Investor Presentation - ulusoyelektrik.com.tr Power Engineering and Production Company ... Colombia...

39

Ulusoy Electric Investor Presentation March 2018

Transcript of Investor Presentation - ulusoyelektrik.com.tr Power Engineering and Production Company ... Colombia...

Ulusoy ElectricInvestor Presentation

March 2018

Table of

Contents

Company Snapshot

Business Overview

Growth & Prospects

Financials

3

6

29

32

Company Snapshot

March 2018 Investor Presentation

Ulusoy Electric at a Glance

4

PRODUCTION FACILITIES

Operations in

Turkey│Indonesia│Algeria

Countries3 Production

750 Employees

Above 15%High-Caliber Engineers

Indoor area of 60K m²built on a area of87K m²

‘’0’’ debt Strong financial

CORPORATE STRUCTURE

Domestic

Over the past decadeMarket Leader

PRODUCTION and R&D

Design&Capabilities Structure

Long term sustainableand solid growthstragety

Min. 2 digit growth

Min. 20% EBITDA margin

FINANCIAL STRUCTURE

Turkey’s Leader Switchgear Producer Operating as Electric Power Engineering and Production Company”

Vertically Integrated

Flexible In-House

Exporting to morethan 50 countries

No major CAPEX investment

March 2018 Investor Presentation

Key Milestones

1985

31-year story of Ulusoy Electric started.

The Company founded by

Mr. Sait Ulusoy

1986

•Contracting activities started (Urban Networks, Airport Electrification, 154 kV Power Cables etc.).

•Manufacturing activities started with 36 kV outdoor switch disconnectors.

1995

The Companywas listed in the first 50

companies in Turkey to qualify for ISO-9000 standards

1997

Firstdomestic

Monoblock Substation

Kiosk production

1999

First domestic MV cable

termination production using liquid

silicon injection

2006

First domestic production of overhead line recloser andsectionalizers

2007

The Company was listed in

the TOP 1,000 biggest

industrial companies in

Turkey

2013

Entered into Indonesia market with a new office

Company’sown design cantilever

insulators was developed

2015

New 31,750 m² manufacturing

facility investment for

distribution transformers and concrete

substation kioskwas completed

2014

Launched its IPO and was listed on the

Borsa Istanbul

2008

Algeria office was established

Company’s own design vacuum circuit breaker and

underground substation kiosks was

developed

5

Business Overview

March 2018 Investor Presentation

Our Business Model Overview

7

March 2018 Investor Presentation

What We Produce

8

March 2018 Investor Presentation

Manufacturing Facilities (Switchgear)

Headoffice & Main Production Facility

• Located in Ankara

• Completed in 2004

• 26,000 m² indoor area

Capacity

25,000-45,000* air insulatedswitchgears

15,000 gas insulated switchgears

1,250 metal clad

9

*Varies on type&configuration of the switchgears

March 2018 Investor Presentation

Manufacturing Facilities (Transformer&Substation)

10

New Transformer Facility Ensured

• Enterance into a new business line

• Completion of vertical integration

• Enhancement in competitive edge

• Diversification in revenue stream

• Improvement in sustainability of revenue

• Located in Ankara

• Completed in 2015

• 31,750 m² indoor area

• 5,000 annual transformer capacity

• 4,500 substation kiosk capacity

• US$10.7mn total investment

• US$ 5000 transformer avg. Price*

*Varies on ratings and types

FY 2016 2017 2018EProd. Unit 863 2189 3500Av. Price (USD) 4200 5700 5500Revenues 3.624.600 12.481.240 19.250.000

March 2018 Investor Presentation

Manufacturing Facilities (Indonesia)

Local Indonesia Assembly Facility

• Located in Jakarta

• Opened in 2017

• 4,000 m² indoor area

Capacity

6,000-7,000* air insulatedswitchgears

11

*Varies on type&configuration of the switchgears

Foreign Direct Investment 100% owned by Ulusoy Elektrik A.S

March 2018 Investor Presentation

Manufacturing Facilities (Algeria)

