INSTITUTIONAL EQUITY RESEARCH Godrej Consumer Product ...

26

INSTITUTIONAL EQUITY RESEARCH Page | 1 | PHILLIPCAPITAL INDIA RESEARCH Please see penultimate page for additional important disclosures. PhillipCapital (India) Private Limited. (“PHILLIPCAP”) is a foreign broker-dealer unregistered in the USA. PHILLIPCAP research is prepared by research analysts who are not registered in the USA. PHILLIPCAP research is distributed in the USA pursuant to Rule 15a-6 of the Securities Exchange Act of 1934 solely by Rosenblatt Securities Inc, an SEC registered and FINRA-member broker-dealer. Godrej Consumer Product (GCPL IN) Gold Flash LV – Could it be GCPL’s pot of gold? INDIA | FMCG | Company Update 26 October 2020 Many thanks for your great response to our latest Ground View – Soap Industry – The Great Indian Soap Opera. In that light, and since we have been pitching GCPL (which garners 30% domestic business from soaps) as our top ‘anti-consensus high-conviction idea’ for a few months now, in this report, we have taken a deeper look into the household insecticides (HI) category (40% of GCPL’s domestic business). The questions we have tried to answer include: What is the evolution of the category? What key challenges has HI been facing? What resolve have large players shown, when faced with severe competitive intensity, to emerge out of the crisis? Have GCPL’s recent innovations in the liquid vaporiser (LV) segment turned around its fortune and medium-term growth trajectory? Is the international HI business (especially Africa) worth entering? And why is the aerosol format much larger than the liquid vaporizer format in Indonesia, which contributes c.17% of GCPL’s consolidated revenue. Can the product GoodKnight Gold Flash turn out to be GCPL’s pot of gold? Our ground checks suggest that sales of GCPL’s liquid vaporizers before it launched Gold Flash were impacted despite having 60mn machines in use in the market because any refill (even competitors’) fit into GCPL’s machines and its peers offered higher trade margins (22-25%) vs. its 15-16%. Customers without much hesitation bought competitors’ refill packs as long as they came from well-known reputed brands and repelled mosquitoes. Moreover, retailers were more interested in pushing other brands (over GCPL) since they offered higher trade margins. GCPL launched GoodKnight Gold Flash in February 2020, where its refills only fit its own machine, thus weeding out competitors’ brands. The best part was that Gold Flash refills fit into competitors’ machines. Also, the formulation of the product was better, enhancing its efficacy. When GCPL launched '‘GK Express’ on a similar proposition in Feb- 2014, it saw strong growth until FY16 despite the Swacch Bharat Mission media blitzkrieg (which might have led to lower mosquito infestation) and it took little more than two years for competitors to replicate the product, after which growth receded along with structural issues that the category faced. As a result, after years of disappointing performance (-1% revenue CAGR fall over FY16-20), GCPL’s HI portfolio is slated for healthy double-digit revenue growth in the medium term (HI revenue CAGR of c.10% over FY20-23). Weakening competitive positioning of local players will aid market share gains in incense sticks (agarbatti) segment: GCPL’s ‘burning’ format portfolio (coils, fast cards) took a significant hit due to increased acceptance of agarbattis made by local, regional, and unorganized players, who usually flout norms pertaining to active ingredients, making these products cheaper and more efficacious. However, lately the competitive positioning of these players has taken a hit (as per our channel checks) because the government has increased customs duty on raw bamboo sticks to 25% from 10%, and because of supply-chain constraints in the wake of the COVID-19 pandemic. These players’ business is down 30-40% yoy over the past six months, indicating market-share gains for organized players such as GCPL. GCPL is spending resources in creating awareness about how its product is better (lasts longer, contains natural ingredients) vs. unorganized players’ products. It is also trying to match the attractive trade schemes of unorganized players. Even if this cannibalizes its sales (shift from coils to agarbattis), it will be margin-accretive because margins on agarbattis are higher than coils, as the former are easier to manufacture and transport. How big is the HI opportunity in Africa? GCPL recently forayed into Nigeria’s HI market. We believe that though the opportunity size is reasonable (US$ 700-800mn) it is going to be long haul as: (1) each country (>50 countries in Africa) has a separate registration process for HI products; (2) there is a need to strengthen the distribution infrastructure for core FMCG products, as current distribution infra is more aligned towards salons/hair stylists, as bulk of business comes from dry hair care; and (3) each category (burning format) will face its own challenges (discussed in this report). BUY (Maintain) CMP RS 671 / TARGET RS 860 (+28%) SEBI CATEGORY: LARGE CAP COMPANY DATA O/S SHARES (MN) : 1022 MARKET CAP (RSBN) : 695 MARKET CAP (USDBN) : 9.1 52 - WK HI/LO (RS) : 771 / 425 LIQUIDITY 3M (USDMN) : 14.6 PAR VALUE (RS) : 1 SHARE HOLDING PATTERN, % Jun 20 Mar 20 Dec 19 PROMOTERS : 63.2 63.2 63.2 FII / NRI : 26.8 26.3 27.7 FI / MF : 3.2 3.1 2.2 NON PRO : 1.7 2.0 1.8 PUBLIC & OTHERS : 5.1 5.3 5.0 PRICE VS. SENSEX KEY FINANCIALS Rs mn FY21E FY22E FY23E Net Sales 1,04,637 1,16,366 1,28,262 EBITDA 24,664 27,624 30,695 Net Profit 16,810 19,315 21,909 EPS, Rs 16.4 18.9 21.4 PER, x 40.8 35.5 31.3 EV/EBITDA, x 28.1 24.8 22.1 PBV, x 8.0 7.4 6.8 ROE, % 19.6 20.9 21.9 Debt/Equity (%) 28.2 23.4 19.1 CHANGE IN ESTIMATES __Revised Est. __ __% Revision__ Rs bn FY22E FY23E FY22E FY23E Revenue 1,16,366 1,28,262 5.2% 5.0% EBITDA 27,624 30,695 6.8% 6.3% Core PAT 19,315 21,909 7.2% 6.8% EPS (Rs) 19 21 7.2% 6.8% Vishal Gutka , Research Analyst (+ 9122 6246 4118) [email protected] Preeyam Tolia, Research Associate (+ 9122 6246 4129)[email protected] 80 100 120 140 160 180 200 220 Apr-16 Apr-18 Apr-20 GCPL BSE Sensex

Transcript of INSTITUTIONAL EQUITY RESEARCH Godrej Consumer Product ...

INSTITUTIONAL EQUITY RESEARCH

Page | 1 | PHILLIPCAPITAL INDIA RESEARCH Please see penultimate page for additional important disclosures. PhillipCapital (India) Private Limited. (“PHILLIPCAP”) is a foreign broker-dealer unregistered in the USA. PHILLIPCAP research is prepared by research analysts who are not registered in the USA. PHILLIPCAP research is distributed in the USA pursuant to Rule 15a-6 of the Securities Exchange Act of 1934 solely by Rosenblatt Securities Inc, an SEC registered and FINRA-member broker-dealer.

Godrej Consumer Product (GCPL IN)

Gold Flash LV – Could it be GCPL’s pot of gold?

INDIA | FMCG | Company Update

26 October 2020

Many thanks for your great response to our latest Ground View – Soap Industry – The Great Indian Soap Opera. In that light, and since we have been pitching GCPL (which garners 30% domestic business from soaps) as our top ‘anti-consensus high-conviction idea’ for a few months now, in this report, we have taken a deeper look into the household insecticides (HI) category (40% of GCPL’s domestic business). The questions we have tried to answer include: What is the evolution of the category? What key challenges has HI been facing? What resolve have large players shown, when faced with severe competitive intensity, to emerge out of the crisis? Have GCPL’s recent innovations in the liquid vaporiser (LV) segment turned around its fortune and medium-term growth trajectory? Is the international HI business (especially Africa) worth entering? And why is the aerosol format much larger than the liquid vaporizer format in Indonesia, which contributes c.17% of GCPL’s consolidated revenue.

Can the product GoodKnight Gold Flash turn out to be GCPL’s pot of gold? Our ground checks suggest that sales of GCPL’s liquid vaporizers before it launched Gold Flash were impacted despite having 60mn machines in use in the market because any refill (even competitors’) fit into GCPL’s machines and its peers offered higher trade margins (22-25%) vs. its 15-16%. Customers without much hesitation bought competitors’ refill packs as long as they came from well-known reputed brands and repelled mosquitoes. Moreover, retailers were more interested in pushing other brands (over GCPL) since they offered higher trade margins. GCPL launched GoodKnight Gold Flash in February 2020, where its refills only fit its own machine, thus weeding out competitors’ brands. The best part was that Gold Flash refills fit into competitors’ machines. Also, the formulation of the product was better, enhancing its efficacy. When GCPL launched '‘GK Express’ on a similar proposition in Feb-2014, it saw strong growth until FY16 despite the Swacch Bharat Mission media blitzkrieg (which might have led to lower mosquito infestation) and it took little more than two years for competitors to replicate the product, after which growth receded along with structural issues that the category faced. As a result, after years of disappointing performance (-1% revenue CAGR fall over FY16-20), GCPL’s HI portfolio is slated for healthy double-digit revenue growth in the medium term (HI revenue CAGR of c.10% over FY20-23).

Weakening competitive positioning of local players will aid market share gains in incense sticks (agarbatti) segment: GCPL’s ‘burning’ format portfolio (coils, fast cards) took a significant hit due to increased acceptance of agarbattis made by local, regional, and unorganized players, who usually flout norms pertaining to active ingredients, making these products cheaper and more efficacious. However, lately the competitive positioning of these players has taken a hit (as per our channel checks) because the government has increased customs duty on raw bamboo sticks to 25% from 10%, and because of supply-chain constraints in the wake of the COVID-19 pandemic. These players’ business is down 30-40% yoy over the past six months, indicating market-share gains for organized players such as GCPL. GCPL is spending resources in creating awareness about how its product is better (lasts longer, contains natural ingredients) vs. unorganized players’ products. It is also trying to match the attractive trade schemes of unorganized players. Even if this cannibalizes its sales (shift from coils to agarbattis), it will be margin-accretive because margins on agarbattis are higher than coils, as the former are easier to manufacture and transport.

