GLOBE TELECOM, INC. 1Q06 Investors’ Briefing · GLOBE TELECOM, INC. 1Q06 Investors’ Briefing...

13

1 1 GLOBE TELECOM, INC. GLOBE TELECOM, INC. GLOBE TELECOM, INC. GLOBE TELECOM, INC. 1Q06 Investors’ Briefing 1Q06 Investors’ Briefing 1Q06 Investors’ Briefing 1Q06 Investors’ Briefing May 9, 2006 May 9, 2006 May 9, 2006 May 9, 2006 2 Q1 Highlights – Sustaining the gains of 2H 2005 ! Operating metrics continuing on upward Operating metrics continuing on upward trajectory trajectory – Subscriber growth across all brands, lower churn – Steady ARPUs despite price-based offers in the market ! Strong financial performance Strong financial performance – EBITDA and EBIT at historic highs, with higher revenues and lower spend – Q1 net income of P3.5 billion, up 19% YoY, despite three-fold growth in income taxes to P1.5 billion – Before FX/MTM gains, net income up 40% YoY and 19% quarter-on-quarter

Transcript of GLOBE TELECOM, INC. 1Q06 Investors’ Briefing · GLOBE TELECOM, INC. 1Q06 Investors’ Briefing...

1

1

GLOBE TELECOM, INC.GLOBE TELECOM, INC.GLOBE TELECOM, INC.GLOBE TELECOM, INC.1Q06 Investors’ Briefing1Q06 Investors’ Briefing1Q06 Investors’ Briefing1Q06 Investors’ Briefing

May 9, 2006May 9, 2006May 9, 2006May 9, 2006

2

Q1 Highlights –Sustaining the gains of 2H 2005

!! Operating metrics continuing on upward Operating metrics continuing on upward trajectorytrajectory

– Subscriber growth across all brands, lower churn

– Steady ARPUs despite price-based offers in the market

!! Strong financial performanceStrong financial performance

– EBITDA and EBIT at historic highs, with higher revenues and lower spend

– Q1 net income of P3.5 billion, up 19% YoY, despite three-fold growth in income taxes to P1.5 billion

– Before FX/MTM gains, net income up 40% YoYand 19% quarter-on-quarter

2

3

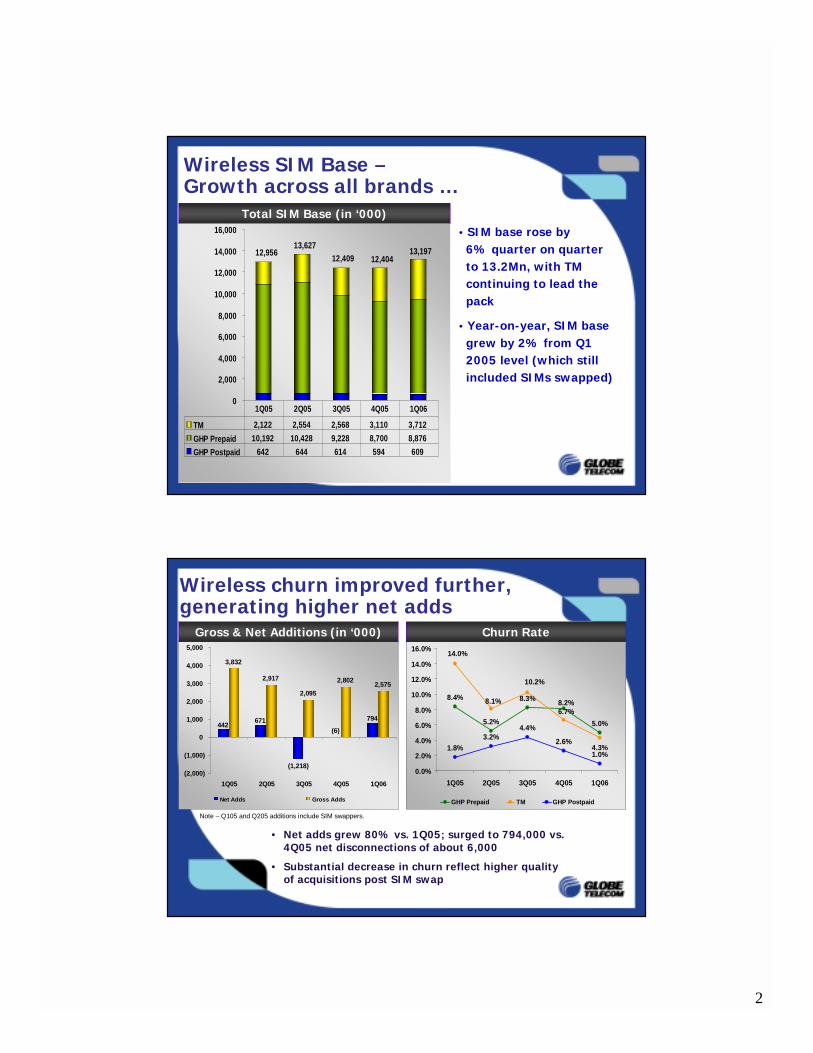

Total SIM Base (in ‘000)

