GUIDELINES ON SUBMISSION OF DEPOSIT PRODUCT INFORMATION … · GUIDELINES ON SUBMISSION OF DEPOSIT...

20

1| Page GUIDELINES ON SUBMISSION OF DEPOSIT PRODUCT INFORMATION ISSUE DATE: 18 August 2010

Transcript of GUIDELINES ON SUBMISSION OF DEPOSIT PRODUCT INFORMATION … · GUIDELINES ON SUBMISSION OF DEPOSIT...

1 | P a g e

GUIDELINES ON SUBMISSION OF DEPOSIT PRODUCT INFORMATION

ISSUE DATE: 18 August 2010

2 | P a g e

TABLE OF CONTENTS

SECTION 1: INTRODUCTION 1

1.1 BACKGROUND 1

1.2 ENQUIRIES 2

SECTION 2: INSURABILITY CRITERIA 2

2.1 INSURABILITY CRITERIA 2

2.2 EXCLUDED DEPOSIT 3

SECTION 3: CERTIFICATION OF DEPOSIT PRODUCTS 3

SECTION 4: DPR FORMS 4

4.1 SUBMISSION OF DPR FORMS 4

4.2 NEGOTIABLE INSTRUMENTS OF DEPOSIT 4

4.3 REPURCHASE AGREEMENTS AND SELL AND BUY BACK AGREEMENTS (“REPOS”) 5

4.4 INVESTMENTS LINKED TO DERIVATIVES 5

4.5 COMBINATION‐TYPE DEPOSIT PRODUCTS 6

4.6 GUIDE TO COMPLETING THE DPR FORMS 6

4.7 SUBMISSION OF COMPLETED DPR FORMS 6

4.8 INSURABILITY STATUS OF DEPOSIT PRODUCTS 7

4.9 SUBMISSION AFTER 30 SEPTEMBER 2010 7

4.10 SUBMISSION OF DECLARATION 8

4.11 IMPLEMENTATION OF THE PRODUCT REGISTRY SYSTEM AND ISSUANCE OF DEPOSIT PRODUCT CODES 8

APPENDIX A 1

1 | P a g

1.1

1.1.1

1.1.2

1.1.3

1.1.4

1.1.5

1 Schedu

N

e

BACKGROUND

As memberson 31 Decembased on the

Also, certainmay not be instruments

In preparatito comply wof Informatiwill resumedetermine wInformation

These GuideIslamic and c

An overviewbelow:

led to be effe

Deposcertpara

No action requnder thesGuideline

D

s are aware,mber 2010. Te provisions

n deposits aninsured by Ps are assesse

on for the ewith the provion on Depoe the proceswhether they Regulations

elines on Subconventiona

w of the proc

ctive on 1 Jan

sit products aified by PIDMgraph 3.1 of tGuidelines)

uired se s

Msf

Pw

SECTION

the GovernThereafter, tof the Malay

nd instrumenPIDM on or ad under PIDM

exit of the Gvisions in theosit Insurancss of certifyy are insurabs are ready to

bmission of Dal members.

cess contemp

nuary 2011

lready (see these

Members willsubmit e‐DPRforms in 2011and Deposit

Product Codeswill be issued tmembers by mid‐2011

N 1: INTROD

ment Deposthe scope of ysia Deposit

nts that are after 1 JanuaM’s insurabi

DG and to ee draft Malayce) Regulatioying all theble or not. Mo be implem

Deposit Prod

plated unde

MembersDeposit Prod

s o

Pcd

Memsub

Formpr

infodocundGuidlateSep

DUCTION

sit Guarantecoverage ofInsurance C

currently guary 2011, acclity criteria.

enable the mysia Deposit ons 20101 (“Ideposit pro

Members willented.

duct Informa

r these Guid

s’ ucts

Deposit prodPIDM. These acurrently offedeposit produ

b

mbers to bmit DPRms and the roduct ormation cuments der these elines not r than 30 ptember 2010

e (“GDG”) isf insured deporporation A

uaranteed uncording to ho

member instiInsurance CoInformation oducts of mel be separate

tion (“Guide

delines is dep

ucts not yet care: (a) deposred by membucts that will bby members

PIDMmember

insurabilitproducts

PIDM wiProdu

member

s scheduled tposit productAct 2005 (“th

nder the GDGow those de

tutions (“meorporation (PRegulationsembers, in ely advised w

elines”) apply

picted in the

certified by sit products ers; and (b) be launched

Mwill inform rs regarding thy status of thes by 31 Octobe2010

ll issue Deposuct Codes to rs by mid‐201

to expire ts will be he Act”).