Local Algeria Assembly Facility

• Located in Constantine

• Opened in 2017

• 2,600 m² indoor area

Capacity

7,000 air insulated switchgears

12

• 100% local factory• owned by SARL INTELEC • Former Main Distributor of Ulusoy Elektrik A.S• Technology & License by Ulusoy

March 2018 Investor Presentation

New Manufacturing Facility Investment

New Facility

• Located in Ankara (just 800 meters to existing Trafo Facility)

• Expected Completion date end of 2019

• 24,000 m² indoor area in a land of 26,000 m²

• Investment Amount : TL 2M (Land) + TL 10M (Building) USD 3M in total

Capacity & Plans

To increase capacity in;

Gas insulated switchgears

Epoxy Resin components

Being ready for any market demand (new product or newmarket)

13

March 2018 Investor Presentation

Production Process & Suppliers

TOP-10 Suppliers

• Galvanized & Grain Oriented sheet steel

• Copper & Aluminum

• Epoxy Resin & Silicone

• Electrical part and component manufacturers

82%

12%6%

COGS Breakdown*

2016

82%

10%

8%

Raw materials Personel expenses Others

2015

COGS

Revenue78% 71%

14

71% FX Exposure in COGS

83% FX Exposure in Raw Materials

* Without amortization

Naturally Hedging Itself thru FX-Based Receivables

85%

8%7%

2017

69%

~38 %Of the Revenues are in foreign currency

March 2018 Investor Presentation

Volume & Capacity Development

15

* Avarage 25.000-45.000 Varies on type &configuration of the switchgears

Product

2012 2013 2014 2015 2016 2017

Dom. Exp. Dom. Exp. Dom. Exp. Dom. Exp. Cap. Util. Dom. Exp. Cap. Util. Dom. Exp. Cap. Util.

Air insulated switchgears

10.643 7.154 11.471 30.365 11.556 9.857 11.992 609 36% 13.779 1.051 42% 16.730 769 50%

