Institutional Presentation 4Q09 Roadshow Presentation ... · Roadshow Presentation February, 2010...

38

Roadshow Presentation February, 2010 Institutional Presentation 4Q09 Investor Relations

Transcript of Institutional Presentation 4Q09 Roadshow Presentation ... · Roadshow Presentation February, 2010...

Roadshow PresentationFebruary, 2010

Institutional Presentation 4Q09

Investor Relations

Agenda

Overview and Strategy

4Q09 Results

Peers Comparison and Conclusion

Appendix

2

Brazilian Credit Market

Dealing with the Global Crisis

Pag. 2

Pag. 6

Pag. 19

Pag. 13

Pag. 28

Pag. 32

36.6%

32.1%28.8%

26.8% 27.9%24.9% 26.4% 24.7%

22.0%24.0% 24.5%

28.1%30.2%

34.2%

41.3%44.6%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

106%

79%

57%

41% 40%32%

26% 24%

China Chile India Brazil Russia Colômbia Peru Mexico

Source: Central Bank, IPEAData, Euromonitor and International Monetary Fund.

(1) As of October, 2009

(2) 2007 data, except for Brazil, which is 2008 data(3) As of September, 2009

Overview of the Brazilian Credit Market vs. Daycoval

3

Credit Evolution in Brazil (% of GDP)1

Total Loans as % of GDP2

216 261335

465652

981

1,639

3,476

3,981 3,945

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Daycoval’s Strong Growth Profile...

Total Loan Portfolio1 - R$ mn

Banco Santos Crisis / Beginning of Payroll Loans

4

3%

9%

31%

15%

21%

29%

39% 40%

51%

67%

112%

28%

21%22%19%

14% 15%

-1%

2001 2002 2003 2004 2005 2006 2007 2008 2009

Brazilian Credit Volume Daycoval Loan Portfolio

Financial System Total Credit Operations vs. Banco Daycoval (% p.a.)

Banco Daycoval

CAGR: 40%

Change: 1,411%

Financial System

CAGR: 20%

Change: 319%

Accumulated since 2000

Branch Expansion Program

IPO

World Crisis

5

...Supported by Consistent Funding in Good and Bad Times

Total Funding1 - R$ mn

Eurobond

U$ 65mn

Eurobond U$ 120

mn / FIDC Middle

Banco Santos Crisis/

Creation of Daycoval Asset

Management

IPO / AB Loan-IFC

U$ 115 mn

Eurobond U$ 225

mn / World Crisis

Private Placement

R$ 410 mn1 Funding = Total Deposits + Foreign Issuances +

Borowing and Onlending (does not include FIDC)

180 217318

498

754

1,226

1,868

2,977

3,273

3,509

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

CAGR 00 – 09: 39.1%

Agenda

6

Overview and Strategy

4Q09 Results

Peers Comparison and Conclusion

Appendix

Brazilian Credit Market

Dealing with the Global Crisis

Daycoval’s Corporate Structure and Presence

27 Branches

Londrina - PR

Maceió - AL

Manaus - AM

Porto Alegre - RS

Recife - PE

Rio de Janeiro - RJ

Salvador - BA

Vitória - ES

Ribeirão Preto - SP

São Bernardo - SP

São Paulo – SP - HQ

Goiânia - GO

Guarulhos - SP

Campo Grande - MS

Caxias do Sul - RS

Cuiabá - MT

Curitiba - PR

Florianópolis - SC

Fortaleza - CE

Aracaju - SE

Belém - PA

Belo Horizonte - MG

Brasília - DF

Campinas - SP

Bom Retiro

Brás

Alphaville

7

National PresenceCapital Structure – December/09

65%

25%

9%

1%

Daycoval Holding Financeira S.A.Free-floatControlling Shareholders (Family Dayan) + Daycoval ExpertTreasury

Total Shares: 216 million shares

Start of the Second Shares Buyback Program in

October/09

First middle market bank to implement a ADR

Level I Program

Coverage by research analysts from 14 local and

international brokerage firms

593 employees

Daycoval’s Strategy

8

Pursue higher returns with the lowest possible risk

Maintain Low Leverage and High Liquidity policy

Maintain the quality of collaterals

Long term funding to match the growing payroll portfolio strategy

Focus and expected share gain along next years

Participate in the market expansion

Reduction of exposure

Auto

Payroll

Middle Market

9

Direct Credit to Consumers (DCC): the product complements the Bank´s operation for individuals

Direct Credit to Consumers

Financing of goods and services through partnershipswith a number of retailers, such as home furnishings,appliances, etc

Payment guaranteed by “pre-dated” checks at rates andterms that are competitive with the market

Partnerships with many shops, seeking to increase sales,offering the end consumer greater purchasing facilities

Total Loan Portfolio - R$ Million

6

10

16

2224

4Q08 1Q09 2Q09 3Q09 4Q09

10

Strategy: New Credit Products and Services

3691

139

241 239

622

2004 2005 2006 2007 2008 2009

Asset Management

11

Created in 2004 for the Bank’s clients who wereseeking sophisticated products customized for theirown profile, the system is supported by aspecialized team of staff members with deepunderstanding of the market.

