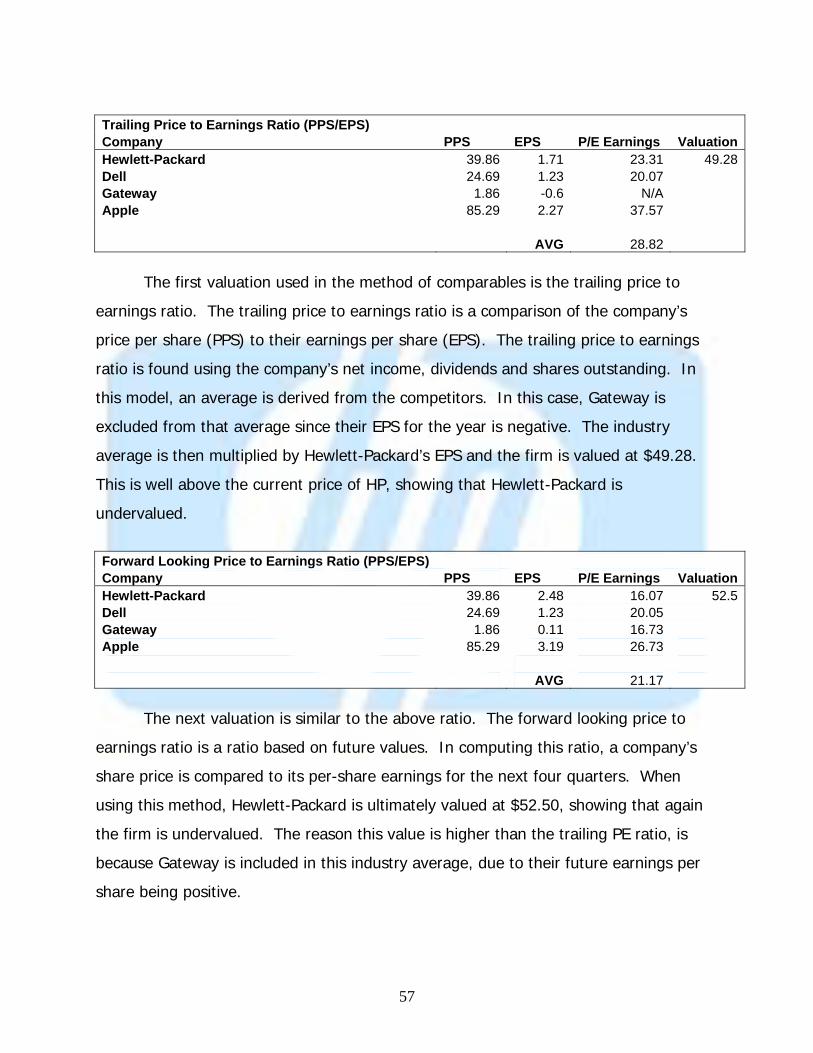

Hewlett-Packard Co. Equity and Valuation...

87

Hewlett-Packard Co. Equity and Valuation Analysis Valued at November 1, 2006 Jessica Myhre: [email protected] Chad Stephenson: [email protected] Lindsey Yantis: [email protected] Greg Zang: [email protected]

-

Upload

truongtuong -

Category

Documents

-

view

249 -

download

1

Transcript of Hewlett-Packard Co. Equity and Valuation...

Hewlett-Packard Co. Equity and Valuation Analysis

Valued at November 1, 2006

Jessica Myhre: [email protected] Chad Stephenson: [email protected]

Lindsey Yantis: [email protected] Greg Zang: [email protected]

Table of Contents

Executive Summary 3 Business/Industry Analysis 5 Accounting Analysis 16 Company Comparisons 24 Financial Analysis 28 Forecasted Financials 51 Valuation Analysis 56 Method of Comparables 56 Cost of Capital 59 Intrinsic Valuations 61 Conclusion 68 Appendices Forecasting (A-D) 69

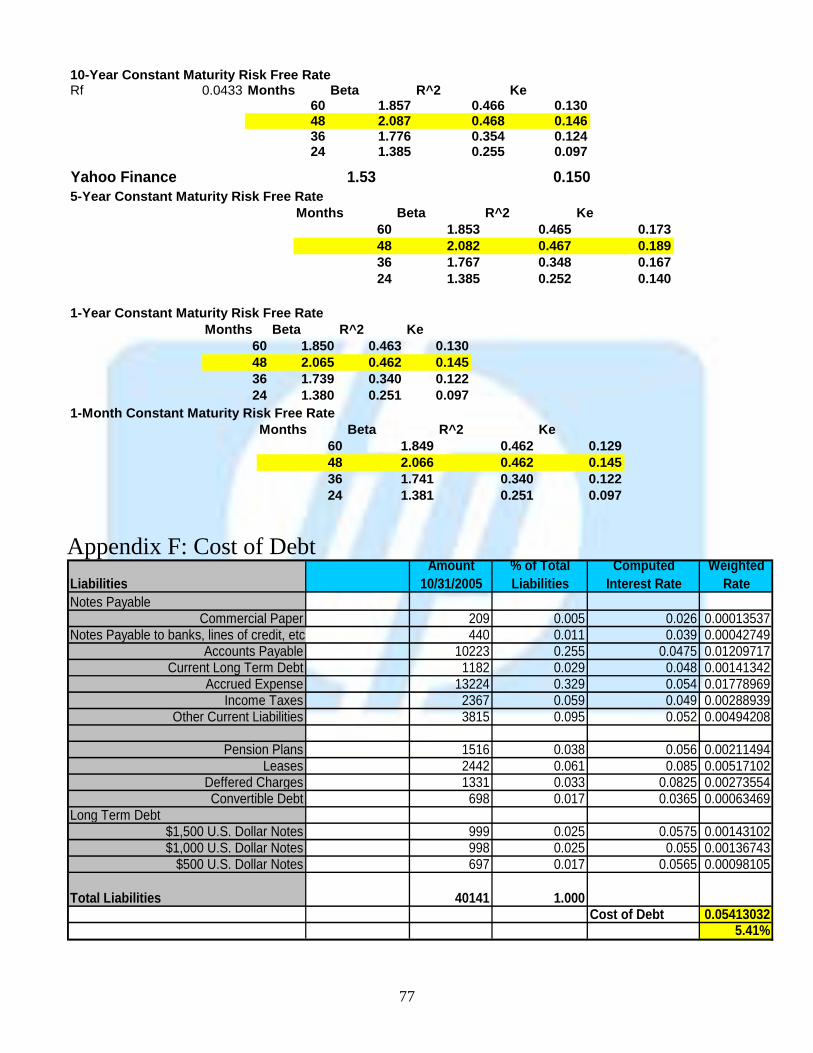

CAPM/Cost of Capital (E) 76 Cost of Debt (F) 77

Intrinsic Valuations (G-K) 78 References 83

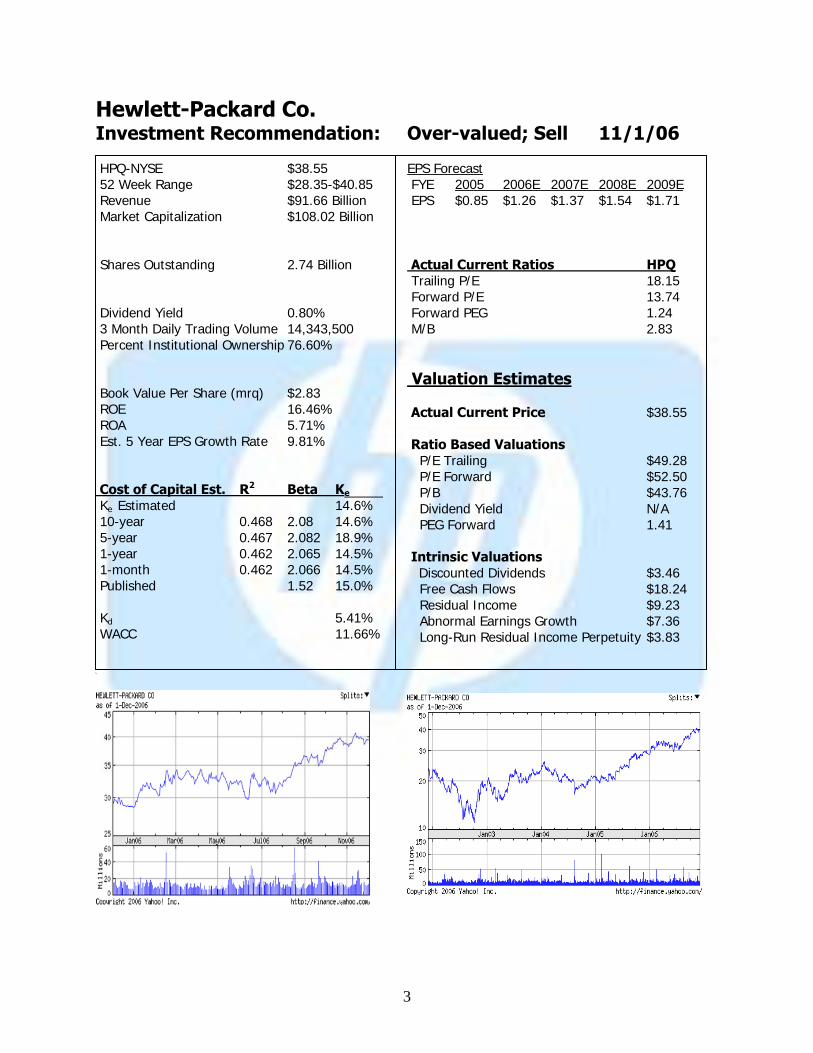

3

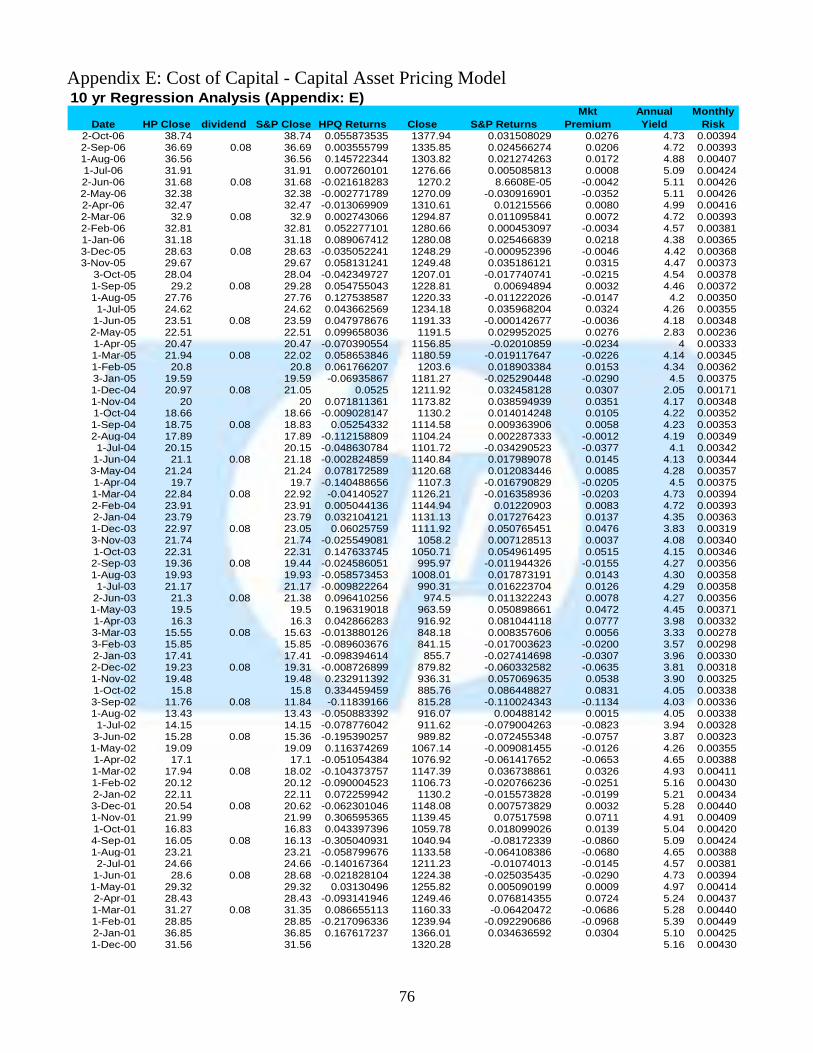

Hewlett-Packard Co. Investment Recommendation: HPQ-NYSE $38.55 52 Week Range $28.35-$40.85 Revenue $91.66 Billion Market Capitalization $108.02 Billion Shares Outstanding 2.74 Billion Dividend Yield 0.80% 3 Month Daily Trading Volume 14,343,500 Percent Institutional Ownership 76.60% Book Value Per Share (mrq) $2.83 ROE 16.46% ROA 5.71% Est. 5 Year EPS Growth Rate 9.81% Cost of Capital Est. R2 Beta Ke Ke Estimated 14.6% 10-year 0.468 2.08 14.6% 5-year 0.467 2.082 18.9% 1-year 0.462 2.065 14.5% 1-month 0.462 2.066 14.5% Published 1.52 15.0% Kd 5.41% WACC 11.66%

