INSIGHT - The IRRV · INSIGHT JANUARY/FEBRUARY 2013 5 David Magor OBE IRRV (Hons) is Chief...

36

INSIGHT INSIDE: Professor Cleverley returns • Welfare reform • Running the Institute • Management January/February 2013 £5.50 www.irrv.net ISSN 1361-1305 The monthly journal of the Institute of Revenues, Rating & Valuation Wales’s ‘magnificent eight’... ...share £1million savings in their groundbreaking single person discount review Jaws – the reunion! Andrew Burton sees a few parallels emerging between council tax support, poll tax, and a classic from the seventies!

Transcript of INSIGHT - The IRRV · INSIGHT JANUARY/FEBRUARY 2013 5 David Magor OBE IRRV (Hons) is Chief...

INSIGHT

INSIDE: Professor Cleverley returns • Welfare reform • Running the Institute • Management

January/February 2013 £5.50 www.irrv.net

ISSN

136

1-13

05

The monthly journal of the Institute of Revenues, Rating & Valuation

Wales’s ‘magnificent eight’......share £1million savings in their groundbreaking single person discount review

Jaws – the reunion!

Andrew Burton sees a few parallels emerging between council

tax support, poll tax, and a classic from

the seventies!

IRRV INSIGHT

Managing Editor

John Roberts

Editorial Director

Lester Dinnie

Art Director

Don Tregartha

Designers

Clare Barker

Roddy Clenaghan

Copy Editor

Vicki Chastney

Publisher

Tregartha Dinnie

Ltd

IRRV

Chief Executive David Magor, OBE IRRV (Hons) Northumberland House 5th Floor 303-306 High Holborn, London WC1V 7JZ T 020 7831 3505 E [email protected] W www.irrv.net

Enquiries Membership 020 7691 8996 Conferences 020 7691 8987 Subscriptions 020 7691 8996

Advertising T 020 7691 8979 E [email protected]

Editorial John Roberts IRRV (Hons) T 07952 659 258 E [email protected]

Tregartha Dinnie Ltd Ibex House, 5 Keller Close, Kiln Farm, Milton Keynes MK11 3LL T 01908 306500 W www.tregartha-dinnie.co.uk

IRRV INSIgHT is produced by Tregartha Dinnie Ltd on behalf of the IRRV.

Unless otherwise indicated, copyright in this publication belongs to the IRRV.

Jan/Feb 2013 ISSN 1361-1305

©IRRV 2013. Reproduction in whole or in part of any article is prohibited without prior written consent. The views expressed in this magazine do not necessarily represent the views of theInstitute. Whilst all due care is taken regarding the accuracy of information, no responsibility can be accepted for errors. Any advice given does not constitute a legal opinion.

Cover story 18

A two-part Insightrevenues specialIn part 1, Phil Round explains the background toWales’s magnificent eight’s £1million savings in their groundbreaking single person discount review.

In the second part, Jaws – the reunion!, Andrew Burton sees a few parallels emerging between council tax support, poll tax, and a classic from the seventies!

2

INSI

GH

T w

ww

.irrv

.net

Your IRRV Council:

IRRV PRESIdENT david Chapman IRRV (Hons)

JuNIoR VICE PRESIdENT Kevin Stewart FIRRV MAAT MCMI

SENIoR VICE PRESIdENT Richard Harbord MPhil CPFA FCCA IRRV (Hons) FIDP FBIM FRSA

HoNoRARy TREASuRER Allan Traynor FCCA IRRV (Hons)

Phil Adlard Tech IRRV MlnstLM MCMI

Alan Bronte FRICS IRRV (Hons)

Robert Brown BSc FRICS FIRRV

Tracy Crowe CPFA FIRRV

Carol Cutler IRRV (Hons)

Tom dixon RD BSc (Est Man) FRICS IRRV (Hons)

Ian Ferguson IRRV (Hons)

Geoff Fisher FRICS (Dip Rating) IRRV (Hons) REV

Richard Guy FRICS (Dip Rating) IRRV (Hons) MCIArb

Mary Hardman IRRV (Hons) FRICS MCMI

Gordon Heath BSc IRRV (Hons)

Julie Holden IRRV (Hons) MCMI CMg

Jim MaCafferty IRRV (Hons)

Kerry Macdermott IRRV (Hons)

Tony Masella MRICS MCIOB FIRRV AFA F.Inst.AM

Maureen Neave Tech IRRV

Roger Messenger BSc (Es Man) FRICS FIRRV MCIArb REV

Nick Rowe IRRV (Hons)

Peter Scrafton FIRRV FCIArb MRSA (Hons)

Angela Storey Tech IRRV MCMI

Bob Trahern IRRV (Hons)

Features

Editor’s welcome

INSIGHT is one of three magazines produced by the Institute. The quarterly offering for members involved in the sphere of valuation, VALUER, is another vital read, as is BENEFIT, the bi-monthly magazine element of the Institute’s Benefits Advisory Service. If you want to subscribe, or to find out more, go to www.irrv.net. In this edition, we welcome back many of our regular contributors, who combine to provide as ever a diverse picture of the Institute’s activities. Students and more seasoned practitioners will be pleased to see that our anonymous academic, Professor Cleverley, returns to give sound advice, and Deborah Davies is on hand to detail some significant developments in the courts. Valuer members will without doubt have views on Simon Wanderer ’s suggestion that mediation has a place in the appeals process. Benefit practitioners will be keen to seek out the views of the DWP, as the welfare reform process gathers pace. Revenues practitioners will be keen to read how North Wales has reacted to single person discount issues, which shares our cover story slot with Andrew Burton’s view of the changes anticipated as council tax support becomes local. That’s only a small snapshot of what our magazine has to offer, though. Management and leadership topics, developments in technology, and the thoughts of the Local Government Association and the Local Government Ombudsman are all in there, together with all the regular news from inside the IRRV. Read on and enjoy!

John Roberts IRRV (Hons) is Managing Editor of the Institute’s magazines

“Welcome to our first 2013 edition of INSIGHT, the membership magazine for all involved with the IRRV.”