How big is the HI opportunity in Africa? GCPL recently forayed into Nigeria’s HI market. We believe that though the opportunity size is reasonable (US$ 700-800mn) it is going to be long haul as: (1) each country (>50 countries in Africa) has a separate registration process for HI products; (2) there is a need to strengthen the distribution infrastructure for core FMCG products, as current distribution infra is more aligned towards salons/hair stylists, as bulk of business comes from dry hair care; and (3) each category (burning format) will face its own challenges (discussed in this report).

BUY (Maintain) CMP RS 671 / TARGET RS 860 (+28%)

SEBI CATEGORY: LARGE CAP

COMPANY DATA

O/S SHARES (MN) : 1022

MARKET CAP (RSBN) : 695

MARKET CAP (USDBN) : 9.1

52 - WK HI/LO (RS) : 771 / 425

LIQUIDITY 3M (USDMN) : 14.6

PAR VALUE (RS) : 1

SHARE HOLDING PATTERN, %

Jun 20 Mar 20 Dec 19

PROMOTERS : 63.2 63.2 63.2

FII / NRI : 26.8 26.3 27.7

FI / MF : 3.2 3.1 2.2

NON PRO : 1.7 2.0 1.8

PUBLIC & OTHERS : 5.1 5.3 5.0

PRICE VS. SENSEX

KEY FINANCIALS

Rs mn FY21E FY22E FY23E

Net Sales 1,04,637 1,16,366 1,28,262

EBITDA 24,664 27,624 30,695

Net Profit 16,810 19,315 21,909

EPS, Rs 16.4 18.9 21.4

PER, x 40.8 35.5 31.3

EV/EBITDA, x 28.1 24.8 22.1

PBV, x 8.0 7.4 6.8

ROE, % 19.6 20.9 21.9

Debt/Equity (%) 28.2 23.4 19.1 CHANGE IN ESTIMATES

__Revised Est. __ __% Revision__

Rs bn FY22E FY23E FY22E FY23E

Revenue 1,16,366 1,28,262 5.2% 5.0%

EBITDA 27,624 30,695 6.8% 6.3%

Core PAT 19,315 21,909 7.2% 6.8%

EPS (Rs) 19 21 7.2% 6.8% Vishal Gutka , Research Analyst (+ 9122 6246 4118) [email protected] Preeyam Tolia, Research Associate (+ 9122 6246 4129)[email protected]

80

100

120

140

160

180

200

220

Apr-16 Apr-18 Apr-20

GCPL BSE Sensex

Page | 2 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

Why is GCPL our high-conviction idea Change in estimates

We increase our EPS estimates for FY22-23 by c7% each on strong FY21 growth prospects.

Maintain GCPL as our top anti-consensus high-conviction BUY with a revised target of Rs 860 (40x FY23) from Rs 770 (40x Sept-22 EPS) earlier.

We believe operating performance is expected to be broad-based across categories / geographies in the medium term, for reasons highlighted below:

Reasons for being positive HI on a strong wicket: The highly profitable domestic HI business, which has

struggled (revenue CAGR of -1% over FY16-20) will see a strong rebound due to consumers’ increasing preference for diseases prevention products in the wake of COVID-19.GCPL’s heightened activity in innovation (Gold Flash LV, natural HI solutions, etc.) will see meaningful traction in FY22 only, as it takes 12-18 months for transition from old to new machines (this is in context to the most promising GK Goldflash innovation). Unorganized players in incense sticks are facing a tough time due to supply chain challenges and increase in import duty on raw bamboo sticks (to 25% from 10%) leading to market share gains for GCPL in its agarbatti segment.

Hair colours to make a roaring comeback in FY22: The highest margin domestic hair colours segment (11% of domestic business) should see strong re-bound in FY22 (expecting revenue growth of c.15%) based on favourable base (revenue CAGR fall of -3% over FY18-21) and the start of social and other functions.

Personal wash segment – becomes an interesting proposition now (vs. narrative of low-growth and highly penetrated category earlier) in the wake of the COVID-19 pandemic: We believe GCPL’s personal wash segment (32% of its domestic revenue) is set for low double-digit revenue growth in the medium term based on price hikes in soaps and scaling up of powder to liquid handwash. Mr Magic powder-to-liquid handwash can achieve revenue size of Rs 1.0-1.5bn vs. negligible size in FY20. Also, there is strong consumer response to health-based soaps (Cinthol Original) in southern markets.

Appointment of FMCG veteran Mr Dharnesh Gordon, ex-CEO of Nestle Nigeria and Indonesia, to turnaround its struggling Africa business (EBITDA CAGR fall of at -11% over FY17-20) through emphasis on execution (focus on dry-hair portfolio and scaling up of FMCG portfolio including wet hair care, HI and soaps, and stringent cost optimisation. In the worst case, even if Africa disappoints, it would not impact GCPL at an aggregate level, as the contribution of Africa to consolidated EBITDA has come down to 11% in FY20 from 18% in FY17.

GCPL will prioritise growth over margins, given RM tailwinds (windfall in crude, calibrated price hikes). It will optimize non-essential spends and ad and trade spends.

Technical factors that could drive re-rating / rally in stock price

DIIs are significantly underweight: DIIs (3.1% stake) are significantly underweight on GCPL vs. weights in Nifty 100 due to GCPL’s underperformance and higher share of international business, where domestic investors lack understanding.

GCPL can make an entry into benchmark indices: GCPL and Dabur are prime candidates to enter Nifty 50 index, whenever the next re-jig happens.

Page | 3 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

Category Dynamics

HI category has suffered over the past few years. Why? GCPL’s HI category saw a 1% revenue CAGR fall over FY16-20. There have been various reasons for that decline:

Archaic regulations: Industry veterans told us that the key reason is archaic regulations of Central Insecticides Board. India continues to work with old molecules which hampers the effectiveness of HI products, as mosquitoes keep evolving; for e.g., average weight of mosquitoes has more than doubled in the past couple of decades. As a result of lower effectiveness, consumers are showing higher resistance towards adopting mosquito-repellent products; whereas other developing and developed countries have advanced molecules. In telecom parlance (this is in relation to archaic regulations) we are still living in a 2G world while the rest of the world has moved onto 4G.

The main mosquito breeding season is January-April and August-September; climatic changes and variations increase or decrease the intensity of mosquitoes. As household insecticides is a need-based solution, customers don’t buy unless it is required.

Swaach Bharat Mission: Govt has spent Rs 40bn annually since 2014 on this. It has led to higher awareness and improved levels of cleanliness and sanitation, which is evident in reducing cases of malaria (annualized)

Proliferation of unorganized and local players in the agarbatti and incense sticks market, significantly denting the prospects of the value segment – which is coils and Good Night’s Fast Card.

Shift towards natural products seen across most mainstream consumer categories, since consumers have a perception that chemicals-based products are not good for their health.

Increased usage of ACs and construction of high rises in metros and tier-1 cities helps reduce mosquito infestation (to some extent).

Increasing penetration of fans in rural areas due to improved electrification has dented consumption of burning formats.

Malaria cases are in a declining trend due to the effectiveness of the Swaach Bharat Mission

Source: https://nvbdcp.gov.in/

1.17 1.09

0.84

0.43

0.33

0

0.2

0.4

0.6

0.8

1

1.2

1.4

CY15 CY16 CY17 CY18 CY19

Malaria cases (mn cases)

On right hand side - In telecom parlance (this is in relation to archaic regulations) we are still living in a 2G world while the rest of the world has moved onto 4G

