GLOBAL LOGISTICS: THE FUTURE IS NOW - CBRE … Investment... · GLOBAL LOGISTICS: THE FUTURE IS NOW...

37

GLOBAL LOGISTICS: THE FUTURE IS NOW 18 MAY 2016 PRESENTED BY: Doug Herzbrun, Global Head of Research Anthony Wirth, Director – Industrial Research John Thomas, Sr. Managing Director – Logistics

Transcript of GLOBAL LOGISTICS: THE FUTURE IS NOW - CBRE … Investment... · GLOBAL LOGISTICS: THE FUTURE IS NOW...

GLOBAL LOGISTICS: THE FUTURE IS NOW

18 MAY 2016

PRESENTED BY:

Doug Herzbrun, Global Head of Research

Anthony Wirth, Director – Industrial Research

John Thomas, Sr. Managing Director – Logistics

THE STRUCTURAL SHIFT BECOMES CLEAR

GLOBAL INVESTMENT SYMPOSIUM 2

E-COMMERCE IS BLURRING THE LINE

BETWEEN RETAIL AND INDUSTRIAL

0%

1%

2%

3%

4%

5%

6%

7%

8%

$0

$50.000

$100.000

$150.000

$200.000

$250.000

$300.000

$350.000

$400.000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

E-C

om

merce Share

U.S. E-C

om

merce Sale

s (m

illio

ns)

Sales

E-Commerce Share

Sources: Census Bureau; Moody’s Analytics

GLOBAL INVESTMENT SYMPOSIUM 3

U.S. INDUSTRIAL DEMAND IS ROBUST

-90

-75

-60

-45

-30

-15

0

15

30

45

60

75

Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q41Q

U

.S. Industrial A

bsorption

SF (m

illio

ns)

Absorption

Long-term Average

4 Qtr Moving Average

* Long-term Average = 1980 - 2016

Sources: CBRE EA; CBRE Global Investors

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

GLOBAL INVESTMENT SYMPOSIUM 4

THE STORY’S THE SAME IN EUROPE

0%

2%

4%

6%

8%

10%

0

50

100

150

200

250

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

F

20

17

F

Online Sale

s Share

Western Europe O

nline Retail Sale

s (EU

R Bn.)

Internet Retailing (EUR Bn.)

Online Sales as % of total sales

Source: Euromonitor

¹ Includes Belgium, Czech Republic, Finland, France, Germany, Italy, Netherlands, Poland, Portugal, Spain, Sweden, United Kingdom

GLOBAL INVESTMENT SYMPOSIUM 5

THERE IS ROOM FOR GROWTH

13,6%

10,2%

9,2%

8,6%

7,8%

6,9% 6,5% 6,4%

4,9%

3,3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

UK China US Germany Sweden Japan Poland Australia Portugal Spain

Online Retail Sale

s as %

of Total Retail Sale

s (2015)

Source: Euromonitor

GLOBAL INVESTMENT SYMPOSIUM 6

U.S. INDUSTRIAL IS AN INVESTOR DARLING

$0

$5

$10

$15

$20

$25

$30

1Q09 1Q10 1Q11 1Q12 1Q13 1Q14 1Q15 1Q16

Volum

es

$Billions

Transaction Volume ($B)

4-Qtr Average

Strong Acquisition Activity

4

5

6

7

8

9

1Q09 1Q10 1Q11 1Q12 1Q13 1Q14 1Q15 1Q16

Cap Rates (%

)