What’s in the next issue... – Kevin Watson points to collaboration as the

way forward

– A new Viewpoint contributor makes her debut

– A special alternative revenues focus on parking issues

Chief Executive’s notes 05

News and events 06

Education and membership 08

Running the Institute 10

From the archives 13

Faculty Board update 14

Case law update 15

Benefits bulletin 17

Professor Cleverley 23

Valuation matters 24

LGA view 26

Welfare reform 27

Technology 28

LGO update 30

Management 31

Doherty’s despatch 32

Viewpoint 34

INSI

GH

T JA

NU

AR

Y/FE

BRU

AR

Y 2

013

3

Regular items

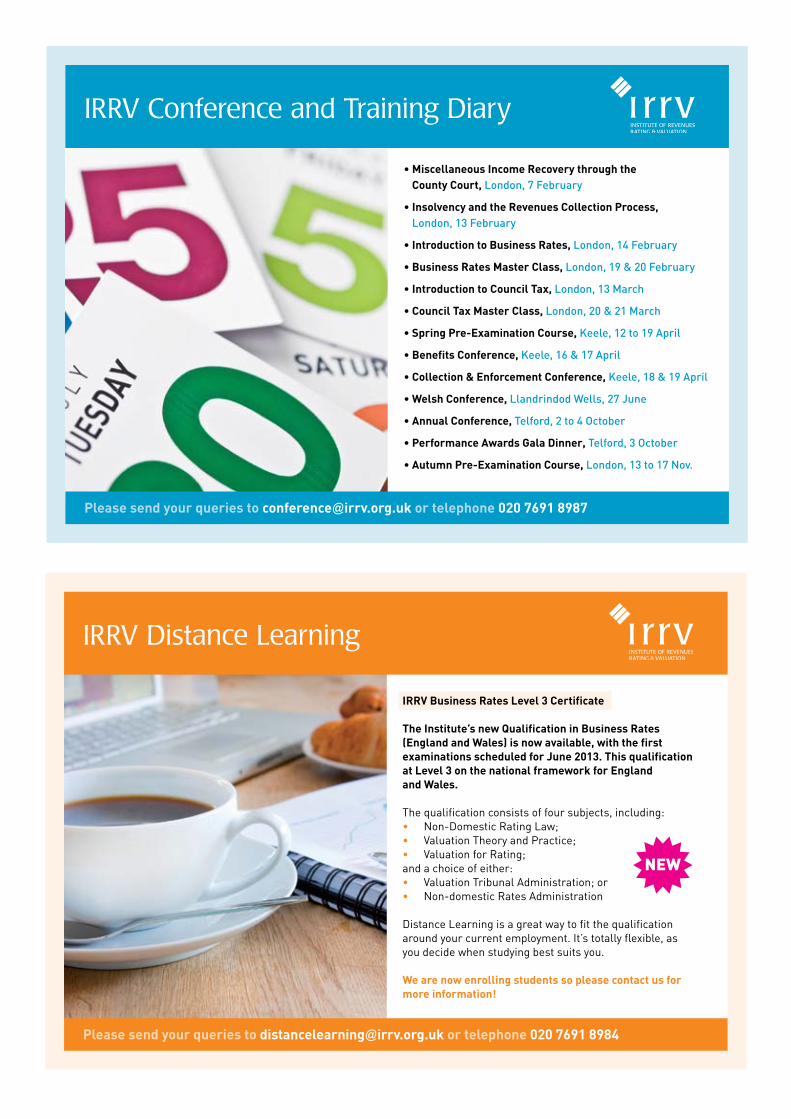

• Miscellaneous Income Recovery through the County Court, London, 7 February

• Insolvency and the Revenues Collection Process, London, 13 February

• Introduction to Business Rates, London, 14 February

• Business Rates Master Class, London, 19 & 20 February

• Introduction to Council Tax, London, 13 March

• Council Tax Master Class, London, 20 & 21 March

• Spring Pre-Examination Course, Keele, 12 to 19 April

• Benefits Conference, Keele, 16 & 17 April

• Collection & Enforcement Conference, Keele, 18 & 19 April

• Welsh Conference, Llandrindod Wells, 27 June

• Annual Conference, Telford, 2 to 4 October

• Performance Awards Gala Dinner, Telford, 3 October

• Autumn Pre-Examination Course, London, 13 to 17 Nov.

IRRV Conference and Training Diary

Please send your queries to [email protected] or telephone 020 7691 8987

IRRV Business Rates Level 3 Certificate

The Institute’s new Qualification in Business Rates (England and Wales) is now available, with the first examinations scheduled for June 2013. This qualification at Level 3 on the national framework for England and Wales.

The qualification consists of four subjects, including:• Non-Domestic Rating Law; • Valuation Theory and Practice;• Valuation for Rating;and a choice of either:• Valuation Tribunal Administration; or• Non-domestic Rates Administration

Distance Learning is a great way to fit the qualificationaround your current employment. It’s totally flexible, asyou decide when studying best suits you.

We are now enrolling students so please contact us for more information!

IRRV Distance Learning

Please send your queries to [email protected] or telephone 020 7691 8984

NEW

INSI

GH

T JA

NU

AR

Y/FE

BRU

AR

Y 2

013

5David Magor OBE IRRV (Hons) is Chief Executive of the Institute

Are we facing a year of destiny or disaster? There are major

changes in the financing of local government, we have the

postponement of the 2015 revaluation, and of course the

implementation of the early phases of Universal Credit.The changes in the financing of local government are

radical. The rating system will deliver a significant proportion

of local income. This part of the wider localism agenda will

see billing authorities become far more active in forecasting

and collecting income. The importance of the valuation process in the new system should not be underestimated.

The relationship between the Valuation Office Agency and

billing authorities will need to improve, as will the quality of

information sharing. If billing authorities cannot access

sufficient accurate data, there will need to be a rethink of their

role in relation to the valuation process.

The introduction of Universal Credit will start in 2013, and will

gain pace during 2014. Senior officials from the Department for Work and Pensions have said publicly that the first major

migration will be the tax credit caseload. Not before time, if

we are to believe the recent statements from the Secretary of

State, Iain Duncan Smith. He tells us that more than £10bn

of public money has been lost in fraud and error under the

tax credit system, put in place by the last Labour government.

He further claims that the system was “not fit for purpose”,

but had been extended ahead of the 2005 and 2010 general

elections to gain support.

In a wide ranging article, the Secretary of State said that the

system was “wide open to abuse” and was “haemorrhaging

money. In the years between 2003 and 2010 £171bn was

spent on tax credits, contributing to a 60% rise in the welfare

bill.” He claimed that Her Majesty’s Revenue and Customs

(HMRC) conducts checks on far fewer tax credit claims than

suspected benefit fraudsters. That is despite about one in 12

tax credit claims being incorrect or fraudulent, compared with

fewer than one in 25 for other benefit claims.

In this revealing article, Mr Duncan Smith stated that HMRC

did not attempt to reclaim overpayments of less than £25,000,

and that is set to be reduced to £5,000 under the coalition,

alongside moves to require proof of payments from those

claiming for childcare, or where children aged between 16 and

19 are in full-time education. Let’s hope the enforcement structures will be put in place to cope with this massive

growth in work, and that the Single Fraud Investigation Service will be able to deal with the increase in caseload.

Of course, the provision of state of the art authentication and verification systems should secure the gateways, and

hopefully reduce the incidence of fraud and error.

Chief Executive’s notes

“This part of the wider localism agenda will see billing authorities become far more active in forecasting and collecting income.”

2013 – a year of destiny or disaster? David Magor ponders the likely outcome

Are we facing a year of destiny or disaster? There are major changes in the financing of local government, we have the postponement of the 2015 revaluation, and of course the implementation of the early phases of Universal Credit.

6

INSI

GH

T w

ww

.irrv

.net

News and events

IRRV asserts its position following Welsh charity rate proposalsFollowing a review for the Welsh government recommending reducing business rate relief and tightening qualifying rules, the IRRV has issued its own response to the proposals.The response has provided the Institute with the chance to voice its long held

views that strongly advocate a total overhaul of the relief system – not only in

Wales, but in Scotland and England too. The response continues, “The review of

course needs to go deeper than any superficial highlighting of the anomalies

in, and potential pitfalls of, including other types of entity in the relief. Any fuller

examination, in which we would be pleased to play a part, should for example

look at the particular issues around the following:

• could the relief be viewed as inefficient and acting against general market

forces, and might other forms of tax relief be less intrusive? For example, is it

important that the charities get the full benefit or is it acceptable that some of

it goes to landlords? Does the certainty of relief price small businesses out of

the market at a time when we should be helping them?

• applying relief to all registered charities

• the ‘wholly and mainly’ rule

• how Community Amateur Sports Clubs should be treated

• not-for-profit entities

• application of reliefs in respect of operating companies

• the appropriateness of the 80% relief to all types of activity and whether

there should be different classes of occupation attracting differential relief

(it would not be easy to sub-divide the various charitable relief bodies, but

they are growing thick and fast, with varying degrees of ‘charity’ within their

organisation)

• the application of relief in respect of ‘Academy’ schools, and

• the growing use of charity occupation to enable empty rate to be avoided.”

It’s caption competition time again...! ...and this time we want to know what IRRV Past President and current chair of the Institute’s Commercial Services Committee Carol Cutler was thinking to herself, as she introduced the domestic announcements at the opening of last year’s Annual Conference.

The December issue’s offering produced a couple of joint winners! As ever, we have a slightly risky one, this time Peter Hurlstone’s “They tell me that it isn’t the size of my instrument that matters, it ’s what I do with it”, as he reads the thoughts of South Eastern Association President, Pat Knight. And “Yet another statutory instrument that no-one knows how to handle”, and “This is actually a double bass scaled down to my size” (sorry Pat, I thought he was your friend – Editor!) were the suggestions of Andy King. Keep ‘em coming!

Captions invited!Captions invited!

