IOC™: Introduction to Securities & Investment · Dear Delegate The syllabus for the Introduction...

31

4 Chiswell Street London EC1Y 4UP Tel: 0845 072 7620 Fax: 020 7496 8607 Email: [email protected] www.7city.com IOC™: Introduction to Securities & Investment Update Supplement This supplement should be used if your examination is on or after 21/07/2012 and your manual is edition 27 or if you are studying for The Foundation Qualification and your manual is edition 4.

Transcript of IOC™: Introduction to Securities & Investment · Dear Delegate The syllabus for the Introduction...

4 Chiswell Street London EC1Y 4UP Tel: 0845 072 7620 Fax: 020 7496 8607 Email: [email protected] www.7city.com

IOC™: Introduction to Securities & Investment Update Supplement This supplement should be used if your examination is on or after 21/07/2012 and your manual is edition 27 or if you are studying for The Foundation Qualification and your manual is edition 4.

Copyright 7city Learning Limited 2012

All rights reserved. No part of this publication may be reproduced, stored in or introduced into a retrieval system, or transmitted, in any form, or by any means (electronic, mechanical, photocopying, recording or otherwise) without the prior permission of the copyright owner. Any person who does any

unauthorised act in relation to this publication may be liable to criminal prosecution and civil claims for damages.

While every effort has been made to ensure its accuracy, no responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication can be accepted by 7city Learning Limited.

Edition 5 (01/04/2004) Edition 5 (1/4/04) Edition 28 (21/07/2012)

Dear Delegate The syllabus for the Introduction to Securities & Investment paper is being updated for exams on or after 21/07/2012. A summary of the changes follows this page. Where new content has been added or amended, updated pages follow the summary. These changes are also reflected in 7C-online where content and questions are constantly updated from the database. Overall, you will see that few additions to the syllabus have been made, with the majority of the amendments serving to tighten up the existing content and better define examinable areas. If you have any concerns about this update, feel free to call the number below and speak to myself or another 7city tutor. Kind regards and good luck with your study. Brendan McLaughlin Head of IOC 4 Chiswell Street London EC1Y 4UP Tel: 0845 072 7620 Fax: 020 7496 8607

SUMMARY OF SYLLABUS CHANGES CHAPTER 2 – THE REGULATORY ENVIRONMENT

Subject 6 – A proposed future role for the Bank of England New subject (subsequent subject numbering updated)

Subject 7 – Complaints and redress The Financial Ombudsman Service (FOS)

Topic updated

CHAPTER 3 – FINANCIAL CRIME Subject 4 – Money laundering (Proceeds of Crime Act 2002)

The Bribery Act 2010 – New topic

CHAPTER 5 – EQUITIES: TYPES AND FEATURES Subject 6 – Title documents

Registered securities Topic updated

CHAPTER 7 – EQUITY MARKETS

Subject 6 – LSE’s central counterpart service (CCP) New subject (subsequent subject numbering updated)

CHAPTER 8 – CREST

Subject 6 – CREST settlement process CREST: transaction reports

Topic updated CHAPTER 9 – DEBT: TYPES AND FEATURES

Subject 3 – Government bonds: features Categories of gilt

Topic updated Subject 4 – Corporate bonds: features

Covered bonds New topic

CHAPTER 11 – ALTERNATIVE INVESTMENTS: DERIVATIVES, FOREIGN EXCHANGE AND PROPERTY

Subject 5 – Foreign exchange Factors affecting foreign exchange rates

New topic

CHAPTER 12 – RETAIL PRODUCTS Subject 2 – Retail products: reasons for investment

Fund management Topic updated

Subject 6 – UCITS Directives 1 & 3 Money market funds

New topic Subject 12 – Life assurance

Protection planning New topic

Subject 13 – Life assurance Pensions

New topic

CHAPTER 13 – TAX Subject 2 – Income tax

Unearned Income (Investment income) Topic updated

Subject 7 – Tax efficient investments Individual Savings Accounts (ISAs)

Topic updated Junior ISAs (JISAs)

New topic

CHAPTER 15 – ECONOMICS Subject 3 – The role of the continuous-linked settlement (CLS) and central banks

New subject (subsequent subject numbering updated)

2CHAPTERThe regulatory environment

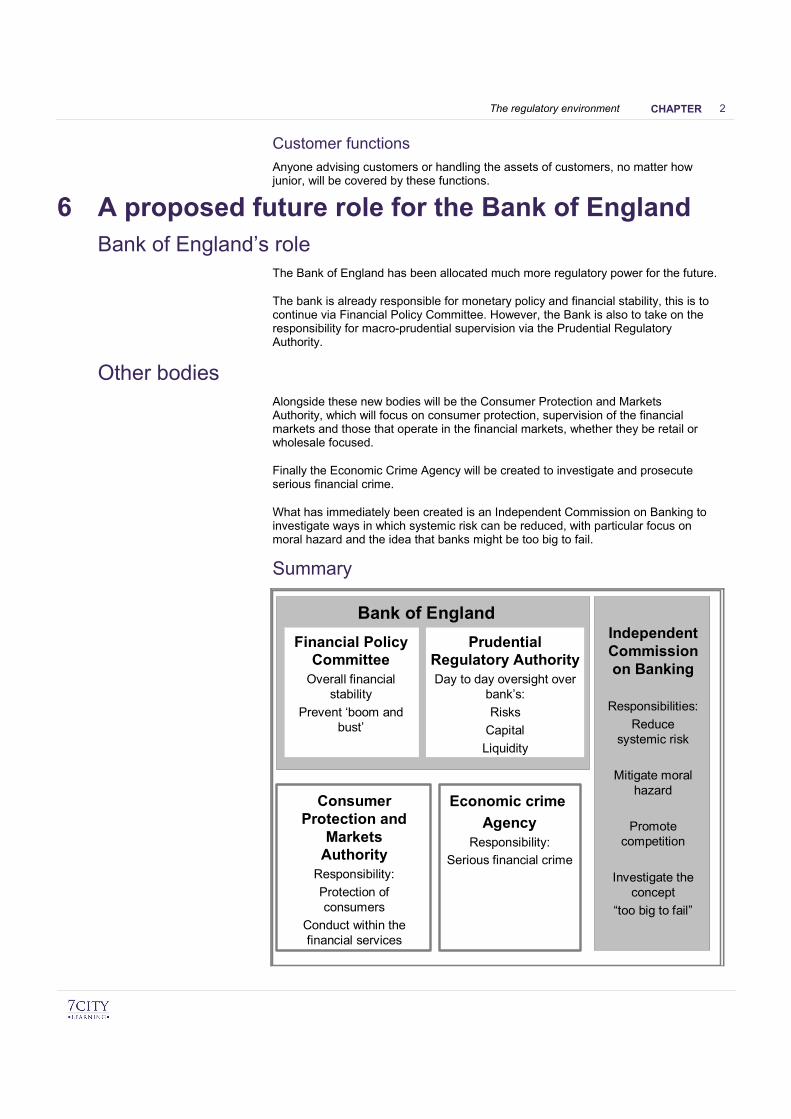

Customer functionsAnyone advising customers or handling the assets of customers, no matter how junior, will be covered by these functions.

