Going Global: A Practical Survival Guide for Canadian ... · PDF fileGuide for Canadian...

44

Baker & McKenzie LLP is a member firm of Baker & McKenzie International, a Swiss Verein with member law firms around the world. In accordance with the common terminology used in professional service organizations, reference to a "partner" means a person who is a partner, or equivalent, in such a law firm. Similarly, reference to an "office" means an office of any such law firm. © 2015 Baker & McKenzie LLP Going Global: A Practical Survival Guide for Canadian Multinational Employers

-

Upload

phungduong -

Category

Documents

-

view

217 -

download

2

Transcript of Going Global: A Practical Survival Guide for Canadian ... · PDF fileGuide for Canadian...

Baker & McKenzie LLP is a member firm of Baker & McKenzie International, a Swiss Verein with member law firms around the world. In accordance with the common terminology used in professional service organizations, reference to a "partner" means a person who is a partner, or equivalent, in such a law firm. Similarly, reference to an "office" means an office of any such law firm.© 2015 Baker & McKenzie LLP

Going Global: A Practical Survival Guide for Canadian Multinational Employers

© 2015 Baker & McKenzie LLP

Introduction‒ Welcome remarks‒ Agenda The Current Landscape for Global Expansion Getting the Structure Right, Early Tax Opportunities and Pitfalls Realities of Global Employment Equity Compensation

The Current Landscape for Global Expansion

© 2015 Baker & McKenzie LLP 4

The Current Landscape – A Strong Outlook for Worldwide M&A

Source: Thomson Reuters M&A Review, March 2015

© 2015 Baker & McKenzie LLP 5

The Current Landscape

72% 56%

Canada Global

expect to pursue acquisitions in the next 12 months

91% 47%expect to complete more deals than in the prior year

88% 77%

Canada Global

say their largest deal in the next 12 months will be $250m or less

91% 84%are focused on cross-border M&A in the next 12 months

© 2015 Baker & McKenzie LLP 6

The Current Landscape – Companies Look Beyond Borders for Growth‒ Domestic v. global growth rates

© 2015 Baker & McKenzie LLP 7

The Current Landscape

‒ National policies Global Markets Action Plan Trade agreements

‒ Challenges Growth outlook Financial market volatility Geopolitical tensions Greater political and regulatory scrutiny Expansion of sanctions regimes

8

Getting the structure right early

© 2015 Baker & McKenzie LLP 9

Traditional Growth – Formation of Subsidiaries, Branches and Other Presences– Subsidiary – legal entity separate from parent company– Branch - extension of main company, fully operational– Representative / Liaison Office – limited to non-income

generating activities (e.g., “preparatory and auxiliary”)– Joint ventures

© 2015 Baker & McKenzie LLP 10

Drivers for Choice of Presence– Business considerations (e.g., legal restrictions on scope of activity)– Marketplace perception – Management structure – Ongoing cost of maintenance– Timing constraints – Employment / Immigration, Work Permits– Tax considerations (e.g., permanent establishment, utilization of

projected losses, access to Canada’s foreign affiliate system, transfer pricing)

© 2015 Baker & McKenzie LLP

Tax Opportunities and Pitfalls

© 2015 Baker & McKenzie LLP

Three Key Phases of Going International: Tax

1 2 3

Get the basics right

• Customs compliance

• Sales tax compliance

Get the Structure Right

• Minimize PE exposure for home country operating company

• Secondment, direct hire or hybrid arrangements for transferred employees

• Payroll compliance, localized equity incentive plans

• Canadian foreign affiliate and FAPI rules

• Structuring, supply chain planning, IP ownership planning

• Capitalization: debt and/or equity

Implement

• More sophisticated IP and supply chain planning

• Monitor group compliance and exposure

• Cash management and financing offshore operations

Sales to International Customers

Sales to International Customers

"Boots on the Ground” /Local Entity

"Boots on the Ground” /Local Entity

Established InternationalStructure

Established InternationalStructure

12

© 2015 Baker & McKenzie LLP 13

An Effective Tax Strategy Gauges and Mitigates Risks

EU tax climate and OECD BEPS project

Possible changes in tax law

Start up losses and path to profitability

Local presence but not too much local tax

Cash management and financing offshore operations

Tax planning vs. operational flexibility

© 2015 Baker & McKenzie LLP 14

Designing a Structure– Two fundamental elements guide much tax planning

Canadian taxation of foreign affiliates and foreign income Taxable income follows functions, assets & risks

– Transfer pricing Maximize value-creating activities in appropriate places International tug of war currently underway on relative contributions of

functions, assets & risks (and markets)