Rating Diploma qualification re-launchedIn November 2012 a new protocol agreement was signed by Paul Ridley, chairman of the RICS Rating Diploma Holders’ Section (left in photo) and Alan Collett, RICS President, launching the new style Rating Diploma Study Course.The first tranche

of candidates

undertaking the

course started

in January 2013,

with further

applications

being sought

later in the year

for a September

2013 start.

The study course consists of nine modules covering areas such

as rating law, valuation, compilation of valuation lists/rolls and

domestic/non-domestic borderline, for which assignments will be

set and marked, followed by a practical test and interview, and is

spread over a two year time frame.

Anyone who would like to find out more about the Rating

Diploma can contact the Project Manager, Duncan McLaren

([email protected]) or the Rating Diploma

Holders’ Section Honorary Secretary, Helen Zammit-Willson

The Rating Diploma Holders provide regular magazine

contributions in the Institute’s popular Valuer magazine.

7

LATEST NEWS

The bailiff debate moves onFollowing the Local Government Ombudsman’s publication of a new focus report on councils’ usage of bailiffs, Local Government Minister Brandon Lewis said,

“Clearly, councils have an obligation to their local residents to

collect council tax, as every penny of uncollected council tax effectively

increases the tax burden on the law-abiding local residents who do

pay their bills on time. Yet councils equally need to show compassion

towards the vulnerable and recognise individual cases of hardship.

The use of bailiffs should also be a last resort, they should not be

commissioned disproportionately, and councils should take direct

responsibility for them.”

(Editor’s note – read Andrew Hobley’s regular LGO column on page 30 of this month’s Insight).

Rate reliefs and exemptions to assist business extendedNorthern Ireland Finance Minister Sammy Wilson has announced that the Empty Retail Premises Relief scheme and the rates exemption for stand alone ATMs in rural areas, due to end in March 2013, will now be extended until the end of the current budget period in March 2015, subject to Assembly approval.The Minister also announced his intention to extend the current 18

month ‘developer exclusion’ applicable under the rating of empty

homes for a further 12 months. Speaking in the Assembly, he

commented, “The Executive recognises the difficulties that our local

businesses are facing, and are committed to helping them in these

challenging financial times. Northern Ireland has led the way with this

innovative scheme, and was the first devolved administration in the

UK to introduce such an initiative.” He continued, “52 businesses have

benefitted from a 50% reduction on their rates totalling £143,000

since the introduction of this new rate relief in April 2012.”

INSI

GH

T JA

NU

AR

Y/FE

BRU

AR

Y 2

013

The President’s travelsInsight is pleased to provide highlights

of President Dave Chapman’s first

months in the hot seat. Regular

excerpts from his blog, which you can

view on www.irrv.net, will be included

in Insight this year.

“After the euphoria of receiving

the President’s chain of office from

Roger Messenger at the Telford Annual Conference in October,

I was quickly introduced into the role of President, attending

the Association Representatives Meeting on the last day of

Conference in the Conference hotel. It was really heart warming to

be welcomed and appreciated by so many revenues and benefits

professionals, with whom I had previously been a counterpart in

the very same meetings. Immediately after the meeting I arranged

a planning meeting for the year ahead with the Chief Executive,

David Magor, at a secret venue in Oxfordshire on the following

Monday! Here I received diary dates of known events, and looked

at identifying future Council meeting dates. I also advised that my

charity for the year would be Rossendale Hospice, and agreed

to set up a Just Giving site to facilitate any donations – if you

want to donate, go to www.justgiving.com/David-Chapman5.

Apart from that initial flurry of activity, I enjoyed a relatively quiet

month in October and couldn’t understand what all the fuss was

about – it was simply business as usual... or so I thought!

November 8th saw my first official function, where I flew

out to Rome to attend the The European Group of Valuers’ Associations (TEGoVA) Conference and General Assembly, a

three day event. It was truly an experience to hear the interpreters

grappling with valuation terminology delivered through our

headsets as we listened to though provoking papers from across

Europe. I had to check sometimes that I was on the correct

language channel, and I have to say pronouncing IRRV is difficult

in any language! One thing became very clear – how really well

thought of the Institute is within these European circles. Of course

there is no higher testimony to that than the fact that Roger Messenger is the current Chair of TEGoVA. I was made to feel

very welcome, and soon found that I knew more about valuation

than I had thought. I also realised there are very real opportunities

to expand both the membership and influence of the Institute

across Europe.

My worst memory of the trip

was the six hour delay I endured

at the Leonardo Da Vinci Airport,

for the return flight, which meant

I now landed in Manchester

at 2:30 in the morning, with a

train booked for my first Council

meeting in London departing

at 7.30am. Of course I advised

my Chief Executive that I may

possibly be late or even stuck

in Rome for my very first meeting chairing Council! As it happened I

managed two hours sleep before boarding my train to London. The

same week on the Friday I attended my first Association Dinner, in

honour of Andrew Solley (photographed here with me), President

of the East Midlands Association, at the Casa in Chesterfield.”

You can read more of President Dave’s travels in next month’s

edition of Insight.

Fraud reduction announcedBenefit fraud fell last year – but more action is needed to stop the £1.2bn cost to the taxpayer each year, Minister for Welfare Reform Lord Freud said recently.The Department for Work and Pensions figures show total

overpayments due to fraud and error stood at 2.1% of all benefit

expenditure or £3.4bn over the last year.

Lord Freud said, “We are fighting the battle against fraud and

making advances, but fraud in the benefits system remains a huge

problem. We have given our teams more resources and more powers

so investigators are now actively tracking fraudsters, using a mixture

of the latest technology and old-fashioned detective work.”

He added, “From next year (2013), Universal Credit will also make

fraud much harder to commit and easier to trace quickly.” We shall

wait and see!

8

INSI

GH

T w

ww

.irrv

.net

Education and membership

Michael Hopkins is on hand with his first education roundup of the New Year

The Institute’s education programme is

both traditional – in the form of day-

release and revision classes – and delivered

electronically. Full details of these options

can be viewed on the Institute’s home page,

www.irrv.net. In addition to examination preparation classes delivered in London

and venues around the country, training sessions for professionals are offered at

the Institute’s London headquarters. Upcoming

training sessions include a session entitled

Current Developments in Council Tax and Non Domestic Rates and a Business Rates Master Class, which are filling up rapidly, with

several ‘sell outs’. For details of these and other

events, see www.irrv.net/trainingdays.

Webinars – and free access to past webinars

– can also be found on the website, and the

Institute continues to offer online training programmes which can be purchased for

access by variable numbers of users. These

provide an invaluable source of training,

briefing and reference. Check prices and

programmes at www.irrv.net/euclidian.

The Qualifications Management Board,

Michael Hopkins is Head of Professional Services

with the Institute. You can contact him on

New members

StudENt MEMbErSNaMe eMployeR

Adrian Johnson South Kesteven

District Council

Clare McIntosh G L Hearn Ltd

Karen Armstrong Durham County Council

Darren Glasper Durham County Council

John Naylor Durham County Council

Jennifer Childs Cardiff Council

Sean O’Donnell Caerphilly County

Borough Council

Vicki Burgess G L Hearn Ltd

Howard Dye Hull City Council

Gaynor Jackson Wakefield Metropolitan

District Council

Andrew Sims Hull City Council

Derek Frankland Preston City Council

Melanie Poole Burnley Borough Council

Richard Chambers Mua Property Services Ltd

Grainne Mears-Bullen Lewisham London

Borough Council

Ademuyiwa Oniwonlu Rochvilles & Co

Jade Pinnock Lewisham London

Borough Council

Angela McDonald Powys County Council

Mark Dent Cardiff Council

Alice Gridley Gerald Eve LLP

Fay Kyson-Waller Gerald Eve LLP

Steven Lavis Gerald Eve LLP

Andrew Rudd Gerald Eve LLP

Matthew Selman Gerald Eve LLP

David Welsh Gerald Eve LLP

Kate Herridge West Berkshire Council

Jodie Gardiner Wakefield Metropolitan

District Council

COrPOrAtE MEMbErS NaMe eMployeR

Baldeo Ramoutar Ministry of Finance (Trinidad)

Amrik Boghan Coventry City Council

Gary Yeardley Normie & Company

dIPLOMA MEMbErS NaMe eMployeR

Stephen Challis South Ayrshire Council

Ishmael Kamal Turney The Land Tax Department

HONOurS MEMbErS NaMe eMployeR

Michael Telford JTR Collections Ltd

Barry Davies Self-employed

Christine Telford SLR Consulting Ltd

David Vernon CBRE Ltd

Lorraine Arrowsmith Valuation Office Agency

Assessment Centre

Andrew McKillop Valuation Office Agency

Assessment Centre

Don’t forget to update your membership details.