Page | 4 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

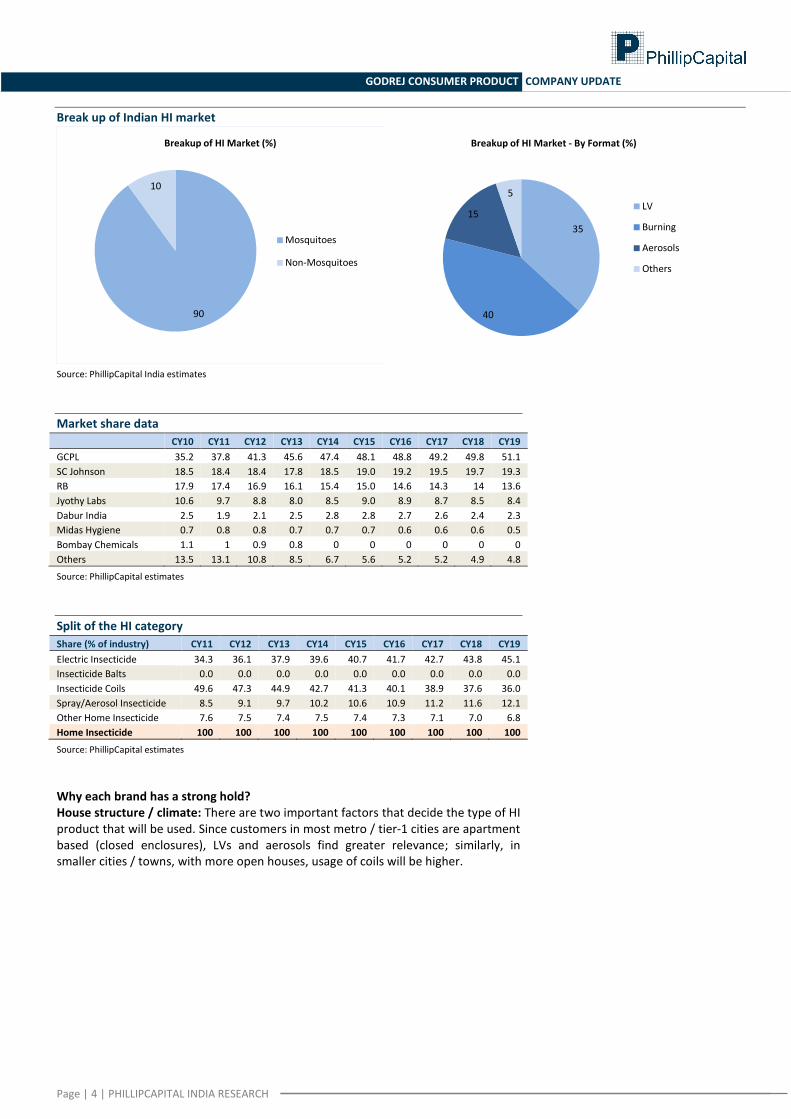

Break up of Indian HI market

Source: PhillipCapital India estimates

Market share data

CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17 CY18 CY19

GCPL 35.2 37.8 41.3 45.6 47.4 48.1 48.8 49.2 49.8 51.1

SC Johnson 18.5 18.4 18.4 17.8 18.5 19.0 19.2 19.5 19.7 19.3

RB 17.9 17.4 16.9 16.1 15.4 15.0 14.6 14.3 14 13.6

Jyothy Labs 10.6 9.7 8.8 8.0 8.5 9.0 8.9 8.7 8.5 8.4

Dabur India 2.5 1.9 2.1 2.5 2.8 2.8 2.7 2.6 2.4 2.3

Midas Hygiene 0.7 0.8 0.8 0.7 0.7 0.7 0.6 0.6 0.6 0.5

Bombay Chemicals 1.1 1 0.9 0.8 0 0 0 0 0 0

Others 13.5 13.1 10.8 8.5 6.7 5.6 5.2 5.2 4.9 4.8

Source: PhillipCapital estimates

Split of the HI category

Share (% of industry) CY11 CY12 CY13 CY14 CY15 CY16 CY17 CY18 CY19

Electric Insecticide 34.3 36.1 37.9 39.6 40.7 41.7 42.7 43.8 45.1

Insecticide Balts 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Insecticide Coils 49.6 47.3 44.9 42.7 41.3 40.1 38.9 37.6 36.0

Spray/Aerosol Insecticide 8.5 9.1 9.7 10.2 10.6 10.9 11.2 11.6 12.1

Other Home Insecticide 7.6 7.5 7.4 7.5 7.4 7.3 7.1 7.0 6.8

Home Insecticide 100 100 100 100 100 100 100 100 100

Source: PhillipCapital estimates

Why each brand has a strong hold? House structure / climate: There are two important factors that decide the type of HI product that will be used. Since customers in most metro / tier-1 cities are apartment based (closed enclosures), LVs and aerosols find greater relevance; similarly, in smaller cities / towns, with more open houses, usage of coils will be higher.

90

10

Breakup of HI Market (%)

Mosquitoes

Non-Mosquitoes

35

40

15

5

Breakup of HI Market - By Format (%)

LV

Burning

Aerosols

Others

Page | 5 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

Region wise breakup of key brands

UP, West Bengal and Bihar (East India)• Maxo (Jyothy Labs) is one the largest players in

these three markets, with maximum contribution coming from Coils, which are predominantly used in rural/ semi- urban areas.

• With these three states having higher rural salience (house structure being more open and less of apartments) , coils is most suitable format

North and West All out • All out is one of the leading players in these two markets and has

maximum revenue coming from high – margin Liquid vaporizer segment.

• Why it has done well in these two regions? – a) Since the Karamchand Appliances (now SC Johnson) originated from North India, thereby giving first mover advantage and b) West India being more urbanized, thereby providing conducive environment for LV business to flourish.

South India• With GCPL being market leader on Pan- India basis, but South

India is strongest and most profitable market (due to higher salience of Liquid vaporizer) for them

• GCPL continues to be dominating player (something similar to Asian Paints for paints market) in Southern India as a) TDPL (now acquired by GCPL) originated from South India b) Increased Literacy levels, better hygiene standards and

higher urbanization standards has led to better adoption of Liquid Vaporizer in this market

Mortein• It is very strong in North and West In coils

portfolio• Has majority of business coming from Coils within

HI portfolio, since it was pioneer in launching Alltherin based coils in 1995, giving them first mover advantage

• Strong on Pan- India basis (ex- South India) as far as coils portfolio is concerned

Page | 6 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

GCPL: LV segment leadership

Gold Flash: Can it turn out to be a pot of gold for the HI segment? Our ground checks suggest that the key reasons hurting GCPL’s high-margin products (liquid vaporizers) within its HI portfolio are exorbitant trade margins and schemes given by its peers, which curtailed consumption of GCPL refills, despite having solid availability (60mn machines in the market).

Competitors are selling at huge discount to GCPL’s price

Because any refill (even competitors’) fit into GCPL’s machines, customers were not very particular about which one they used so long as it was from a reputed brand (All Out, Mortein, Maxo) so long as it worked in terms of repelling mosquitoes. The trade channel was happy pushing competitors’ brands for meatier trade margins and schemes (22-25% vs GCPL’s offer of 16-18%).

Page | 7 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

Smaller players within the liquid vaporizer (LV) segment – Mortein (Reckitt), Maxo (Jyothy Labs), and Casper (Tain Wala Personal Care Product Ltd) follow a straight forward strategy:

Market their products (refills) as ‘fits in all machines’ and price them at a sizeable discount to market leaders, which enables them to grab some market share from almost nothing.

For marginal players (RB, Jyothy Labs) within the LV space, it is difficult to procure machines at reasonable cost due to the lack of scale (see table below).

GCPL has been consistently gaining market share in LVs

Source: PhillipCapital India estimates

LV brands and their variants Company Brand Variant MRP Size (ml) Price/45ml Comment

GCPL Good Knight - Gold Flash Machine + Refill 89 45 89

Refill 75 45 75

Good Knight - Activ Plus Machine + Refill 85 45 85

Refill 72 45 72

Good Knight - Xpress Machine + Refill 99 35 127

Refill 72 35 93

Good Knight - Natural Machine + Refill 99 45 99

Refill 85 45 85 SC Johnson All Out - Ultra Power Plus Slider Machin + Refill 89 45 89

Refill 72 45 72

All Out Sattva Power Plus Refill 72 45 72 RecKitt Benkiser Mortein Insta Vapourizer Machine + Refill 78 35 100 Mortein is priced higher than competition,

where most of the competitors are selling 45ml refill and for the same price, Mortein is offering only 35ml

Refill 72 35 93

Mortein Insta Tulsi Vapourizer Refill 72 35 93

Mortein Smart Machine + Refill 149 45 149 Jyothy Labs Maxo Genius Machine + Refill

89 35 114

Jyothy labs sells its LV (machine + refill) for the similar price of GCPL, however it sells 35 ml vs. GCPL's 45 ml. on relative basis JYL sells machine at cRs37 vs. GCPL Rs 14

Maxo LV Refill 67 45 67

Source: Bigbasket, Amazon, PhillipCapital India

37 41 47 52 53 53 54 54 54 55

42 40

37 34 35 35 35 35 34 33

10 9 9 8 7 7 7 8 8 8 6 5 4 4 4 4 4 4 4 4

0%

20%

40%

60%

80%

100%

CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17 CY18 CY19

GCPL SC Johnson RB Jyothy Labs

Page | 8 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

What is likely to change now? GCPL launched an LV product (Good Knight Gold Flash) where only its own refills would fit into its machine (weeding out competitors). The best part is Gold Flash’s refills can fit into competitors’ machines, providing an edge. Incrementally, Gold Flash’s better formulation vs. Good Knight’s earlier products will improve efficacy claims and in turn customer satisfaction.

Chemical composition of Gold Flash and Power Activ+

Chemical Name Functionality of the ingredient Good Knight

Gold Flash Power Activ+

Transfluthrin (w/w) Fast acting insecticide that helps in

repelling mosquitoes away 1.6% 0.88%

Butylated HydroxyToluene (w/w)

Stabilizer which helps in preventing

insecticide from getting oxidized

owing to heat

1.0% 1.0%

Perfume Drakkar (w/w) Perfume to provide desired

fragrance 1.0% 1.0%

Deodorised Kerosene (w/w) Vaporizer (liquid) 96.4% 97.12%

Total (w/w) 100.% 100.%

Source: Company, mosquito free world

GCPL had done relatively well (reported sales growth of 10/13% respectively in FY15/16) when it launched a product (Good Knight Express) on a similar proposition in FY14 despite blitzkrieg, effective execution of Swacch Bharat Mission at its full force, since this might have led to lower mosquitoes infestation.

HI growth started subsiding from FY17 onwards due to structural factors and competitors emulating GCPL’s ’GK Express’

Source: Company, PhillipCapital estimates

Management had highlighted in its previous concall that it generally takes 12-18 months for customers to transition from older machines (Power Activ) to newer ones (GK Gold flash). We believe meaningful scaling up in HI is likely to happen in FY22 since Goodnight Gold Flash was launched in February 2020. Media reports indicate that almost c.45% of customers use dual formats – i.e., they want the instant effects of a fast card and the longevity, convenience, and all-round protection of a liquid vaporiser (LV). GCPL has incorporated consumer insights and has launched a product that satisfies both requirements of the customers; the product has been priced at a marginal premium to erstwhile products.