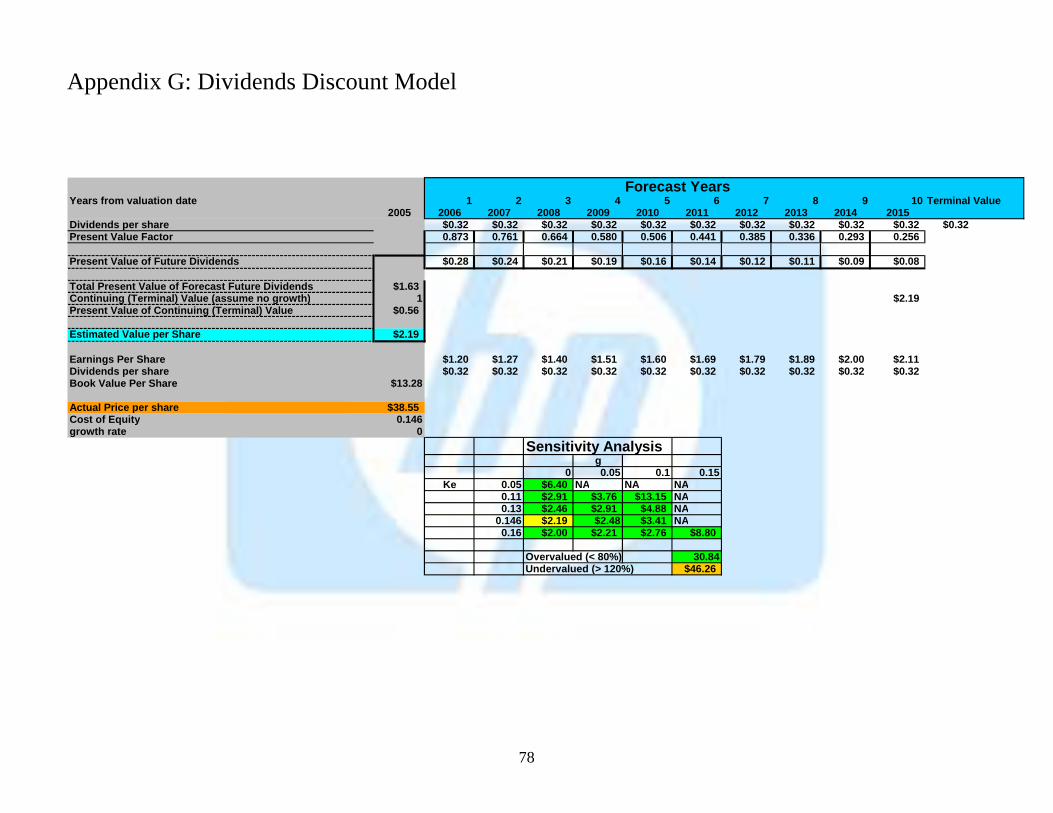

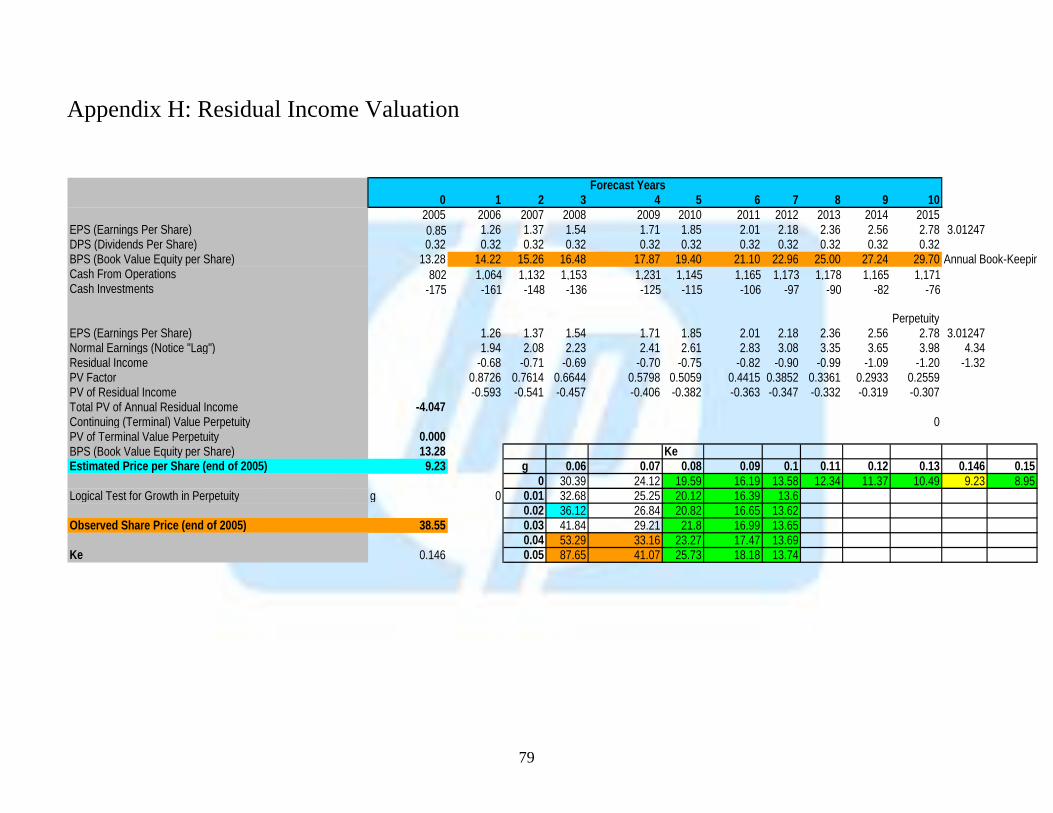

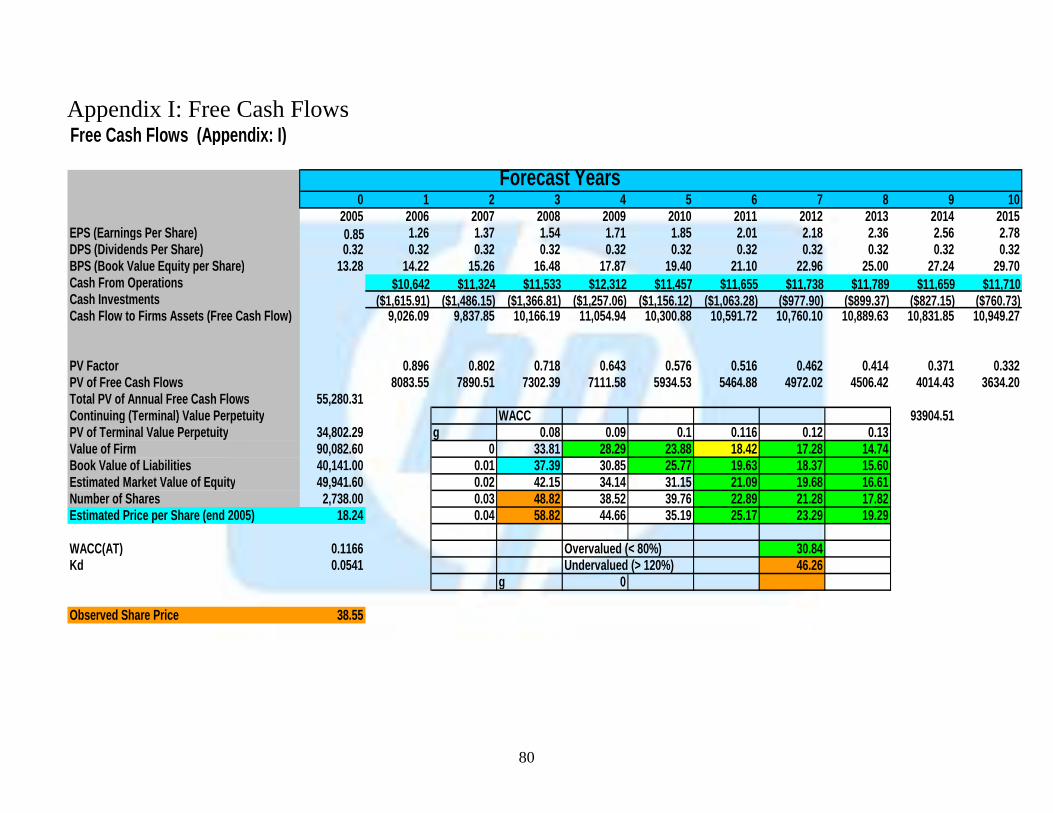

Over-valued; Sell 11/1/06 EPS Forecast FYE 2005 2006E 2007E 2008E 2009E EPS $0.85 $1.26 $1.37 $1.54 $1.71 Actual Current Ratios HPQ Trailing P/E 18.15 Forward P/E 13.74 Forward PEG 1.24 M/B 2.83 Valuation Estimates Actual Current Price $38.55 Ratio Based Valuations P/E Trailing $49.28 P/E Forward $52.50 P/B $43.76 Dividend Yield N/A PEG Forward 1.41 Intrinsic Valuations Discounted Dividends $3.46 Free Cash Flows $18.24 Residual Income $9.23 Abnormal Earnings Growth $7.36 Long-Run Residual Income Perpetuity $3.83

4

Executive Summary

Hewlett-Packard is one of the world’s leaders in providing solutions and services

to individual consumers and businesses through information technology. They are

classified in the Diversified Computer Systems Industry. Hewlett Packard has made a

place in the industry by continuing to deliver quality products with cutting edge

technology, or differentiation. Their products have been set as the industry standard.

They have many different competitors including, Apple, Dell, IBM, Cannon, and

Gateway. The threat of new competitors in their market is low due to the many

barriers of entry. When looking at the possibility of having substitute products in the

market, there is little threat due to the inability to substitute computers and other

technology devices. Because of this, buyers have little bargaining power but suppliers

have high bargaining power. This can be attributed to the demand for technology.

Hewlett-Packard seems to be an honest company when it comes to their

financials. They remain to have conservative accounting policies amidst the SEC probe

and upper management leak. Though their reputation may have been tarnished

through this leak, Hewlett-Packard’s accounting practices seem to be stable with no

signs of manipulation. In Hewlett- Packard’s annual 10-K report, they disclose almost

all possible information, negative and positive. This lowers any concern for possibility

of manipulation.

Next in the analysis was studying Hewlett-Packard’s annual report with

computing their core financial ratios. By computing financial ratios, it is easier to

analyze the firm’s financial performance in relation to the industry. Hewlett Packard’s

overall liquidity is in the lower end of the spectrum, as well as their profitability. This

can be contributed to the high amount of research and development costs Hewlett-

Packard incurs each year to remain the industry leader in technology. In terms of

capital structure, HP also has unfavorable ratios. This is a result of stockholder’s high

confidence that Hewlett-Packard will remain a profitable company and not go bankrupt.

To have a better understanding of where Hewlett Packard will be in the years to

come, it is necessary to forecast the company’s financial statements over the next ten

5

years. With the assumption that there will be no unforeseen abnormalities, it is

believed that Hewlett Packard will grow at a steady, constant rate. These forecasts

must be as accurate as possible to help determine the value of the company.

After forecasting financial statements as accurately as possible, it was then

necessary to run different valuation methods for Hewlett-Packard. These included

discount dividends, abnormal earnings growth, residual income, and discounted cash

flows.

With this thorough evaluation, we strongly believe Hewlett Packard’s stock to be

overvalued by the market. All of our valuation models supported this showing nearly

75% of the actual stock price of $38.55. Based on our in-depth valuations of Hewlett-

Packard, we find their stock HPQ to be overvalued and recommend selling.

Company Profile

Hewlett-Packard was originated in 1939 by William R. Hewlett and David

Packard. Currently, the company is headquartered in Palo Alto, California.2 Hewlett-

Packard presently operates out of six business segments: Enterprise Storage and

Servers, HP Services Software, Personal Systems Group, Imagine and Printing Group,

HP Financial Services, and Corporate Investments. Technology Solutions Group is a

non-operating segment that incorporates Enterprise Storage and Serves and HP

Services into a single division. Underneath these different divisions, Hewlett Packard

provides a wide variety of computer and peripheral products. This diverse product line

includes: personal computers, handheld computer devices, home and business imaging

and printing devices, publishing systems, storage and servers, a wide selection of

information technology services and software solutions.4

In 1939, Hewlett-Packard was originated as a privately owned and operated

company. On November 6, 1957, Hewlett-Packard made the transition into a publicly

traded company at $16.00 per share. Today, Hewlett-Packard is publicly traded on the

New York Stock Exchange.

6

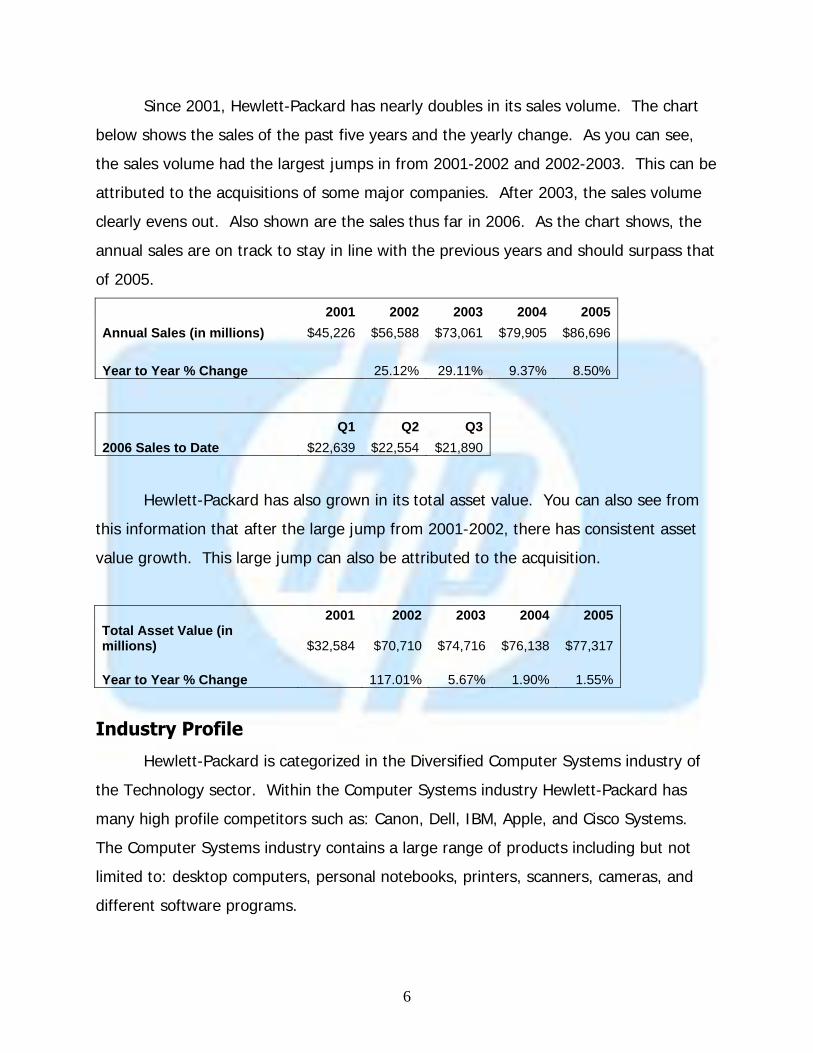

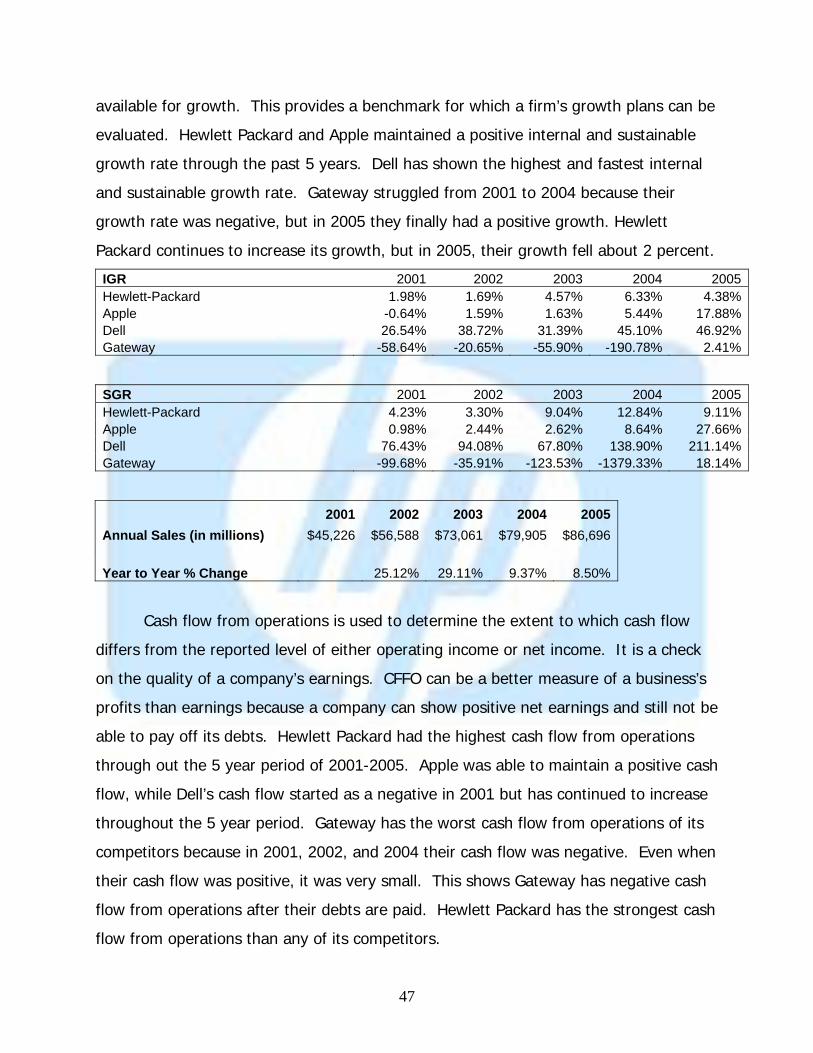

Since 2001, Hewlett-Packard has nearly doubles in its sales volume. The chart

below shows the sales of the past five years and the yearly change. As you can see,

the sales volume had the largest jumps in from 2001-2002 and 2002-2003. This can be

attributed to the acquisitions of some major companies. After 2003, the sales volume

clearly evens out. Also shown are the sales thus far in 2006. As the chart shows, the

annual sales are on track to stay in line with the previous years and should surpass that

of 2005.

2001 2002 2003 2004 2005 Annual Sales (in millions) $45,226 $56,588 $73,061 $79,905 $86,696 Year to Year % Change 25.12% 29.11% 9.37% 8.50%

Q1 Q2 Q32006 Sales to Date $22,639 $22,554 $21,890

Hewlett-Packard has also grown in its total asset value. You can also see from

this information that after the large jump from 2001-2002, there has consistent asset

value growth. This large jump can also be attributed to the acquisition.

2001 2002 2003 2004 2005 Total Asset Value (in millions) $32,584 $70,710 $74,716 $76,138 $77,317 Year to Year % Change 117.01% 5.67% 1.90% 1.55%

Industry Profile

Hewlett-Packard is categorized in the Diversified Computer Systems industry of

the Technology sector. Within the Computer Systems industry Hewlett-Packard has

many high profile competitors such as: Canon, Dell, IBM, Apple, and Cisco Systems.

The Computer Systems industry contains a large range of products including but not

limited to: desktop computers, personal notebooks, printers, scanners, cameras, and

different software programs.

7

Most companies, such as Dell, Apple or Gateway, tend to be limited to a small

product range. Compared to other industry competitors, Hewlett-Packard has a wide

variety of consumer products. This gives HP a competitive advantage in the consumer

market due to their brand name coverage in the technology industry. Hewlett-Packard

offers desktops, notebooks, handhelds (pocket PC’s), monitors, home networking,

televisions, digital photography, printers and printing supplies. Hewlett-Packard does

not specialize in just one product line. With new technology innovations, some of their

previously lesser known lines have grown to be some of their largest. In the past five

years, Hewlett-Packard’s imaging and printing division has grown substantially due to

the popular home photography printing.

Vyomesh Joshi, executive vice president of Hewlett-Packard Co.’s imaging and

printing division, said Tuesday that the most-profitable of HP’s operations should

be able to continue to grow sales by 4% to 6% a year. Joshi said HP sees

tremendous opportunity in the inkjet-printing market, as well as its typically

strong laser-printer business.1

Five Forces Model:

Competitive Force 1: Rivalry among Existing Firms

Competition among existing firms is one of the biggest threats for Technology

Industry companies. There are many large companies with a strong foothold in the

technology industry, making each competitor’s revolutionary idea a factor in the

consumer’s decisions. In the past ten years, the technology industry has grown

exponentially. The size, quality, functions and appearance of all technological devices

and software are continually improving. A good example of the technological revolution

is the ever changing photography world. In the past decade, the camera has changed

from a 35 mm camera, with removable exposures, to the now modernized, sleek digital

camera which stores your images digitally until you are ready to print your pictures.

With what seems like daily changes, companies have to stay on top of their research

and development to keep their product up to date. The same updates are needed with

8

computers, which are always become outdated faster than expected. All of these

factors increase the competition among existing firms.

There is a high degree of concentration in this industry within the largest

companies including: Apple, Dell, HP, IBM, and Sony. At one point, IBM was the

industry leader, setting the bar for price and quality, but over time, other major

competitors have stepped up to the plate with new technology and price cutting

initiatives.3 In today’s market there is not one particular company which dictates the

overall computer pricing, as these leaders work together to avoid harsh price

competition. Along with these larger companies there are also smaller competitors

including: Gateway, Compaq, eMachines, and Velocity Micro. Many of these companies

overlap in competition, with products ranging from desktops to cameras to mp3

players. In each of these markets, there are different industry leaders.

In the computer technology industry, there are incentives to hold a strong

market share by setting lower prices or having new innovative ideas. Dell came into

the market aggressively with a ground-breaking business strategy. They cut out the

middle man, selling their products without a retail store, and were able to offer an

industry leading low price. The other large competitors, such as HP, could not match

this low price incentive, given their higher fixed costs involved in their sales. Hewlett-

Packard’s only way to compete with industry leaders is to keep a low variable cost. To

even begin competing in this industry, one must not only have the technology needed

but also the economy of scale.

In this modern world, a company in this area need not worry about excess

capacity, due to the high level of demand for such sophisticated products. This also

covers the problem of exit barriers, since at this time technology is only rising.

There is obviously a high degree of rivalry among existing firms in the

technology industry. With new ideas and cost cutting initiatives being thought of

everyday, those competing in this industry must keep up with these changes. This

involves creating brand loyalty, diversifying your company, being able to create new

ideas and being able to match your competitor’s advances. Implementing these ideas

allows a chance to keep up with the technology industry leaders.

9

Competitive Force 2: Threat of New Entrants

Having new entrants into the technology industry may seem impossible, but

when you think about the different areas they could enter into, it is not as hard as it

seems. Yes, it may be difficult for a new technology company to come about, but there

is also the angle of existing companies to creating new technological products. With

this idea comes the threat of new entrants.

In order for a company to enter this industry it would require large economies of

scale. To compete in this industry, a large amount of capital is required. New

companies trying to make a foothold in the technology industry will suffer from

economies of scale in research and development, brand advertising, and possibly

physical plant and equipment.3 It takes a lot of research and development before a

product can initially be launched, which is a large problem for new companies without

sound financial backing. In order to keep up with competitors, most companies need to

begin to generate revenue in the early stages of the company’s life, rather than having

to spend excess amounts of money. The companies which are currently competing in

the industry have already established themselves among the consumers as reputable

producers of technological products. Not only have they put in capital, but also the

time to gain their brand recognition. A new company cannot automatically buy brand

recognition; it involves being set in the marketplace to gain consumer confidence.

