Investment Research Challenge Student Research - CFA · PDF fileCFA Society Sri Lanka...

29

CFA Institute Research Challenge Hosted in Sri Lanka University of Colombo

Transcript of Investment Research Challenge Student Research - CFA · PDF fileCFA Society Sri Lanka...

CFA Institute Research Challenge Hosted in

Sri Lanka

University of Colombo

University of Colombo Student Research This report is published for educational purposes only by

students competing in the

CFA Society Sri Lanka Investment Research Challenge, part of

CFA Institute Global Investment Research Challenge

Important disclosures appear at the back of this report 1

Source: Team estimates, Company data

Ticker: DIAL.SL Recommendation: BUY

Price: LKR 8.50 Price Target: LKR 10.96

Highlights

We issue a buy recommendation for the stock of Dialog Axiata PLC (DIAL) of LKR 10.96: The

current trading price is leading to an upside of 29%. The growth of revenue between the years of

2012A to 2016E is CAGR 12.2%. Here it is noticeable that the mobile segment revenue is the main

contributor towards the growth of revenue with a prior breakeven all new subscriber revenue would

directly contribute to profits of the business. The trailing P/E stands at 11.1 and EV/EBITDA at 4.5.

The Company is a typical dividend-paying firm, with dividend yield of 4% in 2012.

Revenue growth prospects: Keeping up with trends and innovations as a service provider in the ever

changing technology business DIAL is able to maintain a steady growth in its revenue portfolio. The

significant YOY growth in 2012A of 24.1% in revenue is expected the slow down to a level of 11%

in 2013E. The expected large investment in data sector makes a significant impact on this change. The

growth in revenue in the mobile and DBN sectors which generate revenue with data, solely

contributes to YOY 10.4% in 2013E. (1) 4G/LTE introduction to increase the data speed and usage

of customers and continuous investments in infrastructure; (2) Innovations in the e-commerce

segment of the business; (3) Strategic investments in Information Communication Technology, are all

contributors towards this growth.

Strong financial position: Liquidity position of dialog is maintained continuously at a stable rate

therefore, there would be a sound business continuity of DIAL. EBITDA margin amounting to 37.7%

in 2013E to 48.3% in 2018E. The ROA is continued to grow from 7%-11% in 2013E to 2018E. EPS

of 2012 0.75 is expected to show positive signs at 2018E at LKR 2.09.

Main risk issues are: the changes made to the floor price by the TRC, relaxing the price band,

USD/LKR exchange rate fluctuation, technological changes, first mover innovations duplication, and

macro economic conditions affecting customer trends.

Forecast Summary

2011A 2012A 2013E 2014E 2015E 2016E 2017E

Revenue (MN) 45,412 56,345 62,552 71,443 81,146 89,260 96,401

EBITDA (MN) 16,511 18,357 23,568 29,059 34,968 39,978 45,101

PAT (MN) 4,869 6,030 4,263 7,336 10,703 12,450 14,598

Per share(LKR)

Earnings 0.61 0.75 0.53 0.92 1.34 1.56 1.83

Dividend 0.25 0.34 0.25 0.35 0.42 0.63 0.81

Returns (%)

Total Asset 7% 7% 5% 7% 9% 10% 11%

Total Equity 15% 16% 11% 16% 20% 20% 21%

Dialog Axiata PLC

Date 30/09/2013

MARKET DATA

52 Week Price Range LKR 9.00/7. 80

Dividend Yield 2012 4%

Shares Outstanding 7,985,206,000

(Excluding the

ESOS)

Market

Capitalization (Rs)

66,778,984,448

Average annual

Volume

166,457,872

As a % of

outstanding shares

2.08%

Parent Holding 83.3%

Public float 14.7%

FINANCIAL DATA

EBITDA/Revenue

(X)

33%

PB(x) 1.8 times

PER (X) 11.1

EV/EBITDA (X) 4.5

Earnings per share .75

Dividend per share .33

Gearing 39%

Debt to Total Capital 1.44 times

Return On Equity 16.2% Source: Company data, CSE

Source: CSE 2013 DATA

Exchange: Colombo Stock Exchange

Sector/Industry: Telecommunication

CFA Society Sri Lanka Investment Research Challenge Student Research October 1, 2013

2

Figure 1- EBITDA

margin

Source: Team estimates

Figure 2 – Coverage

of Dialog

Source: Company data

Figure 3 - Dividend per

share and dividend

payout ratio

Source: Team estimates

Investment Summary

Bullish on DIAL

We issue a buy recommendation on DIAL with a target price of LKR 10.96 an upside movement of 29%. DIAL is

increasingly investing in infrastructure supporting a boom in the small screen data and large screen data revenue

segments together with the recent joint venture with anything.lk in to the E-commerce market. DIAL’s optimistic

movement as the countries competitive quad player seeks to reap the benefits of improving economic and political

stability. Therefore we expect DIAL which is currently trading at a 22% discounted EV/EBITDA and 44%

discounted PE to see a growth in the stock price.

Valuation method

As our primary valuation method we utilize the Discounted Cash Flow (DCF) and peer comparison method is

applied as a secondary valuation to support the value arrived in the primary valuation. In our opinion DCF

correctly reflects the value of a cash rich industry with heavy investments to drive revenue.

Reinvention through strategic acquisitions

In recent years group capital expenditure was directed mainly towards the expansion of High Speed Mobile

Broadband Services, Fixed Broadband services, and Optical Fiber Network. 2012 saw an assortment of business

creation initiatives including the acquisition of Suntel Limited, launch of eZ Cash - Sri Lanka’s first Mobile

Money and Payment service, acquiring a stake in Digital Commerce Lanka (Private) Limited, acquisition of Sky

TV, introduction of per-day Prepaid Television Service and launching HD Television services. We believe these

ventures signify Dialog’s foray in to the space of Digital Commerce and the strategic intent of the Group to

expand its operations in the future through the use of other well established organizations.

Prospects in telecommunications sector

As a revenue driven business mobile services subscribers have reached a level in which penetration has reach 96%

in the world. With the high entry barriers in fixed costs the threat of new competitor entering into the business is

minimum. The large number of player in the sector creates a favorable rivalry which leads towards a more

creativity and innovation in the telco industry. The governments’ encouragement towards the industry further

strengths the growth potential of the industry with the government’s economic policy paper(Road Map

2013)stating that Sri Lanka can reach the goal of becoming a billion dollar IT/BPO industry by 2016.

Importantly, ICT literacy has reached 40 % from around 5% in 2005.

Financial position

As the largest FDI investment in Sri Lanka DIAL is a listed company with high foreign transactions in terms of

financials. The confidence foreign banks have on the parent with a high credit rating gives DIAL the opportunity

to borrow foreign sources with low interest rates. The large debt portfolio (USD 200Mn at low interest rate) which

is obtained by DIAL for expansion of the diversity of the business gives investors the signals that the business

would grow with high liquidity. As the OCBC bank loan matures in 2018E to be USD 200MN, DIAL shows that

it is capable of making timely payments for these loans.

Stable dividend distribution

With investors being concerned on the return on individual investments the dividend payment for FY12 was LKR

.33 with a dividend payout ratio of 45%. It is stated that for future investments internally generated funds would

be used therefore, a significant effect on the dividend payout could be expected. Therefore, the dividend payout

ratio is expected to drop to 37% 2014E. But dividend per share for 2014E to be at a rate of LKR .35 making sure

that the individual investors are kept satisfied with their long term investment.

Downside of the valuation

In the background of an upside movement in the share price investors should be aware of the possible adverse

influences from high level of capital expenditure incurred, the over dependence on the CEO of DIAL as the

visionary leader while looking at the parent company owning 83% stake of DIAL which has brought cheap

financing sources to DIAL thus far and a brand name.

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

3

Table 1 - Valuation

DCF Valuation LKR 10.96

Relative

Valuation

(SLTL)

LKR12.70

Relative

Valuation

(Foreign)

LKR14.60

Source: Team estimates

Table 2 - Market turnover

SLTL DIAL

WTD 3,191 203,309

MTD 99,362 968,895

YTD 3,092,460 166,946,512

Source: Team estimates

Table 3 - WACC

Rf 12.0%

Beta 1.1

Market Risk Premium 9%

Tax Adjusted Kd 13%

Source: Team estimates

Table 4 - Cost of debt

Interest Weight

Local

Loan 20% 30%

Foreign

Loan 10% 70%

Source: Team estimates

Figure 4 - DIAL Share price movement and Information Flow

Source: CSE data (2012-2013)

Valuation

We predict a 29% upside movement in DIAL with share price moving up to LKR 10.96. As our primary valuation

we have used the DCF method and in order to support our recommendation and for completeness a peer

comparison with a relative valuation is obtained. However we do not base our recommendation on the relative

valuation due to;

High investments required - Telco industry requires heavy investments to keep pace with the

advancements in the environment in order to support a growth in its top-line. Therefore a valuation based

on cash flow would be appropriate more than a relative valuation based on earnings.

Inadequate comparisons – SLTL is the only comparable listed company in the CSE. However firstly it is

49.5% government control with high political influence therefore price behaviors would highly sensitive to

any political information and share prices movement would be seen as slightly distorted. Secondly looking

at the turnover SLTL is comparatively is a low liquid stock with low level of turnover. (table 2) Therefore

it is SLTL price being correctly priced is debatable.