12,40913,19712,956

13,627

12,404

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

TM 2,122 2,554 2,568 3,110 3,712

GHP Prepaid 10,192 10,428 9,228 8,700 8,876

GHP Postpaid 642 644 614 594 609

1Q05 2Q05 3Q05 4Q05 1Q06

Wireless SIM Base –Growth across all brands …

• SIM base rose by 6% quarter on quarter to 13.2Mn, with TM continuing to lead the pack

• Year-on-year, SIM base grew by 2% from Q1 2005 level (which still included SIMs swapped)

4

(1,218)

(6)

3,832

2,917

2,095

2,8022,575

794671442

(2,000)

(1,000)

0

1,000

2,000

3,000

4,000

5,000

1Q05 2Q05 3Q05 4Q05 1Q06

Net Adds Gross Adds

8.4%

5.2%

8.3%

5.0%

4.3%1.8%3.2%

4.4%

2.6%

1.0%

8.2%

10.2%

8.1%

14.0%

6.7%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

1Q05 2Q05 3Q05 4Q05 1Q06

GHP Prepaid TM GHP Postpaid

Gross & Net Additions (in ‘000)

Wireless churn improved further, generating higher net adds

Churn Rate

• Net adds grew 80% vs. 1Q05; surged to 794,000 vs. 4Q05 net disconnections of about 6,000

• Substantial decrease in churn reflect higher quality of acquisitions post SIM swap

Note – Q105 and Q205 additions include SIM swappers.

3

5

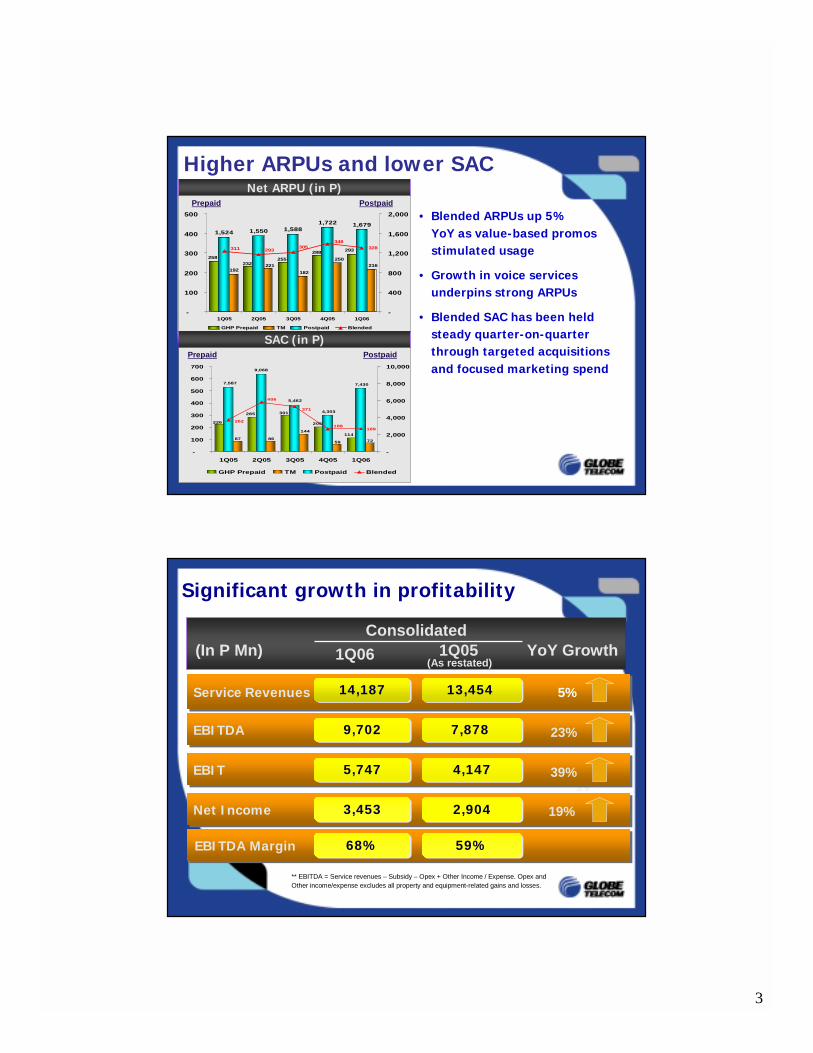

114

205226

285 301

144

87 8659 72

7,587

9,068

5,462

4,303

7,430

188189

406

371

262

-

100

200

300

400

500

600

700

1Q05 2Q05 3Q05 4Q05 1Q06

-

2,000

4,000

6,000

8,000

10,000

GHP Prepaid TM Postpaid Blended

SAC (in P)