Industrial

Retail

Office

Multifamily

Comparable Yields

GLOBAL INVESTMENT SYMPOSIUM 7

CAPITAL MARKETS ARE SHIFTING

Sources: JLL, CBRE, CBRE Global Investors

3

5

7

9

11

13

15

17

Logistics Yields, %

Warsaw

Prague

Paris

Rotterdam

Hamburg

London

GLOBAL INVESTMENT SYMPOSIUM 8

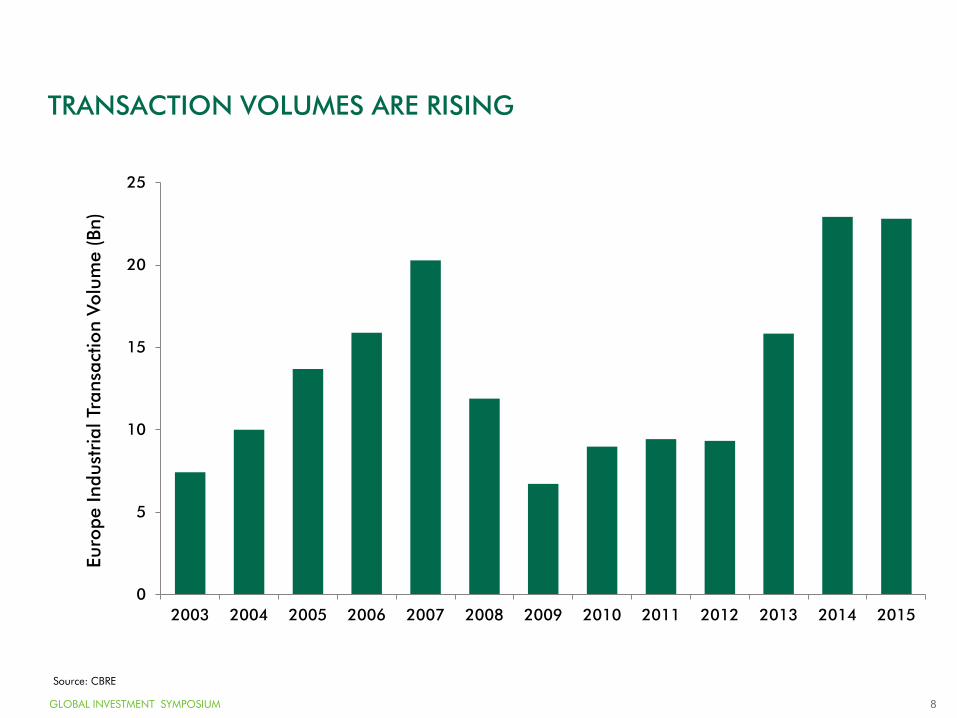

TRANSACTION VOLUMES ARE RISING

Source: CBRE

0

5

10

15

20

25

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Europe Industrial Transaction Volum

e (Bn)

GLOBAL INVESTMENT SYMPOSIUM 9

CROSS-BORDER ONLINE SALES WILL REACH $1T BY 2020

$0

$200

$400

$600

$800

$1.000

2016 2017 2018 2019 2020

Cross-Border O

nline Sales (Bn)

Sources: Accenture, AliResearch

GLOBAL INVESTMENT SYMPOSIUM 10

KEY TRENDS ARE EVOLVING

Technology is creating value Site selection is holistic Supply chain analysis is real time

GLOBAL INVESTMENT SYMPOSIUM 11

• “Cost of Chaos”