DCF Valuation

We use the Free Cash Flow to Firm (FCFF) in our valuation model as DIAL is expecting changes in its capital

structure firstly since we are using historical data to predict the Free Cash Flow (FCF) FCFF growth rate would

reflect fundamentals more clearly than FCFE which reflect fluctuating amounts in leverage, secondly in a forward

looking context the required return on equity might be expected to be more sensitive to changes in leverage than

changes in the WACC, making the use of a constant discount rate.

WACC – DIAL is a low geared company with positive credit ratings. Management is promising a target capital

structure of 50:50 Debt to Equity capital structure. (Appendix 06. A)

Ke (Cost of Equity) - We have utilized the CAPM method in estimating the WACC as we expect the market to be

efficient. Therefore we have used the 5 year T- bond rate(11.17%) of 12.0% adjusted for taxes, and a Beta value of

1.1 using the past data however as the industry matures we expect beta to vary between 0.9 – 1.1. Risk Premium

(Rp) of 9% was assumed based on country risk premium (Appendix 06. B)

Kd (Cost of Debt) – DIAL is enjoying low cost of debt due to the positive credit ratings (AAA(lka) – Fitch) and

the parent company in Berhad enables DIAL to have access to low foreign currency loan. It finances 70% of loan

requirement through foreign loans therefore in our opinion DIAL is exposed foreign exchange loss for which we

have included a 4% average LKR/USD depreciation to the trend in the past floating lending rate the inflation rates

subjective to change in the US. (Appendix 06. C)

Terminal Growth Rate (TGR) – We expect a low TGR at 1% as DIAL is operating in mature industry with low

availability to grow in the long term as the markets saturate and with high level of rivalry.

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

4

Table 6 - Peer Multiples EV/

EBIDA

PE PB D

E

%

DIAL

:SL 4.5 11.1 1.8 40

SLTL

:SL

5.2

2 19.87 1.47 33

BHARTI

:IN

17.

0 30.0 11.0 23

RCOM

:BO

16.

97 46.07 1.08 85

ADVANC

:TB

10.

23 17.05

13.0

6 49

Source: Annual Report data

Table 7 - Relative value on

SLT

Multi

ple

Pric

e

(P)

Weig

ht

(W)

Value

(P*W

)

EV/

EBIT

DA

12.2

4

50% 6.12

P/E 14.9

0

35% 5.22

P/B 6.85 15% 1.03

12.39

Source: Team estimates

Table 8- Relative value on peer Multiple Price Weight Valu

e

EV/

EBITD

A

17.09 50% 8.54

P/E 11.72 35% 4.10

P/B 20.70 15% 3.10

15.75

Source: Team estimates

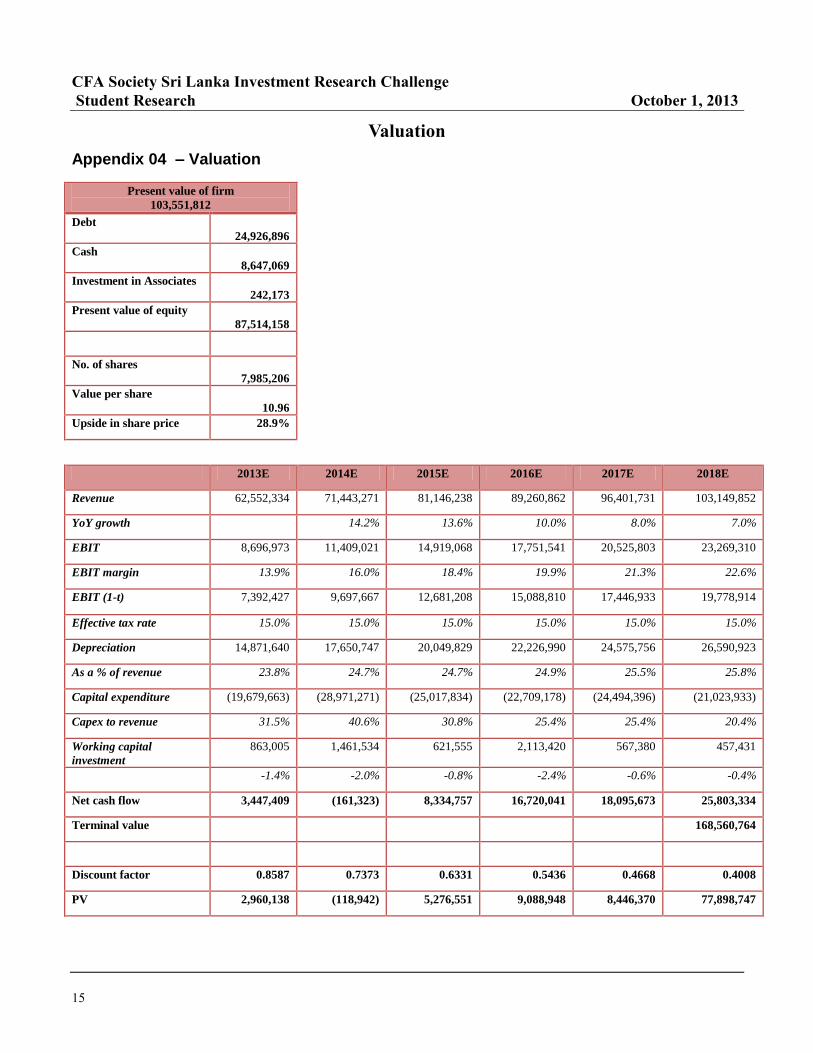

FCFF – FCFF is expected to be very low and negative in FY13 and FY14 due to the heavy capital expenditure

high data growth, DTV revenue growth and through other inventions in to the digital space through its

E-commerce /M-commerce arm. (Appendix 4)

Table 5 - Valuation

FY13E FY14E FY15E FY16E FY17E FY18E

EBIT(1-t) 7,392,427 9,697,667 12,681,208 15,088,810 17,446,933 19,778,914

Depreciation 14,871,640 17,650,747 20,049,829 22,226,990 24,575,756 26,590,923

FAinv (19,679,663) (28,971,271) (25,071,834) (22,709,178) (24,494,396) (21,023,933)

WCinv 863,005 1,461,534 621,555 2,113,420 567,380 457,431

NCF 3,447,409 (161,323) 8,334,757 16,720,041 18,095,673 25,803,334

TGR

(1%)

168,560,764

Source: Team estimates

Secondary Valuation – Peer Comparison

In order to support our recommendation in the DCF method we calculate the intrinsic value of DIAL based on its

local peer SLTL. However due to the lack of comparable peers within the country we have taken regional market

leaders to our valuation not overlooking the differences in the penetration levels, market conditions and macro

factors within the individual countries. ( Appendix 5)

We base our relative valuation on trailing P/E, EV/EBITDA and P/B for our peer companies. Trailing P/E is

commonly used by analysts and investors in determining the intrinsic value of a share as earnings power is

considered to be the driver for value creation therefore we have placed a 35% weight. However EV/EBITDA is

less sensitive to the effects of financial leverage therefore comparable across companies with varying capital

structures Hence we have placed a 50% weight. P/B was used as a valuation multiple because this industry is

mainly driven by the capital expenditure made on assets we have weight it at 15% due to the effect of different

business structures and varying useful life of assets being sensitive to this multiple. We have not based our

valuation on the dividend yield (DY) as DIAL re-invests majority of its earnings in capex to support the

continuous improvement in technology the bottom line of future earnings.

Comparative to SLTL, DIAL is trading at trailing PE of 79% and 31% and 36% discounted EV/EBITDA and 18%

premium PB. In our opinion with the international bandwidth expansion project together with lying of fiber optic

cables the competitive advantage enjoyed by SLTL is removed while reducing DIALs operational cost by a

considerable percentage. Therefore we expect DIALs EPS growth to improve in the future which would drive the

share price upward hence we forecast a relative value of LKR12.36 on currently oversold DIAL share. (Table 5)

We looked at our regional peers with similar corporate characteristics by discounting the multiple by 30% to

adjust for difference in market conditions and macro factors.

Risk to our valuation Our valuation under the DCF is heavily depended on the terminal value. However we

assigned a conservative TGR of 1% despite assuming a TGR of 0% by a pessimistic investor due to the cut throat

competition and the saturation in the target market in our opinion currently DIAL is trading at a discount.

Secondly our valuation is sensitive to the WACC of 16.5% however continued bearish outlook in the market or

dampening macro economic conditions causing the risk outlook of the country to worsen and causes an increase in

the WACC to 18% we see current market prices to be mispriced and an upward move is expected.

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

5

Figure 6- Revenue

segments

Source: Company data

Figure 7- Share

ownership

Source: Company data

the formatting of the

sidebar text box.

Figure 5 - Variation in the Valuation

Source: Team estimates

Business Description

Dialog Axiata PLC, a subsidiary of Axiata Group Berhad (Axiata), operates Sri Lanka’s largest and fastest

growing mobile telecommunications network representing approximately 3% of the total market capitalization of

the CSE, positioning the company within the top 10 largest companies in terms of market capitalization. Company

was incorporated in 1993 as a private limited liability company bearing the name of MTN networks (Private)

limited. In 2004 DIAL was listed in the CSE and by the year 2010 changed its name as Dialog Axiata PLC. The

operations of Dialog Axiata PLC include Mobile, International and Tele-Infrastructure businesses. The Company

delivers advanced mobile telephony and high speed mobile broadband services to a subscriber base in excess of

7.7Mn Sri Lankans, via a 2.5G and 3G/3.5G networks as well as 4G communication networks supporting the very

latest in multimedia and mobile internet services.