6 A proposed future role for the Bank of EnglandBank of England’s role

The Bank of England has been allocated much more regulatory power for the future.

The bank is already responsible for monetary policy and financial stability, this is tocontinue via Financial Policy Committee. However, the Bank is also to take on theresponsibility for macro-prudential supervision via the Prudential RegulatoryAuthority.

Other bodiesAlongside these new bodies will be the Consumer Protection and MarketsAuthority, which will focus on consumer protection, supervision of the financialmarkets and those that operate in the financial markets, whether they be retail orwholesale focused.

Finally the Economic Crime Agency will be created to investigate and prosecuteserious financial crime.

What has immediately been created is an Independent Commission on Banking toinvestigate ways in which systemic risk can be reduced, with particular focus onmoral hazard and the idea that banks might be too big to fail.

Summary

Bank of England

Financial Policy Committee

Overall financial stability

Prevent ‘boom and bust’

Prudential Regulatory AuthorityDay to day oversight over

bank’s:

Risks

Capital

Liquidity

Economic crime

AgencyResponsibility:

Serious financial crime

Consumer Protection and

Markets Authority

Responsibility:

Protection of consumers

Conduct within the financial services

IndependentCommissionon Banking

Responsibilities:

Reduce systemic risk

Mitigate moral hazard

Promote competition

Investigate the concept

“too big to fail”

2CHAPTERThe regulatory environment

The Financial Ombudsman Service (FOS)IntroductionThe FSA has established a system for the consideration of complaints against its firm by customers who feel aggrieved and entitled to seek redress.

The system involves consideration of the complaint by the firm itself and, if the customer is not satisfied, independent investigation of the complaint.

Investigation involves both a mediation stage and a possible subsequent determination stage by the Financial Ombudsman.

The FOS can make awards for a range of reasons including financial loss, pain and suffering, damage to reputation and distress or inconvenience.

Complaints against authorised firms relating to regulated activities fall under the 'Compulsory Jurisdiction' of the FOS.

Unauthorised firms can also submit to the 'Voluntary Jurisdiction' of the FOS by entering into a contract with the FOS as a voluntary participant. This might cover activities such as general insurance, deposit taking and credit/debit card transactions.

Eligible complainantsThe definition of an eligible complainant is the same as that for the application of complaints procedures. Thus, the service is generally available to RETAIL CLIENTS.

Dismissal of complaintsA complaint can be dismissed by the Ombudsman if it considers that:

The complainant has not suffered financial loss, material inconvenience or material distress.

The complaint is frivolous or vexatious.

The firm has already offered reasonable compensation.

InvestigationWhen the Ombudsman investigates a complaint the firm must co-operate with the Ombudsman.

When there is a reasonable possibility of resolution by mediation, the Ombudsman will endeavour to achieve settlement by this route. If mediation is not an option, the Ombudsman will investigate the complaint.

During an investigation, both parties can make representations.

After a provisional assessment is made, if one of the parties objects to the provisional assessment, the Ombudsman will present a written statement of determination.

Only if the complainant accepts the determination is it binding on the firm.

If the complainant rejects the Ombudsman's decision, they can pursue the matter further through the courts.

2CHAPTERThe regulatory environment

CompensationThe Ombudsman can make financial awards to complainants. The MAXIMUM AWARD is £150,000 and reasonable costs (although awards of costs are not common).

If the Ombudsman feels that an amount in excess of the maximum is appropriate it can invite the firm to pay the balance.

The Financial Services Compensation Scheme (FSCS)IntroductionThe Financial Services Compensation Scheme was established to provide compensation where authorised persons and appointed representatives are unable to satisfy claims against them.

Key elements of a claimTo succeed, an ELIGIBLE CLAIMANT must have a PROTECTED CLAIM against a RELEVANT PERSON, and make that claim within the RELEVANT TIME LIMITS.

Note that a claim can only be made once a firm is in liquidation. If the firm still exists the customer must explore all other avenues of redress.

Eligible claimants

The following are eligible claimants:

Private individuals (including experts) - can claim in respect of all losses. Note this does not cover customers connected to the firm (e.g. directors).

A partnership, body corporate, unincorporated association or mutual association with an annual turnover of less than £1 million.

Protected claim

Protected claims are claims made in respect of:

Designated investment business.

Deposits.

Insurance.

The activity subject to a claim must be carried on in the UK or in an EEA state by a firm passporting their services there.

Relevant person

The following are relevant persons:

An authorised firm.

An appointed representative of the above.

(An EEA firm passported into the UK is NOT a relevant person. Customers losing money from the activities of such a firm would have to seek compensation through the firm's home state regulator).

Relevant time limits

Six years from when the claim arose.

3CHAPTERFinancial crime

The penalty for failing to make a report is the same as the penalty for failing to disclose a suspicion of money laundering (i.e. a maximum of a five-year jail sentence and an unlimited fine).

Seizure and forfeiture powers under the Terrorism ActUnder the Terrorism Act, suspected terrorist property may be seized by authorities. Extended detention and forfeiture of such property is possible only by court application. Forfeited terrorist property becomes a part of the Consolidated Fund of HM Treasury.

The Bribery Act 2010The act consolidates and expands upon existing legislation covering bribery at home and overseas. The act applies where individuals are expected to act in good faith, impartially and not abuse their position of trust. The act covers public and corporate officials. The main provisions of the Bribery Act 2010 state that it is an offence to:

Offer, promise or give advantage. This is active bribery.

Request, agree to accept or accept advantage. This is passive bribery.

The Ministry of Justice has produced guidance notes on the act. It emphasises that firms should take a risk-based approach to potential bribery; that firms must have procedures, including training of staff, in place; and that they must monitor and review these on an ongoing basis.

Failure to comply with the act, including failure to prevent bribery, can lead to a ten-year prison sentence.

5 Data protectionData protection: introduction

The basic principle of data protection is that the public should know or should be able to find out who is carrying out processing of personal data and for what purposes the processing is carried out.

To satisfy this principle, the Data Protection Act 1998 (DPA) places obligations on 'data controllers' (anyone who decides how and why personal data - information about identifiable, living individuals - is processed), including requiring them to register with the Information Commissioner.

The Information Commissioner is a UK independent supervisory authority reporting directly to the UK Parliament. The Commissioner has a range of duties including the promotion of good information handling and the encouragement of codes of practice for data controllers.

Where breaches of the DPA occur, the Information Commissioner can:

Enter premises and seize documentation WITHOUT a court warrant.

Issue enforcement notices requiring data controllers to take remedial action to remedy breaches.

Instigate criminal proceedings.

5CHAPTEREquities: types and features

The LSE offers an order driven trading service (call and put, cash and physically settled) for covered warrants with European and US underlying shares, aimed at institutional AND private clients.

