Investor Presentation November 2012 0 - SK · PDF file2. 4G LTE LTE competitiveness Launched...

15

November 2012 Investor Presentation 0

Transcript of Investor Presentation November 2012 0 - SK · PDF file2. 4G LTE LTE competitiveness Launched...

November 2012

InvestorPresentation

0

2

Disclaimer

This presentation has been prepared by SK Telecom Co., Ltd. (“the Company”). This presentation is being

presented solely for your information and is subject to change without notice. No representation or warranty,

expressed or implied, is made and no reliance should be placed on the accuracy, fairness or completeness of the

information presented. The Company, its affiliates, advisers or representatives accept no liability whatsoever for

any losses arising from any information contained in the presentation.

This presentation does not constitute an offer or invitation to purchase or subscribe for any shares of the

Company, and no part of this presentation shall form the basis of or be relied upon in connection with any contract

or commitment.

The contents of this presentation may not be reproduced, redistributed or passed on, directly or indirectly, to any

other person or published, in whole or in part, for any purpose.

3

Contents

1. Wireless

2. 4G LTE

3. B2B

4. SK Planet

5. SK Hynix

6. Financial Results

7. Shareholder Return

Percentage of LTE

Wireless market trend

Total subscribers Penetration

(Unit: Mn, %)

Smartphone subscribers

90%94%

98%

104%106% 106%105% 107%

2007 2008 2009 2010 2Q11 4Q11 2Q12 3Q12

4446

4850

52 53 53

Source: Company & KCC data as of September 30, 2012

1

7

15

23

28

53

31

2%

13%

22%

4

Wireless market overview 1. Wireless

Smartphone population continues to grow inline with demand for LTE services

Market structure remains intact despite disruptive competitive dynamics

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

Wireless market share trend

(Unit: %)

Mar.07: KT first to

complete nationwide

HSDPA rollout

Nov.09: KT first to

release iPhone

Mar.12: LGU+ first to

complete nationwide LTE

network rollout

SKT

50.3

KT

30.9

LGU+

18.8

‘09 ‘10 3Q12 ‘08 ‘11 ‘07 ‘06

5

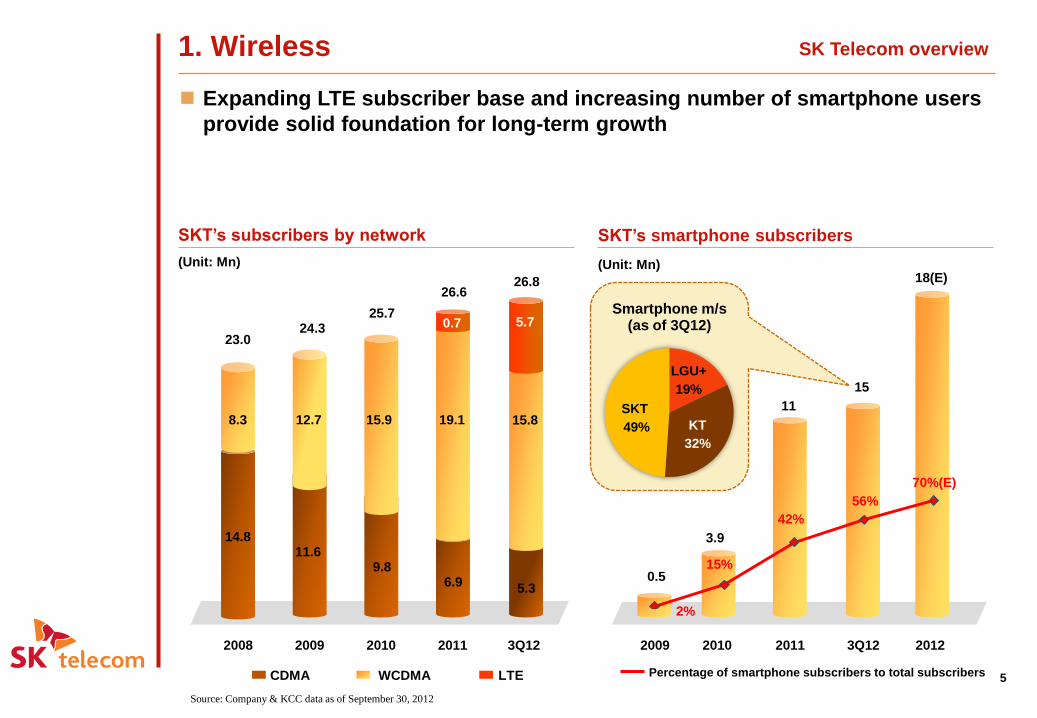

SK Telecom overview1. Wireless

SKT’s subscribers by network

LTEWCDMACDMA

(Unit: Mn)