Log on to

www.irrv.net

Since the early 2000s, the Institute has

been instrumental in the production and

maintenance of National occupational Standards (NOS) in the administration of local Revenues and Benefits. NOS are

statements of competence which express

the particular requirements for workplace

performance. The Standards are public

documents under the stewardship of asset Skills, the Sector Skills Council which

covers the Institute’s professional areas.

NOS can be used as a basis for recruitment

and selection, training design and delivery,

drawing up person specifications and job

descriptions, and can inform the development

of vocational qualifications.

NOS are intended as a high level strategic

overview of the competencies required to fulfil

tasks effectively within industry.

Asset Skills are now formulating a bid for

2013/14 which includes some potential work

in the area of local taxation and benefits.

This work will take in the updating of the NOS

and the apprenticeship framework, in the light,

particularly, of national changes to benefits.

To help justify this work, Asset Skills requires

industry support, and they have asked the

IRRV, as the leading body in the occupational

area, to provide the principal input. To this

end there will shortly be consultation and

requests for views and responses on the

NOS revision. Consideration must be given

to the titles, classification and content of the

NOS. Currently they are laid out under the

headings performance and Knowledge and Understanding, and this aspect as well as the

titles and breakdown of the Standards can all

be reconsidered.

Any individual or organisation wishing to be

involved in this important work should make

contact at the email address at the end of this

article. This work will directly benefit the sector

and serve its employers’ needs.

With Certificate and Diploma qualifications having been updated to take

account of benefits changes, we are currently

in a period of transition. Those students who

have learned material relating to council tax benefit, and who will be taking examinations

based on the housing and council tax benefit

syllabi, will still be able to do so in June

2013, and in housing benefit at least until

December 2013. The Institute has considered

its policy with regard to council tax benefit,

which is withdrawn from April 2013, and in the

interests of fairness has resolved that in June

2013 relevant examinations will still refer to

council tax benefit. Areas such as backdating,

overpayments and appeals, which practitioners

will still need to be aware of at that time, will

be examined. More detailed guidance will

be issued early in 2013, so that students can

revise appropriately.

It is not anticipated that questions on

council tax benefit will be set in or after

December 2013, but this will be confirmed in

the new year guidance. On this subject, the

Institute is revising its l3 QCF vocational qualification. The existing qualification

is being withdrawn, and replaced with

a similar unit-based qualification which

specifies required competence in the areas of

Universal Credit, local council tax support and welfare benefits. At the same time, an

‘advice’ stream is being introduced, aimed

at employees who offer advice rather than

carry out processing work. Further details are

available, as always, from the Institute.

Comment and input may be referred to at

[email protected] Current NOS available from www.irrv.net/education/item.asp?Iid=203&WaI=6

INSI

GH

T JA

NU

AR

Y/FE

BRU

AR

Y 2

013

9

Name QualIfIcaTIoN emPloYeR

Natalie Farr NVQ in Housing and City of Bradford Council Tax Benefits Metropolitan District Council

Claire Norton NVQ in Housing and Exeter City Council Council Tax Benefits

Deborah Collingswood NVQ in Housing and North Devon District Council Council Tax Benefits

Carrie Stratford NVQ in Housing and Cotswold District Council Council Tax Benefits

Kerry Wykes NVQ in Housing and Cotswold District Council Council Tax Benefits

Helen Longworth NVQ in Local Taxation Cheshire East Council

Dorn Pughsley NVQ in Local Taxation Coventry City Council

Christopher Kent NVQ in Local Taxation Cotswold District Council

Hayley Bandry Level 3 QCF Benefits Pathway Shepway District Council

Beverley Madden Level 3 QCF Benefits Pathway Shepway District Council

Dani Cooke Level 3 QCF Generic Pathway Teignbridge District Council

Jemma Graves Level 3 QCF Generic Pathway Maidstone Borough Council

Claire Yeo Level 3 QCF Revenues Pathway Isle of Wight Council

Latest vocational qualification successes

FELLOW mEmbErs Name emPloYeR

Heather Neate The Audit Commission

Anne Firth Self-employed

Nicholas Chatterley Jones Lang LaSalle Ltd

Allan Clark North Hertfordshire District Council

Graham Ryall Colliers International Property Consultants UK

QCF/sVQ mEmbErs Name emPloYeR

William Sloan Shepway District Council

Kathryn Weeks Shepway District Council

Cindy Dickson Isle Of Wight Council

Ruslan Aliyev Southwark London Borough Council

Daniel Langdon Bath & North East Somerset Council

Martin Smith Bath & North East Somerset Council

Melanie Hamill Shepway District Council

Emma Pidwill Gravesham Borough Council

AFFILIATE mEmbErs Name emPloYeR

John Jones Lewes District Council

OrGANIsATIONAL mEmbErs Name

Council Tax Advisors Ltd

Congratulations to everyone!!

New members (Cont/d)

Annotated Council Tax Legislation 2012 (2nd update – December 2012)

Annotated Council Tax Legislation is a comprehensive 3 volume set, containing all the parts of the Local Government Finance Act 1992 relevant to the administration of Council Tax. It includes appropriate sections and schedules from the Local Government Acts of 1999 and 2003, the Human Rights Act 1998 and the Greater London Authority Act 1999, and is fully updated to include changes made by the Localism Act 2011 and the Welfare Reform Act 2012.

All current statutory instruments from 1992 to the publication date are included, and all amendments brought about by these regulations and orders have been made to the originating text.

Annotated Council Tax Legislation is supplied in hard copy format together with an electronic PDF version.

IRRV Publications

To purchase online or for more information, please visit: www.irrv.net or phone 020 7691 8977

Did you know?You may be able to claim tax relief on yourmembership subscription. Download the Tax Relief membership briefing guide to find out how.

Log on to www.irrv.net

10

INSI

GH

T w

ww

.irrv

.net

Running the Institute

people certainly did give you a feeling of

warmth. The Gamesmakers were very helpful

to each other, too, and one of the best

evenings I had was when I was called into

action ‘high-fiving’ children on the spotty

bridge in the Olympic Park.

Around 9pm, Gamesmakers could go up the

Orbit – the view from there was truly stunning.

For me, it was an awesome experience – to be

in the presence of such inspiring athletes, and

to experience the atmosphere in the park and

venues, will also stay with me forever. It made

the hairs stand up on my neck!

The closing ceremony for the Paralympics

brought an end to the volunteering for

most Gamesmakers, but I was on duty for

two further days, missing the GB Athletes’

Parade on the Monday. I finally signed off my

volunteering duties at 7.30pm on Tuesday

11th September, after the last airport run for

my client. Giving up the car was emotional,

and by this time most of the cars had been

decommissioned, so at least I had a choice of

car park spaces.

I have so many memories – friends either

say I was mad, or they are very jealous of my

volunteering – although I think if the authorities

were offered such an opportunity today, they’d

be swamped by the numbers applying. I’ve

made many new friendships. but I’ll miss the

positive ‘can do’ attitude of all that participated.

I’ll miss the bacon butties in the morning, the

infamous packed lunch (I kept the insulated

lunch box!) and the decision on where to eat

my dinner. Was I really eating it in the Athletes

Village of London 2012? And I’ve got an

invitation to go to Kuala Lumpar, and believe

me, they are such fantastic, hospitable people.

There are a few moments for me that stand

The Paralympic Games Opening Ceremony

took place on 29th August – on this day fleet

transport, including the BMWs, should have

been off the road at 3pm.

