Hedge Fund Investment Strategies -Final

19

HEDGE FUNDS AN OVERVIEW AND INVESTMENT STRATEGIES Maniranjan Kumar

-

Upload

killmyklone -

Category

Documents

-

view

218 -

download

0

Transcript of Hedge Fund Investment Strategies -Final

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 1/20

HEDGE FUNDSAN OVERVIEW AND INVESTMENT STRA

Maniranjan Kumar

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 2/20

Hedge Funds aren’t hedged. On the contrary, they are illiquid, quite leverag

and failure prone. However, most Hedge Funds do produce returns at lower s

exhibit low tail risk and low correlations with bond portfolios, in particular.

Despite negative publicity and lack of transparency, Hedge Funds have mushr

continued to attract assets. There’re about 8,000 of them with $2.25 trilliothese funds are normally classified in four buckets, namely Relative Value, Eve

Hedge and Tactical Trading. Of these, Fundamental Value strategy in Equity

Situations and Distressed/Restructuring in Event Driven, Discretionary Themati

Diversified in Tactical Trading, and Fixed Income Arbitrage in Relative Value a

As examples, BHEL can be a case study for a Fundamental Value trade, S

Situations, Indian Rupee for Discretionary Thematic, and India VIX inde

Arbitrage. However, most Hedge Fund strategies are difficult to employ in Ind

liquidity, leverage needs, regulations, public scrutiny or an unavailability of ins

However, Hedge Funds can be evil, very evil. Amaranth, Tiger and LTCM are p

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 3/20

Hedge Funds are leveraged, illiquid, unregula

likely-to-fail but can produce returns at lower

Hedge Funds Mutual Funds Private Equity Venture Capital

Leverage Highly levered up

to 20-30 times

Unlevered almost

always

Except LBO deals,

others unlevered

Unlevered

Liquidity 1 day to many

years

Daily 8-10 years except

exits

3-8 years except

exits

Investment

Horizon

1 day to many

years

Medium-to-long

term, in general

Long-term Long-term

Public or Private Private Public Private Private

Return

Expectations

Uncorrelated and

lower sharpe

Track the market

benchmark

Between 10-25% Around 25%

Active or Passive Active trading but

passive investments

Mostly passive

investments

Mostly active

investments

Very active

investments

Risks Unregulated, very

risky, many fail

Highly regulated,

low returns

Long gestation,

mediocre returns

Long gestation,

7-2-1 model

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 4/20

Hedge Funds outperform stocks, bonds and co

with higher Sharpe ratio and lower tail risk

Source: S&P, Barclays, Dow Jones, HFRI

0%

2%

4%

6%

8%

10%

12%

0% 5% 10% 15% 20%

A n n u a l i z e d R e t u r n

Annualized Standard Deviation

Jan 92 –

Jun 12

S&P 500 Total Return IndexBarclays Capital Global Aggregate Bond IndexDow Jones UBS Commodity (TR) Index

HFRI Fund Weighted Composite Index

S&P 500

Total

Return

BarclaCapita

Globa

Aggre

Bond

Cumulative Return 493% 3

Annualized Return 8%

Annualized Std Deviation 15%

Sharpe Ratio 0.27

Max monthly drawdown -17%

Date max mthly

drawdown 31 Oct 08 30 No

% Positive returns 64%

Skew -0.67 -

Kurtosis 1.18

VaR 99% (Historical) 27%

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 5/20

There are diversification benefits with Hedge

particularly low correlations with bond portfo

Source: NBER, S&P, Barclays, Dow Jones, HFRI

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

J a n 9 5

J a n 9 6

J a n 9 7

J a n 9 8

J a n 9 9

J a n 0 0

J a n 0 1

J a n 0 2

J a n 0 3

J a n 0 4

J a n 0 5

J a n 0 6

J a n 0 7

J a n 0 8

3 year rolling correlation with HFRI fund weighted composite index from Dec 1991 thr

S&P 500 Total Return Index Barclays Capital Global Aggregate Bond Index Dow Jones U

Shaded a

(Mar 01-

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 6/20

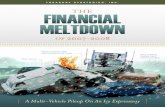

There are selection and survivorship biases in

but evidences do prove that Hedge Funds out

Source: NBER, S&P, Barclays, Dow Jones, HFRI, KPMG

0

100

200

300

400

500

600

700

800

900

D e c 9 1

D e c 9 2

D e c 9 3

D e c 9 4

D e c 9 5

D e c 9 6

D e c 9 7

D e c 9 8

D e c 9 9

D e c 0 0

D e c 0 1

D e c 0 2

D e c 0 3

D e c 0 4

D e c 0 5

D e c 0 6

D e c 0 7

D e c 0 8

D e c 0 9

D e c 1 0

D e c 1 1

Cumulative Returns of asset classes from Dec 1991 through Jun 2012

S&P 500 Total Return Index Barclays Capital Global Aggregate Bond Index

Dow Jones UBS Commodity (TR) Index HFRI Fund Weighted Composite Index

Shaded areas include US recessions

(Mar 01-Nov 01 & Dec 07-Jun 09)