The market affords investors the following benefits:

Gearing: the ability to make high returns without actually buying the underlying share

Limit losses: limited to the premium paid for the covered warrant

Reduced stamp duty: stamp duty is not payable on cash settled covered warrants

Wide variety of underlying products: the ability to trade a range of markets and underlying shares through one broker

Hedging: with both put and call covered warrants available, synthetic long and short positions can be created to hedge both short and long holdings of the underlying

6 Title documentsBackground

A document of title is the proof that an investor actually has legal ownership of the security.

There are different methods by which an investor can hold securities and these are considered below.

Registered securitiesA registered security is one which is registered in the owner's name.

Just as your car or house is registered in your name, so will the shares in any UK companies you own.

The company will maintain a register of shareholders which will be updated every time there is a change in ownership.

The company will issue a registered share certificate which will include information on who the registered owner is.

Corporate and government debt (i.e. debentures and gilts) are also registered instruments.

Note that, as a matter of administrative simplicity, registered holdings are often in 'nominee names' - thus an investor's shareholding will be held in the name of the nominee company of her stockbroker. Investors using nominee names benefit from lower charges - they may lose 'shareholder perks' as a result, but they will not lose their fundamental rights to voting or income.

For equities entry onto the shareholder register confers voting rights. Rights to receipt of dividends are determined by the trade date.

5CHAPTEREquities: types and features

These days, a registered security does not need to be certified. A name on the register is conclusive proof of ownership. Therefore, the certificates are either centrally held, but not altered. This is immobilised, or they are destroyed: this is dematerialised.

Bearer securitiesBearer securities are best described as anonymous, freely transferable securities.

They do not show the owners name on the certificate and no register is maintained of legal title.

The very fact you have physical possession of a bearer security is proof that you have legal title.

UK shares are not normally issued in bearer form. However, eurobonds, money market instruments and bank notes are.

Instruments which are issued in bearer form may have tear-off slips attached to them, each of which represents a dividend / interest payment.

On the due date, an investor will tear off the slip (also known as the coupon) and submit it to the paying agent before payment of the dividend / interest will be made.

Such a system is not required for registered securities, as the paying agent already knows who to send dividend / interest payments out to. The name and address of each investor is recorded in the register of members.

7 Equities types and features: summaryKey concepts

Limited companiesThe process by which a company is incorporated.

The distinction between shareholders and directors.

The distinction between issued and authorised share capital.

Types of shareholderThe types of organisation holding the majority of issued shares.

Ordinary and preference sharesThe two main types of share: ordinary and preference.

The basic rights attaching to ordinary and preference shares.

Warrants and Covered WarrantsDefinition of a warrant and a covered warrant

Function of a warrant and a covered warrant

7CHAPTEREquity markets

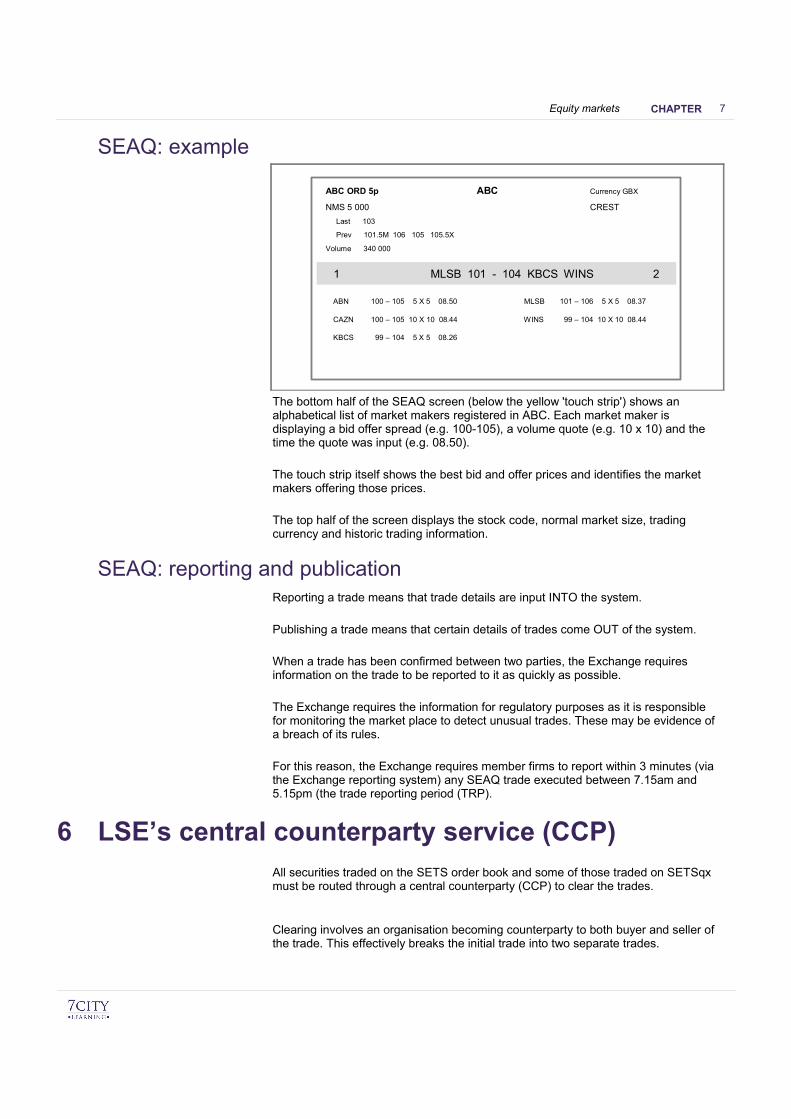

ABN 100 – 105 5 X 5 08.50 MLSB 101 – 106 5 X 5 08.37

CAZN 100 – 105 10 X 10 08.44 WINS 99 – 104 10 X 10 08.44

KBCS 99 – 104 5 X 5 08.26

1 MLSB 101 - 104 KBCS WINS 2

ABC ORD 5p ABC Currency GBX

NMS 5 000 CREST

Last 103

Prev 101.5M 106 105 105.5X

Volume 340 000

SEAQ: example

The bottom half of the SEAQ screen (below the yellow 'touch strip') shows an alphabetical list of market makers registered in ABC. Each market maker is displaying a bid offer spread (e.g. 100-105), a volume quote (e.g. 10 x 10) and the time the quote was input (e.g. 08.50).

The touch strip itself shows the best bid and offer prices and identifies the market makers offering those prices.

The top half of the screen displays the stock code, normal market size, trading currency and historic trading information.

SEAQ: reporting and publicationReporting a trade means that trade details are input INTO the system.

Publishing a trade means that certain details of trades come OUT of the system.

When a trade has been confirmed between two parties, the Exchange requires information on the trade to be reported to it as quickly as possible.

The Exchange requires the information for regulatory purposes as it is responsible for monitoring the market place to detect unusual trades. These may be evidence of a breach of its rules.

For this reason, the Exchange requires member firms to report within 3 minutes (via the Exchange reporting system) any SEAQ trade executed between 7.15am and 5.15pm (the trade reporting period (TRP).

