Insured Savings/Checking Accounts Shaianne Kealoha Period 7.

9

Insured Savings/Checkin g Accounts Shaianne Kealoha Period 7

-

Upload

terence-parsons -

Category

Documents

-

view

215 -

download

0

Transcript of Insured Savings/Checking Accounts Shaianne Kealoha Period 7.

Insured Savings/Checking AccountsShaianne KealohaPeriod 7

What are insured savings and checking accounts?

• A checking account is an account at a bank against which checks can be withdrawn by the account depositor.• An insured savings account is an account that are

insured up to $100,000 by the Federal Deposit Insurance Corporation (FDIC). This means that if your bank goes bankrupt, you will still receive all the money in your account up to $100,000. Banks are insured by the FDIC, so your accounts are, too.

Checking Accounts – Limits• Account Balance• In order to open an account, most banks require you to have a starting

minimum balance. This balance may range anywhere from $1 – $25. • Liquidity• Money held in a checking account is very liquid and can be drawn using

checks, ATMs, debit cards, or heading straight to your bank teller. These accounts are often referred to as “demand accounts” or “transaction accounts”.

• Age Limits• There are no age restrictions on checking accounts. Most banks allow

minors to open one as long as a parent/guardian serves as a signatory adult.

• Interest• Generally, individuals cannot receive interest on a checking account.

There are, however, specialized checking accounts that carry interest, such as those for non-profit businesses.

Checking Accounts – Investors• Checking accounts are usually opened as personal accounts

for individuals looking for a safe and secure way to save their money.

• Parents and children may open joint checking accounts as a way to easily transfer funds (for allowance or in case of emergency). This also provides a safe and easy introduction to the formal banking system.

• Spouses/partners might open checking accounts in order to pay communal expenses and ensure both partners’ spendings are aimed towards financial goals and activities.

• Non-profit businesses could also make use of checking accounts because they are welcome to opening an interest-collecting checking account. For-profit businesses, however, are not.

• Generally, individuals do not make money from their checking accounts (unless they are non-profit business owners). Because they receive no interest, the money in their account is made solely from the money they put in/take out.

• On the other hand, banks make a lot of money off checking accounts. Because of the free start up and no minimum balance requirement after opening the account, depositors often pay little mind to their balance. This may result in overdrafts and bounced checks, where banks can charge a fee for profit. Also, because checking accounts don’t pay interest, it gives the banks a cheap source of money which they can then invest elsewhere.

• Because checking accounts are based solely on the depositor’s spendings/input, there is no “right time” to open an account.

Checking Accounts – Making Money/Economic Climate

Opening Checking Accounts

• At the Bank of Hawaii, you can open a free checking account.

• The minimum starting balance is $100, but after the account has been opened there is no minimum balance requirement.

• No monthly service fee• Free 24/7 online, phone, and

mobile banking

• Students may be able to open a free checking account.

• There is no monthly maintenance fee when you make at least one deposit of $250 monthly, or maintain an average daily balance of at least $1,500. Otherwise, there is a $12 monthly maintenance fee.

• Unlimited teller access• Online, mobile, and text banking• Over draft protection

Checking Account – Risks• Fees• Because banks offer free checking accounts, there are numerous financial

institution charges. Banks charge depositors overdraft fees when a check bounces or funds that do not exist are withdrawn. Also, using a non-bank ATM may result in a charge of a few dollars.

• Holds• When depositing a check, the bank may place a temporary hold on the

funds until the check is cleared. This can be problematic, especially if you need access to the money immediately.

• Theft• Checking accounts are highly susceptible to theft. Thieves can easily steal

checks and write them in your name, use a chemical to remove the ink and change the amount of the name of the person it is written to, take over your account information and be added on as a joint holder, or copy your information from blank checks such as your account number and routing number in order to have access to your account.

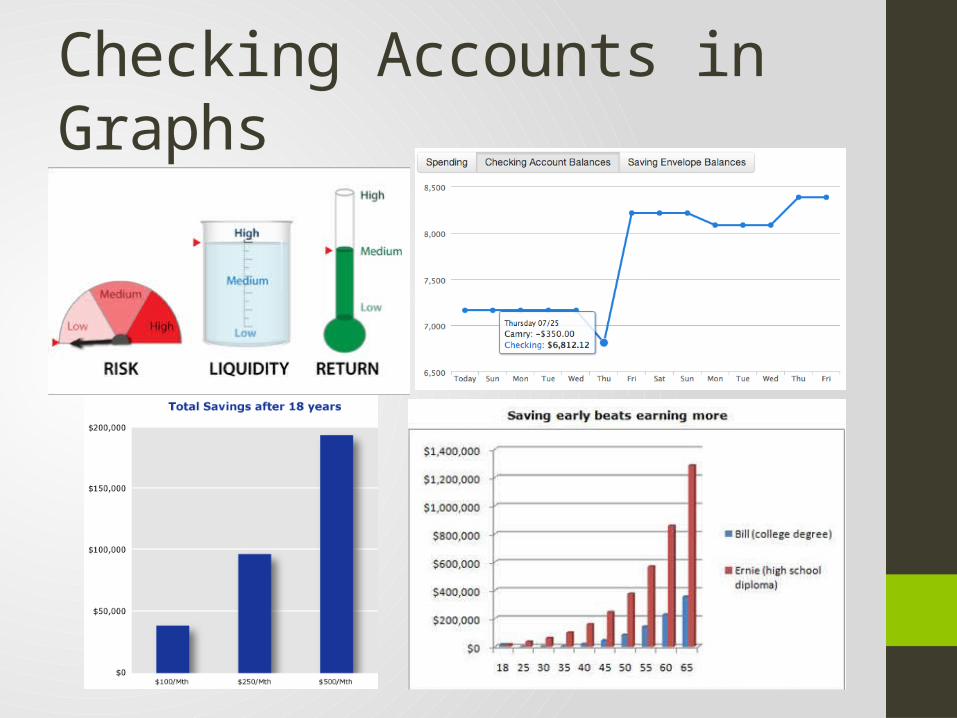

Checking Accounts in Graphs

Top 3 URL’s• The Cons of Checking Accounts• http://www.ehow.com/list_7489955_cons-checking-

accounts.html

• FAQ: Should We Open A Personal Joint Checking Account?• http://www.nerdwallet.com/blog/2012/personal-joint-checking/

• MyAccess Checking Account• https://www.bankofamerica.com/deposits/checking/myaccess-p

ersonal-checking-account.go