Investor Presentation February 2013 - Indian Oil Corporation · PDF file ·...

47

Investor Presentation February 2013

Transcript of Investor Presentation February 2013 - Indian Oil Corporation · PDF file ·...

Investor Presentation February 2013

1

IOCL – An Overview

Oil Industry In India

IOCL’s Core Operations

Strategic Initiatives

Financial Performance

Ongoing Projects

Nine Months Snapshot

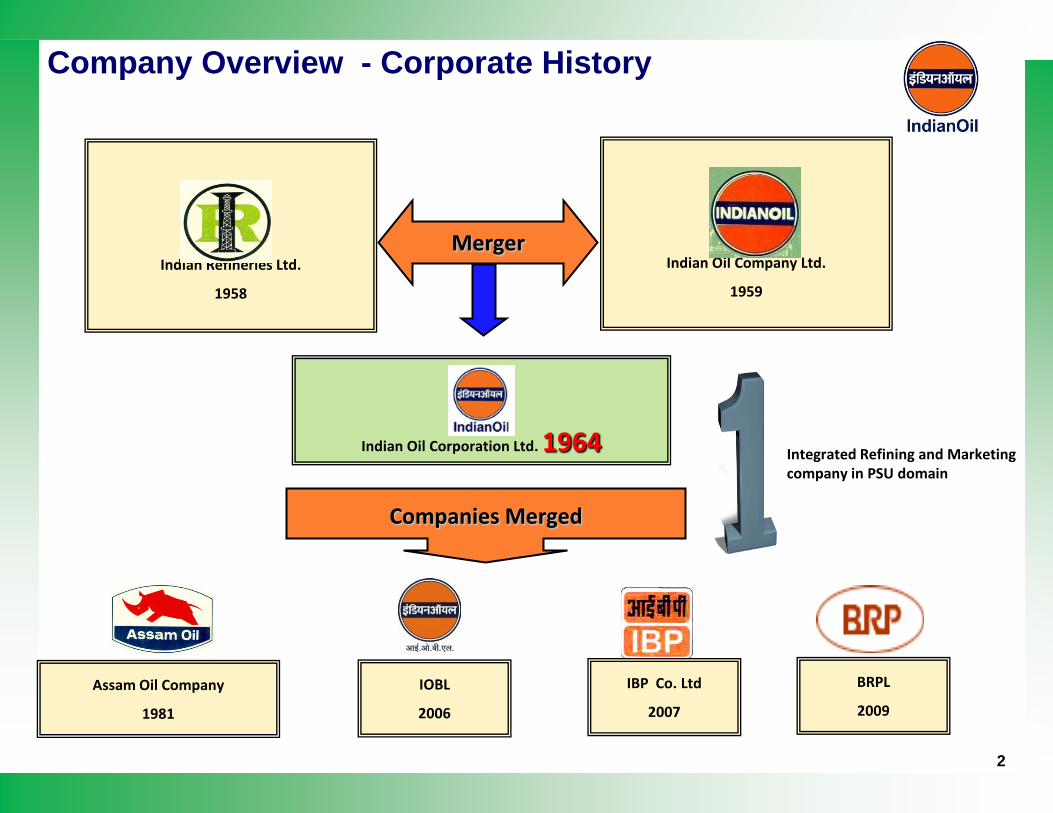

Company Overview - Corporate History

Indian Oil Company Ltd.

1959

Indian Refineries Ltd.

1958

Indian Oil Corporation Ltd. 1964

Merger

Assam Oil Company

1981

IOBL

2006

Companies Merged

IBP Co. Ltd

2007

BRPL

2009

Integrated Refining and Marketing company in PSU domain

2

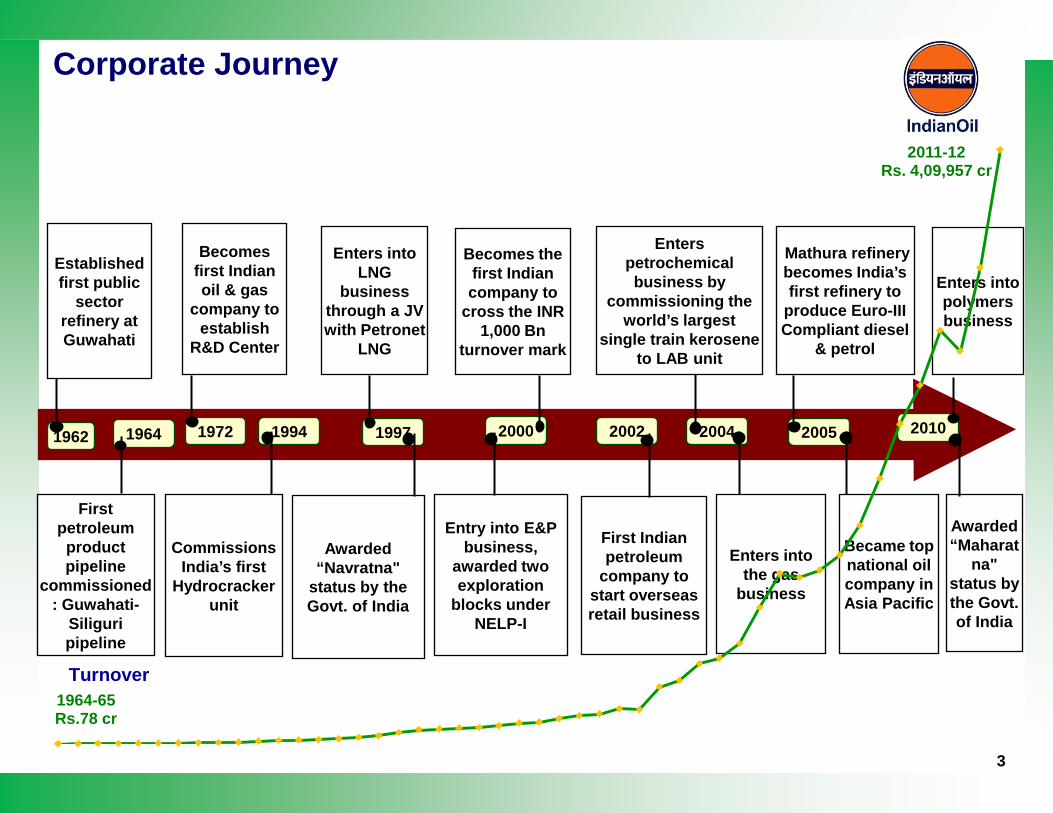

Corporate Journey

1964 20101997 2000 2002 20041972 1994

First petroleum

product pipeline

commissioned: Guwahati-

Siliguripipeline

Enters into LNG

business through a JV with Petronet

LNG

Entry into E&P business,

awarded two exploration

blocks under NELP-I

Enters into polymers business

Awarded “Maharat

na" status by the Govt. of India

Becomes first Indian oil & gas

company to establish

R&D Center

Commissions India’s first

Hydrocracker unit

Becomes the first Indian company to

cross the INR 1,000 Bn

turnover mark

First Indian petroleum

company to start overseas retail business

Enters petrochemical business by

commissioning the world’s largest

single train kerosene to LAB unit

Enters into the gas

business

2005

Mathura refinery becomes India’s first refinery to

produce Euro-III Compliant diesel

& petrol

Became top national oil company in Asia Pacific

1962

Established first public

sector refinery at Guwahati

Awarded “Navratna"

status by the Govt. of India

1964-65Rs.78 cr

2011-12Rs. 4,09,957 cr

Turnover

3

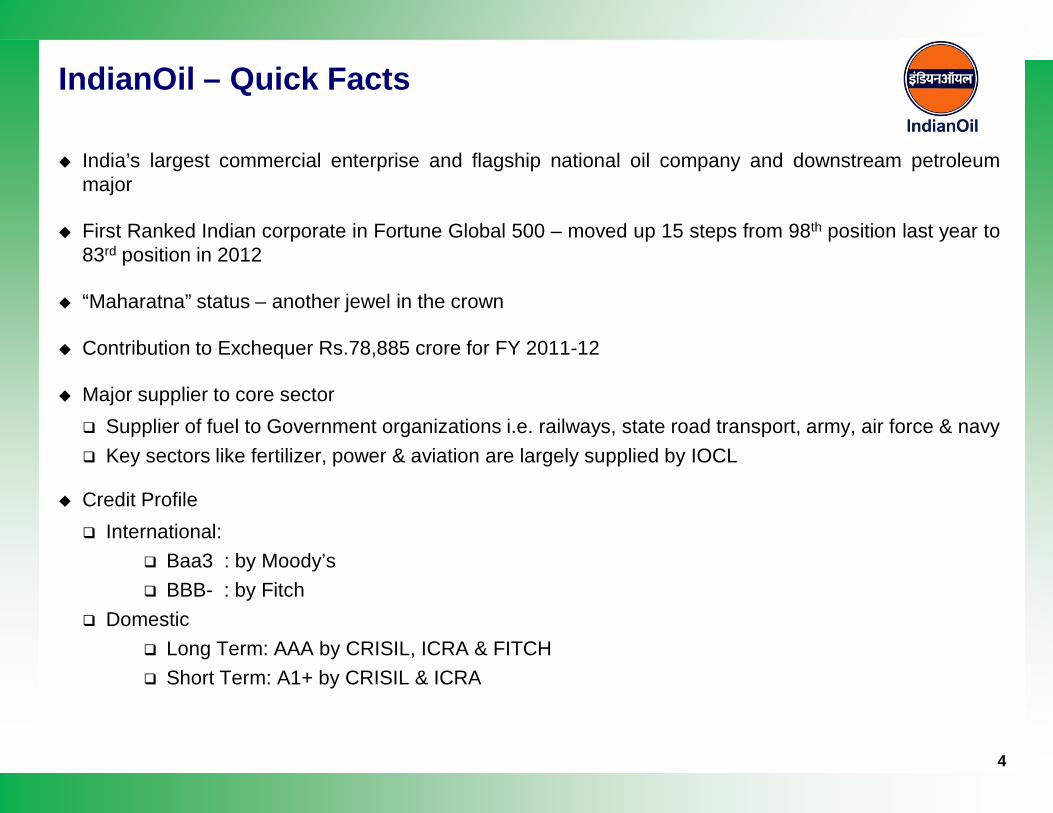

India’s largest commercial enterprise and flagship national oil company and downstream petroleummajor

First Ranked Indian corporate in Fortune Global 500 – moved up 15 steps from 98th position last year to83rd position in 2012

“Maharatna” status – another jewel in the crown

Contribution to Exchequer Rs.78,885 crore for FY 2011-12

Major supplier to core sector Supplier of fuel to Government organizations i.e. railways, state road transport, army, air force & navy Key sectors like fertilizer, power & aviation are largely supplied by IOCL

Credit Profile International:

