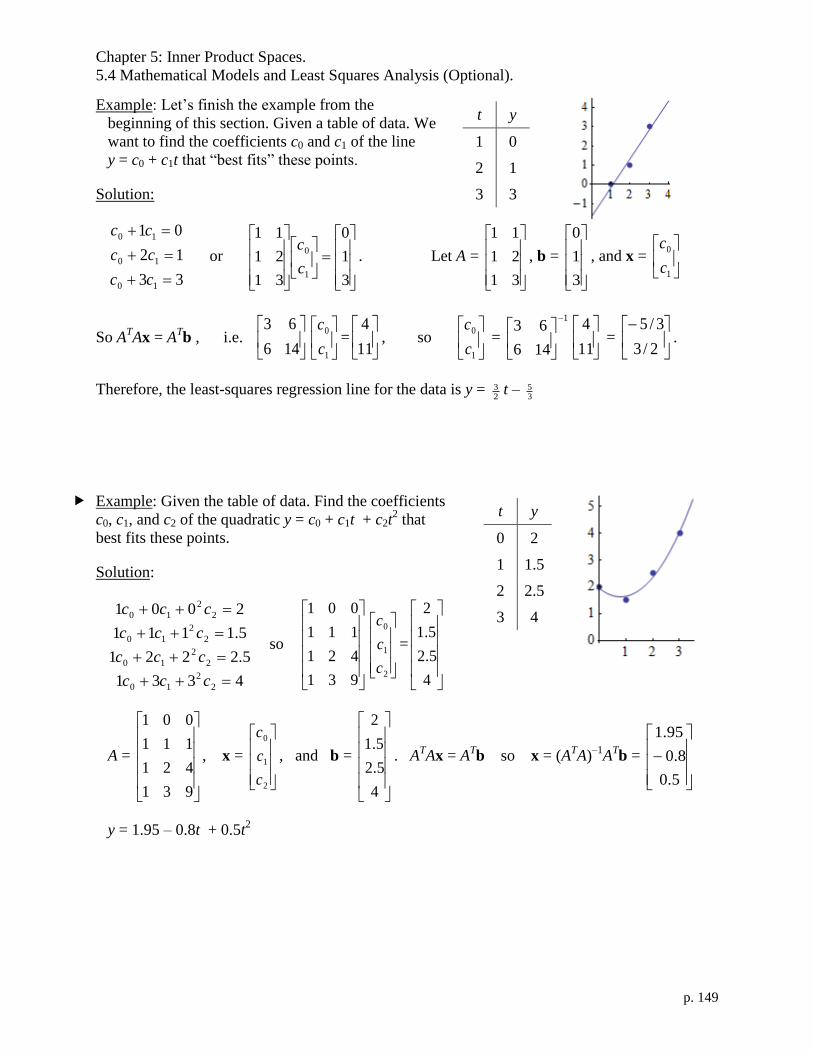

Holtmann75 / Module Math 75 Holtmann Revised 2015-11-18.pdf

287

p. i Math 75 Linear Algebra Class Notes Prof. Erich Holtmann For use with Elementary Linear Algebra, 7 th ed., Larson Revised 21-Nov-2015

Transcript of Holtmann75 / Module Math 75 Holtmann Revised 2015-11-18.pdf

p. i

Math 75

Linear Algebra

Class Notes

Prof. Erich Holtmann

For use with

Elementary Linear Algebra,

7th

ed., Larson

Revised 21-Nov-2015

p. i

Contents

Chapter 1: Systems of Linear Equations 1

1.1 Introduction to Systems of Equations. 1

1.2 Gaussian Elimination and Gauss-Jordan Elimination. 9

1.3 Applications of Systems of Linear Equations. 15

Chapter 2: Matrices. 19

2.1 Operations with Matrices. 19

2.2 Properties of Matrix Operations. 23

2.3 The Inverse of a Matrix. 27

2.4 Elementary Matrices. 31

2.5 Applications of Matrix Operations. 37

Chapter 3: Determinants. 41

3.1 The Determinant of a Matrix. 41

3.2 Determinants and Elementary Operations. 45

3.3 Properties of Determinants. 51

3.4 Applications of Determinants. 55

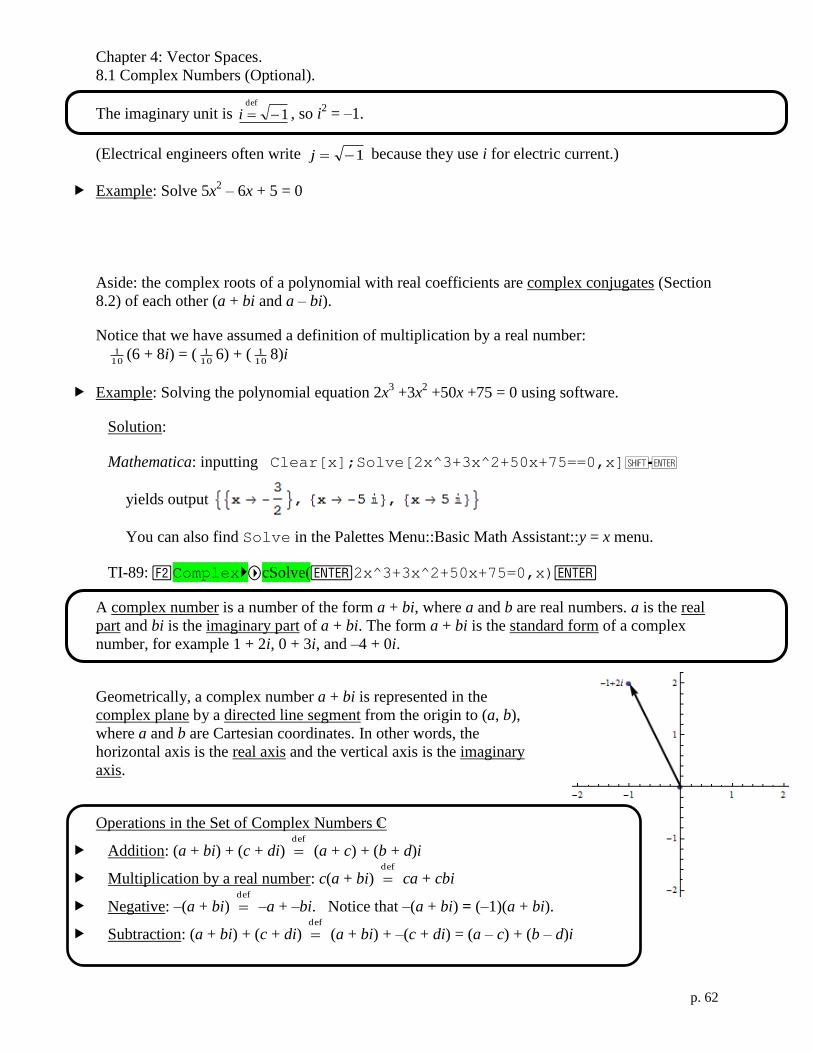

Chapter 4: Vector Spaces. 61

8.1 Complex Numbers (Optional). 61

8.2 Conjugates and Division of Complex Numbers (Optional). 67

4.1 Vectors in Rn. 71

4.2 Vector Spaces. 77

4.3 Subspaces of Vector Spaces. 82

4.4 Spanning Sets and Linear Independence. 86

4.5 Basis and Dimension. 97

4.6 Rank of a Matrix and Systems of Linear Equations. 105

4.7 Coordinates and Change of Basis. 117

Chapter 5: Inner Product Spaces. 121

5.1 Length and Dot Product in Rn. 121

5.2 Inner Product Spaces. 129

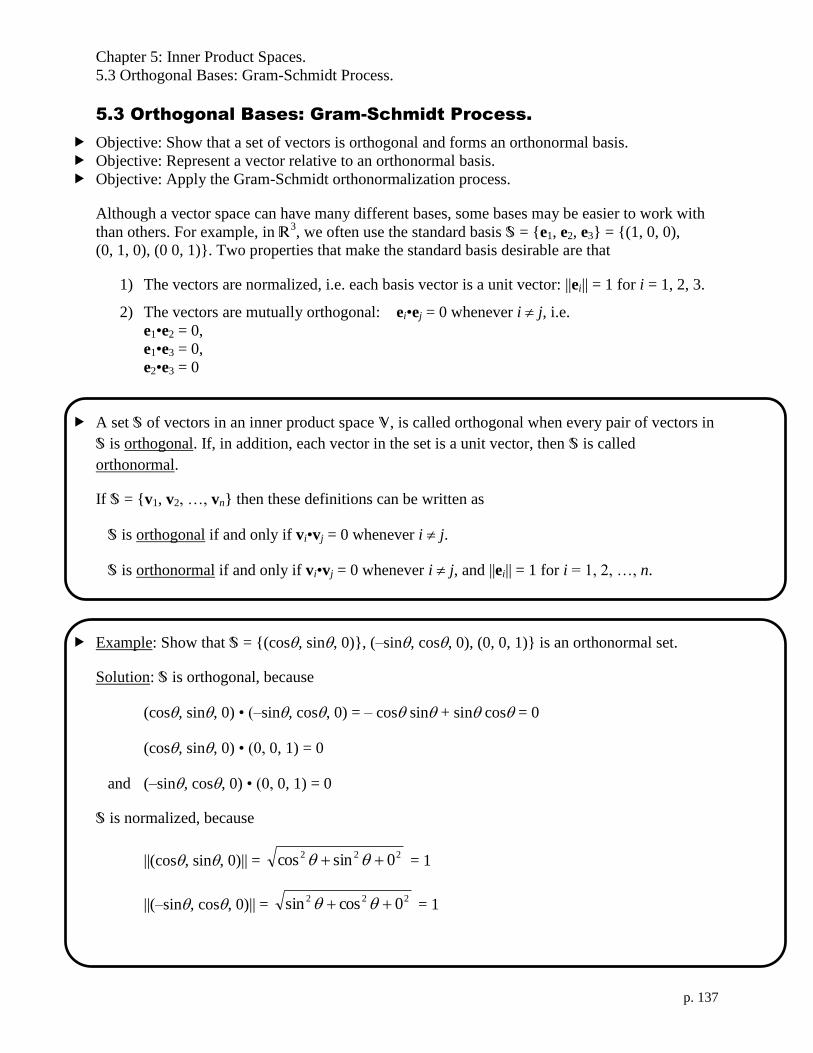

5.3 Orthogonal Bases: Gram-Schmidt Process. 137

5.4 Mathematical Models and Least Squares Analysis (Optional). 145

5.5 Applications of Inner Product Spaces (Optional). 151

8.3 Polar Form and De Moivre's Theorem. (Optional) 157

8.4 Complex Vector Spaces and Inner Products. 163

p. ii

Chapter 6: Linear Transformations. 169

6.1 Introduction to Linear Transformations. 169

6.2 The Kernel and Range of a Linear Transformation. 175

6.3 Matrices for Linear Transformations. 183

6.4 Transition Matrices and Similarity. 191

6.5 Applications of Linear Transformations. 193

Chapter 7: Eigenvalues and Eigenvectors. 201

7.1 Eigenvalues and Eigenvectors. 201

7.2 Diagonalization. 209

7.3 Symmetric Matrices and Orthogonal Diagonalization. 215

7.4 Applications of Eigenvalues and Eigenvectors. 223

8.5 Unitary and Hermitian Spaces. 223

Chapter 1: Systems of Linear Equations

1.1 Introduction to Systems of Equations.

p. 1

Chapter 1: Systems of Linear Equations

1.1 Introduction to Systems of Equations.

Objective: Recognize and solve mn systems of linear equations by hand using Gaussian

elimination and back-substitution.

a1x1 + a2x2 + … + anxn = b is a linear equation in standard form in n variables xi.

The first nonzero coefficient ai is the leading coefficient. The constant term is b.

Compare to the familiar forms of linear equation s in two variables y = mx + b and x = a.

Example: Linear and Nonlinear Equations

(sin ) x1 – 4x2 = e2

sin x1 + 2x2 – 3x3 = 0

Linear Nonlinear

An mn system of linear equations is a set of m linear equations in n unknowns.

Example: Systems of Two Equations in Two Variables

Solve and graph each 22 system.

a. 2x – y = 1

x + y = 5

b. 2x – y = 1

–4x + 2y = –2

c. 2x – y = 1

–4x + 2y = 5

For a system of linear equations, exactly one of the following is true.

1) The system has exactly one solution (consistent, nonsingular system).

2) The system has infinitely many solutions (consistent, singular system).

Use a free parameter or free variable (or several free parameters) to represent the solution set.

3) The system has no solution (inconsistent, singular system).

Chapter 1: Systems of Linear Equations

1.1 Introduction to Systems of Equations.

p. 2

To solve mn systems of linear equations (when m and n are large) we use a procedure called

Gaussian elimination to find an equivalent system of equations in row-echelon form. Then we

use back-substitution to solve for each variable.

Row-echelon form means that the leading coefficients of 1 (called “pivots”) and the zero terms

below them form a stair-step pattern. You could walk downstairs from the top left. You might

have to move more than one column to the right to reach the next step, but you never have to

step down more than one row at a time.

Row-echelon form

91

841

11

731251

5

54

3

54321

x

xx

x

xxxxx

Row-echelon form

00

00

11

731251

3

54321

x

xxxxx

Not row-echelon form

931

8421

1231

731251

54

543

543

54321

xx

xxx

xxx

xxxxx

The goal of Gaussian elimination is to find an equivalent system that is in row-echelon form. The

three operations you can use during Gaussian elimination are

1) Swap the order of two equations.

2) Multiply an equation on both sides by a non-zero constant.

3) Add a multiple of one equation to another equation.

In Gaussian elimination, you start with Equation 1 (the first equation of your mn system).

1) Find the leading coefficient in the current equation. (Sometimes you need to swap

equations in this step.)

2) Eliminate the coefficients of the corresponding variable in all of the equations below the

current equation.

3) Move down to the next equation and go back to Step 1. Repeat until you run out of

equations or you run out of variables.