© 2015 Baker & McKenzie LLP

Realities of Global Employment

© 2015 Baker & McKenzie LLP 16

Key Employment Issues

‒ Hiring entity‒ Kind of hire‒ Onboarding questions‒ Form of offer‒ Key employment terms‒ Policies

© 2015 Baker & McKenzie LLP 17

Pick the Right Engaging Entity: Key Considerations – It’s All Interrelated!– Canadian tax consequences / local country tax consequences– Taxable presence or permanent establishment– Doing business requirements– Employment law requirements Mandatory benefits requirements Foreign exchange control Immigration

– Employee benefits entitlements– Local country pension issues– Eligibility for equity grants

© 2015 Baker & McKenzie LLP 18

Pick the Right Engaging Entity: What are the Options? – “Foreign” employers Canadian parent company or holding company

– Local employers Local subsidiary, branch or representative / liaison office

– Third party entity Partners, distributors, vendors Staffing agencies and PEOs

– Individual Independent contractors

Caution! Extra-territorial application of some Canadian laws CB3

Slide 18

CB3 Need to confirm _, 4/13/2015

© 2015 Baker & McKenzie LLP 19

Who is Being Hired / Engaged?– Director / manager v. non-manager – Employee v. independent contractor Ensure the nature of the relationship is properly classified, i.e.,

reality v. the “label” Continued / extensive use of independent contractors globally

raises misclassification risks worldwide– Employee through third party employer– Employee on expatriate assignment / secondment / TCN

© 2015 Baker & McKenzie LLP 20

Setting Up: Payroll, Benefits, CBAs– Local payroll and benefits provider?– Do application forms comply with local requirements?– Limits / requirements on pre-employment checks? – Do documents require translation?– National Collective Bargaining Agreements?– Additional government filing requirements?

Caution! Data privacy laws

© 2015 Baker & McKenzie LLP 21

Documenting the Hire: Employment Contract– Offer letter v. employment contract?

– Must be compliant with local laws

– Changes may require express consent or be unenforceable, avoid binding statements re: bonus/commission or benefits

– Cultural differences

© 2015 Baker & McKenzie LLP 22

Documenting the Hire: Employment Contract – Key Terms

– Identify the employer– Probationary periods– Duration of employment (definite v. indefinite)– Compensation / benefits– Hours / location– Vacation / holiday– Termination– Choice of law / forum– Arbitration

© 2015 Baker & McKenzie LLP 23

Documenting the Hire– PIIAs Included in employment contracts v. free-standing Intellectual property protection Confidentiality Non competition / solicitation Enforceability of restrictive covenants

‒ Key Policies Handbooks, work rules, internal regulations, etc. Codes of Conduct

‒ Global Compensation Programs Variable compensation / commission / bonus plans

© 2015 Baker & McKenzie LLP 24

Employee Policies

‒ Key approaches: Global Policy; Local Policy; or Hybrid Approaches

‒ Advantages and disadvantages ‒ Implementation requirements‒ Company culture and values

© 2015 Baker & McKenzie LLP 25

Plan Exit Strategy Going In– Plan for flexibility in hiring Consider types of hires depending on short / long term plans

– Plan for notice, severance and consultation obligations Statutory notice / severance can be “hidden” costs

– Trap for the unwary – nonsolicit / noncompetes Rapidly changing laws on enforceability (and costs) of

noncompetes– Be prepared for business change Understand compliance obligations from the outset

© 2015 Baker & McKenzie LLP

Equity Compensation

© 2015 Baker & McKenzie LLP 27

Equity Awards: Preliminary Considerations– Does equity compensation make sense outside of Canada?

Consider local practices and expectations

Consider communication challenges

Consider alternatives such as cash awards / deferred share units (DSUs)

– Review eligibility requirements (note if recipient is employee or contractor)

– Conduct compliance analysis before grant

Review regulatory requirements (e.g., securities or exchange control filings)

Review employer / employee tax obligations (e.g., tax withholding/reporting and social tax obligations)