Baa3 : by Moody’s BBB- : by Fitch

Domestic Long Term: AAA by CRISIL, ICRA & FITCH Short Term: A1+ by CRISIL & ICRA

IndianOil – Quick Facts

4

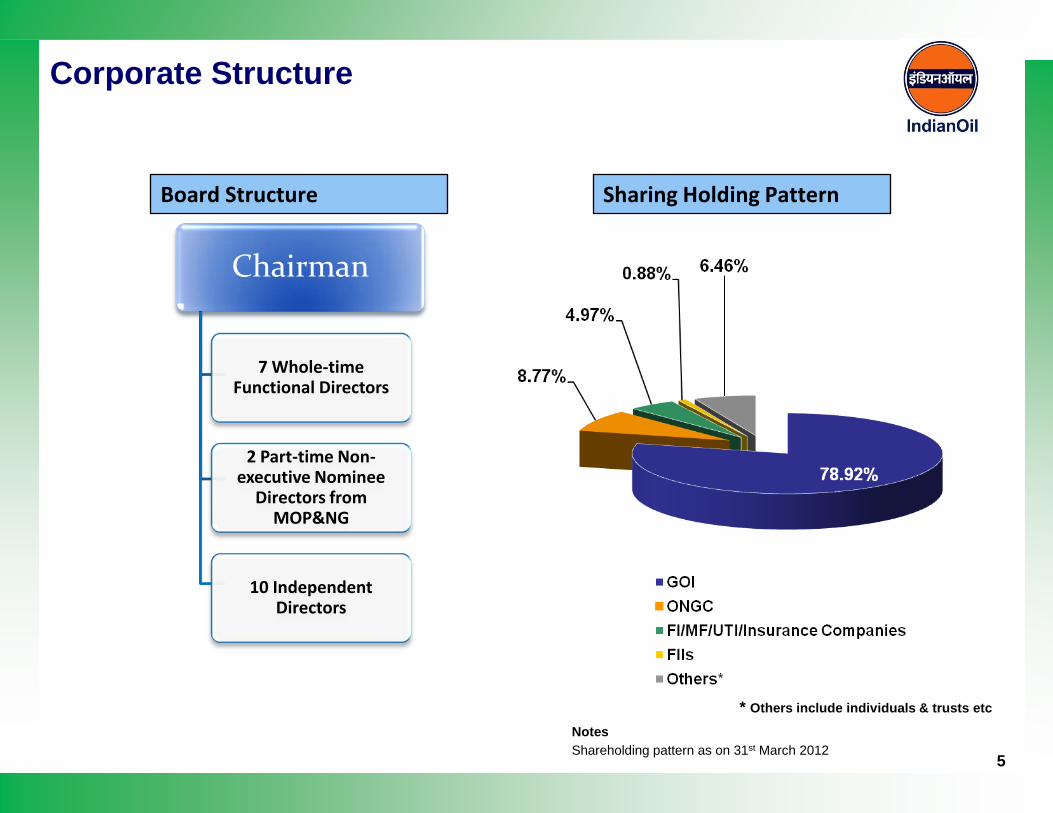

Corporate Structure

Chairman

7 Whole-time Functional Directors

2 Part-time Non-executive Nominee

Directors from MOP&NG

10 Independent Directors

Board Structure

NotesShareholding pattern as on 31st March 2012

Sharing Holding Pattern

* Others include individuals & trusts etc

5

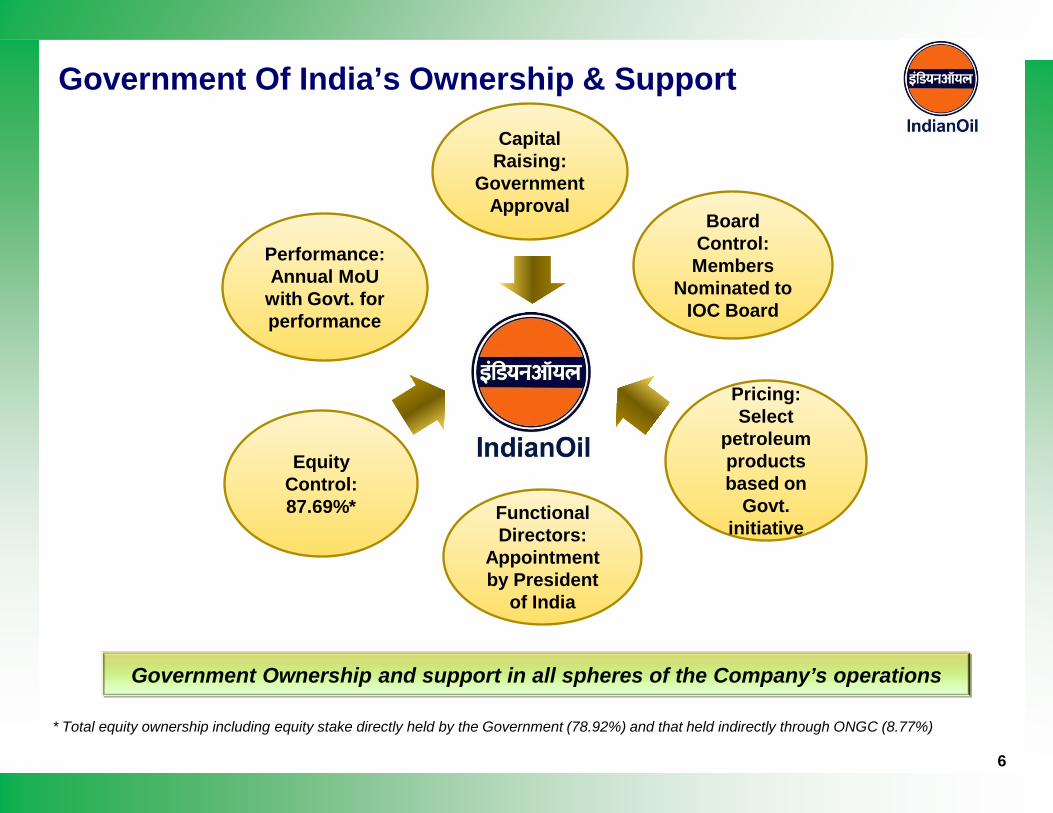

6

Government Ownership and support in all spheres of the Company’s operations

* Total equity ownership including equity stake directly held by the Government (78.92%) and that held indirectly through ONGC (8.77%)

Performance:Annual MoU

with Govt. for performance

Capital Raising:

Government Approval

Board Control:Members

Nominated to IOC Board

Pricing:Select

petroleum products based on

Govt. initiative

Functional Directors:

Appointment by President

of India

Equity Control:87.69%*

Government Of India’s Ownership & Support

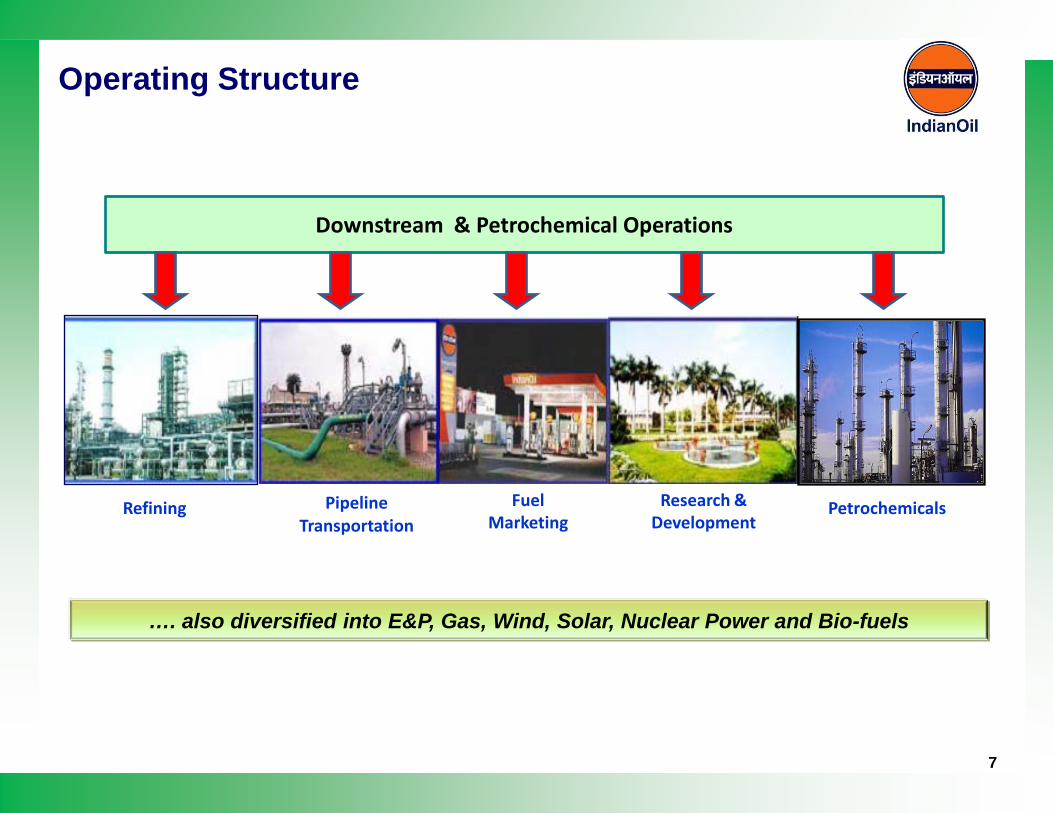

Operating Structure

…. also diversified into E&P, Gas, Wind, Solar, Nuclear Power and Bio-fuels

Downstream & Petrochemical Operations

Refining PipelineTransportation

Fuel Marketing

Research & Development

Petrochemicals

7

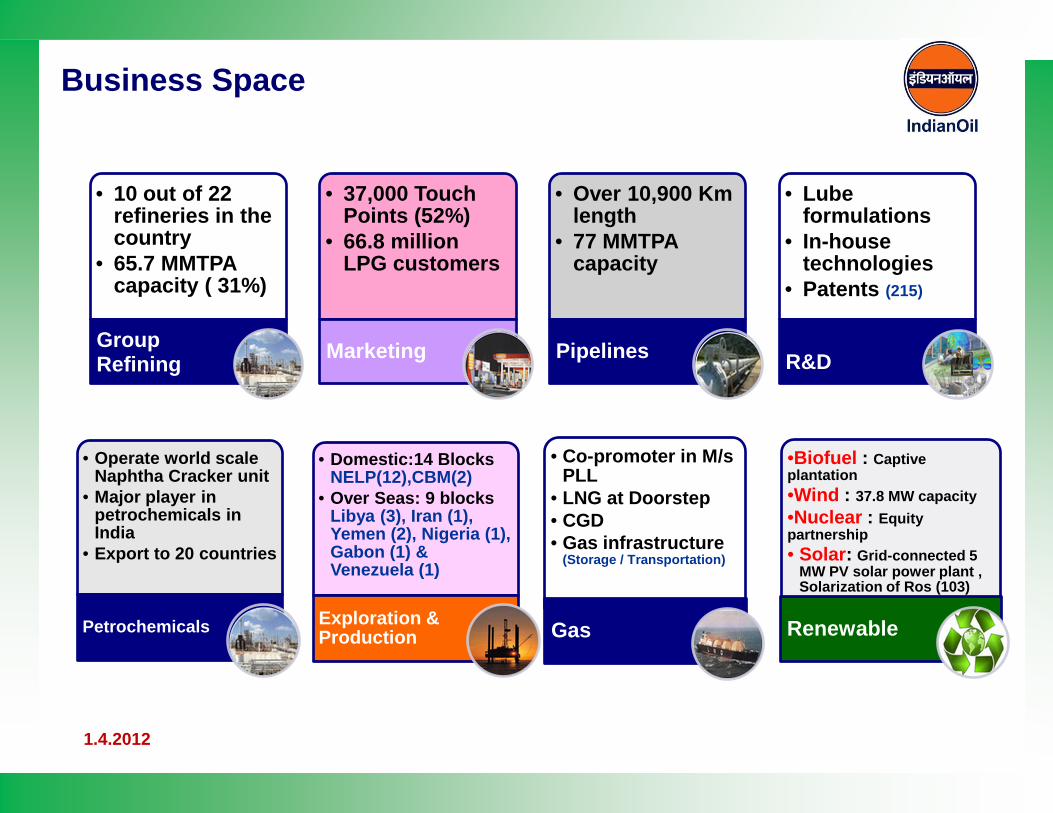

• 10 out of 22 refineries in the country

• 65.7 MMTPA capacity ( 31%)

Group Refining

• 37,000 Touch Points (52%)

• 66.8 million LPG customers

Marketing

• Over 10,900 Km length

• 77 MMTPA capacity

Pipelines

• Lube formulations

• In-house technologies

• Patents (215)

R&D

1.4.2012

• Operate world scale Naphtha Cracker unit

• Major player in petrochemicals in India

• Export to 20 countries

Petrochemicals

• Domestic:14 Blocks NELP(12),CBM(2)

• Over Seas: 9 blocks Libya (3), Iran (1), Yemen (2), Nigeria (1), Gabon (1) & Venezuela (1)

Exploration & Production

• Co-promoter in M/s PLL

• LNG at Doorstep• CGD • Gas infrastructure

(Storage / Transportation)

Gas

•Biofuel : Captive plantation•Wind : 37.8 MW capacity•Nuclear : Equity partnership• Solar: Grid-connected 5

MW PV solar power plant , Solarization of Ros (103)

Renewable

Business Space

9

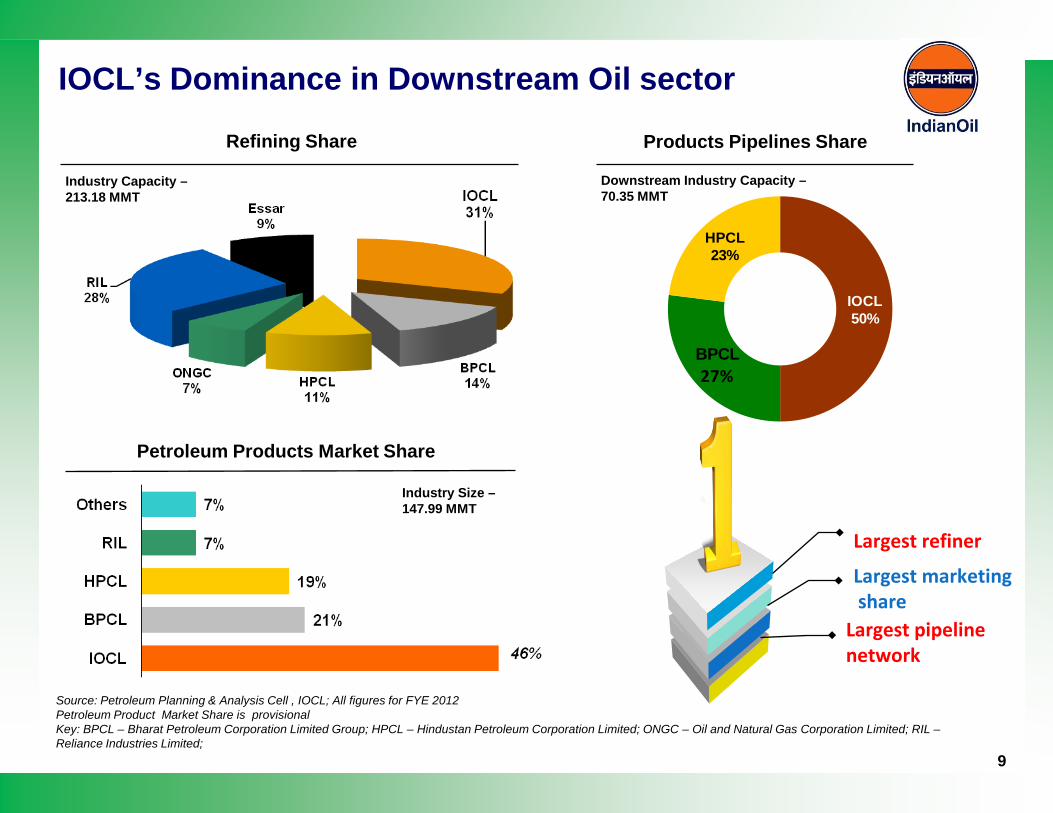

IOCL’s Dominance in Downstream Oil sector

Source: Petroleum Planning & Analysis Cell , IOCL; All figures for FYE 2012Petroleum Product Market Share is provisionalKey: BPCL – Bharat Petroleum Corporation Limited Group; HPCL – Hindustan Petroleum Corporation Limited; ONGC – Oil and Natural Gas Corporation Limited; RIL –Reliance Industries Limited;