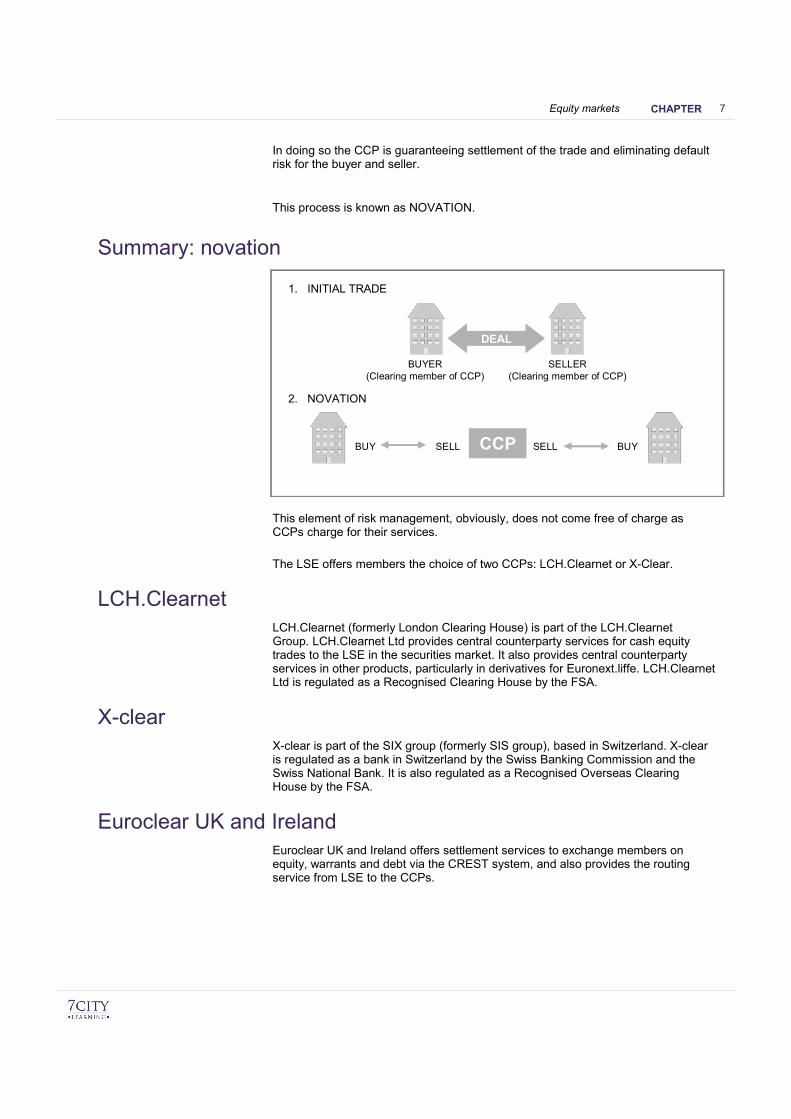

6 LSE’s central counterparty service (CCP)All securities traded on the SETS order book and some of those traded on SETSqxmust be routed through a central counterparty (CCP) to clear the trades.

Clearing involves an organisation becoming counterparty to both buyer and seller ofthe trade. This effectively breaks the initial trade into two separate trades.

7CHAPTEREquity markets

In doing so the CCP is guaranteeing settlement of the trade and eliminating defaultrisk for the buyer and seller.

This process is known as NOVATION.

Summary: novation

1. INITIAL TRADE

2. NOVATION

BUYER(Clearing member of CCP)

DEAL

SELLER(Clearing member of CCP)

SELLBUY SELL BUYCCP

This element of risk management, obviously, does not come free of charge asCCPs charge for their services.

The LSE offers members the choice of two CCPs: LCH.Clearnet or X-Clear.

LCH.ClearnetLCH.Clearnet (formerly London Clearing House) is part of the LCH.ClearnetGroup. LCH.Clearnet Ltd provides central counterparty services for cash equitytrades to the LSE in the securities market. It also provides central counterpartyservices in other products, particularly in derivatives for Euronext.liffe. LCH.ClearnetLtd is regulated as a Recognised Clearing House by the FSA.

X-clearX-clear is part of the SIX group (formerly SIS group), based in Switzerland. X-clearis regulated as a bank in Switzerland by the Swiss Banking Commission and theSwiss National Bank. It is also regulated as a Recognised Overseas ClearingHouse by the FSA.

Euroclear UK and IrelandEuroclear UK and Ireland offers settlement services to exchange members onequity, warrants and debt via the CREST system, and also provides the routingservice from LSE to the CCPs.

8CHAPTERCREST

Sponsored members - able to hold investments in their own name within CREST but need to pay an information provider for access to information.

Anyone who is able to communicate directly with CREST is called a CREST USER. Direct access with CREST is via Electronic Communication Networks (ECNs). To use the gateway users must have signed a contract with a network provider who will provide the technical capacity (SWIFT Securenet, BT Syntegra or the LSE). Members are users because of these links. A sponsored member will not be a user.

SWIFT (Society for Worldwide Interbank Financial Telecommunications) in turn allows STRAIGHT THROUGH PROCESSING to take place: direct transfer of securities resulting from a single input of instructions at the time of trade.

Straight through processing reduces the risk of settlement delays due to, for example, failure to use ISIN codes, transcription errors made by custodians when keying in customers’ instructions or delays in transmission of instructions.

3 CREST settlement processCREST: transaction reports

CREST acts as an electronic trade confirmation system (ETC) by accepting transaction reports from counterparties involved in a deal.

Both parties are required to report to CREST the details of the transaction, and the system will check that the details match. Should the details not agree, the system will not be able to match them and will not proceed to settlement. CREST will not send unsolicited information regarding the status of orders. Members therefore need to monitor their order status.

If unmatched orders are not remedied, they will automatically be deleted by CREST 30 days after input.

CREST: settlementDeadlinesCREST continually monitors all matched trades, and determines whether they are ready to be settled.

Standard settlement for LSE trades is 3 business days after the day of the transaction, i.e. T+3.

Change of ownershipBefore CREST records the change in legal title of the security, it will check that:

The seller (or deliverer) has sufficient stock recorded in their member account to satisfy the deal in full.

The buyer has sufficient available credit with a payment bank to complete the bargain. The level of available credit is recorded within the cash memorandum account (CMA).

If these checks are satisfactory, CREST will record, via book entry transfer, the change in ownership of the shares. This is done by adjusting the members' accounts in CREST.

9CHAPTERDebt: types and features

Exchequer

Funding

Conversion

Consolidated

War loan

The names 'Treasury' and 'Exchequer' indicate that at one time, these were the government departments responsible for raising the funds. 'Consolidated' stocks derive from the gathering together, or consolidation, of a number of smaller, earlier issues.

If the title of a gilt contains the word 'loan' rather than the more common 'stock', it indicates that the bond is available in bearer as well as registered form.

RedemptionThe redemption date is the specified date on which the capital is repaid by the Government. Normally, redemption is at par, i.e. £100 for each £100 nominal value held.