© 2015 Baker & McKenzie LLP 28

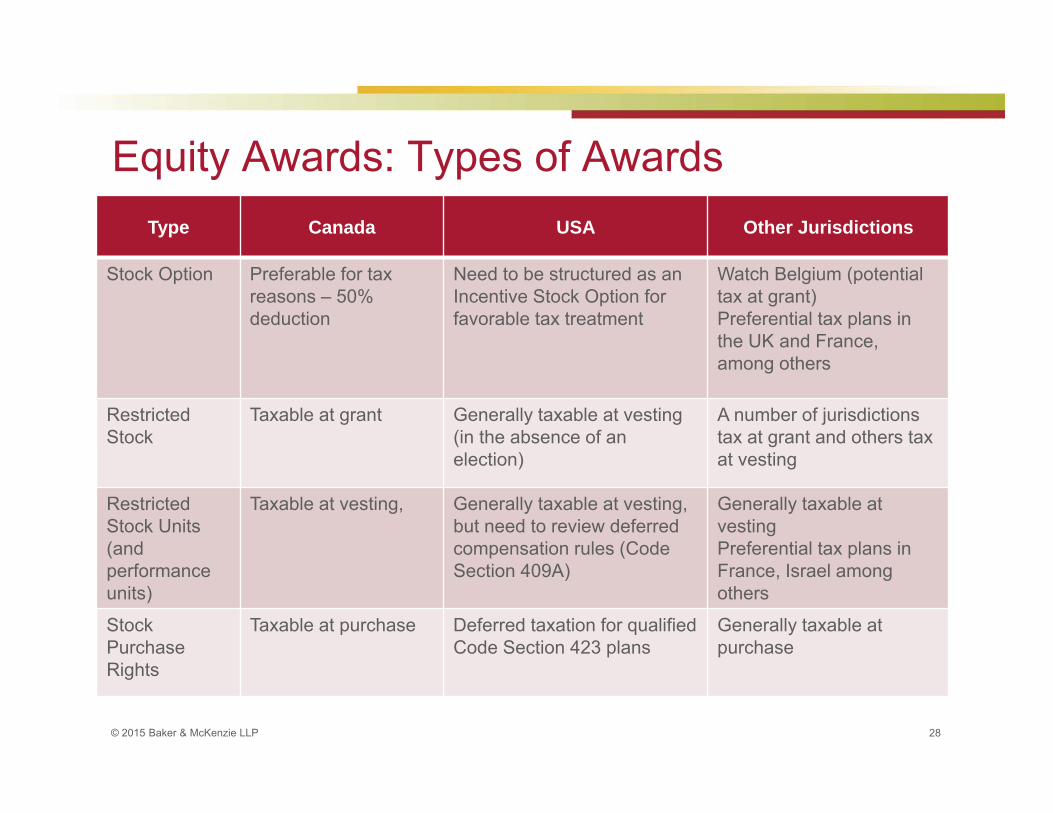

Equity Awards: Types of AwardsType Canada USA Other Jurisdictions

Stock Option Preferable for tax reasons – 50% deduction

Need to be structured as an Incentive Stock Option for favorable tax treatment

Watch Belgium (potential tax at grant)Preferential tax plans in the UK and France, among others

RestrictedStock

Taxable at grant Generally taxable at vesting (in the absence of an election)

A number of jurisdictions tax at grant and others tax at vesting

Restricted Stock Units(and performanceunits)

Taxable at vesting, Generally taxable at vesting, but need to review deferred compensation rules (Code Section 409A)

Generally taxable at vestingPreferential tax plans in France, Israel among others

Stock Purchase Rights

Taxable at purchase Deferred taxation for qualified Code Section 423 plans

Generally taxable at purchase

© 2015 Baker & McKenzie LLP 29

Equity Awards: Design Considerations

– Separate plan for other jurisdictions or part of global omnibus plan?

Often use US subplan for tax-qualified awards

– Avoid Canada-centric award documents (e.g. reference to 50% deduction for tax purposes) Instead, prepare global or non-Canada versions of award

documents Possible to use one agreement and cover country-specific terms

in appendix

© 2015 Baker & McKenzie LLP 30

Equity Awards: Best Practices– Parent company (Issuer) should administer awards and minimize

involvement by local employing entity Ensures consistent approach in all countries Avoids possible plan compliance violations for issuer Decreases risk of vested rights / entitlement and other labor law

issues– Avoid mentioning awards in employment-related documents from

local employing entity– Use separate equity offer letter (side letter from issuer) to

communicate equity awards

© 2015 Baker & McKenzie LLP 31

Equity Awards: Securities Laws

– Impact of Canadian securities requirements on global awards

National Instrument 55-104 Insider Reporting Requirements and Exemptions requires certain insiders of reporting issuers to report their personal holdings on Sedi (System for Electronic Disclosure by Insiders)

• includes the CEO, CFO and CCO of a major subsidiary of the issuer

• also includes a person responsible for a principal business unit, division or function of the issuer

• catch-all for any other insider that has routine access to material or undisclosed information and exercises significant power or influence over the business, operations, capital or development of the issuer

© 2015 Baker & McKenzie LLP 32

Equity Awards: Securities Laws cont’d– Stock Exchange Requirements

If dual-listed in the U.S., SEC Form S-8 requirement applies to equity compensation plans that have U.S. participants