Solve using back-substitution: solve the last equation for the leading variable, then substitute into

the preceding (i.e. second-to-last) equation and solve for its leading variable, then substitute into

the preceding equation and solve for its leading variable, etc. Variables that are not leading

variables are free parameters, and we often set them equal to t, s, ….

Chapter 1: Systems of Linear Equations

1.1 Introduction to Systems of Equations.

p. 3

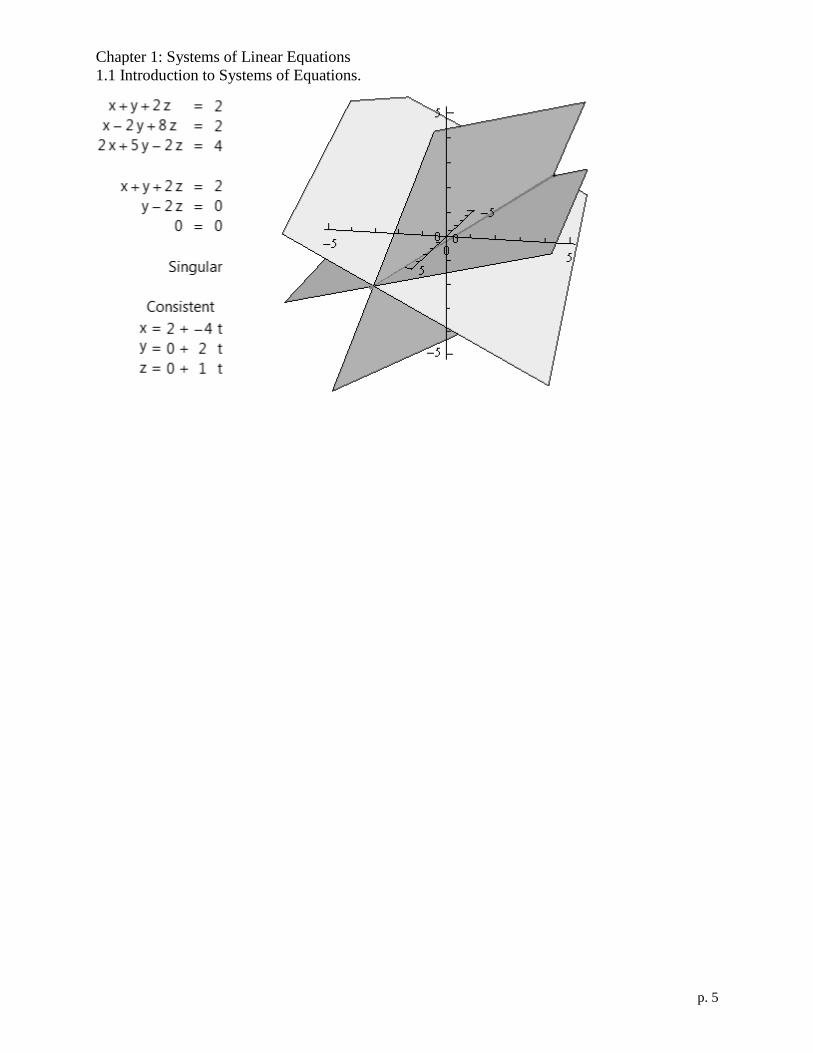

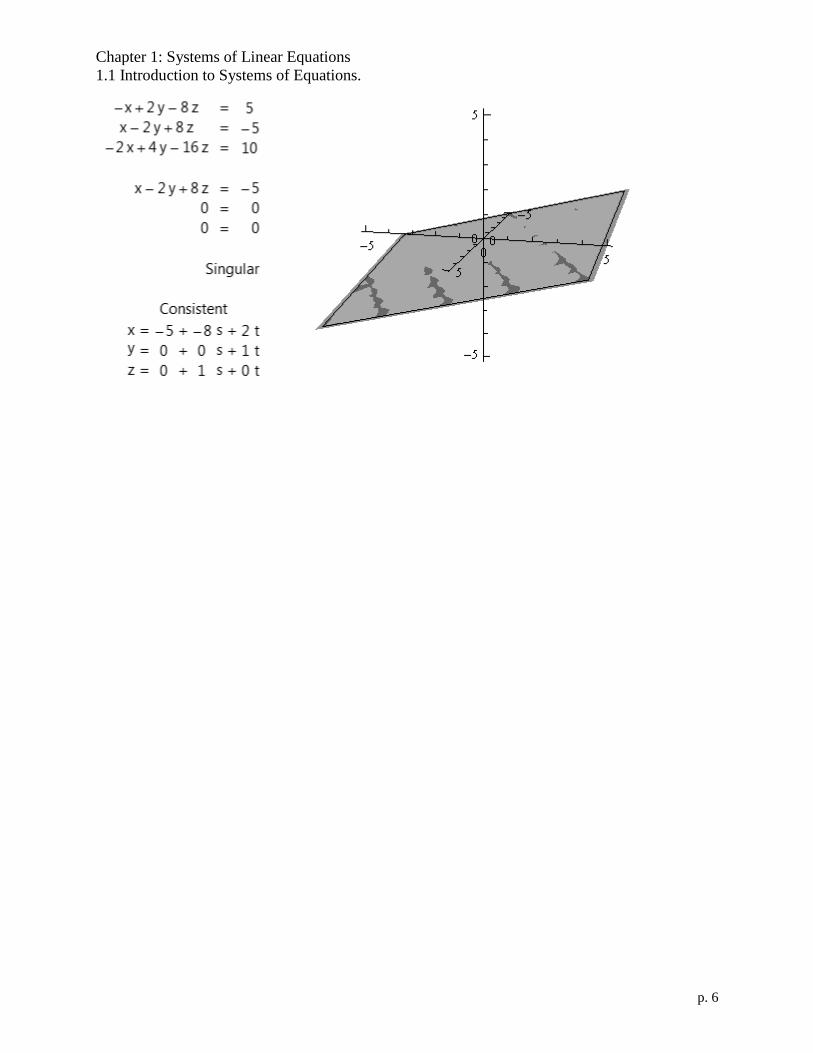

Examples: Gaussian Elimination and Back-Substitution on 33 Systems of Linear Equations.

Chapter 1: Systems of Linear Equations

1.1 Introduction to Systems of Equations.

p. 4

Chapter 1: Systems of Linear Equations

1.1 Introduction to Systems of Equations.

p. 5

Chapter 1: Systems of Linear Equations

1.1 Introduction to Systems of Equations.

p. 6

Chapter 1: Systems of Linear Equations

1.1 Introduction to Systems of Equations.

p. 7

Example: Chemistry Application

Write and solve a system of linear equations for the chemical reaction

(x1)CH4 + (x2)O2 (x3)CO2 + (x4)H2O

Solution: write a separate equation for each element, showing the balance of that element.

C: 1x1 + 0x2 = 1x3 + 0x4 so 1x1 + 0x2 – 1x3 + 0x4 = 0

H: 4x1 + 0x2 = 0x3 + 2x4 so 4x1 + 0x2 + 0x3 – 2x4 = 0

O: 0x1 + 2x2 = 2x3 + 1x4 so 0x1 + 2x2 – 2x3 – 1x4 = 0

Chapter 1: Systems of Linear Equations

1.2 Gaussian Elimination and Gauss-Jordan Elimination.

p. 9

1.2 Gaussian Elimination and Gauss-Jordan Elimination.

Objective: Use matrices and Gauss-Jordan elimination to solve mn systems of linear equations

by hand and with software.

Objective: Use matrices and Gaussian elimination with back-substitution to solve mn systems

of linear equations by hand and with software.

Use row-echelon form or reduced row-echelon form to determine the number of solutions of a

homogeneous system of linear equations, and (if applicable) the number of free parameters.

A matrix is a rectangular array of numbers, called matrix

entries, arranged in horizontal rows and vertical columns.

Matrices are denoted by capital letters; matrix entries are

denoted by lowercase letters with two indices. In a given

matrix entry aij, the first index i is the row, and the second

index j is the column. The entries a11, a22, a33, … compose the

main diagonal. If m = n then A is called a square matrix.

A linear system

mnmnmmm

nn

nn

bxaxaxaxa

bxaxaxaxa

bxaxaxaxa

332211

22323222121

11313212111

can represented either by a coefficient matrix A and a column vector b

mnmmm

n

n

n

aaaa

aaaa

aaaa

aaaa

A

331

3333231

2232221

1131211

and

mb

b

b

b

3

2

1

b

or by an augmented matrix M, which I will sometimes write as [A | b]

mmnmmm

n

n

n

baaaa

baaaa

baaaa

baaaa

M

331

33333231

22232221

11131211

(The book, Mathematica, and the calculator do not display the dotted vertical line.)

To create M in Mathematica from A and b, type m=Join[a,b,2]

To create M on the TI-89 from A and b, type

Matrixaugment(A

B

M

mnmmm

n

n

n

aaaa

aaaa

aaaa

aaaa

A

321

3333231

2232221

1131211

Chapter 1: Systems of Linear Equations

1.2 Gaussian Elimination and Gauss-Jordan Elimination.

p. 10

In a similar manner to that used for an mn system of linear equations, we can use a Gaussian

elimination on the coefficient side A of the augmented matrix [A | b] to find an equivalent

augmented matrix [U | c] in row-echelon form. Then we use back-substitution to solve for each

variable. U is called an upper triangular matrix because all non-zero entries are on or above the

main diagonal.

row-echelon form row-echelon form not row-echelon form

20000

41000

50100

31251

00000

00000

50100

31251

31000

42100

23100

31251

Example: Use Gaussian elimination and back-substitution to solve. The three elementary row

operations you can use during Gaussian elimination are

1) Swap the two rows.

2) Multiply a row by a non-zero constant.

3) Add a multiple of one row to another row.

2111

3123

8346

zyx

zyx

zyx

2111

3123

8346

2100

210

1

23

34

21

32

1)2()1( so

1)2(2 so 2

2

21

32

34

34

21

32

23

23

xzyx

yzy

z

Steps:

Chapter 1: Systems of Linear Equations

1.2 Gaussian Elimination and Gauss-Jordan Elimination.

p. 11

Instead of using back-substitution, we can take the row-echelon form [U | c] and eliminate the

coefficients above the pivots by adding multiples of the pivot rows. The result [R | d] is called

reduced row-echelon form.

reduced row-echelon form reduced row-echelon form

20000

41000

50100

110051

30000

40000

23100

31051

Example: Use Gauss-Jordan elimination to solve.

2111

3123

8346

zyx

zyx

zyx

2111

3123

8346

2100

210

1

23

34

21

32

2100

1010

1001

2

1

1

z

y

x

Chapter 1: Systems of Linear Equations

1.2 Gaussian Elimination and Gauss-Jordan Elimination.

p. 12

Example Using software to find the Reduced Row-Echelon Form (Exercise 1.2 #39)

Mathematica

Go to the Palettes Menu and open the Basic Math

Assistant. Under Basic Commands, open the Matrix

Tab.

Type a=

and click

Use the Add Row and Add Column buttons to expand

the matrix, so you can enter the augmented matrix

(If you make the matrix to large, use to remove rows and columns.) Press (or

on the number pad) when you are finished entering the augmented matrix.

Another way to enter the augmented matrix is to type (or download) a={{1,-1,2,2,6,6},{3,-2,4,4,12,14},{0,1,-1,-1,-3,-3},{2,-

2,4,5,15,10},{2,-2,4,4,13,13}}

MatrixForm[a]

You can download this matrix from http://holtmann75.pbworks.com. Click on Electronic

Data Sets and open 1133110878_323834.zip/DataSets/Mathematica/0102039.nb (Ch. 01,

Section 02, Problem 039). Notice that A and a are different variables! User-defined variables

should always begin with a lower-case letter, because Mathematica’s built-in fuctions and

commands begin with capital letters. (For example, N and C are already defined by

Mathematica.)

On the Basic Math Assistant palette, click on MatrixForm RowReduce and type a so you have

MatrixForm[RowReduce[a]]

Converting back to a system of linear equations, we have

x1 = 2 x4 = 5

x2 = 2 x5 = 1

x3 = 3

Chapter 1: Systems of Linear Equations

1.2 Gaussian Elimination and Gauss-Jordan Elimination.

p. 13

TI-89: Type

Data/Matrix Editor

New...

Type: Matrix

Folder: main

Variable: A

(A is above . If you type = instead of a, use .

If a already exists, then use Open... on the previous

screen instead of New....)

Use and the

arrow keys to type

in the coefficient matrix

(If you need to insert or delete a row or column, use )

When you are finished, press .

Another way to enter the matrix is to type (from the

home screen) 1,1,2,2,6,6

3,2,4,4,12,14

0,1,1,1,3,3

2,2,4,5,15,10

2,2,4,4,13,13

A

After the matrix is entered, type A

Matrix rref( A

Converting back to a system of linear equations, we have

x1 = 2

x2 = 2

x3 = 3

x4 = 5

x5 = 1

Chapter 1: Systems of Linear Equations

1.2 Gaussian Elimination and Gauss-Jordan Elimination.

p. 14

Mathematica can help you perform row operations. If your augmented matrix is in a, then

a[[2]] is row 2 of the matrix. To view a in the usual format, type

MatrixForm[a]

To swap rows 2 and 3 of a, type a[[{2,3}]]=a[[{3,2}]]

To multiply row 2 of a by 7, type a[[2]]=7*a[[2]]

To add 7 times row 2 to row 1, type a[[1]]=a[[1]]+7*a[[2]]

Mathematica performs operations in the order that you type them in, not as they appear on the

screen. If you go back and edit your work, you can use Evaluate Notebook under the Evaluation

menu to recalculate the notebook in the order on the screen.

The TI-89 can also help you perform row operations. If your augmented matrix is in a, then …

To swap rows 2 and 3 of a and store the result in a1, type

Matrix Row opsrowSwap(A,2,3,)

A1

To multiply row 2 of a1 by 7 and store the result in a2, type

Matrix Row opsmRow(7,A1,2)

A2

To add 7 times row 2 of a2 to row 1 and store the result in a3, type

Matrix Row opsmRowAdd(7,A2,1,3)

A3

About notation:

43

21 and

43

21 are matrices, but

43

21 is a determinant (Ch. 3).