Currently with total equity of approximately R$ 620million and has been launching new funds anddifferentiated products, such as portfoliomanagement.

Daycoval Asset ManagementAssets Under Management – R$ mn

CAGR 04 – 09: 76.8%

Ratings: raised by Standard&Poors and Fitch Ratings

Global ScaleLong Term BBShort Term B

National ScaleLong Term brAA-Short Term brA-2

Stable

November 2009

Global ScaleLong Term BBShort Term B

National ScaleLong Term A + (bra)Short Term F1 (bra)

Stable

December 2009

National ScaleLong Term AA-Short Term A-1

Stable

October 2009

Low Risk – mid-termIndex 11.11

January 2010

12

Agenda

13

Overview and Strategy

4Q09 Results

Peers Comparison and Conclusion

Appendix

Brazilian Credit Market

Dealing with the Global Crisis

14

Conservative Risk Profile and Improved Efficiency

Primary focus on liquidity

Raising of R$410mn through the issuance of a 5y private convertible note (Cartesian Capital Group, LLC, International Finance Corporation - IFC and Wolfensohn Capital Partners Holdings II)

Managing portfolio to match available funding

Strict credit policies

Strategic reduction of credit portfolio from 4Q08, with a gradual and more conservative recovery in production since 2Q09

Shorter tenors and improvement of collateral package for new loans

Non-renewal of defaulted loans and execution of guarantees

Effort to maintain low costs

Personnel and administrative expenses declined by 28.8% in 2009, compared to 2008

15

Conservative Recovery in Production since 2Q09

4,626

3,981

3,548 3,533 3,656

3,945 2,439

1,070 9691,172

1,262

1,579

500

1,000

1,500

2,000

2,500

3,000

3,500

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

3Q08 4Q08 1Q09 2Q09 3Q09 4Q09

Loan Portfolio Production

2,811

2,231

1,860 1,860 1,994

2,256 2,073

982864

1,0051,083

1,350

500

750

1,000

1,250

1,500

1,750

2,000

2,250

2,500

500

1,000

1,500

2,000

2,500

3,000

3Q08 4Q08 1Q09 2Q09 3Q09 4Q09

Middle Market Total Loans Production

869 858 853

899

957

1,052

183

68 83

139

158

203

0

50

100

150

200

250

300

350

400

500

600

700

800

900

1,000

1,100

3Q08 4Q08 1Q09 2Q09 3Q09 4Q09

Payroll Total Loans Production

946 892

835

774

706

637

184

20

20 19 18 26

0

50

100

150

200

250

200

300

400

500

600

700

800

900

1,000

3Q08 4Q08 1Q09 2Q09 3Q09 4Q09

Vehicles Total Loans Production

Total Loans - R$ million Middle Market + Others Loans - R$ million

Payroll Total Loans - R$ million Vehicles Total Loans - R$ million

16

Establishment of Provision - R$

MM1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 2008 2009

Middle Market + Trade Finance 12.5 17.2 28.9 44.4 38.6 40.9 36.7 (4.1) 103.0 112.2

Payroll 4.0 2.8 7.4 4.6 7.0 7.1 6.0 8.5 18.8 28.6

Auto 13.0 8.1 15.2 18.5 29.2 30.5 24.9 12.0 54.8 96.7

DCC - - 0.1 0.2 0.4 0.6 0.6 0.6 0.3 1.9

Total 29.5 28.1 51.6 67.7 75.2 79.1 68.2 17.0 176.9 239.5

Conservative Provisioning Measures Implemented

Write-offs - R$ MM 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 2008 2009

Middle Market + Trade Finance 6.1 8.7 6.6 21.3 20.6 26.4 29.8 37.6 42.7 114.2

Retail 2.7 4.1 6.8 11.8 19.5 21.9 29.6 34.5 25.4 105.7

Total 8.8 12.8 13.4 33.1 40.1 48.3 59.4 72.1 68.1 219.9

Write-offs / Total Loan Portfolio

(%)

0.2% 0.3% 0.3% 1.0% 1.3% 1.5% 1.8% 2.0% 2.0% 6.1%

Recovered Loans - R$ MM 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 2008 2009