3Q122009 2010

23.024.3

25.7

26.6

20112008

8.3 12.7 15.9 19.1

14.811.6

9.86.9

0.7

26.8

15.8

5.3

5.7

Expanding LTE subscriber base and increasing number of smartphone users

provide solid foundation for long-term growth

2010

11

0.5

3.9

18(E)

Percentage of smartphone subscribers to total subscribers

SKT’s smartphone subscribers

2011 20122009

15%

42%

2%

(Unit: Mn)

15

3Q12

56%

70%(E)

Smartphone m/s(as of 3Q12)

SKT

49% KT

32%

LGU+

19%

Source: Company & KCC data as of September 30, 2012

6

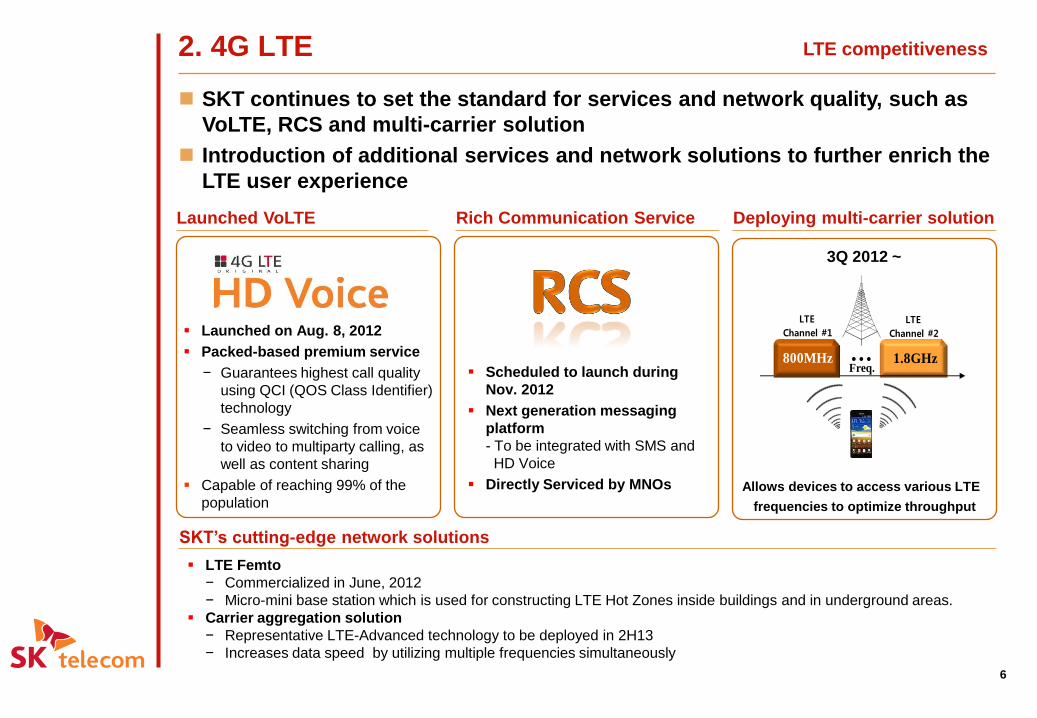

LTE competitiveness2. 4G LTE

Launched VoLTE

SKT continues to set the standard for services and network quality, such as

VoLTE, RCS and multi-carrier solution

Introduction of additional services and network solutions to further enrich the

LTE user experience

Launched on Aug. 8, 2012

Packed-based premium service

− Guarantees highest call quality

using QCI (QOS Class Identifier)

technology

− Seamless switching from voice

to video to multiparty calling, as

well as content sharing

Capable of reaching 99% of the

population

3Q 2012 ~

Deploying multi-carrier solution

Freq.…800MHz 1.8GHz

LTE

Channel #1

LTE

Channel #2

Allows devices to access various LTE

frequencies to optimize throughput

LTE Femto

− Commercialized in June, 2012

− Micro-mini base station which is used for constructing LTE Hot Zones inside buildings and in underground areas.