Theorem 1.1. Every homogeneous (constants on right-hand side are all zeroes) system of linear

equations is consistent. The number of free parameters in the solution set is the number of

variables minus the number of pivots (leading coefficients). If there are zero free parameters,

then there is exactly one solution.

Examples:

0112

0201

0511

0121428205

0559211

011150

042511

02131500

0377208

0454156

012352

Solutions:

0000

0310

0201

Chapter 1: Systems of Linear Equations

1.3 Applications of Systems of Linear Equations.

p. 15

1.3 Applications of Systems of Linear Equations.

Objective: Set up and solve a system of equations to fit a polynomial function to a set of data

points.

Objective: Set up and solve a system of equations to represent a network.

Polynomial Curve Fitting.

Given m data points (t1, y1), (t2, y2), …, (tm, ym). We want to find a polynomial of degree m–1 that

passes through these points.

p(t) = c0 + c1t + c2t2 + … + cmt

m Notice that yj = c0 + c1(tj)+ c2(tj)

2 + … + cm–1(tj)

m–1

This produces an mm linear system:

1

1

22

1

11

)(1

)(1

)(1

m

mm

m

m

tt

tt

tt

1

1

0

mc

c

c

=

my

y

y

2

1

that you can solve using Gauss-Jordan elimination.

Example 1.3#7

086028

21012

y

t

Chapter 1: Systems of Linear Equations

1.3 Applications of Systems of Linear Equations.

p. 16

Example 1.3#9

1275

200820072006

y

t

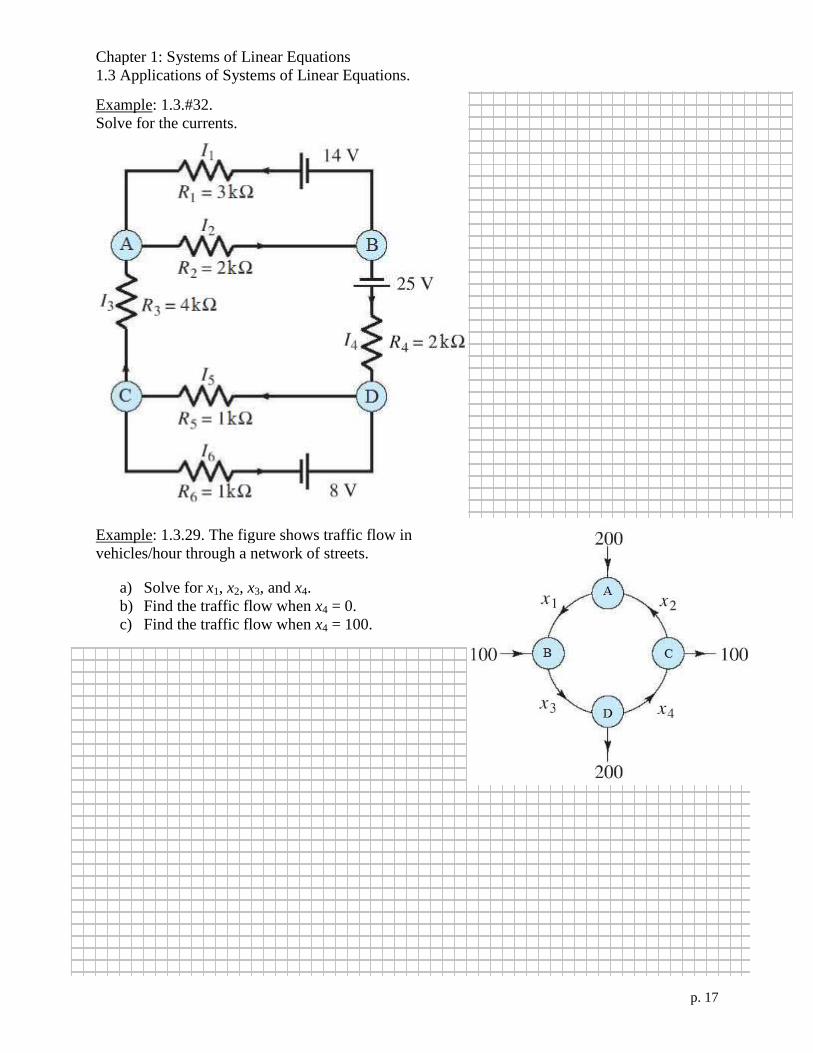

Network Analysis: write a system of linear equations using Kirchoff’s Laws.

1) Flow into each node (also called vertex) equals flow out.

2) In an electrical network, the sum of the products IR (I = current and R = resistance) around

any closed path of edges (lines) is equal to the total voltage in the loop from the batteries.

A resistor is represented by the symbol Resistance is measured in ohms ().

1 k = 1000

A battery is represented by the symbol If the current flows through the battery

from the short line (–) to the long line

(+), then the voltage is positive.

Current is measure in amps (A). 1 mA = 0.001 A.

Flow into a node is positive. Flow out of a node is negative.

To write a system of equations,

1) Pick a direction (at random) for each current I.

2) For each node, write an equation for the current input and output.

3) For each loop, write the V = IR equation.

I

Chapter 1: Systems of Linear Equations

1.3 Applications of Systems of Linear Equations.

p. 17

Example: 1.3.#32.

Solve for the currents.

Example: 1.3.29. The figure shows traffic flow in

vehicles/hour through a network of streets.

a) Solve for x1, x2, x3, and x4.

b) Find the traffic flow when x4 = 0.

c) Find the traffic flow when x4 = 100.

Chapter 2: Matrices.

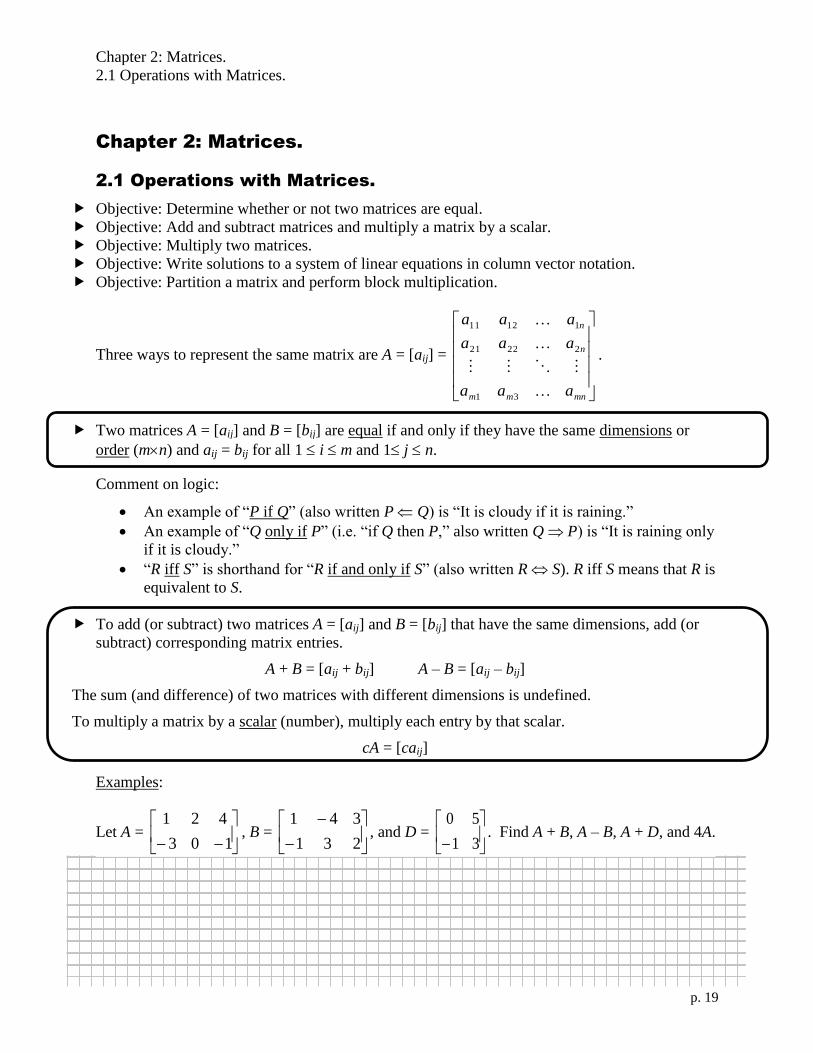

2.1 Operations with Matrices.

p. 19

Chapter 2: Matrices.

2.1 Operations with Matrices.

Objective: Determine whether or not two matrices are equal.

Objective: Add and subtract matrices and multiply a matrix by a scalar.

Objective: Multiply two matrices.

Objective: Write solutions to a system of linear equations in column vector notation.

Objective: Partition a matrix and perform block multiplication.

Three ways to represent the same matrix are A = [aij] =

mnmm

n

n

aaa

aaa

aaa

31

22221

11211

.

Two matrices A = [aij] and B = [bij] are equal if and only if they have the same dimensions or

order (mn) and aij = bij for all 1 i m and 1 j n.

Comment on logic:

An example of “P if Q” (also written P Q) is “It is cloudy if it is raining.”

An example of “Q only if P” (i.e. “if Q then P,” also written Q P) is “It is raining only

if it is cloudy.”

“R iff S” is shorthand for “R if and only if S” (also written R S). R iff S means that R is

equivalent to S.

To add (or subtract) two matrices A = [aij] and B = [bij] that have the same dimensions, add (or

subtract) corresponding matrix entries.

A + B = [aij + bij] A – B = [aij – bij]

The sum (and difference) of two matrices with different dimensions is undefined.

To multiply a matrix by a scalar (number), multiply each entry by that scalar.

cA = [caij]

Examples:

Let A =

103

421, B =

231

341, and D =

31

50. Find A + B, A – B, A + D, and 4A.

Chapter 2: Matrices.

2.1 Operations with Matrices.

p. 20

In Mathematica, use a+b, a–b, and 4*a or 4a to add matrices, subtract matrices, and multiply

scalars c by matrices. Remember, you can enter D =

31

50 from the Palettes Menu::Basic

Math Assistant::Basic Commands::Matrix Tab.

On the TI-89, use ab, a b, and ca or 4a to add matrices A and B, subtract matrices,

and multiply scalars c by matrices. Remember, you can enter D =

31

50 from the home screen

as [0,5;-1,3]D or from Data/Matrix Editor. (Be sure to use

Type: Matrix)

Matrix multiplication is defined in a much more complex manner. For a 11 system, we can

write ax = b. We want a definition of matrix multiplication that allows us to write an mn system

mnmnmmm

nn

nn

bxaxaxaxa

bxaxaxaxa

bxaxaxaxa

332211

22323222121

11313212111

as Ax = b,

where A is the coefficient matrix

mnmm

n

n

aaa

aaa

aaa

A

21

22221

11211

,

and x and b are column matrices (or column vectors):

nx

x

x

2

1

x and

mb

b

b

2

1

b .

Observe that each row of A was multiplied by the column x to give the corresponding row of b.

If A = [aij] is an mn matrix and B = [bij] is an np matrix, then the product AB is an mp matrix

A = [cij] where

[cij] =

n

k

kjikba1

= ai1b1j + ai2b2j + ai3b3j + … ainbnj

If the column dimension of A does not match the row dimension of B, then the product is

undefined

Chapter 2: Matrices.

2.1 Operations with Matrices.

p. 21

Examples

52

33

23

32

512

014

In Mathematica, use a.b to multiply matrices.(Do not use a*b)

On the TI-89, use ab multiply matrices.

Example: Write solutions to a system of linear equations in column vector notation.

Solve

2110

1011

3121

4

3

2

1

x

x

x

x

=

0

0

0

4

3

2

1

x

x

x

x

= t

1

1

1

2

Block multiplication on partitioned matrices works whenever the dimensions are OK.

Examples

2221

1211

1200

0001

0010

AA

AAA with

1200

00

00

01

10

2221

1211

AA

AA and

2221

1211

265

134

011

021

BB

BBB with

2

1

65

34

0

0

11

21

2221

1211

BB

BB

Then AB =

2222122121221121

2212121121121111

BABABABA

BABABABA =

2222212211

2211211111

000

000

BABAB

BABBA=

01213

021

011

Chapter 2: Matrices.

2.1 Operations with Matrices.

p. 22

Ax=

mnmm

n

n

aaa

aaa

aaa

21

22221

11211

nx

x

x

2

1

=

nmnmm

nn

nn

xaxaxa

xaxaxa

xaxaxa

2211

2222121

1212111

=n

mn

n

n

mm

x

a

a

a

x

a

a

a

x

a

a

a

2

1

2

2

22

12

1

1

21

11

In block matrix notation, we write [ a1 | a2 | … | an ] =

mnmm

n

n

aaa

aaa

aaa

21

22221

11211

where the ai are

m1 column matrices. The Ax = [ a1 | a2 | … | an ]

nx

x

x

2

1

= a1x1 + a2x2 + … + anxn

Similarly, if B is an lm matrix (so BA is defined), then

BA = B[ a1 | a2 | … | an ] = [ Ba1 | Ba2 | … | Ban ], i.e. the columns of BA are Bai.

Notice that B is lm, ai is m1, Bai is l1, and BA is ln.

On the other hand, we could partition A into 1m row matrices ri

A =

mnmm

n

n

aaa

aaa

aaa

21

22221

11211

=

mr

r

r

2

1

. Then Ax =

mnmm

n

n

aaa

aaa

aaa

21

22221

11211

nx

x

x

2

1

=

mr

r

r

2

1

x =

xr

xr

xr

m

2

1

.

Notice that ri is 1n, x is n1, rix is 11 (i.e. a number), and Ax is m1.

If E =

lmll

m

m

eee

eee

eee

21

22221

11211

=

le

e

e

2

1

then EA =

le

e

e

2

1

A =

A

A

A

le

e

e

2

1

.

Notice that ei is 1m, A is mn, eiA is 1n, and EA is ln

If e = [ e1 | e2 | … | em], then eA = [ e1 | e2 | … | em]

mr

r

r

2

1

= e1r1 + e2r2 + … + emrm

Notice that e is 1m, A is mn, ei is a number, ri is 1n, and eA is 1n.