G may or eposits or

embers”) Provision s”), PIDM order to when the

y to both

diagram

he ese er

sit

1

2 | P a g e

1.2 ENQUIRIES

Enquiries on the Guidelines may be directed to [email protected]

SECTION 2: INSURABILITY CRITERIA

2.1 INSURABILITY CRITERIA 2.1.1 A deposit product is insurable by PIDM if it satisfies the insurability criteria. The insurability

criteria are set out in the Guidelines on Insurability of Deposits2 (“Insurability Guidelines”), which will be issued in October 2010.

2.1.2 The insurability criteria are as follows:

(a) monies received by the member constitute an Islamic deposit or a conventional deposit, whichever is the case, as defined under subsection 2(1) of the Act;

(b) monies are received by the member in the usual course of its business of deposit‐taking. This criterion will exclude, for example, monies received from Bank Negara Malaysia and monies received by the member strictly for the purpose of payment transactions (e.g. payment through GIRO or an issued traveller’s cheque);

(c) repayment of the principal amount is made in money and not in money’s worth; (d) the liability of the member in respect of monies received by it constitutes a deposit

liability or is treated as a “deposit accepted” in the records of the member. Monies which are provided to the member as security for a conventional credit facility or an Islamic financing facility are included in this criterion if such monies are treated as a “deposit accepted” for purposes of FISS reporting to Bank Negara Malaysia;

(e) the person entitled to a repayment by the member is identifiable from the contract

between the member and the depositor; (f) in the case of an Islamic product only, the monies deposited shall be used by the

member for one or more of the banking business purposes as specified by Bank Negara Malaysia in its Framework Of Rate Of Return namely, provision of finance, investment in securities, interbank placements, or such other business prescribed by Bank Negara Malaysia that complies with Shariah;

2 For the “Consultation Paper on Proposed Guidelines on the Criteria for Determining Insured Deposits” (issued in June 2007) and the “Reponses on the Consultation Paper on the Proposed Guidelines on the Criteria for Determining Insured Deposits”, please visit PIDM’s website at www.pidm.gov.my

3 | P a g e

(g) in the case of a conventional product only, the member is obliged to repay the

principal amount in full. This obligation may be specified in the contract between the member and depositor, or by established principles of law, for example, in the case of a savings or current account; and

(h) an investment linked to derivatives or a structured product3 may be eligible for

deposit insurance provided it satisfies the criteria set above. The fact that deductions may be made from the principal amount on early withdrawal, redemption or termination of an investment by the investor or the member, prior to the maturity date of such investment does not, by itself, mean that the criteria cannot be fulfilled.

2.2 EXCLUDED DEPOSIT 2.2.1 The Act also provides that certain deposit products are excluded from deposit insurance.

SECTION 3: CERTIFICATION OF DEPOSIT PRODUCTS 3.1 DEPOSIT PRODUCTS THAT HAVE ALREADY BEEN CERTIFIED BY PIDM AS INSURABLE 3.1.1 Prior to the implementation of the GDG, members have submitted and PIDM has certified

certain of their deposit products as insurable (“Existing Insurable Deposit Products”). 3.1.2 No action from the members is required under these Guidelines in respect of the Existing

Insurable Deposit Products. 3.2 OTHER DEPOSIT PRODUCTS 3.2.1 We are resuming the process of certifying members’ deposit products to confirm their

insurability status. The deposit products that PIDM will certify are those that: (a) are currently offered by the members; and (b) will be launched by the members.

3 Including any investment product that falls within the definition of “securities” under the Securities Commission Act 1993 and which derives its value by reference to the price or value of an underlying reference (e.g. any security, currency, commodity, index or other assets or reference, or combination of such assets or reference).

4 | P a g e

3.2.2 The cut‐off date for submission of the information on deposit products referred to in Section 3.2.1 is 30 September 2010. PIDM will inform members regarding the insurability status of these products by 31 October 2010. Notwithstanding the cut‐off date, members are required to submit to PIDM, information regarding new deposit products that will be launched after 30 September 2010.