Total 1.1 1.7 1.3 2.9 1.4 7.1 12.6 7.7 7.0 28.8

17

Overdue Loans > 60 days - R$ MM 1Q08 3

T

2Q08 3

T

3Q08 3

T

4Q08 1Q09 2Q09 3Q09 4Q09

Middle Market + Trade Finance 41.2 46.6 98.9 104.8 120.3 120.4 123.1 66.8

Payroll 3.0 3.4 3.9 4.8 5.4 6.5 6.2 6.8

Auto 4.2 8.0 12.7 17.3 21.7 25.7 25.3 21.4

DCC - - - 0.1 0.3 0.5 0.6 0.9

Total 48.4 58.0 115.5 127.0 147.7 153.1 155.2 95.9

Overdue Loans > 60 days / Total Loan 1.3% 1.3% 2.7% 3.7% 4.8% 4.9% 4.7% 2.6%

LLP Balance / Overdue Loans > 60 days (%) 196.7% 190.5% 128.7% 144.3% 147.9% 162.8% 166.2% 212.0%

Daycoval Overview

Loan D-H - R$ MM 1Q08 3

T

2Q08 3

T

3Q08 3

T

4Q08 1Q09 2Q09 3Q09 4Q09

Middle Market + Trade Finance 64.4 62.2 130.3 149.8 194.8 233.8 220.5 146.1

Payroll 18.0 17.9 21.1 23.0 26.4 28.2 25.3 30.7

Auto 39.3 46.4 66.5 86.7 112.7 126.4 119.1 97.2

DCC - - 0.1 0.5 0.9 1.5 1.7 1.9

Total 121.7 126.5 218.0 260.0 334.8 389.9 366.6 275.9

Loan D-H / Total Loan Portfolio (%) 3.3% 2.9% 5.0% 7.5% 10.8% 12.4% 11.0% 7.3%

18

Rating Loan - R$ MM % Provision - R$ MM

AA 115.0 3.1% -

A 1,577.2 42.0% 7.9

B 1,531.3 40.8% 15.3

C 127.9 3.4% 3.8

D 54.2 1.4% 5.4

E 37.4 1.0% 11.2

F 36.3 1.0% 18.2

G 23.1 0.6% 16.2

H 124.9 3.3% 124.9

Subtotal 3,627.3 96.5% 202.9

Credit Assignments 130.0 3.5% 1.0

Total 3,757.3 100.0% 203.9

Credit Portfolio QualityDecember/2009

Agenda

19

Overview and Strategy

4Q09 Results

Peers Comparison and Conclusion

Appendix

Brazilian Credit Market

Dealing with the Global Crisis

20

Liquidity: positive gap between liabilities and assets in maturities over the next 12 months

Average Term of

Loan Portfolio:

404 days

Cash Evolution - R$ Million Cash / Total Deposits – %

% Loan Portfolio - Outstanding Operations – 4Q09

Average Term of

Funding Portfolio:

516 days

% Funding - Outstanding Operations – 4Q09

1,138

1,674 1,511

1,708

1,372

4Q08 1Q09 2Q09 3Q09 4Q09

64.8

87.1

74.4 73.3

57.6

4Q08 1Q09 2Q09 3Q09 4Q09

33%

31%

29%

6% 1%

Up to 3 months From 3 to 12 monthsFrom 1 to 3 years From 3 to 5 yearsOver 5 years

19%

33%28%

15%

1% 4%

Up to 3 months From 3 to 12 monthsFrom 1 to 3 years From 3 to 5 yearsOver 5 years No maturity

56%27%

16%

1%

Middle Market / Trade FinancePayroll

Auto Loans

DCC

3,706 3,312 3,334 3,493 3,815

275 236 199 163

130

4Q08 1Q09 2Q09 3Q09 4Q09

54% 57% 62% 65% 68%

24% 23% 20% 17% 11%

22% 20% 18% 18% 21%

4Q08 1Q09 2Q09 3Q09 4Q09

Total Deposit Foreign IssuancesBorrowing and Onlending

Funding – R$ MillionBreakdown of Funding

Loan Portfolio - R$ MillionBreakdown of Loan Portfolio – 4Q09 (*)

(*) includes credit assignmentsCredit assignments

3,273 3,5673,2643,377 3,509

3,9813,548 3,533 3,656

3,945

Funding & Credit Portfolio: volume of the portfolio returns to 2008’s level

21

Funding (R$ MM) 4Q09 3Q09 Chg. %

Total Deposits 2,381.8 2,331.4 2.2%

Demand Deposits + Other Deposits 124.7 92.0 35.5%

Time Deposits 2,122.5 2,088.7 1.6%

Interbank Deposits 134.6 150.7 -10.7%

Foreign Issuances 373.4 589.5 -36.7%

Borrowing and Onlending 753.6 646.1 16.6%

Total 3,508.8 3,567.0 -1.6%

Average Ticket – Middle Market + Trade Finance – 4Q09Middle Market + Trade Finance - R$ Million

