,781

4,437 3,823 3,860

135,125

182,953 153,451

37,773 36,016 30,244

2017 2018 2019 1Q19 4Q19 1Q20

Lube Base

Refinery

200 190 188 Crude Run (KBD)

84% 97% 92%

2019 MKT GRM was $2.5/bbl: $2.8/bbl decrease as lower petroleum spread, especially Diesel and Gasoline

2.1 3.2 3.5 2.0 5.1 5.3Premium over Dubai ($/bbl)

YoY 5%

65% 63% 68% 64% 68% 71%

18% 15% 17% 22% 16% 16%7% 8% 6% 6% 6% 5%10% 14% 9% 8% 10% 8% Others

Domestic

Far East

Middle East

93% 89% 87% % Utilization

YoY 4%

YoY 20%(price 15%, volume 5%)

YoY 4%

YoY 16% (price 12%, volume 4%)

Unit : Mbbl

Unit : MB

84% 97% 92% 93% 89% 87% % Utilization

76% 85% 82% 84% 84% 79% Lube Base

80% 99% 102% 70% 112% 93% RDCC

YoY 6%

QoQ 2%

YoY 5%

QoQ 4%

YoY 4%

QoQ 3%

18.0 17.5 17.1

QoQ 16%(price 12%, volume 4%)