If a company was attempting to enter into the industry it would be beneficial for

them to have a new innovative product. This would allow them to gain a first mover

advantage over the existing competition. For example, Apple has gained an advantage

over the rest of the technology industry with their addition of iPod and iTunes in 2004.

Since it was the first, iPod is now the benchmark mp3 player, making it difficult to rival

their ever-changing technology. This is where the idea of already existing companies

bringing in new products comes into play. For example, recently there has been the

development of a portable USB port. This allows a PC user to insert a device (the USB)

into their computer and save their work in the USB. They can then insert the USB into

10

any other computer and have their work uploaded, quickly and simply. This has

become a large industry, and many companies have begun producing these products.

Another barrier to entry is the already established distribution channels and

relationships among suppliers. It is common in an industry which uses many different

suppliers, for exclusive relationships to be developed. In cases such as this, many

times it becomes difficult for new competition to gain such advantages. In the

technology industry many of the components are produced overseas. These foreign

barriers also create another problem for new entrants.

Seeing that the computer systems industry is so research-intensive, there are

many patents and copyrights already in existence. This creates legal barriers for the

companies trying to gain a new market share.

With such high barriers of entry into the technology industry, it is apparent why

we haven’t seen a new company come into the market. Although, it is unlikely for a

new company to gain market share in this industry, you still have to be aware of the

possibility of new products entering the industry. This is the main threat of new

entrants.

Competitive Force 3: Threat of Substitute Products

In this modern technology era that we live in today, technology companies

service the everyday and practical needs of the consumer. In most businesses and

homes today, people use some form of computers, software, printers, networks,

cameras and televisions. There is currently no substitution for these sophisticated

devices unless you resort to the old technology. The problem is that we rely upon the

technologies of these new devices in our everyday day lives.

Before the invention of the computer, the most commonly used mechanical

device in the business world was the typewriter. Many people do not use this

substitution to the computer in this day and age. The computer took over the

typewriter long ago and will continue to be the most popular tool for consumers in the

future. The invention of the digital camera has paved the way for a whole new line of

home accessories for home photography. Digital cameras have replaced the old 35 mm

11

cameras that were used by every family just ten year ago. There is currently no

substitution for the quality and the convenience of the cameras produced today.

Overall, you could say there are limited threats of substitute products currently in

this industry. While new products are invented regularly, it is hard to think of

something that has the possibility of replacing the computer all together. It also seems

that a digital camera is a technologically advanced as it is going to get for a good

amount of time. For this reason, there is a limited threat of substitute products.

Competitive Force 4: Bargaining Power of Buyers

Factors that affect the bargaining power of buyers are price sensitivity and

relative bargaining power. The computer industry is comprised of several other

companies such as Apple, Dell, Hewlett Packard, and Gateway. Some of these

companies specialize only in producing computers; while others produce computers

along with other electronic products such as printers, cameras, and other hardware.

Each company needs to be aware of their buyers through their price sensitivity and the

bargaining power of buyers.

Price sensitivity determines the extent buyers choose to bargain on price.

Buyers are typically less-price sensitive because of the amount of differentiated

products. The buyers’ price sensitivity also depends on the importance of the product

to the buyer. For example, computers are used every day in people’s lives. This makes

the computer industry very valuable to customers. In return the buyers are going to be

sensitive to the price of the product due to the importance of the product in their lives.

This causes the buyer to shop around more for a similar product at a better price. The

shows that buyers are price sensitive, which encourages other companies to compete

for a lower price and better quality. Some computer companies such as Hewlett

Packard already compete on quality. The importance of the product quality to the

buyers determines whether or not price becomes an important determinant in the

buying decision.

Buyers have a relatively strong bargaining power in the computer industry. A

buyers’ relative bargaining power depends on volume of purchases bought by a single

12

buyer, number of alternative product available to the buyer, and buyer’s cost of

switching from one product to another. First, there are several major electronic stores,

such as Best Buy and Circuit City, which carry a large quantity and variety of

computers. This makes stores product cost of computers cheaper because they can

purchase a large inventory at one time. Buyers also have strong bargaining power

because there are several computer companies in the industry, all with a similar product

that performs similar functions. This allows the buyer to “shop around” for the best

deal on a computer. The switching cost is relatively low because most software

programs can run on any computer. Also, other electronic items such as cameras and

printers are compatible to be set up on any brand of computer.

Buyers relative bargaining power depends on volume of purchases buy a single

buyer, number of alternative product available to the buyer, and buyer’s cost of

switching from one product to another. Buyer’s bargaining power also increases due to

the number of alternative products available. Local electronic stores have high

competition from products that offer the same hardware but at a cheaper price. Buyers

benefit from the number of alternative products available and the competitiveness of

the companies. Overall in the computer industry buyers have a relatively strong

bargaining power.

Competitive Force 5: Bargaining Power of Suppliers

Suppliers are powerful when there are few substitutes, the product is critical for

buyer’s business, and when they pose a credible threat of forward integration.

Suppliers are most powerful when there are only a few companies and few substitutes

available to their customers. The computer industry has several companies that all

produce similar products that are needed by the customers for their daily business.

Suppliers are powerful when there are only a few companies and few substitutes

available to their customers. In this industry, suppliers show a low bargaining power

due to the amount of substitutes available. Several companies such as Apple, Dell,

Hewlett Packard, and Gateway all produce computers that compete with each other.

Each computer company is very powerful over their suppliers of hardware for the

13

computer. There are several companies and several substitutes available to the

customers which make the supplier’s bargaining power low.

Suppliers also have power over buyers when the suppliers’ product or services is

critical to buyers’ business. Suppliers realize that technology is leading the world today.

From calculators to personal computers, the human population is relying more on

technology for everyday use. This lets suppliers control the industry price. Even

though there is intense competition in the computer industry, suppliers realize how

important computers are to everyday business and can maintain a sustainable price to

meet the demand.

There is very little threat from the suppliers to forward integrate. The threat is

minimal because Intel, AMD, and Microsoft can not sell directly to customers because

they do not make personal computers, imaging devices, or servers. For the competitors

to advance in this area it would cost too much and there are too many disadvantages

due to barriers of entry.

Suppliers have high bargaining power when there are few substitutes, the

product is critical for buyer’s business, and when they pose a credible threat of forward

integration. Suppliers have a low bargaining power when it comes to substitutes

products, but are able to maintain an overall high bargaining power because computers

are critical to everyday business. Although suppliers possess little integrations and high

competition, they still maintain a high bargaining power through the high demand for

technology.

Value Chain Strategies

Firms within an industry need to be able to identify their competitive advantage

through either cost leadership or product differentiation. In order to attract a premium

price to customers, there needs to be adequate company differentiation or cost

leadership within the industry. The computer industry focuses mainly on differentiating

their products.

14

Differentiation plays a vital role in adding value to the industry. There is a large

demand, by customers, in the computer industry. Every year new products enter into

the market that customers either want or think they have to have. The high demand

for technology has led to many firms being present in this industry. Several firms make

the same product which is why it is so important for the industry to be able to

differentiate their products. These companies aggressively compete on price

competition, quality, and customer service, which allows for differentiation.

Some drivers of industry are product quality, product variety, and delivery

timing. Hewlett-Packard is a good example of product quality and variety. They

specialize in making a variety of high quality products. Dell, on the other hand, does

not sell their products in a store; they have chosen to focus on their sales through the

internet and phone orders. Because of this Dell has to offer fast delivery and timing.

These drivers all help to set the firms apart in the industry.

The computer industry needs unique firms in order to differentiate their

computers. In order for the computer industry to differentiate their products firms

must identify the attributes, meet the needs of customers, and differentiate at a lower

price than the customer is willing to pay. Computers typically meet the needs of

customers because they can perform more functions faster and easier than a person

can do. Most computers can perform the same tasks, but they all have different

functions and specializations. Apple is an example of a firm that specializes their own

software. Apple is the only firm with their own operating system; the other firms

operate using Microsoft Windows. One of the most important factors of differentiation

is being able to differentiate at a price lower than the customer is willing to pay. Firms

that compete on differentiation still need to focus on costs so that the differentiation

can be achieved at an acceptable cost.

In order for a firm to have industry power, they need to maintain their

competitive advantage. Once this advantage is created, firms need to maintain

creativity and innovation to continue with their advantage.

Creating a Competitive Advantage

15

Each segment in the five factor model is characterized by vigorous competition,

long established companies, and a large number of rapidly growing firms. Hewlett-

Packard strives to compete primarily on what they consider their core competencies of

technology, performance, price, quality, and reliability. With these strengths the

company has been able to be an industry leader in each of their principal business

segments. In this industry, product lives are short, and to remain competitive Hewlett-

Packard must develop new products and services, as well as continually enhance their

existing products and services.4

Product differentiation plays a large role in creating value within Hewlett-

Packard. HP has a product line that ranges from desktop computers to servers to

digital entertainment. Hewlett-Packard has successfully spanned their range of

products and product categories. This allows customers to enjoy a broad range of

digital entertainment experiences, while enjoying the same brand recognition. They

have also been able to target their businesses to individual customer segments, while

also targeting small and medium businesses to large enterprises.4

Hewlett-Packard is a company of high quality specialized products. In an

industry with so many competitors, they have chosen a differentiation strategy.

Hewlett-Packard chose to differentiation their products by focusing on performance,

quality, reliability, and price. They can offer a high quality durable product at a price a

everyone can afford. Hewlett-Packard does not have cost leadership because they do

not have the lowest cost, but they do have a low cost for the quality and functions of

their product.

Hewlett-Packard’s competitive advantage in the compute industry comes from

their product differentiation. Hewlett-Packard has successfully created a product line

that has been able to reach a wide variety of customers in the consumer and

commercial customer groups. HP has continued to strengthen its company while

focusing on differentiating its product’s technology, performance, quality and reliability.

A strong quality that Hewlett-Packard possesses has been its ability to bring its product

line together. All of Hewlett-Packard’s products in one way or another are

complimentary to each other. Most competitors in this industry have found themselves

16

focusing on one strong product; such as, Dell with their computers or Canon with their

digital imaging equipment. Hewlett-Packard has been able to have success in all of

their product segments, including their commercial and consumer computers,

workstations, handheld computing, and digital entertainment.

Using differentiation as a competitive advantage has allowed Hewlett-Packard to

set itself apart from the industry as a whole. While HP does not have the lowest cost in

the industry, they continue to strive to cut costs wherever possible. Combining this

effort with their product differentiation strategy has allowed Hewlett-Packard to become

a recognizable brand, and ultimately made them an industry leader.

Accounting Analysis

The purpose of accounting analysis is to evaluate the degree to which a firm’s

accounting captures the underlying business reality.3 Hewlett-Packard is in the

Diversified Computer Systems industry making it important to focus on strategic

necessities within the individual product categories and then manage across the entire

portfolio to drive growth while optimizing cost structure.4 Hewlett-Packard prepares its

Financial Statements under the Generally Accepted Accounting Principles standards,

which states that management must make estimates, judgments and assumptions

which would affect the disclosure of their assets and liabilities. Hewlett-Packard

management has a thorough process of making these estimates, which are vital to the

overall outcome of the company. These estimates are based on past experiences,

along with other assumptions that they must make due to the ambiguous parts of

accounting that are not readily available from other sources. After this step, the Audit

Committee and senior management of Hewlett-Packard discuss the estimates at hand,

and how to disclose this information.

Key Accounting Policies

Hewlett-Packard makes many significant estimates and assumptions in different

areas for the overall preparation of their Financial Statements. They then choose the

information to be publicized, with the necessary revisions added. Being that Hewlett-

17

Packard is reliant upon having such a differentiated product line, it is important for

them to disclose their accounting information to reflect this strategy. Differentiation is a

main competitive strategy for Hewlett-Packard, making the key accounting policies:

research and development, goodwill, warranty provisions and inventory management.

Hewlett-Packard falls into an industry that is highly reliant upon research and

development. In order to keep up with the ever changing technology, Hewlett-Packard

spends a large amount of time and money on research and development, making it one

of the most important success factors. Spending time on R&D allows Hewlett-Packard

to deliver the most modern technology to the consumer’s changing needs. Hewlett-

Packard spends more time in research and development than their competitors to

follow their business model, which promotes innovation and high quality.4 HP Labs, a

part of the Corporate Investments Segment, is in charge of the research and

development for the company. Research and development is expensed as incurred.

Even though this research and development generates future sales, Hewlett-Packard

decides to write it off as an expense rather than record it as an asset. In fiscal year

2005, HP expensed $3.5 billion in research and development.

Goodwill is another part of Hewlett-Packard’s key financial reporting policies.

According to SFAS No, 142, “Goodwill and Other Intangible Assets”, goodwill is valued

with an indefinite life with annual impairments. In Hewlett-Packard’s case, the

impairment of goodwill is a two step process beginning with comparing the fair value of

each reporting unit with its carrying value. The fair value is determined by weighting

the income and market approaches. If the carrying value of net assets exceeds the fair

value, then the second step must be performed. The amount it exceeds is then

recorded as an impairment loss. The fair values, which are used in these comparisons,

are estimated using an income approach. Estimating the revenue growth rates and

operating margins, risk adjusted discount rates, assumed royalty rates, future economic

and market conditions and determining the appropriate market comparables is

necessary in finding the fair and carrying values. These estimates are based upon

assumptions.

18

Being a retail company, it is important to have a strong inventory management.

Hewlett-Packard succeeds in this area, having a large amount of control of how the

inventory is reported. This is very apparent in their decision to use the first-in-first-out

method when keeping track of their inventory. The first-in-first-out method assumes

that the first unit entered into inventory will also be the first to be sold. This keeps the

company’s inventory costs down in times of high costs. Another advantage to using

FIFO is that this method keeps the cost of goods sold lower, allowing the company’s net

income to increase. Using this method can also decrease the amount of income tax the

company will be held accountable for at year end. Since technology is such a major

influence in this industry, and is rapidly changing, Hewlett-Packard benefits from using

the first-in-first-out accounting method. This benefit arises from the ability to get the

latest and most up to date product out in the market, before it becomes obsolete. This

is noticeably seen in the financial statements of Hewlett-Packard.

These key accounting policies, which Hewlett-Packard uses, parallel with the

company’s competitive strategy of differentiation. The accounting policies allow

Hewlett-Packard to attempt to make the most accurate estimates and financial reports.

Assess Accounting Flexibility

Under the GAAP guidelines, firms are subject to different degrees of accounting

flexibility. The amount and detail to which a firm discloses their financials to investors,

is left to the management’s discretion. This management team must work together and

approve their decisions with the Audit Committee of Hewlett-Packard’s Board of

Directors.

Research and development is an important aspect of Hewlett-Packard’s

accounting policies, however there is no management discretion in how this is reported.

Research and development must be expensed as it is incurred. Since there is no

flexibility in how this is reported, there cannot be any chance for the management to

manipulate these numbers in order to benefit the standing of the company.

19

With research and development comes the opportunity for acquisitions. Hewlett-

Packard has had some major acquisitions such as Triaton GmbH, Triaton France SAS

and Triaton N.A., Inc. These additions to Hewlett-Packard would obviously affect the

accounting records of the following years. A good example of this effect is in 2001,

when Hewlett-Packard acquired Compaq. The next year the company’s asset’s doubled

and the net revenue increased by 25%. This means that HP began incorporating

Compaq’s sales into their net revenues and not as a separate entity. Without the

previous knowledge of the acquisition of Compaq the substantial increase in sales would

be a red flag to investors.

Inventory management is an area which is highly flexible at the company’s

discretion. While Hewlett-Packard practices the method of first-in-first-out, there are

other ways to record inventory. These ways include last-in-first-out and average cost.

In the technology industry, using first-in-first-out is the most relevant method. If the

company used last-in-first-out, they would be distributing the oldest inventory held,

while the newest technology would be gathering in inventory. Although Hewlett-

Packard has chosen a method which ultimately helps their company, there is still that

option to choose how you want to account for inventory.

“Goodwill and Other Intangible Assets” is outlined by the Statement of Financial

Accounting Standards, No. 142. This properly defines the methods in which goodwill

and intangible assets should be accounted for. This allows no flexibility within the

company, because the standards are laid out for you. The problem with Statement No.

142, is that all of these values are based solely on estimates. There is great room for

error when using this standard accounting process.

The key accounting policies for Hewlett-Packard vary in flexibility. Some remain

very flexible, while the majority do not allow for flexibility. Flexibility allows company’s

to gain an advantage when reporting. Although this is true, accounting requires strict

standards and consistency in order for financial reporting to be valuable.

Evaluate Accounting Strategy

20

Hewlett-Packard gives a very thorough disclosure of their accounting policies and

financial information to the public. A very conservative approach is taken when

reporting annual numbers. This type of approach gives a realistic view of the

company’s financials, without attempting to distort their company’s financial standing.

You can see this through comparisons with competitors’ reports, historical data and

auditor’s analysis.

Hewlett-Packard’s conservative approach to accounting can be seen through

their compliance with Generally Accepted Accounting Principles (GAAP). When GAAP

does not provide standards, Hewlett-Packard tends to follow the industry norm. This

can be seen through the similarities between the discussed computer industry

competitors.

Hewlett-Packard’s main competitors, in the computer section of their multi-

product industry, are Dell and Apple. Mainly, the accounting policies of these three

firms are consistent with each other. Hewlett-Packard, along with Apple and Dell, use

the first in first out method when accounting for inventory. These three companies also

recognize revenues when the items are delivered and there is a final acceptance of the

good. Another similarity between these companies is the use of SFAS No. 142 when

dealing with their Goodwill and Other Intangible Assets. The only difference we found

between Hewlett-Packard’s competitors is that they use straight-line depreciation based

on a thirty year time frame for buildings, and two-five year time frame for equipment.

Hewlett-Packard, on the other hand, uses a time frame of five to forty years, based on

the asset being depreciated.

Management has the opportunity to manipulate accounting strategies and

choose what they disclose. If management has the incentive to distort accounting

policies, it adds another area which must be thoroughly assessed. Management,

including the CEO, CFO and other chief executives receive stock options on a yearly

basis. This gives management some incentive to imply that their company may be

doing better than they are. The Compensation Committee established a performance

metrics for the first and second halves of the fiscal 2005, respectively, which were

weighted 40% based on revenue, 40% based on net profit and 20% based on total

21

customer experience for the executive officers.4 Since 20% of this compensation is

based on consumer experience, it leads to the belief that Hewlett-Packard’s

management would not distort their accounting strategies, in order to keep their

customer satisfaction.