Capacity* 21.600 35.000 35.000 35.000 35.000 35.000

Gas insulated switchgears

1.001 109 1.344 14 127 80 1.508 185 16% 1.943 304 21% 3.548 328 %37

Capacity* 1.350 2.750 2.750 10.500 10.500 10.500

Substation kiosks

2.539 60 2.693 31 2.494 - 2.540 46 81% 3.058 1 68% 4.183 %93

Capacity 2.400 3.000 3.200 3.200 4.500 3.200

Metal Clad Switchgears

46 107 25 193 7 202 73 150 18% 193 90 23% 91 129 %18

Capacity 400 750 750 1.250 1.250 1.250

Transformers - - - - - - 29 1% 478 385 17% 991 1.166 %43

Capacity - - - 5.000 5.000 5.000

March 2018 Investor Presentation

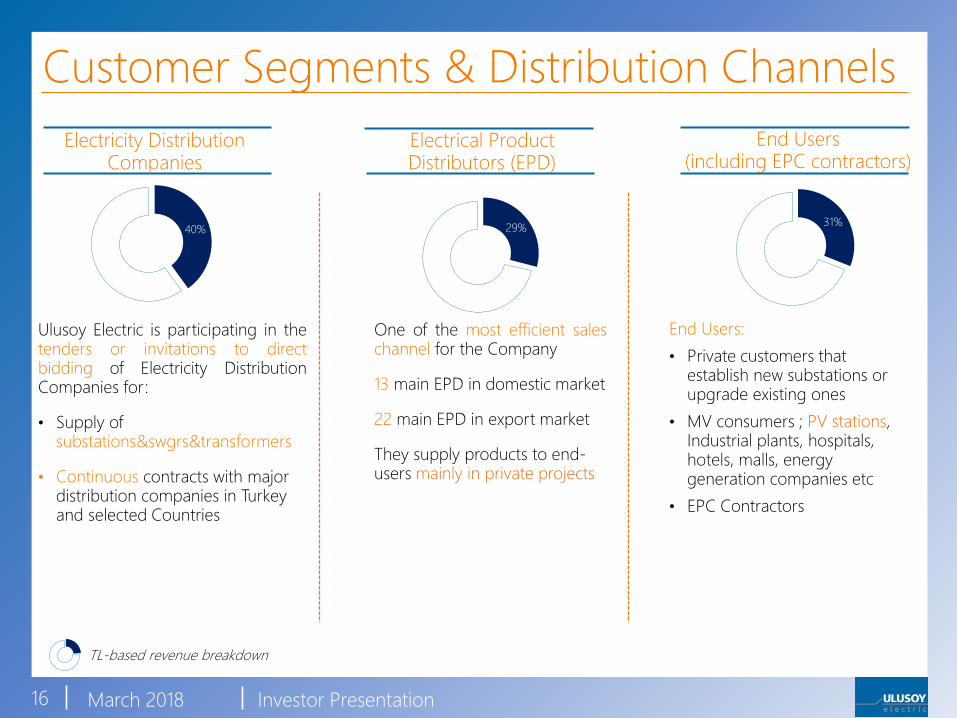

Customer Segments & Distribution Channels

Electricity Distribution Companies

End Users (including EPC contractors)

29%

One of the most efficient saleschannel for the Company

13 main EPD in domestic market

22 main EPD in export market

They supply products to end-users mainly in private projects

Electrical Product Distributors (EPD)

31%

Ulusoy Electric is participating in thetenders or invitations to directbidding of Electricity DistributionCompanies for:

• Supply of substations&swgrs&transformers

• Continuous contracts with major distribution companies in Turkey and selected Countries

40%

End Users:

• Private customers that establish new substations or upgrade existing ones

• MV consumers ; PV stations, Industrial plants, hospitals, hotels, malls, energy generation companies etc

• EPC Contractors

TL-based revenue breakdown

16

March 2018 Investor Presentation

Sector (Domestic)

17

ELECTRICITY DISTRIBUTION COMPANIES

Investment Implementation PeriodInvestmentBudget (TL)

2006-2010 (before privatization) 550 M

2011-2015 3,69 B

2016-2020 18,4 B2016 (official investment result) 3,7 B

2016 Dist.Co. Sales 2017 Dist.Co. Sales

91.9 M TL 155.3 M TL % 69

*2017 realization+ 4 Billion

March 2018 Investor Presentation

Sector (Domestic)

18

ELECTRICAL PRODUCT DISTRIBUTORS (EPD)

2016 EPD Sales 2017 EPD Sales

48.9 M TL 118.8 M TL % 143

• Positive Economic Environment• Residential & Industrial Investments• New Distributors• PV Investments

March 2018 Investor Presentation

Sector (Domestic)

19

DIRECT SALES

2016 Direct Sales 2017 Direct Sales

47.2 M TL 104,2 M TL % 121

• Photo-Voltaic & Wind Electricity Generation Projects • 500 MW Wind Project in the coming 5 years (already been awarded)• 1000MW YEKA tender (generation & turbine production)

March 2018 Investor Presentation

Sector (Domestic)

20

DOMESTIC REVENUE BREAKDOWN BY CUSTOMER SEGMENTS

52%16%

32%

2016

Dist.Co. Retailers

Direct Sales

378.3 M TL 188.0 M TL

% 101

41%

32%

27%

2017

Dist. Co. Retailers

Direct Sales

March 2018 Investor Presentation

International Market

Global Distributor Network

• 22 distributors across the globe

• Easy access to markets via local

partners (distributors)