Subsidiaries

Dialog Axiata supplements its market leading position in the Mobile Telecommunications sector with a robust

footprint and market presence in Sri Lanka’s Fixed Telecommunications and Digital Television markets through

its fully owned subsidiaries Dialog Broadband Networks (Private) Limited (DBN) and Dialog Television (Private)

Limited, (DTV).

Dialog Mobile

Dialog mobile with a customer base of over 7.5 million, provides the best in mobile coverage, with over 2600 base

stations spanning all provinces. In addition customers are linked to over 200 global destinations via international

roaming, including 3G services. The Company also holds the distinction of being the first service provider in

South Asia to launch 3G and HSPA+ services, and most recently Mobile 4G services based on FD-LTE

technology contributing more than 80% of the total revenue of the group.

Dialog Broadband Networks

DBN the second largest fixed Telecommunication provider contributed 8% to the total revenue in the year 2012.

DBN has the distinction of being the first telecommunication operator in Sri Lanka to launched 4th generation

LTE High Speed Broad band Services. DBN remained dilutive to the Group at NPAT level, but registered

significant improvements in revenue and operational performance on the back of strong revenue and synergies

achieved through acquisition, merger and operational consolidation of Suntel Limited.

Dialog TV

Dialog TV which is the smaller contributor to the total revenue of Dialog Axiata PLC comparing with other

segments, is the market leader in Sri Lanka’s Pay TV sector. DTV supports a broad array of international and local

content in both Standard Definition (SD) and High Definition (HD) formats alongside a wide portfolio of Sri

Lankan television channels and delivers high quality infotainment to a viewer base in excess of 275000 Sri

Lankan Households.

Other Operations

Dialog Axiata has the distinction of being the first mobile operator in Sri Lanka to be awarded a Payment Systems

Provider license by the Central Bank of Sri Lanka, based on which it operates eZ Cash, the country’s pioneering

mobile money service.

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

6

Figure 8 - Composition of free

float

Source: Company data

Figure 9- Sustainabile aspects

Source : Company data

Figure 10- Mobile-cellular

Penetration 2013

Source : ITU/ICT indicators database

The Dialog Group also established a position of strength in Sri Lanka’s Digital Commerce space through a Joint

Venture (Digital Commerce Lanka) encompassing Sri Lanka’s leading daily deals site Anything.lk and the

incumbent e-commerce properties of the Dialog Group WoW.lk, ibuy.lk and tradenet.lk.

Dialog Axiata PLC’s Management

The CEO Dr.Wijayasuriya counts over 17 years experience in technology related business management. Under his

leadership company has achieved many awards and also expanded the business into several categories. Other

members in the team also have greater experience and knowledge related to the area they are handling which have

contributed and will contribute to the continuous success of Dialog Axiata PLC.

Other Headings Relevant to Dialog

Corporate governance safeguarding the best interest of shareholders and other stakeholders

To uphold accountability and sound internal control systems Dialog Axiata follows an internally generated Code

of Corporate governance which includes all regulatory and non regulatory standards. The Maintaining the highest

standards of business integrity, professionalism and ethical values is strictly followed by this code. The Securities

& Exchange Commission and the Institute of Chartered Accountants Sri Lanka were instrumental in drafting the

Corporate Governance Listing Rules, which are applicable to listed companies via the Colombo Stock Exchange

Listing Rules. Therefore all criteria on this Code of Best Practice on Corporate Governance are evident on the

corporate conduct of DIAL.(Appendix 8)

Assuring a sustainable future

For business continuity DIAL follows a strict sustainability policy where a three-fold incorporation of

Sustainability: into the core of our operations, into the consciousness of every employee, and in every facet of the

business is followed. To ensure the proper conduct of the organization in terms of sustainability DIAL prepares an

annual sustainability report under the guidelines of the Global Reporting Initiative (GRI). Within the past few

years DIAL has made progress with achieving partially sustainable targets set for the company where a fair

percentage of the targets have created a competitive advantage for the company.(Appendix 9 )

Giving back through corporate responsibility

Dialog operates with Triple Bottom Line spheres in economic, social and environmental performance to adhere to

its commitments. As a service provider DIAL has a large responsibility towards one of its largest stakeholders in

the business its customers who come from all walks of life. Therefore, DIAL gives high priority to this cause of

including everyone despite the demographic location to access of information and communication. Through

further innovation and creation DIAL looks into different aspects of social issues which could be mitigated

through proper allocation of technology.

Conditional drivers of additional upside

Possible consolidation of the industry. DIAL as the market leader on mobile communication has a well

established position in the market and sees little threat from other player. Where-as small players are facing many

difficulty in keeping up their businesses due to over heads. Therefore, there is high possibility the industry would

soon consolidate to a fewer number of player with time. In such instance DIAL would be at an advantage if it

acquires a small player due to the need of ever growing spectrum. Further through future consolidations there

adverse affects of unfair competition would reduce to a favorable condition

Growth through innovation. The R&D of DIAL keep innovating added services to give customers with better

features on a regular basis taking the company and industry to grater heights. As the first mover in the industry in

the past in many instances DIAL has been able to capture a larger customer base on based on the innovation and

push strategy. By attracting a loyal customer base DIAL is able to maintain such a relationship by providing

various VAS.

Partnerships for inorganic growth. DIAL has been serving in the telco industry so far with many partnerships

and it looks at improving and entering into more in the future. (1) Over The Top (OTT) content providers entering

into data and content sharing agreements (2) partnership through integration with parties in the ICT industry (3)

looking into cloud computing technology generation.

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

7

. It is often aligned on the left

or right of the page, or located

at the top or b

Figure 11: Subscriber

composition of service

providers

Source: Company data

Figure 12 :Global GDP vs

Global Telecom

Source: IMF

]

Figure 13- Vertical to

horizontal integration

Source: Company data

Industry Overview and Competitive Positioning

Current situation of the Industry in the words of Brahima Sanou, Director of the ITU Telecommunication

Development Bureau “I am pleased to present the latest ICT facts and figures which shows continued and almost

universal growth in ICT uptake. Every day we are moving closer to having almost as many mobile-cellular

subscriptions as people on earth. This is exciting news. The mobile revolution is empowering people in

developing countries by delivering ICT applications in education, health, government, banking, environment and

business. Let us all celebrate this mobile miracle that I have no doubt will hasten our pace towards sustainable

development”

In 2013, there are almost as many mobile-cellular subscriptions as people in the world, with more than half in the

Asia-Pacific region (3.5billion out of 6.8 billion total subscriptions). As global mobile-cellular penetration

approaches 100% and market saturation is reached, growth rates have fallen to their lowest levels in both

developed and developing countries. Mobile-cellular penetration rates stand at 96% globally; 128% in developed

countries; and 89% in developing countries. (Figure 10)

Growth in Internet Protocol Traffic

Total global Internet users will reach an estimated 2.7 billion worldwide by end of 2013. In developing countries,

the number of Internet users will have more than tripled between 2007 and 2013, to reach more than 1.8 billion.

Despite this rapid growth, however, less than a third of inhabitants in the developing world will be online by end

of 2013. In 2013, IP traffic is expected to grow by some 14’000 petabytes/month, the equivalent of twice the

global cumulated traffic over the whole decade from 1994 to 2003 (According to Telegeography data) These

tremendous volumes are driven by growth in the number of connected people and devices, and the growing

availability of abundant, diversified, and in most cases free, online content. In 2012, the number of individuals

using the Internet reached the milestone of 2.7 billion people according to the ITU and the total number of

applications downloaded over all types of mobile devices is estimated to have surpassed 50 billion. (ABI Research

2012)

High barriers to entry and high exit barriers

It comes as no surprise that in the capital-intensive telecom industry the biggest barrier to entry is access to

finance. To cover high fixed costs a lot of cash is typically required. When capital markets are generous, the threat

of competitive entrants escalates. When financing opportunities are less readily available, the pace of entry slows.

Meanwhile, ownership of a telecom license can represent a huge barrier to entry. There is also a finite amount of

"good" radio spectrum that lends itself to mobile voice and data applications. In addition, it is important to

remember that solid operating skills and management experience is fairly scarce, making entry even more difficult.

Subscriber acquisition and retention costs (SARCs) are likely to remain high so long as six telecom operators

compete for Sri Lanka’s 21 million population. High SARCs should affect challengers more than incumbents

(which benefit from greater economies of scale). Profitability pressure also stems from higher energy costs and

inflationary pressures since early 2012, as well as higher regulatory levies.