Sectors Breakdown – Middle Market – 4Q09 Geographic Distribution – Middle Market – 4Q09

Middle Market + Trade Finance: sector’s recovery continues to be consistent

22

2,028 1,689 1,705 1,787

2,043

197

171 155 185

189

4Q08 1Q09 2Q09 3Q09 4Q09

Middle Market Trade Finance

2,2251,972

1,8601,860

2,232

59%

13%

12%

10%

6%Southeast

South

Northeast

Mid-west

North

42%

33%

18%

7%Industry

Services

Commerce

Other

Final Balance R$ Per

Volume

Per

Client

< 500,000 6.8% 61.7%

500,000 to 1 million 8.1% 13.3%

1 to 3 million 22.3% 15.6%

3 to 5 million 11.8% 3.7%

5 to 10 million 22.3% 3.8%

> 10 million 28.7% 1.9%

Total 100.0%

40%

15%

22%

9%

7%6%

1%

INSS

State Government

Army

Law Courts and Legislative Bodies

Municipalities

Other

Private

23

Daycred Payroll: Government related risk dictate the pace of origination

Total Origination – R$ Million Total Origination 2009 – R$ 203 mn

Total Loan Portfolio (*) - R$ Million Total Loan Portfolio 2009 – R$ 1,052 mn

(*) Includes credit assignments in all of the quarters (R$ 71 million in 4Q09)

858 854 899 9571,052

4Q08 1Q09 2Q09 3Q09 4Q09

6583

139158

203

4Q08 1Q09 2Q09 3Q09 4Q09

27%

17%45%

5%5%

1%

INSS

State Government

Army

Law Courts and Legislative Bodies

Municipalities

Private + Others

24

Daycred Vehicles: reducing the portfolio continues to be the strategy

Total Origination - R$ Million

Total Loan Portfolio (*) – R$ Million Total Loan Portfolio 4Q09 - R$ 637 million

(*) Includes credit assignments in all of the quarters (R$ 59 million in 4Q09)

892 835774

706637

4Q08 1Q09 2Q09 3Q09 4Q09

20 20 19 18

26

4Q08 1Q09 2Q09 3Q09 4Q09

66%21%

13%

Small Vehicles

Heavy-duty Vehicles

Motorcycles

Liquidity of Auto Loans Portfolio -

Aug/06 to Set/09R$ MM %

%

Accum.

PMT´s received in advance 282.3 33.6% 33.6%

PMT´s received on date of maturity 111.2 13.2% 46.8%

PMT´s received with delay of 30 days 258.5 30.8% 77.6%

PMT´sreceived with delay of 60 to 120 days 96.6 11.5% 262.1%

PMT´s received with delay over 120 days 16.6 2.0% 91.1%

PMT´s overdue 75.1 8.9% 100.0%

Liquidity of the Auto Loans Portfolio 765.2 91.1%

Outstanding PMT´s Total Amount 840.3 100.0%

25

Efficiency Ratio: increase in costs did not force the indicator during the quarter

4Q09 3Q09 Chg. % 4Q08 Chg. % 2009 2008 Chg. %

Personnel Expenses (17.8) (15.5) 14.7% (18.9) -6.0% (63.9) (71.0) -10.0%

Other Administrative Expenses (17.5) (15.7) 11.6% (18.7) -6.5% (65.8) (68.9) -4.6%

Subtotal (35.3) (31.2) 13.1% (37.6) -6.2% (129.7) (139.9) -7.3%

Payroll (4.9) (6.1) -19.9% (10.0) -51.2% (23.6) (58.0) -59.3%

-1.5%Auto Loan (4.0) (4.5) -11.3% (7.7) -47.9% (18.7) (45.5) -58.8%

DCC (0.4) (0.4) 0.0% (0.1) n.a. (1.3) (0.2) n.a.

Comission Expenses (total)(1) (9.3) (11.0) -15.7% (17.8) -47.9% (43.6) (103.7) -58.0%