9.4

13.1

3.0

(4.6)

(0.4)

(2.8)

-6

-4

-2

0

2

4

6

8

10

12

14

FY15 FY16 FY17 FY18 FY19 FY20

HI sales gr (%)

Page | 9 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

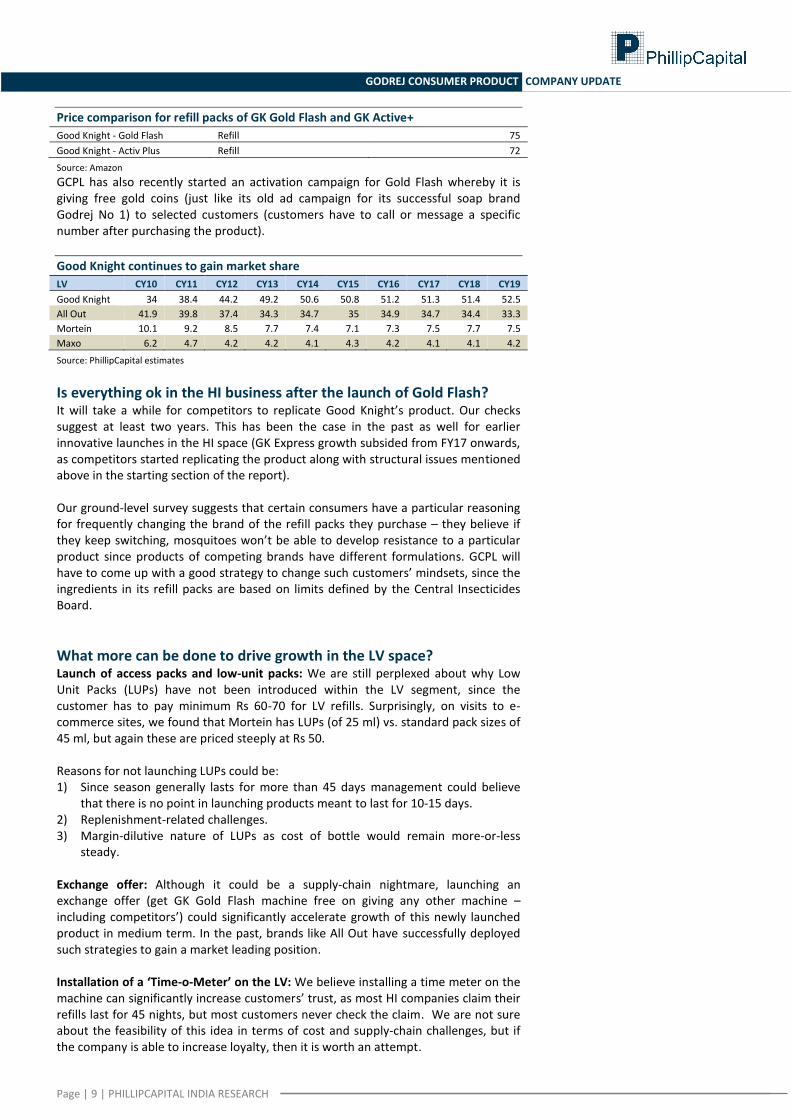

Price comparison for refill packs of GK Gold Flash and GK Active+

Good Knight - Gold Flash Refill 75

Good Knight - Activ Plus Refill 72

Source: Amazon

GCPL has also recently started an activation campaign for Gold Flash whereby it is giving free gold coins (just like its old ad campaign for its successful soap brand Godrej No 1) to selected customers (customers have to call or message a specific number after purchasing the product).

Good Knight continues to gain market share

LV CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17 CY18 CY19

Good Knight 34 38.4 44.2 49.2 50.6 50.8 51.2 51.3 51.4 52.5

All Out 41.9 39.8 37.4 34.3 34.7 35 34.9 34.7 34.4 33.3

Mortein 10.1 9.2 8.5 7.7 7.4 7.1 7.3 7.5 7.7 7.5

Maxo 6.2 4.7 4.2 4.2 4.1 4.3 4.2 4.1 4.1 4.2

Source: PhillipCapital estimates

Is everything ok in the HI business after the launch of Gold Flash? It will take a while for competitors to replicate Good Knight’s product. Our checks suggest at least two years. This has been the case in the past as well for earlier innovative launches in the HI space (GK Express growth subsided from FY17 onwards, as competitors started replicating the product along with structural issues mentioned above in the starting section of the report). Our ground-level survey suggests that certain consumers have a particular reasoning for frequently changing the brand of the refill packs they purchase – they believe if they keep switching, mosquitoes won’t be able to develop resistance to a particular product since products of competing brands have different formulations. GCPL will have to come up with a good strategy to change such customers’ mindsets, since the ingredients in its refill packs are based on limits defined by the Central Insecticides Board.

What more can be done to drive growth in the LV space? Launch of access packs and low-unit packs: We are still perplexed about why Low Unit Packs (LUPs) have not been introduced within the LV segment, since the customer has to pay minimum Rs 60-70 for LV refills. Surprisingly, on visits to e-commerce sites, we found that Mortein has LUPs (of 25 ml) vs. standard pack sizes of 45 ml, but again these are priced steeply at Rs 50. Reasons for not launching LUPs could be: 1) Since season generally lasts for more than 45 days management could believe

that there is no point in launching products meant to last for 10-15 days. 2) Replenishment-related challenges. 3) Margin-dilutive nature of LUPs as cost of bottle would remain more-or-less

steady. Exchange offer: Although it could be a supply-chain nightmare, launching an exchange offer (get GK Gold Flash machine free on giving any other machine – including competitors’) could significantly accelerate growth of this newly launched product in medium term. In the past, brands like All Out have successfully deployed such strategies to gain a market leading position. Installation of a ‘Time-o-Meter’ on the LV: We believe installing a time meter on the machine can significantly increase customers’ trust, as most HI companies claim their refills last for 45 nights, but most customers never check the claim. We are not sure about the feasibility of this idea in terms of cost and supply-chain challenges, but if the company is able to increase loyalty, then it is worth an attempt.

Page | 10 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

Are more premium products likely to follow suit within the LV space? GCPL is working on a strategy to launch products in niche segments such as matics / machines that keep on dispensing liquids at regular intervals and more efficacious natural-based products that can provide much higher realizations than traditional liquid vaporizers. Time will only tell whether the company will be able to scale up these launches. We believe there will be intense competition in natural-based LVs, since it does not require any approval from Central Insecticides Board. Approvals / long gestation period in getting government permission has been the key moat for incumbents. Incrementally, our consumer survey suggests that natural-based LVs do not have efficacy levels that compare well with chemicals-based LVs despite being priced at a premium.

Naturals are far more expensive than chemical LVs

Active+ (Rs 72) Natural’s Neem (Rs 85)

Unorganised players are mainly present in the naturals format and are expensive than chemical based LV (which sells at Rs c70-75 / Refill)

Brand ml MRP Price/45 ml

Strategi Herbal 40 85 96

Catche Ayurvedic 45 90 90

Mos-Quit 35 80 103

Novosynth Mosqpel Kidzee 45 99 99

Mangalam CamPure Camphor Power 45 99 99

Source: Amazon

Page | 11 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

How did GoodKnight give sleepless nights to All Out? In the past, GCPL has been able to dislodge market leaders operating in the sub-segment of household insecticides category and in turn, achieve No.1 position in respective sub-segments. All Out (now a part of the SC Johnson group, owned earlier by Karamchand Appliances) was a pioneer in bringing LV products to the Indian market . It used to rule the roost, commanding c.70% market share in the LV space at one point, because of its innovative marketing campaign and first-mover advantage. After the brand was acquired by SC Johnson from Karamchand Appliances in 2005, its market share has been constantly falling because:

The brand got a lot of recognition for its innovative marketing campaign – with its mosquito-eating frog mascot. However, SC Johnson decided to drop the frog mascot in 2011 – their reasoning was that since All Out had become an insect repellent brand from being just a mosquito repellent brand, the mascot has outlived its utility. In doing so, while SC Johnson jumped on to the family bandwagon, it killed the uniqueness that the frog provided in a cluttered market. Its latest ad has the same look and feel as many other mosquito repellent commercials that revolve around a mom fighting mosquitoes and protecting her kids. This strategy has led to a decline in market share within the LV segment to 33% in CY19 from 41% in CY10.

During this time, GCPL had become extremely aggressive about the launch of its new products (Activ+), beefing up the direct distribution network in urban areas, and promotions and schemes to trade channels, which would swing the game in its favour.

Merger of GHPL + GCPL: GHPL (household insecticides) which was strong in north India was merged with GCPL (soaps and hair colours), which was strong in south India, giving significant synergies in term of distribution network.

All Out gradually lost its shine to Good Knight

Source: PhillipCapital estimates

34

38.4

44.2

49.2 50.6 50.8 51.2 51.3 51.4

52.5

41.9

39.8

37.4

34.3 34.7 35 34.9 34.7 34.4 33.3

30

35

40

45

50

55

CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17 CY18 CY19

Good Knight All Out

We believe GCPL has taken the responsibility of driving market-leading growth via innovative products, and in the past, it has triumphed over brands such as All Out, who used to command more than 70% market share.

Page | 12 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

GCPL and the ‘burning’ format repellents

Past track record on new launches within HI segment has been mixed Evolution of the formats: Our research indicated that the formats for repelling mosquitoes has kept changing since the introduction of the category for the first time in India in mid-1980, based on consumer trends and preference, convenience, and formulation of the product. But based on the analysis from various media reports, we found that GCPL has the required “right to win” despite constant change in formats and intense competition due to:

Ability to launch differentiated, innovative, and value-for-money products, keeping customers’ needs and purchasing power at the forefront.

Solid distribution strength: It has the deepest reach – pan-India network, strong chemist salience, and decent depth in rural areas – which most of its peers lack by a wide margin.

Market leadership position: Which enables it to make the maximum out of its foray into new formats, despite being a late entrant.

Companies pioneer in HI space

Company Brand Format

GCPL GoodKnight Mats

Reckitt Benkiser Mortein Coils

SC Johnson All Out LV

What came first? Coils or mats We were surprised to know that mats were in existence much before the introduction of chemicals-based coils in the mid-1990s, given the conventional belief that coils are a rudimentary product that should have started first. However, herbal based coils (Tortorise brand) were introduced by Bombay Chemical Industries in 1970. Before GCPL’s entry into HI, mosquito repellents had low penetration in a market ruled by creams, mosquito nets, and herbal coils. GCPL was a pioneer in launching EMD i.e., Electronic Mosquito Destroyers (in simple terms - mats) and gained market leadership in less than two years.

