Inside the Multinationals 25th Anniversary Edition978-0-230-62516-7/1.pdf · 10 9 S 7 6 5 4 3 2 1...

30

Inside the Multinationals 25th Anniversary Edition

Transcript of Inside the Multinationals 25th Anniversary Edition978-0-230-62516-7/1.pdf · 10 9 S 7 6 5 4 3 2 1...

Inside the Multinationals 25th Anniversary Edition

ALso by ALan M. Rugman

International Diversification and the Multinational Enterprise Multinationals in Canada New Theories of the Multinational Enterprise (editor)

Multinationals and Technology Transfer (editor)

Multinationals and Transfer Pricing (co-editor)

International Business: Firm and Environment (co-author)

Megafirms Administered Protection in America (editor)

Multinationals and Canadian US Free Trade Global Corporate Strategy and Trade Policy (co-author)

Foreign Investment and NAFTA (editor)

The Theory of Multinational Enterprises Multinational Enterprises and Trade Policy International Business: A Strategic Management Approach (co-author)

Environmental Regulations and Corporate Strategy (co-author)

Multinationals as Flagship Firms (co-author)

The End of Globalization The Oxford Handbook of International Business (co-editor)

The Regional Multinationals Analysis of the Strategic Management of Multinationals (co-author)

Inside the Multinationals 25th Anniversary Edition

The economics of internaL markets

Alan M. Rugman

* © Alan M. Rugman 2006 Softcover reprint of the hardcover 1st edition 2006 978-1-4039-9591-9

All rights reserved. No reproduction, copy or transmission of this publication may be made without written permission.

No paragraph of this publication may be reproduced, copied or transmitted save with written permission or in accordance with the provisions of the Copyright, Designs and Patents Act 1988, or under the terms of any licence permitting limited copying issued by the Copyright Licensing Agency, 90 Tottenham Court Road, London wn 4LP.

Any person who does any unauthorized act in relation to this publication may be liable to criminal prosecution and civil claims for damages.

The author has asserted his right to be identified as the author of this work in accordance with the Copyright, Designs and Patents Act 1988.

First published in 1981 by Croom Helm and Columbia University Press.

25th anniversary edition published 2006 by PALGRAVE MACMILLAN Houndmills, Basingstoke, Hampshire RG21 6XS and 175 Fifth Avenue, New York, N.Y. 10010 Companies and representatives throughout the world.

PALGRAVE MACMILLAN is the global academic imprint of the Palgrave Macmillan division of St. Martin's Press, LLC and of Palgrave Macmillan Ltd. Macmillan® is a registered trademark in the United States, United Kingdom and other countries. Palgrave is a registered trademark in the European Union and other countries.

ISBN 978-1-349-54488-2 ISBN 978-0-230-62516-7 (eBook) DOI 10.1057/9780230625167

This book is printed on paper suitable for recycling and made from fully managed and sustained forest sources.

A catalogue record for this book is available from the British Library.

Library of Congress Cataloging-in-Publication Data

Rugman,Alan M. Inside the multinationals 25th anniversary edition: the economics of

internal markets / Alan M. Rugman - 25th anniversary ed. p.cm.

Includes bibliographical references and index.

1. International business enterprises. I. Title: Inside the multinationals twenty-fifth anniversary edition. II. Title: Inside the multinationals. IIl.ntle.

HD2755.5.R82 2006 338.S'8--dc22

10 9 S 7 6 5 4 3 2 1 15 14 13 12 11 1009 OS 0706

Transferred To Digital Printing 2011

2006043207

To my parents

Contents

List of Tables and Figures viii

Preface ix

Acknowledgements xii

Foreword Mark Casson xiii

Introduction to the 25th Anniversary Edition xx

Appendix 1: Inside the Multinationals: The Economics of Internal Markets - A Statistical Analysis of the Rugman (1981) Citation Record Elitsa Banalieva xxiii

Appendix 2: List of Reviews for Inside the Multinationals: The Economics of Internal Markets xxvii

Selected Quotes from Reviews xxviii

1 Multinationals and the New Theory of Internalization 1

2 Internalization as a General Theory of Foreign Direct Investment 18

3 The Choice Between Trade, Foreign Direct Investment and Licensing 34

4 Implications of the Theory of Internalization for Corporate International Finance 56

5 Multinational Banking and the Theory of Internalization 71

6 Internalization and the Transfer of Technology 87

7 The Regulation of Multinational Corporations

8 Conclusions: The Future of Internalization

Bibliography

Index

vii

119

142

151

159

List of Tables and Figures

Tables

A1.1 Citation record of Rugman (1981) by document type xxiv A1.2 Citation record of Rugman (1981) by subject category xxiv A1.3 Citation record of Rugman (1981) by year xxv

5.1 The Degree of Multinationality in Canadian Banking 78 5.2 Canadian Banks' Rates of Return on Equity,

Per Cent, 1962-79 81 5.3 Earnings of Leading Canadian Banks Mean and Standard

Deviation of Profits, 1967-79 82 5.4 Leading Canadian Chartered Banks, Rate of Return

on Average Assets, Per Cent 84 5.5 Differentials between Chartered Bank Rates of Return on

Domestic and Foreign Currency Assets 85 5.6 Domestic and International Business: Five Largest

Canadian Banks, 1970-5 85 6.1 Canadian Business Payments to Non-residents for

Technology Transfers, 1970-7 98 6.2 Summary of the Determinants of Rand D 102 6.3 Expenditures on Rand D by Twelve Multinational