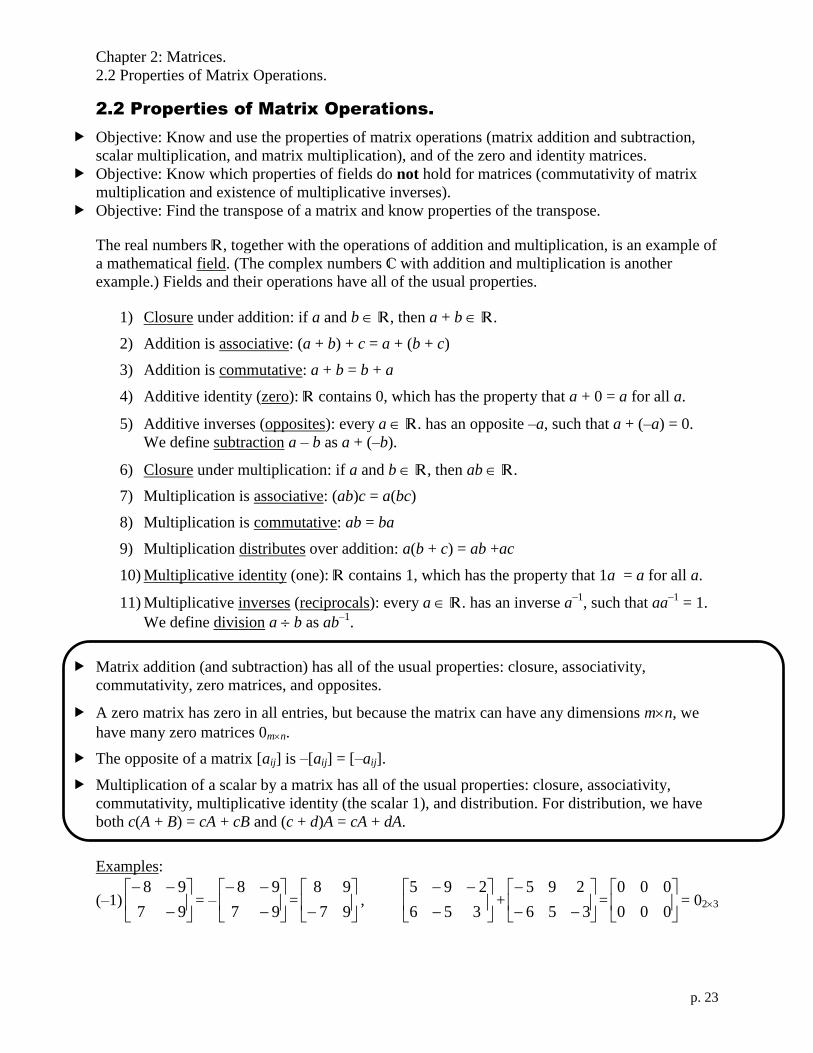

Chapter 2: Matrices.

2.2 Properties of Matrix Operations.

p. 23

2.2 Properties of Matrix Operations.

Objective: Know and use the properties of matrix operations (matrix addition and subtraction,

scalar multiplication, and matrix multiplication), and of the zero and identity matrices.

Objective: Know which properties of fields do not hold for matrices (commutativity of matrix

multiplication and existence of multiplicative inverses).

Objective: Find the transpose of a matrix and know properties of the transpose.

The real numbers R, together with the operations of addition and multiplication, is an example of

a mathematical field. (The complex numbers C with addition and multiplication is another

example.) Fields and their operations have all of the usual properties.

1) Closure under addition: if a and b R, then a + b R.

2) Addition is associative: (a + b) + c = a + (b + c)

3) Addition is commutative: a + b = b + a

4) Additive identity (zero): R contains 0, which has the property that a + 0 = a for all a.

5) Additive inverses (opposites): every a R. has an opposite –a, such that a + (–a) = 0.

We define subtraction a – b as a + (–b).

6) Closure under multiplication: if a and b R, then ab R.

7) Multiplication is associative: (ab)c = a(bc)

8) Multiplication is commutative: ab = ba

9) Multiplication distributes over addition: a(b + c) = ab +ac

10) Multiplicative identity (one): R contains 1, which has the property that 1a = a for all a.

11) Multiplicative inverses (reciprocals): every a R. has an inverse a–1

, such that aa–1

= 1.

We define division a b as ab–1

.

Matrix addition (and subtraction) has all of the usual properties: closure, associativity,

commutativity, zero matrices, and opposites.

A zero matrix has zero in all entries, but because the matrix can have any dimensions mn, we

have many zero matrices 0mn.

The opposite of a matrix [aij] is –[aij] = [–aij].

Multiplication of a scalar by a matrix has all of the usual properties: closure, associativity,

commutativity, multiplicative identity (the scalar 1), and distribution. For distribution, we have

both c(A + B) = cA + cB and (c + d)A = cA + dA.

Examples:

(–1)

97

98= –

97

98=

97

98,

356

295+

356

295=

000

000= 023

Chapter 2: Matrices.

2.2 Properties of Matrix Operations.

p. 24

Multiplication of matrices is closed, is associative, and distributes over matrix addition. The

multiplicative identity matrices are square matrices with ones on the main diagonal and zeros

everyplace else: Inn =

100

010

001

. If A is mn, then Imm Amn = Amn and Amn Inn = Amn

We define exponents for square matrices A and positive integers k: Ak =

timesk

AAA . Also, we

define A0 = I.

Multiplication of matrices is not commutative in general.

Many matrices do not have multiplicative inverses. Division of matrices is undefined.

Examples:

10

01

356

295=

356

295

100

010

001

=

97

98

356

295 =

356

295

97

98=

356

295

13

12

01

=

13

12

01

356

295=

Theorem 2.5: For a system of linear equations, exactly one of the following is true.

1) The system has no solution (inconsistent, singular system).

2) The system has exactly one solution (consistent, nonsingular system).

3) The system has infinitely many solutions (consistent, singular system).

Use a free parameter or free variable (or several free parameters) to represent the solution set.

Proof using matrix operations:

Given a system of linear equations Ax = b. Exactly one of the following is true: the system has

no solution, the system has exactly one solution, or the system has at least two solutions (call

them x1 and x2).

Chapter 2: Matrices.

2.2 Properties of Matrix Operations.

p. 25

*

If the system has two solutions, then Ax1 = b and Ax2 = b so

A(x1 – x2) = Ax1 – Ax2 = b – b = 0.

Let xh = x1 – x2, so xh is a nonzero solution to the homogenous equation Ax = 0.

Then for any scalar t, x1 + txh is a solution of Ax = b because

A(x1 + txh) = Ax1 + tAxh = b+ t 0 = b.

Thus, in the last case, the system has infinitely many solutions with a parameter t.

The transpose AT of a matrix A is formed by writing its columns as rows. For example,

if

mnmmm

n

n

n

aaaa

aaaa

aaaa

aaaa

A

321

3333231

2232221

1131211

then

mnnnn

m

m

m

T

aaaa

aaaa

aaaa

aaaa

A

321

3332313

2322212

1312111

.

Equivalently, the transpose of A is formed by writing rows as columns. The ij entry of AT is aji.

Example: Find the transpose of A =

8251

4803

0739

Mathematica: to take the transpose of a matrix, either type Transpose[a] (also available on

the Basic Math Assistant palette) or type a followed by tr (four separate keystrokes).

After the first three keystrokes, you will see atr. After the fourth keystroke, atr will

change to aT. Of course, at the end, type

TI-89: A

MatrixT

Properties of the transpose:

1) (AT)T = A

2) (A + B)T = A

T +B

T

3) (cA) T

=cAT

4) (AB) T

= BTA

T

Chapter 2: Matrices.

2.2 Properties of Matrix Operations.

p. 26

Example of Property #4:

Consider A = and B =

The 32 entry of (AB)T is the 23 entry of AB =

which is a21b13 + a22b23 + a23b33

If we look at AT and B

T, we much reverse the order of multiplication to obtain row column.

BTA

T =

The 32 entry BTA

T is b13a21 + b23a22 + b33a23. You can see that (AB)

T = B

TA

T

A matrix M is symmetric iff MT = M.

Example: M =

525

246

5610

is symmetric. Prove that AAT is symmetric for any matrix A.

Proof:

Chapter 2: Matrices.

2.3 The Inverse of a Matrix.

p. 27

2.3 The Inverse of a Matrix.

Objective: Find the inverse of a matrix (if it exists) by Gauss-Jordan elimination.

Objective: Use properties of inverse matrices.

Objective: Use an inverse matrix to solve a system of linear equations.

A square nn matrix is invertible (or nonsingular) when there exists an nn matrix A–1

such that

AA–1

= Inn and A–1

A = Inn

where Inn is the identity matrix. A–1

is called the (multiplicative) inverse of A. A matrix that does

not have an inverse is called singular (or noninvertible). Nonsquare matrices do not have

inverses.

Theorem 2.7: If A is an invertible matrix, then the inverse is unique.

Proof: let B and C be inverses of A. Then BA = I an AC = I. So

B = BI = B(AC) = (BA)C = IC =C. Therefore, B = C and the inverse of A is unique.

Example: Find the inverse of A =

21

53.

Solution: We need to solve the system AX = I, or

21

53

2221

1211

xx

xx =

10

01,

which gives four equations 121021

053153

22122111

22122111

xxxx

xxxx

To solve these four equations, we take the reduced row echelon forms

021

153

110

201 and

121

053

310

501, so A

–1 = X =

31

52

Since the row operations performed to find the reduced row echelon form depend only on the

coefficient part of the augmented matrix

21

53, we could solve all four equations

simultaneously by using a doubly augmented matrix

[ A | I ] =

1021

0153

3110

5201= [ I | A

–1 ]

To create the doubly augmented matrix in Mathematica from A, type

m=Join[a, IdentityMatrix[2],2]

To create the doubly augmented matrix on the TI-89 from A, type

Chapter 2: Matrices.

2.3 The Inverse of a Matrix.

p. 28

*

Matrix

augment(

A,

Matrix

identity(2))

M

We used IdentityMatrix[2] and identity(2) because we wanted a 22 matrix.

To find the inverse of an nn matrix A by Gauss-Jordan elimination, find the reduced row

echelon form of th n2n augmented matrix [ A | I ]. If the nn block on the left can be reduced to

I, then the nn block on the right is A–1

[ A | I ] [ I | A–1

]

If the nn block on the left cannnot be reduced to I, then A is not invertible.

Example: Invert A =

321

221

111

using Gauss-Jordan elimination.

Example: Invert A =

332

221

111

using Gauss-Jordan elimination.

Example: Invert M =

dc

ba using Gauss-Jordan elimination.

You can also use software. First clear the variables using Clear[a,b,c,d] or

Clear a-z, then type Inverse[m] or

M^1

(also on Basic Math Assistant palette)

Chapter 2: Matrices.

2.3 The Inverse of a Matrix.

p. 29

*

Theorem 2.8 Properties of Inverse Matrices

If A is an invertible matrix, k is a positive integer, and c is a nonzero scalar, then A–1

, Ak, cA, and

AT are invertible, and

1) (A–1

) –1

= A

2) (Ak)–1

= (A–1

)k

3) (cA) –1

= c1 A

–1

4) (AT)–1

= (A–1

)T

Proof:

1)

2) Proof by Induction (see the Appendix)

When k = 1,

If (Ak)–1

= (A–1

)k,

By mathematical induction, we conclude that (Ak)

–1 = (A

–1) for all positive integers k.

3)

4)

Chapter 2: Matrices.

2.3 The Inverse of a Matrix.

p. 30

*

*

*

Theorem 2.9 Inverse of a Product

If A and B are invertible nn matrices, then (AB)–1

= B–1

A–1

.

Proof:

Theorem 2.10 Cancellation Properties

Let C be an invertible matrix.

1) If AC = BC, then A = B. (Right cancellation property)

2) If CA = CB, then A = B. (Left cancellation property)

Theorem 2.11 Systems of Equations with Unique Solutions.

If A is an invertible matrix, then the system Ax = b has a unique solution x = A–1

b.

Review: What is wrong with the following “proof” that if AB = I and CA = I then B = C?

A

CA

A

AB

B = C

What is wrong with the following “proof” that if AB = I and CA = I and A is invertible then B =

C?

AB = CA

A–1

AB = CAA–1

IB = CI

B = C

Chapter 2: Matrices.

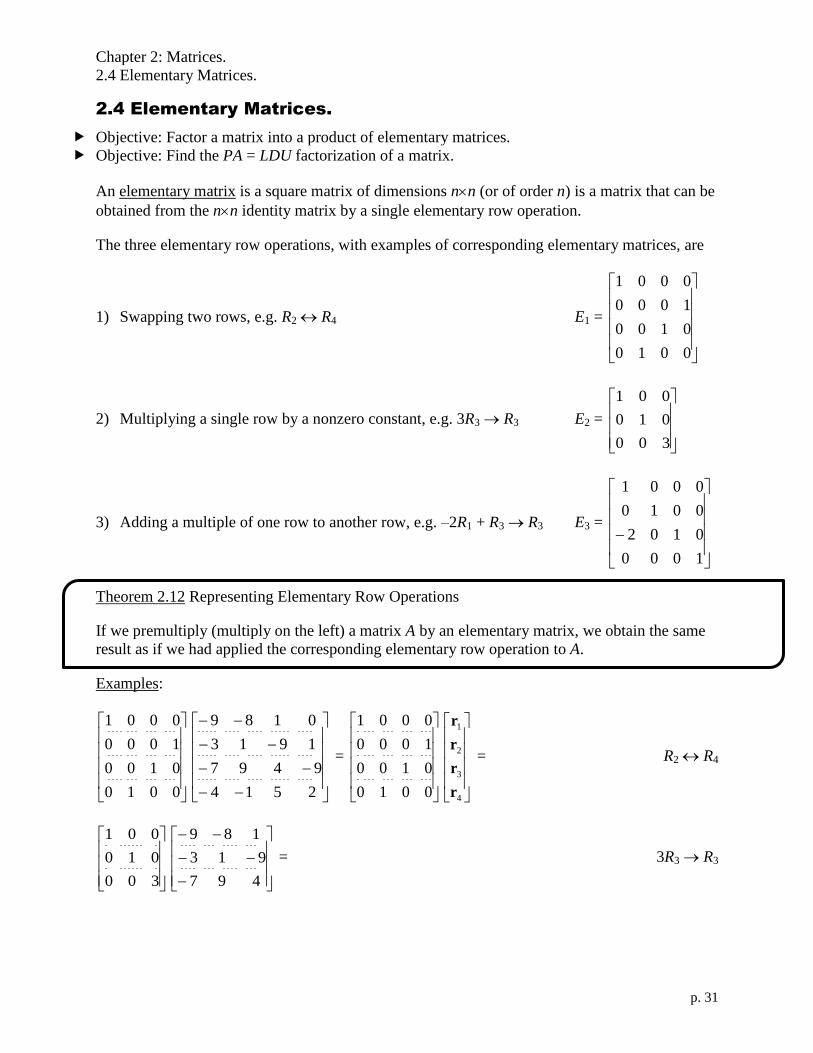

2.4 Elementary Matrices.

p. 31

2.4 Elementary Matrices.

Objective: Factor a matrix into a product of elementary matrices.