IOCL50%

BPCL27%

HPCL23%

Refining Share Products Pipelines Share

Industry Capacity –213.18 MMT

Downstream Industry Capacity –70.35 MMT

Petroleum Products Market Share

Industry Size –147.99 MMT

Largest refiner

Largest pipeline network

Largest marketingshare

10

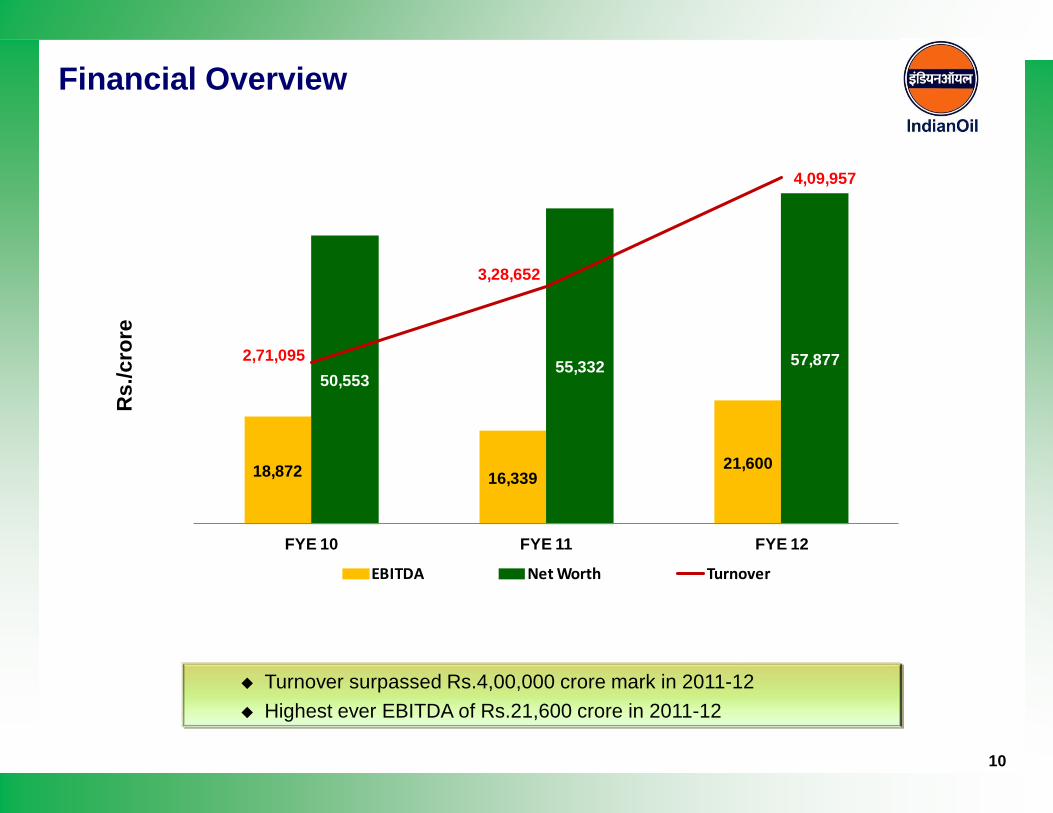

Financial OverviewR

s./c

rore

18,872 16,33921,600

50,55355,332 57,8772,71,095

3,28,652

4,09,957

FYE 10 FYE 11 FYE 12

EBITDA Net Worth Turnover

Turnover surpassed Rs.4,00,000 crore mark in 2011-12 Highest ever EBITDA of Rs.21,600 crore in 2011-12

11

IOCL – An Overview

Oil Industry In India

IOCL’s Core Operations

Strategic Initiatives

Financial Performance

Ongoing Projects

Nine Months Snapshot

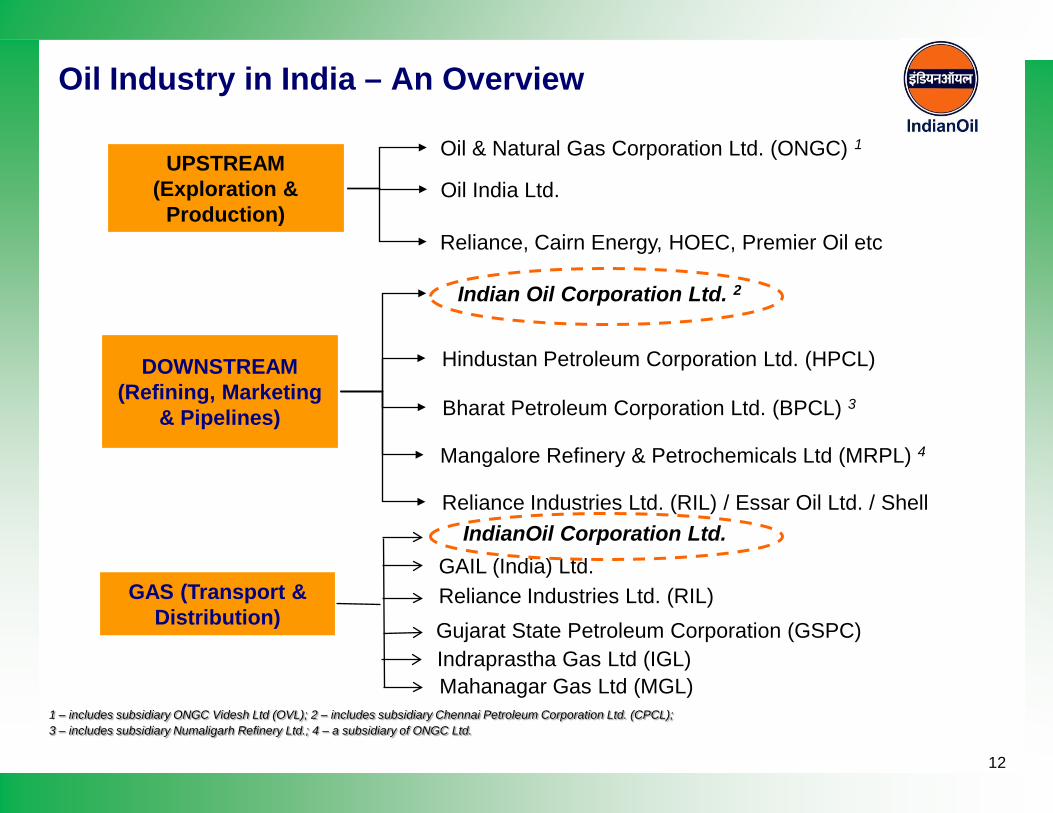

UPSTREAM (Exploration &

Production)

DOWNSTREAM (Refining, Marketing

& Pipelines)

GAS (Transport & Distribution)

Oil Industry in India – An Overview

Oil & Natural Gas Corporation Ltd. (ONGC) 1

Oil India Ltd.

Indian Oil Corporation Ltd. 2

Hindustan Petroleum Corporation Ltd. (HPCL)

Bharat Petroleum Corporation Ltd. (BPCL) 3

GAIL (India) Ltd.

Reliance, Cairn Energy, HOEC, Premier Oil etc

Reliance Industries Ltd. (RIL) / Essar Oil Ltd. / Shell

1 – includes subsidiary ONGC Videsh Ltd (OVL); 2 – includes subsidiary Chennai Petroleum Corporation Ltd. (CPCL); 3 – includes subsidiary Numaligarh Refinery Ltd.; 4 – a subsidiary of ONGC Ltd.

Mangalore Refinery & Petrochemicals Ltd (MRPL) 4

IndianOil Corporation Ltd.

Reliance Industries Ltd. (RIL)Gujarat State Petroleum Corporation (GSPC)Indraprastha Gas Ltd (IGL)Mahanagar Gas Ltd (MGL)

12

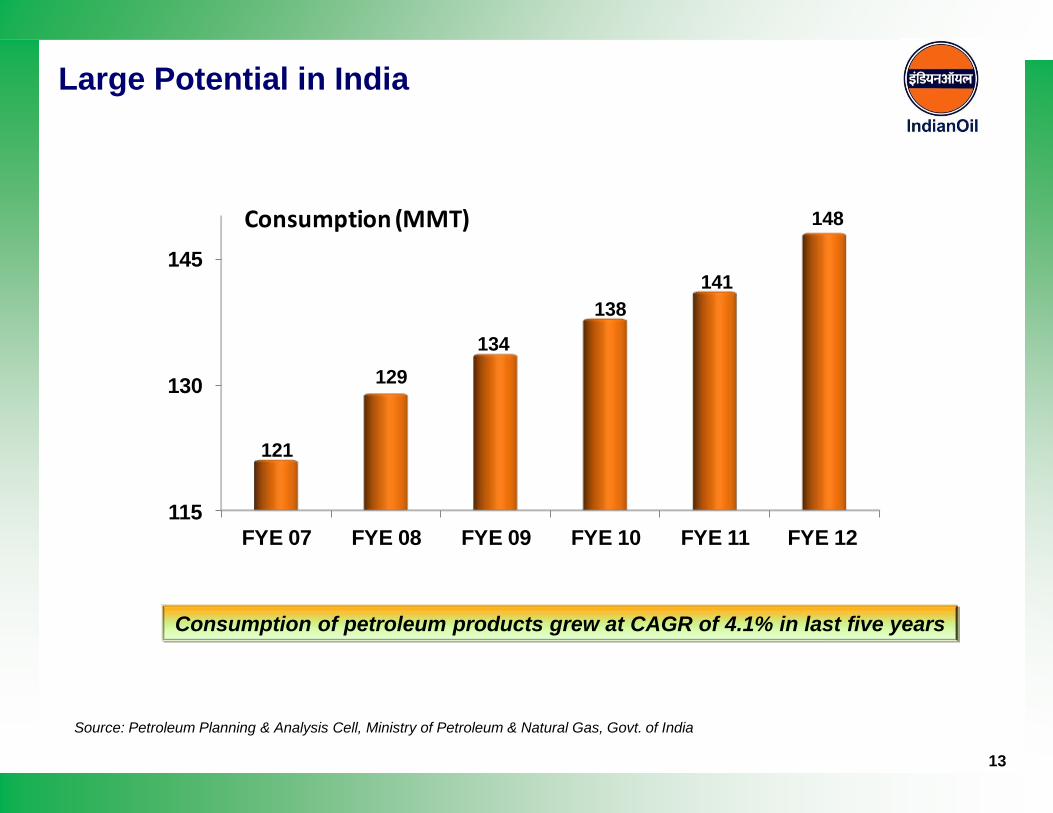

115

130

145

FYE 07 FYE 08 FYE 09 FYE 10 FYE 11 FYE 12

121

129134

138141

148Consumption (MMT)

Source: Petroleum Planning & Analysis Cell, Ministry of Petroleum & Natural Gas, Govt. of India

Consumption of petroleum products grew at CAGR of 4.1% in last five years

Large Potential in India

13

14

IOCL – An Overview

Oil Industry In India

IOCL’s Core Operations

Strategic Initiatives

Financial Performance

Ongoing Projects

Nine Months Snapshot

15

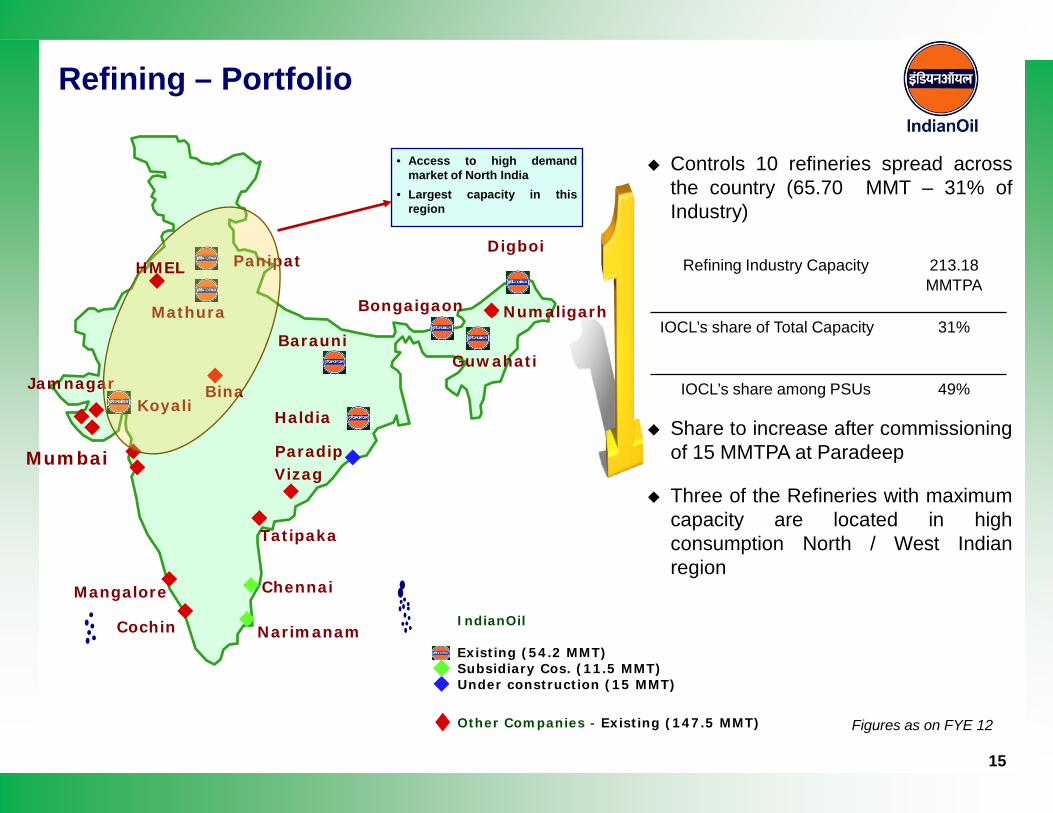

Refining – Portfolio

Controls 10 refineries spread acrossthe country (65.70 MMT – 31% ofIndustry)

Share to increase after commissioningof 15 MMTPA at Paradeep

Three of the Refineries with maximumcapacity are located in highconsumption North / West Indianregion

Figures as on FYE 12

Refining Industry Capacity 213.18 MMTPA

IOCL’s share of Total Capacity 31%

IOCL’s share among PSUs 49%

MumbaiVizag

Chennai

Cochin Narimanam

Bongaigaon

Mangalore

Panipat

Guwahati

Haldia

Barauni

Mathura

Koyali

Digboi

Jamnagar

Tatipaka

Numaligarh

IndianOil

Existing (54.2 MMT) Subsidiary Cos. (11.5 MMT) Under construction (15 MMT)

Other Companies - Existing (147.5 MMT)

