Handout: Principles of establishing and introducing a cost ... · This paper is intended as a...

41

Economic Development and Employment Division (41) Technical and Vocational Education and Training Section (4115) Handout: Principles of establishing and introducing a cost accounting system for technical and vocational education and training institutions Andreas Jörk August 2006 On behalf of Deutsche Gesellschaft für Technische Zusammenarbeit (GTZ) GmbH - German Technical Cooperation -

Transcript of Handout: Principles of establishing and introducing a cost ... · This paper is intended as a...

Economic Development and Employment Division (41) Technical and Vocational Education and Training Section (4115)

Handout: Principles of establishing and introducing a cost accounting system for technical and vocational education and training institutions

Andreas Jörk

August 2006

On behalf of Deutsche Gesellschaft für Technische Zusammenarbeit (GTZ) GmbH - German Technical Cooperation -

CONTENTS Preface.............................................................................................................................. 1 1 The context, Steps ................................................................................................ 2 1.1 The context............................................................................................................ 2 1.2 Organisational structure ........................................................................................ 2 1.3 Personnel structure ............................................................................................... 2 1.4 Structure of training and participants..................................................................... 3 1.5 Documenting and allocating usable floor space.................................................... 3 1.6 Material consumption in training............................................................................ 3 1.7 Utilities (electricity, heating, water and sewage) ................................................... 4 1.8 Service areas ........................................................................................................ 4 2 Cost accounting..................................................................................................... 6 2.1 Annual financial statements .................................................................................. 6 2.2 Definition and areas of cost accounting ................................................................ 6 2.3 Cost category accounting...................................................................................... 7 2.4 Cost centre and cost unit accounting ................................................................... 7 2.5 Allocation of overheads ......................................................................................... 8 2.6 Contribution accounting......................................................................................... 8 3 Summary ............................................................................................................. 10 4 Sources and comments....................................................................................... 11 5 Annexes .............................................................................................................. 12

Preface

Economic growth by means of technology-based industrial development needs qualified experts for their goal of industrial development. Technical and Vocational Education and Training (TVET) institutions play a key function in the formation of this human capital. International technical and financial cooperation projects and programmes accompany reform processes in the TVET sector in many partner countries. Besides technical investment it is therefore essential to take a close look at the financing and financiability of TVET. At the business administration level this requires - among other things - installing elements of commercial cost accounting at TVET institutions, based on the public accounting principles by. This means that the pure income-expenditure accounting which is still often used will soon no longer be sufficient to satisfy financial administration requirements. Detailed records of costs and charges are the only way to enable these institutions in future to operate efficiently and at optimal cost, while taking strategic decisions on the basis of solid financial analyses.

This paper is intended as a practical handout to assist in establishing a cost accounting system at TVET institutions.

The following sections and annexes refer to a completed project at a TVET school in Viet Nam.

One essential requirement for the success of the undertaking ‘establishing and introducing a cost accounting system at a TVET institution’ is unreserved support from senior management:

Active involvement of middle management is particularly important in ensuring swift provision of the necessary resources - such as statutory regulations and provisions. It creates the necessary acceptance for the work in the field, and hence ensures successful implementation of a cost accounting system.

Actively involving the staff at the TVET institution practically ensures the desired sustainability. Experience shows that assistance from the financial accounting staff of the educational institution is essential. These human resources are needed for providing data already recorded, various support functions and further processing of accounting vouchers.

On the basis of current experience, a period of two to three years should be set for the implementation of such an advisory project. Achieving the goal requires the continuous presence of an expert (e.g. CIM) onsite, and provision of human, technical and logistical resources by the educational institution. Other factors which are of decisive importance for the time required are the context at the start of the project, the size of the educational institution, and the technical competence and availability of the locally integrated team.

1

1 The context, Steps

1.1 The context

At the start of such a project you often encounter opposing views of the nature of cost accounting. At this point the emphasis is generally on how carefully all income and expenditure is already recorded within the institution. However, this view is only concerned with the aspects of bookkeeping, voucher handling and the monetary changes in the cash holdings and accounts. This provides no information on the profitability of TVET measures or the efficiency of a vocational training institution in management terms. To have a prospect of success, installing cost accounting must be able to access the existing data in the financial accounting. The necessary information and data (see 1.2 to 1.8) must be provided by the educational institution.

1.2 Organisational structure

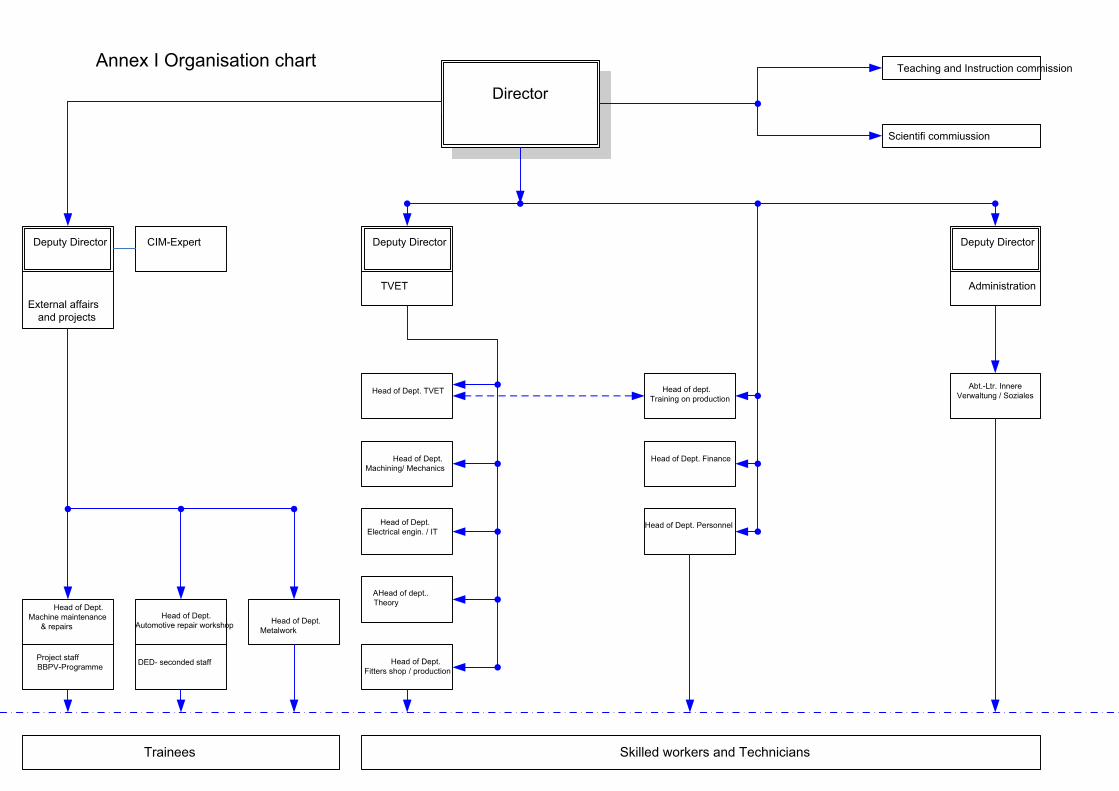

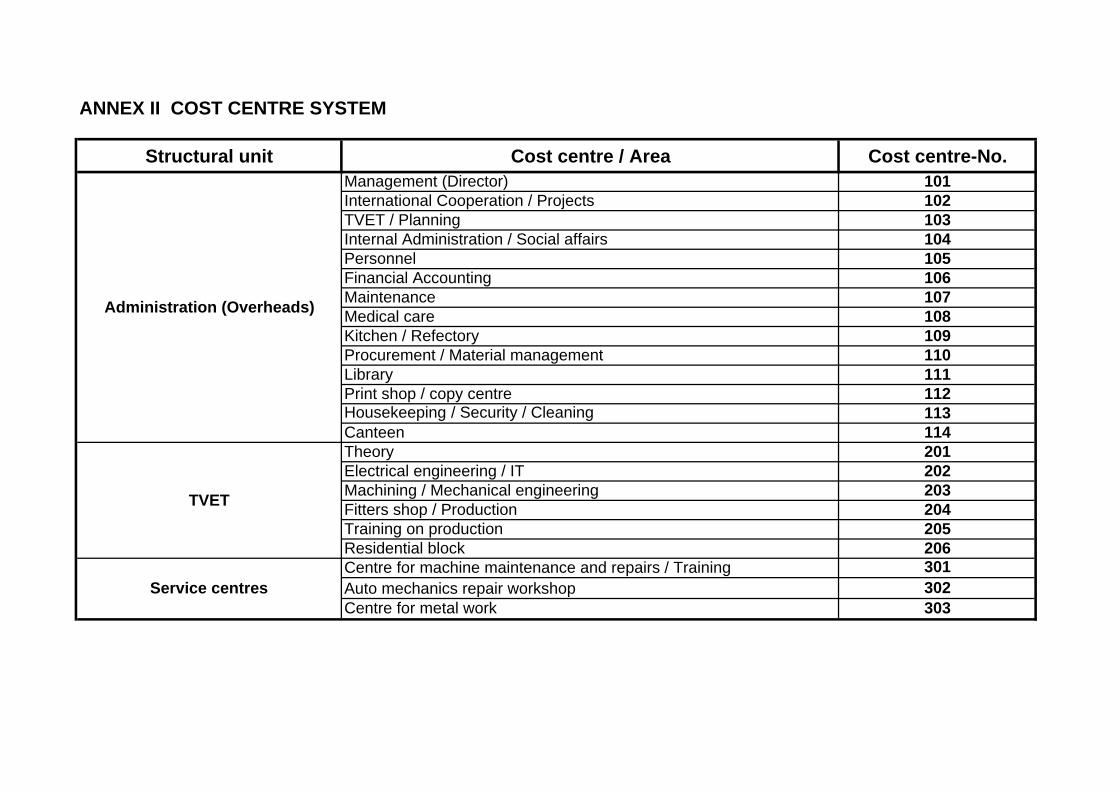

First, it is necessary to obtain an overview of existing organisational structures. The organisation chart shows the responsibilities and management layers (Annex I). This visual presentation provides the necessary transparency for the cost centre structure. It includes the scopes of tasks and areas of responsibility regardless of the persons involved. Based on this, a cost centre system can be formulated (Annex II). A cost centre system is necessary to define the boundaries of areas within the educational institution, either in physical terms or relating to expenditures. If a clear organisation chart is already available at the start of the project, the management of the TVET institution is generally prepared to accept the numerically arranged cost centre system based on this. If no organisation chart is available at this point, there must be immediate discussions with school management to obtain the necessary information. Based on this a draft chart should be drawn up and presented to school management for further discussion. The final version should be initialled by the top level of management at the educational institution. This establishes an authorised document which ensures the necessary priority for subsequent steps.