Total (44.6) (42.2) 5.6% (55.4) -19.6% (173.3) (243.6) -28.9%

Efficiency Ratio - %

30.3

21.7 22.723.2 22.6

33.0 30.328.0 25.8

22.5

4Q08 1Q09 2Q09 3Q09 4Q09

Quarterly Last 12 months

26

Profitability: increase of all indicators in the quarterly and annual variations

Return on Average Equity (ROAE) - %

Net Income - R$ Million

Net Interest Margin (NIM) - %

20.442.0

82.5

200.2 211.1

4Q08 3Q09 4Q09 2008 2009

5.1

10.7

21.4

12.6 12.9

4Q08 3Q09 4Q09 2008 2009

11.4 12.2 13.010.6

12.1

4Q08 3Q09 4Q09 2008 2009

27

Capital Structure: maintenance of a low level of leverage

Basel Index - %Shareholders’ Equity – R$ Million

Loan Portfolio / Shareholders’ Equity - times

2.21.9 1.9 2.0 2.1

4Q08 1Q09 2Q09 3Q09 4Q09

28.2 30.1 30.5 29.3 28.6

4Q08 1Q09 2Q09 3Q09 4Q09

1,607.2 1,634.1 1,631.1 1,646.3 1,692.7

4Q08 1Q09 2Q09 3Q09 4Q09

Agenda

28

Overview and Strategy

4Q09 Results

Peers Comparison and Conclusion

Appendix

Brazilian Credit Market

Dealing with the Global Crisis

Source: Banks reports

1. as of December 2009

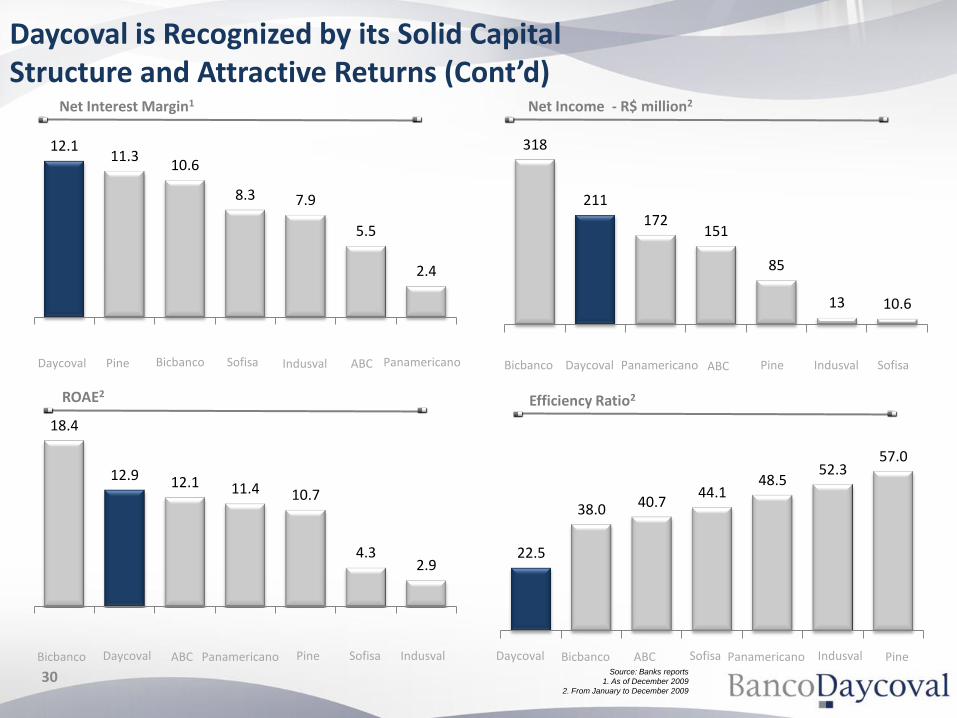

Daycoval is Recognized by its Solid Capital Structure and Efficiency

29

Loan Portfolio (R$bn)1

BIS Ratio1Shareholders’ Equity (R$bn)1

Loan Portfolio / Shareholder´s Equity 1

1.81.7

1.6

1.2

0.80.7

0.4

Bicbanco Daycoval Panamericano ABC Pine Sofisa Indusval

28.6

22.5

17.0 17.2 16.0 15.6 14.6

BicbancoDaycoval Panamericano ABCPineSofisaIndusval

10.09.1

8.5

4.1 3.93.0

1.7

Bicbanco DaycovalPanamericano ABC Pine Sofisa Indusval

2.33

3.93 4.284.99 5.16

6.336.98

BicbancoDaycoval Panamericano ABCPineSofisaIndusval

Source: Banks reports

1. As of December 2009

2. From January to December 2009

Daycoval is Recognized by its Solid Capital Structure and Attractive Returns (Cont’d)