Bina

Paradip

• Access to high demandmarket of North India

• Largest capacity in thisregion

HMEL

50.7

53.0

55.6

FYE 10 FYE 11 FYE 12

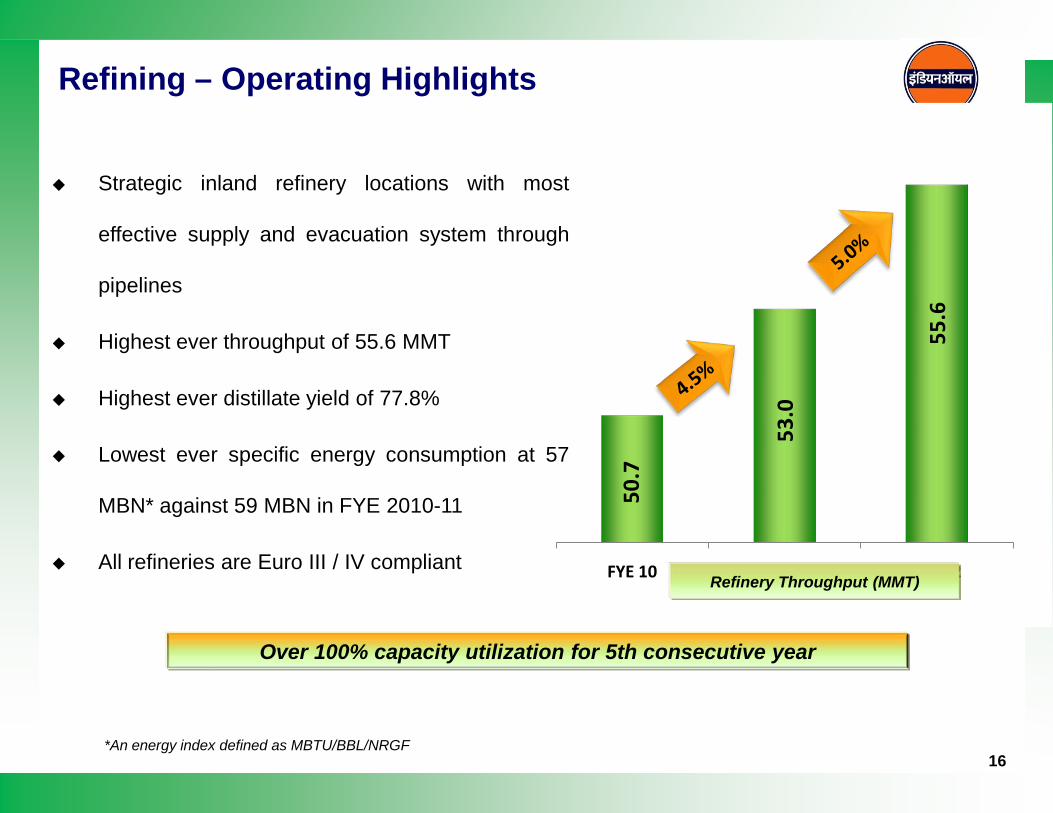

Strategic inland refinery locations with most

effective supply and evacuation system through

pipelines

Highest ever throughput of 55.6 MMT

Highest ever distillate yield of 77.8%

Lowest ever specific energy consumption at 57

MBN* against 59 MBN in FYE 2010-11

All refineries are Euro III / IV compliantRefinery Throughput (MMT)

Refining – Operating Highlights

*An energy index defined as MBTU/BBL/NRGF16

Over 100% capacity utilization for 5th consecutive year

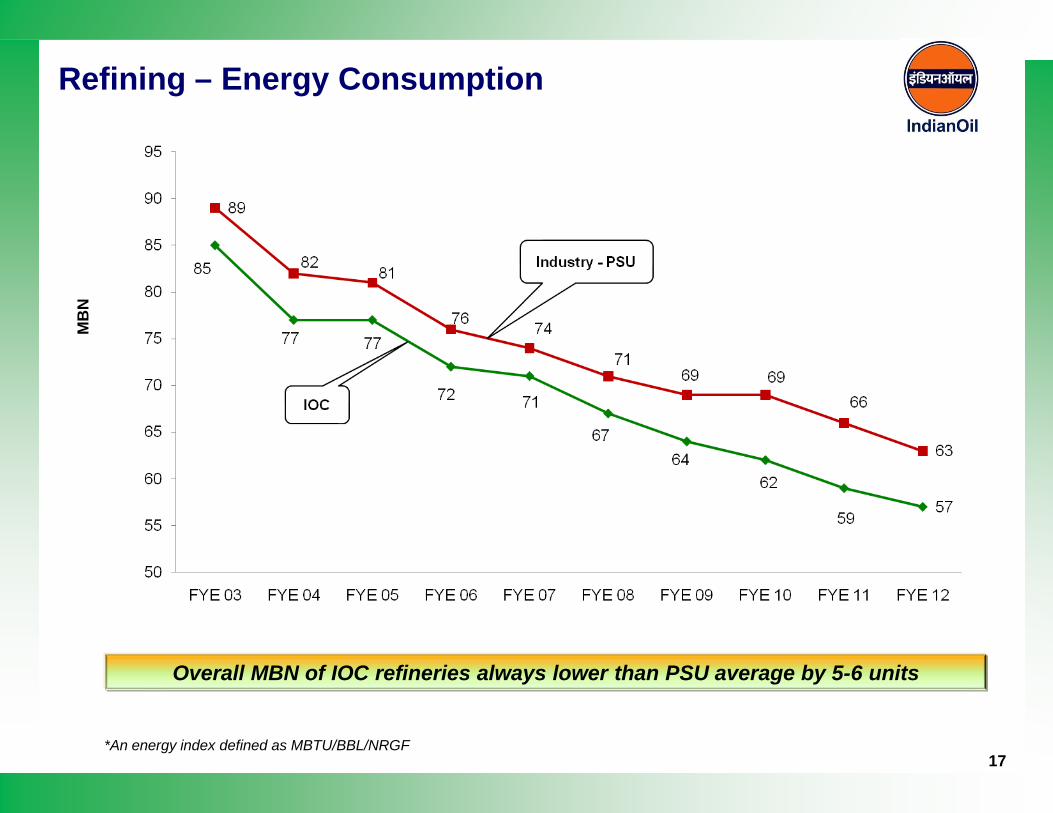

Refining – Energy Consumption

*An energy index defined as MBTU/BBL/NRGF17

Overall MBN of IOC refineries always lower than PSU average by 5-6 units

MB

N

18

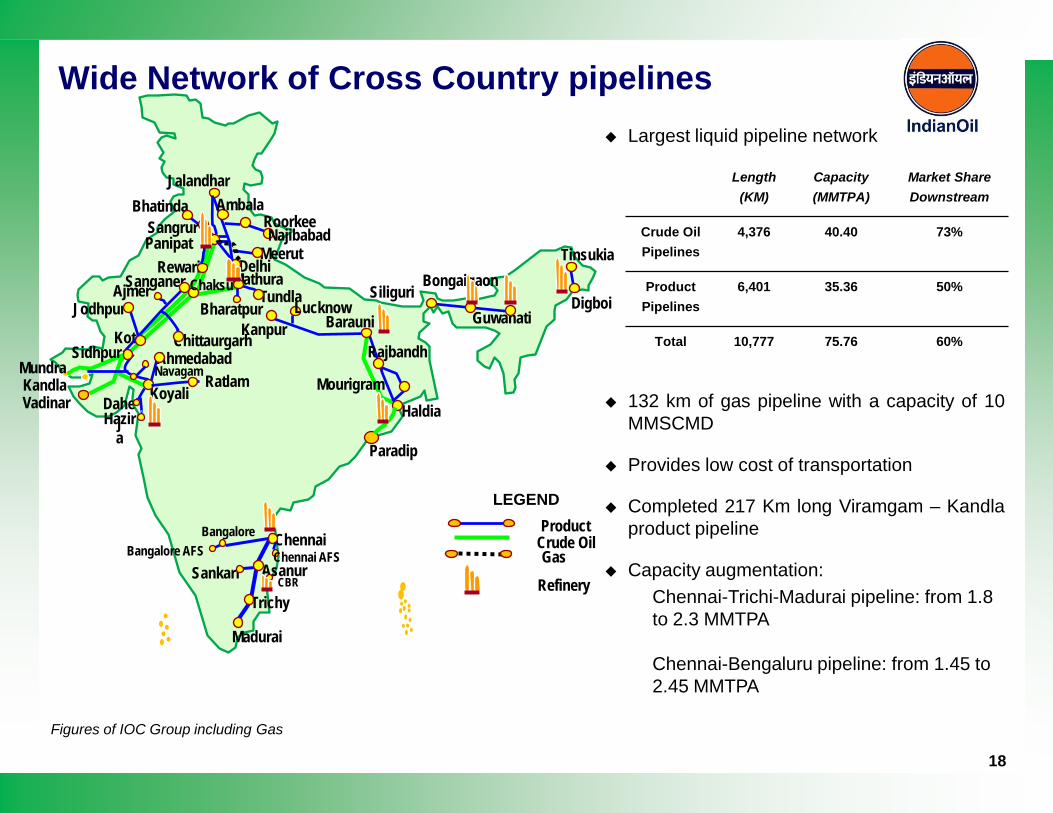

Largest liquid pipeline network

132 km of gas pipeline with a capacity of 10MMSCMD

Provides low cost of transportation

Completed 217 Km long Viramgam – Kandlaproduct pipeline

Capacity augmentation:Chennai-Trichi-Madurai pipeline: from 1.8 to 2.3 MMTPA

Chennai-Bengaluru pipeline: from 1.45 to 2.45 MMTPA

Wide Network of Cross Country pipelines

Figures of IOC Group including Gas

Length (KM)

Capacity (MMTPA)

Market Share Downstream

Crude Oil Pipelines

4,376 40.40 73%

Product Pipelines

6,401 35.36 50%

Total 10,777 75.76 60%

KandlaVadinar

Mundra

Chaksu

Guwahati

BongaigaonSiliguri Digboi

Tinsukia

Jalandhar

DelhiMeerut

Tundla

NajibabadRoorkee

Ambala

Mathura

KotSidhpur Ahmedabad

Jodhpur

Navagam

SanganerAjmer

Dahej

Chittaurgarh

Koyali

BhatindaSangrurPanipat

Rewari

Haldia

BarauniKanpurLucknow

Mourigram

Rajbandh

Chennai

Sankari Asanur

Trichy

Madurai

CBR

BangaloreBangalore AFS

Paradip

Ratlam

Chennai AFS

Bharatpur

Hazira

ProductLEGEND

Crude Oil

Refinery

Gas

FYE 10 FYE 11 FYE 12

23.0 26.0 28.0

42.042.5

47.5Crude

Product

Surpassing performance continues

Highest ever throughput of 75.5 MMT achieved by IOCL’s pipelines in FYE 12

Highest ever capacity utilization of 118% for crude oil pipelines

Pipelines Throughput (MMT)