1.3 Personnel structure

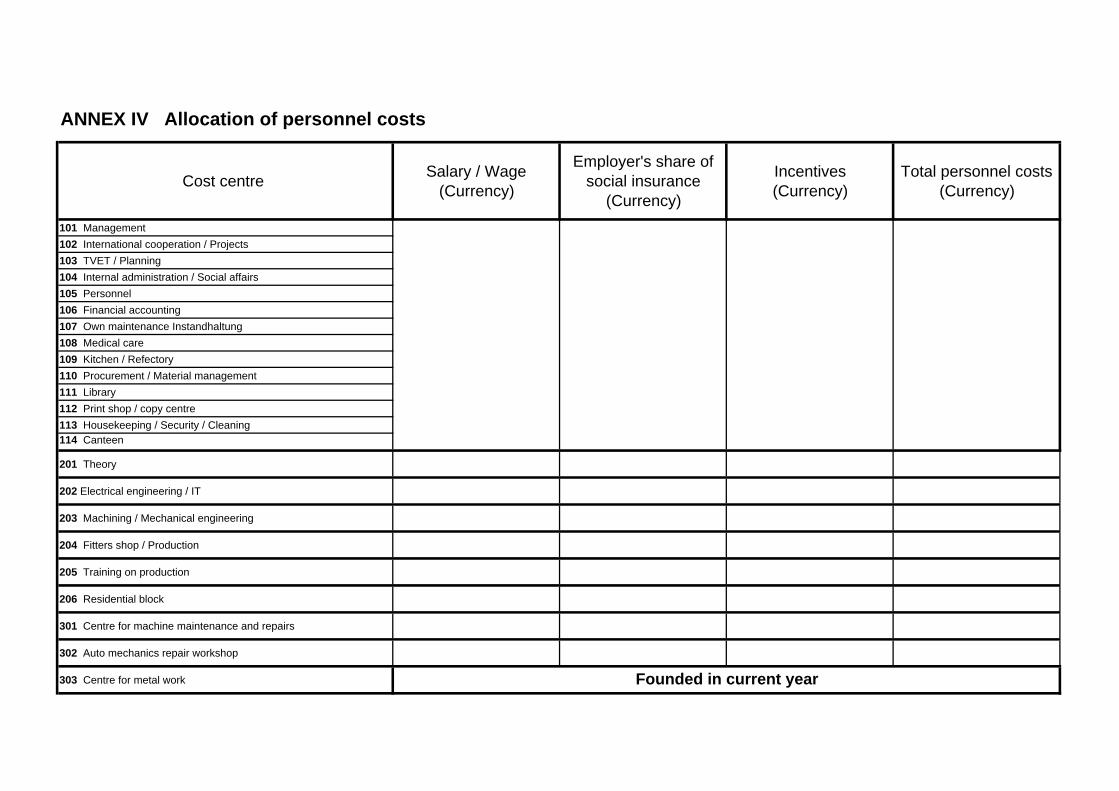

Staff is then assigned by name to the individual cost centres in accordance with the authorised cost centre system (Annex III). It is helpful at this point to involve the personnel department of the educational institution. The cost centre breakdown (e.g. faculties, departments etc) can then be used to allocate the monthly or annual personnel costs, including the employer’s social security contributions and any bonuses or premiums (Annex IV). Person-related (direct) allocation of personnel costs is a touchy issue. Practical experience here suggests that one possible initial approach is to allocate personnel costs on the basis of cost centres. For financial forecasting or ex post costing of individual educational measures (cost unit accounting), however, the concrete personnel costs for the instructors are needed subsequently to arrive at accurate ratios.

2

1.4 Structure of training and participants

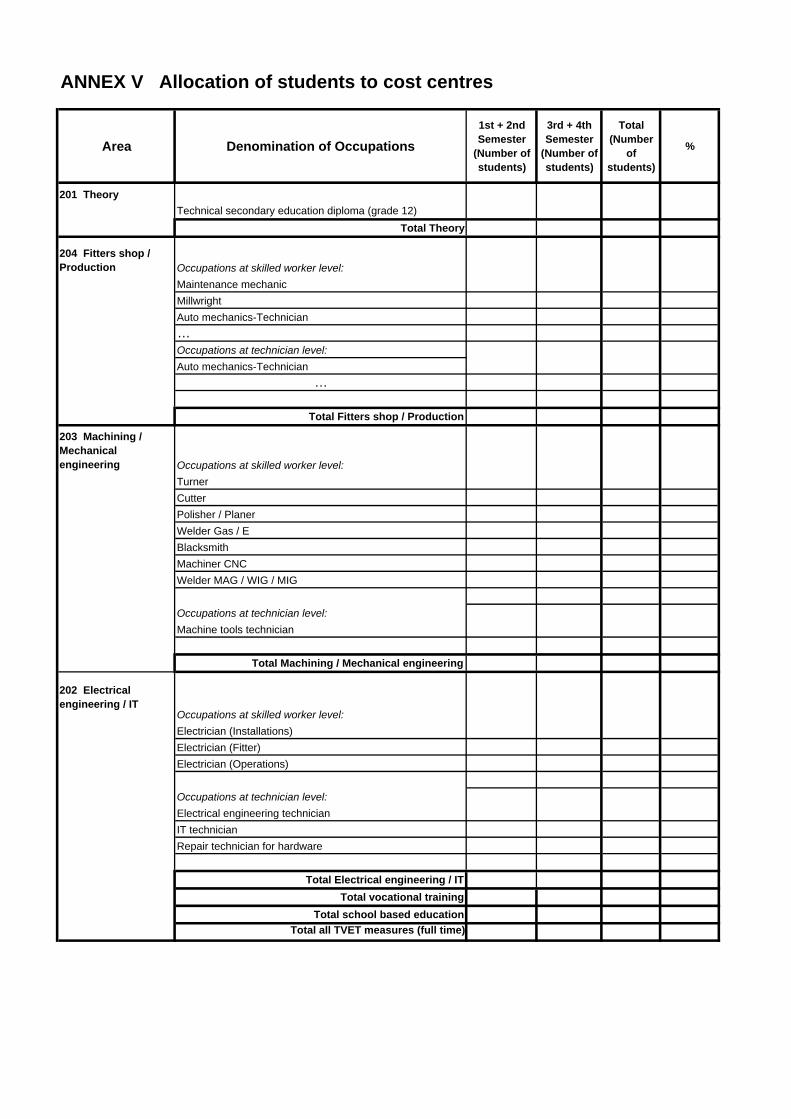

In the next step all the educational measures at the educational institution and other services offered (vocational training, general school leaving certificates, upgrading and CPE, services and consulting) are recorded and allocated individually to the cost centre system. This makes each measure a cost unit. Management analysis of the individual educational measures is an important goal of cost accounting. Using relevant documents such as class registers and other records and statistics of the TVET institution, it is possible to determine the number of participants in the individual educational measures, broken down by student semester or year of vocational training, and allocate them to the corresponding cost centres (Annex V).

1.5 Documenting and allocating usable floor space

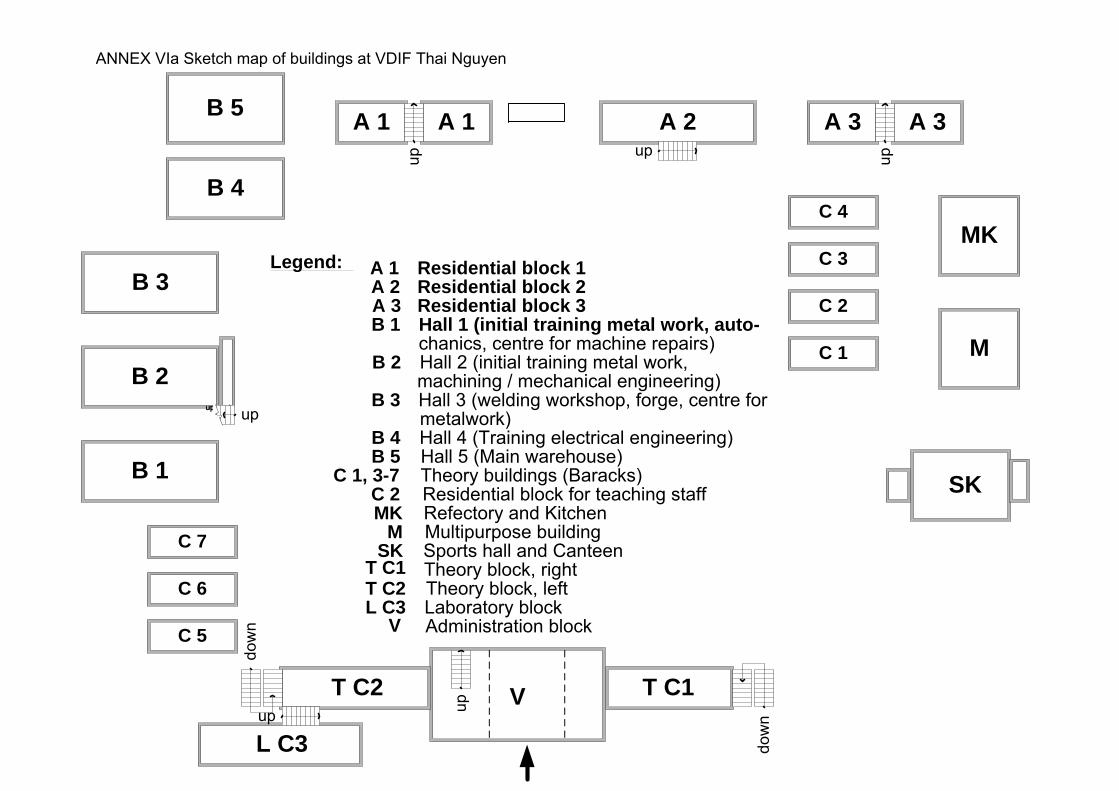

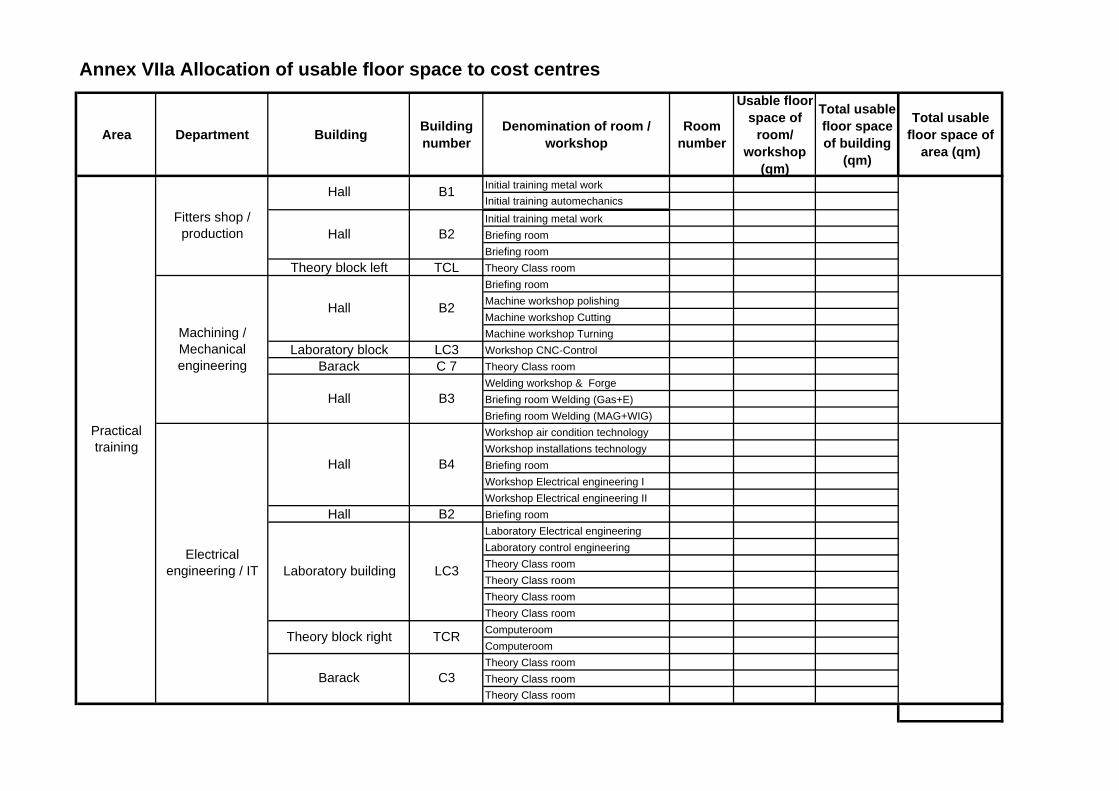

In documenting and allocating existing premises it is advisable to start by using available construction drawings or floor plans. Based on experience, it is necessary to check a random sample of supplied figures. It is also necessary to check that construction drawings supplied match current reality. If no documents are available, all buildings on the educational institution site must be documented (Annex VIa). This step is necessary so that the overheads can be allocated subsequently in line with their cause. This creates a "layout", which is advisable for general orientation. Subsequently, ground plans showing the recorded buildings and storeys are drawn with dimensions stated (Annex VIb). It is helpful to use a PC drawing program (e.g. MS Visio or similar software) to document the data. Subsequent changes (new construction and conversion) can then be relatively quickly incorporated and updated. Based on the recorded data, the usable floor space is then allocated to the individual cost centres (Annex VIIa). The recorded data can be used to draw up the allocation table for overheads (e.g. current maintenance for buildings) based on floor area (Annex VIIb).