Net ARPU (in P)

Higher ARPUs and lower SAC

Prepaid Postpaid

Prepaid Postpaid

• Blended ARPUs up 5% YoY as value-based promos stimulated usage

• Growth in voice services underpins strong ARPUs

• Blended SAC has been held steady quarter-on-quarter through targeted acquisitions and focused marketing spend

293288

255232

258

216250

182

221192

1,524 1,550

1,722 1,6791,588

328348

311 293305

-

100

200

300

400

500

1Q05 2Q05 3Q05 4Q05 1Q06-

400

800

1,200

1,600

2,000

GHP Prepaid TM Postpaid Blended

6

Significant growth in profitability

(In P Mn) 1Q06 1Q05 YoY Growth(As restated)

Service RevenuesService Revenues

3.9

13,454 13,454 14,18714,187 5%

EBITDAEBITDA 7,878 7,878 9,7029,702 23%

EBITEBIT 4,1474,1475,7475,747 39%

Net Income Net Income 2,9042,9043,4533,453 19%

EBITDA Margin EBITDA Margin 68%68% 59%59%

** EBITDA = Service revenues – Subsidy – Opex + Other Income / Expense. Opex and Other income/expense excludes all property and equipment-related gains and losses.

Consolidated

4

7

Drivers of Sustained Growth: Value offers beyond traditional discounting

" Per-second charging continues to be a unique Globe offering in the industry

" Program now extended to IDD arena with calls as low as $0.003 per second (launched March 31)

8

Drivers of Sustained Growth:Products designed for specific usage profiles …

UNLIMITXT now a permanent plan

TM-to-TM SMS at P0.75 (currently, lowest intra-network rate in market)

5

9

Drivers of Sustained Growth:… and targeted subscriber segments

Kababayan program –Reduced rates for calls to Japan & Saudi Arabia, and mobile calls to HK CSL &

Singtel

Php 7.50/minute for calls to US and Canada during off-peak

hours

10

• Improving subscriber experience in tandem with value offers through

! Improved customer service

! Superior local and international coverage

! Relevant innovations

• Building brand equity –“Dahil ang lakas mo saGlobe”

Drivers of Sustained Growth:Stronger brand image …

6

11

Launched last April 16 –P 0.90 to all networks

(lowest rate in the market today)

Drivers of Sustained Growth:… enabled by continuous enhancements in connectivity …

12

Drivers of Sustained Growth:… and relevant, forward-looking innovations

• 1st in High-Speed Data Packet Access (HSDPA or 3.5G) in Asia-Pacific – Launched last March 30 for corporate accounts

7

13

4.04.6 4.9

5.76.4

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2001 2002 2003 2004 2005

227,999 223,249261,254

323,094362,143

0

100,000

200,000

300,000

400,000

2001 2002 2003 2004 2005

Drivers of Sustained Growth:Steady gains in our wireline business …

Wireline Service Revenues –In P Bn

Wireline Subscribers

13% Compounded Growth Rate

5% Compounded Growth Rate

14

+148%

… supported by an aggressive push for our broadband services

25,880

10,437

22,479

Q1 2006 Q1 2005 Q4 2005

Globelines Broadband Subscribers

• Consumer broadband subscribers up 15% from Q4 ‘05, and 148% YoY

• Expected to be a key source of long-term growth for Innove, as we work to bring down prices of high-speed internet access to more affordable levels