Objective: Find the PA = LDU factorization of a matrix.

An elementary matrix is a square matrix of dimensions nn (or of order n) is a matrix that can be

obtained from the nn identity matrix by a single elementary row operation.

The three elementary row operations, with examples of corresponding elementary matrices, are

1) Swapping two rows, e.g. R2 R4 E1 =

0010

0100

1000

0001

2) Multiplying a single row by a nonzero constant, e.g. 3R3 R3 E2 =

300

010

001

3) Adding a multiple of one row to another row, e.g. –2R1 + R3 R3 E3 =

1000

0102

0010

0001

Theorem 2.12 Representing Elementary Row Operations

If we premultiply (multiply on the left) a matrix A by an elementary matrix, we obtain the same

result as if we had applied the corresponding elementary row operation to A.

Examples:

0010

0100

1000

0001

2514

9497

1913

0189

=

0010

0100

1000

0001

4

3

2

1

r

r

r

r

= R2 R4

300

010

001

497

913

189

= 3R3 R3

Chapter 2: Matrices.

2.4 Elementary Matrices.

p. 32

1000

0102

0010

0001

2514

9497

1913

0189

= –2R1 + R3 R3

Gaussian elimination can be represented by a product of elementary matrices. For example,

A =

3963

5121

2310

R1 R2 E1 =

100

001

010

3963

2310

5121

3R1+ R3 R3 E2 =

103

010

001

12600

2310

5121

61 R3 R3 E3 =

6/100

010

001

2100

2310

5121

so

2100

2310

5121

= E3(E2(E1A)) =

6/100

010

001

103

010

001

100

001

010

3963

5121

2310

Two nn matrices A and B are row-equivalent when there exist a finite number of elementary

matrices such that B = EnEn–1…E2E1A.

Chapter 2: Matrices.

2.4 Elementary Matrices.

p. 33

A square matrix L is lower triangular if all entries above the main diagonal are zero, i.e. lij = 0

whenever i < j. A square matrix U is upper triangular if all entries below the main diagonal are

zero, i.e. uij = 0 whenever i > j. A square matrix D is diagonal if all entries not on the main

diagonal are zero, i.e. dij = 0 whenever i j.

L =

0

00

U =

00

0 D =

00

00

00

Theorem 2.13+ Elementary Matrices are Invertible

If E is an elementary matrix, then E–1

exists and is an elementary matrix. Moreover, if E is lower

triangular, then E–1

is also lower triangular. And if E is diagonal, then E–1

is also diagonal.

Examples:

E1 =

100

001

010

R1 R2 E1–1

=

100

001

010

R1 R2

E2 =

103

010

001

3R1+ R3 R3 E2–1

=

103

010

001

–3R1+ R3 R3

E3 =

6/100

010

001

61 R3 R3 E3

–1 =

600

010

001

6R3 R3

You can check these using matrix multiplication.

E.g.

103

010

001

103

010

001

=

100

010

001

and

103

010

001

103

010

001

=

100

010

001

.

Theorem 2.14 Invertible Matrices are Row-Equivalent to the Identity Matrix

A square matrix A is invertible if and only if it is row equivalent to the identity matrix:

A = En…E2E1I = En…E2E1

if and only if A is a product of elementary matrices.

Proof of “If A is invertible, then A is a product of elementary matrices”:

Since A is invertible, Ax = b has a unique solution (namely, x = A–1

b). But this means that we

can use row operations to reduce [ A | b ] to [ I | c ] (where c = A–1

b, of course). If the

Chapter 2: Matrices.

2.4 Elementary Matrices.

p. 34

corresponding elementary matrices are E1, E2, …, En, then I = EnEn–1…E2E1A so

A = E1–1

E2–1

… En–1–1

En–1

, which is a product of elementary matrices.

Proof of “If A is a product of elementary matrices, then A is invertible”:

If A = E1E2… En–1En, then A–1

exists and A–1

= En–1

En–1–1

…E2–1

E1–1

because every elementary

matrix is invertible.-

Theorem 2.15 Equivalent Conditions for Invertibility

If A is an n n matrix, then the following statements are equivalent.

1) A is invertible.

2) Ax = b has a unique solution for every n1 column matrix b (namely, x = A–1

b).

3) Ax = 0 has only the trivial solution.

4) A is row-equivalent to Inn.

5) A can be written as a product of elementary matrices.

Returning to our example of Gaussian elimination using elementary matrices, we found the

reduced echelon form of the augmented matrix

3963

5121

2310

2100

2310

5121

=

6/100

010

001

103

010

001

100

001

010

3963

5121

2310

Look just at the 33 coefficient matrix instead of the 34 augmented matrix. We have

U

formechelon -row

100

310

121

=

mRows

6/100

010

001

mRowAdds

103

010

001

swaps row

100

001

010

A

963

121

310

The row-echelon form is upper triangular. In general, we may have more than one mRow

(multiply a row by a nonzero constant) elementary matrix, more than one mRowAdd (add a

multiple of one row to another row) elementary matrix, and more than one row swap matrix. The

product of and arbitrary number of row swap matrices is called a permutation matrix P.

U=

mRows

12 FFFn

mRowAdds

12 EEEm PA

Chapter 2: Matrices.

2.4 Elementary Matrices.

p. 35

ngularlower tria

mRowAdds

11

2

1

1

mEEE

diagonal

mRows

11

2

1

1

nFFF U= PA

Lemma The product of diagonal matrices is diagonal. The product of lower triangular matrices is

lower triangular.

LDU = PA

L

EEE m11

21

1

103

010

001

D

FFF n11

21

1

6/100

010

001

U

formechelon -row

100

310

121

=

P

swaps row

100

001

010

A

963

121

310

Theorem LU-Factorization

Every square matrix can be factored as PA = LDU, where P is a permutation matrix, L is lower

triangular with all ones on the main diagonal, D is diagonal, and U is upper triangular with all

ones on the main diagonal.

A variation on this is PA = LU, where this L equals the LD from above, and does not necessarily

have ones on the diagonal.

The PA = LU factorization is the usual method used by computers for solving systems of linear

equations, finding inverse matrices, and calculating determinants (Chapter 3). It is also useful in

proofs.

Chapter 2: Matrices.

2.4 Elementary Matrices.

p. 36

*

Example: Find the PA = LDU factorization of A =

632

101

110

Solution: A =

632

101

110

21 RR

632

110

101

3312 RRR

430

110

101

3323 RRR

100

110

101

22 RR

100

110

101

= U

U

100

110

101

=

F

100

010

001

2

130

010

001

E

1

102

010

001

E

P

100

001

010

A

632

101

110

1

1

102

010

001

E

1

2

130

010

001

E

1

100

010

001

F

U

100

110

101

=

P

100

001

010

A

632

101

110

L

132

010

001

D

100

010

001

U

100

110

101

=

P

100

001

010

A

632

101

110

Chapter 2: Matrices.

2.5 Applications of Matrix Operations.

p. 37

drop

A B

*

2.5 Applications of Matrix Operations.

Objective: Write and use a stochastic (Markov) matrix.

Objective: Use matrix multiplication to encode and decode messages.

Objective: Use matrix algebra to analyze and economic system (Leontief input-output model).

Consider a situation in which members of a population occupy a finite number of states {S1, S2,

…, Sn}. For example, a multinational company has $4 trillion in assets (the population). Some of

the money is in the Americas, some in Asia, and the rest is in Europe (the three states). In a

Markov process, at each discrete step in time, members of the population may move from one

state to another, subject to the following rules:

1) The total number of individuals stays the same.

2) The numbers in each state never become negative.

3) The new state depends only on the current state (history is disregarded).

The behavior of a Markov process is described by a matrix

of transition probabilities (or stochastic matrix or Markov

matrix).

pij is the probability that a member of the population will

change from the j th

state to the i th

state. The rules above

become

1) Each column of the transition matrix adds up to one.

2) Every probability entry is 0 ≤ pij ≤ 1.

Example: Stochastic Matrix. A chemistry course is taught in two sections. Every week,41 of the

students in Section A and31 of the students in Section B drop, and

61 of each section transfer to

the other section. Write the transition matrix. At the beginning of the semester, each section has

144 students. Find the number of students in each section and the number of students who have

dropped after one week and after two weeks.

Solution:

P =

1

01

01

31

41

31

61

61

61

61

41

(d)

(B)

(A)

=

1

0

0

31

41

21

61

61

127

.

P

0

144

144

=

84

96

108

(d)

(B)

(A)

. P

84

96

108

=

143

66

79

(d)

(B)

(A)

to

from

2

1

21

22221

11211

21

nnnnn

n

n

n

S

S

S

ppp

ppp

ppp

P

SSS

61

61

31

004

1

127

21

1

61

Chapter 2: Matrices.

2.5 Applications of Matrix Operations.

p. 38

*--

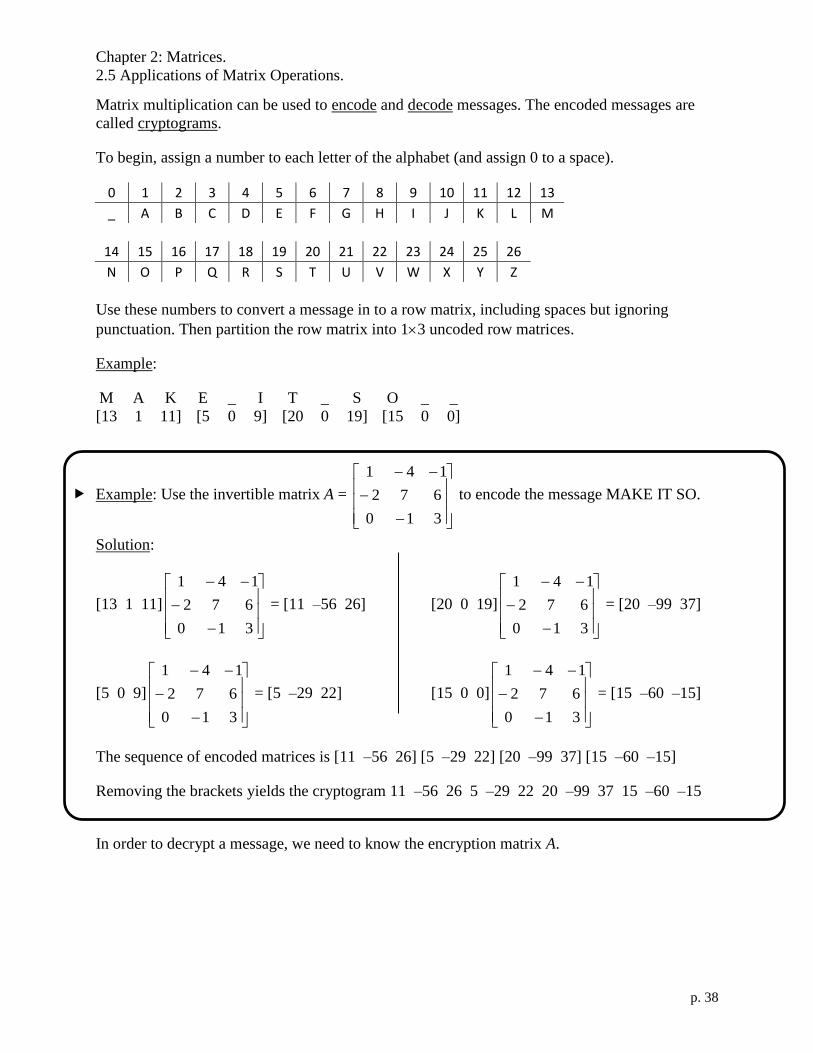

Matrix multiplication can be used to encode and decode messages. The encoded messages are

called cryptograms.

To begin, assign a number to each letter of the alphabet (and assign 0 to a space).

0 1 2 3 4 5 6 7 8 9 10 11 12 13

_ A B C D E F G H I J K L M

14 15 16 17 18 19 20 21 22 23 24 25 26

N O P Q R S T U V W X Y Z

Use these numbers to convert a message in to a row matrix, including spaces but ignoring

punctuation. Then partition the row matrix into 13 uncoded row matrices.

Example:

M A K E _ I T _ S O _ _

[13 1 11] [5 0 9] [20 0 19] [15 0 0]

Example: Use the invertible matrix A =

310

672

141

to encode the message MAKE IT SO.

Solution:

[13 1 11]

310

672

141

= [11 –56 26] [20 0 19]

310

672

141

= [20 –99 37]

[5 0 9]

310

672

141

= [5 –29 22] [15 0 0]

310

672

141

= [15 –60 –15]

The sequence of encoded matrices is [11 –56 26] [5 –29 22] [20 –99 37] [15 –60 –15]

Removing the brackets yields the cryptogram 11 –56 26 5 –29 22 20 –99 37 15 –60 –15

In order to decrypt a message, we need to know the encryption matrix A.

Chapter 2: Matrices.

2.5 Applications of Matrix Operations.

p. 39

*-–-

Example: Use the invertible matrix A =

310

672

141

to decode

–8 26 31 13 –73 50 19 –97 44 16 –64 –16.