1.6 Material consumption in training

Material consumption by educational measures and the directly related costs need to be analysed in a further stage. Experience shows that material costs differ between training areas and measures. There are usually major problems here in obtaining concrete figures for the use of types and quantities of materials by the individual educational measures. Materials are generally issued from a central store. At this point withdrawals of materials are mostly recorded by faculty (cost centre) but not by training measure (cost unit). A management analysis requires recording of material consumption over defined training periods (duration of the measure/s) by vouchers. If this important information is lacking, the only alternative is to fall back on "figures based on years of experience” for the individual areas of training (Annex VIII).

Note: Recording consumption of materials for individual measures must be discussed with the responsible individuals at the educational institution at the start of the project. If necessary, clear rules must be agreed on how to proceed. If the numbers provided

3

are based solely on “years of experience”, then there is reason for doubt about their accuracy.

1.7 Utilities (electricity, heating, water and sewage)

Because of the context frequently encountered (no meters or measuring devices available), allocation of utilities to cost centres requires an indirect approach. The installed ratings of all electrical devices in each room (workshop, classroom, laboratory, office etc) must be recorded (Annex IX). Based on the allocation table, the total electricity cost can be allocated to the cost centres (Annex X).

Note: Average consumer use times and use periods (e.g. shift work, vacation periods and the like) must be taken into account. Exact data (allocation based on consumption) can always be obtained by installing suitable meters. School management should be advised in this connection, so that proposed modernisation, conversion, and new construction measures can be influenced already in the planning phase.

1.8 Service areas

Often we find areas or departments which are supposed to generate additional income for the TVET institution. These service areas often supplement the instruction, which constitutes “production” in the vocational training. In this context, we usually talk about a “production school model”.