Evolution of various sub-segments within HI category along with name of innovator

Mats Coils* LV Fast Card Agarbatti**

Good Knight GCPL

(1984)

Mortein Reckitt

(1993)

All Out SC Johnson

(1989)

Good Knight GCPL

(2013)

Good Knight GCPL

(2019)

*Tortoise (Herbal base coil) was launched in 1970 ; however chemicals based coils were introduced in 1993

** Agarbatti although has been present in unorganized for the past 7-8 years, but in our view, GCPL was one of

the first organized player to launch mosquito repellent stick

Page | 13 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

Coiling the shots Electronic Mosquito destroyers (EMD, were extremely effective since they contain a chemical called Allethrin (1%). In order to dislodge the dominating position of GCPL, Reckitt decided to make a big-bang foray into the HI segment through coils in 1993 (when GCPL did not have coils in its portfolio). Initially, the launch was restricted to south India, but given massive success, the company decided to take it pan-India in 1996. Why does Reckitt continue to garner healthy market share in coils despite being a laggard in the most profitable LV category within HI business?

Reckitt’s coils (Mortein brand) contained allethrin (the same active ingredient available in mats) while most other coils were pyrethrum-based herbal mosquito coils. Allethrin coil manufacturers claim that that the active ingredient is more effective against mosquitoes.

Media report indicate Reckitt went on a media blitzkrieg to market this product. This first mover advantage had enabled it to command meaningful market share in coils and once upon a time (late 1990s) it was a market leader in coils (c.35% market share) with the second position (26% share) being occupied by Tortoise (Bombay Chemicals).

GCPL continues to gain market share within coil segment

Source: PhillipCapital India estimates

GCPL (erstwhile Godrej Sara Lee) had consolidated its presence in mats via acquisitions (it took over Jet mats from Sonic Electronics and Banish mats from P L Chemicals in 1995). Its positioned was challenged due to increased salience of coils, which it tried to combat through the launch of Supermat; but customers did not much take to it. Coils’ efficacy with mats was narrowing – since both products repelled mosquitoes equally – and coils worked out much cheaper for users since there were no hardware costs. Customers saw a no reason for paying a premium for mats and shifted to coils.

37.4 38.9

40.8 41.7 42.6 43.1 43.5 43.7 44.2 44.5

26.5 26.8 27.4 27.2 27.1 26.7 26.2 25.8 25.4 25.2

16.7 16.3 15.3

14.3 16.2

17.4 17.7 17.8 17.9 17.9

13

18

23

28

33

38

43

48

CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17 CY18 CY19

GCPL RB Jyothy Labs

GCPL fought fiercely and came out with an innovative product (red coils) in the coil segment, which lasted much longer (10 hours) vs. Competitors’ coils, which lasted only for eight hours and this again restored its lost glory.

GCPL did not sit on past laurels and decided to come with more innovation (Jumbo coils), which had a maroon colour vs. Other coils which were green. A jumbo coil lasts for 12-14 hours, although the company never aggressively claims this.

Page | 14 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

Coils mix chart at industry level

Source: PhillipCapital India estimates

Why have coils (burning format) done reasonably well despite cost per application vs. LVs being higher, and being a low-margin category? Coils shouldn’t have gotten this much attention from the management Although cost of coils (on per night use basis) is higher than other formats available in the market, there is the flexibility of purchasing a single coil (Rs 2.5-3.0), while customers have to shell out Rs 70-75 for purchasing LV refills. Coils can be placed anywhere – any corner of the room – which might not be possible for mats/ LVs, which have to be plugged into an electricity board. As a result, their efficacy might be lower in open homes. Moreover, customers relate more to the smoke emitting out of coils as a sign of efficacy, which is difficult to gauge in case of LVs. However, of late, we have seen some change in customer behaviour and there is a shift towards product that cause lower smoke – such as smokeless coils, fast cards, and agarbattis. GCPL has been a pioneer in launching disruptive innovations such as smokeless coils (Rs 3.5 per coil) and fast cards (Rs 1 per card), but the company had to take a significant beating as far as the launch of agarbattis is concerned, where unorganised players have stolen a march Smokeless coils have not made much headway, apart from some gains in urban areas, as customers for this kind of product perceive smoke to be the panacea for all mosquito-related problems. Brand Variant MRP Price/coil

GCPL Good Knight Green Shakti Coil 10 coils 34 3.4

Good knight Green shakti Coil Sachet 4 coils 10 2.5

Good Knight Activ+ Low Smoke Coil 10 coils 34 3.4

Good Knight Jumbo Coil 10 coils 30 3.0

Good Knight Mini Jumbo Coil 10 coils 27 2.7

Good Knight Maha Jumbo Coil 10 coils 34 3.4

Brand MRP Nos Duration Price/coil

GCPL Good Knight Green Shakti Coil 10 coils 34 10 12 3.4

Good Knight Activ+ Low Smoke Coil 10 coils 34 10 12 3.4

Good Knight Maha Jumbo Coil 10 coils 34 10 12 3.4

SC Johnson All Out 12 Hour Anti Dengue Coil 14 coils 33 14 12 2.4

RB Mortein PowerBooster Coil 12 Hr 10 Coils 30 10 12 3.0

Mortein Naturegard Low Smoke Coil 12 Hr 10 Coils 33 10 12 3.3

GCPL Good Knight Mini Jumbo Coil 10 coils 27 10 8 2.7

Jyothy Labs Maxo A Grade Coil 14 coils 34 14 8 2.4

RB Mortein PowerBooster Coil 8 Hr 10 Coils 26 10 8 2.6

50

47

45

43 41

40 39

38 36

30

35

40

45

50

55

CY11 CY12 CY13 CY14 CY15 CY16 CY17 CY18 CY19

Coils (% of HI share)

Coils have held the fort despite emergence of various other new formats. Coils (% of HI market) has marginally moved down to 36% in CY19 from 50% in CY11.

Page | 15 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

GoodKnight present across price point in the burning format (Rs /unit)

Fast Card

Rs 1 Agarbatti

Rs 1.5

Coil

Rs 3 Format Year Comment

Fast card 2013 Cross pollinated from Indonesia, based on success from Hit Magic paper

Low smoke coil 2009 80% less smoke

Why did agarbatti do well but fast card flagged after the initial bump? Fast cards were actually meant for use during the day given the increasing cases of dengue and initial response was solid given its value-for-money proposition.

Dengue cases are rising

Source: https://nvbdcp.gov.in/

However, since the fast card burned for only for 5 minutes, consumers perceived that its impact on repelling mosquitoes lasted only for 45 minutes to one hour vs. the company’s claim that it lasted for more than two hours. Almost at the same time, unorganized / local players developed mosquito repellent incense sticks and consumers started shifting in a meaningful manner to this product because:

The costs were the same (Rs 10 pack for 10 sticks for incense sticks) as fast cards.

They were familiar with the format, as it is used for most religious / social functions.

It had better, as it contained active ingredients in the ratio of 20%, while legal norms allow only 1-2%.

Realizing that the company had lost golden opportunity to make foray into fast growing mosquito repellent incense sticks market size worth of Rs 7-8bn, GCPL decided to foray into the agarbatti segment in January 2019 via the launch of GoodKnight Neem Agarbatti (priced at Rs 15 for 10 sticks).

100

129

188

101

157

0

20

40

60

80

100

120

140

160

180

200

CY15 CY16 CY17 CY18 CY19

Dengue cases ('000 cases)

Page | 16 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

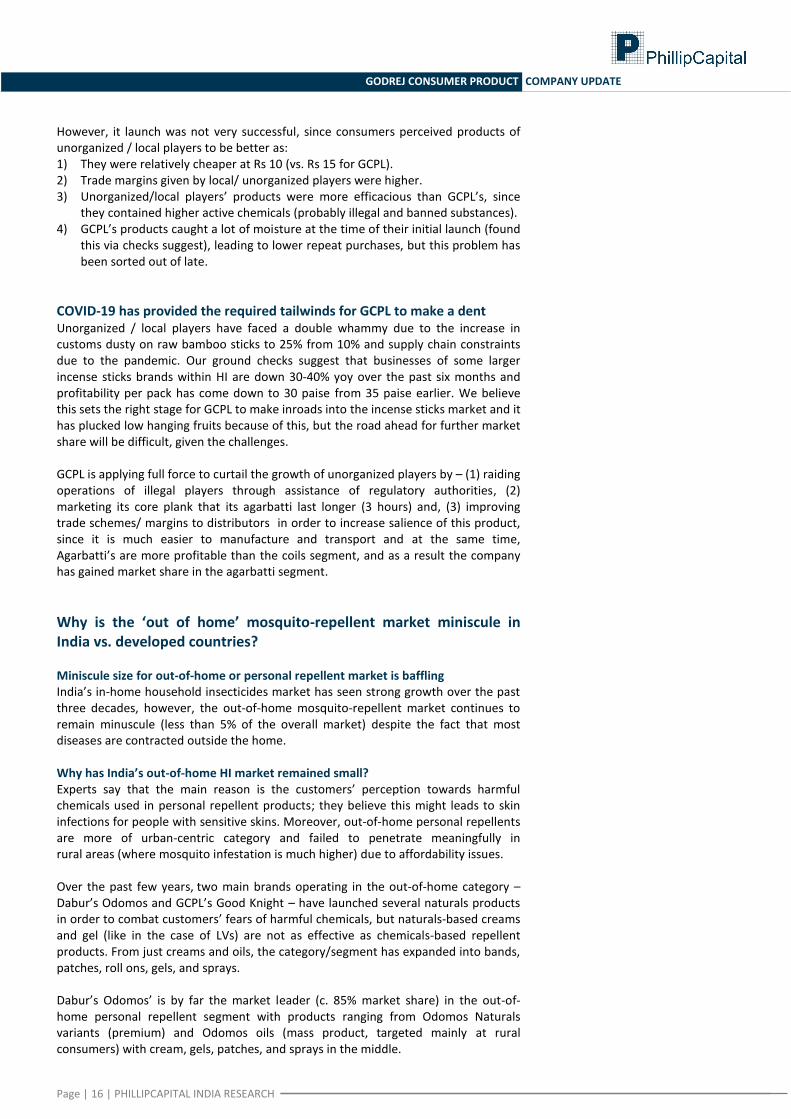

However, it launch was not very successful, since consumers perceived products of unorganized / local players to be better as: 1) They were relatively cheaper at Rs 10 (vs. Rs 15 for GCPL). 2) Trade margins given by local/ unorganized players were higher. 3) Unorganized/local players’ products were more efficacious than GCPL’s, since

they contained higher active chemicals (probably illegal and banned substances). 4) GCPL’s products caught a lot of moisture at the time of their initial launch (found

this via checks suggest), leading to lower repeat purchases, but this problem has been sorted out of late.