30

ROAE2Efficiency Ratio2

Net Income - R$ million2Net Interest Margin1

12.111.3

10.6

8.3 7.9

5.5

2.4

BicbancoDaycoval PanamericanoABCPine Sofisa Indusval

18.4

12.9 12.1 11.4 10.7

4.32.9

Bicbanco Daycoval PanamericanoABC Pine Sofisa Indusval

22.5

38.0 40.744.1

48.552.3

57.0

BicbancoDaycoval PanamericanoABC PineSofisa Indusval

318

211

172151

85

13 10.6

Bicbanco Daycoval Panamericano ABC Pine SofisaIndusval

Daycoval’s Strengths

31

Growth capability with reduced costs

Low leverage levelAccess to diversified funding sources

Experienced management team compromised with corporate governance

Recognized as one of the best Brazilian

Middle Market Banks Conservative profile

and solid capital structure

Strict credit policy

Agenda

32

Overview and Strategy

4Q09 Results

Peers Comparison and Conclusion

Appendix

Brazilian Credit Market

Dealing with the Global Crisis

Daycoval’s Financial Highlights

33

41.2%

35.8%33.1%

25.6% 25.6%28.2%

30.1% 30.5% 29.3% 28.6%

3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09

12.1%12.7%

12.0%10.8%

9.8%

11.4%12.6% 13.0%

12.2%13.0%

3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09

BIS Ratio

Net Interest Margin

Total Assets (R$ MM) & ROAA

Net Income (R$mn) & ROAE

5,388

6,5577,199

7,972 8,085

6,831 6,7286,196 6,177

7,061

4.5% 4.5% 4.2%3.6%

2.5%

1.2%

2.9% 2.5%2.8%

5.3%

3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09

Total Assets ROAA

57.762.2

70.262.5

47.1

20.4

48.0

38.5 42.0

82.5

16.9% 17.1%19.4%

16.7%15.6%

9.4%

12.3%9.8%

10.7%

21.4%

3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09Net Income ROAE

Serasa – December 2009

Breakdown of the Middle Market Credit Portfolio by Sectors

COMMERCE 18.0% INDUSTRY 41.8%

Commerce of pharmacy products 1.5% Sugar and Alcohol Mill 6.7%

Trading 1.2% Ind. of smal vehicles 2.4%

Commerce of import and export of soybean 1.2% Ind. of clothes in general 1.9%

Commerce of house appliances 1.1% Ind. of flooring and tiles 1.3%

Commerce of clothes in general 1.0% Ind. of eletronic products 1.2%

Other 12.0% Ind. of plastics 1.0%

Other 27.3%

SERVICE 33.0% FINANCIAL 2.4%

Transportation 4.0%

Electricity distribution 2.8% PRIMARY 1.3%

Holding 2.7%

Mixed cooperative 2.3% INDIVIDUALS 3.0%

Real Estate and Home Builders 2.1%

Other 19.1% THIRD SECTOR 0.5%

34

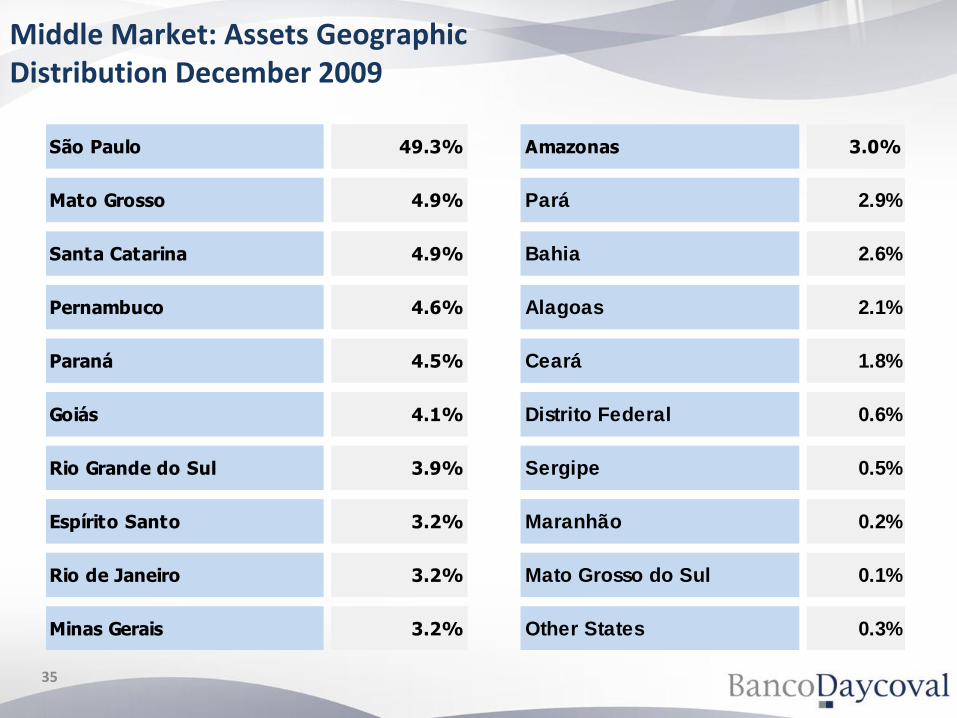

Middle Market: Assets Geographic Distribution December 2009

São Paulo 49.3% Amazonas 3.0%

Mato Grosso 4.9% Pará 2.9%

Santa Catarina 4.9% Bahia 2.6%

Pernambuco 4.6% Alagoas 2.1%

Paraná 4.5% Ceará 1.8%

Goiás 4.1% Distrito Federal 0.6%

Rio Grande do Sul 3.9% Sergipe 0.5%

Espírito Santo 3.2% Maranhão 0.2%

Rio de Janeiro 3.2% Mato Grosso do Sul 0.1%

Minas Gerais 3.2% Other States 0.3%

35

Balance Sheet

Amounts in R$’000Assets 4Q09 3Q09 4Q08 2009 2008Current Assets 5,021,043 4,573,561 5,219,130 5,021,043 5,219,130

Cash and Cash Equivalents 31,542 30,766 45,785 31,542 45,785