3.2.4 Enclosed in the Guidelines is a CD containing softcopies of the deposit product registration forms (“DPR Forms”) in MS Word for Islamic deposit product and conventional deposit product respectively. The contents of the Islamic and conventional DPR Forms are in Appendix A of the Guidelines.

SECTION 4: DPR FORMS

4.1 SUBMISSION OF DPR FORMS 4.1.1 The Islamic and conventional DPR Forms set out the questions to be completed by the

members. Members are required to use the Islamic DPR Form for Islamic deposits and conventional DPR Form for conventional deposits. Subject to the specific provisions on negotiable instruments of deposits, repurchase agreements, investments linked to derivatives and combination‐type of deposit products below, members are required to complete one DPR Form for every deposit product offered.

4.2 NEGOTIABLE INSTRUMENTS OF DEPOSIT 4.2.1 Conventional negotiable instruments deposits (“NIDs”) and Islamic negotiable instruments

(“INIs”) are not insurable by PIDM. 4.2.2 In respect of conventional NIDs, the DPR Form is to be submitted according to the type of

the NIDs. The members are required to submit one DPR Form, on a collective and one‐off basis, for each type of NID, namely, fixed, zero coupon or floating rate or a combination of either of the three. The members are also required to submit one (1) set of master or generic deposit product information4 applicable for that type of NID.

Example: A member has issued numerous zero coupon NIDs. One DPR Form is to be submitted in respect of the zero coupon NIDs issued on a collective and on‐off basis. The master or generic deposit product information is to be submitted. The member is not required to submit a new DPR Form in respect of new launches or issuance of zero coupon NIDs.

4.2.3 In respect of INIs, the DPR Form is to be submitted according to the Shariah contract or contracts applied to the INIs. Members are required to submit one DPR Form, on a collective

4 Product brochure, term sheet, contract terms and conditions, deposit application form, sample deposit placement receipt and/or product description.

5 | P a g e

and one‐off basis, for each group of INIs that apply the same Shariah contract or contracts. The members are required to submit one (1) set of master or generic deposit product information applicable for that type of INI.

Example: A member has issued numerous INIs according to the Shariah contract of

Mudharabah. One DPR Form is to be submitted in respect of this type of INIs on a collective and on‐off basis. The master or generic deposit product information is to be submitted. The member is not required to submit a new DPR Form in respect of new launches or issuance of INIs that are based on the Shariah contract of Mudharabah.

4.3 REPURCHASE AGREEMENTS AND SELL AND BUY BACK AGREEMENTS (“REPOS”)

4.3.1 Conventional repurchase agreements (“conventional repos”) and Sell and Buy Back Agreement (“Islamic repos”) are not insurable by PIDM.

4.3.2 In respect of conventional repos, members are required to submit one DPR Form, on a

collective and on‐off basis, for all types of conventional repos. The members are also required to submit one (1) set of master or generic deposit product information applicable for the conventional repos.

4.3.3 In respect of Islamic repos, members are also required to submit one DPR Form, on a

collective and one‐off basis, for all types of Islamic repos. The members are also required to submit one (1) set of master or generic deposit product information applicable for the Islamic repos.

4.4 INVESTMENTS LINKED TO DERIVATIVES 4.4.1 Generally, conventional investments linked to derivatives or structured products (“ILDs”) are

insurable if they are 100% principal guaranteed if held to maturity provided that they satisfy the other insurability criteria.

4.4.2 In respect of non‐principal guaranteed conventional ILDs, the DPR Forms are to be

submitted according to the underlying reference or combination of underlying references. Hence, members are required to submit one DPR Form, on a collective and one‐off basis for each group of ILDs that derive their values by reference to the same type of underlying reference or the same combination of underlying references. Members are not required to submit a fresh DPR Form in respect of future launches of that group of ILDs. The members are required to submit one (1) set of master or generic deposit product information applicable for that type of ILDs.

Example: If a member has issued numerous non‐principal guaranteed conventional ILDs that derive their values by reference to the price of commodity, then, one DPR Form is to be submitted for this group of ILDs. The member does not need to submit a fresh DPR Form in respect of future launches of ILDs that derive their values by reference to the price of commodity. If the underlying references of the non‐principal guaranteed conventional ILDs

6 | P a g e

are a combination of commodity and another reference, the member will have to submit a separate DPR Form in respect of that group of ILDs.