Hewlett-Packard has had many policy changes within their company in the past

few years. In 2003, Hewlett-Packard encountered a large restructuring charge of $752

million. With this came new plans to better implement cost structure and business

operations. The 2004 financials demonstrate the effects of these changes. Another

management improvement plan involved the termination of about 1,450 employees,

which was finalized as of October 31, 2005.4 With this reorganization came a charge of

$109 million in severance and other related costs. $87 million of this amount has been

paid as of October 31, 2005, and the difference is expected to be paid off by the end of

fiscal 2006. Also at the end of 2005, the Board of Directors approved another

restructuring plan to reduce costs. Under this plan, roughly 15,300 employees will be

terminated through the first quarter of fiscal 2007.4 This plan is estimated to cost

Hewlett-Packard $1.6 billion. The last change of strategy for Hewlett-Packard, was the

reduction of retirement programs, effective January 1, 2006. With this came a

curtailment gain of $199 million in the fourth quarter of fiscal 2005.

One of the most recent acquisitions under Hewlett-Packard has been that of

Compaq computers. This acquisition led to many changes in the financial reports

between 2001 and 2002. This is obviously shown in the total assets, and explained in

the footnotes of the 10-K. Other than this, Hewlett-Packard does not have any other

related entities that have affected their accounting position.

Hewlett-Packard’s accounting strategy is very unique along with sharing some

characteristics with their competition. These techniques allow for HP to do a very

thorough accounting disclosure.

Qualitative Disclosure

22

It is the discretion of the management to choose how easy or difficult it is to find

information in the company’s financial reports. Many people access these reports on a

daily basis whether it is an auditor, another analyst or even stockholder. When the

information is clear and easy to identify, it makes a huge difference.

Hewlett Packard is a company interested in putting their stockholders at ease by

having unsurpassed quality of disclosure. In their annual 10K, they explain in great

detail the reasoning for their accounting choices in recording revenues and expenses.

Also contained in the 10K is a candid and very frank report of their risk management

strategies, which include managing foreign currency exchange rate risk, interest rate

risk, and equity price risk. Their strategy is to use derivative financial instruments to

“manage existing underlying exposures of HP”, not on speculative purposes.4 In

addition to this, their 10K has a long listing of footnotes that outlines and explains their

choices in accounting and revenue allocation. For example, in the footnote titled

Reclassifications and Segment Reorganization, they go into great detail outlining their

information technology infrastructure. Hewlett-Packard reclassified the division’s cost of

services and administrative expenses to costs of products, services, and research and

development expenses to better reflect the cost of their active areas to better reflect

the cost allocation in each of these underlining areas. This results in an increase in cost

of sales and an equal decrease in operating expenses.

Their business strategy has always been very diverse due to their vast portfolio.

Hewlett-Packard operates under seven business segments: Enterprise Storage and

Servers, HP Services Software, Personal Systems Group, Imaging and Printing Group,

HP Financial Services, and Corporate Investment. Outlined in their 10K is a detailed

description of revenues and growth for each of the business segments. Hewlett-

Packard is a global technology company, and they are always studying trends in the

market place to maintain their competitive edge and increase profits. In the firm’s

Management Discussion and Analysis section of their 10K, they even go on to talk about

workforce restructuring and reinvesting half of the cost savings from the downsizing

back into the firm. In addition to this, HP is also very forthright in the disclosing of bad

news. In the segment titled Losses on Investments, the firm speaks openly about

23

reductions to value. Once a reduction in value of a segment is identified, it is

investigated to determine if the loss will persist. If it is deemed “other-than-

temporary,” HP will put an impairment charge on the segment and establish a new cost

structure at its fair value. Impairments have been recorded at $43 million, $26 million,

and $72 million respectively in the last 3 fiscal years.

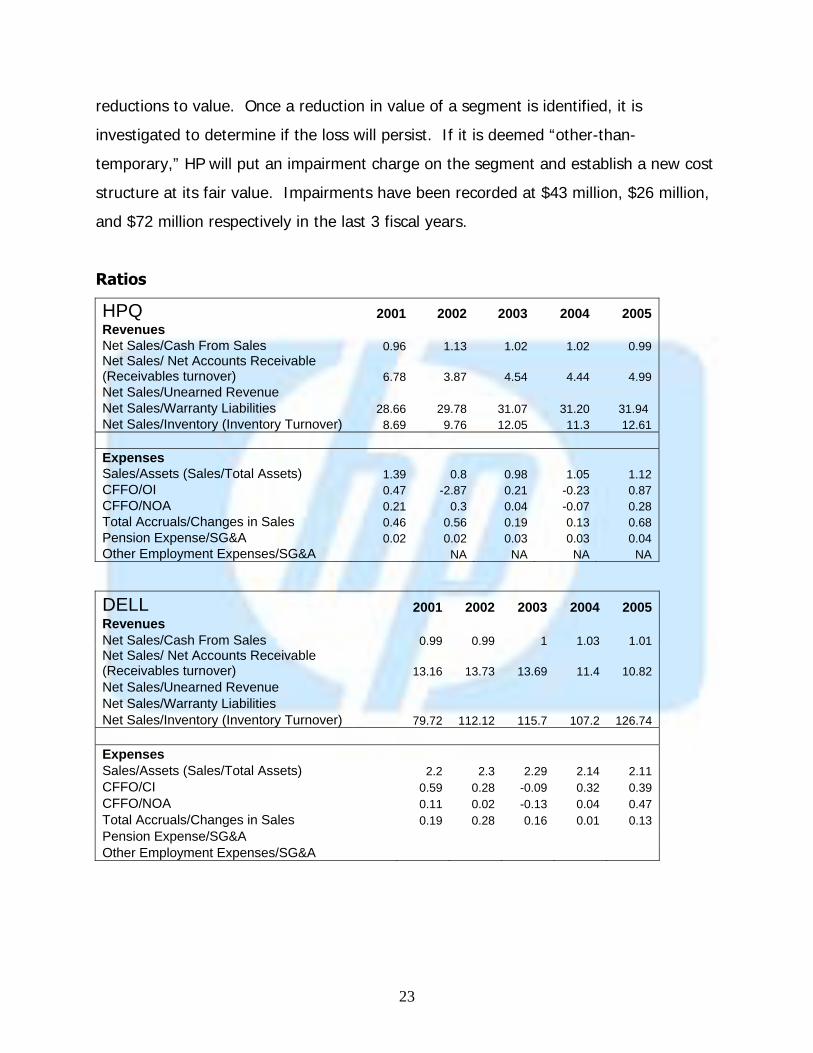

Ratios

HPQ 2001 2002 2003 2004 2005 Revenues Net Sales/Cash From Sales 0.96 1.13 1.02 1.02 0.99 Net Sales/ Net Accounts Receivable (Receivables turnover) 6.78 3.87 4.54 4.44 4.99 Net Sales/Unearned Revenue Net Sales/Warranty Liabilities 28.66 29.78 31.07 31.20 31.94 Net Sales/Inventory (Inventory Turnover) 8.69 9.76 12.05 11.3 12.61 Expenses Sales/Assets (Sales/Total Assets) 1.39 0.8 0.98 1.05 1.12 CFFO/OI 0.47 -2.87 0.21 -0.23 0.87 CFFO/NOA 0.21 0.3 0.04 -0.07 0.28 Total Accruals/Changes in Sales 0.46 0.56 0.19 0.13 0.68 Pension Expense/SG&A 0.02 0.02 0.03 0.03 0.04 Other Employment Expenses/SG&A NA NA NA NA

DELL 2001 2002 2003 2004 2005 Revenues Net Sales/Cash From Sales 0.99 0.99 1 1.03 1.01 Net Sales/ Net Accounts Receivable (Receivables turnover) 13.16 13.73 13.69 11.4 10.82 Net Sales/Unearned Revenue Net Sales/Warranty Liabilities Net Sales/Inventory (Inventory Turnover) 79.72 112.12 115.7 107.2 126.74 Expenses Sales/Assets (Sales/Total Assets) 2.2 2.3 2.29 2.14 2.11 CFFO/CI 0.59 0.28 -0.09 0.32 0.39 CFFO/NOA 0.11 0.02 -0.13 0.04 0.47 Total Accruals/Changes in Sales 0.19 0.28 0.16 0.01 0.13 Pension Expense/SG&A Other Employment Expenses/SG&A

24

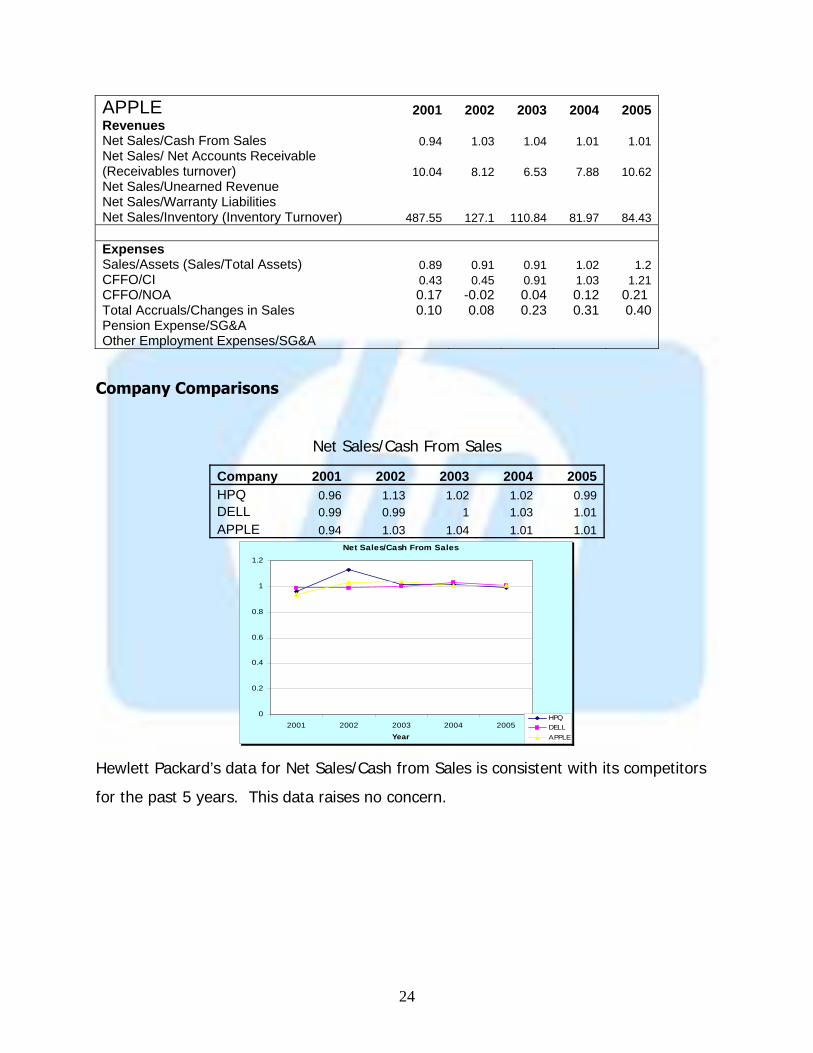

APPLE 2001 2002 2003 2004 2005 Revenues Net Sales/Cash From Sales 0.94 1.03 1.04 1.01 1.01 Net Sales/ Net Accounts Receivable (Receivables turnover) 10.04 8.12 6.53 7.88 10.62 Net Sales/Unearned Revenue Net Sales/Warranty Liabilities Net Sales/Inventory (Inventory Turnover) 487.55 127.1 110.84 81.97 84.43 Expenses Sales/Assets (Sales/Total Assets) 0.89 0.91 0.91 1.02 1.2 CFFO/CI 0.43 0.45 0.91 1.03 1.21 CFFO/NOA 0.17 -0.02 0.04 0.12 0.21 Total Accruals/Changes in Sales 0.10 0.08 0.23 0.31 0.40 Pension Expense/SG&A Other Employment Expenses/SG&A

Company Comparisons

Net Sales/Cash From Sales

Company 2001 2002 2003 2004 2005 HPQ 0.96 1.13 1.02 1.02 0.99 DELL 0.99 0.99 1 1.03 1.01 APPLE 0.94 1.03 1.04 1.01 1.01

Net Sales/Cash From Sales

0

0.2

0.4

0.6

0.8

1

1.2

2001 2002 2003 2004 2005Year

HPQDELLAPPLE

Hewlett Packard’s data for Net Sales/Cash from Sales is consistent with its competitors

for the past 5 years. This data raises no concern.

25

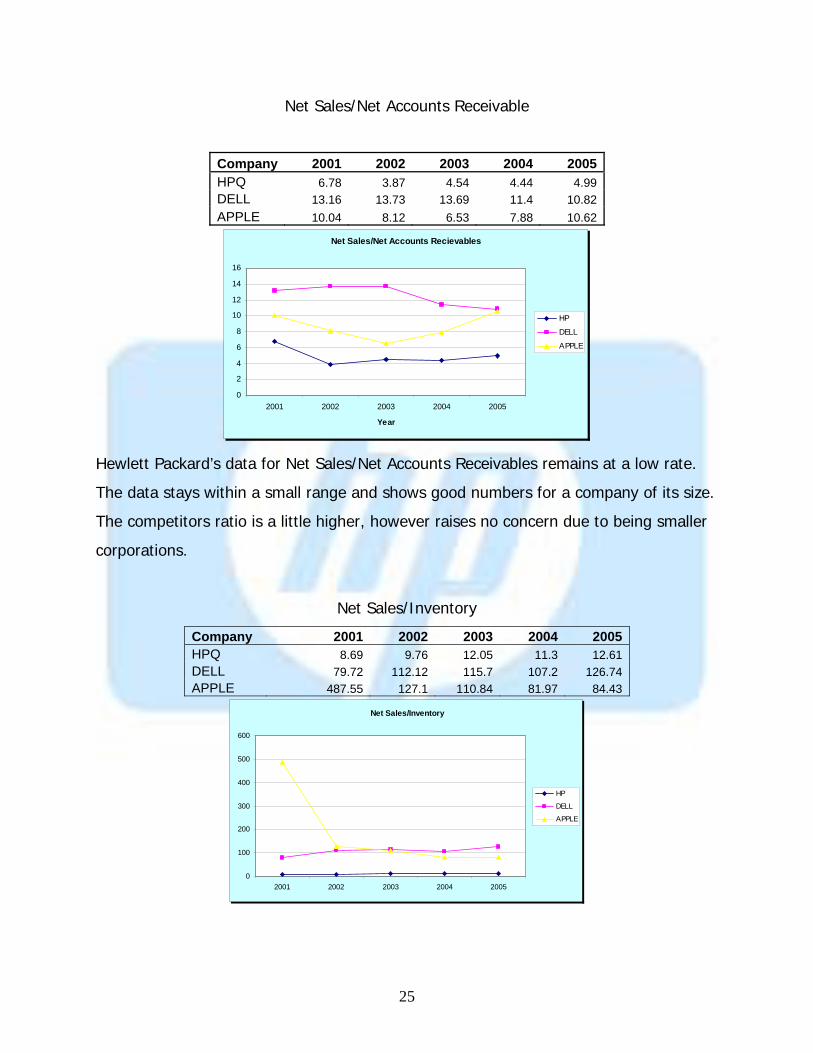

Net Sales/Net Accounts Receivable

Company 2001 2002 2003 2004 2005 HPQ 6.78 3.87 4.54 4.44 4.99 DELL 13.16 13.73 13.69 11.4 10.82 APPLE 10.04 8.12 6.53 7.88 10.62

Net Sales/Net Accounts Recievables

0

2

4

6

8

10

12

14

16

2001 2002 2003 2004 2005

Year

HP

DELL

APPLE

Hewlett Packard’s data for Net Sales/Net Accounts Receivables remains at a low rate.

The data stays within a small range and shows good numbers for a company of its size.

The competitors ratio is a little higher, however raises no concern due to being smaller

corporations.

Net Sales/Inventory

Company 2001 2002 2003 2004 2005 HPQ 8.69 9.76 12.05 11.3 12.61 DELL 79.72 112.12 115.7 107.2 126.74 APPLE 487.55 127.1 110.84 81.97 84.43

Net Sales/Inventory

0

100

200

300

400

500

600

2001 2002 2003 2004 2005

HP

DELL

APPLE

26

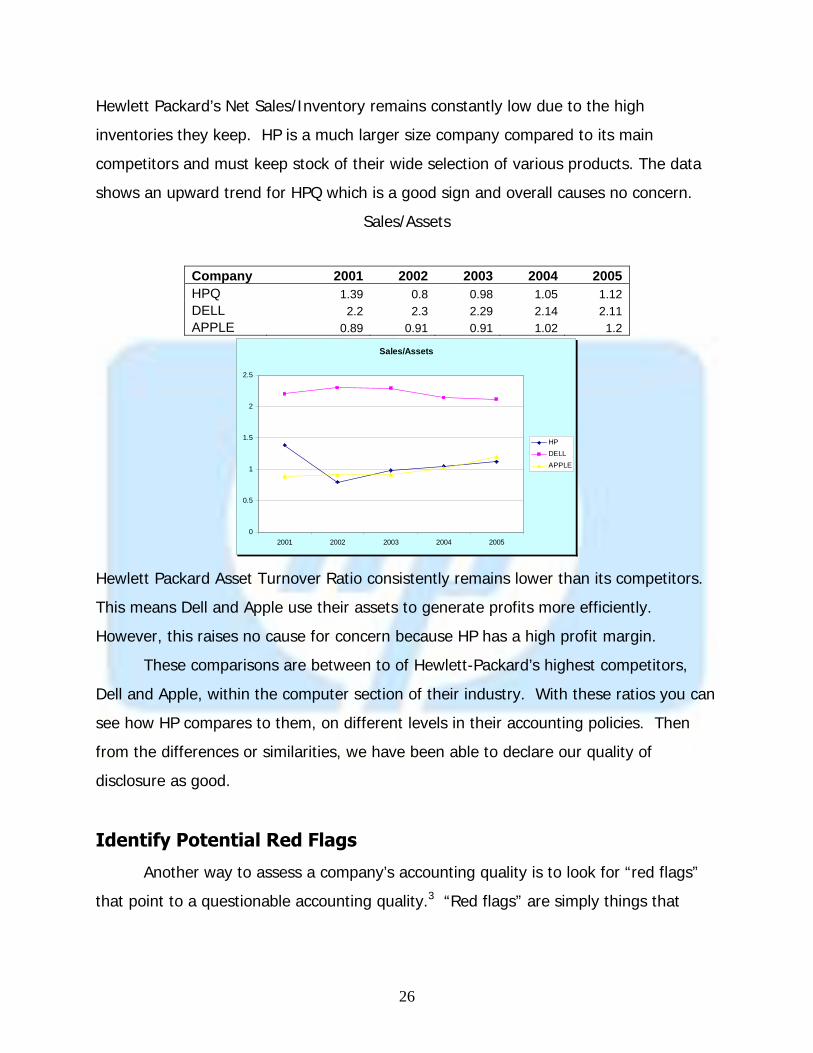

Hewlett Packard’s Net Sales/Inventory remains constantly low due to the high

inventories they keep. HP is a much larger size company compared to its main

competitors and must keep stock of their wide selection of various products. The data

shows an upward trend for HPQ which is a good sign and overall causes no concern.