Carrier aggregation solution

− Representative LTE-Advanced technology to be deployed in 2H13

− Increases data speed by utilizing multiple frequencies simultaneously

SKT’s cutting-edge network solutions

Rich Communication Service

Scheduled to launch during

Nov. 2012

Next generation messaging

platform

- To be integrated with SMS and

HD Voice

Directly Serviced by MNOs

7

LTE subscribers2. 4G LTE

2011 2012 2013 2014

54% CAGR

(2012~2014)

13.5(E)

0.6

7(E)

16.7(E)

2011 1Q12 2Q12 3Q12

630

1,140

LTE subscriber targetsLTE subscriber additions

LTE subscriber growth continues to gain momentum

Targeting at 7mn subscribers by year-end; surpassed 6 mn subscribers in

October

1,570

3%

26%

50%

62%

■

■

■

Percentage of LTE subscribers

(Unit: Mn)(Unit: ‘000)

■

2,330

8

LTE price plan and ARPU2. 4G LTE

Popular tariff plan

Price

(KRW)

Revenue

discount

(KRW)

Net

ARPU

(KRW)

% of

new

subs

≥ LTE-62 62,000 16,000 46,000over

80%

≥ 3G-54 54,000 17,500 36,500over

70%

Diff. +8,000 -1,500 +9,500 -

Popular LTE price plans provide ARPU uplift effect; currently over 80% of new

LTE subscribers on LTE-62 or higher price plans

LTE ARPU is significantly higher than smartphone and blended ARPU

Additional charge of up to KRW 18,000 for incremental

3GB LTE data consumption in excess of allotment

ARPU comparison

(Unit: KRW ‘000)

LTE Smartphones

(3G + LTE)

52.0

41.5

25%

higher

Blended ARPU

33.1

57%

higher

as of 3Q12

9

profitability improvement2. 4G LTE

2Q11 3Q11 4Q11 1Q12 2Q12 3Q12

33.2

32.6

33.6

Note: Includes SK Planet revenues

32.2

2013

Blended ARPU

(Unit: KRW ‘000)

Ta

riff cu

t

LT

E u

plift

ARPU to continue its upward trajectory; expect 4Q12 ARPU to show healthy

growth

Market competition cooling initiatives to have positive profit impact

33.1

Rational market competition

− Subsidies for new and renewing

subscribers reduced by 70-100K Won

in 2Q12

− Penalties for premature contract

termination on Nov. 1, 2012

; terminating subscribers subject to a fee

for discount benefits received

Cost control initiatives

32.9

10

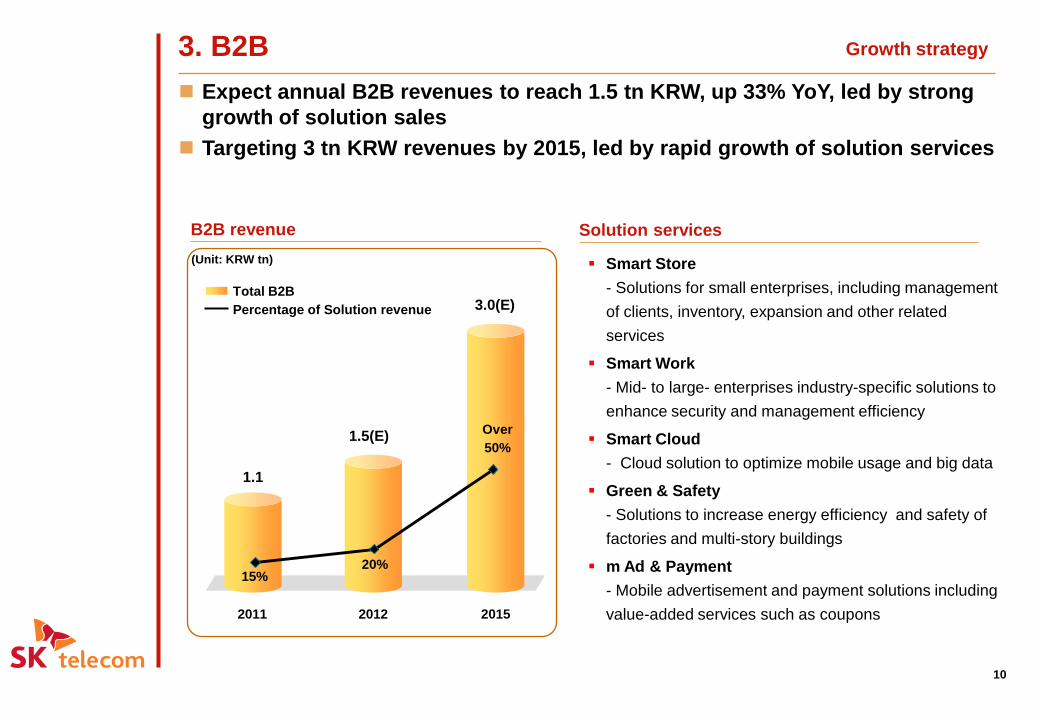

Growth strategy3. B2B

Solution servicesB2B revenue

1.1

(Unit: KRW tn)