Categories of giltConventional gilts

Shorts - remaining life < 7 years

Mediums - remaining life 7 - 15 years

Longs - remaining life > 15 years

It is the REMAINING maturity of the gilt that is used for categorisation purposes. For instance, a 20 year bond starts off as a 'long' when initially issued, but five years later it becomes a medium, and 8 years later a short.

Undated/irredeemable giltsThere is no obligation for the government to redeem undated gilts, but they may still do so at their discretion.

Undated gilts do not usually include redemption dates, e.g. Consolidated 2 1/2%. However, a few carry the abbreviation 'Aft' (e.g. 3% Treasury 1966 Aft). This implies the Government has the right to redeem the gilt in 1966 or at any time after.

Other non-conventional gilts

Double-dated giltsDouble-dated gilts are described with two dates, e.g. Treasury 11 3/4% 2017-2021.The Government has the option of redeeming AFTER the first date, but no laterthan the last date.

Double-dated gilts are categorised by using the latter date: e.g. Exchequer 12%2017-2025 is categorised as a long-dated gilt.

9CHAPTERDebt: types and features

Convertible giltsConvertibles grant the owner the right to convert the gilt into predefined amounts ofa DIFFERENT gilt at some time in the future.

Convertibles are usually short- to medium-term bonds which may be converted intoa longer issue at the discretion of the INVESTOR.

In the 'Financial Times', they are identifiable by the abbreviation 'Conv' in the title:e.g. Conv 9% 2019.

Floating rate gilts

Floating rate gilts are unusual in that they pay variable coupons. The coupon is setby reference to the London Inter-bank Bid Rate (LIBID) at the beginning of eachinterest payment period. (LIBOR - x% may also be used as a reference rate.)

They are also unusual in that they pay interest four times a year instead of semiannually.

They tend to trade at around their par (nominal) value.

The DMO does not currently issue floating rate gilts.

The strips marketSTRIPS stands for Separate Trading of Registered Interest and Principal of Securities.

For example, a five year gilt is strippable into ten semi-annual coupons and a final capital payment. If the cash flows are separated out, this equates to eleven individual zero coupon securities, with maturities of 6, 12, 18 months and so on to maturity.

4 Corporate bonds: featuresCorporate bonds: background

All companies raise equity finance from their shareholders.

However, a large part of the total capital raised by companies is in the form of debt.

Companies issue securities such as debentures and unsecured loan stock to investors. These instruments are debt securities, and the company is committed to repaying the capital as well as any associated interest to the holders of these instruments.

DebenturesA debenture is a document which acknowledges a company's indebtedness to a third party.

The London Stock Exchange limit the use of the term 'debenture' to refer to SECURED debt instruments.

The meaning of security in this context is that debenture holders have the right to sell assets owned by the company if the company does not pay out on the coupon or principal amount. Debenture holders are therefore relatively secure. Security can be given over specific assets, known as a FIXED charge, or over a class of assets, known as a FLOATING charge.

9CHAPTERDebt: types and features

Asset Backed SecuritiesAn asset-backed security (ABS) is a financial instrument secured by a pool of assets such as property, loans or credit card receivables.

They are often issued by companies specially created for the purpose (special purpose vehicles or SPVs). This enables them to be a separate legal entity from the original owner of the underlying assets leaving them unaffected by any bankruptcy issue.

These instruments are often called 'passthrough securities' as the cash flows from the pool of underlying assets, e.g. rental income on property or interest on loans, are distributed and a pro-rata basis to the holders of the ABS. In other words, the cash flows from the underlying assets have been SECURITISED.

The most common types of ABS are collateralised bond obligations (CBOs), collateralised debt obligations (CDOs), mortgage backed securities (MBSs) and collateralised loan obligations (CLOs)

Covered bondsA variation on an asset-backed security is a covered bond. These are typically issued in Europe by the public and mortgage sector. The regulation of covered bonds is more stringent than that of an ABS. They give more protection than an ABS, as:

They remain on the issuer's balance sheet, as oppose to being sold on to a special purpose vehicle

They ensure that the holders have a priority claim on the asset pool if the issuer defaults

5 Domestic and overseas bonds: featuresDomestic bonds

A domestic bond refers to one in which the nationality of the issuer, the denomination of the bond and the country of issue are the same. For example, a sterling denominated bond issued in London by a UK company.

Foreign bondsA foreign bond is one in which the nationality of the issuer is different to that of the denomination of the bond and the country of issue. For example, a sterling bond issued in London by a US company.

Foreign bonds are known as BULLDOGS in the UK, YANKEES in the US, MATADORS in Spain and SAMURAI in Japan.

International bonds (also called eurobonds)An international bond (EUROBOND) is a security where the denomination of the bond and the country of issue are all different. For example, a company issuing dollar bonds in Paris and Tokyo, or a company issuing Yen bonds in Frankfurt and Dublin.

11CHAPTERAlternative investments: derivatives, foreign exchange and property

As different countries have different public holidays, a good day in one currency is not necessarily a good day for another.

Factors affecting foreign exchange ratesPurchasing Power Parity – If you have an iPad that can be bought cheaper in theUS, a UK resident will sell their sterling and buy dollars. This will weaken thecurrency. Therefore if one economy has an inflation rate (the price of money)greater than its competitors then its currency will deteriorate against its tradingpartners.

Supply and DemandWith regards to supply and demand for a currency there is an inverse relationshipdue to price:

Demand

- Foreigners need currency for exports to overseas markets

- Foreigners want to invest capital into the UK

- Speculation – currency expected to increase relative to another

- Currency rate management by the central bank

Supply

- Imports will increase supply as they pay for imported goods

- UK residents want to invest capital into overseas assets will have to sell sterlingto buy foreign currency

- Speculation – currency expected to decrease relative to another

- Currency rate management by the central bank

6 Property marketFeatures of the property market

The property market has certain characteristics that differ from other financial markets.

Specifically, these are:

It is heterogeneous: the property market is very segmented and is comprised of a number of different sub-sectors, e.g. residential, commercial and agricultural. This is unlike the market in shares or bonds where the investment vehicle is relatively standardised compared to property/real estate.

It is indivisible: property is difficult to split-up into smaller 'bundles', potentially excluding smaller investors from participation.

Transaction costs are higher than for other investments: for example, lawyers, estate agents and land registry charges.

It is decentralised: there is no central market place for property which makes is difficult for investors to compare investment opportunities in different parts of the country or across borders.

It requires maintenance: the costs associated with repairs and maintenance can be a significant factor in the overall cost of a property investment.

12CHAPTERRetail products

PensionsKnow the basic characteristics of state, occupational, stakeholder and personal pensions.

Know the characteristics of self-invested personal pensions and small self-administered schemes.

2 Retail products: reasons for investmentRisk and return

The risk borne by an investor is a measure of the uncertainty of future cash flows arising from the investment.

The return from the investment is the income and capital growth enjoyed by the investor.

The greater the risk, the greater the potential return that may arise. For example, hi-tech stocks are high risk but may generate a very healthy return.

Risk also increases with time, and so the prices of long-dated gilts are more volatile than those which are short-dated.

DiversificationRisk is reduced by diversifying into different companies, business sectors, and types of security and market. These are known as NEGATIVELY CORRELATED stocks as they will often respond differently to changing economic circumstances.