8

15

29.8

20.5

15.8

21.2

14.8

27%

52%

40%

106%

33%

0

5

10

15

20

25

30

35

2001 2002 2003 2004 2005

0%

20%

40%

60%

80%

100%

120%

Capex % of sales

Capex – In P Bn and as % of service revenues

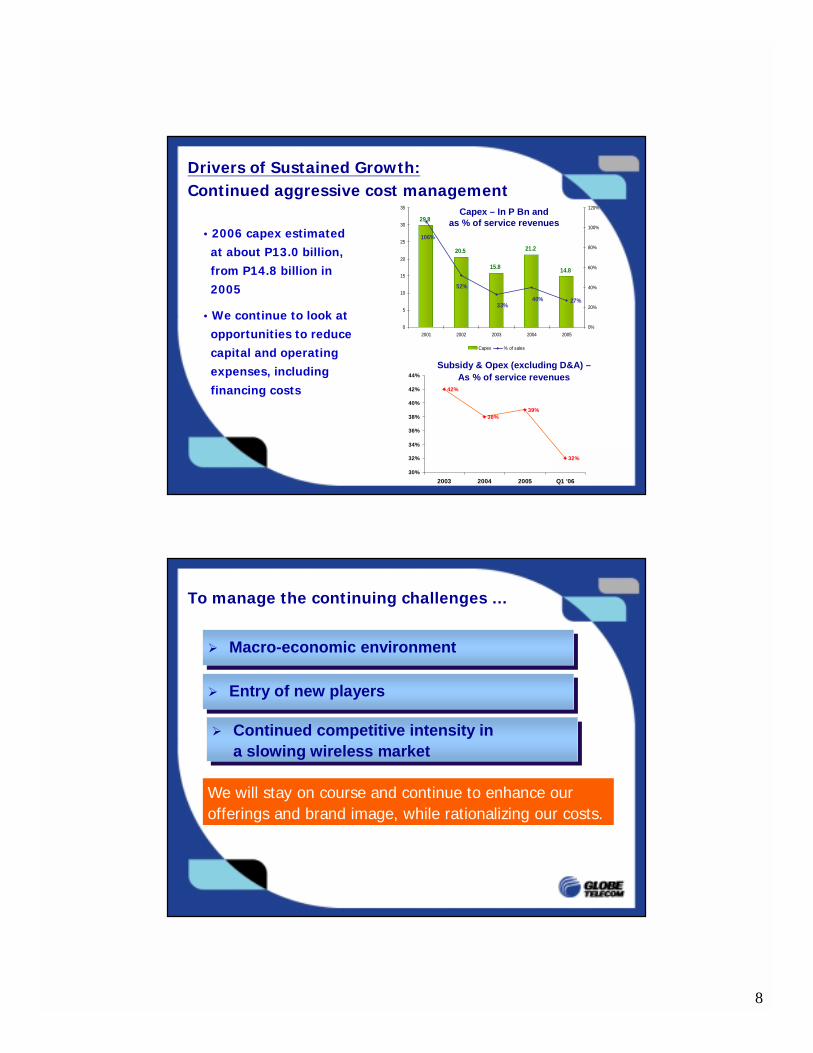

• 2006 capex estimated at about P13.0 billion, from P14.8 billion in 2005

• We continue to look at opportunities to reduce capital and operating expenses, including financing costs

Drivers of Sustained Growth:Continued aggressive cost management

42%

38%39%

32%

30%

32%

34%

36%

38%

40%

42%

44%

2003 2004 2005 Q1 '06

Subsidy & Opex (excluding D&A) –As % of service revenues

16

! Entry of new players! Entry of new players

! Macro-economic environment! Macro-economic environment

! Continued competitive intensity in a slowing wireless market

! Continued competitive intensity in a slowing wireless market

To manage the continuing challenges …

We will stay on course and continue to enhance our offerings and brand image, while rationalizing our costs.