Sales/Assets

Sales/Assets

0

0.5

1

1.5

2

2.5

2001 2002 2003 2004 2005

HPDELLAPPLE

Hewlett Packard Asset Turnover Ratio consistently remains lower than its competitors.

This means Dell and Apple use their assets to generate profits more efficiently.

However, this raises no cause for concern because HP has a high profit margin.

These comparisons are between to of Hewlett-Packard’s highest competitors,

Dell and Apple, within the computer section of their industry. With these ratios you can

see how HP compares to them, on different levels in their accounting policies. Then

from the differences or similarities, we have been able to declare our quality of

disclosure as good.

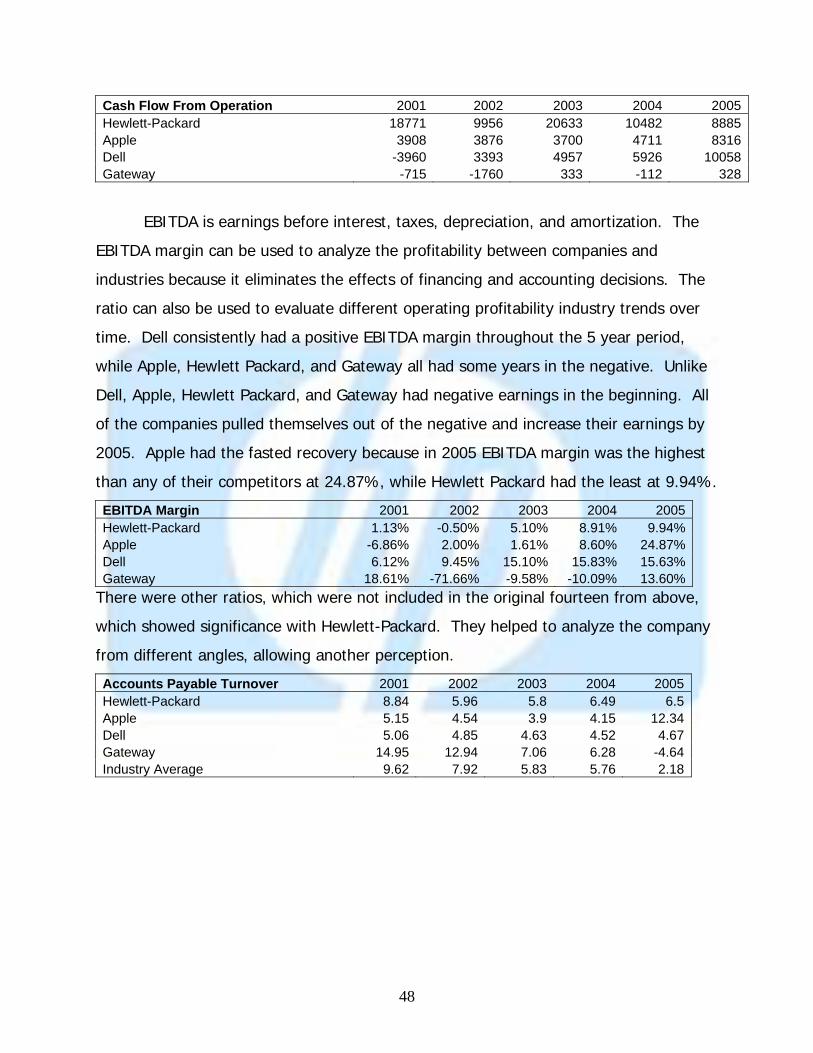

Identify Potential Red Flags

Another way to assess a company’s accounting quality is to look for “red flags”

that point to a questionable accounting quality.3 “Red flags” are simply things that

Company 2001 2002 2003 2004 2005 HPQ 1.39 0.8 0.98 1.05 1.12 DELL 2.2 2.3 2.29 2.14 2.11 APPLE 0.89 0.91 0.91 1.02 1.2

27

stand out to analysts, good or bad. These items will then be looked at closer to find

out why that particular event occurred.

Hewlett-Packard steered clear of red flags by properly disclosing their financial

data and using notes to support misaligned data. In 2002, 2003, and 2004 there was

substantial increase of costs that might raise red flags. The increase in amortization

expense in the fiscal years 2002 to 2004 are primarily due to amortization of intangible

assets. HP acquired Triaton GmbH, Triaton France SAS and Triaton N.A., Inc. (USA) in

2004 and Compaq in 2002.10 This increase might raise potential red flags due to the

offset by elimination of goodwill amortization, and the write-off of purchased intangible

assets related to the Compaq acquisition.

Expenses incurred during the fiscal period 2002 to 2004, contained substantial

costs due to the Compaq acquisition. Acquisition related charges in fiscal year 2004

consisted primarily of the amortization of deferred compensation, merger-related

inventory adjustments, and professional fees. Costs in fiscal year 2003 and 2002 were

attributed primarily to costs incurred for employee retention bonuses, professional fees

and consulting services. Other charges in fiscal year 2002 also included costs incurred

for proxy solicitation and advertising for the Compaq acquirement.10 Hewlett-Packard

recorded approximately $1.2 billion of restructuring liability as part of the acquisition of

Compaq. It was allocated as a liability of the original purchase price in fiscal year 2002.

Approximately $960 million of this amount related to pre-merger expenses and $259

million was related to pre-existing Compaq restructuring liabilities.10 These Compaq

related restructuring plans have been recorded as decreases to Compaq-related

goodwill and increases have been recorded as restructuring expense.10 After the

purchase of Compaq, Hewlett-Packard implemented strategic restructuring programs to

align Compaq and Hewlett Packard.

The restructuring program lasted for a three year period ending on October 31,

2004. When net restructuring charges ended, they totaled approximately $2.7 billion

during fiscal years 2002 to 2004. The majority of restructuring charges in fiscal 2004

represent charges from fiscal year 2003 because the expenses did not meet the

recognition criteria for accrual during 2003. These charges were primarily related to

28

asset impairments for buildings vacated after the purchase of Compaq. Hewlett-

Packard leases the majority of their buildings. During the acquisition, Hewlett-Packard

had to convert into Compaq’s space, sell the property, or cancel/finish lease

agreements. On October 31, 2004, the restructuring program ended and the financial

statements returned to normal in the fiscal year2005. Hewlett-Packard’s biggest

impairment of vacated buildings finally balanced out in 2005. In 2005, Hewlett-Packard

owned 39% of building space and leased the remaining 61% of space.10 The goal of

the restructuring programs put in play after the acquisition of Compaq, has been to

reduce costs by removing duplication and leverage the benefits for Hewlett-Packard.

Hewlett-Packard wrote in their 10K report, “Any failure by us to manage

acquisitions, divestitures and other significant transactions successfully could harm our

financial results, business and prospects.” Hewlett-Packard properly disclosed all

potential harmful financial information in the 10K report. Financial information was

properly disclosed and there were no red flags raised when reviewing the company’s

10K report.

Financial Analysis

Financial analysis is the process of examining and interpreting a company’s

financial statements in order to evaluate the financial standing of that company. When

performing financial analysis you are able to determine the company’s strengths and

weaknesses, find the source of changes, and determine trends for future forecasting.

There are two ways to perform financial analysis, which are ratio analysis and cash flow

analysis. The financial statements of Hewlett-Packard will be broken down into

liquidity, profitability and capital structure; and will be analyzed in the following

sections.

Financial Ratio Analysis

One method of financial analysis is a ratio analysis. “Ratio analysis involves

relating the financial numbers to the underlying business factors in as much detail as

29

possible.”3 After the first assessment of ratio analysis, which involves comparing a

companies financials from previous years, it is possible to go further into the process

comparing those numbers to the industry as well.

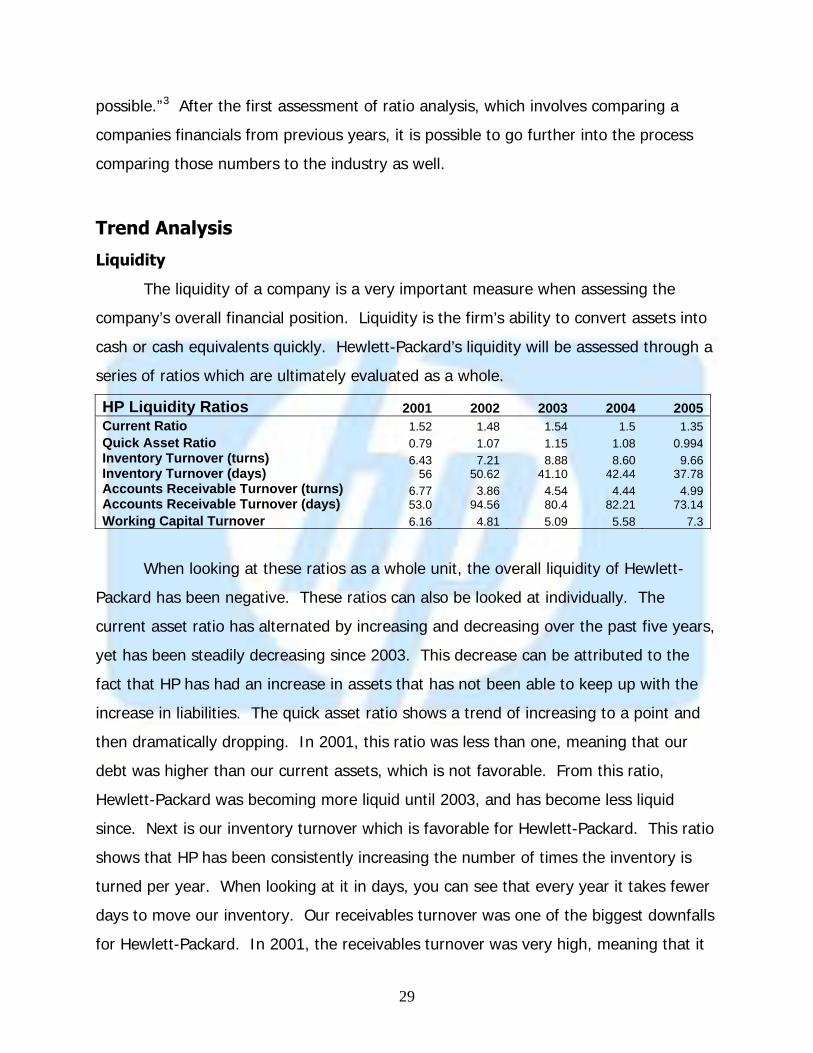

Trend Analysis

Liquidity

The liquidity of a company is a very important measure when assessing the

company’s overall financial position. Liquidity is the firm’s ability to convert assets into

cash or cash equivalents quickly. Hewlett-Packard’s liquidity will be assessed through a

series of ratios which are ultimately evaluated as a whole.

HP Liquidity Ratios 2001 2002 2003 2004 2005Current Ratio 1.52 1.48 1.54 1.5 1.35 Quick Asset Ratio 0.79 1.07 1.15 1.08 0.994 Inventory Turnover (turns) Inventory Turnover (days)

6.43 56

7.21 50.62

8.88 41.10

8.60 42.44

9.66 37.78

Accounts Receivable Turnover (turns) Accounts Receivable Turnover (days)

6.77 53.0

3.86 94.56

4.54 80.4

4.44 82.21

4.99 73.14

Working Capital Turnover 6.16 4.81 5.09 5.58 7.3

When looking at these ratios as a whole unit, the overall liquidity of Hewlett-

Packard has been negative. These ratios can also be looked at individually. The

current asset ratio has alternated by increasing and decreasing over the past five years,

yet has been steadily decreasing since 2003. This decrease can be attributed to the

fact that HP has had an increase in assets that has not been able to keep up with the

increase in liabilities. The quick asset ratio shows a trend of increasing to a point and

then dramatically dropping. In 2001, this ratio was less than one, meaning that our

debt was higher than our current assets, which is not favorable. From this ratio,

Hewlett-Packard was becoming more liquid until 2003, and has become less liquid

since. Next is our inventory turnover which is favorable for Hewlett-Packard. This ratio

shows that HP has been consistently increasing the number of times the inventory is

turned per year. When looking at it in days, you can see that every year it takes fewer

days to move our inventory. Our receivables turnover was one of the biggest downfalls

for Hewlett-Packard. In 2001, the receivables turnover was very high, meaning that it

30

took fewer days for HP to collect their receivables. From 2001-2002, HP more than

doubled it receivables due to the acquisition of a major company, making that years

receivables turnover very low, meaning it took more days to collect this money. Since

2002, it has been improving, but is still at a very high number of days to collect on the

receivables. The last ratio, working capital turnover, was a positive change for HP.

After the decrease in this ratio, due to the major acquisition, HP’s working capital

turnover is steadily increasing. This ratio has a positive impact on the liquidity of

Hewlett-Packard.

The current overall liquidity of Hewlett-Packard is unfavorable. They have a high

receivables turnover in days compared to the industry, the current ratio is declining and

a slow inventory turnover. The only positive ratio in overall liquidity is the working

capital ratio. This shows the overall analysis of HP’s liquidity is negative.

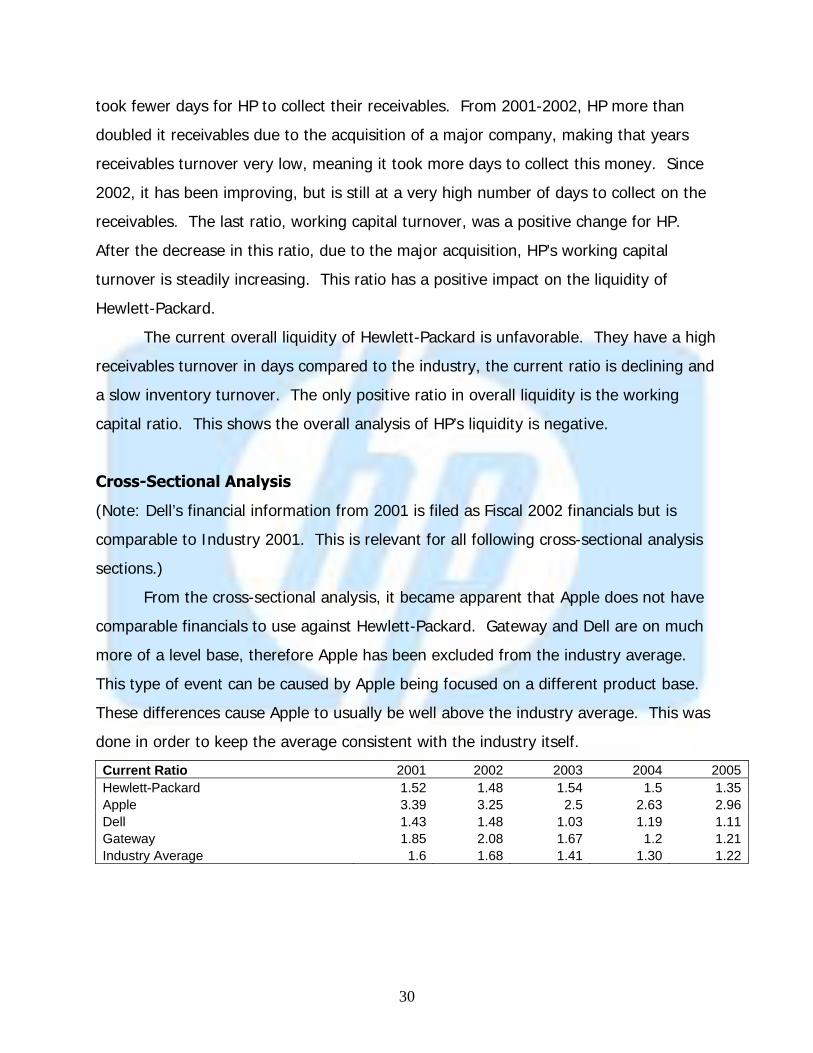

Cross-Sectional Analysis

(Note: Dell’s financial information from 2001 is filed as Fiscal 2002 financials but is

comparable to Industry 2001. This is relevant for all following cross-sectional analysis

sections.)

From the cross-sectional analysis, it became apparent that Apple does not have

comparable financials to use against Hewlett-Packard. Gateway and Dell are on much

more of a level base, therefore Apple has been excluded from the industry average.

This type of event can be caused by Apple being focused on a different product base.

These differences cause Apple to usually be well above the industry average. This was

done in order to keep the average consistent with the industry itself.

Current Ratio 2001 2002 2003 2004 2005Hewlett-Packard 1.52 1.48 1.54 1.5 1.35Apple 3.39 3.25 2.5 2.63 2.96Dell 1.43 1.48 1.03 1.19 1.11Gateway 1.85 2.08 1.67 1.2 1.21Industry Average 1.6 1.68 1.41 1.30 1.22

31

Current Ratio

0

0.5

1

1.5

2

2.5

3

3.5

4

2001 2002 2003 2004 2005

Hewlett-PackardAppleDell GatewayIndustry Average

Current Ratio= Current Assets/Current Liabilities

The current ratio is a way of showing the firm’s short term liquidity. Analysts say

that a current ratio above one shows favorability. When the current ratio is above one

it shows that a firm can cover its current liabilities with their current cash assets. As

shown above, Hewlett-Packard is right at the industry average. They have an average

current ratio of approximately 1.5, which is just above the industrial average. While

analysts believe one is good current ratio, he preferred current ratio by many bankers is

2. This is because too high of a number indicates an excess of unutilized assets, while

too low of a number can imply that there is not enough cash on hand to cover their

liabilities.