Solution:

A–1

=

112

436

171327

[–8 26 31]

112

436

171327

= [2 5 1] [19 –97 44]

112

436

171327

= [19 0 21]

[13 –73 50]

112

436

171327

= [13 0 21] [16 –64 –16]

112

436

171327

= [16 0 0]

[2 5 1] [13 0 21] [19 0 21] [16 0 0]

B E A M _ U S _ U P _ _

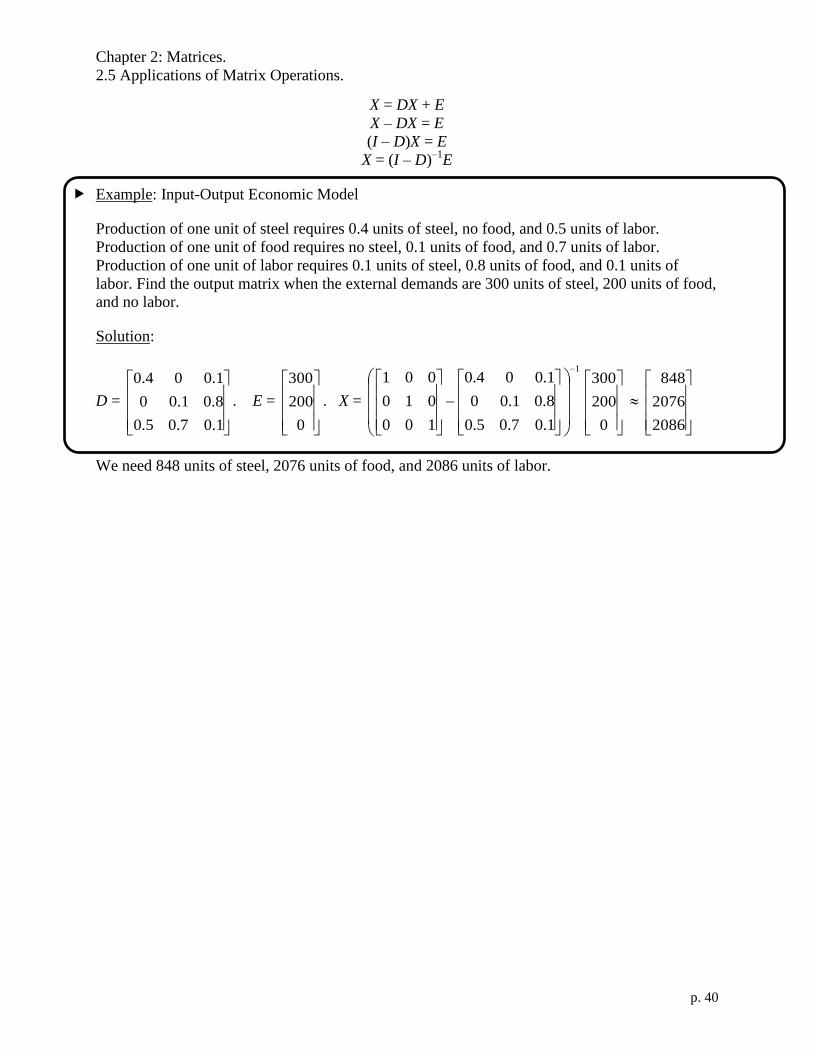

In economics, an input-output model (developed by

Leontief) consists of n different industries In, each of

which needs inputs (e.g. steel, food, labor, …) and has

and output. To produce a unit (e.g. $1 million) of output,

an industry may use the outputs of other industries and of

itself. For example, production of steel may use steel,

food, and labor.

Let dij be the amount of output the industry j needs from industry i to produce one unit of output

per year. (We assume the dij are constant, i.e. fixed prices.) The matrix of these coefficients is

called the input-output matrix or consumption matrix D. A column represents all of the inputs to

a given industry. For this model to work, 0 ≤ dij ≤ 1 and the sum of the entries in each column

must be less than or equal to 1. (Otherwise, it costs more than one unit to produce a unit in that

industry.)

Let xi be the total output matrix of industry i, and X = [xi]. If the economic system is closed (self-

sustaining: total output = “intermediate demand,” i.e. what is needed to produce it), then X = DX.

If the system is open with external demand matrix E (e.g. exports) then X = DX + E.

To find what output matrix is needed to produce a given external demand matrix, we solve

(Input)

Supplier

(Output)User

2

1

21

22221

11211

21

nnnnn

n

n

n

I

I

I

ddd

ddd

ddd

D

III

Chapter 2: Matrices.

2.5 Applications of Matrix Operations.

p. 40

*-–-

X = DX + E

X – DX = E

(I – D)X = E

X = (I – D)–1

E

Example: Input-Output Economic Model

Production of one unit of steel requires 0.4 units of steel, no food, and 0.5 units of labor.

Production of one unit of food requires no steel, 0.1 units of food, and 0.7 units of labor.

Production of one unit of labor requires 0.1 units of steel, 0.8 units of food, and 0.1 units of

labor. Find the output matrix when the external demands are 300 units of steel, 200 units of food,

and no labor.

Solution:

D =

1.07.05.0

8.01.00

1.004.0

. E =

0

200

300

. X =

1

1.07.05.0

8.01.00

1.004.0

100

010

001

0

200

300

2086

2076

848

We need 848 units of steel, 2076 units of food, and 2086 units of labor.

Chapter 3: Determinants.

3.1 The Determinant of a Matrix.

p. 41

Chapter 3: Determinants.

3.1 The Determinant of a Matrix.

Objective: Find the determinant of a 22 matrix.

Objective: Find the minors and cofactors of a matrix.

Objective: Use expansion by cofactors to find the determinant of a matrix.

Objective: Find the determinant of a triangular matrix.

Every square matrix can be associated with a scalar called its determinant. Historically,

determinants were recognized as a pattern of nn systems of linear equations. The system

2222121

1212111

bxaxa

bxaxa

has the solution

21122211

2122211

aaaa

baabx

and

21122211

2112112

aaaa

abbax

.

The determinant of a 11 matrix A = 11a is det(A) = |A| = a11. The |…| symbols mean

determinant, not absolute value.

The determinant of a 22 matrix A =

2221

1211

aa

aa is det(A) = |A| =

2221

1211

aa

aa = a11a22 – a12a21.

Geometrically, the signed area

of a parallelogram with

vertices at (0, 0), (x1, y1), (x2,

y2), and (x1 + x2, y1 + y2) is

A = 22

11

yx

yx

(The area is positive if the angle from

(x1, y1) to (x2, y2) is counterclockwise;

otherwise, the area is negative.)

Proof:

The area A of the parallelogram is

A = area of large rectangle areas of four triangles areas of two small rectangles

= (x1 + x2)(y1 + y2) 21 x1y1

21 x1y1

21 x2y2

21 x2y2 2x2y1

= x1y1 + x1y2 + x2y1 + x2y2 x1y1 x2y2 2x2y1

= x1y2 x2y1 = 22

11

yx

yx

(x2, y2)

(x1, y1)

Chapter 3: Determinants.

3.1 The Determinant of a Matrix.

p. 42

To define the determinant of a square matrix A of order (dimensions) higher than 2, we define

minors and cofactors. The minor Mij of the entry aij is the determinant of the matrix obtained by

deleting row i and column j of A. The cofactor Cij of the entry aij is Cij = (–1)i+j

Mij. Notice that

(–1)i+j

is a “checkerboard” pattern: (–1)i+j

=

Examples: Finding Cofactors. Let A =

Find C21. Solution: C21 = –3332

1312

aa

aa = –a12a33 + a13a32

Find C22. Solution: C22 = +3331

1311

aa

aa = a11a33 – a13a31

The determinant of an nn matrix A (n ≥ 2) is the sum of the entries in the first row of A

multiplied by their respective cofactors.

det(A) =

n

j

jjCa1

11 = a11C11 + a12C12 + … + a1nC1n

Example:

953

786

433

= 395

78

+ 3

93

76 + 4

53

86

= 3(–72 – 35) +3(54 – 21) + 4(30 + 24) = 3(–107) +3(33) +4(54) = –6

Theorem 3.1 Expansion by Cofactors

Let A be a square matrix of order n. Then the determinant of A is given by an expansion in any

row i

det(A) =

n

j

ijijCa1

= ai1Ci1 + ai2Ci2 + … + ainCin

and also by an expansion in any column j

det(A) =

n

i

ijijCa1

= a1jC1j + a2jC2j + … + anjCnj

Chapter 3: Determinants.

3.1 The Determinant of a Matrix.

p. 43

When expanding, you don’t need to find the cofactors of zero entries, because aijCij = (0)Cij = 0.

The definition of the determinant is inductive, because it uses the determinant of a matrix of

order n – 1 to define the determinant of a matrix of order n.

Example: Expanding by Cofactors to Find a Determinant

= = –1 + 3(– )

= –1(2 +7 ) +3(–2 ) = –1(2(3) + 7(–6)) + 3(–2)(0) = –(6 – 42) = 36

To find a determinant using Mathematica, type Det[a]

(also on Basic Math Assistant, More drop-down menu)

To find a determinant on the TI-89, type

Matrix

det(

A

To find a determinant of a 33 matrix, you can also use the following shortcut. Copy Columns 1

and 2 into Columns 4 and 5. To calculate the determinant, add and subtract the indicated

products.

333231

232221

131211

aaa

aaa

aaa

3231

2221

1211

333231

232221

131211

aa

aa

aa

aaa

aaa

aaa

333231

232221

131211

aaa

aaa

aaa

= a11a22a33 + a12a23a31 + a13a21a32 – a31a22a13 – a32a23a11 – a33a21a12

Example:

851

640

311

51

40

11

851

640

311

so

851

640

311

= 32 + 6 + 0 – 12 – 30 – 0 = –4

subtract

add

32 6 0

12 30 0

Chapter 3: Determinants.

3.1 The Determinant of a Matrix.

p. 44

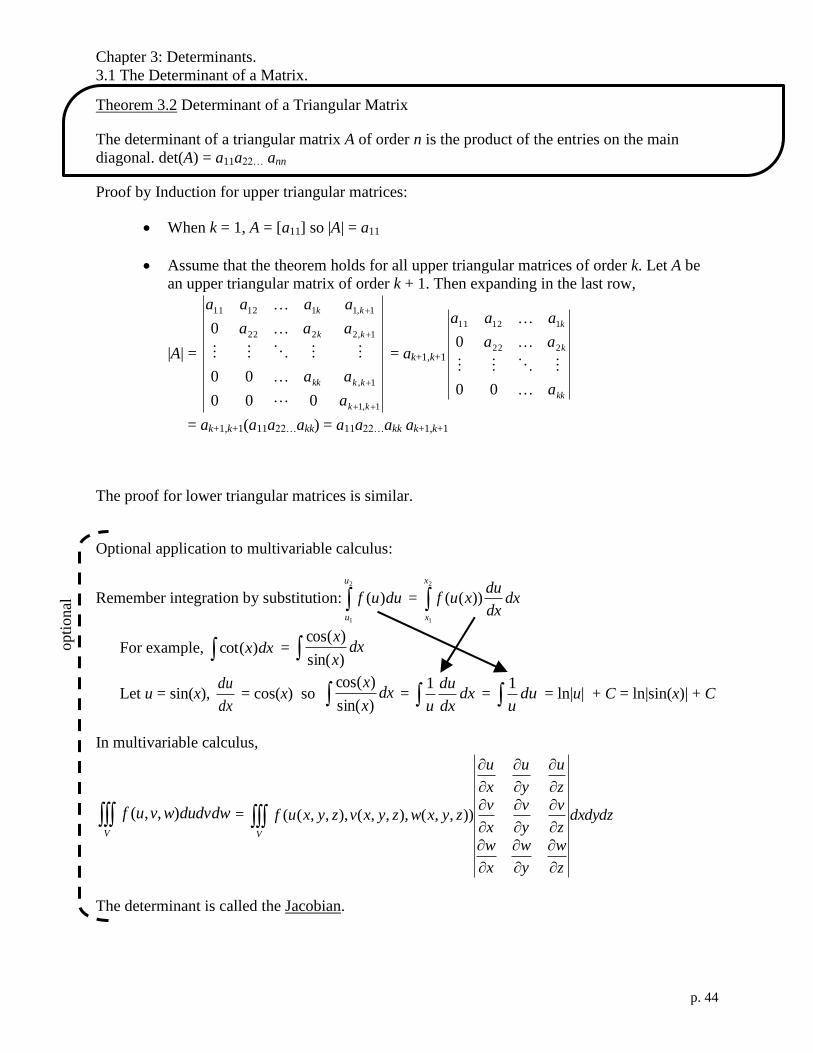

Theorem 3.2 Determinant of a Triangular Matrix

The determinant of a triangular matrix A of order n is the product of the entries on the main

diagonal. det(A) = a11a22… ann

Proof by Induction for upper triangular matrices:

When k = 1, A = [a11] so |A| = a11

Assume that the theorem holds for all upper triangular matrices of order k. Let A be

an upper triangular matrix of order k + 1. Then expanding in the last row,

|A| =

1,1

1,

1,2222

1,111211

000

00

0

kk

kkkk

kk

kk

a

aa

aaa

aaaa

= ak+1,k+1

kk

k

k

a

aa

aaa

00

0 222

11211

= ak+1,k+1(a11a22…akk) = a11a22…akk ak+1,k+1

The proof for lower triangular matrices is similar.

Optional application to multivariable calculus:

Remember integration by substitution: 2

1

)(

u

u

duuf = 2

1

))((

x

x

dxdx

duxuf

For example, dxx)cot( = dxx

x

)sin(

)cos(

Let u = sin(x), dx

du = cos(x) so dx

x

x

)sin(

)cos( = dx

dx

du

u

1 = du

u

1 = ln|u| + C = ln|sin(x)| + C

In multivariable calculus,

V

dudvdwwvuf ),,( =

V

dxdydz

z

w

y

w

x

w

z

v

y

v

x

v

z

u

y

u

x

u

zyxwzyxvzyxuf )),,(),,,(),,,((

The determinant is called the Jacobian.

opti

onal

Chapter 3: Determinants.