Telecom Sector growth still outpacing GDP growth

The potential of shaking business confidence everywhere in the world has risen to new heights, and the IMF

lowered its growth forecast and is warning of recession risks due to downward revision of global GDP. Economic

readings are worrisome everywhere but the U.S., but so far the impact on global telecom and enterprise remains

tame, and considerable growth in capex can be forecasted according to the principal analyst for mobile

infrastructure and carrier economics at Infonetics Research. Globally, mobile service revenue is the main growth

engine in the overall telecom. (Figure 12)

Shift from vertical integration to horizontal integration-supplier power reduce

Consumers and businesses are more demanding, expecting always-on service everywhere, forcing operators to

boost network capacity and connectivity. Industries are becoming increasingly digitized, demanding new services

like mobile payment platforms and cloud computing. Vertically integrated technologies, on which operators have

long depended, are growing increasingly modular and open and the telecom ecosystem is becoming more

competitive. These challenges and opportunities are creating a fundamental shift among operators from the

vertically integrated business models that dominated the industry for most of the past century. Now, four distinct,

though by no means mutually exclusive, horizontal business models designed to take full advantage of the

opportunities are emerging: Network Guarantors, Business Enablers, Experience Providers, Global Multi-

marketers. (Appendix 10)

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

8

Figure 14- Sri Lanka vs DIAL

Subscriber Growth

Source -TRC

Figure 15-Competitive position

Market

share % 38 25 22 8 7

Revenue

share % 55 28 17 - -

Source Industry data

Figure 16 – Internet

subscriber growth fixed and

mobile

Source TRC

Figure 17 – Porters five

forces

Source – Team estimates(Appendix 11)

Marketing, sales and customer care are becoming entirely digital

The web is nowadays the most important marketing, sales and customer care channel for operators. According to

eMarketer, telecom brands are the most successful at engaging consumers through online advertising. In fact,

telecom advertisements achieve a click-through rate six times that of standard online banners, thus providing a

high ROI. Customer self-service is regarded as highly profitable for operators, since the bottom-line savings in

online self-service are between 40-90%. In addition, when the self-service system is well designed, it can help

with customer retention and provide up-selling and cross-selling opportunities. This high efficiency achieved by

the existing service providers, weaken the entry of new comers.

Power of up- stream suppliers

Unarguably, the telecommunication operators will not be in existence if there were no telecom equipment

suppliers for the business of the former largely and mainly dependent on their ability to transmit voice and data

effectively which is done through the telecom equipment. But a single supplier becomes less powerful with a large

number of equipment makers around. There are enough vendors, arguably, to dilute bargaining power. The

telecom equipment industry was the first industry where private Chinese companies successfully expanded

overseas. Beginning in the late 1990s, Chinese firms began to establish a presence in foreign markets. After more

than a decade of growth, Chinese firms now account for more than 30% of the global market. These cheap

alternatives make the telecom operators powerful.

Economic support

Sri Lankan Economy is growing at 6.8% (June 2013) as per the State Statistics Office. Rubber, paddy, mining,

transport, hotels, banking and finance, wholesale, retail, textile, apparel sectors showed high performance as up-

to-date while tea, fishing, coconut showed contracted performance. Despite the inflationary situation telco

industry has grown by 8.9% which is a considerable growth. With the globalization and fast growth in technology,

we can hardly find a person without a mobile to make their life easy. Our idea is that Sri Lankan Telco industry

has promising prospects and with the growth in the economy telco industry would further expands.

Cut Throat Competition

With the massive industry deregulation coupled with flexible credit opened doors for the new entrants, this lead

the industry to be more competitive than before. Nearly everybody already pays for phone services, so all

competitors now must provide customers with lower prices and more exciting services. Sri Lanka’s Telecom

industry has been overcrowded during the last couple of years and this remains the key medium-term risk to

telecom operators in the country.

Sri Lanka’s mobile industry is one of the most competitive markets in the region with five operators competing for

a total addressable population of approximately 21.7 million and the competition among the five operators,

Dialog, Mobitel, Etisalat, Airtel and Hutch is expected to remain high in years ahead. With Bharti Airtel, India’s

biggest mobile operator launching its operations in Sri Lanka later in 2008 the other 4 operators engaged in

different strategies to block Airtel’s entry. With existing players reducing the prices so low and Airtel being well

equipped to face that, ultimate result was the Price war.

Dialog is Sri Lanka’s undisputed Mobile Market Leader-positioning

In terms of revenue and market share dialog is well above its competitors (with 55% revenue share and 38%

market share). Further, dialog has the widest distribution network within the country with the highest number of

arcades, service centers and outlets spread through-out the country. With Dialog’s strategic acquisition of Suntel

in 2012, it was ranked as the 2nd largest player in the fixed telecommunications sector in Sri Lanka. High fixed

cost increases rivalry since total costs are mostly fixed costs and high exit barriers place high cost in abandoning

the product (asset specificity)

DIAL, one of the largest companies on the Colombo Stock Exchange contributes towards 3.08% of the total

market capitalization.(with the distinction of being the first on the Colombo stock market with a market

capitalization exceeding $1 billion) DIAL also contributes for more than 40% of the market capitalization of the

telecommunication sector. Being Sri Lanka's largest foreign direct investor with a total FDIs exceeding US$ 1.5

billion during the last two decades. It also had entered into infrastructure investment agreements totaling to US$

150 million with the Board of Investment (BoI). Company has switched on its 4G LTE Network in Colombo—

said to be the first LTE pilot network in Southern Asia.

Sri Lanka reduces broadband tax to promote internet use

Sri Lanka has been ranked No.1 in the world with the lowest entry level fixed broadband charges according to a

report published by the International Telecommunication Union in 2012. Sri Lanka has achieved this global rating

for broadband charges within a short period of time after the TRC took steps to ensure subscribers got value for

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

9

Figure 18 - Growth in data

segment

Source: TRCSL and Student Estimates

Figure 19 - CAPEX and

Return

Source: Company data, student estimates

Figure 20 – Growing Margins

Source: Company data, student estimates

Figure 21 – Debt Capacity

Source: Company data, student estimates

money and entry prices were affordable to as many people. Telecommunication levy on the internet and

broadband services was reduced by 50% from Jan 1st 2013 from 20% - 10%. The Director General of TRC

pointed out that 1.2 million Sri Lankans use internet now in Sri Lanka and the government aims to increase it to

three million by 2015.

Financial Analysis

Revenue: DIAL has been able to realize superlative results over the years recording a strong growth across all

sectors. Group revenue demonstrated a 24%YoY growth in 2012 while revenue CAGR in years 2008-2012 was

ca. 11.6%. Our predictions suggest YoY revenue will decrease in the voice sector over the coming years as a

result of saturated voice penetration and aggressive competition, and DTV will only be able to sustain its market

share through economies of scale and price advantages. However, this will be compensated by the growth in other

sectors as group CAPEX has been directed mainly towards an assortment of business creation initiatives such as

the introduction of 4G technology, High Speed Mobile Broadband Services, Optical Fibre Network, the

international cable landing station and Investment in new submarine cable to boost international bandwidth We

believe these ventures signify Dialog’s foray in to the space of Digital Commerce and the strategic intent to

expand its operations through cost reductions. Thus we expect a CAPEX to Revenue of 30% and 40% in 2013

and 2014 respectively and a ratio around 25%-30% is expected to be maintained for the rest of the forecasted

period.

Data segment (mobile and fixed broadband) is anticipated to be the main revenue driver in the near future as the

data market penetration is expected to grow at a 2013-15E CAGR of 35% as a result of increase in data

penetration (2012 - 6.7% to 2015E – 23%), increase in smartphone penetration as smartphone users are expected

to spend more time on the internet than on traditional calls and SMS’s and regional trends. DBN is expected to

achieve consolidated benefits to costs while subscriber growth potential in terms of corporate customers is high

post acquisition. Implementation of high speed 4G technology is expected to convert subscribers to DIAL and

forecasted economic developments are likely to attract a larger number of high income earning corporate

personnel contributing revenue CAGR of 9% 2013-15E.In line with its past trends International telephony

revenue is expected to grow at a CAGR of 14% 2013-15E which is justified by low international tariffs and the

fact that Sri Lanka is poised to become one of the largest knowledge hubs in the world.

Margins and Performance: In 2012 Group EBITDA increased only by a mere 11% YoY and EBITDA margin

dropped 3 percentage points. However the potency of the group is emphasized by the astounding 23.2% growth in

PAT including non-cash exceptional items such as translational foreign exchange losses and network

modernization related impairment charges. But these extraordinary growth rates are expected to be held back in

2013 (YoY reduction of 29%) as the company is opting for a 2% revenue tax following the expiry of the tax

holiday along with volatile finance costs. We predict that the EBITDA and NP margins will remain at levels

similar to 2012 (refer Appendix 13 for a detailed ratio analysis) while EBITDA and NP will grow at CAGR of

16% and 32% respectively in 2013-18E. We anticipate these predictions will hold in the absence of dramatic

strategic acquisitions and investments.

ROA and ROE performance is expected to be relatively flat in 2013-14E. Low levels of performance are

attributable to the large investments in fixed assets made continuously to secure revenue and the plough back of

retained earnings. But ROE is expected to increase to an average 20% after 2014E as the quantum of investments

begins to reap benefits.

Debt: Over the years DIAL has maintained a Gearing and Debt ratio at around 70% along with a strong interest

cover (6 times of EBIT in 2012). Our forecasts depict that future investments will be funded through a

combination of debt and retained earnings and DIAL will attempt to maintain a debt equity ratio of 50%. The

high dependency on debt financing for strategic expansion is justifiable as most of this debt is acquired at a very

low interest rate from DIAL’s parent company in Malaysia, a healthy cash balance and lucrative investments that

adds up to a strong asset base.

Cash generation and Liquidity: In line with previous years cash from investing activities is expected to remain

negative as a result of high CAPEX. Cash flow from financing activities mainly consisting of borrowings and the

repayment of borrowings is expected to be positive as a result of the USD 200mn syndicated term loan, other

rupee loans and an estimated 40% dividend payout ratio (well below the 45% in 2012). DIAL’s liquidity ratios are

expected to improve from their current low levels (current ratio 0.86 and cash ratio 0.46 in 2015E) as a result of a

strong cash base. A comparison of DIALs key performance indicators is illustrated in table 9 below.