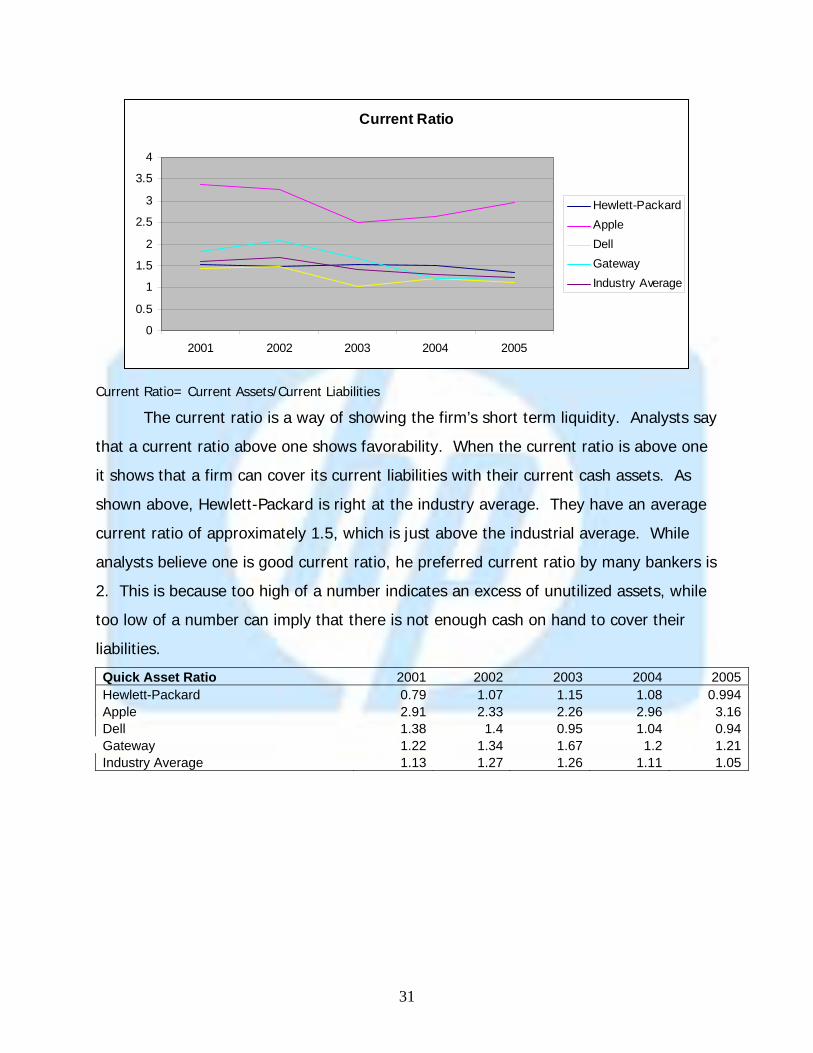

Quick Asset Ratio 2001 2002 2003 2004 2005Hewlett-Packard 0.79 1.07 1.15 1.08 0.994Apple 2.91 2.33 2.26 2.96 3.16Dell 1.38 1.4 0.95 1.04 0.94Gateway 1.22 1.34 1.67 1.2 1.21Industry Average 1.13 1.27 1.26 1.11 1.05

32

Quick Asset Ratio

0

0.5

1

1.5

2

2.5

3

3.5

2001 2002 2003 2004 2005

Hewlett-PackardAppleDell GatewayIndustry Average

Quick Asset Ratio= Cash+ Securities+ Accounts Receivable/ Current Liabilities

The quick asset ratio is somewhat similar to the current ratio, except it only

utilizes the cash and cash equivalent assets in its calculation. A higher quick asset ratio

shows that your company is more liquid. Hewlett-Packard is below the industry

average due to the cash outflows associated with the acquisition of other companies.

This cash outflow also increased their liabilities, driving the ratio down. The industry is

seen as being relatively consistent with one another.

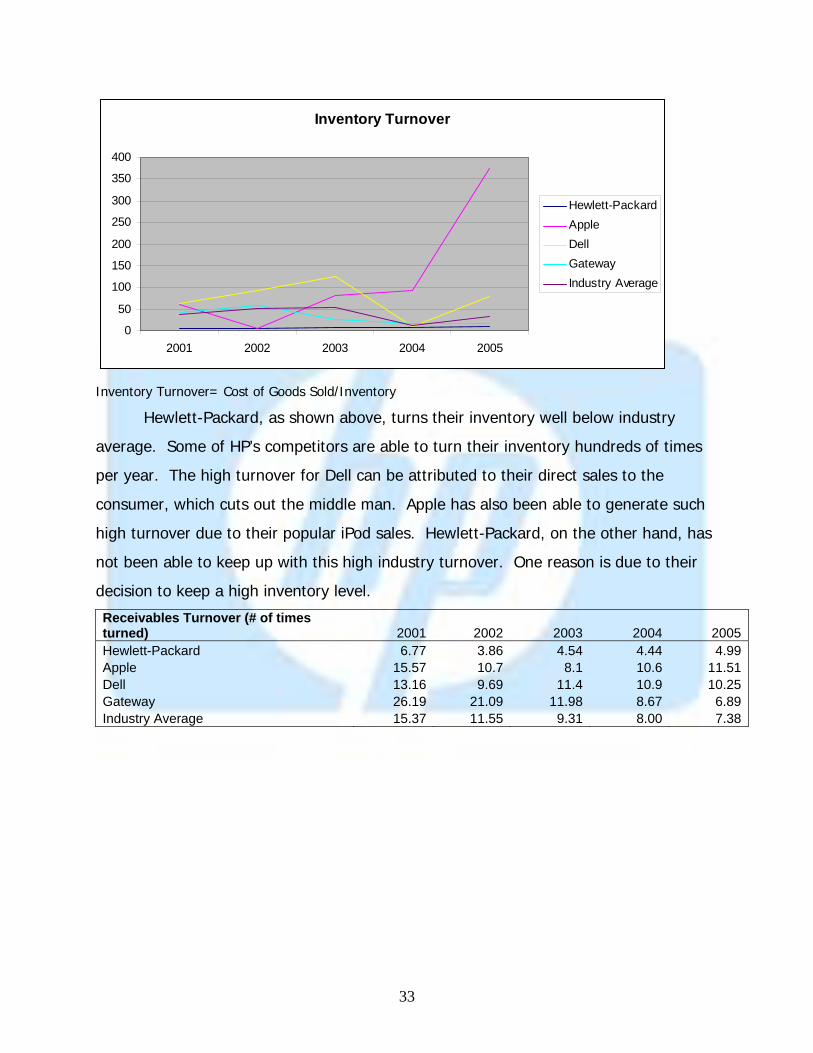

Inventory Turnover (# of times turned) 2001 2002 2003 2004 2005Hewlett-Packard 6.43 7.21 8.88 8.6 9.66Apple 59.93 5.96 80.34 91.98 375.27Dell 63.61 91.27 126.74 10.81 79.78Gateway 42.4 57.45 25.74 17.03 16.1Industry Average 37.48 51.98 53.79 12.15 35.18

33

Inventory Turnover

0

50

100

150

200

250

300

350

400

2001 2002 2003 2004 2005

Hewlett-PackardAppleDell GatewayIndustry Average

Inventory Turnover= Cost of Goods Sold/Inventory

Hewlett-Packard, as shown above, turns their inventory well below industry

average. Some of HP’s competitors are able to turn their inventory hundreds of times

per year. The high turnover for Dell can be attributed to their direct sales to the

consumer, which cuts out the middle man. Apple has also been able to generate such

high turnover due to their popular iPod sales. Hewlett-Packard, on the other hand, has

not been able to keep up with this high industry turnover. One reason is due to their

decision to keep a high inventory level.

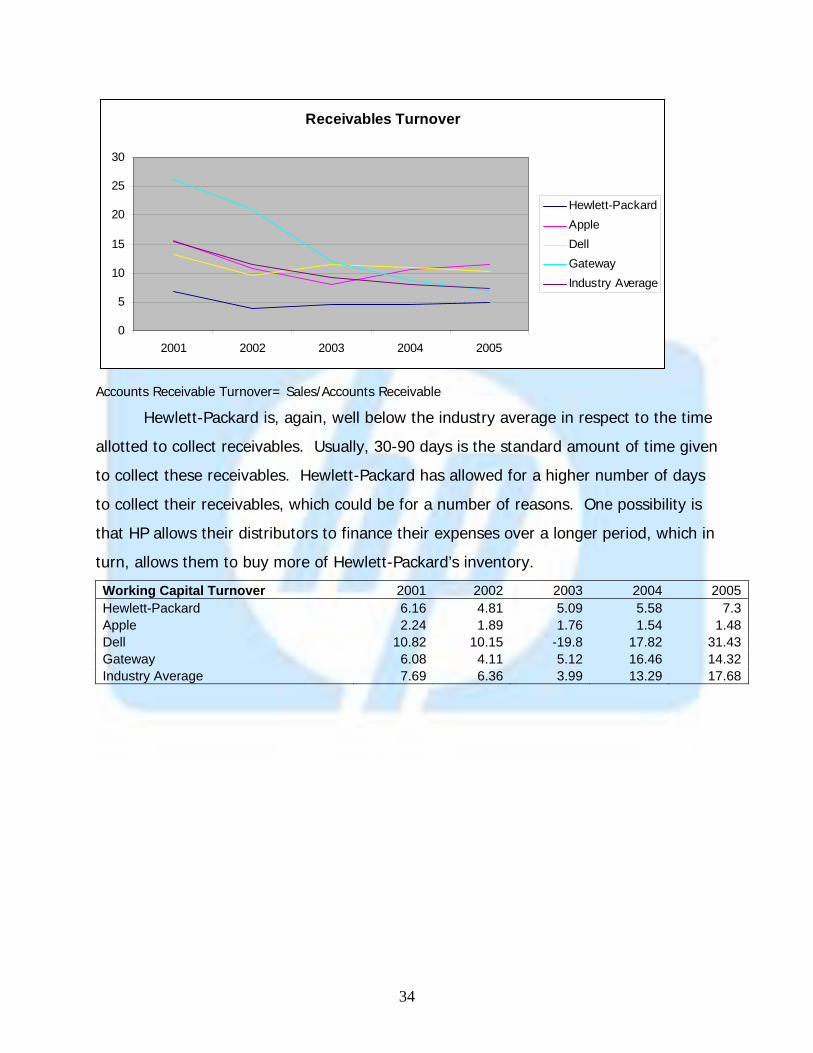

Receivables Turnover (# of times turned) 2001 2002 2003 2004 2005Hewlett-Packard 6.77 3.86 4.54 4.44 4.99Apple 15.57 10.7 8.1 10.6 11.51Dell 13.16 9.69 11.4 10.9 10.25Gateway 26.19 21.09 11.98 8.67 6.89Industry Average 15.37 11.55 9.31 8.00 7.38

34

Receivables Turnover

0

5

10

15

20

25

30

2001 2002 2003 2004 2005

Hewlett-PackardAppleDellGatewayIndustry Average

Accounts Receivable Turnover= Sales/Accounts Receivable

Hewlett-Packard is, again, well below the industry average in respect to the time

allotted to collect receivables. Usually, 30-90 days is the standard amount of time given

to collect these receivables. Hewlett-Packard has allowed for a higher number of days

to collect their receivables, which could be for a number of reasons. One possibility is

that HP allows their distributors to finance their expenses over a longer period, which in

turn, allows them to buy more of Hewlett-Packard’s inventory.

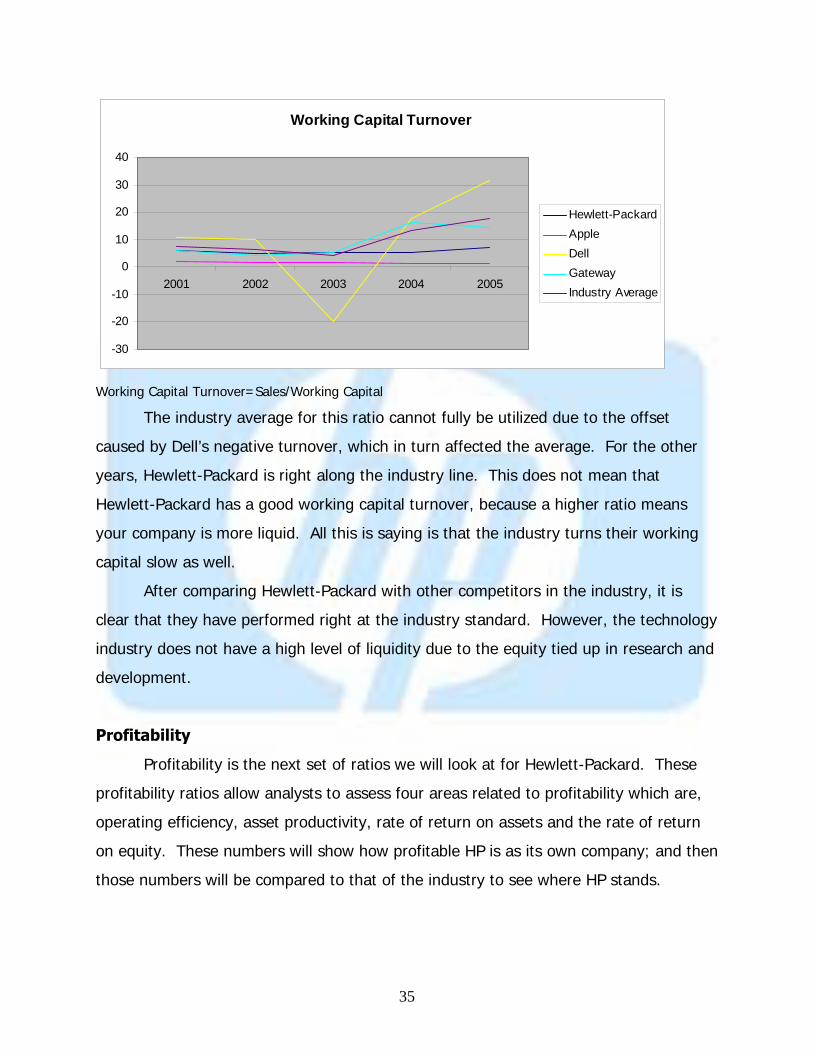

Working Capital Turnover 2001 2002 2003 2004 2005Hewlett-Packard 6.16 4.81 5.09 5.58 7.3Apple 2.24 1.89 1.76 1.54 1.48Dell 10.82 10.15 -19.8 17.82 31.43Gateway 6.08 4.11 5.12 16.46 14.32Industry Average 7.69 6.36 3.99 13.29 17.68

35

Working Capital Turnover

-30

-20

-10

0

10

20

30

40

2001 2002 2003 2004 2005

Hewlett-PackardAppleDellGatewayIndustry Average

Working Capital Turnover=Sales/Working Capital

The industry average for this ratio cannot fully be utilized due to the offset

caused by Dell’s negative turnover, which in turn affected the average. For the other

years, Hewlett-Packard is right along the industry line. This does not mean that

Hewlett-Packard has a good working capital turnover, because a higher ratio means

your company is more liquid. All this is saying is that the industry turns their working

capital slow as well.

After comparing Hewlett-Packard with other competitors in the industry, it is

clear that they have performed right at the industry standard. However, the technology

industry does not have a high level of liquidity due to the equity tied up in research and

development.

Profitability

Profitability is the next set of ratios we will look at for Hewlett-Packard. These

profitability ratios allow analysts to assess four areas related to profitability which are,

operating efficiency, asset productivity, rate of return on assets and the rate of return

on equity. These numbers will show how profitable HP is as its own company; and then

those numbers will be compared to that of the industry to see where HP stands.