9

17

Financial Performance

18

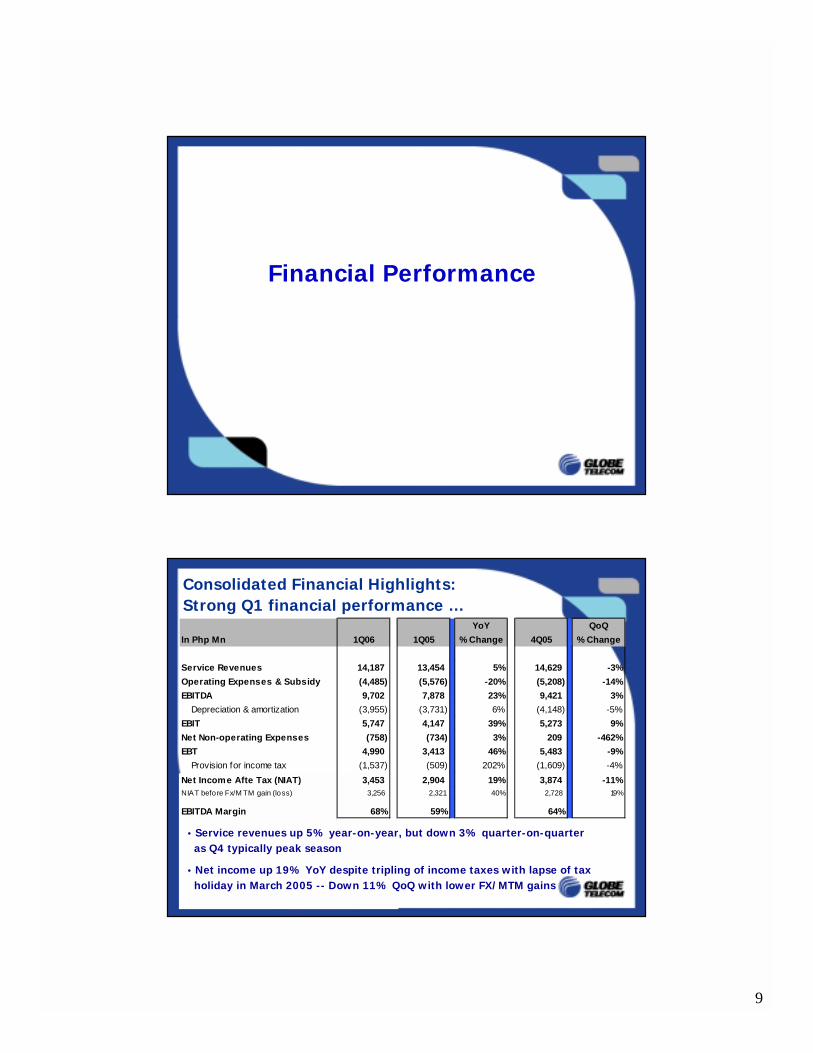

Consolidated Financial Highlights: Strong Q1 financial performance …

• Service revenues up 5% year-on-year, but down 3% quarter-on-quarter as Q4 typically peak season

• Net income up 19% YoY despite tripling of income taxes with lapse of tax holiday in March 2005 -- Down 11% QoQ with lower FX/MTM gains

YoY QoQ

In Php Mn 1Q06 1Q05 % Change 4Q05 % Change

Service Revenues 14,187 13,454 5% 14,629 -3%

Operating Expenses & Subsidy (4,485) (5,576) -20% (5,208) -14%

EBITDA 9,702 7,878 23% 9,421 3%

Depreciation & amortization (3,955) (3,731) 6% (4,148) -5%

EBIT 5,747 4,147 39% 5,273 9%

Net Non-operating Expenses (758) (734) 3% 209 -462%

EBT 4,990 3,413 46% 5,483 -9%

Provision for income tax (1,537) (509) 202% (1,609) -4%

Net Income Afte Tax (NIAT) 3,453 2,904 19% 3,874 -11%NIAT before Fx/M TM gain (loss) 3,256 2,321 40% 2,728 19%

EBITDA Margin 68% 59% 64%

10

19

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2003 2004 2005 2006

9,702

-

1,000

2,000

3,000

4,000

5,000

6,000

2003 2004 2005 2006

5,747

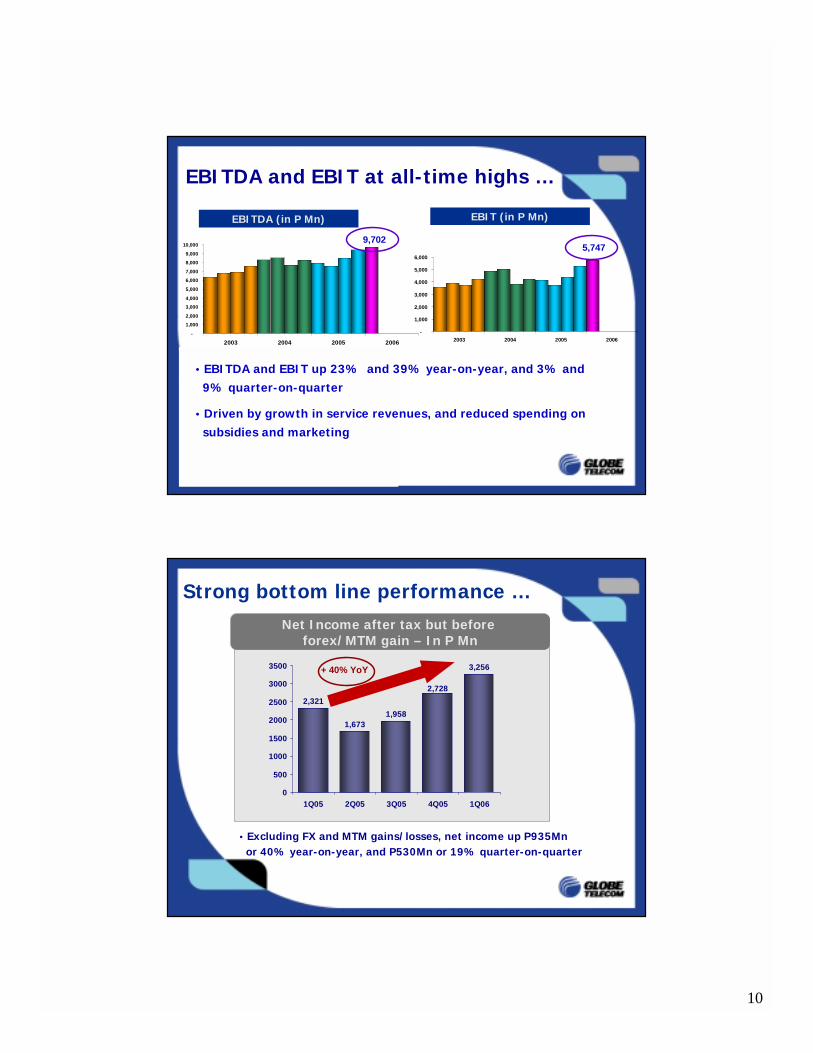

EBITDA and EBIT at all-time highs …

EBITDA (in P Mn) EBIT (in P Mn)