Pipelines Operating highlights

19

65.068.5

75.5

20

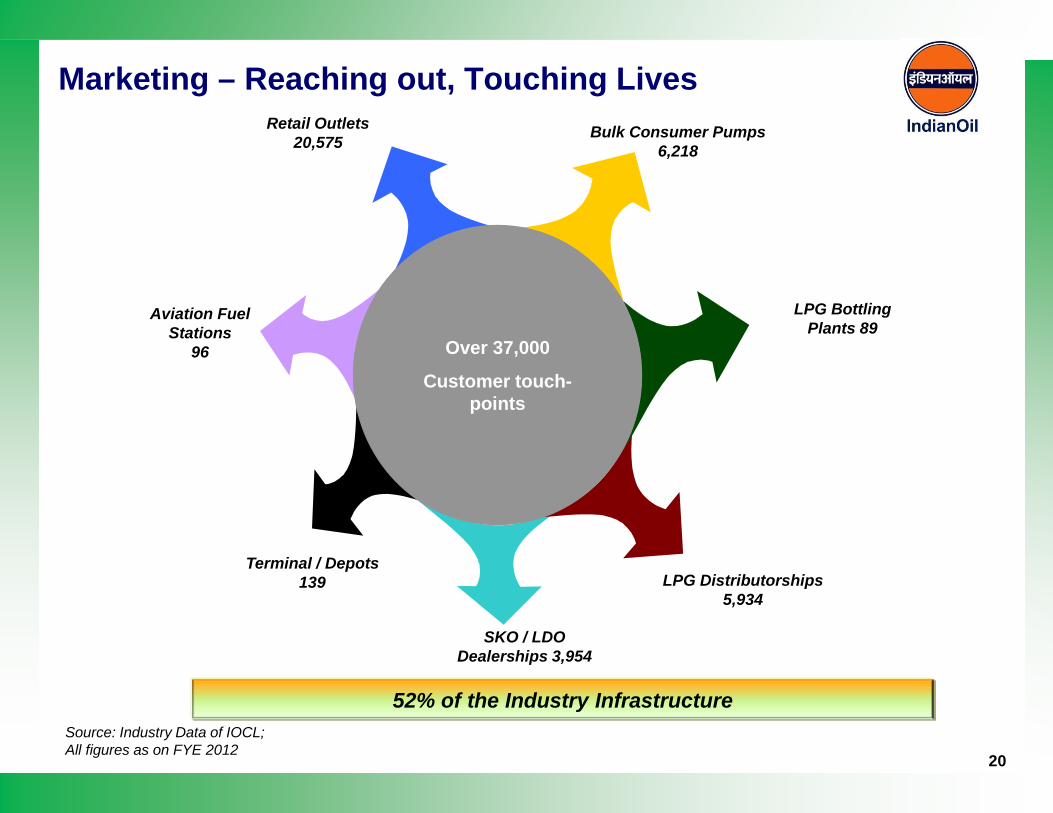

Marketing – Reaching out, Touching Lives

52% of the Industry Infrastructure

Over 37,000

Customer touch-points

LPG Bottling Plants 89

LPG Distributorships 5,934

SKO / LDO Dealerships 3,954

Terminal / Depots 139

Aviation Fuel Stations

96

Retail Outlets20,575 Bulk Consumer Pumps

6,218

Source: Industry Data of IOCL; All figures as on FYE 2012

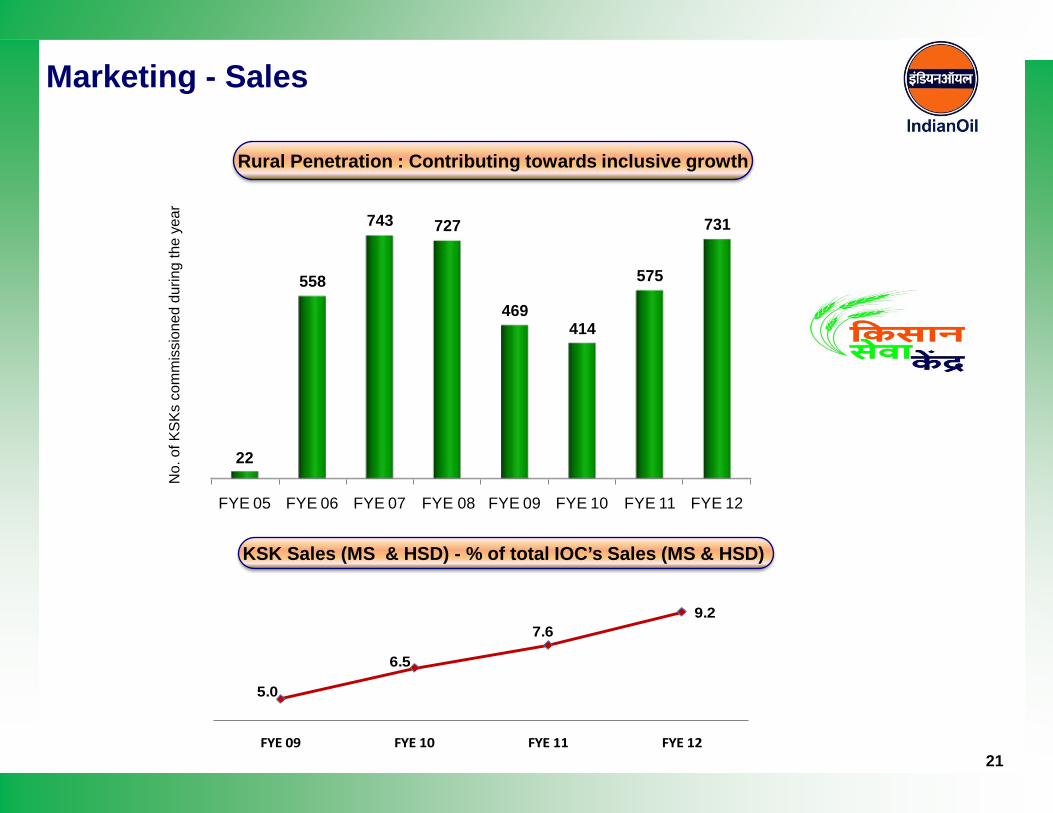

Marketing - Sales

Rural Penetration : Contributing towards inclusive growthN

o. o

f KSK

s co

mm

issi

oned

dur

ing

the

year

KSK Sales (MS & HSD) - % of total IOC’s Sales (MS & HSD)

FYE 05 FYE 06 FYE 07 FYE 08 FYE 09 FYE 10 FYE 11 FYE 12

22

558

743 727

469414

575

731

5.0

6.5

7.69.2

FYE 09 FYE 10 FYE 11 FYE 1221

22

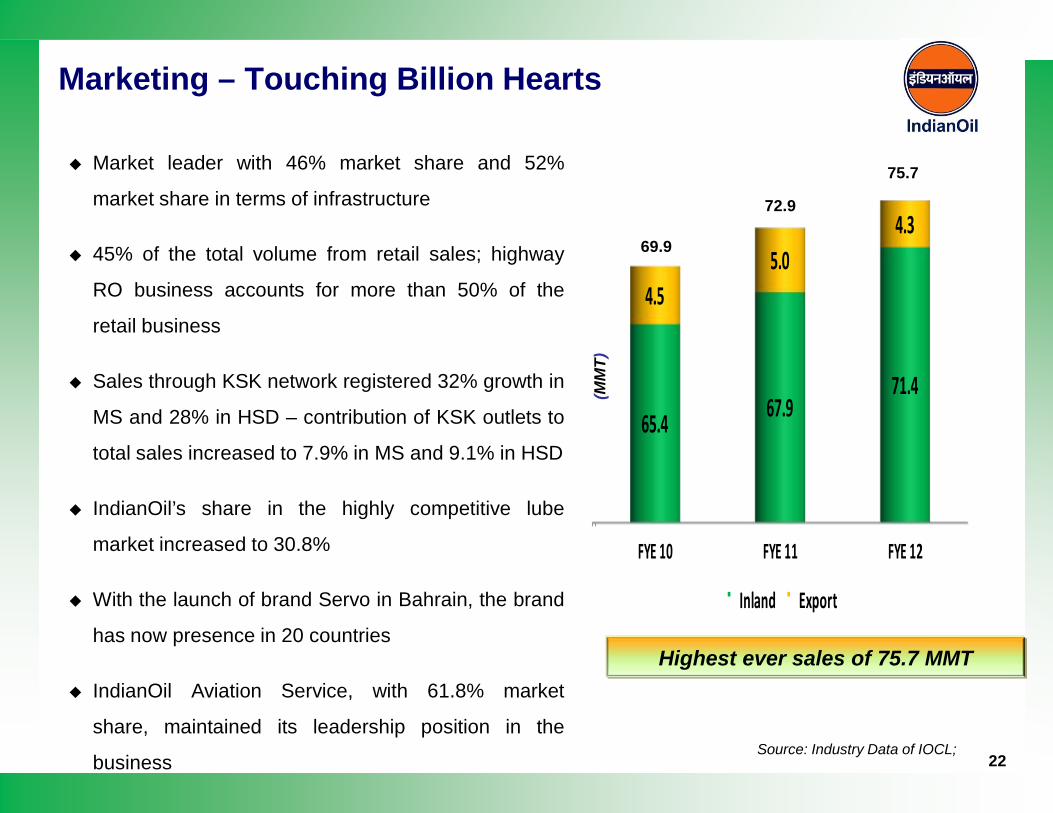

Marketing – Touching Billion Hearts

Market leader with 46% market share and 52%

market share in terms of infrastructure

45% of the total volume from retail sales; highway

RO business accounts for more than 50% of the

retail business

Sales through KSK network registered 32% growth in

MS and 28% in HSD – contribution of KSK outlets to

total sales increased to 7.9% in MS and 9.1% in HSD

IndianOil’s share in the highly competitive lube

market increased to 30.8%

With the launch of brand Servo in Bahrain, the brand

has now presence in 20 countries

IndianOil Aviation Service, with 61.8% market

share, maintained its leadership position in the

businessSource: Industry Data of IOCL;

FYE 10 FYE 11 FYE 12

65.467.9

71.4

4.55.0

4.3

Inland Export

Highest ever sales of 75.7 MMT

69.9

72.9

(MM

T)

75.7

23

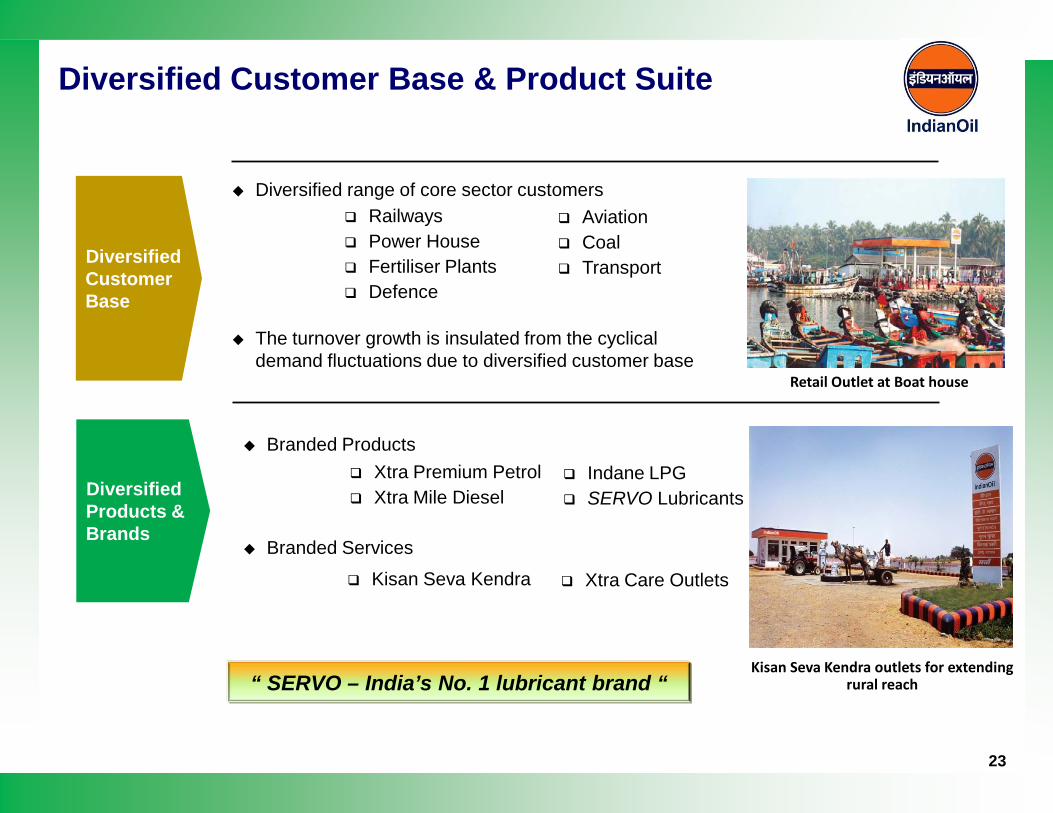

Branded Products

Branded Services

Diversified range of core sector customers

The turnover growth is insulated from the cyclical demand fluctuations due to diversified customer base

Diversified Customer Base

Diversified Products & Brands

Xtra Premium Petrol Xtra Mile Diesel

Indane LPG SERVO Lubricants

Diversified Customer Base & Product Suite

Railways Power House Fertiliser Plants Defence

Aviation Coal Transport

Kisan Seva Kendra Xtra Care Outlets

“ SERVO – India’s No. 1 lubricant brand “Kisan Seva Kendra outlets for extending

rural reach

Retail Outlet at Boat house

24

Commercialization of technologies

INDMAX :For maximisation of LPG & light distillates from Refinery Residue.

Marine Oils : One of six companies to have developed “Original Equipment

Manufacturer Approved Marine Technology Equipment”

Needle Coke :One of three companies in world that possess technology to make high

value needle coke

Diesel Hydrotreating (DHDT) and Light Naphtha Isomerisation units commissioned at

Bongaigaon Refinery to produce Bharat Stage IV complaint Diesel & Euro III/IV MS

Widening horizons

New petrochemical and polymer labs fully functional

MOU with the Department of Bio-Technolodgy to set up “Advanced Bio-energyResearch Centre”

Commissioned fluidized bed gasification pilot

R&D Providing The Cutting Edge

25

Lubricants

154 product formulations developed, 108 commercialized, 56 approvals obtained fromuser Industries / OEMs

In a first overseas business gain, Mauritius Shipping Corporation adopted indigenously

developed Servo Marine grades

Patents

Six patents granted during the year

Details of active patent

Central Development Center at Faridabad

India USA Others Total

119 46 50 215

Lubes Refinery Others Total

42 101 72 215

R&D Providing The Cutting Edge

All figures as on FYE 2012

26

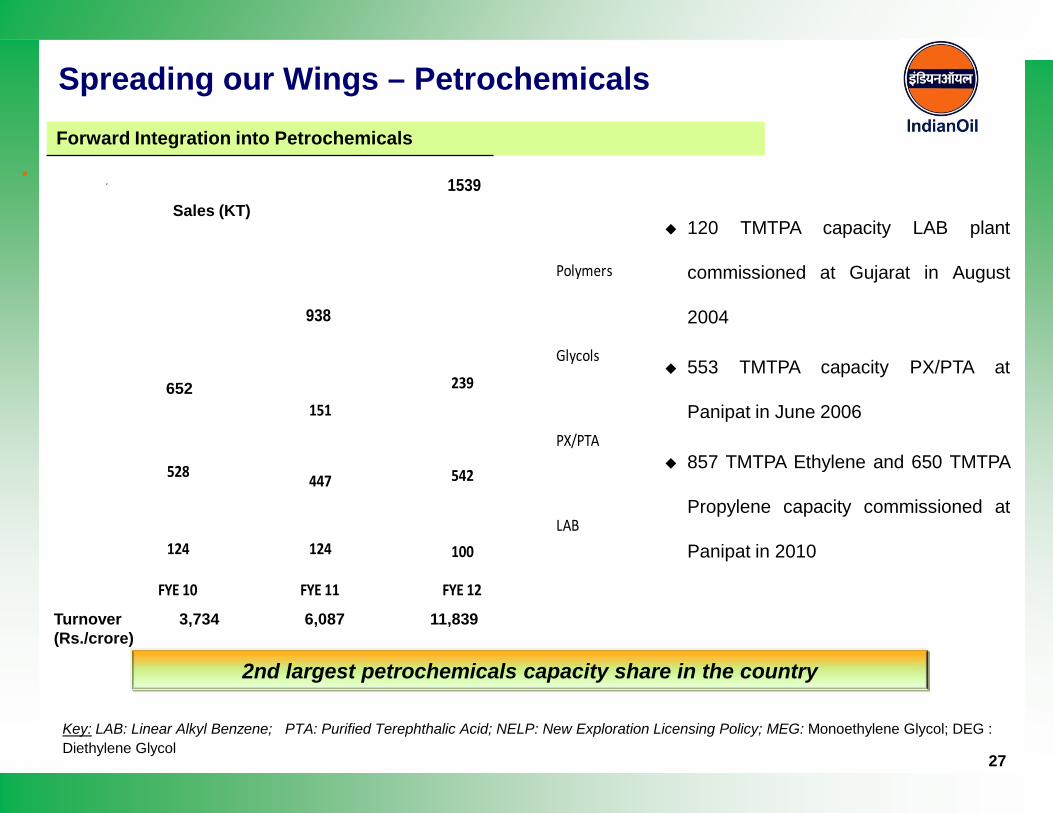

IOCL – An Overview

Oil Industry In India

IOCL’s Core Operations

Strategic Initiatives

Financial Performance

Ongoing Projects

Nine Months Snapshot

FYE 10 FYE 11 FYE 12

124 124 100

528 447 542

151

239216

658 Polymers

Glycols

PX/PTA

LAB

938

1539

27

Spreading our Wings – PetrochemicalsForward Integration into Petrochemicals

Key: LAB: Linear Alkyl Benzene; PTA: Purified Terephthalic Acid; NELP: New Exploration Licensing Policy; MEG: Monoethylene Glycol; DEG : Diethylene Glycol