YoY 56%

QoQ 52% YoY 52%

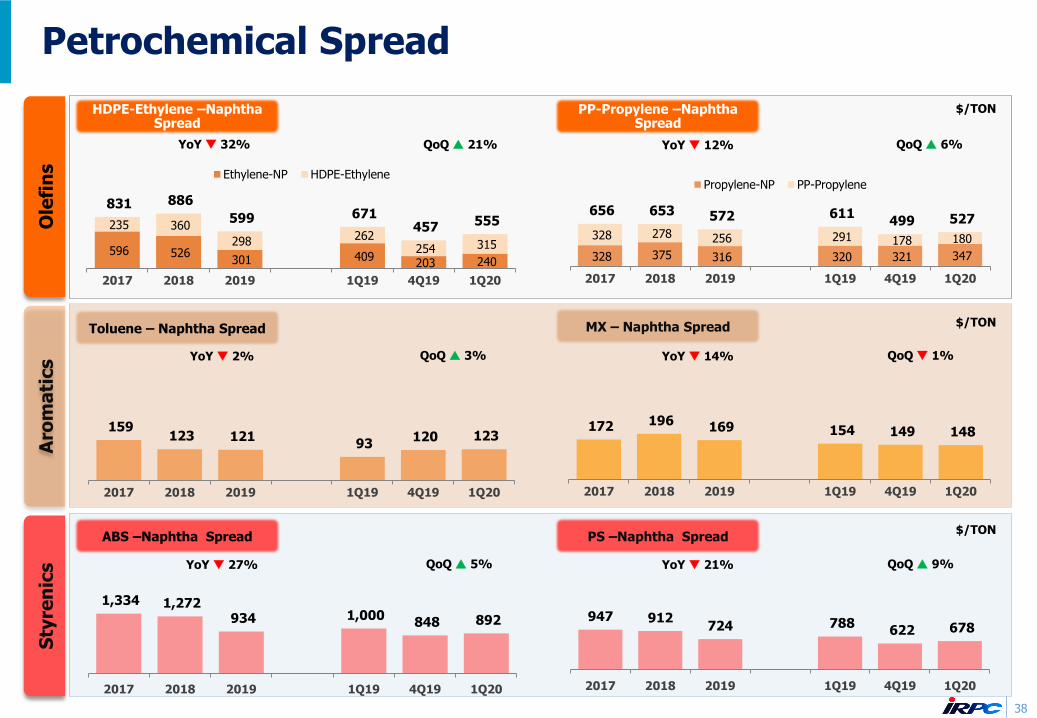

Petrochemical Spread

1,334 1,272 934 1,000

848 892

2017 2018 2019 1Q19 4Q19 1Q20

159 123 121

93 120 123

2017 2018 2019 1Q19 4Q19 1Q20

596 526 301 409

203 240

235 360

298 262 254 315

831 886

599 671 457 555

2017 2018 2019 1Q19 4Q19 1Q20

Ethylene-NP HDPE-Ethylene

172 196 169 154 149 148

2017 2018 2019 1Q19 4Q19 1Q20

947 912724 788

622 678

2017 2018 2019 1Q19 4Q19 1Q20

328 375 316 320 321 347

328 278 256 291 178 180

656 653 572 611 499 527

2017 2018 2019 1Q19 4Q19 1Q20

Propylene-NP PP-Propylene

HDPE-Ethylene –Naphtha Spread

PP-Propylene –Naphtha Spread

MX – Naphtha SpreadToluene – Naphtha Spread

PS –Naphtha SpreadABS –Naphtha Spread

Ole

fin

sS

tyre

nic

sA

rom

ati

cs

38

YoY 32%

YoY 2%

YoY 27%

$/TON

YoY 12%

YoY 14%

YoY 21%

$/TON

$/TON

QoQ 21% QoQ 6%

QoQ 3%

QoQ 9% QoQ 5%

QoQ 1%

3.0 2.6 1.5 1.5 1.3 1.2

5.2 4.7 3.5 4.2

2.5 3.4

8.3 7.3

5.1 5.7

3.8 4.7

2017 2018 2019 1Q19 4Q19 1Q20

Olefins &Polyolefins

Aromatics &Styrenics

24,684 28,760 21,985 5,642 5,150 4,407

35,044 43,980

37,671

9,987 8,277 8,090

59,728

72,740

59,656

15,629 13,427 12,497

2017 2018 2019 1Q19 4Q19 1Q20

Olefins &Polyolefins

Aromatics &Styrenics

39

Petrochemical Group2019 : According to Trade War, products spread dropped caused the decrease PTF1Q20 : Sharp fall in Naphtha price support Petrochemical product spread

Production

Market PTF

Sales Volume and Revenue

631 728 702 181 168 155

952 1,107 1,117

282 266 274

1,583 1,835 1,819

463 434 429

2017 2018 2019 1Q19 4Q19 1Q20

Olefins &Polyolefins

Aromatics &Styrenics

Revenue

YoY 1%

Unit : KMT

Crude intake (Mbbl)

Unit : $/bbl

350 400 395 107 91 92

12 28 9

8

313 338 300

50 88 81

317 295

246

68 53 60

600

807 828

186 199 209

1,591 1,868 1,777

411 431 450

2017 2018 2019 1Q19 4Q19 1Q20

Polyolefins

Olefins

Polystyrenics

Styrenics

Aromatics

Unit : KMT Sales Volume

Unit : MB

YoY 5%

YoY 18%

QoQ 24% YoY 30%

YoY 20%(price 13%, volume 7%)

QoQ 7%(price 6%, volume 1%)

YoY 18%(price 17%, volume 1%)

87% 94% 95% 89% 90% 95% % Utilization

91% 90% 92% 83% 88% 92% Polyolefins

83% 100% 98% 97% 92% 99% Olefins

90% 101% 93% 82% 96% 94% % Utilization

88% 93% 83% 69% 95% 88% Polystyrenics

100% 110% 94% 57% 104% 105% Styrenics

88% 103% 101% 107% 92% 93% Aromatics

YoY 9%

QoQ 4%

QoQ 1%

YoY 7%

65.576.1 72.0

18.0 17.5 17.1

1Q20 : Petrochemical revenue was Bt 12 bn

QoQ : 7% decrease from 6% price decrease & 1% vol. decrease

YoY : 20% decrease from 13% price decrease & 7% vol. decrease

1Q20 Market PTF was $4.7/bbl:

QoQ : $0.9/bbl increase as higher products spread

YoY : $1.0/bbl decrease as lower products spread

2019 : Petrochemical revenue was Bt 60 bn

YoY : 18% decrease from 17% price decrease & 1% vol. decrease

2019 Market PTF was $5.1/bbl:

YoY : $2.3/bbl decrease as lower products spread through trade war tension

1,629 1,947 2,071

534 531 505

916

1,034 1,153

277 303 308

196

245

246

61 60 63

2,741

3,226 3,470

872 894 876

2017 2018 2019 1Q19 4Q19 1Q20

Other

Steam

Electricity

40

Power & Utility 2019: U-Rate of power & utility declined owing to the planned shutdown of RDCC plant1Q20 : Increasing margin due to higher steam u-rate

Utilization Rate

GIM

Revenue

1.01 1.08

1.19 1.10

1.24 1.32

2017 2018 2019 1Q19 4Q19 1Q20

Power &Utility

Unit : $/bbl

Unit : MB

75% 79% 71% 67% 71% 71%

2017 2018 2019 1Q19 4Q19 1Q20

Electricity

73% 79%60% 59% 60% 66%

2017 2018 2019 1Q19 4Q19 1Q20

Steam

YoY 10%

YoY 19%

YoY 8%

YoY 20%

QoQ 6%

QoQ 2%

YoY 0.5%

YoY 8%

2019 U-Rate of Steam was 60%; 19%

2019 U-Rate of Electricity was 71%; 8%

YoY : decrease due to the planned shutdown of RDCC plant

2019 : Power & Utility revenue was 3,470 MB

YoY : 8% increase from higher electricity sales vol. & avg. selling prices of steam

YoY 7%

QoQ 6%

YoY 4%

QoQ - Unchanged

1Q20 U-Rate of Steam was 66%; 6% QoQ, 7% YoY

QoQ & YoY : increase after industrial area customers return to normal operations

1Q20 U-Rate of Electricity was 71%; Unchanged QoQ, 4% YoY

QoQ & YoY : increase owing to planned shutdown of RDCC plant in 1Q19

1Q20 : Power & Utility revenue was 876 MB

QoQ : 2% decrease from lower electricity sales vol. to EGAT VS higher steam vol. to IRPC industrial area customers

YoY : 0.5% increase from higher steam sales vol. VS lower electricity sales vol.

Accounting GIM

2019 Acct GIM was $9.0/bbl,

YoY: $4.1/bbl due to $0.3/bbl net stock gain compared to net stock loss of $0.5/bbl in 2018 & $4.9/bbl lower market GIM

1Q20 Acct GIM was $-5.8/bbl,

QoQ: $14.0/bbl due to $12.7/bbl net stock loss compared to $1.4/bbl net stock gain in 4Q19

YoY: $15.8/bbl due to $12.7/bbl net stock loss compared to net stock gain of

$1.3/bbl in 1Q19 and $1.9/bbl lower market GIM

3.0 2.6 1.5 1.5 1.3 1.2

5.2 4.7 3.5 4.2 2.5 3.4

8.3 7.3 5.1 5.7

3.8 4.7

Aromatics&Styrenics Olefins

14.5 13.6 8.7 8.7 6.8 6.8

1.7

(0.5) (0.03)

1.3 0.7

(13.3)(0.7)

0.01 0.3 0.7 0.6

15.5 13.1 9.0

9.9 8.1

(5.8)

Market GIM Stk G/(L) & LCM Hedging

5.2 5.2 2.5 1.9 1.7 0.8

8.3 7.3 5.1 5.7 3.8 4.7

1.0 1.1

1.2 1.1 1.2 1.3

14.5 13.6

8.7 8.7 6.76 6.82

Petroleum Petrochem Power & Utility

3.1 3.5 1.1

0.8 0.1 (0.9)