3.2 Determinants and Elementary Operations.

p. 45

3.2 Determinants and Elementary Operations.

Objective: Use elementary row operations to evaluate a determinant.

Objective: Use elementary column operations to evaluate a determinant.

Recognize conditions that yield zero determinants.

In practice, we rarely evaluate determinants using expansion by cofactors. The properties of

determinants under elementary operations provide a much quicker way to evaluate determinants.

Theorem 3.9 det(AT) = det(A). [Proof is in Section 3.4]

Theorem 3.3 Elementary Row (Column) Operations and Determinants.

Let A and B be nn square matrices.

a) When B is obtained from A by swapping two rows (two columns) of A, det(B) = –det(A).

b) When B is obtained from A by adding a multiple of one row of A to another row of A (or one

column of A to another column of A), det(B) = det(A).

c) When B is obtained from A by multiplying of a row (column) of A by a nonzero constant c,

det(B) = c det(A).

Theorem 3.4 Conditions that Yield a Zero Determinant.

If A is an nn square matrix and any one of the following conditions is true, then det(A) = 0

a) An entire row (or an entire column) consists of zeros.

b) Two rows (or two columns) are equal.

c) One row is a multiple of another row (or one column is a multiple of another column).

Proof by Induction of 3.3a (for rows):

When k = 2, A =

2221

1211

aa

aa and B =

1211

2221

aa

aa so

det(B) = a21a12 – a22a11 = –(a11a22 – a12a21) = –det(A)

Assume that the theorem holds for all matrices of order k. Let A be a matrix of order k

+ 1 and B be a matrix obtained by swapping two rows of A. To find det(A) and det(B),

expand in any row other than the swapped rows. The respective cofactors are

opposites, because they come from kk matrices that have two rows swapped. Thus,

det(B) = –det(A).

Proof of 3.4a (for rows): Suppose that row i of A is all zeroes. Expand by cofactors in row i.

det(A) =

n

j

ijijCa1

=

n

j

ijC1

0 = 0

Chapter 3: Determinants.

3.2 Determinants and Elementary Operations.

p. 46

Proof of 3.4b: Let B be the matrix obtained from A by swapping the two identical rows

(columns) of A, so det(B) = –det(A). But B = A, so det(A) = –det(A) so det(A) = 0.

Proof of 3.3b (for rows): Suppose B is obtained from A by adding c times row k to row i. Expand

by cofactors in row i. Note that the cofactors of Cij are the same for matrices A and B,

because the matrices are the same everywhere except row i.

det(B) =

n

j

ijijCb1

=

n

j

ijijkj Caca1

)( =

n

j

ijkjCac1

+

n

j

ijijCa1

= c·0 + det(A) = det(A).

because

n

j

ijkjCa1

is the determinant of a matrix with two identical rows (row k and row i).

See Theorem 3.4b.

Another way of writing this is

nnn

inknik

knk

n

aa

acaaca

aa

aa

1

11

1

111

)()(

= c

nnn

knk

knk

n

aa

aa

aa

aa

1

1

1

111

+

nnn

ini

knk

n

aa

aa

aa

aa

1

1

1

111

= c·0 + det(A) = det(A).

Proof of 3.3c (for rows): Suppose B is obtained from A by multiplying row i by a nonzero scalar

c. Expand by cofactors in row i.

det(B) =

n

j

ijijCb1

=

n

j

ijijCca1

= c

n

j

ijijCa1

= c det(A)

Proof of 3.4c: Suppose B is a matrix with two equal rows (or two equal columns), and A is

obtained from B by multiplying one of those rows (or columns) by a nonzero scalar c. Using

3.3c on that row (or column), det(A) = c det(B). Using 3.4b, det(B) = 0. Thus, det(A) = 0.

Geometrically, the signed area of a parallelogram with edges from

(0, 0) to (x1, y1) and from (0, 0) to (x2, y2) has the same properties

as 22

11

yx

yx when you perform an elementary row operation. Also,

the signed area of a parallelepiped with edges from (0, 0) to (x1, y1,

z1), from (0, 0) to (x2, y2, z2), and from (0, 0) to (x3, y3, z3) has the

same properties as

333

222

111

zyx

zyx

zyx

when you perform an elementary

row operation.

Chapter 3: Determinants.

3.2 Determinants and Elementary Operations.

p. 47

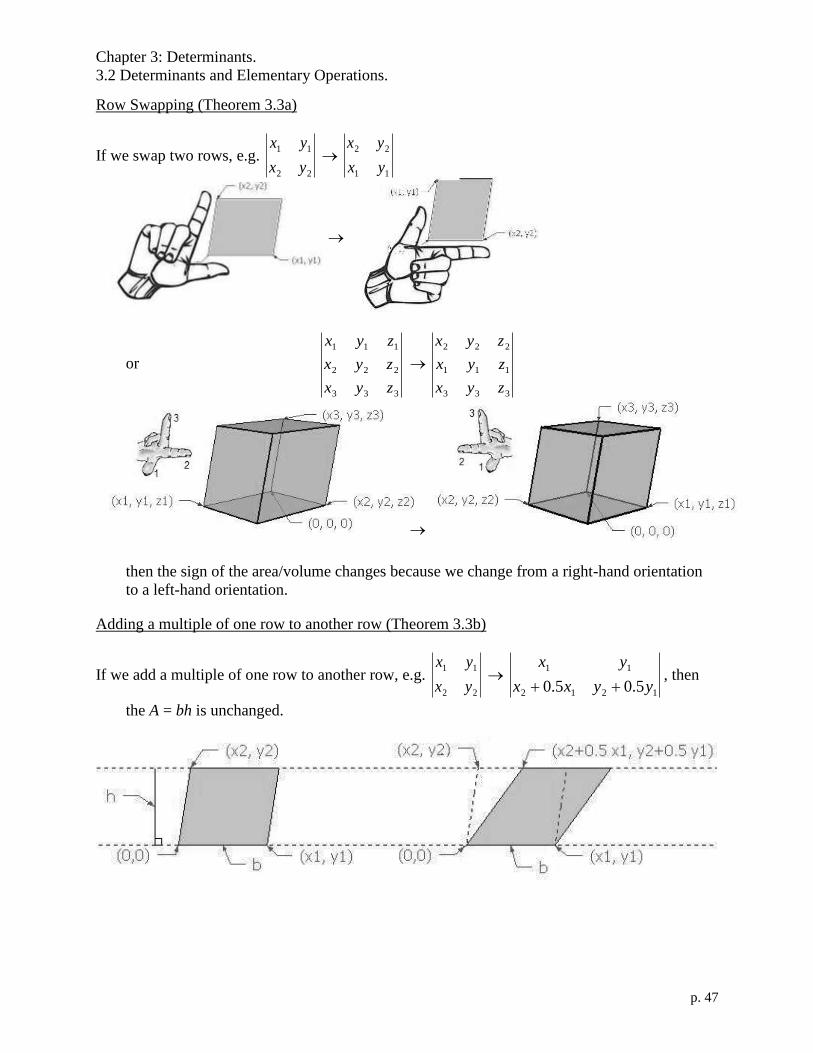

Row Swapping (Theorem 3.3a)

If we swap two rows, e.g. 22

11

yx

yx

11

22

yx

yx

or

333

222

111

zyx

zyx

zyx

333

111

222

zyx

zyx

zyx

then the sign of the area/volume changes because we change from a right-hand orientation

to a left-hand orientation.

Adding a multiple of one row to another row (Theorem 3.3b)

If we add a multiple of one row to another row, e.g. 22

11

yx

yx

1212

11

5.05.0 yyxx

yx

, then

the A = bh is unchanged.

Chapter 3: Determinants.

3.2 Determinants and Elementary Operations.

p. 48

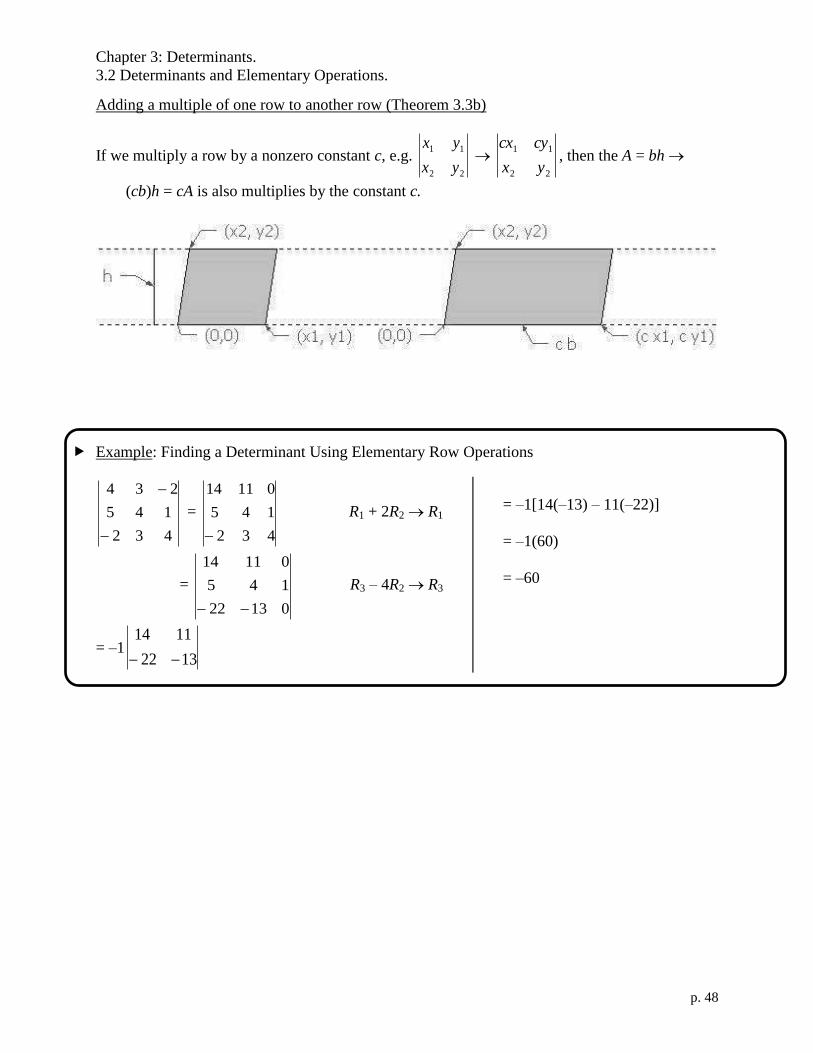

Adding a multiple of one row to another row (Theorem 3.3b)

If we multiply a row by a nonzero constant c, e.g. 22

11

yx

yx

22

11

yx

cycx, then the A = bh

(cb)h = cA is also multiplies by the constant c.

Example: Finding a Determinant Using Elementary Row Operations

432

145

234

=

432

145

01114

R1 + 2R2 R1

=

01322

145

01114

R3 – 4R2 R3

= –11322

1114

= –1[14(–13) – 11(–22)]

= –1(60)

= –60

Chapter 3: Determinants.

3.2 Determinants and Elementary Operations.

p. 49

Example: Finding a Determinant Using Elementary Column Operations

2159

3157

5642

4331

=

______9

______7

______2

0001

44

33

212

____

____

3

CC

CC

CCC

= (__)

______9

______7

____12

0001

22___ CC

= (__)

______9

______7

0012

0001

4

3

__________

__________

C

C

= (__)(__) ______

______

001

= (__)(__)(__) ____

____

=

Chapter 3: Determinants.

3.3 Properties of Determinants.

p. 51

3.3 Properties of Determinants.

Objective: Find the determinant of a matrix product and of a scalar multiple of a matrix.

Find the determinant of an inverse matrix and recognize equivalent conditions for a nonsingular

matrix.

Find the determinant of the transpose of a matrix.

Theorem 3.5 Determinant of a Matrix Product

If A and B are square matrices of the same order, then det(AB) = det(A) det(B).

Proof: To begin, let E be an elementary matrix. By Thm 2.12, EB is the matrix obtained from

applying the corresponding row operation to B. By Thm. 3.3,

det(EB) =

)det(

)det(

)det(

Bc

B

B

if the row operation is

cconstant nonzero aby row a gmultiplyin

another torow one of multiple a adding

rows twoexchanging

Also by Thm 3.3,

det(E) = det(EI) =

c

1

1

if the row operation is

cconstant nonzero aby row a gmultiplyin

another torow one of multiple a adding

rows twoexchanging

Thus, det(EB) = det(E) det(B). This can be generalized by induction to conclude that

|Ek…E2E1B| = |Ek| |…| |E2| |E1| |B| where the Ei are elementary matrices. If A is nonsingular,

then by Thm. 2.14, it can be written as the product A = Ek…E2E1 so |AB| = |A| |B|.

If A is singular, then A is row-equivalent to a matrix with an entire row of zeroes (for example,

the reduced row echelon form). From Thm 3.4, we know |A| = 0. Moreover, because A is

singular, it follows that AB must be singular. (Proof by contradiction: if AB were nonsingular,

then A[B(AB)-1

] = I would show that A is not singular, because A–1

= B(AB)-1

.) Therefore, |AB|

= 0 = |A| |B|.

Comment on Proof by Contradiction: “P implies Q” is equivalent to “not Q implies not P.”

Theorem 3.6 Determinant of a Scalar Multiple of a Matrix

If A is a square matrix of order n and c is a scalar, then det(cA) = cndet(A).

Proof: Apply Property (c) of Thm. 3.3 to each of the n rows of A to obtain n factors of c.

Theorem 3.7 Determinant of an Invertible Matrix

A square matrix A is invertible (nonsingular) if and only if det(A) 0.

Proof: On the one hand, if A is invertible, then AA–1

= I, so . |A| |A–1

| = | I | = 1. Therefore, |A| 0.

On the other hand, assume det(A) 0. Then use Gauss-Jordan elimination to find the reduced

row-echelon form R. Since R is in reduced row-echelon form, it is either the identity matrix or

Chapter 3: Determinants.

3.3 Properties of Determinants.

p. 52

it must have at least one row of all zeroes. The second case is not possible: if R had a row of all

zeroes, then det(R) = 0, but then det(A) = 0 (which contradicts the assumption). Therefore, A is

row-equivalent to R = I, so A is invertible.