The Olympic Park and other venues were

largely accessible by public transport to the

vast majority of spectators. However, there

was a complex network of service roads

linked to all stadiums and venues, including

the Olympic Park. The car would find its way

towards the front door of each venue for

me to drop off my important clients. In the

Olympic Park they had both a southern and

northern circular route, and you quickly worked

out where to go. If in the Olympic Park we’d

mostly park in the Westfield Shopping Centre,

as that car park was closed to shoppers during

the games, although the shopping centre itself

of course remained open.

The first of those special moments was

to come on 31st August. This happened to

be the 55th year since Malaysia obtained

independence from the UK. They held a

ceremony at their ambassador’s residence and

then laid on some lovely food. I was invited

to attend – a real honour – and the Malaysian

hospitality was brilliant.

The next day I was asked to report to a

residence in South Kensington. I was being

asked to drive a former Prime Minister (from

2003 to 2009) of Malaysia to the Olympic

Stadium in the Park. I drove him there and

back, together with his wife, and afterwards

they kindly invited me to their official

residence for lunch.

The hours for me were very long, and would

often change as the day progressed. I had to

be available at a moment’s notice to pick up

the client. This could mean short waits, or

waits of up to ten hours... as happened on

one occasion. Around this I tried to get into

various events, which I succeeded to do at

the Olympic Athletics Stadium, the Aquatics

Centre, Excel, Brands Hatch and Archery at the

Royal Artillery Barracks, amongst others!

The atmosphere in the park was like a big

positive bubble. Both the Great British public

and the Gamesmakers played their full part.

The noise in the stadiums I’ll remember for

life. I was very lucky to have such access.

Seeing the smiles on the faces of so many

out even more, and that is the thanks of the

public. I travelled to and from my volunteering

duty in my uniform, and the public would come

up and thank you for your efforts on the tube

and on the buses. They’d stop you on the street,

but for me the highest point of thanks was the

complete stranger who stopped their car whilst I

waited at a bus stop early one Saturday morning,

and offered me a lift to the tube, as he wanted

to thank a Gamesmaker for the wonderful

experience he had in the park the Monday

before. It really was a magical Disneyland style

event for nearly three weeks, and I am pleased

to say that I played my small part.

...maybe the oldest IRRV torchbearer?

Photographed is former long-standing

Institute member and revenues chief Ted

Morris, who, although well into his nineties,

still found time to join in the Olympic

celebrations earlier this year, at his nursing

home in Newquay!

“ For me, it was an awesome experience – to be in the presence of such inspiring athletes, and to experience the atmosphere in the park and venues, will also stay with me forever.”

Kevin Stewart continues his tale of Paralympic volunteer Gamesmaker, in the final part of a two part feature

Kevin Stewart FIRRV MAAT MCMIis Junior Vice-President of the IRRV

INSI

GH

T JA

NU

AR

Y/FE

BRU

AR

Y 2

013

11Gary L Watson IRRV (Hons) is Deputy Chief Executive of the Institute

Running the Institute

Commercial Services CommitteeThe meeting was chaired by Carol Cutler (having been re-elected for a further year).

Key agenda items included:

• Sales and sponsorship

• Conferences (including Performance Awards)

• Professional meetings and training courses

• Forum (and Benefit Advisory) Services

• Update on activities in Scotland and

Northern Ireland

• Communications Working Group

(magazines, website and publications).

Committee focussed their attention on the

Annual Conference (including Performance

Awards) that had taken place in October. The

latest position on the outturn was reported.

The feedback from delegates, exhibitors and

finalists was noted, and it was agreed this

would be discussed in further detail at the

next meeting, when the arrangements for

2013 would also be finalised. In the meantime,

a Conference Sub-committee was set up to

approve the conference programmes for 2013.

Education and Membership CommitteeThe meeting was chaired by Julie Holden

(having been re-elected for a further year).

Key agenda items included:

• Qualifications

• Membership (including a strategy to

increase membership)

• Qualifications Management Board

• Electronic learning

• IRRV courses.

A comprehensive report updating members

on the existing qualifications, together with

the planned qualifications in enforcement

and non-domestic rate was received. There

was discussion on the existing Level 3

Certificate and Diploma syllabi, and the

changes proposed by the Syllabus Review

Committee. With decisions now taken, the key

was communicating these to course providers,

employers and students straight away. With

time for the meeting limited, a detailed

discussion on membership was deferred to the

next meeting in January.

IRRV HQ was again the venue for the fourth

(and final) cycle of quarterly Council meetings

in 2012. A summary of what was discussed is

detailed below:

CouncilThe meeting was chaired for the first time

by the new President, Dave Chapman.

Key agenda items included:

• Reports of standing committees

• Chief Executive’s report

• President’s report.

In addition, Council received a presentation

from consultants engaged to review the public

relations, media, press and image of the

Institute. This was an interim report based on

interviews with those that had attended annual

conference the previous month. A final report

would be received early in the New Year.

Policy and Resources Committee The meeting was chaired by Richard Harbord.

Key agenda items included:

• ‘Options’ paper

• Management accounts at 31st August 2012

• Administration

• Media and marketing

• Revenue streams from Europe.

The key discussion was around the options

paper, and the decisions that needed to be

taken by Council when agreeing the budget

for 2013. Whilst the financial position of the

Institute remained sound, it was necessary to

set a budget once Council had agreed where

they would like the Institute to be in the short,

medium and long term. It was agreed that the

Chief Executive and Deputy Chief Executive

would put together a budget that reflected the

views of Council members, and present it to

Council in January for approval.

The management accounts at 31st August

2012 were also received and discussed in detail.

As with all organisations, there remained a need

to keep costs down whilst maximising income.

The Honorary Treasurer had revised the forecast

for the year – this had taken into consideration

the outturn from Annual Conference in October,

and the potential income streams scheduled to

arrive later in the calendar year.

Law and Research CommitteeThe meeting was chaired by Peter Scrafton

(having been elected chairman at the start of

the meeting). Key agenda items included:

• Reports of the three Faculty Boards

• Meetings with government bodies

• Research, consultancy and educational

funding streams.

Since the last meeting, the Institute (through

the Faculty Boards) had been actively involved

in putting together responses to the following

consultation documents (copies of the

responses are available on request):

• Localised Support for Council Tax Funding

Arrangements (England) (July)

• Universal Credit Regulations 2012 (including

other regulations) (July)

• Implementation of Universal Credit (August)

• Scottish Social Fund Successor (note:

submitted by the Scottish Association)

(August)

• New rules for the First Tier Lands Chamber

(England & Wales) (September)

• DCLG: Localising Support for Council Tax

(Council Tax Base) (October)

• Council Tax Reduction Scheme – Default

Scheme (Wales) (October)

• Council Tax: Long-Term Empty Homes in

Wales (October)

• DCLG: Empty Homes Premium: Calculation of

council tax base (October).

Although a number of reports are deemed

to be ‘commercially sensitive’ (particularly

those considered by Commercial Services

Committee, where a number of papers

are only circulated to those that sit on this

committee), Council remains keen for the

membership to be made aware of matters

discussed at the quarterly cycle of meetings.

Should a member require further information

on any of the reports considered by Council

at this cycle of meetings, they should contact

Gary Watson (Deputy Chief Executive) on

Gary Watson summarises the latest cycle of IRRV Council meetings, held in London on 12th November, 2012

This is a web-based, interactive learning tool designed for Revenues, Benefits & Customer Service staff. Training officers’ time is at a premium, so this versatile product has been designed to meet the business needs of Local Authorities.

The IRRV Online Training programmes are designed to train officers to a high standard AND also feature an ‘upto-date’ Resources Centre which is maintained daily with the latest circulars from the DWP. The programmes have a tutor functionality which will allow you to monitor staff progress.The programmes are written by practising specialists.

Where it fits in the workplace

• It does not replace the Training Officer.• It does allow training to take place where and

when the trainee and the employer wish.• With centrally updated programmes your managers and

trainers have more time to focus on ‘one-to-one’ tuition.• Trainees will be able to have control over their own

development.

Please send your queries to [email protected] or telephone 020 7691 8994

The IRRV Vocational qualifications can be achieved whilst at work. This benefits the employer as members of staff are always present at work to complete the qualification.