36

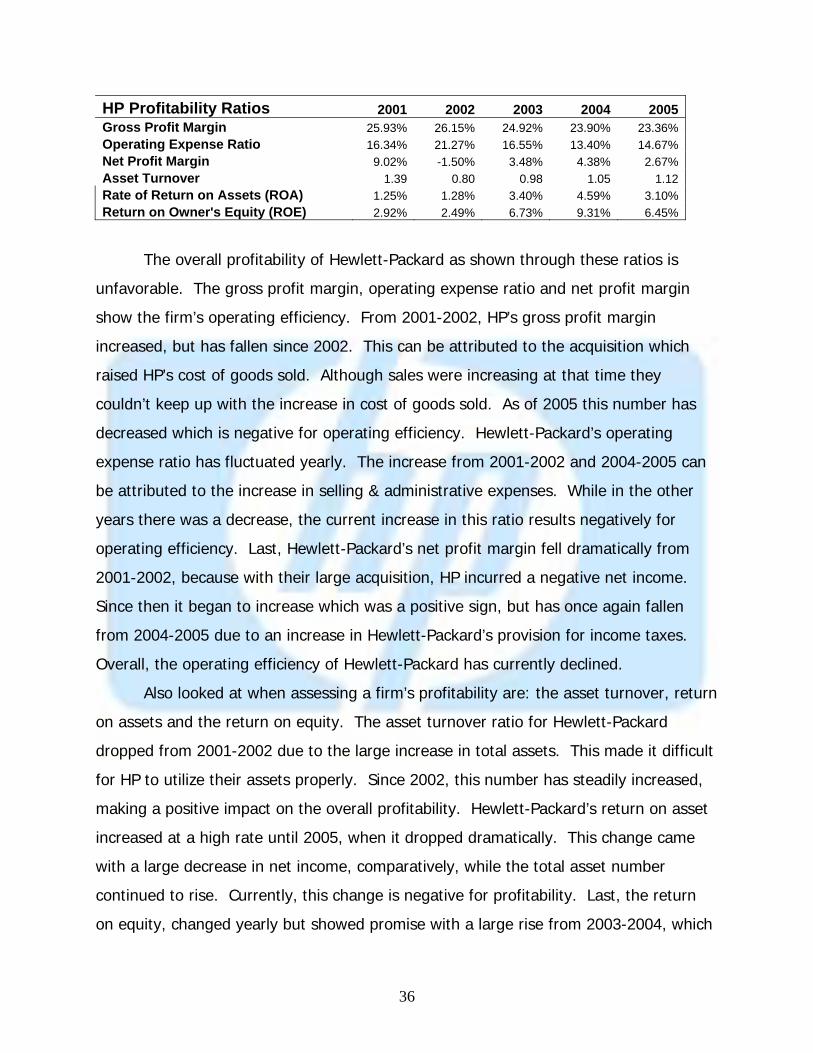

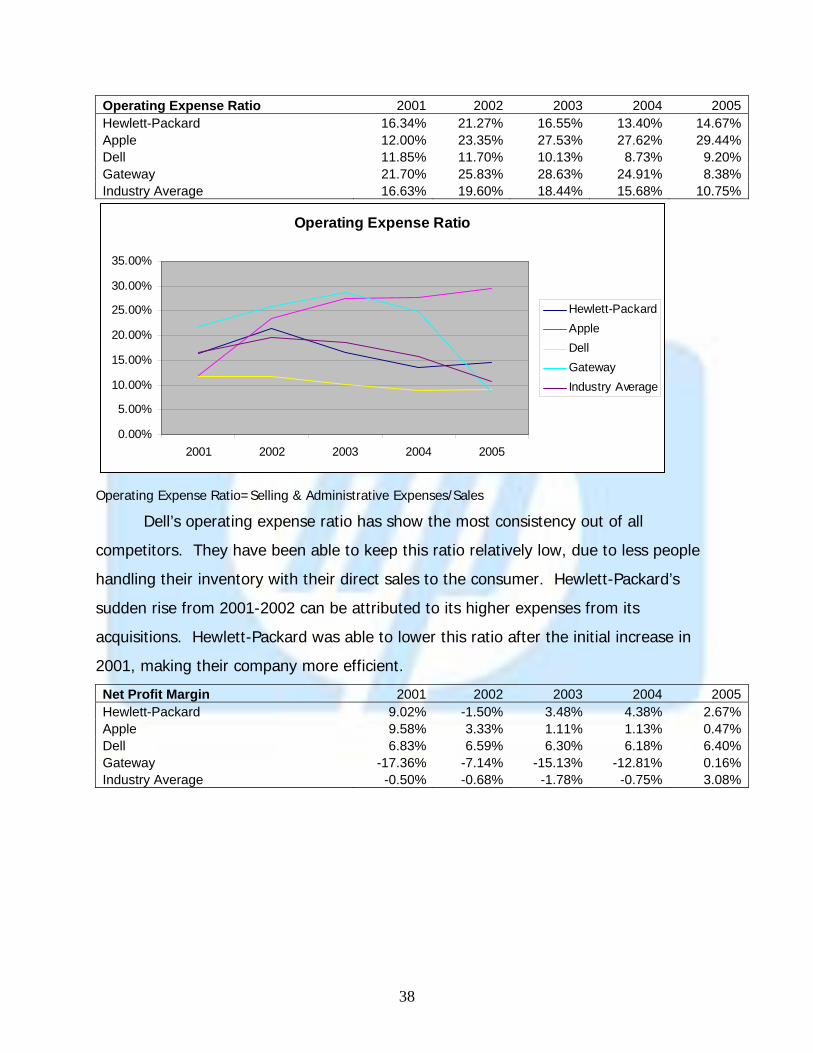

HP Profitability Ratios 2001 2002 2003 2004 2005Gross Profit Margin 25.93% 26.15% 24.92% 23.90% 23.36% Operating Expense Ratio 16.34% 21.27% 16.55% 13.40% 14.67% Net Profit Margin 9.02% -1.50% 3.48% 4.38% 2.67% Asset Turnover 1.39 0.80 0.98 1.05 1.12 Rate of Return on Assets (ROA) 1.25% 1.28% 3.40% 4.59% 3.10% Return on Owner's Equity (ROE) 2.92% 2.49% 6.73% 9.31% 6.45%

The overall profitability of Hewlett-Packard as shown through these ratios is

unfavorable. The gross profit margin, operating expense ratio and net profit margin

show the firm’s operating efficiency. From 2001-2002, HP’s gross profit margin

increased, but has fallen since 2002. This can be attributed to the acquisition which

raised HP’s cost of goods sold. Although sales were increasing at that time they

couldn’t keep up with the increase in cost of goods sold. As of 2005 this number has

decreased which is negative for operating efficiency. Hewlett-Packard’s operating

expense ratio has fluctuated yearly. The increase from 2001-2002 and 2004-2005 can

be attributed to the increase in selling & administrative expenses. While in the other

years there was a decrease, the current increase in this ratio results negatively for

operating efficiency. Last, Hewlett-Packard’s net profit margin fell dramatically from

2001-2002, because with their large acquisition, HP incurred a negative net income.

Since then it began to increase which was a positive sign, but has once again fallen

from 2004-2005 due to an increase in Hewlett-Packard’s provision for income taxes.

Overall, the operating efficiency of Hewlett-Packard has currently declined.

Also looked at when assessing a firm’s profitability are: the asset turnover, return

on assets and the return on equity. The asset turnover ratio for Hewlett-Packard

dropped from 2001-2002 due to the large increase in total assets. This made it difficult

for HP to utilize their assets properly. Since 2002, this number has steadily increased,

making a positive impact on the overall profitability. Hewlett-Packard’s return on asset

increased at a high rate until 2005, when it dropped dramatically. This change came

with a large decrease in net income, comparatively, while the total asset number

continued to rise. Currently, this change is negative for profitability. Last, the return

on equity, changed yearly but showed promise with a large rise from 2003-2004, which

37

was followed by a drastic drop again in 2005. This negative factor can be attributed to

the lower amount of owner’s equity from 2004-2005, due to a lower common stock

from share buybacks.

These ratios collectively show an unfavorable profitability standing for Hewlett-

Packard. This could be attributed to the high research and development needed to stay

competitive in the technology industry.

Cross-Sectional Analysis

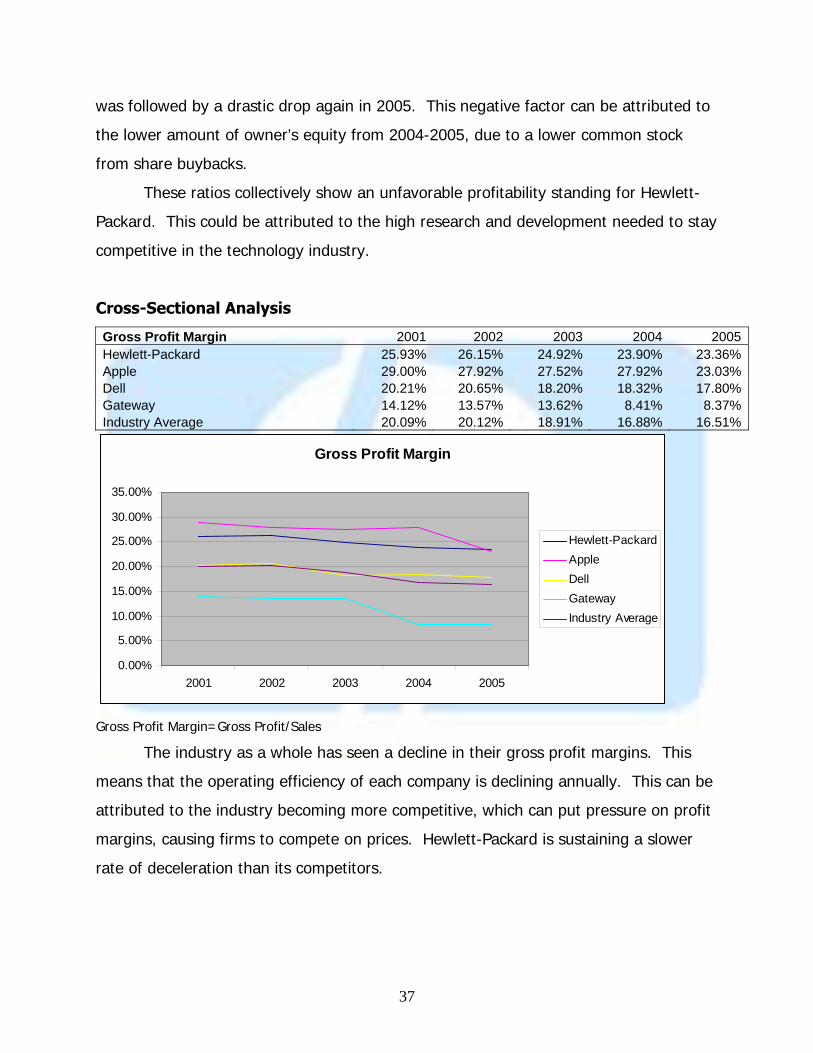

Gross Profit Margin 2001 2002 2003 2004 2005Hewlett-Packard 25.93% 26.15% 24.92% 23.90% 23.36%Apple 29.00% 27.92% 27.52% 27.92% 23.03%Dell 20.21% 20.65% 18.20% 18.32% 17.80%Gateway 14.12% 13.57% 13.62% 8.41% 8.37%Industry Average 20.09% 20.12% 18.91% 16.88% 16.51%

Gross Profit Margin

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

2001 2002 2003 2004 2005

Hewlett-PackardAppleDellGatewayIndustry Average

Gross Profit Margin=Gross Profit/Sales

The industry as a whole has seen a decline in their gross profit margins. This

means that the operating efficiency of each company is declining annually. This can be

attributed to the industry becoming more competitive, which can put pressure on profit

margins, causing firms to compete on prices. Hewlett-Packard is sustaining a slower

rate of deceleration than its competitors.

38

Operating Expense Ratio 2001 2002 2003 2004 2005Hewlett-Packard 16.34% 21.27% 16.55% 13.40% 14.67%Apple 12.00% 23.35% 27.53% 27.62% 29.44%Dell 11.85% 11.70% 10.13% 8.73% 9.20%Gateway 21.70% 25.83% 28.63% 24.91% 8.38%Industry Average 16.63% 19.60% 18.44% 15.68% 10.75%

Operating Expense Ratio

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

2001 2002 2003 2004 2005

Hewlett-PackardAppleDellGatewayIndustry Average

Operating Expense Ratio=Selling & Administrative Expenses/Sales

Dell’s operating expense ratio has show the most consistency out of all

competitors. They have been able to keep this ratio relatively low, due to less people

handling their inventory with their direct sales to the consumer. Hewlett-Packard’s

sudden rise from 2001-2002 can be attributed to its higher expenses from its

acquisitions. Hewlett-Packard was able to lower this ratio after the initial increase in

2001, making their company more efficient.

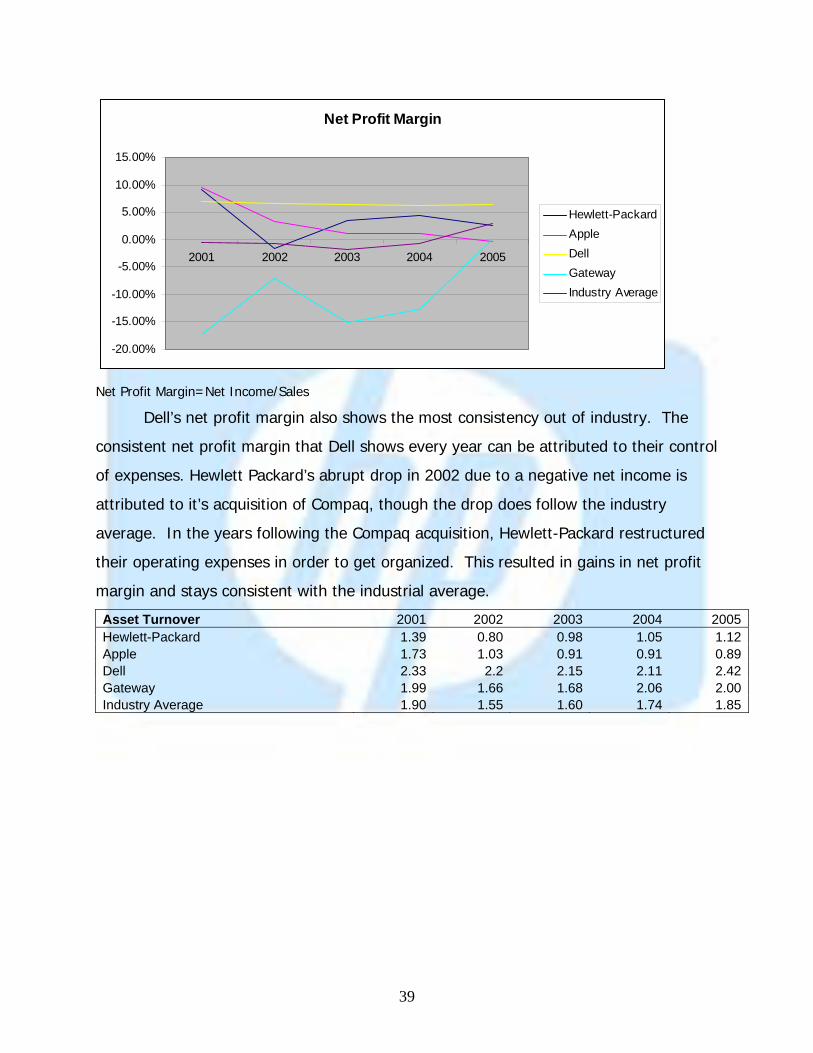

Net Profit Margin 2001 2002 2003 2004 2005Hewlett-Packard 9.02% -1.50% 3.48% 4.38% 2.67%Apple 9.58% 3.33% 1.11% 1.13% 0.47%Dell 6.83% 6.59% 6.30% 6.18% 6.40%Gateway -17.36% -7.14% -15.13% -12.81% 0.16%Industry Average -0.50% -0.68% -1.78% -0.75% 3.08%

39

Net Profit Margin

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

2001 2002 2003 2004 2005

Hewlett-PackardAppleDellGatewayIndustry Average

Net Profit Margin=Net Income/Sales

Dell’s net profit margin also shows the most consistency out of industry. The

consistent net profit margin that Dell shows every year can be attributed to their control

of expenses. Hewlett Packard’s abrupt drop in 2002 due to a negative net income is

attributed to it’s acquisition of Compaq, though the drop does follow the industry

average. In the years following the Compaq acquisition, Hewlett-Packard restructured

their operating expenses in order to get organized. This resulted in gains in net profit

margin and stays consistent with the industrial average.

Asset Turnover 2001 2002 2003 2004 2005Hewlett-Packard 1.39 0.80 0.98 1.05 1.12Apple 1.73 1.03 0.91 0.91 0.89Dell 2.33 2.2 2.15 2.11 2.42Gateway 1.99 1.66 1.68 2.06 2.00Industry Average 1.90 1.55 1.60 1.74 1.85

40

Asset Turnover

0.00

0.50

1.00

1.50

2.00

2.50

3.00

2001 2002 2003 2004 2005

Hewlett-PackardAppleDellGatewayIndustry Average

Asset Turnover=Sales/Total Assets

Asset turnover is the measure of the revenue productivity of all available

resources employed by a company. The greater the asset turnover is, the greater the

utilization of resources is. Hewlett Packard remains to below the industry average each

year. From 2001 to 2002, HP’s assets more than doubled while their sales only

increased by 11%. However, HP does show that they can allocate their resources

better in the following years and pass Apple’s turnover. Both Dell and Gateway’s asset

turnover remain above their competitors and the industry average. The industry

average over the past 5 years shows that for every dollar of assets results in

approximately $1 of sales. Although those companies with low asset turnover, it

remains true that they will have an average higher gross profit margin.

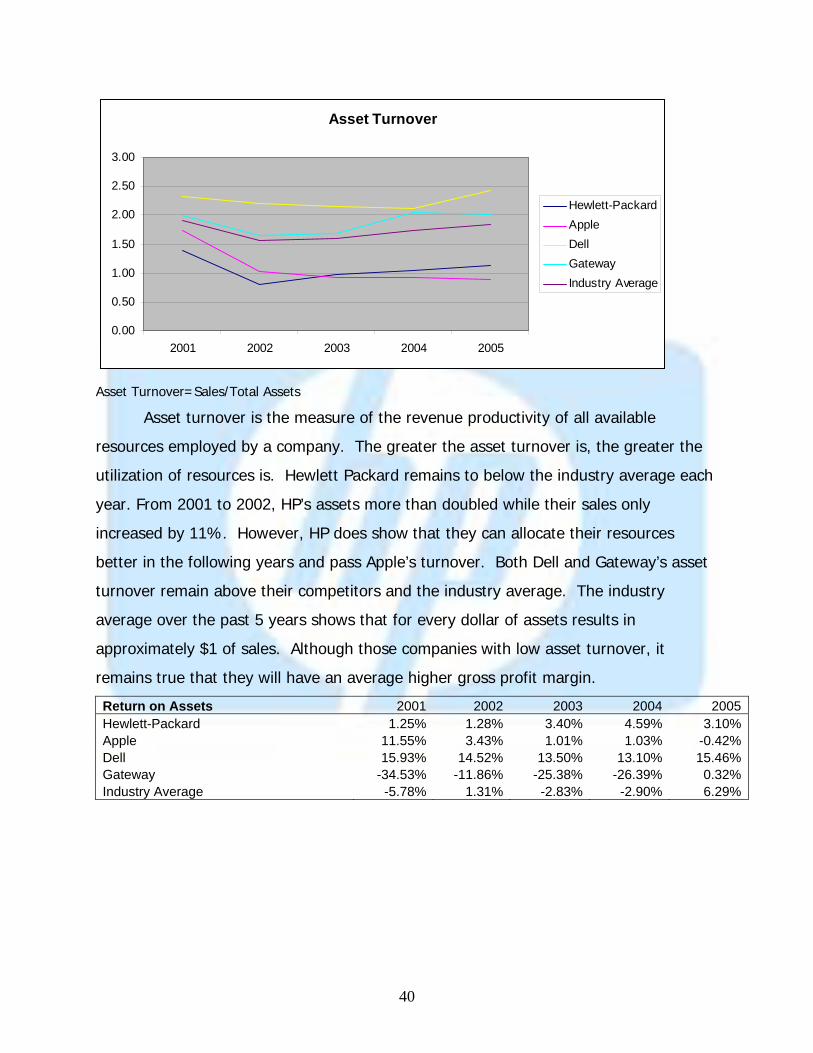

Return on Assets 2001 2002 2003 2004 2005Hewlett-Packard 1.25% 1.28% 3.40% 4.59% 3.10%Apple 11.55% 3.43% 1.01% 1.03% -0.42%Dell 15.93% 14.52% 13.50% 13.10% 15.46%Gateway -34.53% -11.86% -25.38% -26.39% 0.32%Industry Average -5.78% 1.31% -2.83% -2.90% 6.29%

41

Return on Assets

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

2001 2002 2003 2004 2005

Hewlett-PackardAppleDellGatewayIndustry Average

Return on Assets=Net Income/Total Assets

This profitability ratio is affected by operating efficiency and asset productivity.