Firms in Canada, 1977 113 6.4 Expenditures on Rand D by the Subsidiaries of Twelve

Multinational Firms in Canada, 1977 114 6.5 Expenditures on Rand D by Twelve Canadian Owned

Corporations, 1977 115 7.1 Performance of the Largest US Multinationals, 1970--9 126 7.2 Performance of the Largest Non-US Multinationals,

1970--9 129

Figures

0.1 Transaction Costs of Internal and External Markets xviii 3.1 The Choice of Entry Mode 45 3.2 The Sequencing of Entry Mode over Time 48

viii

Preface

Conceived at Columbia University, New York, developed and expanded in Montreal, Quebec and finally brought to fruition in Halifax, Nova Scotia, this book reflects the varied nature of its subject matter - the multinational enterprise. Yet it belongs to none of these places. Rather the genesis of the central idea in this book is the University of Reading in England, where I first developed an interest in the concept of internalization. There the work of John Dunning and Mark Casson and the frequent visitors to the international business side of the economics department has developed an oral tradition of analysis of the multinational enterprise (MNE). In this oral tradition, the internalization of markets as a theoretical rationale for the MNE was becoming a central concept by the academic year 1976 to 1977, which I spent there as a Visiting Research Fellow. The Reading oral tradition has been supplemented by the influential series of Reading 'greenbacks', edited by Professor Dunning, where the elements of internalization are sketched out in issues over the last several years. I am grateful to him for very helpful suggestions and to Mark Casson for many stimulating conversations and for consenting to write the Foreword.

When teaching international business at Columbia University from 1978 to 1979 it became clear to me that internalization is a unifying paradigm for the theory of foreign direct investment (FDI). In reviewing the literature on the determinants of FDI I found that each scholar is writing about one or another market imperfection, which induces the MNE to use an internal market. This analysis is the cornerstone of this book. Yet there are situations in which internalization is not the most efficient response to a market imperfection. In one of the chapters here Ian Giddy and I consider alternatives to internalization, such as exporting and licensing. We explore the conditions under which each one of these modes of servicing a foreign market is optimal at certain points of time, and how the choice of modality may vary over time. The materials in Chapter 3 were developed jointly with Ian Giddy, although the use of them here is my responsibility.

ix

x Preface

While in the finance department of Concordia University, Montreal, I wrote the chapters which apply internalization to financial aspects of MNEs and to multinational banking. The applications of internalization to Canadian policy issues, namely the transfer of technology between the US and Canada and the issue of regulation of the MNE, were commenced during the period spent in Quebec but completed at Dalhousie. Preparation of the final draft of this book was facilitated by the Centre for International Business Studies at Dalhousie University.

Turning to other specific intellectual debts, I have received helpful comments on Chapter 2 by Winston Brown, Mark Casson, John Dunning, Ian Giddy, Stefan Robock and Raymond Vernon. A previous version of this chapter was presented at the Eastern Economic Association meeting in Boston, May 1979.

For the first half of Chapter 3, on modes of entry to a foreign market, written jointly with Ian Giddy, useful comments were received from Mark Casson, Bernie Wolf, Hugh Neuberger, Larry Kryznowski, Sylvester Damus, Sandra Dow, Evan Douglas, Robert Grosse, Rebecca Klemm and members of seminars at Columbia, Miami and Dallas. Part of the chapter was presented at the annual meetings of the North American Economic Studies Association at Atlanta in December 1979 and the rest revised in late 1980.

The work on implications of internalization for international finance in Chapter 4 was improved by helpful comments from Solomaz Ayarslan, Gary Craig, Ian Giddy, Gunter Dufey and Kenneth Riener. A previous version of this chapter was presented at the annual meetings of the Financial Management Association in Boston in October 1979.

Chapter S benefited from comments by Ian Giddy, James Dean, Jack Galbraith and James Desreumaux. Research assistance was provided by Penny Ellison, who prepared the tables used here for her MBA research paper at Concordia University, 1979-80.

Work on Chapter 6 dealing with the transfer of technology to Canada was supported by a grant from the Tenth Associates' Workshop in Business Research of the University of Western Ontario. Under this fellowship I am pleased to acknowledge the help of Terry Deutscher and the research assistance of Roland Ghanem. Helpful comments on this technology transfer chapter have been provided by Judith Alexander, Evan Douglas, Gary Hewitt, Danny Shapiro,

Preface xi

Harold Crookell, Peter Killing, Don Lecraw and others at Western Ontario and by members of seminars at Dalhousie and Western. Other versions of this chapter were presented at the annual meetings of the North American Economic Studies Association in Denver, Colorado in September 1980, and at the European International Business Association Annual Conference in Antwerp, December 1980.

A previous version of Chapter 7 was presented to a Conference on the Transnational Corporation hosted by the University of Sudbury, October 1980. In this chapter research assistance has been provided by Mara Crassweller, one of the Student Fellowship holders of the Centre for International Business Studies of Dalhousie University.

The manuscript was helped along at Concordia University by Susan Regan, Susan Altimas and Lorraine Vineberg. It was prepared and typed in its final form by Pat Zwicker, Centre for International Business Studies at Dalhousie University.

Helen Rugman did most of the proofreading of the numerous drafts of the manuscript and helped prepare the bibliography and index.