• Not your grandfather’s 3PL

• Provide the grease

• Innovation is key

OUTSOURCED LOGISTICS IS BECOMING MORE PREVALENT

GLOBAL INVESTMENT SYMPOSIUM 12

RISKS MUST BE CONSIDERED

Cyclical

Risk

Political

Risk

Technological

Risk

OPTIMIZING THE LOGISTICS SUPPLY CHAIN

GLOBAL INVESTMENT SYMPOSIUM 14

FLOW OF GOODS TO THE CONSUMER

GLOBAL INVESTMENT SYMPOSIUM 15

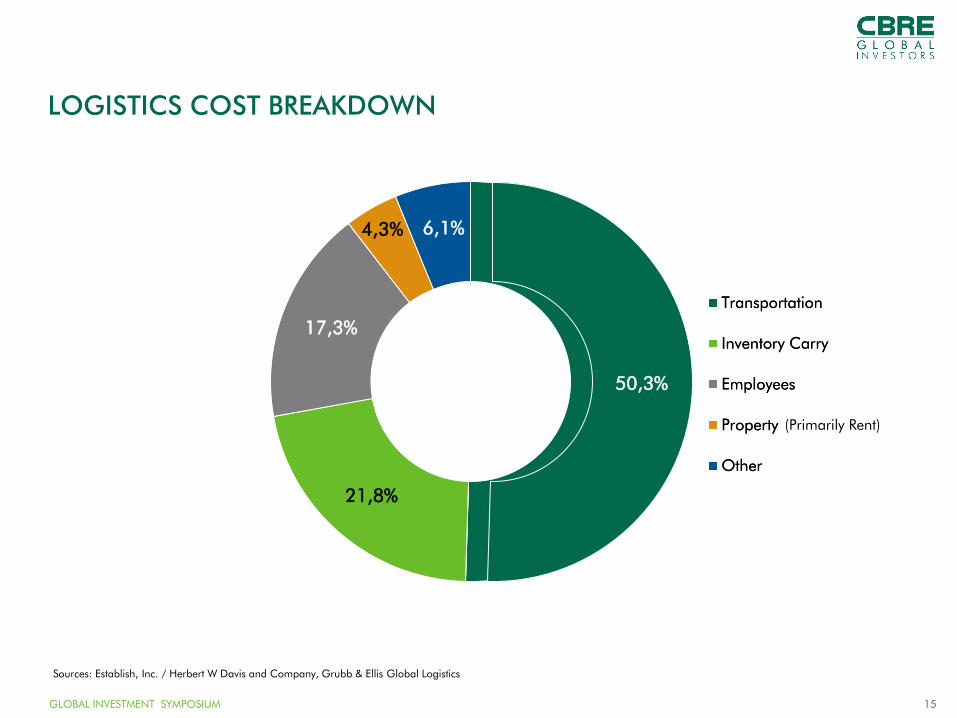

LOGISTICS COST BREAKDOWN

Sources: Establish, Inc. / Herbert W Davis and Company, Grubb & Ellis Global Logistics

50,3%

21,8%

17,3%

4,3% 6,1%

Transportation

Inventory Carry

Employees

Property

Other

50,3%

21,8%

17,3%

4,3% 6,1%

Transportation

Inventory Carry

Employees

Property

Other

(Primarily Rent)

GLOBAL INVESTMENT SYMPOSIUM 16

GLOBAL SHIPPING TRADE ROUTES

Logistics refers to the management of the flow of goods and other resources between

the point of origin and the point of consumption

GLOBAL INVESTMENT SYMPOSIUM 17

Rank Port, Country Millions of TEUs (2013)

1 Shanghai, China 34

2 Singapore, Singapore 33

3 Shenzhen, China 23

4 Hong Kong, China 22

5 Busan, South Korea 18

6 Ningbo-Zhoushan, China 17

7 Qingdao, China 16

8 Guangzhou Harbor, China 15

9 Jebel Ali, Dubai, United Arab Emirates 14

10 Tianjin, China 13

11 ROTTERDAM, NETHERLANDS 12

12 Dalian, China 11

13 Port Kelang, Malaysia 10

14 Kaohsiung, Taiwan, China 10

15 HAMBURG, GERMANY 9

16 ANTWERP, BELGIUM 9

17 Keihin Ports, Japan 8

18 Xiamen, China 8

19 Los Angeles, U.S. 8

20 Tanjung Pelepas, Malaysia 8

21 Long Beach, U.S. 7

22 Tanjung Priok, Jakarta, Indonesia 7

23 Laem Chabang, Thailand 6

24 Ho Chi Minh, Vietnam 6

25 BREMEN/BREMERHAVEN, GERMANY 6

WORLD PORT STATS

GLOBAL INVESTMENT SYMPOSIUM 18

• 97 ultra-large container vessels are

on order:

– Capable of handling between

18,000 and 20,000 TEUs

– Scheduled for delivery by mid-

2019

• 36 in 2015

• 12 in 2016

• 22 in 2017

• 22 in 2018

• 5 in 2019

• Fuel Consumption for the 15,000+

TEU vessels is expected to be 50%

below the industry average

– This is the driver behind the

demand for the big ships

MEGA SHIPS ARE CHANGING THE LANDSCAPE

www.imsw.com

Foreign Trade Zone, Logistics and Supply Chain Consulting

GLOBAL INVESTMENT SYMPOSIUM 19

• Bigger ships mean less vessels

• Less vessel calls mean less

ports visited by the major

carriers

• Ultra-large ships must be

matched on the land side with:

– Adequate water-depth

– Port infrastructure

• Cranes

• Labor

• Space

– Distribution channels

• Rail

• Highways

• Trucking

LARGE SHIPS IMPACT ON PORTS 2015-2020

GLOBAL INVESTMENT SYMPOSIUM 20

INLAND TRANSPORT

GLOBAL INVESTMENT SYMPOSIUM 21

Pros

• About twice as fast as sea route

• More reliable service

• 20% of the cost of airfreight

• Chinese and German

governments are advocates

Cons

• Several customs stops

• Different rail gauges

• 2.5 times the cost of sea route

• Smaller load capacity (about

100 containers/train)