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

10

Figure 22 – Cash flow

patterns

Source: Company data, student estimates

Table 10- Mobile Cellular

Tariff

ols

Rank

Country Value

$

04 Bangaladesh 0.03

05 Sri Lanka 0.04

06 India 0.04

43 Malyasia 0.19

91 United

Kingdom 0.37

Source: Company data

Figure 23 USD/LKR 2008-

2013Sep

Source: CB Sri Lanka

Figure 11- Likely hood and

impact Risks Likely

hood Impa

ct

Rati

ng

Regulator

risk

1 5 H

Forex 1 5 H

ASPI

Volatility

2 3 M

Demand

Assumpti

ons

3 5 H

Rivalry 1 5 H

Longer

Payback

1 5 H

Parent

company

linkages

5 5 H

(Likely hood of a risk occurring: 5 –

very unlikely 1 – very probable /

Impact: 5 – High impact 1 – Low

Imapct) Source: student estimates

Table 09: Peer Financial Ratios

Source: Bloomberg, Company data

Investment Risks

Regulator risk - Telco industry in Sri Lanka is highly regulated with a floor price as well as heavy duties as VAT,

income taxes and licensing fee. Relaxation of the floor price with the current over populated industry or an increase

in the effective tax rates from current level of 15% to 25% could hurt the top line as well as the NP of DIAL. The

overcrowding in the industry with 5 mobile operators, 3 operators providing fixed telephony and pay TV providers

in an addressable population of 21mn is situation in the industry attributable to regulator risk together with

regulators independence from the political frame work draws our concerns.

Forex – We expect the LKR to depreciate by 6% against the USD (Appendix). DIAL holds over 80% loan in USD

causing major exchange losses. (Appendix 14)

ASPI Volatility – CSE has been facing major shocks with high volatility in share prices. CSE is highly sensitive

towards the foreign investors therefore economic and political changes especially in the US would affect the

volatility of the local index. This overall behavior of the index could affect DIALs share prices to be highly volatile

resulting in share prices to trade at a discounted value.

Demand Assumptions – Our valuation is highly sensitive towards the GDP growth rate, Computer literacy and

purchasing power of the consumers. Telco considered the engine of technological enhancement of the country is

highly correlated with the macro economic conditions. Major revenue generating sources for Data, DBN and DTV

are seen from business as BPOs and hotel projects, dampening GDP growth would affect the revenue in this

segment as well further deterioration of purchasing power caused through an inflation rate in excess of 7% would

cause the revenue of DIAL to decline. 87% of its revenue is generated through voice however with the replacement

of its cash cow with cheap third party mobile applications is a threat DIAL would face.

Rivalry – DIAL was experiencing a low ARPU growth because of the low tariffs in operation (Table 10). We see

consolidations taking place in the future taking away the prevailing cut throat price war we see this as a positive in

terms of DIALs top line which could cause an increase in the RPU. However we see potential threat of other forms

of competition such as number portability which if introduced enables the consumer to move between networks

freely. We see reasonably a less threat to DIAL as it is the market leader in introduction of new technology with a

reasonably loyal customer base.

Longer Payback - DIAL has shown signs of heavy Capex in FY13 FY14 and FY15 causing the high level of

depreciation cost in their financial statement as well as liquidity risk with non - recoverability of its investments in

the future.

Parent company linkages – Axiata Bhd is the parent of DIAL claiming 83% ownership of DIAL creates both

positive and negative impact on DIAL. DIAL uses Axiata brand name in its business activities which has enabled

DIAL to obtain a AAA(lka)Fitch rating creating a positive impact of having access to cheap debt financing,

however we also identify the risk with a large controlling parent in the event of DIAL loses its status as the

subsidiary of Axiata it would face a liquidity crisis.

EBITDA

Margin

NP Margin Capex/ Revenue Debt/Equity Current Ratio ROE

DIAL 33% 11% 31% 64% 0.54 16%

SLT 33% 7% 33% 25% 0.92 7%

Airtel 33% 6% 20% 129% 1.89 9%

AIS 43% 25% 8% 47% 1.05 84%

Reliance 32% 5% 29% 96% 0.56 2%

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

11

Appendix – Table of Content page

HISTORICAL AND PRO FORMA FINANCIAL STATEMENTS 12 – 14

Appendix 01 : Statement of Comprehensive Income

Appendix 02 : Balance sheet

Appendix 03 : Statement of Cash Flow

VALUATION 15 - 19

Appendisx 04 – Valuation

Appendix 05 – Business Model

Appendix 07 : Peer Comparison

OTHER TOPICS 20 – 22

Appendix 08 – Corporate Governance

Appendix 09 – Sustainability Report

INDUSTRY OVERVIEW AND COMPETITIVE POSITIONING 23 - 24

Appendix 10– Horizontal Business Models

Apendix 11 – Porter’s five forces

Appendix 12 – SWOT of Sri Lanka

FINANCIAL ANALYSIS 25

Appendix 13 – Key Financial Ratios

INVESTMENT RISK 26

Appendix 14 – Foreign Exchange loss expected

Appendix 15 – Risk Mitigation

ABBREVIATION 27

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

12

HISTORICAL AND PRO FORMA FINANCIAL STATEMENTS

Appendix 1: Statement of Comprehensive Income (In millions)

(LKR 000 000) 2010 2011 2012 2013E 2014E 2015E 2016E 2017E 2018E

Revenue 41,423 45,412 56,345 62,552 71,443 81,146 89,261 96,402 103,150

Direct costs 23,600 24,949 32,216

35,029

39,294

43,413

46,416

48,683

50,543

Gross profit 17,822 20,463 24,129 27,523 32,149 37,733 42,845 47,719 52,606

Gross profit Margin 43% 45% 43%

Distribution Costs 5,432 6,265 7,601

8,423

9,621

10,927

12,020

12,982

13,890

Administrative Costs 7,112 8,074 9,865

10,556

11,295

12,085

13,292

14,448

15,700

Other Income 134 83 138

153

175

199

219

236

253

Operating Profit 5,413 6,207 6,801 8,697 11,409 14,919 17,752 20,526 23,269

Finance Costs – Net 125 769 2,727 3,683 2,782 2,332 3,107 3,355 3,604

Share of (loss)/profit associates 0 10 9 2 4 6 4 4 4

Profit before income tax 5,538 5,448 4,066 5,016 8,631 12,593 14,648 17,175 19,670

Income Tax 490 579 1,965 752 1,295 1,889 2,197 2,576 2,951

Profit for the year 5,047 4,870 6,030 4,263 7,336 10,704 12,451 14,598 16,720

Other comprehensive income 0 19 9 0 0 0 0 0 0

Total comprehensive income for

the year 5,047 4,888 6,021 4,263 7,336 10,704 12,451 14,598 16,720

Margin 12% 11% 11% 7% 10% 13% 14% 15% 16%

EBITDA 11,468 16,512 18,357 23,569 29,060 34,969 39,979 45,102 49,860

EBITD Margin 28% 36% 33% 38% 41% 43% 45% 47% 48%

EPS 0.63 0.61 0.75 0.53 0.92 1.34 1.56 1.83 2.09

DPS 0.25 0.34 0.21 0.34 0.46 0.62 0.73 0.84 0.25

Dividend payout ratio 32% 42% 45% 40% 37% 34% 40% 40% 40%

Source: Company Documents, Student Estimates

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

13

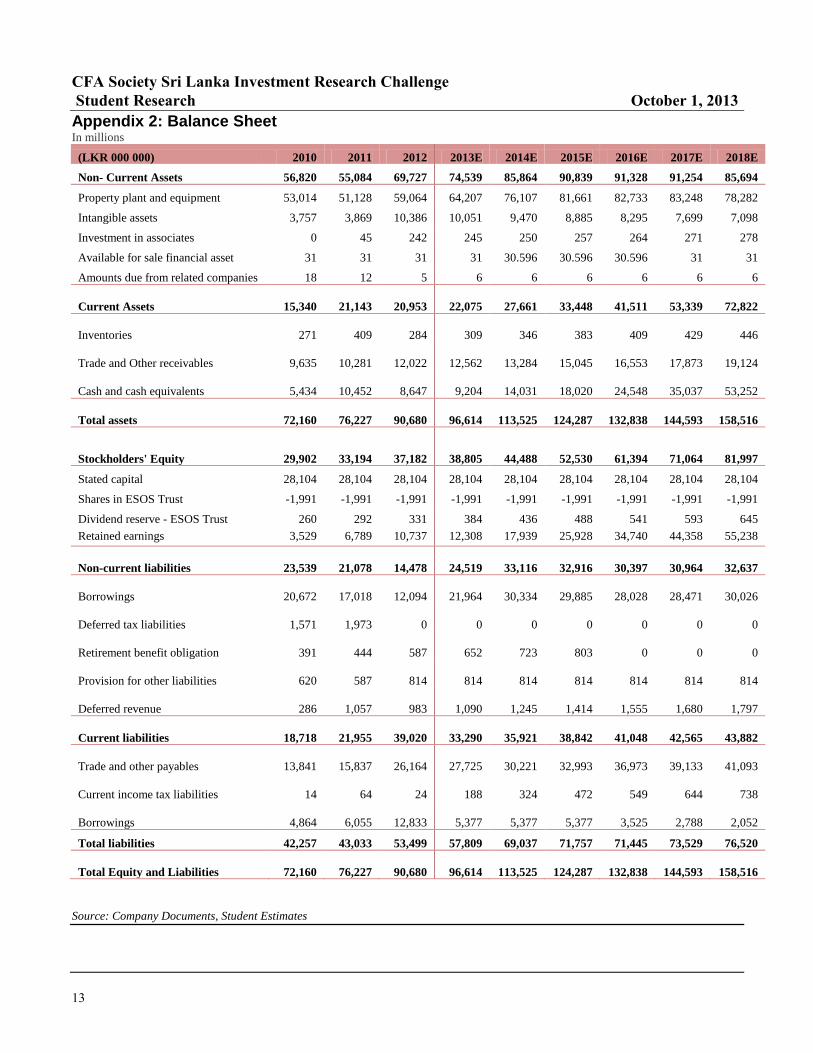

Appendix 2: Balance Sheet In millions

(LKR 000 000) 2010 2011 2012 2013E 2014E 2015E 2016E 2017E 2018E

Non- Current Assets 56,820 55,084 69,727 74,539 85,864 90,839 91,328 91,254 85,694