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 7/20

The industry has grown consistently and is now

consolidating and commoditizing, to an exten

Source: HFRI

(5,00,000)

0

5,00,000

10,00,000

15,00,000

20,00,000

25,00,000Estimated Asset Flow ($ mm)

Estimated Assets ($ mm)

Estimated # of Funds (ex FoFs)

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 8/20

It is difficult to classify Hedge Funds due to a

range of styles and strategies that are deplo

Relative Value Event Driven Equity Hedge Ta

FIXED INCOME

Sovereign

Corporates

Asset Backed

Convertible Arbitrage

EQUITY

Merger Arbitrage

Special Situations

Activist

Private Issue/ Regulation D

FUNDAMENTAL

Equity Market Neutral

Long-Only / Long-Bias

Long / Short

Short-Only / Short-Bias

Geography-Specific

Sector-Specific

Dis

Sy

VOLATILITY

ConvertiblesDerivatives

MULTI-STRATEGY MULTI-STRATEGY MULTI-STRATEGY M

CREDIT

Credit Arbitrage

Distressed / Restructuring

QUANTITATIVE

Statistical Arbitrage

Factor

Diversified Equity

Multi-model

YIELD ALTERNATIVE

Energy Infrastructure

Insurance

Real Estate

MAN

Source: Credit Suisse, HFRI, Russell

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 9/20

Value (EH), Special Situations (ED), Systematic

Multi-strategy (RV) are the most sought strate

Source: HFRI

0

50,000

1,00,000

1,50,000

2,00,000

2,50,000

3,00,0003,50,000

4,00,000

I n m i l l i o n d o l l a

r s

As of June 30, 2012

1 2 3

2 3

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 10/20

Fundamental Value, classified under Equity

very popular, and it encompasses many distin

1

Passive Contrarian Activist

- Screening for market mistakes

- Low risk and high quality earnings

- P/BV < 2/3rd of BV

- P/E < 40% of 5yr average

- P/E < 1/Yield on AAA corp. bond

- Dividend yield > 2/3rd of yield on

AAA corp. bond- D/E < 1

- P < 2/3rd of Net Current Assets

- Growth in EPS in a business cycle

- Quality management

- Consistent operating history

- High and stable profit margins

- High return on equity and capital

employed

Investing in stocks where market

has overreacted

- Stocks that have had bad earnings

declines or deals that have gone

bad are likely to be under valued

- Significant negative serial

correlation in returns (bad yearsfollow good years)

Investing in bad companies

- Markets underestimate the value

of the firm quality

- On the other hand, markets

overpay for good quality firms

- Creating valu

management a

or redeployme

- Divestiture va

value of the ba

- If losing mone

down and sell - ROC < WAC

- Debt and eq

- Cost-cutting m

- Build on comp

and find new b

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 11/20

As an example, BHEL might be a good fund

value candidate, as market has most likely ov

1

2012-13* 2011-12 2010-11 2009-10 2008-09 2007-08

Average price 224.71 331.50 468.98 441.48 302.62 387.47

Price / Sales 1.14 1.70 2.78 3.06 2.57 4.91

Price / BV 1.80 3.19 5.70 6.79 5.72 8.80

Price / Earning 8.22 11.45 19.10 25.07 23.60 33.17

YoY EPS growth -5.56% 17.90% 39.47% 37.35% 9.76% 18.43%

Debt / Equity 0.09 0.01 0.01 0.01 0.01 0.01

EV / EBITDA 5.25 7.51 11.02 13.96 12.33 20.94

Dividend Yield 2.41% 1.93% 1.33% 1.06% 1.12% 0.79%

Net Profit Margin 13.91% 14.89% 14.56% 12.21% 10.87% 14.81%

ROCE / ROE 20% / 22% 28% / 28% 30% / 30% 27% / 27% 24% / 24% 26% / 27%

Order book (Rs. Cr) 1,15,200 1,27,700 1,55,100 1,44,300 1,17,000 85,200

Market Share Decreasing from about 70% in new equipment orders to 50%

Revenue growth 1.07% 15.25% 17.01% 22.30% 49.51% 11.99% * Estimated

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 12/20

Distressed Restructuring and Special Situatio

classified under Event Driven, are very similar

2

Distressed Restructuring Special Situations

- Opportunities in corporate and sovereign fixed

income instruments such as bonds, notes, loans, leases

and unpaid bills

- Instruments trading at significant discounts to FV either

due to bankruptcy proceedings or such an expectation

- Concentrate on sound companies that have taken on

too much debt (‘good company but bad balance sheet’)and that have no operational issue