Observations

• Higher cost items such as

electronics and automobile

parts work best

• Still a new service, so with the

government backing, will

improve overtime

• Central China to CEE saves

over 2,000 km of distance

CHINESE SILK ROAD – CONTAINER TRAIN ALTERNATIVE

GLOBAL INVESTMENT SYMPOSIUM 22

Algeciras

24 days

€1,000

Top 20 Major Seaports

Major Inland Ports

Other Seaports

MAJOR PORTS

Shanghai

Valencia

29 days

€1,000

Barcelona

31 days

€1,000

Marseille

33 days

€1,000

Genoa

29 days

€835

Trieste

32 days

€835

Piraeus

21 days

€1,000

Aliaga

23 days

€1,000

Botas

22 days

€1,000

Izmit

24 days

€1,000

Ambarli

25 days

€1,000

Novorossiysk

27days

€835

Moscow

39 days

€880

Dusseldorf

30 days

€1,550

Paris

29 days

€1,500

Hamburg

32 days

€835

St Petersburg

38 days

€310

Bergen

39 days

€1,000

Bremerhaven

36 days

€835

Amsterdam

41 days

€1,000

Rotterdam

29 days

€1,000

Antwerp 31 days

€1,000

Le Havre

28 days

€1,000

Liege

30 days

€1,365

Grimsby

34 days

€1,000

Felixstowe

29 days

€1,000

London

36 days

€1,000

Source: SeaRates.com. Cost includes ocean freight cost only for 2TEU container. Inland Ports

include road haul costs from nearest port..

GLOBAL INVESTMENT SYMPOSIUM 23

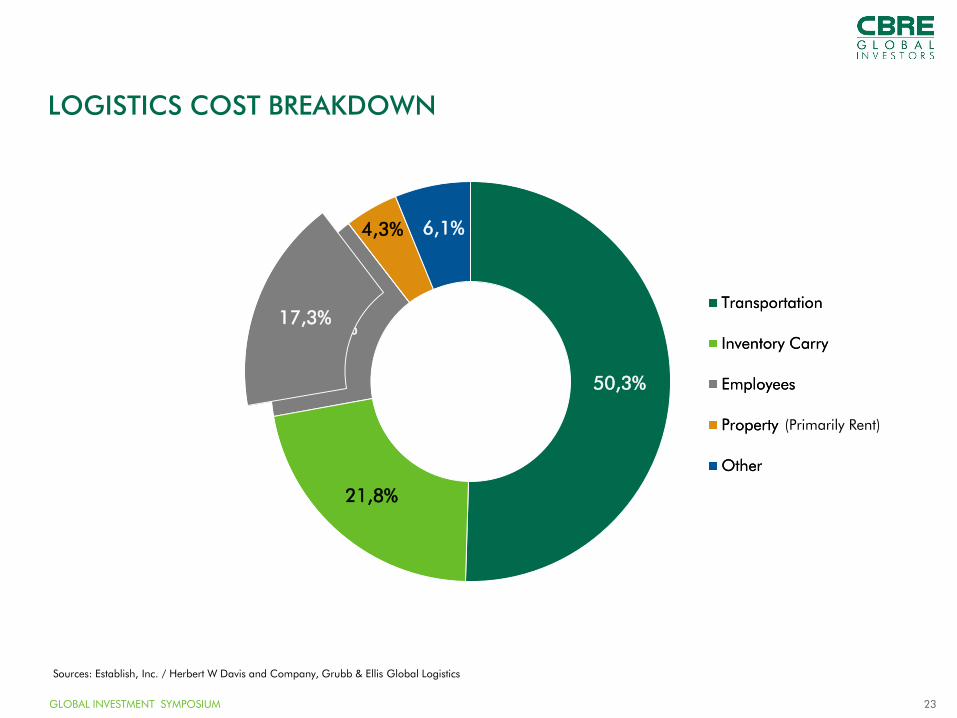

LOGISTICS COST BREAKDOWN

Sources: Establish, Inc. / Herbert W Davis and Company, Grubb & Ellis Global Logistics

50,3%

21,8%

17,3%

4,3% 6,1%

Transportation

Inventory Carry

Employees

Property

Other

50,3%

21,8%

17,3%

4,3% 6,1%

Transportation

Inventory Carry

Employees

Property

Other

(Primarily Rent)

GLOBAL INVESTMENT SYMPOSIUM 24

Today’s Integrated Logistics Solutions had their beginnings as local specialists in practices such as

dedicated trucking, warehousing operations, and freight forwarding.