4.4.3 Generally, conventional ILDs which are 100% principal guaranteed are insurable, subject to these ILDs meeting the insurability criteria. As such, PIDM will assess these ILDs against the insurability criteria to determine their respective insurability status. Members are required to submit one DPR Form for each principal guaranteed conventional ILD. The members are required to submit the deposit product information for that ILD.

4.4.4 Members are required to submit one DPR Form for each Islamic ILD. The members are

required to submit the deposit product information for that ILD.

4.5 COMBINATION‐TYPE DEPOSIT PRODUCTS

4.5.1 These refer to deposit products that are made up of two or more deposit products (“component deposit product”) but are “packaged” together and marketed under one brand or name. Under these circumstances, the member is to submit one DPR Form for each component deposit product.

Example 1: A member offers a foreign currency savings account and a foreign currency fixed

deposit account. These accounts are marketed under one brand. The member is required to submit one DPR Form each for the foreign currency savings account and the foreign currency fixed deposit account, together with the relevant deposit product information for these accounts.

Example 2: A member offers a cheque book facility in respect of its savings account. One DPR Form is to be submitted in respect of the savings account. This is not a combination‐type account.

4.6 GUIDE TO COMPLETING THE DPR FORMS 4.6.1 Appendix A sets out the instructions and guidance to assist members to complete the DPR

Forms.

4.7 SUBMISSION OF COMPLETED DPR FORMS 4.7.1. Members are required to submit the softcopy of the completed DPR Forms (in MS Word)

together with the softcopies of the deposit product information in the following manner:

(a) members are to create one folder for each deposit product and save, in the said folder, the softcopies of the completed DPR Form and the deposit product information. Separate folders should be created for separate deposit products. Please follow this naming convention for the folder: name of the member‐name of the deposit product‐deposit type, for example, abc‐super‐fd (where ABC is the name of the member, Super Returns is the name of the product and the deposit type is fixed deposit). Use short words, if possible;

7 | P a g e

(b) the DPR Form and the deposit product information are to be saved according to their document type, namely, dpr for DPR Form; bre for Product Brochure; ts for Term Sheet; appn for Application Form; rect for Sample Deposit Placement Receipt; illus for Product Description or Illustration and formula for the Formulation for Calculation of Interest;

(c) the DPR Form is to be saved as an MS Word document. The deposit product

information and other attachments are to be saved in any of the following file formats: (a) xls; (b) xlsx; (c) doc; (d) docx; (e) ppt; (e) pptx; (f) pdf (searchable); (g) txt; or (h) rtf. If the aforesaid file formats are not available, please save in any of the following: (a) jpeg; (b) jpg; (c) bmp; (d) tiff; (e) gif; (f) png; or (g) pdf (not searchable); and

(d) the folders in respect of all the deposit products submitted are to be saved in a CD(s)

and delivered to PIDM by 30 September 2010. See below for the illustration:

4.8 INSURABILITY STATUS OF DEPOSIT PRODUCTS 4.8.1 PIDM will inform the members, not later than 31 October 2010, regarding the insurability

status of the deposit products submitted.

4.9 SUBMISSION AFTER 30 SEPTEMBER 2010 4.9.1 Notwithstanding the cut‐off date referred to in Section 3.2.1, members are required to

submit to PIDM, the deposit product information regarding new deposit products that will be launched after 30 September 2010 to enable PIDM to assess their insurability status.

4.9.2 The deposit product information referred to in Section 4.9.1 and the completed DPR Form

should be provided to PIDM at least 14 business days before the expected launch date. Members can submit to PIDM the draft version of the deposit product information rather than the final version. However, there should not be any amendments to the draft deposit product information after the submission which will affect or change any of the answers given in respect of the questions marked with an asterisk (*) in the DPR Forms in Appendix A, as such change may affect the deposit product code or the insurability status of the deposit product. Where the draft version of deposit product information is given to PIDM, members are required to submit the final documents immediately upon launching the deposit product. Members are also required to inform PIDM if the deposit products are not launched.

abc‐super‐fd [Folder name of the deposit product] .......... dpr.doc [File name for DPR Form]

......... bre.txt [File name for Brochure] .......... ts.doc [File name for Term Sheet] .......... appn.pdf [File name for Application Form] .......... rect.ppt [File name for Sample Deposit Placement Receipt] .......... illus.txt [File name for the Product Description or Illustration] .......... formula.txt [File name for the Formulation for Calculation of Interest]

8 | P a g e

4.10 SUBMISSION OF DECLARATION 4.10.1 Upon informing the members regarding the insurability status of the deposit products or

soon thereafter, PIDM will request the members to sign the relevant declarations. The person signing the Declaration must be a senior officer designated by the member, holding a senior position in Management or charged with the responsibility of a department within the member, and is able to engage PIDM in discussions and clarification on the deposit product.