I am grateful to all these people for their help and advice in the completion of this project. Their comments and interest in my work have been of great value in making my thinking and writing more precise. The remaining errors in this book are my responsibility alone.

ALAN M. RUGMAN

Centre for International Business Studies Dalhousie University

Acknowledgements

For granting permission to reproduce his materials published elsewhere the author thanks the following journals:

Chapter 2: 'Internalization as a General Theory of Foreign Direct Investment: A Re-Appraisal of the Literature,' Weltwirtschaftliches Archiv (Review of World Economics) vol. 116, no. 2 (Tubingen: J.C.B. Mohr, June 1980): 365-79.

Chapter 4: 'Implications of Internalization for Corporate International Finance,' California Management Review vol. 23, no. 2 (Winter 1980): 73-9. Reprinted by permiSSion of the Regents of the University of California.

Chapter 7: Book review of Tamir Agmon and Charles P. Kindleberger, eds. Multinationals from Small Countries. Cambridge, Mass.: MIT Press, 1977. From Economic Development and Cultural Change vol. 28, no. 4 Guly 1980): 871-5.

xii

Foreword

There is now a vast literature on the multinational enterprise (MNE) and the related subject of foreign direct investment. Much of the literature consists of case studies of particular firms operating in particular host economies. To interpret the results of these case studies correctly it is necessary to have a satisfactory theory of the MNE, and until recently such a theory was lacking. Alan Rugman has played a major role in the development of this theory, and it is a pleasure to see his work made available to a wider audience through this book.

There are three major problems facing anyone who attempts to theorize about the MNE. The first is that the subject is interdisciplinary. Understanding of the MNE requires a grasp not only of economic theory, but of the theory of finance as well. Within economics, it is necessary to draw upon both the theory of international trade and the theory of industrial organization. Alan Rugman has a detailed knowledge of all these areas, and this has enabled him to provide a balanced perspective on the MNE.

Secondly, the complexities of the MNE mean that the theorist must tread a careful path between overSimplification on the one hand, and a preoccupation with minor detail on the other. A major pitfall when theorizing is to try to take account of too many different phenomena at once. This mistake is very common in international economics, and particularly so in studies of the MNE. Some theorists are overambitious, and range too widely to do full justice to anyone aspect of their subject. Their work frequently degenerates into mere taxonomy. They list all the factors which could conceivably influence the MNE, demonstrate the multifarious ways in which these factors interact, and conclude by listing all possible outcomes which could result from these interactions.

There is no doubt that taxonomy is valuable as a preliminary to theorizing. It provides an analytical framework which ensures that the concepts and definitions are mutually consistent. But it is not a substitute for theorizing itself. Taxonomies can only explain the real world in a very limited way, either by pigeon-holing observed

xiii

xiv Foreword

phenomena within the categories defined by the taxonomy, or by telling anecdotes illustrative of the possibilities they raise.

Ultimately, the weakness of taxonomy is that everything is possible; the taxonomy provides labels for real world events, but gives no predictions of them. Predictions are obtained by imposing restrictions on the taxonomy - by postulating that certain cases identified by the taxonomy will never be observed.

Alan Rugman is a theorist, not a taxonomist. He draws his inspiration from the theory of efficient markets. The predictions of this theory stem from the postulate that no two individuals will forego a mutually beneficial opportunity for trade. Trade proceeds up to the point where no one can be made better off without someone else being made worse off; in the jargon of the economist, the allocation of resources is Pareto efficient. This insight into economic behaviour has proved very successful in many fields of inquiry, and the theory of the MNE is no exception.

This brings us to the third problem facing the student of the MNE. Orthodox economic theory has been developed on the assumption that there are no transaction costs. But as recent work has shown, transaction costs are fundamental to the theory of the MNE - indeed to the theory of the firm itself. In a world of no transaction costs the rationale for the firm is unclear. To explain the existence of the MNE it is necessary to introduce transaction costs into conventional economic theory. In this respect students of the MNE have become theoretical innovators.

However, conventional theory affords a number of important insights into economic behaviour, and it is important not to lose sight of these in the course of modifying the theory. One of the great strengths of Alan Rugman's work is that in expounding the theory of the MNE he keeps these insights to the fore, and builds the theory around them. This gives his exposition a coherence which is lacking in many other works on the MNE.

As noted above, it is the introduction of transaction costs that links conventional theory to the theory of the MNE. The important point is that transaction costs vary according to the kind of market institution used. The relative costs of alternative institutional arrangements influence the choice of market institution. Competition tends to lead to the selection of the most efficient market institution. Where international technology transfer, and international trade in

Foreword xv

intermediate products are concerned, the most efficient institution is often the MNE.

The introduction of transaction costs into economic theory is sometimes seen as complicating matters and removing most of the theory's predictive power. Nothing could be further from the truth. Certainly, the introduction of transaction costs removes some of the more absurd counterfactual predictions of the theory. But at the same time it generates a wealth of new predictions which explain phenomena - such as the MNE - about which the orthodox theory has nothing interesting to say.

The proposition that individuals will seek out mutually beneficial trading opportunities still applies when there are transaction costs. But now trade takes place only up to the margin where the gain from additional trade is just equal to the additional transaction cost involved. In the long run it does not matter who actually incurs the transaction cost - the buyer or the seller - for this will be reflected in the negotiated price: ultimately the incidence of the transaction costs on the two parties will be determined solely by the competitive conditions that prevail. (However, this result no longer applies if there are externalities, so that some of the transaction costs are borne by those who are not party to the transaction.)