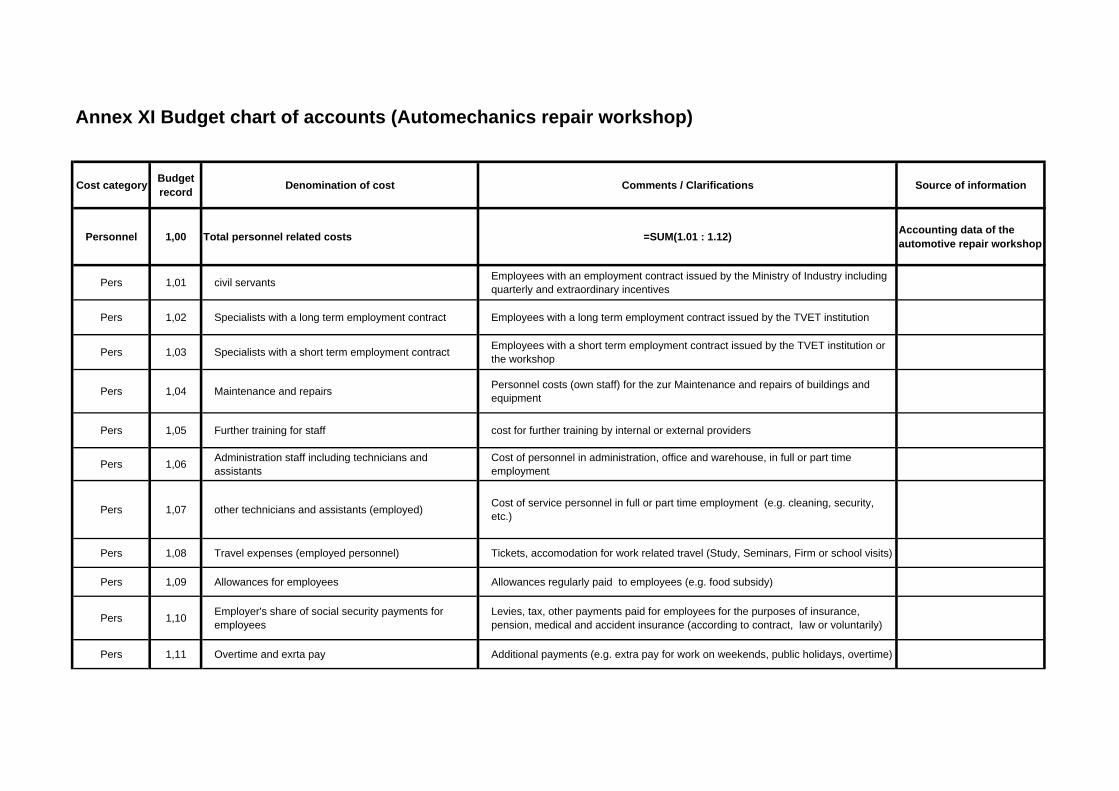

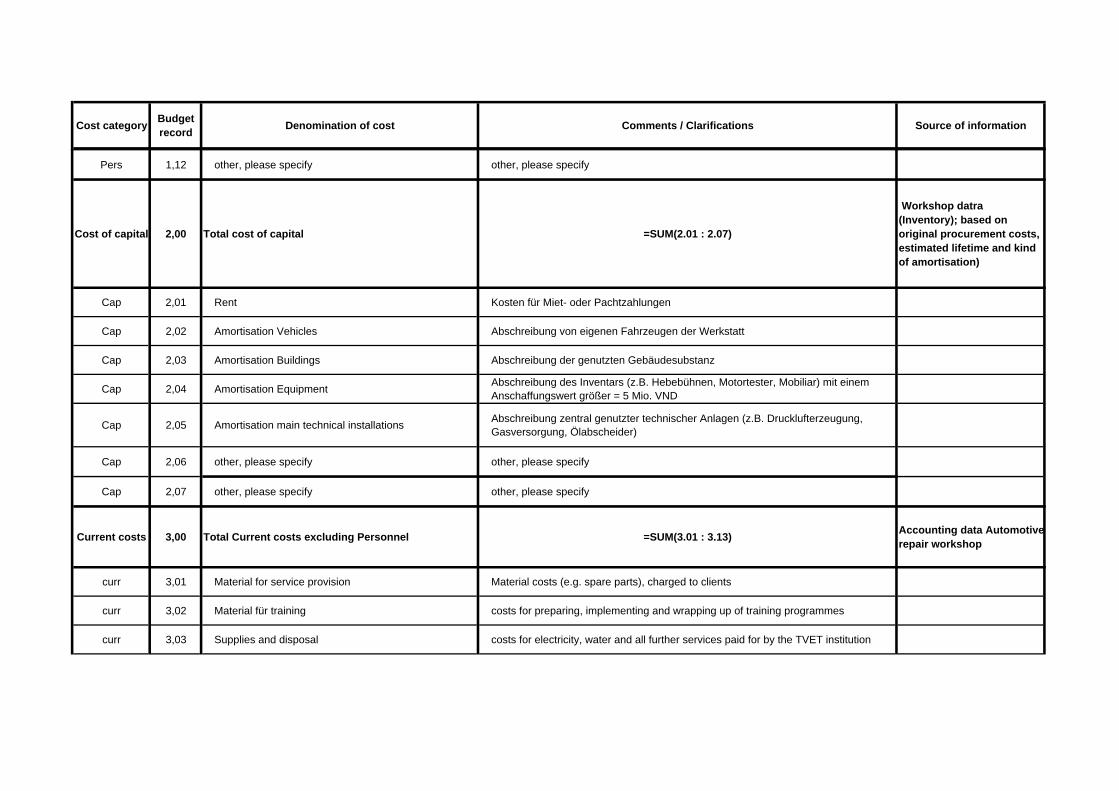

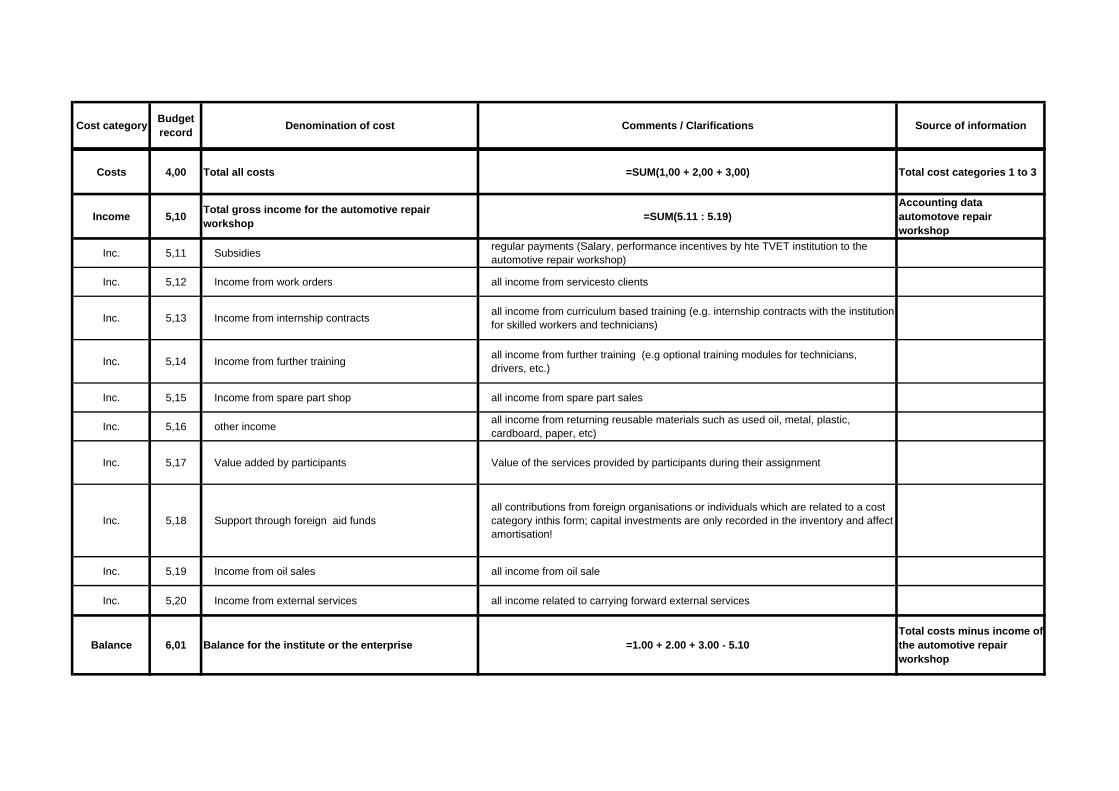

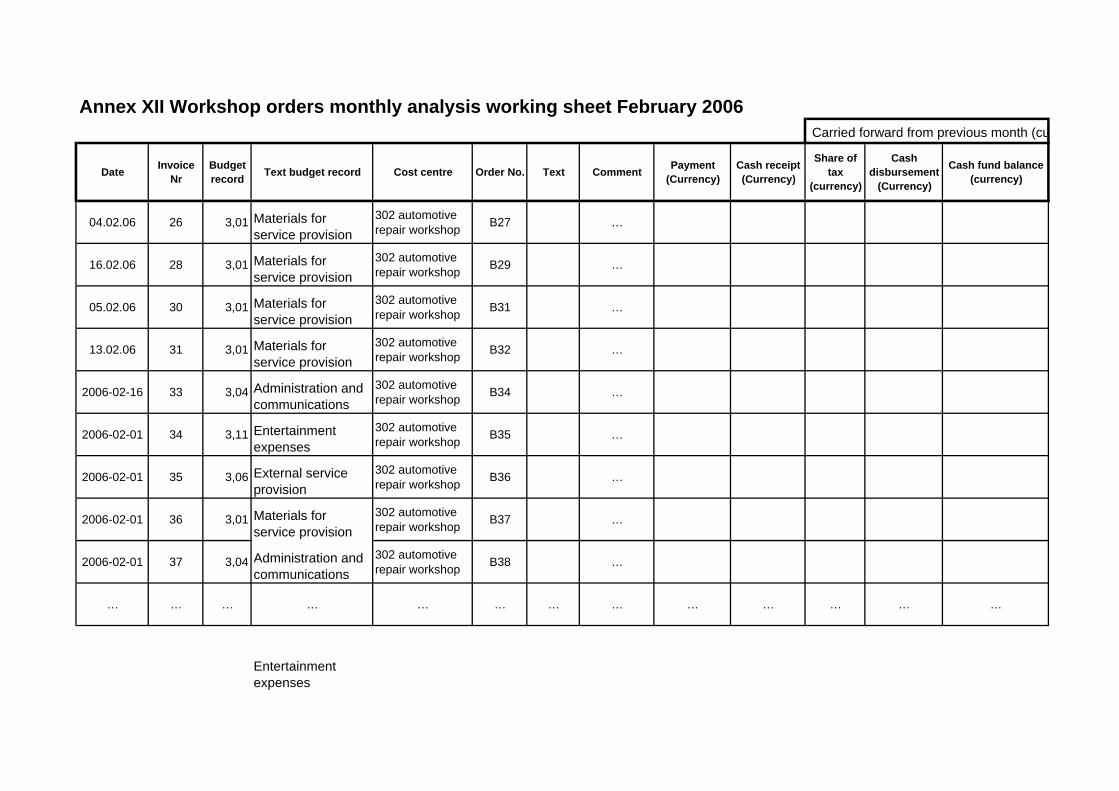

In the project described here, an automotive repair workshop (a rented property on a main road) is carrying out external orders and orders from the TVET institution (e.g. maintaining the fleet of vehicles). In the workshop the procedures related to the orders are recorded and documented, and a cash fund is administered. However, the monthly data for the financial bookkeeping of the TVET institution is not appropriate for management analyses. As this is a small operation with relatively clear cost structures, a computerised cost recording system was established following the GTZ guidelines “Financing vocational training”. Focusing on the essential aspects, the budget chart of accounts was modified for the specific needs of a service division (Annex XI). The budget chart of accounts documents the transactions (budget records) for income and expenditure, mostly broken down numerically by the main groups. These budget items can be further broken down, as required. The record system used previously in the automotive repair workshop did not provide any information (or only very vague information) on outstanding receivables and/or payables. The Excel table in the GTZ guidelines allows modifications according to the user’s needs. Workshop orders are broken down into customer orders or supplier orders and numbered consecutively. Cash receipts or disbursements were allocated to the order number and given a sequential cashbook number. The working sheet for the monthly analysis shows all transactions and financial movements. The identifying number is assigned in accordance with the budget chart of accounts (Annex XII). For a quick overview of outstanding receivables or payables, the necessary elements such as order number, order date, customer name and amount should be transferred to a separate sheet by copying the records. This is illustrated taking the above automotive repair

4

workshop as an example (Annex XIII). The outstanding receivables and payables are shown by order. This makes it possible to analyse these “special transactions”. Establishing a reminder system needs to be sorted out with the educational institution with due account to the specific conditions and needs. In line with the country-specific context, payments and disbursements are very frequently made in cash. Bank accounts were accordingly omitted initially, but can easily be added subsequently.

5

2 Cost accounting

2.1 Annual financial statements

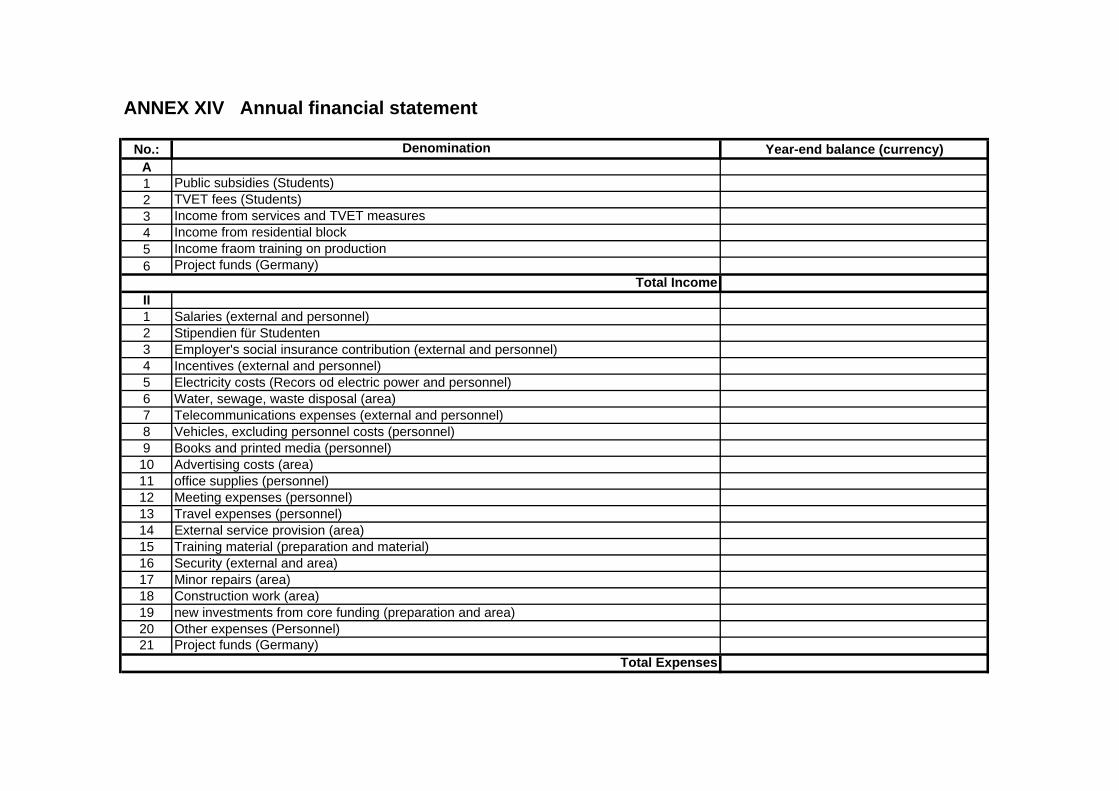

Annual financial statements provide a snapshot. They must be drawn up for a specific balance sheet date (mostly 31 December) and are supposed to present a picture of the institution’s assets, finances and earnings. Experience shows that they are drawn up specifically for accountability and disclosure to organisations at a higher level. Given this, it is very likely that such documents will exist. The annual financial statements for the previous year are the starting point from which to take further steps. Analysis of these in connection with the country-specific statutory provisions often allows conclusions to be drawn about an existing structure of income and expenditure (Annex XIV).

Particularly the provision of usable and credible figures often turns out to be an initial problem. A certain level of personal trust is first needed to overcome this barrier.

Note: As the annual financial statements document the past (mostly the past calendar year), the figures for creating the allocation table and subsequent analyses must always be applied to the year of the subject annual financial statements.

2.2 Definition and areas of cost accounting

Costs are the monetary value of resources used to produce an output (e.g. personnel costs, material costs, energy costs). Providing premises and equipment are also cost factors (imputed costs). The way the latter costs are financed depends largely on policy decisions at a higher level. This applies to the development policy context, too.

Expenditures, on the other hand, are payments representing an outflow of money and which are effective at an exactly defined time (e.g. supplier invoices).

Cost analysis and financing considerations accordingly have to be separated. Cost analysis is concerned with analysing completed financial transactions. By contrast, financing considerations are concerned with the future, based on existing cost analyses for past periods, and include various factors (e.g. expected number of participants, new educational services, investment, public sector transfer payments etc) in the planning. The results are budgets and investment plans.

The following sections will be primarily concerned with cost analysis (recording costs, calculating key ratios). The allocation of direct costs to the defined cost centres and cost units (training areas, educational measures) offers a practical solution. You should always try to start by allocating the most cost and income intensive items (e.g. public sector transfer payments, fees by participants, personnel costs, materials costs, energy costs). For secondary budget items, direct allocation has to be considered in terms of the benefit. When analysing actual costs, we distinguish between the following options, which are logically connected:

(a) Cost category accounting

(b) Cost centre accounting

6

(c) Cost unit accounting

(d) Contribution accounting.

Cost category accounting answers the question of what costs were incurred. (For example personnel costs for teachers, materials costs for training, costs of premises, administrative costs …)

Cost centre accounting asks where these costs were incurred. (For example turning workshop, welding workshop, electronic workshop, residential block ...)

Cost unit accounting tells us what the costs were incurred for. (For example vocational training for fitters, additional course for auto mechanics, foreign language course …)

Contribution accounting investigates the difference between income and expenditure within the predefined cost centres (For example fitters shop/production, machining/mechanical engineering, electrical engineering/IT, administration, etc.).

2.3 Cost category accounting

Cost category accounting takes the income and expenditure recorded in the financial accounts as a simple statement of income and expenditure and allocates it for management purposes. Absolute values (direct costs) have to be established and comparative ratios calculated. In cost category accounting, we distinguish between costs which can be allocated directly (direct costs) and costs which have to be allocated indirectly (overheads).

Direct costs (e.g. personnel costs for teachers, expendable materials and supplies, costs of using premises) can be recorded directly for the cost units (e.g. specific course or occupation in vocational training) and allocated to these.

Overheads (personnel costs in administration, material expenditures for land and buildings, insurance, vehicles) cannot be identified for the individual cost units, as they are incurred for all services offered, workshops and training areas generally.

Overheads are allocated using allocation tables. Cost category accounting together with cost centre accounting provides the basis for subsequent analysis.

2.4 Cost centre and cost unit accounting

An educational institution can be broken down by cost centres (e.g. faculties or workshops) or cost units (e.g. educational measures, see 1.2 Organisational structure). Which procedure is followed depends on the actual situation and the goals agreed with senior management. We recommend providing advice to support this process, particularly when setting up a new educational institution or fundamentally reorganising financial procedures. In this situation, the focus should if possible be on cost centre or cost unit accounting. Compared with cost category accounting, these represent a more precise form of accounting. Income and expenditure can be broken down not only by their type, but also by the faculties, workshops or educational measures. Key ratios, and particularly allocation tables, can be created for the individual areas or educational measures and

7

services. The allocation table enables us to allocate costs (overheads) which cannot be directly allocated. We recommend creating a number of tables for each cost category. All costs are considered here in terms of their causes and relationships (cleaning costs by usable floor space, vehicles by number of personnel, administrative costs by participants etc). These allocation tables need to be checked regularly (annually) where public sector accounting methods are applied, and adjusted if necessary. It is more effective to provide a partial breakdown (cost category and cost centre/unit) on the accounting vouchers. However, this assumes that a global invoice (e.g. for supply of welding electrodes) can be broken down into direct cost vouchers with cost centre or cost unit numbers to identify them.

2.5 Allocation of overheads

These are costs which apply to several cost centres and are allocated to the individual cost centres using an allocation table. Overheads are primarily fixed costs which are incurred regardless of the output (educational measures, services) and which by their nature ensure the ability of an educational institution to operate (administration, infrastructure). With regard to comprehensive management analysis it is essential to determine the overheads for the educational institution and allocate these to the “productive areas” (e.g. training, services, consulting). At this point we use the data already collected (see 1.3 - 1.7). To allocate overheads in a way which is logical and causally driven, it is necessary to create allocation tables (Annex XVI). Application of these depends on the type of cost (e.g. electricity costs in terms of kW consumed). The data from 1.3 - 1.7 above generally change periodically (e.g. calendar or training year). This is why the allocation tables need to be reviewed for each period being analysed and adjusted if necessary. Experience shows that the problem of overheads (school administration and unproductive infrastructural areas) and imputed costs (depreciation of self-funded assets, interest on equity and borrowed capital) is very often neglected at state or public-law educational institutions. Often a decisive role is played by the modalities of subsidies and promotional funding for investments in TVET in the country in question. No imputed costs can be applied to public sector transfer payments (e.g. non-repayable grants).