EVOLUTION OF LOGISTICS

Integrated Broad Services

1970s

Local services in specific

transportation mode

• Warehouse operators

• Trucking companies

• Freight Forwarders

Local Specialists

Customer Centric

Current Era

• Lead Logistics Providers (4PL)

• Integrated in customer’s value

chain

Globalization/Integration

• Consulting services

• Global coverage for customers

across transportation modes

Fragmented Narrow

Service Offering

1990s

GLOBAL INVESTMENT SYMPOSIUM 25

From real estate to solutions design and operations we provide our customers with the expertise

required to manage & grow their business

HOLISTIC SOLUTIONS FOR CUSTOMERS

Customer

Solution

Real

Estate

Solutions

Design

In-House

Experts

• Network design

• Facility design, engineering and

simulation

• Transportation design and

optimization

• Expertise in development

• Customer focused suite of real estate services

• Exclusively focused on logistics related real

estate solutions

• Operational expertise

• Tax credits & incentives

• Legal & licensing

GLOBAL INVESTMENT SYMPOSIUM 26

LOGISTICS COST BREAKDOWN

Sources: Establish, Inc. / Herbert W Davis and Company, Grubb & Ellis Global Logistics

50,3%

21,8%

17,3%

4,3% 6,1%

Transportation

Inventory Carry

Employees

Property

Other

50,3%

21,8%

17,3%

4,3% 6,1%

Transportation

Inventory Carry

Employees

Property

Other

(Primarily Rent)

GLOBAL INVESTMENT SYMPOSIUM 27

COMMON EUROPEAN LOGISTICS FACILITY

GLOBAL INVESTMENT SYMPOSIUM 28

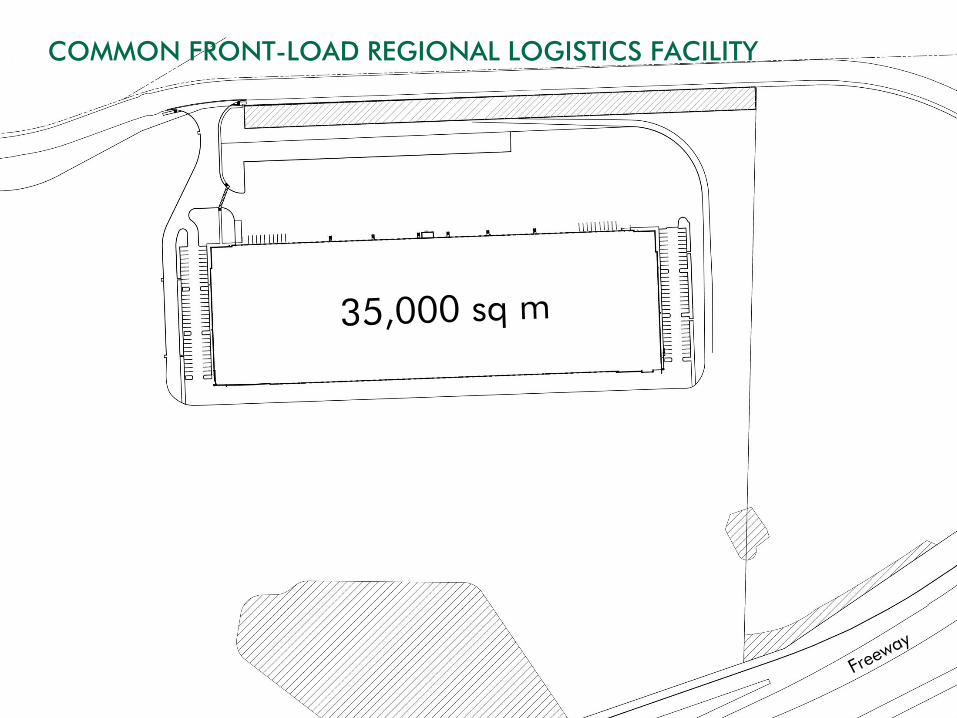

COMMON FRONT-LOAD REGIONAL LOGISTICS FACILITY

GLOBAL INVESTMENT SYMPOSIUM 29

MODERN REGIONAL LOGISTICS FACILITY

GLOBAL INVESTMENT SYMPOSIUM 30

The Last Mile Opportunity

GLOBAL INVESTMENT SYMPOSIUM 31

POTENTIAL LAST MILE FACILITY

GLOBAL INVESTMENT SYMPOSIUM 32

LAST MILE FACILITY INTERIOR

GLOBAL INVESTMENT SYMPOSIUM 33

MODERN LAST MILE CENTER

GLOBAL INVESTMENT SYMPOSIUM 34

“Others have seen

what is and asked why.

I have seen what could

be and asked why not.”

– Pablo Picasso

GLOBAL INVESTMENT SYMPOSIUM 35

• Logistics is the management of the flow of goods and other resources

between the point of origin and the point of consumption

• Efficiency drives logistics tenant demand; location and capabilities of the

facility far more important than rental price

• Last mile is the newest opportunity, but it requires imagination and vision

to execute

KEY TAKEAWAYS

GLOBAL INVESTMENT SYMPOSIUM 36

SPECIAL THANKS