• EBITDA and EBIT up 23% and 39% year-on-year, and 3% and 9% quarter-on-quarter

• Driven by growth in service revenues, and reduced spending on subsidies and marketing

20

2,321

1,6731,958

3,256

2,728

0

500

1000

1500

2000

2500

3000

3500

1Q05 2Q05 3Q05 4Q05 1Q06

Net Income after tax but before forex/MTM gain – In P Mn

Strong bottom line performance …

• Excluding FX and MTM gains/losses, net income up P935Mn or 40% year-on-year, and P530Mn or 19% quarter-on-quarter

+ 40% YoY

11

21

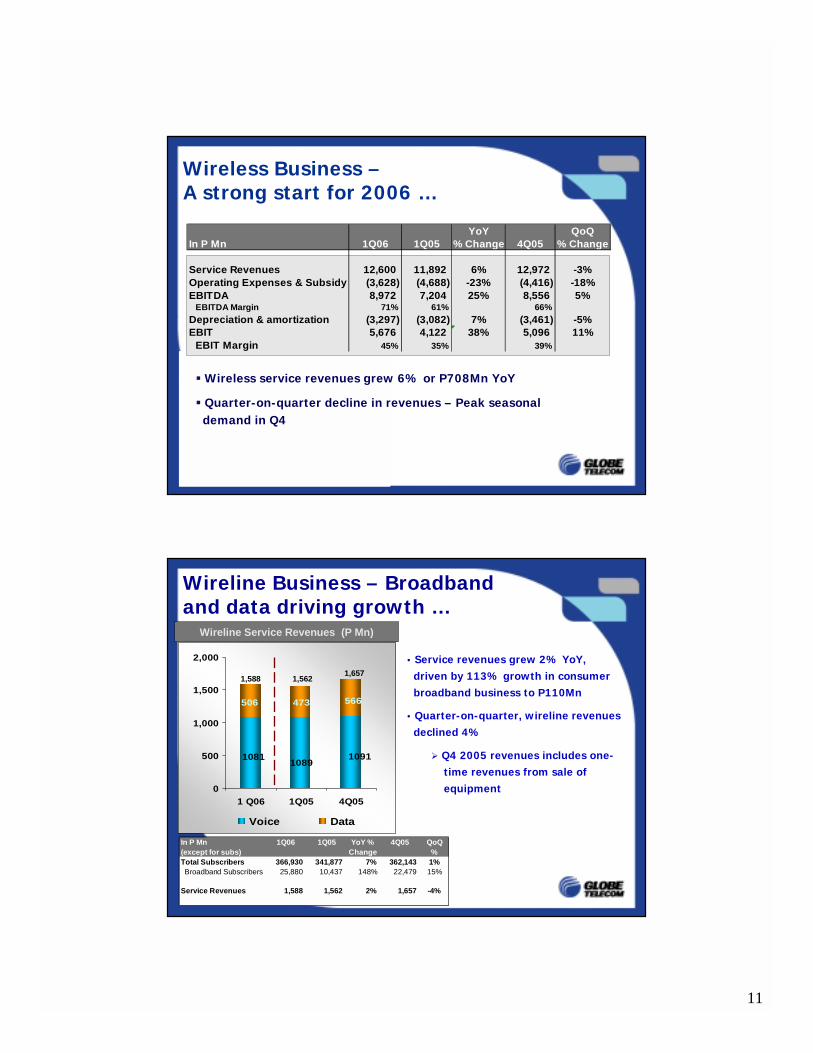

Wireless Business –A strong start for 2006 …

" Wireless service revenues grew 6% or P708Mn YoY

" Quarter-on-quarter decline in revenues – Peak seasonal demand in Q4

YoY QoQIn P Mn 1Q06 1Q05 % Change 4Q05 % Change

Service Revenues 12,600 11,892 6% 12,972 -3%Operating Expenses & Subsidy (3,628) (4,688) -23% (4,416) -18%EBITDA 8,972 7,204 25% 8,556 5%

EBITDA Margin 71% 61% 66%

Depreciation & amortization (3,297) (3,082) 7% (3,461) -5%EBIT 5,676 4,122 38% 5,096 11%

EBIT Margin 45% 35% 39%

22

10811089

1091

566473506

0

500

1,000

1,500

2,000

1 Q06 1Q05 4Q05

Voice Data

Wireline Service Revenues (P Mn)