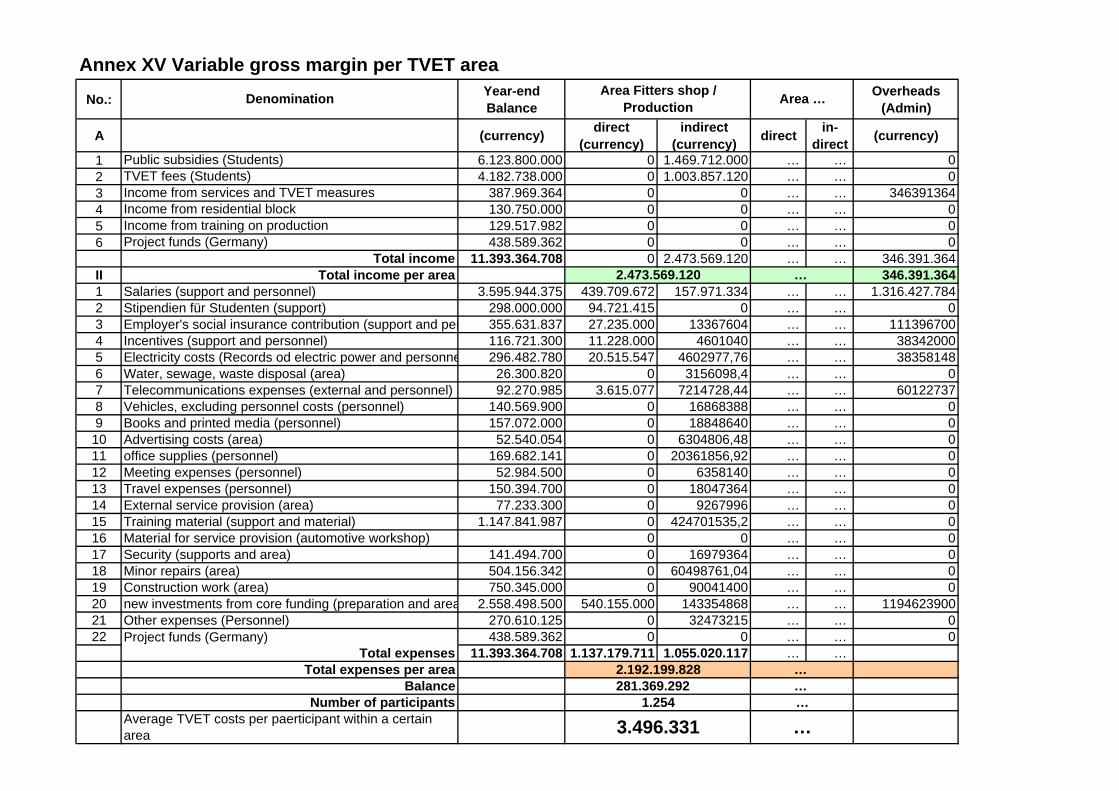

2.6 Contribution accounting

Contribution accounting is a special form of cost unit accounting. In this, the difference is calculated between all income and direct expenditures (personnel costs for teachers, materials costs for courses, other directly attributable costs) which is available to cover other costs (e.g. administration, insurance, vehicles). In this special form of cost unit accounting, we distinguish between different levels of contribution. Retrospectively, we can determine to what extent which cost centres were involved in the value adding process through which educational, service and advisory measures. Contribution accounting is particularly suitable for costing and ex post costing of educational measures (setting course fees, identifying costs per participant hour) and decisions on whether it makes sense to offer a planned educational measure or service.

8

(a) Contribution I Income less directly attributable expenditure results in the contribution available to cover all other costs of the cost centre or institution

(b) Contribution II Contribution I less overheads results in the contribution available to cover imputed costs (e.g. depreciation on self-funded assets, imputed interest on equity)

(c) Contribution III Contribution II less imputed costs (e.g. depreciation on self-funded assets and imputed interest on equity) results in the contribution available to cover assets funded by borrowing

(d) Contribution IV Contribution III less imputed costs for assets funded by borrowing (e.g. capital service) results in the commercial profit or loss.

At TVET institutions which are state owned or operate under public law, it is advisable to start by calculating contribution II. For management reasons this contribution should be positive (i.e. greater than zero), because this means that not only directly attributable costs but also overheads (e.g. administration, maintenance costs for land and buildings, vehicles) are covered. The remaining surplus is used to cover depreciation on self-funded assets or represents the remaining profit.

9

3 Summary

Based on personal experience in setting up and introducing a cost accounting system at a TVET institution in Germany, the project described attempted to integrate the most important elements at a Vietnamese vocational training institution. A particular concern here was to create simple, logical and – above all — modifiable structures. The aim was to enable future users to adapt the cost accounting to their specific needs and subsequently expand it. For this reason, standard international spreadsheet software was used rather than special-purpose software. Most TVET institutions are required by the government or a ministry to use a specific form of financial accounting. This is often a kind of public sector accounting method. If a software application is already available for financial accounting, it should be reviewed whether this can be adapted or expanded at reasonable cost for internal management analyses.

At the start of the project in Viet Nam only the annual financial statements were available for management analyses. This document did not permit any conclusions to be drawn on the efficiency of the training areas and the educational and other services they offered. Pricing, particularly for services, was carried out by comparisons with existing market prices. After two years, at the end of the project the TVET institution in Viet Nam was able to perform the following management accounting activities:

determine overheads

allocate overheads using an allocation table

calculate contribution II for the cost centres (with restrictions on consumption of materials for practical vocational training)

record outstanding receivables and payables for the service areas

ascertain the bases for costing.

The contribution accounting for the training areas together with information on the training costs per participant in the faculty now give the TVET institution’s management solid management figures for the first time. The same applies to the consistent recording of outstanding receivables and payables in the service areas. This information is of particular interest to the management of the institution for strategic decisions about future investment and the technical orientation of the TVET institution. They also provide the basis for costing new educational and other services.

Consistent application of the above results would also allow calculation of training costs per participant/hour and measure and billing rates by instruction period. This would require setting up a cost unit accounting system. Under this, each training measure is a separate cost unit. All the cost elements then have to be allocated to the cost unit in detail.

The sustainability of the project depends crucially on the attitude of senior management and the commitment of the individuals directly involved in implementing it. Consistent application of the results to date would also make it possible to set up a controlling system.

10

4 Sources and comments

1 Schilling, Gerhard (Heinz-Piest-Institut für Handwerkstechnik an der Universität Hannover): Kostenrechnung für überbetriebliche Berufsbildungsstätten (“Cost accounting for independent vocational training centres”), 2nd ed. 1988

2 Kugler, Gernot: Betriebswirtschaftslehre der Unternehmung, Europa-Lehrmittel (“Business administration principles at Europa-Lehrmittel”), 13th ed. 1995

3 Schmolke, Siegfried; Deitermann, Manfred: Industrielles Rechnungswesen IKR (“Industrial accounting – industrial chart of accounts”), Winklers Verlag, 16th ed. 1991

4 Lipsmeier, Antonius; Georg, Walter; Idler, Horst: Dealing with financing of vocational education, Excel sheet (structure of the cost calculation form), December 2003

11

5 Annexes

Annex I Organisation chart

Annex II Cost centre system

Annex III Allocation of staff to the cost centre system

Annex IV Allocation of personnel costs

Annex V Allocation of students to cost centres

Annex VIa Sketch of buildings at VDIF Thai Nguyen

Annex VIb Ground plan of Hall B1 at VDIF Thai Nguyen

Annex VIIa Allocation of usable floor space to cost centres

Annex VIIb Allocation table for overheads based on floor area

Annex VIII Allocation of material costs to TVET measures

Annex IX Allocation of electrical devices per room (practical training section)

Annex X Allocation of total electricity cost to each cost centres

Annex XI Budget chart of accounts (Car repair workshop)

Annex XII Workshop orders monthly analysis working sheet

Annex XIII Overview of outstanding receivables and payables

Annex XIV Annual financial statement

Annex XV Variable gross margin per TVET area

Annex XVI Overheads allocation table

12

Director

Head of dept. Training on production

Head of Dept. Finance

Head of Dept. Personnel

Deputy Director Deputy Director Deputy Director

External affairs and projects

TVET Administration

Head of Dept. Machine maintenance

& repairsHead of Dept.

Automotive repair workshop Head of Dept.Metalwork

Head of Dept. TVET

Head of Dept. Machining/ Mechanics

Head of Dept. Electrical engin. / IT

AHead of dept..Theory

Head of Dept. Fitters shop / production

Abt.-Ltr. Innere Verwaltung / Soziales

CIM-Expert

Scientifi commiussion

Project staff BBPV-Programme DED- seconded staff

Skilled workers and TechniciansTrainees

Teaching and Instruction commissionAnnex I Organisation chart

Structural unit Cost centre / Area Cost centre-No.Management (Director) 101International Cooperation / Projects 102TVET / Planning 103Internal Administration / Social affairs 104Personnel 105Financial Accounting 106Maintenance 107Medical care 108Kitchen / Refectory 109Procurement / Material management 110Library 111Print shop / copy centre 112Housekeeping / Security / Cleaning 113Canteen 114Theory 201Electrical engineering / IT 202Machining / Mechanical engineering 203Fitters shop / Production 204Training on production 205Residential block 206Centre for machine maintenance and repairs / Training 301Auto mechanics repair workshop 302Centre for metal work 303

ANNEX II COST CENTRE SYSTEM

TVET

Service centres

Administration (Overheads)

Cost centre Name Activity / Task Area Kind of personnel cost allocation

101 Management Director Administration IndirectProjects Deputy director Administration Indirect103 TVET / Planning Deputy director

Head of DivisionDeputy Head of DivisionEmployee

104 Internal Administration / Social Affairs Deputy directorHead of DivisionIT-AdminstratorinMail roomHousekeeperDriverEmployee

105 Personnel Head of DivisionDeputy Head of DivisionEmployee

106 Financial accounting Head of DivisionEmployeeEmployee (Cashier)Employee / Team leader…

107 Maintenance Team leaderEmployee…

108 Medical care Nurse Administration Indirect109 Kitchen / Refectory Head of Division

Employee…

110 Procurement / Material management Deputy Head of DivisionDeputy Head of DivisionEmployee…

111 Bibliothek Employee…

112 Druckerei / Kopierstelle Employee…

113 Hausdienste Employee…

114 Canteen Employee…

201 Theory Head of Division / TeacherDeputy Head of DivisionTeacher / Team LeaderTeacher…

202 Electrical engineering / IT Head of DivisionInstructor…

Indirect

Indirect

Direct

Indirect

Direct

Indirect

ANNEX III Allocation of staff to the cost centre system

Indirect

Indirect

Indirect

Theory

Electrical engineering / IT

Administration

Administration

Canteen

Indirect

Indirect

Indirect

IndirectAdministration

Administration

Administration

Administration

Administration

Administration

Administration

Administration

Cost centre Name Activity / Task Area Kind of personnel cost allocation

203 Machining / Mechanical engineering Head of DivisionDeputy Head of DivisionDeputy Head of DivisionInstructor Team leaderInstructor Team leaderTeacher / InstructorTeacher / Instructor Team leadProduction technician…

204 Fitters shop / Production Head of Division / TeacherTeacher / Instructor Team leadTeacher / Instructor…

205 Training on production Head of DivisionDeputy Head of DivisionEmployee…

206 Residential block Head of DivisionEmployee / Team leaderEmployee…

301 Centre for machine maintenance and repairs / Training- Instandsetzung u. Training

Head Centre for machine maintenance and repairs / Training

ElectricianMechanicMechanic / Measuring labSekretary…

302 Auto mechanics repair workshop Head of automechanics repair workshopWarehouse and salesWorkshop foremanCar Mechanic…

303 Metal workshopHead Metal workshop

FitterWelder…

Direct

Direct

Direct

Direct

Direct

Direct

Direct

Centre for machine maintenance and repairs /

Training

Auto mechanics repair workshop

Metal workshop

Machining / Mechanical engineering

Fitters shop / Production

Training on production

Residential block

ANNEX IV Allocation of personnel costs

Cost centre Salary / Wage (Currency)

Employer's share of social insurance

(Currency)

Incentives (Currency)

Total personnel costs (Currency)

101 Management102 International cooperation / Projects103 TVET / Planning104 Internal administration / Social affairs105 Personnel106 Financial accounting107 Own maintenance Instandhaltung108 Medical care 109 Kitchen / Refectory110 Procurement / Material management111 Library112 Print shop / copy centre113 Housekeeping / Security / Cleaning114 Canteen

201 Theory

202 Electrical engineering / IT

203 Machining / Mechanical engineering

204 Fitters shop / Production

205 Training on production

206 Residential block

301 Centre for machine maintenance and repairs

302 Auto mechanics repair workshop

303 Centre for metal work Founded in current year

ANNEX V Allocation of students to cost centres

Area Denomination of Occupations1st + 2nd Semester

(Number of students)

3rd + 4th Semester

(Number of students)

Total (Number

of students)