Interbank Investments 2,142,757 1,669,362 1,801,367 2,142,757 1,801,367

Securities and Derivatives 303,813 448,135 633,285 303,813 633,285

Interbank Accounts 16,120 9,102 12,901 16,120 12,901

Lending Operations 2,223,052 2,125,050 2,371,330 2,223,052 2,371,330

Other Receivables 246,477 234,243 293,886 246,477 293,886

Other Assets 57,282 56,903 60,576 57,282 60,576

Long-Term Assets 2,028,941 1,592,614 1,598,789 2,028,941 1,598,789

Securities and Derivatives 550,368 355,554 333,312 550,368 333,312

Lending Operations 1,242,116 1,001,935 1,027,877 1,242,116 1,027,877

Other Receivables 212,814 204,533 182,980 212,814 182,980

Other Assets 23,643 30,592 54,620 23,643 54,620

Permanent 10,844 11,208 13,064 10,844 13,064

Investments 382 382 356 382 356

Property and Equipment in Use 10,390 10,746 12,597 10,390 12,597

Intangible 72 80 111 72 111

Total Assets 7,060,828 6,177,383 6,830,983 7,060,828 6,830,983

Liabilities 4Q09 3Q09 4Q08 2009 2008Current Liabilities 3,314,096 2,539,005 3,435,684 3,314,096 3,435,684

Deposits 1,241,391 1,274,649 1,258,451 1,241,391 1,258,451

Money Market Funding 1,189,987 320,858 1,290,642 1,189,987 1,290,642

Funds from Acceptance and Issuance of Securities 206,023 417,078 285,134 206,023 285,134

Interbank Accounts 1,296 1,885 494 1,296 494

Interbranch Accounts 960 4,325 2,665 960 2,665

Borrowings and Onlendings 495,038 356,117 369,635 495,038 369,635

Derivatives 5,908 404 19,044 5,908 19,044

Provisions of Insurance 5,698 6,552 2,521 5,698 2,521

Other payables 167,795 157,137 207,098 167,795 207,098

Long-term Liabilities 2,048,455 1,985,805 1,780,005 2,048,455 1,780,005

Deposits 1,140,438 1,056,804 498,518 1,140,438 498,518

Funds from Acceptance and Issuance of Securities 167,437 172,438 500,361 167,437 500,361

Borrowings and Onlendings 380,530 400,865 511,858 380,530 511,858

Derivatives 19,316 18,334 1,085 19,316 1,085

Other Payables 340,734 337,364 268,183 340,734 268,183

Deferred Income 5,006 5,689 7,558 5,006 7,558 246 246

Minority Interest 553 544 508 553 508

Shareholders´ Equity 1,692,718 1,646,340 1,607,228 1,692,718 1,607,228

Capital of Brazilian Residents 1,359,143 1,359,143 1,359,143 1,359,143 1,359,143

( - ) Treasury Stocks (14,533) (38,992) (16,874) (14,533) (16,874)

Capital Reserves 192 192 170 192 170

Revaluation Reserves 1,569 1,595 1,991 1,569 1,991

Profit Reserves 345,887 323,332 267,717 345,887 267,717

Adjustment to Fair Value - Securities and

Derivatives Available for Sale 460 1,070 (4,919) 460 (4,919)

Total Liabilities 7,060,828 6,177,383 6,830,983 7,060,828 6,830,983

36

Income Statement

Amounts in R$’0004Q09 3Q09 Chg. % 4Q08 Chg. % 2009 2008 Chg. %

Income from Financial Intermediation 257,626 169,564 51.9% 569,552 -54.8% 801,145 1,650,443 -51.5%

Lending Operation 211,096 192,469 9.7% 311,240 -32.2% 790,866 1,073,824 -26.4%

Securities Operations 57,991 66,529 -12.8% 63,261 -8.3% 263,198 267,249 -1.5%

Derivatives (18,859) (89,434) -78.9% 152,154 n.a. (252,919) 219,074 n.a.