• Sales offices in Istanbul, Algeria,

Jakarta and Dusseldorf

• 12 seasoned sales professionals dedicated to export sales and marketing

21

ASIA & MIDDLE EAST

AFRICA

IBERIA & LATAM

Russia

Kazakhstan

Palestine

Iraq

Turkmenistan

Jordan

Malaysia

Qatar

UAE

KSA

Algeria

Morocco

Tunisia

Sudan

Peru

Colombia

Uruguay

Spain

Portugal

• Diversified Export Breakdown

• Exposure to expand in Europe going forward

• Sustainable presence in 12 countries

• Indonesia PLN approval completed& USD 3,5M tender awarded

March 2018 Investor Presentation

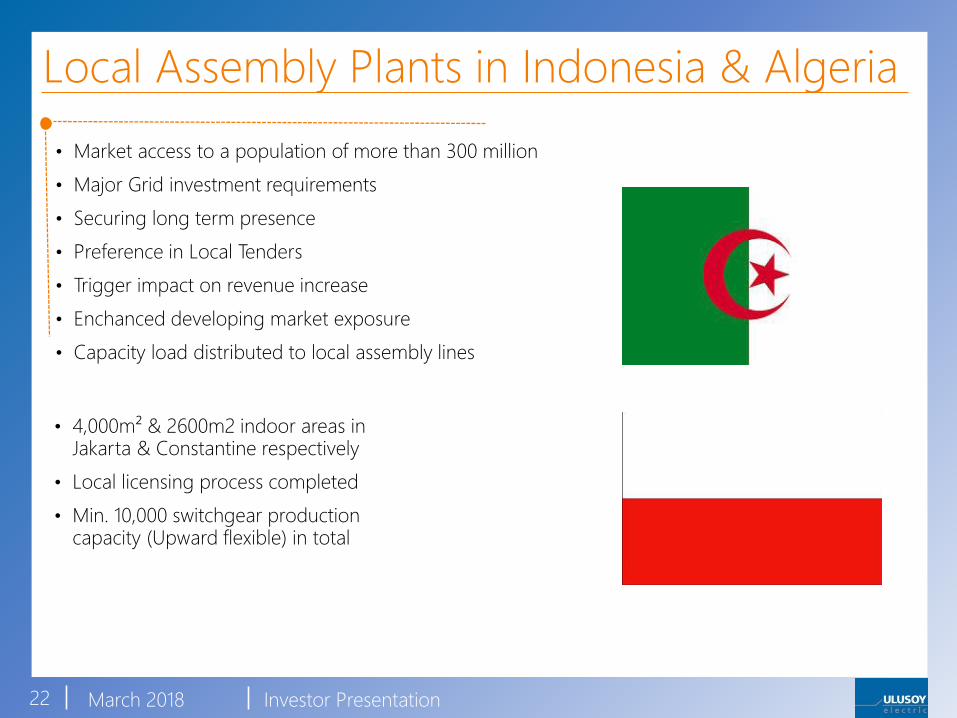

Local Assembly Plants in Indonesia & Algeria

22

• 4,000m² & 2600m2 indoor areas in Jakarta & Constantine respectively

• Local licensing process completed

• Min. 10,000 switchgear productioncapacity (Upward flexible) in total

• Market access to a population of more than 300 million

• Major Grid investment requirements

• Securing long term presence

• Preference in Local Tenders

• Trigger impact on revenue increase

• Enchanced developing market exposure

• Capacity load distributed to local assembly lines

March 2018 Investor Presentation

21%

11%

10%

10%

47%

Ethiopia SpainTunisia IndonesiaOther 29 Countries

87%

4%3%

6%

Algeria Iraq

Turkmenistan Other 26 Countries

65%

11%

5%

18%

Algeria Kirghizstan

Iraq Other 29 Countries

Country Breakdown of Exports (mn TL)2012 (40,8 mn) 2013 (148,8 mn) 2014 (70,2 mn)

2015 (22,6 mn)

23

70%

16%

5%4%

6%

Algeria JordanTurkmenistan IraqOther 16 Countries

20%

17%

9%9%

8%

5%

4%

4%

3%

3%

18%

Iraq Tunusia FinlandPalastine Uruguay AlgeriaLithuania Kazakhstan MoroccoSpain Other 23 Countries

2017 (65,0 mn)2016 (42,4 mn)

26%

9%

6%5%5%4%

4%3%

3%3%

3%

28%

Jordan Iraq Kosovo

Sudan France Albania

Azerbaijan Kazakhistan Morocco

Ethiopia Finland Other 40 Countries

March 2018 Investor Presentation

Sector (Export)

24

EXPORT REVENUES

FY 2017FY 2016

42.4 M 65.0 M%53

A significant jump in export revenues expected in 2018 due to diversified exportmarkets and localization operations.