120 TMTPA capacity LAB plant

commissioned at Gujarat in August

2004

553 TMTPA capacity PX/PTA at

Panipat in June 2006

857 TMTPA Ethylene and 650 TMTPA

Propylene capacity commissioned at

Panipat in 2010

Turnover (Rs./crore)

3,734 6,087 11,839

2nd largest petrochemicals capacity share in the country

652

Sales (KT)

28

Spreading our Wings – E&P

Domestic Exploration Blocks

NELP – 14 blocks with ONGC / OIL / GAIL / GSPC / Petrogas / HPCL /

HOEC / AWEL (15-100% participating interest)

Coal Bed Methane – 2 blocks with ONGC (20% participating interest)

International Exploration Blocks

Total 10 blocks- Libya(3), Iran (1), Yemen(2) , Nigera(1), Gabon (1) &

Venezuela (1), USA (1)

Backward Integration into E&P

Key: NELP: New Exploration Licensing Policy

29

Diversification to Other Energy Sources

Gas sales of 1.72 MMT in FYE 2012, Turnover grew by 4.9% against previous year

Operating City Gas Distribution (CGD) network with JV company Green Gas Ltd in Agra &

Lucknow

Consortium with Adani Gas Ltd to develop CGD network on pan India basis

Setting up 5 MMTPA LNG regasification and storage terminal at Ennore

Formed a consortium with Gujarat State Petronet Ltd, BPCL & HPCL to build three cross-

country pipeline through a joint venture; IOC’s share at 26%

On 6th April 2011 formed JV with Nuclear Power Corporation of India to establish (700*2)

MW nuclear plant at Rawatbhatta, Rajasthan. IOC’s Share 26% (Rs.961 crore)

NUCLEAR

GAS

30

Diversification to Other Energy Sources

Wind Power, Biofuels & Solar Energy

Commissioned 21MW plant at Kachchh, Gujarat in Jan 09

Second plant of 48.3 MW capacity consisting of 23 windmills under implementation in Andhra

Pradesh; out of 23, 8 windmills commissioned in March’12

Chhattisgarh Project: Subsidiary with Chhattisgarh Renewable Development Authority for

plantation of Jatropha in 30,000 hectare wasteland

Madhya Pradesh Project: IOC alloted 2,000 hectare wasteland for Jatropha plantation

UP Project: Formed LLP with Ruchi Soya Industries Limited with objective of Jatropha

plantation on 50,000 hectare wasteland

Commissioned 5 MW solar plant in Rajasthan

Solar plants at Retail Outlets / PLHO

Solar Lanterns launched in IOC’s state offices

SOLAR

Wind Power

BIOFUELS

• Aviation, terminaling and retail• Leader in aviation• 24,000 Metric Ton capacity storage

Terminal at Port Louis• 18 retail outlets

IndianOil Mauritius

Ltd.

(100% )

• Storage, terminaling and retail business• 157 retail outlets• 1/3rd share in Ceylon Petroleum Storage

Terminals Ltd• Listed on Colombo Stock Exchange

Lanka IOC Ltd.

(75.1% )

• Marketing of SERVO lube & petroleum products in Middle East, Africa and CIS countries.

• Exports finished lubes to Oman, Yemen , Bahrain, UAE and Nepal.

IOC Middle East FZE

(100% )

Overseas Downstream Marketing: Leveraging core competence

Overseas Presence

32

IOCL – An Overview

Oil Industry In India

IOCL’s Core Operations

Strategic Initiatives

Financial Performance

Ongoing Projects

Nine Months Snapshot

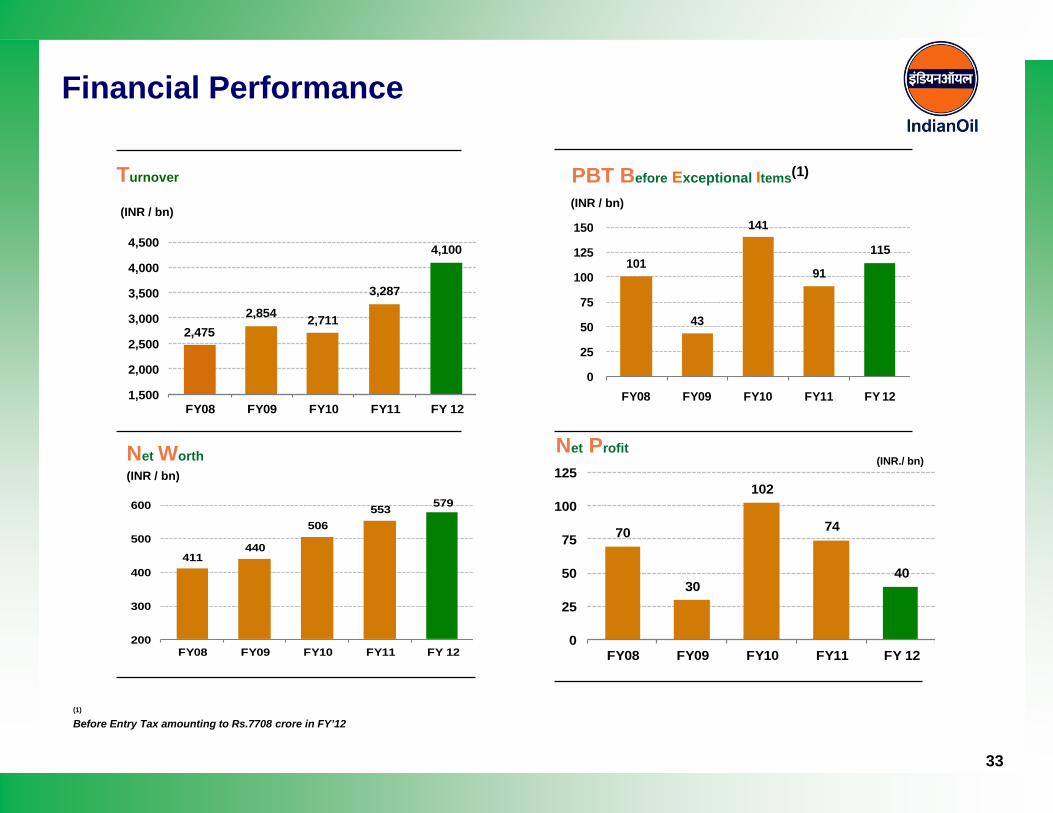

Financial Performance

Net Profit

Turnover

Net Worth

(INR / bn)(INR / bn)

(INR / bn)(INR./ bn)

411440

506553 579

200

300

400

500

600

FY08 FY09 FY10 FY11 FY 12

2,4752,854 2,711

3,287

4,100

1,500

2,000

2,500

3,000

3,500

4,000

4,500

FY08 FY09 FY10 FY11 FY 12

70

30

102

74

40

0

25

50

75

100

125

FY08 FY09 FY10 FY11 FY 12

101

43

141

91

115

0

25

50

75

100

125

150

FY08 FY09 FY10 FY11 FY 12

PBT Before Exceptional Items(1)

(1)

Before Entry Tax amounting to Rs.7708 crore in FY’12

33

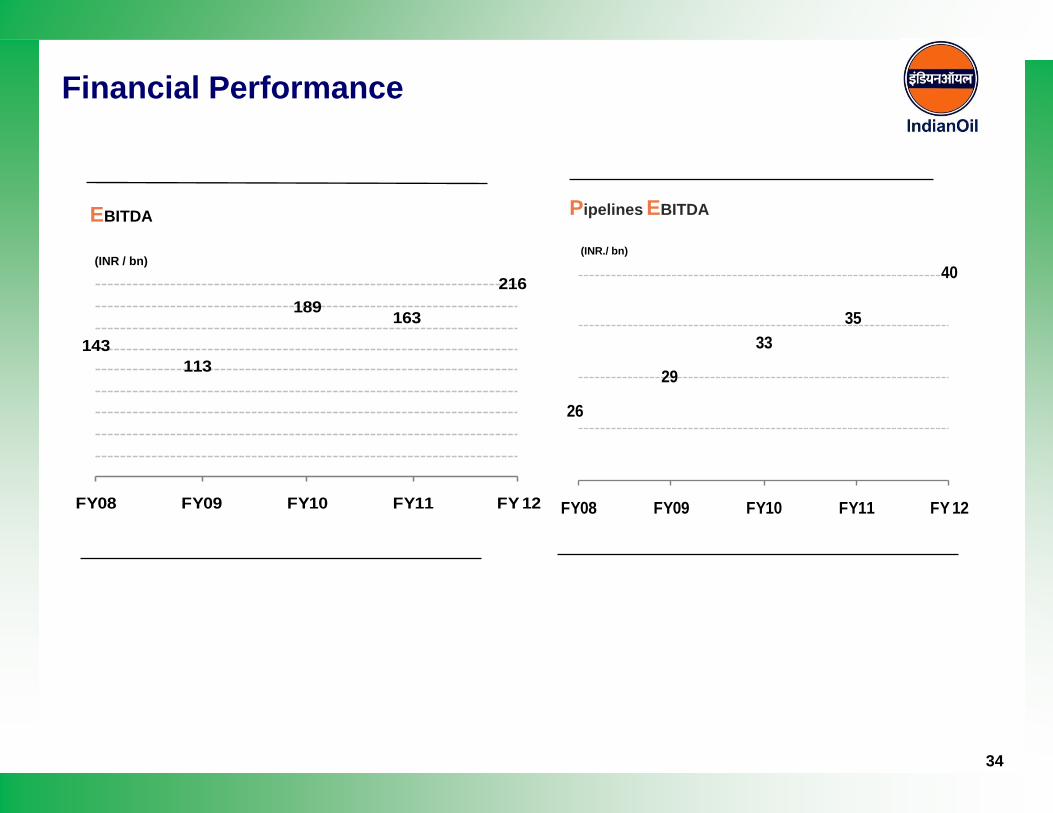

Financial Performance

EBITDA

(INR / bn)

Pipelines EBITDA

26

29

3335

40

FY08 FY09 FY10 FY11 FY 12

(INR./ bn)

143113

189 163

216

FY08 FY09 FY10 FY11 FY 12

34

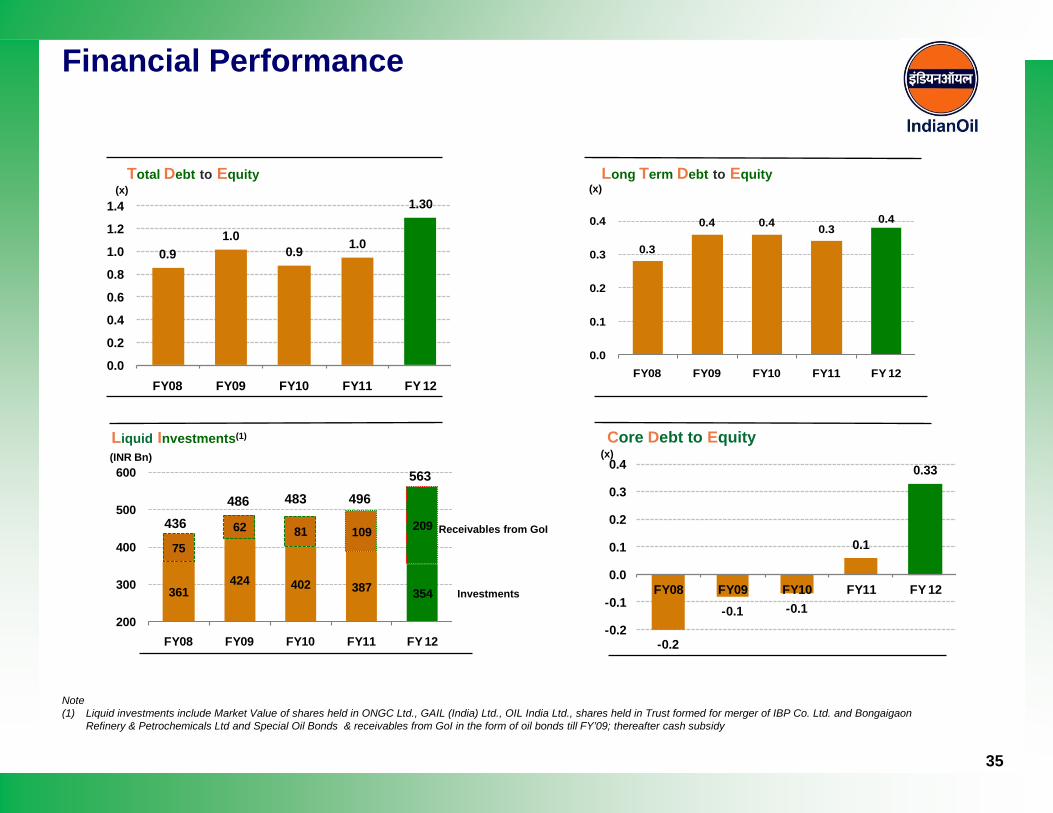

Financial Performance

361424 402 387 354

7562 81 109 209

200

300

400

500

600

FY08 FY09 FY10 FY11 FY 12

Liquid Investments(1)

(INR Bn)

(x)

0.3

0.4 0.4 0.30.4

0.0

0.1

0.2

0.3

0.4

FY08 FY09 FY10 FY11 FY 12

0.91.0

0.9 1.0

1.30

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

FY08 FY09 FY10 FY11 FY 12

Total Debt to Equity

Core Debt to Equity(x)