Property plant and equipment 53,014 51,128 59,064 64,207 76,107 81,661 82,733 83,248 78,282

Intangible assets 3,757 3,869 10,386 10,051 9,470 8,885 8,295 7,699 7,098

Investment in associates 0 45 242 245 250 257 264 271 278

Available for sale financial asset 31 31 31 31 30.596 30.596 30.596 31 31

Amounts due from related companies 18 12 5 6 6 6 6 6 6

Current Assets

15,340

21,143

20,953 22,075 27,661 33,448 41,511 53,339 72,822

Inventories

271

409

284

309

346

383

409

429

446

Trade and Other receivables

9,635

10,281

12,022 12,562 13,284 15,045 16,553 17,873 19,124

Cash and cash equivalents

5,434

10,452

8,647 9,204 14,031 18,020 24,548 35,037 53,252

Total assets

72,160

76,227

90,680 96,614 113,525 124,287 132,838 144,593 158,516

Stockholders' Equity

29,902

33,194

37,182 38,805 44,488 52,530 61,394 71,064 81,997

Stated capital 28,104 28,104 28,104 28,104 28,104 28,104 28,104 28,104 28,104

Shares in ESOS Trust -1,991 -1,991 -1,991 -1,991 -1,991 -1,991 -1,991 -1,991 -1,991

Dividend reserve - ESOS Trust 260 292 331 384 436 488 541 593 645

Retained earnings 3,529 6,789 10,737 12,308 17,939 25,928 34,740 44,358 55,238

Non-current liabilities

23,539

21,078

14,478 24,519 33,116 32,916 30,397 30,964 32,637

Borrowings

20,672

17,018

12,094 21,964 30,334 29,885 28,028 28,471 30,026

Deferred tax liabilities

1,571

1,973 0 0 0 0 0 0 0

Retirement benefit obligation

391

444

587 652 723 803 0 0 0

Provision for other liabilities

620

587

814 814 814 814 814 814 814

Deferred revenue

286

1,057

983 1,090 1,245 1,414 1,555 1,680 1,797

Current liabilities

18,718

21,955

39,020 33,290 35,921 38,842 41,048 42,565 43,882

Trade and other payables

13,841

15,837

26,164 27,725 30,221 32,993 36,973 39,133 41,093

Current income tax liabilities

14

64

24

188

324

472

549

644

738

Borrowings

4,864

6,055

12,833

5,377

5,377

5,377

3,525

2,788

2,052

Total liabilities 42,257 43,033 53,499 57,809 69,037 71,757 71,445 73,529 76,520

Total Equity and Liabilities

72,160

76,227

90,680 96,614 113,525 124,287 132,838 144,593 158,516

Source: Company Documents, Student Estimates

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

14

Appendix 3: Statement of Cash Flows In millions

(LKR 000 000) 2010 2011 2012 2013E 2014E 2015E 2016E 2017E 2018E

Cash generated from operations 14,789 17,087 21,727 24,736 31,023 36,192 38,515 41,743 45,315

Interest received 86 384 347 307 307 307 412 450 488

Interest paid -665 -355 -286 -1,371 -1,370 -1,556 0 0 0

TDC refunds received -95 1,650 0 0 0 0 0 0 0

Tax paid 210 -106 -126 -588 -1,159 -1,740 -2,120 -2,481 -2,857

Retirement benefit obligation paid -43 -20 -80 0 0 0 0 0 0

Net cash generated from operations 14,283 18,640 21,583 23,083 28,801 33,203 36,807 39,712 42,946

Purchase of property, plant and

equipment -78 -8,335 -17,248 -18,766 -28,577 -24,344 -22,315 -24,100 -20,630

Purchase of intangible assets -23 -385 -161 -114 -114 -114 -114 -114 -114

Investment in associates -13

-11

-156 0 0 0 0 0 0

Expenditure incurred on capital work-

in-progress -6,689 0 0 0 0 0 0 0 0

Acquisition of subsidiary, net of cash

acquired 0 0 -3,363 -800 -280 -560 -280 -280 -280

Proceeds from sale of subsidiary 0 69 0 0 0 0 0 0 0

Proceeds from sale of property, plant

and equipment 55 10 63 0 0 0 0 0 0

Net cash used in investing activities -6,748 -8,651 -20,864 -19,680 -28,971 -25,018 -22,709 -24,494 -21,024

Repayment of finance leases -26 -6 -11 0 0 0 0 0 0

Repayment of borrowings -7,899 -3,161 -3,917 -16,931 -7,256 -6,700 -5,360 -4,676 -5,651

Proceeds from borrowings 3,492 1,096 4,885 26,800 15,627 6,251 3,503 5,118 7,207

Net Current Borrowings 0 0 0 -7,456 0 0 -1,852 -737 -737

Redemption of rated cumulative

redeemable preference shares -1,250 -1,250 -1,250 0 0 0 0 0 0

Dividend paid to equity holders -343 -1,629 -2,036 -2,687 -1,705 -2,714 -3,639 -4,980 -5,839

Dividend received by ESOS Trust 0 32 40 52 52 52 52 52 52

Dividend paid to rated cumulative

redeemable - preference shareholders 0 -177 -83 0 0 0 0 0 0

Direct cost on share issue 0 0 -38 -5 0 0 0 0 0

Net cash used in financing activities -6,025 -5,095 -2,409 -227 6,718 -3,111 -7,296 -5,222 -4,968

Net (decrease) / increase in cash and

cash equivalents 1,510 4,893 -1,691 3,176 6,546 5,072 6,799 9,993 16,951

Movement in cash and cash

equivalents

At start of the year 3,019 4,476 9,406 8,647 9,204 14,031 18,020 24,548 35,037

(Decrease) / increase 1,510 4,893 -1,691 3,176 6,546 5,072 6,799 9,993 16,951

Exchange (losses) / gains on cash and

cash equivalents -53 37 -347 -2,619 -1,719 -1,083 -271 496 1,264

At end of the year 4,476 9,406 7,368 9,204 14,031 18,020 24,548 35,037 53,252

Source: Company Documents, Student Estimates

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

15

Valuation

Appendix 04 – Valuation

Present value of firm

103,551,812

Debt

24,926,896

Cash

8,647,069

Investment in Associates

242,173

Present value of equity

87,514,158

No. of shares

7,985,206

Value per share

10.96

Upside in share price 28.9%

2013E 2014E 2015E 2016E 2017E 2018E

Revenue 62,552,334 71,443,271 81,146,238 89,260,862 96,401,731 103,149,852

YoY growth 14.2% 13.6% 10.0% 8.0% 7.0%

EBIT 8,696,973 11,409,021 14,919,068 17,751,541 20,525,803 23,269,310

EBIT margin 13.9% 16.0% 18.4% 19.9% 21.3% 22.6%

EBIT (1-t) 7,392,427 9,697,667 12,681,208 15,088,810 17,446,933 19,778,914

Effective tax rate 15.0% 15.0% 15.0% 15.0% 15.0% 15.0%

Depreciation 14,871,640 17,650,747 20,049,829 22,226,990 24,575,756 26,590,923

As a % of revenue 23.8% 24.7% 24.7% 24.9% 25.5% 25.8%

Capital expenditure (19,679,663) (28,971,271) (25,017,834) (22,709,178) (24,494,396) (21,023,933)

Capex to revenue 31.5% 40.6% 30.8% 25.4% 25.4% 20.4%

Working capital

investment

863,005 1,461,534 621,555 2,113,420 567,380 457,431

-1.4% -2.0% -0.8% -2.4% -0.6% -0.4%

Net cash flow 3,447,409 (161,323) 8,334,757 16,720,041 18,095,673 25,803,334

Terminal value 168,560,764

Discount factor 0.8587 0.7373 0.6331 0.5436 0.4668 0.4008

PV 2,960,138 (118,942) 5,276,551 9,088,948 8,446,370 77,898,747

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

16

Appendix 05 – Business Model

Revenue

Segment Subscriber ARPU Market Share

Mobile Subscriber growth of 2%CAGR over FY13E – FY18E

1. Voice Saturating with current penetration levels nearing

100%

2.Data revenue to increase mainly due to

Smartphone penetration FY18E - 40%

Growing middle class

ARPU growth of 9%CAGR

over FY13E – FY18E

1.RPU would deteriorate

2.MoU would increase as the

rate cuts make mobile usage

cheaper

48%

(57% Revenue

share)

Expect – Data

revenue to

increase to 25% -

30% of total

revenue

Broadband and

Fixed line

Subscriber growth of 2%CAGR over FY13E – FY18E

1.100% penetrated. But DIAL is targeting the corporates

with Suntel acquisition. With the economic development we

expect the growth in the service and industry sector.