COVID-19 has provided the required tailwinds for GCPL to make a dent Unorganized / local players have faced a double whammy due to the increase in customs dusty on raw bamboo sticks to 25% from 10% and supply chain constraints due to the pandemic. Our ground checks suggest that businesses of some larger incense sticks brands within HI are down 30-40% yoy over the past six months and profitability per pack has come down to 30 paise from 35 paise earlier. We believe this sets the right stage for GCPL to make inroads into the incense sticks market and it has plucked low hanging fruits because of this, but the road ahead for further market share will be difficult, given the challenges. GCPL is applying full force to curtail the growth of unorganized players by – (1) raiding operations of illegal players through assistance of regulatory authorities, (2) marketing its core plank that its agarbatti last longer (3 hours) and, (3) improving trade schemes/ margins to distributors in order to increase salience of this product, since it is much easier to manufacture and transport and at the same time, Agarbatti’s are more profitable than the coils segment, and as a result the company has gained market share in the agarbatti segment.

Why is the ‘out of home’ mosquito-repellent market miniscule in India vs. developed countries? Miniscule size for out-of-home or personal repellent market is baffling India’s in-home household insecticides market has seen strong growth over the past three decades, however, the out-of-home mosquito-repellent market continues to remain minuscule (less than 5% of the overall market) despite the fact that most diseases are contracted outside the home. Why has India’s out-of-home HI market remained small? Experts say that the main reason is the customers’ perception towards harmful chemicals used in personal repellent products; they believe this might leads to skin infections for people with sensitive skins. Moreover, out-of-home personal repellents are more of urban-centric category and failed to penetrate meaningfully in rural areas (where mosquito infestation is much higher) due to affordability issues. Over the past few years, two main brands operating in the out-of-home category – Dabur’s Odomos and GCPL’s Good Knight – have launched several naturals products in order to combat customers’ fears of harmful chemicals, but naturals-based creams and gel (like in the case of LVs) are not as effective as chemicals-based repellent products. From just creams and oils, the category/segment has expanded into bands, patches, roll ons, gels, and sprays. Dabur’s Odomos’ is by far the market leader (c. 85% market share) in the out-of-home personal repellent segment with products ranging from Odomos Naturals variants (premium) and Odomos oils (mass product, targeted mainly at rural consumers) with cream, gels, patches, and sprays in the middle.

Page | 17 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

GCPL has upped the ante in the category recently by launching a series of products GoodKnight roll-on, patches, gel. In its Q1FY21 concall, GCPL management said that the main reason India’s out-of-home category has not grown meaningfully in India vs. US and Indonesia (where out-of-home is bigger than in-home) are: (1) right set of products meant for the Indian consumers were not available and (2) very little investment in the habit creation/formation. With products such as fabric roll-ons (Rs 75), personal repellent creams (Rs 20), and products available at the right value for money proposition, GCPL is expected to see strong growth ahead in the out-of-home space.

Page | 18 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

HI Africa market – is it worth it? Prima facie, Africa business seems to be quite promising, given:

Population size.

Tropical terrain.

Improving per captia because of improvement in infrastructure. GCPL, at the time of acquisition of Darling Ltd in 2011, had aggressive plans to foray into household insecticides; but this was delayed for a significant period, as its base business (dry-hair-care) faced challenges. Moreover, the registration / approval process for each country is quite tedious and it took almost a decade before it finally forayed into Nigeria in December 2019. We believe foray into HI might not move the needle much, as:

Household insecticides market for Africa (total) is only US$ 700-800mn (our estimates), with each of the 50+ countries having its own set of registration / laws. It is going to be a long haul for this business to become meaty.

All three formats within LV are likely to face challenges.

Africa is a porous market; there is intense dumping of burning formats (coils/ incense sticks) from China. GCPL might find it difficult to compete here since it will comply with all taxes.

African continent has lower electricity generation, making the proposition of liquid vaporizers less attractive.

African households may not have sufficient purchasing power to purchase aerosol, given low per-captia income.

Moreover, strengthening of distribution infrastructure for the FMCG range; current distribution set-up is skewed towards salons / hair stylists.

GATES foundation / WHO spends millions of dollars providing bed nets (mosquito nets) to African households, thereby making the proposition of consumer pull less attractive towards HI products.

Why is aerosol business within HI much bigger in Indonesia? Despite having a conducive environment for electric-based liquid vaporizers in Indonesia, the below mentioned reasons shed light on why aerosol is a much bigger there. And also, why has the aerosol category not yet become material for the India business , given it is large HI market.

Significant difference in the psyche of both customers. Indonesian customers prefer to have control and want to see mosquitoes get killed when they spray aerosols; Indian customers are generally more religious and believe in the principle of non-violence.

Structure/construction of house play an important role in deciding what format (aerosols / liquids) will be applied inside the home. Only few households have fans installed in Indonesian homes (Indonesians don’t like any direct air blowing on their body as they believe they will fall ill) and most have air-ventilating windows in their homes. LVs works best in closed spaces, whereas aerosol works better in the house structures that most of Indonesian families live in.

Cost of aerosols is US$ 2 (Rs 150) in Indonesia for a 600ml bottle that provides 120 applications; each time, users will use c.5ml. Assuming a household sprays the aerosol four times a day, it will last for 30 days effectively. A small aerosol bottle costs much higher at Rs 230-240 in India, as the government imposes a lot of duties on imported packaging material (cans / sheets) making the proposition of aerosols less attractive to Indian customers.

Page | 19 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

Table of new product launches

Variants MRP

Good Knight Gold Flash (Refill + Mashine) 89

Good Knight Neem (Refill + Mashine) 99

Good Knight Power Chip (chip + machine) 45

Goodl Knight Power Shot 199

Goodknight Naturals Neem Anti-Fly Surface Spray 299

Goodknight Naturals Neem Anti-Mosquito Room Spray 299

Good knight Fabric Roll-on 75

Good Knight Patches 75

Good Knight Cool Gel 75

HIT Anti Roach Gel 240

HIT Gel Stick 334

Source: Company

Page | 20 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

Annexure

GoodKnight The beginning of GoodKnight The story of GoodKnight begins with the loving father R. Mohan (aka, GoodKnight Mohan) looking for a solution for his daughter – to save her from mosquito bites. In early 1980s, the market was dominated by coils, such as Tortoise (aka kachhua chaap), EMR (Electronics Mosquito Repellent) mats – Deemos and Vape. An electronic engineer, R. Mohan, took up the distribution of Vape, as he found it to be the most effective for mosquito bites. But the product did not pick up. Mohan decided to enter the market with a brand of his own. In 1987, he partnered with Arumugham Mahendran and launched GoodKnight, HIT, under Transelektra Domestic Products Ltd (TDPL). After some initial hiccups, sales of GoodKnight products picked up tremendously, and it became a dominant player in EMR. How it came into GCPL’s Kitty In 1994, Godrej Group acquired TDPL from R. Mohan, and formed Godrej Hicare Ltd. After this, the brand saw tremendous response with new and improved products that were launched. It launched “Supermat”, its 10-hour red jumbo coils, and 12-hours jumbo coils (world’s longest lasting coils) – primarily to target the rural market – and took away market share from major brands. When competition intensified in the vaporiser market, GoodKnight launched the 45-night refill in 1995, followed by 60-90 nights refills (first in the industry), turbo refills in 2003, and Activ+ in 2007 – which gave it an unshakeable lead. After the acquisition of TDPL by Godrej, A Mahendran then became the MD of Godrej Hicare Ltd.; within a year, he sold a 51% stake in Godrej Hicare to Sara Lee Corporation. In 2010, Godrej Group acquired Sara Lee’s 51% stake in Godrej Hicare and integrated the business with GCPL.