Note (1) Liquid investments include Market Value of shares held in ONGC Ltd., GAIL (India) Ltd., OIL India Ltd., shares held in Trust formed for merger of IBP Co. Ltd. and Bongaigaon

Refinery & Petrochemicals Ltd and Special Oil Bonds & receivables from GoI in the form of oil bonds till FY’09; thereafter cash subsidy

Long Term Debt to Equity

Receivables from GoI

Investments

436486 483 496

563

(x)

-0.2

-0.1 -0.1

0.1

0.33

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

FY08 FY09 FY10 FY11 FY 12

35

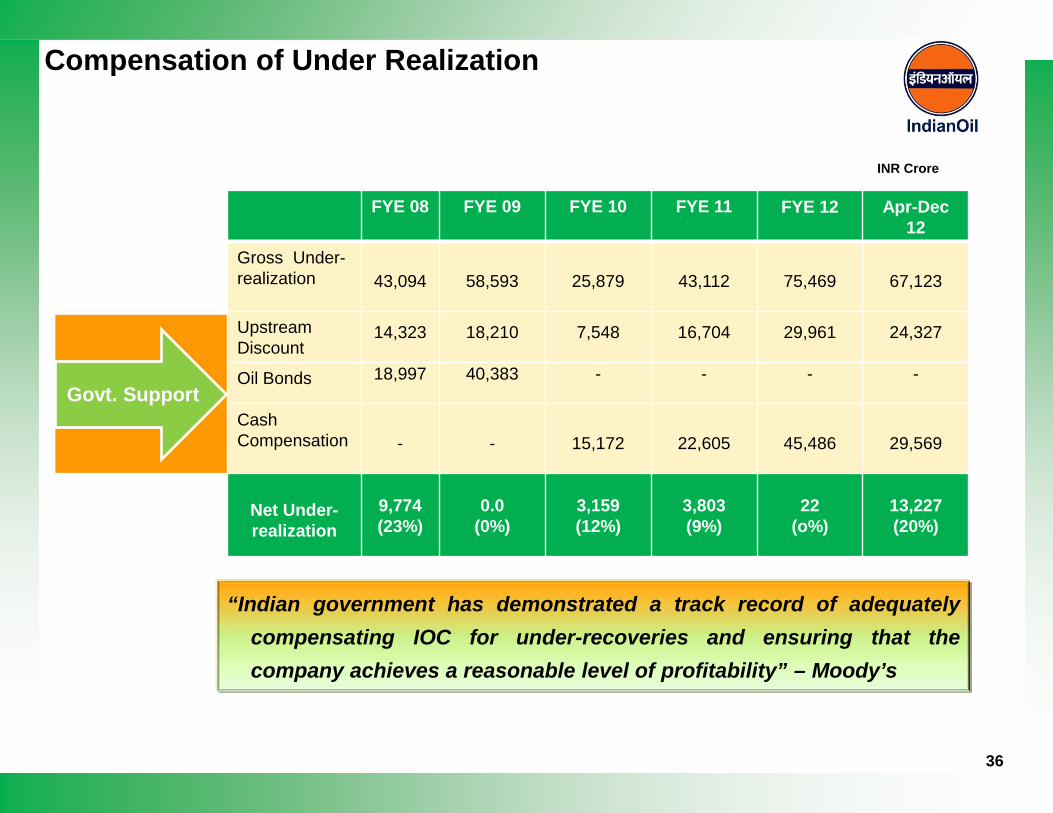

INR Crore

Compensation of Under Realization

“Indian government has demonstrated a track record of adequatelycompensating IOC for under-recoveries and ensuring that thecompany achieves a reasonable level of profitability” – Moody’s

FYE 08 FYE 09 FYE 10 FYE 11 FYE 12 Apr-Dec12

Gross Under-realization 43,094 58,593 25,879 43,112 75,469 67,123

Upstream Discount

14,323 18,210 7,548 16,704 29,961 24,327

Oil Bonds 18,997 40,383 - - - -

CashCompensation - - 15,172 22,605 45,486 29,569

Net Under-realization

9,774 (23%)

0.0 (0%)

3,159 (12%)

3,803 (9%)

22(o%)

13,227(20%)

Govt. Support

36

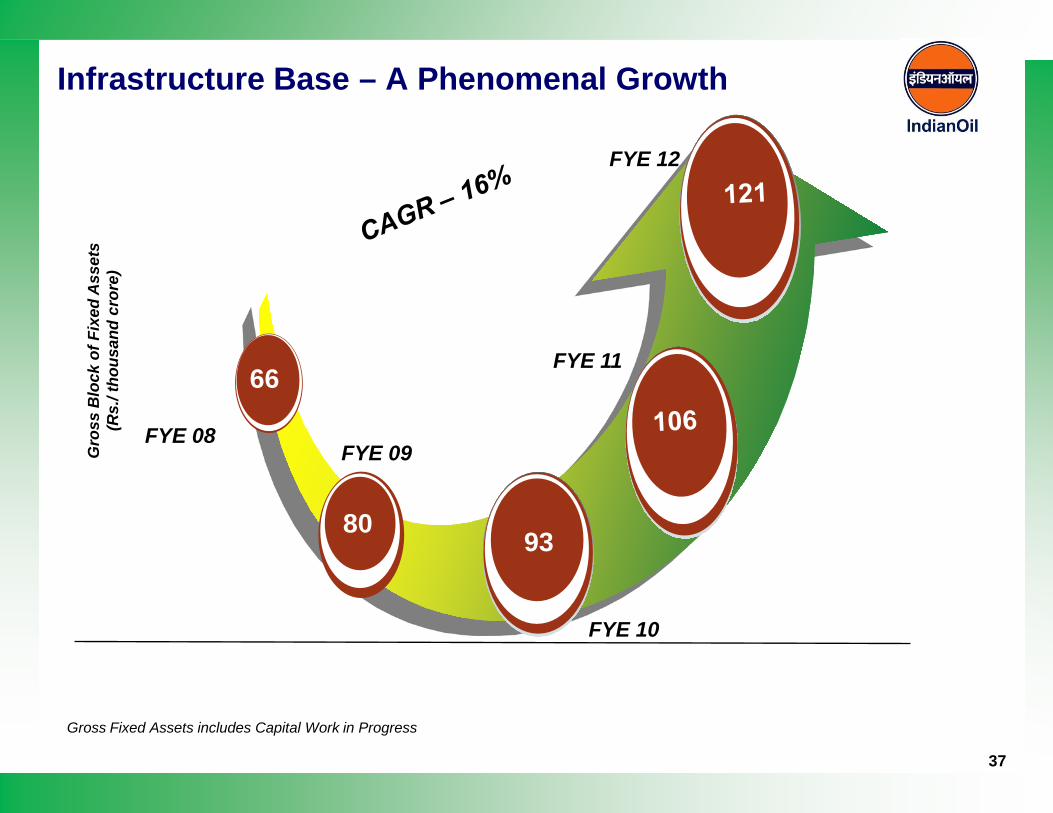

Infrastructure Base – A Phenomenal GrowthG

ross

Blo

ck o

f Fix

ed A

sset

s

(Rs.

/ tho

usan

d cr

ore)

Gross Fixed Assets includes Capital Work in Progress

FYE 08FYE 09

80

66

FYE 10

93

FYE 11

37

FYE 12

38

IOCL – An Overview

Oil Industry In India

IOCL’s Core Operations

Strategic Initiatives

Financial Performance

Nine Months Snapshot

Ongoing Projects

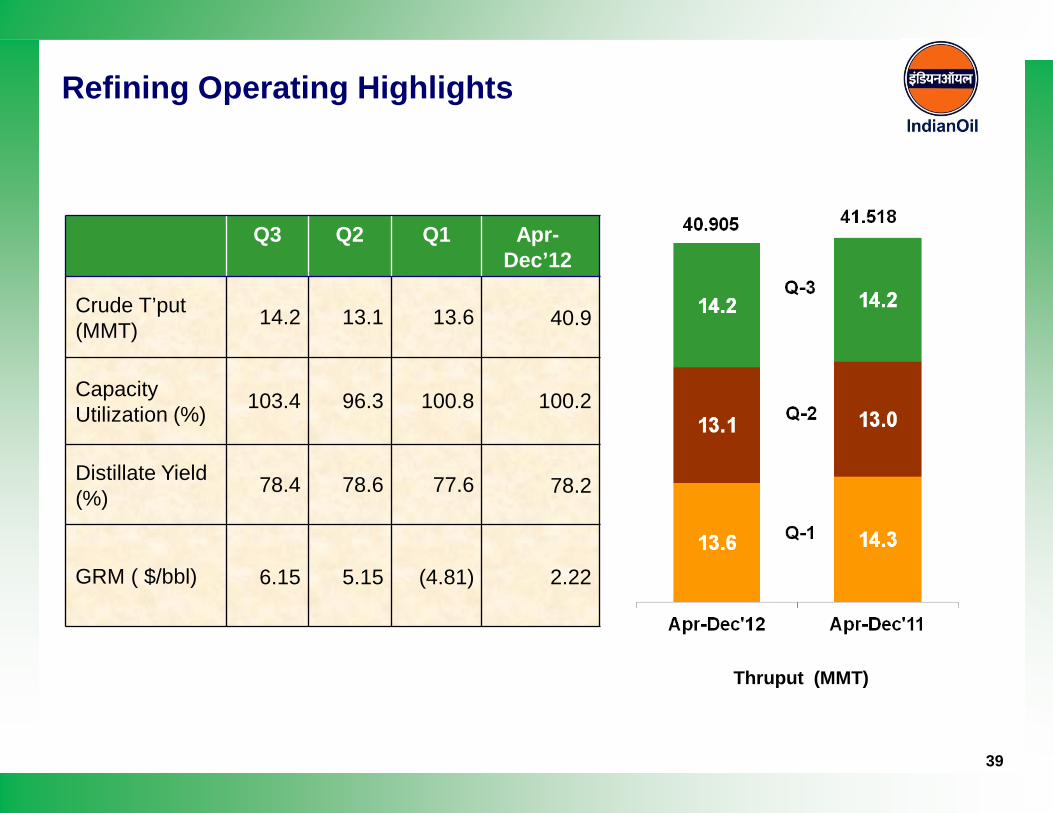

Refining Operating Highlights

39

Q3 Q2 Q1 Apr-Dec’12

Crude T’put (MMT) 14.2 13.1 13.6 40.9

Capacity Utilization (%) 103.4 96.3 100.8 100.2

Distillate Yield (%) 78.4 78.6 77.6 78.2

GRM ( $/bbl) 6.15 5.15 (4.81) 2.22

Thruput (MMT)

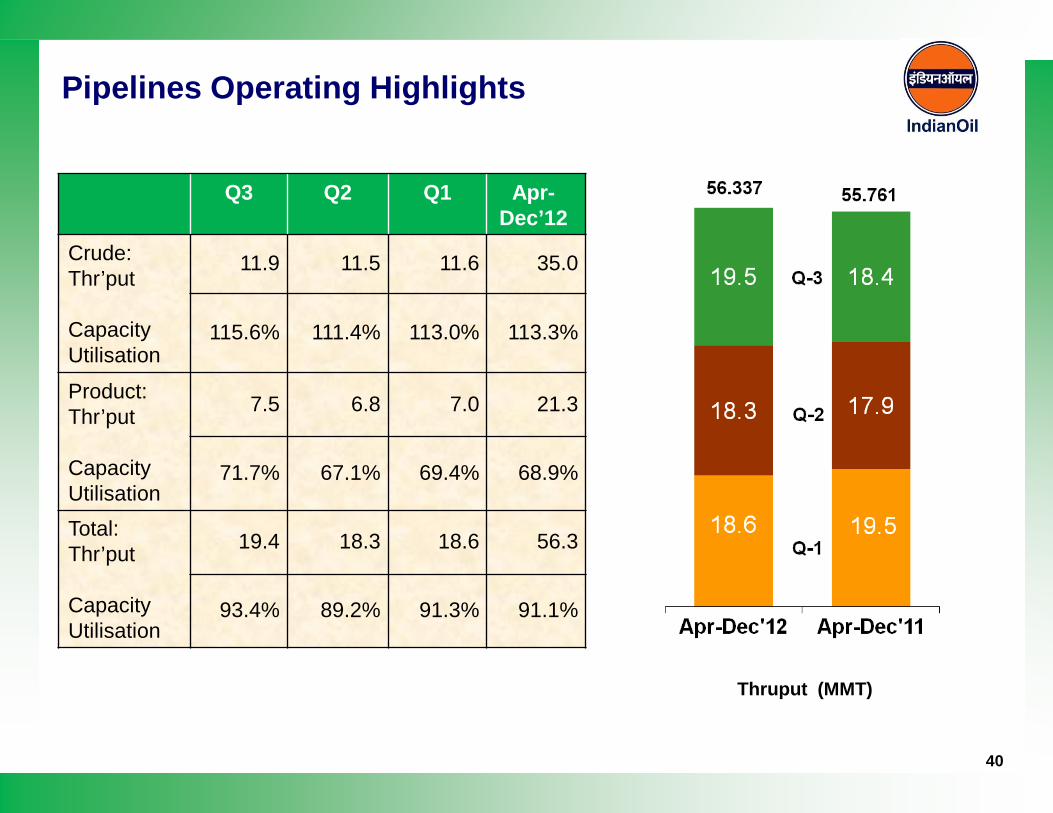

Pipelines Operating Highlights

40

Q3 Q2 Q1 Apr-Dec’12

Crude:Thr’put

Capacity Utilisation

11.9 11.5 11.6 35.0

115.6% 111.4% 113.0% 113.3%

Product:Thr’put

Capacity Utilisation

7.5 6.8 7.0 21.3

71.7% 67.1% 69.4% 68.9%

Total:Thr’put

Capacity Utilisation

19.4 18.3 18.6 56.3

93.4% 89.2% 91.3% 91.1%

Thruput (MMT)