A second postulate can now be introduced: namely that transactors have a mutual interest in reducing transaction costs, and so will collaborate in seeking out least-cost methods of transaction. The firm is an institution for minimizing transaction costs. The reason why managers control the allocation of resources within the firm is that it is too expensive to negotiate separately over every single activity that needs to be performed. This accounts for a number of aspects of corporate behaviour which are so familiar that they are usually just taken for granted.

It explains why employment contracts give management discretion over the deployment of workers between various tasks, instead of specifying the precise tasks that each worker must perform under each set of possible circumstances. The use of a single contract of employment in place of multifarious contracts for specific tasks reduces the number of transactions involved in the employment of labour, and so economizes on transaction costs in the labour market.

The same principle explains why firms own physical assets rather than hire them, or buy specific asset-services from independent assetowners. It is cheaper to own rather than to hire because ownership of

xvi Foreword

the asset secures a continuous stream of future asset-services with a single transaction - the purchase of the asset - while if the same stream of services were hired, the contract of hire would periodically have to be renegotiated and renewed - involving several separate transactions. It is cheaper to hire rather than to purchase specific assetservices because the hirer obtains a range of possible uses of the asset without having to negotiate separately over each of these uses.

The minimization of transaction costs also implies that complementary assets, when utilized together, should have a common owner, so that their use can be co-ordinated not by negotiation but by control. Sometimes complementarity is fully exploited only when the assets are physically adjacent to each other - this is the case of plant economies in production. In other cases complementarity can be exploited at a distance. This is exemplified by the geographical division of labour in production: different assets are at different locations, and are connected by flows of intermediate products, e.g. flows of components, semiprocessed materials, even proprietary know-how. Complementarity at a distance is associated with multiplant economies. Multiplant operations that span national boundaries generate MNEs.

The rationale for the MNE is that it reduces transaction costs by buying up complementary assets located in different nations and integrating their operations within a single unit of control. In doing so it creates an 'internal market' for the intermediate products. The concept of an internal market is particularly apt if administration within the firm is decentralized, with powers of control being delegated to the managers of individual plants. In this case control over the intermediate product actually changes hands as the product moves between plants, though ownership of the product does not.

But it is change of ownership, rather than change of control, which is mainly responsible for transaction costs. Change of ownership creates an incentive for both parties to haggle over the price, for where change of ownership is involved it is price which determines the distribution of the gains from trade. Change of ownership also creates an incentive to default, for each party gains most if the other party fulfils his obligations, but they themselves do not. Neither of these incentives occurs in an internal market; it is for this reason that in many instances an internal market is a more efficient institution for allocating resources than is an external one.

The predictive power of the internalization theory may be illustrated in the following way. Assume that each market has a set-up

Foreword xvii

cost, incurred in bringing buyers and sellers together, or otherwise establishing channels of communication between them. There is also a variable cost associated with negotiating and enforcing each transaction. This variable cost is independent of the value of the transaction. However, there is a maximum quantity that can be transacted at anyone time, for example, all transactions. may have to be effected spot, and there may be a maximum bulk sale that the physical storage and distribution system can accommodate. Suppose that this maximum quantity is fairly small, so that variations in the quantity traded in the market have to be accommodated by variations in the number of transactions. It follows that the total variable cost is directly proportional to the quantity traded.

Consider an intermediate product market linking two stages of a vertical production process, and suppose that there is just one plant producing at each stage of the process. Assuming no barriers to either take-over, merger or divestment, equilibrium in the equity market requires that the joint profits of the two plants are maximized. Given the cost function of the selling plant and the cost and revenue functions of the buying plant, the contribution of intermediate product trade to the joint profits of the two plants can be derived; it is illustrated by the curve AA 1 in Figure 0.1, which peaks at B. In the absence of transaction costs B determines the equilibrium volume of trade qo.

Suppose now that the establishment of an internal market incurs greater set-up costs than the establishment of an external market. The cost of the internal market may be identified with the cost of taking over both plants and establishing an integrated system of control. By comparison, the set-up cost of the external market is negligible. However, the internal market has much lower variable costs than the external market because there is less incentive to haggle and default. The transaction costs of the internal market are illustrated by the locus CC I while the costs of the external market are illustrated by the locus DDl; it can be seen that CCI has a larger intercept and a lower slope than DDI.

The lines CCI and DDI intersect at E. To the left of E the external market has the lowest transaction costs, and so the minimum transaction cost is indicated by the segment DE. To the right of E the internal market has the lowest transaction cost, and so the minimum transaction cost is indicated by the segment ECI. Thus overall, the minimum transaction cost is indicated by the locus DEO, which has a kink at E, corresponding to the volume of trade ql. At quantities below ql the plants will be separately owned, and will trade at arm's

xviii Foreword

length, while above ql the plants will be integrated and trade will be internalized.

Whether the market is actually internal or external depends upon the volume of trade, and this in turn depends upon the way both the gains from trade and minimum transaction cost vary with the quantity traded. Profits, measured by the gains from trade net of transaction costs, are represented by the vertical discrepancy between AN and DEC. They are measured in the figure FF1, which peaks at G, giving a profit-maximizing output qz. Since in this example qz > ql the market is internalized.