4.11 IMPLEMENTATION OF THE PRODUCT REGISTRY SYSTEM AND ISSUANCE OF DEPOSIT PRODUCT CODES 4.11.1 When the Product Registry System is implemented by PIDM in 2011, PIDM will require

members to submit the electronic DPR forms (“e‐DPR Forms”) in respect of the Existing Insurable Deposit Products and all new deposit products to be launched by the members during that time. The contents of the e‐DPR Form will be substantially similar to the DPR Forms. Members will be advised on this in due course.

4.1.12 The deposit product codes in respect of all the deposit products will be issued to the

members in mid‐2011.

THE REST OF THIS PAGE HAS BEEN INTENTIONALLY LEFT BLANK

1 | P a g e

APPENDIX A (Instructions and Guidance to Complete the DPR Form)

A. MEMBER INSTITUTION’S INFORMATION QUESTIONS FURTHER DETAILS

1. ∗ Name and FISS Code Fill in the name of the Bank and the FISS Code. 2. Name of Contact Person Fill in the name of the officer completing this form (“Officer”). 3. Designation Fill in the designation of the Officer. 4. Department Fill in the department in which the Officer works. 5. Street Name 1 Questions 5 – 9: Fill in the address where the Officer works. 6. Street Name 2 7. City 8. Postcode 9. State 10. Telephone No. Fill in the Officer’s telephone number and the general number. 11. Fax No. Fill in the Officer’s fax number. 12. Email Address Fill in the Officer’s e‐mail address. We will not accept postmaster or general

use e‐mail addresses, eg. [email protected]. 13. MI Reference This is the reference number that the Bank may insert so that PIDM can

quote this reference if there is a need to correspond on this matter. 14. MI Business Type Conventional Banking

Islamic Banking Both

This refers to the type of banking business the Bank operates. If the Bank operates both conventional and Islamic banking (window), then the Bank is to select “Both”.

B. DEPOSIT PRODUCT INFORMATION

∗ See paragraph 4.9.2 of the Guidelines. If draft versions are submitted, there must not be any change to this answer

QUESTIONS FURTHER DETAILS 15. Name of Product Fill in the name of the Product. 16. Date of Launch • If the Product is already launched, and the date is not known, to state

“Already Launched; Launch Date Not Available”. • If the Product will be launched and the launch date is not known, to

provide answer in general terms, eg, first quarter of 2011. • Where one DPR Form is to be submitted for launched deposit products

on a collective basis (eg: NIDs and Repos), to state “Collective Submission ‐ Various Launch Dates”.

2 | P a g e

∗ ∗ See paragraph 4.9.2 of the Guidelines. If draft versions are submitted, there must not be any change to this answer

17. Please indicate which of the following documents are attached:

Product brochure Term Sheet Contract Terms & Conditions Deposit Application Form Sample Deposit Placement Receipt Product Description or Product Illustration Others (please specify)

Select the documents you have attached. If a master agreement is applicable for various deposit products, members have to attach the master agreement for every deposit product and indicate the sections in the master agreement that are relevant for the deposit product.

18.∗ What is the deposit currency?

Ringgit Only Foreign Only Ringgit and Foreign

Select the currency type of the deposit product.

19.∗ Please select ONE of the following deposit types:

Demand Deposit Savings Deposit Fixed Deposit Specific Investment General Investment Commodity Murabahah Short Term Deposit Bearer Deposit Negotiable Instrument of Deposit / Islamic Negotiable Instrument Repurchase Agreement Money Market Deposit Investment Linked to Derivatives Offered / Structured Product Other Deposits Accepted (please specify)

• Select the deposit type. • Please note that “Money Market Deposit” referred to above means a

deposit in a specific account opened or maintained with a member who is an approved interbank institution (approved by Bank Negara Malaysia) expressly for the purpose of placement in the interbank money market (including, where applicable, the Islamic Interbank Money Market).