%

201 TheoryTechnical secondary education diploma (grade 12)

Total Theory

204 Fitters shop / Production Occupations at skilled worker level:

Maintenance mechanicMillwright Auto mechanics-Technician …Occupations at technician level:Auto mechanics-Technician

…

Total Fitters shop / Production

203 Machining / Mechanical engineering Occupations at skilled worker level:

TurnerCutter Polisher / PlanerWelder Gas / E Blacksmith Machiner CNCWelder MAG / WIG / MIG

Occupations at technician level:Machine tools technician

Total Machining / Mechanical engineering

202 Electrical engineering / IT

Occupations at skilled worker level:Electrician (Installations)Electrician (Fitter)Electrician (Operations)

Occupations at technician level:Electrical engineering technician IT technicianRepair technician for hardware

Total Electrical engineering / ITTotal vocational training

Total school based educationTotal all TVET measures (full time)

dow

nup

dow

n

up

C 5

C 6

C 7

upup up

upup up

C 4

C 3

C 2

C 1

B 1

B 2

B 3

B 4

B 5 A 1 A 1 A 2 A 3 A 3

V

SK

M

MK

T C1T C2

L C3

Legend: A 1A 2A 3B 1

B 2

B 3

B 4 B 5

C 1, 3-7C 2MK

MSK

T C1T C2L C3

V

Residential block 1Residential block 2 Residential block 3 Hall 1 (initial training metal work, auto- chanics, centre for machine repairs) Hall 2 (initial training metal work, machining / mechanical engineering) Hall 3 (welding workshop, forge, centre for metalwork) Hall 4 (Training electrical engineering)Hall 5 (Main warehouse)Theory buildings (Baracks)Residential block for teaching staff Refectory and KitchenMultipurpose building Sports hall and CanteenTheory block, right Theory block, leftLaboratory blockAdministration block

ANNEX VIa Sketch map of buildings at VDIF Thai Nguyen

B1/1

B1/2

B1/3B1/4B1/5

B1/6

B1/7

B1/8

B1/1 - Head officeB1/2 - Teacher/ Instructor roomB1/3 - Initial training metal work B1/4 - Automechanics trainingB1/5 - Competence centre

B1/6 - Mesurement labB1/7 - Office & Secretary's office Head of Competence centreB1/8 - Electrics workshop

= 24,0 qm= 48,0 qm= 216,0 qm= 216,0 qm= 266,0 qm (360,0 qm)

= 22,0 qm= 22,0 qm

= 22,0 qm

B1/

9

B1/

10

B1/9 - Store room 1B1/10 - Store room 2

= 16,0 qm= 12,0 qm

8 m

4 m

6 m18 m18 m3 m4 m5,50 m 17,50 m

72 m

12 m

4 m

4 m

4 m

Annex VIbGround plan of Hall B1 at VDIF Thai Nguyen

Annex VIIa Allocation of usable floor space to cost centres

Area Department Building Building number

Denomination of room / workshop

Room number

Usable floorspace of

room/ workshop

(qm)

Total usablefloor space of building

(qm)

Total usable floor space of

area (qm)

Practical training

Fitters shop / production

Hall B1 Initial training metal workInitial training automechanics

Hall B2Initial training metal workBriefing roomBriefing room

Theory block left TCL Theory Class room

Machining / Mechanical engineering

Hall B2

Briefing roomMachine workshop polishingMachine workshop CuttingMachine workshop Turning

Laboratory block LC3 Workshop CNC-ControlBarack C 7 Theory Class room

Hall B3Welding workshop & ForgeBriefing room Welding (Gas+E)Briefing room Welding (MAG+WIG)

Electrical engineering / IT

Hall B4

Workshop air condition technology Workshop installations technologyBriefing roomWorkshop Electrical engineering IWorkshop Electrical engineering II

Hall B2 Briefing room

Laboratory building LC3

Laboratory Electrical engineeringLaboratory control engineeringTheory Class room Theory Class room Theory Class room Theory Class room

Theory block right TCR ComputeroomComputeroom

Barack C3Theory Class room Theory Class room Theory Class room

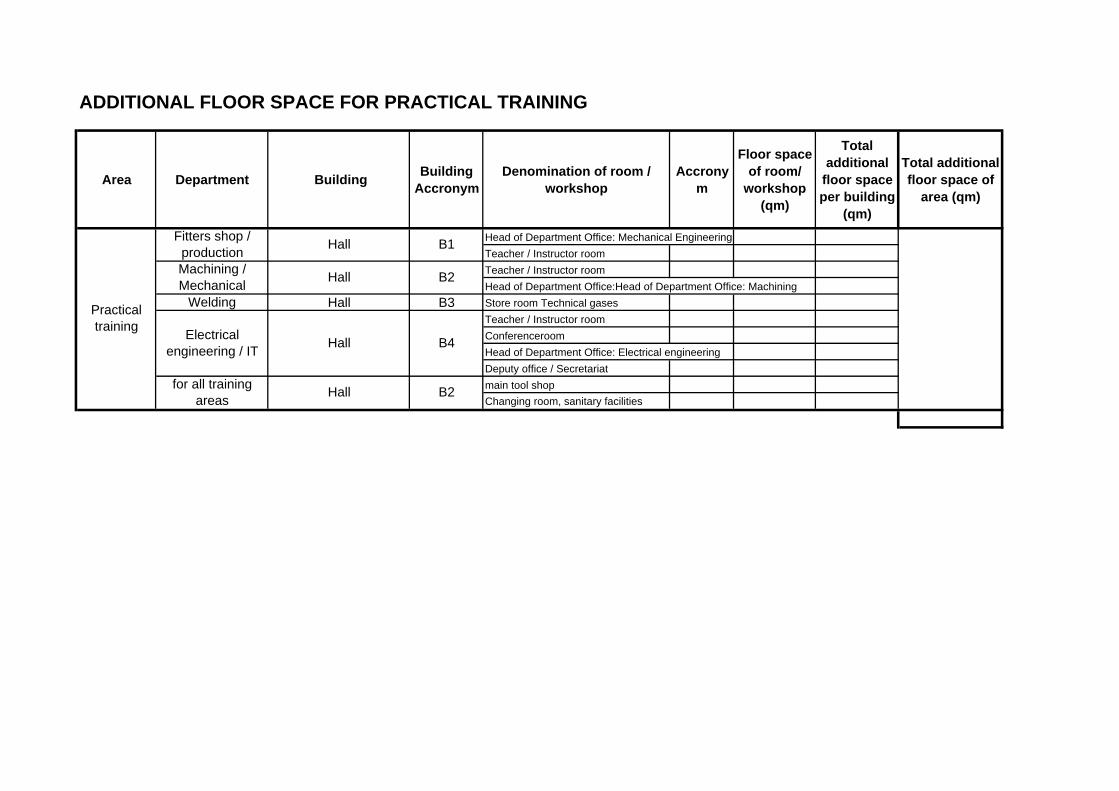

ADDITIONAL FLOOR SPACE FOR PRACTICAL TRAINING

Area Department Building Building Accronym

Denomination of room / workshop

Accronym

Floor space of room/

workshop (qm)

Total additional

floor space per building

(qm)

Total additional floor space of

area (qm)

Practical training

Fitters shop / production Hall B1 Head of Department Office: Mechanical Engineering

Teacher / Instructor room Machining / Mechanical Hall B2 Teacher / Instructor room

Head of Department Office:Head of Department Office: MachiningWelding Hall B3 Store room Technical gases

Electrical engineering / IT Hall B4

Teacher / Instructor room ConferenceroomHead of Department Office: Electrical engineeringDeputy office / Secretariat

for all training Hall B2 main tool shopareas Changing room, sanitary facilities

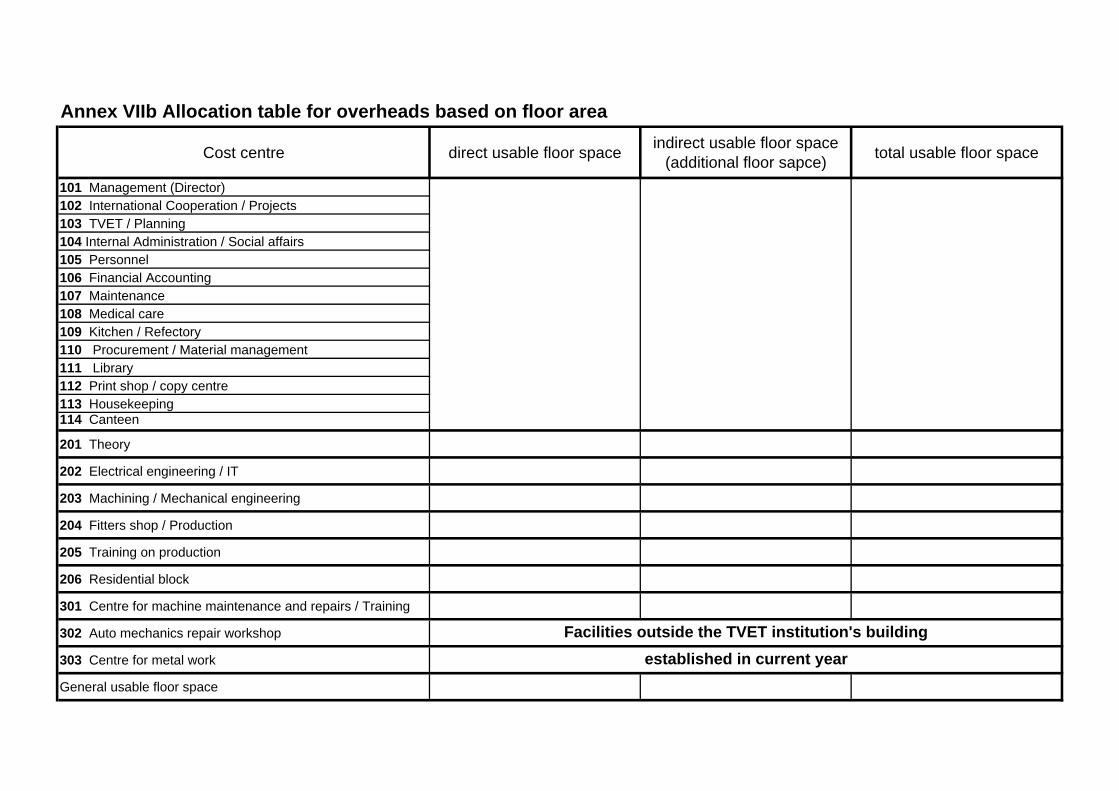

Annex VIIb Allocation table for overheads based on floor area

Cost centre direct usable floor space indirect usable floor space (additional floor sapce) total usable floor space

101 Management (Director)102 International Cooperation / Projects103 TVET / Planning104 Internal Administration / Social affairs105 Personnel106 Financial Accounting107 Maintenance108 Medical care109 Kitchen / Refectory110 Procurement / Material management 111 Library112 Print shop / copy centre113 Housekeeping114 Canteen