2.1 1.7

1.3 1.1 1.6 1.7

5.2 5.2

2.5 1.9 1.7 0.8

2017 2018 2019 1Q19 4Q19 1Q20

Refinery Lube Base

11,663 12,858 5,504 1,084 931 449

18,443 18,085

11,379 3,247 2,014 2,503

2,264 2,663

2,672

627 660 713

32,370 33,607

19,555

4,958 3,605 3,665

2017 2018 2019 1Q19 4Q19 1Q20

32,370 33,607 19,555

4,958 3,605 3,665

3,720

(1,268) (62)

719 363

(7,134)(1,452)

30

676 1 373

323

34,638 32,370

20,169

5,678 4,341

(3,146)2017 2018 2019 1Q19 4Q19 1Q20

Market GIM

Unit: $/bbl

Accounting GIM

Unit: $/bbl

Unit: MB

Market GIM by business

Unit: $/bblPetrochemical

Petroleum

Unit: MB

41

Gross Integrated Margin (GIM)2019: The market downturn towards global threaten had led to the decline in MKT GIM1Q20 : The COVID-19 outbreak affected to stock loss

YoY 36%

YoY 32%

YoY 42%

YoY 38%

YoY 22%

QoQ 1%

YoY 26%

QoQ 2%

Market GIM

2019 Market GIM was $8.7/bbl,

YoY: $4.9/bbl due to lower products spread

1Q20 Market GIM was $ 6.8/bbl,

QoQ: $0.1/bbl from higher petrochemical spreads versus lower petroleum spreads

YoY: $1.9/bbl due to lower spread & higher crude premium

YoY 159%

QoQ 172%

YoY 155%

QoQ 172%

42

Important Events in History

2009 2011 2013 2015 2016

HISTORY

KEY MILESTONES OF THE DECADE

• Increased refinery capacity from 65 kbd to 215 kbd

• Entered Rehabilitation Plan

Successful Rehabilitation new major shareholders:

Founded by “Leophairatana” Family as TPI

IPO Restructuring Plan was approved

Exited from Rehabilitation

plan and Registered as

IRPC Plc.

Operated first LDPE plant in

SEA

Debt Moratorium

MOF was appointed as plan

administrator

1978 1982 1995 1997 2000 2003 2004 2005 2006

Efficiency improvement#1 under “DELTA” Project

Capacity Increase: ABS/SAN to 179 KTA

Efficiency improvement#2 :

Launched “EVEREST” project

Business Improvement under Phoenix

Project

Commenced operation of

Combined Heat and Power Project

(CHP I)

• Commenced UHV project in July 2016

• PTT 31.5%• Gov’t (Vayupak) Fund

10%• Gov’t Saving Bank 10%• Gov’t Pension Fund

Group 10%

UHV: Upstream Project for Hygiene and Value Add Products

2017

• Commenced PPE project in Sept. 2017

• Commenced PPC project in Dec. 2017

2018

• Launched “GDP” project : Growth, Digital, People

Plant

2020

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Total

Pe

tro

leu

m

ADU1 0

ADU2 0

Hyvahl 31 31

RDCC 0

LUBE 0

Pe

tro

ch

em

ica

l

EBSM 0

HDPE 6 6 12

PP 20 20

ABS/SAN 23 23

PS 13 13

43

Maintenance Shutdown Plan 2020

This presentation material has been prepared solely for informational purposes only. IRPC is furnishing it solely for use by prospective investors / analysts in the

proposed event. IRPC makes no representations or warranties as to the accuracy or completeness of such information. By accepting this material each recipient

agrees that IRPC shall not have any liability for any representations (express or implied) contained in, or for any omissions from this presentation.

The information contained herein does not purport to be all-inclusive or to contain all of the Information that may be material to the recipient’s decision. Each recipient

of the information and data contained herein should perform its own independent investigation and analysis of the transaction and the creditworthiness of IRPC . Reference in this Disclaimer to this shall include references to the Appendices (if any) hereto.

Investor Relations Contact: [email protected]

Tel. +662-765-7380, Fax. +662-765-7379

Thank You

Disclaimers