Health spending 14.1% of GNP in 2002; 17.7% in 2012 Private health insurance spending = $500+...

22

-

Upload

maximilian-sharp -

Category

Documents

-

view

213 -

download

0

Transcript of Health spending 14.1% of GNP in 2002; 17.7% in 2012 Private health insurance spending = $500+...

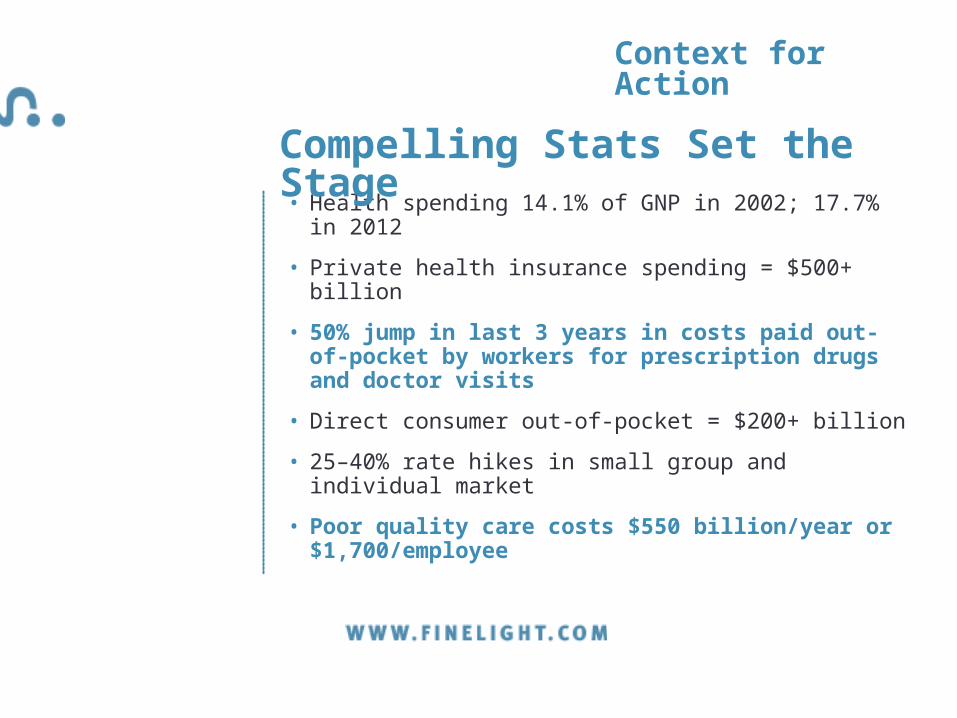

• Health spending 14.1% of GNP in 2002; 17.7% in 2012

• Private health insurance spending = $500+ billion

• 50% jump in last 3 years in costs paid out-of-pocket by workers for prescription drugs and doctor visits

• Direct consumer out-of-pocket = $200+ billion

• 25–40% rate hikes in small group and individual market

• Poor quality care costs $550 billion/year or $1,700/employee

Compelling Stats Set the Stage

Context for Action

• 98% of the 6 million U.S. companies have fewer than 100 employees

• 60% of employers with fewer than 10 employees have stopped offering health coverage (38% of those with 10–49 employees)