For example, you would not diversify a holding of Corus shares (a steel company) by buying shares in Thyssen Krupp (another steel company). You may buy shares in BT, a company unaffected by the steel sector.

It is never possible to diversify away all risk. Any portfolio will always be exposed to risks the whole world faces (such as global recession). These global risks are known as market risk (or systematic risk or business risk). Only UNSYSTEMATIC (or idiosyncratic) risk may be diversified.

Some investors diversify further by taking funds offshore, but this may increase risk because of differing exchange rates, regulatory environments and settlement systems.

Fund managementFund managers can assist with diversification by managing a fund that takes collective investments from many people and invests in a range of assets. Funds can be established in different legal forms, including unit trusts, Investment Companies with Variable Capital (ICVCs), and Investment Trusts.

Some funds are designed to follow a particular market or index. These are known as TRACKER funds. Charges tend to be low and they ensure the investor will do as well as their chosen market. A tracker fund is called a PASSIVE investment strategy as the fund manager is reflecting the market and not trying to outperform it.

12CHAPTERRetail products

The alternative is an ACTIVELY MANAGED fund, where a fund manager takes investment decisions as to what to buy or sell. Charges are higher but the manager will aim to beat the market.

There is also an investment strategy that combines passive and active elements. This is known as core-satellite management, where, for example, 70% of the portfolio is in a tracker fund, and 30% is actively managed.

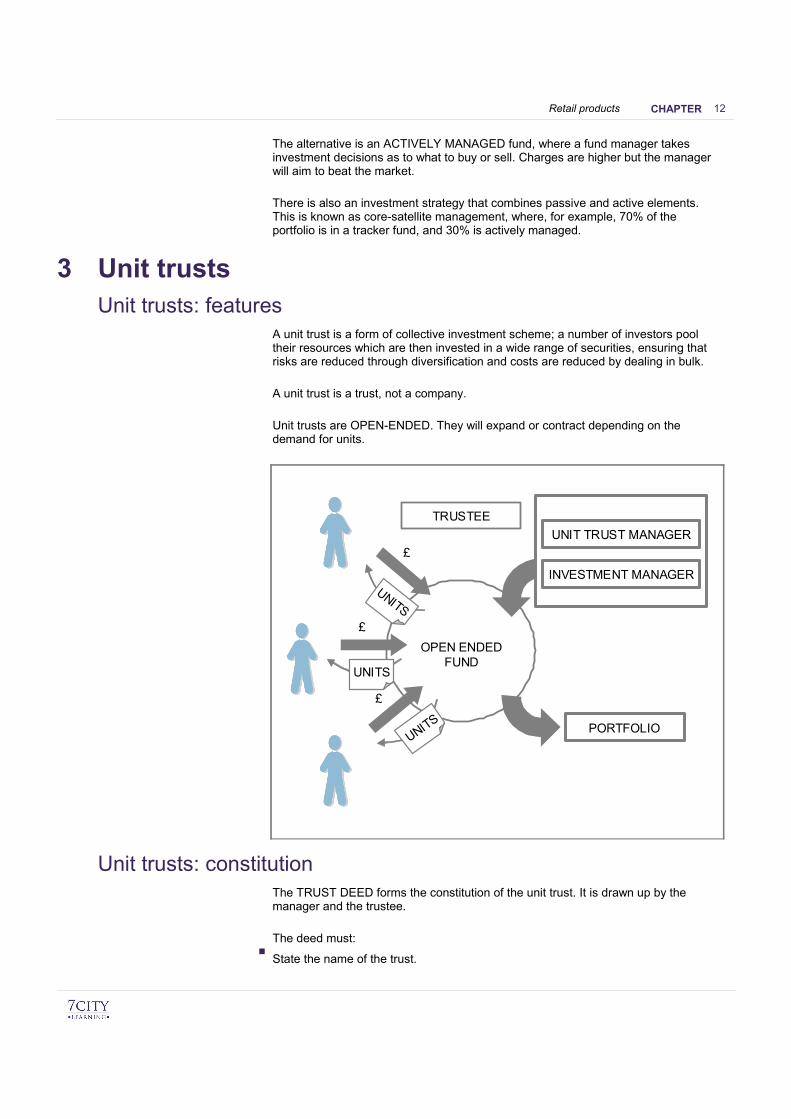

3 Unit trustsUnit trusts: features

A unit trust is a form of collective investment scheme; a number of investors pool their resources which are then invested in a wide range of securities, ensuring that risks are reduced through diversification and costs are reduced by dealing in bulk.

A unit trust is a trust, not a company.

Unit trusts are OPEN-ENDED. They will expand or contract depending on the demand for units.

£

£

PORTFOLIO

TRUSTEE

UNITS

£

UNITS

UNITS

OPEN ENDED FUND

UNIT TRUST MANAGER

INVESTMENT MANAGER

Unit trusts: constitutionThe TRUST DEED forms the constitution of the unit trust. It is drawn up by the manager and the trustee.

The deed must:

State the name of the trust.

12CHAPTERRetail products

UCITS 1UCITS 1 was the original UCITS Directive adopted by the UK in 1989. It only allowed certain types of collective investment schemes ('UCITS compliant schemes') to be marketed throughout the EEA.

To gain compliant status schemes had to:

Invest in 'transferable securities' (stocks and shares).

Invest no more than 10% of the fund in the shares or bonds of a single issuer.

Invest no more than 5% of the fund in other CISs.

Only use financial derivatives for hedging purposes.

UCITS 3 (The Product Directive)UCITS 3 (the Product Directive) was adopted in 2002 and had the effect of widening the investment powers of UCITS schemes.

UCITS 3 allows investment in the following:

Money market instruments: e.g. Treasury Bills, thus allowing money market funds to be UCITS compliant

100% of the fund in other UCITS schemes, or up to 30% in non-UCITS schemes, thus allowing funds of funds to be UCITS compliant

Bank deposits, provided no more than 20% of the scheme's assets are held with the same institution

Financial derivatives as part of the scheme's investment policy (rather than just hedging)

Index tracker funds

A UCITS 4 Directive is currently being implemented

Money market fundsMoney market funds invest in cash or near-cash assets. They are generally low-risk. It can either be a fund with a constant NAV, in which case the income of the fund is paid-out to investors, or it can have an accumulating NAV, where the income rolls-up inside the fund. The objective of both types of fund is to preserve the investor's capital and to give a better rate of return than is available on a bank deposit.

12CHAPTERRetail products

Investment BondsAn investment bond is a unit linked, single premium, whole life assurance policy. Part of the premium gives life cover whilst the balance is invested in unitised funds.

An investor will make a large one-off payment purchasing the investment bond, which will mature on a fixed date. The bond itself represents units from a range of investment funds, which can rise or fall in value taking the bond with it.

Under certain circumstances, since the bond is a life policy, certain tax advantages may be enjoyed. For example if the capital and annual interest are reinvested in full, there is no immediate liability to higher rate tax. If the proceeds of the bond are subsequently taken when a former higher rate tax payer has become a basic rate payer, there is no higher rate tax liability.