1.5(E)

3.0(E)

2011 2012 2015

Percentage of Solution revenue

Total B2B

15%20%

Over

50%

Expect annual B2B revenues to reach 1.5 tn KRW, up 33% YoY, led by strong

growth of solution sales

Targeting 3 tn KRW revenues by 2015, led by rapid growth of solution services

Smart Store

- Solutions for small enterprises, including management

of clients, inventory, expansion and other related

services

Smart Work

- Mid- to large- enterprises industry-specific solutions to

enhance security and management efficiency

Smart Cloud

- Cloud solution to optimize mobile usage and big data

Green & Safety

- Solutions to increase energy efficiency and safety of

factories and multi-story buildings

m Ad & Payment

- Mobile advertisement and payment solutions including

value-added services such as coupons

Financial results4. SK Planet

11

SK Planet’s financial results

(Unit: KRW Bn)

11st revenue

261

174

(Unit: KRW Bn) 330(E)

7561

2010 2011 2012

SK Planet continues to show strong growth led by 11st, T store and T map

7661

243

1Q12

6

250

3Q12

18

Revenue

Operating income

Annual

2Q12

267

30

7975

3Q

(Unit: Mn)

2011 2Q12 2012

T map active users

T store active users

1Q12

(Unit: Mn)

3Q12

2111 2Q12 20121Q12 3Q12

6.6

8.5(E)

5.86.3

7.6

4.8

4.0

6.2(E)

4.3

5.8

1Q

2Q

12

5. SK Hynix Impact on SKT’s results

Recent results

SKT recorded KRW 8.4bn in SK Hynix-related

equity accounting gain in 3Q12

Market consensus forecast

10.2

(Unit: KRW Tn)

2012

3.2

-0.2

12.0

2013

5.0

1.2

Revenue EBITDA Net income

Source: Thomson One, as of November 5, 2012

SK Hynix’s performance is expected to show gradual improvement as firmer DRAM and NAND demand through the release of Windows 8 and new products of smartphone and tablet PC

13.3

2014

5.7

1.7

Unit: KRW Bn 2010 2011 3Q12 YoY QoQ

Revenue 12,106 10,396 2,423 6% -8%

EBITDA 6,069 3,746 776 +26% -2%

Oper. profits 2,975 325 -15 N/A N/A

Net income 2,598 -56 2 N/A N/A

Debt 6,041 6,776 6,720 -343 Bn 92 Bn

Net debt 3,839 4,900 4,930 -138 Bn 1,292 Bn

Debt/Equity 76% 85% 69% -16%p +2%p

Net debt/Equity 48% 61% 50% -11%p +13%p

6. Financial Results (K-IFRS)

13

Operating Income

EBITDA

Net Income

3Q12

4,126

301

960

176

3Q11(Unit: KRW Bn)

YoY

-46.4%

-21.1%

-54.2%

2.0%4,045

561

1,216

384

2Q12 QoQ

-27.6%

-7.7%

45.7%

2.9%Revenues

Consolidated

Net Debt/Equity 47.3% 22.5%pt24.8% -0.6%pt

SKT CapEx

(Non-consolidated) 788 42.7%552 28.0%

4,008

416

1,040

121

47.9%

616

7. Shareholder Return

Total shareholder returns

(Units: KRW Bn)

Cash dividend Share buyback*

Maintain strong shareholder return policy

Paid annual cash dividend of KRW

9,400/share since 2007

- Includes interim dividend of KRW 1,000/share

Commenced share buybacks in 4 out of

past 5 years

- KRW 208bn in 2011

Strong shareholder return policy

14

* The total number of treasury stocks stood at 11,050,712 shares(13.69% of total stock issued) as of 3Q12

680

2009 2010

880 864

2011

210 208

774

2008

92

801

2007

119

15

Website: http://www.sktelecom.com → Investor relations