• The number of uninsured Americans increased by 2.4 million 2001–2003

• Direct-to-consumer pharmaceutical advertising is estimated at $3 billion

• 1.2 million Americans buy prescription drugs from reimporters

Compelling Stats Set the Stage

Context for Action

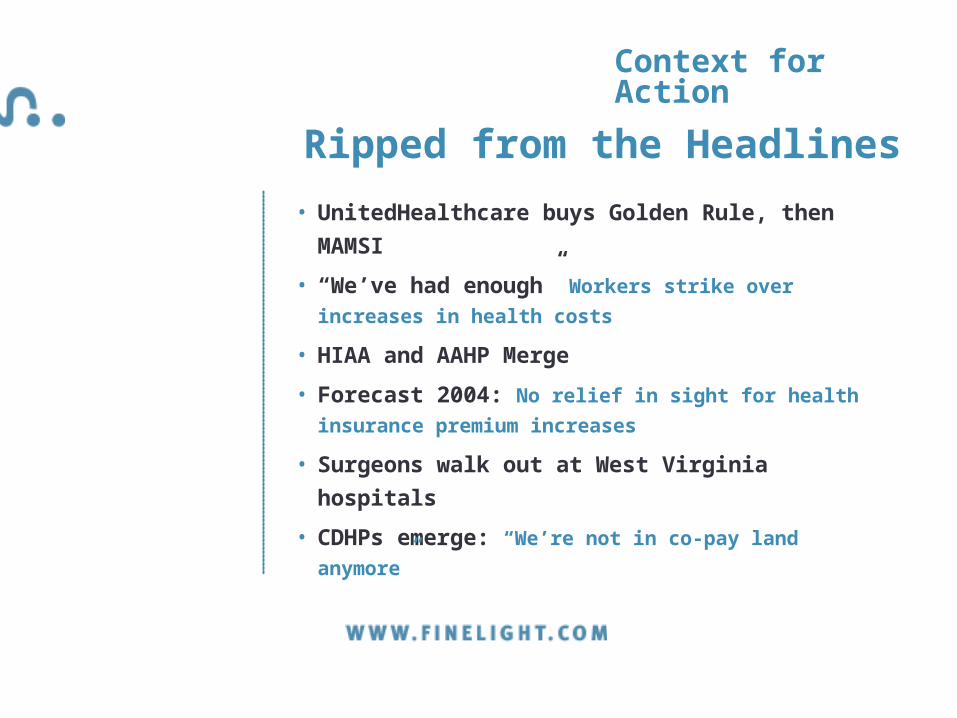

Ripped from the Headlines

Context for Action

• UnitedHealthcare buys Golden Rule, then MAMSI

• “We’ve had enough” Workers strike over increases in

health costs

• HIAA and AAHP Merge

• Forecast 2004: No relief in sight for health insurance

premium increases

• Surgeons walk out at West Virginia hospitals

• CDHPs emerge: “We’re not in co-pay land anymore”