Wireline Business – Broadband and data driving growth …

In P Mn 1Q06 1Q05 4Q05(except for subs)Total Subscribers 366,930 341,877 7% 362,143 1% Broadband Subscribers 25,880 10,437 148% 22,479 15%

Service Revenues 1,588 1,562 2% 1,657 -4%

YoY % Change

QoQ %

1,5881,657

1,562

• Service revenues grew 2% YoY, driven by 113% growth in consumer broadband business to P110Mn

• Quarter-on-quarter, wireline revenues declined 4%

! Q4 2005 revenues includes one-time revenues from sale of equipment

12

23

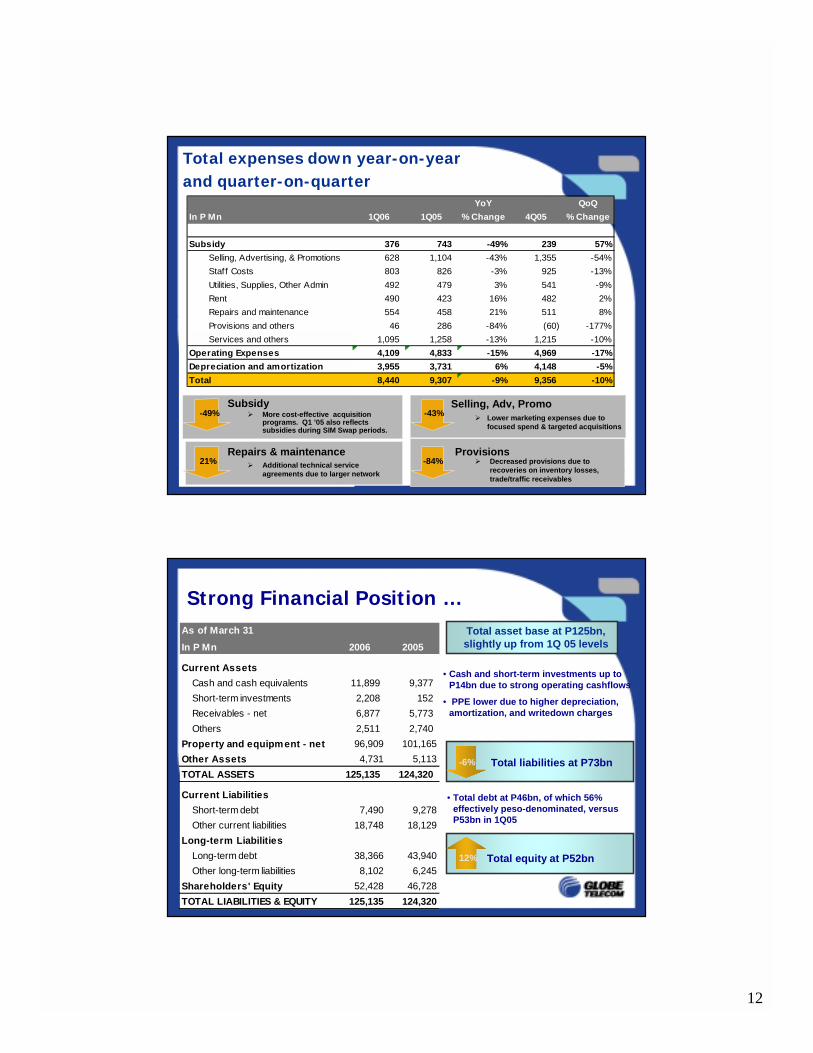

Total expenses down year-on-yearand quarter-on-quarter

Selling, Adv, PromoSubsidy

Repairs & maintenance21%

Provisions

YoY QoQ

In P Mn 1Q06 1Q05 % Change 4Q05 % Change

Subsidy 376 743 -49% 239 57%

Selling, Advertising, & Promotions 628 1,104 -43% 1,355 -54%

Staff Costs 803 826 -3% 925 -13%

Utilities, Supplies, Other Admin 492 479 3% 541 -9%

Rent 490 423 16% 482 2%

Repairs and maintenance 554 458 21% 511 8%

Provisions and others 46 286 -84% (60) -177%

Services and others 1,095 1,258 -13% 1,215 -10%

Operating Expenses 4,109 4,833 -15% 4,969 -17%

Depreciation and amortization 3,955 3,731 6% 4,148 -5%

Total 8,440 9,307 -9% 9,356 -10%

! More cost-effective acquisition programs. Q1 ’05 also reflects subsidies during SIM Swap periods.