The qualification introduces aspects of revenues and benefits that many members of staff have never encountered before, but which help them to gain a fuller view of their job role. Completing this qualification will allow the member of staff to have the letters Tech IRRV after their name.

Benefits of Vocational Qualifications

• Learning fits around your organisation’s needs and work demands.

• Learners gather evidence in their normal work activities for parts of the qualification.

• The qualifications are up-to-date, and can be adapted to suit the changing needs of the revenues and benefits field.

Some learners are eligible for funding to achieve this qualification.

IRRV Vocational Qualifications

Please send your queries to [email protected] or telephone 020 7691 8994

Having agreed the recommendation to the

AGM for a change to Rule 5 (the creation of a

Benevolent and Defence Fund) at their meeting

on 7th September, the executive committee

then considered communications from Messrs

Rust (Islington) and Moyers (Kensington) relative

to a claim from Mr Westbrook, in respect of his

superannuation as a collector of St. Pancras.

The position was explained to the committee

by Mr Crane, who stressed that at this time,

Mr Westbrook did not require any pecuniary

assistance. However, if further action against the

vestry of St Pancras proved necessary, he hoped

that his brother-collectors would not allow the

entire burden to fall upon himself. The matter

was adjourned sine die for the time being. The

meeting then concluded with the secretary

being asked to send out a reminder to those

that had outstanding membership fees.

The executive next met on 30th November,

when Mr Gane alluded to Mr Westbrook’s action

against the Vestry of St. Pancras that had now

been considered by the Queens Bench Division

of the High Court. They had issued an ‘order of

mandamus’ commanding the Vestry to consider

and determine the grant of a pension to Mr

Westbrook. A report of the case was covered in

The Times on 23rd November 1889 – a relatively

quiet day for news, although it was on this day

the first juke box was ever used, having been

installed in the Palais Royal Saloon, San Francisco.

The scene from the Palais Royal Saloon... a

similar scene is no doubt being created in

organisations now the Institute has launched its

monthly webinar to members

It was recorded in The Times that Mr Westbrook

(aged 73) had 30 years in office as a rate

collector. In December 1888, he had given notice

to resign on the next Lady Day on a retiring

allowance. His salary was £480, and his retiring

allowance would be £230. The Vestry Committee

had considered the matter, and decided he

should only receive an allowance of £150 a year.

This was refused, and he was duly dismissed,

with a successor appointed. Lord Coleridge and

Mr Justice Mathew concurred – a ‘Rule absolute

for the mandamus’ was duly granted in favour of

Mr Westbrook in the High Court.

Mr Crane concluded the discussion by stating

it would be very gratifying for Mr Westbrook if

a communication was sent by the association

offering him some form of encouragement. It

was agreed the secretary would send such a

letter to say the association was pleased to learn

of his success to date and it was hoped this

would continue now the vestry have decided to

appeal against the decision of the High Court.

The chairman then referred to a letter he had

sent to the Right Honourable Charles J Ritchie

MP, who was the current Chairman of the Local

Government Board (and went on to become

Home Secretary and Chancellor of the Exchequer)

– a result of rate collectors being prejudicially

affected by actions of the London County Council

under the Local Government Act 1888.

The letter read:

Sir,Having seen in one of the daily papers that the provisions of the measure dealing with vestries were virtually settled and that vested interests would be preserved, I take liberty on behalf of the association I represent to draw your attention to what appears to us the inadequacy of the clause dealing with this matter in the Local Government Act of last year.

It seems that some of the Metropolitan Collectors collect the vestry rates only, and now that the county council precept is added to the Poor Rate, they lose the commission they formally received on the Metropolitan Board of Works Consolidated Rate, which was included with the Vestry Rates.

Now the former part of Section 120 of the Local Government Act clearly states that every officer suffering “pecuniary loss by...

diminution or loss of fees or salary shall be

entitled to have compensation paid to him”, but it adds “by the county council to whom

the powers of the authority, whose officer he

was, are transferred under this Act.” In the cases referred to, the officers still continue to serve the same authorities and their powers have not been transferred, but the direct pecuniary loss has in some areas been considerable.

We feel sure this was not the intention of the government, and shall esteem it a great honour if you will cause such addition to be made to the new Bill, as may remove any doubt, if you think any exists, as to the application of the above mentioned section to the cases referred to.

May I also be permitted to say that on a former occasion we were asked to supply certain information and to express an opinion concerning the practical working of such portions of a proposed measure, as came within our immediate knowledge, and that we shall be very pleased to render similar service, or any other in our power, on the present occasion, if desired.

I have the honour to be, Sir, your most obedient servant.

W HughesChairman, Metropolitan Rate Collectors Association

A letter was then considered from Mr

Earles who had expressed concern over

the difficulties which had arisen under the

Advertising Stations (Rating) Act 1889,

a matter which was deferred to the next

meeting. The meeting then concluded with

the date of the Annual General Meeting (and

Dinner) being fixed for 11th January 1889 and

the appointment of the dinner committee.

They then met on 14th December 1889, when

the Chairman was given a budget of £5.50 to

engage artistes for the evening.

Members are invited to contribute towards the feature and come forward with their own personal

memories of the Institute. The Deputy Chief Executive is also happy to try and answer any questions

on the Institute’s history. In addition, copies of previous articles can be provided on request.

Please contact him on [email protected] L Watson IRRV (Hons) is Deputy Chief Executive of the IRRV

From theGary Watson dusts down the time machine with the second part of his visit into 1889

INSI

GH

T JA

NU

AR

Y/FE

BRU

AR

Y 2

013

13

14

INSI

GH

T w

ww

.irrv

.net

Faculty Board update

in December 2012 Insight magazine, it

also generated several requests for it to be

turned into an IRRV webinar, a matter which

I am following up, as well as reporting it on

LinkedIn, as the topic had not been debated

in public in the UK, apparently, before Telford.

We must not forget, either, Keith Wheeler and John Swinnerton’s joint session

on valuation for local housing allowance.

This coverage demonstrated a distinct link

between the Valuation and Benefits Faculties of the Institute.

If you were not at Telford – you missed

some first-rate sessions – you would be wise to

pencil in a trip to this year’s conference, once

again in Telford, from 2nd to 4th October 2013, so that you do not miss out once again

next time!

Apart from its efforts in Parliament, through

our member the Earl of Lytton, to secure

improvements to the Local Government Finance Bill (he also spoke at Telford), the

Board has contributed to the recent review of

the impact of business rates relief for charities

in Wales. It is substantively a revenues topic

(and therefore led upon by the LTR Faculty Board), but it does have consequences

for private sector valuers advising ratepayer

clients, hence the VFB input. We commended

the Welsh Government’s stated intention

to “bring together partners representing

charities, business and other partners to

examine the evidence and suggest some next

steps.” The Institute has offered its full input to

that process.

In similar vein, the Board, in conjunction

with the Institute’s Scottish Association, will

provide input to the Scottish Government’s

consultation on non-domestic rates, to inform

future Scottish business rates policy – the

deadline for submissions being 22nd February.

The paper, Supporting Business, Promoting Growth, seeks views on how the business

rates system can better support sustainable

economic growth, whilst still delivering the

I begin this piece by recalling some quite

superb valuation sessions, which were provided

as part of the Institute’s Annual Conference

in Telford last October. The Rating Diploma Holders’ day was held very successfully within

the IRRV conference timetable for the second

year running, and it generated many thought-

provoking presentations.

A second day of the conference was given

over to a stream covering more non-rating

valuation topics. The December 2012 issue of

Valuer magazine has reports of the sessions

by Roger Messenger (regarding contractor’s

basis of valuation), Duncan McLaren (an

update on recent cases) and me (completion

notices). I feel it is worth mentioning in

despatches, however, Simon Layfield’s

paper on asset valuation, Stan Edwards’

presentation on retail-led CPOs and Ted Westlake and Richard Harbord’s joint

coverage of ‘planning gain, increased rate

retention and associated valuation problems’.