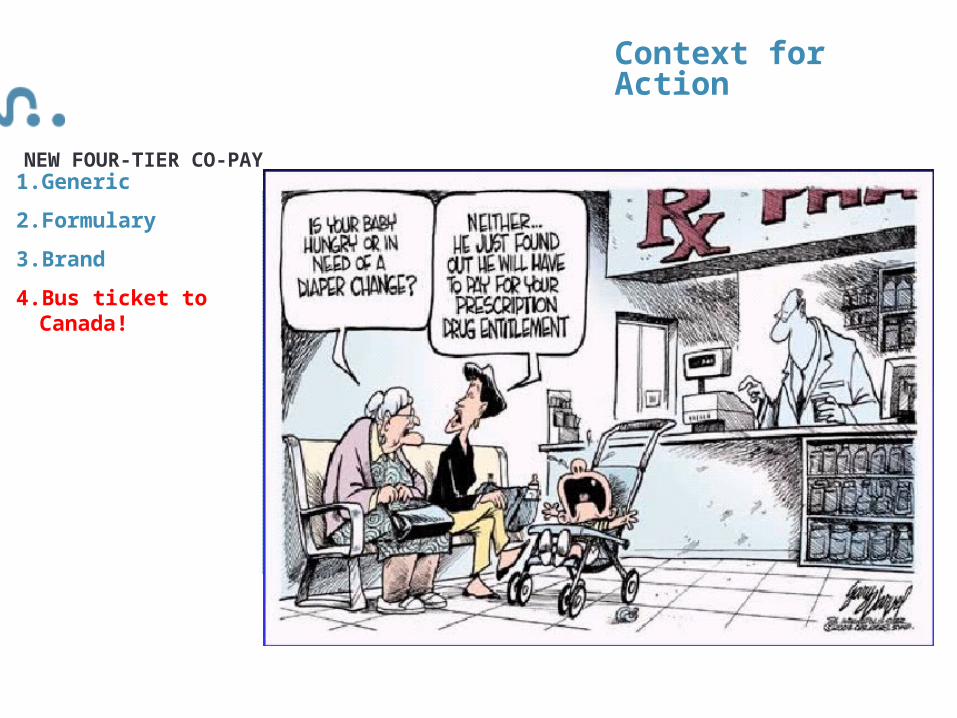

NEW FOUR-TIER CO-PAY

1. Generic

2. Formulary

3. Brand

4. Bus ticket to Canada!

Context for Action

Drill Down: Challenges Driving Change

• Skyrocketing premiums

• Cost shifting

• Industry consolidation

• Technology advances

• Struggling economy

• Increasing uninsured

• Price transparency

• Changing population trends

• Business process outsourcing

• Managed care backlash

• Single payer system

• Erratic price competition

• Prescription drug crisis

• Consumerism tipping point

Context for Action

Insurance 101

“It’s not the big that eat the small, it’s the fast that eat the slow.”

— J. Jenning and L. Houghton

Regional Health Players

• Well-positioned to capture market share

• Local presence, local brand

• Local-based provider contracts and loyalty

• Agility to embrace change and move quickly

• Small employers, individuals and seniors are prime growth targets

Mega Competitors

• Well-positioned to capture market share

• Multi-market presence, mega-brand

• Leverage-based provider contracts

• Deep pockets to invest in change

• Small employers, individuals and seniors are prime growth targets

Competitive Reality

CDHP Tipping Point

• Regardless of size, payers jumping in—quickly

• Benefit consultants making big bets on CDHP

• Barriers to entry broken down with technology and partner availability

• Products reflect consumer decision making• Point of Enrollment – benefit risk and reward• Point of Care – price and quality transparency

In a Consumer-Centric World

“There’s no reason anyone would want a computer in their home.”

“I think the world market may be five computers.”

“This anti-trust thing will blow over.”

— Ken Olson, Chairman, Digital Equipment Corp., 1977

— Thomas Watson, Chairman, IBM, 1943

— Bill Gates, Chairman, Microsoft, 1995

CDHP: Fad or Trend?

Customers

• Need to be motivated to voluntarily make economical, logical choices about services they want and their willingness to pay

• Old Way – unmotivated, isolated consumers with no information, co-pay mentality and managed care restrictions

• New Way – engaged, accountable customers with price/quality information, benefit choices and rewards for shopping

In a Consumer-Centric World

Payers

• Need to recognize that health insurance no longer sells itself

• Topline Growth means an investment in market intelligence, lead generation and marketing ROI

• Customer Satisfaction means practical, education-based consumer communication and continuous after-sale selling

In a Consumer-Centric World

Market Reality“Buy-Knowing is when a buyer already knows what they need to know.

Buy-Learning is when a buyer needs to acquire knowledge and weigh alternatives.

A new approach is required for Buy-Learning.”

— Kevin Davis

New business models . New marketing tactics . New partnerships

Payer

Employer

Employee

Provider

• Financial stability

• Tightly integrated, consistent operations

• Superior customer service

• Current technology platform

PayersWinners v. Losers: Run With The Pack Strategy

Prepare for the Future

Payers Winners v. Losers: Breakout Strategy

• Product differentiation

• Unique selling proposition

• Expectation setting

• Preemptive customer experience

• Baseline communications

• Rules of Engagement

• Continuous education

• Frequent customer touches

Prepare for the Future

EmployersTreat health care like other business decisions

• Promote change through choice

• Educate employees

• Measure and demonstrate results

Prepare for the Future

EmployeesRenew healthcare accountability, knowledge and engagement

• Recognize true cost of care

• Willing buy-in vs. force-in

• Understand differences among providers

Prepare for the Future

ProvidersMove from managing insurer to managing customer

• Get ready for knowledgeable patients

• Prepare for different flow of money

• Make performance indicators available

Prepare for the Future

2121

•Topline growth•Support and accelerate profitable sales revenue

•Marketing assessment•Evaluate effectiveness of strategic and tactical plans

•Competitive positioning•Guide internal and external communications

•Brand architecture•Influence customer preference and boost valuation

•Integrated execution•Provide full-service marketing and creative solutions

800.951.6226

Driving Growth Through Marketing