3 | P a g e

C. INFORMATION RELATING TO INVESTMENT LINKED TO DERIVATIVES/STRUCTURED PRODUCT QUESTIONS FURTHER DETAILS20. ∗ Please state the category of

underlying assets/reference or combination of underlying reference

State the type of underlying reference or the combination of underlying references (eg. security, index, currency, commodity or other assets or reference).

21. Have you obtained the necessary approvals from the Securities Commission and Bank Negara Malaysia in respect of the issue, offer, invitation for or making available this ILD?

Yes No

If Yes, to attach copies of the approval.

22. * If repayment of principal is not by way of money, please state how or in what method will the principal be repaid

To complete if applicable.

∗ See paragraph 4.9.2 of the Guidelines. If draft versions are submitted, there must not be any change to this answer

4 | P a g e

D. SPECIAL CONDITIONS QUESTIONS FURTHER DETAILS23. Are there any special

conditions for this product? Yes No

If your answer to question 23 is Yes, please answer question 24 If there is a special condition for a customer to meet in order to be eligible to open an account of this deposit product, to select “Yes” and provide the information in Question 24.

24. Please select the special condition that applies and provide the details

Age Income Level Occupation Purpose of Account Others (please specify)

Eg. if only adults above 55 years of age are eligible to open this account, to select “Age” and state that only adults above 55 years of age are eligible to open this account.

5 | P a g e

E. DEPOSIT PRODUCT INFORMATION 1. ISLAMIC DPR FORM QUESTIONS FURTHER DETAILS25. ∗ Is this an Islamic deposit? Yes

No If your answer to question 25 is Yes, please answer question 26 This is an Islamic DPR Form, and if the deposit product is an Islamic deposit, to select “Yes”. For conventional deposit products, use the Conventional DPR Form. Notwithstanding that an Islamic ILD is referred to as an “investment”, it will qualify as an Islamic deposit if it fulfils the definition of Islamic deposit referred to below.

26. Please specify which clause in which document supports your answer

• An Islamic deposit is a “sum of money or money’s worth received or paid on terms by any person, under which the receipt and repayment shall be in accordance with the terms of any agreement consistent with the Shariah”.

• If there is no specific clause in any of the documents attached to support your” Yes” answer to Question 26, a sample response could be: There is no specific clause in any of the documents attached. The money is received or paid on terms under which the receipt and repayment shall be in accordance with the terms of any agreement consistent with the Shariah.

Please tick all applicable Shariah contracts and specify the tiering amount or percentage below 27. How is the tiering

apportioned? By Amount By Percentage

If there are 2 or more Shariah contracts applicable for the deposit product, to state if the tiering is apportioned according to amount or percentage.

28. * Please select all that apply and specify the amount / percentage and indicate the ranking

Wadiah Qard Murabahah Wakalah Musyarakah Mudharabah Other

If there are more than two (2) Shariah contracts, to select the applicable Shariah contracts. If tiering is apportioned by amount, to state the amount and if by percentage, to state the percentage. To also indicate the ranking of the respective Shariah contracts. If there is no tiering, please state “No tiering applicable”. Eg. If the Shariah contracts of Wadiah and Mudharabah are applicable, to select both Wadiah and Mudharabah. If tiering is apportioned by amount,

∗ See paragraph 4.9.2 of the Guidelines. If draft versions are submitted, there must not be any change to this answer

6 | P a g e

QUESTIONS FURTHER DETAILSstate the amount apportioned for Wadiah and Mudharabah respectively. Also state which of the Shariah contract ranks first and which, second.