The latter followed on from Michael MacBrien’s paper on ‘EU legislative advances

on energy conservation and sustainability

and their impact on valuation’, which was

very well received, and while it was reported

same level of income needed to provide

the local services on which businesses and

communities rely. It includes questions on the

effectiveness of current reliefs, the valuation

appeals system, transparency and openness,

and tax avoidance.

The Board continues its involvement in the

Valuation Tribunal Users’ Group (VTUG)

on the Institute’s behalf. It would not be

appropriate for me to comment in depth on

the recent issues discussed within VTUG,

when the minutes of the meetings are not yet

in the public domain. It is, however, fair to say

that the bringing together of VTS, VTE, VOA,

the Bar, local government, small business and

the professional bodies to discuss (sometimes

quite complex) current issues in a candid

manner is, I feel, going to be of significant

longer term benefit to VT users at large, and I

wish continued power to VTUG’s elbow in the

coming year.

The Institute also continues to contribute,

along with the Rating Surveyors Association

and the RICS, to the VOA’s Professional Bodies Liaison Group. I look forward to

hearing the outcome of discussions arising

from the next meeting of that group, given the

recent announcement to postpone the 2015

rating revaluation.

At its last meeting, the Board noted with

pleasure the continuing success of viva

admissions to the Institute at Diploma level,

both from the UK and the Commonwealth, and

the increasing awareness of the importance of

Recognised European Valuer accreditation,

which may be applied for through the Institute.

Finally, the past year has seen the Board

continuing its work in the development of the

valuer qualifications in conjunction with the

Royal Agricultural College, which is now to

become a university in its own right. We are

now approaching the end of what has been a

long and a major, but satisfying, undertaking,

and an essential one which will help the

Institute in its aim to broaden its valuation

scope and to attract more valuers into

membership. We often say that we are a broad

church in the Institute – by our actions we are

showing that we are just that.

“ We commended the Welsh Government’s stated intention to “bring together partners representing charities, business and other partners to examine the evidence and suggest some next steps’.”

Valuation Faculty Board Chairman Peter Scrafton combines reflections on the Telford Annual Conference with the Board’s important contributions to valuation and rating reforms

Peter Scrafton FIRRV FCIArb MRSA (Hon)

Solicitor (Non-Practising) and Accredited

Mediator is a legal and valuation consultant

and member of the IRRV Council. Contact him

on Valuation Faculty Board matters via

The Institute is a broad church

INSI

GH

T JA

NU

AR

Y/FE

BRU

AR

Y 2

013

15

Deborah Davies IRRV (Hons) is Customer

and Benefit Services Manager with Craven

District Council. Contact her on

Case law update

people. The property was rented for a fixed

three years term, but at the end of the period,

Camden did not give up possession, as there

was still an occupier. When the occupier did

move out, the property remained vacant,

but Camden continued to pay rent, thereby

creating a periodic tenancy. Some months

later there was a dispute about the state of

the property, and at that point the council

stopped paying the rent, and attempted to

surrender their interest by mailing the keys to

the landlord.

Meanwhile, over in council tax, it was

determined that the landlord was liable for

council tax for the time during which the

periodic tenancy subsisted. The landlord

contested liability before the Valuation Tribunal (VT), and they accepted the

appellant’s submission that a periodic tenancy

had arisen when the council continued to

pay rent after the expiry of the original lease

agreement. However, the VT also determined

that the periodic tenancy did not constitute a

material interest under the above definition,

as it was a leasehold interest for less than six

months. Therefore Ms MacAttram was held to

be liable for council tax. She then appealed to

the High Court.Ms MacAttram argued that the original

tenancy had been granted for three years,

and that the periodic tenancy was a tenancy

which arose out of the fixed term, and should

therefore be annexed to the main tenancy,

making a total tenancy period of over five

years. This would mean that Camden would

have remained liable for council tax. However,

the High Court found that the fixed term

and periodic tenancies could not be joined

together this way, as it undermined the

wording of the LGFA 1992. The court held that

the conduct of the parties involved indicated

that the tenancy was not a continuation of the original tenancy, but actually the grant

of a new monthly periodic tenancy, and

so, at the creation of the periodic tenancy, the

The hierarchy of liability

As many local authorities prepare to reduce,

or even abolish completely, entitlement to

an exemption under what we will soon think

of as ‘the former Class C ’, I am reminded

of a case, MacAttram v LB Camden, going

back to the first half of 2012, where the issue

was the correct interpretation of s6 (2) Local Government Finance Act (LGFA) 1992, the

hierarchy of liability.

In simple terms, to determine liability,

we work down the prescribed list and bill

the first person(s) that appear to meet

the description. Therefore, residents with

a leasehold interest appear near the top,

and at the bottom we get to the ‘owner ’

as the liable party. The ‘owner’ is defined

in s6(5) as a person having a material interest in the premises. A material interest

is a freehold interest, or a leasehold interest

granted for a term of six months or more.

The MacAttram case would have particular

relevance in circumstances where a landlord,

perhaps mindful of being charged council

tax otherwise, allows a periodic tenancy to

arise on an unoccupied property.

The landlord, Ms MacAttram, had rented

a property to the London Borough of Camden. They had used it to house homeless

obligation to pay council tax reverted to the

landlord, as the council would not have had a

material interest.

The High Court went on to find against

the idea of the liability switching back and

forth depending on the length of the periodic

tenancy, but did agree that if the periods had

been six monthly, then a different decision

might have been made.

The appellant, Ms MacAttram, had also

argued that the posting of the keys did not constitute a surrender, but the High Court

found that the surrender was effective,

because the landlord had accepted it by

her conduct.

Thus the High Court upheld the decision

of the Valuation Tribunal, and the appeal

was dismissed.

Deborah Davies is on hand to showcase a key decision focusing on landlord and tenant issues and their effect on council tax liability

“ However, the VT also determined that the periodic tenancy did not constitute a material interest under the above definition, as it was a leasehold interest for less than six months.”

Jobs Online is a web based job vacancy service offering organisations a platform from which to advertise their jobs throughout the UK to professionals in the fields of revenues, benefits and valuation. The site offers search facilities by location, salary level or area of interest for people looking for a job.

Your subscription to jobs online includes the following:

• Publication of an unlimited number of job advertisements on the web throughout your subscription period

• Unrivalled exposure to IRRV qualified local authority contacts in all areas of revenues, benefits and valuation

• Manageable and easy-to-use password protected web account

• Link to your authority website

• Search facilities by location, salary level and area of interest

You can subscribe to Jobs online under the following price tiers:

Annual subscription . . . . . . . £1000

6 months . . . . . . . . . . . . . . . . . £600

3 months . . . . . . . . . . . . . . . . . £400

Have just one job to advertise? Rather than take out a subscription you can simply register online and pay just £200 per job.

To subscribe to the service please go to http:/www .irrv .org .uk/jobs

Jobs Online

If you require further information please contact membership@irrv .org .uk or phone 020 7691 8996

new horizons new opportunities

Miscellaneous Income Recovery through the County Court, London, 7 FebruaryThe aims of the course are:• To provide you with a detailed insight into collection and

enforcement of sundry related debts.• To help you understand the legal requirements and adopt

best practice for different debt streams.• To give you pointers geared to service improvements and

increasing collections.• To help you understand the legal process of enforcing

a County Court Judgment.• To help you understand the importance, and use of, the

telephone in debt collection.• To equip you with key skills in assertiveness, negotiation

and listening.• To help you deal with callers in a professional, efficient

manner.

We also offer bespoke in-house training on the topics of your choosing. Great rates guaranteed.

Please check www.irrv.net/trainingdays regularly as courses are added continually.

Insolvency and the Revenues Collection Process, London, 13 FebruaryIn a time where formal insolvencies are at a historically high level and where such insolvencies impact disproportionately upon the collection activities of local authorities it has never been more important that revenues professionals understand the insolvency regime and its workings. There has been an increasing prevalence of schemes and behaviours in the operation of insolvency procedures that have led to avoidance of liability for NNDR and CT and this course examines, as one of its modules, both this problem and the potential to resolve it. The course is designed in order that delegates will be better armed to protect their authority’s position and promote the maximisation of returns in insolvency proceedings.