- Focus on assets selling for 75 cents a dollar or less

- Typically, 60-70% of assets are successfully

restructured and target of 25-25% IRR

- Employ fundamental credit processes focused on

valuation, asset coverage and recovery and not on

actively managing turnaround

- Opportunities in equity and equi

- Employ an investment process foc

wide spectrum of corporate life cy

but not limited to distressed, bank

bankruptcy security issuance, anno

and corporate division spin-offs, a

security issuance/repurchase or co- Merger Arbitrage is a niche in its

separately

- Realization of shareholder value

occurrence of some identifiable ca

- Focus on assets about to appreci

catalyst

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 13/20

Suzlon acquired RE Power, an excellent busi

too big for the belly, now it faces a Special S

2

P&L Statement (In Cr except per share data)

Revenue 18,913.53

Net Income -4,723.96

Earnings per Share -26.58

Share Price 13.65

P/E -0.51

EBITDA Calculatio

Net Income

+ Taxes

+ Interest Expen

+ Dep. & Amor

EBITDA

Balance Sheet (In Cr except per share data)

Current Assets 14,690.89

Property, Plant & Equipment 6,588.42

Goodwill on consolidation 7,727.59

Total Assets 29,006.90

Current Liabilities 13,415.94

Other Liabilities & Provisions 912.48

Debt 13,692.35

Total Shareholder's Funds 986.13

Total Liabilities & Equity 29,006.90

Number of Shares 178

Selected Data

EBITDA/Revenue % -9.41%

Debt/EBITDA -7.70x

EBIDTA/Share -10.01

Interest Rate 13.55%

Tax Rate Consolidated

Revenue/Assets 65.20%

Enterprise Value (

Equity Market Cap

+ Debt

- Cash

Enterprise Value

EV/EBITDA

[(LTM EBITDA*6) - No of Shares

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 14/20

By lengthening the amortization of debt an

the capital, a good return can be made

2

Period

1 2 3 4 5 6 7 8

EBITDA - Capex 1,500 1,575 1,654 1,737 1,824 1,915 2011 21

Interest 700 630 560 490 420 350 280 2

Available 800 945 1,094 1,247 1,404 1,565 1,731 1,90

Beginning Debt 7,000 6,300 5,600 4,900 4,200 3,500 2,800 2,10

Amortization 700 700 700 700 700 700 700 70

For equity owners 100 245 394 547 704 865 1,031 1,20

EBITDA – Capex 1,500 Crores

Growth Rate % 5%

Debt

Amortizat

Infuse equity worth 6,692 Crores and retire debt, and economic cycle turns expansionary