More than TL 80M order intake as of 27.02.2018

March 2018 Investor Presentation

TOP-10 Clients

TOP-10 Clients in Total Domestic

TOP-10 Clients in Total Export

2016

51%

56%

TOP-10 Clients in Total Domestic

TOP-10 Clients in Total Export

2017

25

2016

2017

CustomerName

Domestic/Type

Amount % of

Export (TL mn) Total Sales

Customer A Domestic Elect. Dist. Comp. 36.5 8%

Customer B Domestic Elect. Dist. Comp. 30.1 7%

Customer C Domestic Distributor 28,9 7%

Customer D Domestic Distributor 22.5 5%

Customer E Domestic Elect. Dist. Comp 17.6 4%

Customer F Export Elect. Dist. Comp. 12.9 3%

Customer G Domestic Distributor 12.1 3%

Customer H Domestic Elect. Dist. Comp. 11.8 3%

Customer I Domestic Elect. Dist. Comp. 11.6 3%

Customer J Domestic Distributor 10.4 2.5%

Total: 194.7 44%

CustomerName

Domestic/Type

Amount % of

Export(TL mn)

Total Sales

Customer A Domestic Elect. Distrib. Comp. 20.1 9%

Customer B Domestic Elect. Distrib. Comp. 16.6 7%

Customer C Domestic Elect. Distrib. Comp. 15.2 6%

Customer D Domestic Distributor 14.9 6%

Customer E Domestic Elect. Distrib. Comp. 11.0 5%

Customer F Domestic Elect. Distrib. Comp. 8.9 4%

Customer G Export Distributor 8.4 4%

Customer H Domestic Distributor 8.2 4%

Customer I Export Elect. Distrib. Comp. 7.4 3%

Customer J Domestic End User 6.4 3%

Total: 117.1 50%

49% 70%

March 2018 Investor Presentation

Competitive-Edge in Production

Efficienct Production

Capable to Compete with Global Players

26

Newly Completed Transformer Facility enables to be one-step ahead of competitiors

via vertical integration

│Switchgear│ │Transformer│ │Substation Kiosk│

Natural Entry Barrierto the sector

market players need to hold & make

│Know-How│ │Licensing│ │Type Test│

In-House Flexible Quality-Oriented Vertically-Integrated

Faster responses & aftersales support

Economies of Scale Attractive Prices

March 2018 Investor Presentation

Local & Int’l Competition

27

ABB,SIEMENS,SCHNEIDER, GE

LUCY (UK),ORMAZABAL(SPAIN),

EFACEC (PORTUGAL)

ULUSOY, ELIMSAN, SAREL, TAMCO, DREISCHER, SEL, ZPUE

BIG FOUR

GLOBAL MULTINATIONALS

+ BILLION EURO/USD

TURNOVER

FOLLOWERS

BECOMING

MULTINATIONAL

300-500M EURO TURNOVER

REGIONAL LEADERS

50-100M EURO TURNOVER

Growth &

Strategy

March 2018 Investor Presentation

Growth Prospects & Strategy

Sustainable & Diversified Revenue Stream

with

Double Digit Growth in Local and Other Developing Markets

Solid and Sustainable Growth in Domestic Market

Dominant market leader positionin a booming market benefiting

from higher margins andsustained revenue stream

New Transformer FacilityNewly-Completed Huge

Transformer Facility Enabiling the Vertical Integration &

Higher Market Share

29

Inorganic GrowthOpportunities

Strategically keeping eyesopen for interesting merger

opportunities potentially for a new product range, increasingthe market share and/or cost

minimization

Vast Opportunities around the Globe

Improved brand awarness, enhanceddistributor network and recently

completed long lasting certificationprocesses has opened door forsustainable & diversified export

revenues

March 2018 Investor Presentation

Global Electricity TrendsPV industry & Electric Vehicles

30

• From today until 2040, USD 11.4tn will be invested in powergeneration. Of that USD 7.8tn will be invested in renewable energy.At least half of this amount is for Solar.

• The World’sCumulative installed PV capacity of 302 GW will reachto 740 GW by 2022 and 5600 GW by 2050

• EV market grew 60% in 2016, Plug in automobiles may reach 30%market penetration by 2030

• the world will need 600 million electric vehicles by 2040, comparedto existing 2,5 million as of 2017.