201 Theory

202 Electrical engineering / IT

203 Machining / Mechanical engineering

204 Fitters shop / Production

205 Training on production

206 Residential block

301 Centre for machine maintenance and repairs / Training

302 Auto mechanics repair workshop

303 Centre for metal work

General usable floor space

established in current yearFacilities outside the TVET institution's building

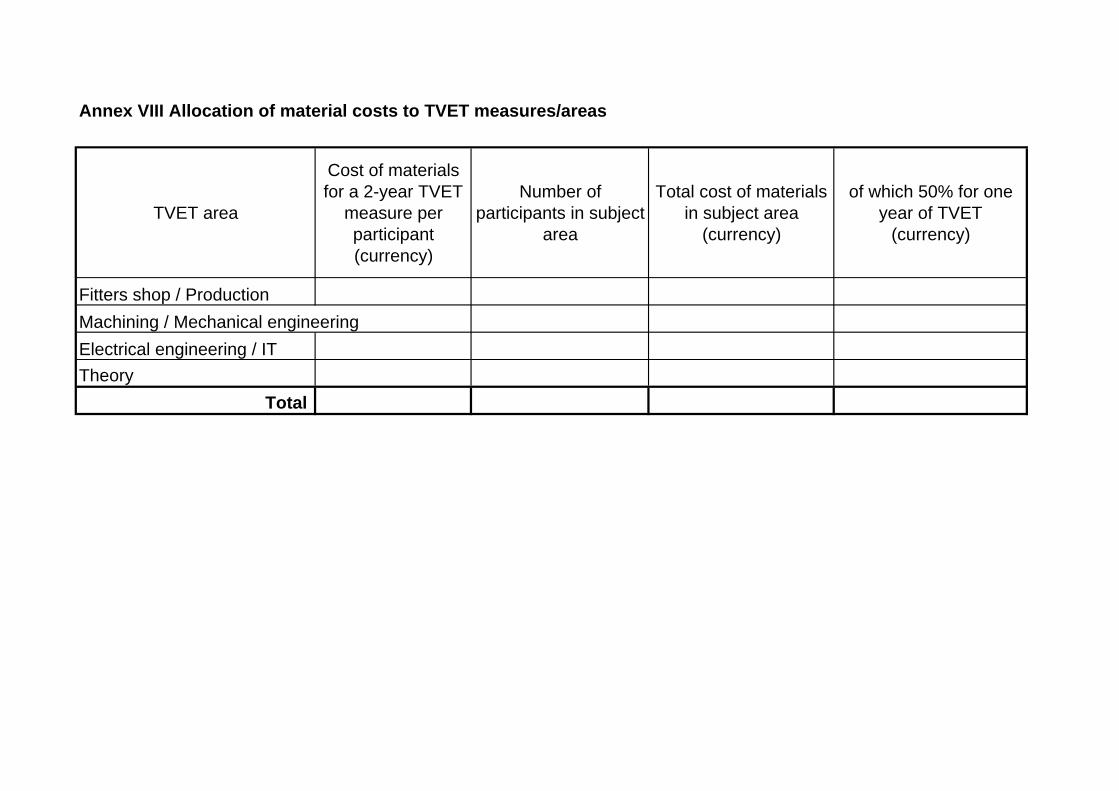

Annex VIII Allocation of material costs to TVET measures/areas

TVET area

Cost of materials for a 2-year TVET

measure per participant (currency)

Number of participants in subject

area

Total cost of materials in subject area

(currency)

of which 50% for one year of TVET

(currency)

Fitters shop / ProductionMachining / Mechanical engineeringElectrical engineering / ITTheory

Total

g

Annex IX Allocation of electrical devices per room (practical training section)

Area Department Building Building Number Denomination of room / workshop Room

NumberLighting

(kW)

Ventilator Air condi-

tioner (kW)

Techn. equipment

(kW)

Total (kW)

Practical training

Fitters shop / Production

Hall B1

Head of department office B 1/1Teacher / Instructor room B 1/2Initial training metal work B 1/3Initial training automechanics B 1/4

Hall B2Initial training metal work B 2/20

Briefing room B 2/1B 2/4

Theory block left TC2 Classroom training Hydr. / Pneum. TC 2/2

Office for teachers Theory FB Mechanical engineerin TC 2/1Laboratory

block LC3 Measuring laboratory digital LC 3/7Measuring laboratory analog LC 3/8Total per kind of device Fitters shop / Production

Total Fitters shop / Production

Machining / Mechanical engineering

Hall B2

Briefing room B 2/2B 2/3

Machine workshop polishing / planing B 2/7Changing room B 2/Umain tool shop B 2/10Machine workshop cutting B 2/12Machine workshop turning B 2/14Teacher / Instructor room B 2/16 Head of department office: Machining B 2/17

Laboratory block LC3

Workshop CNC control technology LC 3/3Barack C 6 Theory class room C 6/3

Hall B3

Office instructors welding and forge B 3/4Prefabrication B 3/5storeroom technical gases B 3/6Welding and forge workshop B 3/9Briefing room welding (Gas+E) B 3/7Briefing room welding (MAG+WIG) B 3/11

Total per kind of device Machining / Mechanical engineering

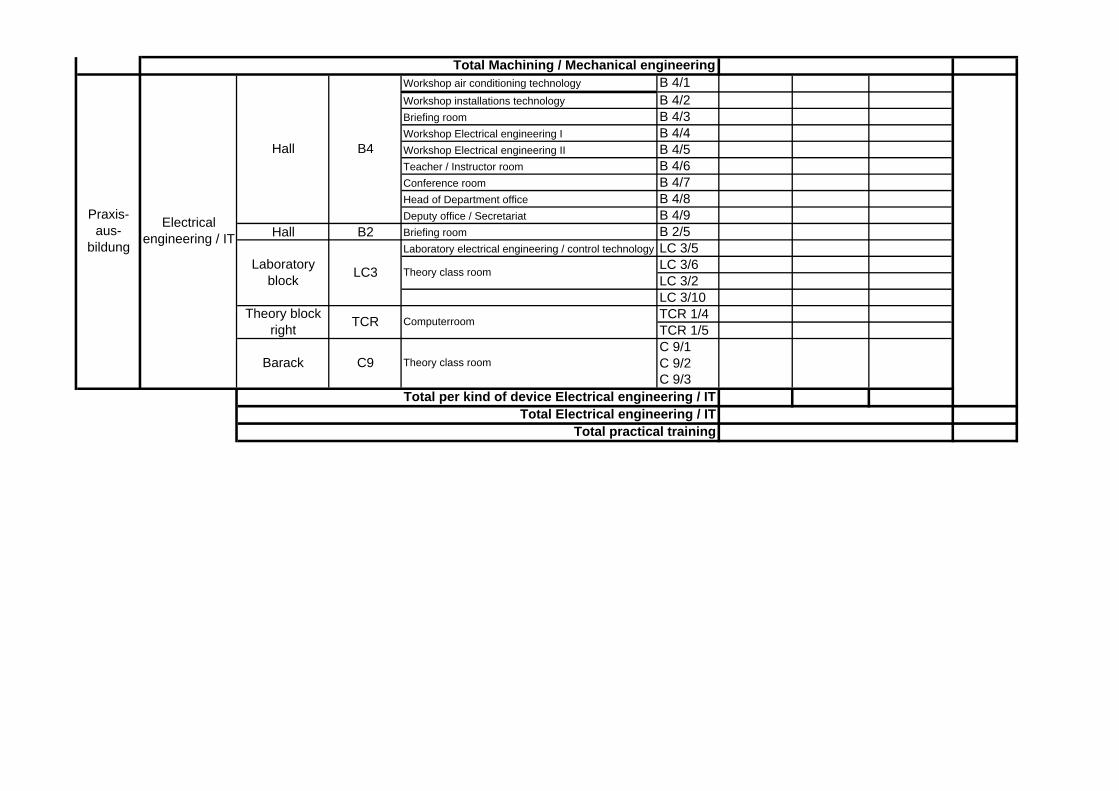

Total Machining / Mechanical engineering

Praxis- aus-

bildung

Electrical engineering / IT

Hall B4

Workshop air conditioning technology B 4/1Workshop installations technology B 4/2Briefing room B 4/3Workshop Electrical engineering I B 4/4Workshop Electrical engineering II B 4/5Teacher / Instructor room B 4/6Conference room B 4/7Head of Department office B 4/8Deputy office / Secretariat B 4/9

Hall B2 Briefing room B 2/5

Laboratory block LC3

Laboratory electrical engineering / control technology LC 3/5

Theory class room LC 3/6LC 3/2LC 3/10

Theory block right TCR Computerroom TCR 1/4

TCR 1/5

Barack C9 Theory class roomC 9/1C 9/2C 9/3

Total per kind of device Electrical engineering / ITTotal Electrical engineering / IT

Total practical training

it c t

ek

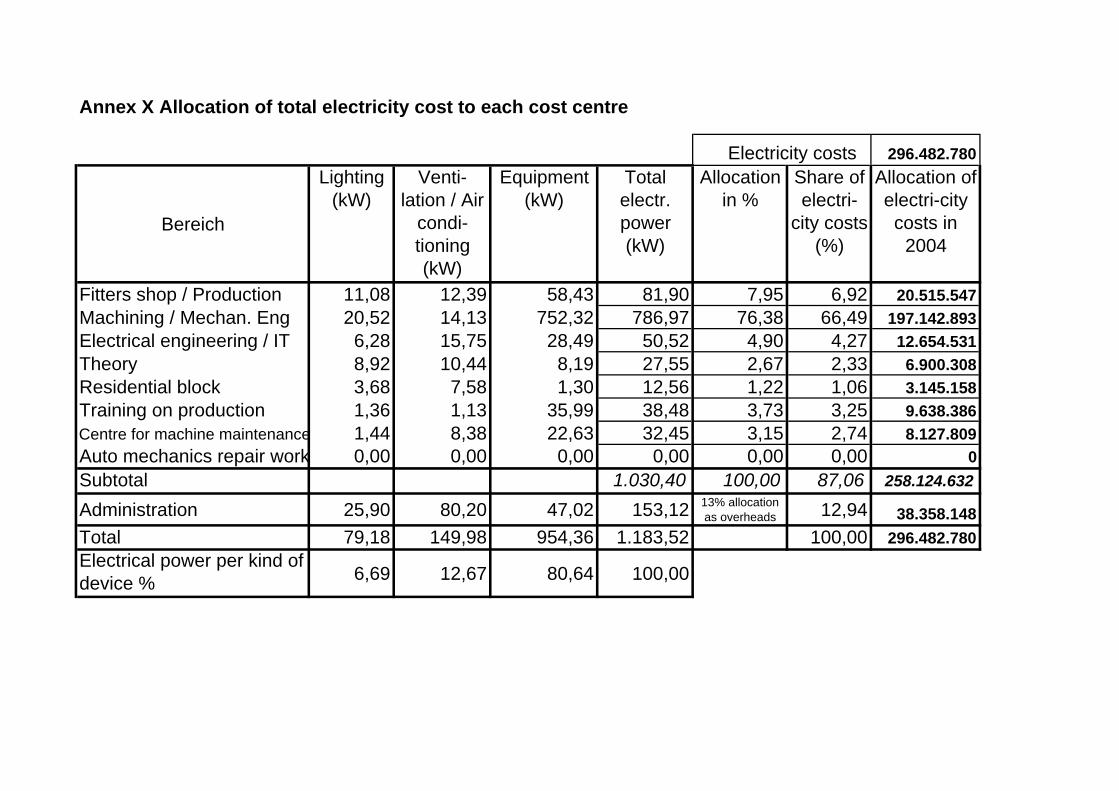

Annex X Allocation of total electricity cost to each cost centre

Electricity costs 296.482.780

Bereich

Lighting (kW)

Venti-lation / Air

condi-tioning (kW)

Equipment (kW)

Total electr. power (kW)

Allocation in %

Share of electri-

c y os s(%)

Allocation of electri-city costs in

2004

Fitters shop / Production 11,08 12,39 58,43 81,90 7,95 6,92 20.515.547Machining / Mechan. Eng 20,52 14,13 752,32 786,97 76,38 66,49 197.142.893Electrical engineering / IT 6,28 15,75 28,49 50,52 4,90 4,27 12.654.531Theory 8,92 10,44 8,19 27,55 2,67 2,33 6.900.308Residential block 3,68 7,58 1,30 12,56 1,22 1,06 3.145.158Training on production 1,36 1,13 35,99 38,48 3,73 3,25 9.638.386Centre for machine maintenanc 1,44 8,38 22,63 32,45 3,15 2,74 8.127.809Auto mechanics repair wor 0,00 0,00 0,00 0,00 0,00 0,00 0Subtotal 1.030,40 100,00 87,06 258.124.632

Administration 25,90 80,20 47,02 153,12 13% allocation as overheads 12,94 38.358.148

Total 79,18 149,98 954,36 1.183,52 100,00 296.482.780Electrical power per kind of device % 6,69 12,67 80,64 100,00

Cost category Budget record Denomination of cost Comments / Clarifications Source of information

Personnel 1,00 Total personnel related costs =SUM(1.01 : 1.12) Accounting data of the automotive repair workshop

Pers 1,01 civil servants Employees with an employment contract issued by the Ministry of Industry including quarterly and extraordinary incentives

Pers 1,02 Specialists with a long term employment contract Employees with a long term employment contract issued by the TVET institution

Pers 1,03 Specialists with a short term employment contract Employees with a short term employment contract issued by the TVET institution or the workshop

Pers 1,04 Maintenance and repairs Personnel costs (own staff) for the zur Maintenance and repairs of buildings and equipment

Pers 1,05 Further training for staff cost for further training by internal or external providers

Pers 1,06 Administration staff including technicians and assistants

Cost of personnel in administration, office and warehouse, in full or part time employment

Pers 1,07 other technicians and assistants (employed) Cost of service personnel in full or part time employment (e.g. cleaning, security, etc.)