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 15/20

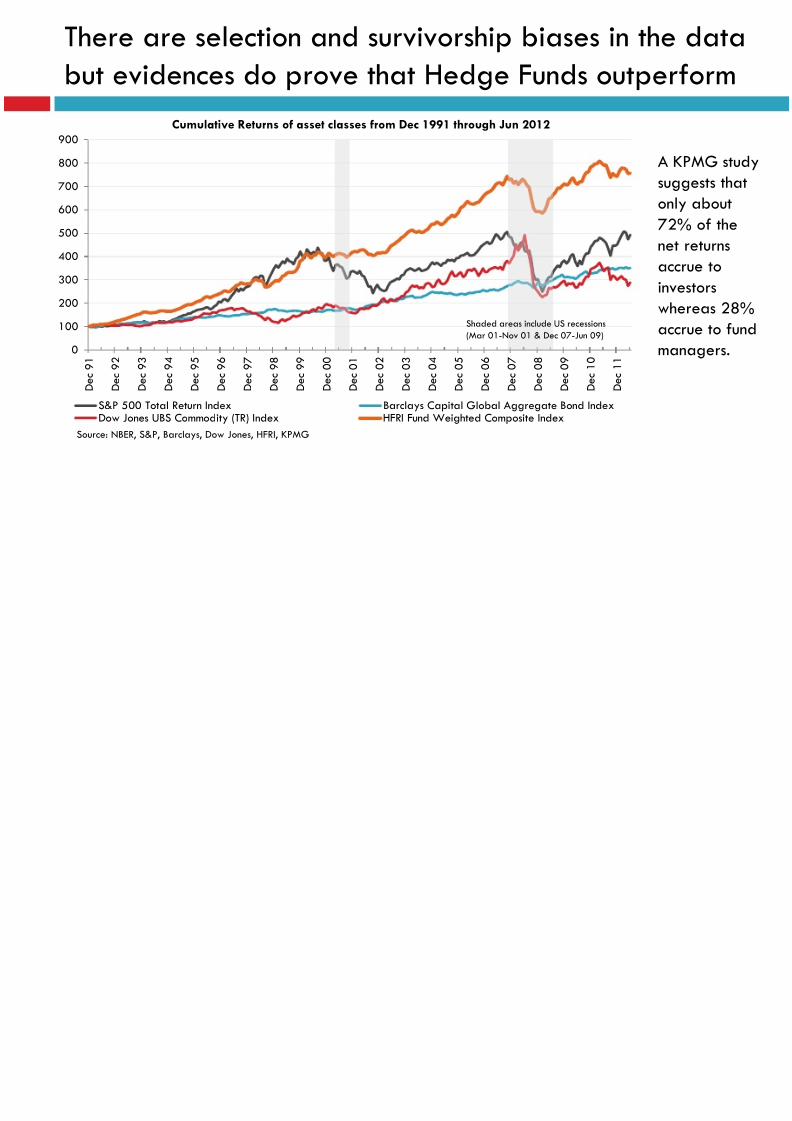

Within the Tactical Trading or Macro strate

systematic and discretionary are most used st

3

Systematic Diversified Discretionary Thematic

- Investment processes typically as function of

mathematical, algorithmic and technical models, with

little or no influence of individuals over the portfolio

positioning

- Signal based like technical analysis

- Suffer huge losses when trends reverse and model

fails or signals change

- Typically focus on highly liquid instruments and

maintain shorter holding periods of one day to one

month

- Strict stop losses and positional restrictions such as no

greater than 35% of portfolio in either dedicated

currency or commodity exposures over a given market

cycle

- Investment process most heavily i

down analysis of macroeconomic v

- Perhaps George Soros’ billion do

of England, shorting pound in 199

example

- Frequently employing spread tra

differential between instrument ide

Investment Manager to be inconsis

value

- Extremely heavy losses when ma

perhaps this is the category that w

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 16/20

A possible discretionary macro trade was b

since 2008 credit crisis to short Indian Rupee

3

0

500

1000

1500

2000

2500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 20

Gross domestic product, current prices USD Billions Total External Debt USD BillioCurrent account balance % of GDP Inflation, average consumer p

Source: IMF, World Bank, Ministry of Finance, Reserve Bank of India

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 17/20

Shorting of Rupee could be combined with

NIFTY long, as they appear inversely uncorre

3

50

52

54

56

58

60

62

64

5000

5200

5400

5600

5800

6000

6200

6400

01-Jan-13 01-Feb-13 01-Mar-13 01-Apr-13 01-May-13 01-Jun-13

Nifty

USD-INR

Source: National Stock Exchange, Reserve Bank of India

1. OnNIFTY

rollov

2. Sel

3. Ap

5% in

3. In t

may b

far-of

liquid

and m

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 18/20

Relative Value trades are predicated on re

of a spread between related yield instrumen

4

- One or multiple components of the spread typically contains a fixed income or volatility ins

- Fixed Income instruments include Asset Backed financial obligations, Convertible Bonds (for carbitrage), Sovereign Debt and Corporate Debt

- Volatility instruments are both listed and unlisted, and typically maintain characteristic sensit

implied and realized volatilities

0

10

20

30

40

50

60

70

0

1000

2000

3000

4000

5000

6000

7000

02-Mar-09 02-Mar-10 02-Mar-11 02-Mar-12 02-Mar-13

CNX Nifty

Market’s ex

short-term v

indicated nemarket since

has stayed i

Selling VIX a

could have

short volatil

trade for po

Source: National Stock Exchange

India VIX is a volatility index based on the NIFTY Index Option prices. From the best bid-ask prices of NIFTY Options contracts, acalculated which indicates the expected market volatility over the next 30 calendar days

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 19/20

Hedge Funds or not, investing in particular, or

as such, are very humbling

Amaranth Advisors

(Managed Futures) 2006 Lost$6bn of

$9bn

1. Long natural gas futures in expectation of eithestrong hurricane season

2. Energy trader Brian Hunter had made $100mm

on natural gas prices on back of hurricane Katr

Tiger Funds

(Fundamental Value)

2000 Lost

$2bn of

$22bn

1. Its not the losses but Julian Robertson’s bullishne

made him famous or rather look miserable

2. Also, his shorting of tech stocks became an irony

highs before bursting

3. He lost about $2bn on a single day move in ye

Long-term Capital

Management

(FI Sovereign)

1998 Lost

$4bn of

$4.8bn

1. The failure is even more remarkable because o

celebrated partners, Myron Scholes and Rober

prize winners of economics

2. Leverage and short volatility positions were the

$4.8bn in equity and $124.5bn in borrowings)

3. Russian default was the nail in the coffin

8/13/2019 Hedge Fund Investment Strategies -Final

http://slidepdf.com/reader/full/hedge-fund-investment-strategies-final 20/20

Thank you