! Lower marketing expenses due to focused spend & targeted acquisitions

! Additional technical service agreements due to larger network

! Decreased provisions due to recoveries on inventory losses, trade/traffic receivables

-49% -43%

-84%21%

24

Total asset base at P125bn, slightly up from 1Q 05 levels

• Cash and short-term investments up to P14bn due to strong operating cashflows

• PPE lower due to higher depreciation, amortization, and writedown charges

1Q05

Strong Financial Position …

• Total debt at P46bn, of which 56% effectively peso-denominated, versus P53bn in 1Q05

Total liabilities at P73bn-6%

Total equity at P52bn

As of March 31

In P Mn 2006 2005

Current Assets

Cash and cash equivalents 11,899 9,377

Short-term investments 2,208 152

Receivables - net 6,877 5,773

Others 2,511 2,740

Property and equipment - net 96,909 101,165

Other Assets 4,731 5,113

TOTAL ASSETS 125,135 124,320

Current Liabilities

Short-term debt 7,490 9,278

Other current liabilities 18,748 18,129

Long-term Liabilities

Long-term debt 38,366 43,940

Other long-term liabilities 8,102 6,245

Shareholders' Equity 52,428 46,728

TOTAL LIABILITIES & EQUITY 125,135 124,320

12%

13

25

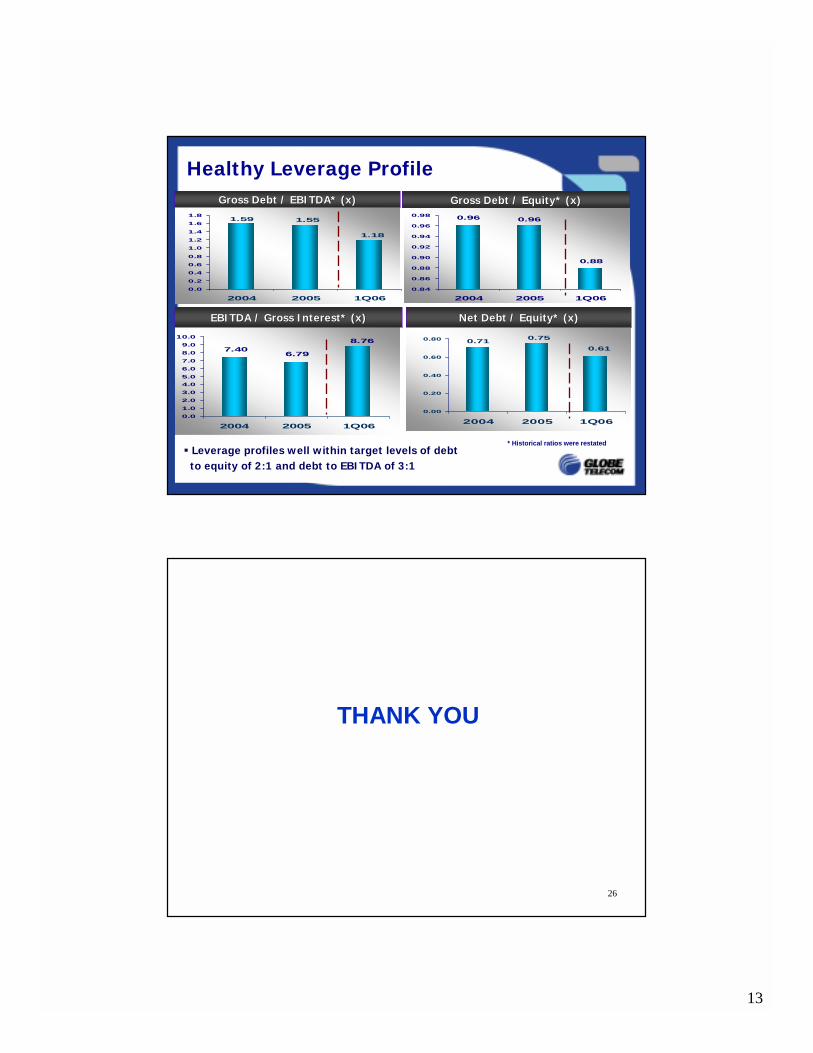

0.71 0.75

0.61

0.00

0.20

0.40

0.60

0.80

2004 2005 1Q06

0.88

0.960.96

0.84

0.86

0.88

0.90

0.92

0.94

0.96

0.98

2004 2005 1Q06

8.76

6.797.40

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

2004 2005 1Q06

1.18

1.551.59

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2004 2005 1Q06

Healthy Leverage ProfileGross Debt / EBITDA* (x)Gross Debt / EBITDA* (x) Gross Debt / Equity* (x)Gross Debt / Equity* (x)

EBITDA / Gross Interest* (x)EBITDA / Gross Interest* (x) Net Debt / Equity* (x)Net Debt / Equity* (x)

* Historical ratios were restated" Leverage profiles well within target levels of debt

to equity of 2:1 and debt to EBITDA of 3:1

26

THANK YOU