One obvious prediction of this theory is that the propensity to internalize is greater the greater is the volume of trade between the two plants. However, it should be emphasized that this result depends upon a large volume of trade being associated with a high frequency of transactions in the external market. If the frequency of transactions could be reduced, either by long-term contracts, or by purchasing more occasionally in greater bulk, then the incentive to internalize would diminish. Thus the theory predicts that not only

Value

c

o o

A F

Quantity Needed

Figure 0.1 Transaction Costs of Internal and External Markets

Foreword xix

the volume of trade, but also the scope for long-term contracts and for bulk-buying, will influence the degree of internalization.

At present it is possible to test these predictions only in terms of anecdotal evidence, but the results are nevertheless quite encouraging. For example, when applied to the market for technical knowhow, the theory predicts that firms with large-scale Rand D producing a continuous stream of innovations are more likely to internalize them than is a firm with a smaller Rand D effort, whose innovations are essentially 'one-off'. Thus foreign direct investment is most likely to be associated with large-scale Rand D activity, and licensing with small-scale Rand D activity.

Similarly, firms selling high-quality branded products are likely to purchase regularly from a small number of high-quality component or raw material producers, while firms selling unbranded products are more likely to shop around the world markets for the cheapest supplies, since they have less goodwill to lose if the quality they sell is poor. Because of their frequent purchases from the same suppliers the brand operators have a greater incentive to internalize through backward integration. The theory therefore predicts that foreign direct investment in component production or raw material extraction will be more common among suppliers of branded products than among suppliers of unbranded products.

In both these examples there are, of course, other factors at work besides the ones stated by the theory. The point to be emphasized is that a general theory of transaction costs does exist, and that this theory is very rich in predictions about the role of internal and external markets in a competitive economy. The theory of the MNE, as developed by Alan Rugman and others, testifies to its considerable potential in just one area of economics. At present, this is the bestdeveloped area of the theory. It is to be hoped that these insights will soon be applied to other areas of economics. I believe that Alan Rugman's book, by emphasizing the generality of the theory, will expedite this process.

MARK CASSON

University of Reading

Introduction to the 25th Anniversary Edition

I am extremely pleased that Palgrave Macmillan is republishing my 1981 book which explored internalization theory in a North American context. Previously, Peter Buckley and Mark Casson had provided the now classic statement of internalization theory in Chapter 2 of their 1976 book, The Future of the Multinational Enterprise, also published by Palgrave Macmillan. My book was published by Peter Sowden, a young editor at Croom Helm which later merged into Routledge. Peter co-published the book with Bernard Gronert of Columbia University Press, and copies of the book sold out by 1983. Despite a back list of some 60 orders, Peter decided not to reprint the book, and it was put out of print by Croom Helm in 1986 and by Columbia University Press in 1993. At Palgrave Macmillan I would like to thank Stephen Rutt for initiating this project and also Jacky Kippenberger for helping with the searches for the out-of-print documents and for valuable suggestions about this new Introduction.

As the analysis of citations in Appendix 1 (below) reveals, the 1981 book was well reviewed (in over 15 journals), but the theory of internalization was still slow to catch on in the international business academic community. It was only with a renewed set of journal articles on this topic by colleagues, such as J.F. Hennart, Peter Buckley, Mark Casson, Alain Verbeke and others, and our presentations at AIB conferences, that Scholarly interest developed over the mid to late 1980s and into the 1990s. By the time that internalization theory became more widely accepted, a new generation of scholars in the 1990s turned to the resource-based view (RBV) as an alternative approach to the transaction cost economics basis of internalization theory. This was something of a paradox since the focus of internalization theory is on proprietary knowledge as an intermediate product of firms and this predates the RBV interest in learning, knowledge, routines, codification, and related internal managerial issues. But every cloud has a silver lining, so, with Alain Verbeke, I

xx

Introduction xxi

was able to demonstrate in more recent work (e.g. in JIBS 2003) that the RBV and internalization theory are perfectly compatible, and both explain the strategic and economic performance of multinational enterprises. Thus, REV scholars should still find my 1981 book a useful introduction to internalization theory and a bridge to the literature of international business.

In re-reading some of the reviews of my 1981 book I was disappOinted to note that several scholars in Europe criticized the focus of my empirical work on Canada, even suggesting that Canada was an unrepresentative country for tests of internalization theory. Today, we can see how parochial such criticism was as we recognize the power of internalization theory as it has been tested on multinationals worldwide. It continues to provide a powerful analytical device to explain and assess the firm-specific advantages (FSAs), or 'capabilities' in RBV terms, of multinational enterprises, and of smaller firms. Internalization theory also retains strong linkages to public policy and the other country-specific advantages (CSAs) that govern the strategies of multinational enterprises.

For example, chapter 6 provides the insight that a country effect fully explains why the subsidiaries of US multinational enterprises in Canada undertake only half the Rand D of their parents. I set up a control group of Canadian owned firms of the same size as the subsidiaries and found that there was no statistically significant difference in the Rand D to sales ratios of these Canadian based firms -both sets carried out half the Rand D of US firms. The importance of this country effect was probably underemphasized in chapter 6, although I did use it to debunk the then Canadian government's policy of denial of national treatment to foreign subsidiaries unless they obtained a world product mandate and promised to increase the perceived inadequate Rand D in Canada.