• We need more Charging Stations, more Grid substations

*Source: International Energy Agency www.iea.org

Financials

March 2018 Investor Presentation

Revenues

Total Revenue in TLmn

2013

32

260

177

144

228

437

2014 2015 2016 2017

March 2018 Investor Presentation

Revenue Development

33

234,2

442,2

+77

+131

0,0

100,0

200,0

300,0

400,0

500,0

600,0

700,0

2016 Revenues Volume change Price change 2017 Revenues

TLm

n

March 2018 Investor Presentation

Revenue BreakdownBreakdown by Product Type (TLmn)

Breakdown by Destination (TLmn)

34

15 16 17 27500,5

13

46

10 11 910

15192

11878

110

22510

13

19

30

44

34

20

21

38

57

2013 2014 2015 2016 2017

Substation kiosks Transformers Metal Clad Air insulated switchgers Gas insulated switchgers Other

112 108 120 188378149 70 23

42

65

0

500

2013 2014 2015 2016 2017

Domestic Export

March 2018 Investor Presentation

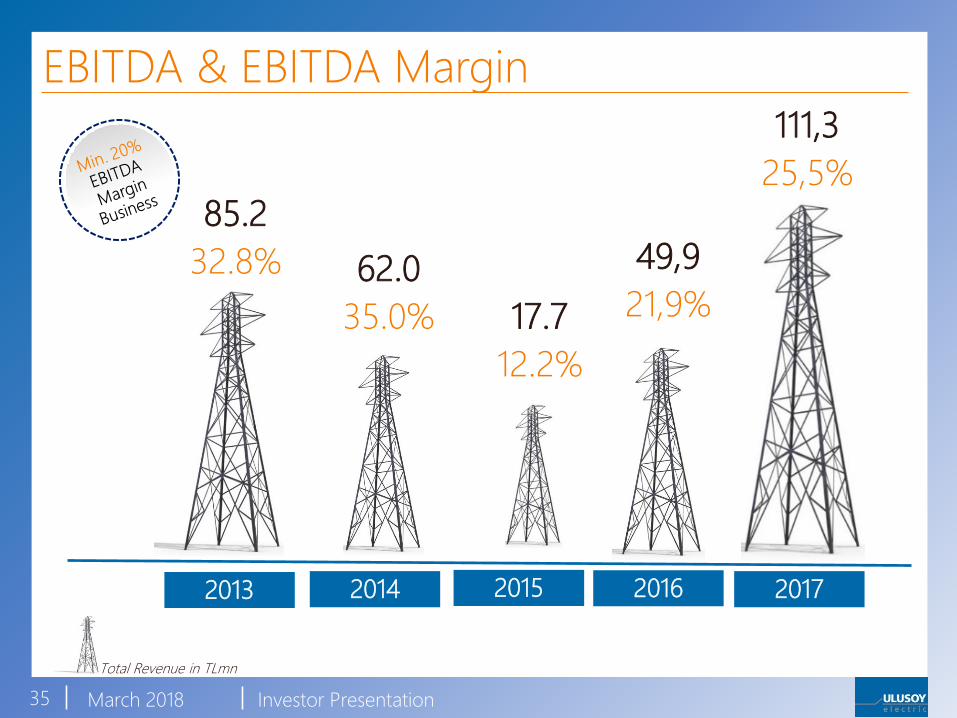

EBITDA & EBITDA Margin

Total Revenue in TLmn

2013

35

85.2

32.8% 62.0

35.0% 17.7

12.2%

49,9

21,9%

111,3

25,5%

2014 2015 2016 2017

March 2018 Investor Presentation

Capital Expenditures Pattern of Progress

36

4.1 3.9

16.6

12.6

17.0

2011 2012 2013 2014 2015

Capex for Maintenance

~TL1mn per annum

5,2

6,2

2016 2017

Heavy investment period for the new transformer facility is

already completed

March 2018 Investor Presentation

Summary of Financial Statements

37

TL mn 2013 2014 2015 2016 2017Revenues 260,0 177,2 144,5 227,8 436,5Domestic 112,5 108,1 120,6 188,0 378,3Export 148,8 70,2 22,6 42,4 65,0Gross Profit 95,5 73,4 29,5 63,1 128,6EBITDA 85,2 62,0 17,7 49,9 111,3Net Income 71,7 45,2 13,6 35,9 87,1