Pers 1,08 Travel expenses (employed personnel) Tickets, accomodation for work related travel (Study, Seminars, Firm or school visits)

Pers 1,09 Allowances for employees Allowances regularly paid to employees (e.g. food subsidy)

Pers 1,10 Employer's share of social security payments for employees

Levies, tax, other payments paid for employees for the purposes of insurance, pension, medical and accident insurance (according to contract, law or voluntarily)

Pers 1,11 Overtime and exrta pay Additional payments (e.g. extra pay for work on weekends, public holidays, overtime)

Annex XI Budget chart of accounts (Automechanics repair workshop)

Cost category Budget record Denomination of cost Comments / Clarifications Source of information

Pers 1,12 other, please specify other, please specify

Cost of capital 2,00 Total cost of capital =SUM(2.01 : 2.07)

Workshop datra (Inventory); based on original procurement costs, estimated lifetime and kind of amortisation)

Cap 2,01 Rent Kosten für Miet- oder Pachtzahlungen

Cap 2,02 Amortisation Vehicles Abschreibung von eigenen Fahrzeugen der Werkstatt

Cap 2,03 Amortisation Buildings Abschreibung der genutzten Gebäudesubstanz

Cap 2,04 Amortisation Equipment Abschreibung des Inventars (z.B. Hebebühnen, Motortester, Mobiliar) mit einem Anschaffungswert größer = 5 Mio. VND

Cap 2,05 Amortisation main technical installations Abschreibung zentral genutzter technischer Anlagen (z.B. Drucklufterzeugung, Gasversorgung, Ölabscheider)

Cap 2,06 other, please specify other, please specify

Cap 2,07 other, please specify other, please specify

Current costs 3,00 Total Current costs excluding Personnel =SUM(3.01 : 3.13) Accounting data Automotiverepair workshop

curr 3,01 Material for service provision Material costs (e.g. spare parts), charged to clients

curr 3,02 Material für training costs for preparing, implementing and wrapping up of training programmes

curr 3,03 Supplies and disposal costs for electricity, water and all further services paid for by the TVET institution

Cost category Budget record Denomination of cost Comments / Clarifications Source of information

curr 3,04 Administration and communications Costs for consumables and forworkshop administration (e.g. office supplies, printer cartridges, software, phone, fax, internet, e-mail)

curr 3,05 Consumanbles for maintenance and service of main technical installations Einrichtungen Cleaning products, spare parts for internal maintenance

curr 3,06 External services costs for external service providers (e.g. waste disposal, plant maintenance,security, repairs, maintenance)

curr 3,07 Insurance Insurance premiums not for specified individuals but for the whole workshop (e.g. accidents, legal liability, damages caused by fire, lightning, floods)

curr 3,08 Concept development and updating cost for updating, developing, instroducing, training manuals by own personnel

curr 3,09 Advertising and marketing Advertising costs for services and training offered

curr 3,10 Claims and guarantee items Claims (post-sale) caused by faulty or sub standard repair work (e.g. loss of material, damage, extra work load, extra usage of equipment and tools)

curr 3,11 Entertaining expenses costs for entertaining (e.g. food and drinks) during meetings, visits by delegations, guests

curr 3,12 Consumables for service provision Material for clients' orders which is not charged separately (e.g.anto-rust spray, grease, ...)

curr 3,13 Oil procurement all expenses with regard to procurement of motor and gearbox oil

curr 3,14 External services for client orders all external services associated to clients orders (e.g. Paint, bodywork, welding jobs)

curr 3,15 Cost of procurement for material Expenses for material procurement (e.g. transport, fuel, delivery of material by external providers)

Cost category Budget record Denomination of cost Comments / Clarifications Source of information

Costs 4,00 Total all costs =SUM(1,00 + 2,00 + 3,00) Total cost categories 1 to 3

Income 5,10 Total gross income for the automotive repair workshop =SUM(5.11 : 5.19)

Accounting data automotove repair workshop

Inc. 5,11 Subsidies regular payments (Salary, performance incentives by hte TVET institution to the automotive repair workshop)

Inc. 5,12 Income from work orders all income from servicesto clients

Inc. 5,13 Income from internship contracts all income from curriculum based training (e.g. internship contracts with the institution for skilled workers and technicians)

Inc. 5,14 Income from further training all income from further training (e.g optional training modules for technicians, drivers, etc.)

Inc. 5,15 Income from spare part shop all income from spare part sales

Inc. 5,16 other income all income from returning reusable materials such as used oil, metal, plastic, cardboard, paper, etc)

Inc. 5,17 Value added by participants Value of the services provided by participants during their assignment

Inc. 5,18 Support through foreign aid fundsall contributions from foreign organisations or individuals which are related to a cost category inthis form; capital investments are only recorded in the inventory and affect amortisation!

Inc. 5,19 Income from oil sales all income from oil sale

Inc. 5,20 Income from external services all income related to carrying forward external services

Balance 6,01 Balance for the institute or the enterprise =1.00 + 2.00 + 3.00 - 5.10Total costs minus income of the automotive repair workshop

u

Annex XII Workshop orders monthly analysis working sheet February 2006Carried forward from previous month (c

Date Invoice Nr

Budget record Text budget record Cost centre Order No. Text Comment Payment

(Currency)Cash receipt (Currency)

Share of tax

(currency)

Cash disbursement

(Currency)

Cash fund balance (currency)

04.02.06 26 3,01 Materials for service provision

302 automotive repair workshop B27 …

16.02.06 28 3,01 Materials for service provision

302 automotive repair workshop B29 …

05.02.06 30 3,01 Materials for service provision

302 automotive repair workshop B31 …

13.02.06 31 3,01 Materials for service provision

302 automotive repair workshop B32 …

2006-02-16 33 3,04 Administration and communications

302 automotive repair workshop B34 …

2006-02-01 34 3,11 Entertainment expenses

302 automotive repair workshop B35 …

2006-02-01 35 3,06 External service provision

302 automotive repair workshop B36 …

2006-02-01 36 3,01 Materials for service provision

302 automotive repair workshop B37 …

2006-02-01 37 3,04 Administration and communications

302 automotive repair workshop B38 …

… … … … … … … … … … … … …

Entertainment expenses

Annex XIII Overview of outstanding receivables and payables automotive repair workshop FEBR. 06Sequential cash book

number

Name Employee /

Client

Value of order (currency) Receipt (currency) Disbursement

(currency)Receivables (currency)

Outstanding payables

(Währung)

Auftrag Saldo (Währung)

1 2 3 4 5 6= 1-2(3)B27 … 53.000 - 53.000 - - 0

… … … … … … … …

A65 … 150.000 150.000 - - - 0

… … … … … … … …

A85 … 170.000 - - - 170.000 170.000

… … … … … … … …

- 170.000 170.000

ANNEX XIV Annual financial statement

No.: Denomination Year-end balance (currency)A1 Public subsidies (Students)2 TVET fees (Students) 3 Income from services and TVET measures 4 Income from residential block5 Income fraom training on production 6 Project funds (Germany)

Total IncomeII1 Salaries (external and personnel)2 Stipendien für Studenten3 Employer's social insurance contribution (external and personnel)4 Incentives (external and personnel)5 Electricity costs (Recors od electric power and personnel)6 Water, sewage, waste disposal (area)7 Telecommunications expenses (external and personnel)8 Vehicles, excluding personnel costs (personnel)9 Books and printed media (personnel)10 Advertising costs (area)11 office supplies (personnel)12 Meeting expenses (personnel) 13 Travel expenses (personnel)14 External service provision (area)15 Training material (preparation and material)16 Security (external and area)17 Minor repairs (area)18 Construction work (area)19 new investments from core funding (preparation and area)20 Other expenses (Personnel)21 Project funds (Germany)

Total Expenses

a

Annex XV Variable gross margin per TVET area

No.: Denomination Year-end Balance

Area Fitters shop / Production Area … Overheads

(Admin)

A (currency) direct (currency)

indirect (currency) direct in-

direct (currency)

1 Public subsidies (Students) 6.123.800.000 0 1.469.712.000 … … 02 TVET fees (Students) 4.182.738.000 0 1.003.857.120 … … 03 Income from services and TVET measures 387.969.364 0 0 … … 3463913644 Income from residential block 130.750.000 0 0 … … 05 Income from training on production 129.517.982 0 0 … … 06 Project funds (Germany) 438.589.362 0 0 … … 0

Total income 11.393.364.708 0 2.473.569.120 … … 346.391.364II Total income per area 2.473.569.120 … 346.391.3641 Salaries (support and personnel) 3.595.944.375 439.709.672 157.971.334 … … 1.316.427.7842 Stipendien für Studenten (support) 298.000.000 94.721.415 0 … … 03 Employer's social insurance contribution (support and pe 355.631.837r 27.235.000 13367604 … … 1113967004 Incentives (support and personnel) 116.721.300 11.228.000 4601040 … … 383420005 Electricity costs (Records od electric power and personn 296.482.780e 20.515.547 4602977,76 … … 383581486 Water, sewage, waste disposal (area) 26.300.820 0 3156098,4 … … 07 Telecommunications expenses (external and personnel) 92.270.985 3.615.077 7214728,44 … … 601227378 Vehicles, excluding personnel costs (personnel) 140.569.900 0 16868388 … … 09 Books and printed media (personnel) 157.072.000 0 18848640 … … 010 Advertising costs (area) 52.540.054 0 6304806,48 … … 011 office supplies (personnel) 169.682.141 0 20361856,92 … … 012 Meeting expenses (personnel) 52.984.500 0 6358140 … … 013 Travel expenses (personnel) 150.394.700 0 18047364 … … 014 External service provision (area) 77.233.300 0 9267996 … … 015 Training material (support and material) 1.147.841.987 0 424701535,2 … … 016 Material for service provision (automotive workshop) 0 0 … … 017 Security (supports and area) 141.494.700 0 16979364 … … 018 Minor repairs (area) 504.156.342 0 60498761,04 … … 019 Construction work (area) 750.345.000 0 90041400 … … 020 new investments from core funding (preparation and are 2.558.498.500 540.155.000 143354868 … … 119462390021 Other expenses (Personnel) 270.610.125 0 32473215 … … 022 Project funds (Germany) 438.589.362 0 0 … … 0

Total expenses 11.393.364.708 1.137.179.711 1.055.020.117 … … Total expenses per area 2.192.199.828 …

Balance 281.369.292 … Number of participants 1.254 …

Average TVET costs per paerticipant within a certain area 3.496.331 …

Annex XVI Overheads allocation table

Areaby personnel (number of)

by participants (number of)

by usable floor space (qm) by (KWh) Materialver-

brauch

direct % direct % direct % direct % direct %Fitters shop / Production 23 12 1.254 24 840 12 82 8 37Machining / Mechanical engineeri 37 20 1.648 32 1.516 21 787 76 17Electrical engineering / IT 23 12 826 16 1.108 15 51 5 32Theory 50 26 1.435 28 1.541 22 28 3 14Resindetial block 20 11 `523 0 1.231 17 13 1 0Training on production 18 10 0 0 600 8 38 4 0Centre for machine maintenance and repairs / Training

10 5 0 0 360 5 32 3

Automotive repair workshop 7 4 0 0 0 0 0188 100 5.163 100 7.196 100 1.031 100 100

Published by Deutsche Gesellschaft für Technische Zusammenarbeit (GTZ) GmbH - German Technical Cooperation - Dag-Hammarskjöld-Weg 1-5 65760 Eschborn / Germany

Economic Development and Employment Division (41) Technical and Vocational Education and Training (4115) Staff responsible for publication: Edda Grunwald Telefon: 00 49 (0)6196 791222 Telefax: 00 49 (0)6196 79 80 1222 Email: [email protected] Author: Andreas Jörk August 2006