2.4G technology is expected to attract competitor’s internet

users.

ARPU growth of 4%CAGR

over FY13E – FY18E

1.4G perceived as a high speed

internet. DIAL’s broadband

revenue would improve

16%

(2nd player in

terms of revenue

share)

Pay TV Subscriber growth of 23%CAGR over FY13E – FY18E

1. DIAL’s current marketing campaign penetrates in to low

income earning population.

2. Improving entertainment industry and the hotel industry

which subscribe to DTV over competitive pay TV brands

3. Technological advancements and Number of channels

offered is more compared to competitors.

ARPU growth of 0%CAGR

over FY13E – FY18E

1. Still at the initial stage of the

industry cycle.

2. making offers with rate cuts

and pre – paid options being

introduced

75%

(Market leader)

Joint Venture – Anything.lk – CAGR 15%

Joint venture with Anything.lk was entered in to in the FY 12. This venture enhances the E-Commerce and M-Commerce segments of the

country. In our opinion this is a revenue source that could expect a boom in its performance with the

rapid increase in Smartphone penetration

Increasing SMEs

GDP growth.

Appendix 06 - WACC

A) WACC Computation

Financing

Method

Cost Weight Value

Ke 21.0% 0.5 10.5%

Kd 13.0% 0.5 6.5%

DCF 16.5%

Current capital structure - Debt 40% and Equity 60%.

Target Capital Structure – Debt 50% and Equity 50%

B) Cost of Equity Estimation

We assume the capital market to be efficient therefore we utilize the CAPM in estimating the Ke.

Risk Free (Rf) 12%

Beta 1.1

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

17

Market Risk Premium (Rp) 9%

Risk Free Rate - 5 Year T – Bond rate

DIAL Beta Calculation

Past 6 Year Beta – 1.065

Expect Beta – 0.9 – 1.1 (Due to behavior of DIAL’s share with the ASPI coupled with the maturing industry with great potential to

reduce risk we expect DIAL’s beta to be trading in the range of 0.9 – 1.1.)

Market Risk Premium Calculation

Method 01 - Country Bond Default Spread

adjust the mature market risk premium for the emerging market default spread.

Therefore in arriving at Sri Lankan equity risk premium we have added 4% Sri Lankan Bond default spread to US risk premium of 4.8%.

(Source : (A. Damodaran) - http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/ctryprem.html)

Method 02 – Relative Country Risk Premium

According to this method we add the relative country risk (Standard deviation of Equity/Standard deviation of Bond) to the risk premium

of the mature market.

(Source : http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/ctryprem.html)

Sri Lanka Country risk premium 6%

US risk Premium 6%

Total 12%

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

18

Method 03 – Macro – economic conditions

Variables

Expected Inflation (EINFL) 6%

Expected growth rate in real earnings per share (EGREPS) 8%

Expected growth rate in PE (EGPE) 0

Expected income component (EINC) 12%

Risk Free rate (Rf) 10%

Expected Inflation and Expected growth rate in real earnings per share was estimated based on the senior government officials

statements made regarding the economic.

Expected growth rate in PE – we assume the capital market to be efficient in the long run therefore the growth in PE to be 0.

Expected income component was arrived at by assuming the average turnover in the CSE over the period of past 6 years.

Risk Free rate is the 5 year T – Bond rate offered by the Central Bank.

EINFL) (1+EGREPS)(1+EGPE) – 1]+ ENIC} – Rf

Conclusion

Historically Sri Lanka’s Rp moves between 5% - 9% during a bearish market Rp of 8% could be observed. However we are optimistic on

DIAL risk premium at 9% as DIAL being a company with a 3.09% of total market capitalization with a large public float and good

governance would be highly attractive to foreign investors.

C) Cost of Debt Estimation

Debt Category Loan Interest Rate Interest Cost

Sri Lankan Rupee Loan 15,626,926 11%* 1,718,962

USD Loan 30,825,000 2%* 616,500

Total 46,451,926 2,335,462

*Interest rate for Sri Lankan rupee loan was assumed at the AWPLR and the USD loan interest was the average interest rate DIAL had in

its previous USD loans

Cost of debt adjusted for Taxes (Kd)

Kd 5%

Tax 15%

Kd(1-t) 4.27%

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

19

Appendix 07 – Peer Comparison

A) Peer Company Business Characteristic Comparison

DIAL:SL SLTL:SL RCOM:BO BHAR:IN ADVANC:TB

Market Position Market Leader and

First mover

Government 49.5%

control Competitive

in Fixed line

Second largest

player in the market

Market leader and

First mover

Market leader and

First Mover

(44%Subscriber

market share 54%

Revenue share)

Network Coverage 2G – 97%

3G – 82%

4G – Introduced in

2012

2G – 97%

3G – 80%

4G –introduced in

2012

2G – 100%

3G -

2G – 100%

3G -

4G – introduced in

2013 April

2G–100%

3G – Yet to introduce

Subscriber CAGR Mobile – 6.63%

Fixed – 32%

TV – 21%

Megaline – 4.67%

CDMA – (3.1%)

Broadband - 28%

PEOTV – 65%

Wireless – 35%

Broadbad – 14%

Mobile – 45%

Broadband –15%

TV – 160%

7.0%

Revenue Model Mobile – 87%

Fixed – 7%

TV – 5%

Megaline – 52%

CDMA – 26.7%

Broadband – 17.4%

PEOTV – 3.5%

Wireless – 67%

Broadband – 33%

Voice Revenue –

78%

Other – 22%

Voice – 72%

Non Voice – 20.2%

International – 3.1%

Capex 4G network, Fiber

optic and

International

Bandwidth

4G , Next

Generation Network

implementing all

access network in to

a single platform,

Fiber optic cables,

Internet protocol

enabled PEO Tv

facility,

Infrastructure

sharing agreements,

Introducing of

Reliance 3G Tablet

Increase global

foot print – African

countries

3G and 4G roll out

Obtaining the license

to operate

Roll out of 3G

Dividend 40% Payout ratio 37.9% Payout ratio 34.2% Payout Ratio 9% Payout ratio 100% Payout ratio

Tele density 79.82% 79.82%

B) DIAL Value Relative to SLTL

Company PE EV/EBITDA PB

SLTL 19.87 5.32 1.47

DIAL 11.1 4.5 1.8

Discount 44% 15% (22%)

Peer

Multiple

DIAL

(Accounting

Information)

Price W Price * W

Peer PE

19.87

0.75

14.98 0.35 5.24

Peer

EV/EBITDA

5.32

2.30

12.23 0.5 6.12

Peer P/B

1.47

4.66

6.84 0.15 1.03

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

20

12.39

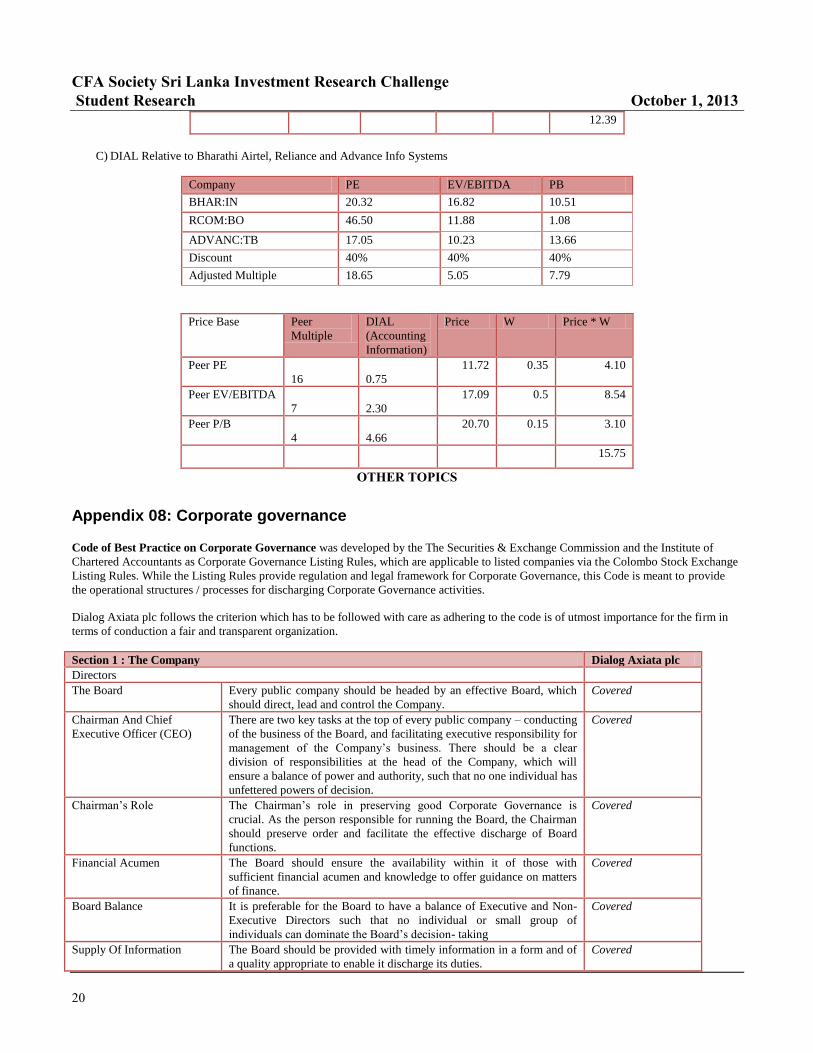

C) DIAL Relative to Bharathi Airtel, Reliance and Advance Info Systems

Company PE EV/EBITDA PB

BHAR:IN 20.32 16.82 10.51

RCOM:BO 46.50 11.88 1.08

ADVANC:TB 17.05 10.23 13.66

Discount 40% 40% 40%

Adjusted Multiple 18.65 5.05 7.79

Price Base Peer

Multiple

DIAL

(Accounting

Information)