Page | 21 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

All out The beginning of All Out Karamchand Appliances was promoted by the Arya brothers – Anil, Naveen and Bimal from Maharashtra. The brothers shifted to Rajkot, Gujarat to join one of their relatives in manufacturing diesel engines for agriculture, but were keener on the FMCG business. Impressed by the success of a small mosquito repellent company in Rajkot, the trio decided to venture into manufacturing mosquito repellents and set up KAPL. To get technical knowledge, KAPL collaborated with Japanese company Earth Chemical Co. Ltd. for vaporiser technology, as most players where focused on mats. The trio decided to focus on liquid vaporisers, as the strength of mats reportedly weakened after a few hours while vaporisers could function consistently throughout the night. Initially, when the product was launched in Mumbai in 1990, the company faced a number of challenges – delays in supply of packing material, limited market acceptance despite hiring the lead media agency of that time (Avenues, HTA); it ended up paying more on making advertising and did not get the required traction. While other companies concentrated on coils and mats, KAPL promoted the use of vaporizers. By the mid-1990s, vaporizers had attained a market share of 5%. This segment was almost completely dominated by KAPL, whose sales reached Rs 253mn in 1996-97. GSLL (now Godrej Consumer Ltd) could no longer ignore this growing segment and launched its own vaporizer under the GoodKnight brand in 1996-97. GoodKnight soon acquired a 40% market share of the vaporizer market. However, this did not affect the sales of KAPL, as the launch of GoodKnight had led to a growth in the overall size of the vaporizer market. Instead of eating into All Out's sales, GSLL ended up expanding the market. However, GoodKnight could not sustain its success, and by 1999, the brand's market share had gone down to 21% – a major portion of the 19% loss being taken up by All Out. Although the initial success of All Out was largely due to technological innovation and first-mover advantages, it was widely believed that what had kept the brand going was strong marketing. Indian jugaad mindset KAPL took the advertising mandate into its own hands and launched its well know frog campaign (which later become the brand identity). The iconic campaign featured an animated jumping frog with (All Out vaporizer) eating mosquitoes; this cost a mere Rs 50,000 to make but saw tremendous success. Over the years, KAPL continued the same advertisement with minor adjustments to support new promotions. KAPL advertised on videocassettes of Hindi movies (as during those days video cassettes got duplicated (pirated) 20 times from one cassette and cost a fraction of the cost of TV advertisements), FM Radio, during test cricket commentary, and sponsored news programs (as daily TV shows and serials were costly). KAPL also pioneered the concept of sponsoring song/dance and fight sequences in movies on many satellite television channels (primarily) SitiCable and Doordarshan. All Out’s advertisements would appear before each song/dance and fight sequence in the movie. As Hindi movies typically featured 4-5 songs/dances, the viewers watched the All Out advertisement at least 4-5 times. This resulted in the brand attaining a very high mind-share among consumers. All Out had an overall share of voice of 31% vs. the nearest competitor GoodKnight’s low 5% in 2000. As competition intensified, the company lowered its price over the years aided partly be manufacturing components in-house as during those days, components were mainly imported from Japan.

Page | 22 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

We highly recommend investors read the below-mentioned link, which gives a holistic perspective to why All-Out was able to make it big despite the presence of strong FMCG companies in the same domain. https://www.icmrindia.org/free%20resources/casestudies/ALL%20OUT-marketing.htm Downfall began after the acquisition by SC Johnson and increased competition from GoodKnight After the acquisition of All Out by SC Johnson in 2005, the company made several changes in brand communication. The most Iconic mascot “frog” and jingle “Maccharon Ka Yamraaj” were pulled out. Instead, SC Johson changed its tagline to “Maccharon Pe Vaar Surakshit Aapka Parivaar” and the focus shifted from the product to the concerns of a family (like most other brands) which led to limited differentiation. The merger of Godrej Household Product Ltd (GHPL) with Godrej Consumer Product Ltd (GCPL) in 2011 also impacted All Out’s market share, as integration helped it to achieve economies of scale in terms of distribution. GHPL was strong in south India while GCPL was strong in north India. GHPL mainly sold household insecticides while GCPL had major contribution from soaps and hair colours. While All Out, was stronger in North India. As GCPL launched newer products, higher promotions All Out gradually started losing market share.

Page | 23 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

Financials Income Statement Y/E Mar, Rs mn FY20 FY21E FY22E FY23E

Net sales 98,265 1,04,637 1,16,366 1,28,262 Growth, % -3.9 6.5 11.2 10.2 Other operating income 933 843 885 929 Raw material expenses -42,617 -45,493 -50,043 -55,197 Employee expenses -10,188 -10,698 -11,767 -12,591 Other Operating expenses -24,873 -24,667 -27,861 -30,754 EBITDA (Core) 21,430 24,664 27,624 30,695 Growth, % 1.2 15.1 12.0 11.1 Margin, % 21.8 23.6 23.7 23.9 Depreciation -1,973 -2,114 -2,229 -2,344 EBIT 19,458 22,550 25,394 28,351 Growth, % (0.1) 15.9 12.6 11.6 Margin, % 19.8 21.6 21.8 22.1 Interest paid -2,174 -2,065 -1,859 -1,673 Other Income 1,123 1,067 1,227 1,411 Non-recurring Items -811 0 0 0 Pre-tax profit 17,604 21,551 24,762 28,089 Tax provided -2,639 -4,741 -5,448 -6,180 Profit after tax 14,966 16,810 19,315 21,909 Net Profit 14,966 16,810 19,315 21,909 Growth, % (36.1) 12.3 14.9 13.4 Net Profit (adjusted) 14,140 16,810 19,315 21,909 Unadj. shares (m) 1,022 1,022 1,022 1,022 Wtd avg shares (m) 1,022 1,022 1,022 1,022

Balance Sheet Y/E Mar, Rs mn FY20 FY21E FY22E FY23E

Cash & bank 7,702 11,160 14,987 19,473 Marketable securities at cost 6,372 6,372 6,372 6,372 Debtors 11,573 12,323 13,704 15,105 Inventory 17,031 18,135 20,168 22,230 Loans & advances 33 33 33 33 Other current assets 5,374 5,374 5,374 5,374 Total current assets 48,083 53,396 60,637 68,587 Investments 0 0 0 0 Gross fixed assets 98,403 1,00,903 1,03,403 1,05,903 Less: Depreciation -6,308 -8,422 -10,651 -12,995 Add: Capital WIP 789 789 789 789 Net fixed assets 92,884 93,270 93,541 93,697 Non-current assets 1,786 1,786 1,786 1,786 Total assets 1,49,570 1,55,269 1,62,781 1,70,886 Current liabilities 45,466 47,074 50,035 53,038 Provisions 1,170 1,170 1,170 1,170 Total current liabilities 46,635 48,244 51,205 54,207 Non-current liabilities 23,951 21,451 18,951 16,451 Total liabilities 70,587 69,695 70,156 70,659 Paid-up capital 1,022 1,022 1,022 1,022 Reserves & surplus 77,961 84,552 91,603 99,205 Shareholders’ equity 78,984 85,574 92,625 1,00,227 Total equity & liabilities 1,49,570 1,55,269 1,62,781 1,70,886

Source: Company, PhillipCapital India Research Estimates

Cash Flow Y/E Mar, Rs mn FY20 FY21E FY22E FY23E

Pre-tax profit 17,604 21,551 24,762 28,089 Depreciation 1,973 2,114 2,229 2,344 Chg in working capital 5,231 -246 -453 -460 Total tax paid -3,611 -4,741 -5,448 -6,180 Cash flow from operating activities 21,197 18,678 21,090 23,794 Capital expenditure -7,634 -2,500 -2,500 -2,500 Chg in investments 0 0 0 0 Chg in marketable securities -1,559 0 0 0 Cash flow from investing activities -9,186 -2,500 -2,500 -2,500 Free cash flow 12,011 16,178 18,590 21,294 Equity raised/(repaid) 2,110 0 0 0 Debt raised/(repaid) -4,597 -2,500 -2,500 -2,500 Dividend (incl. tax) -12,300 -10,220 -12,263 -14,307 Cash flow from financing activities -14,787 -12,720 -14,763 -16,807 Net chg in cash -2,776 3,458 3,827 4,486

Valuation Ratios

FY20 FY21E FY22E FY23E

Per Share data

EPS (INR) 13.8 16.4 18.9 21.4 Growth, % (4.8) 18.9 14.9 13.4 Book NAV/share (INR) 77.3 83.7 90.6 98.1 FDEPS (INR) 15.4 16.4 18.9 21.4 CEPS (INR) 18.2 18.5 21.1 23.7 CFPS (INR) 17.2 17.2 19.4 21.9 DPS (INR) 10.0 10.0 12.0 14.0 Return ratios

Return on assets (%) 11.8 12.4 13.3 14.1 Return on equity (%) 20.0 19.6 20.9 21.9 Return on capital employed (%) 16.6 17.8 19.2 20.5 Turnover ratios

Asset turnover (x) 1.2 1.2 1.4 1.5 Sales/Total assets (x) 0.7 0.7 0.7 0.8 Sales/Net FA (x) 1.1 1.1 1.2 1.4 Working capital/Sales (x) (0.1) (0.1) (0.1) (0.1) Receivable days 43.0 43.0 43.0 43.0 Inventory days 63.3 63.3 63.3 63.3 Payable days 116.6 119.2 119.6 119.9 Working capital days (42.6) (39.1) (33.7) (29.3) Liquidity ratios Current ratio (x) 1.1 1.1 1.2 1.3 Quick ratio (x) 0.7 0.7 0.8 0.9 Interest cover (x) 8.9 10.9 13.7 16.9 Total debt/Equity (%) 33.7 28.2 23.4 19.1 Net debt/Equity (%) 24.0 15.2 7.2 (0.3) Valuation PER (x) 48.5 40.8 35.5 31.3 PEG (x) - y-o-y growth (1.8) 6.2 2.4 2.3 Price/Book (x) 8.7 8.0 7.4 6.8 EV/Net sales (x) 7.1 6.6 5.9 5.3 EV/EBITDA (x) 32.6 28.1 24.8 22.1 EV/EBIT (x) 35.9 30.7 27.0 24.0

Page | 24 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

Stock Price, Price Target and Rating History

Rating Methodology We rate stock on absolute return basis. Our target price for the stocks has an investment horizon of one year. We have different threshold for large market capitalisation stock and Mid/small market capitalisation stock. The categorisation of stock based on market capitalisation is as per the SEBI requirement.

Large cap stocks Rating Criteria Definition

BUY >= +10% Target price is equal to or more than 10% of current market price

NEUTRAL -10% > to < +10% Target price is less than +10% but more than -10%

SELL <= -10% Target price is less than or equal to -10%.

Mid cap and Small cap stocks Rating Criteria Definition

BUY >= +15% Target price is equal to or more than 15% of current market price

NEUTRAL -15% > to < +15% Target price is less than +15% but more than -15%

SELL <= -15% Target price is less than or equal to -15%.