Foreign Exchange Operations 7,398 - n.a. 42,897 n.a. - 82,765 n.a.

Compulsory Investments - - n.a. - n.a. - 7,531 n.a.

Expenses of Financial Intermediation (103,696) (156,644) -33.8% (460,847) -77.5% (624,690) (1,181,738) -47.1%

Funding Expenses (75,077) (74,482) 0.8% (281,794) -73.4% (323,713) (762,088) -57.5%

Borrowing and Onlendings (11,650) (12,390) -6.0% (111,391) -89.5% (61,088) (242,827) -74.8%

Foreign Exchange Operations - (1,541) n.a. - n.a. (348) - n.a.

Loan Losses Provisions (16,969) (68,231) -75.1% (67,662) -74.9% (239,541) (176,823) 35.5%

Gross Profit from Financial Intermediation 153,930 12,920 n.a. 108,705 41.6% 176,455 468,705 -62.4%

Other Operating Income (Expenses) (28,258) 42,992 -165.7% (66,764) -57.7% 120,522 (191,951) n.a.

Income from Services Provided 5,457 4,831 13.0% 4,332 26.0% 18,499 26,190 -29.4%

Personnel Expenses (17,772) (15,451) 15.0% (18,929) -6.1% (63,927) (70,995) -10.0%

Other Administrative Expenses (26,794) (26,700) 0.4% (47,326) -43.4% (109,437) (172,646) -36.6%

Tax Expenses (10,203) (9,282) 9.9% (5,943) 71.7% (37,395) (32,899) 13.7%

Other Operating Income 31,822 106,934 -70.2% 9,597 n.a. 367,075 94,425 n.a.

Other Operating Expenses (10,768) (17,340) -37.9% (8,495) n.a. (54,293) (36,026) 50.7%

Income from Operation 125,672 55,912 124.8% 41,941 199.6% 296,977 276,754 7.3%

Non-operating Expenses (1,057) (2,473) -57.3% (13,521) n.a. (12,929) (14,904) -13.3%

Income before Taxes and Minority Interest 124,615 53,439 133.2% 28,420 n.a. 284,048 261,850 8.5%

Income and Social Contribution Taxes (35,842) (8,713) n.a. 2,005 n.a. (58,309) (44,115) 32.2%

Provision for Income Tax (11,324) (23,151) -51.1% 692 n.a. (70,133) (66,389) 5.6%

Provision for Social Contribution Tax (10,858) (12,661) -14.2% (1,399) n.a. (42,622) (33,140) 28.6%

Deferred Taxes (13,660) 27,099 -150.4% 2,712 n.a. 54,446 55,414 -1.7%

Profit-Sharing (6,294) (2,667) 136.0% (10,043) n.a. (14,610) (17,541) -16.7%

Minority Interest (8) (10) -20.0% (11) -27.3% (41) (44) -6.8%

Net Income 82,471 42,049 96.1% 20,371 n.a. 211,088 200,150 5.5%

Interest on Shareholders´ Equity (21,000) (25,451) -17.5% (21,472) -2.2% (94,566) (93,416) 1.2%

Earnings per Share (R$) 0.38 0.19 97.6% 0.09 n.a. 0.98 0.91 8.0%

Number of Shares 214,767,212 216,324,512 -0.7% 220,018,112 -2.4% 214,767,212 220,018,112 -2.4%

37

Institutional Presentation 4Q09

Investor Relations

“This report may include estimates and forward-looking statements. These estimates and forward-looking statements are to a large extent based on current expectations andprojections about future events and financial trends that affect or may come to affect our business. Many important factors may adversely affect the results of BancoDaycoval as described in our estimates and forward-looking statements. These factors include, but are not limited to, the following: the Brazilian and international economicconjunctures, fiscal, foreign-exchange and monetary policies, higher competition in the middle-market segment, the ability of Banco Daycoval to obtain funding for itsoperations, and amendments to Central Bank regulations.The words “believe”, “may”, “could”, “seek”, “estimate”, “continued”, “anticipate”, “plan”, “expect” and other similar words have the objective of identifying estimates andprojections. The considerations involving estimates and forward-looking statements include information related to results and projections, strategies, competitivepositioning, the environment in the industry, growth opportunities, the effects of future regulations, and the impacts from competitors. Said estimates and projections referonly to the date on which they were expressed, and we do not assume any obligation to publicly update or revise any of these estimates arising from the occurrence of newinformation, future events, or any other factors. In view of the risks and uncertainties described above, the estimates and forward-looking statements contained herein maynot materialize. Given these limitations, shareholders and investors should not make any decisions based on the estimates, projections and forward-looking statementscontained in this report”.

Phone: +55 (11) 3138.1024/[email protected]