In this context, another unfair and basically ex post comment on my 1981 book was the criticism that my assumption that multinationals operated on a hierarchical and centralized basis was naive. Yet this was the empirical reality of the organizational structures of US multinationals in Canada at that time - using data from the 1960s and 1970s. Only subsequent to 1981, and partly due to my early focus on the possibilities of subsidiary specific advantages, has the theory of integration and national responsiveness become relevant in a situation of more decentralized structures, alliances and network

xxii Introduction

relationships - few of which existed in 1981. There now exists a different population of multinationals with more foreign sales, but still with the vast majority within their home region of the triad. Thus we can observe more potential international strategic mixes of integration and responsiveness but at a regional rather than a global level. In my 1981 book I found most US multinationals were ethnocentric, centralized, and home-region based. In my recent book on The Regional Multinationals I find that US multinationals still average 72 per cent of the sales in North America. How much has really changed in the last 2S years? Are firms really more global? While this is the research agenda for the future, it appears to be not all that different from the past.

In general, I still believe that my focus in the book on the efficiency aspects of multinationals was a fresh insight into the analysis of the multinational enterprise in the early 1980s. At that time, public policy was to regulate multinationals on the assumption that they operated in oligopolistic industries, earned excess profits, underperformed on Rand D, and otherwise exploited host economies. I could not find any serious evidence to support these misconceptions in a Canadian context, and so the 'Canadian model' has been a useful pioneer for later work across other countries and regions with similar findings. This is even more relevant today in a world where multilateral trade and investment agreements are failing to progress and where international business is increasingly occurring on an intra-regional basis.

I hope that the republication of this book will serve the now vastly expanded and more theoretically sophisticated community of scholars in the field of international business. I was pleased to start my serious theoretical analysis of the multinational enterprise in my 1981 book, and I hope that its propositions and tests will still provoke and provide a basis for research efforts today and in the future.

ALAN M. RUGMAN

Indiana University January 2006

Appendix 1: Inside the Multinationals: The Economics of Internal Markets - A Statistical Analysis of the Rugman (1981) Citation Record Elitsa Banalieva

One sign of a thought-provoking book, in addition to its reviews, is the number of dtations recorded over time. These reflect the interests of other scholars in the book. A book's dtation record is a method of analyzing the overall impact that the work has had on its respective field and audience. Alan Rugman's (1981) book Inside the Multinationals: The Economics of Internal Markets has provoked many reviews that focus on Rugman's ability to relate internalization theory to international banking, finance, and technology transfer of firm-spedfic advantages (FSAs) in an attempt to show that internalization can be viewed as a general theory of multinational enterprises (MNEs). The purpose of the present note is to analyze the overlooked statisticaJ1 significance of Rugman's dtation record of his 1981 book, as evidence that the book has continued to influence the field of International Business (IS), and other disdplines.

As Table Al.1 shows, Inside the Multinationals has been cited 215 times in the Web of Science. These include citations in 173 articles, which account for approximately 80 percent of its citations by document type. It has also inspired a total of 31 reviews since its inception 25 years ago, or more than one review per year on average. These figures demonstrate a continued interest in Rugman's analysis of internalization theory in a North American context.

Table Al.2 shows that Inside the Multinationals has gained popularity among a wide array of scholarly disciplines; naturally, it has been cited extensively in professional journals spedalizing in business (111 dtations), management (104 dtations), economics (59 dtations), and international relations (23 citations). Interestingly, scholars

xxiii

xxiv Appendix 1

Table A1.l Citation record of Rugman (1981) by document type

Document type Record count Percentage of 215

Article 173 80.5 Book review 16 7.4 Review 15 7.0 Note 6 2.8 Editorial material 5 2.3 Total 215 100.00

Table Al.2 Citation record of Rugman (1981) by subject category

Subject category Record count Percentage of 215

Business 111 51.6 Management 104 48.5 Economics 59 27.4 International Relations 23 10.7 Planning and Development 10 4.7 Environmental Studies 9 4.2 Business, Finance 6 2.8 Public Administration 6 2.8 Geography 5 2.3 Operations Research &

Management Science 4 1.9 Political Science 4 1.9 History of Social Sciences 3 1.4 Law 3 1.4 Engineering, Multidisciplinary 2 0.9 Social Sciences, Mathematical Methods 2 0.9 Sociology 2 0.9 Communication 1 0.5 Computer Science, Information Systems 1 0.5 Engineering, Manufacturing 1 0.5 Health Policy and Services 1 0.5 Industrial Relations and Labor 0.5 Social Sciences, Interdisciplinary 1 0.5 Urban Studies 1 0.5

Note: Citations by subject category add up to more than 215 and exceed 100 per cent due to overlaps across journal categories, see lSI Web of Science.

Appendix 7 xxv

from the fields of geography, sociology, public administration, law, urban studies, operations research, computer science, and engineering have also found the book to be a source of ideas for their own research. There are eight self-citations by Rugman plus 13 self-citations in his co-authored articles. These 21 self-citations essentially leave the impact of the book unchanged, as they decrease the article record to 78.4 per cent from the 80.5 per cent reported in Table ALl.

Many of the 215 citations of Alan Rugman's book come from specialized international business and international economics journals such as: JIBS, MIR, and Weltwirtschaftliches Archiv. The most popular citations to Inside the Multinationals are 53 times in JIBS, and 21 times in SMJ, the two main journals of record in international business strategy.