Price W Price * W

Peer PE

16

0.75

11.72 0.35 4.10

Peer EV/EBITDA

7

2.30

17.09 0.5 8.54

Peer P/B

4

4.66

20.70 0.15 3.10

15.75

OTHER TOPICS

Appendix 08: Corporate governance Code of Best Practice on Corporate Governance was developed by the The Securities & Exchange Commission and the Institute of

Chartered Accountants as Corporate Governance Listing Rules, which are applicable to listed companies via the Colombo Stock Exchange

Listing Rules. While the Listing Rules provide regulation and legal framework for Corporate Governance, this Code is meant to provide

the operational structures / processes for discharging Corporate Governance activities.

Dialog Axiata plc follows the criterion which has to be followed with care as adhering to the code is of utmost importance for the firm in

terms of conduction a fair and transparent organization.

Section 1 : The Company Dialog Axiata plc

Directors

The Board Every public company should be headed by an effective Board, which

should direct, lead and control the Company.

Covered

Chairman And Chief

Executive Officer (CEO)

There are two key tasks at the top of every public company – conducting

of the business of the Board, and facilitating executive responsibility for

management of the Company’s business. There should be a clear

division of responsibilities at the head of the Company, which will

ensure a balance of power and authority, such that no one individual has

unfettered powers of decision.

Covered

Chairman’s Role The Chairman’s role in preserving good Corporate Governance is

crucial. As the person responsible for running the Board, the Chairman

should preserve order and facilitate the effective discharge of Board

functions.

Covered

Financial Acumen

The Board should ensure the availability within it of those with

sufficient financial acumen and knowledge to offer guidance on matters

of finance.

Covered

Board Balance It is preferable for the Board to have a balance of Executive and Non-

Executive Directors such that no individual or small group of

individuals can dominate the Board’s decision- taking

Covered

Supply Of Information The Board should be provided with timely information in a form and of

a quality appropriate to enable it discharge its duties.

Covered

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

21

Appointments To The Board There should be a formal and transparent procedure for the appointment

of new Directors to the Board.

Covered

Re Election All Directors should be required to submit themselves for re-election at

regular intervals and at least once every three years.

Covered

Appraisal Of Board

Performance

Boards should periodically appraise their own performance in order to

ensure that Board responsibilities are satisfactorily discharged.

Covered

Disclosure Of Information In

Respect Of Directors

Shareholders should be kept advised of relevant details in respect of

Directors.

Covered

Appraisal Of Chief Executive

Officer (CEO)

The Board should be required, at least annually, to assess the

performance of the CEO.

Covered

Directors’ Remuneration

Remuneration Procedure Companies should establish a formal and transparent procedure for

developing policy on executive remuneration and for fixing the

remuneration packages of individual Directors. No Director should be

involved in deciding his/her own remuneration.

Covered

The Level And Make Up Of

Remuneration

Levels of remuneration of both Executive and Non-executive Directors

should be sufficient to attract and retain the Directors needed to run the

Company successfully. A proportion of Executive Directors’

remuneration should be structured to link rewards to corporate and

individual performance.

Covered

Disclosure Of Remuneration

The Company’s Annual Report should contain a Statement of

Remuneration Policy and details of remuneration of the Board as a

whole

Covered

Relations With Shareholders

Constructive Use Of The

Annual General Meeting

(AGM) And

Conduct Of General

Meetings

Boards should use the AGM to communicate with shareholders and

should encourage their participation.

Covered

Major Transactions Further to compliance with the requirements under the Companies Act,

directors should disclose to shareholders all proposed corporate

transactions, which if entered into, would materially alter/vary the

Company’s net assets base or in the case of a company with

subsidiaries, the consolidated group net asset base.

Covered

Accountability And Audit

Financial Reporting The Board should present a balanced and understandable assessment of

the Company’s financial position, performance and prospects.

Covered

Internal Control The Board should maintain a sound system of internal control to

safeguard shareholders’ investments and the Company’s assets.

Covered

Audit Committee The Board should establish formal and transparent arrangements for

considering how they should select and apply accounting policies,

financial reporting and internal control principles and maintaining an

appropriate relationship with the Company’s Auditors.

Covered

Code Of Business Conduct

& Ethics

Companies must adopt a Code of Business Conduct & Ethics for

directors, and members of the senior management team and must

promptly disclose any waivers of the Code for directors or others.

Covered

Corporate Governance

Disclosures

Directors should be required to disclose the extent to which the

Company adheres to established principles and practices of good

Corporate Governance.

Covered

Section 2 : Shareholders

Institutional Investors

Shareholder Voting Institutional shareholders have a responsibility to make considered use

of their votes and should be encouraged to ensure their voting intentions

are translated into practice.

Covered

Evaluation Of Governance

Disclosures

When evaluating Companies’ governance arrangements, particularly

those relating to board structure and composition, institutional investors

should be encouraged to give due weight to all relevant factors drawn to

their attention.

Covered

Other Investors

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

22

Investing/ Divesting

Decision

Individual shareholders, investing directly in shares of companies

should be encouraged to carry out adequate analysis or seek

independent advice in investing or divesting decisions.

Covered

Shareholder Voting Individual shareholders should be encouraged to participate in General

Meetings of companies and exercise their voting rights.

Covered

Appendix 09 : Sustainability Reporting

The Global Reporting Initiative (GRI) is a leading organization in the sustainability field. GRI promotes the use of sustainability reporting

as a way for organizations to become more sustainable and contribute to sustainable development.

Within the years DIAL has been able to set targets as well as make progress to the set targets to an extent,

Economic

Introduce Vendor Code of Conduct - Vendor CoC introduced, incorporating requirements specified by ISO14001/SA8000.

Increase local procurement to 60% of total procurement -Local procurement spent was 37%.

Social

Increase regional employees to 25% of total employee base - Regional employee base increased to 23%.

Introduce human rights training- Few trainings on anti-sexual harassment were conducted.

Review whistle blowing policy and implement changes - Operationalization of whistle blowing policy reviewed through employee

focus-group discussions.

Distribute Sinhala and Tamil code of conduct booklets

Environment

Add 5 Green Base Stations to network -5 new sites added during 2012.

350 M-waste collection points by 2014 -120 collection points by end 2012.

Implement Environment Management System - Aspect-impact analysis complete.

Increase e-bill subscriber base by 25% - Achieved a 1222% growth in the e-bill subscriber base. Percentage of e-bill subscribers

increased from 1.58% to 20.93% in 2012 of the total base.

Reduce water consumption in office sites by 10% -Water consumption reduced by 7%. This maybe a result of the modified data

capturing system.

Add 300 more free cooling and hybrid sites to network - 70 more free cooling and hybrid sites added.

Introduce carbon calculator for customers-DIAL will carry this target to 2013 as progress was not made against the stated target.

Det Norske Veritas AS (‘DNV’) had also been commissioned by the Management of Dialog Axiata PLC for the assessment of Sustainable

business in their conclusion it was stated that Dialog Axiata PLC Sustainability Report - 2012, provides a fair representation of the

Company’s sustainability policies, objectives, management approach and performance during the reporting year. And it was confirmed that

the Report generally meets the requirements for GRI application level A+.

CFA Society Sri Lanka Investment Research Challenge

Student Research October 1, 2013

23

INDUSTRY OVERVIEW AND COMPETITIVE POSITIONING

Appendix 10 : Horizontal Business Models Network Guarantors

Offering network infrastructure and related services to other players

Capabilities:

Cost efficiency in the operation of their infrastructure

Scalability in replicating their technology platforms and operating models

Reliability in terms of network and IT availability and quality

Smoothly integrated IT platforms and applications

What next: Building these capabilities requires operators to make large investments in new fiber and LTE infrastructure, which may limit

competitors to government-led networking companies and operators willing to share costs with other like-minded players.

Business Enablers

Monetize assets by opening up their infrastructures and extending their business strategy.

Capabilities:

Ability to broker and manage relationships with different partners, offering tailored services to each

Flexibility and willingness to cater to the needs of partners with different business models

Capacity for aggregating platforms and services into attractive packages for its partners

Willingness to partner with others to augment portfolio of offerings

What next: Incumbents that have embraced the concept and plan to open up their networks and assets to third parties should build on their

partner management and wholesaling capabilities.

Experience Providers

Offer the best combination of targeted applications and content, and a high level of user experience.

Capabilities:

Ability to develop innovative new applications and services