Disclosures and Disclaimers PhillipCapital (India) Pvt. Ltd. has three independent equity research groups: Institutional Equities, Institutional Equity Derivatives, and Private Client Group. This report has been prepared by Institutional Equities Group. The views and opinions expressed in this document may, may not match, or may be contrary at times with the views, estimates, rating, and target price of the other equity research groups of PhillipCapital (India) Pvt. Ltd.

This report is issued by PhillipCapital (India) Pvt. Ltd., which is regulated by the SEBI. PhillipCapital (India) Pvt. Ltd. is a subsidiary of Phillip (Mauritius) Pvt. Ltd. References to "PCIPL" in this report shall mean PhillipCapital (India) Pvt. Ltd unless otherwise stated. This report is prepared and distributed by PCIPL for information purposes only, and neither the information contained herein, nor any opinion expressed should be construed or deemed to be construed as solicitation or as offering advice for the purposes of the purchase or sale of any security, investment, or derivatives. The information and opinions contained in the report were considered by PCIPL to be valid when published. The report also contains information provided to PCIPL by third parties. The source of such information will usually be disclosed in the report. Whilst PCIPL has taken all reasonable steps to ensure that this information is correct, PCIPL does not offer any warranty as to the accuracy or completeness of such information. Any person placing reliance on the report to undertake trading does so entirely at his or her own risk and PCIPL does not accept any liability as a result. Securities and Derivatives markets may be subject to rapid and unexpected price movements and past performance is not necessarily an indication of future performance.

This report does not regard the specific investment objectives, financial situation, and the particular needs of any specific person who may receive this report. Investors must undertake independent analysis with their own legal, tax, and financial advisors and reach their own conclusions regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realised. Under no circumstances can it be used or considered as an offer to sell or as a solicitation of any offer to buy or sell the securities mentioned within it. The information contained in the research reports may have been taken from trade and statistical services and other sources,

B (TP 1100)

B (TP 1240) B (TP 1260)

B (TP 1430)

B (TP 765) S (TP 645)

F-19

S (TP 520)

S (TP 585)

S (TP 600)

S (TP 510)

B (TP 770)

200

400

600

800

1000

1200

A-17 O-17 N-17 J-18 F-18 A-18 M-18 J-18 A-18 O-18 N-18 J-19 F-19 A-19 J-19 J-19 S-19 O-19 D-19 J-20 M-20 A-20 J-20 J-20

Page | 25 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

which PCIL believe is reliable. PhillipCapital (India) Pvt. Ltd. or any of its group/associate/affiliate companies do not guarantee that such information is accurate or complete and it should not be relied upon as such. Any opinions expressed reflect judgments at this date and are subject to change without notice.

Important: These disclosures and disclaimers must be read in conjunction with the research report of which it forms part. Receipt and use of the research report is subject to all aspects of these disclosures and disclaimers. Additional information about the issuers and securities discussed in this research report is available on request.

Certifications: The research analyst(s) who prepared this research report hereby certifies that the views expressed in this research report accurately reflect the research analyst’s personal views about all of the subject issuers and/or securities, that the analyst(s) have no known conflict of interest and no part of the research analyst’s compensation was, is, or will be, directly or indirectly, related to the specific views or recommendations contained in this research report.

Additional Disclosures of Interest: Unless specifically mentioned in Point No. 9 below: 1. The Research Analyst(s), PCIL, or its associates or relatives of the Research Analyst does not have any financial interest in the company(ies) covered in

this report. 2. The Research Analyst, PCIL or its associates or relatives of the Research Analyst affiliates collectively do not hold more than 1% of the securities of the

company (ies)covered in this report as of the end of the month immediately preceding the distribution of the research report. 3. The Research Analyst, his/her associate, his/her relative, and PCIL, do not have any other material conflict of interest at the time of publication of this

research report. 4. The Research Analyst, PCIL, and its associates have not received compensation for investment banking or merchant banking or brokerage services or for

any other products or services from the company(ies) covered in this report, in the past twelve months. 5. The Research Analyst, PCIL or its associates have not managed or co-managed in the previous twelve months, a private or public offering of securities for

the company (ies) covered in this report. 6. PCIL or its associates have not received compensation or other benefits from the company(ies) covered in this report or from any third party, in

connection with the research report. 7. The Research Analyst has not served as an Officer, Director, or employee of the company (ies) covered in the Research report. 8. The Research Analyst and PCIL has not been engaged in market making activity for the company(ies) covered in the Research report. 9. Details of PCIL, Research Analyst and its associates pertaining to the companies covered in the Research report:

Sr. no. Particulars Yes/No

1 Whether compensation has been received from the company(ies) covered in the Research report in the past 12 months for investment banking transaction by PCIL

No

2 Whether Research Analyst, PCIL or its associates or relatives of the Research Analyst affiliates collectively hold more than 1% of the company(ies) covered in the Research report

No

3 Whether compensation has been received by PCIL or its associates from the company(ies) covered in the Research report No

4 PCIL or its affiliates have managed or co-managed in the previous twelve months a private or public offering of securities for the company(ies) covered in the Research report

No

5 Research Analyst, his associate, PCIL or its associates have received compensation for investment banking or merchant banking or brokerage services or for any other products or services from the company(ies) covered in the Research report, in the last twelve months

No

Independence: PhillipCapital (India) Pvt. Ltd. has not had an investment banking relationship with, and has not received any compensation for investment banking services from, the subject issuers in the past twelve (12) months, and PhillipCapital (India) Pvt. Ltd does not anticipate receiving or intend to seek compensation for investment banking services from the subject issuers in the next three (3) months. PhillipCapital (India) Pvt. Ltd is not a market maker in the securities mentioned in this research report, although it, or its affiliates/employees, may have positions in, purchase or sell, or be materially interested in any of the securities covered in the report.

Suitability and Risks: This research report is for informational purposes only and is not tailored to the specific investment objectives, financial situation or particular requirements of any individual recipient hereof. Certain securities may give rise to substantial risks and may not be suitable for certain investors. Each investor must make its own determination as to the appropriateness of any securities referred to in this research report based upon the legal, tax and accounting considerations applicable to such investor and its own investment objectives or strategy, its financial situation and its investing experience. The value of any security may be positively or adversely affected by changes in foreign exchange or interest rates, as well as by other financial, economic, or political factors. Past performance is not necessarily indicative of future performance or results.

Sources, Completeness and Accuracy: The material herein is based upon information obtained from sources that PCIPL and the research analyst believe to be reliable, but neither PCIPL nor the research analyst represents or guarantees that the information contained herein is accurate or complete and it should not be relied upon as such. Opinions expressed herein are current opinions as of the date appearing on this material, and are subject to change without notice. Furthermore, PCIPL is under no obligation to update or keep the information current. Without limiting any of the foregoing, in no event shall PCIL, any of its affiliates/employees or any third party involved in, or related to computing or compiling the information have any liability for any damages of any kind including but not limited to any direct or consequential loss or damage, however arising, from the use of this document.

Copyright: The copyright in this research report belongs exclusively to PCIPL. All rights are reserved. Any unauthorised use or disclosure is prohibited. No reprinting or reproduction, in whole or in part, is permitted without the PCIPL’s prior consent, except that a recipient may reprint it for internal circulation only and only if it is reprinted in its entirety.

Caution: Risk of loss in trading/investment can be substantial and even more than the amount / margin given by you. Investment in securities market are subject to market risks, you are requested to read all the related documents carefully before investing. You should carefully consider whether trading/investment is appropriate for you in light of your experience, objectives, financial resources and other relevant circumstances. PhillipCapital and any of its employees, directors, associates, group entities, or affiliates shall not be liable for losses, if any, incurred by you. You are further cautioned that trading/investments in financial markets are subject to market risks and are advised to seek independent third party trading/investment advice outside PhillipCapital/group/associates/affiliates/directors/employees before and during your trading/investment. There is no guarantee/assurance as to returns or profits or capital protection or appreciation. PhillipCapital and any of its employees, directors, associates, and/or employees, directors, associates of PhillipCapital’s group entities or affiliates is not inducing you for trading/investing in the financial market(s). Trading/Investment decision is your sole responsibility. You must also read the Risk Disclosure Document and Do’s and Don’ts before investing.

Kindly note that past performance is not necessarily a guide to future performance.

Page | 26 | PHILLIPCAPITAL INDIA RESEARCH

GODREJ CONSUMER PRODUCT COMPANY UPDATE

For Detailed Disclaimer: Please visit our website www.phillipcapital.in IMPORTANT DISCLOSURES FOR U.S. PERSONS This research report is a product of PhillipCapital (India) Pvt. Ltd. which is the employer of the research analyst(s) who has prepared the research report. PhillipCapital (India) Pvt Ltd. is authorized to engage in securities activities in India. PHILLIPCAP is not a registered broker-dealer in the United States and, therefore, is not subject to U.S. rules regarding the preparation of research reports and the independence of research analysts. This research report is provided for distribution to “major U.S. institutional investors” in reliance on the exemption from registration provided by Rule 15a-6 of the U.S. Securities Exchange Act of 1934, as amended (the “Exchange Act”). If the recipient of this report is not a Major Institutional Investor as specified above, then it should not act upon this report and return the same to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any U.S. person, which is not a Major Institutional Investor.

Any U.S. recipient of this research report wishing to effect any transaction to buy or sell securities or related financial instruments based on the information provided in this research report should do so only through Rosenblatt Securities Inc, 40 Wall Street 59th Floor, New York NY 10005, a registered broker dealer in the United States. Under no circumstances should any recipient of this research report effect any transaction to buy or sell securities or related financial instruments through PHILLIPCAP. Rosenblatt Securities Inc. accepts responsibility for the contents of this research report, subject to the terms set out below, to the extent that it is delivered to a U.S. person other than a major U.S. institutional investor.