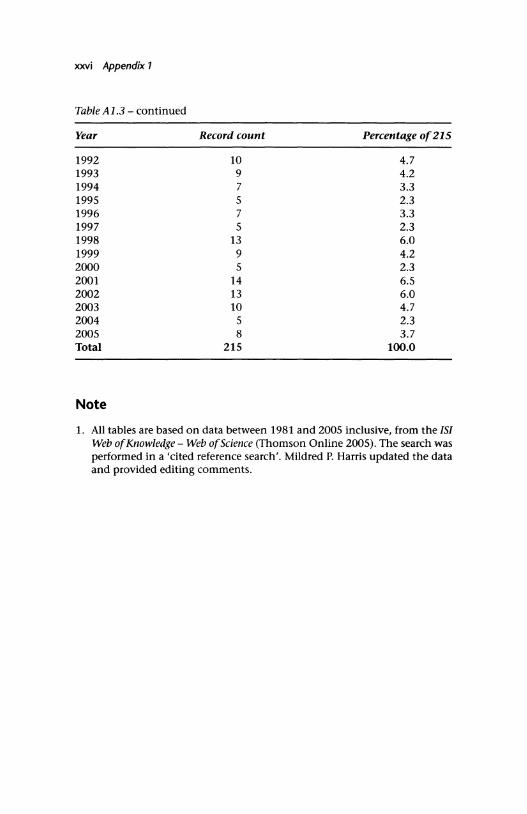

Table A1.3 presents the historical record of citations, arranged by year of citation. For instance, only two years after its initial publication, Inside the Multinationals was already cited 10 times, reaching its highest popularity of 15 citations in a single year in 1986, with another upsurge in more recent years. Table A1.3 shows that Inside the Multinationals has been enjoying a steady increase in usage and popularity since 1981. This suggests that citations would continue in the coming years, which is a sign that the momentum and relevance of the book would endure, based on its past performance.

In conclusion, it should be then of no surprise to the profession why Inside the Multinationals: the Economics ofInternal Markets (1981) has remained topical and relevant. It has been representative of the subsequent work of Alan Rugman, a prolific scholar in the field of international business.

Table Al.3 Citation record of Rugman (1981) by year

Year Record count Percentage of 215

1981 1 0.5 1982 8 3.7 1983 10 4.7 1984 4 1.9 1985 7 3.3 1986 15 7.0 1987 9 4.2 1988 11 5.1 1989 10 4.7 1990 8 3.7 1991 12 5.6

xxvi Appendix 1

Table AI.3 - continued

Year

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 Total

Note

Record count

10 9 7 5 7 5

13 9 5

14 13 10

5 8

215

Percentage of 215

4.7 4.2 3.3 2.3 3.3 2.3 6.0 4.2 2.3 6.5 6.0 4.7 2.3 3.7

100.0

1. All tables are based on data between 1981 and 2005 inclusive, from the lSI Web of Knowledge - Web of Science (Thomson Online 2005). The search was performed in a 'cited reference search'. Mildred P. Harris updated the data and provided editing comments.

Appendix 2: List of Reviews for Inside the Multinationals: The Economics of Internal Markets

Journal ofInternational Business Studies 15(1) (1984): 187-8 by Donald Pattillo. Managerial and Decision Economics 6(1) (1985): 64-5 by Peter Buckley. Canadian Public Administration 26(1) (1983): 134-5 by D.C. MacCharles. The Manchester School (1983): 88-9 by M. Yamin. Business History Review 57(1) (1983): 112-14 by Julienne Laureyssens. Canadian Journal of Economics 15(3) (August 1982): 562-5 by Lorraine Eden. Annals of the American Academy of Political and Social Science 464: 235-6 by Harold Johnson. International Affairs (Royal Institute ofInternational Affairs) 58 (1982): 336-7 by Charles Jones. The World Economy 2(2) (1982): 221-2 by Simon Webley. The Business Economist 3(3): 62 by c.c. Davis. British Book News (February 1982): 338-88 by Michael]. Thomas. Canadian Public Policy (1982): 395-6 by Edward H. Shaffer. Arabia: The Islamic World Review (1983): 63 by Eric Jacobs. Weltwirtschaftliches Archiv 119 (1983): 590 by PaulgeorgJuhl. Kyklos 36(4) (1983): 676-7 by Rameshwar Tandon. Third World Quarterly Ganuary 1982) by Raphael Kaplinsky. Sloan Management Review (Winter 1982). Choice Gune 1982): 550.

xxvii

Selected Quotes from Reviews

Rugman, recognized as a leading proponent of internalization, seeks to pull together a cohesive case for the internalization theory of the multinational enterprise, to explain the development, growth, performance, and possibly the future of the institution. Rugman's work is an outgrowth of his experiences at the University of Reading, and draws extensively from the disciplines of economics and finance. Rugman works from the premise of which there can be little debate, that there is a need for a general theory of the multinational enterprise and of foreign direct investment. He advocates internalization as that theory.

Rugman concludes that the MNE is an institution organized to create and exploit internal markets, and that the most logical and efficient way for the firms to utilize their firm-specific advantages is by foreign direct investment. Finally, Rugman mentions the broader socio-political implications of the MNE. We are reminded that MNEs are creatures of their environment, and that they did not create their environment.

Journal ofInternational Business Studies 15(1) (1984): 187-8 by Donald Pattillo

Rugman is unafraid of the bold, contentious statement: 'Regulation is always inefficient. Multinationals are always efficient' (pp. 156--7). In deciding what is good and what needs rethinking in the current theory of the MNE, Rugman's book is an excellent place to begin.