TSX / TSXV rules apply to security-based compensation arrangements if it involves the granting of listed securities or securities convertible into listed securities regardless of where the grantee(s) is resident

Evergreen plans are subject to maximum of 10% of the issued and outstanding shares of the issuer

Insider participation under all of the issuers security based compensation arrangements is limited to 10% of the issued and outstanding shares

© 2015 Baker & McKenzie LLP 33

Equity Awards: Securities Laws cont’d

‒ Both TSX and TSXV require shareholder approval for any equity compensation plans or amendments if listed shares will be issued

‒ ISS and Glass Lewis Canadian Proxy Voting Guidelines not necessarily the same as the U.S. version be careful when structuring plans and check both sets of

guidelines as they can differ on some points

© 2015 Baker & McKenzie LLP 34

Equity Awards: Securities Laws – Other Jurisdictions– Securities Laws – generally territorial, usually exemption

available (but understand thresholds and / or necessary disclosure) & typically applies at grant (but may be applicable at issuance) Key problem countries: Australia, Japan (options/ESPP), EU

(ESPP), Italy (financial intermediary), Malaysia, New Zealand, the Philippines, and Saudi Arabia

© 2015 Baker & McKenzie LLP 35

Equity Awards: Exchange Controls/Foreign Asset Reporting

– Exchange Controls – generally based on residency, may restrict funds or shares, usually an employee (not company) obligation & be careful about repatriation Key problem countries: Argentina, China, Ukraine, Vietnam;

also India and Russia (repatriation)– Foreign Asset Reporting – mature shares and even equity awards

may be reportable as “foreign assets.” Brokerage accounts used for plan administration may be reportable as “foreign accounts.” Use of trusts can also implicate local reporting requirements A few examples of countries with these requirements include:

Belgium, India, Spain, US (FATCA individual reporting)

© 2015 Baker & McKenzie LLP 36

Equity Awards: Tax & Social Tax Issues– Not all countries tax awards at the same time, in the same manner or

based on the same value – Key countries: Australia (options taxation at vesting in some cases),

Belgium (options can be taxed at grant ), Denmark, India (valuation), Malaysia, United States (deferred taxation of ISOs if holding periods satisfied)

– Both Income and Social Taxes (at high uncapped rates) typically apply Key countries: Sweden (31.42% uncapped), UK (13.8%

uncapped)– Know where your withholding and reporting obligations exist

Key countries: China, India, France, Germany, Malaysia, Taiwan, UK

‒ Consider application of deferred compensation rules such as Code Section 409A in the United States

© 2015 Baker & McKenzie LLP 37

Equity Awards – Tax & Social Tax Issues– Special annual reporting exists for equity that differs

from compensation Key countries: France, Japan, Switzerland, Taiwan, UK, US (for

certain plans) – Tax favored plans available to avoid or minimize

Social Taxes Key countries: France (New law in process), Israel, UK , US

– Beware of penalties and bad press related to tax on equity Key countries: France, Japan, Korea, Taiwan, UK

© 2015 Baker & McKenzie LLP 38

Equity Awards – Tax Issues– Although Canadian tax rules generally prohibit a corporate tax

deduction for equity compensation, this is not the case in a number of other countries

– However, a reimbursement of the equity compensation “costs” by the foreign subsidiary may be required in order for the foreign subsidiary to be eligible for a corporate tax deduction

– Also need to consider whether such reimbursement triggers other withholding requirements or social taxes which would not otherwise apply

© 2015 Baker & McKenzie LLP 39

Equity Awards: Best Practices

– Revisit tax / compliance issues on regular basis and adjust award practices accordingly

– Create tools to manage ongoing compliance (e.g., grant checklist, compliance chart, grant document chart)

– Take advantage of free information on global equity NASPP Global Portal Global Equity Organization (Toronto Chapter) B&M GES website – www.bakermckenzie.com/ges

© 2015 Baker & McKenzie LLP 40

Global Equity Matrix app – now in 50 countries

© 2015 Baker & McKenzie LLP 41

Questions?

© 2015 Baker & McKenzie LLP

Suite of Baker & McKenzie

Resources

Opportunities Across High-Growth Markets: Trends in Cross-Border M&A – with the Economist Intelligence Unit

Cross-Border Transactions Handbook

The Global Employer: Focus on Trade Unions and Work Councils

Pre-Transaction Restructuring Handbook

Post-Acquisition Integration Handbook

The Global Employer: Focus on Termination, Employment Discrimination and Workplace Harassment Laws

© 2015 Baker & McKenzie LLP 43

Doing Business Guides in 33 jurisdictions