Alternatively 5% of the original investment can be withdrawn each year for 20 years, deferring the taxation until final encashment.

Protection planningAs well as life insurance, other areas require protection as part of prudent financial planning. This includes cover for: mortage repayments; critical illness; income protection; accident and sickness; household; medical and long-term care. In more detail:

Critical illness coverDesigned to pay a lump sum in the event that a person suffers from any one of a range of critical illnesses

Critical illness will be closely defined

Available to those aged 18-64 years (ends before 70th birthday)

Individual must survive 28 days from date of diagnosis

Expectation of death within 12 months

Income protection coverDesigned to pay-out an income benefit when a person is unable to work

Premiums are relatively expensive

Policy runs for a set term

Provides regular income after set waiting period

Payment will cease on return to work

Available to those aged 18-59 years (ends before 65th birthday)

Premiums are lower the longer the deferred period: e.g. four, eight, 13, 26, 52 weeks

12CHAPTERRetail products

Mortgage payment protection coverDesigned to ensure that mortgage payments are covered if the borower is unable to work

Designed to cover short-term problems (redundancy)

Similar principles to income protection

Accident and sickness coverProvides income or lump sum payments in the event of an accident

Renewed on an annual basis

Waiting period may be 30 or 60 days

Household coverBuildings and contents insurance

Exclusions likely to apply

Medical insuranceCovers the cost of medical and hospital expenses

There will be limits on what will be paid-out per claim/per year

Exclusions likely to apply

Long-term careTo provide funds that will be needed in later life to meet the cost of care

Benefit will be paid as income to cover the expenditure

Business insurance protection

Key person protection

Company insures itself against financial loss that it may suffer from the death or illness of a key employee

Cover can be based on:

- Loss-of-profit calculation

- Salary multiple

- Time to recover

- Business loans secured on those individuals

Shareholder protection/Partnership protection

With a private company, the death or illness of a major shareholder can have a serious impact on the future of the business

Shareholder protection can provide sufficient funds to enable the purchase of the deceased's shares

12CHAPTERRetail products

The policy is written under trust, so proceeds are payable to the surviving shareholders

13 PensionsIntroduction

Pensions are long-term investments that payout on retirement. They are highly tax efficient as a tax payer is given tax relief on their contribution.

There are four basic types of pension:

State pensions.

Occupational pensions.

Stakeholder pensions.

Personal pensions.

Each is considered in turn below.

State pensionsThere are two elements to the state pension in the UK:

Basic; and

The State Second Pension (S2P) - formerly SERPS

Basic pensionThe basic state pension is paid to everyone of a pensionable age (65 for men and 60 for women, although the retirement age for women is due to rise to 65 in 2018, and by 2020 it will be 66 for both men and women) who has paid sufficient National Insurance (NI) contributions.

The basic state pension is currently approximately £100 per week.

State Second Pension (S2P)The State Earnings-Related Pension Scheme (SERPS) was introduced in 1978 to provide earnings-related pensions. SERPS was only available to employees, not the self-employed.

S2P replaced SERPS in April 2002, and individuals with accrued benefits under SERPS retained them at the transition. S2P is still earnings-related and provides most help to those on lower earnings.

Employees were able to 'contract out' of S2P, in which case the government makes contributions to an employer's scheme or a personal pension.

Occupational pension schemesMost employers run some form of occupational pension scheme. Schemes can be contributory (employees pay part of the pension contributions from their salary in addition to the amount paid by the employer) or non-contributory (totally funded by the employer).

12CHAPTERRetail products

Residential property is not permitted within a SIPP. However, indirect property investments, such as property bonds or REITs, are permitted even if they are based on residential property.

Small Self-Administered Schemes (SSAS)The SSAS is a type of occupational pension scheme (OPS) ideal for small businesses (up to 12 members) who wish to build their own pension portfolio and have full control of the management of their funds before and after retirement.

With a range of contribution options and portfolio choices, SSAS pensions are especially good for small businesses as they enable them to invest in the employing company's shares or in property occupied by it (and pay rent back to the fund).

The members are normally controlling directors and senior executives of a company. They are also, more often than not, the trustees of the SSAS and therefore have substantial control over the scheme funds.

Due to this substantial control of the fund by the directors, the Financial Services and Markets Act states that all members of a SSAS should be trustees. If this is not to be the case, trustees should be authorised, as they can take investment decisions affecting other member's pension benefits.

SSAS's are fully supported by the tax authorities, they also provide tax savings for directors.

NEST and auto-enrolmentThe government has introduced legislation to make it compulsory for employers to provide a work-based defined contribution pension scheme from 2012. If there is no existing scheme, employers must enrol employees aged 22 or older, and earning more than £7,475 (2012) pa, in the new scheme. These are 'eligible jobholders'. The employer is required to make a minimum contribution of 3% into the scheme. Additionally, the tax relief and the employee's contribution can bring the minimum up to 8% of relevant earnings. The National Employee Savings Trust is a qualifying scheme for auto-enrolment. If an employee does not wish to join the scheme, they can opt-out.

14 Retail products: summaryKey concepts

Retail products: reasons for investmentThe motivating factors behind investors choosing retail products, like collective investment schemes.

Unit trustsThe features of a unit trust.

The implications for a unit trust of being authorised by the FSA.

The concept of offshore funds.

The features of the UCITS Directive.

13CHAPTERTax

Husbands and wives are taxed separately and each is entitled to the allowance. If one is non-earning it may be wise to transfer income earning assets into the name of the non-earning spouse.

No allowance is given for being married, but a CHILDREN'S TAX CREDIT may apply to those with children.

Unearned Income (Investment income)Individuals may well receive income from their savings and investments. Most investment income is taxable and is split into two categories:

Savings income

Dividend income

Savings income (interest) – A good way to remember this category is to include investment that pays interest such as: deposits, gilts, bonds, permanent interest bearing securities (PIBS) and local authority bonds.

Some forms of interest are said to be received after deduction of income tax; this is because the payer is required to deduct income tax (at a rate of 20%) and pay that amount across to the Inland Revenue. This gives the Inland Revenue a cash flow advantage.

If interest is received after deduction of income tax, the taxpayer is given a credit for the tax that they have suffered when their income tax for the year is calculated; non-taxpayers will receive a refund. Alternatively, non-taxpayers can complete an R85 to receive their interest gross.

Interest income on investments in an ISA is tax free.

Dividend Income – Income from dividends from UK companies. Dividends received from UK companies come with a 10% tax credit. This is because when UK companies declare a dividend they pay these dividends out of profits after tax.

For UK investors, this 10% tax is deemed already paid on each dividend and is given to them in the form of a tax credit. Higher rate tax payers still have more tax to pay over and above this 10% on UK dividends.

For example, Mr Smith is a higher rate taxpayer and has £10,000 of unearned interest income. He has had 20% (£2,000) deducted at source and therefore owes a further 20% (£2,000) bringing his tax liability to £4,000 on the £10,000.