Gross Profit Margin 36,7% 41,4% 20,4% 27,7% 29,5%EBITDA Margin 32,8% 35,0% 12,2% 21,9% 25,5%Net Margin 27,6% 25,5% 9,4% 15,8% 19,9%

Current Assets 114,0 107,4 79,8 117,8 211,6Cash&Cash Equivalents 45,8 17,7 14,0 13,8 30,3Non-Current Assets 25,8 37,6 71,2 72,2 73,0Property,Plant and Equipment 23,4 32,9 66,6 67,7 68,3Total Assets 156,3 145,6 151,0 190,0 284,6Total Liabilities 38,5 28,3 44,2 55,1 80,7S.T.Liabilities 36,0 27,2 42,5 52,6 78,1L.T. Liabilities 2,5 1,1 1,7 2,5 2,6Equity 117,8 116,8 106,8 134,9 203,9ROE 61,1% 38,9% 12,8% 26,6% 42,7%

Depreciation&Amortization 1,6 1,9 3,1 4,6 5,2Net Debt Position -45,2 -17,2 -7,2 -6,2 -25,7CAPEX 16,6 12,6 17,0 5,2 6,3

March 2018 Investor Presentation

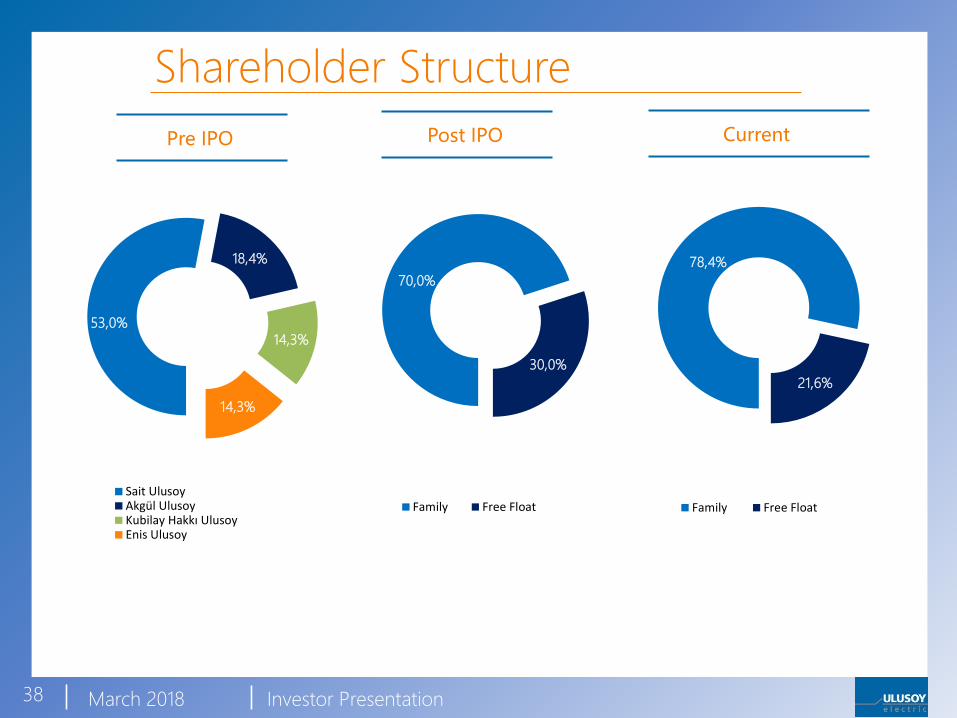

Shareholder Structure

Pre IPO Post IPO Current

38

70,0%

30,0%

Family Free Float

78,4%

21,6%

Family Free Float

53,0%

18,4%

14,3%

14,3%

Sait UlusoyAkgül UlusoyKubilay Hakkı UlusoyEnis Ulusoy

Thank YouFor further information please e-mail

or call Ulusoy Electric Investor Relations

at (+90 312 267 0712)