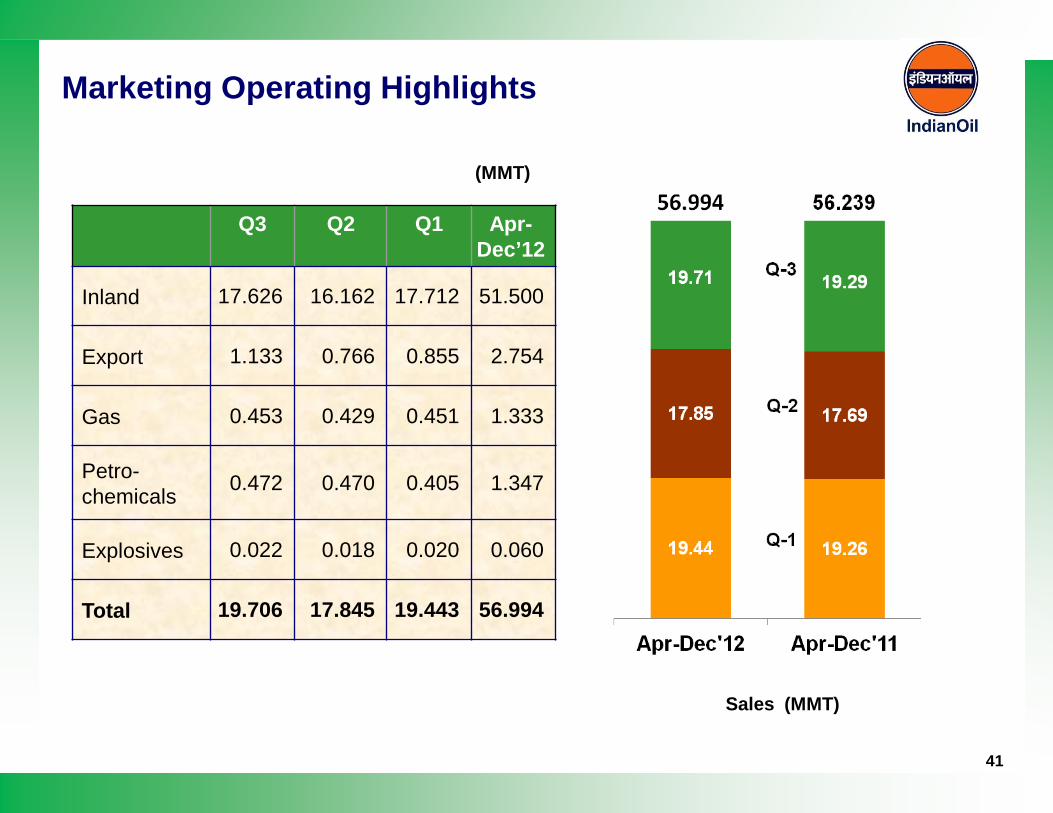

Marketing Operating Highlights

41

Q3 Q2 Q1 Apr-Dec’12

Inland 17.626 16.162 17.712 51.500

Export 1.133 0.766 0.855 2.754

Gas 0.453 0.429 0.451 1.333

Petro-chemicals 0.472 0.470 0.405 1.347

Explosives 0.022 0.018 0.020 0.060

Total 19.706 17.845 19.443 56.994

Sales (MMT)

(MMT)

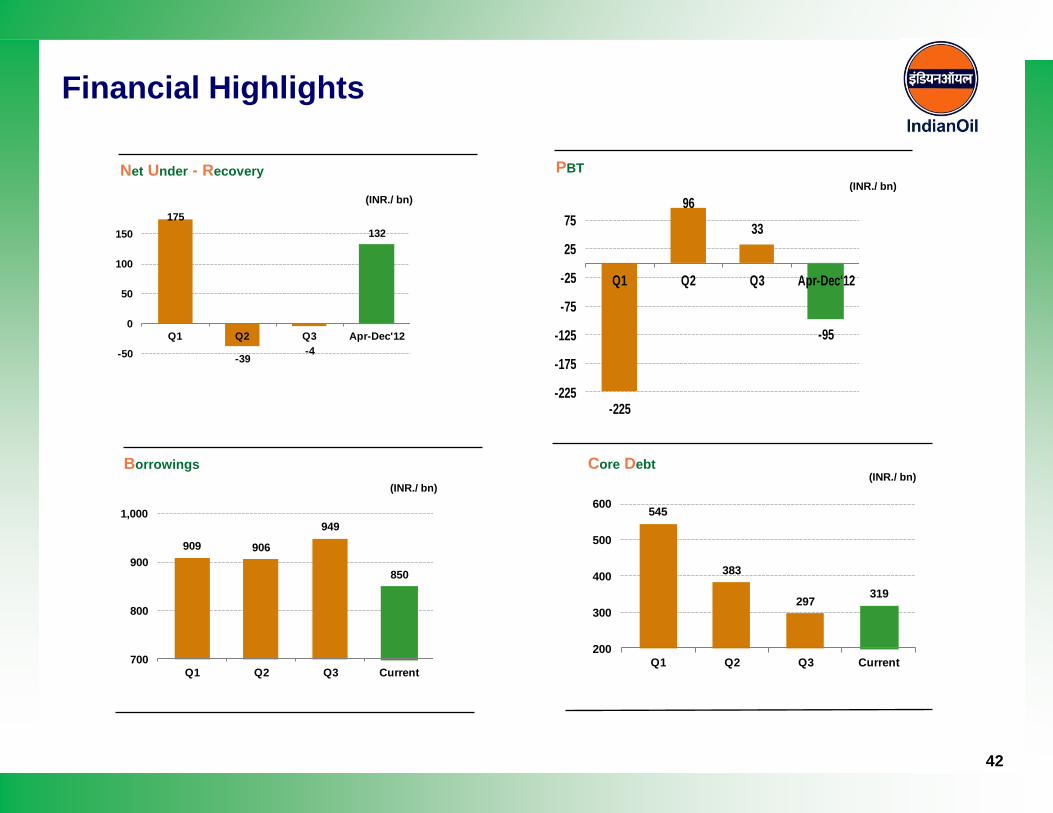

Financial Highlights

42

545

383

297319

200

300

400

500

600

Q1 Q2 Q3 Current

Core Debt

PBT

-225

96

33

-95

-225

-175

-125

-75

-25

25

75

Q1 Q2 Q3 Apr-Dec'12

(INR./ bn)

175

-39-4

132

-50

0

50

100

150

Q1 Q2 Q3 Apr-Dec'12

(INR./ bn)

Net Under - Recovery

909 906

949

850

700

800

900

1,000

Q1 Q2 Q3 Current

(INR./ bn)

Borrowings(INR./ bn)

43

IOCL – An Overview

Oil Industry In India

IOCL’s Core Operations

Strategic Initiatives

Financial Performance

Ongoing Projects

Nine Months Snapshot

44

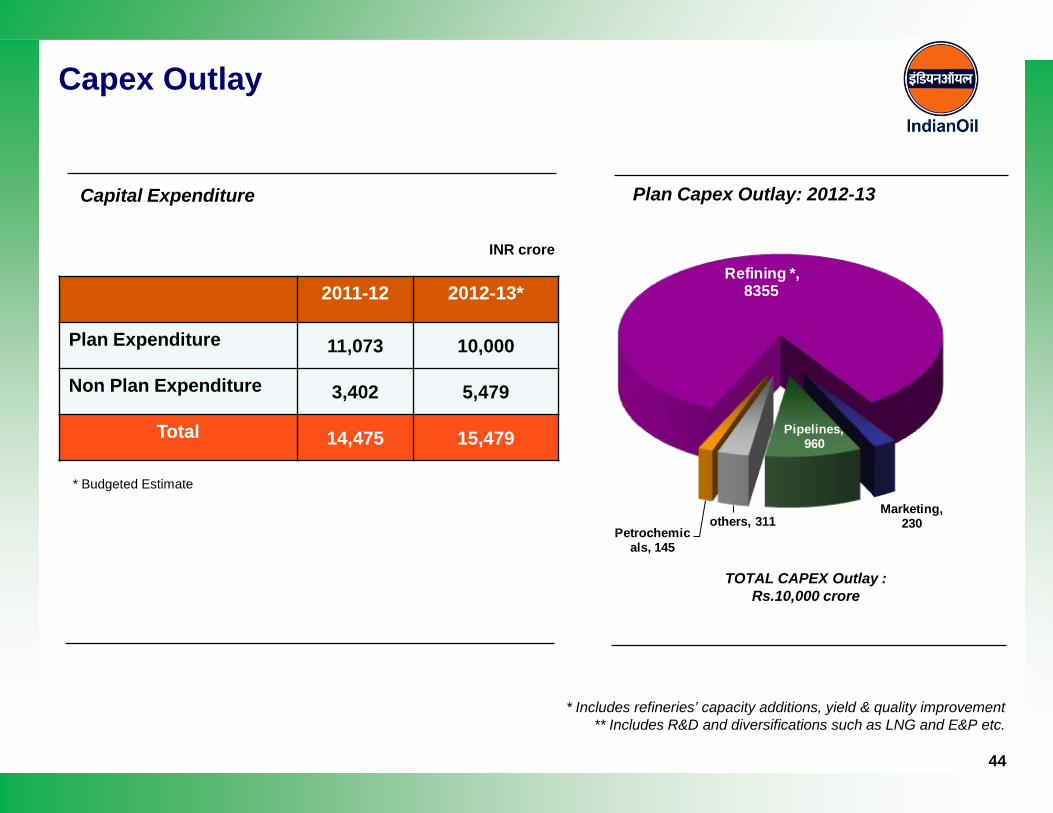

Petrochemicals, 145

Refining *, 8355

Marketing, 230

Pipelines, 960

others, 311

TOTAL CAPEX Outlay : Rs.10,000 crore

* Includes refineries’ capacity additions, yield & quality improvement** Includes R&D and diversifications such as LNG and E&P etc.

Plan Capex Outlay: 2012-13

Capex Outlay

INR crore

2011-12 2012-13*

Plan Expenditure 11,073 10,000

Non Plan Expenditure 3,402 5,479

Total 14,475 15,479

* Budgeted Estimate

Capital Expenditure

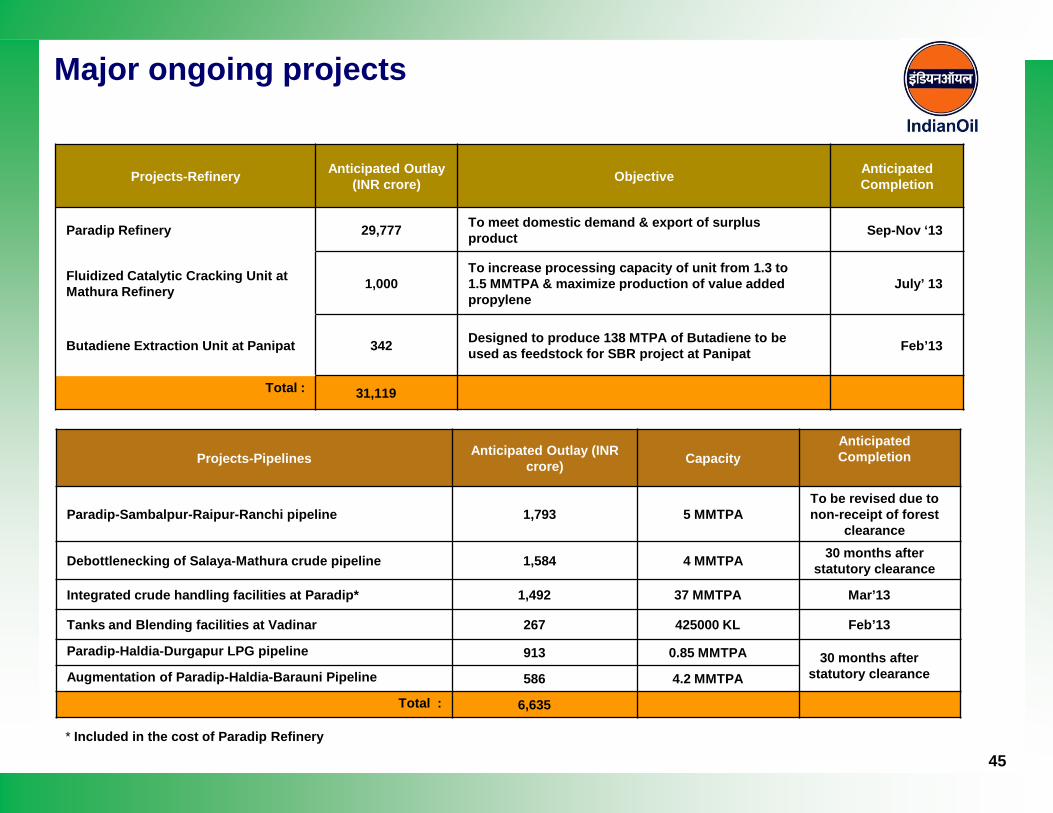

Major ongoing projects

Projects-Refinery Anticipated Outlay (INR crore) Objective Anticipated

Completion

Paradip Refinery 29,777 To meet domestic demand & export of surplus product Sep-Nov ‘13

Fluidized Catalytic Cracking Unit at Mathura Refinery 1,000

To increase processing capacity of unit from 1.3 to 1.5 MMTPA & maximize production of value added propylene

July’ 13

Butadiene Extraction Unit at Panipat 342 Designed to produce 138 MTPA of Butadiene to be used as feedstock for SBR project at Panipat Feb’13

Total : 31,119

Projects-Pipelines Anticipated Outlay (INR crore) Capacity

Anticipated Completion

Paradip-Sambalpur-Raipur-Ranchi pipeline 1,793 5 MMTPATo be revised due to non-receipt of forest

clearance

Debottlenecking of Salaya-Mathura crude pipeline 1,584 4 MMTPA 30 months after statutory clearance

Integrated crude handling facilities at Paradip* 1,492 37 MMTPA Mar’13

Tanks and Blending facilities at Vadinar 267 425000 KL Feb’13

Paradip-Haldia-Durgapur LPG pipeline 913 0.85 MMTPA 30 months after statutory clearanceAugmentation of Paradip-Haldia-Barauni Pipeline 586 4.2 MMTPA

Total : 6,635

45* Included in the cost of Paradip Refinery

Thank You