3 Capital gains taxPersons chargeable to CGT

Capital gains tax is charged on the chargeable gains of an individual for a fiscal year. In essence a chargeable gain is assessed if an individual sells an asset at a profit (as long as they do not regularly trade in that asset, or profits would be assessed as income).

13CHAPTERTax

7 Tax efficient investmentsIndividual Savings Accounts (ISAs)

ISA: featuresAn ISA is a scheme of investment with limited tax liability on income or capital gains arising from assets held within the scheme.

The investments within the ISA are held within a tax-free wrapper. This is administered by an account manager. The investor must balance the potential tax savings against the account manager’s charges.

To obtain the special tax treatment investors must be UK residents aged 16 or over for a cash ISA or 18 for a stocks and shares ISA.

New ISA informationFrom 6th April 2008, the Government changed the way Individual Savings Account (ISAs), and its predecessor, Personal Equity Plans (PEPs) work. The key changes are:

New Subscription LimitIn the new tax year, an investor may make investments up to set subscription limits in a combination of cash, stocks and shares:

Cash component: £5,640 (2012/13)

Stocks and shares component: The balance up to £11,280 (2012/13)

No more than £10,200 may be put into an ISA vehicle within a tax year.

From 2012/13 onwards, the annual ISA allowance will rise with the rate of the consumer price index (CPI) rounded up to the nearest multiple of £120.

PEPs become ISAs

All current PEP accounts will become Stocks and Shares ISAs, and be subject to ISA rules. The investment that may be held remains unchanged.

Mini and Maxi ISAs

These terms are now redundant. You may now either subscribe to a Cash ISA or a Stocks and Shares ISA.

Transfer of Cash ISA to Stocks and Shares ISA

You may transfer all or some of the money in Cash ISAs to Stocks and Shares ISAs, but not vice-versa.

National Savings Bank productsThe National Savings Bank provides a wide range of investment products. These can be particularly attractive for higher rate tax payers as many of them pay returns tax free. They are also free of default risk as they are guaranteed by the Treasury.

13CHAPTERTax

Junior ISAs (JISAs)The JISA was introduced by the government in 2011 to replace the child trust fund (CTF). All UK resident children under the age of 18 who do not already have a CTF are eligible.

Just like the full ISA, there is a cash and/or stocks and shares component(s). A major difference is that the investment is only £3,600 in total each year. This will be indexed using the CPI.

A parent or guardian may open a JISA on behalf of the child, but from the age of 16 the child can assume management of the funds until the age of 18. At this point, the fund will be automatically rolled into an ISA. So, at this stage, all of the funds could be witdrawn. This is not possible before the age of 18.

8 TrustsTrusts: introduction

A trust is a way of holding or managing money or investments on behalf of a beneficiary who may not be ready or old enough to do it themselves.

For example, if a parent wishes to ensure that their child receives certain investments should that parent die, they could place those investments in trust until the child is old enough to benefit fully from those assets. If the parent dies, then the investments would be held in trust by a trustee who would manage the investments until the child reached a specified age. Once the child reached a specified age, the investments would pass into their possession.

The terms of this agreement would be set out in a legal document called a trust deed.

Trusts: jargonThere are various terms necessary to understand when considering trusts.

Trustees

Trustees are the 'legal owners' of the trust property and must deal with it in the way set out in the trust deed - the legal document setting out how the trust property is managed. They also deal with the trust administration. There can be one or more trustees.

Settlor

The settlor creates the trust and puts property into it at the start - in our example this would be the parent - possibly adding more later. The settlor says in the trust deed how the trust's property and income should be used.

Beneficiary

This is anyone who benefits from the trust - in our example this would be the child. The trust deed may name the beneficiaries individually or define a class of beneficiary, such as the settlor's family. The beneficiaries are the 'beneficial owners' of the investments.

15CHAPTEREconomics

It only includes:

Notes and coins in circulation.

The clearing banks' operational balances at the Bank of England to cover daily settlement between the bank.

M2M2 is a measure of transaction balances, bringing in a range of products which can be used to settle debts.

It only includes:

Bank wholesale deposits (including certificates of deposit).

Building society deposits (including certificates of deposit).

M4M4 has become the measure that the government has shown the greater interest in over recent years.:

M4 is the combination of M0 and M2

Open market operationsThe Bank of England is not able to set interest rates in a formal way. Instead it influences interest rates by conducting open market operations, that is buying and selling securities on the money markets. The rates of interest implied in these transactions (the REPO RATE) is the starting point for the banks in calculating their rates.

The MONETARY POLICY COMMITTEE of the Bank of England meets monthly to decide what interest rate policy should be adopted, particularly with a view to controlling inflation. The current inflation rate target is 2.0% pa (although plus or minus 1% is acceptable).

Additionally the Bank of England can act through the markets to affect the level of cash in the economy. If there is too much cash it may sell securities into the market; if there is a cash shortage it may buy up securities. In this way it is said to act as LENDER OF LAST RESORT.

The Bank of England uses these techniques to ensure STABILITY in the UK economy.

3 The role of the continuous-linked settlement (CLS) and central banksCLS bank

CLS Bank is a multi-currency bank that holds accounts with the relevant CentralBanks.

15CHAPTEREconomics

Payments to and from CLS Bank are made through the Bank of England in the UK.Payments are processed individually during the day in the RTGS (real-time grosssettlement system). Payments involving UK clearing banks are made through theClearing House Automated Payment System (CHAPS).

Target 2With the advent of the Euro in 1999, a real-time cross-border system wasimplemented to promote efficient payment mechanisms across the EU. This linkedEuro RTGS systems in all of the EU central banks with each other and enabled theEuropean Central Bank to create the TARGET system, which has been replaced with Target 2.

Federal Reserve systemThe FED is made-up of 12 regional central banks in the US. They are responsiblefor banking supervision and liquidity in their districts. The most important FED is theFED of New York. It is a permanent member of the Federal Open MarketCommittee, which sets interest rates in the US, the equivalent of the UK's baserate. Five of the other FOMC are from other FED districts. The purpose of thecommittee is to achieve price stability and sustainable economic growth in the US.The FOMC typically meets every six weeks to assess the US economy and setinterest rates accordingly.

European Central BankThe ECB is only responsible for price stability in the eurozone. This means meetingan inflationary target of 2% using the CPI. This is the same objective as that of theBank of England.

The governing body of the ECB is made-up of the heads of the central banks of thecountries that have joined the euro. The ECB, unlike most central banks in theworld, is not a lender of last resort. This is the responsibility of the national centralbanks.

4 Economic indicatorsEconomic indicators: introduction

Economic indicators are statistics collected by the government and published on a regular basis, either monthly, quarterly or annually.

A nation's economy is a many layered and complex entity. Economic indicators enable it to be monitored and measured by economists in an effort to predict its behaviour and thereby apply some sort of control.

Public sector net cash requirement (PSNCR)PSNCR is the difference between what the government receives (such as taxes and customs duties) and what it spends in a given year. In recent years it has been referred to as the Central Government Net Cash Requirement (CGNCR).

PSNCR can be funded through the issue of gilts.