Managerial and Decision Economics 6(1) (1985): 64-5 by Peter Buckley

Internalization allows the firms to retain appropriability over the knowledge since it never goes outside the sphere of control of the corporate entity. Therefore, internalization provides a theoretical explanation for the existence of multinational enterprises (MNE's).

Canadian Public Administration 26(1) (1983): 134-5 by D.C. MacCharles

xxviii

Selected Quotes from Reviews xxix

The book by Rugman will probably be read only by specialists and deals with a theory of DFI which is only slightly differentiated from that of Dunning. This theory is a skillful application of the Coasian concept of the firm, which regards firms as essentially a means of suppressing the price mechanism. In his book, Rugman has attempted to argue that the 'internalization paradigm' provides a general theory of the multinationals (in the sense that it encompasses all previous explanations as special cases). Rugman's extension of the Hirsch model of DFI is very illuminating. In the book there is an overreliance on Canada, and the author does not seem at all worried that Canada may be a very unrepresentative case. In spite of these criticisms, I believe that there is much in the book that is both original and interesting, and deserves serious study by the specialist.

The Manchester School (1983): 88-9 by M. Yamin

Rugman's objective is not to deal with the theory itself but to claim it as a general theory of direct foreign investment and therefore as a fundamental rationale for multinational corporations. Rugman is to be commended for his attempt to get a grip on solid data on Rand D expenses on a company level. Such data are hard to come by and are difficult to interpret.

Business History Review 57(1) (1983): 112-14 by Julienne Laureyssens

Rugman provides a persuasive theoretical argument that the FSA in knowledge enjoyed by MNEs, which causes them to center Rand D in the parent firm, is responsible for Canada's poor Rand D performance. His view of the efficient MNE hampered by inefficient government regulations may be right, but more detailed theoretical or empirical work is required to make his case convincing.

Canadian Journal of Economics 15(3) (August 1982): 562-6 by Lorraine Eden

Rugman as a free-market economist stresses in a world of effective market competition the efficiency-achieving characteristic of profitmaximizing MNEs. When government intervenes with various and sundry protectionist programs, matters go from not-so-bad to worse. Rugman closes with counsel to MNE managers that they be increasingly

xxx Selected Quotes from Reviews

sensitive as a matter of prudence to the crucial social/political environment in which MNEs function.

Annals of the American Academy of Political and Social Science 464: 235-6 by Harold Johnson

Rugman and Dunning, good liberals that they are, both remind their readers that many practices of multinationals to which national governments have taken exception, such as the abuse of intra-firm transferpricing, are no more than rational responses to price-structures already distorted by earlier government policies. Similarly, while Rugman subtitles his book 'the economics of internal markets' he is in fact almost exclusively concerned with explaining how the economics of imperfect markets may lead firms to internalize ownership specific advantages hardly at all with analysis of the administrative structures which they substitute for markets, and which he rather misleadingly refers to as internal markets.

International Affairs (Royal Institute ofInternational Affairs) 58 (1982): 336-7 by Charles Jones

Professor Rugman ... sheds more light on the development of an important analytical tool that helps to explain why a company sets up production facilities abroad rather than relying on international trade.

The World Economy 2(2) (1982): 221-2 by Simon Webley

Rugman also tells us that the transfer prices are correct internal administrative prices required to make internationalization function; it is meaningless to examine transfer prices on their own or to try to compare them to non-existent arms' length prices.

Kyklos 36(4) (1983): 676-7 by Rameshwar Tandon

In short this book has little to offer its readers, least of all those who are concerned with the distributional implications of imperfect markets. It is largely based upon a series of articles previously published in other forms and its central tenet can therefore be obtained in a less costly and shorter version. But most importantly the book must be seen in the context of a growing attack on the disproportionate power wielded by MNEs, whose interests it represents.

Third World Quarterly Oanuary 1982) by Raphael Kaplinsky

Selected Quotes from Reviews xxxi

This criticism notwithstanding, I am happy to recommend this book to anyone interested in the phenomenon of the MNE.

British Book News (February 1982): 338-88 by Michael J. Thomas

In Alan Rugman's view, multinationals are simply a rational response to the obstacles placed in the path of trade by governments. Denied the freedom of a conventional marketplace, expanding businesses seek to reproduce market conditions internally. Since they do not have market incentives to tell them how to allocate their resources of capital and labour, output and research, they create their own internal markets themselves. Rugman's view makes a lot of sense, at any rate, if you perceive it as a theoretical economist or a multinational director. 'Regulation is always inefficient,' he says. 'Multinationals are always efficient.'

Arabia: The Islamic World Review (1983): 63 by Eric Jacobs

Altogether, Rugman has with this book, once again proven his profound knowledge of the literature. Indeed, at times, the literature is laboured too much.

Weltwirtschaftliches Archiv 119 (1983): 590 by PaulgeorgJuhl

It is a more positive approach to understanding how multinationals work and has been developed by the economists of the Reading School.

British Business 22(1) (1982): 158

Finally, however, these reservations do little to invalidate the conclusion that Rugman has usefully drawn attention to the fact that the MNE is simply a creature of its environment, which Governments still carry the responsibility for creating.

The Business Economist 3(3): 62 by c.c. Davis

![[20대연구소] 주간뉴스클리핑(20140630 0706)](https://static.fdocuments.net/doc/165x107/55904b421a28aba6718b45f7/20-20140630-0706.jpg)