• Insolvency and the formal regimes in England and Wales.• Enforcement Rights and Obligations in Insolvency.• Anti-Avoidance Strategies for Recovery Professionals.• The Appropriate Use of Insolvency as an Enforcement

Remedy.

IRRV Training

Please send your queries to [email protected] or telephone 020 7691 8987

INSI

GH

T JA

NU

AR

Y/FE

BRU

AR

Y 2

013

17

Maureen Neave IRRV (Tech) MBA is Benefit

Manager with Vale of Glamorgan Council,

and an IRRV Council member

Benefits bulletin

more households stand to lose out under its flagship welfare scheme than previously thought. In a revised impact assessment report recently published, the DWP have stated that under Universal Credit (UC), roughly 2.8 million households will get less in benefits than first thought, compared to 2 million in October 2011.

The majority of losers will be full time and part time workers, and lone parents will also be affected. They will all receive lower entitlements under UC than they would under the current system, and they will principally be those who currently receive a large amount of support through working tax credits. Also, working families on low income lose out on other benefits, such as free school meals, because they are in work. Obviously the decision to increase benefits below the rate of inflation will impact on UC. Therefore, we will see the income of the poorest fall yet again, when they are already struggling to make ends meet. There are now more adults in poverty from working households than from homes where no-one works. This goes against what the government keep reminding us all of – that a lack of work is the key to Britain’s poverty problems, and that benefit reforms are designed to ensure those in employment will not be worse off than those out of work. Liam Byrne, the Shadow Works and Pensions Secretary, told the Independent that “the report lays bare the scale of working poverty”, and added, “Britain’s ‘strivers’ are getting ‘screwed’”.

Following on from my last article, it was confirmed by Lord Freud at the IRRV Annual Conference in October that UC will go ahead next year, with the pilots kicking off in April 2013, and national roll out in October 2013. However, he did

Things are looking bleak at the moment...

As I write this article things are looking quite bleak in Wales, and I don’t mean the weather! The Welsh Government, at their last full meeting of the year, failed to temporarily set aside rules so that the new regulations for the council tax reduction scheme for all of Wales could be rushed through. Opposition Assembly Members criticised ministers for tabling more than 300 pages of regulations late, just minutes before they were due to be debated, not giving them enough time to read the documents. They also accused the Welsh Labour government of treating the Assembly and the public with ‘contempt’, and ‘being negligent in their duty’. Another meeting has been scheduled for the Christmas recess, so hopefully they will come to an agreement.

In the autumn statement, the Chancellor unveiled changes that will cut a further £3.8 billion from the benefit bill. This will be done by limiting the annual benefit increases to one per cent for each of the next three years, rather than increasing them in line with inflation, which will include tax credits as well as social security benefits. A number of critics have said this is a move that will lead to benefits being eroded over time, as they fall behind the cost of living. It has been reported that the government has admitted that 800,000

state this would be for new JSA claims for single people, as the government would be taking the soft approach. After he finished speaking, I clarified this with him, and he stated it would be for single people that had no housing element included at the start, as the government was not going to rush into doing everything at once. I also confirmed that this was correct with the DWP, and they said that the housing element will not be included to start with, but once someone was receiving UC they would continue to receive it, irrespective that at a later date the housing element was claimed. In other words, ‘the lobster pot effect’ – once they are caught, they will not get away!

Further on the UC front, Whitehall sources have claimed that two civil servants working on the UC project have been replaced, and a third, the most senior civil servant overseeing the project, is on sick leave. We have been informed that Julia Sweeney has moved on to another role in DWP, and Bill Hern is taking over her role as the Head of Housing Delivery. I leave you to contemplate all this!

As the welfare reforms bite, I thought I would add a bit of trivia to end on a lighter note. For those of you that didn’t attend the IRRV Annual Conference, Lord Freud comes from my neck of the woods – Wales. Please don’t hold this against the Welsh, but I would add that he moved to England when he was six years old, so I think there should be a bit of give and take on this one!

...says Maureen Neave, and it’s not just the weather!

“ It has been reported that the government has admitted that 800,000 more households stand to lose out under its flagship welfare scheme than previously thought.”

18

INSI

GH

T w

ww

.irrv

.net

Cover story

we do a complete review. We knew it should

be done, so what did we do? I did consider

hiding under my desk and hoping it would

go away, but that didn’t work, so we needed

another plan to review 20,000 plus SPDs.

With this in mind, a short walk around the

IRRV Annual Conference exhibition

brought me in touch with a company who

said they could help me with my problem

and willing to discuss possible solutions. A

discussion with my Chief Officer and other

revenues and benefits service heads at the

North and Mid Wales Revenues Practitioners

Group concluded that this was possible, with

benefits for all authorities.

Why we did itWith eight authorities now involved, there

were over 135,000 SPDs to be reviewed, and

sending out that number of reviews would be

a massive task, never mind the phone calls,

letters and other enquiries we would get from

such an exercise. As mentioned before there

had been staff cuts, or should I say posts that

had not been filled when someone left. We

needed help!

What were the processes?Our first task was to get some intelligence on

what and who was out there to help with such

a big project. Discussions took place with a

number of market players in the field, so that

we could understand what was available in the

market place.

What were the problems?The problems were as mentioned before lack

of staff, lack of available resources, and lack

Wales’s ‘magnificent eight’!

Three years ago, after a period of years of new

systems, system changes (including changes

from the revenues and benefits Fujitsu

system to Pericles and then to Northgate),

the introduction of a document management

system, e-benefits and various other changes,

time has been limited, with staff being

taken from their normal day job to work on

these projects. Inevitably, with years of cuts

and savings, some work is curtailed or not

completed at all. The review of single person discounts (SPDs) was one of these victims,

where only parts were reviewed each year –

what was needed was a complete review.

This was an excellent idea – let’s review all

the SPDs we hold on our system. But with the

savings that all councils had to make at that

time, and staff not being replaced when they

left, the resources were not there to complete

the process.

So we were left stuck in the middle, with

internal and external auditors requesting that

of time, albeit with an audit requirement to

review all our SPDs.

What were the benefits?• evidence from previous reviews completed

by these companies appeared to show

that there was something like 2% to 4% in

savings to be made

• our staff could get on with the normal ‘day

job’ of collecting council tax

• the cost of the review was paid for out of

the savings

• an initial view of doing the review in-house

was that it would cost us as much as

collaborating with a specialist company

• working in collaboration as a group meant

that we had one tender, which we all had

input into drawing up. However, I must

thank a couple of the midland authorities

who put their SPD tender document on

the internet – this was a very helpful

starting point

• we had one procurement for the contract,

which was done electronically through Buy

for Wales

• one council produced the contract

• one council did all the translation for the

letters and documents into Welsh.

• we had a dedicated person in the Northgate

contact centre who could speak Welsh to

those citizens who wanted help in their

own language

• all the calls and letters that were received as

a result of the canvas were handled by the

Northgate centre

• we had one point of contact in Northgate to

obtain statistics and deal with any queries.

In an Insight revenues special, Wales’s ‘magnificent eight’ share £1million savings in their groundbreaking single person discount review. In the second part, ‘Jaws – the reunion!’, Andrew Burton sees a few parallels emerging between council tax support, poll tax, and a classic from the seventies!

Phil Round explains the background to the £1million savings in their groundbreaking single person discount review

19

Who did we work with?The winning contract was awarded to

Northgate Information Solutions, who

worked with Experian on comparing our SPD

data with all their records.

What did we do?There was a considerable amount of work

involved in agreeing the tender document and

selecting the winning bidder. After that stage,

we were left with extracting the data from our

system and loading it on in a secure site. We

were then tasked with removing the discount

from our system for all those households

which admitted they were no longer entitled

to a SPD.

The process also included checking all cases

where there had been no response to the

canvas, or where reminders had been issued.

This was probably the most difficult task, as it

meant checking about 400 cases per authority,

trying to find why there was no response.

After checking the ‘non-responders’, about

25% were removed, on top of those that had

admitted that they were no longer entitled.

What was surprising was the very limited

number of people who appealed against the

decision to remove their SPD, and no-one