Theorem 3.8 Determinant of an Inverse Matrix

If A is an invertible matrix, then det (A–1

) = )det(

1

A

Proof: AA–1

= I, so . |A| |A–1

| = | I | = 1 and |A| 0, so |A–1

| =||

1

A.

Equivalent Conditions for a Nonsingular nn Matrix (Summary)

1) A is invertible.

2) Ax = b has a unique solution for every n1 column matrix b.

3) Ax = 0 has only the trivial solution for the n1 column matrix 0.

4) A is row-equivalent to I.

5) A can be written as a product of elementary matrices.

6) det(A) 0.

Theorem 3.9 Determinant of a the Transpose of a Matrix

If A is a square matrix, then det(AT) = det(A).

Proof: Let A be a square matrix of order n.

From Section 2.4, we know that A can be factored as PA = LDU, where P is a permutation

matrix, L is lower triangular with all ones on the main diagonal, D is diagonal, and U is upper

triangular with all ones on the main diagonal.

L is obtained from I by adding a multiple of the rows containing the diagonal ones to the rows

below the diagonal, so

|L| = |I | = 1

by Thm. 3.3b. Likewise, U is obtained from I by adding a multiple of the rows containing the

diagonal ones to the rows above the diagonal, so

|U| = |I | = 1

by Thm. 3.3b.

By Thm. 3.2,

|D| = d11d22… dnn

i.e. the product of its diagonal elements.

P is a product of elementary row-swap matrices, each of which has determinant –1. So |P| is

the product of some number of –1’s.

|P| = 1 if the number of row swaps is even;

|P| = –1 if the number of row swaps is odd.

Chapter 3: Determinants.

3.3 Properties of Determinants.

p. 53

Let e1 =

0

0

1

, e2 =

0

1

0

, …, en =

1

0

0

be n1 matrices. Then P =

T

i

T

i

T

i

ne

e

e

2

1

where i1, i2, …, in is

some permutation of 1, 2, …, n. Now PT =

niii eee 21

, so

PPT =

nnnn

n

n

i

T

ii

T

ii

T

i

i

T

ii

T

ii

T

i

i

T

ii

T

ii

T

i

eeeeee

eeeeee

eeeeee

21

22212

12111

=

100

010

001

= I,

and by Thm. 3.5, det(P) det(PT

) = det(PPT

) = det(I) = 1.

Then either det(P) = 1 so det(PT) = 1, or det(P) = –1 so det(P

T) = –1. In both cases,

det(P) = det(PT).

So we have PA = LDU which gives us |P| |A| = |L| |D| |U| = (1) |D| (1) =|D|, so

|A| = ||

||

P

D.

Taking the transpose, we have ATP

T = U

TD

TL

T which gives us |A

T| |P

T| = |U

T| |D

T| |L

T|.

Now |PT| = |P|; |D

T| = |D| because

DT = D

since D is diagonal;

|LT| = 1

because LT is upper triangular with all ones on the main diagonal; and

|UT| = 1

because UT is lower triangular with all ones on the main diagonal.

Thus, |AT| |P

T| = |U

T| |D

T| |L

T| becomes |A

T| |P

T| = (1) |D| (1), so

|AT| =

||

||TP

D =

||

||

P

D = |A|.

Chapter 3: Determinants.

3.4 Applications of Determinants.

p. 55

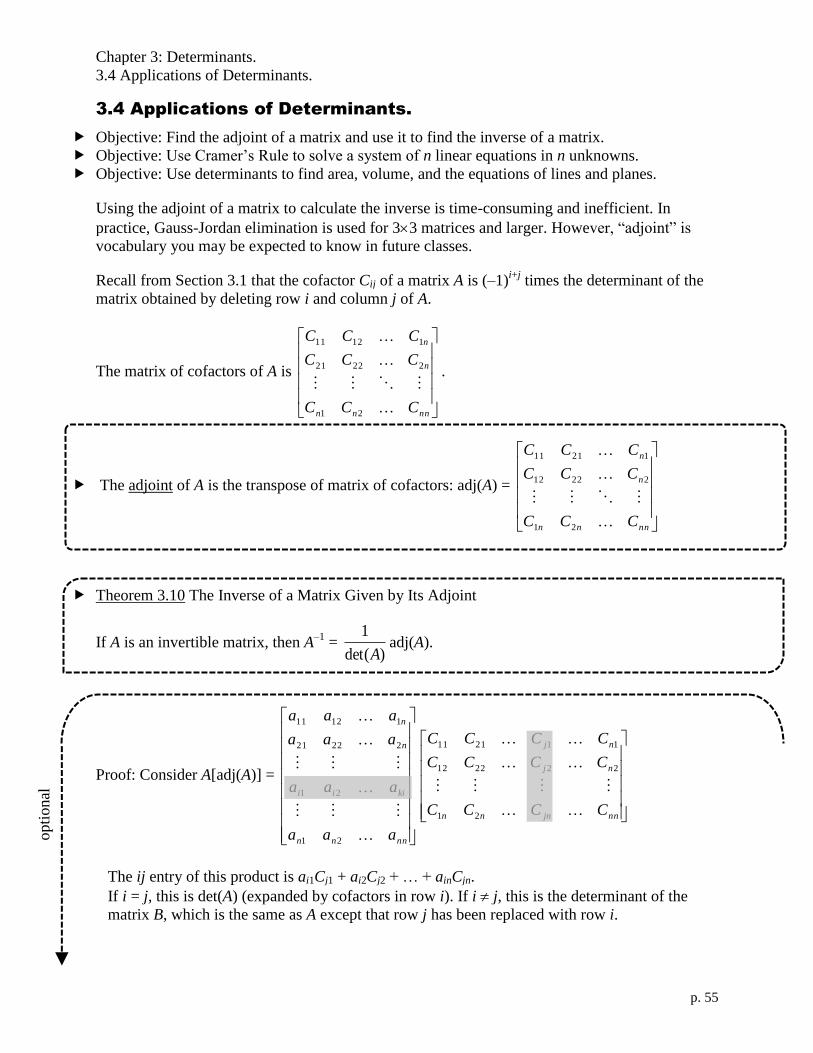

3.4 Applications of Determinants.

Objective: Find the adjoint of a matrix and use it to find the inverse of a matrix.

Objective: Use Cramer’s Rule to solve a system of n linear equations in n unknowns.

Objective: Use determinants to find area, volume, and the equations of lines and planes.

Using the adjoint of a matrix to calculate the inverse is time-consuming and inefficient. In

practice, Gauss-Jordan elimination is used for 33 matrices and larger. However, “adjoint” is

vocabulary you may be expected to know in future classes.

Recall from Section 3.1 that the cofactor Cij of a matrix A is (–1)i+j

times the determinant of the

matrix obtained by deleting row i and column j of A.

The matrix of cofactors of A is

nnnn

n

n

CCC

CCC

CCC

21

22221

11211

.

The adjoint of A is the transpose of matrix of cofactors: adj(A) =

nnnn

n

n

CCC

CCC

CCC

21

22212

12111

Theorem 3.10 The Inverse of a Matrix Given by Its Adjoint

If A is an invertible matrix, then A–1

=)det(

1

Aadj(A).

Proof: Consider A[adj(A)] =

nnnn

kiii

n

n

aaa

aaa

aaa

aaa

21

21

22221

11211

nnjnnn

nj

nj

CCCC

CCCC

CCCC

21

222212

112111

The ij entry of this product is ai1Cj1 + ai2Cj2 + … + ainCjn.

If i = j, this is det(A) (expanded by cofactors in row i). If i j, this is the determinant of the

matrix B, which is the same as A except that row j has been replaced with row i.

opti

onal

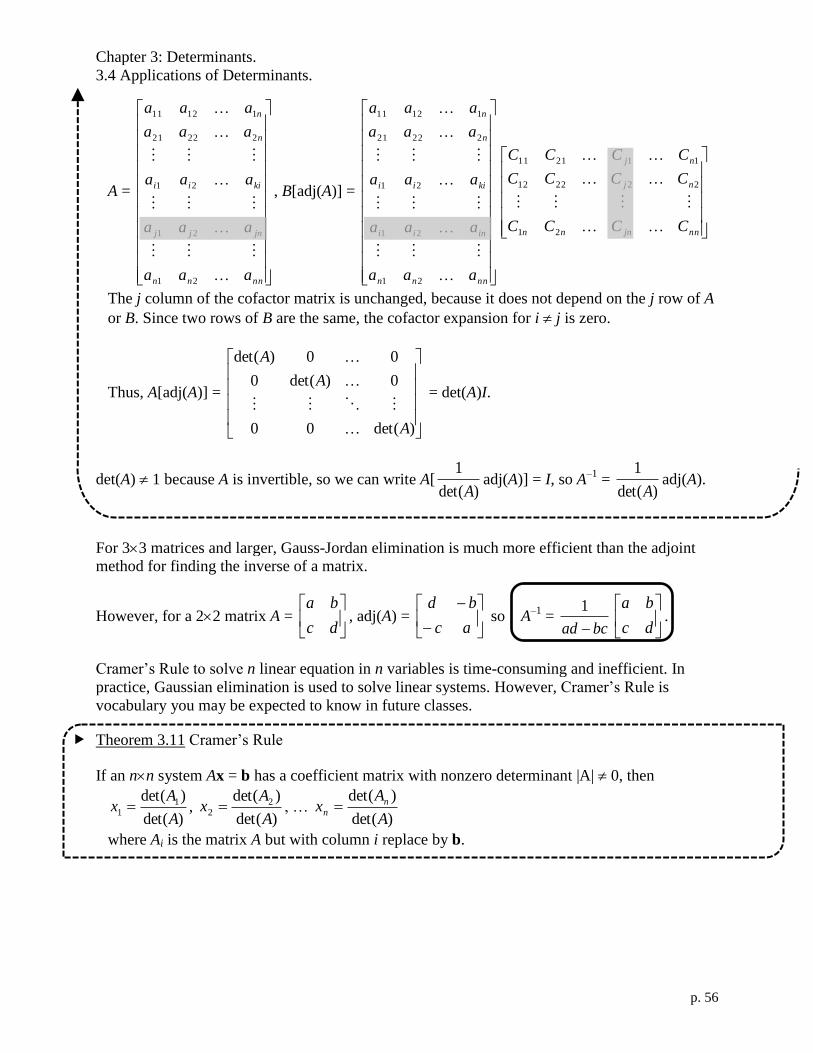

Chapter 3: Determinants.

3.4 Applications of Determinants.

p. 56

A =

nnnn

jnjj

kiii

n

n

aaa

aaa

aaa

aaa

aaa

21

21

21

22221

11211

, B[adj(A)] =

nnnn

inii

kiii

n

n

aaa

aaa

aaa

aaa

aaa

21

21

21

22221

11211

nnjnnn

nj

nj

CCCC

CCCC

CCCC

21

222212

112111

The j column of the cofactor matrix is unchanged, because it does not depend on the j row of A

or B. Since two rows of B are the same, the cofactor expansion for i j is zero.

Thus, A[adj(A)] =

)det(00

0)det(0

00)det(

A

A

A

= det(A)I.

det(A) 1 because A is invertible, so we can write A[)det(

1

Aadj(A)] = I, so A

–1 =

)det(

1

Aadj(A).

For 33 matrices and larger, Gauss-Jordan elimination is much more efficient than the adjoint

method for finding the inverse of a matrix.

However, for a 22 matrix A =

dc

ba, adj(A) =

ac

bd so A

–1 =

bcad

1

dc

ba.

Cramer’s Rule to solve n linear equation in n variables is time-consuming and inefficient. In

practice, Gaussian elimination is used to solve linear systems. However, Cramer’s Rule is

vocabulary you may be expected to know in future classes.

Theorem 3.11 Cramer’s Rule

If an nn system Ax = b has a coefficient matrix with nonzero determinant |A| 0, then

)det(

)det( 11

A

Ax ,

)det(

)det( 22

A

Ax , …

)det(

)det(

A

Ax n

n

where Ai is the matrix A but with column i replace by b.

Chapter 3: Determinants.

3.4 Applications of Determinants.

p. 57

Proof:

nx

x

x

2

1

x = A–1

b = )det(

1

Aadj(A)b =

)det(

1

A

nnnn

n

n

CCC

CCC

CCC

21

22212

12111

nb

b

b

2

1

so xi = )det(

1

A(b1C1i + b2C2i + … + bnCni). The sum in parentheses is the cofactor expansion of

det(Ai), so xi = )det(

)det(

A

Ai

Example: Solve 1543

1021

yx

yx using Cramer’s Rule.

Solution: x =

43

21

415

210

= 2

10

= –5; y =

43

21

153

101

= 2

15

=

2

15

Area, Volume and Equations of Lines and Planes:

We already know that the signed area of a parallelogram

is given by a 22 determinant (Section 3.1). A = 22

11

yx

yx

The signed area of a triangle with vertices (x1, y1), (x2, y2), and (x3, y3) is A =

1

1

1

33

22

11

yx

yx

yx

Proof:

The area of a triangle is half of the area of a

parallelogram. So the area of the triangle we want is

21

pos

33

22

yx

yx+

21

neg

11

33

yx

yx+

21

neg

22

11

yx

yx=

1

1

1

2

1

33

22

11

yx

yx

yx

For a triangle the signed area is A =

1

1

1

2

1

33

22

11

yx

yx

yx

If the vertices (x1, y1), (x2, y2), and (x3, y3) are ordered clockwise then the area is positive;

otherwise, it is negative. (The homework asks for the absolute value of the area.)

(x2, y2) (x1, y1)

(x3, y3)

Chapter 3: Determinants.

3.4 Applications of Determinants.

p. 58

The area of the triangle is zero if and only if the three points are collinear.

(x1, y1), (x2, y2), and (x3, y3) are collinear if and only if

1

1

1

33

22

11

yx

yx

yx

= 0

The equation of a line through distinct points (x1, y1) and (x2, y2) is

1

1

1

22

11

yx

yx

yx

= 0

Similarly to the two-dimensional case of a parallelogram,