It measures the overall profitability of a company. Dell continues to be the industry

leader, consistently by high above the industry average. Gateway sets the bar very low

compared to Dell and the industry average as they struggle to cut their costs and

maintain stability. Apple’s return on assets is also low, but not as much with respect to

the volatile Gateway. Hewlett Packard rates between Dell and Apple while showing

some promise as their overall trend in the past 5 years continue to inch closer to the

industry average. One reason HP remains below the industry average is that they spend

more than 5 times the amount on Research and Development then their two closest

competitors, Apple and Dell. Still, HP needs to show some “improvements in cutting

costs and its efficiency, as it will be striving to do the next couple years as they cut

jobs.” 11

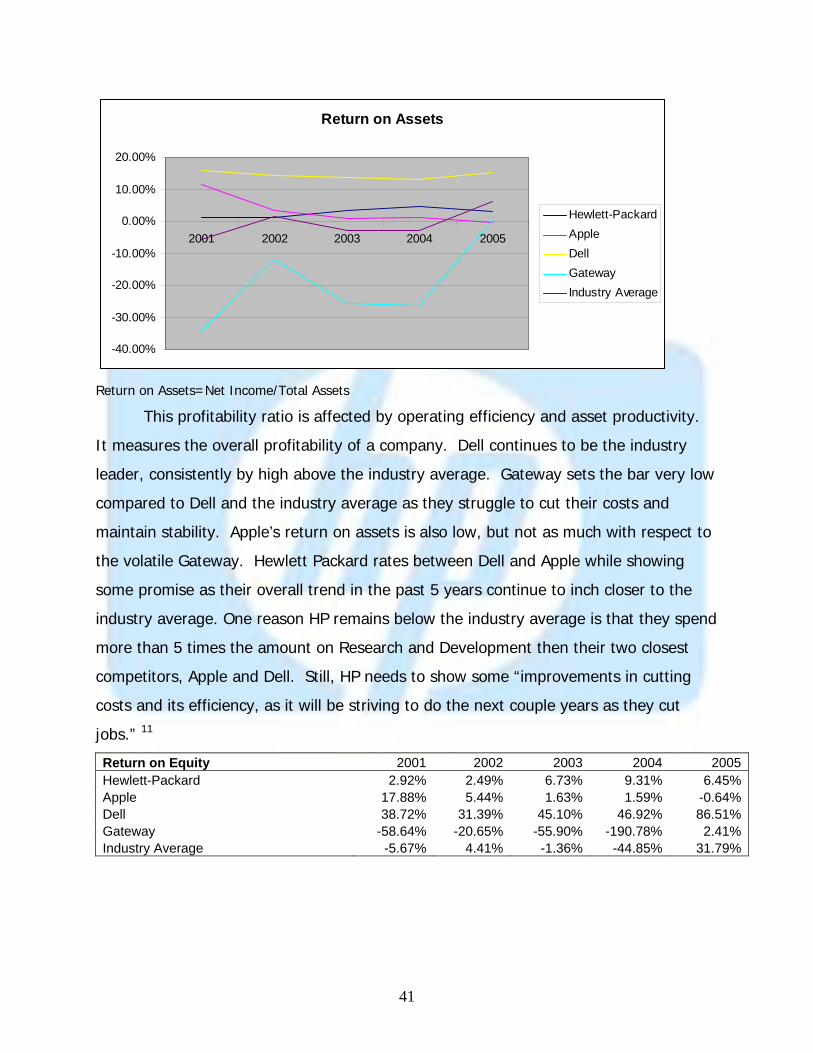

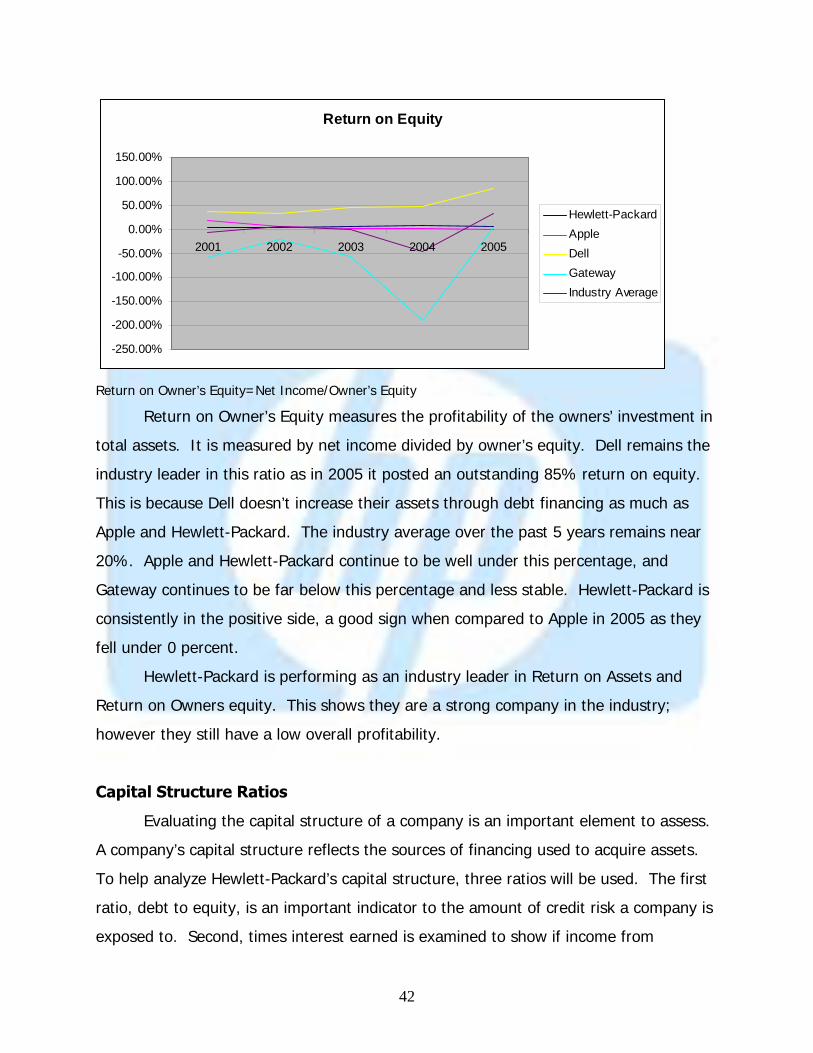

Return on Equity 2001 2002 2003 2004 2005Hewlett-Packard 2.92% 2.49% 6.73% 9.31% 6.45%Apple 17.88% 5.44% 1.63% 1.59% -0.64%Dell 38.72% 31.39% 45.10% 46.92% 86.51%Gateway -58.64% -20.65% -55.90% -190.78% 2.41%Industry Average -5.67% 4.41% -1.36% -44.85% 31.79%

42

Return on Equity

-250.00%

-200.00%

-150.00%

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

2001 2002 2003 2004 2005

Hewlett-PackardAppleDellGatewayIndustry Average

Return on Owner’s Equity=Net Income/Owner’s Equity

Return on Owner’s Equity measures the profitability of the owners’ investment in

total assets. It is measured by net income divided by owner’s equity. Dell remains the

industry leader in this ratio as in 2005 it posted an outstanding 85% return on equity.

This is because Dell doesn’t increase their assets through debt financing as much as

Apple and Hewlett-Packard. The industry average over the past 5 years remains near

20%. Apple and Hewlett-Packard continue to be well under this percentage, and

Gateway continues to be far below this percentage and less stable. Hewlett-Packard is

consistently in the positive side, a good sign when compared to Apple in 2005 as they

fell under 0 percent.

Hewlett-Packard is performing as an industry leader in Return on Assets and

Return on Owners equity. This shows they are a strong company in the industry;

however they still have a low overall profitability.

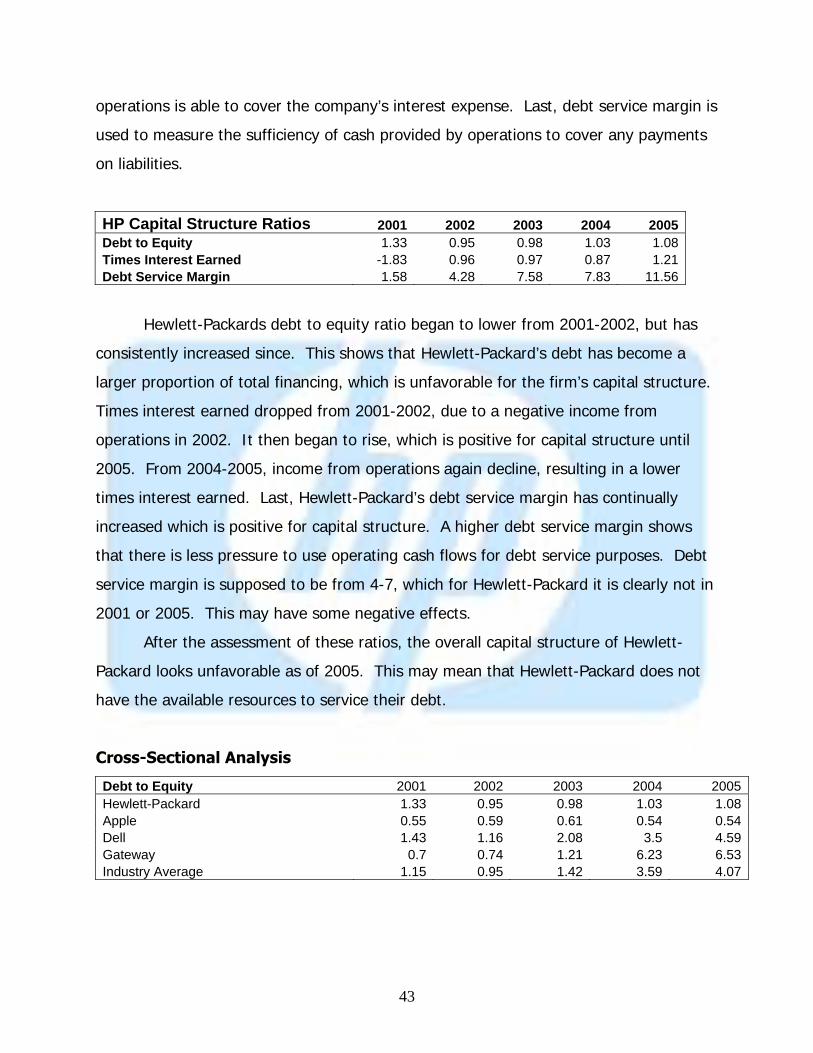

Capital Structure Ratios

Evaluating the capital structure of a company is an important element to assess.

A company’s capital structure reflects the sources of financing used to acquire assets.

To help analyze Hewlett-Packard’s capital structure, three ratios will be used. The first

ratio, debt to equity, is an important indicator to the amount of credit risk a company is

exposed to. Second, times interest earned is examined to show if income from

43

operations is able to cover the company’s interest expense. Last, debt service margin is

used to measure the sufficiency of cash provided by operations to cover any payments

on liabilities.

HP Capital Structure Ratios 2001 2002 2003 2004 2005Debt to Equity 1.33 0.95 0.98 1.03 1.08Times Interest Earned -1.83 0.96 0.97 0.87 1.21Debt Service Margin 1.58 4.28 7.58 7.83 11.56

Hewlett-Packards debt to equity ratio began to lower from 2001-2002, but has

consistently increased since. This shows that Hewlett-Packard’s debt has become a

larger proportion of total financing, which is unfavorable for the firm’s capital structure.

Times interest earned dropped from 2001-2002, due to a negative income from

operations in 2002. It then began to rise, which is positive for capital structure until

2005. From 2004-2005, income from operations again decline, resulting in a lower

times interest earned. Last, Hewlett-Packard’s debt service margin has continually

increased which is positive for capital structure. A higher debt service margin shows

that there is less pressure to use operating cash flows for debt service purposes. Debt

service margin is supposed to be from 4-7, which for Hewlett-Packard it is clearly not in

2001 or 2005. This may have some negative effects.

After the assessment of these ratios, the overall capital structure of Hewlett-

Packard looks unfavorable as of 2005. This may mean that Hewlett-Packard does not

have the available resources to service their debt.

Cross-Sectional Analysis

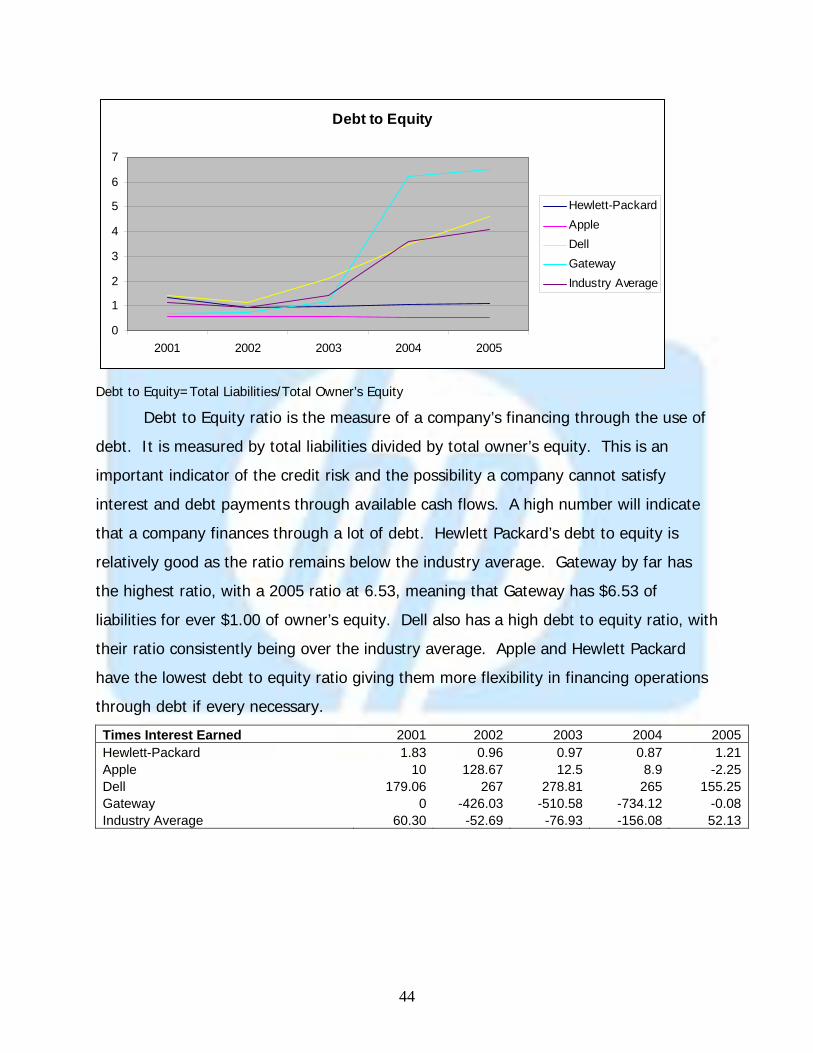

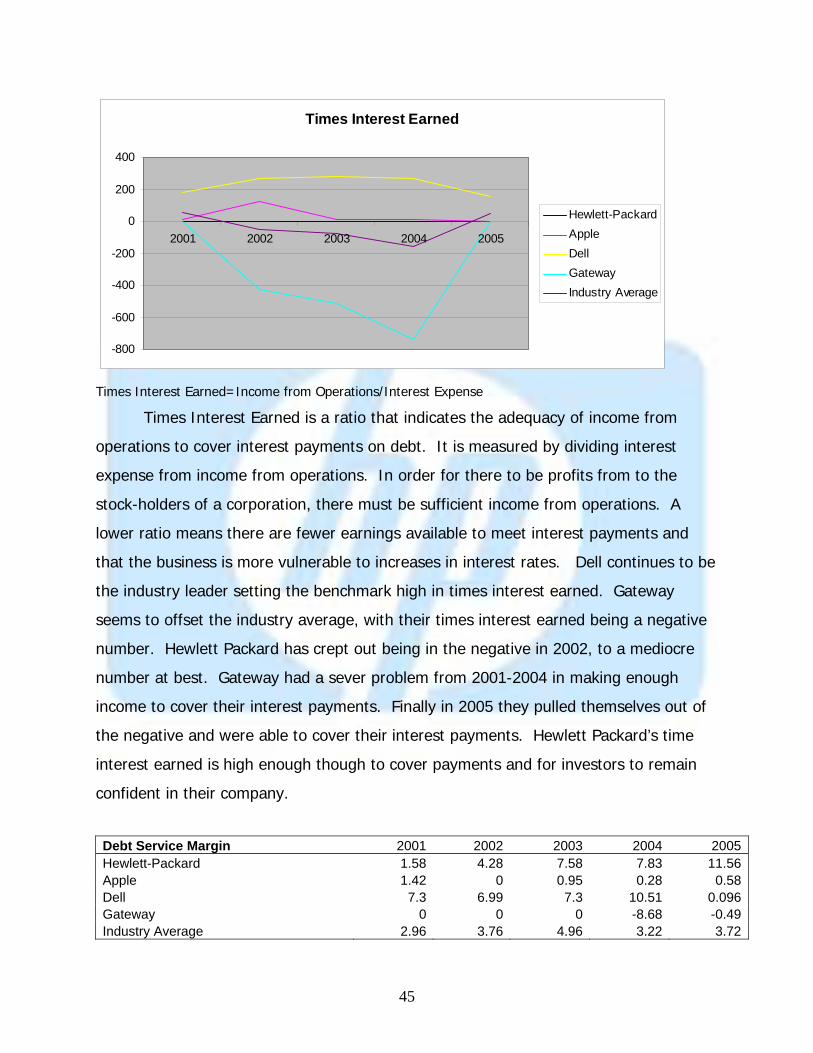

Debt to Equity 2001 2002 2003 2004 2005Hewlett-Packard 1.33 0.95 0.98 1.03 1.08Apple 0.55 0.59 0.61 0.54 0.54Dell 1.43 1.16 2.08 3.5 4.59Gateway 0.7 0.74 1.21 6.23 6.53Industry Average 1.15 0.95 1.42 3.59 4.07

44

Debt to Equity

0

1

2

3

4

5

6

7