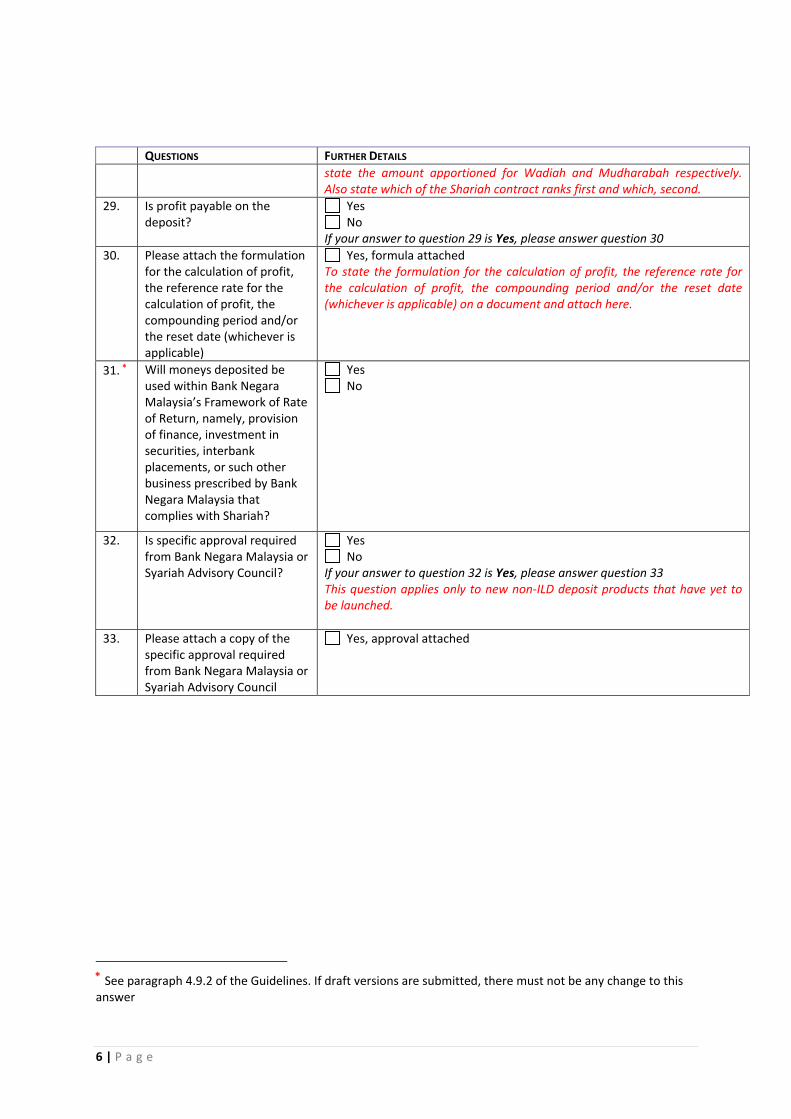

29. Is profit payable on the deposit?

Yes No

If your answer to question 29 is Yes, please answer question 30 30. Please attach the formulation

for the calculation of profit, the reference rate for the calculation of profit, the compounding period and/or the reset date (whichever is applicable)

Yes, formula attachedTo state the formulation for the calculation of profit, the reference rate for the calculation of profit, the compounding period and/or the reset date (whichever is applicable) on a document and attach here.

31. ∗ Will moneys deposited be used within Bank Negara Malaysia’s Framework of Rate of Return, namely, provision of finance, investment in securities, interbank placements, or such other business prescribed by Bank Negara Malaysia that complies with Shariah?

Yes No

32. Is specific approval required from Bank Negara Malaysia or Syariah Advisory Council?

Yes No

If your answer to question 32 is Yes, please answer question 33 This question applies only to new non‐ILD deposit products that have yet to be launched.

33. Please attach a copy of the specific approval required from Bank Negara Malaysia or Syariah Advisory Council

Yes, approval attached

∗ See paragraph 4.9.2 of the Guidelines. If draft versions are submitted, there must not be any change to this answer

7 | P a g e

2. CONVENTIONAL DPR FORM: QUESTION FURTHER DETAILS25. * Is this a conventional (i.e.,

non‐Islamic) deposit? Yes No

If your answer to question 25 is Yes, please answer question 26 This is a Conventional DPR Form, and if the deposit product is a conventional deposit, to select “Yes”. For Islamic deposit products, use the Islamic DPR Form. Notwithstanding that a conventional ILD is referred to as an “investment”, it will qualify as a Conventional deposit if it fulfils the definition of deposit referred to below.

26. Please specify which clause in which document supports your answer

A deposit is “a sum of money received or paid on terms under which it will be repaid or is repayable, with or without interest or a premium, or with any consideration in money, either on demand or at a time or in circumstances agreed by or on behalf of the person making the payment and the person receiving it”. • If there is no specific clause in any of the documents attached to support

your “Yes” answer to Question 26, a sample response could be: There is no specific clause in any of the documents attached. The money is received from the customer on terms that it will be repaid or is repayable, @with/without interest or a premium, or with any consideration in money, either on demand or at a time or in circumstances agreed by or on behalf of the member and the customer (@delete whichever inapplicable)

27. ∗ Is the MI obliged to repay the principal in full?

Yes No

If your answer to question 27 is Yes, please answer question 28 28. Please specify which clause in

which document supports your answer

• The obligation to repay in full may be specified in the contact between the member and the depositor, or by established principles of law.

• For ILDs, the fact that deductions may be made from the principal amount on early withdrawal, redemption or termination of an investment by the investor, prior to the maturity date of such investment does not, by itself, mean that the criterion cannot be fulfilled.

29. Is interest payable on the deposit?

Yes No

If your answer to question 29 is Yes, please answer question 30 30. Please attach the formulation

for the calculation of interest, the reference rate for the calculation of interest, the compounding period and/or the reset date (whichever is applicable)

Yes, formula attachedTo state the formulation for the calculation of interest, the reference rate for the calculation of interest, the compounding period and/or the reset date (whichever is applicable) on a document and attach here.

∗ See paragraph 4.9.2 of the Guidelines. If draft versions are submitted, there must not be any change to this answer

8 | P a g e

3. ISLAMIC DPR FORM AND CONVENTIONAL DPR FORM QUESTIONS FURTHER DETAILS34. * (315)

Is this deposit repayable outside Malaysia?

Yes No

Withdrawal of money via an ATM outside Malaysia does not render the deposit as one that is repayable outside Malaysia.

35. * (32)

Is this deposit in a foreign currency?

Wholly in foreign currency Partly in Ringgit and partly in foreign currency No (MYR only)

36. * (33)

Is this a money market deposit?

Yes No

“Money Market Deposit” means a deposit in a specific account opened or maintained with a member who is an approved interbank institution (approved by Bank Negara Malaysia) expressly for the purpose of placement in the interbank money market (including, where applicable, the Islamic Interbank Money Market).

37. * (34)

Is this a bearer deposit? Yes No

38. * (35)

Is this a negotiable instrument of deposit?

Yes No

39.* (36)

Is this a deposit pursuant to a repurchase agreement?

Yes No

5 The numbers in parenthesis correspond to the Conventional DPR Form

9 | P a g e

F. DEPOSIT LIABILITY

∗ See paragraph 4.9.2 of the Guidelines. If draft versions are submitted, there must not be any change to this answer 6 The numbers in parenthesis correspond to the Conventional DRP Form

QUESTION FURTHER DETAILS

40.∗ (376)

Is the deposit received in the usual course of the MI’s business of deposit taking?

Yes No

(If your answer to question 40 is Yes, please answer question 41) This will exclude, for example, monies received from Bank Negara Malaysia and monies received by the members strictly for the purpose of payment transactions (eg. payment through GIRO or an issued traveller’s cheque).

41. (38)

Please specify which clause in which document supports your answer

If there is no specific clause in any of the documents attached to support your “Yes” answer to Question 40, to state that there is no specific clause in any of the documents attached and that the deposit is received in the usual course of the member’s business of deposit taking.

42.* (39)

Is the deposit repayable in money?

Yes No

(If your answer to question 42 is Yes, please answer question 43) This includes payment by way of cash, or cheque payment or crediting into a deposit account with the member. The answer is No if the deposit is repayable in money’s worth, for example, by the delivery of a commodity.

43. (40)

Please specify which clause in which document supports your answer

If there is no specific clause in any of the documents attached, to explain if the deposit is repayable in money.

44.* (41)

Is the MI’s liability a deposit liability or a deposit accepted?

Yes

No(If your answer to question 44 is Yes, please answer question 45) • This is based on the member’s reporting to Bank Negara Malaysia

under the Guideline for Submission of FISS Reports. • Monies which are provided to the member as security for a

conventional credit facility or an Islamic financing facility are regarded as a deposit liability or deposit accepted if such monies are treated as a “deposit accepted” for purposes of FISS reporting to Bank Negara Malaysia.

45. (42)

Please specify which clause in which document supports your answer

If there is no specific clause in any of the documents attached to support your “Yes” answer to Question 44, to state the FISS Code that is or will be submitted to Bank Negara Malaysia under the Guideline for Submission of FISS Reports.

46.* (43)

Is the person entitled to repayment identifiable from the contract with the depositor?

Yes No

(If your answer to question 46 is Yes, please answer question 44)

10 | P a g e

THE REST OF THIS PAGE HAS BEEN INTENTIONALLY LEFT BLANK

47. (44)

Please specify which clause in which document supports your answer

Such document would include the application form that the depositor is required to fill up.